![[Draft] Strategy for 2020–2023 · IAASB [Draft] Strategy for 2020‒2023. IAASB Main Agenda (December 2019) Agenda Item 3-A (Revised) Page 5 of 6 . The IAASB developed this Strategy](https://static.fdocuments.in/doc/165x107/5ec75b92157be373b17499e4/draft-strategy-for-2020a2023-iaasb-draft-strategy-for-2020a2023-iaasb-main.jpg)

Breakout Session 2 – Track B International Standards on Auditing: Adoption and Implementation...

9

Breakout Session 2 – Track B International Standards on Auditing: Adoption and Implementation Challenges and Tools Prof. Arnold Schilder, IAASB Chairman 31 October 2012

-

Upload

allison-constance-richardson -

Category

Documents

-

view

218 -

download

3

Transcript of Breakout Session 2 – Track B International Standards on Auditing: Adoption and Implementation...

Breakout Session 2 – Track B

International Standards on Auditing:

Adoption and Implementation Challenges and Tools

Prof. Arnold Schilder, IAASB Chairman

31 October 2012

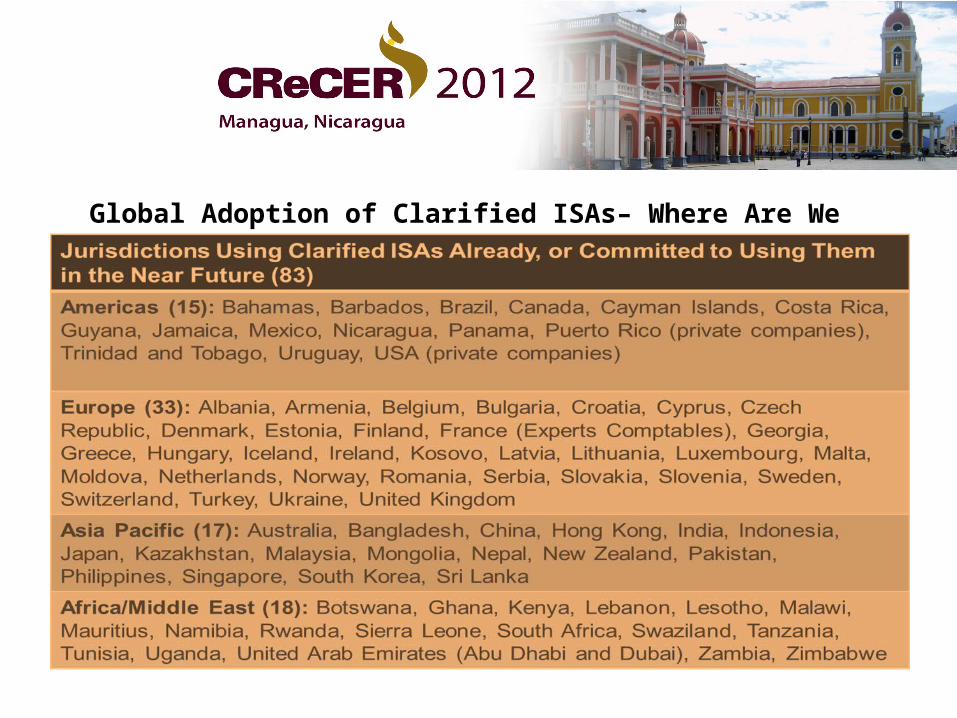

Global Adoption of Clarified ISAs– Where Are We Now?

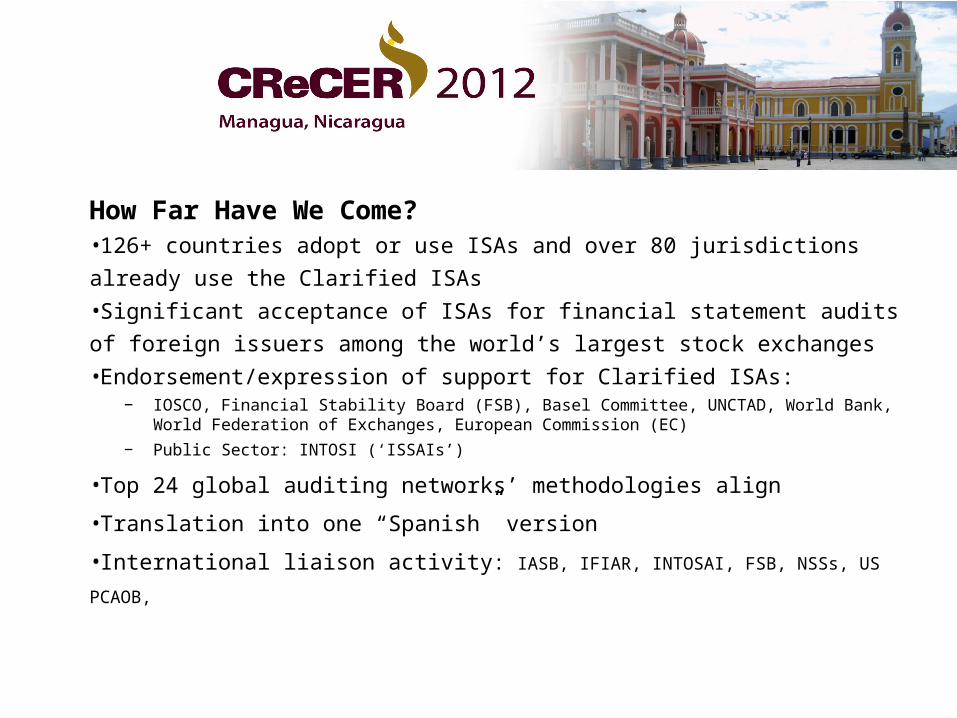

How Far Have We Come?•126+ countries adopt or use ISAs and over 80 jurisdictions already use the

Clarified ISAs

•Significant acceptance of ISAs for financial statement audits of foreign

issuers among the world’s largest stock exchanges

•Endorsement/expression of support for Clarified ISAs:− IOSCO, Financial Stability Board (FSB), Basel Committee, UNCTAD, World Bank, World

Federation of Exchanges, European Commission (EC)

− Public Sector: INTOSI (‘ISSAIs’)

•Top 24 global auditing networks’ methodologies align

•Translation into one “Spanish” version

•International liaison activity: IASB, IFIAR, INTOSAI, FSB, NSSs, US PCAOB,

Key Features of the Clarified ISAs•Principle-based and emphasize the use of professional judgment and professional skepticism, i.e., a “thinking audit”•Greater clarity, understandability and consistency of application

– New structure, conventions and obligations

•More robust with strengthened requirements in key areas:– Risk assessment (e.g., estimates and related parties)– Materiality and its use in evaluating misstatements– Audit evidence (e.g., confirmations and representations)– Using the work of others (e.g., group audits and experts)– Auditor reporting and communications (including with those charged with

governance)

Proportionality of ISAs for SME/SMPs•Application of ISAs designed to be proportionate in view of size, nature and complexity of entities

− Proportionality ≠ modification of requirements

•Requirements are not prescriptive − Application material highlights specific SME considerations and alternative

procedures

•IAASB Staff Questions and Answers (Staff Q&A)• Applying ISAs Proportionately with the Size and Complexity of an Entity• Applying ISQC 1 Proportionately with the Nature and Size of a Firm (to be released

end of October/early November 2012)

•IFAC SMP Committee’s Guides− Using ISAs in the Audits of SMEs− Quality Control for SMPs, etc.

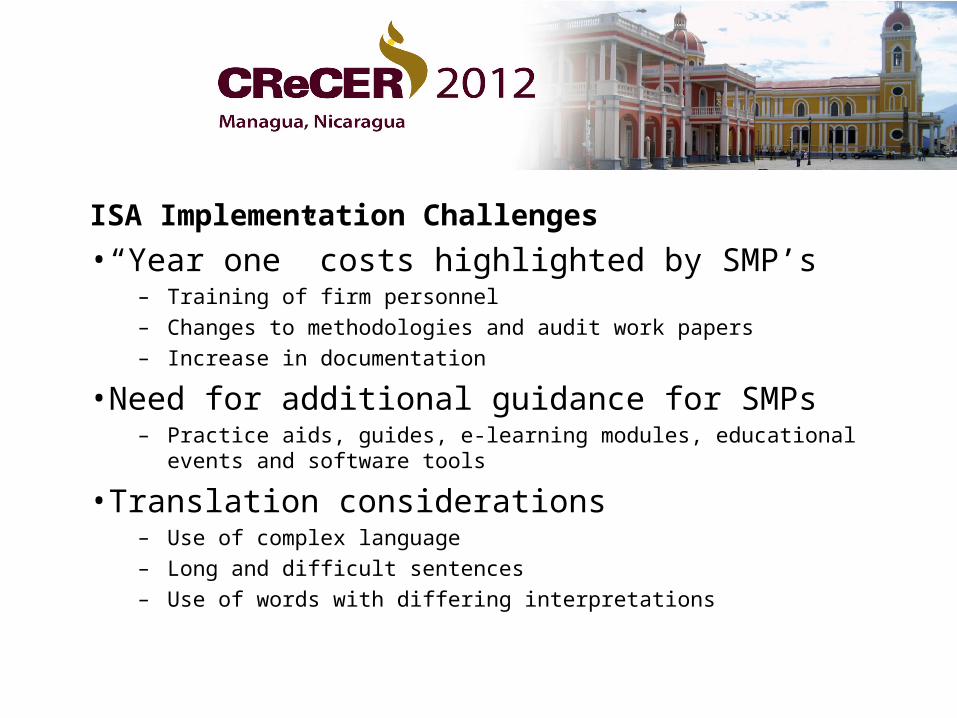

ISA Implementation Challenges

•“Year one” costs highlighted by SMP’s– Training of firm personnel– Changes to methodologies and audit work papers– Increase in documentation

•Need for additional guidance for SMPs– Practice aids, guides, e-learning modules, educational events and software

tools

•Translation considerations– Use of complex language– Long and difficult sentences– Use of words with differing interpretations

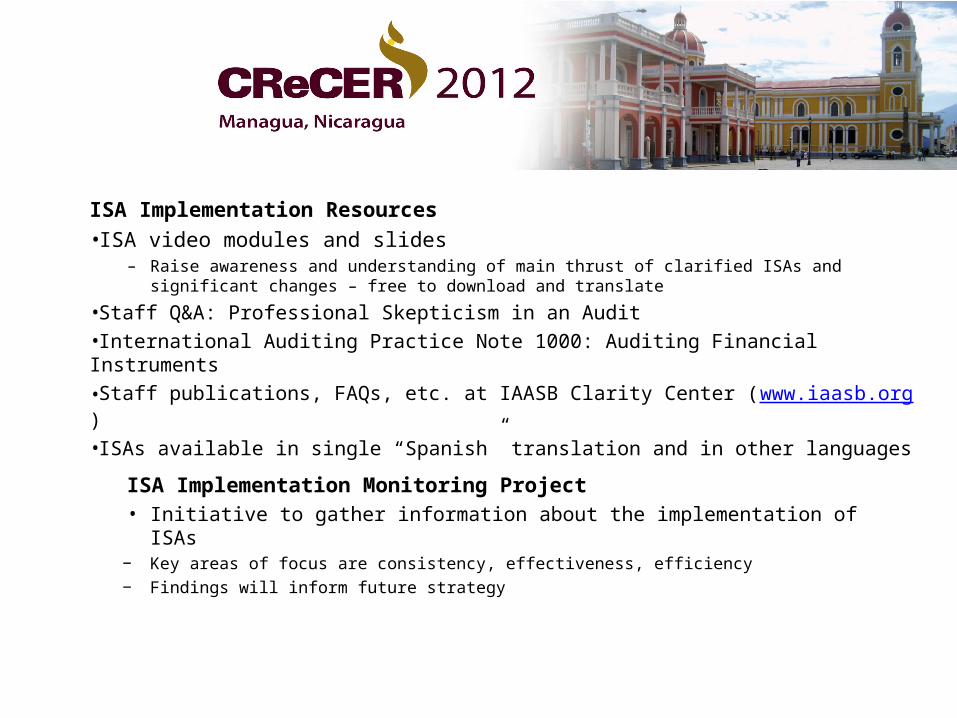

ISA Implementation Resources•ISA video modules and slides

– Raise awareness and understanding of main thrust of clarified ISAs and significant changes – free to download and translate

•Staff Q&A: Professional Skepticism in an Audit•International Auditing Practice Note 1000: Auditing Financial Instruments•Staff publications, FAQs, etc. at IAASB Clarity Center (www.iaasb.org)•ISAs available in single “Spanish” translation and in other languages

ISA Implementation Monitoring Project• Initiative to gather information about the implementation of ISAs

− Key areas of focus are consistency, effectiveness, efficiency− Findings will inform future strategy

Recent New or Revised Standards and Releases•Audits of Financial Statements

– Using the Work of Internal Auditors (Revised ISA 610)(Dec 2011)– Disclosures (Feedback Statement) (Jan 2012)

•Assurance Engagements and Related Services– Compilation of Pro Forma Information Included in a Prospectus (New ISAE

3420) (Sept 2011)– Greenhouse Gas Statements (New ISAE 3410) (March 2012)

•Other Assurance and Related Services Focused on SME Needs

– Review Engagements (Revised ISRE 2400 (June 2012)– Compilation Engagements (Revised ISRS 4410) (Dec 2011)

IAASB Projects and Initiatives•Current Projects

– Auditor Reporting: key priority for 2012 - 2014

– Auditing Disclosures (project proposal Q3 2012)

– Auditor Responsibilities relating to Other information (ED Q3 2012)

– Audit Quality (consultation paper Q4 2012)

– ISA Implementation Monitoring

– Assurance Engagements (“ISAE 3000”) (post-ED, first read Q4 2012)

• IAASB Strategy and Work Program 2012-2014– Revision of agreed-upon procedures (ISRE 4400)

– Estimates/fair values (ISAs 540/500), Banking, etc.

– Working group to monitor developments in integrated reporting, corporate governance, internal control, etc.