Breaking down the barriers to interest rate · PDF fileIn fact, increasing a scheme’s...

4

Breaking down the barriers to interest rate hedging

-

Upload

phungduong -

Category

Documents

-

view

213 -

download

0

Transcript of Breaking down the barriers to interest rate · PDF fileIn fact, increasing a scheme’s...

Breaking down the barriers to interest rate hedging

Interest rate risk is one of the biggest financial risks that pension schemes face. Yet, still the vast majority of schemes have not taken sufficient measures to adequately address this risk. Why? There are a number of reasons cited, but do they all hold true today? This short note aims to break down the common barriers to interest rate hedging and calls trustees to action to mitigate this risk.

Understanding your risksTrustees have for some time been aware of the significant equity risk and interest rate risk within their schemes as they have witnessed a, seemingly, ever-increasing level of volatility in their funding levels. Many schemes have taken, and continue to take, measures to protect against equity market risk by diversifying their growth assets and acting more nimbly. However, taking action to build or extend interest rate protection has often stalled in the education, the planning or even the implementation stages.

Interest rate risk is one of a pension scheme’s biggest risks. It refers to a change in a scheme’s funding position due to a change in the level of long term interest rates (usually measured by gilt yields). Hedging this interest rate risk, by investing in assets whose value moves in the same way as the liabilities, allows trustees to manage this risk.

Inflation risk also impacts a scheme’s funding level and should also be addressed. However, to hedge or not to hedge the interest rate risk has been of considerable debate and therefore is the focus of this note. Even for those pension schemes that have taken action, the level of hedge is usually somewhat below their strategic long term targets leaving a large number of pension schemes exposed more than they regard as ideal. Whilst individual considerations are key we believe that, on average, closed and frozen schemes should be hedging at least 70% of their interest rate risk — and even higher for inflation risk — as measured by liabilities. How much are you hedging?

What are the barriers to hedging? There are differing reasons for not hedging interest rate risk including:

scheme size and complexity of the investment tools

affordability and the need to invest in return seeking assets

historic low levels of interest rates

Breaking down the barriers to interest rate hedging

Scheme size and complexityOver the last decade the market has changed considerably. It used to be the case that only the largest schemes were able to access the investment tools necessary to efficiently hedge interest rate risk. Nowadays, with the widespread availability of pooled funds, a scheme of any size can access the investment tools to increase interest rate hedging with capital efficiency. We appreciate that the concepts involved with these investment tools can appear quite complex. However, this can be overcome with the right support and training.

Scheme size and complexity are barriers that can be overcome by trustees with the right support to develop an optimal solution.

Affordability and the need to invest in return seeking assetsBy improving the capital efficiency of your scheme’s matching portfolio, increasing the level of hedging does not have to mean reducing future returns. In fact, increasing a scheme’s interest rate and inflation hedge whilst retaining its growth allocation will maintain return expectations and reduce risk.

Increasing hedging does not have to mean reducing return.

Historic low levels of interest ratesOver the last few years we have seen gilt yields fall to record lows. At the beginning of 2013, it was a common view (and one shared by Aon Hewitt) that gilt yields would rise in the long term; this would see the value of liabilities decrease. On this basis, many trustee boards concluded any significant hedging should be delayed.

What has changed?

However, over 2013 we saw a significant rise in gilt yields and, more importantly, a significant rise in future interest rate expectations. Looking forward, the market consensus is for a gradual rise in gilt yields as the economy gradually improves and short term rates gradually rise.

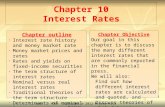

When you de-risk and hedge some of your interest rate risk, you effectively lock into a certain interest rate, typically that on gilts or swaps. As the chart above shows, you can presently lock into expected future gilt yields that are above 4%. This wasn’t the case a year ago.

The increase that the market is pricing in, on a 3 year time frame, is broadly in line with Aon Hewitt’s outlook. However, over a 5 year period we expect yields to rise by 0.5% more than the market is currently pricing in. This could be an argument for leaving a proportion of interest rate risk unhedged at this point.

On the other hand, there remains significant uncertainty and yields will not necessarily rise — they could indeed fall, stay flat, or rise by less than the market expects. In each of these three scenarios your funding level would fall. By how much will depend on your level of interest rate hedging. If yields rise in line with market expectations you will be no better or worse off by hedging today.

Trustees have been holding off putting in place interest rate protection until rates rise, but you can now lock into future expected gilt yields that are above 4%. By not hedging interest rates, schemes are vulnerable to yields falling, staying flat or rising by less than the market expects.

What next?Many trustees are currently running a lot of interest rate risk, which may be an optimal risk portfolio for those not overly concerned with funding level fluctuations in the short term — perhaps due to an extremely strong covenant. However, there are many trustees and scheme sponsors who are concerned about short term volatility but who are still running significant risks in their portfolios.

The key question is: what is preventing you increasing your hedge now?

3.4%

3.5%

3.6%

3.7%

3.8%

3.9%

4.0%

4.1%

4.2%

4.3%

Current In 1 year In 3 years In 5 years

These yields areover 4% which is a much better

level than a year ago!

How high will gilt yield go?

(20 year duration gilt yield expected in the market)

Disclaimer

Nothing in this document should be treated as an authoritative statement of the law on any particular aspect or in any specific case. It should not be taken as financial advice and action should not be taken as a result of this document alone. Unless we provide express prior written consent, no part of this document should be reproduced, distributed or communicated. This document is based upon information available to us at the date of this document and takes no account of subsequent developments. In preparing this document we may have relied upon data supplied to us by third parties and therefore no warranty or guarantee of accuracy or completeness is provided. We cannot be held accountable for any error, omission or misrepresentation of any data provided to us by any third party. This document is not intended by us to form a basis of any decision by any third party to do or omit to do anything. Any opinion or assumption in this document is not intended to imply, nor should be interpreted as conveying, any form of guarantee or assurance by us of any future performance or compliance with legal, regulatory, administrative or accounting procedures or regulations and accordingly we make no warranty and accept no responsibility for consequences arising from relying on this document.

Copyright © 2014 Aon Hewitt Limited Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales. Registered No: 4396810. Registered Office: 8 Devonshire Square, London EC2M 4PL

OS 33916 02.14