Brazil: Economic and Monetary Outlook · 1 Tiago Berriel Deputy Governor for International Affairs...

43

1 Tiago Berriel Deputy Governor for International Affairs and Corporate Risk Management JP Morgan Investor Seminar Washington, USA April 21 st , 2017 Brazil: Economic and Monetary Outlook

Transcript of Brazil: Economic and Monetary Outlook · 1 Tiago Berriel Deputy Governor for International Affairs...

1

Tiago BerrielDeputy Governor for International Affairs

and Corporate Risk Management

JP Morgan Investor Seminar

Washington, USA

April 21st, 2017

Brazil: Economic and Monetary Outlook

2

1. International Context and External Sector

2. Growth Dynamics: stabilization and signals of recovery

3. Monetary Policy

4. Structural Reforms and Resilience

3

• Positive outlook for global economic activity, despite underlying uncertainty• US tightening with limited impacts on global yields• Mitigating factors for some EMEs:

• Terms of trade and commodity prices, despite recent volatility;• Resilient capital flows and asset prices;• Growth Stimulus in G4 with low inflationary risks: Europe and Japan

• Risks:• Sustainability of current growth momentum.• Commodities prices volatility• Faster than expected MP tightening in advanced economies• Protectionism and global growth• Outlook for Chinese economy

International Context: uncertainty and mitigating factors for some EMEs

4

Source: Thomson Reuters Datastream

Sovereign Bonds – 2 year (G4) Sovereign Bonds – 10 year (G4)

US tightening with limited impacts on global yields

5

Market Indicators

US Elections

Skew Index vs VIX

Brexit

Skew IndexVIX (RH Scale)

Source: Thomson Reuters Datastream

6

Emerging Markets and US Corporative Spreads

6

High Yield Spread*

Emerging Markets Corporate Spread*

Source: Thomson Reuters Datastream

7

CDS Sovereigns5 year

Stock Markets – Emerging Economies01/01/10 = 100

EME benefiting from better risk perception

Source: Thomson Reuters Datastream

8

Commodity prices

Iron OrePetroleumBrent & WTI

Source: Thomson Reuters Datastream

9

• The global outlook coincides with a period of economicstabilization in the Brazilian economy, and improvement in itsfundamentals.

• Brazil is now less vulnerable to external shocks.

Brazil in the International Context

1010

US$

bill

ion

Source: BCB *through April 19th

Brazil: International Reserves vs. FX Swap and Repo Lines or FX Loans

376.2

-17.8

1.3

-150

-100

-50

0

50

100

150

200

250

300

350

400

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

international reserves FX swap position repo lines + FX loan operations

11

79 75*

- 24 - 26*

- 150

- 100

- 50

-

50

100

150

2010 2011 2012 2013 2014 2015 2016 2017

FDI

CC

US$ BI

Source: BCB*Market Expectations – Focus Report, Apr 13th - 2017

Brazil: Current Account x FDI

1212

12m until Feb/17

Exports/GDP

Total exports 10.1%

Latin America and the Caribbean 1.8%

European Union 1.8%

Asia (ex-ME and China) 1.3%

USA 1.3%

China 2.0%

others 1.8%

Mar/16 – Feb/17: US$191.0 billion

Apr/16 – Mar/17: US$195.1 billion

Apr/16 – Mar/17

Latin America and the

Caribbean18,1%

EU17,4%

Asia (ex-ME and China)

12,9%

US12,3%

China21,6%

others17,6%

Brazil: Exports by Destination

Source: BCB

1313

External Vulnerability Indicators (% of GDP)

Net external debt Total external debt International reserves Current transactions

Reduction of External Vulnerability

Source: BCB, National Treasury Secretariat

14

% %%

12,4

12,7

13,8

13,8

13,9

14,1

14,2

14,3

14,5

14,8

15,5

15,6

16,2

17,1

17,9

18,0

0 5 10 15 20

Russia

India

Australia

Canada

South Africa

USA

Korea

Spain

Mexico

Italy

Japan

Turkey

Brazil

France

UK

Germany

Capital Adequacy Ratio

-32,3

-24,0

-18,0

-8,3

-7,2

-5,8

-4,5

-3,9

-3,8

4,6

12,0

14,3

17,0

-50 -40 -30 -20 -10 0 10 20

Spain

Japan

South Africa

Australia

USA

Canada

UK

Turkey

Korea

Mexico

Brazil

Russia

India

(Provisions – NPL) / Capital

24,6

33,4

36,8

38,7

39,3

44,5

47,7

69,6

91,2

93,1

118,4

121,8

153,1

195,2

0 70 140 210

India

South Africa

UK

Japan

Australia

Mexico

Canada

Turkey

USA

Italy

Korea

Russia

Germany

Brazil

Liquid Assets to Short Term Liabilities

Financial Soundness Indicators

Source: FMI (FSI) – latest available data

15

1. International Context and External Sector

2. Growth Dynamics: stabilization and signals of recovery

3. Monetary Policy

4. Structural Reforms and Resilience

16

• Recovery in businessmen confidence indexes

• Monetary Policy easing cycle

• Deleveraging process well advanced

• Strong growth in agricultural sector

• Infrastructure Concessions. Asset Sales and Privatization Agenda. Concessions tothe Private Sector: Logistics Investment Program (PIL) and Infrastructure Workswith regulatory stability

• Business Climate improvement and efficiency and productivity gains

• Structural Reforms (government expenditure cap, social security, tax and laborreforms)

Stabilization and signs of gradual recovery

17

80

84

88

92

96

100

104

108m

ai 1

3

jul 1

3

set

13

no

v 1

3

jan

14

mar

14

mai

14

jul 1

4

set

14

no

v 1

4

jan

15

mar

15

mai

15

jul 1

5

set

15

no

v 1

5

jan

16

mar

16

mai

16

jul 1

6

set

16

no

v 1

6

jan

17

Industrial Production

20

12

=10

0, s

.a.

132

134

136

138

140

142

144

146

148

150

ago

13

no

v 1

3

fev

14

mai

14

ago

14

no

v 1

4

fev

15

mai

15

ago

15

no

v 1

5

fev

16

mai

16

ago

16

no

v 1

6

fev

17

IBC-BR Index

3mma

montly

Industrial Production and IBC-BR Index

Source: IBGE

18

%

Sources: BCB / IBGE *Market Expectations – Focus Survey of Apr 13th

4,0

1,9

3,0

0,5

-3,8 -3,6

0,40*

2,5* 2,5*

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

20

11

20

12

20

13

20

14

20

15

20

16

20

17

*

20

18

*

20

19

*

GDP Real Growth

19

Source: FGVObs.: proportion of favorable answers – proportion of unfavorable answers + 100

60

70

80

90

100

110

jun

13

ou

t 1

3

fev

14

jun

14

ou

t 1

4

fev

15

jun

15

ou

t 1

5

fev

16

jun

16

ou

t 1

6

fev

17

services

industry

3m

ma,

s.a

.

3m

ma,

s.a

.

60

70

80

90

100

110

jun

13

ou

t 1

3

fev

14

jun

14

ou

t 1

4

fev

15

jun

15

ou

t 1

5

fev

16

jun

16

ou

t 1

6

fev

17

construction

commerce

Agents’ Confidence - Businessmen

20

mill

ion

hec

tare

s, m

illio

nto

ns

Source: Conab

*average estimate in Apr 17

Production (1991-2016)

Growth: 222% = 4.8% / year

Cropped Area (1991-2016)

Growth: 54% = 1.7% / year

37,9

60,157,9

227,9

20

40

60

80

100

120

140

160

180

200

220

240

90/9

1

91/9

2

92/9

3

93/9

4

94/9

5

95/9

6

96/9

7

97/9

8

98/9

9

99/0

0

00/0

1

01/0

2

02/0

3

03/0

4

04/0

5

05/0

6

06/0

7

07/0

8

08/0

9

09/1

0

10/1

1

11/1

2

12/1

3

13/1

4

14/1

5

15/1

6

16/1

7*

Grains, Production and Cropped Area

21

% o

fin

com

eHousehold Debt

17

22

27

32

37

42

47

jan

08

jul 0

8

jan

09

jul 0

9

jan

10

jul 1

0

jan

11

jul 1

1

jan

12

jul 1

2

jan

13

jul 1

3

jan

14

jul 1

4

jan

15

jul 1

5

jan

16

jul 1

6

jan

17

debt debt ex-housing credit

Deleveraging Process (I)

Source: BCB

22

% o

fin

com

eDebt Service

17

18

19

20

21

22

23

jan

08

jul 0

8

jan

09

jul 0

9

jan

10

jul 1

0

jan

11

jul 1

1

jan

12

jul 1

2

jan

13

jul 1

3

jan

14

jul 1

4

jan

15

jul 1

5

jan

16

jul 1

6

jan

17

debt service, s.a.

Deleveraging Process (II)

Source: BCB

23

% p

.a.

11,25

7

8

9

10

11

12

13

14

15

ou

t 11

ab

r 1

2

ou

t 12

ab

r 1

3

ou

t 13

ab

r 1

4

ou

t 14

ab

r 1

5

ou

t 15

ab

r 1

6

ou

t 16

ab

r 1

7

Selic Rate

Source: BCB

24

mill

ion

s

R$

, in

rea

l ter

ms

formal employees(accumulated in 12 months)

average salary(12-month average)

14

15

16

17

18

19

20

21

22fe

v 1

0

fev 1

1

fev 1

2

fev 1

3

fev 1

4

fev 1

5

fev 1

6

fev 1

7dismissals admissions

1.200

1.250

1.300

1.350

1.400

1.450

1.500

1.550

1.600

1.650

fev

10

fev

11

fev

12

fev

13

fev

14

fev

15

fev

16

fev

17

admissions dismissals

Admissions and Dismissals vs. Salaries

Sources: MTPS (CAGED) / IBGE (INPC)

25

1. International Context and External Sector

2. Growth Dynamics: stabilization and signals of recovery

3. Monetary Policy

4. Structural Reforms and Resilience

26

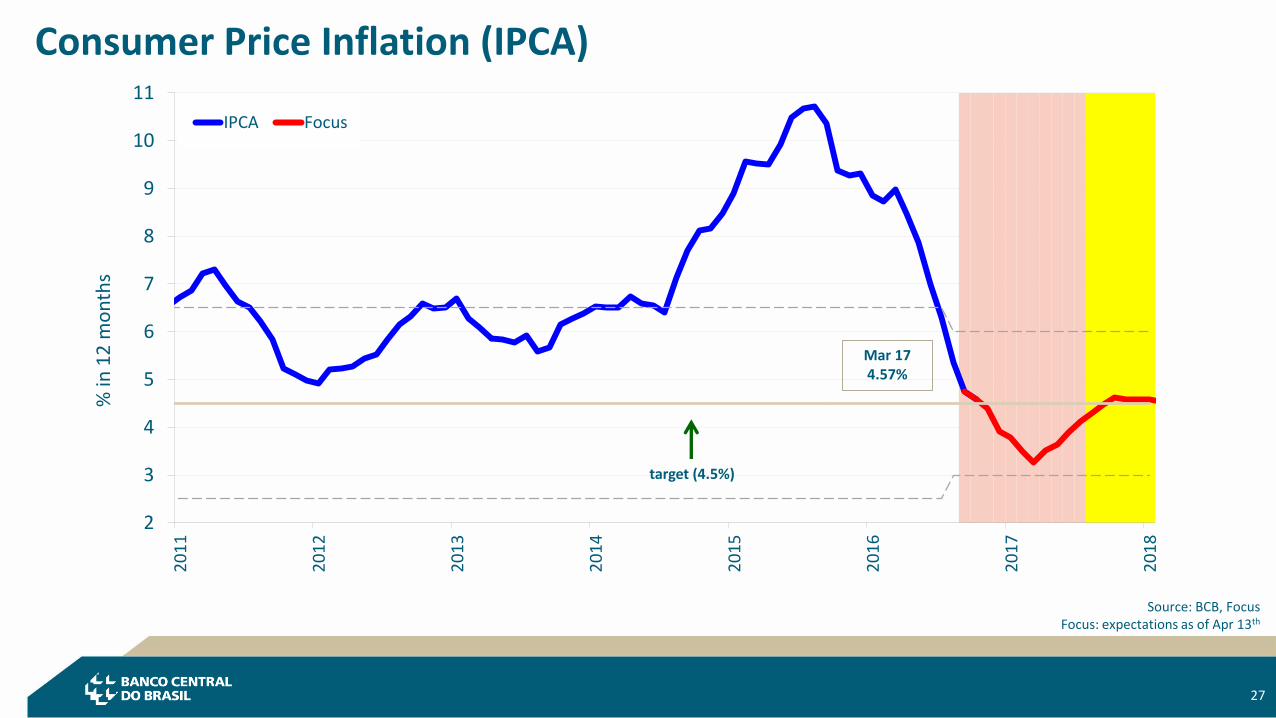

• Consolidation of a disinflation for inflation components that are most sensitiveto the economic cycle and to monetary policy justified a moderateintensification of the monetary easing process. The Committee judged thepace of 100bps adequate.

• IPCA diffusion indexes exhibited a relatively large drop in recent months

• Favorable inflation dynamics, with widespread disinflation, lower persistenceand expectations well anchored in longer horizons.

Monetary Policy Outlook: Inflation and current easing cycle

27

2

3

4

5

6

7

8

9

10

11

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

IPCA Focus

target (4.5%)

Mar 174.57%

% in

12

mo

nth

s

Source: BCB, FocusFocus: expectations as of Apr 13th

Consumer Price Inflation (IPCA)

28

Mar 175.6

Mar 174.3

0

2

4

6

8

10

12

14

16

18

20ju

n 1

0

dez

10

jun

11

dez

11

jun

12

dez

12

jun

13

dez

13

jun

14

dez

14

jun

15

dez

15

jun

16

dez

16

20

17

IPCA regulated prices IPCA market prices

y-o

-y c

han

ge(%

)

Sources: BCB, IBGE

*as of April 13th

IPCA Regulated Prices (%)2015 18.072016 5.50mkt expectations 2017* 5.50

IPCA Market Prices (%)2015 8.512016 6.54mkt expectations 2017* 3.60

marketexpectations*

Market, Regulated and Food Prices

29

% in

12

mo

nth

s

%

IPCA Diffusion Index

4

5

6

7

8

9

10

11

jul 14

nov 1

4

ma

r 1

5

jul 15

nov 1

5

ma

r 1

6

jul 16

nov 1

6

ma

r 1

7

IPCA smoothed trimmed means

exclusion of regulated prices and household food double weight

50

55

60

65

70

75

80

jul 14

nov 1

4

ma

r 1

5

jul 15

nov 1

5

ma

r 1

6

jul 16

nov 1

6

ma

r 1

7

monthly

IPCA – Headline, Cores and Diffusion Index

Source: IBGE

30

3

4

5

6

7

8

9

10

11

12

Mar2010

Mar2011

Mar2012

Mar2013

Mar2014

Mar2015

Mar2016

Mar2017

12

m V

aria

tio

n (

%)

12M Inflation – Underlying Services(*)

Underlying Services - 12M 3M Dessaz

Source: BCB(*) Overall services excluding domestic services, courses, communication and tourism.

Services Prices Path (CPI-IPCA): Underlying Component (moving average)

31

0

2

4

6

8

10

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

% in

12

mo

nth

sScenario with Focus Selic and Exchange Rates

Conditional Inflation Forecasts

Source: BCB

32

1. International Context and External Sector

2. Growth Dynamics: stabilization and signals of recovery

3. Monetary Policy

4. Structural Reforms and Resilience

33

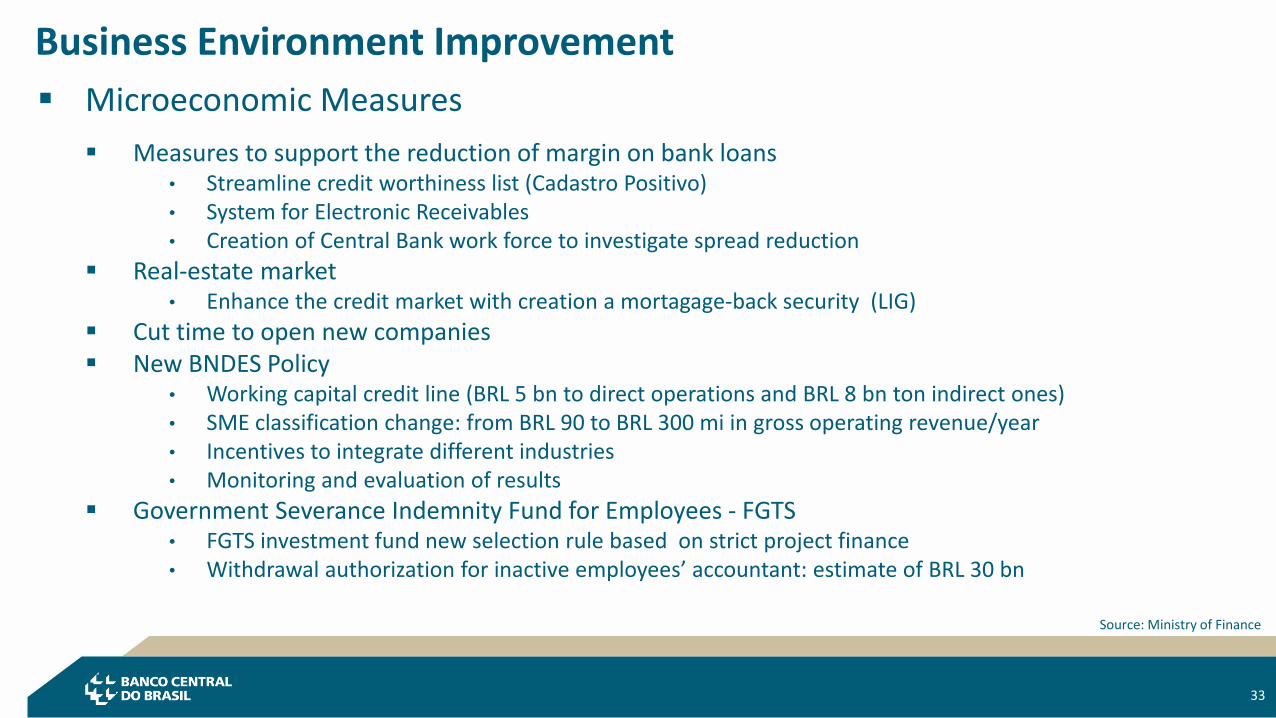

Microeconomic Measures

Measures to support the reduction of margin on bank loans• Streamline credit worthiness list (Cadastro Positivo)• System for Electronic Receivables• Creation of Central Bank work force to investigate spread reduction

Real-estate market• Enhance the credit market with creation a mortagage-back security (LIG)

Cut time to open new companies New BNDES Policy

• Working capital credit line (BRL 5 bn to direct operations and BRL 8 bn ton indirect ones)• SME classification change: from BRL 90 to BRL 300 mi in gross operating revenue/year• Incentives to integrate different industries• Monitoring and evaluation of results

Government Severance Indemnity Fund for Employees - FGTS• FGTS investment fund new selection rule based on strict project finance• Withdrawal authorization for inactive employees’ accountant: estimate of BRL 30 bn

Business Environment Improvement

Source: Ministry of Finance

34

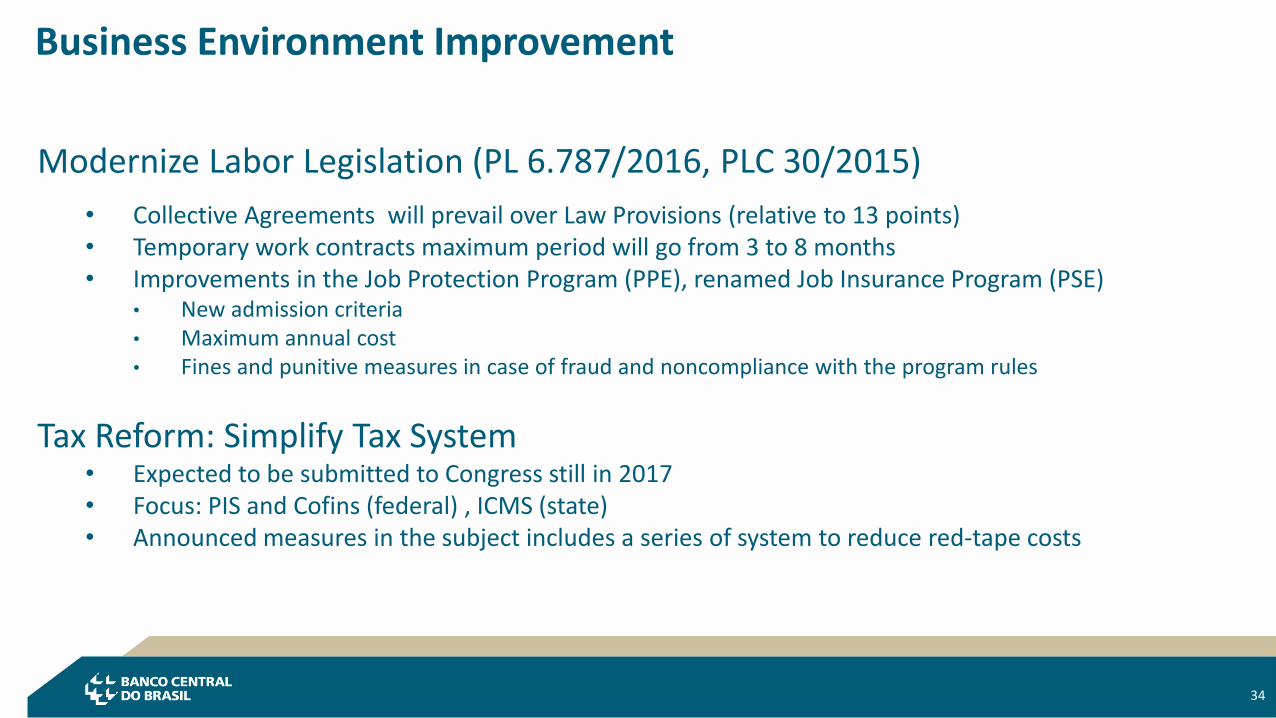

Modernize Labor Legislation (PL 6.787/2016, PLC 30/2015)

• Collective Agreements will prevail over Law Provisions (relative to 13 points)• Temporary work contracts maximum period will go from 3 to 8 months• Improvements in the Job Protection Program (PPE), renamed Job Insurance Program (PSE)

• New admission criteria• Maximum annual cost• Fines and punitive measures in case of fraud and noncompliance with the program rules

Tax Reform: Simplify Tax System• Expected to be submitted to Congress still in 2017• Focus: PIS and Cofins (federal) , ICMS (state)• Announced measures in the subject includes a series of system to reduce red-tape costs

Business Environment Improvement

35

- The main goal is to pursue a more efficient financial system, with more free market

credit, contributing to increase the power of monetary policy.

- Based on four Pillars:

I. Increase financial citizenship III. Improve legal framework

II. Increase financial system efficiency IV. Reduce cost of credit

Agenda BC+: lower neutral rate and higher MoP Effectiveness

36

• New economic policy involved a significant decrease in expansionary quasi-fiscalimpulses

• From the monetary policy standpoint, a more efficient financial system, with more freemarket credit, contributes to increase the power of monetary policy.

• Structural measures (Agenda BC+) aim to reach a sustainable reduction in overall costof credit, increasing economic efficiency and productivity, thereby helping monetarypolicy effectiveness

• New methodology for TLP (parameter for the remuneration system of directed credit)aligned with market rates favors monetary policy effectiveness.

Directed Credit, Quasi-Fiscal Impulses and Long Term Rates

37

34,3

37,538,9

36,3

33,532,0

33,5 32,5

36,438,4

39,541,1

44,5

47,849,1 49,9 50,2

0

5

10

15

20

25

30

35

40

45

50

55

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017*

% o

fto

tal c

red

it

Source: BCB

new methodology since Mar 07

*Feb/17

Earmarked Credit

38

Structural Fiscal Reform Agenda and Monetary Policy Effectiveness

• Persistent growth in expenditures caused a fiscal deterioration that eroded confidence.

• Structural Fiscal Reform Agenda is critical to bring fiscal equilibrium back, assuring public debt sustainability through a recovery in primary surpluses' horizon;

• Intertemporal consistency in fiscal policy is critical for monetary policy effectiveness, definitively removing uncertainty for longer horizons.

• Spending Ceiling - Constitutional Amendment was approved in October 2016.

• Social Security Reform is under sound debate in the society, and in advanced consideration in the Chamber, with expected examination in the floor by mid-May.

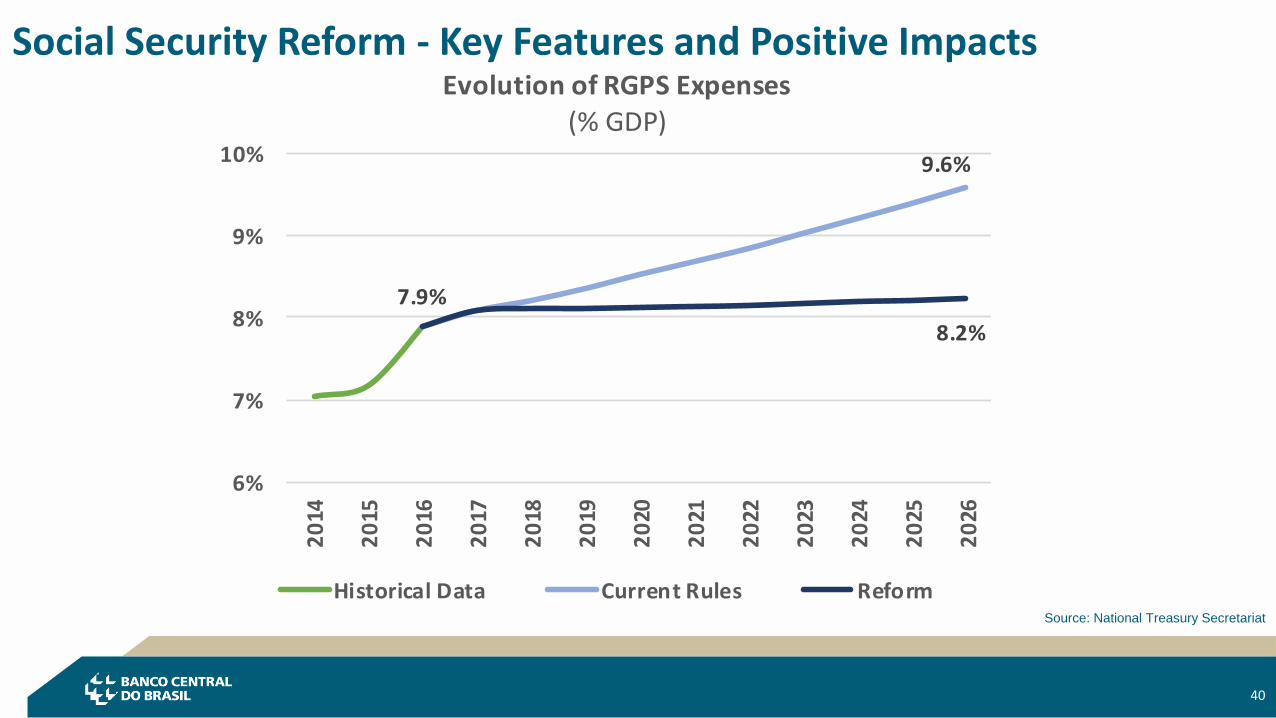

39

Spending Cap will anchor fiscal policy opening room for primary surpluses

Source: National Treasury Secretariat

Projection of Primary Expenditures with and without Expenditures Cap (% GDP)

40

Source: National Treasury Secretariat

9.6%

7.9%

8.2%

6%

7%

8%

9%

10%

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

Evolution of RGPS Expenses

(% GDP)

Historical Data Current Rules Reform

Social Security Reform - Key Features and Positive Impacts

41

• Positive outlook for global economic activity, but relevant global uncertainty and risks for EME (faster tightening in US, protectionism, Europe´s politics, Protectionism and global growth, and Outlook for Chinese economy)

• Brazil is resilient to external volatility and risks. Sound current account financing through FDI; Low overall exposure to forex liabilities including corporates; diversified trade ties (global trader) and financial system with solid capital structure and limited leverage.

• Monetary Policy easing, microeconomic reform agenda, and structural sound growth in agriculture favor a gradual growth recovery along 2017.

• Real and nominal interest rates are falling in Brazil. The policy rate (Selic) fell during the past few months and it is expected to fall further. The real interest rate have also receded.

Outlook for the Brazilian Economy: Conclusions (I)

42

• Favorable inflation dynamics, with widespread disinflation, lower persistence andexpectations well anchored for longer horizons

• Consolidation of a disinflation for inflation components that are most sensitive to theeconomic cycle and to monetary policy justified a moderate intensification of themonetary easing process. The Committee judged the pace of 100bps adequate.

• Structural Fiscal Reform Agenda is critical to assure public debt sustainability, definitively removing uncertainty for longer horizons. Spending Ceiling was approved in Oct/16, and the Social Security Reform is under advanced consideration in Congress.

Outlook for the Brazilian Economy: Conclusions (II)

43

Thank You!

43

Tiago BerrielDeputy Governor for International Affairs

and Corporate Risk Management