BrasilAgro 2010 Corporate Presentation Slides Deck PPT

35

February, 2010

-

Upload

ala-baster -

Category

Documents

-

view

220 -

download

0

Transcript of BrasilAgro 2010 Corporate Presentation Slides Deck PPT

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 1/35

February, 2010

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 2/35

22

Disclaimer – Forward-Looking Statements

This presentation may contain certain forward-looking statements and information relating to

BrasilAgro - Companhia Brasileira de Propriedades Agrícolas (“BrasilAgro” or the “Company”)

that reflect the current views and/or expectations of the Company and its management withrespect to its business plan. Forward-looking statements include, without limitation, any

statement that may predict, forecast, indicate or imply future results, performance or

achievements, and may contain words like “believe”, “anticipate”, “expect”, “envisage”, “will

likely result”, or any other words or phrases of similar meaning. Such statements are subject to

a number of significant risks, uncertainties and assumptions. We caution that a number of

important factors could cause actual results to differ materially from the plans, objectives,

expectations, estimates and intentions expressed in this presentation. In any event, neither the

Company nor any of its affiliates, directors, officers, agents or employees shall be liable before

any third party (including investors) for any investment or business decision made or action

taken in reliance on the information and statements contained in this presentation or for any

consequential, special or similar damages. The Company does not intend to provide eventual

holders of shares with any revised forward-looking statements of analysis of the differences

between any forward-looking statements and actual results.

This presentation and its contents are proprietary information and may not be reproduced or

otherwise disseminated in whole or in part without BrasilAgro‟s prior written consent.

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 3/35

33

Introduction to BrasilAgro

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 4/35

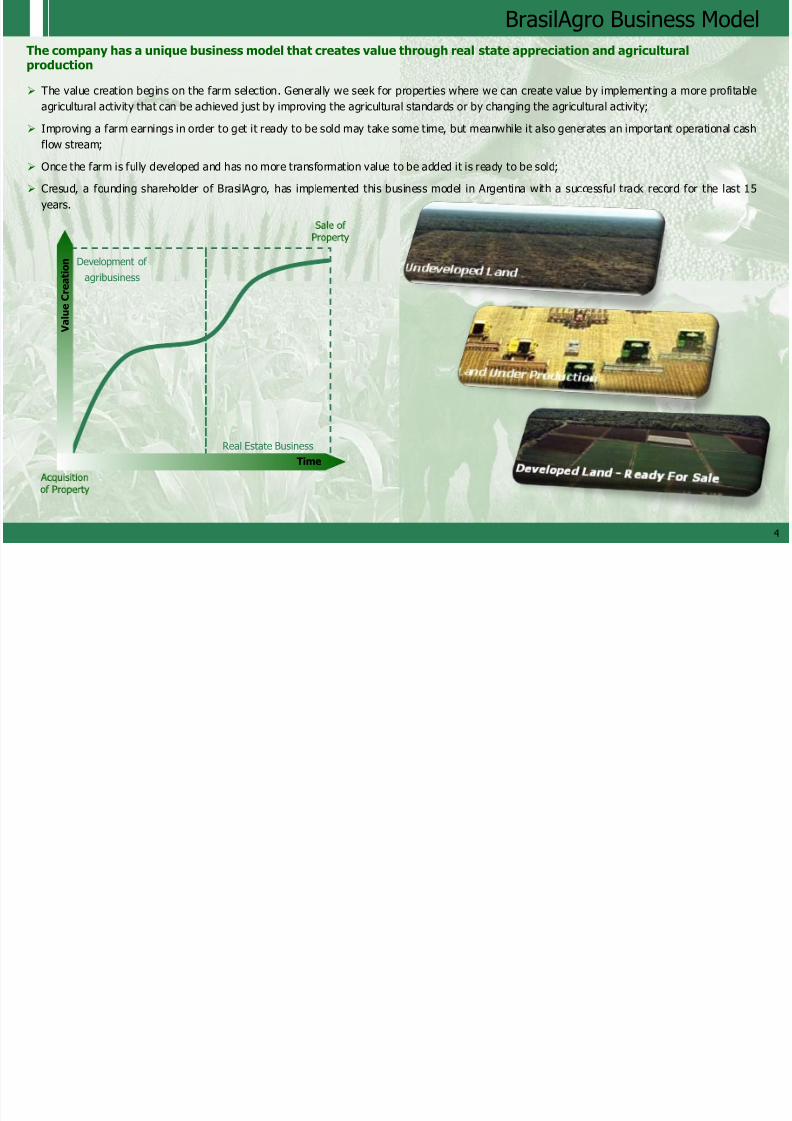

BrasilAgro Business Model

4

Development of

agribusiness

Real Estate Business

The company has a unique business model that creates value through real state appreciation and agriculturalproduction

The value creation begins on the farm selection. Generally we seek for properties where we can create value by implementing a more profitable

agricultural activity that can be achieved just by improving the agricultural standards or by changing the agricultural activity;

Improving a farm earnings in order to get it ready to be sold may take some time, but meanwhile it also generates an important operational cash

flow stream;

Once the farm is fully developed and has no more transformation value to be added it is ready to be sold;

Cresud, a founding shareholder of BrasilAgro, has implemented this business model in Argentina with a successful track record for the last 15

years.

V a l u e

C r e a t

i o n

Time

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 5/35 55

Mr. Elie Horn

(Cape Town LLC)

Founders

(1) As of Feb 18th 2010 (Bloomberg)

Cresud was founded in 1935, went public in Buenos Aires stock exchange

in 1960 and Nasdaq in 1997

One of the largest holders of farmland in Argentina: over 760 thousand ha

in 17 properties located in one of the most fertile areas in the world

Producer of soybean, corn, wheat, sunflower, beef and milk

Value drivers: agricultural activities and complementary rural real estate

operations

Mr. Elie Horn is Chairman of the Board, CEO and controlling shareholder o

Cyrela Brazil Realty S.A. (“Cyrela”)

Cyrela (CYRE3) is one of the most recognized and largest player in Brazil‟scommercial and residential real estate markets

Cyrela has built a track record of sound investment and steady growth

Cyrela‟s market cap. of approx. US$5.5 billion(1)

Founded in 2002, Tarpon is one of the largest Brazilian independent asset

managers dedicated to long term equity investments in South America

Over US$1.4 billion under management Its fund‟s investor base profile is composed of US Endowments, Pension

Plan and SWFs

Tarpon‟s market cap. of approx. US$168.7 million(1) (TRPN3)

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 6/35 66

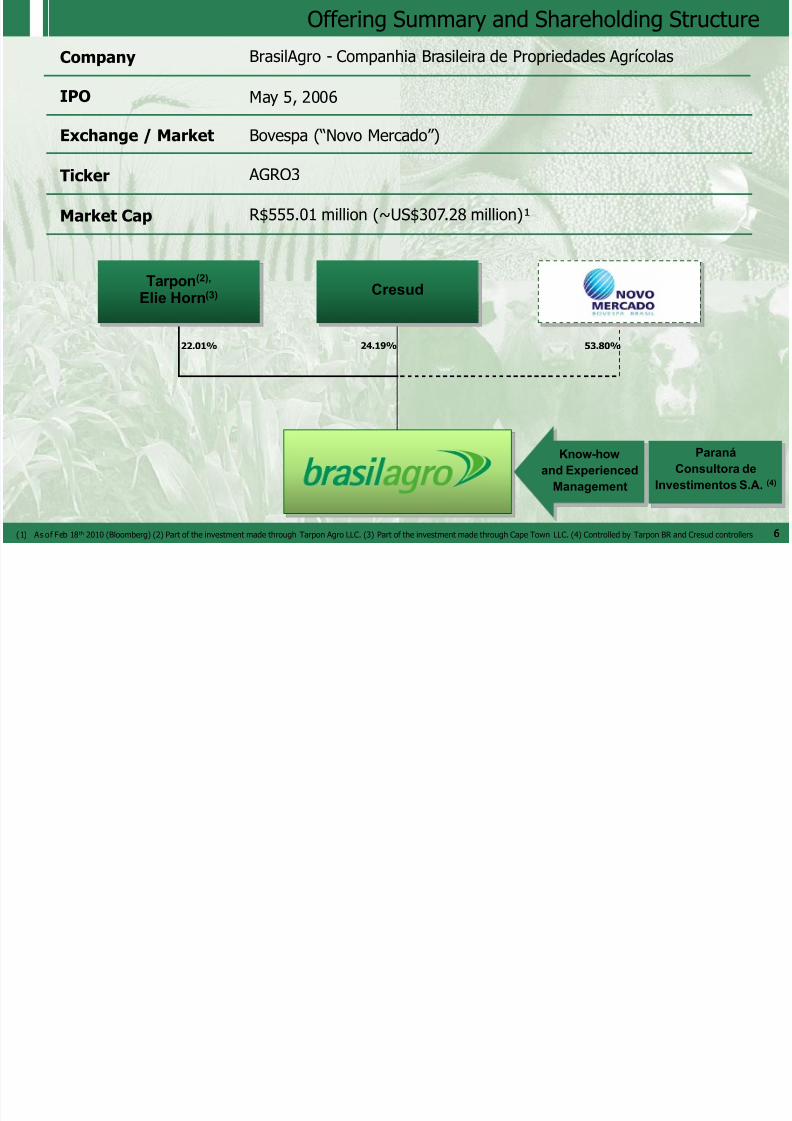

Offering Summary and Shareholding Structure

Exchange / Market Bovespa (“Novo Mercado”)

IPO May 5, 2006

Market Cap

Ticker AGRO3

R$555.01 million (~US$307.28 million)¹

(1) As of Feb 18th 2010 (Bloomberg) (2) Part of the investment made through Tarpon Agro LLC. (3) Part of the investment made through Cape Town LLC. (4) Controlled by Tarpon BR and Cresud controllers

Paraná

Consultora de

Investimentos S.A. (4)

22.01% 24.19% 53.80%

Know-how

and Experienced

Management

Tarpon(2),

Elie Horn(3) Cresud

Company BrasilAgro - Companhia Brasileira de Propriedades Agrícolas

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 7/35

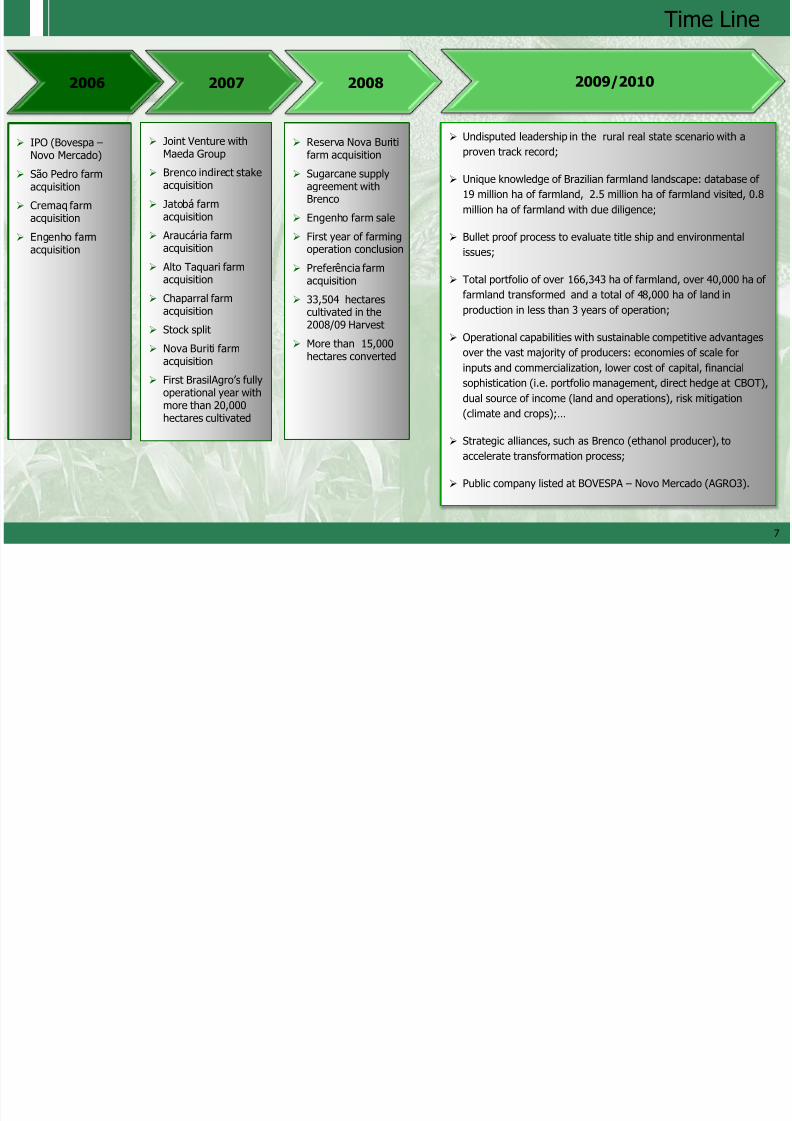

Time Line

7

Undisputed leadership in the rural real state scenario with aproven track record;

Unique knowledge of Brazilian farmland landscape: database of

19 million ha of farmland, 2.5 million ha of farmland visited, 0.8

million ha of farmland with due diligence;

Bullet proof process to evaluate title ship and environmental

issues;

Total portfolio of over 166,343 ha of farmland, over 40,000 ha offarmland transformed and a total of 48,000 ha of land in

production in less than 3 years of operation;

Operational capabilities with sustainable competitive advantages

over the vast majority of producers: economies of scale for

inputs and commercialization, lower cost of capital, financial

sophistication (i.e. portfolio management, direct hedge at CBOT),

dual source of income (land and operations), risk mitigation

(climate and crops);…

Strategic alliances, such as Brenco (ethanol producer), to

accelerate transformation process;

Public company listed at BOVESPA – Novo Mercado (AGRO3).

IPO (Bovespa –Novo Mercado)

São Pedro farmacquisition

Cremaq farmacquisition

Engenho farmacquisition

Joint Venture withMaeda Group

Brenco indirect stakeacquisition

Jatobá farmacquisition

Araucária farmacquisition

Alto Taquari farm

acquisition

Chaparral farmacquisition

Stock split

Nova Buriti farmacquisition

First BrasilAgro‟s fullyoperational year withmore than 20,000

hectares cultivated

Reserva Nova Buritifarm acquisition

Sugarcane supplyagreement withBrenco

Engenho farm sale

First year of farmingoperation conclusion

Preferência farm

acquisition

33,504 hectarescultivated in the2008/09 Harvest

More than 15,000hectares converted

2009/20102006 2007 2008

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 8/35 88

Sector Context

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 9/3599

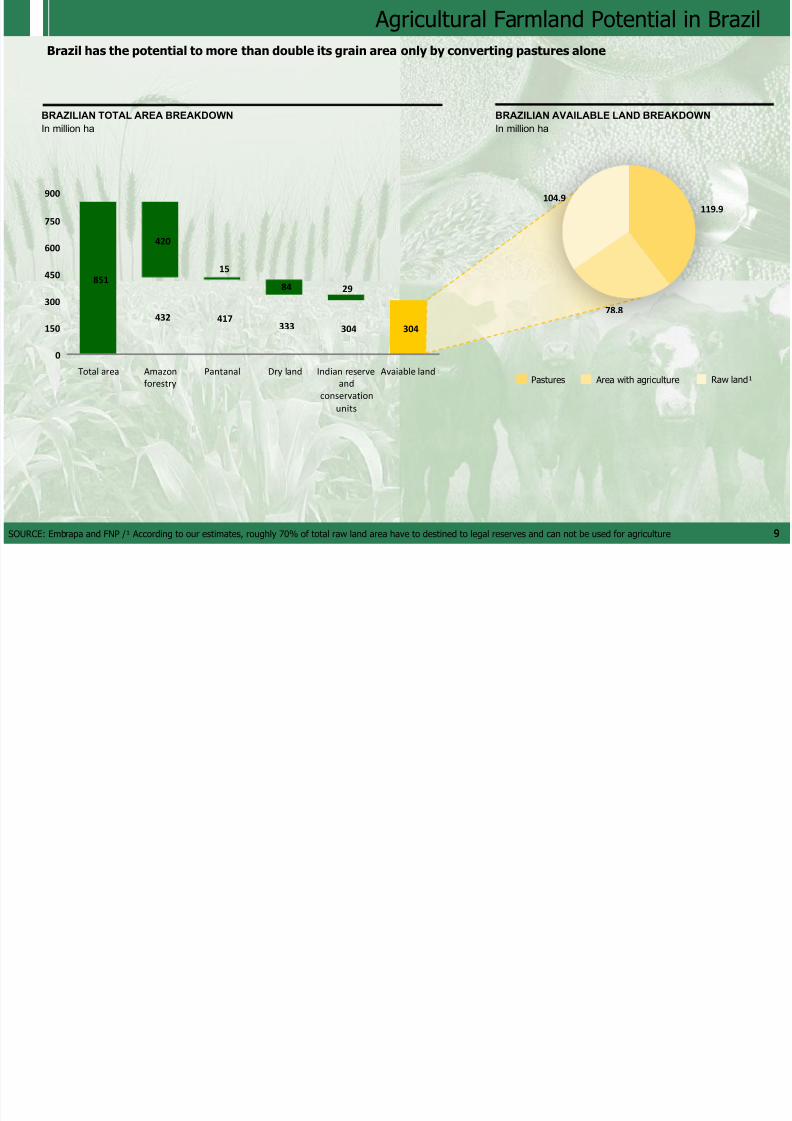

Agricultural Farmland Potential in Brazil

851

432 417333 304

420

15

84 29

304

0

150

300

450

600

750

900

Total area Amazon

forestry

Pantanal Dry land Indian reserve

and

conservation

units

Avaiable land

BRAZILIAN TOTAL AREA BREAKDOWN

In million ha

BRAZILIAN AVAILABLE LAND BREAKDOWN

In million ha

Pastures Area with agriculture Raw land¹

119.9

78.8

104.9

SOURCE: Embrapa and FNP /¹ According to our estimates, roughly 70% of total raw land area have to destined to legal reserves and can not be used for agriculture

Brazil has the potential to more than double its grain area only by converting pastures alone

l h ll l d f l

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 10/351010

Brazil has excellent natural conditions for agriculture

Climatic Factors

Stable temperature

Regular rainfall

(1) Source: Mapa, Embrapa as cited in Warnken (1999). (2) Cerrados (scrubland region in Brazil's Midwest).

Cerrados ( 2)

ParanaMato GrossoCorn Belt

Source: Calculated using data from Joint Agricultural Weather Facility, USDA and NOAA.

30

25

20

15

10

5

0

-5

-10

Sep Nov Jan Mar Mai JulOct Dec Feb Apr Jun Aug

Average monthly temperature (centigrade)

Abundant solar energy

Production season lasts entire year

S i L d P i E l ti i B il

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 11/35

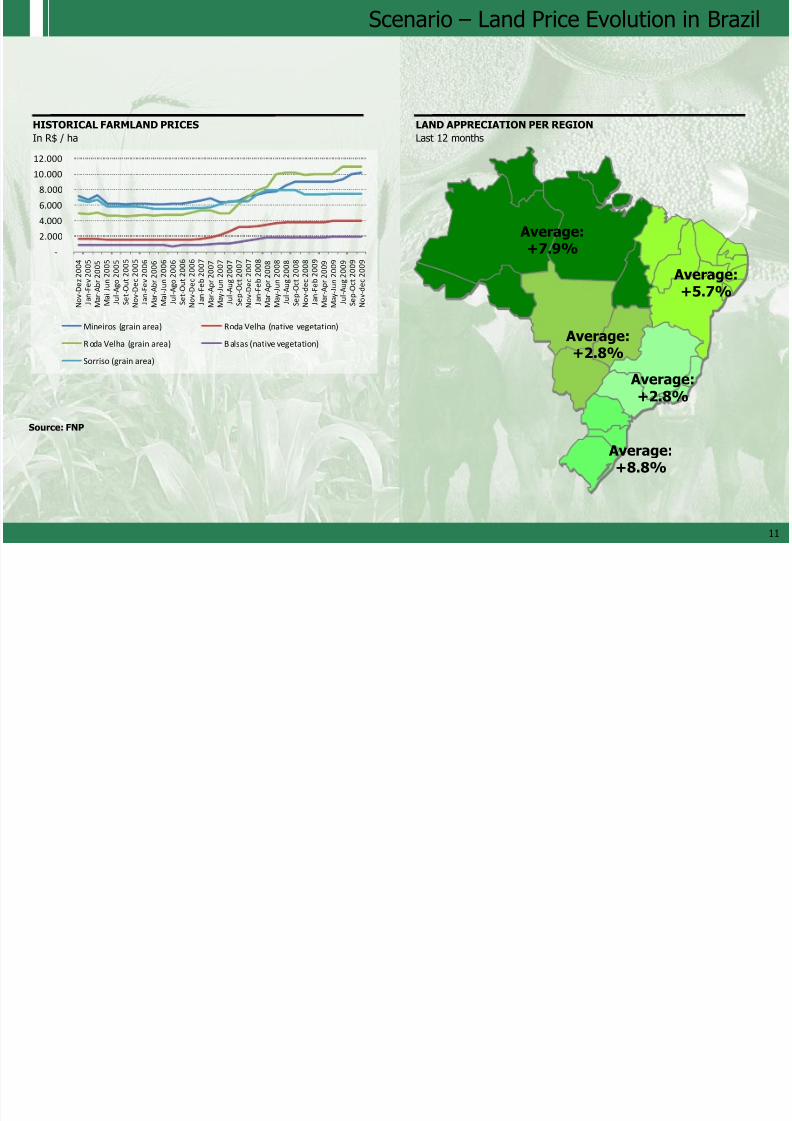

Scenario – Land Price Evolution in Brazil

1

LAND APPRECIATION PER REGION

Last 12 months

HISTORICAL FARMLAND PRICES

In R$ / ha

Source: FNP

Average:+7.9%

Average:+5.7%

Average:+2.8%

Average:+2.8%

Average:+8.8%

-

2.000

4.000

6.000

8.000

10.000

12.000

N o v - D e z 2 0 0 4

J a n - F e v 2 0 0 5

M a r - A b r 2 0 0 5

M a i - J u n 2 0 0 5

J u l - A g o 2 0 0 5

S e t - O u t

2 0 0 5

N o v - D e c

2 0 0 5

J a n - F e v 2 0 0 6

M a r - A b r 2 0 0 6

M a i - J u n 2 0 0 6

J u l - A g o 2 0 0 6

S e t - O u t

2 0 0 6

N o v - D e c

2 0 0 6

J a n - F e b

2 0 0 7

M a r - A p r 2 0 0 7

M a y - J u n 2 0 0 7

J u l - A u g 2 0 0 7

S e p - O c t 2 0 0 7

N o v - D e c

2 0 0 7

J a n - F e b

2 0 0 8

M a r - A p r 2 0 0 8

M a y - J u n 2 0 0 8

J u l - A u g 2 0 0 8

S e p - O c t 2 0 0 8

N o v - d e c

2 0 0 8

J a n - F e b

2 0 0 9

M a r - A p r 2 0 0 9

M a y - J u n 2 0 0 9

J u l - A u g 2 0 0 9

S e p - O c t 2 0 0 9

N o v - d e c

2 0 0 9

Mineiros (grain area) Roda Velha (native vegetation)

R oda Velha (grain area) B alsas (native vegetation)

Sorriso (grain area)

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 12/35

11

Strategy

B asilAg o St ateg

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 13/35

1313

Productivity directly related to technology investments

• Mechanization

• Soil correction

• Selected seeds

Aiming to achieve highest productivity and land appreciation

State-of-the Art

Agriculture

Long and successful track record of agricultural development

Expertise in Brazil‟s real estate market

Knowledge of financial markets with extensive experience inrisk management

Proven

Management

Practices

BrasilAgro Strategy

Acquire large areas of undeveloped farmland with appreciationpotential

Distressed and/or conversion strategy for developing properties

Sale of properties after development

Real Estate

Approach

Portfolio

Strategy

Investment portfolio diversification through different locationsand agricultural projects

Minimize potential risk effects (climate, prices, regions, etc…)

Lower risk, without decreasing expected returns

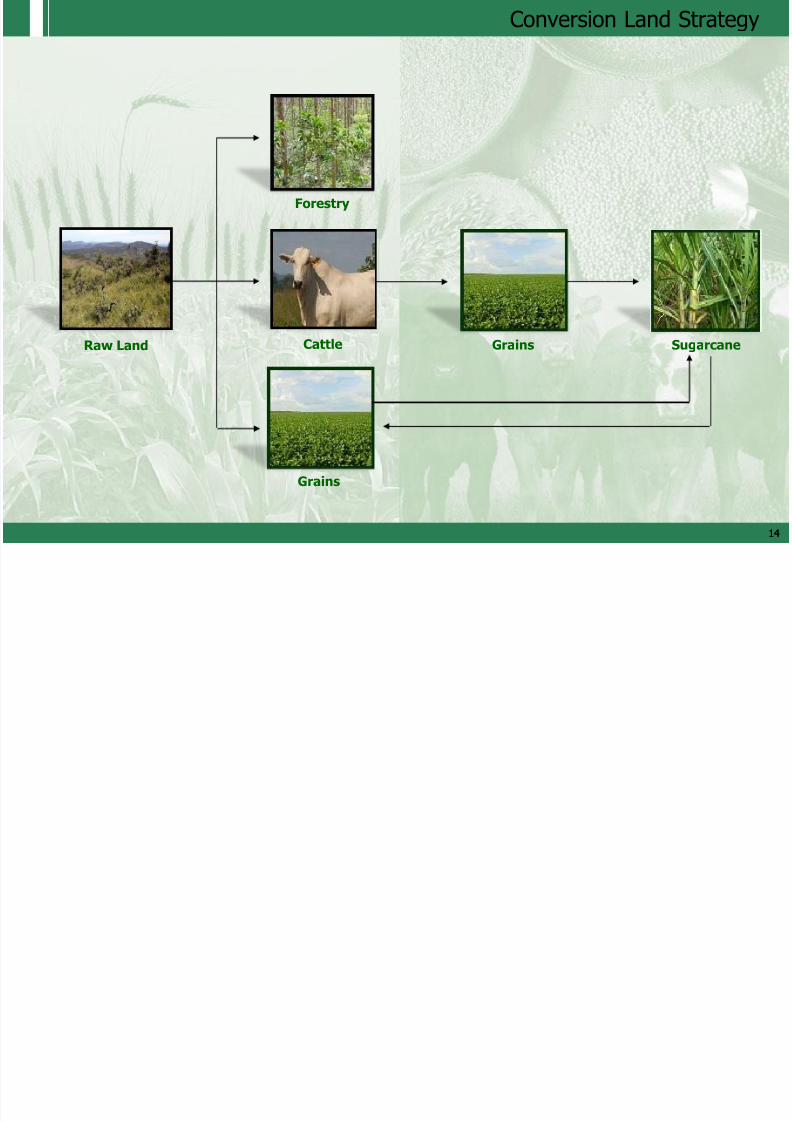

Conversion Land Strategy

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 14/35

1414

Raw Land Cattle Grains Sugarcane

Forestry

Grains

Conversion Land Strategy

Expansion Land Strategy

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 15/35

11

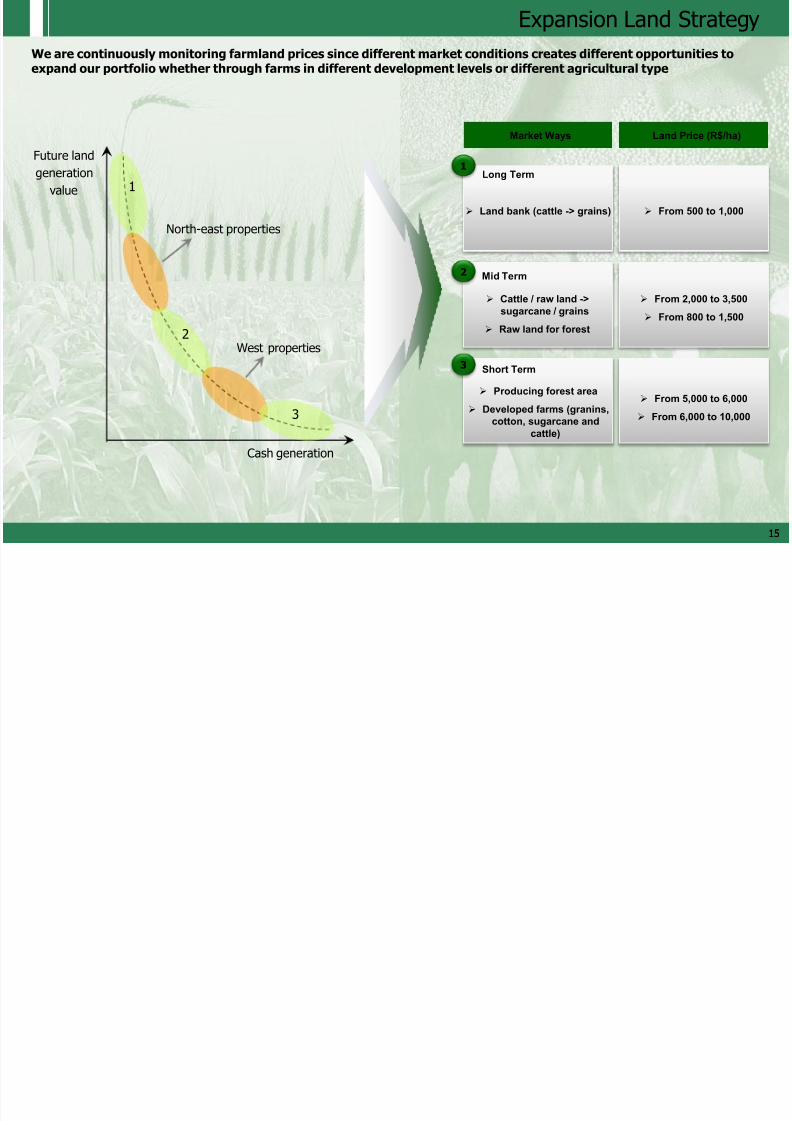

Expansion Land Strategy

Cash generation

Future land

generation

value

North-east properties

2

1

3

West properties

Market Ways Land Price (R$/ha)

Long Term

From 500 to 1,000

Mid Term

From 2,000 to 3,500

From 800 to 1,500

Short Term

Producing forest area

Developed farms (granins,

cotton, sugarcane andcattle)

From 5,000 to 6,000

From 6,000 to 10,000

Cattle / raw land ->sugarcane / grains

Raw land for forest

1

2

3

Land bank (cattle -> grains)

We are continuously monitoring farmland prices since different market conditions creates different opportunities toexpand our portfolio whether through farms in different development levels or different agricultural type

BrasilAgro Portfolio vs Soybean Price

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 16/35

BRASILAGRO PORTFOLIO VS SOYBEAN PRICEIn R$ / 60 kg bag, bubble size equivalent to amount involved

São Pedro

farm

Cremaqfarm

Jatobáfarm

Araucáriafarm

Alto Taquarifarm

Chaparralfarm

Nova Buritifarm

Preferênciafarm

Raw landPartially ready areaReady area

Engenhofarm

Sold area

Engenho¹farm

20

25

30

35

40

45

50

55

60

65

03/2006 08/2006 01/2007 06/2007 11/2007 04/2008 09/2008

BRASILAGRO PORTFOLIO VS SOYBEAN PRICEIn R$ / 60 kg bag, bubble size equivalent to amount involved

São Pedro

farm

Cremaqfarm

Jatobáfarm

Araucáriafarm

Alto Taquarifarm

Chaparralfarm

Nova Buritifarm

Preferênciafarm

Raw landPartially ready areaReady area

Engenhofarm

Sold area

Engenho¹farm

161616

BrasilAgro Portfolio vs Soybean Price

1 – The farm was sold in 06/2008 for R$ 21.7 millions

Note: The size of the bubbles represents total value paid for each farm: R$ 9.9 MM for São Pedro, R$ 42.2 MM for Cremaq, R$ 10.1 MM for Engenho, R$ 35.4 MM for Jatobá, R$ 67.5MM for Araucária, R$ 34.0 MM for Alto Taquari, R$ 47.7 MM for Chaparral, R$ 21.9 for Nova Buriti and R$ 10.1 MM for Preferência.

Source: Bloomberg and BrasilAgro

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 17/35

1717

Company Update

Projects

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 18/35

1818

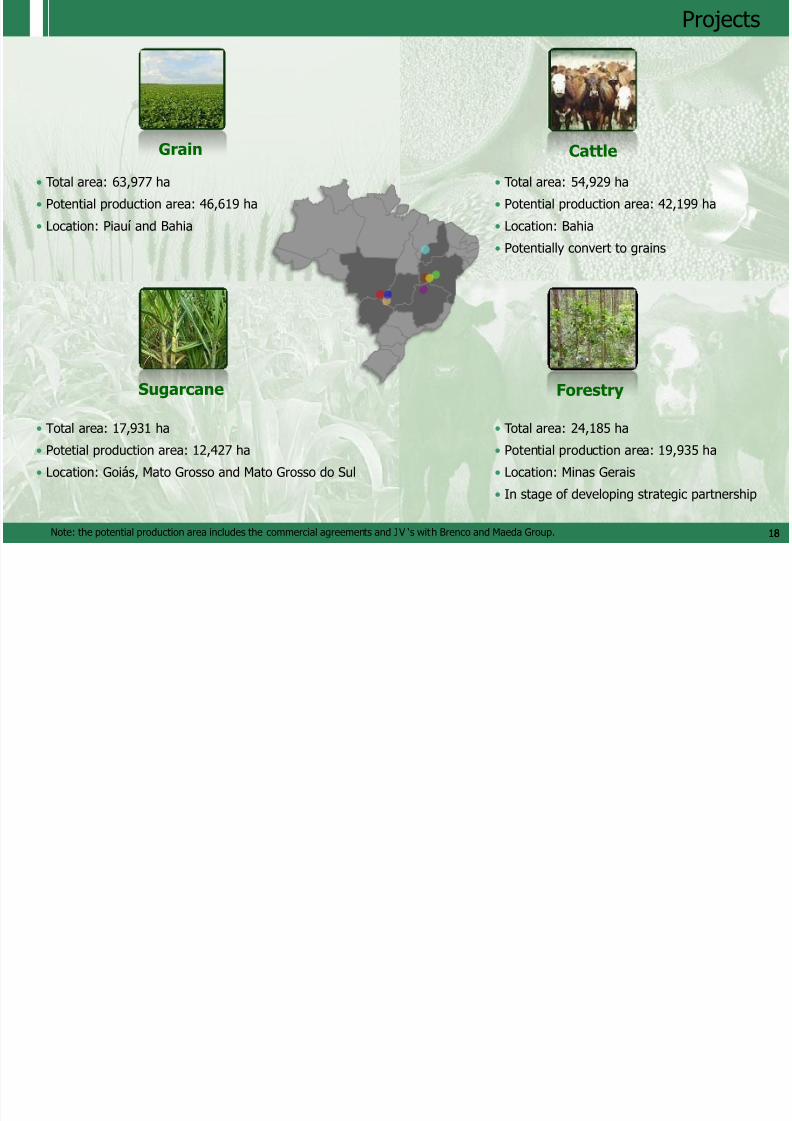

Projects

Sugarcane

Grain Cattle

Forestry

• Total area: 17,931 ha

• Potetial production area: 12,427 ha

• Location: Goiás, Mato Grosso and Mato Grosso do Sul

• Total area: 63,977 ha

• Potential production area: 46,619 ha

• Location: Piauí and Bahia

• Total area: 24,185 ha

• Potential production area: 19,935 ha

• Location: Minas Gerais

• In stage of developing strategic partnership

• Total area: 54,929 ha

• Potential production area: 42,199 ha

• Location: Bahia

• Potentially convert to grains

Note: the potential production area includes the commercial agreements and JV „s with Brenco and Maeda Group.

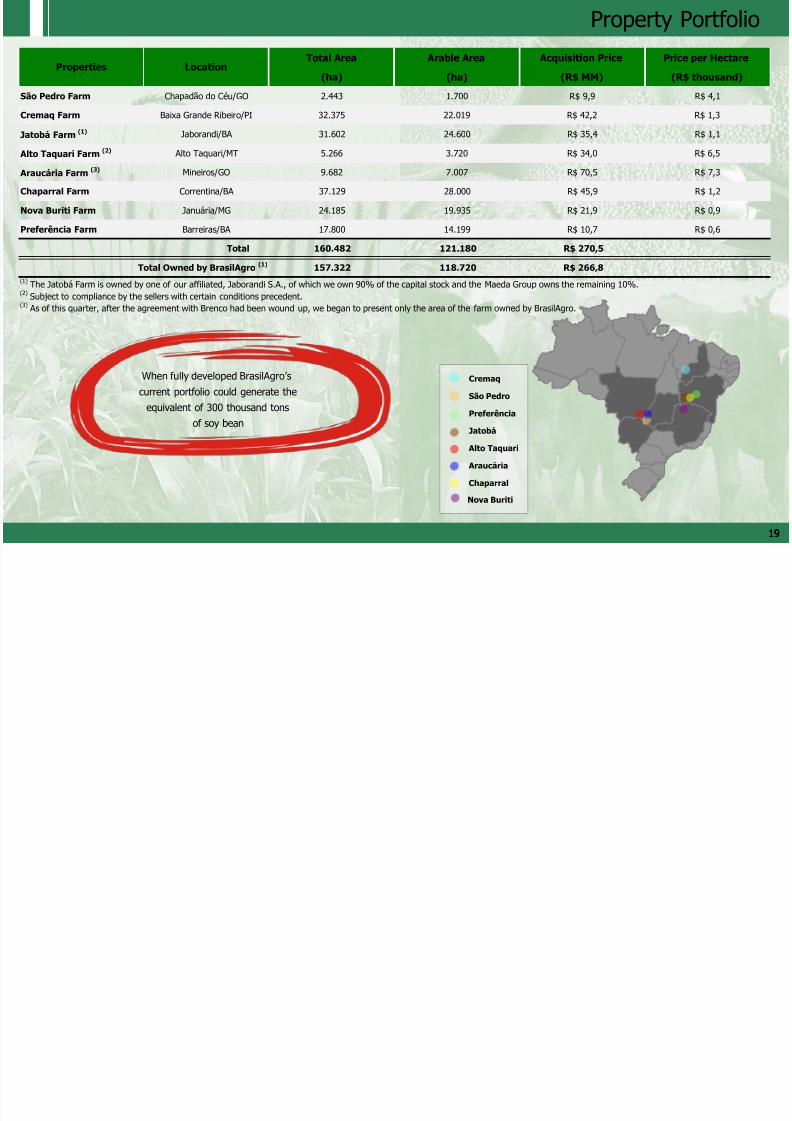

Property Portfolio

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 19/35

Araucária

Preferência

Cremaq

Jatobá

São Pedro

Alto Taquari

Chaparral

Nova Buriti

19191919

Property Portfolio

When fully developed BrasilAgro‟s

current portfolio could generate the

equivalent of 300 thousand tons

of soy bean

Total Area Arable Area Acquisition Price Price per Hectare

(ha) (ha) (R$ MM) (R$ thousand)

São Pedro Farm Chapadão do Céu/GO 2.443 1.700 R$ 9,9 R$ 4,1

Cremaq Farm Baixa Grande Ribeiro/PI 32.375 22.019 R$ 42,2 R$ 1,3

Jatobá Farm (1) Jaborandi/BA 31.602 24.600 R$ 35,4 R$ 1,1

Alto Taquari Farm (2) Alto Taquari/MT 5.266 3.720 R$ 34,0 R$ 6,5

Araucária Farm (3) Mineiros/GO 9.682 7.007 R$ 70,5 R$ 7,3

Chaparral Farm Correntina/BA 37.129 28.000 R$ 45,9 R$ 1,2

Nova Buriti Farm Januária/MG 24.185 19.935 R$ 21,9 R$ 0,9

Preferência Farm Barreiras/BA 17.800 14.199 R$ 10,7 R$ 0,6

Total 160.482 121.180 R$ 270,5

157.322 118.720 R$ 266,8

(2) Subject to compliance by the sellers with certain conditions precedent.(3) As of this quarter, after the agreement with Brenco had been wound up, we began to present only the area of the farm owned by BrasilAgro.

Total Owned by BrasilAgro (1)

(1) The Jatobá Farm is owned by one of our affiliated, Jaborandi S.A., of which we own 90% of the capital stock and the Maeda Group owns the remaining 10%.

Properties Location

Grain Project – Cremaq Farm

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 20/35

20

Grain Project Cremaq Farm

Cremaq farm 2 years ago: Cremaq farm today:

19.500 ha in native vegetation

3.000 ha with grains

5 employee‟s house (practically destroyed)

2 supplies warehouse (practically destroyed)

1 main house

1 lunch room

16,000 ha with grains (soybean, corn and rice)

216 Km of roads, of which 37 km of gravel roads

(suitable for heavy weight trucks)

The existing infra-structure was completely reformed orebuilt: 1 office, 1 warehouse and 1 outsourced

employee‟s house

17 BrasilAgro‟s and 250 outsourced direct employees

Grain Project – Jatobá Farm

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 21/35

2

Grain Project Jatobá Farm

Jatobá farm 2 years ago: Jatobá farm today:

24.600 ha of total arable area corresponding to 6,000

ha of native vegetation and 18,600 of harvested forest

Few practically destroyed buildings

8,500 ha with grains (soybean)

The existing infra-structure was completely reformed

or rebuilt: 1 office, 1 supply warehouse, 1 outsourced

employee‟s house, 1 technical house and 1 lunch room 1 truck size scale

4 BrasilAgro‟s and 200 outsourced direct employees

Sugarcane Project

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 22/35

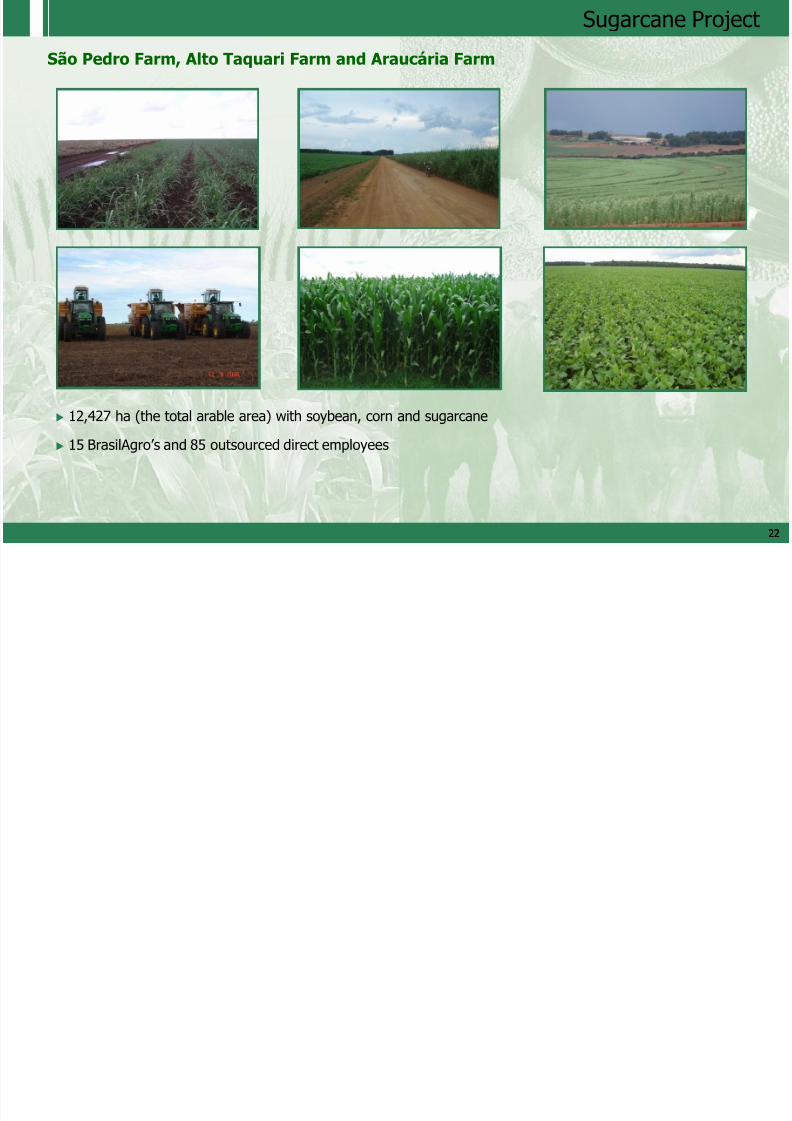

22

Suga ca e oject

São Pedro Farm, Alto Taquari Farm and Araucária Farm

12,427 ha (the total arable area) with soybean, corn and sugarcane 15 BrasilAgro‟s and 85 outsourced direct employees

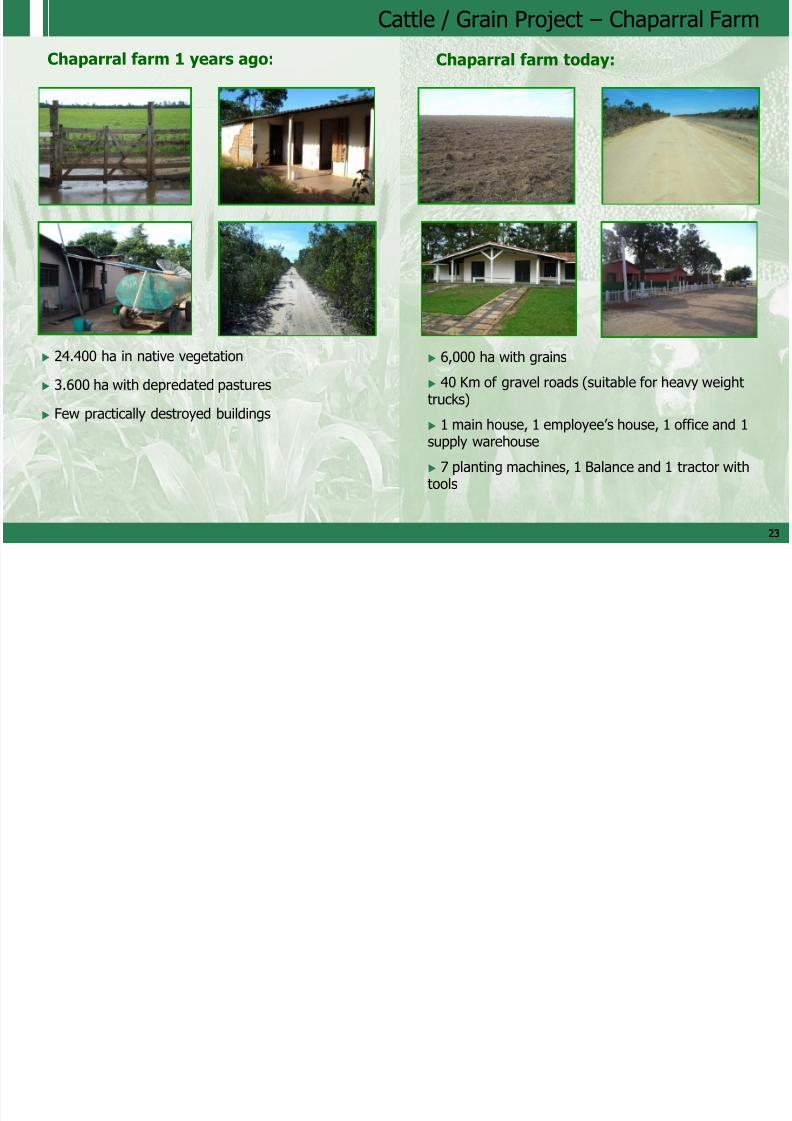

Cattle / Grain Project – Chaparral Farm

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 23/35

2323

/ j p

Chaparral farm 1 years ago: Chaparral farm today:

24.400 ha in native vegetation

3.600 ha with depredated pastures

Few practically destroyed buildings

6,000 ha with grains

40 Km of gravel roads (suitable for heavy weighttrucks)

1 main house, 1 employee‟s house, 1 office and 1supply warehouse

7 planting machines, 1 Balance and 1 tractor withtools

Cattle / Grain Project – Preferência Farm

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 24/35

2424

Preferência Farm

Location: Barreiras/BA

Total area : 17,800 ha

Potential production area : 14,199 ha

/ j

TO

PI

BA

CERN

PE

PB

AL

SE

MA

GO

MG

TO

PI

BA

CERN

PE

PB

AL

SE

MA

GO

MG

Chaparral

Preferência

Forestry Project

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 25/35

22

y j

Nova Buriti Farm

Location: Januária/MG

Total area : 24,185 ha

Potential production area : 19,935 ha

MG

BA

GO

SP

RJ

ES

PR

MG

BA

GO

SP

RJ

ES

PRNova Buriti

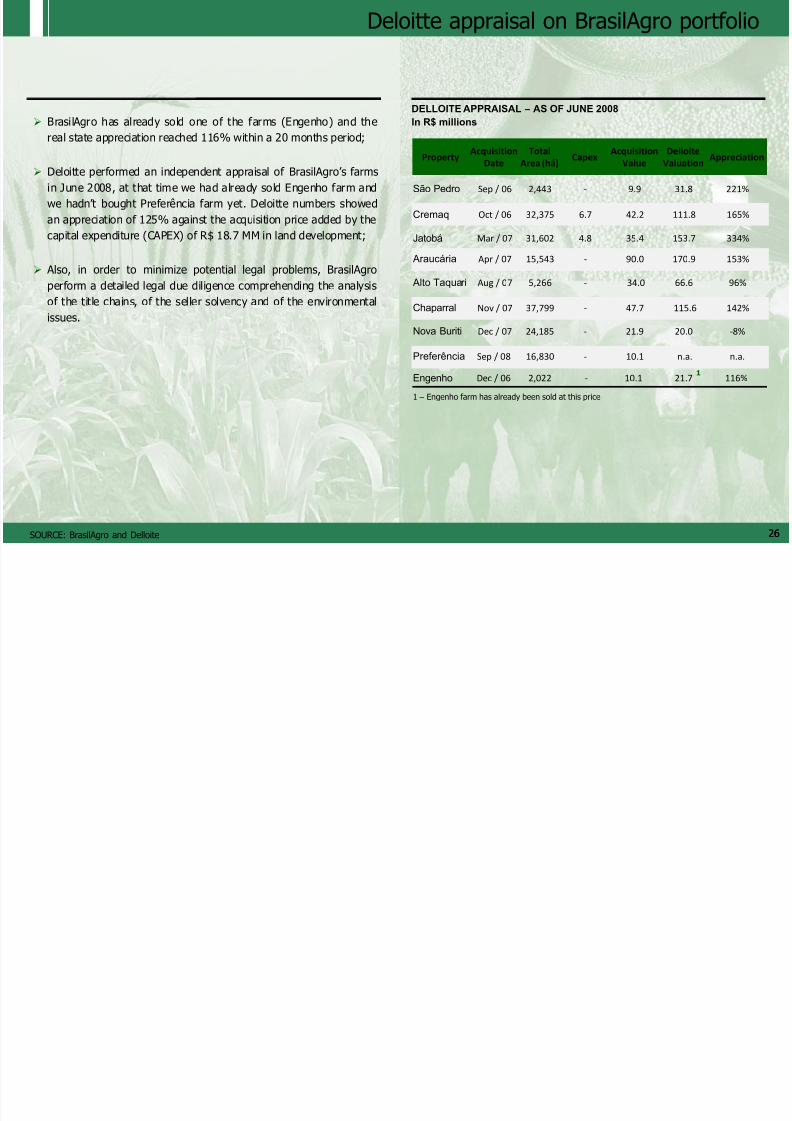

Deloitte appraisal on BrasilAgro portfolio

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 26/35

2626

pp g p

1

PropertyAcquisition

Date

Total

Area (há)Capex

Acquisition

Value

Delloite

ValuationAppreciation

São Pedro Sep / 06 2,443 - 9.9 31.8 221%

Cremaq Oct / 06 32,375 6.7 42.2 111.8 165%

Jatobá Mar / 07 31,602 4.8 35.4 153.7 334%

Araucária Apr / 07 15,543 - 90.0 170.9 153%

Alto Taquari Aug / 07 5,266 - 34.0 66.6 96%

Chaparral Nov / 07 37,799 - 47.7 115.6 142%

Nova Buriti Dec / 07 24,185 - 21.9 20.0 -8%

Preferência Sep / 08 16,830 - 10.1 n.a. n.a.

Engenho Dec / 06 2,022 - 10.1 21.7 116%

SOURCE: BrasilAgro and Delloite

DELLOITE APPRAISAL – AS OF JUNE 2008

In R$ millions BrasilAgro has already sold one of the farms (Engenho) and the

real state appreciation reached 116% within a 20 months period;

Deloitte performed an independent appraisal of BrasilAgro‟s farms

in June 2008, at that time we had already sold Engenho farm and

we hadn‟t bought Preferência farm yet. Deloitte numbers showed

an appreciation of 125% against the acquisition price added by the

capital expenditure (CAPEX) of R$ 18.7 MM in land development;

Also, in order to minimize potential legal problems, BrasilAgro

perform a detailed legal due diligence comprehending the analysisof the title chains, of the seller solvency and of the environmental

issues.

1 – Engenho farm has already been sold at this price

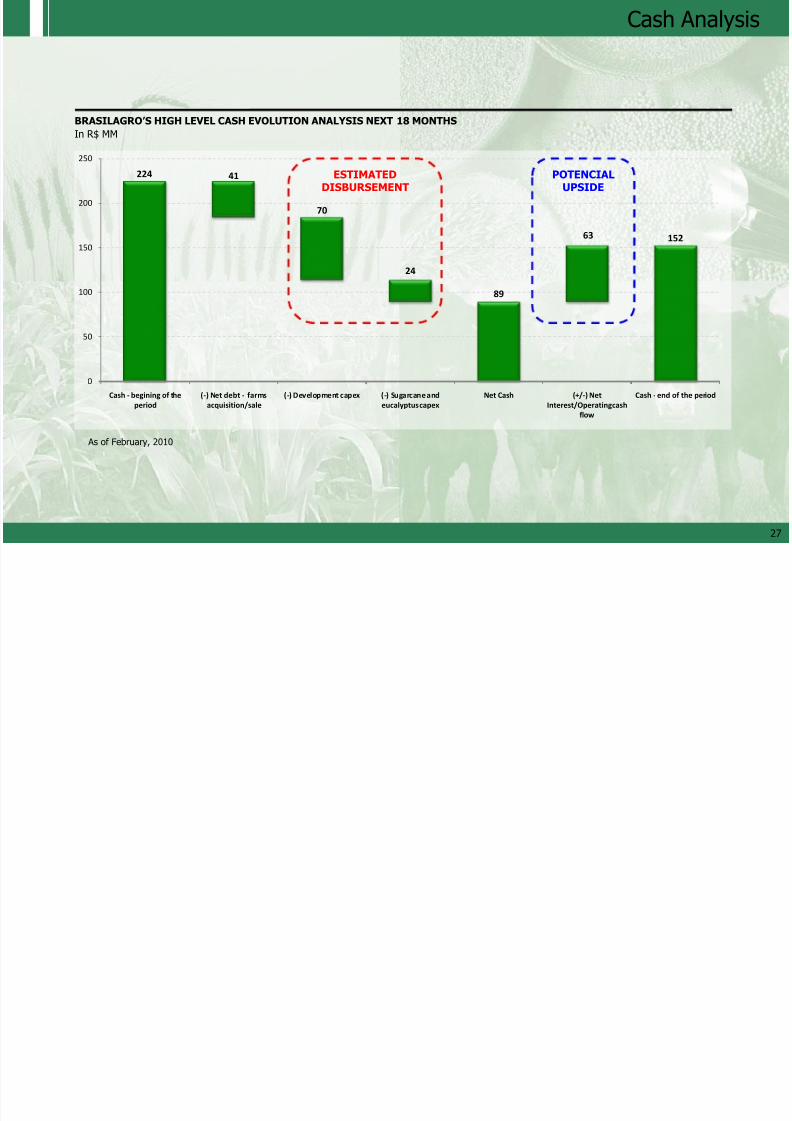

Cash Analysis

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 27/35

2

224 41

70

24

89

63 152

0

50

100

150

200

250

Cash - begining of the

period

(-) Net debt - farms

acquisition/sale

(-) Development capex (-) Sugarcane and

eucalyptus capex

Net Cash (+/-) Net

Interest/Operating cash

flow

Cash - end of the period

BRASILAGRO’S HIGH LEVEL CASH EVOLUTION ANALYSIS NEXT 18 MONTHS

In R$ MM

ESTIMATEDDISBURSEMENT

POTENCIALUPSIDE

As of February, 2010

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 28/35

2828

Commercial Agreements, Joint Ventureand Corporate Structure

Commercial Agreements and JV

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 29/35

2929

On March 6, 2008, BrasilAgro signed a

Sugarcane Supply Agreement with Brenco for

the total production of two full crops cycles

of six crops years each. The agreement is for

Araucária and Alto Taquari farms.

Under the agreement, the sugarcane price

per tonne will be established based on the

TRS per tonne of sugarcane delivered, aspublished by CONSECANA-SP.

BrasilAgro also acquired a 40.64% stake in

Green Ethanol LLC, which represents 3.8% of

BRENCO‟s shares.

BRENCO – Brazilian Renewable Energy Company The Maeda Group

Partnership to explore agribusiness

opportunities aimed at increasing the value

of rural properties

Partnership through the constitution of two

subsidiaries

• Real-Estate Company: dedicated to the

acquisition of properties. BrasilAgro will

retain 90% and Maeda 10%

• Operating Company: dedicated to crop

development and management.

BrasilAgro will retain 75% and Maeda

25%

The Operating Company will lease the Real

Estate Company‟s properties to carry out

agricultural activities and sublease these

properties to farmers

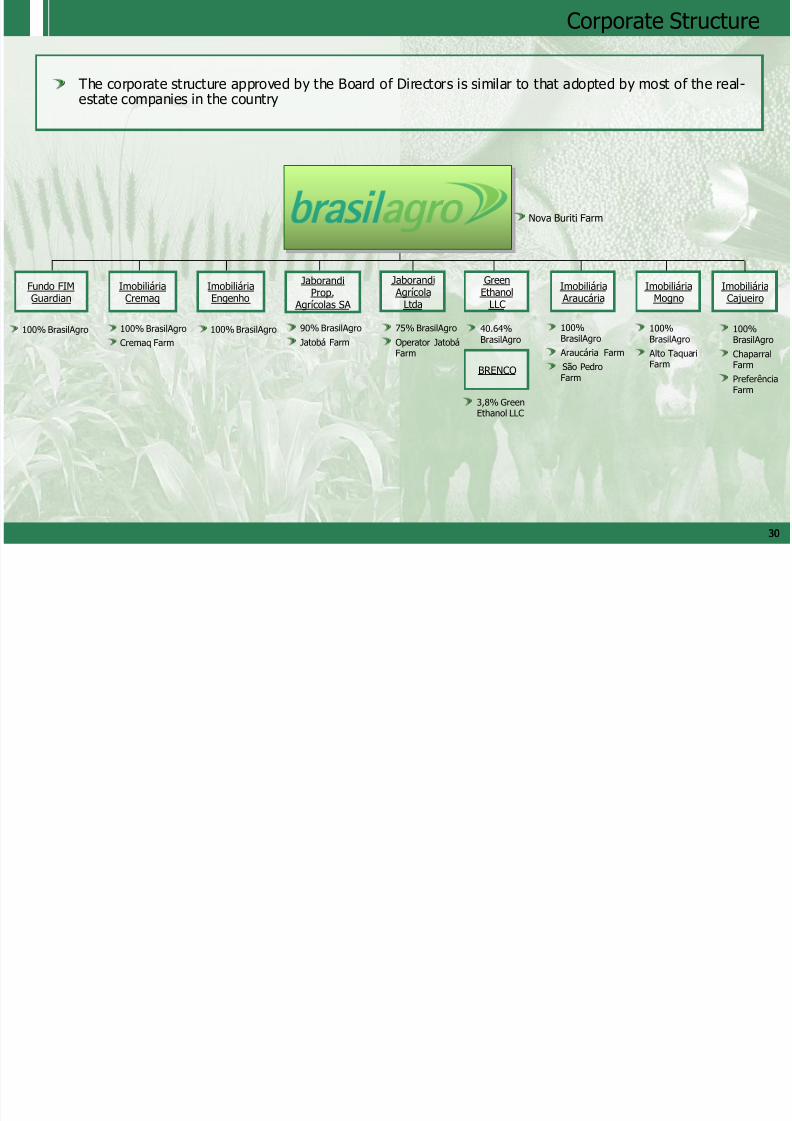

Corporate Structure

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 30/35

3030

The corporate structure approved by the Board of Directors is similar to that adopted by most of the real-estate companies in the country

ImobiliáriaCremaq

ImobiliáriaEngenho

Fundo FIMGuardian

100% BrasilAgro 100% BrasilAgro

Cremaq Farm

100% BrasilAgro

JaborandiProp. Agrícolas SA

90% BrasilAgro

Jatobá Farm

Jaborandi AgrícolaLtda

75% BrasilAgro

Operator JatobáFarm

GreenEthanolLLC

BRENCO

40.64%BrasilAgro

3,8% GreenEthanol LLC

Imobiliária Araucária

100%BrasilAgro

Araucária Farm

São PedroFarm

ImobiliáriaMogno

100%BrasilAgro

Alto TaquariFarm

Nova Buriti Farm

ImobiliáriaCajueiro

100%BrasilAgro

ChaparralFarm

PreferênciaFarm

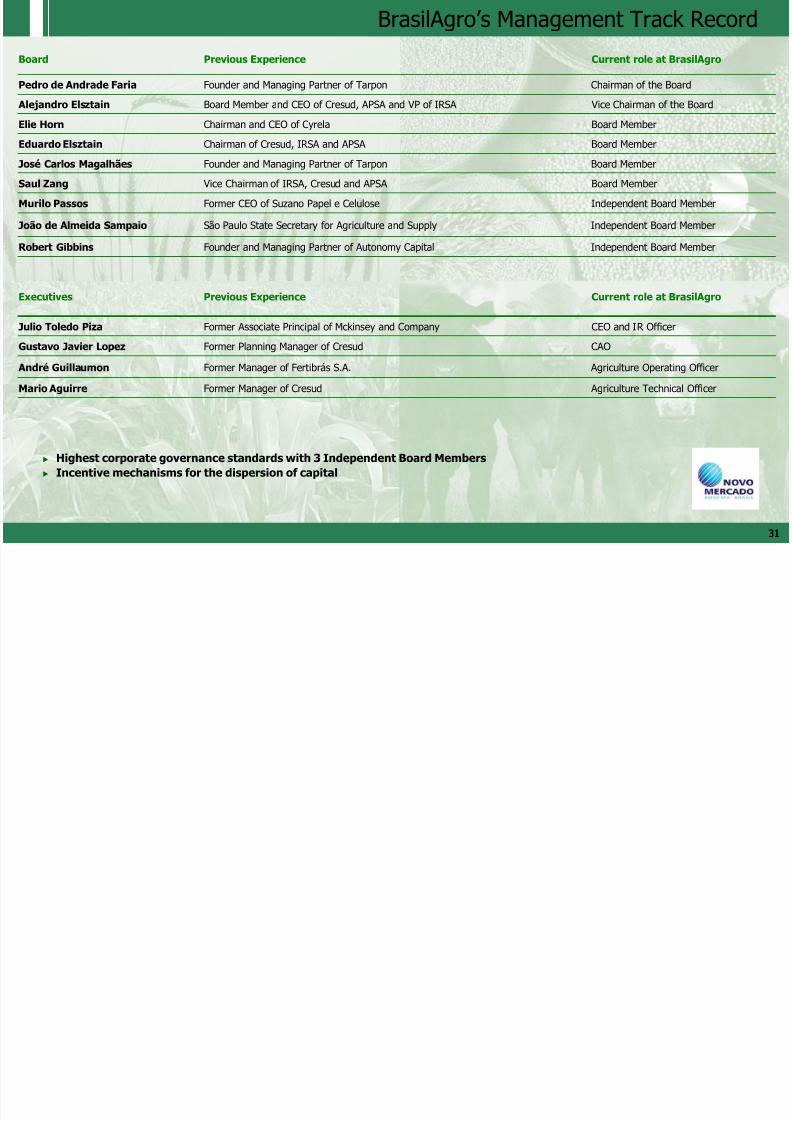

BrasilAgro‟s Management Track Record

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 31/35

33

Highest corporate governance standards with 3 Independent Board Members

Incentive mechanisms for the dispersion of capital

Board Previous Experience Current role at BrasilAgro

Pedro de Andrade Faria Founder and Managing Partner of Tarpon Chairman of the Board

Alejandro Elsztain Board Member and CEO of Cresud, APSA and VP of IRSA Vice Chairman of the Board

Elie Horn Chairman and CEO of Cyrela Board Member

Eduardo Elsztain Chairman of Cresud, IRSA and APSA Board MemberJosé Carlos Magalhães Founder and Managing Partner of Tarpon Board Member

Saul Zang Vice Chairman of IRSA, Cresud and APSA Board Member

Murilo Passos Former CEO of Suzano Papel e Celulose Independent Board Member

João de Almeida Sampaio São Paulo State Secretary for Agriculture and Supply Independent Board Member

Robert Gibbins Founder and Managing Partner of Autonomy Capital Independent Board Member

Executives Previous Experience Current role at BrasilAgro

Julio Toledo Piza Former Associate Principal of Mckinsey and Company CEO and IR Officer

Gustavo Javier Lopez Former Planning Manager of Cresud CAO

André Guillaumon Former Manager of Fertibrás S.A. Agriculture Operating Officer

Mario Aguirre Former Manager of Cresud Agriculture Technical Officer

BrasilAgro‟s Management Track Record

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 32/35

33

Installation of the Fiscal Council with 1 member appointed by the minority shareholders

Fiscal Council Previous Experience Current role at BrasilAgro

Renato Pereira Stetner Partner at Castro, Barros, Sobral, Gomes Advogados, specializing in the area ofCorporate Law

Sitting member elected by the controllingshareholder

Breno Takeshi Former financial and cash control analyst of TarponSitting member elected by the controllingshareholder

Anthonny Dias dos SantosLawyer and consultant specializing in corporate and capital market law at Fialdine,Penna and Tilkian Advogados

Sitting member elected by the minorityshareholder

Tiago Franco da Silva Gomes Associate at Castro, Barros, Sobral, Gomes Advogados, specializing in mergers andacquisitions, corporate restructurings and commercial agreements

Alternate member elected by thecontrolling shareholder

Flávio StammPartner at Stamm & Stamm Consultoria Empresarial Ltda and a member of the IBGC(Brazilian Institute of Corporate Governance)

Alternate member elected by thecontrolling shareholder

Alfredo Ferreira Marques Filho Auditing partner at the firm Horwath Tufani Reis & Soares Auditores Independentes Alternate member elected by theminority shareholder

Incentive mechanisms aligned with minority shareholders

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 33/35

3333

Founding Shareholders were granted, proportionally to their pre-IPO ownership, two series of

warrants

Size

Strike price

Anti-dilutionprotection

Vestingperiod

Transferability

Exerciseperiod

1st Series - Stock Based Remuneration

20% of shares outstanding on a fully diluted basis

Weighted average price of capital injections,

adjusted by IPCA

15 years

In the event that additional capital is issued, theunderlying amount of shares will be adjusted to reflect20% of shares outstanding, on a fully diluted basis

1/3 in year one, 1/3 in year two and 1/3 in year three,provided the founders maintain 80% of the initialownership in BrasilAgro

Transferable within founder After vesting, founders will be free to

transfer the warrants

2nd Series - “Anti Take Over Protection”

20% of shares outstanding on a fully diluted basis

At the price of Offer, in case of a mandatory tender

offer

In the event that additional capital is issued, theunderlying amount of shares will be adjusted to reflect20% of shares outstanding, on a fully-diluted basis

No vesting

15 years and only in the event of a mandatorytender offer, provided founders maintain 80% of theinitial ownership in BrasilAgro

Non-transferable Transferable within founder

Preemptiverights tominority

shareholders

In case of capital increase below IPO priceadjusted by IPCA None

Management Consulting Contract

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 34/35

3434

Paraná Consultora de Investimentos S.A.

Consulting services will be provided by Paraná Consultora de Investimentos S.A., a joint venturebetween Tarpon BR and Consultores Asset Management

Consultingservices

Investments and divestitures in agricultural properties

Technical assistance

M&A

Hedging

Other

Compensation Management fee: 1% of paid in capital (adjusted by IPCA), excluding capitalized profits (1) (2)

Terminationand

penalty clause

Termination fee: R$4.3 million (approx. US$2,6 million), in the event of termination without cause

No termination fee in case of willful misconduct or gross negligence

(1) 1% Management fee will be applied only to capital raised, either through a private or a public capital increase.

(2) In case BrasilAgro issues additional capital, the management fee will equal the original management fee adjusted by IPCA + 1% of capital raised.

Contacts

8/8/2019 BrasilAgro 2010 Corporate Presentation Slides Deck PPT

http://slidepdf.com/reader/full/brasilagro-2010-corporate-presentation-slides-deck-ppt 35/35

33

Julio Toledo Piza

BrasilAgro - Companhia Brasileira de Propriedades Agrícolas

Avenida Brigadeiro Faria Lima, 1.3095o. Andar - CEP 01452-002São Paulo - SP - BrazilTelephone: +55 (11) 3035-5350Fax: +55 (11) 3035-5366

www.brasil-agro.com

CEO and IR Officer Ana Paula Ribeiro

BrasilAgro - Companhia Brasileira de Propriedades Agrícolas

Avenida Brigadeiro Faria Lima, 1.3095o. Andar - CEP 01452-002São Paulo - SP - BrazilTelephone: +55 (11) 3035-5374Fax: +55 (11) 3035-5366

www.brasil-agro.com

Investor Relations