Brandhouse Retails Limitedbrandhouseretails.com/lb/pdf/BHRL-Presentation.pdf · Retails Ltd. Global...

49

The Fashion Enabler BRANDHOUSE Retails Limited The Fashion Enabler March 2009

Transcript of Brandhouse Retails Limitedbrandhouseretails.com/lb/pdf/BHRL-Presentation.pdf · Retails Ltd. Global...

The Fashion Enabler

BRANDHOUSE Retails LimitedThe Fashion Enabler

March 2009

The Fashion Enabler

Section 1 : Corporate Overview

The Fashion Enabler

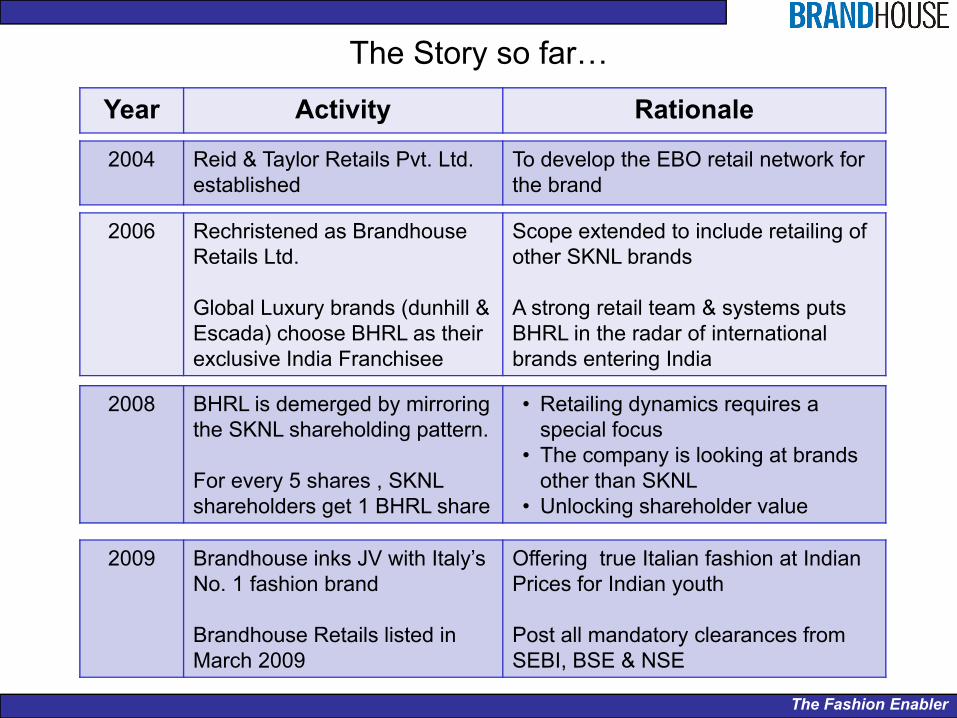

The Story so far…

2004 Reid & Taylor Retails Pvt. Ltd. established

To develop the EBO retail network for the brand

2006 Rechristened as Brandhouse Retails Ltd.

Global Luxury brands (dunhill & Escada) choose BHRL as their exclusive India Franchisee

Scope extended to include retailing of other SKNL brands

A strong retail team & systems puts BHRL in the radar of international brands entering India

Year Activity Rationale

2008 BHRL is demerged by mirroring the SKNL shareholding pattern.

For every 5 shares , SKNL shareholders get 1 BHRL share

• Retailing dynamics requires a special focus

• The company is looking at brands other than SKNL

• Unlocking shareholder value

2009 Brandhouse inks JV with Italy’s No. 1 fashion brand

Brandhouse Retails listed in March 2009

Offering true Italian fashion at Indian Prices for Indian youth

Post all mandatory clearances from SEBI, BSE & NSE

The Fashion Enabler

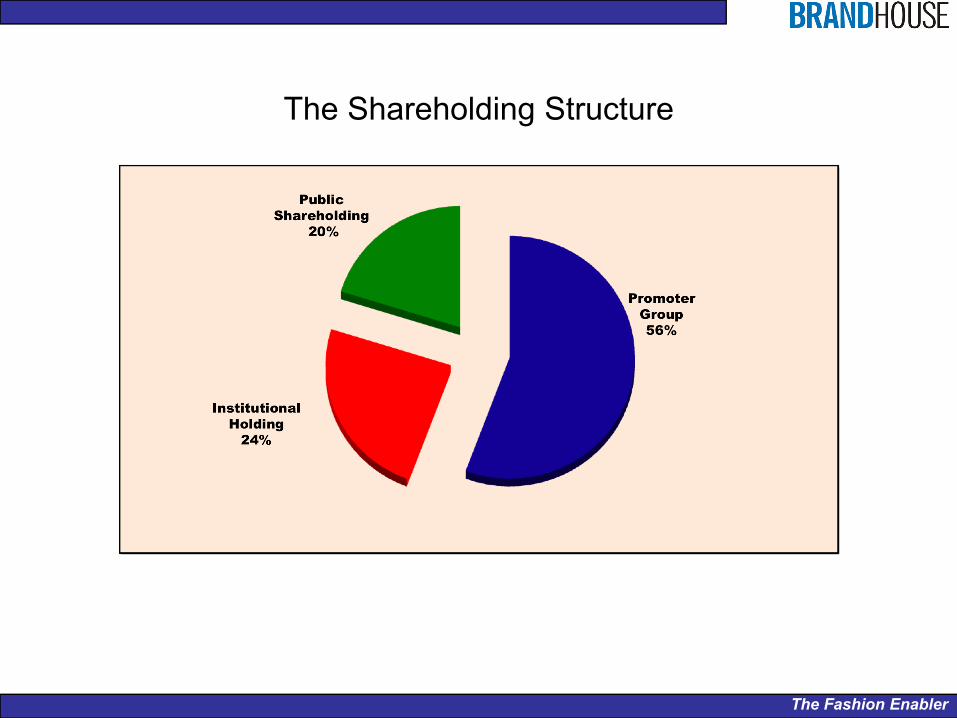

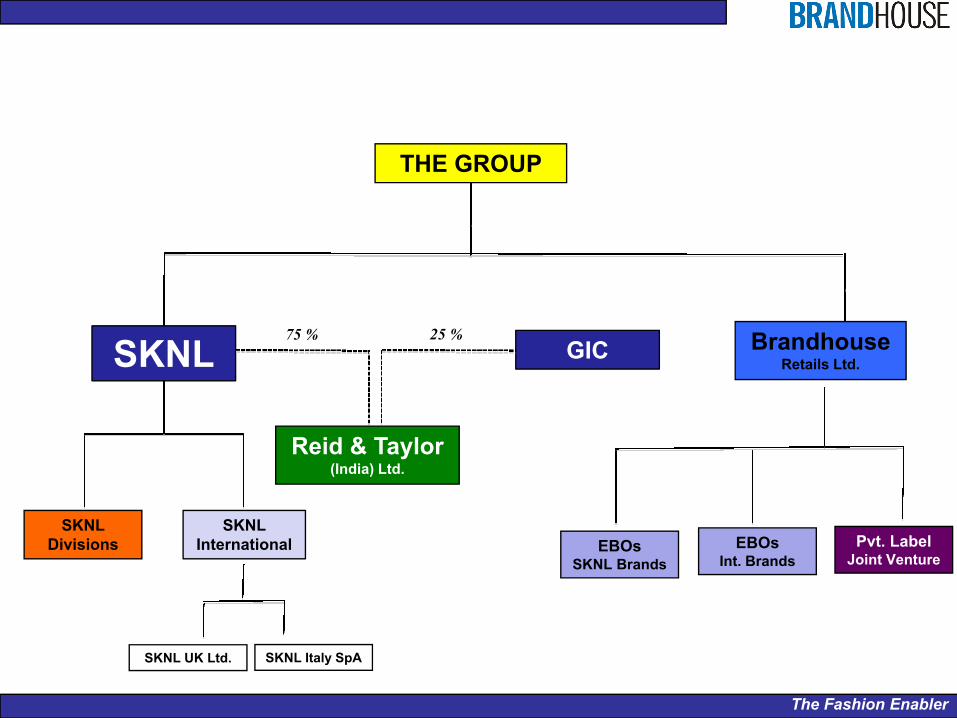

The Shareholding Structure

The Fashion Enabler

THE GROUP

SKNL

SKNL International

SKNL Divisions

Reid & Taylor (India) Ltd.

Brandhouse Retails Ltd.

GIC

SKNL UK Ltd. SKNL Italy SpA

EBOs SKNL Brands

EBOs Int. Brands

Pvt. Label Joint Venture

75 % 25 %

The Fashion Enabler

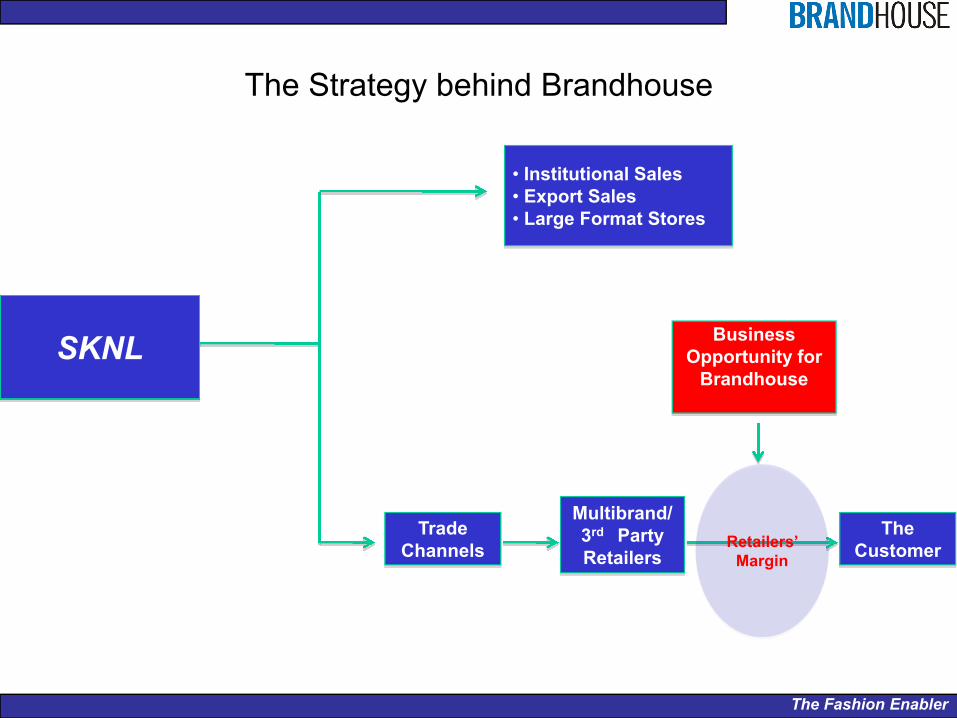

The Strategy behind Brandhouse

SKNL

• Institutional Sales• Export Sales• Large Format Stores

Trade Channels

Multibrand/ 3rd Party Retailers

The Customer

Business Opportunity for

Brandhouse

Retailers’ Margin

The Fashion Enabler

Section 2 : The Business Dynamics

The Fashion Enabler

Vision & Mission

The Retail Gateway of India for Fashion & Lifestyle

Provide a distinct competitive edge to our brands by creating

an International Retail Experience for addressing the booming

Indian Consumerism

The Fashion Enabler

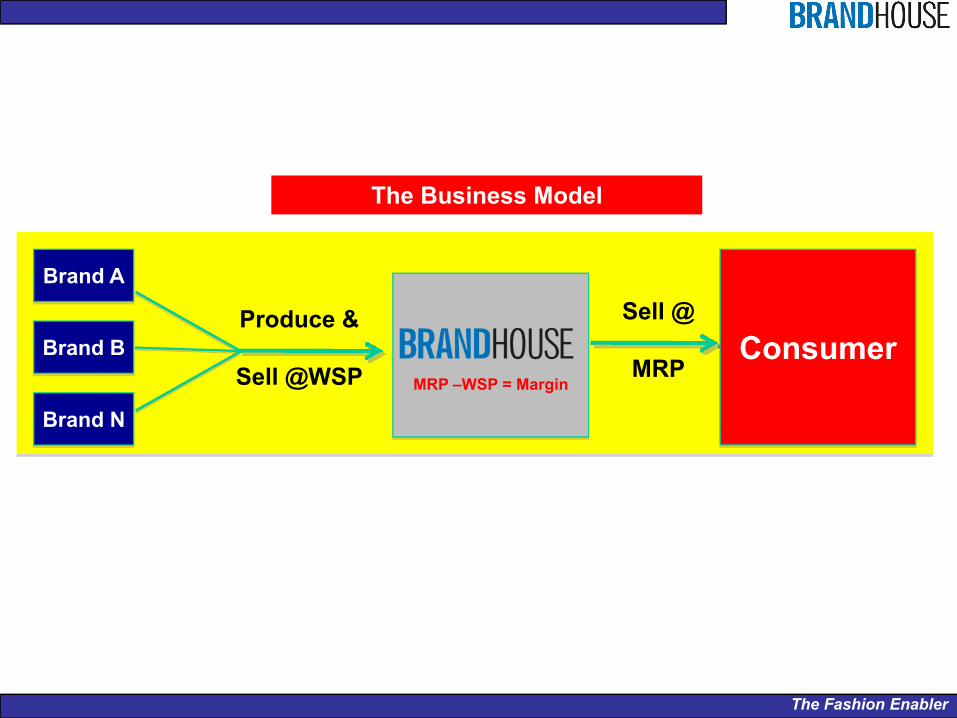

Sell @

MRP

Produce &

Sell @WSP MRP –WSP = Margin

Brand A

Brand B

Brand N

Consumer

The Business Model

The Fashion Enabler

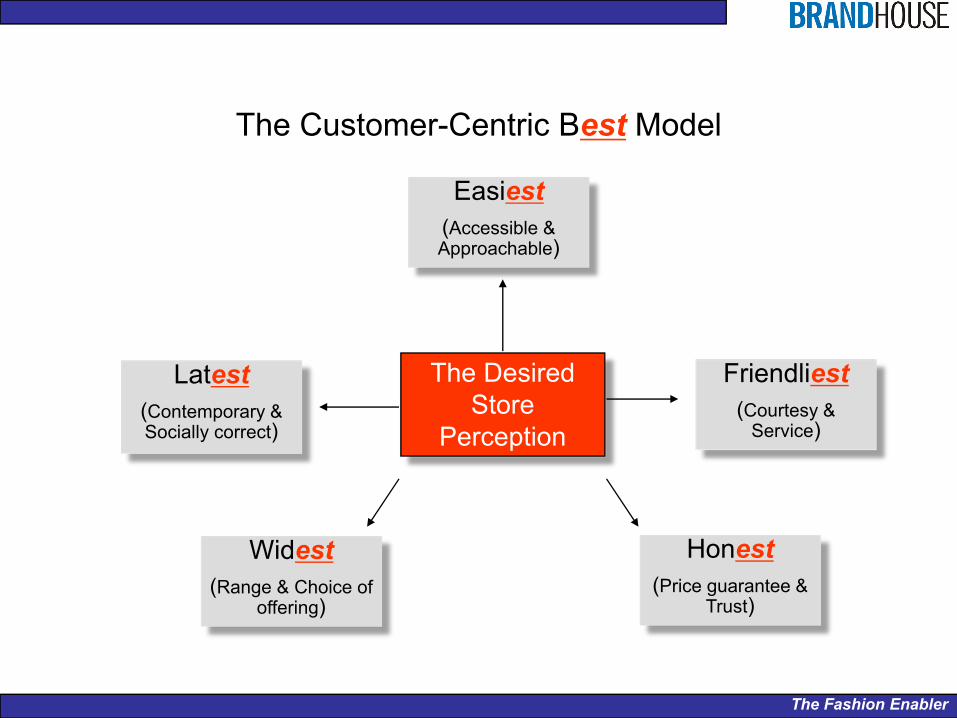

The Customer-Centric Best Model

The Desired Store

Perception

Easiest (Accessible & Approachable)

Friendliest (Courtesy &

Service)

Honest (Price guarantee &

Trust)

Latest (Contemporary & Socially correct)

Widest (Range & Choice of

offering)

The Fashion Enabler

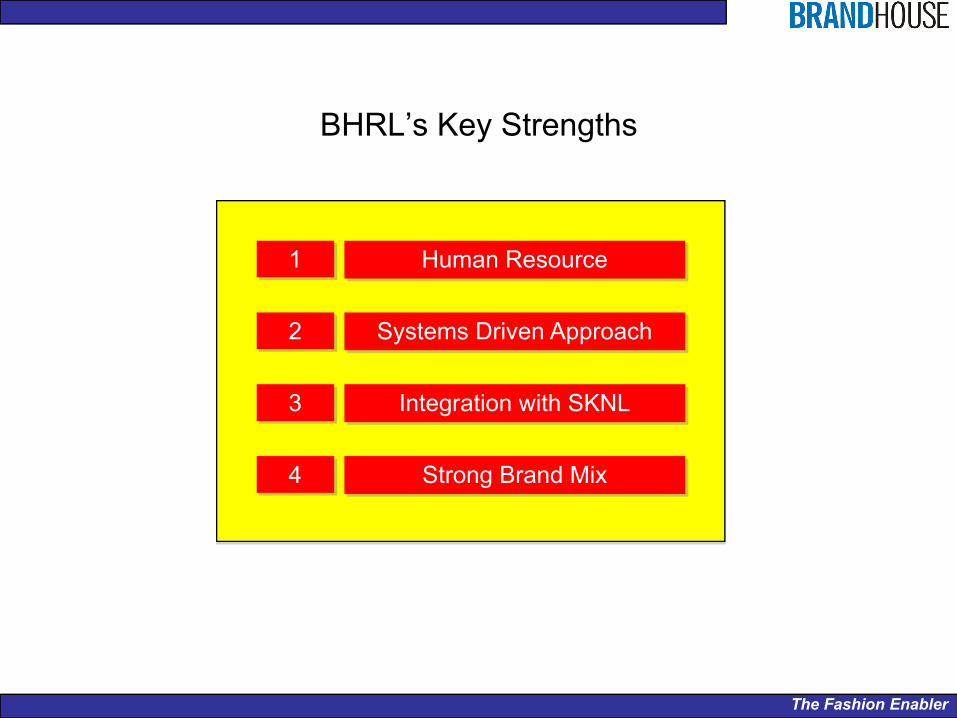

BHRL’s Key Strengths

1 Human Resource

2 Systems Driven Approach

3 Integration with SKNL

4 Strong Brand Mix

The Fashion Enabler

1 Human Resource

A strong, experienced team of retail professionals create the cutting edge in a very competitive scenario

The Fashion Enabler

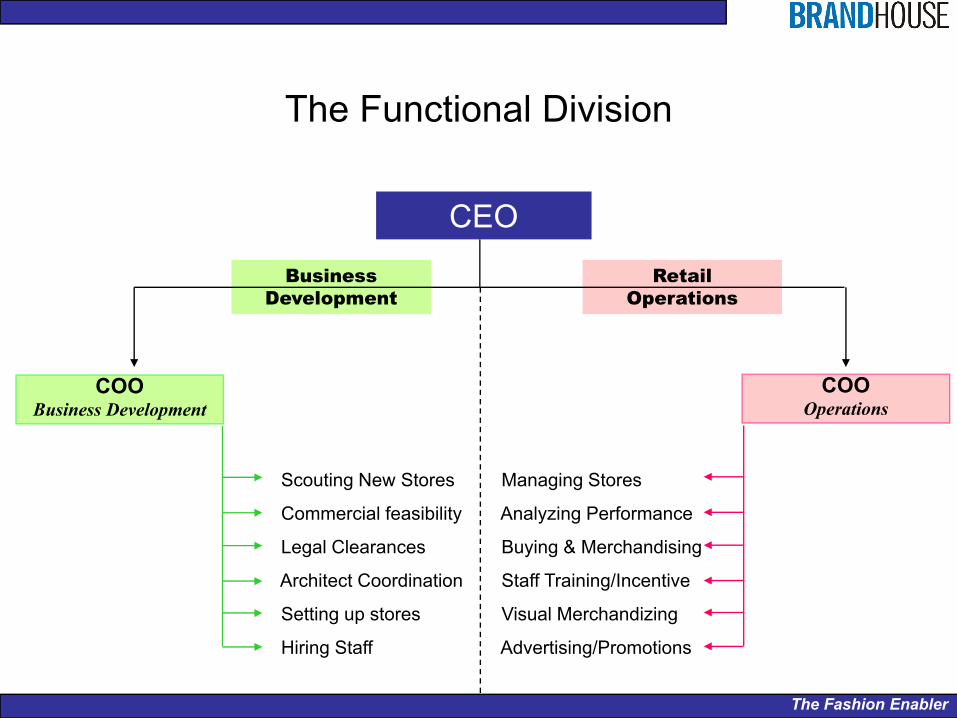

Retail Operations

Business Development

CEO

COOBusiness Development

COOOperations

Scouting New Stores

Commercial feasibility

Legal Clearances

Architect Coordination

Setting up stores

Hiring Staff

Managing Stores

Analyzing Performance

Buying & Merchandising

Staff Training/Incentive

Visual Merchandizing

Advertising/Promotions

The Functional Division

The Fashion Enabler

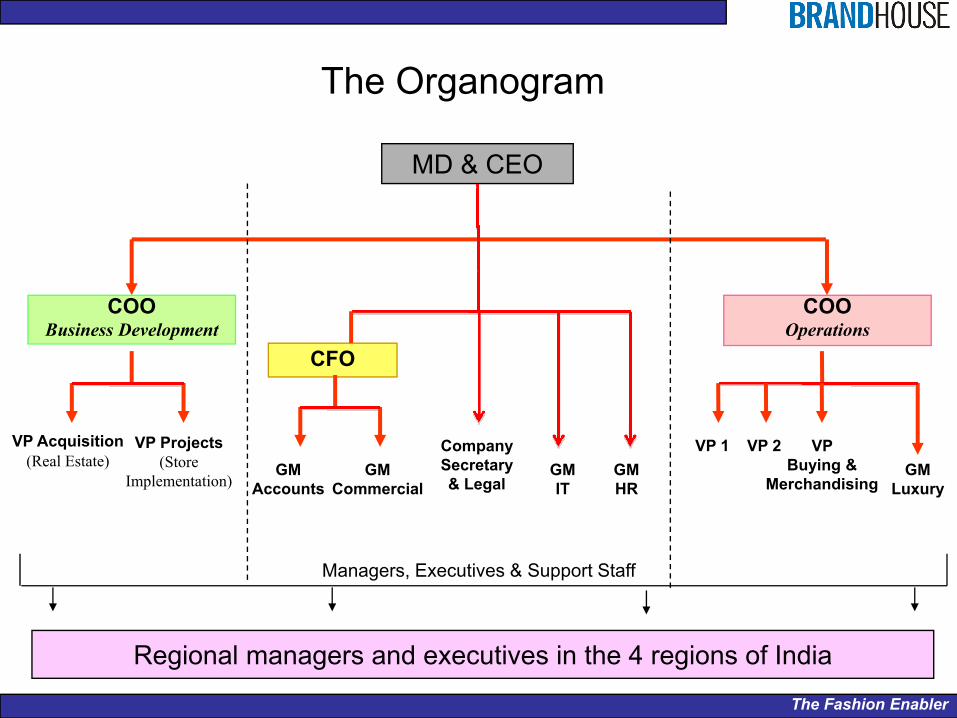

Managers, Executives & Support Staff

The Organogram

MD & CEO

COOBusiness Development

COOOperations

CFO

VP Acquisition(Real Estate)

VP Projects (Store

Implementation)

VP 1 GM

Accounts

Company Secretary & Legal

GM IT

GM Commercial

Regional managers and executives in the 4 regions of India

VP Buying &

MerchandisingGM

Luxury

VP 2GM HR

The Fashion Enabler

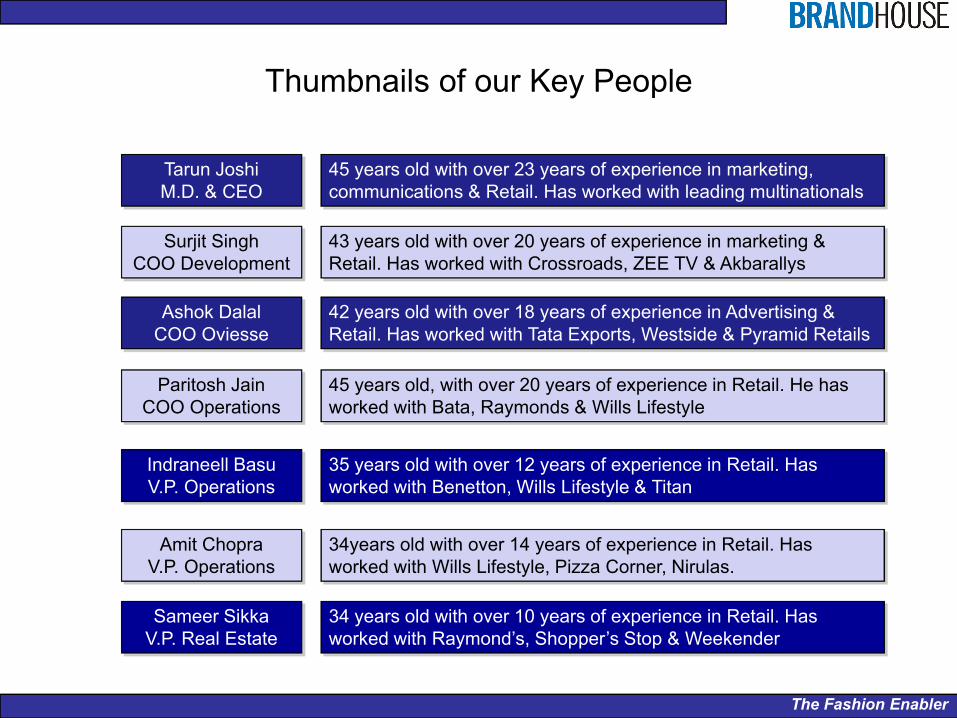

Thumbnails of our Key People

Tarun Joshi M.D. & CEO

45 years old with over 23 years of experience in marketing, communications & Retail. Has worked with leading multinationals

Surjit Singh COO Development

43 years old with over 20 years of experience in marketing & Retail. Has worked with Crossroads, ZEE TV & Akbarallys

Ashok Dalal COO Oviesse

42 years old with over 18 years of experience in Advertising & Retail. Has worked with Tata Exports, Westside & Pyramid Retails

Indraneell Basu V.P. Operations

35 years old with over 12 years of experience in Retail. Has worked with Benetton, Wills Lifestyle & Titan

Amit Chopra V.P. Operations

34years old with over 14 years of experience in Retail. Has worked with Wills Lifestyle, Pizza Corner, Nirulas.

Sameer Sikka V.P. Real Estate

34 years old with over 10 years of experience in Retail. Has worked with Raymond’s, Shopper’s Stop & Weekender

Paritosh Jain COO Operations

45 years old, with over 20 years of experience in Retail. He has worked with Bata, Raymonds & Wills Lifestyle

The Fashion Enabler

2 Systems Driven Approach

Objective, systematic approach that maximizes productivity & efficiencies

The Fashion Enabler

Integrated, Systems-Driven Retail footprint

Shoppers IT Software

SAP

Buying & Merchandising

Marketing

Store OperationsFinance

Human Resource

Development

Information Technology

Logistics & Supply Chain

Business Development

The Fashion Enabler

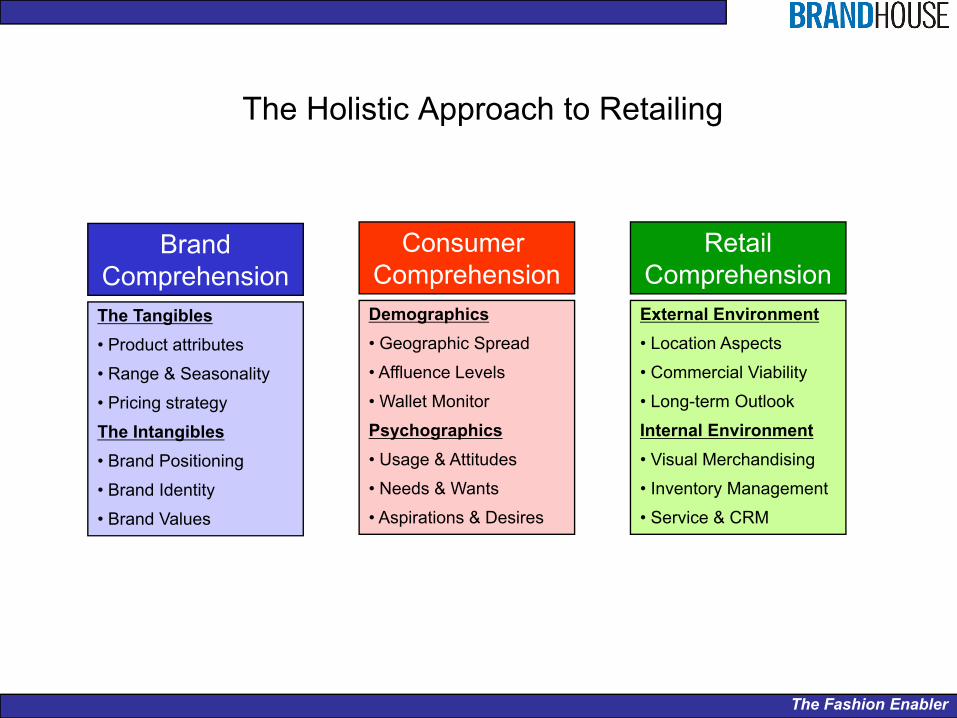

The Holistic Approach to Retailing

Consumer ComprehensionDemographics• Geographic Spread

• Affluence Levels

• Wallet Monitor

Psychographics• Usage & Attitudes

• Needs & Wants

• Aspirations & Desires

BrandComprehensionThe Tangibles• Product attributes

• Range & Seasonality

• Pricing strategy

The Intangibles• Brand Positioning

• Brand Identity

• Brand Values

RetailComprehensionExternal Environment• Location Aspects

• Commercial Viability

• Long-term Outlook

Internal Environment• Visual Merchandising

• Inventory Management

• Service & CRM

The Fashion Enabler

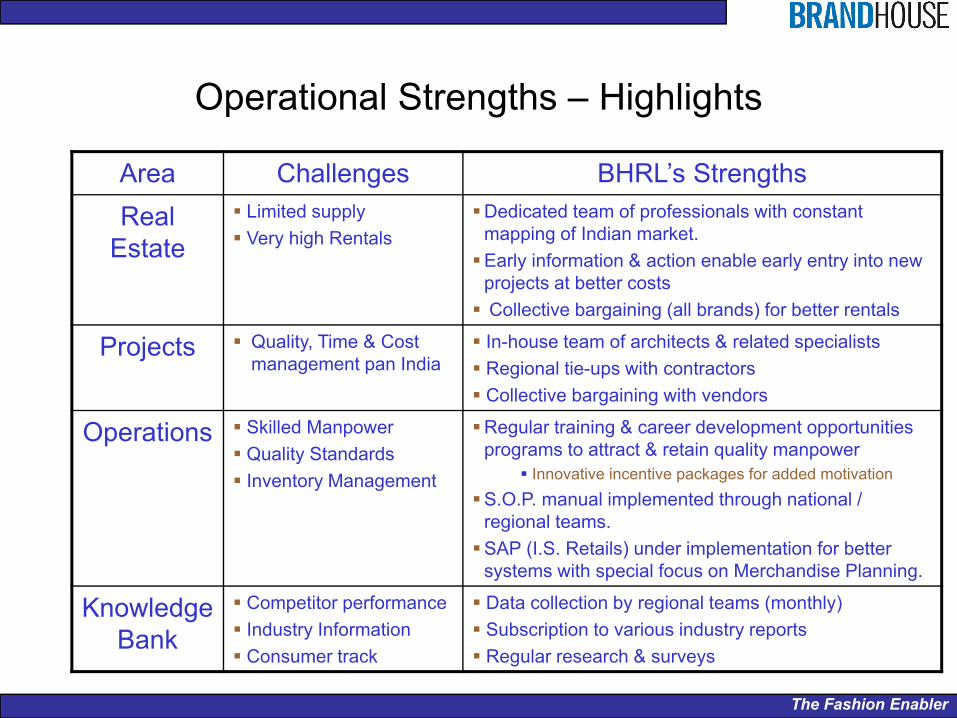

Operational Strengths – Highlights

Area Challenges BHRL’s Strengths Real

EstateLimited supplyVery high Rentals

Dedicated team of professionals with constant mapping of Indian market. Early information & action enable early entry into new projects at better costsCollective bargaining (all brands) for better rentals

Projects Quality, Time & Cost management pan India

In-house team of architects & related specialists Regional tie-ups with contractorsCollective bargaining with vendors

Operations Skilled ManpowerQuality Standards Inventory Management

Regular training & career development opportunities programs to attract & retain quality manpower

Innovative incentive packages for added motivationS.O.P. manual implemented through national / regional teams.SAP (I.S. Retails) under implementation for better systems with special focus on Merchandise Planning.

Knowledge Bank

Competitor performanceIndustry InformationConsumer track

Data collection by regional teams (monthly)Subscription to various industry reportsRegular research & surveys

The Fashion Enabler

3 Integration with SKNL Group

The advantages of being a part of a large group with over six decades of experience in textiles & fashion

The Fashion Enabler

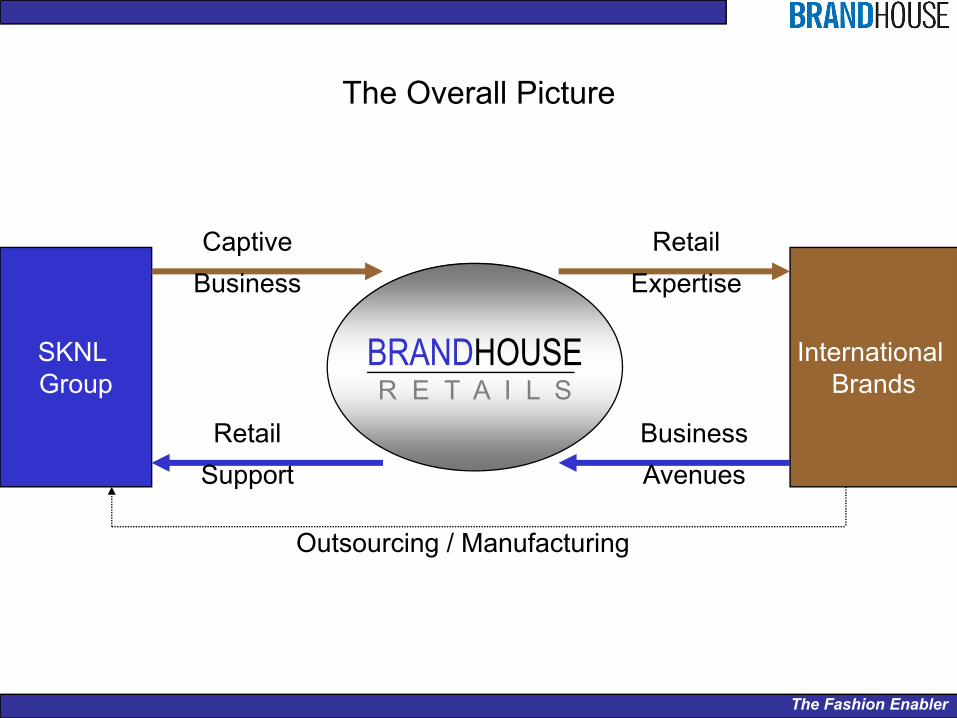

The Overall Picture

BRANDHOUSER E T A I L S

SKNL Group

International Brands

CaptiveBusiness

RetailSupport

RetailExpertise

BusinessAvenues

Outsourcing / Manufacturing

The Fashion Enabler

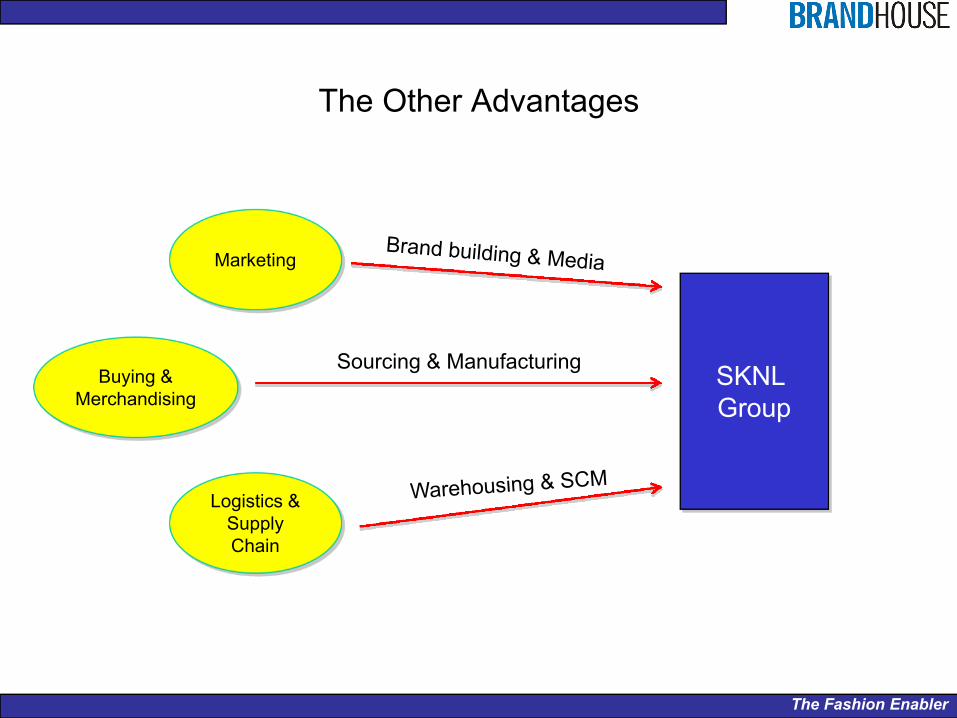

The Other Advantages

Marketing

Logistics & Supply Chain

Buying & Merchandising

SKNL Group

Sourcing & Manufacturing

The Fashion Enabler

4 Strong Brand Mix

The advantages of having a strong portfolio of brands with strong equity & a well- established track record

The Fashion Enabler

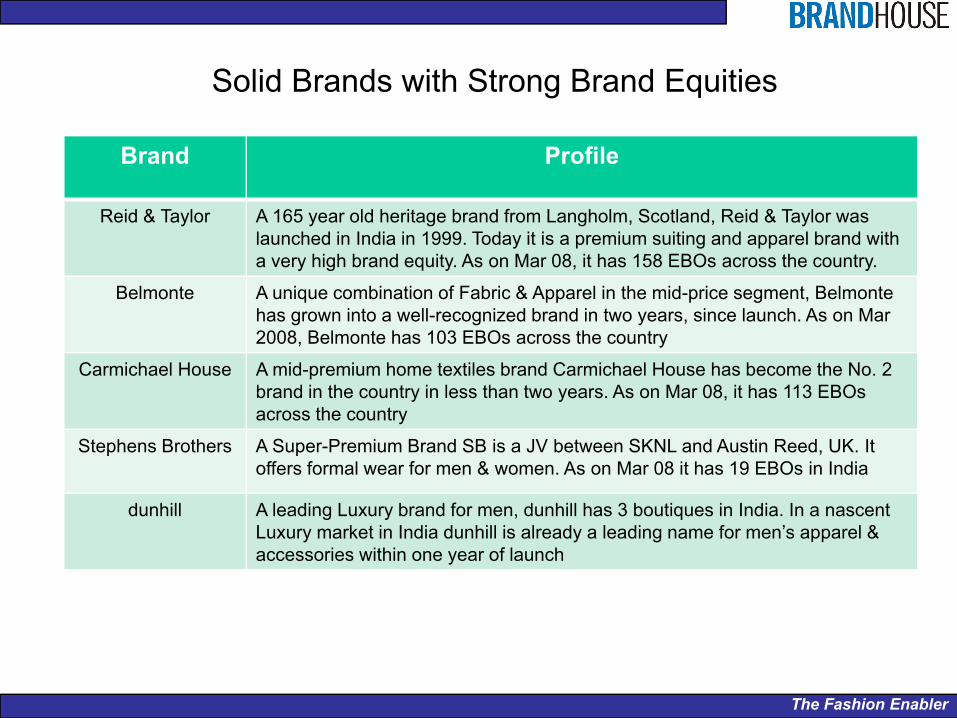

Solid Brands with Strong Brand Equities

Brand Profile

Reid & Taylor A 165 year old heritage brand from Langholm, Scotland, Reid & Taylor was launched in India in 1999. Today it is a premium suiting and apparel brand with a very high brand equity. As on Mar 08, it has 158 EBOs across the country.

Belmonte A unique combination of Fabric & Apparel in the mid-price segment, Belmonte has grown into a well-recognized brand in two years, since launch. As on Mar 2008, Belmonte has 103 EBOs across the country

Carmichael House A mid-premium home textiles brand Carmichael House has become the No. 2 brand in the country in less than two years. As on Mar 08, it has 113 EBOs across the country

Stephens Brothers A Super-Premium Brand SB is a JV between SKNL and Austin Reed, UK. It offers formal wear for men & women. As on Mar 08 it has 19 EBOs in India

dunhill A leading Luxury brand for men, dunhill has 3 boutiques in India. In a nascent Luxury market in India dunhill is already a leading name for men’s apparel & accessories within one year of launch

The Fashion Enabler

Section 3 : Performance & Projections

The Fashion Enabler

Financial Overview

2007-08Audited

2008-09Audited

2009-10Projected

No. of Stores 398 683 909

Area (Sq.ft.) 4,18,415 666,575 911,100

Revenues (Rs. Cr.) 313.79 552.35 812.72

EBIDTA (Rs. Cr.) 31.22 41.18 78.84

EBIDTA % 9.95% 7.45% 9.7%

PBT (Rs. Cr.) 22.63 24.12 33.40

PBT % 7.2% 4.4% 4.1%

PAT (Rs. Cr.) 13.31 13.39 22.15

PAT % 4.2% 2.4% 2.70%

The Fashion Enabler

Rental matrix – Own StoresRent/PSF month Metro Tier 1 Tier 2

Reid & Taylor 225 175 125

Carmichael House 175 125 80

Stephens Brothers 300 200 -

Belmonte 160 125 90

Luxury 800 - -

The Fashion Enabler

Growth Plan in terms of Sales/Sq ft/ Day (PSFPD)

Sales/PSFPD 2008-09

Reid & Taylor 27.06

Carmichael House 16.41

Stephens Brothers 31.88

Belmonte 19.15

Luxury 53.33

TOTAL 22.69• All PSFPD figures in INR• All PSFPD is calculated on carpet area

The Fashion Enabler

Section 4 : The Indian Retail Industry & Fashion

The Fashion Enabler

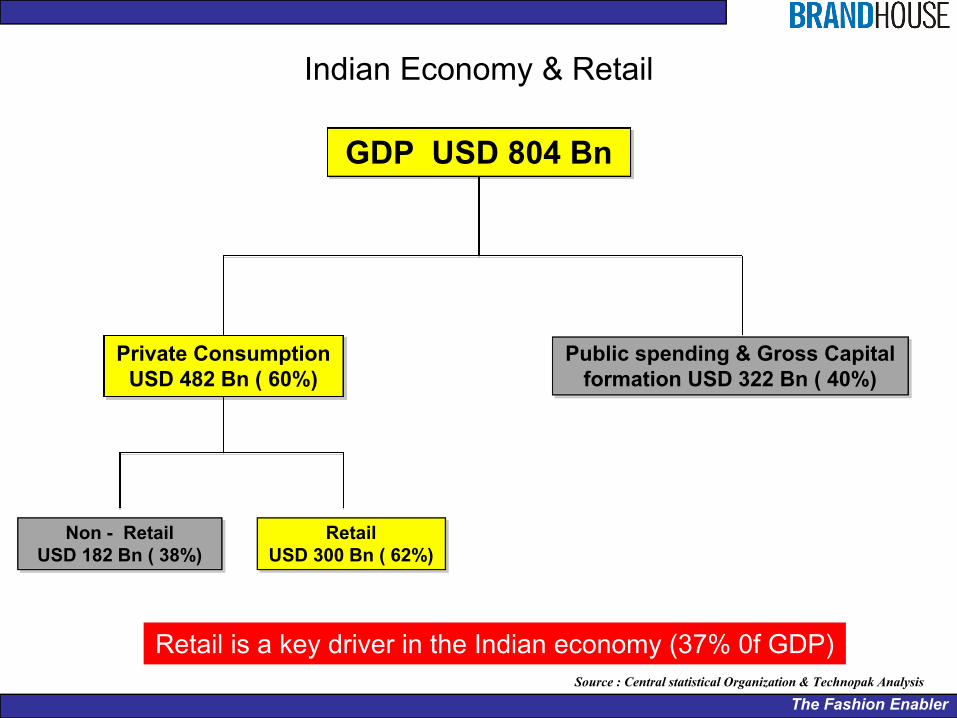

Indian Economy & Retail

GDP USD 804 Bn

Private Consumption USD 482 Bn ( 60%)

Public spending & Gross Capital formation USD 322 Bn ( 40%)

Non - Retail USD 182 Bn ( 38%)

Retail USD 300 Bn ( 62%)

Source : Central statistical Organization & Technopak Analysis

Retail is a key driver in the Indian economy (37% 0f GDP)

The Fashion Enabler

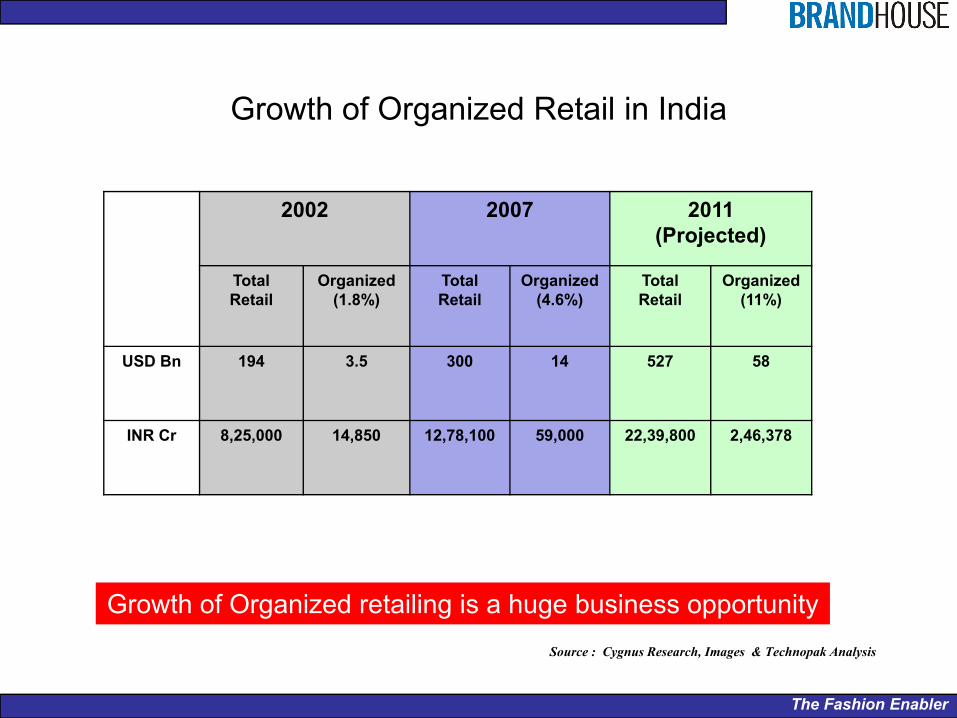

Growth of Organized Retail in India

2002 2007 2011 (Projected)

Total Retail

Organized (1.8%)

Total Retail

Organized (4.6%)

Total Retail

Organized (11%)

USD Bn 194 3.5 300 14 527 58

INR Cr 8,25,000 14,850 12,78,100 59,000 22,39,800 2,46,378

Source : Cygnus Research, Images & Technopak Analysis

Growth of Organized retailing is a huge business opportunity

The Fashion Enabler

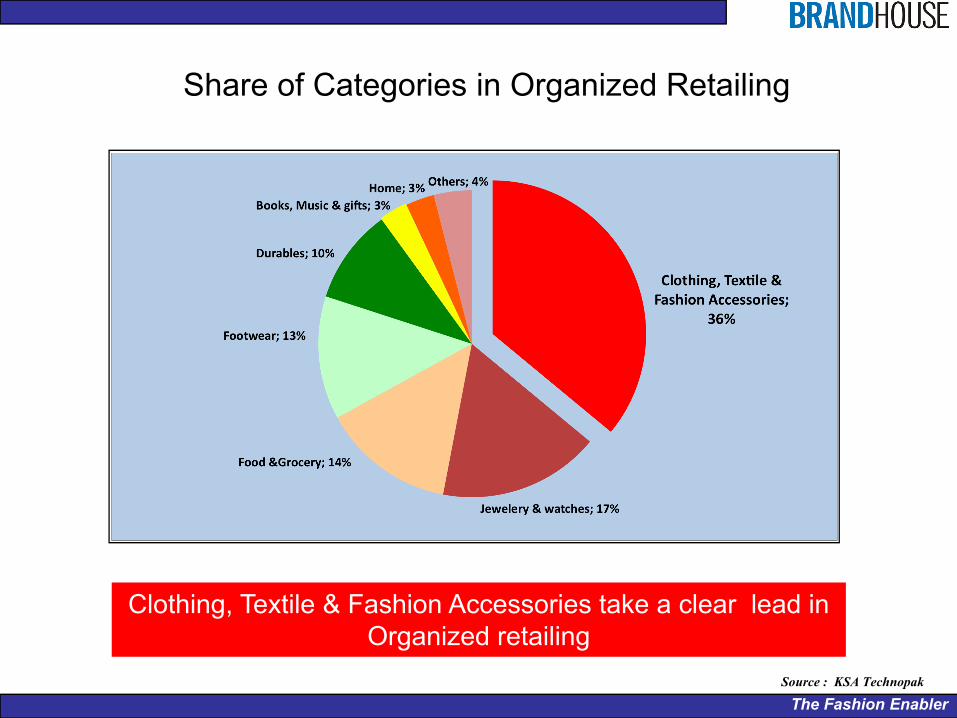

Share of Categories in Organized Retailing

Source : KSA Technopak

Clothing, Textile & Fashion Accessories take a clear lead in Organized retailing

The Fashion Enabler

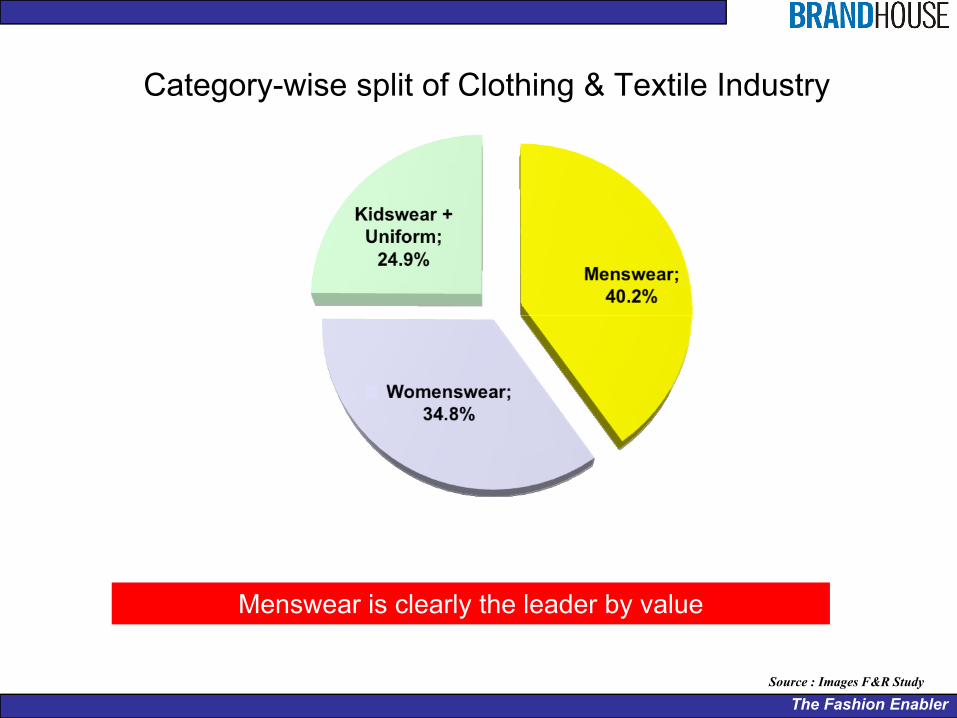

Category-wise split of Clothing & Textile Industry

Source : Images F&R Study

Menswear is clearly the leader by value

The Fashion Enabler

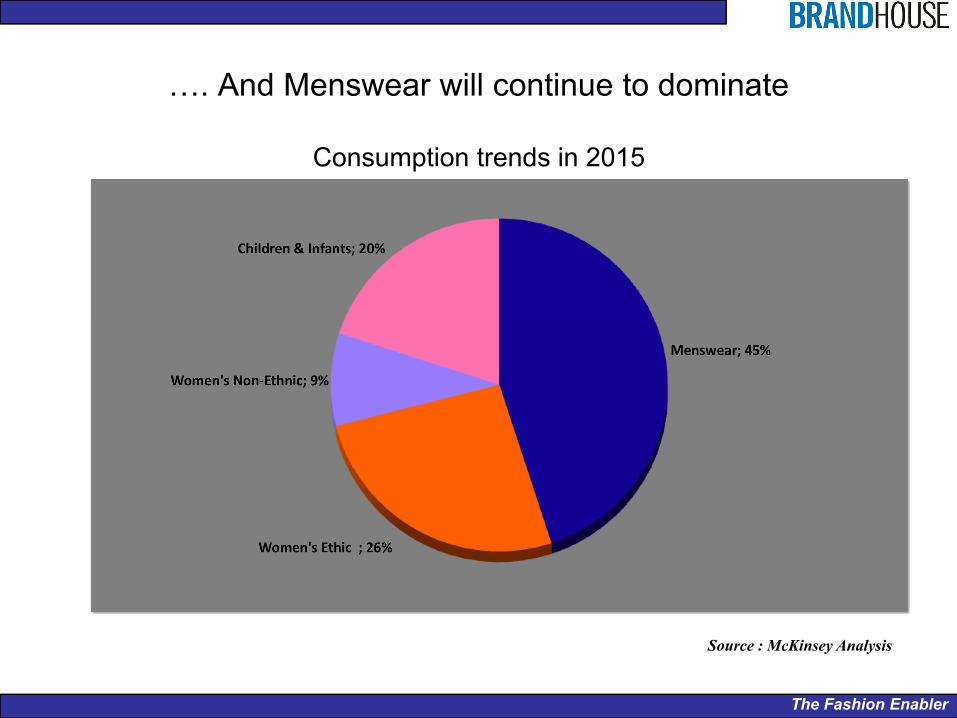

…. And Menswear will continue to dominate

Consumption trends in 2015

Source : McKinsey Analysis

The Fashion Enabler

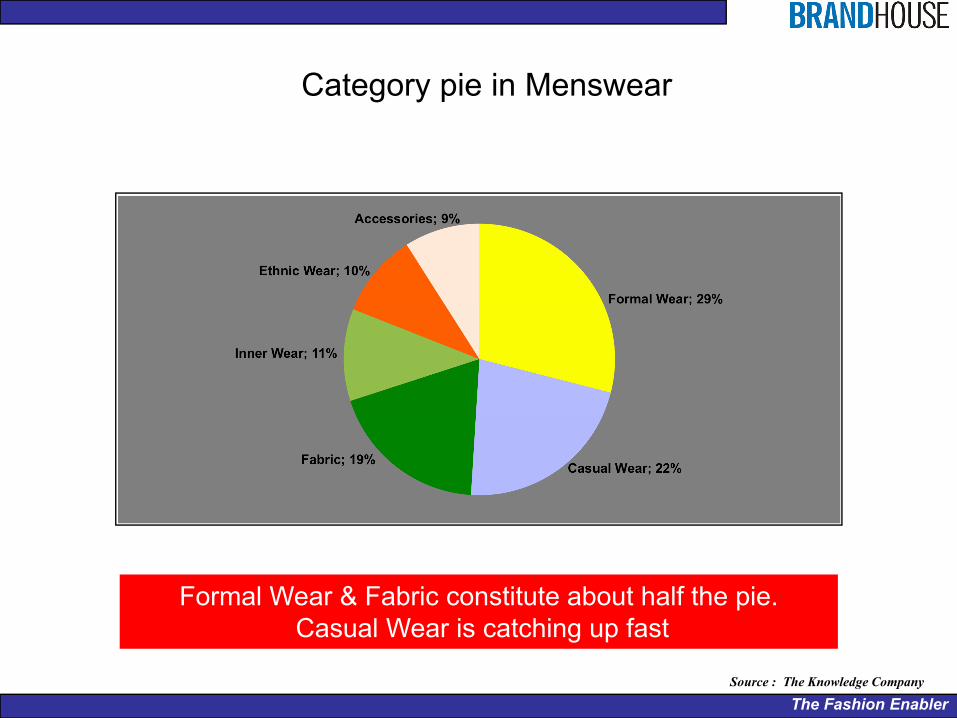

Category pie in Menswear

Source : The Knowledge Company

Formal Wear & Fabric constitute about half the pie.Casual Wear is catching up fast

The Fashion Enabler

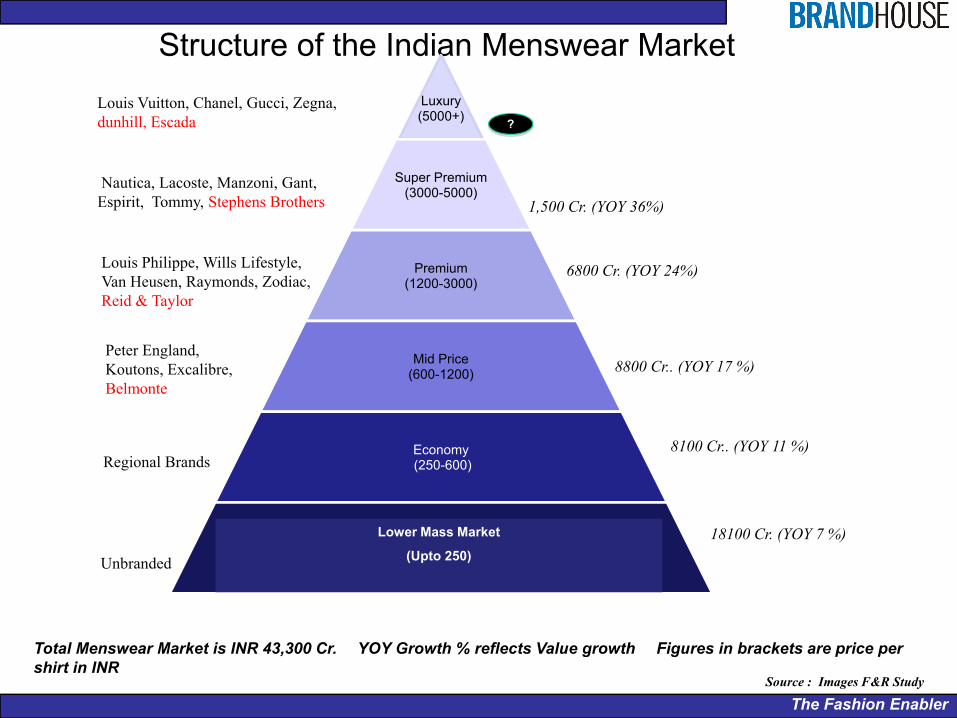

Structure of the Indian Menswear Market

Source : Images F&R Study

Louis Vuitton, Chanel, Gucci, Zegna, dunhill, Escada

Nautica, Lacoste, Manzoni, Gant, Espirit, Tommy, Stephens Brothers

Louis Philippe, Wills Lifestyle, Van Heusen, Raymonds, Zodiac, Reid & Taylor

Peter England, Koutons, Excalibre, Belmonte

Unbranded

1,500 Cr. (YOY 36%)

Regional Brands

Total Menswear Market is INR 43,300 Cr. � YOY Growth % reflects Value growth � Figures in brackets are price per shirt in INR

?

Lower Mass Market

(Upto 250)

Luxury(5000+)

Super Premium(3000-5000)

Premium(1200-3000)

Mid Price(600-1200)

Economy(250-600)

Lower Mass Market (Upto 500)

6800 Cr. (YOY 24%)

8800 Cr.. (YOY 17 %)

8100 Cr.. (YOY 11 %)

18100 Cr. (YOY 7 %)Lower Mass Market

(Upto 250)

The Fashion Enabler

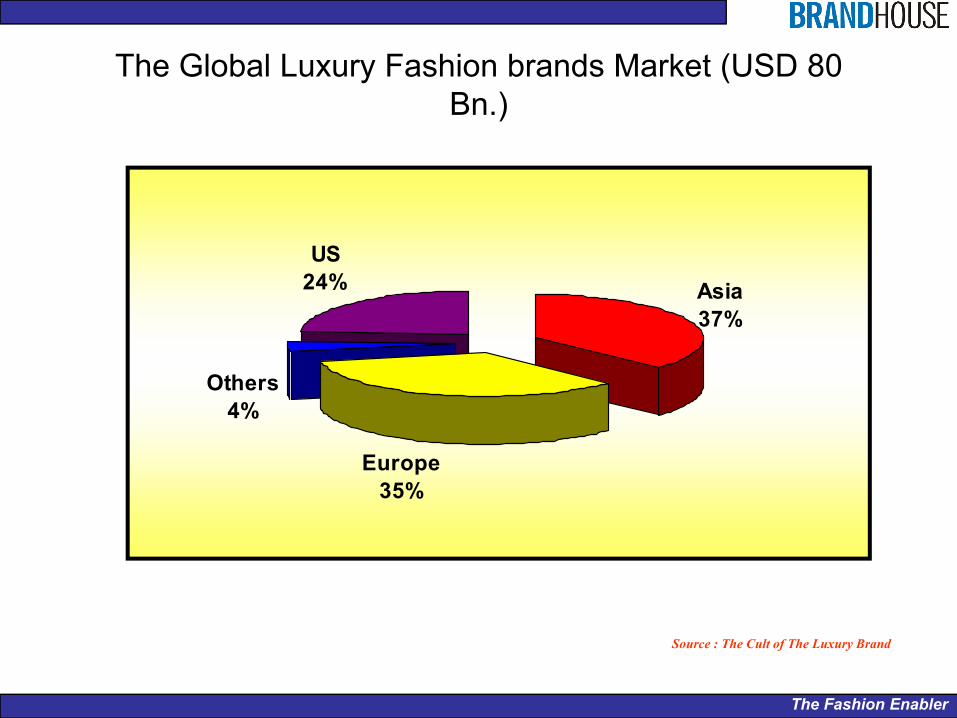

The Global Luxury Fashion brands Market (USD 80 Bn.)

Asia37%

Europe35%

Others4%

US24%

Source : The Cult of The Luxury Brand

The Fashion Enabler

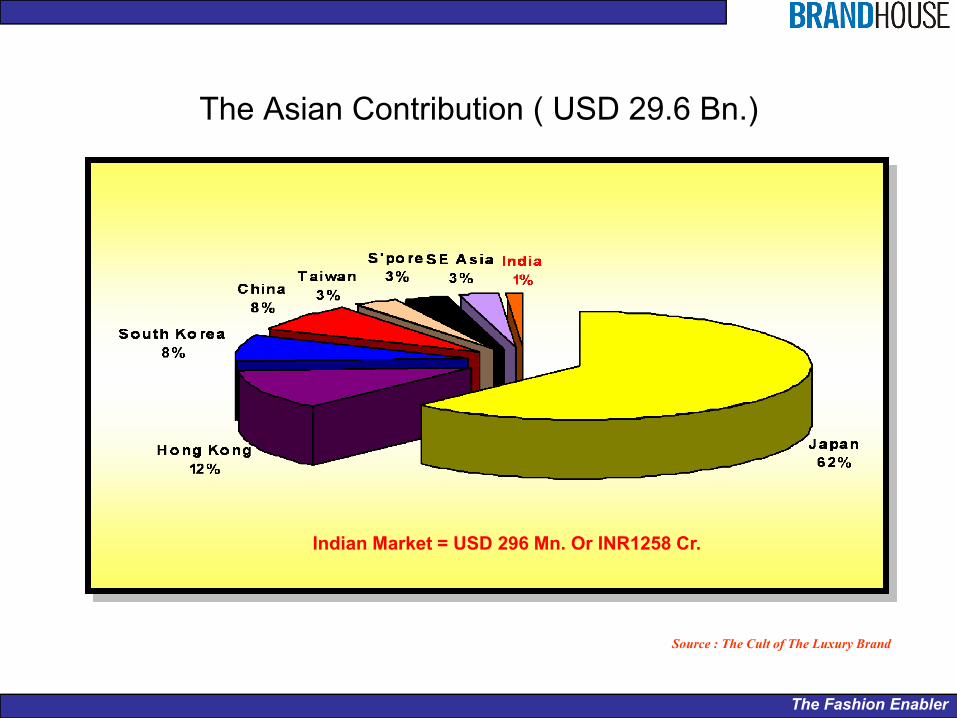

The Asian Contribution ( USD 29.6 Bn.)

Source : The Cult of The Luxury Brand

Indian Market = USD 296 Mn. Or INR1258 Cr.

The Fashion Enabler

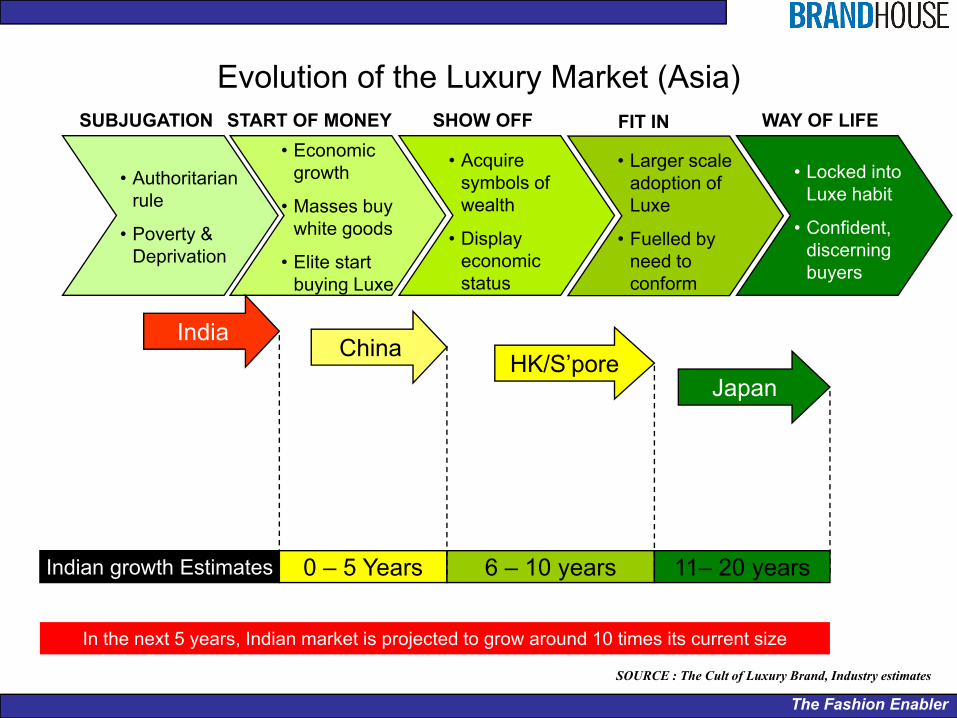

Evolution of the Luxury Market (Asia) SUBJUGATION

• Authoritarian rule

• Poverty & Deprivation

START OF MONEY• Economic

growth

• Masses buy white goods

• Elite start buying Luxe

SHOW OFF

• Acquire symbols of wealth

• Display economic status

FIT IN

• Larger scale adoption of Luxe

• Fuelled by need to conform

WAY OF LIFE

• Locked into Luxe habit

• Confident, discerning buyers

SOURCE : The Cult of Luxury Brand, Industry estimates

IndiaChina

HK/S’poreJapan

0 – 5 Years 6 – 10 years 11– 20 yearsIndian growth Estimates

In the next 5 years, Indian market is projected to grow around 10 times its current size

The Fashion Enabler

Section 5 : Looking Ahead (Future Plans)

The Fashion Enabler

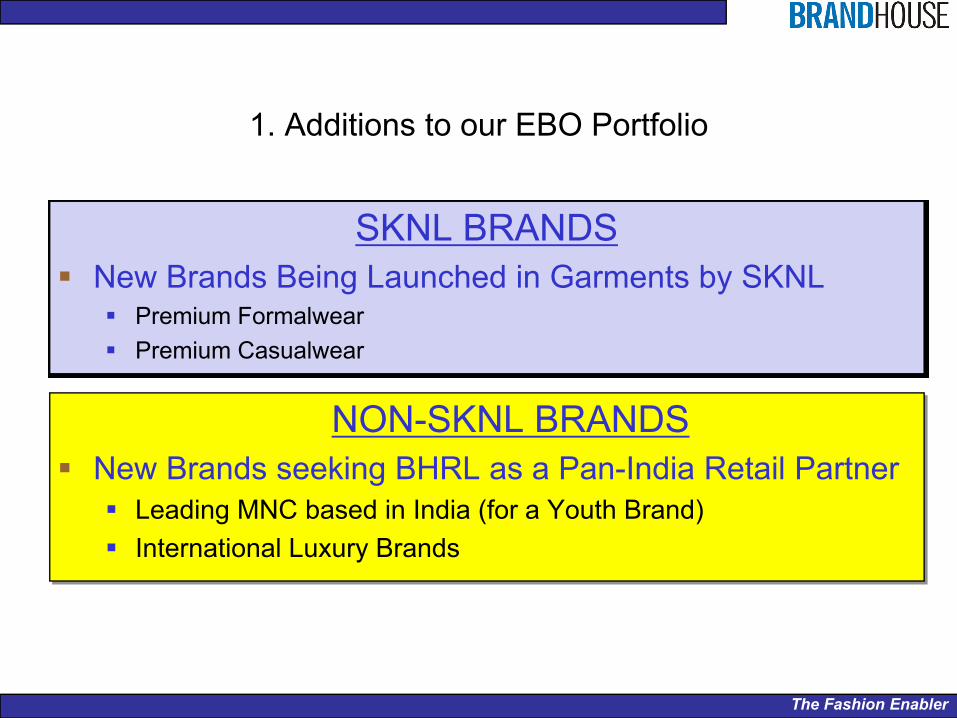

1. Additions to our EBO Portfolio

SKNL BRANDSNew Brands Being Launched in Garments by SKNL

Premium FormalwearPremium Casualwear

NON-SKNL BRANDSNew Brands seeking BHRL as a Pan-India Retail Partner

Leading MNC based in India (for a Youth Brand)International Luxury Brands

The Fashion Enabler

2. Introduction of the JV

The Fashion Enabler

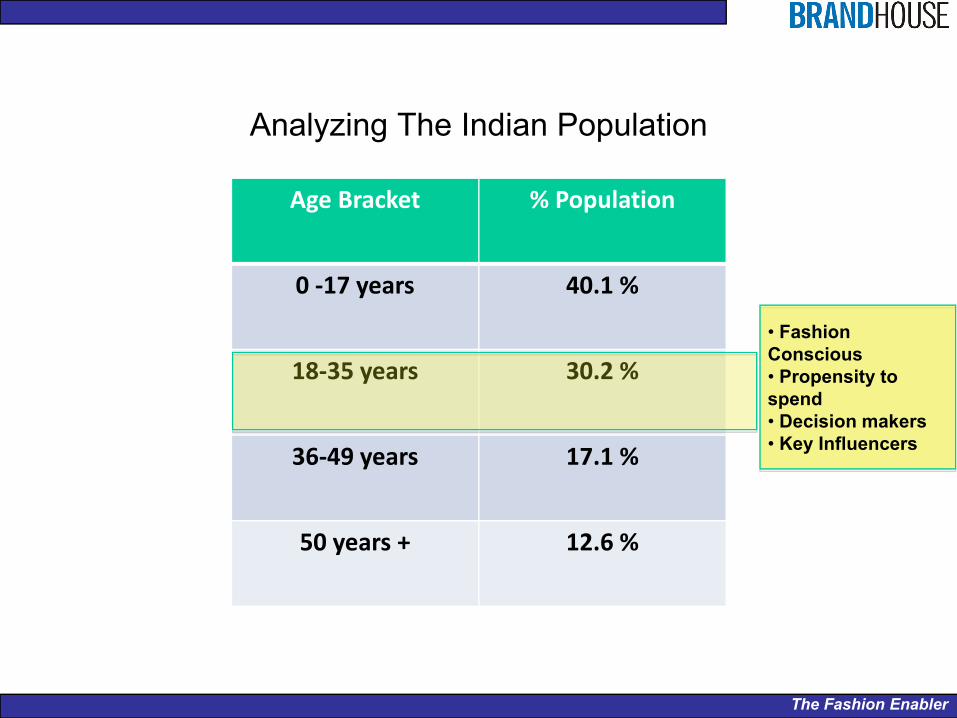

Age Bracket % Population

0 ‐17 years 40.1 %

18‐35 years 30.2 %

36‐49 years 17.1 %

50 years + 12.6 %

Analyzing The Indian Population

• Fashion Conscious• Propensity to spend• Decision makers • Key Influencers

The Fashion Enabler

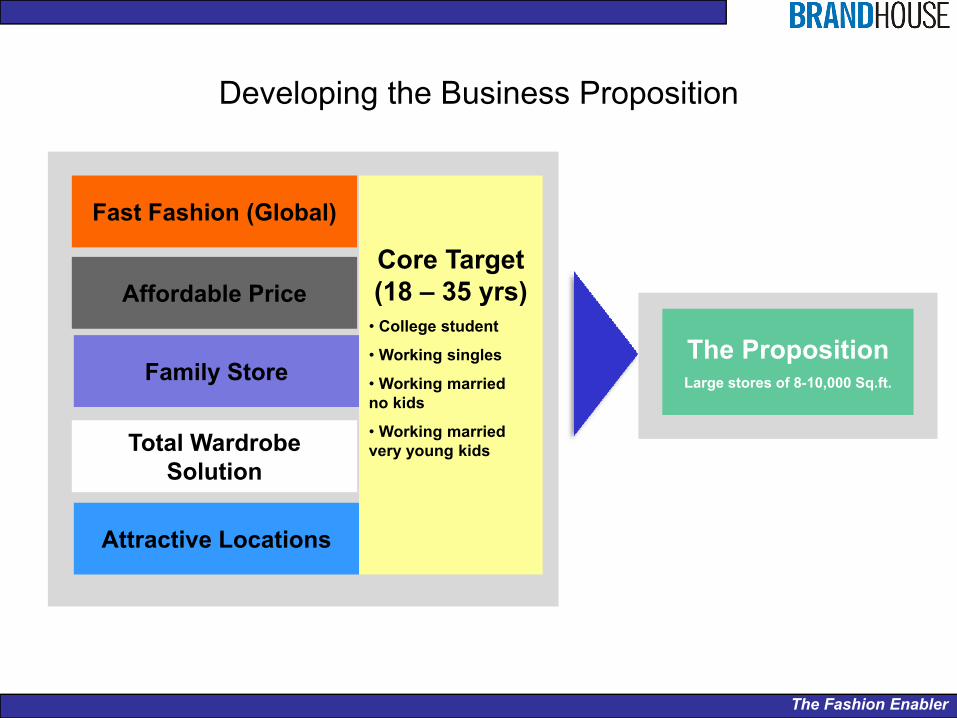

Developing the Business Proposition

Fast Fashion (Global)

Affordable Price

Attractive Locations

Family Store

Total Wardrobe Solution

Core Target (18 – 35 yrs)

• College student

• Working singles

• Working married no kids

• Working married very young kids

The PropositionLarge stores of 8-10,000 Sq.ft.

The Fashion Enabler

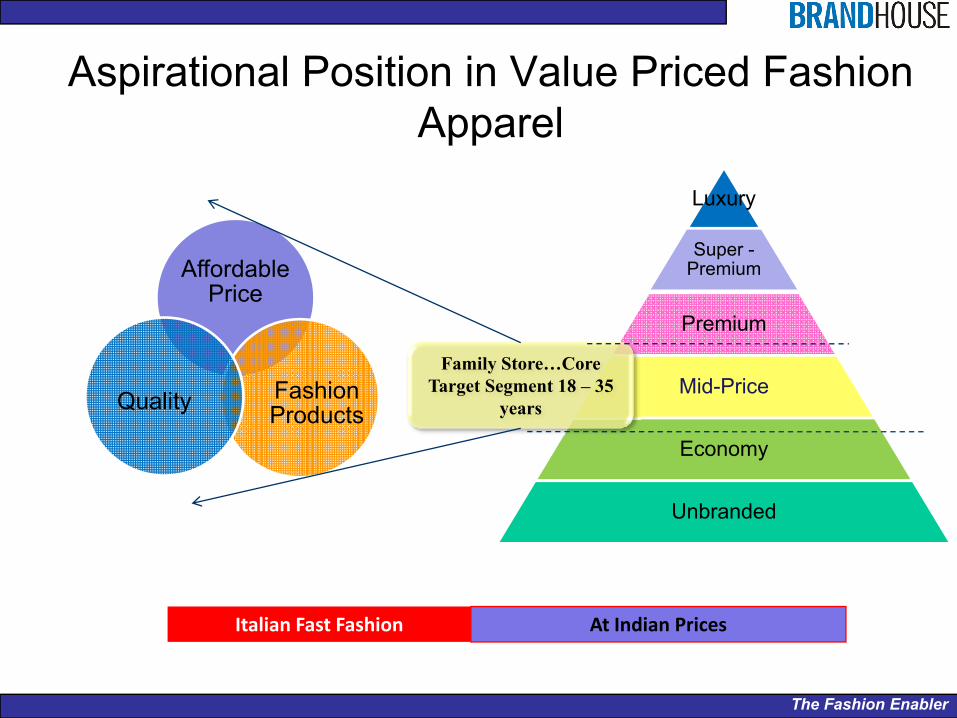

Aspirational Position in Value Priced Fashion Apparel

Luxury

Super -Premium

Premium

Mid-Price

Economy

Unbranded

Affordable Price

Fashion ProductsQuality

Family Store…Core Target Segment 18 – 35

years

At Indian PricesItalian Fast Fashion

The Fashion Enabler

Our Partner Oviesse –The Leader in Italian Fast Fashion

Part of Gruppo Coin, Italy’s leading fashion retailer with sales of over 1.1 billion EurosOviesse, the benchmark in Italian Fast Fashion

Over 11 million customers in Italy every yearOver 100 million garments sold every yearSales of over 820 million Euros

A favorite with Italian shoppers9% of the share of the wallet of Italian Consumers1in every 5 Italians shop at Oviesse every year1 in every 3 Italian Kids wear Oviesse apparel

Spreading beyond ItalyOver 340 stores in Italy & abroad

The Fashion Enabler

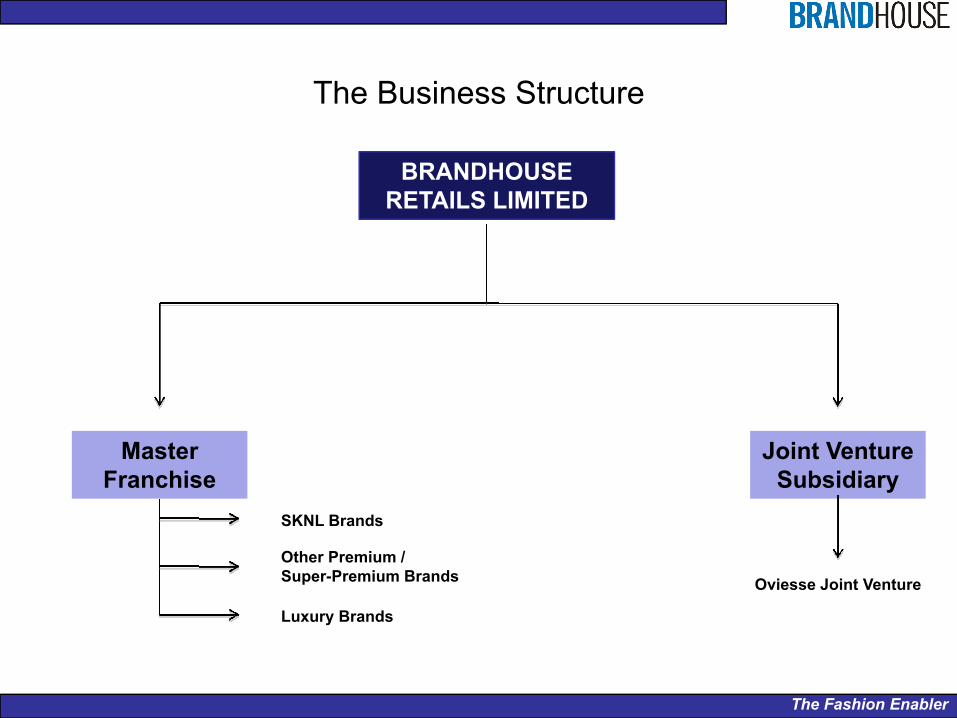

The Business Structure

BRANDHOUSE RETAILS LIMITED

Master Franchise

SKNL Brands

Other Premium / Super-Premium Brands

Joint Venture Subsidiary

Luxury Brands

Oviesse Joint Venture

The Fashion Enabler

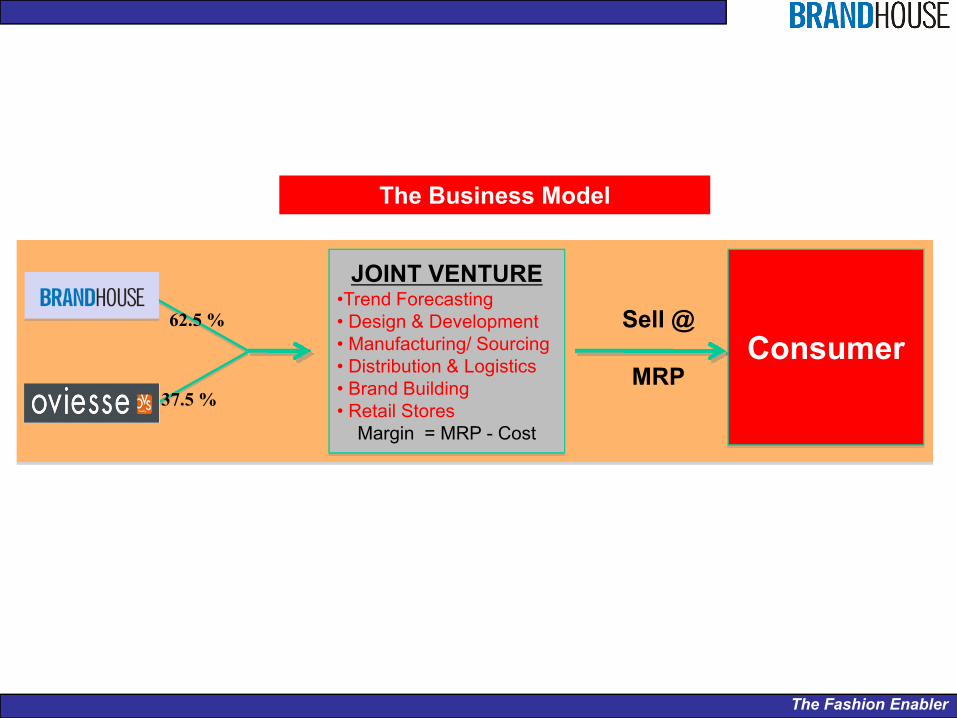

JOINT VENTURE•Trend Forecasting• Design & Development• Manufacturing/ Sourcing• Distribution & Logistics• Brand Building• Retail Stores

Margin = MRP - Cost

Consumer

The Business Model

Sell @

MRP

62.5 %

37.5 %

The Fashion Enabler

Thank You