Brand Behemoths United States - NYUpages.stern.nyu.edu/.../Lectures/brand_behemoths.pdf · Brand...

88

See page 86 for Analyst Certification and Important Disclosures Citigroup Research is a division of Citigroup Global Markets Inc. (the "Firm"), which does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Non-US research analysts who have prepared this report, and who may be associated persons of the member or member organization, are not registered/qualified as research analysts with the NYSE and/or NASD, but instead have satisfied the registration/qualification requirements or other research-related standards of a non-US jurisdiction. United States Edward M. Kerschner, CFA 212-816-3532 [email protected] Michael Geraghty 212-816-3534 [email protected] EQUITY RESEARCH: UNITED STATES Thematic Investing March 31, 2006 Brand Behemoths Executing Brand Leadership on a Global Basis ➤ Most brands fail, either in the near term or over the long run. Today, 30,000 new consumer products are launched each year, but more than 90% fail. Of the leading brands in 1923, only 23% remained leaders in the 1990s, while 28% had failed outright. ➤ In this environment, a handful of “brand behemoths” have a track record of successfully leveraging a leadership position in one region or category and extending their franchises into new markets. ➤ Examining more than 3,500 consumer nondurable brands, we identify ten brand behemoths for 2010: Colgate-Palmolive, Danone, Kellogg, Kimberly-Clark, L’Oréal, Nestlé, PepsiCo, Procter & Gamble, Unilever, and Wrigley. ➤ These ten brand behemoths are growing. We estimate they will be the leaders (i.e., No. 1 in market share) in about 50% of the consumer nondurable “brands space” by 2010, with the remaining 50% dispersed among 88 other companies; so these brand behemoths are still far from mature. ➤ There are projected to be 1.2 billion more consumers able to buy packaged goods by 2010 than there were in 2000. ➤ Four key factors that drive brand dominance: 1) a distinct competitive advantage, 2) exposure to regional growth opportunities, 3) “stretching” brands across categories, and 4) a prolonged period of share stability in a market.

Transcript of Brand Behemoths United States - NYUpages.stern.nyu.edu/.../Lectures/brand_behemoths.pdf · Brand...

See page 86 for Analyst Certification and Important Disclosures

Citigroup Research is a division of Citigroup Global Markets Inc. (the "Firm"), which does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Non-US research analysts who have prepared this report, and who may be associated persons of the member or member organization, are not registered/qualified as research analysts with the NYSE and/or NASD, but instead have satisfied the registration/qualification requirements or other research-related standards of a non-US jurisdiction.

Unit

ed S

tate

s

Edward M. Kerschner, CFA 212-816-3532 [email protected]

Michael Geraghty 212-816-3534 [email protected]

E Q U I T Y R E S E A R C H :

U N I T E D S T A T E S

Thematic Investing March 31, 2006

Brand Behemoths Executing Brand Leadership on a Global Basis

➤ Most brands fail, either in the near term or over the long run. Today, 30,000 new consumer products are launched each year, but more than 90% fail. Of the leading brands in 1923, only 23% remained leaders in the 1990s, while 28% had failed outright.

➤ In this environment, a handful of “brand behemoths” have a track record of successfully leveraging a leadership position in one region or category and extending their franchises into new markets.

➤ Examining more than 3,500 consumer nondurable brands, we identify ten brand behemoths for 2010: Colgate-Palmolive, Danone, Kellogg, Kimberly-Clark, L’Oréal, Nestlé, PepsiCo, Procter & Gamble, Unilever, and Wrigley.

➤ These ten brand behemoths are growing. We estimate they will be the leaders (i.e., No. 1 in market share) in about 50% of the consumer nondurable “brands space” by 2010, with the remaining 50% dispersed among 88 other companies; so these brand behemoths are still far from mature.

➤ There are projected to be 1.2 billion more consumers able to buy packaged goods by 2010 than there were in 2000.

➤ Four key factors that drive brand dominance: 1) a distinct competitive advantage, 2) exposure to regional growth opportunities, 3) “stretching” brands across categories, and 4) a prolonged period of share stability in a market.

Brand Behemoths – March 31, 2006

2

Investment Summary ...................................................................................................................................... 3 Why Brands Matter......................................................................................................................................... 4 Looking for Brand Behemoths.......................................................................................................................... 6 The Origin of Brands ...................................................................................................................................... 8 Wedgwood: An Aspirational Brand ................................................................................................................ 9 19th Century Branding: Quality and Reliability........................................................................................... 11 Professional Brand Management.................................................................................................................... 15 Postwar Market Segmentation ........................................................................................................................ 18 Behind Branding .............................................................................................................................................. 22 The Importance of Intangibles........................................................................................................................ 22 It’s Not Enough Just to Be First...................................................................................................................... 25 Identifying Brand Behemoths...................................................................................................................... 26 A Unique Database .......................................................................................................................................... 26 Brand Leaders and Brand Behemoths............................................................................................................ 27 A Distinct Competitive Advantage.............................................................................................................. 30 Branding the Basics ......................................................................................................................................... 31 Globally Local.................................................................................................................................................. 36 Behavior Modification..................................................................................................................................... 43 New and Improved........................................................................................................................................... 49 “Economies of Skill” ....................................................................................................................................... 51 Exposure to Regional Growth Opportunities............................................................................................ 53 “Stretching” — Extending Brands Across Categories ............................................................................ 60 Stretching and Brand Behemoths.................................................................................................................... 61 A Prolonged Period of Share Stability in a Market ................................................................................. 66 Appendix A ..................................................................................................................................................... 71 Biographies....................................................................................................................................................... 71 Appendix B...................................................................................................................................................... 72 General Forecasting Principles ....................................................................................................................... 72 Appendix C ..................................................................................................................................................... 75 Projected Brand Leaders in 2010.................................................................................................................... 75 Appendix D ..................................................................................................................................................... 82 Projected Brand Leader in 2010 by Region for 30 Categories ..................................................................... 82

The following analysts contributed to this report: Warren Ackerman, Chip Dillon, David Driscoll, Bonnie Herzog, Wendy Nicholson, and Andy Smith.

Peter N. Golder, PhD (associate professor, department of marketing, Stern School of Business, New York University) and Joel H. Steckel, PhD (professor, department of marketing, Stern School of Business, New York University) acted as consultants for this report.

Table of Contents

Brand Behemoths – March 31, 2006

3

Brand behemoths successfully leverage a leadership position in one category or region and extend that franchise into new markets.

Four key factors drive brand dominance. 1 A distinct competitive advantage, reflected in a large market share lead, and

derived through the following strategies:

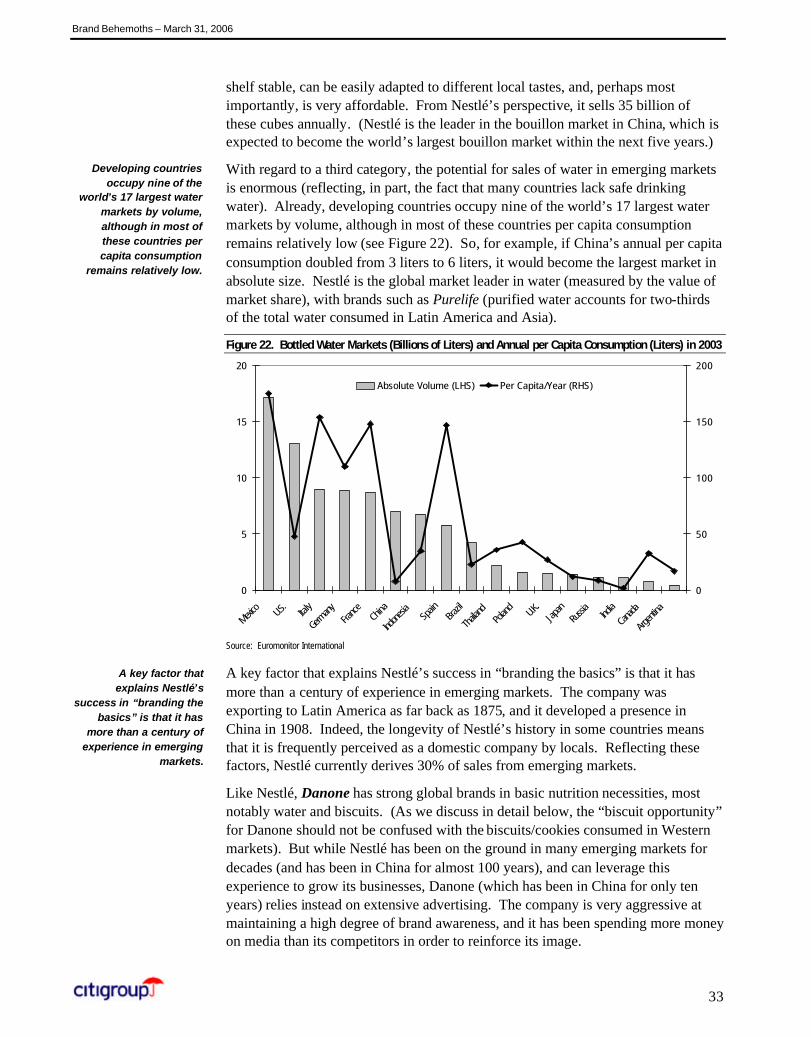

➤ Branding the Basics: Benefiting from the growing number of global consumers who can afford the most basic packaged foodstuffs such as bottled water, biscuits, and milk (Nestlé and Danone).

➤ Globally Local: A strategy that stimulates consumer purchasing of more advanced packaged foodstuffs by carefully adapting products to local market conditions, such as roasted hot pepper–flavored mayonnaise in Brazil, Masala-flavored chips in India, and raisin-flavored bran cereal targeted at the elderly in the U.S. (Unilever, PepsiCo, and Kellogg).

➤ Behavior Modification: Changing consumer habits, e.g., from cleaning teeth with a stick to using a toothbrush, and from washing hair with soap to using shampoo (Colgate-Palmolive, Wrigley, and Procter & Gamble).

➤ New and Improved Products: Driving sales growth by encouraging consumers to “trade up” to products such as new and improved lipstick that stays on longer (L’Oréal).

➤ “Economies of Skill”: Reflecting an intense focus on, and a technological understanding of, a few key categories, such as facial tissues, where the production process adds value of $1,900 per ton (Kimberly-Clark).

2 Exposure to regional growth opportunities, e.g., the 1.2 billion incremental consumers Nestlé forecasts to be able to afford packaged goods by 2010.

3 Stretching, that is, extending brands across categories, e.g., from Kellogg’s cereals to breakfast bars, from Kimberly-Clark’s baby diapers to adult incontinence products, or from L’Oréal’s women’s skin care products to skin care products for men.

4 A prolonged period of share stability in a market — these behemoths have been around a long time, and not just in their home markets. The longer a company has enjoyed market share stability, the more time it will have had to exploit that position by extending its distribution network and/or by more fully understanding consumer preferences.

Our thematic outlook is not without risk. The key risk to our behemoth theme is that some of the ten companies we have identified lose their ability to maintain brand leadership. We further note that our analysis does not consider stock-specific metrics such as valuation, EPS, and P/E ratios, or balance sheets, market capitalization, and liquidity. Accordingly, when making decisions, investors should view thematic analysis as only one input. Further, since this analysis employs a longer-term methodology, its results may differ from the conclusions of fundamental analysis.

Brand Behemoths – March 31, 2006

4

Professional brand management has been practiced for close to a century. However, it is likely that it is more difficult to build a brand today than it was only a few decades ago.

➤ First, it is increasingly difficult to reach consumers due to greater media fragmentation.

➤ Second, the number of brands is proliferating. According to the Harvard Business Review1, 30,000 new consumer products are launched each year — although more than 90% of them fail — which means increased competition for consumer mindshare, access to the distribution channel, and marketing dollars.

It is likely, then, that leading brands have become even more valuable given that they can offer some, or all, of the following attributes:

➤ Premium Pricing. An increased emphasis on price, often involving the heavy use of price promotions, is resulting in a growing number of commodity-like products. In this environment, leading brands can usually command relatively high margins by way of premium pricing, as well as reduced reliance on promotions. The power of brands to command superior pricing is well illustrated by the unusual case of Chivas Regal, which used a high price to turn itself into a premium brand. Chivas was a struggling brand until it decided to raise its price to be dramatically higher than competitors’, at which point its sales took off. Price clearly became a quality cue for this brand, as the product itself was not changed. More recently, Grey Goose redefined the vodka category and fueled the super-premium boom — the brand’s French provenance, the distinctive frosted bottle, and the wooden case all helped justify a hefty price to consumers.

➤ Economies of Scale. A market leader can operate at a more efficient volume and earn higher profits than a rival that commands a narrow market niche. So, for example, Procter & Gamble reaps tremendous economies of scale because of its leadership position in household products.

➤ Barriers to Entry. Once familiar with a brand, consumers are likely to exhibit a degree of brand loyalty, making it much more difficult for a competing product to succeed in the marketplace. It’s likely that loyalty explains why Wrigley has remained the dominant brand in its category for decades — after all, chewing gum is quite easy to manufacture. (Then, too, most consumers will only put in their mouths something that comes from a trusted company.)

➤ Brand Extensions. Brands can offer a company an opportunity for growth via brand extensions (e.g., Unilever’s extension of its Dove soap brand into deodorant and shampoo). A promotion of a new product will likely be more effective if the brand is familiar, and if there is no need to combat consumer skepticism about brand quality.

1 Clayton M. Christensen, Scott Cook, and Taddy Hall, “Marketing Malpractice,” Harvard Business Review, December 2005.

The key risk to our behemoth

Why Brands Matter

30,000 new consumer products are launched

each year, although more than 90% of them

fail.

The power of brands to command superior

pricing is well illustrated.

Most consumers will only put in their mouths

something that comes from a trusted company.

Brand Behemoths – March 31, 2006

5

➤ Leverage in the Distribution Channel. A leading brand is likely to enjoy superior product placement or preferred shelf space in retail outlets frequented by increasingly time-starved consumers.

➤ Growth Potential in Developing Markets. Standards of living are rising rapidly in developing economies. As a result, consumers in these markets have growing amounts of disposable income to spend on branded products, which are often valued because of the perceived quality they offer. That’s not to say, however, that there is a global market for strictly uniform products. To the contrary, varying global tastes explain why, for example, in India, Frito-Lay offers a Masala-flavored potato chip (seasoned with freshly ground spices) and, in Latvia, it offers a paprika-flavored chip.

Reflecting the increased scarcity of quality brands, some of the recent corporate takeover frenzy has been focused on companies that possess assets that are virtually impossible to build quickly: strong, well-regarded franchises. A June 23, 2005, Wall Street Journal article, “Buying Spree by China Firms Is a Bet on Value of U.S. Brands,” pointed out that:

In recent months, a string of Chinese electronics makers with little international name recognition have attempted to vault into American and European homes by buying Western brands. Chinese television-set maker TCL Corp. did it first, taking control of the manufacturing operations of RCA-brand owner Thomson SA of France. Then computer maker Lenovo Group bought the personal computer operations of International Business Machines Corp., of the U.S., earlier this year. And this month Taiwanese electronics maker BenQ Corp. took over the cell phone operations of Germany’s Siemens AG.

In addition, China’s Haier Group launched a bid for home-appliance icon Maytag Corp. The reason behind this trend, according to the June 2005 Journal, article is as follows:

The toughest challenge facing the Chinese companies that already make many of the world’s appliances and electronics: how to transition from low-cost, often no-name manufacturers to respected global brands [italics added].

In India, Frito-Lay offers a Masala-flavored potato

chip and, in Latvia, a paprika-flavored chip.

Recent takeover activity has been focused on

companies that possess assets that are virtually

impossible to build quickly: strong, well-regarded franchises.

Brand Behemoths – March 31, 2006

6

Looking for Brand Behemoths For some observers, it’s conventional wisdom that the “first immutable law of marketing” is that “it’s better to be first, than it is to be better.”2 For the most part, we disagree. Today, there are many companies that maintain brand dominance largely because they were first to market — Clorox and Coca-Cola are examples of two companies whose business models remain largely unchanged from their earliest days.

Then there are another set of companies that are dominant branders — these “brand behemoths” have the skill set necessary to continuously develop brands in multiple categories and multiple regions. They leverage a leadership position in one category or region and extend that franchise into new markets. Importantly, these companies succeed where many others fail — as outlined above, the failure rate of new products is more than 90%. (In addition, we note that, with advertising and production costs on the rise, failure in a product introduction is not an insignificant event.) As we discuss in detail below, brand behemoths offer the potential for growth, in sharp contrast to other branded companies that struggle to innovate beyond their core franchise.

But what is the skill set necessary for a company to be a dominant brander? How does a company establish brand leadership in one category or region and then leverage that position into other markets? In other words, what does it take to be a brand behemoth?

Those are some key questions we set out to address. Working with Citigroup Investment Research analysts, and with Professors Peter N. Golder and Joel H. Steckel of the marketing department at New York University’s Stern School of Business, we examined hundreds of companies in 30 consumer nondurable product categories across eight geographic regions. (Please see Appendix A for the biographies of Professors Golder and Steckel.) The result of our research is that we have identified ten brand behemoths — companies that we believe clearly demonstrate “branding skill” by their ability to expand market share across categories and regions (see Figure 1).

As part of the study of these ten companies, Citigroup Investment Research strategists and the relevant fundamental industry analysts sought the viewpoints of key personnel at the companies in order to gain a deep understanding of how they approach branding. We note that the Citigroup Investment Research analysts sought out the managers responsible for the development and implementation of branding strategies rather than investor relations contacts.

2 Al Ries and Jack Trout, The 22 Immutable Laws of Marketing (New York: HarperCollins, 1993).

“Brand behemoths” leverage a leadership

position in one category or region and extend that

franchise into new markets.

We examined hundreds of companies in 30

consumer nondurable product categories

across eight geographic regions.

Brand Behemoths – March 31, 2006

7

Figure 1. Ten Brand Behemoths

Colgate-Palmolive is adept at changing global consumer habits, most notably in the area of oral hygiene. It educates consumers (mainly in

developing regions) on the benefits of regularly cleaning their teeth with a toothbrush and toothpaste, and then expands their usage of oral hygiene products, e.g., into mouthwash and tooth whiteners.

Danone is skilled at branding some of the basic necessities (e.g., water and nutritious biscuits), for which there is strong demand in emerging

markets. In many countries without safe drinking water, Danone’s brands are a trusted source — it owns four of the world’s largest water brands,

and is the global market leader by volume. Danone’s biscuits are perceived as a cheap source of nutrition for low-income consumers in emerging

markets.

Kellogg is skilled at assimilating its ready-to-eat cereals into changing markets. It modifies its cereals to reflect 1) jaded taste buds (consumers

get tired of the same old cereal each day); 2) the latest consumer trends (e.g., demand for “healthy” products); and 3) demographic factors (e.g., an

aging population’s appetite for bran). The company has used its strong cereal franchise to support an expansion into breakfast snack bars.

Kimberly-Clark is intensely focused on a few key categories, which enables it to reap “economies of skill” in the manufacture of its products. Its

key tissue business accounts for more than half of revenues, in sharp contrast to some of its larger competitors that are much more diversified.

For diapers (about 20% of sales), the emerging markets of China and India offer tremendous potential as, for example, spreading urbanization

means that parents likely won’t want to risk an “accident” by their child in, say, a store or an office. Adult incontinence currently represents only

about 10% of revenues, but that segment should grow rapidly as Kimberly leverages the expertise gained in diapers to exploit the opportunity created by aging boomers in the Western world.

L’Oréal is notable for its innovation, a key factor that drives sales growth in developed markets by encouraging consumers to “trade-up.” So, it

has recently developed a “new and improved” lipstick (that stays on longer) and mascara (that makes eyelashes curlier). A shift in the company’s

portfolio towards skin care reflects, in part, L’Oréal’s focus on developing markets, such as China and India, where skin care — including whiteners and anti-blemish creams — is a major area of growth.

Nestlé has a deep understanding of the basic nutrition needs of global consumers, particularly those in emerging markets. When the company

was founded in 1867, infant formula was its first product, and milk, in all its forms, is still at the heart of Nestlé. The company has over a century

of experience in emerging markets — it was exporting to Latin America as far back as 1875, and established a presence in China in 1908. The

longevity of Nestlé’s history in some countries means that it is frequently perceived as a domestic company by locals, a factor that reinforces trust

in its brands.

PepsiCo assimilates its snack products by carefully adapting to local market conditions, which typically means catering to different taste

preferences in developing markets (e.g., a Masala-flavored potato chip in India, paprika-flavored in Latvia), and changing taste preferences in

developed markets (e.g., the current interest in “eating healthy” in the U.S., and preference for tasty snacks with relatively little fat).

Procter & Gamble is particularly skilled at analyzing, understanding, and modifying consumer behavior on a global basis. In developing markets,

P&G launches new product categories (e.g., laundry detergent) with value pricing, conditions consumers to use the product, and then encourages

those consumers to trade up to a more value-added version.

Unilever is notably successful in difficult categories and difficult markets thanks, in large part, to its expertise at assimilation. By carefully adapting

to local preferences, the company has the No. 1 market share position in most of the global food categories in which it competes. This is despite

the fact that, in contrast to many household products, it is generally difficult to migrate global consumers to higher-priced, branded, packaged

foods, reflecting sharp differences in local tastes. In fast-growth emerging markets that lack a conventional supermarket format, Unilever has a unique distribution infrastructure that reaches 6 million retail outlets throughout Asia and Africa.

Wrigley is adept at integrating chewing gum into societies where gum consumption was previously not part of the culture. In addition, thanks to

heavy spending on new product innovation, the company has been expanding its product line to offer a full range of fresh breath solutions e.g.,

thin-film breath strips and mints. Wrigley’s commanding market shares support high margins which, in turn, enable it to defend its position by way of 1) heavy advertising and 2) aggressive consumer promotions.

Source: Citigroup Investment Research

Brand Behemoths – March 31, 2006

8

In order to understand how we find ourselves in an environment in which 30,000 new consumer products are launched each year, it is instructive to briefly review the evolution of brands. The Oxford English Dictionary (OED) traces the word “brand” back to about the tenth century, when it connoted a burning piece of wood. By the 16th century, the word’s meaning had widened to include distinctive marks, including those made by burning the hide of animals with a hot iron in order to designate ownership (see Figure 2).

Figure 2. The Evolution of the Word “Brand”

Recorded Use Meaning

c. 950 A piece of wood that is, or has been, burning on the hearth.

1552 The mark made by burning with a hot iron.

1827 A trademark, whether made by burning or otherwise.

1854 A particular sort or class of goods, as indicated by the trademarks on them.

1958 The impression of a product in the minds of potential users or consumers.

Source: Oxford English Dictionary

The OED records that a mark (or brand) on a product (made by burning or otherwise), also came to indicate specific quality standards and genuineness. Trademarks were applied to casks of wine, timber, and metals, including gold. So, for example, trade guilds like the Goldsmith’s Company of London stamped all its goods. In this way, the use of a brand had primarily defensive connotations: trademarks on products were used to protect buyers from fraudulent goods.

While the word “brand” appears to have originated around the tenth century, the concept of a brand has certainly been around for much longer. For example, in ancient Rome some potters identified their products by imprinting their initials into the pot’s wet clay (see Figure 3), reflecting that pottery was sometimes sold far from the workshops where it was made, and buyers looked for the stamp of reliable potters as a guide to quality. Chinese porcelain was also brand-marked, as were metal tools and implements in ancient China.

The Origin of Brands

A brand came to indicate specific quality standards and genuineness.

While the word “brand” appears to have

originated around the tenth century, the

concept of a brand has certainly been around for

much longer.

Brand Behemoths – March 31, 2006

9

Figure 3. Roman Bronze Stamp Used as a Pottery Workshop Trademark (Initials C B V) second to fourth century AD

Source: Hixenbaugh Ancient Art

For centuries, however, factors that limited the development of brands as they are known today included the absence of mass-production techniques, inadequate transportation systems, the lack of printing technologies, and widespread illiteracy. It would take until the 18th century for those hurdles to be overcome.

Wedgwood: An Aspirational Brand It’s arguable that one of the first consumer brands, in the modern sense, was the pottery and china of Josiah Wedgwood. Of course, in the mid-18th century, a handful of luxury goods — such as Chippendale furniture and Meissen porcelain — were known by their manufacturer’s name, but Wedgwood succeeded in creating a mass market for his products.

Until Wedgwood, the vast majority of Britons ate off wood and pewter plates. The exception was the aristocracy who, in the early 18th century, ate off elegant, hand-painted china made by skilled artisans. But rising incomes in 18th century Britain meant that the lower classes had more money to spend on nonessential goods, including china. Those rising incomes were directly attributable to the Industrial Revolution in Britain, which boosted industrial productivity. At the same time, agricultural and commercial productivity also increased, while the nation’s international trade boomed too.

In a highly class-conscious society, a growing number of middle class Britons opted to use this increased income for the purpose of social emulation, i.e., imitating the habits and purchases of the classes above them. In that regard, the ultimate arbiters of fashion in 18th century England were aristocrats and the nobility. Significantly, like many companies today, Josiah Wedgwood understood the value of celebrity endorsement. So, thanks to gifts of his finest products, Wedgwood was appointed as “Potter to Her Majesty,” Queen Charlotte, wife of George III. Wedgwood was also commissioned by Catherine the Great of Russia to make a 50-person dinner and dessert service, consisting of 952 hand-painted pieces.

One of the first consumer brands, in the

modern sense, was the pottery and china of

Josiah Wedgwood.

Like many companies today, Josiah Wedgwood

understood the value of celebrity endorsement.

Brand Behemoths – March 31, 2006

10

Wedgwood outlined his “mass-market” strategy in a letter to a partner about the market for his vases:

The Great People have had their vases in their Palaces long enough for them to be seen and admired by the Middling Class of People, which class we know are vastly, I had almost said, infinitely superior in number to the Great, and though a great price was, I believe, at first necessary to make the vases esteemed Ornament for Palaces, that reason no longer exists. Their character is established, and the middling People would probably buy quantitys [sic] of them at a reduced price.3

Although it is improbable that Wedgwood ever used the word “brand” in the modern sense, he had a firm grasp of the concept, especially when it came to his own products. In another letter, he implicitly acknowledged that the demand for his china was driven by factors other than its “utility” and, instead, by what we would call today, the aspirational appeal of the brand:

It is really amazing how rapidly…[our china] has spread over almost the whole Globe, & how universally it is liked. How much of this general use, & estimation, is owing to the mode of its introduction & how much to its real utility & beauty? are questions in which we may be a good deal interested for the government of our future Conduct.…For instance, if a Royal, or Noble Introduction be as necessary to the sale of an Article of Luxury as real Elegance & beauty, then the manufacturer, if he consults his own interest will bestow as much pains, & expense too if necessary, in gaining the former of these advantages, as he would in bestowing the latter.4

With regard to an actual trademark, until about 1770, most British potters did not mark their products. The few manufacturers that did typically used signs, symbols, or the location of the factory as identifying marks. Wedgwood changed this practice in the late 1760s by impressing his own name in the wet clay. His earthenware was thus much less vulnerable to forgery and, perhaps, more importantly, every piece advertised the Wedgwood name.

While demand side factors were critical to Wedgwood’s success, innovations on the supply side were important too. As noted above, the hand-painted china used by the aristocracy was made by skilled artisans. However, novel manufacturing methods and organizational arrangements brought about by the Industrial Revolution facilitated the production of simpler, much less expensive, china for the masses. Wedgwood employed a division of labor in the manufacture of china and separated the production of useful ware from that of ornamental ware, with the workshops for both the useful and ornamental incorporating all the latest technologies.

Wedgwood also took advantage of advancements in transportation, so that finished goods traveled by ship and canal barge to burgeoning urban areas. In addition, taking advantage of greater levels of literacy, Wedgwood sought to reach out to households through company catalogs (see Figure 4) and newspaper ads. 3 Josiah Wedgwood to Thomas Bentley, August 1772, Wedgwood Manuscripts, Keele University Library. 4 Josiah Wedgwood to Thomas Bentley, September 1767, Wedgwood Manuscripts, Keele University Library.

Demand for Wedgwood’s china was driven by the

aspirational appeal of the brand.

By impressing his own name in the wet clay, he

was less vulnerable to forgery, and every piece

advertised the Wedgwood name.

Brand Behemoths – March 31, 2006

11

Figure 4. Page from the Wedgwood Useful Ware Catalogue, 1774

Source: Image courtesy of the Wedgwood Museum Trust, Barlaston, Staffordshire (England)

19th Century Branding: Quality and Reliability One hundred years later, the demand-supply environment in the U.S. was very similar to that in which Wedgwood first developed a mass market for his products. On the demand side, productivity gains spurred by industrialization raised Americans’ incomes, while urbanization reduced the reliance on self-production (and also helped increase literacy, with the percentage of illiterate Americans dropping from 20% in 1870 to 10% in 1900). In addition, women were entering the paid workforce in large numbers, which spurred demand for convenient processed foods although, as we discuss below, the quality and reliability of products was a critical factor in the minds of consumers. On the supply side, improvements in manufacturing and communications allowed the mass marketing of consumer products.

From Middlemen to Mass Production For most of the 19th century, wholesalers controlled the distribution of consumer products in the U.S. The major factor dictating the fragmented marketplace was the absence of a transportation and communication infrastructure spanning the continent. These middlemen bought in large quantities and sold in small ones, putting their own names on the products they offered. (Indeed, one business historian5 observed that “prior to the 1880s most manufacturers were unknown to the people who bought their products.”) But given that these small-scale middlemen supplied just a local market, the quality of products varied considerably from region to region, especially given that several suppliers’ products were often mixed together.

5 Richard Tedlow, New and Improved: The Story of Mass Marketing in America (New York: Basic Books, 1990).

Productivity gains, spurred by

industrialization, raised Americans’ incomes,

while urbanization reduced the reliance on

self-production.

Women entering the workforce spurred

demand for convenient processed foods.

Brand Behemoths – March 31, 2006

12

In the 1880s, new methods of manufacturing (such as mass production) led to greatly increased output, decreased costs, and standardized products for the makers of consumer goods. (As we discuss below, it wasn’t until production techniques became more flexible, after World War II, that market segmentation became feasible.) Continuous process machinery was invented almost simultaneously for making cigarettes, matches, flour, breakfast cereals, soups and other canned products, and photographic film.

At the same time, improvements in packaging facilitated the manufacture of individual (as opposed to bulk) packages. Some of these packaging improvements included the toothpaste tube (1890), an effective cap for soda bottles (1892), easily fillable cans (1898), and freshness-sealing packaging for crackers and cereals (1899).

On top of these developments, the branding of individual packages with a proprietary trademark could be achieved, in part, through the creative design of packaging, which no longer served the sole purpose of protecting the contents. High-speed lithographic presses and other printing advances facilitated the reproduction of colorful and distinctive labels.

The brands of many of the consumer product companies at the forefront of these various 19th century advances remain well-known today, including Borden, Campbell Soup, Carnation, Eastman Kodak, Heinz, Pillsbury Flour, and Quaker Oats. It was early in this period that the Moon and Stars began to appear as the unofficial trademark of Procter & Gamble (see Figure 5). Wharf hands used the symbol to distinguish boxes of Star Candles. By the 1860s, the Moon and Stars appeared on all P&G products and correspondence.

Figure 5. Procter & Gamble’s Moon and Stars Trademark

Source: Used with permission of Procter & Gamble

Two other factors that facilitated the development of a mass consumer market in the U.S. in the late 19th century were the continental railroad system and the telegraph network. Consumer goods companies came to realize that what they could distribute nationally, they could advertise nationally.

In the 1880s, mass production led to greatly

increased output, decreased costs, and

standardized products.

Improvements in packaging facilitated the

manufacture of individual packages.

Printing advances facilitated the

reproduction of colorful and distinctive labels.

Brand Behemoths – March 31, 2006

13

Advertising was quite prevalent throughout the 19th century, although among the most widely advertised consumer products were patent medicines, about which extravagant claims were often made. Medicine potions such as Swaim’s Panacea, Fahnestock’s Vermifuge, and Perry Davis’s Vegetable Pain Killer were well known brands to the public. Indeed, one study6 showed that, as late as 1893, more than half of a sample of 104 firms that spent more than $50,000 annually on advertising were patent medicine manufacturers. (Only seven of the companies in this 1893 sample of 104 firms would still be major national advertisers 20 years later — American Tobacco Company, Armour, Cudahy Packing, P. Lorillard, Procter & Gamble, Quaker Oats, and Remington Typewriters.)

By contrast, if their products were to survive and be successful, consumer goods companies needed to build a bond of trust with their customers by using advertising to establish the quality and reliability of their brands, especially when it came to products that many consumers had previously made for themselves (see Figure 6).

Another important factor supporting the emergence of consumer brands was the development of new retail institutions, such as department and variety stores and national mail-order houses. These retail outlets facilitated the introduction of branded products to large numbers of potential customers. Some of these retailers became brands in their own right. So, for example, Marshall Field’s Chicago department store was renowned for its high-quality products, as well as the superior customer service that his staff was known to offer.

Then, too, changes in U.S. trademark law made it easier to protect trademarks, which were key to brand identity. One business writer7 describes the evolution of U.S. trademark law as follows:

As the use of brand names and trademarks spread, so did the practice of imitation and counterfeiting. Although the laws were somewhat unclear, more and more firms sought protection by sending their trademarks and labels to district courts for registration. Congress finally separated the registration of trademarks and labels in 1870 with the enactment of the country’s first federal trademark law. Under the law, registrants were required to send a facsimile of their mark with a description of the type of goods on which it was to be used to the Patent Office in Washington along with a $25 fee.

6 Daniel Pope, The Making of Modern Advertising (New York: Basic Books, 1983). 7 Kevin Lane Keller, Strategic Brand Management (New Jersey: Prentice Hall, 2002).

The emergence of consumer brands was

supported by the development of

department stores.

In 1870, the country’s first federal trademark

law was enacted.

Brand Behemoths – March 31, 2006

14

Figure 6. Brand building: Quaker Oats, Heinz, Pillsbury’s

Quaker Oats, 1896: “Pure”

Heinz, 1902: “Cleanliness is the first consideration…”

Pillsbury’s, 1908: “When best quality and most delicious taste is a consideration”

Sources: Quaker Oats: Reprinted permission of The Quaker Oats Company; Heinz: H.J. Heinz Company, L.P., owner of the copyright to the advertisement (used with permission); Pillsbury’s: Courtesy of The J.M. Smucker Company

Brand Behemoths – March 31, 2006

15

Professional Brand Management In this first stage of brand development — which lasted from about 1870 until the early 1900s — it was, in many instances, determined firm owner-entrepreneurs who created nationally branded consumer products.

➤ Asa G. Candler, owner and chief executive from 1891 to 1916, made Coca-Cola a powerful national brand by focusing on building national distribution.

➤ King C. Gillette became obsessed with his idea of a disposable blade and, after much effort, finally succeeded in developing one.

➤ H.J. Heinz dedicated much of his time to the production advances and promotions that built up the Heinz brand name.

➤ Harley Procter, one of the founders of Procter & Gamble, named the firm’s white soap “ivory” after hearing a sermon based on the 45th Psalm: “All thy garments smell of myrrh, and aloes, and cassia, out of ivory palaces.”

In the second stage of brand development, which extended from about 1915 to 1929, the market leadership of certain brands in various categories was firmly established by specialized managers. To be sure, this was a golden age for brand owners: Consumers, grateful for the improved quality that brands offered, and more heavily influenced by advertising than consumers before — due to large marketing expenditures (see Figure 7) — gladly purchased branded products.

Figure 7. 20 Largest Advertisers in National Magazines in 1915

Rank Rank 1 Quaker Oats Co. 11 R.J. Reynolds Tobacco Co.

2 Willys-Overland Co. 12 Colgate & Co.

3 Procter & Gamble Co. 13 Cream of Wheat Co.

4 American Tobacco Co. 14 Postum Cereal Co.

5 Victor Talking Machine Co. 15 Maxwell-Chalmers Motor Car Co.

6 Liggett & Myers Tobacco Co. 16 Kellogg Toasted Corn Flake Co.

7 Goodyear Tire & Rubber Co. 17 Hudson Motor Car Co.

8 Eastman Kodak Co. 18 Studebaker Corp.

9 Joseph Campbell Co. 19 U.S. Rubber Co.

10 Cudahy Packing Co. (Old Dutch Cleanser) 20 Columbia Graphophone Co.

Source: Daniel Pope, The Making of Modern Advertising (New York: Basic Books, 1983)

Business historian Alfred Chandler writes that, by 1914, firms that employed “a hierarchy of middle and top salaried managers to monitor and coordinate the work of the [multiple] units…had become the dominant business institution in many sectors of the American economy.”8 These sectors included those in which brand development had flourished — canned foods, soap, and tobacco.

8 Alfred D. Chandler Jr., The Visible Hand: The Managerial Revolution in American Business, (Cambridge, MA: Harvard University Press, 1977).

In this first stage, firm owner-entrepreneurs

created nationally branded consumer

products.

In the second stage of brand development,

market leadership was firmly established by

specialized managers.

Brand Behemoths – March 31, 2006

16

The managers who managed such enterprises “form[ed] an entirely new class of businessmen” (in the words of Alfred Chandler). As the old visionary entrepreneurs retired, died off, or simply could not shoulder the increasingly technical and complex burdens of decision making, specialized professional managers assumed the responsibility for brand management.

Moreover, the belief that advertising agencies possessed key insights into demand creation for brands led executives to look to agencies for assistance on a wide range of activities, including market research, product testing, package development, consumer sales promotions, and creating advertisements. The intuitive and commonsense approaches that had previously characterized marketing functions gave way to systematic and knowledge-based approaches that promised more effective brand management.

The preeminence that brands achieved in consumers’ minds as a result of this more systematic approach to brand management was demonstrated by a research study in the early 1920s of “100 typical” consumer product categories. The respondents were 512 male and 512 female students from a sample of “15 representative universities” across the United States. The research was based on respondents’ unaided recall of brand names in the 100 product categories.

Figure 8 lists the 28 product categories for which more than 85% of the respondents recalled at least one brand. These categories ranged from inexpensive, simple items, such as chewing gum and canned milk, to costly products such as automobiles and sewing machines. Significantly, all of these categories were advertised heavily, usually for 20 years or more. A key conclusion of the authors of the study:

In the great majority of fields…practically every one discriminates between brands in making a purchase. The tendency to do so is far more common today than it was a few years ago [italics added]. In many lines it has come to be regarded as the simplest and surest way to obtain standard quality and service.9

9 George B. Hotchkiss and Richard B. Franken, The Leadership of Advertised Brands, (New York: Doubleday, 1923).

As the old visionary entrepreneurs retired,

specialized professional managers assumed

responsibility for brand management.

Intuitive and commonsense

approaches gave way to systematic and

knowledge-based approaches.

Brand Behemoths – March 31, 2006

17

Figure 8. Product Categories with a High Degree of Brand Familiarity in 1923 category and best known brand in category

Category

Familiarity With Brands in Category (% of Respondents) Best Known Brand(s)*

Chewing Gum 96.0% Wrigley

Automobiles 95.3 Ford

Soap 95.1 Ivory

Baked Beans 93.6 Heinz

Watches 92.6 Elgin, Waltham

Soup 92.4 Campbell

Toothpaste 92.2 Colgate

Sewing Machines 92.1 Singer

Pens 91.8 Waterman

Phonographs 91.7 Victor (RCA), Edison

Breakfast Food 91.3 Kellogg’s Corn Flakes

Cameras 90.7 (Eastman) Kodak

Cleanser 90.5 Old Dutch

Flour 90.4 Gold Medal

Bacon 89.8 Swift Premium, Beech-Nut

Chocolates 89.8 Hershey’s

Crackers 89.7 National Biscuit Co.

Cocoa 89.5 Baker’s

Toilet Soap 89.4 Palm Olive

Talcum Powder 89.0 Mennen, Colgate

Candy 88.7 Huyler’s

Cigarettes 88.3 Camel, Fatima

Typewriters 88.0 Underwood, Remington

Tires 87.4 Goodyear

Coffee 86.8 Yuban

Shoes 86.6 Douglas

Canned Milk 86.5 Borden, Carnation

Laundry Soap 85.9 Fels Naptha

*Brands in boldface were mentioned by more than twice as many respondents as other brands in their categories. Italicized brands had only weak leadership. Where two brands are mentioned, both were close in familiarity but led all others.

Source: George B. Hotchkiss and Richard B. Franken, The Leadership of Advertised Brands, (New York: Doubleday, 1923).

Brand Behemoths – March 31, 2006

18

Postwar Market Segmentation The sharp drop in incomes during the Great Depression, and the rationing introduced during World War II, curbed consumer demand for all goods, including branded products. Reflecting this unfavorable demand environment, advertising volumes peaked in 1929, fell sharply thereafter, and did not regain the 1929 peak until 1947 (see Figure 9).

Figure 9. Volume of Advertising per Capita

$0

$10

$20

$30

$40

1860 1870 1880 1890 1900 1910 1920 1 9 3 0 1 9 4 0 1950

Source: Historical Statistics of the United States

The economic boom that followed the end of World War II fueled increases in personal income, the birth rate, and the growth of the suburban middle class. These demand trends were immensely positive for brands.

On the supply side, continuing the prewar trend, branding spread to more categories, including women’s apparel and home furnishings. In addition, an explosion of new consumer products, following the raw material shortages and rationing during World War II, as well as the impact of television, further increased the importance of brands.

Then too, as post war shortages eased, manufacturers were able to take advantage of the latest advances in manufacturing technologies, which permitted more diverse output. Techniques for altering the mix of raw materials became more widespread, as did means of packaging and labeling different product sizes and assortments. In addition, automatic control machinery could rapidly change the mix of products a plant turned out without greatly increasing costs.

The focus of consumer marketing in this next phase of branding became market segmentation (as opposed to the unification of the market by a dominant brand). Marketers used considerations such as demographics (age, income, and education) and psychographics (lifestyle) to create divisions in markets that they could exploit.

The economic boom that followed the end of

World War II was immensely positive for

brands.

New techniques for altering the raw materials

mix, and new means of packaging and labeling different product sizes

and assortments, became more

widespread.

Marketers used demographics and psychographics to create divisions in

markets.

Brand Behemoths – March 31, 2006

19

These segments had to be sufficiently large so that scale economies could be obtained. The goal, however, was not only to achieve scale economies, but also to gain the freedom to price in accord with the special value that a particular market segment placed on the product.

To be sure, market segmentation was not entirely a post–World War II concept, although, for the reasons outlined above, its practice exploded in the postwar years. In 1920, Alfred P. Sloan recognized the profit potential in marketing variations and features that could be added onto the basic vehicle manufactured by General Motors. Sloan decided that General Motors should:

[first], produce a line of cars in each price area from the lowest price up…; second, that the price steps should not be such as to leave wide gaps in the line, and yet should be great enough to keep their number within reason…; and third, that there should be no duplication by the corporation in the price fields or steps.10

Five brand names would each focus on a different segment with a distinct product offering, with Chevrolet at the bottom (offering lower-priced quality cars), and Cadillac at the top (being the standard of luxury). Chevrolet was intended to compete directly against the stripped-down basic transportation of Ford’s Model T. As a result of this market segmentation strategy, General Motors’ sales rose quickly in the 1920s, while Henry Ford continued to insist that the customer could have a car in any color he wanted as long as it was black.

As noted above, it was in the postwar years that market segmentation became widely embraced. Procter & Gamble became an adept practitioner of the strategy (see Figure 10), which goes a long way toward explaining how the company today holds a 50%-plus share of the mature laundry detergent category in the U.S.

Figure 10. Market Segmentation in Laundry Detergent ten Procter & Gamble brands have targeted different market segments

Ivory Snow “Mild, gentle soap for diapers and baby clothes”

Tide For extra-tough family laundry jobs

Cheer Works in cold, warm, or hot water

Gain Originally an “enzyme” detergent but now a detergent with a fragrance

Bold Includes fabric softener

Dash Concentrated power, less suds to avoid clogging washing machines

Dreft With “Borax, nature’s natural sweetener” for baby’s clothes

Oxydol Contains bleach — for “Sparkling whites — with color-safe bleach”

Era Concentrated liquid detergent — with proteins to clean stains

Solo Heavy-duty, with a fabric softener

Source: David A. Aaker, Managing Brand Equity (New York: The Free Press, 1991)

10 Alfred P. Sloan, Jr., My Years with General Motors (New York: Macfadden-Bartell, 1965).

In 1920, GM’s Alfred P. Sloan recognized the

profit potential in marketing variations and

features.

It was in the postwar years that market

segmentation became widely embraced.

Brand Behemoths – March 31, 2006

20

In the soft drinks sector, while Coca-Cola was slow to embrace market segmentation, Pepsi-Cola was not. Until 1955, Coca-Cola was available in only two forms — at the soda fountain and in the traditional 6.5-ounce, hobble-skirted bottle. In the words of one business historian, “Coke was, the company believed, perfect for everyone. There was no need to devote special attention to one group or another.” 11 (In addition, as recently as 2003, one financial analyst wrote, “Coca-Cola has tended to focus on one Global marketing message at a time rather than targeting consumers based on geographic or demographic differences.”12)

By contrast, Pepsi’s advertisements in the 1950s did not tout the product as much as they did the context in which the product was consumed: “Be sociable, look smart. Keep up to date with Pepsi” rang one jingle from the 1950s. This strategy was refined with the inauguration of the “Pepsi Generation” in the 1960s, which targeted the postwar baby boomers, then in their teenage years (see Figure 11). So, unlike Coke, Pepsi was about variety and change. (Note that market segmentation was greatly facilitated by the advent of television — it is hard to imagine the Pepsi Generation without television advertising.)

Figure 11. “Come Alive! You’re in the Pepsi Generation!”

Source: PEPSI and PEPSI-COLA are registered trademarks of PepsiCo, Inc. Used with permission.

11 Richard Tedlow, New and Improved: The Story of Mass Marketing in America (New York: Basic Books, 1990). 12 See Bonnie Herzog’s March 6, 2003, report, “The Coca-Cola Company.”

While Coca-Cola was slow to embrace market

segmentation, Pepsi-Cola was not.

Market segmentation was greatly facilitated by the advent of television.

Brand Behemoths – March 31, 2006

21

Figure 12. A Branding Timeline notable dates in the development of branding

0 A.D. Trademarks on Roman pottery.

900 Brand-marked metal tools in China.

1266 English law requires bakers to put their mark on every loaf of bread.

1597 Two English goldsmiths nailed to pillory by their ears for marking their wares falsely.

1665 Mark of ownership impressed on cattle by branding in American colonies.

1700 Technological advances facilitate the inexpensive printing of handbills and posters.

1722 Unique symbol used to distinguish Meissen porcelain from other manufacturers.

1770 Josiah Wedgwood begins to brand his china.

1850 The “Moon and Stars” begins to appear as the unofficial trademark of Procter & Gamble.

1870 First U.S. trademark law.

1870–1900 Nationally branded consumer products established in U.S. by firm owner-entrepreneurs.

1880-1890 Continuous process machinery invented.

1890–1900 Advances in packaging. Development of high-speed lithographic presses.

1893 Advertising in U.S. still dominated by ads for patent medicines.

1915–1928 Explosion of brands thanks to professional brand management.

1920 Alfred P. Sloan develops market segmentation by General Motors.

1929 Great Depression begins. Advertising spending collapses.

1939-1945 Many brands become relatively scarce during World War II.

1945- Post war explosion of brands driven, in part, by market segmentation.

Source: Citigroup Investment Research

Brand Behemoths – March 31, 2006

22

Behind Branding To review, key factors behind the evolution of brands through the ages (see Figure 12) include:

➤ Quality assurance. A mark (or brand) on products, ranging from casks of wine to metals, which came to indicate specific standards and genuineness.

➤ Mass-market products. In the late 19th century, continuous process machinery was invented almost simultaneously for making cigarettes, matches, flour, breakfast cereals, soups and other canned products, and photographic film.

➤ A sprawling distribution network. The continental railroad system facilitated the development of a mass consumer market in the U.S.

➤ A close relationship with a retail system. Department and variety stores and national mail-order houses aided in the introduction of branded products to large numbers of potential customers.

➤ A judicious use of advertising. In the 19th century, consumer goods companies needed to build a bond of trust with their customers, especially when it came to products that many consumers had previously made for themselves.

➤ Careful protection of brand identity. As the use of brand names and trademarks spread, so did the practice of imitation and counterfeiting; changes in U.S. trademark law made it easier to protect trademarks.

➤ Innovation. King C. Gillette became obsessed with his idea of a disposable blade and, after much effort, finally succeeded in developing one.

➤ Management focus. In the second stage of brand development, which occurred during the first decades of the 20th century, the intuitive and commonsense approaches that previously had characterized marketing functions gave way to systematic and knowledge-based approaches.

➤ Market segmentation. In the post–World War II years, marketers used considerations such as demographics and psychographics to create divisions in markets that they could exploit with competitive advantages.

➤ An aspirational element surrounding certain brands. As Josiah Wedgwood implicitly acknowledged, the demand for his china was driven by factors other than its “utility.”

The Importance of Intangibles By the late 20th century, what often determined the value of a brand was not so much the tangible factors outlined above — many of which were easily replicated (e.g., mass market products, advertising, etc) — as it was intangible factors such as quality, brand identity, innovation, and aspirations.

By the late 20th century, the value of a brand was not so much in tangible

factors, as it was in intangibles.

Brand Behemoths – March 31, 2006

23

Quality In 1989, Perrier dominated the market for bottled water, with almost a 50% share. Indeed, so strong was the brand power that, for many consumers, “Perrier” was synonymous with “bottled water.” However, in 1990, Perrier recalled its product worldwide after it was found to be contaminated by traces of benzene, a suspected carcinogen.

When the supply of Perrier was interrupted, consumers had to sample other brands, which they found were as good as or better than Perrier. Although Perrier rebounded from this fiasco, it never regained its previous market preeminence. (The Perrier brand is currently owned by Nestlé, but it is estimated that it accounts for just 6% of Nestlé’s total global water sales. So, for example, in the U.S. water market, where Nestlé is the leader by a wide margin, Poland Spring is a key brand.)

Schlitz suffered a much worse fate than Perrier. In 1976, Schlitz was the No. 2 premium beer brand in the U.S., with 16.1% of the market, as compared to 19.5% for Anheuser-Busch and 12.2% for Miller. In 1977, the Schlitz firm lost the No. 2 position to Miller, and by 1986 the brand had all but disappeared. (Today, Miller is still the No. 2 brand, behind Anheuser-Busch).

The simple reason behind the downfall of Schlitz was the decision by management in 1974 to reduce costs by changing the beer production method, and by substituting corn syrup for barley malt. Although the company’s belief was that the average beer drinker could not tell the difference between the taste of the new, cheaper beer and the original beer, the new beer did have a lighter taste and sales fell. The Joseph Schlitz Brewing Company limped along until 1982 when it was acquired by Stroh.

Brand Identity An inadequate commitment to a brand’s identity can take the form of either a muddled advertising strategy or a muddled corporate strategy. The example of Smirnoff below illustrates the first situation, while the example of IBM’s PCs illustrates the second.

Although it had been the leading brand for several decades, Smirnoff’s share of the U.S. vodka category peaked at 22% in 1974 and declined steadily thereafter, losing share to competitors such as Absolut and Stolichnaya. A key factor behind its market share loss was that Smirnoff’s advertising was not consistent over time, with 14 different advertising campaigns between 1953 and 1994 (and at least ten since 1978), each with different themes and visual imagery: The “self-expression” campaign was a reaction to the cultural changes of the Vietnam and Woodstock era; the “quality/value” theme was in direct response to a recession, and the “reigning vodka” theme attempted to defend the upscale position threatened by Absolut. As marketing professor David A. Aaker writes:

Because of the endless changes…it was usually unclear what Smirnoff stood for. The Smirnoff identity was muddled in terms of its personality, its visual image, its value proposition, and the basis of its relationship with the customer.13

13 David A. Aaker, Building Strong Brands (New York: The Free Press, 1996).

In February 1990, Perrier recalled its product

worldwide after it was found to be

contaminated.

The simple reason behind the downfall of

Schlitz was substituting corn syrup for barley

malt.

Smirnoff’s advertising was not consistent over

time, with 14 different advertising campaigns

between 1953 and 1994.

Brand Behemoths – March 31, 2006

24

With regard to a muddled corporate strategy, Apple was the dominant firm in the personal computer (PC) market in the late 1970s. When IBM entered the market, it quickly surpassed Apple, thanks to IBM’s brand name, which, at the time, represented quality, leading-edge products supported by outstanding service. However, as the PC grew in popularity, IBM felt that it threatened its core mainframe computer franchise. So the firm was not as willing as others to promote the growth of PCs, and it eventually lost its market leadership position to competitors, the most notable of which, in recent years, has been Dell.

Innovation In the 1980s, CompuServe and Prodigy lost their leadership positions in the online community sector to America Online, which offered something new and improved. Before AOL’s entry, CompuServe and Prodigy were leading brands catering to a niche market of sophisticated users; so, for example, CompuServe provided valuable financial information for investors, although in a hard-to-use format.

At the same time that its competitors cultivated niche markets, AOL worked to create a mass market of users by emphasizing community, a simple interface, and easy installation. As we now know, AOL was ultimately so successful that it acquired CompuServe, and pushed Prodigy into insignificance.

Aspirations Weight Watchers (then owned by Heinz) was one of the great brand success stories of the 1980s. Heinz had acquired Weight Watchers in the late 1970s in an effort to capitalize on a heightened concern with health and fitness by obtaining a brand with a strong association with professional weight control. This turned out to be a good investment, as the health and fitness trend was one of the growth areas of the 1980s.

In the late 1980s, however, consumer interest in weight control was eclipsed by a broader concern about a healthy diet. Many processed foods were high in fat and sodium, which have been linked to heart disease. Along came Healthy Choice (from ConAgra), a brand designed to address this new market opportunity. The brand’s objective was to minimize fat and control the level of other undesirable components, such as cholesterol and sodium, while simultaneously offering tasty products.

Purchasers of Weight Watchers products, which were positioned more as weight control brands, represented the target market of Healthy Choice because many of the consumers interested in weight control were the same individuals that were concerned about overall health. So, reflecting these new health concerns, Healthy Choice was one of the most successful new brands in the 1990s, although it did not entirely displace Weight Watchers.

Similarly, in the mid-1980s, increasingly health-conscious customers associated Kentucky Fried Chicken with high fat and cholesterol content, and began to patronize restaurants offering healthier alternatives, such as Boston Market.

IBM felt that PCs threatened its core

mainframe computer franchise, and so it

eventually lost its market leadership position in

PCs to competitors.

AOL worked to create a mass market of users by emphasizing community,

a simple interface, and easy installation.

In the late 1980s, consumer interest in

weight control was eclipsed by a broader

concern about a healthy diet.

Brand Behemoths – March 31, 2006

25

It’s Not Enough Just to Be First Not surprisingly then, brand leadership is not stable over time. Figure 8 illustrated perceived brand leaders in 1923. While many of the brand names are still familiar today, a detailed study showed that, by 1997, more of the leading brands in 1923 had failed (28%) than had remained leaders (23%) — see Figure 13.

Figure 13. Long-Term Success Rate of 1923 Market Leaders market rank in 1997

23%

8%9%

8%7%

1 6 %

28%

0%

10%

20%

30%

N u m b e r 1 N u m b e r 2 N u m b e r 3 Top 5 T o p 1 0 B e l o w 1 0 Fa i l ed

Source: Peter N. Golder, “Historical Method in Marketing Research with New Evidence on Long-Term Market Share Stability,” Journal of Marketing Research, May 2000

These data are a sharp refutation of the aforementioned “first immutable law of marketing” — that “it’s better to be first, than it is to be better.” According to this thesis, a firm’s probability of surviving and its share of market are in proportion to the order in which it enters a market. The firm that first enters a market is believed to have enormous advantages in terms of long-term market leadership.

However, Professor Golder believes that it’s not that simple. In his book Will and Vision: How Latecomers Grow to Dominate Markets14 (co-authored with Gerard J. Tellis), he argues that:

Market pioneers rarely endure as leaders. Most of them have low market share or fail completely. Actually, market pioneering is neither necessary nor sufficient for enduring success. The real causes of enduring market leadership are vision and will. Enduring market leaders have a revolutionary and inspiring vision of the mass market, and they exhibit an indomitable will to realize that vision. They persist under adversity, innovate relentlessly, commit financial resources, and leverage assets to realize their vision.

Although Professor Golder’s book is focused on the subject of “how latecomers grow to dominate markets,” in our view, the characteristics he outlines above apply just as well to what we label “brand behemoths” who may be latecomers to, or pioneers in, various categories and regions:

They persist under adversity, innovate relentlessly, commit financial resources, and leverage assets to realize their vision.

14 Gerard J. Tellis & Peter N. Golder, Will and Vision: How Latecomers Grow to Dominate Markets (New York: McGraw-Hill, 2002).

By 1997, more of the leading brands in 1923

had failed (28%) than had remained leaders (23%).

These data provide a sharp refutation of the “first immutable law of marketing” — that “it’s

better to be first, than it is to be better.”

“Market pioneers rarely endure as

leaders…market pioneering is neither

necessary nor sufficient for enduring success.”

Brand Behemoths – March 31, 2006

26

A Unique Database As noted, we define a “brand behemoth” as a company that can leverage a leadership position in one category or region and extend that franchise into new markets. In our search for brand behemoths, we could, of course, have taken a subjective approach. Instead, we chose to be more rigorous, and so, working with Professors Golder and Steckel, we constructed a unique database.

Current academic research on brand leadership tends to be based on U.S. data only, with little known about brand leadership on a global basis. However, Euromonitor International’s Integrated Market Information System (IMIS) offers market shares across many categories and countries. The traditional use of these data is for brand managers to perform analysis within their own individual categories. We are not aware of any publicly available study that, until now, has used similar data to understand brand leadership on a global basis.

Utilizing this database, we gathered global market share data for 30 consumer nondurable product categories — see Figure 14. (Note here that, in the opinion of Citigroup Investment Research analysts, given that we only focus on 30 categories and exclude others, our analysis may underestimate the extent to which some companies truly are brand behemoths.)

Figure 14. 30 Consumer Nondurable Product Categories

Food, Beverages, and Tobacco Household Products

Baby Food Functional Drinks Bath & Shower

Beer Gum Color Cosmetics

Biscuits Ice Cream Deodorant

Bottled Water Ready Meals Diapers

Breakfast Cereals Sauces & Dressings Facial Tissues

Carbonates Soups Hair Care

Chocolate Confectionery Spirits Laundry Care

Cigarettes Sweet & Savory Snacks Oral Hygiene

Coffee Tea Surface Care

Fast Food Yogurt

Fruit/Vegetable Juice

Source: Citigroup Investment Research

We aggregated 2004 market share data by company based on over 3,500 brands that compete in the 30 product categories. We then sorted the data into eight regions/countries: China, East Asia, Eastern Europe, India, Japan, Latin and South America, the U.S., and Western Europe. (Note that, for the regions, we simply focused on those countries that, combined, account for 75%-plus of a region’s GDP. So, for example, “Western Europe” represents market share data for Germany, the U.K., France, Italy, and Spain.)

Identifying Brand Behemoths

The traditional use of these data is for brand

managers to perform analysis within their own

individual categories.

We aggregated 2004 market share data by

company based on over 3,500 brands that compete in the 30

product categories.

Brand Behemoths – March 31, 2006

27

Given that we examined 30 product categories in eight regions, there are 240 category/region combinations for companies to compete in. We then asked Professors Golder and Steckel to forecast the market leaders in 2010 for the 240 category/region combinations. Their methodology is discussed in detail in Appendix B. As explained in that appendix, the 2010 market share forecasts are based on four primary factors (as well as many ancillary factors):

1 A company’s current market share, as well as its market share advantage over the No. 2 and No. 3 companies. (The larger a company’s market share advantage over its nearest competitors, the more likely it is to continue its lead.)

2 A company’s global and regional market shares. (A company that is strong globally or locally can leverage its knowledge into other markets.)

3 A company’s leadership position in more than one category. (This enables companies to, for example, leverage their distribution systems.)

4 A company’s market share stability (or lack thereof) over time.

The forecasts of the market leaders in the 240 category/region combinations in 2010 are contained in Appendix C. Figure 15 lists companies that are forecast to have at least four leadership positions in 2010.15

Figure 15. 2010 Brand Leaders: Total Number of No. 1 Positions in 240 Category/Region Combinations companies with at least four projected No. 1 market share rankings

Unilever 38 Kellogg 6

Nestlé 17 Colgate-Palmolive 5

Procter & Gamble 14 Kraft Foods Inc. 5

Coca-Cola 11 Lotte Group 5

PepsiCo 10 McDonald’s 5

Danone 9 L’Oréal 4

Kimberly-Clark 9 Wrigley 4

Source: Professors Peter N. Golder and Joel H. Steckel and Citigroup Investment Research

Brand Leaders and Brand Behemoths The 14 brand leaders listed in Figure 15 have competed in various markets for decades, have successful brands, and have enjoyed No. 1 market positions for some time. So, all of them are potential brand behemoths. However, in the opinion of Citigroup Investment Research analysts, only ten of these companies have the skill set necessary to be classified as a brand behemoth.16

15 Note that these forecasts do not include any assumptions about mergers and acquisitions that could lead to a material change in rankings. M&A has been a part of some companies’ expansion strategies in the past, and could well occur again in the future. 16 The four brand leaders that we do not make a case for as brand behemoths are Coca-Cola, Kraft Foods, Lotte Group, and McDonald’s. Citigroup Investment Research does not follow Lotte Group or McDonald’s. With regard to Coca-Cola (2M), the company already has a dominant position in carbonated soft drinks — and is the leader in that mature category in all eight regions we studied — but, in the opinion of Citigroup Investment Research analyst Bonnie Herzog, it has not experienced much success in extending its brand name across other categories. In addition, while Kraft Foods (2M) has an interesting portfolio of brands, questions remain in the mind of Citigroup Investment Research analyst David Driscoll about the company’s marketing commitment to those brands, especially in light of cuts to its advertising budget in recent years.

We forecast the market leaders in the 240

category/region combinations in 2010.

Brand Behemoths – March 31, 2006

28

Importantly, a key implication of Figure 15 is that brand behemoths are far from mature. The ten companies are projected to have the No. 1 position in less than half (48%) of the 240 category/region combinations by 2010 (see Figure 16).

Figure 16. Number of Projected No. 1 Positions Held by Ten Brand Behemoths in 240 Categories/Regions for 2010

Unilever

Nestle

Procter & Gamble

PepsiCo

Danone

Kimberly-Clark

Kellogg

Colgate-Palmolive

L'Oreal

Other(124 positions held by

88 companies)

Wrigley

Source: Professors Peter N. Golder and Joel H. Steckel and Citigroup Investment Research

To be sure, the dominance of brand behemoths has been growing over time, and it is forecast to continue to increase. As Figure 17 illustrates, the ten brand behemoths had the No. 1 position in more than 46% of the 240 category/region combinations in 2001 and in 47% of the category/region combinations in 2004, and that number is forecast to rise to 48% in 2010.

Figure 17. Percent of No. 1 Positions Held by Ten Brand Behemoths in 240 Categories/Regions cumulative number held by Unilever, Nestlé, Procter & Gamble, PepsiCo, Danone, Kimberly-Clark, Kellogg, Colgate-Palmolive, L’Oréal, and Wrigley

46.7%

47.1%

48.3%

45%

50%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010e

Source: Citigroup Investment Research, Euromonitor International, and Professors Peter N. Golder and Joel H. Steckel