Vidicode uk providing choice, clarity and expert consultation

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

To: [email protected] 23 August 2016

Introduction

1. The BPF represents the commercial real estate sector – an industry with a market value of £1,662bn, which contributed more than £94bn to the economy in 2014. We promote the interests of those with a stake in the UK built environment, and our membership comprises a broad range of owners, managers and developers of real estate as well as those who support them. Their investments help drive the UK's economic success, provide essential infrastructure, and create great places where people can live, work and relax.

2. The UK’s Commercial Real Estate sector contributes about 5.4% of GDP, and directly employs 2.1 million people, or 6.8% of the labour force. It provides the nation’s built environment and is spreading out from its core investment in the nation’s offices, shops, leisure facilities and factories, to support the new economy through investments in logistics, healthcare, student accommodation, infrastructure, and increasingly through Build-to-Rent investment in new housing.

3. The sector is one of the most successful in the world at attracting domestic and overseas long-term investment capital into the renewal of the UK’s towns and cities. Such large, long-term, patient investors are critical to the urban redevelopment and regeneration of our country, which the vote on Brexit has illustrated, is so important if we are to feel we are all part of one nation.

4. Post-Brexit business uncertainty is having a predicted squeeze on activity, with reduced investment and stalled decision-making. The drop off in demand for business space is seeing projects mothballed, which means less construction activity and future job creation, itself feeding back into less consumer demand.

5. Changes to the UK’s long-established loss relief rules were announced by the government at the Budget in March 2016, before this uncertainty took hold. These changes were not however expected by business, and their timing - taking effect at the same time as the new interest restrictions - means that businesses will face significant practical challenges (and costs) in being ready for the new rules on 1 April 2017. This is both operationally (in terms of compliance) but even more importantly in terms of having identified the consequences of these two significant reforms on the business - at a time when there is much general economic uncertainty in any event.

6. Although overall we welcome the willingness of the government to seek to modernise loss relief through increased flexibility, we are unconvinced that these proposals are the best way to do this.

7. The current loss rules recognise that within any tax system, there is the potential for a mismatch between the commercial/economic and tax profitability of a company - linked in part to fact that tax systems measure profits within specific reporting periods (in the UK, 12 month accounting periods).

8. Whilst the new proposals accept that relief should be given in full for losses, their impact is such that many businesses will find their tax bills - and their tax compliance bills - increasing significantly over the medium term at least (with the policy costings showing £1.3bn in expected additional revenues from this measure by 2020/2021).

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

9. Our concern is that many of these businesses are not the target of these reforms - they are not “companies making substantial UK profits [that] can end up not paying corporation tax for many years due to losses incurred from historic events and activities” as per Objective 2. However, they will still be caught by the changes. Even if over the longer term, the increased flexibility offsets some of the cost resulting from loss restriction, many businesses will struggle to quantify any benefit from this.

10. We therefore welcome the opportunity to respond to the Consultation on reforms to corporation tax loss relief (the Consultation). If you would like to discuss any aspect of our response in more detail, please get in touch..

11. Our response is structured as follows:

Part I: Summary of real estate concerns and key recommendations Part II: Responses to consultation questions Appendices: 1. Comparison of loss restriction regimes in G7 and selected OECD countries 2. The 3 Step Process: simple and effective? 3. Property Development Activities

a. “Develop to sell” b. “Develop to hold” c. Joint ventures

4. REITs Rachel Kelly Senior Policy Officer (Finance) British Property Federation St Albans House 57-59 Haymarket London SW1Y 4QX

020 7802 0115 [email protected]

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

Part I: Summary of real estate concerns and key recommendations

Complexity 12. The Consultation presents the loss reform proposals as being in line with the government’s objective to

simplify and modernise the tax system. But, reading through detail of the Consultation, this seems to be far from the case.

13. First, the reforms fall short of a true modernisation of the loss relief rules. The existing rules are broadly untouched, given the maintenance of the schedular system. Although additional flexibility is being provided for, it comes at a cost: the use of “own” carry forward losses, including those that arose before the reforms were announced, is being restricted significantly. The cessation rules are being left untouched - even though the effect of the reforms could be that some businesses (like property developers) find material differences between their economic and taxable profits over a business cycle.

14. Secondly, although the logic behind the 3-step process is simple enough (i.e. replicating on a carry forward basis the same relief against total profits as is available on a current year basis), the means by which this is achieved in incredibly complex. Again, this derives from the decision to maintain “streaming” of losses at all stages in the 3-step process - which means that, in practice, those businesses affected by the reforms will face a heavy compliance burden when trying to work out how they apply across a group.

15. It is disappointing that the government did not take the opportunity afforded by this Consultation to reform not just the loss rules but also the UK’s schedular and group systems. This would provide stakeholders with a proper opportunity to work with the government to create a corporate tax system fit for the 21st century.

16. Instead, the changes have been already announced, with the Consultation limited to the detail of implementation. However, at the same time, the Office of Tax Simplification has been asked to review some of the broader issues affecting how corporation tax works in practice - and is due to report by Budget 2017. This review is clearly pertinent to the issues underlying some of the complexity within the current loss reform proposals.

17. We therefore consider that the government should delay the implementation of the loss reform proposals until 1 April 2018. Rather than rush into unnecessarily complex reforms, we ask government to use the period until the Office of Tax Simplification reports to consult widely with stakeholders on creating a loss relief regime that is simple, comparable with that of other G7 countries and meets the government’s objectives. For further discussion of issues arising from the complexity of the proposals, see Appendix 2.

Cost to business of restricting losses 18. Although the Consultation focuses on the flexibility that the proposals will offer business, there is also a cost

for businesses with carried forward losses above the proposed £5m allowance (whether individually or across a tax grouping). The policy costings estimate that cost at £1.36bn over the first four years.

19. Although imposing a cap on the use of carry forward losses is consistent with the position in other G7 jurisdictions, we are concerned that the level of cap chosen is particularly low. First, only one G7 country imposes a 50 per restriction. Secondly, other G7 jurisdictions allow group consolidation for tax purposes, providing a flexibility that the reforms are not able to fully replicate, given they are bolted onto a naturally

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

restrictive schedular system. Finally, for pre-1 April 2017 losses, the restriction is imposed without the corollary of any additional flexibility.

20. We appreciate that the amount of cap and the losses it applies to raise fiscal considerations for the government and that, in increasing access to losses through extending carry forward relief, the Exchequer needs to be sensitive both to short and long term costs of such measure. A balance has to be reached that is fair to business and fair to the general body of taxpayers.

21. However, we are concerned that the current proposals do not achieve the right balance. Based on HMRC’s statistics, it seems that just over 5 per cent of corporation tax payers will benefit from these proposals, with 1 per cent of companies bearing the cost. Of those 5 per cent who benefit, it seems the majority will benefit primarily through access to the £5m allowance.

22. We have no information as to the stock of losses within UK companies as at Budget 2016. However, we ask government to reconsider (at least) the exclusion of pre-2017 losses from the proposed flexibility: in addition to simplifying the rules, it would also be more equitable given that Objective 1 of the reforms is said to be “increased flexibility”.

23. For pre-2017 losses, there is no such flexibility, just restriction. Although prior to Budget 2016, companies would have had no expectation of additional flexibility, equally, a company that made a loss prior to that date would have had a reasonable expectation that it could carry that loss forward in full to offset future profits. Even though such losses will continue to be available for relief, it will be over a longer period - and that means the value of the relief available to a company for an economic loss already suffered is being diminished.

Developers - a special case: “new’ terminal loss relief 24. Fundamental to loss relief for tax purposes is the recognition that taxing profits, but not giving relief for

losses, may well provide a disincentive to pursue a particular activity. As the Institute of Fiscal Studies pointed out in its Briefing Note No. 30:

“It is an inherent feature of a tax system that collects tax on profits but does not provide full relief for losses (i.e. does not pay out an equivalent ‘negative tax’ on negative profits) that provision “needs to be made to allow unrelieved losses to be carried forward and offset against past or future profits if manifest inequity is to be avoided”1

25. Under the proposals, there is no general intention to prevent the indefinite carry forward of losses: the objective seems mainly to defer the period over which relief can be claimed (in effect, accelerating the taxation of profits within a loss-making group).

26. However, for certain businesses, such as property development the effect of the reforms could be to deny relief for losses that reflect the true economic cost of the profit-making activity. This is because of how the proposed restrictions interact with the cessation rules.

27. Commercially, a developer’s economic profit from its activities is the excess of sales proceeds over its costs. The nature of property development means that there will always be a timing mismatch between (a) when

1 Section 3.1, Institute of Fiscal Studies Briefing Note No 30 - Reform of Corporation Tax: A Response to the Government’s Consultation

Document [2002].

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

costs are incurred and (b) profits are earned. This timing gap can, on larger development projects, be several years. However, when the developer incurs those costs, it does so in the expectation that, when the development is complete, it will not only recover those costs but also make a profit from its activities.

28. It is therefore reasonable to expect that the tax system should also recognise the economics of such commercial activity and thus aim to tax a developer’s “real” profit, rather than (in effect) substitute an alternative amount as taxable profit that does not reflect the commercial reality. Within a development context, the (restricted) losses are not historic - the type of loss that Objective 2 is directed at restricting -but an intrinsic part of the activities that generate the relevant profit.

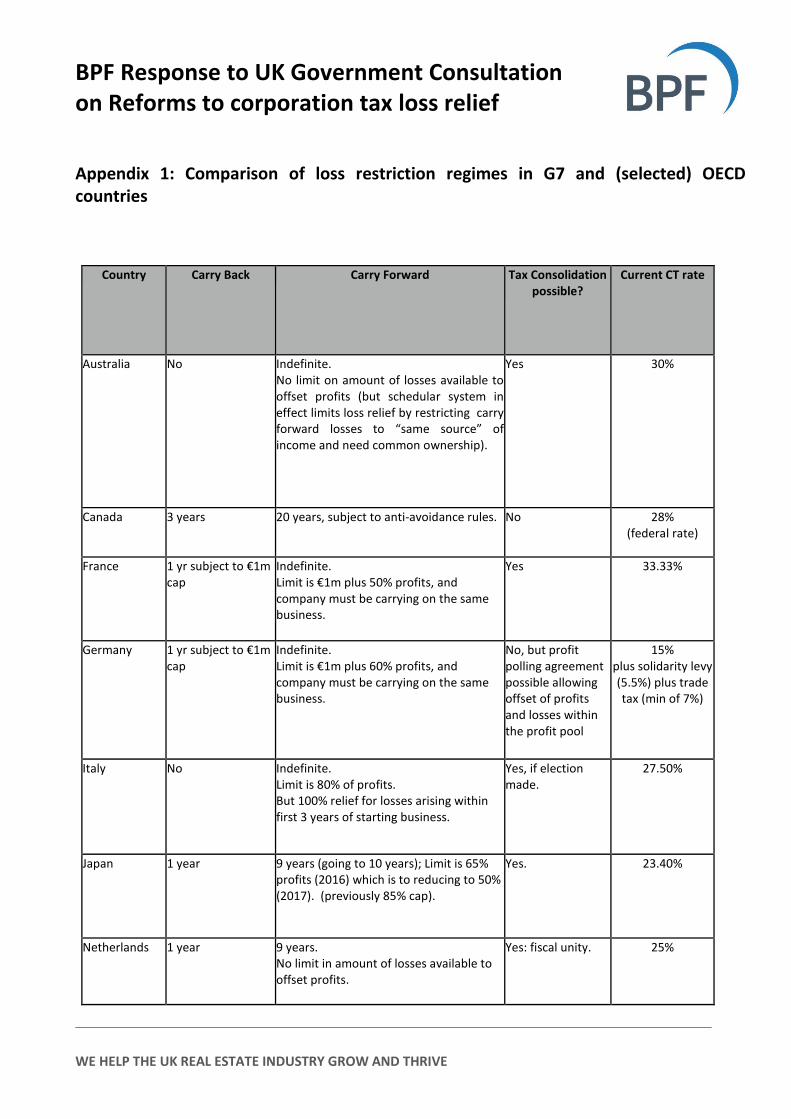

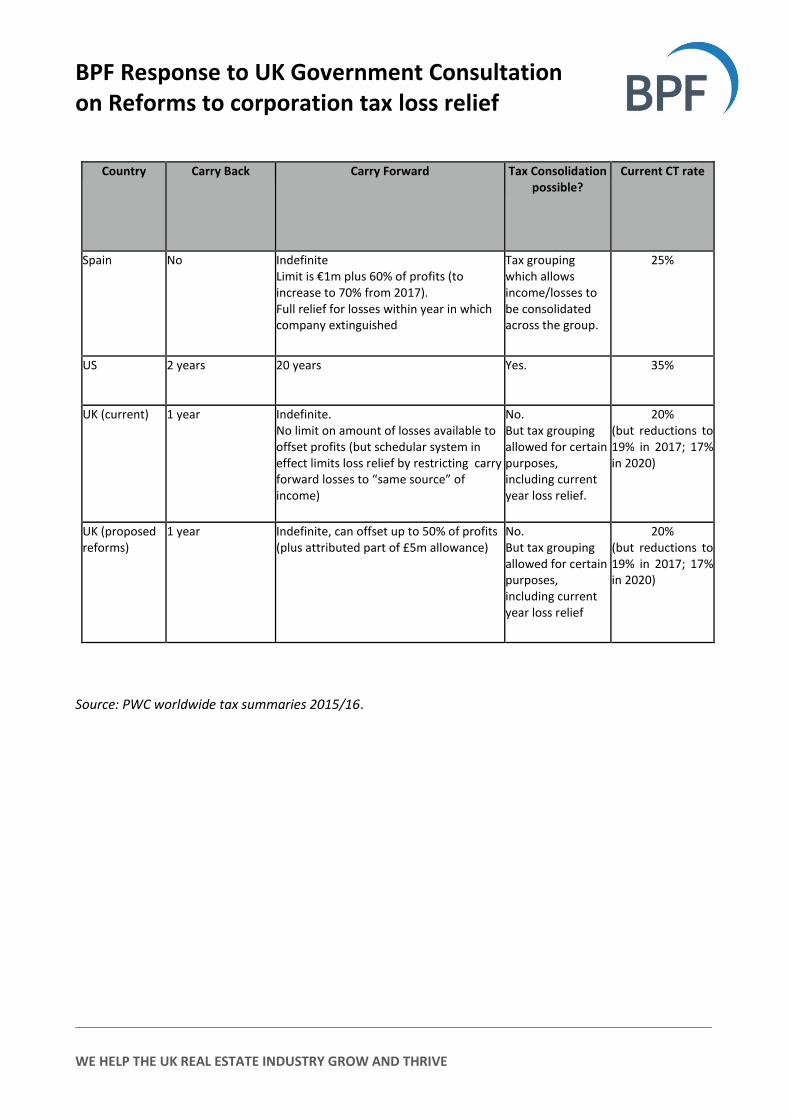

29. The current loss rules recognise the importance of tax neutrality in this context. Recognising that the division of continuous commercial activity into separate 12 month periods for compliance purposes risks producing arbitrary results, the carry forward loss rules allow smoothing of losses and profits over the life cycle of a development.

30. The proposed reforms cut across this. By limiting carry forward relief in such circumstances, developers risk being taxed on more than their (commercial) development profit. Development costs will be reflected in carry forward losses at the point at which the developer starts making its profits. A successful developer will sell down a completed project within one or two accounting periods only, creating a real risk that, at the point the trade ceases, losses will be left stranded.

31. Although there are a number of possible ways to try and address this concern, we recommend that the government focus on two key measures that should help ensure that, for developers, taxable and economic profits will remain aligned after these reforms - measures based on rules brought in by other countries with similar loss restrictions to help smooth out the economic cycle:

31.1. first, allow a developer to obtain full relief for carry forward losses in the final 2 years of a company’s taxable activity; and/or

31.2. secondly, allow a developer to obtain full relief for carry forward losses that arise in the first three accounting periods after commencing its business for tax purposes.

For further detail on the impact of the proposals on property developers, see Appendix 3.

REITs: the ring-fence means losses are already restricted 32. REITs are already subject to restrictions on the use of loss relief given the imposition of a ring-fence

between the exempt property business of a REIT and its residual (and hence taxable) business - both at single company and group level.

33. That ring-fence means that a REIT would not be able to benefit from the additional flexibility that the reforms offer alongside the restriction.

34. In addition, imposing a further corporation tax restriction on already restricted losses runs counter to the underlying policy of the REIT regime - that it is investors, not the REIT itself, that are taxed on the REIT’s property profits. Many of those investors are not corporation tax payers. Applying the proposed loss restriction to REITs would therefore impose a restriction on such shareholders to which they would not be subject if they had carried on the REIT’s property business themselves.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

35. We therefore recommend that the exempt property business of REITS be excluded from the reforms. For further detail on the impact of the proposals on REITS, see Appendix 4.

Keep it simple: make implementation as straightforward as possible 36. If the government decides to continue with the reforms as announced at the Budget, then these new rules

should be effective not on 1 April 2017, but instead for accounting periods beginning on or after the commencement date.

37. This measure is not one directed at countering perceived avoidance: instead it is described as being in pursuance of the government’s simplification and modernisation agenda. We therefore see no justification for having a “one size fits all” start date.

38. Loss relief works by reference to actual accounting periods. Respecting this underlying principle in relation to these reforms avoids companies having to apply different rules to losses arising within the same period. The potential risk of companies looking to change their accounting date to delay the application of the rules can readily be managed by a targeted anti-avoidance provision. For further detail on this, see our detailed comments in Appendix 2.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

Part II: Responses to consultation questions

Question 1: Will the proposed model be effective in delivering the objective of allowing businesses greater flexibility in the use of carried-forward losses? 39. Not necessarily.

40. A commercial real estate (CRE) business will generally involve both property investment and trading activities. It is common for each individual business to be operated by a separate subsidiary. Therefore, within a group, there could be a significant number of single purpose property investment companies, each holding one property. Similarly, trading projects will be operated by separate companies. An established property group can easily have up to 200 companies within it.

41. Looking at how the model would apply in practice to such a group:

Step 1: Within each individual group member, there should be little change in terms of current year losses. Property investment subsidiaries should only generate non-trading profits. Trading subsidiaries may generate both development and investment income, and so may need to carry out the trading/non-trading allocation.

Step 2: The effect for individual group companies is a reduction in the amount of carry forward loss

relief they can access.

Step 3: Given that each individual group member is in general carrying on one business, its Relevant Total Profits should be broadly the same as its non-trading/trading profits - so the first limb of step 3 is unlikely to be relevant. Similarly, the approach of “one company: one business” within the group structure means that sideways carry forward relief (the second limb of step 3) is likely to be irrelevant.

42. Thus, the only possible flexibility comes from the potential for carry forward group relief. Modelling for that

across a mixed group of more than 100 companies beyond, say, one year will be very difficult. This means that, in practice, the potential value of this increased flexibility has to be discounted.

43. Looking beyond the CRE sector to corporation tax payers more generally, the Consultation states that 99 per cent of companies will be unaffected by the restriction because of the £5m allowance. This means that these companies are able to offset carry forward losses in full against future profits.

44. The Consultation however sets out an order of priority for loss relief within the allowance (see paragraph 5.7 of the Consultation). Priority is given to the current streaming rules. This means that carry forward losses will first be applied as now (trade losses offsetting “next period” trading profits and non-trading deficits offsetting “next period” non-trading profits).

45. As a result, it is only if, within that £5m allowance, there are losses that would not be fully utilised under current rules that the new flexibility becomes relevant. It is unclear therefore the extent to which this particular class of corporation tax payers will, in practice, benefit from Step 3: their losses may well be used up in full at Step 2 - and so they are no better off than now.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

46. In this context, in his Budget speech, the then Chancellor stated that the loss reforms “will help over 70,000 mostly British companies”. This suggests that (proportionally) very few companies will think that this objective has been met.

47. On the basis of the HMRC’s Corporation Tax Statistics, there were 1,330,897 companies with either trading profits or other income in financial year 2013/14.2 Assuming the number of companies within the charge to corporation tax is now 1,350,000 (and so a slight increase since 2013/14), only 5.2 per cent of companies will benefit from the reforms.

48. Thus the vast majority of companies within the “unaffected” 99 per cent will be no better off than now under the reforms. Plus, their benefit would appear to come from being outside the reforms, rather than because of the flexibility offered by Step 3.

49. The 13,500 companies affected by the reforms (i.e. the 1 per cent) will however be worse off. This is clear from the policy costings published with the Budget.

50. The costings predict increased Exchequer receipts of £395m (2017/18), £415m (2018/19), £295m (2019/20) and £255m (2020/21) - and these will presumably come from this particular subset of corporation tax payers. For these companies, any benefit from increased flexibility is likely to be more than outweighed by the negative impact of the restriction to be imposed on carry forward loss relief.

51. While the costings are subject to a fairly high level of uncertainty, they indicate that, in practice, very few companies will actually benefit from the reforms. If the goal of these reforms is to modernise the UK’s loss provisions by providing a flexibility that the schedular system does not currently allow, we are concerned that this goal cannot be achieved by the reforms as currently proposed.

52. In our view, the government’s objectives would be better served by coupling reforms to loss relief with (i) a broader review (and potentially abolition) of the schedular system and (ii) a consultation on introducing group consolidation within the UK. This would also assist in ensuring that the UK offers business a loss relief system that is, in all respects, consistent with the approach of G7 countries.

53. We therefore recommend that the government defer this reform until after the OTS has reported on its review of corporation tax computations

54. Appendix 1 contains a comparison of loss regime rules with the G7, plus Netherlands, Spain and Australia (the latter because, like the UK, it has a schedular system).

55. Although the majority of these jurisdictions do indeed impose a restriction on carry forward loss relief, they also allow a group consolidation for corporation tax purposes, which impacts on how loss relief works. In particular, consolidation allows greater flexibility than the UK’s schedular system (even after these reforms). Plus, of these countries, only France currently sets the loss cap at 50 per cent (with Japan planning to reduce its profits cap to 50 per cent from 2017). Spain, in contrast, is about to increase its cap from 60 per cent to 70 per cent.

2 HMRC Corporation Tax Statistics: Analysis of Corporation Tax Receipts and liabilities under the Bank Levy (published 26 May 2016): see

Table 11.4.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

56. The Consultation says that imposing a restriction is consistent with the approaches taken in a number of other G7 countries. Given the nature of the current UK corporation tax system, we are not convinced that what is now proposed is truly consistent with the position elsewhere.

Question 2: Could the calculation be made simpler or more effective? 57. Yes. See our detailed comments at Appendix 2.

Question 3: To what extent does this proposed model provide an effective means of applying the existing and proposed loss restriction rules to the banking sector? 58. No comments.

Question 4: Could the calculation be made simpler or more effective? 59. No comments.

Question 5: Is there any reason why the definition of a group for the surrender of carried-forward losses shouldn’t be aligned with the existing group relief definition? 60. No.

61. Step 3 means that (subject to the priority rules) losses arising in a group company are available for surrender, regardless of whether those losses are current year or carried forward. In effect, the proposals simply add carried forward losses to the list of amounts surrenderable under Chapter 2 of Part 5 CTA 2010. The same definition of “group” as used for current year losses should therefore apply to the proposed rules for carried forward losses.

Question 6: What definition of a group should be used for the purposes of applying the £5 million allowance? 62. In the interests of consistency and simplicity we strongly recommend that “group” for the purposes of the

allowance be the group relief definition. In substance, the £5m allowance is an early application of Step 3.

63. Using the group relief definition also has the advantage of mirroring what would be expected to happen in practice.

64. It is not perfect: the arrangements rules mean that a company could be degrouped (and not within the scope of the allowance) as a result of sale negotiations. Only after the sale was complete would it revert to being in a group. Provision would need to be included to ensure that, whilst degrouped, it would not be entitled to its own (proportionate) £5m allowance.

65. The Consultation refers to concerns as to potential avoidance as the reason for a different definition of group to the group relief definition. We consider that such concerns could be managed.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

66. First, fragmenting a group will have a number of consequences. Other tax groupings could be affected, depending on the manner in which the group relationship is broken. The cost/benefit analysis of breaking a group to increase the number of £5m allowances an (economic) group can access is unlikely to be a simple exercise.

67. Secondly, there are certain well-known (and simple) ways of breaking a group of which HMRC will be aware. If the risk of avoidance is seen as material, modifications to the definition of group could be made (for this purpose only) to ensure that any “break” companies are brought back in to the group.

68. Thirdly, the rules could rely on an unmodified group relief definition of group but include a targeted anti-avoidance provision that allows HMRC to direct that companies in the same IFRS group should be treated as part of the same group if they reasonably believe steps have been taken to break the group for the purposes of maximising access to the allowance.

69. Given that HMRC currently anticipates that only 1% of companies will be affected by the rules, this third option may provide sufficient comfort that groups will not try to claim multiple allowances. In the event that taxpayer behaviour proves otherwise, then a different approach could be taken.

70. We do not agree with either of the two options set out in the Consultation.

71. A test based purely based on accounting control within IFRS 10 would give rise to inappropriate results. It would create particular difficulty for UK businesses owned by private equity funds. In particular, such businesses may not have information as to other companies owned by their private equity parent.

72. If the government decides that an accounting-based test should be used, we recommend that the loss reform rules use the same test of control as is proposed for the interest restriction measures, outlined in paragraphs 8.18 and 8.19 of the consultation on the tax deductibility of interest deductions (May 2016). Given that both the interest restriction and loss relief reforms have similar effects, there is merit in consistency between them in terms of a “group” definition. Under the interest deductibility proposals, certain entities are excluded from being a parent for IFRS purposes - which should include private equity funds

73. A test based on association could also be ineffective for this purpose. Based on other definitions of association, there is a risk that it would be too broad and there is the potential for a company to be associated with more than one group. There would then need to be a “tie-breaker” to prevent double allowance allocation (for example, see the capital gains group rules). An association test that is appropriately targeted is likely to be quite complex. As a result, in practice, assuming that any company within a group relief group would be “associated”, most groups would limit their allocation of the £5m to group relief group members in any event.

Question 7: How should the reforms be applied to consortia relationships? Consortium relief: entitlement to carry forward surrenders 74. We welcome the government’s willingness to include consortium companies within the proposed reform. If

this can be done effectively - and thus simply - the potential additional flexibility it will provide to consortium arrangements will be commercially welcome. In particular, at best, the reforms could mean that if, in a given year, consortium members have insufficient capacity to absorb losses arising in the consortium company, those losses will not then be stranded in that company- consortium members may instead be

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

able to access those losses in a future period when they have capacity. Given that consortia are often formed to run particularly capital-intensive projects, involving significant capex and funding costs, the ability to flex access to losses is particularly important given the impact of a 50 per cent loss cap on existing business models.

75. However the challenge is ensuring the proposals relating to consortia are straightforward and easy to administer. Otherwise, any extra flexibility may not actually be used in practice: consortia will stick with the current year relief they know.

76. This highlights the overarching issue with the government’s consortium proposals. Notwithstanding their logic, they add a significant amount of complexity to a reformed loss relief regime which itself appears to be unduly complex. The consortium company and its members will need to keep detailed records of its losses to be able to identify both (a) the period in which they arose and (b) the interests of consortium members at that time. This is in addition to the detailed records needed in respect of all losses, given the retention of streaming under the UK’s schedular system. See our response to questions 1 and 2 for more on this.

77. We set out an example to illustrate this. The facts are as follows:

(i) In Year 1, Companies A, B, C and D establish a joint venture (Company X). Their shareholdings are 40%, 30% 26% and 4% respectively.

(ii) At the end of Year 3, Company A buys out part of Company’s B stake, increasing its holding to 55%. Company B‘s stake reduces to 15%.

(iii) In Year 1, Company X makes a loss of 100.

(iv) In Year 2, Company X makes a loss of 50.

(v) In Year 3, Company X makes neither a profit nor loss.

(vi) In Year 4, Company X makes a profit of 4.

(vii) None of Company A, B and C can claim consortium relief in Year 1. In Year 2, Companies A, B and C claim current year consortium relief in full. In Year 4, Companies A and B consider carry forward consortium relief claims in respect of the Year 1 carried forward loss.

78. Had current year consortium relief been possible, relief for current year losses would be by reference to the economic/shareholding interests of the consortium members.

79. We accept that it makes sense for a similar approach to apply to carry forward losses - with the economic entitlement of any given consortium member to a carried forward loss being by reference to its economic/shareholding interest at the time the losses arose.

80. Consistent with this approach, it makes sense that if a consortium member leaves the consortium, carry forward losses allocated to that consortium member should be then available for relief within the consortium company only (i.e. reverting to the pre-reform position).

81. This basic principle appears relatively straightforward conceptually. In terms of the example above:

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

(i) In Year 1 entitlement to consortium relief would have been: Company A (40); Company B (30): Company C (26) and Company D (0). That means a loss of 4 will be carried forward in Company X, and can only be used in Company X.

(ii) In Year 4, Company C’s notional entitlement of (26) from year 1 is carried forward in Company X from then on.

82. The carry forward loss of (4) in year 1 relates to Company D’s interest: Company D is never a consortium

member (because its holding is less than 5 per cent). In year 4, Company C is bought out and so its share of the Year 1 loss is restricted from then on in.

83. As the Consultation acknowledges, the difficulty comes when the economic interest of a consortium member changes over the life of the consortium, but that company remains a member. There are a variety of commercial circumstances in which a change could occur - and it could be minor (1 or 2 per cent) or significant (including where a consortium member increases its interest to the extent that it becomes grouped with the consortium company).

84. Our view is that the only workable solution is that a consortium member’s economic/shareholding interest at the time the loss arose should be determinative of that member’s entitlement to loss relief, irrespective of any future changes in their ownership interests. This would only be the case as long as that member remains a consortium member (and so retains an interest of at least 5 per cent in the consortium company). This principle would apply regardless of whether the consortium member’s interest increases or decreased over time and would also apply in respect of (past) losses if the consortium member and company become grouped.

85. Such an outcome would reflect the economic position of the parties - i.e. that consortium member will have borne the cost of that loss when it arose, and should therefore be entitled to the benefit (albeit it a future date) by reference to its share of that economic cost.

86. Existing anti-avoidance provisions within the group relief rules (relating to the existence of arrangements and option arrangements) should ensure that relief will only be available where the consortium member retains a substantive interest in the consortium company (with economic consequences).

87. Protection from avoidance risk would also be provided for the requirement that all consortium members need to consent to any surrenders: if there was a concern as to value leakage, other members would choose to retain the carry forward loss within the consortium. If the government had any residual avoidance concerns from this, a targeted anti-avoidance rule could be introduced.

88. Again, to go back to the example:

(i) In Year 1 entitlement to consortium relief would have been: Company A (40); Company B (30): Company C (26) and Company D (0). That means a loss of 4 will be carried forward in Company X, and can only be used in Company X.

(ii) In Year 2, a loss of (2) is carried forward in Company X and can only be used in Company X.

(iii) In Year 4, Company X can only use (2) of its carry forward losses, leaving 100 losses from Year 1.

Assuming entitlement to relief in Year 4 is fixed by Year 1 entitlement, and the 50% cap is not exceeded by the consortium members, Company A can claim (40), Company B (30). Company C’s notional entitlement of (26) is carried forward.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

89. The example highlights that, even with a relatively simple rule (and in the context of a simple fact-pattern)

the consortium relief position is particularly complex. Tracking the loss entitlement over time, maintaining pools of losses notionally allocated to particular members and re-allocating should that member leave the consortium, will be administratively burdensome. Hence the component parts of how the reforms apply should be as “easy” as possible - hence our suggestion above.3

90. For this reason, we do not think it appropriate to allocate losses between consortium members by reference to the lesser of (a) the member’s interest at the time the loss arose and (b) the member’s interest at the time of the surrender. 4

91. Going back to the example, if this alternative (i.e. lesser of) test applied, then:

(i) Company A can still claim (40) but Company B is restricted and can only claim (15).

(ii) This means, 3 years after incurring the loss, Company X has to look back to its losses from earlier years (that are still within its carry forward pool) and then re-allocate - in this case an additional (15) - as “own use” from then on.

92. Such an approach would not only seem to run counter to the economic logic of the government’s proposals

for consortia, but would add additional complexity to a structure that is already complex enough.

93. Further, a number of factors suggest that, as a practical matter, this alternative approach is not justified as a means of avoiding the risk of loss to Exchequer. First, any delay in accessing relief for the losses means their value to the consortium member is reduced (making surrender less likely). Secondly:

a) a consortium surrender to that member is at the end of Step 3 (in terms of its own computation) – i.e. after it had used its own current year and carry forward losses;

b) any surrender is subject to the 50 per cent cap; and c) in all likelihood, that consortium member would need to pay for any surrendered losses.

In addition, having a right to carry forward losses that is constantly changing may mean that, on a cost-benefit analysis, very few consortia would see carry forward as worthwhile given the administrative and compliance burdens they would face.

94. However, even with the simpler (day one) test for allocating losses, if the government introduces these

changes, we recommend that it monitors the extent to which consortia avail themselves of this new flexibility over, say, the period to 31 March 2021.

95. If take-up is limited (and assuming that the rules have not by then been simplified following the OTS’ review of the UK’s schedular system), we recommend the government then considers alternative ways to provide consortia with the flexibility that these proposals appear intended to offer. In particular, one option could be to allow (all or certain capital-intensive) consortia to “opt out” of the new flexibility, retaining the ability to carry forward losses in full as under current law (subject of course to any State Aid restrictions then applicable).

3 For similar reasons, this further supports the argument that pre- and post- 1 April 2017 losses should be treated the same way.

4 As a matter of policy, the maximum entitlement to losses should not exceed the interest of the member at the time the loss arose.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

Consortium relief: meaning of consortium company 96. Given the potential adverse impact of the reforms on property development carried out in a joint venture,

we recommend that the government amends the consortium relief conditions in sections 132 and 133 CTA 2010 to allow consortium relief claims where the consortium company carries on a UK property business for tax purposes. See our comments in Appendix 3 concerning property development activities.

97. Such a change to the consortium relief rules would help alleviate some of the costs that could otherwise arise in joint ventures that develop to hold as a result of the reforms.

98. In particular, it would level the playing field between “own account” developers and joint ventures, ensuring that companies are not economically disadvantaged because of a commercial decision to carry out a particular project using a joint venture (for example, because of the amount of capital needed for the development and/or to benefit from a joint venture partner’s particular expertise).

Question 8: How could the legislation be protected from abuse in a way that is simple and administrable for businesses? 99. The loss rules contain a significant number of anti-avoidance rules. These should only be added to if there is

a clearly identifiable risk of avoidance that is not already caught by existing provisions. Any new anti-avoidance provisions should be targeted and clear in their scope.

Question 9: Do you have any concerns regarding the government’s proposed approach to loss-buying and trade cessation? Loss- buying 100. We agree that the starting point should be that the existing change of ownership rules should apply to the

“new” more flexible carried forward losses. These rules are understood by business and work well in practice.

101. This means that a company (Co A) acquired by a group (Group X) can continue to use its carried forward losses against its total profits (as permitted under the model) provided that there is no major change in its activities within the specified three years.

102. Losses arising after the change in ownership in both Co A and Group X should also benefit from carry forward group relief in the normal way.

103. We acknowledge that the position is less clear-cut in terms of carry forward group relief for pre-change of ownership carry forward losses (within Co A and Group X).

104. This issue has been approached in different ways by other G7 countries. For example, we understand that Japan effectively separates Co A from the rest of Group X, so that such losses can only be carried forward in Co A.

105. This means that, following a change in ownership, if Co A has losses, it will need to create separate pools for pre- and post- takeover losses (in broad terms, a similar position to that which applies as at 1 April 2017 in relation to pre- and post 2017 losses). This could add to the complexity of applying the rules in practice, even though this approach seems to be the simpler way of dealing with this issue.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

106. In contrast, we understand that Australia allows Group X to access a proportion of Co A’s pre-takeover carry forward losses, but subject to limitation. The limitation is based on a relative market value basis. The rationale behind this it to ensure that the tax system does not stand in the way of commercial group restructuring, whilst at the same time not facilitating the earlier or greater use of those losses.

107. An alternative approach would be to allow the group of which Co A was a member before the takeover to continue to be able to use the losses (given that the economic cost of those losses was borne by that group) - this too could be subject to limitation.

108. Both these latter two options raise technical challenges, particularly in the context of the UK’s schedular system. However both ensure that a company is not subject to further restriction in relation to the use of its losses simply because of it has been the subject of a commercial transaction. In policy terms, this seems preferable as an approach to the Japanese model.

109. If the Australian approach was followed, potential safeguards could include a similar special limitation, a change of activities condition (as applies under the existing rules - any such material change would suggest that access to losses was a factor in the deal) and/or potentially a purpose test (a bona fide commercial purposes test, potentially with a pre-clearance system).

Trade cessation: general 110. The proposed reforms are likely to extend the period over which a company can obtain full relief for its

losses. It therefore increases the risk that a company will have unused losses at the point it ceases to trade/carry on its property business.

111. This could particularly be an issue for companies engaged in property development activities.

112. The nature of property development means that there will always be a timing mismatch between (a) when costs are incurred and (b) profits are earned. This timing gap can, on larger development projects, be several years.

113. Commercially, a developer’s economic profit from its activities is the excess of sales proceeds over its costs. It is therefore reasonable to expect that the tax system should also recognise the economics of such commercial activity and thus aim to tax a developer’s “real” profit, rather than (in effect) substitute an alternative amount as taxable profit that does not reflect this commercial reality. However, the effect of the reforms, because of their interaction with the cessation rules, is that developers risk not being able to claim full relief for their development costs

114. See our detailed comments in Appendix 3.

Trade cessation: property losses 115. Similar concerns arise in relation to UK property business losses. Although the existing rules allow a

company that has ceased to carry on a UK property business to convert unused UK property business losses into expenses of management5, this is likely to be of limited benefit in practice. This is because the ability to convert property business losses into expenses of management is dependent on the company continuing to carry on an investment business.

55

Section 63 CTA 2010.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

116. Within property groups, properties are often owned by single purpose property companies (PropCos). There are a number of commercial reasons for this. For example, it may be a requirement of financing arrangements. It also provides flexibility if the property is ever disposed of, as the sale could take place by disposing of the PropCo shares or the underlying property asset, depending on the buyer’s preference.

117. As PropCo’s property business will generally own one property, if it sells that property, its property rental business will cease. For a limited period, it may have an investment business as a result of investing proceeds of sale: but this will be short-lived. This means that there is limited scope to claim relief for any converted expenses of management, particularly given that they too are subject to the 50 per cent cap.

118. In the Consultation, the government asks for views on whether there should be a special rule for property losses (i.e. property losses set against property income before any remaining losses are set against total profits).

119. Although such a rule may provide a little more flexibility, we consider that this is outweighed by the additional complexity that a further step in the model would add. In general, the circumstances in which a property loss could arise are limited to (a) where a property is untenanted for significant period; (b) a key tenant is in default and (c) significant capital allowance claims.

120. As long as a property business is not a REIT, (c) is something that can be managed over the business cycle given the ability to disclaim capital allowances. Interest and financing costs can be significant for CRE businesses, given their capital-intensive nature, but for non-REIT property companies, relief for such items is provided by way of non-trading deficits. It therefore makes sense to maintain the order of relief as per Step 2 in the Consultation Document.

121. However, the application of the proposals to REITs raises special considerations - see our comments in Appendix 4.

Trade cessation: automatic loss expiry on certain events 122. We do not agree with the inclusion of a general provision that losses should be deemed to expire on the

happening of certain events, linked to there being “no possibility that the losses can be used”.

123. The UK loss rules are broadly based on an indefinite carry forward period, subject to carrying on the same activity and the application of certain targeted anti-avoidance rules. A statutory “cut-off” of losses of the type envisaged in the Consultation would be a significant departure from that model.

124. We see no reason for including such a provision. We think the rules should remain as they are now: we do not understand why expiry needs to be brought forward particularly given that the cessation rules are being left untouched (save for this proposal).

125. The description in the Consultation suggests that the provision would list events which the government considers means that there is no possibility of future use. There is therefore a risk that the assumption underlying the selected events is inaccurate. As a result a company could be prevented from using losses (representing an economic cost) to offset profits that arise after the relevant event, but before actual cessation.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

126. For trade and property losses, there would therefore seem to be no downside to letting the rules continue as now. Plus, the loss rules already contain a number of anti-avoidance provisions to counter loss selling, and so we assume avoidance is not the basis for this proposal.

127. The Consultation provides no explanation of why this is being proposed. Given that such a provision runs counter to the basis on which the loss rules work, there needs to be a clear policy basis for its inclusion.

128. We note that the rules for non-trading deficits do not contain a similar cessation provision. However, to be within the loan relationship rules, a company must be within the charge to corporation tax. This means that it must have a source of income. If a company has a source of income, then it should be allowed to access (past) losses to offset profits from that source. This pre-condition to being within the loan relationship rules is (effectively) a cessation rule (albeit applied to all sources, not just one particular activity).

129. The reforms additionally allow carried forward non-trading deficits to be group relieved. This means that, assuming a company with carried forward non-trading deficits continues to be within the charge to corporation tax, its deficits can offset other group companies’ profits.

130. The structure of the loan relationship rules mean that the position here is different to that which applies to trading and property losses. The reforms simply accentuate this difference. In some ways it could be argued that this new flexibility should similarly allow carried forward trading and property losses to continue to be available within the group following cessation: as the group would have borne the economic cost of those losses as they arose, there is a policy case - disregarding fiscal factors - for allowing continued access going forward.

131. We are not therefore convinced that group relief for non-trading deficits should be disallowed. The non-trading deficit will exist because of an economic cost that had arisen to the group. Existing anti-avoidance rules within the loan relationship rules and the new interest restrictions provide assurance that the deficit represents a bona fide commercial cost. The 50 per cent cap, and the fact that group relief is only brought in at the end of Step 3, itself limits the extent to which profits can be sheltered by any such deficit. We do not see an expiry rule as necessary.

132. Further, we question whether such a provision, even if appropriate, is needed now. The review of corporation tax by the OTS may result in significant change to the corporation tax system. Any consideration of an “automatic” expiry provision should be deferred until after the OTS has reported. For example, if the OTS recommend (and the government accepts) a radical overhaul of the schedular system and/or revised grouping arrangements (such as tax consolidation), the loss position could be very different. We recommend deferral.

133. Finally, if such a provision were to be introduced, it would be very important to ensure that the listed events are appropriate in relation to the policy intention. Any such provision should set out clear, factual events - there can be no ambiguity given the “cliff-edge” effect of the provision. In particular, the provision should not apply purely because there is “no possibility of future use”, with guidance then providing examples of when that might be

Question 10: Are there other areas of the tax system with which these rules would have a significant impact? If so, what are these, and what might the consequences of that impact be? REITs

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

134. The REIT regime imposes a ring-fence on losses arising in a REIT’s exempt property business. Adding an additional loss restriction on REITs would have a significant impact on those REITs that have carry forward losses in their exempt property business. See our detailed comments in Appendix 4.

135. We recommend that REITs are carved out of the proposed reforms. Any carve out would only be in relation to the exempt property business of a REIT.

136. In terms of a REIT’s residual business, we see no reason why the reforms (once finalised) should not apply to that residual business in the same way they apply to non-REIT corporate taxpayers. This is because, although losses within the residual business are also ring-fenced (albeit to a lesser extent)6 , profits of the residual business are calculated using normal corporation tax principles (without adjustment) and are not taken into account in calculating a REIT’s mandatory property income distribution (PID).

Property Development Activities 137. See our response to question 9 and our detailed comments in Appendix 3.

Offshore property traders 138. At Budget 2016, the government announced that offshore property developers would be subject to

corporation tax on trading profits derived from UK land, regardless of whether the developer had a UK permanent establishment.7 These rules took effect on 5 July 2016.

139. Losses arising to an offshore property developer are therefore within the scope of corporation tax.8 An offshore property developer would not however appear to be “UK related”9 for the purposes of the UK group relief rules and so, even if within a group for group relief purposes, would not be able to surrender its UK corporation tax losses to “UK related” group companies.

140. The Consultation does not mention whether the proposed loss reforms would apply to offshore property developers that are now within the charge to corporation tax.

141. Chapter 2 of the Consultation infers that the 50 per cent cap and the Step 3 flexibility are seen as part of a single package. If the proposed reforms apply to offshore property developers, they will be subject to restriction without the benefit of flexibility. Plus, as the new offshore property development regime applies to a trade of developing land, the issues discussed in Appendix 2 would apply at the point at which the developer realises its profit for tax purposes.

142. We understand from discussions with HM Treasury and HMRC that the government does not intend offshore property developers to be within the scope of the proposed loss reforms.

143. However, the intention behind the offshore property developer rules is to ensure that offshore developers have the same tax treatment as onshore developers. On this basis, offshore property developers should be

6 Sections 541(2)(b), (3)(b), (4)(a) and (b) and (5) CTA 2010.

7 See HMRC Technical Note: Profits from Trading in and Developing UK Land (16 March 2016) at

https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/507766/1044_Budget_Day_Technical_Note__v2_0__3_.pdf 8 Under the proposed section 356OF CTA 2010

9 Section 134 CTA 2010 (although the draft legislation proposes amendments to section 107 CTA 2010, the draft legislation does not

currently seek to amend section 134 CTA 2010.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

able to group relieve losses to create a level playing field between them and UK tax resident developers. This would then suggest that the loss reforms should apply to such developers.

Question 11: Do you have views on the government’s proposed approach to oil and gas and life insurance companies? 144. No comments.

Question 12: What impact could the reforms have on public-private partnership or private finance initiative projects? 145. No comments.

Question 13: What other sectors or specialist areas of taxation need consideration as part of these reforms? 146. See our response to questions 9 and 10.

Question 14: What will be the impact of the reforms on insurers’ regulatory capital? 147. No comments.

Question 15: To what extent could the reforms impact on the business plans of new-entrant companies? 148. Please see our comments in relation to :

148.1. new development projects in Appendix 3; and

148.2. “new entrant” REITS in Appendix 4.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

Appendix 1: Comparison of loss restriction regimes in G7 and (selected) OECD countries

Country Carry Back Carry Forward Tax Consolidation possible?

Current CT rate

Australia

No Indefinite. No limit on amount of losses available to offset profits (but schedular system in effect limits loss relief by restricting carry forward losses to “same source” of income and need common ownership).

Yes 30%

Canada

3 years 20 years, subject to anti-avoidance rules. No 28% (federal rate)

France 1 yr subject to €1m cap

Indefinite. Limit is €1m plus 50% profits, and company must be carrying on the same business.

Yes 33.33%

Germany

1 yr subject to €1m cap

Indefinite. Limit is €1m plus 60% profits, and company must be carrying on the same business.

No, but profit polling agreement possible allowing offset of profits and losses within the profit pool

15% plus solidarity levy (5.5%) plus trade tax (min of 7%)

Italy

No Indefinite. Limit is 80% of profits. But 100% relief for losses arising within first 3 years of starting business.

Yes, if election made.

27.50%

Japan

1 year 9 years (going to 10 years); Limit is 65% profits (2016) which is to reducing to 50% (2017). (previously 85% cap).

Yes. 23.40%

Netherlands

1 year 9 years. No limit in amount of losses available to offset profits.

Yes: fiscal unity. 25%

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

Country Carry Back Carry Forward Tax Consolidation possible?

Current CT rate

Spain

No Indefinite Limit is €1m plus 60% of profits (to increase to 70% from 2017). Full relief for losses within year in which company extinguished

Tax grouping which allows income/losses to be consolidated across the group.

25%

US

2 years 20 years Yes. 35%

UK (current) 1 year Indefinite. No limit on amount of losses available to offset profits (but schedular system in effect limits loss relief by restricting carry forward losses to “same source” of income)

No. But tax grouping allowed for certain purposes, including current year loss relief.

20% (but reductions to 19% in 2017; 17% in 2020)

UK (proposed reforms)

1 year Indefinite, can offset up to 50% of profits (plus attributed part of £5m allowance)

No. But tax grouping allowed for certain purposes, including current year loss relief

20% (but reductions to 19% in 2017; 17% in 2020)

Source: PWC worldwide tax summaries 2015/16.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

Appendix 2: The 3 Step Process: simple and effective?

Complexity 1. The effect of the reforms will be to add further complexity to an already complex system for loss relief.

2. In an article in 2012, Dominic de Cogan10 wrote:

“The relief of losses for income and corporation tax purposes is not the most difficult field of tax law in conceptual terms. Yet policymakers, legislators and judges in the early twentieth century managed to complicate it beyond any reasonable measure by losing sight of the purpose of relief and focusing too strongly on immediate technical problems. ...... we have been bequeathed a structure of relief that makes little sense in some respects, and which occupies an unnecessarily lengthy portion of the statute book as a result.”

3. The proposed reforms risk making the position even worse.

4. The main reason for this derives from Objective 5: the government’s intention to maintain the existing rules for computing corporation tax income under the schedular system. Absent this, Step 2 and the first limb of Step 3 could be merged into a single carry forward sideways relief for all losses.

5. The maintenance of the schedular system - and the resultant need to “stream” losses - creates multiple orders of priority and allocations throughout the model, many of which are “new” as far as compliance is concerned, adding to the practical challenges for business in applying the measures. For example:

a) at step 1, profits need to be streamed into trading and non-trading profits to determine a “proportion” ;

b) at step 1, losses needed to be allocated proportionately between trading and non-trading profits;

c) at step 1, an order of priority applies to the £5m allowance (order being basically a mini-application of Step 2 and Step 3 even though, technically, they do not apply to a group that does not have losses over the allowance);

d) at step 2, an order of priority for pre-2017 amounts ahead of post 2017 amounts; and

e) at step 3, we understand that it is intended that an order of priority will apply to the (unutilised) losses available to be surrendered out).

6. In a group context, complexity is also added by the lack of a group consolidation system within the UK. As shown in Appendix 1, the UK is alone within the G7 in not having such an option for companies - even Australia, that also has a schedular system, allows group consolidation.

7. Concerns about the possibility of avoidance (particularly as a result of carry forward group relief) compound the complexity: targeted anti-avoidance rules are proposed; a new “loss expiry” provision is discussed and a different definition of group (for the allowance) is also proposed.

10

See B.T.R. 2012, 5, 655-671 (At the time, Leverhulme funded Early Career Research Fellow at the University of Birmingham; currently

lecturer and fellow of Christ’s College Cambridge.)

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

8. The compliance burden for business arising from these proposals alone cannot be underestimated.11

9. Within the CRE sector, groups can consist of up to 200 subsidiaries. For each company, a number of tax factors will need to be taken into account in determining its net position - such as capital allowance entitlement (and the amount to be disclaimed); interest deductions; transfer pricing adjustments; brought forward and any current year losses (including non-trading deficits) and chargeable gains (which also requires consideration of the availability of allowable losses within the group and the possibility of section 171A elections).

10. This exercise, once done, then has to be repeated across the group as a whole. It is a very time consuming exercise - and (even today - under legacy rules) is not something capable of being done by a software programme. This group tax management exercise is about optimising across the group the usage of reliefs that Parliament has allowed for economic losses suffered over a business cycle - this is not about looking to avoid paying tax on current substantial profits “due to losses incurred from historic events and activities”.

11. The proposed reforms - and in particular the way they are being implemented because of the policy decision to keep the schedular system as is - will make this group tax exercise even more time-consuming for those groups potentially within their scope.

12. This raises serious questions around the government’s tax simplification agenda.

Pre-2017 Losses and Post-2017 losses 13. A significant factor in this complexity is the differentiation between pre-1 April 2017 and post-1 April 2017

losses.

14. As a result of the proposed reform, a company could be in the position of having to create and monitor up to nine carry forward loss pools12. In addition, under the proposed interest restriction rules, that company will also need to create and monitor two further pools (for restricted interest and excess capacity). The equivalent number for a company today is five. The total of nine is without regard to additional complications should the company be part of a consortium. In addition, it ignores current year losses.

15. For example, within the CRE sector, a property developer may carry on a trade (of developing). It may let out properties prior to sale - or may indeed have one it developed to hold: these could include UK and overseas properties. It may also carry on certain management functions elsewhere in the group. Generally, it will be carrying on business to realise a profit (and not make losses). If losses do arise across its businesses, then it could have:

• trading losses (pre-2017 and post-2017)

• UK property business losses (pre-2017 and post-2017)

• expenses of management (pre-2017)

• carry forward expenses of management (post-2017)

• overseas property losses

11

Note: at the same time, companies will also have to come to terms with their compliance responsibilities within the new interest restriction rules. 12

Ignoring non-trading losses on intangible fixed assets: that would add another two loss pools.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

• non-trading deficit (pre-2017 and post-2017)

16. If that company is a parent of a group, companies within the group will themselves be running one or more loss pools. Managing the tax position of the overall group will involve understanding the profile of each company

17. The operation of the rules would be simplified if the distinction between pre-2017 and post-2017 losses was removed. This would mean that pre-2017 carry forward losses would be able to benefit from the same flexibility as post-2017 losses (under the current proposals, pre-2017 losses are restricted at Step 2 and cannot be used at Step 3).

18. In addition to simplifying the rules, it would also be more equitable. Objective 1 of the reforms is said to be “increased flexibility”. For pre-2017 losses, there is no such flexibility, just restriction.

19. For those losses that arose pre-Budget 2016, there would not have been an expectation of any additional flexibility: however, as a corollary, a company that made a loss prior to that date would have had a reasonable expectation that it could carry that loss forward in full to offset future profits. As a result, we consider that, as a policy matter, those losses should benefit from the same flexibility that attaches to post 2017 losses. Similarly losses arising since Budget 2016 should have that flexibility.

20. The Consultation Document states that the reason for restricting flexibility to post 2017 losses only:

“This increased flexibility will have a significant impact on the Exchequer, both in terms of accelerating relief for companies’ carried-forward losses and providing relief for losses that may otherwise have been unutilised.”

21. We have no information as to the stock of losses within UK companies as at Budget 2016. However we note that the policy costings for this measure13 show additional tax of £395m and £415m in 2017-18 and 2018-19 respectively. Such costings are however subject to high uncertainty given they are dependent on assumptions as to profits (and recent events may affect those assumptions: see our response to question 1).

22. We ask government to reconsider the exclusion of pre-2017 losses from the proposed flexibility: allowing losses to be treated the same under these reforms would not only be fair, but would make the reforms administratively easier to manage.

Commencement 23. The timetable for introduction of these reforms is ambitious.

24. The current timetable gives businesses very little time to assess fully the implications of the proposals. The Consultation outlines how the reform will work in principle, but the detail of the proposals will only be identifiable when draft legislation is published. This unlikely to be available until early December 2016 at the earliest - four months before it is due to come into effect.

25. The policy costings published by the government at Budget 2016 anticipated an overall tax cost of £395m in 2017/18. This evidences that the proposals are likely to have a detrimental effect on the 1 per cent of companies impacted by the proposals.

13

HM Government - Budget 2016: Policy Costings: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/508147/PU1912_Policy_Costings_FINAL3.pdf

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

26. Plus, many of the businesses affected by these reforms will also be affected by changes to the tax deductibility of interest, which the government has also announced will come into effect on 1 April 2017.

27. The combined effect of the proposed interest deductibility rules and the loss reforms on interest expense is not yet fully understood: not least because the complexity of both rules makes it incredibly difficult to model.

28. Accordingly, the government should delay the implementation of the loss reform proposals until 1 April 2018 at the earliest. The Consultation states that the reforms are part of the government’s modernisation programme. As a result, we ask that the government does not rush into these reforms - but consults widely with stakeholders on creating a loss relief regime that is simpler than that proposed, comparable with that of other G7 countries and that meets the government’s objectives (including a restriction on the use of carry forward losses).14

29. Such a delay will allow stakeholders and government to reflect on any recommendations made by the OTS on corporation tax computation. The review that the OTS has been asked to carry out is clearly pertinent to the issues underlying some of the complexity within the current loss reform proposals. The OTS is committed to provide its report before Budget 2017.

30. Plus, in any event, regardless of whether the government decides to stick with its current timetable, these new rules should be effective for accounting periods beginning on or after the commencement date, to avoid businesses having to apply different rules to losses in the same actual accounting period. The measure is not one directed at countering perceived avoidance: therefore we see no justification for having a “one size fits all” start date. Loss relief works reference to actual accounting periods. The risk of companies changing their accounting date to delay the application of the rules can readily be managed by a targeted anti-avoidance provision.

Gateway 31. We recommend that the government include a gateway test within the rules.

32. The government has acknowledged that the proposals have been structured on the basis that 99 per cent of companies will not be affected15. A gateway would provide a clearer commitment to ensuring that such companies fall outside the reforms - and would reflect, in a more concrete form, the importance of the £5m allowance in this context.

33. Absent a gateway, the proposed re-ordering of the priority rules for loss relief apply to all companies, regardless of whether they have material carried forward losses. Step 1 requires a company to categorise its profits into two categories, and then allocate its current year losses proportionately between those categories.

34. We understand that it is not intended to create a different result to that which would apply currently, but this is difficult to test in the abstract, particularly in the absence of draft legislation detailing how the various loss rules will interact.

14

By way of comparison, when the government last looked at loss reform, the consultation was run over a three year period from 2002 - 2005, involving publication of a number of papers for comment. 15

Paragraph 1.18 of the Consultation.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

35. Step 1 appears to be a preparatory step ahead of Step 2. If Step 2 is not applicable - either because the company does not have carried forward losses or because the group has carry forward losses of less than £5m allowance - then is Step 1 necessary?

36. Companies/groups without material carry forward losses are not the target of the reforms. This is evidenced by their not being subject to restriction nor (in most cases) benefitting from any increased flexibility within Step 3 (absent surrenders from a group company).

37. If a gateway test applied, then, assuming the £5m carry forward allowance is not exceeded, the company would continue to use the current rules relating to loss relief. Where a company is a member of a group relief group, the gateway test would apply across that group (as any surrender of carry forward losses would be between members of that group). This would ensure consistency as between group members: i.e. all group members are treated the same way, whether under current rules or the new regime.

38. The gateway test would need to be applied on an accounting period by period basis. However, once a company/ group fails the gateway test (i.e. has carry forward losses in excess of £5m) and falls within the new regime, it will remain in the regime from then on.

39. In some ways, the gateway offers a form of transitional relief, ensuring that companies/groups that are not the target of the reforms stay within the current rules unless and until their tax profile changes. This means that (a) small and medium sized enterprises and (b) profitable groups will be able to continue as now - applying rules with which they are familiar.

40. This would also ensure that the position of those companies/groups that would not get beyond Step 1 is guaranteed to be the same before and after the reforms are introduced.

41. Plus, including a gateway would alleviate some of the pressure on companies referred to in paragraphs [ commencement] above - as only those companies targeted by the government by this reform (the 1 per cent as per the Consultation) would be affected by them in terms of compliance.

42. We do not think running the two regimes (current and new) concurrently would be problematic from a legislative or administrative standpoint, not least because two such loss systems have been operating in parallel since 2015 when restrictions were first applied to banks. Plus, many of the existing loss relief rules will apply as now in any event16. The cross-over would be the gateway test itself - and companies could be asked to “tick a box” in terms of making that gateway election in the first accounting period the rules apply.

43. Further, the OTS is about to embark on a review of the corporation tax computation rules. That review could lead to fundamental reform of the schedular system as the Consultation itself alludes. If there were such reform, then the detail of the proposed loss restrictions would have to change. Providing transitional relief through a gateway until the outcome of the OTS review is known would avoid companies having to change compliance systems twice within a short period - without impact on the success of the reform in terms of meeting its stated objectives.

Trading and non-trading proportions 44. Step 1 requires a company to apportion profits between “trading” and “non-trading” profits. We

understand that where a company carries on more than one trade Step 1 requires it to aggregate all trading

16

This seems to be implied by the Consultation, although we appreciate that the Consultation is focused on the principles, rather than the detail, of the proposals.

BPF Response to UK Government Consultation on Reforms to corporation tax loss relief

WE HELP THE UK REAL ESTATE INDUSTRY GROW AND THRIVE

profits. Current year losses are offset against total profits, and so the same rules will apply as now to any current year sideways relief claim.