BP Solar and Wind Employee Savings Plan Summary Plan Description

48

BP Solar and Wind Employee Savings Plan Summary Plan Description October 2012

Transcript of BP Solar and Wind Employee Savings Plan Summary Plan Description

BP Solar and Wind Employee Savings Plan Summary Plan Description

October 2012

Who Is Eligible 2How To Enroll 2

Hired or Rehired Before January 1, 2011 2Hired or Rehired On or After January 1, 2011 2After You Enroll 3Beneficiary Designations 3

How the Plan Works 4Your Contributions 5

Minimum Contribution 5Maximum Contribution 5Catch-Up Contributions 6What Is Included in “Eligible Pay” 7The Advantages of Before-Tax Savings 8The Advantages of After-Tax Savings 8The Advantages of Roth 401(k) Savings 8Roth In-Plan Conversions 9Changing Your Contribution Amount 9Rollover Contributions 10

Company Match Contributions 10Investment Options 11

Setting Your Investment Direction 12Exchanging Investment Options 12

Vesting 13How To Access Your Account Information 14How To Take a Loan 14

Types of Loans 14Minimum Loan Amount 15Maximum Loan Amount 15Interest Rate on Plan Loans 15How To Apply for a Plan Loan 15Repayment of Plan Loans 16

Prepaying a Plan Loan 16How To Take a Withdrawal While You Are Employed 17

Special Rule for Permissible Withdrawal after Auto-Enrollment 17In-Service Withdrawal Sources and Timing 17

Hardship Withdrawals 18Tax Consequences of Withdrawals 19How To Request a Withdrawal 20

While You Are Employed at the Company 20What Happens If You Take a Leave of Absence 20

Earning Vesting Service While on a Leave of Absence 20Earning Vesting Service While You Are Disabled 21

What Happens If You Die 21Payments To Your Beneficiary 21

What Happens If You Are Rehired 22Calculating Your Service After Rehire 22Restoring Forfeitures 22

What Happens If You Are No Longer Eligible To Participate Due To a Transfer 23What Happens If You Take a Qualified Military Leave of Absence 23

If You Die or Become Disabled While on a Qualified Military Leave of Absence 24

BP solar and wind employee savings plan

When You Leave the Company 24Automatic Distribution or Rollover of Account Balance Valued at $5,000 or Less 24

Benefits Valued at Greater Than $1,000 But Not More Than $5,000 25Benefits Valued at $1,000 or Less 25

Requesting a Distribution 25Minimum Required Distributions 25

Lump-Sum Distributions 26Rollover Distributions 26

Installment Payments 27How Installment Payments Are Calculated 27How Installment Payments Are Withdrawn From Your Account 27Changing the Distribution of Installment Payments 28If You Die While Receiving Installment Payments 28

Deferring Your Distribution 28Partial Withdrawals 28If You Are Not Vested 29Tax Considerations 29

Special Tax Considerations for Roth 401(k) Contribution Source 30Required Tax Withholding 30Postponing Taxes and Tax Withholding 30Additional Taxes 31Reduction for Overpayment 31

What Happens If Benefits Are Denied 31When the Plan Changes or Ends 31Administrative Information 31

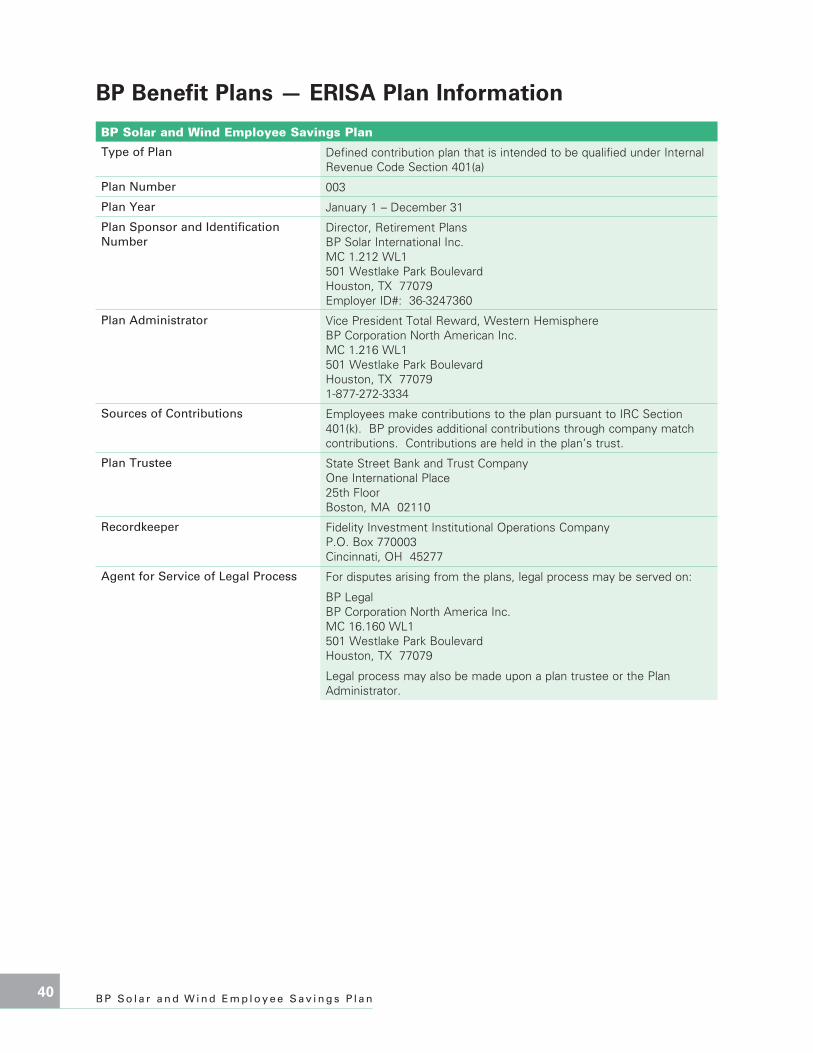

Plan Trustee 32Plan Sponsor and Identification Number 32Plan Administrator 32Plan Recordkeeper 33Agent for Service of Legal Process 33

Governing Plan Documents 33Pension Benefit Guaranty Corporation 33No Right to Employment 33Assignment of Interest/Liens on Funds or Property 34Qualified Domestic Relations Orders (QDROs) 34Incapacity of Participant or Beneficiary 35The Future of the Plan 35

What Your Rights Are Under ERISA 35If You Have Questions About Your Benefits 36How to File a Formal Claim Under ERISA 37

Formal Claims and Appeals Process 37Claims Process 37Appeals Process 38Effect of the Appeals Administrator’s Decision 39After the Claims and Appeals Process Has Concluded 39Time Limits and Venue for Bringing Suit 39Importance of Exhausting the Administrative Review Process 39

BP Benefit Plans — ERISA Plan Information 40Accessing Additional Resources 41

BP Retirement Services at Fidelity 41

NoteThe sponsor of the plan is BP Solar International Inc., which is sometimes referred to in this document as ‘the company.’ As the context requires, ‘the company’ may also refer to another subsidiary of BP plc that adopts this plan.

Features To Help You

Within this summary, you will find several features to help increase your understanding of your benefits, use your benefits wisely or find answers to your questions. These features include:

z Icons — The following icons placed in the text highlight essential information for you:

c Directs you to important information you should pay special attention to.

l Alerts you to key deadlines you must meet.

* Points you to other sections in this summary which provide you with additional information.

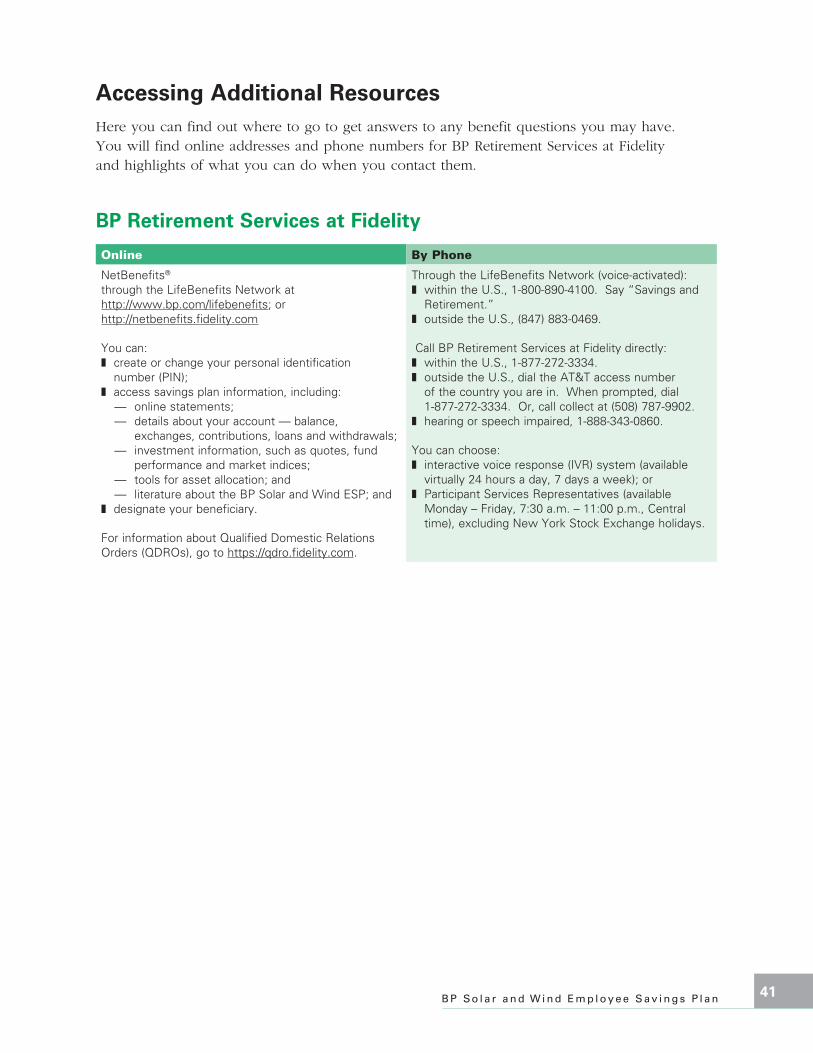

z Contacts — “Accessing Additional Information” on page 41 gives you the phone numbers and websites for claims administrators.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n 1

investment losses as well. You may invest in any of the funds described in the BP Solar and Wind Investment Options Guide.

You have access to your account balance through the BP Solar and Wind Employee Savings Plan’s loan provision, and, under certain conditions, you may take a withdrawal of a portion of your account while you are still working for the company.

This plan is intended to be a “qualified retirement plan” under Section 401(a) of the Internal Revenue Code and to meet the requirements of Code Section 401(k).

Important documents that you should review before deciding to participate in this plan include:

z this summary of the BP Solar and Wind Employee Savings Plan;

z the most recent BP Solar and Wind Investment Options Guide, including any Updates;

z the most recent Quarterly Investment Performance Statement;

z all documents incorporated by reference into the above documents; and

z future supplements and amendments to these documents.

In the event of any inconsistency between a statement contained in this summary and the plan document, the terms of the plan document will control. In the event of any inconsistency between the online version of this document and the print version, the terms of the print version will control.

Because your future financial security is so important, the company offers you the BP Solar and Wind Employee Savings Plan. Participation in this plan is completely voluntary and, if you are eligible, you may enroll at any time.

The BP Solar and Wind Employee Savings Plan is a 401(k) plan that lets you save whatever percentage of your eligible pay you elect, up to plan and legal limits, toward your retirement. The company matches 100% of every dollar you contribute, up to 7% of your eligible pay. You can elect to contribute on a before-tax, after-tax or Roth 401(k) basis, or a combination of all three.

BP makes saving for retirement under the BP Solar and Wind Employee Savings Plan easier by offering an automatic enrollment feature. If hired or rehired on or after January 1, 2011, you will automatically contribute to the plan unless you specifically choose not to.

If you do not change your contribution election, you will be automatically enrolled as soon as administratively possible in the BP Solar and Wind Employee Savings Plan starting with your first paycheck on or after your 30th day of employment. A before-tax deduction of 7% of your eligible pay will be automatically contributed to your plan account each pay period.

All contributions and investment gains or losses are credited to your plan account. Unless you choose a different investment option, your plan account will be invested in the Solar/Wind Target Date Fund nearest to your retirement date (assumed to be age 65). However, you can choose how your savings are invested from a wide variety of investment options. You — not the company — assume all investment risk. That means your account will benefit from any investment gains and experience any

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n2

Who Is EligibleIn general, you are eligible to participate in the BP Solar and Wind Employee Savings Plan (the “BP Solar and Wind ESP”) if you are an employee of BP Solar International Inc, BP Wind Energy North America Inc. or another subsidiary of BP that has adopted this plan (and on a U.S. dollar payroll).

You are immediately eligible to enroll if you have met the above requirements and are not excluded in one of the categories below.

Regardless of your employee classification above, you are not eligible to participate in the BP Solar and Wind ESP if you are:

z a leased employee;

z a non-resident alien with no U.S. income;

z an employee based in Puerto Rico;

z an independent contractor or fee-for-service worker, even if reclassified as an employee;

z a member of a collective bargaining unit (union), unless your collective bargaining agreement provides that you may participate in the BP Solar and Wind ESP;

z covered by an agreement specifying that you are not eligible to participate in the BP Solar and Wind ESP;

z receiving employer contributions under or making contributions to another company tax-qualified defined contribution retirement plan, which provides for before-tax or after-tax contributions; or

z not classified as an employee on a participating employer’s payroll, even if you are reclassified as an employee.

If you are (or were) a leased employee and are later hired as a regular employee by the company, you may be entitled to vesting service for the time you worked as a leased employee. Contact BP Retirement Services at Fidelity for more information.

* “Accessing Additional Resources,” page 41

How To Enroll

Hired or Rehired Before January 1, 2011

If you are eligible to participate, you can enroll at any time through BP Retirement Services at Fidelity.

* “Accessing Additional Resources,” page 41

Hired or Rehired On or After January 1, 2011

If you are eligible to participate, you will automatically be enrolled in the plan unless you specifically choose not to. If you do not change your contribution election, you will be automatically enrolled as soon as administratively possible in the savings plan starting with your first paycheck on or after your 30th day of employment. A before-tax deduction of 7% of your eligible pay will be automatically contributed to your plan account each pay period.

If you do not wish to participate, you can change your contribution rate to 0% within the first 30 days of your employment, or you can adjust your contribution rate to any whole percentage between 1% and 80%, as appropriate for you.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n 3

After You Enroll

When you change your contribution rate — or after you are automatically enrolled in the savings plan — you will need to:

z determine how much to contribute to the plan (if you choose a different contribution rate than the automatic before-tax 7% of your eligible pay);

z determine the type of contribution to make (before-tax, after-tax and/or Roth 401(k));

z choose your investment options (unless you choose different investment options, your plan account will automatically be invested in the Solar/Wind Target Date Fund nearest your retirement date (assumed to be age 65)); and

z designate a beneficiary, who will receive your plan benefits in the event of your death.

* “Your Contributions,” page 5; “Investment Options,” page 11; “Beneficiary Designations,” at right

By enrolling in the plan, you authorize your employer to take payroll deductions each pay period based on the percentage of eligible pay you elect to contribute. Contributions to the plan will begin as soon as administratively feasible after you enroll — normally one or two pay periods after you enroll.

The first time you access BP Retirement Services, the system will prompt you for personal information so you can establish your personal identification number (PIN). The personal information may include your Social Security number, your birth date or your mailing address. Information required to set up or change your PIN may vary over time for account security purposes.

Beneficiary Designations

When you enroll in the BP Solar and Wind ESP, you will need to designate a beneficiary, who will receive your BP Solar and Wind ESP account in the event of your death.

* What Happens If You Die,” page 21

z If you are married, your spouse is automatically your beneficiary. If you want to designate someone other than your spouse to be your beneficiary, your spouse must consent in writing each time you make a new designation. A notary public must verify that consent. In any case, a beneficiary designation should be completed.

z If you are not married, you may designate anyone you wish to be your beneficiary, and you may change this designation as often as you like. If you do not designate a beneficiary, if no designated beneficiary survives you or if your beneficiary designation was not filed properly, upon your death your account will be paid to your estate.

You can name one person, more than one person, or a trust or other legal entity as your primary beneficiary. You can also name a secondary beneficiary, or contingent beneficiary, to receive your account in the event your primary beneficiary(ies) dies before you. If you name more than one primary beneficiary and one of those beneficiaries does not survive you, his or her portion will be shared equally among any remaining beneficiaries of the same type (primary or contingent), except to the extent otherwise provided on the applicable beneficiary form. Payment will be made to your contingent beneficiary(ies) only if there is no surviving primary beneficiary(ies).

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n4

You should be aware of some additional provisions that apply to beneficiary designations:

z Your beneficiary designations cannot be changed by anyone after your death.

z No beneficiary can refuse to accept his/her benefit.

z A divorce does not automatically revoke your former spouse as a designated beneficiary. You must change your beneficiary designation to replace him or her.

z A divorce does not automatically revoke your former spouse as a designated beneficiary. You must change your beneficiary designation to replace him or her. However, if the Plan Administrator receives a qualified domestic relations order (QDRO) and you do not re-designate your former spouse as a beneficiary, your former spouse will no longer be your designated beneficiary. Please be aware that a QDRO may affect your beneficiary designation. If you are impacted by a QDRO, please refer to your court documentation for information about any required named beneficiaries.

* “Qualified Domestic Relations Orders (QDROs),” page 34

c

Remember to review your beneficiary designations in the event your family status changes — for example, if you marry, divorce or become widowed.

To designate your beneficiary or change your beneficiary designation, contact BP Retirement Services online or by phone.

* “Accessing Additional Resources,” page 41

You may need to properly complete any required forms such as a notarized consent and return them to BP Retirement Services in order for your new or changed beneficiary designation to become effective. If any required forms are not completed properly or accepted by BP Retirement Services, your designation will not be valid and you will be notified accordingly.

How the Plan WorksYou may save whatever percentage of your eligible pay you desire (in whole percentages) on a before-tax, after-tax or Roth 401(k) basis, up to plan and legal limits, toward your retirement. If hired or rehired on or after January 1, 2011, you will be automatically enrolled at 7% on a before-tax basis, unless you decline or change your automatic contribution.

* “What Is Included in ‘Eligible Pay,’” page 7

Participation is entirely voluntary.

Based on your elections, your contributions are deducted automatically from each paycheck on a before-tax basis, after-tax basis, Roth 401(k) basis or a combination of the three. You may also make rollover contributions to the plan. You choose how to invest your savings from a wide variety of investment options. And, the company makes a company match contribution equal to 100% of every dollar you contribute (excluding rollover contributions), up to 7% of your eligible pay.

When you enroll (or are automatically enrolled) in the BP Solar and Wind ESP, an account is set up in your name. Your account consists of the following contribution sources, if applicable:

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n 5

z before-tax, which holds your before-tax contributions and catch-up contributions, if applicable;

z after-tax, which holds your after-tax contributions;

z Roth 401(k), which holds your after-tax contributions to your Roth 401(k) account and catch-up contributions, if applicable;

z company match, which holds your company match contributions;

z before-tax rollover, which holds any taxable amounts you have transferred — or “rolled over” — from another tax-qualified retirement arrangement or IRA;

z after-tax rollover, which holds non-taxable amounts you have transferred — or “rolled over” — from another tax-qualified retirement arrangement; and

z Roth 401(k) rollover, which holds any Roth 401(k) amounts you have transferred — or “rolled over”— from another tax-qualified retirement plan.

Each of these contribution sources also reflects any gains or losses on your contributions.

You have access to your account balance through the BP Solar and Wind ESP’s loan provision, and, under certain conditions, you may take a withdrawal of a portion of your account while you are still working for the company. When you leave the company, you may choose from several distribution options, including a rollover distribution to another employer’s qualified plan or to an IRA, or you may leave your account in the BP Solar and Wind ESP under certain conditions if your balance exceeds $5,000.

Your Contributions

You make your contributions through automatic payroll deductions. Your contributions are transferred to the trustee after each payroll cycle as soon as administrative procedures allow.

When you contribute to the BP Solar and Wind ESP on a before-tax basis, your contribution is not subject to current federal and, in most cases, state or local income taxes while held in the plan. However, your before-tax contributions are subject to federal employment taxes (i.e., FICA).

Minimum Contribution

The minimum contribution you may make is 1% of your eligible pay.

* “What Is Included in ‘Eligible Pay,’” page 7

Maximum Contribution

You may designate whatever whole percentage of your eligible pay you wish to contribute, subject to the following plan and legal contribution limits:

z There is an annual 402(g) dollar limit set by the Internal Revenue Service (IRS) on before-tax and Roth 401(k) contributions to 401(k) plans such as the BP Solar and Wind ESP. In 2012, this annual limit is $17,000. (If you are age 50 or older as of December 31, 2012, you may make an additional $5,500 in catch-up contributions.)

Your employee contributions will automatically change from before-tax and/or Roth 401(k) to regular after-tax once you reach the annual 402(g) contribution limit (including catch-up contributions, if applicable), and will automatically revert to your before-tax and/or Roth 401(k) elections at the beginning of the next year. Keep in mind that if you are a new employee, this 402(g) limit applies to your combined before-tax and Roth 401(k) contributions to all 401(k) plans in which you have participated during the calendar year. As a result, you will need to keep track of your own total before-tax contributions — including catch-up contributions, if applicable — and request a refund of those that exceed the limit by contacting your previous employer or BP Retirement Services.

The deadline for making this request to BP Retirement Services is March 15 of the year following the year in which your contribution exceeds the limit. l

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n6

z The IRS also limits total annual additions to savings plans, which includes both employee and employer contributions. This annual limit is $50,000 for 2012. (For purposes of this limit, “compensation” may include more than the definition of eligible pay under the plan — it is essentially equal to your W-2 income plus your before-tax contributions for benefits.)

z The IRS also places an annual limit on the amount of eligible pay that can be recognized under the plan. For 2012, this annual limit is $250,000. If you reach the annual compensation limit, your contributions will stop without notice.

* ”Accessing Additional Resources,” page 41

Your actual contribution percentage may be lower because of tax withholding and certain other payroll deductions that the company places as a higher deduction priority (i.e., federal, state and local taxes, health and protection benefit deductions, etc.) or because an applicable tax limit is reached. For example, if you elect to contribute 75% of your eligible pay to the BP Solar and Wind ESP, your actual contribution may be only 60% after other payroll deductions are taken. Depending on your contribution rate and other payroll deductions, your take home pay (or direct deposits) could be significantly reduced or eliminated. However, you can adjust your contribution rate at any time.

If you reach the annual additions limit ($50,000 in 2012), your contributions will stop. However, your contributions will automatically resume at the beginning of the next year, as long as you have not otherwise stopped your contributions.

If you reach the annual additions limit — or if your eligible pay exceeds the annual limit described above — you may be eligible for a non-qualified savings plan benefit. Contact BP Retirement Services for more information.

* “Accessing Additional Resources,” page 41

The BP Solar and Wind ESP must also satisfy legal non-discrimination rules, designed to ensure that qualified retirement plans do not pay a disproportionate portion of their benefits to highly compensated employees. If you are a highly compensated employee, your contributions — other than catch-up contributions, which are not subject to these rules — may need to be reduced or partially refunded in order for the plan to comply with these rules. You will be notified if you are affected.

Catch-Up Contributions

In any year in which you are (or reach) age 50 or older (based on company records), you are eligible to make before-tax and/or Roth 401(k) contributions in excess of the annual 402(g) limit, which is $17,000 in 2012 and the total contribution level ($50,000 in 2012). These contributions are referred to as “catch-up contributions.” The maximum catch-up contribution for 2012 is $5,500, so your total before-tax and Roth 401(k) savings opportunity for 2012 — if eligible — is $22,500.

Eligibility for catch-up contributions is based on your date of birth as found in payroll records. It is your responsibility to make sure the date on file is correct. Corrective changes will not be made if you have not verified your date of birth in a timely manner.

c

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n 7

When you reach the increased annual before-tax and Roth 401(k) limit (including the catch-up contribution), your employee contributions will automatically convert to after-tax for the remainder of the year. They will revert to before-tax and Roth 401(k) at the beginning of the next year. All your employee contributions — including the catch-up contribution — will be matched by the company up to 7% of eligible pay.

What Is Included in “Eligible Pay”

Your BP Solar and Wind ESP contributions are based on a percentage of your eligible pay. For purposes of the plan, “eligible pay” includes the following components of your pay from the company:

z basic salary or wages (including before-tax contributions for benefits);

z overtime pay;

z shift and rate differentials;

z pay based on piecework;

z payment by mileage for drivers;

z commissions;

z payments under an annual incentive plan at the business unit or stream level;

z lump-sum performance awards paid in connection with annual salary administration;

z payment from a deferred compensation plan, if paid prior to your termination; and

z pay in lieu of vacation.

If you leave the company, keep in mind that any of these eligible forms of payment received beyond 30 days following your last date of employment will generally not be considered eligible pay.

The law sets an annual limit on the amount of eligible pay that can be considered for plan purposes. For 2012, this annual limit under the Internal Revenue Code is $250,000 of eligible pay. However, if your pay is over this limit, you may be eligible for a non-qualified savings plan benefit.

What Is Not Included in “Eligible Pay”

“Eligible pay” does not include the following components of your pay:

z sign-on, retention or ratification payments;

z relocation payments or allowances;

z educational assistance reimbursement;

z expense allowances or premium pay based on your work site;

z the value of any stock award or long-term incentive payment;

z the value of any share appreciation right or stock option grant or exercise;

z spot awards, reward or recognition payments, or any other comparable payments;

z severance or separation payments;

z additional pay to compensate you for working during all or part of a 60-day period following notice in connection with a severance or separation program;

z deferred compensation (including salary, bonus or variable pay);

z tax reimbursements;

z payments made under an annual incentive plan: (1) that are paid when the employee is no longer an eligible employee, or (2) in connection with an employee’s termination of employment paid before the time that payments are made to similarly situated active employees of the business unit or stream;

z payments excluded as eligible pay under the plan by an employment contract or bonus plan; and

z any other compensation not described as eligible pay on this page.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n8

The Advantages of Before-Tax Savings

Each dollar you contribute to the BP Solar and Wind ESP on a before-tax basis is a dollar that is not included in your taxable income for that calendar year. So you do not pay taxes on that money (including any investment income) until it is distributed from the plan.

Before-tax contributions do not reduce the amount of your compensation that is used to calculate pay-related benefits, such as life insurance, disability insurance or retirement benefits. And, because Social Security taxes are based on your unreduced pay, your Social Security benefits will not be affected by your contributions to the BP Solar and Wind ESP. Remember, you are always 100% vested in the market value of your before-tax contribution source.

* “Vesting,” page 13

The following example shows how making before-tax contributions instead of after-tax contributions can increase take-home pay. The example is based on a married employee who files a joint tax return with two allowances. The employee earns $80,000 in eligible pay (base salary and annual bonus) and decides to save 7% of that amount.

The Advantages of After-Tax Savings

Making after-tax contributions offers several benefits:

z You pay taxes on your contributions now at current tax rates, so if tax rates are higher later on at time of distribution you are better off.

z Any gains or income you earn on your investment options accumulates on a tax-deferred basis.

z You save through convenient payroll deductions.

z You can take an in-service withdrawal of your after-tax contributions. (In contrast, withdrawals from your before-tax and Roth 401(k) contribution sources are restricted.)

z You are always 100% vested in the market value of your after-tax contributions.

* “How To Take a Withdrawal While You Are Employed,” page 17

The Advantages of Roth 401(k) Savings

Making Roth 401(k) contributions offers several benefits:

z You pay taxes on your contributions now at current tax rates, so if tax rates are higher later on at time of distribution you are better off.

z Any gains or income you earn on your investment options are tax-free when distributed in a qualified distribution. A qualified distribution is a distribution that is made five taxable years after you make your first Roth 401(k) contribution and after you reach age 59½, die or become disabled.

z You have access to your Roth 401(k) contributions through in-service withdrawals, the same as before-tax contributions.

z You are always 100% vested in the market value of your Roth 401(k) contributions.

Before-Tax After-Tax Savings Savings

Eligible pay: $ 80,000 $ 80,000Before-tax savings (at 7% of eligible pay): – 5,600 – 0Taxable income: $ 74,400 $ 80,000Federal income tax*: $ 7,935 $ 8,775After-tax savings (at 7% of eligible pay): – 0 – 5,600Annual take-home pay: $ 66,465 $ 65,625

Difference in take-home pay: $ 840

* State and local taxes are not included in this example.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n 9

Roth In-Plan Conversions

Effective January 1, 2012, you may convert eligible assets in your account into Roth amounts. This gives you the potential to earn tax-free income and take tax-free withdrawals, provided certain requirements are met.

* “Tax Considerations,” page 29

Generally, you can only convert assets that are otherwise eligible for in-service withdrawal. Some examples include:

z Before-tax contributions if you are over age 59½;

z After-tax contributions;

z Vested portions of your company match based on the rules below:

— If you have participated in this plan for five years or more, your entire company matching contribution balance;

— If you have participated in this plan for less than five years, only the portion of your company matching contribution that has been in the plan for at least two years; and

z Before-tax and after-tax rollover contributions.

Unlike a Roth IRA, there is no IRS limit on the amount that you can convert in a Roth in-plan conversion, nor any restrictions based on the amount of your income.

Roth in-plan conversion contributions are available for loans.

If you are a resident of Puerto Rico and you are subject to the income tax laws of Puerto Rico, you may not make a Roth in-plan conversion election.

Your beneficiary or alternate payee may make a Roth in-plan conversion election only if he or she is your spouse.

To make an election, contact BP Retirement Services at Fidelity. Please note that a Roth in-plan conversion election is irrevocable and cannot be changed.

* “Accessing Additional Resources,” page 41

Changing Your Contribution Amount

After you enroll (or are automatically enrolled) in the BP Solar and Wind ESP, you may change your contribution amount (in 1% increments), stop contributing or restart your contributions at any time before you terminate employment. Changes will be effective as soon as administrative procedures allow.

If you reduce your contribution amount to less than 7% of eligible pay or stop contributing entirely, your company match contributions will accordingly be reduced.

* “What Is Included in ‘Eligible Pay,’” page 7

To change your contribution amount or stop contributing, contact BP Retirement Services.

* “Accessing Additional Resources,” page 41

The decision of whether and when to make a Roth in-plan conversion within the plan depends on a number of factors that you should weigh carefully. We encourage you to consult your tax advisor before making an election.

c

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n10

Rollover Contributions

If you qualify and elect a lump-sum distribution from another tax-qualified retirement arrangement or IRA, you may be able to contribute — or “roll over” — the taxable portion of your distribution directly into the BP Solar and Wind ESP. You are always 100% vested in the market value of your rollover contribution source.

To make a rollover contribution, you need to follow specific procedures that are available from BP Retirement Services, including:

z Taxable distributions can be rolled over from a tax-qualified retirement arrangement or IRA either directly or indirectly. Only a direct rollover is permitted from a Roth 401(k) plan or Roth IRA.

z Non-taxable distributions can only be rolled over via a direct rollover from tax-qualified retirement arrangements (not from IRAs). Also, note that the plan will not track tax-basis in any non-taxable amounts rolled into the plan. This means, for example, that you will lose any tax advantage on pre-1987 after-tax contributions made to the prior plan.

* “Accessing Additional Resources,” page 41

Company Match Contributions

Each pay period you receive a dollar-for-dollar company match contribution on the first 7% of eligible pay you contribute to the BP Solar and Wind ESP on a before-tax, Roth 401(k) or after-tax basis, or a combination of the three.

* “What Is Included in ‘Eligible Pay,’” page 7

Your company match contributions and any investment income on those contributions are subject to a vesting requirement.

* “Vesting,” page 13

Here is an example of how company match contributions are calculated. In this example, an employee earns $32,000 in eligible pay and decides to save 10% of that amount.

Company Match ContributionsBP Solar and Wind ESP contribution ($32,000 x 10%): $ 3,200The company match contribution — 100% of the employee contribution, up to 7% of eligible pay (100% x 7% x $32,000): + $ 2,240Total annual contribution (excluding investment gains or losses): $ 5,440

Company match contributions are credited to your company match contribution source and invested initially in the same way as you elected to invest your employee contributions, but you may make exchanges to other investment options at any time. If you have not set an investment direction for your employee contributions, your company matching contributions will be automatically invested in the applicable Solar/Wind Target Date Fund for you based on an estimated retirement age of 65, but you may exchange to other investment options at any time.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n 11

Investment Options

The BP Solar and Wind ESP allows you to choose from a variety of investment options. You decide which options best suit your investment plan and then set your investment direction. Remember, it is important to review your investments periodically, and to rebalance your allocation or adjust your investment strategy.

Unless you choose a different investment option, your BP Solar and Wind ESP account will be automatically invested in the Solar/Wind Target Date Fund nearest to your expected retirement date (assumed to be age 65).

A complete list of all of the investment options available under the BP Solar and Wind ESP is contained in the BP Solar and Wind Investment Options Guide, which is incorporated by reference.

Read the entire BP Solar and Wind Investment Options Guide, Quarterly Investment Performance Statements (QIPS) and Updates for information about the investment options available under the BP Solar and Wind ESP. Contact BP Retirement Services at Fidelity if you would like a printed copy of the BP Solar and Wind Investment Options Guide.

* “Accessing Additional Resources,” page 41

Keep in mind that you have sole responsibility for choosing those investment options in which you invest initially and for exchanging your investment options over time. Neither the company nor any other plan fiduciary is liable for any loss in value of your investment holdings resulting from your exercise of your investment responsibility to the extent permitted under Section 404(c) of ERISA.

c

Keep in mind that any of the plan’s investment options may be changed, closed to new investments or eliminated at any time and without prior notice.

c

You should also consider the benefits of maintaining a diversified investment portfolio. In general, spreading your assets across different types of asset classes (such as stock, bonds and short-term investments) can lower your portfolio’s overall risk. This is because market or other economic conditions that cause one asset class or particular security to perform well may cause another asset class or specific security to perform poorly. Although diversification is not a guarantee against loss, it can be an effective strategy to help you manage investment risk.

As part of understanding your investment options, it is also important to know the cost (fees and expenses) of your investments, since cost can impact your net return (investment results after fees and expenses are deducted).

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n12

Generally, you can set your investment direction for new contributions or exchange investment options for your account balance at any time.

Setting Your Investment Direction

You may set your investment direction for all contributions sources — both employee and company — as often as you would like by contacting BP Retirement Services at Fidelity either online or by phone.

* “Accessing Additional Resources,” page 41

Read the Investment Options Guide and Updates for information about any restrictions or limitations on your investment direction, exchanges or other plan transaction requests. For example, some of the investment funds may have transfer restrictions on frequent traders. Contact BP Retirement Services if you would like a printed copy of the Investment Options Guide.

* “Accessing Additional Resources,” page 41

c

If you do not set an investment direction when you enroll in the BP Solar and Wind ESP, your employee contributions, company matching contributions, and any rollovers will be automatically invested in the applicable Solar/Wind Target Date Fund for you based on an estimated retirement age of 65. You can change this election at any time.

Exchanging Investment Options

You may exchange the investment options of the funds currently in your account anytime — as often as you would like — by contacting BP Retirement Services either online or by phone.

* “Accessing Additional Resources,” page 41

You may exchange all or a portion of your plan account among the BP Solar and Wind ESP’s investment options.

* “Investment Options,” page 11

Read the entire text of the Investment Options Guide, the most recent Quarterly Investment Performance Statement (QIPS) and any Updates to the Guide for a more complete description of all the investment options described in this summary, for the performance history of the funds and for information about selecting your investment options. The information about investment options contained in the Investment Options Guide supersedes the investment option information included in this summary. Contact BP Retirement Services if you would like a printed copy of the Investment Options Guide.

* “Accessing Additional Resources,” page 41

c

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n 13

If you are not yet vested when you leave the company, the unvested portion of your company match contribution source will be forfeited as of the earlier of the following two dates:

z the date you take a total distribution of your plan account; or

z seven years from the date you leave the company, unless you are rehired.

Forfeitures are used to reduce future employer contributions or reduce plan expenses.

* “What Happens If You Are Rehired,”

page 22; “If You Are Not Vested,” page 29

Vesting

Your right to ownership of your BP Solar and Wind ESP account is known as vesting.

You are always 100% vested in the value of your before-tax and Roth 401(k) contribution sources (including catch-up contributions), your after-tax contribution source and your rollover contribution sources. That means you will be entitled to receive 100% of the market value of these contribution sources when you leave the company, regardless of your length of service.

You are fully vested in your company matching contributions when any of the following occur:

z You have completed at least three years of vesting service with the company;

z You reach at least age 65 while employed by BP;

z You are terminated while disabled (as determined under BP’s long-term disability plan); or

z You die while employed by BP.

You may also become 100% vested in your company match contribution source immediately if you terminate employment:

z involuntarily as a result of a sale of all or part of your employer to an unrelated entity, the closing of a facility, or the cessation of operations at a facility;

z under the terms of a written severance plan adopted by the company;

z involuntarily as a result of your employment function being outsourced in accordance with a contract between the company and the outsourcer; or

z under a separation agreement between you and the company.

This special vesting provision does not apply to term contract employees.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n14

How To Access Your Account InformationYou have daily access to view your account information securely online via Fidelity’s NetBenefits® site or you may receive printed quarterly statements. If you elect the online feature, you will have access to your account balances and your personal rate of return for any month or calendar quarter within the last 24 months. No matter how you decide to review your account — quarterly hardcopy statements or online — you will receive a paper statement and Quarterly Investment Performance Statement annually following the fourth quarter of each year.

In these statements — both hardcopy and online — you will see how your plan investment options are performing and how much you and the company have contributed during the relevant period. You will also get the status of any outstanding loans you have from the BP Solar and Wind ESP, plus summaries of any transactions performed during the relevant period. Contact BP Retirement Services if you have any questions about the information on these statements.

* “Accessing Additional Resources,” page 41

How To Take a LoanYou may take out a loan from your BP Solar and Wind ESP account for any reason before you leave the company. You may have no more than two loans outstanding at one time. However, special rules apply to participants who had loans transfer from the BP Employee Savings Plan on December 31, 2007.

When you take out a plan loan, you make loan repayments to your BP Solar and Wind ESP account with interest. Repayments are made through automatic payroll deductions in equal installments over a specific period of time. If you have an outstanding loan and you are not receiving a paycheck from the company, BP Retirement Services will provide a coupon book for repayments. Contact BP Retirement Services for more details.

* “Accessing Additional Resources,” page 41

Types of Loans

Two types of loans are available: general purpose loans and residential loans. You may take a general purpose loan for any reason. Residential loans can be used only to purchase your principal place of residence. Applications for residential loans require submittal of a sales agreement.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n 15

How To Apply for a Plan Loan

You may apply for or model a loan from your BP Solar and Wind ESP account through BP Retirement Services.

* “Accessing Additional Resources,” page 41

In addition to the loan amount, a loan setup fee of $35 will be charged against your account each time you take out a loan. This setup fee may be changed from time to time. There is no charge for modeling a loan.

Unless you elect otherwise by contacting BP Retirement Services at Fidelity, your loan will be prorated across your plan investment options. Your loan and setup fee will be taken from the contribution sources in your BP Solar and Wind ESP account in accordance with procedures established by the Plan Administrator.

For example, suppose an employee has a vested account balance of $20,000 — including $8,000 in the before-tax contribution source, $4,000 in the before-tax rollover contribution source and $8,000 in the company match contribution source — and wants to take out a loan for as much as possible. The maximum loan amount possible would be $10,000, or 50% of the total account value.

Special rules apply for participants on a qualified military leave from the company. For information, contact BP Retirement Services.

* “Accessing Additional Resources,” page 41

c

Minimum Loan Amount

The minimum amount you may borrow from your BP Solar and Wind ESP account is $1,000.

Maximum Loan Amount

The maximum amount you may borrow from your BP Solar and Wind ESP account is 50% of your vested balance, or $50,000, whichever is less. Any outstanding loans you have taken over the previous 12 months under a company plan will reduce the amount you have available to borrow.

Interest Rate on Plan Loans

The interest rate on any loan you take out from your BP Solar and Wind ESP account will be based on the prime rate as indicated in The Wall Street Journal on the last business day of the previous quarter, plus 1%. Once established, the rate is fixed and will not change for the term of your loan. So, if the interest rate as published in The Wall Street Journal is 4% on March 31 (a business day), your interest rate for a loan initiated on June 1 would be 5%.

Special rules apply for participants on a qualified military leave from the company. For information, contact BP Retirement Services.

* “Accessing Additional Resources,” page 41

c

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n16

If you apply for a loan and satisfy the conditions that apply to your application, you will be sent a check or electronic funds transfer (EFT), if elected, for the amount of the loan. The loan agreement that contains a truth-in-lending disclosure will be sent to you, or provided online if EFT is elected. You should read your loan agreement carefully before endorsing your loan check or endorsing online, as your endorsement will bind you to the terms of the loan agreement.

Repayment of Plan Loans

If you take out a loan from your BP Solar and Wind ESP account, your loan repayments — including principal and interest — will be automatically deducted in equal amounts from each paycheck on an after-tax basis. If you have an outstanding loan and you are not receiving a paycheck from a participating employer (for example, you have terminated employment with BP or you are on an unpaid leave of absence), a kit to set up automatic payments via Direct Deposit will be provided. If you do not respond, a coupon book will be sent. Contact BP Retirement Services at Fidelity for more information.

Your loan repayments are credited back to your account in reverse order that they were taken out. If you are making contributions at the time of the repayment, the loan payments are invested according to your current investment direction on file.

If you do not make a loan payment when it is due, your entire loan balance will be considered in default and will be treated as a withdrawal. Withdrawals are subject to regular income taxes, including — if applicable — a 10% early withdrawal penalty, unless you make full payment of your missing payment(s) within a 90-day grace period. If you default on a loan, you must repay the defaulted loan (plus interest) before you take out a new loan. Special rules apply for participants on a qualified military leave from BP. For more information, contact BP Retirement Services at Fidelity.

c

The minimum repayment period is six months. The maximum time period for repayment of general purpose loans is five years. However, if the loan is for the purchase of your principal place of residence, the maximum time period for loan repayment is 15 years.

If you change payroll frequencies (e.g., weekly to semi-monthly), your loan will be automatically reamortized.

c

Prepaying a Plan Loan

You may prepay the total unpaid balance of your loan at any time without penalty. To arrange for prepayment, contact BP Retirement Services.

* “Accessing Additional Resources,” page 41

You can always make additional payments by check and the amount will be applied to the principal.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n 17

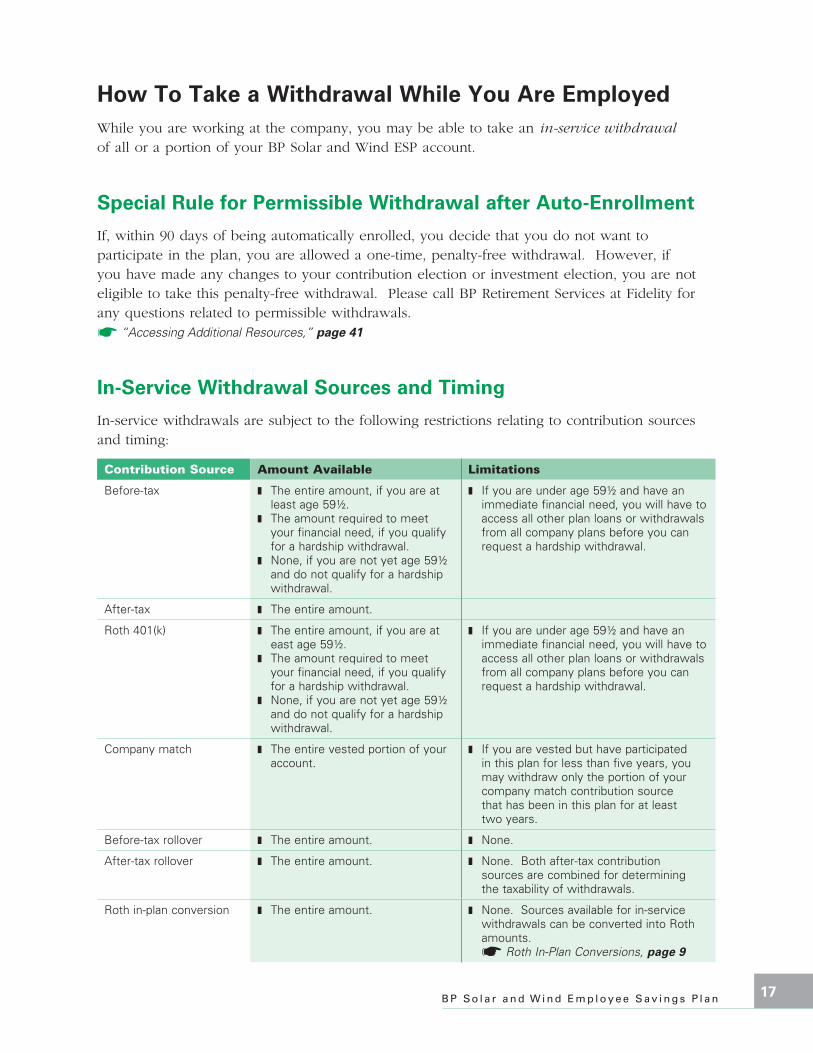

How To Take a Withdrawal While You Are EmployedWhile you are working at the company, you may be able to take an in-service withdrawal of all or a portion of your BP Solar and Wind ESP account.

Special Rule for Permissible Withdrawal after Auto-Enrollment

If, within 90 days of being automatically enrolled, you decide that you do not want to participate in the plan, you are allowed a one-time, penalty-free withdrawal. However, if you have made any changes to your contribution election or investment election, you are not eligible to take this penalty-free withdrawal. Please call BP Retirement Services at Fidelity for any questions related to permissible withdrawals.

* “Accessing Additional Resources,” page 41

In-Service Withdrawal Sources and Timing

In-service withdrawals are subject to the following restrictions relating to contribution sources and timing:

Contribution Source Amount Available Limitations

Before-tax z The entire amount, if you are at least age 59½.

z The amount required to meet your financial need, if you qualify for a hardship withdrawal.

z None, if you are not yet age 59½ and do not qualify for a hardship withdrawal.

z If you are under age 59½ and have an immediate financial need, you will have to access all other plan loans or withdrawals from all company plans before you can request a hardship withdrawal.

After-tax z The entire amount.

Roth 401(k) z The entire amount, if you are at east age 59½.

z The amount required to meet your financial need, if you qualify for a hardship withdrawal.

z None, if you are not yet age 59½ and do not qualify for a hardship withdrawal.

z If you are under age 59½ and have an immediate financial need, you will have to access all other plan loans or withdrawals from all company plans before you can request a hardship withdrawal.

Company match z The entire vested portion of your account.

z If you are vested but have participated in this plan for less than five years, you may withdraw only the portion of your company match contribution source that has been in this plan for at least two years.

Before-tax rollover z The entire amount. z None.

After-tax rollover z The entire amount. z None. Both after-tax contribution sources are combined for determining the taxability of withdrawals.

Roth in-plan conversion z The entire amount. z None. Sources available for in-service withdrawals can be converted into Roth amounts. * Roth In-Plan Conversions, page 9

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n18

Withdrawals are generally considered taxable and may also be subject to penalties and withholding. Of course, income tax laws are complex and subject to change.

Hardship Withdrawals

If you are not yet age 59½, you may apply to take a hardship withdrawal of your before-tax contributions or Roth 401(k) contributions only if you satisfy IRS rules about financial hardship withdrawals. You must provide acceptable proof that you have a severe financial hardship before your withdrawal can be approved. To qualify for a financial hardship withdrawal under IRS rules, you must:

z Need the money for an immediate and severe financial need;

z Not be able to meet the need by stopping contributions to the plan;

z Have no other funds available to you, your spouse or your minor children to meet this need, including reimbursements or compensation by insurance, liquidation of assets or loans, including loans or withdrawals from the plan; and

z Withdraw only enough money necessary to meet this need (including any federal, state and local taxes, and penalties).

When you apply for a hardship withdrawal, you will be required to provide proof of hardship. Once you have received the withdrawal, you will not be allowed to make contributions (including catch-up contributions) to your BP Solar and Wind ESP account or receive company match contributions for the following six months.

* “Company Match Contributions,” page 10

c

You have an immediate financial need if you experience any of the following:

z For the purchase or construction of your principal residence (excluding mortgage payments);

z To pay expenses for the repair of damage to your primary residence that would qualify for a casualty deduction on your federal income tax return (determined without regard as to whether the loss exceeds 10% of adjusted gross income);

z For the payment of tuition, related post-secondary education expenses, and room and board expenses for the next 12 months for yourself, your spouse, your child or any other person who is your dependent for federal income tax purposes;

z To prevent eviction from or foreclosure on your principal residence;

z To pay for certain uninsured medical expenses for yourself, your spouse, your child or any other person who is your dependent for federal income tax purposes (determined without regard as to whether the loss exceeds 7.5% of adjusted gross income); or

z To pay funeral expenses for your spouse, your child or any other person who is your dependent for federal income tax purposes.

* “How To Take a Loan,” page 14; “In-Service Withdrawal Sources and Timing,” page 17

In addition to the amount you need for any of these expenses, you may withdraw enough of your account to pay the taxes you will owe on your withdrawal.

It is a good idea to consult a tax advisor to learn about the impact each BP Solar and Wind ESP withdrawal option has on your personal situation before you request a withdrawal.

* “Tax Consequences of Withdrawals,” page 19

c

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n 19

All or a portion of your hardship withdrawal is considered taxable and is subject to penalties. In addition, hardship withdrawals cannot be rolled over to an Individual Retirement Account (IRA) or another qualified retirement plan — they must be used toward relief of your hardship.

Withdrawals for Employees Called to Active Military Duty

As allowed under the Heroes Earnings Assistance and Relief Tax Bill of 2007, if you are a reservist or national guardsman called to active duty after September 11, 2011, and serve for six months (180 days) or more, you may withdraw some or all of your contributions to the plan without having to pay the 10% early withdrawal penalty. However, regular income taxes continue to apply to these payments in most cases. Also, you may redeposit all or part of the withdrawal amount to an Individual Retirement Account (IRA) within two years after the end of your active duty. For more information, contact BP Retirement Services at Fidelity.

* “Accessing Additional Resources,” page 41

c

Tax Consequences of Withdrawals

Taxable withdrawals from your BP Solar and Wind ESP account are taxed as ordinary income in the year withdrawn. If you have not left the company and are not yet age 59½, you also may be subject to a 10% tax penalty for early withdrawal, unless you elect a rollover of your non-hardship withdrawal to an individual retirement account (IRA) or another qualified retirement plan.

* “Rollover Distributions,” page 26

Permissible withdrawals made during the 90-day period following automatic enrollment are taxed as ordinary income but are not subject to the 10% early withdrawal tax penalty.

c

Withdrawals from your Roth 401(k) account that are not “qualified distributions” have additional tax consequences.

* “Special Tax Considerations for Roth 401(k)

Contribution Source,” page 30

A federal income tax withholding of 20% applies to the taxable portion of withdrawals that are eligible for rollover but are not directly rolled over to another tax-qualified retirement arrangement or IRA. You also may be responsible for state and local taxes.

Withdrawals are generally considered taxable and may also be subject to penalties and withholding. Of course, income tax laws are complex and subject to change. It is a good idea to consult a tax advisor to learn about the impact each plan withdrawal option has on your personal situation before you request a withdrawal.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n20

To avoid the tax consequences of withdrawing from your BP Solar and Wind ESP account, you may want to consider a plan loan instead.

* “How To Take a Loan,” page 14

How To Request a Withdrawal

To determine how much you may have available for an in-service withdrawal or to request a withdrawal, contact BP Retirement Services.

* “Accessing Additional Resources,” page 41

You will receive a single cash payment of your withdrawal amount. Your withdrawal will be taken from your contribution sources according to your request.

Unless you elect otherwise by speaking with BP Retirement Services at Fidelity, your withdrawal will be prorated across your investment options.

While You Are Employed at the CompanySpecial rules apply to your participation in the BP Solar and Wind ESP if certain life events occur.

What Happens If You Take a Leave of Absence

In general, your BP Solar and Wind ESP employee and company match contributions will continue while you are still receiving a regular paycheck from the company. Specifically:

z If you are on a paid leave of absence, your contributions will continue during your leave. You may change or stop your contributions at any time by contacting BP Retirement Services.

z If you are on an unpaid leave of absence (including a medical/long-term disability leave), your contributions will stop until you return.

z If you are on a qualified military leave, upon your return you may make up any missed contributions. You will receive the full company match you would have received while you were on qualified military leave, reduced by any match you did receive during that time. Contact BP Retirement Services at Fidelity for more information about eligibility for qualified military leaves of absence and make-up contributions.

* “What Happens If You Take a Qualified Military Leave of Absence,” page 23; “Accessing Additional Resources,” page 41

Earning Vesting Service While on a Leave of Absence

Regardless of whether your leave of absence is paid or unpaid, you will continue to earn credit toward vesting service during the period you are on an approved leave.

* “Vesting,” page 13

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n 21

The amount of credit you can earn depends on the type of leave you take:

z If you are on a medical/long-term disability leave, you may earn up to 24 months of service.

z If you are on a family medical leave, you may earn up to 12 months of service.

z If you are on a military leave, you will earn service for your entire absence from work, as long as you return to work within the time period prescribed by law.

z If you are on any other type of approved leave, you may earn up to 12 months of service.

Earning Vesting Service While You Are Disabled

If you become totally and permanently disabled while employed by the company (as defined under the company’s Long-Term Disability Plan), you will automatically become 100% vested in your company match contribution source, if you were not already vested.

What Happens If You Die

If you die while employed by the company, your beneficiary gains the right to your total BP Solar and Wind ESP account balance — including company match contributions — even if you were not already vested.

* “Beneficiary Designations,” page 3

To change your beneficiary designation, contact BP Retirement Services.

* “Accessing Additional Resources,” page 41

Payments To Your Beneficiary

If you die, BP Retirement Services should be notified as soon as possible.

* “Accessing Additional Resources,” page 41

As long as your account balance exceeds $5,000, your beneficiary can:

z leave the account balance in the plan until the end of the fifth calendar year following your date of death; or

z take an immediate lump-sum distribution.

Installment or partial distributions are not permitted.

* “Beneficiary Designations,” page 3

Your beneficiary may elect to:

z make exchanges between investment options;

z pay off any outstanding loan in full to avoid having it treated as a defaulted loan; or

z request a rollover of your account balance. The IRS rules governing a rollover vary depending on whether your beneficiary is your spouse or someone other than your spouse. Special rules apply to a rollover; consult your tax advisor.

— Your surviving spouse beneficiary may directly roll over your account balance to a tax-qualified plan or an IRA

— Your non-spouse beneficiary may elect a direct trustee-to-trustee rollover to an IRA.

Other than the elections above, your beneficiary has no other rights or options under the BP Solar and Wind ESP. For example, he/she may not take a loan or choose to delay payment of benefits beyond the fifth calendar year following the date of your death. If no distribution election is received by the end of the 5-year period, a lump-sum payment will automatically be made to your beneficiary.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n22

z If you were not vested in your account when you left the company, the treatment of your prior service depends on how long you were away from the company.

— If your absence from employment was less than one year, there is no break in service, and the time you were absent will be recognized by the plan for vesting purposes.

— If your break in service was at least one year but less than seven years, all of your prior years of service will be counted toward vesting in your company match contributions after you return to the company.

— If your break in service was seven years or more, none of your prior service will be counted for vesting purposes, and you will begin earning vesting service again on your rehire date.

Restoring Forfeitures

If all or a part of your company match contribution source was previously forfeited because you left the company before you were fully vested, in some cases the forfeited amount may be restored to your account. In general, if you are rehired and had previously forfeited all or a portion of your company match contribution source, your previously forfeited amounts will be restored to your BP Solar and Wind ESP account if your absence was less than seven years.

The amount restored will be the amount that was originally forfeited, without any adjustment for investment gains or losses since the date of forfeiture.

What Happens If You Are Rehired

If you leave the company and are later rehired as an eligible employee, you will be automatically enrolled at 7% on a before-tax basis as soon as administratively possible starting with your first paycheck on or after your 30th day of employment. If you do not want to participate, you can change your contribution rate to 0% within the first 30 days of your employment, or you can adjust your contribution rate to any whole percentage between 1% and 80%, as appropriate for you. Unless you choose a different investment option, you savings plan account will be invested in the Solar/Wind Target Date Fund nearest to your retirement date (assumed to be age 65). To enroll online or by phone contact BP Retirement Services.

* “Accessing Additional Resources,” page 41

However, some special rules apply for calculating your vesting service after you have been rehired. If all or a part of your company match contribution source was previously forfeited because you left the company before you were fully vested, in some cases the forfeited amount may be restored to your account.

* “Restoring Forfeitures,” at right

Calculating Your Service After Rehire

In general:

z If you were 100% vested in your account when you left, you will be 100% vested after your return, regardless of your service.

z If you were at least partially vested in your account when you left the company, all of your prior service will be recognized by the plan for vesting purposes, regardless of how long you were gone.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n 23

What Happens If You Are No Longer Eligible To Participate Due To a Transfer

If you are no longer eligible to participate in the plan due to a transfer to a related company, you will no longer be eligible to contribute to the plan.

* “Who Is Eligible,” page 2

Your service after the transfer will continue to count toward vesting service if you are not already 100% vested.

* “Vesting,” page 13

If you are currently a participant in the BP Solar and Wind ESP and become eligible for a different savings plan administered by BP Retirement Services, you will need to make new contribution percentage, investment and beneficiary elections.

Your current account balance will remain in the BP Solar and Wind ESP, unless you choose to transfer it to your new plan. You may arrange to have your BP Solar and Wind ESP account balance transferred to your new plan by contacting BP Retirement Services.

* “Accessing Additional Resources,” page 41

If you elect a transfer, you may transfer your account to the same investment options and contribution sources in your new plan, if available. If your investment elections cannot be transferred to your new plan, your new employee contributions will be invested in the applicable Target Date Fund for you based on an estimated retirement age of 65. You may transfer your account balance or change your investment elections at any time.

What Happens If You Take a Qualified Military Leave of Absence

If you are on a qualified military leave, upon your return you may make up any missed contributions. You will receive the full company match you would have received while you were on a qualified military leave, reduced by any match you did receive during that time.

The company match resumes automatically for current contributions. From the date of reemployment, you have the lesser of five years or three times the period of military service to repay the missed contributions. You will receive a letter with more details when your return from military leave.

If you are on a qualified military leave, you will earn vesting service credit for your entire absence from work, as long as you return to work within the time period prescribed by law.

If you were called to active duty for more than 30 days, you may be eligible to elect a distribution of all or a part of your vested account. A 10% early withdrawal penalty will apply if you are younger than 59½ and you will not be permitted to make contributions to the plan for six months after the distribution.

The Plan Administrator may ask you to show that you have been engaged in military service.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n24

If You Die or Become Disabled While on a Qualified Military Leave of Absence

If you die or become disabled (as determined under BP’s long-term disability plan) while on a qualified military leave, you will receive a company match determined on the basis of your contributions made during the 12 months prior to the beginning of your qualified military leave.

If you die while on a qualified military leave, you will become 100% vested in your account. If you become disabled while on a qualified military leave, you will receive vesting service credit for the time you were on a qualified military leave prior to becoming disabled.

When You Leave the CompanyWhen your employment with the company ends, you have several options to consider. You may request a distribution of your vested benefit in the BP Solar and Wind ESP, or, in certain circumstances, you may defer receipt of your account balance. To request a distribution, contact BP Retirement Services at Fidelity.

Automatic Distribution or Rollover of Account Balance Valued at $5,000 or Less

If your vested account balance is valued at $5,000 or less when you leave the company or at any time after you leave (as determined during a quarterly review of your account value), and you do not initiate a full distribution or rollover within 90 days of your separation date, your vested account balance will automatically be paid to you as a lump sum distribution (if your account balance is valued at $1,000 or less) or rolled over to an IRA at Fidelity (if your account balance is valued at greater than $1,000 but not more than $5,000). This could happen even if your account had been previously valued at $5,000 or more and you chose to defer your distribution.

You may roll over this one-time lump sum payment directly into an Individual Retirement Account (IRA), another tax-qualified plan or an eligible employer plan.

If you receive a minimum required distribution or begin receiving installment payments, you should not automatically receive a lump sum distribution.

If you do not initiate a rollover or distribution, your lump sum benefit will be paid out as follows.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n 25

Benefits Valued at Greater Than $1,000 But Not More Than $5,000

The Internal Revenue Code (IRC) requires that your lump sum payment be rolled over into a qualified IRA which will defer taxes until you choose to withdraw your distribution.

The lump sum will be rolled over into a Fidelity Rollover IRA in your name and will be invested in the Fidelity Cash Reserves Fund (FDRXX), a money market vehicle designed to preserve principal and provide a reasonable rate of return and liquidity. The Cash Reserves Fund investment management fees will be charged to your IRA and will not be paid by BP or the plan(s).

If one of these IRAs is established for you, Fidelity will provide you information about your account. No further benefits will be payable from the plan.

To learn more about this IRA, call BP Retirement Services at Fidelity.

* “Accessing Additional Resources,” page 41

Benefits Valued at $1,000 or Less

If your vested account balance is valued at $1,000 or less, a check for the entire amount of the lump sum will be sent to you with the required 20% federal income tax withheld. Additional state taxes will also be withheld, if applicable. No further benefits will be payable from the plan.

Requesting a Distribution

When your employment with the company ends, you will receive an BP Solar and Wind ESP distribution kit. You will need to decide how your distribution will be made and when distribution will begin. The distribution options you have will depend on the amount of your vested benefit:

z If your vested benefit is valued at $5,000 or less:

— your distribution will be made as described in the previous section; or

— you may take advantage of another option, such as a direct rollover of your vested benefit (without taxes being withheld) into another tax-qualified plan or IRA that accepts rollovers.

* “Automatic Distribution or Rollover of Account Balance Valued at $5,000 or Less,” page 24

z If your vested benefit is valued at over $5,000, you have several options for your account:

— deferring your distribution (however, the law requires that you begin receiving distributions by a certain date);

— an immediate lump-sum distribution;

— installment payments; or

— a partial withdrawal.

* “Lump-Sum Distributions,” page 26; “Rollover Distributions,” page 26; “Installment Payments,” page 27; “Deferring Your Distribution,” page 28; “Partial Withdrawals,” page 28; “Accessing Additional Resources,” page 41

Minimum Required Distributions

By law, you must start receiving your vested BP Solar and Wind ESP account no later than April 1 of the year following the calendar year in which you reach age 70½. Additional required distributions must be made by December 31 of each year thereafter.

Your minimum required distribution amount for each year is generally calculated by dividing your account balance (as of December 31 of the preceding calendar year) by your life expectancy or the joint life expectancies of you and your beneficiary.

If you do not specify that this calculation be based on the joint life expectancy, your calculation will be based on your life expectancy only. Joint life expectancy is the total number of years, based on statistical averages, that two people of specified ages are expected to live.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n26

Lump-Sum Distributions

If your BP Solar and Wind ESP vested account balance is valued at $5,000 or less and you do not initiate a full distribution or rollover within 90 days of your last day of employment, your account balance will be automatically distributed to you in a lump sum or rolled over to an IRA as previously described.

If your vested account balance is over $5,000, you may request a lump-sum distribution at any time.

A lump-sum distribution will be made in cash. Your lump-sum benefit will be paid to you as soon as administrative procedures allow.

Rollover Distributions

In general, distributions from the plan are eligible for rollover into another tax-qualified plan or IRA that accepts rollovers. Roth 401(k), Roth 401(k) rollover and Roth in-plan conversion contributions may only be directly rolled over to a Roth elective deferral account under a tax-qualified retirement arrangement or a Roth IRA. Contact BP Retirement Services at Fidelity for more information.

When you roll over part or all of a distribution, you postpone income taxes on the amounts rolled over until you withdraw them. This can provide substantial tax savings if you are in a lower tax bracket when you receive your distribution.

A Special Tax Notice Regarding Plan Payments with more information on rollovers from the plan is available from BP Retirement Services at Fidelity.

* “Accessing Additional Resources,” page 41

c

There are two ways to roll over your plan benefits to another tax-qualified plan or IRA:

z Direct rollover — You instruct the Plan Administrator to pay all or part of your eligible distribution directly to the trustee or administrator of the other plan. No taxes are withheld from a direct rollover. Any non-taxable portion of your distribution (after-tax contributions) you want to roll over must be made via a direct rollover.

z Indirect rollover — You receive a check for the distribution (payable to you) and you choose to roll part or all of the eligible distribution into another plan or IRA within 60 days of the date of receipt. Mandatory federal (and, in some cases, state) tax withholding applies to all indirect rollovers. You may not make an indirect rollover of non-taxable distributions (after-tax contributions).

Because taxes have been withheld, you may want to replace the amount withheld with money from another source, so you will not incur income taxes on the amount withheld.

If you have Roth 401(k), Roth 401(k) rollover or Roth in-plan conversion contributions and are entitled to a distribution from the plan, you may roll over your Roth 401(k) accounts to a Roth IRA or to another qualified retirement plan that accepts Roth 401(k) contributions, but you may not roll over your Roth 401(k) account to a regular IRA. The rules regarding rollovers of Roth 401(k) accounts are complicated; please contact your tax advisor.

B P So l a r a n d W i n d E m p l o y e e S a v i n g s P l a n 27

You are responsible for following all the guidelines and deadlines that apply to the rollover in order to ensure that your distribution is not ultimately taxable.

The distribution kit you’ll receive when you leave the company has instructions for requesting a rollover distribution.

Installment Payments

When your employment with the company ends, you may receive your BP Solar and Wind ESP vested benefit as installment payments — a series of payments made over time — but only if your vested benefit is more than $5,000. Installments may be paid monthly, quarterly or annually. You may change the frequency of these payments — for example, from monthly to annual, or vice versa — one time per year after you have made your initial election.

Each installment must be at least $50, and payments will be made only in cash. You may also request partial withdrawals while your installments continue.

* “Partial Withdrawals,” page 28

If you choose this payment option, contact BP Retirement Services at Fidelity.

* “Accessing Additional Resources,” page 41

How Installment Payments Are Calculated

You may request any amount or percentage. However, your payments must be completed over a period of time that is less than or equal to the combined life expectancies of you and your designated beneficiary.

You may choose from three different payment approaches: