BOTSWANA ECONOMY: RECENT DEVELOPMENTS AND...

60

BOTSWANA ECONOMY: RECENT DEVELOPMENTS AND PROSPECTS Keith Jefferis – August 15 th , 2016

Transcript of BOTSWANA ECONOMY: RECENT DEVELOPMENTS AND...

BOTSWANA ECONOMY: RECENT DEVELOPMENTS AND PROSPECTS

Keith Jefferis – August 15th, 2016

Contents

¨ Structure of economy ¤ Growth drivers; mining/non-mining

¨ External account ¤ Exports, imports, balance of trade ¤ Exchange rates

¨ Money & prices ¤ Inflation & interest rates

¨ Fiscal accounts ¤ Revenues, spending & budget balance; savings

¨ Banking/financial sector ¤ Credit growth, profitability, liquidity.

¨ Employment, poverty etc ¨ Economic Prospects

Economic Structure & Growth

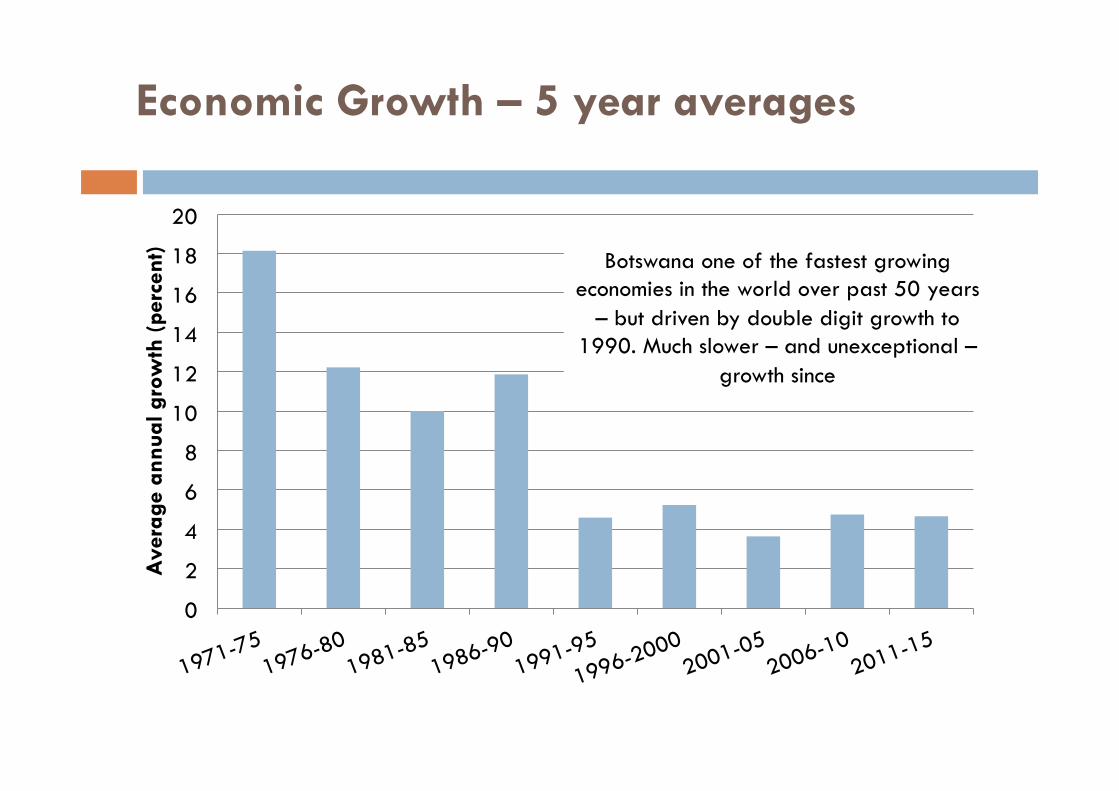

Economic Growth – 5 year averages

0

2

4

6

8

10

12

14

16

18

20

Ave

rage

ann

ual g

row

th (

perc

ent) Botswana one of the fastest growing

economies in the world over past 50 years – but driven by double digit growth to

1990. Much slower – and unexceptional – growth since

Long-term structural change

0%

20%

40%

60%

1966

71

/72

75/7

6 78

/79

81/8

2 84

/85

87/8

8 90

/91

93/9

4 19

96

1999

20

02

2005

20

08

2011

20

14

Mining

0%

20%

40%

60%

1966

71

/72

75/7

6 78

/79

81/8

2 84

/85

87/8

8 90

/91

93/9

4 19

96

1999

20

02

2005

20

08

2011

20

14

Agriculture

0% 5%

10% 15% 20% 25%

1966

71

/72

75/7

6 78

/79

81/8

2 84

/85

87/8

8 90

/91

93/9

4 19

96

1999

20

02

2005

20

08

2011

20

14

Manuf, Constr. Utilities

0% 10% 20% 30% 40% 50%

1966

71

/72

75/7

6 78

/79

81/8

2 84

/85

87/8

8 90

/91

93/9

4 19

96

1999

20

02

2005

20

08

2011

20

14

Services (excl. govt.)

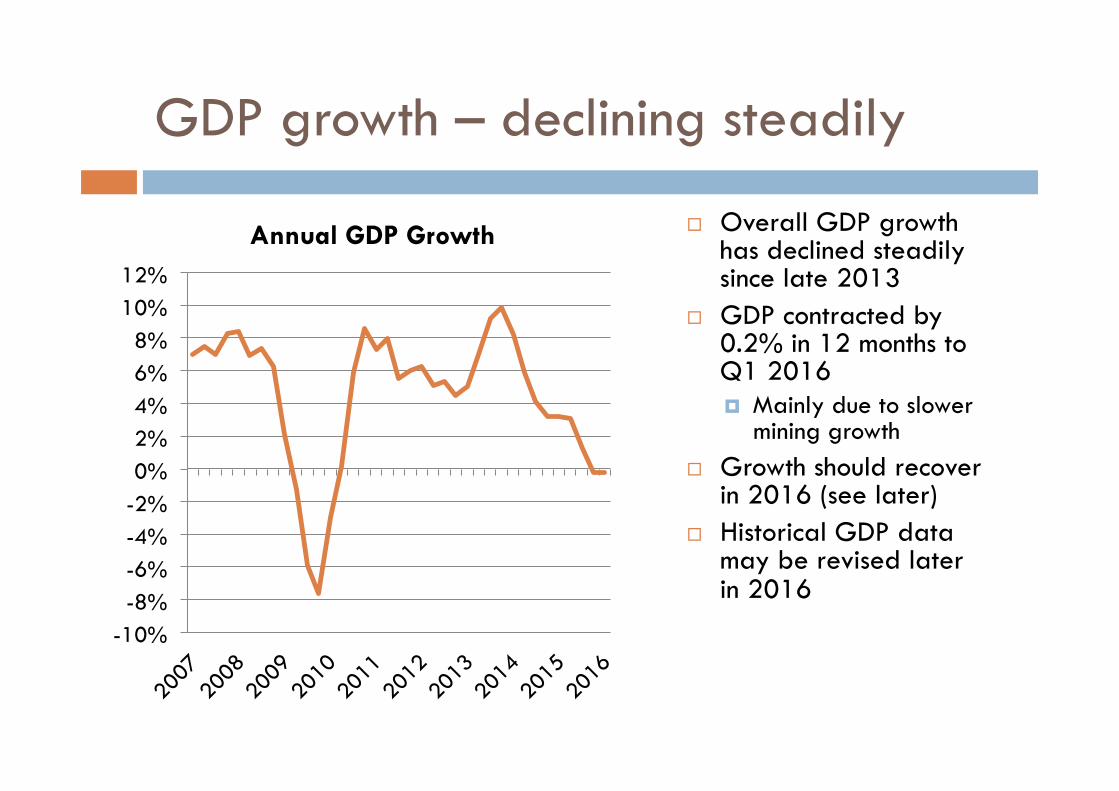

GDP growth – declining steadily

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8%

10% 12%

Annual GDP Growth ¨ Overall GDP growth has declined steadily since late 2013

¨ GDP contracted by 0.2% in 12 months to Q1 2016 ¤ Mainly due to slower

mining growth ¨ Growth should recover

in 2016 (see later) ¨ Historical GDP data

may be revised later in 2016

Mining the main reason for lower growth

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30% Annual GDP Growth

Mining NMPS-VA

¨ In March 2016: ¤ Annual growth of

mining was minus 21.4%

¤ NMPS was the main driver of growth, at 3.9%

¤ NMPS growth is steady, but is offset by significant mining contractions

Sectoral growth: services still the main driver

-64%

-21%

Water & Elec.

Mining

Agriculture

Total VA

Manuf

Construction

Soc. & Pers. Serv.

Govt

Fin. & Bus. Serv.

Trans. & Comm.

Trade etc ¨ Mixed picture across sectors

¨ Strongest growth in various services sectors

¨ Relatively weak performance in primary/secondary sectors

Source: Stats Botswana

Economic structure – increasingly diversified

Agric 2%

Mining 20%

Manuf 6%

Water & elec 0%

Construc-tion 7% Trade etc

18% Transp. & comms

7%

Fin. & bus. Serv. 16%

Govt 17%

Soc & pers. Serv.

7%

¨ Mining less than one quarter of national output (value added) – 20% in 2015

¨ Economy is more diversified – in terms of production – than is often recognised

¨ Has been becoming more diversified over time

¨ Services now almost 50% (47% in 2015)

Agriculture

Live Stock 63%

Crops 11%

Other 26%

Share of Output – 2015

-6 -5 -4 -3 -2 -1 0 1 2 3 4

Live Stock

Crops Other Agric

perc

ent

Annual Growth Rates

2014 2015

Unstable performance of sub-sectors; weak policy environment; BMC – highly politicised, reforms difficult Other policies – focused on social welfare not commercialisation

Mining

Diamonds 81%

Copper 10%

Coal 0.8%

Soda Ash 3%

Prospecting 3%

Other 2%

Share of Output – 2015

14.2

-40 -35 -30 -25 -20 -15 -10 -5 0

perc

ent

Annual Growth Rates

2014 2015

Overall performance still driven by diamonds; copper-nickel performing badly

Manufacturing

Meat etc 16% Beverage

s 13%

Textiles 3%

Tanning &

Leather 0.3%

Other Manuf 68%

Share of Output – 2015

-10 -8 -6 -4 -2 0 2 4 6 8

10

perc

ent

Annual Growth Rates

2014 2015 Poor data – no breakdown of “other”; doesn’t include diamond cutting yet; textiles highly volatile..

Construction – conflicting data signals

-15% -10% -5% 0% 5%

10% 15% 20% 25% 30% 35% 40%

2007

20

08

2009

20

10

2011

20

12

2013

20

14

2015

20

16

Ann

ual G

row

th

Cement Imports (vol.)

Construction Output (real)

¨ Construction activity has slowed sharply, although still positive growth as recorded by GDP data

¨ Cement import data shows sharper slowdown and negative growth, but more of a recent recovery

¨ Lack of major government projects squeezes whole industry

¨ No sign of ESP impact yet

Services (excl. govt)

Whole-sale 4%

Retail 13%

Hotels & Rest. 15%

Petrol Stn 2.2%

Vehicle deal. 3%

Road 2%

Rail 1%

Air 1%

Communic.

6%

Banks 8%

Insurance 3%

Real Est. 3%

Business Serv. 13%

Other 26%

Share of Output – 2015

-15%

-10%

-5%

0%

5%

10%

15%

Who

lesa

le

Reta

il H

otel

s &

Res

t. Pe

trol S

tn

Vehi

cle

deal

. Ro

ad

Rail

Air

Com

mun

ic.

Bank

s In

sura

nce

Real

Est

. Bu

sines

s Se

rv.

Oth

er

Annual Growth Rates

2014 2015 NB does not fully reflect diamond-related services, e.g.

DBGSS and ODC not yet included

Where is growth coming from?

-6% -4% -2% 0% 2% 4% 6% 8%

10%

Avg. real growth, 2005-15 ¨ Botswana increasingly services driven

¨ Is that growth sustainable, with strong domestic focus?

¨ Long-term services growth will depend on: ¤ Services exports (e.g.

tourism, some business services)

¤ External (regional/international) investment

Sources of growth 2005-2015 – also diversified

-30%

-20%

-10%

0%

10%

20%

30%

Con

tribu

tion

to o

vera

ll VA

gro

wth

External Sector

Exports & Imports – weak performance in 2015H2 but recovery in 2016

¨ Both exports and imports volatile due to impact of diamond aggregation – diamonds now the largest import as well as largest export

¨ Softening of minerals prices (copper, diamonds) as well as Chinese economic slowdown negatively affected mineral exports in second half of 2015

¨ Import bill benefitting from lower international fuel prices

¨ Diamond slowdown apparent in both imports and exports

¨ Strong diamond recovery in Q1 2016

0 2,000 4,000 6,000 8,000

10,000 12,000 14,000 16,000 18,000 20,000 22,000

P m

illio

n/qu

arte

r

Exports Imports

Global Diamond Market - DBGSS sights

0

100

200

300

400

500

600

700

800

900

1000

US$

mill

ion

¨ Dismal H2 2015 apparent in De Beers total sales figures ¤ Price margins between polished and

rough diamonds very narrow ¤ Limited purchasing by cutters &

polishers ¤ Weak final demand (mainly

jewellery) ¤ Diamond pipeline not flowing ¤ Debswana forced to cut production in

response

¨ Strong recovery in 1st 5 sights of 2016 (to June) ¤ Averaging over $600m ¤ Enabling stocks accumulated in 2015

to be sold ¤ Cautious optimism about recovery ¤ Production not yet increased to higher

levels – guidance of 20mcts for 2016 remains, unchanged from 2015

Diamond Exports (Rough, Polished & Re-exports)

-5,000

0

5,000

10,000

15,000

20,000

P m

illio

n

Rough Polished Re-exports

¨ Diamond exports of rough diamond increased drastically in 2016 ¤ From P1,198 at the

end of 2015 to P9,130 in March

¨ Other categories of diamond exports (polished and re-exports) declined in Q1 2016

¨ Botswana is the “swing” producer – sales of BW rough dropped faster than total sales

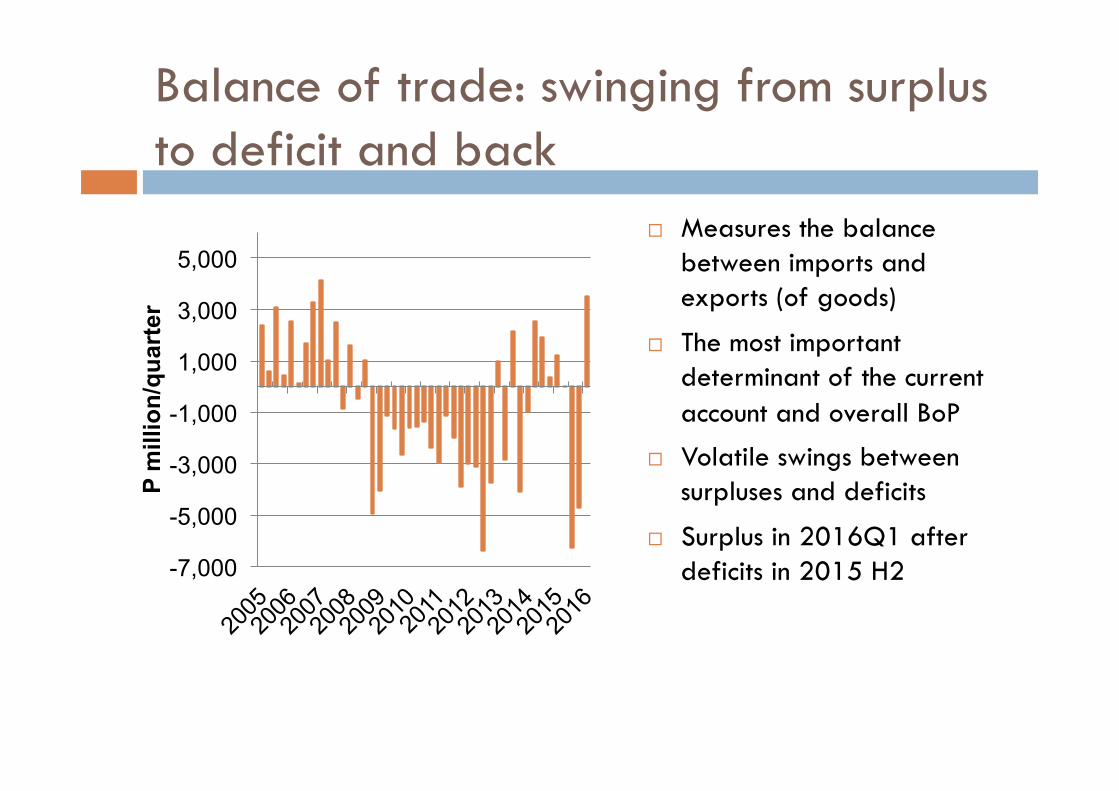

Balance of trade: swinging from surplus to deficit and back

¨ Measures the balance between imports and exports (of goods)

¨ The most important determinant of the current account and overall BoP

¨ Volatile swings between surpluses and deficits

¨ Surplus in 2016Q1 after deficits in 2015 H2

-7,000

-5,000

-3,000

-1,000

1,000

3,000

5,000

P m

illio

n/qu

arte

r

Composition of exports

Diamonds still dominate – but services (mainly

tourism) increasingly important

Meat 2%

Soda Ash 1%

Gold 1%

Textiles 1%

Vehicles and parts 1%

Machinery & electrical eq.

4%

Other manufactures 3%

Copper-nickel 7%

Polished Diamonds 8%

Rough Diamonds 48%

Services 24%

Composition of Exports, 2015 (exc. aggregation)

Exchange Rates

¨ Exchange rates dominated by ZAR weakness & volatility

¨ Trend of depreciation vs USD through to early 2016 has been reversed with ZAR strength

¨ ZAR caught up in EM XR weakness / volatility, compounded by SA specific issues

¨ BWP up from lowest ever level vs USD

¨ Small change in rate of crawl in Jan 2016 (to +0.38%) will have little impact

6

7

8

9

10

11

12 1.00

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40

1.45 20

08

2009

2010

2011

2012

2013

2014

2015

2016

ZAR per BWP(LHS) BWP per USD (RHS)

Inflation and Monetary Policy

Inflation ... at unprecedented low levels but has probably bottomed out

0% 2% 4% 6% 8%

10% 12% 14% 16%

2007

20

08

2009

20

10

2011

20

12

2013

20

14

2015

20

16

2017

BoB upper BoB lower

Forecast Inflation

¨ Inflation fell below 6% in June 2013 and has been below the upper end of the BoB range for almost 3 years

¨ At 2.7% in June 2016, inflation is below the lower end of the BoB range.

¨ Main drivers: ¤ Declining international fuel prices ¤ Generally low international inflation ¤ Weak domestic inflationary pressures

¨ Risks: ¤ Water & electricity ¤ Regional food prices

¨ Inflation expected to rise slowly over the next 12 months

¨ Medium-term inflation expectation – around 4%

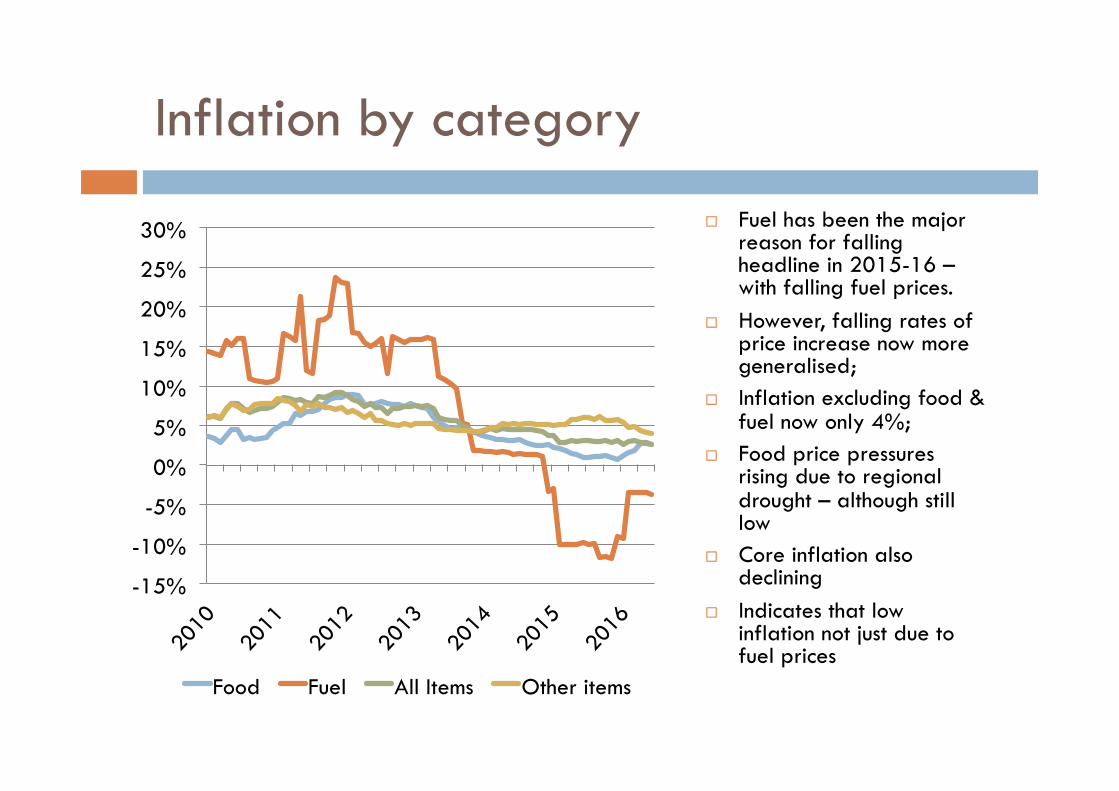

Inflation by category

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Food Fuel All Items Other items

¨ Fuel has been the major reason for falling headline in 2015-16 – with falling fuel prices.

¨ However, falling rates of price increase now more generalised;

¨ Inflation excluding food & fuel now only 4%;

¨ Food price pressures rising due to regional drought – although still low

¨ Core inflation also declining

¨ Indicates that low inflation not just due to fuel prices

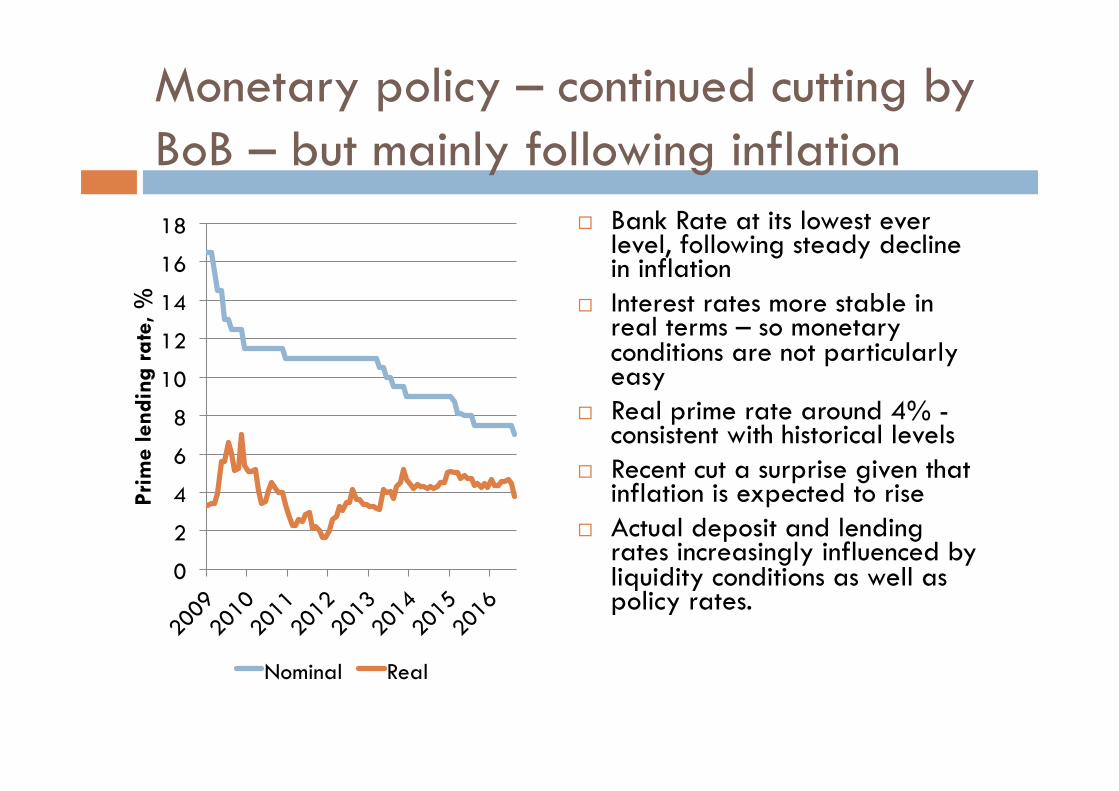

Monetary policy – continued cutting by BoB – but mainly following inflation

0

2

4

6

8

10

12

14

16

18

Prim

e le

ndin

g ra

te, %

Nominal Real

¨ Bank Rate at its lowest ever level, following steady decline in inflation

¨ Interest rates more stable in real terms – so monetary conditions are not particularly easy

¨ Real prime rate around 4% - consistent with historical levels

¨ Recent cut a surprise given that inflation is expected to rise

¨ Actual deposit and lending rates increasingly influenced by liquidity conditions as well as policy rates.

Government Budget

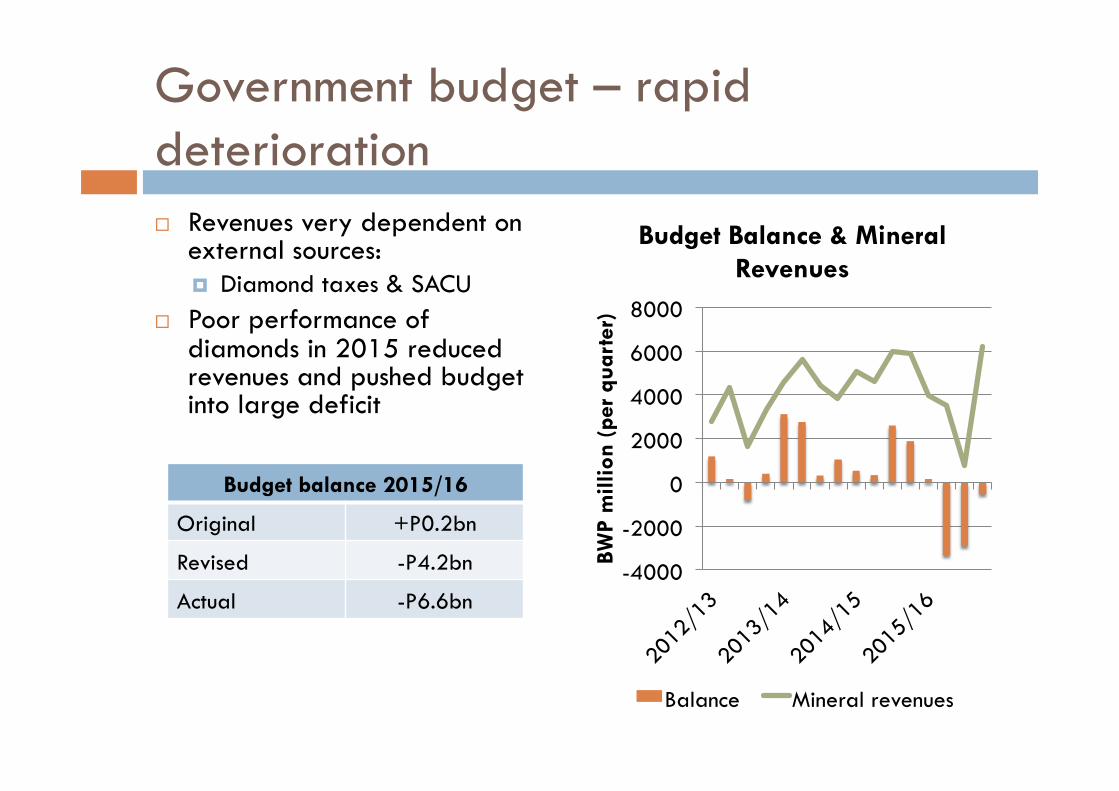

Government budget – rapid deterioration ¨ Revenues very dependent on

external sources: ¤ Diamond taxes & SACU

¨ Poor performance of diamonds in 2015 reduced revenues and pushed budget into large deficit

-4000

-2000

0

2000

4000

6000

8000

BWP

mill

ion

(per

qua

rter

)

Budget Balance & Mineral Revenues

Balance Mineral revenues

Budget balance 2015/16

Original +P0.2bn

Revised -P4.2bn

Actual -P6.6bn

Government budget – entering era of prolonged deficits ¨ Revenues in long-term

decline ¨ Spending also has to be

cut (as % of GDP) ¨ MTEF projects deficits

through to 2018 ¨ Revised projections for

NDP11 suggests deficits throughout

¨ Deficit can be funded but will require both additional borrowing and drawdown of savings

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

2009

20

10

2011

20

12

2013

20

14

2015

20

16

2017

20

18

Perc

ent o

f G

DP

Balance Spending Revenue

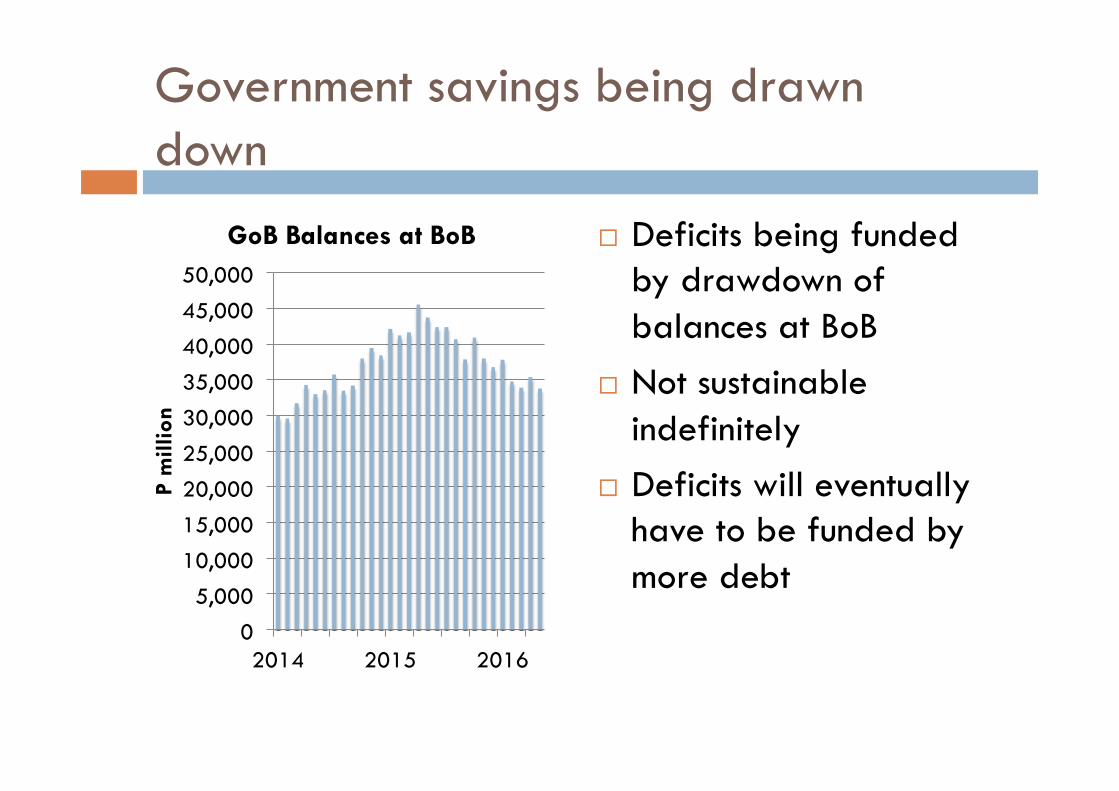

Government savings being drawn down

0 5,000

10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000

2014 2015 2016

P m

illio

n

GoB Balances at BoB ¨ Deficits being funded by drawdown of balances at BoB

¨ Not sustainable indefinitely

¨ Deficits will eventually have to be funded by more debt

How much does government have to finance budget deficits?

¨ Pula Fund: P61.1 billion (December 2015)

¨ o/w GoB share: P35.0 billion (=GIA balance)

¨ Approx. 24% of GDP

¨ Statutory limit: 40% of GDP

¨ Current borrowing: 22% of GDP (March 2016)

¨ In principle, could raise a further 18% of GDP (P27bn)

¨ Commitments to g’tee BCL USD bond will exhaust FX borrowing limit – additional borrowing will have to be in BWP

Financial Assets (Gross) Borrowing Capacity

Pula Fund and GIA have dual purposes: - short-term stabilisation - to provide long-term income once diamonds run out (Fund for Future Generations) - no rules on allocation between two functions - can easily be depleted for short-term gain

NDP 11 – behind schedule

¨ NDP 11 still being finalised ¤ Updating of macro projections, expenditure ceiling ¤ Project list and funding ¤ Co-ordination with Vision 2036

¨ Has been presented to Cabinet ¨ Will be presented to Parliament in Nov/Dec ¨ List of approved development projects will be

crucial

The Banking Sector

Rapidly declining profitability

0%

10%

20%

30%

40%

50%

60%

2003

20

04

2005

20

06

2007

20

08

2009

20

10

2011

20

12

2013

20

14

2015

Return on Equity (post-tax) ¨ Profitability (RoE) has been declining for a long period

¨ Dropped further to 12.5% 2015.

¨ Profits decline due to: ¤ Competition ¤ Saturation of key

market segments ¤ Lower policy interest

rates ¤ Regulatory

interventions

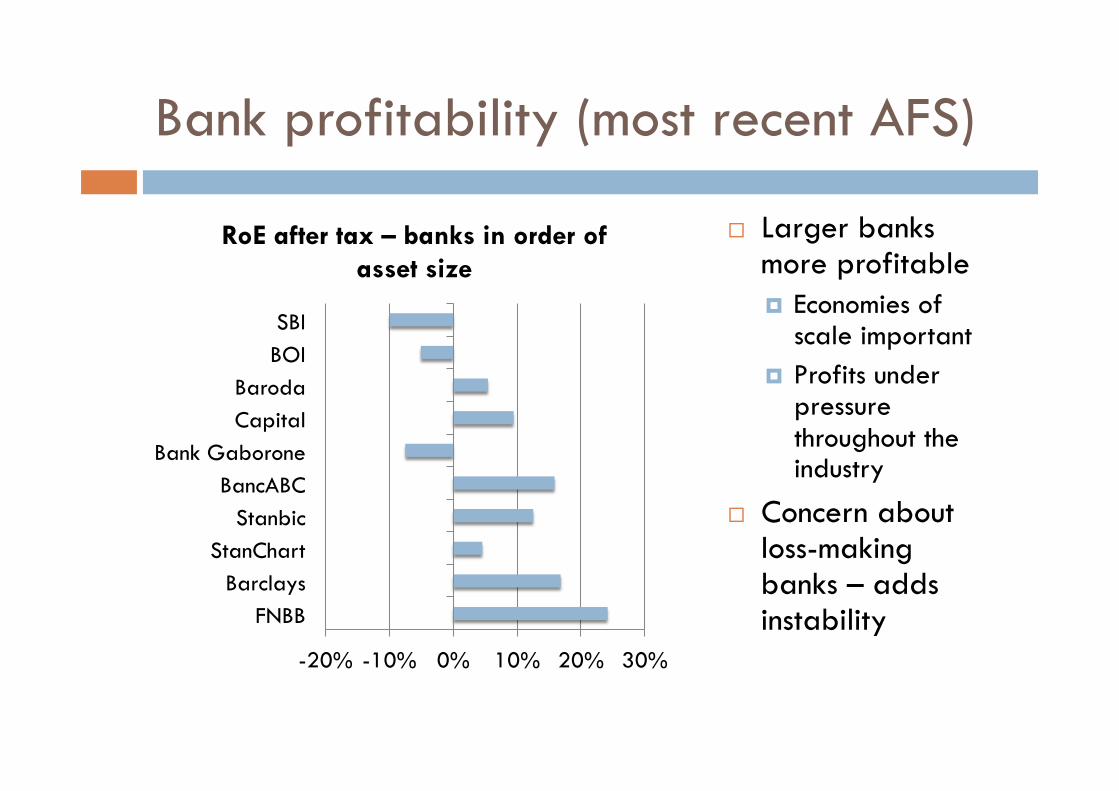

Bank profitability (most recent AFS)

-20% -10% 0% 10% 20% 30%

FNBB Barclays

StanChart Stanbic

BancABC Bank Gaborone

Capital Baroda

BOI SBI

RoE after tax – banks in order of asset size

¨ Larger banks more profitable ¤ Economies of

scale important ¤ Profits under

pressure throughout the industry

¨ Concern about loss-making banks – adds instability

Bank credit: slowdown continues, but stabilised

¨ Overall credit growth declining from early 2012 to May 2016

¨ Decline appears to have bottomed out

¨ Annual growth of 9.7% in May 2016

¨ Comparable to nominal non-mining GDP growth (10.5% in yr to March)

0%

5%

10%

15%

20%

25%

30%

35%

Year

on

year

gro

wth

Bank credit: divergence between household and business credit

¨ Households the main driver of credit growth

¨ Growth in credit to businesses still very weak

¨ Growth in year to May: ¤ Private business:

4.3% ¤ Households:

12.9%

0% 5%

10% 15% 20% 25% 30% 35% 40% 45% 50%

Year

on

year

gro

wth

Arrears on bank credit

0% 1% 2% 3% 4% 5% 6% 7% 8% 9%

10%

Business HH Total

¨ Sharp upturn in arrears in 2016Q1 (but new reporting?)

¨ Across all categories – business & households

¨ Business arrears (March 2016): ¤ Agriculture 13.8% ¤ Manufacturing 1.8% ¤ Construction 8.6% ¤ Trade 4.0% ¤ Real estate 1.9%

Banking environment volatility – especially deposits

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

P m

illio

n

Deposits Lending

¨ Bank deposit base much less stable than lending ¤ BPOPF funds ¤ Parastatals

¨ Reflects maturity differences

¨ Deposit-lending gap highly unstable

Liquidity environment – volatile

0%

2%

4%

6%

8%

10%

12%

14%

Perc

ent o

f to

tal a

sset

s

Excess banking liquid assets

¨ Banking liquidity: ¤ Recovered strongly after

2014 crisis, ¤ Due to regulatory changes

and faster deposit growth ¤ Has since fallen back

somewhat ¤ Has largely stabilized at

manageable level ¤ Banks no longer chasing

deposits with high interest rates

¨ Still concerns that deposit base will prove unstable – hence caution in lending

Payments Trends (volumes)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

No.

of

tran

sact

ions

(‘0

00)

Cheques EFTs

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2006

20

07

2008

20

09

2010

20

11

2012

20

13

2014

20

15

No.

of

tran

sact

ions

(‘0

00)

EFT-POS ATM

Pension Funds

0

10

20

30

40

50

60

70

80 20

04

2005

20

06

2007

20

08

2009

20

10

2011

20

12

2013

20

14

2015

Assets (P bn) Offshore %

¨ Still growing in BWP terms – P74.8bn in 2015

¨ Almost as large as banking system (P76.7bn)

¨ 2015 increase largely driven by exchange rates – steady at just over USD$6bn in recent years

¨ Offshore proportion steady around 60% - unlikely to change dramatically

Labour Market

Formal employment – very slow growth

¨ Very little increase in formal employment in past four years

¨ Average employment growth rate less than 0.5% p.a.

¨ Approx 1,500 new jobs a year

¨ Compares with approx 20,000 net new entrants to the labour force each year

¨ Unemployment officially around 20% but in reality much higher 0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

2014

20

15

Form

al S

ecto

r Em

ploy

men

t

Private Parastatal Govt

Entry to and exit from labour force

New entrants (40k)

Labour Force (26k)

Formal sector (3k) Unemployed,

informal, agric (23k)

Not in LF (14k)

About 6,000 retirees from labour force, releasing around 1,500 formal jobs

Importance of Govt. wage and welfare payments Category Number (‘000) Total Value (per year)

Employees

Employment – private sector 190 12,000

Employment – public sector 150 18,000

Govt Transfer Recipients

Old Age Pensioners* 100 400

WW2 vets*

Destitutes* 32 150

Ipelegeng 60 350

OVC carers* 40 200

Tertiary students 40 600

ISPAAD farmers 130 400

LIMID farmers 18 100

Total welfare recipients 420 2,200

Total Govt Dependents (transfers + employees)

570 20,000

Economic Outlook

Business Confidence % of firms rating current business conditions satisfactory

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

100%

Exporters Non-Exporters All

¨ Volatile confidence levels, especially amongst exporters (small sample?)

¨ Long-term downward trend

¨ No real recovery since global financial crisis

¨ Private sector concerns about water & electricity shortages

Growth forecasts - IMF

-2

0

2

4

6

8

10

12

2012

20

13

2014

20

15

2016

20

17

2018

20

19

2020

perc

ent

Actual Projected

¨ IMF and GoB forecasting a reasonable recovery in 2016 ¤ Diamond market

stability ¤ ESP

¨ Medium-term growth rates of 4-5% (NDP11)

Global Diamond Market

¨ 2015 was very difficult : ¤ Weakening final demand (for jewellery), with global growth slowdown,

especially China ¤ Cutters/polishers squeezed between high rough prices (De Beers) and weak

final demand (cannot pass on high input prices) ¤ Reduction in prices mid-year, with sharp reduction in rough supply in H2 ¤ Enabled excess stock to be run down

¨ First half of 2016 much better ¤ Christmas 2015 season was positive ¤ Re-stocking lifted the market in early 2016 ¤ Pipeline now flowing again, albeit at lower levels

¨ Still high risk and uncertainty ¤ Shortage of financing – Stanchart withdrawal from diamond chain financing ¤ Final demand still weak ¤ Not enough recovery to lift rough production

Botswana diamond industry

¨ Failure of downstream market to recover in mid 2015, and small sights forced Debswana to cut back production (could not continue to stockpile)

¨ 2016 production target cut by 20% from 24 to 20mcts. ¨ Still maintained despite some market recovery ¨ ODC also experienced weak market in 2015, better in 2016 ¨ Mixed picture from small mines

¤ Karowe (Lucara) lifted by large stones ¤ Ghagoo (Gem) struggling – production cut back ¤ Lerala (Kimberley) restarting production

¨ Cutting & polishing still under pressure – employment only half of peak

Domestic growth outlook – balance shifting towards positives ¨ Positive news:

¤ Inflation and interest rates at historic lows, should remain ¤ Fears of large fiscal and BoP deficits in 2015H2 somewhat alleviated ¤ Diamond market stabilised, although not yet recovering ¤ Copper-nickel prices off lows, although still weak ¤ ESP impact on construction, infrastructure ¤ Alleviation of power, water supply problems

¨ Negative news: ¤ Increased global uncertainty; risks mostly on the downside ¤ Regional drought impact on food prices ¤ Regional economies: SA slow growth, Zimbabwe crisis, Zambia downturn ¤ BCL sustainability issues ¤ Ability to implement changes envisaged in NDP 11 & V2036

Regional Expansion – BSE-listed companies Company Industry Country

Letshego Financial Services Uganda, Swaziland, Tanzania, Zambia, Namibia, Mozambique, Kenya, Lesotho, Rwanda, South Sudan*

Turnstar Property Tanzania

Funeral Services Group (FSG)

Consumer Services, Financial Services Zambia, South Africa

Sefalana Retail Zambia, Namibia

PrimeTime Property Zambia

RDCP Property, Tourism Madagascar, South Africa

Choppies Retail South Africa, Zimbabwe, Zambia, Kenya

Chobe Tourism Namibia

Cresta Marakanelo Tourism Zambia

Furnmart Retail South Africa, Namibia, Zambia

Wilderness Tourism Namibia, South Africa, Malawi, Zimbabwe, Zambia, Seychelles, Congo, Kenya

BIHL Financial Services Zambia, Malawi, Mozambique, Tanzania, Uganda, Zambia

Imara Financial Services UK, Malawi, South Africa, Namibia, Zambia, Zimbabwe, Mauritius, Angola, Kenya, Nigeria

Drivers of Regional Expansion

¨ Limits of BW market reached ¨ Mostly services (non-tradeables) – cannot be

exported directly – hence outward FDI needed ¨ Domestic success ¨ Strong management teams ¨ Good business model ¨ BW suited to regional HQ ¨ Capital on balance sheet ¨ Access to competitive loan funding

SSA growth projections 2016-20 (IMF)

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000

0

1

2

3

4

5

6

7

8

9

Swaz

iland

So

uth

Afr

ica

Rep.

of

Con

go

Ang

ola

Seyc

helle

s N

iger

ia

Com

oros

Zi

mba

bwe

Eritr

ea

Cha

d C

abo

Verd

e Le

soth

o M

aurit

ius

The

Gam

bia

Botsw

ana

Buru

ndi

Mal

awi

Gab

on

Mad

agas

car

Cam

eroo

n M

ali

Sier

ra L

eone

Za

mbi

a G

uine

a-Bi

ssau

N

amib

ia

Sout

h Su

dan

Beni

n To

go

Cen

t. A

f. Re

p.

Libe

ria

São

Tom

é D

RC

Gui

nea

Burk

ina

Faso

U

gand

a G

hana

Ke

nya

Tanz

ania

N

iger

Et

hiop

ia

Rwan

da

Sene

gal

Moz

ambi

que

Côt

e d'

Ivoi

re

GD

P/ca

pita

(U

SD)

2015

Ave

rage

ann

ual g

row

th

Average 2016-20 GDP/cap SADC countries In brown

Macroeconomic Forecasts (Econsult)

2016 2017

GDP growth (real) 3.2% 3.1%

- mining -2.0% 2.0%

- non-mining 4.1% 3.3%

Govt. spending growth (real)

0% 0%

Bank rate (eoy) 5.5% 6.0%

Inflation rate (eoy) 3.5% 4.2%

BWP per USD 10.5 ..

ZAR per BWP 1.33 ..

Economic Stimulus Package

¨ Not much public information has been provided, other than what is contained in the initial transcript, and brochure listing broad ESP initiatives

¨ Plan will target tourism, manufacturing, farming, building of roads and homes, education and health facilities

¨ Key aspects (in theory): ¤ High impact projects that have substantial ROI ¤ Firm M&E Framework (so as to avoid cost overruns and

delivery of quality products efficiently and effectively)

Economic Stimulus Package - 2

¨ ESP is a medium-term project (3 years), so will take a while to have an impact

¨ Very few “shovel-ready” projects – major new projects need detailed design and specification (e.g. by-passes) or organisational development (SEZs)

¨ Initial ESP projects are those that had already been planned & designed, but postponed due to lack of funds

¨ Some re-packaging of projects that would have happened anyway (e.g. SEZs)

¨ Approx P1.4 bn of ESP money in 2015/16 budget, P2.2bn in 2016/17 budget, which should contribute around 1.5% to GDP growth.

¨ Concerns that proper project appraisal and procurement may be overlooked

Thank You