Bootstrapping Spot Rate

37

Spot Rates, and Forward Rates

description

report

Transcript of Bootstrapping Spot Rate

Spot Rates, and Forward Rates

Theoretical Spot Rates• The theoretical spot rate is the interest rate that should be used to

discount a default-free cash flow.

• Because there are a limited number of on-the-run Treasury securities traded in the market, interpolation is required to obtain the yield for interim maturities; hence, the yield for most maturities used to construct the Treasury yield curve are interpolated yields rather than observed yields.

• Default-free spot rates can be derived from the Treasury yield curve by a method called bootstrapping.

• The basic principle underlying the bootstrapping method is that the value of a Treasury coupon security is equal to the value of the package of zero-coupon Treasury securities that duplicates the coupon bond’s cash flows.

Theoretical Spot Rates“Bootstrapping”

• In order to value default-free cash flows, the theoretical spot rate for Treasury securities must be determined.

• The default-free theoretical spot rate curve is constructed from the observed Treasury yield curve.

• Several techniques are used to create the yield curve; however, the most commonly employed method is called “bootstrapping”

Bootstrapping Spot Rates• Bootstrapping uses the yield for the on-the-run

Treasury issues (since there are no credit or liquidity risks).

– A problem exists because there may be an insufficient number of data points for on-the-run issues to construct a yield curve.

• Issuance of Treasury securities– 3-month, 6-month, 2-year, 3-year, 5-year, and 10-year

notes (the 30-year has recently been reissued)– This leaves gaps in the yield curve which can be filled

in with simple linear interpolation

Bootstrapping Spot Rates• To fill in the gap for each missing one year maturity, it is

possible to start with the lowest maturity and work up to the highest maturity with the following formula:

(yield at higher maturity – yield at lower maturity)

Number of years between two observed maturity points

• The estimated on-the-run yield for all intermediate whole-year maturities is found by adding the amount computed to the yield at the lower maturity.

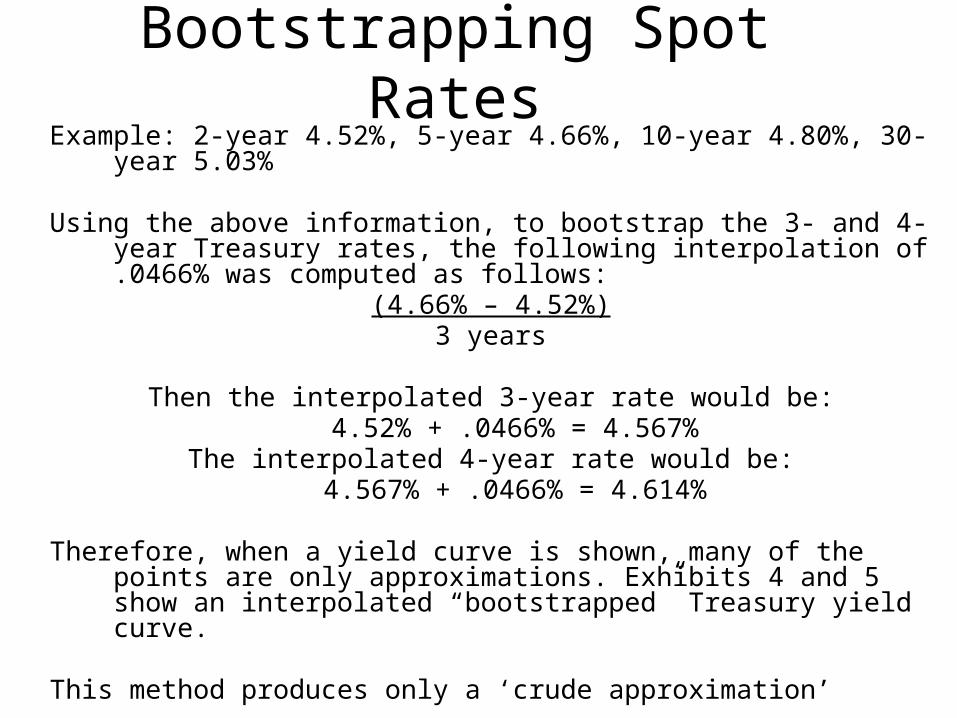

Bootstrapping Spot RatesExample: 2-year 4.52%, 5-year 4.66%, 10-year 4.80%, 30-year 5.03%

Using the above information, to bootstrap the 3- and 4-year Treasury rates, the following interpolation of .0466% was computed as follows:

(4.66% – 4.52%)3 years

Then the interpolated 3-year rate would be:4.52% + .0466% = 4.567%

The interpolated 4-year rate would be:4.567% + .0466% = 4.614%

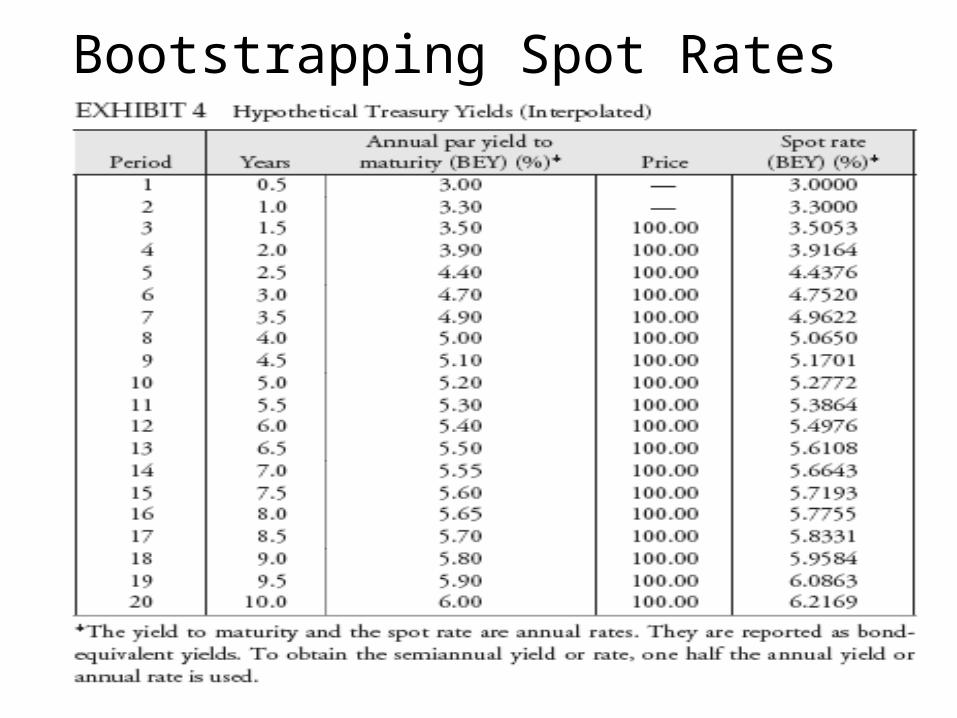

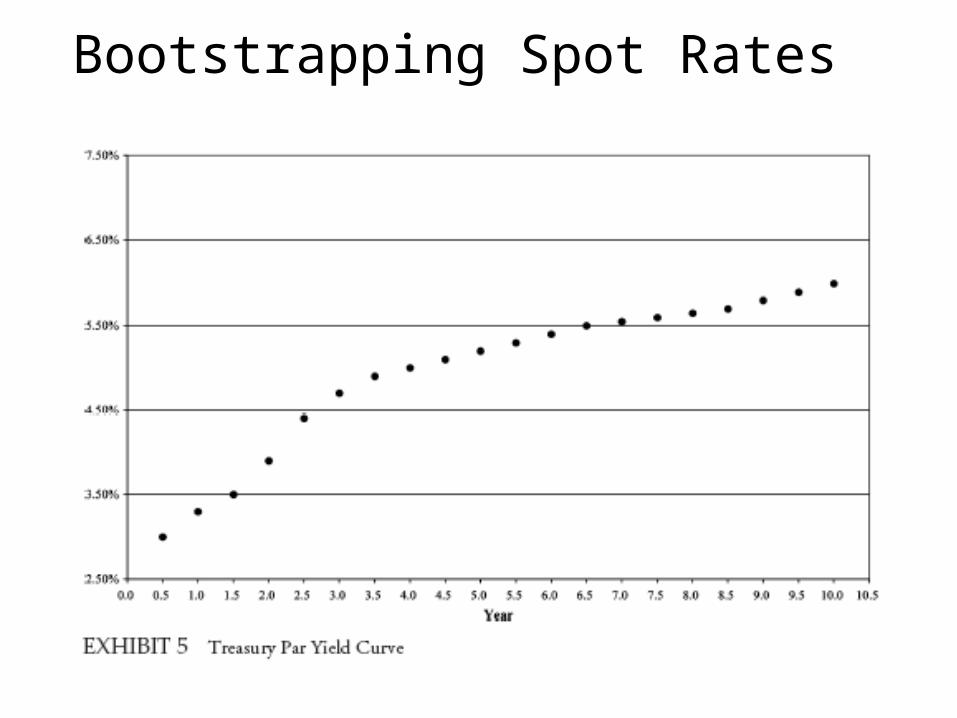

Therefore, when a yield curve is shown, many of the points are only approximations. Exhibits 4 and 5 show an interpolated “bootstrapped” Treasury yield curve.

This method produces only a ‘crude approximation’

Bootstrapping Spot Rates

Bootstrapping Spot Rates

Theoretical Spot Rates• The basic principle is that the value of a Treasury

coupon series should be equal to the value of a package of zero-coupon Treasuries that duplicates the coupon bond’s cash flows.

• Using the arbitrage-free method, it is possible to compute the approximate yield of bonds (spot rates) over any maturity range (including months) and going forward in time.

– These will be more precise that the linear interpolated results from bootstrapping.

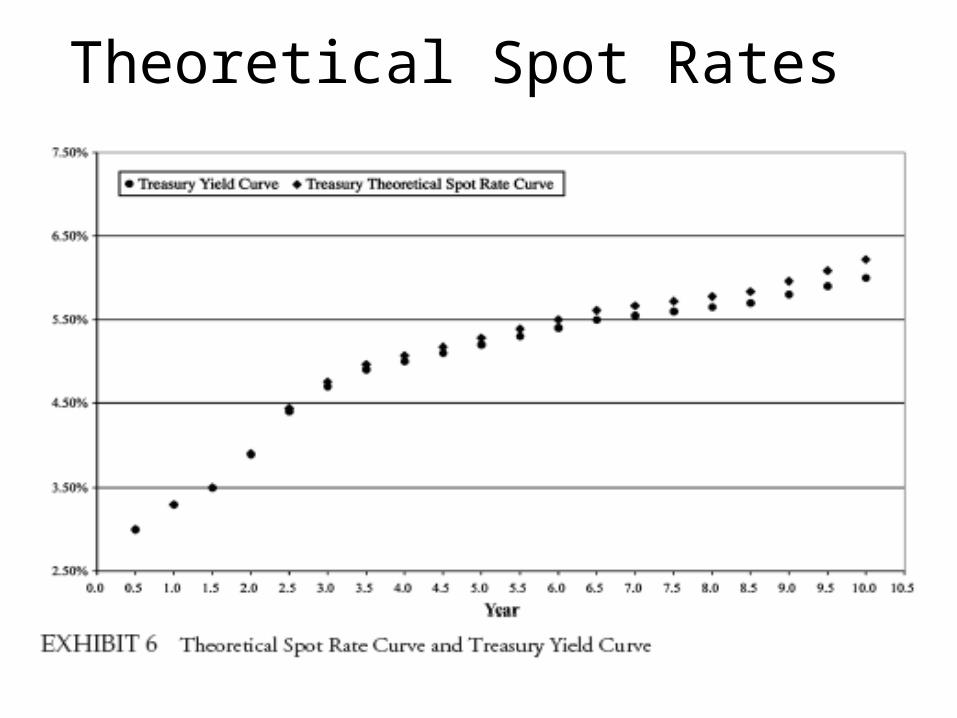

– Exhibit 6 shows the plot of the theoretical spot rates and the par value Treasury yield curve.

Theoretical Spot Rates

Method of Bootstrapping Spot Rates from the Par Yield Curve

1. Begin with the 6-month spot rate.2. Set the value of the 1-year bond equal to the

present value of the cash flows with the 1-year spot rate divided by 2 as the only unknown.

3. Solve for the 1-year spot rate.4. Use the 6-month and 1-yar spot rates and

equate the present value of the cash flows of the 1.5 year bond equal to its price, with the 1.5 year spot rate as the only unknown.

5. Solve for the 1.5 year spot rate.

Example• Consider the yields on coupon Treasury bonds

trading at par (given in the table). • YTM for the bonds is expressed as a bond

equivalent yield (semi-annual YTM).

Par Yields for Three Semiannual-Pay Bonds

Maturity YTM Coupon Price6 months 5.00% 5.00% $100.00

1 year 6.00% 6.00% $100.0018 months 7.00% 7.00% $100.00

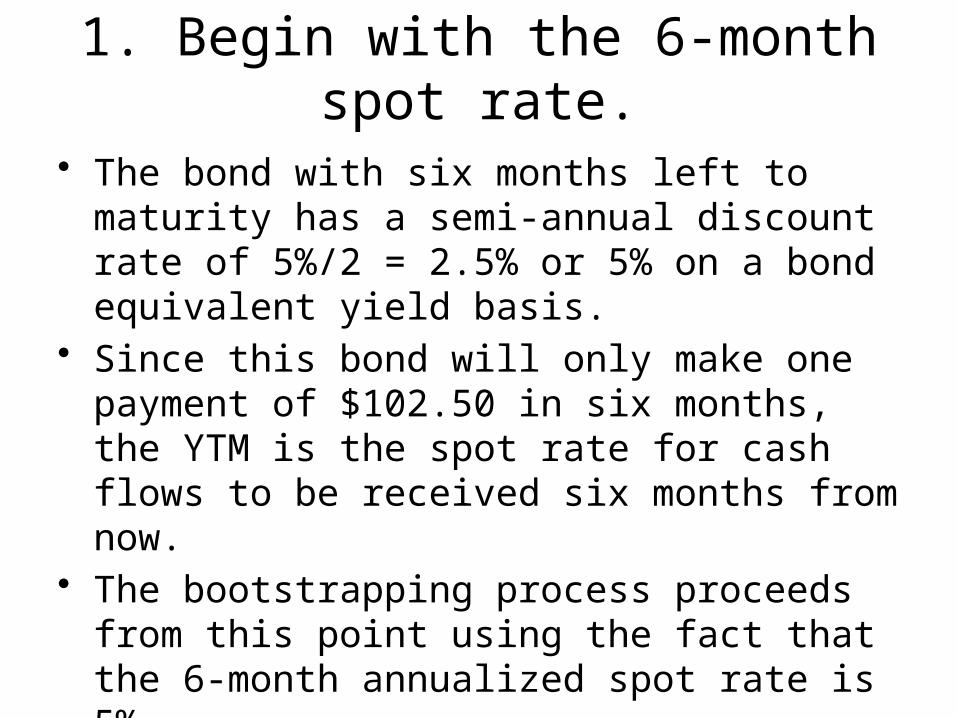

1. Begin with the 6-month spot rate.

• The bond with six months left to maturity has a semi-annual discount rate of 5%/2 = 2.5% or 5% on a bond equivalent yield basis.

• Since this bond will only make one payment of $102.50 in six months, the YTM is the spot rate for cash flows to be received six months from now.

• The bootstrapping process proceeds from this point using the fact that the 6-month annualized spot rate is 5%.

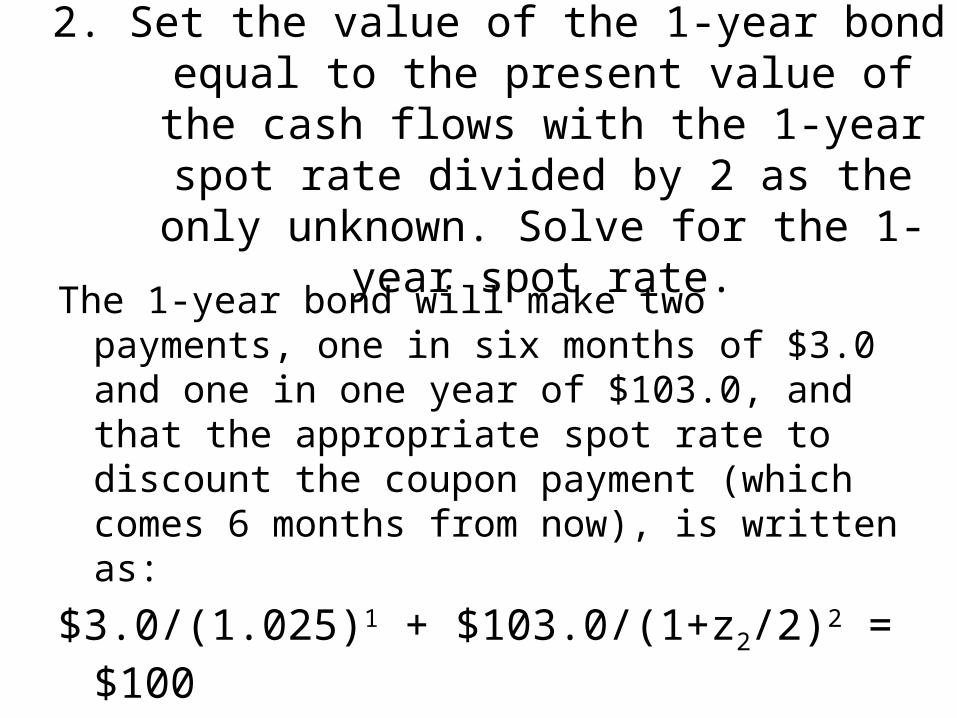

2. Set the value of the 1-year bond equal to the present value of the cash flows with the 1-

year spot rate divided by 2 as the only unknown. Solve for the 1-year spot rate.

The 1-year bond will make two payments, one in six months of $3.0 and one in one year of $103.0, and that the appropriate spot rate to discount the coupon payment (which comes 6 months from now), is written as:

$3.0/(1.025)1 + $103.0/(1+z2/2)2 = $100

where z2 is the annualized 1-year spot rate

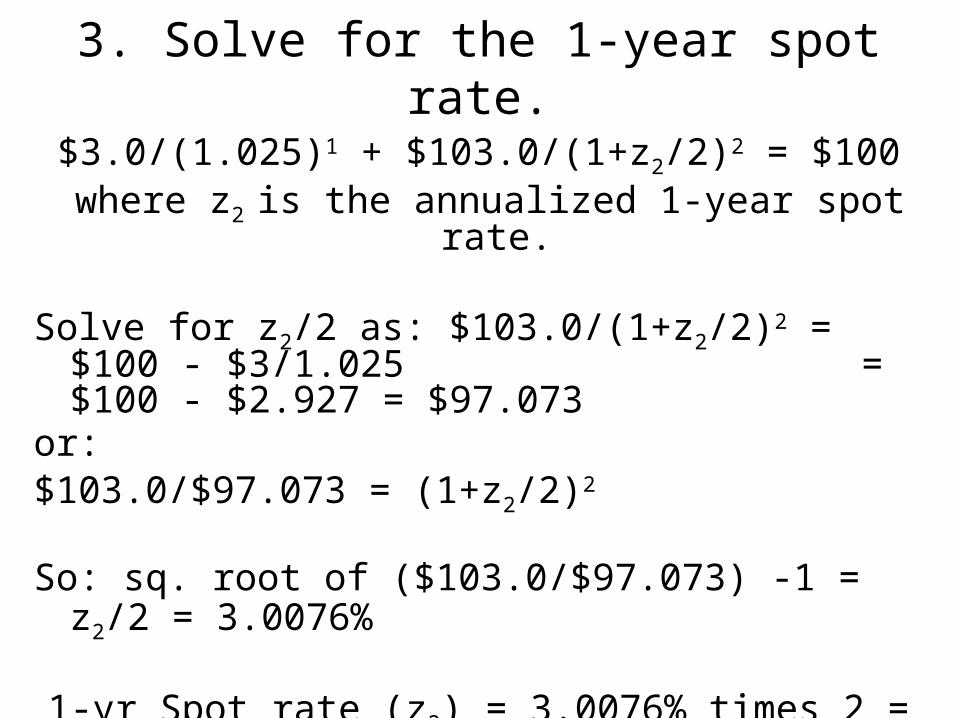

3. Solve for the 1-year spot rate.

$3.0/(1.025)1 + $103.0/(1+z2/2)2 = $100 where z2 is the annualized 1-year spot rate.

Solve for z2/2 as: $103.0/(1+z2/2)2 = $100 - $3/1.025 = $100 - $2.927 =

$97.073or: $103.0/$97.073 = (1+z2/2)2

So: sq. root of ($103.0/$97.073) -1 = z2/2 = 3.0076%

1-yr Spot rate (z2) = 3.0076% times 2 = 6.0152%

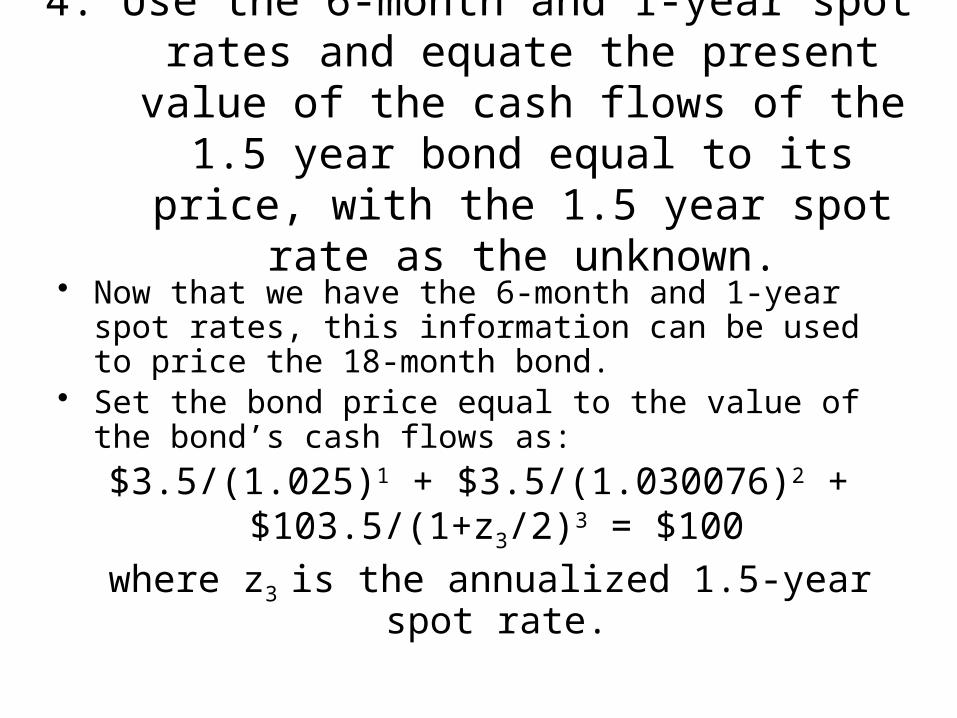

4. Use the 6-month and 1-year spot rates and equate the present value of the cash flows of the 1.5 year bond equal to its price, with

the 1.5 year spot rate as the unknown.

• Now that we have the 6-month and 1-year spot rates, this information can be used to price the 18-month bond.

• Set the bond price equal to the value of the bond’s cash flows as:

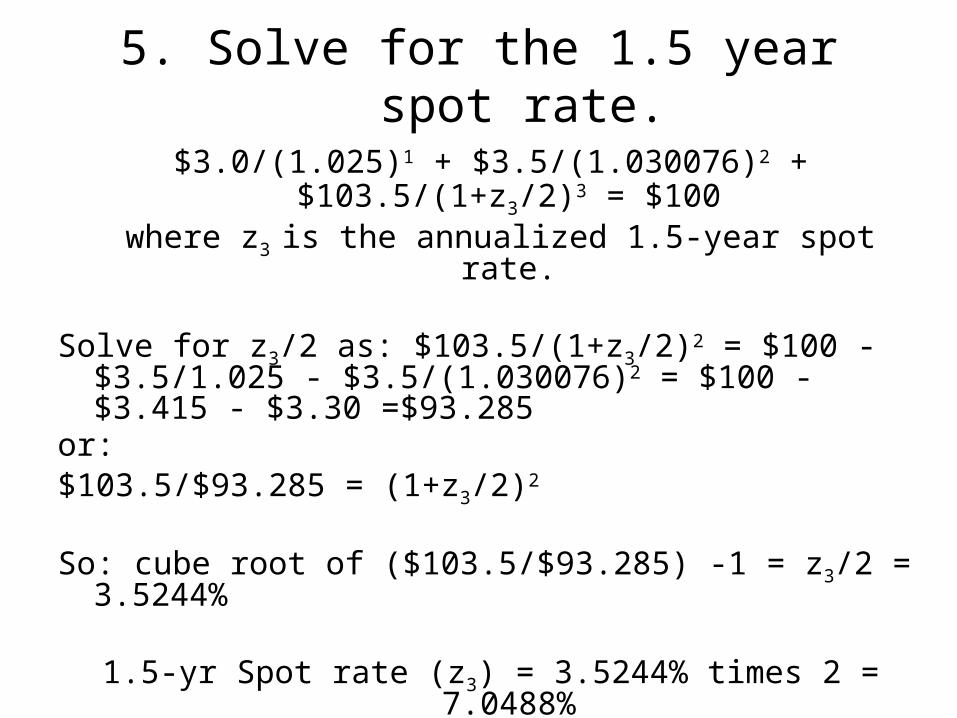

$3.5/(1.025)1 + $3.5/(1.030076)2 + $103.5/(1+z3/2)3 = $100

where z3 is the annualized 1.5-year spot rate.

5. Solve for the 1.5 year spot rate.

$3.0/(1.025)1 + $3.5/(1.030076)2 + $103.5/(1+z3/2)3 = $100 where z3 is the annualized 1.5-year spot rate.

Solve for z3/2 as: $103.5/(1+z3/2)2 = $100 - $3.5/1.025 - $3.5/(1.030076)2 = $100 - $3.415 - $3.30 =$93.285

or: $103.5/$93.285 = (1+z3/2)2

So: cube root of ($103.5/$93.285) -1 = z3/2 = 3.5244%

1.5-yr Spot rate (z3) = 3.5244% times 2 = 7.0488%

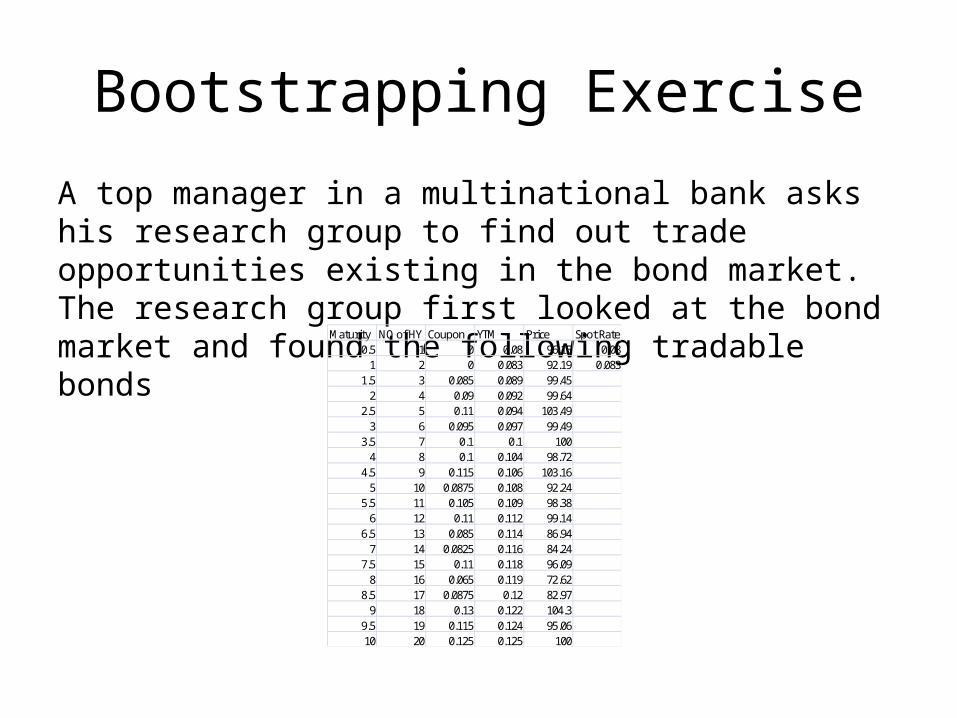

Bootstrapping Exercise

A top manager in a multinational bank asks his research group to find out trade opportunities existing in the bond market. The research group first looked at the bond market and found the following tradable bonds

Maturity NO of HY Coupon YTM Price Spot Rate0.5 1 0 0.08 96.15 0.08

1 2 0 0.083 92.19 0.0831.5 3 0.085 0.089 99.45

2 4 0.09 0.092 99.642.5 5 0.11 0.094 103.49

3 6 0.095 0.097 99.493.5 7 0.1 0.1 100

4 8 0.1 0.104 98.724.5 9 0.115 0.106 103.16

5 10 0.0875 0.108 92.245.5 11 0.105 0.109 98.38

6 12 0.11 0.112 99.146.5 13 0.085 0.114 86.94

7 14 0.0825 0.116 84.247.5 15 0.11 0.118 96.09

8 16 0.065 0.119 72.628.5 17 0.0875 0.12 82.97

9 18 0.13 0.122 104.39.5 19 0.115 0.124 95.0610 20 0.125 0.125 100

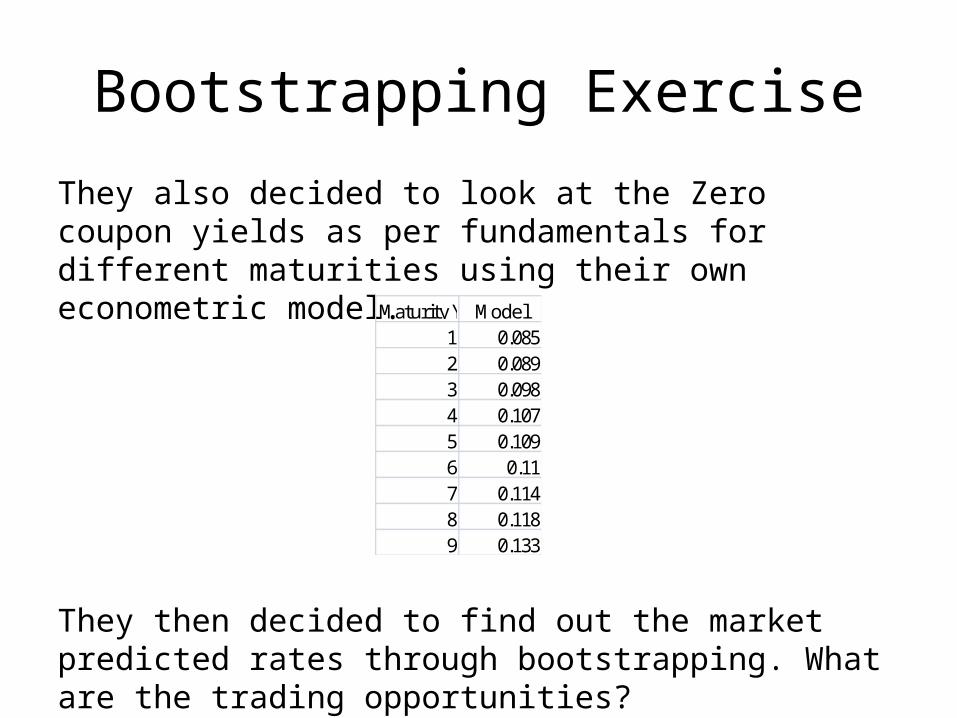

Bootstrapping Exercise

They also decided to look at the Zero coupon yields as per fundamentals for different maturities using their own econometric model.

They then decided to find out the market predicted rates through bootstrapping. What are the trading opportunities?

Maturity Yr Model1 0.0852 0.0893 0.0984 0.1075 0.1096 0.117 0.1148 0.1189 0.133

Forward Rates• Besides default-free theoretical spot rate curves

extrapolated from the Treasury yield curve, it is possible to compute forward rates.

• Since forward rates are extrapolated from the default-free theoretical spot rate curve, these rates are referred to as implied forward rates.

• Besides using the Treasury yield curve, it is possible to compute forward rates from other interest rate curves (i.e. LIBOR).

Forward Rates• Using arbitrage arguments, forward rates

can be extrapolated from the Treasury yield curve or the Treasury spot rate curve.

• The spot rate for a given period is related to the forward rates; specifically, the spot rate is a geometric average of the current 6-month spot rate and the subsequent 6-month forward rates.

Forward Rates

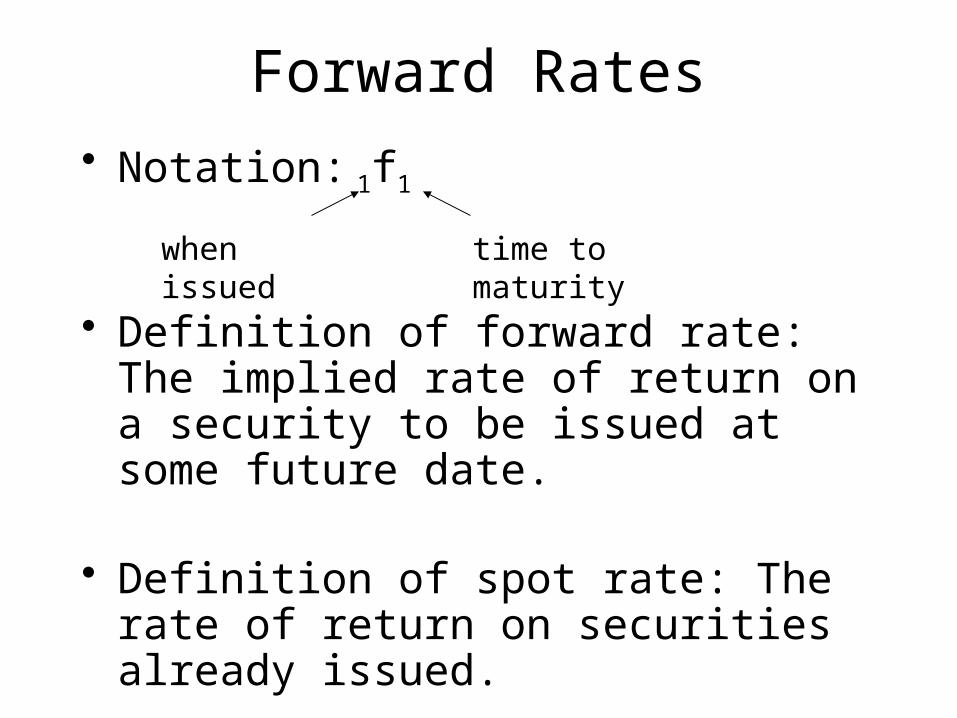

• Notation: 1f1

• Definition of forward rate: The implied rate of return on a security to be issued at some future date.

• Definition of spot rate: The rate of return on securities already issued.

when issued time to maturity

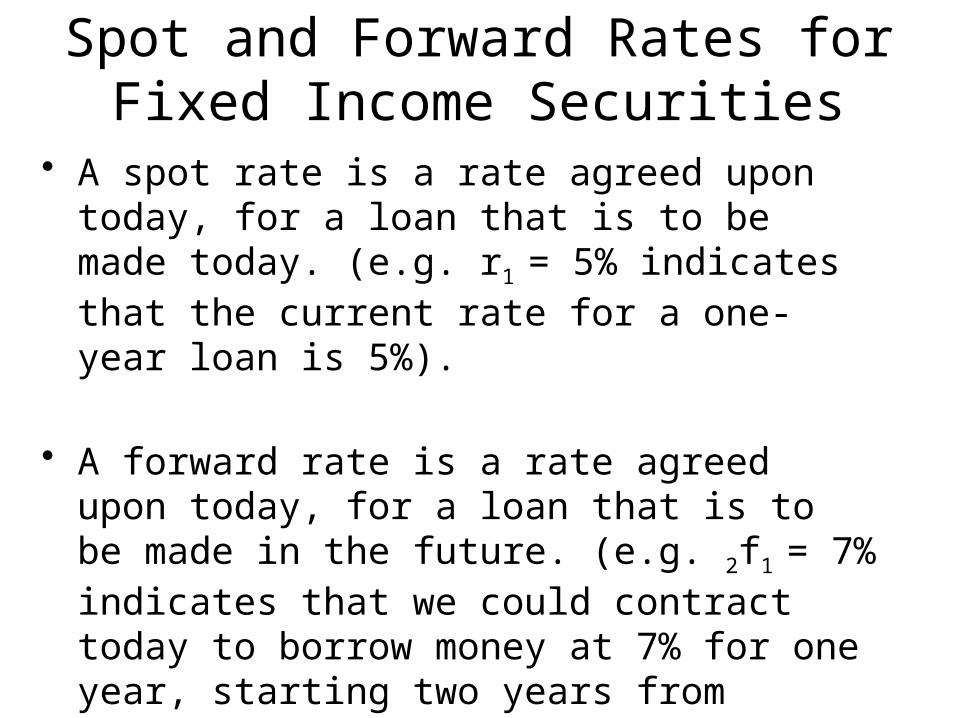

Spot and Forward Rates for Fixed Income Securities

• A spot rate is a rate agreed upon today, for a loan that is to be made today. (e.g. r1 = 5% indicates that the current rate for a one-year loan is 5%).

• A forward rate is a rate agreed upon today, for a loan that is to be made in the future. (e.g. 2f1 = 7% indicates that we could contract today to borrow money at 7% for one year, starting two years from today).

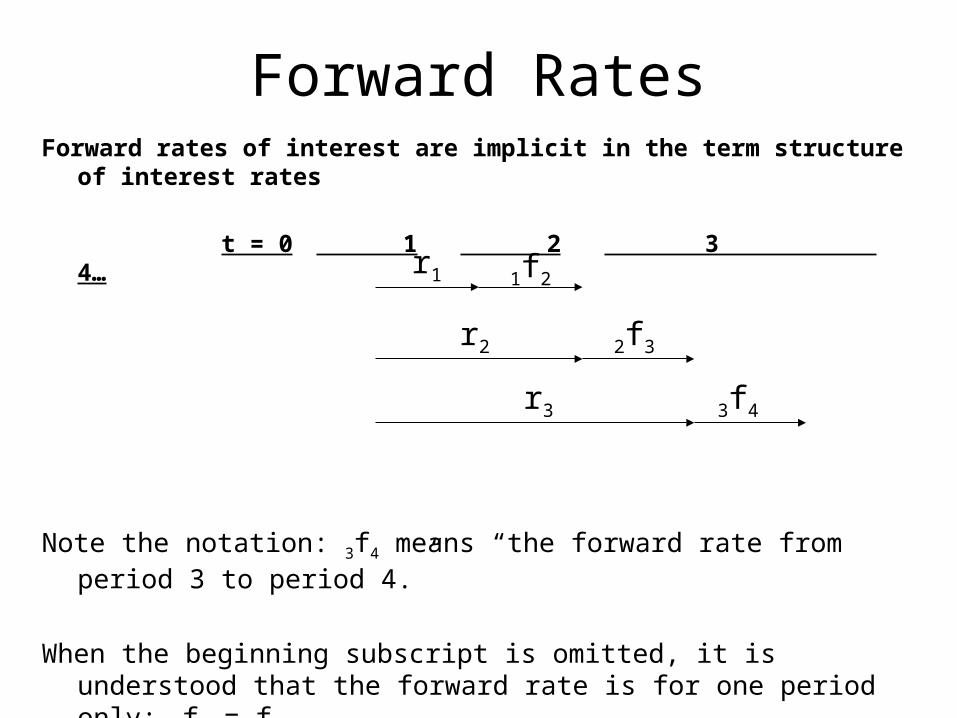

Forward RatesForward rates of interest are implicit in the term structure of

interest rates

t = 0 1 2 3 4…

Note the notation: 3f4 means “the forward rate from period 3 to period 4.”

When the beginning subscript is omitted, it is understood that the forward rate is for one period only: 3f4 = f4 .

r1

r2

r3

1f2

2f3

3f4

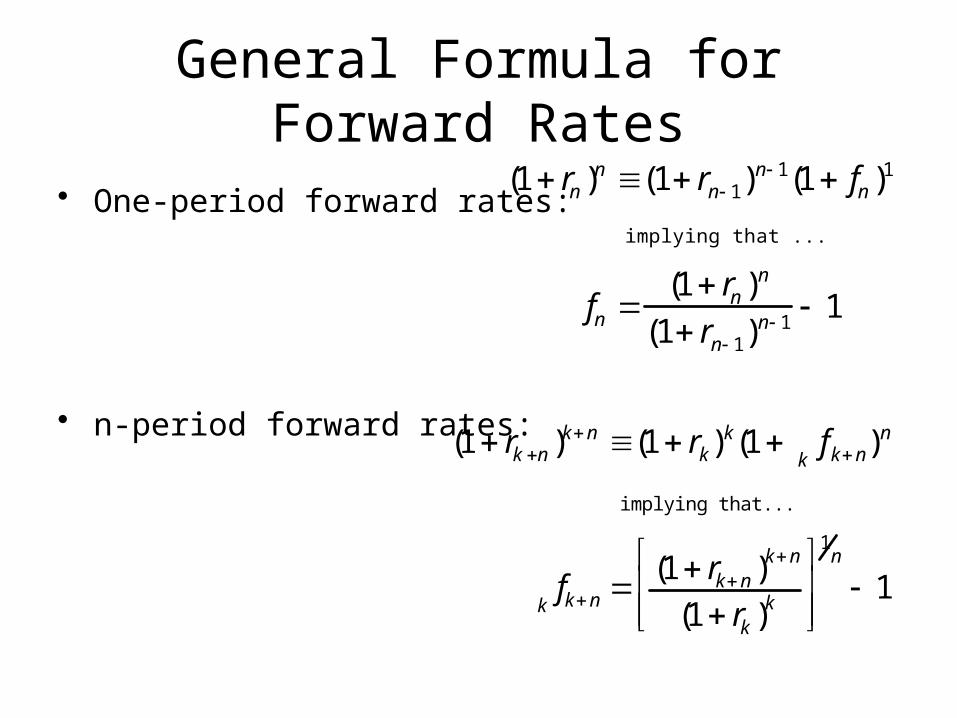

General Formula for Forward Rates

• One-period forward rates:

• n-period forward rates:

(1 rn )n (1 rn 1)

n 1(1 fn )1

implying that ...

fn (1 rn )

n

(1 rn 1)n 1

1

(1 rk n )kn (1 rk)

k(1 kfkn)

n

implying that...

kfkn (1 rkn )

kn

(1 rk )k

1n

1

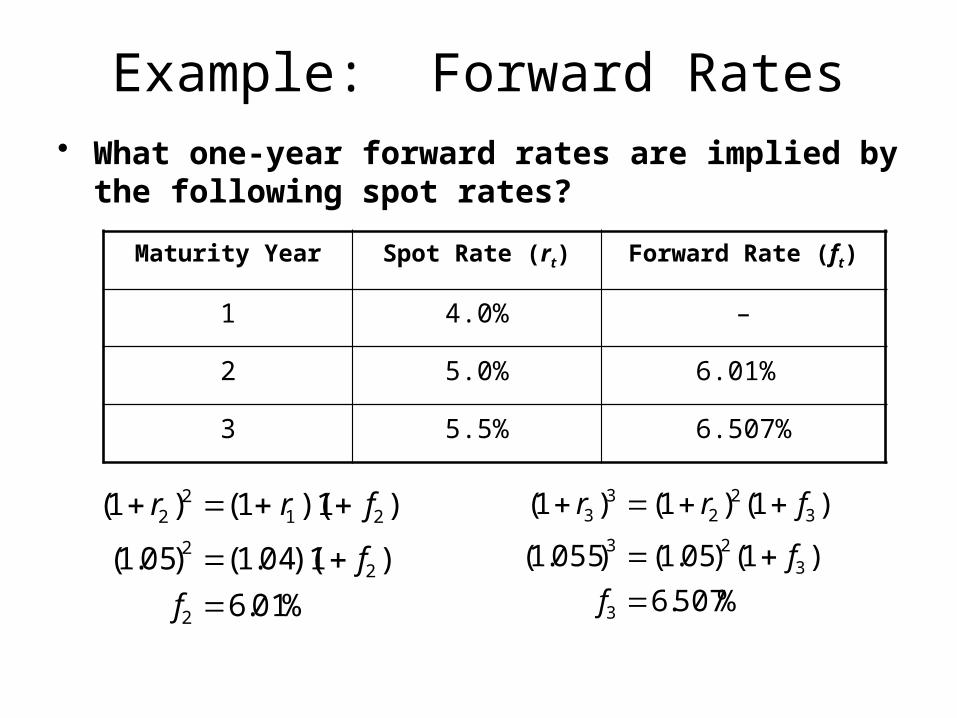

Example: Forward Rates• What one-year forward rates are implied by

the following spot rates?

Maturity Year Spot Rate (rt) Forward Rate (ft)

1 4.0% –

2 5.0% 6.01%

3 5.5% 6.507%

(1 r2 )2 (1 r1 )(1 f2 )

(1.05)2 (1.04)(1 f2 )

f2 6.01%

(1 r3 )3 (1 r2 )2 (1 f3 )

(1.055)3 (1.05)2 (1 f3 )

f3 6.507%

Implied Forward Rate Example• Suppose the spot term structure of zero-

coupon yields is: {r1=0.08, r2=0.10, r3=0.13,

r4=0.14,…}

• If investors wish to invest $1,000,000 for two years. They can choose between:– buying a 2-yr. discount bond, and– buying a sequence of two 1-yr. bonds, i.e.,

one now and one in one year from now.

What Will the Investor Choose?

• The alternative that pays the higher cumulative return over the 2-yr time horizon.

• Caveat: The rate of return on the bond issued one year from now is uncertain.

• How do we estimate it?– With the implied forward rate

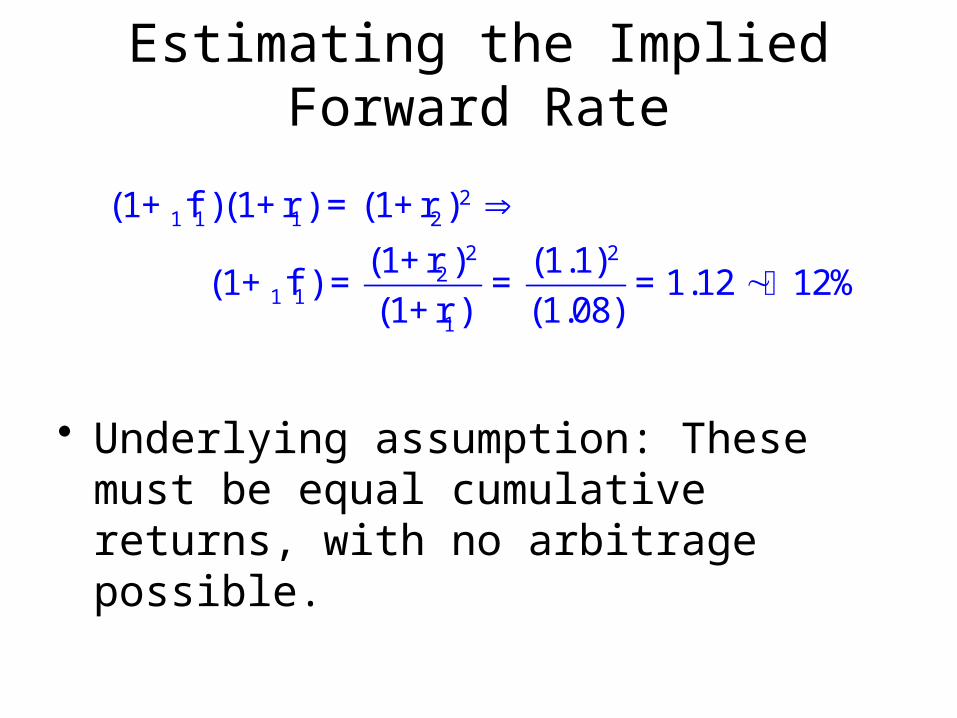

Estimating the Implied Forward Rate

• Underlying assumption: These must be equal cumulative returns, with no arbitrage possible.

21 1 1 2

2 22

1 11

(1+ f )(1+r ) =(1+r )

(1+r ) (1.1)(1+ f ) = = =1.12 12%

(1+r ) (1.08)

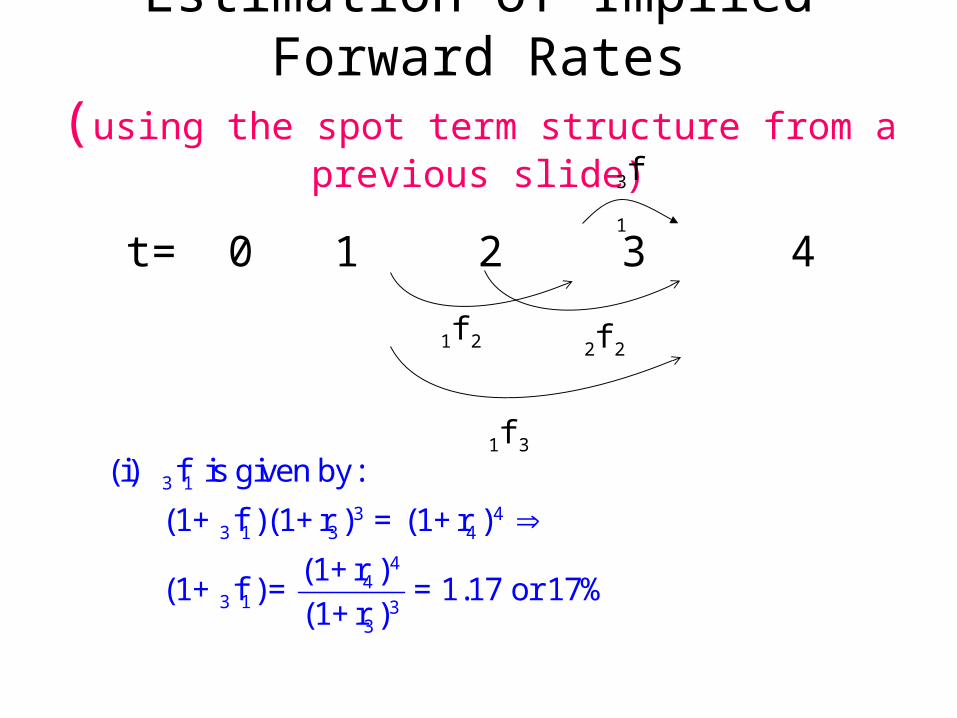

Estimation of Implied Forward Rates(using the spot term structure from a previous slide)

t= 0 1 2 3 4

3f1

1f2 2f2

1f3

3 1

3 43 1 3 4

44

3 1 33

(i) fi s givenby:

(1+ f )(1+r ) =(1+r )

(1+r )(1+ f )= =1.17 or 17%

(1+r )

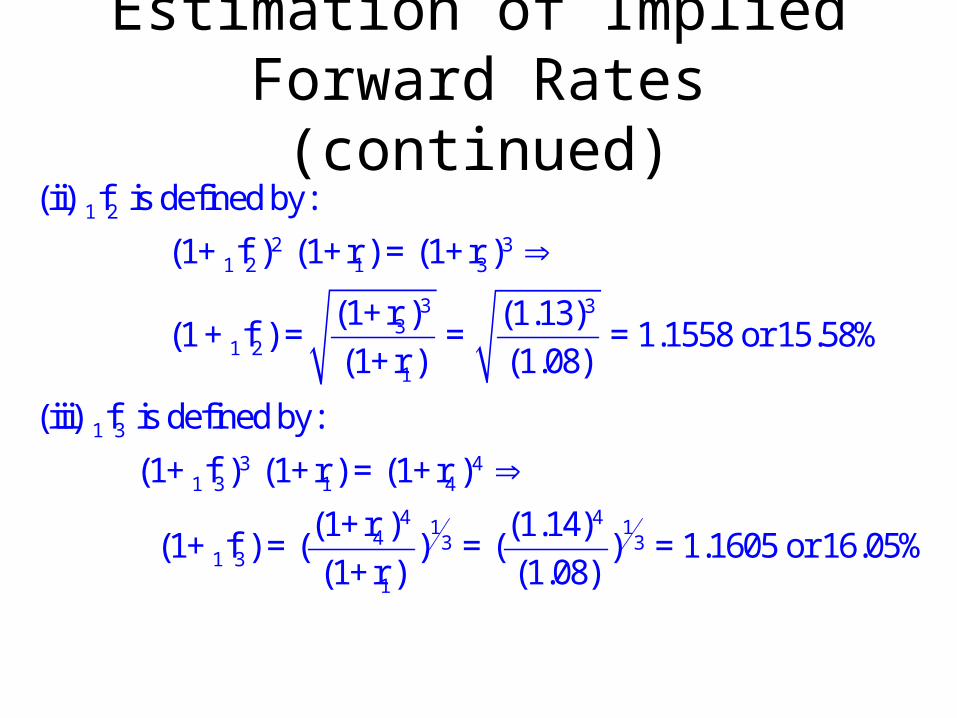

Estimation of Implied Forward Rates (continued)

1 2

2 31 2 1 3

3 33

1 21

1 3

3 41 3 1 4

4 41 14 3 31 3

1

(ii) fi s definedby:

(1+ f ) (1+r ) =(1+r )

(1+r ) (1.13)(1+ f ) = = =1.1558 or 15.58%

(1+r ) (1.08)

(iii) fi s definedby:

(1+ f ) (1+r ) =(1+r )

(1+r ) (1.14)(1+ f ) =( ) =( ) =1.1605 or 16.05%

(1+r ) (1.08)

General Formula for Implied Forward Rates

• Note that implied fwd rates are internally consistent, e.g.,

1i+j j

i+ji j i

i

(1+r )1+ f =

(1+r)

2 31 2 3 1 1 3

12 3

1 3 1 2 3 1

(1 ) (1 ) (1 )

(1 ) (1 ) (1 )

ff f

ff f

Deriving a 6-Month Forward Rate

To compute a 6-month forward rate, it is necessary to utilize a yield curve and the corresponding spot rate curve.

• The following 2 investments should have the same value:

– 1-year Treasury bill and– 2 six-month Treasury bills (one purchased now and the other in

six months)

• An investor should be indifferent since they should produce the same investment income over the same investment horizon.

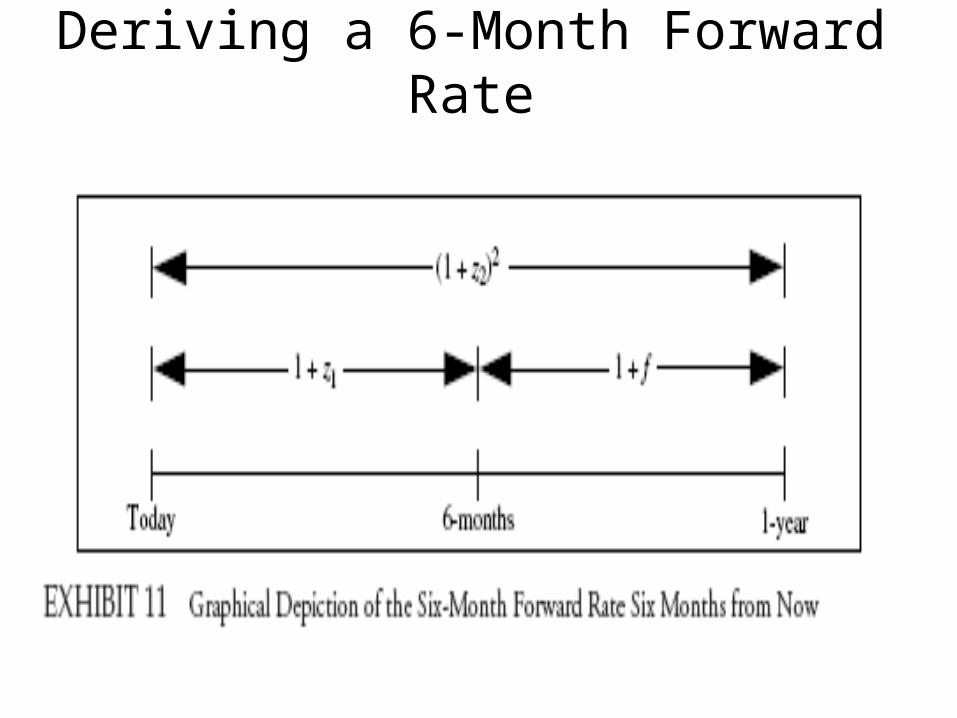

Deriving a 6-Month Forward Rate

Although an investor does not know the interest rate of the second 6-month T-bill, it is possible to compute it because the “forward” rate must such that it equalizes the dollar return between the two alternatives.

Exhibit 11 shows the timeline for the two investment alternatives:

• The value of first six-month T-bill is: X(1 + z1) • The value of the total investment following the second six-

month T-bill is: X(1 + z1)(1 + f)– Where z1 is one-half the bond-equivalent yield of the 6-month spot

rate and f is one-half the forward rate on a 6-month Treasury bill available 6 months from now. X is the amount of the investment.

Deriving a 6-Month Forward Rate

Relationship Between Spot Rates and Short-Term Forward Rates

• The value of alternative investment (a 1-year T-bill) is computed as:

X(1 + z2)2

• Because the two alternatives should generate identical returns:

X(1 + z1)(1 + f) = X(1 + z2)2

• Solving for f = [(1 + z2)2 / (1 + z1)] -1

– Multiplying f by 2 to get the forward rate on a bond-equivalent yield basis.

• Forward rates can be computed on various combinations of short- and longer-term interest rates

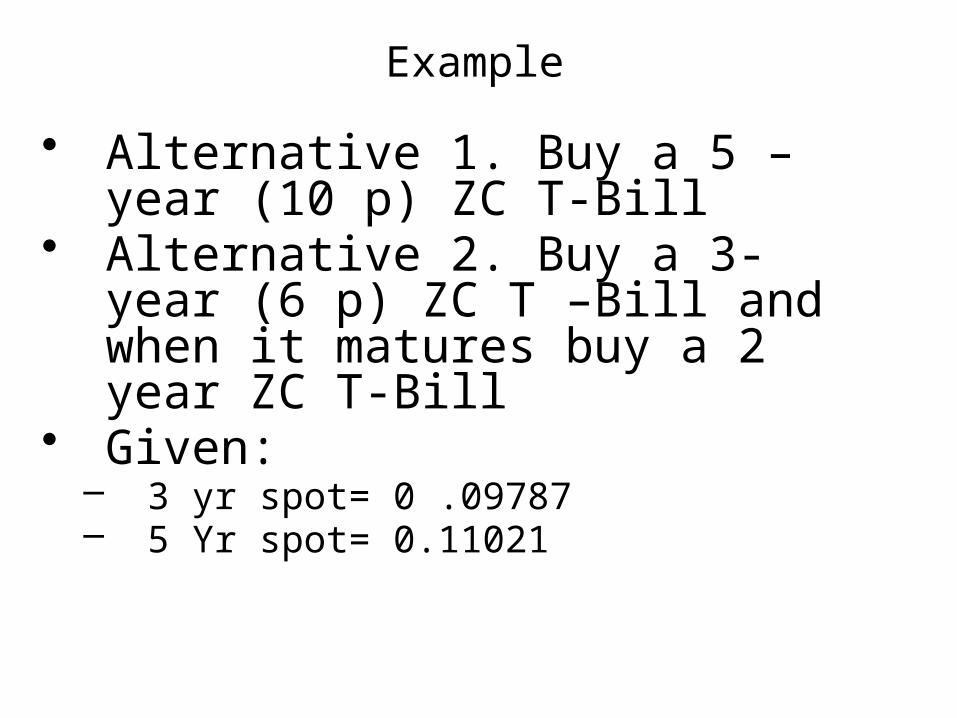

Example

• Alternative 1. Buy a 5 – year (10 p) ZC T-Bill

• Alternative 2. Buy a 3- year (6 p) ZC T –Bill and when it matures buy a 2 year ZC T-Bill

• Given: – 3 yr spot= 0 .09787– 5 Yr spot= 0.11021