Boa Offshore - 28 November 2014 3Q 2014 Results presentation Boa Offshore - 28 November 2014 ... •...

21

Boa Offshore - 28 November 2014 3Q 2014 Results presentation Helge Kvalvik, CEO

Transcript of Boa Offshore - 28 November 2014 3Q 2014 Results presentation Boa Offshore - 28 November 2014 ... •...

Boa Offshore - 28 November 2014

3Q 2014 Results presentation

Helge Kvalvik, CEO

This presentation is made by Boa Offshore (or the ”Company”). The information contained herein

include statements that are ”forward-looking” in their nature. These forward-looking statements include

all matters that are not historical facts and are based on the Company’s current intentions, believes

and expectations about among other things, the Company’s results of operations, financial condition,

prospects, growth, strategies and the industry in which the Company operates. Such forward-looking

information and statements reflect current views with respect to future events. The Company cannot

give any assurance as to the correctness of information and statements related to such future events.

Furthermore, these forward-looking statements involve known and unknown risks, uncertainties and

other factors that are in many cases beyond the Company’s control that could cause the actual results

of operations, financial condition, liquidity and the development of the industry in which the Company’s

businesses operate to differ materially from the impression created by the forward-looking statements

contained herein, because they relate to events and depend on circumstances that may or may not

occur in the future. Although the Company believes that its intentions, beliefs and expectations, and

the statements in this presentation, are based on reasonable assumptions as of today, the Company

can not give any assurance that the actual results will be as set out in this presentation. Financing the

Company involves risks, and several factors could cause the actual results, performance or

achievements of the Company to be materially different from the impression created by the forward-

looking statements contained herein. Neither the Company, nor any company within the Boa Offshore

Group, is making any representation or warranty (express or implied) as to the accuracy, reliability or

completeness of the information and statements in this presentation, and neither the Company, any

company within the Boa Group, nor any of their directors, officers or employees will have any liability

to any persons resulting from the possible use of information in the presentation.

Disclaimer

2 2

3 Boa Offshore Financials

Contents

3

2 Boa Offshore update and overview

4 Boa Offshore Business segments

5 Market Outlook

1 Boa Offshore summary

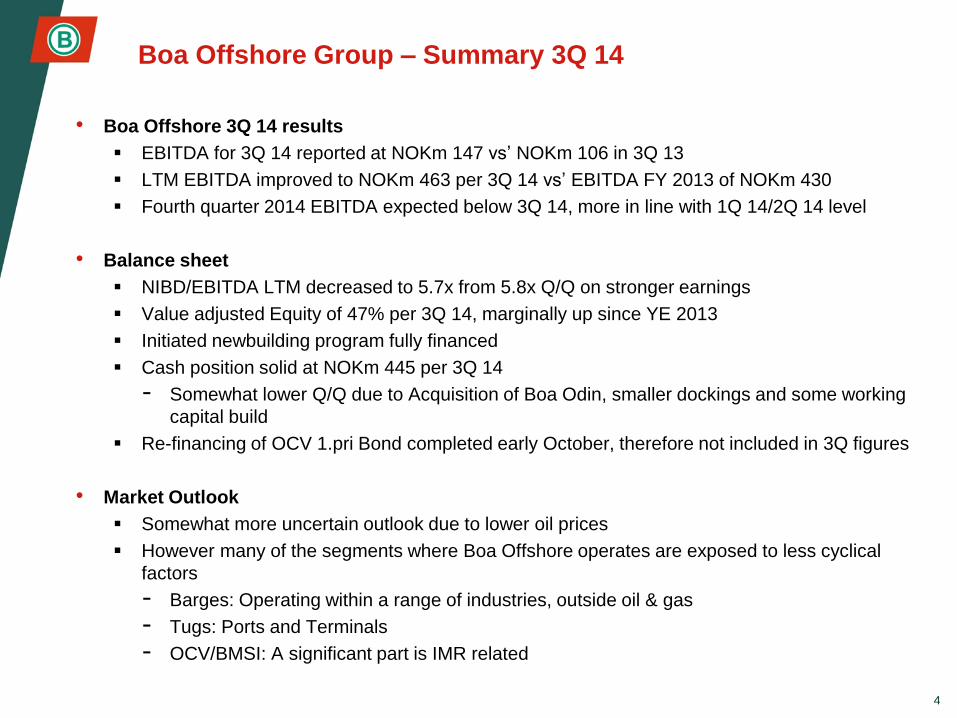

Boa Offshore Group – Summary 3Q 14

• Boa Offshore 3Q 14 results

EBITDA for 3Q 14 reported at NOKm 147 vs’ NOKm 106 in 3Q 13

LTM EBITDA improved to NOKm 463 per 3Q 14 vs’ EBITDA FY 2013 of NOKm 430

Fourth quarter 2014 EBITDA expected below 3Q 14, more in line with 1Q 14/2Q 14 level

• Balance sheet

NIBD/EBITDA LTM decreased to 5.7x from 5.8x Q/Q on stronger earnings

Value adjusted Equity of 47% per 3Q 14, marginally up since YE 2013

Initiated newbuilding program fully financed

Cash position solid at NOKm 445 per 3Q 14

- Somewhat lower Q/Q due to Acquisition of Boa Odin, smaller dockings and some working

capital build

Re-financing of OCV 1.pri Bond completed early October, therefore not included in 3Q figures

• Market Outlook

Somewhat more uncertain outlook due to lower oil prices

However many of the segments where Boa Offshore operates are exposed to less cyclical

factors

- Barges: Operating within a range of industries, outside oil & gas

- Tugs: Ports and Terminals

- OCV/BMSI: A significant part is IMR related

4

3 Boa Offshore Financials

Contents

5

2 Boa Offshore update and overview

4 Boa Offshore Business segments

5 Market Outlook

1 Boa Offshore summary

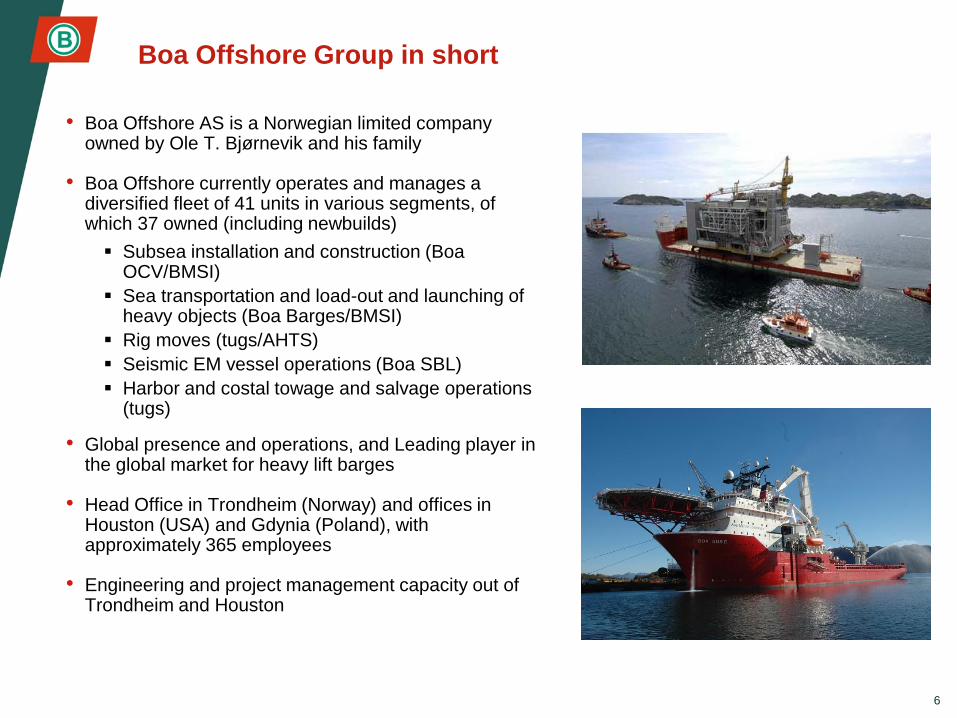

Boa Offshore Group in short

• Boa Offshore AS is a Norwegian limited company owned by Ole T. Bjørnevik and his family

• Boa Offshore currently operates and manages a diversified fleet of 41 units in various segments, of which 37 owned (including newbuilds)

Subsea installation and construction (Boa OCV/BMSI)

Sea transportation and load-out and launching of heavy objects (Boa Barges/BMSI)

Rig moves (tugs/AHTS)

Seismic EM vessel operations (Boa SBL)

Harbor and costal towage and salvage operations (tugs)

• Global presence and operations, and Leading player in the global market for heavy lift barges

• Head Office in Trondheim (Norway) and offices in Houston (USA) and Gdynia (Poland), with approximately 365 employees

• Engineering and project management capacity out of Trondheim and Houston

6

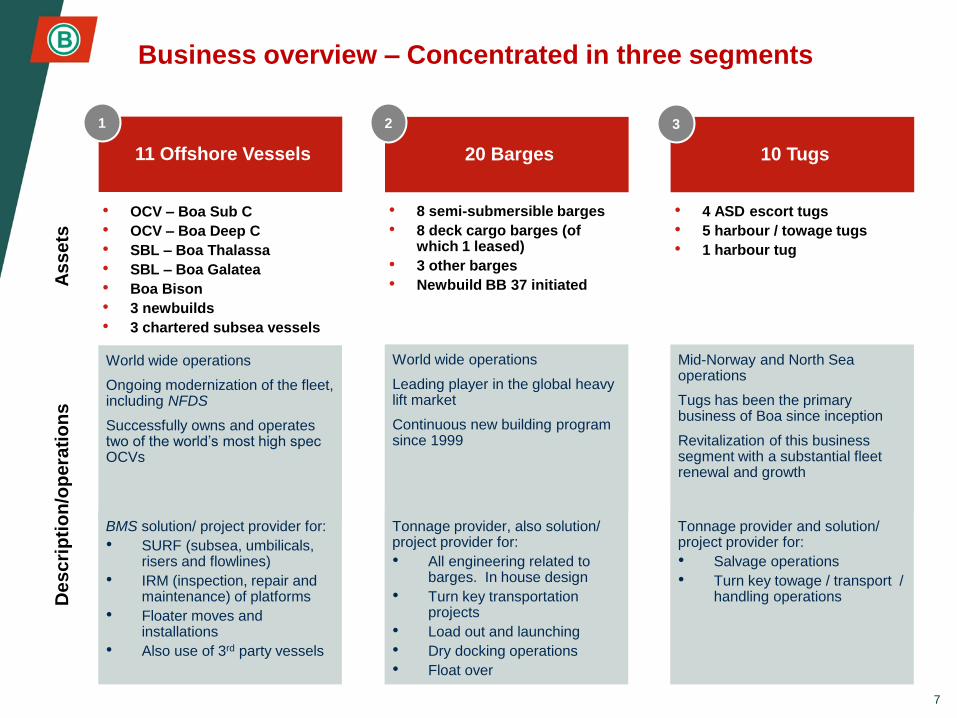

Business overview – Concentrated in three segments

10 Tugs 20 Barges 11 Offshore Vessels

• 4 ASD escort tugs

• 5 harbour / towage tugs

• 1 harbour tug

• 8 semi-submersible barges

• 8 deck cargo barges (of which 1 leased)

• 3 other barges

• Newbuild BB 37 initiated

• OCV – Boa Sub C

• OCV – Boa Deep C

• SBL – Boa Thalassa

• SBL – Boa Galatea

• Boa Bison

• 3 newbuilds

• 3 chartered subsea vessels

Mid-Norway and North Sea operations

Tugs has been the primary business of Boa since inception

Revitalization of this business segment with a substantial fleet renewal and growth

World wide operations

Leading player in the global heavy lift market

Continuous new building program since 1999

World wide operations

Ongoing modernization of the fleet, including NFDS

Successfully owns and operates two of the world’s most high spec OCVs

Tonnage provider and solution/ project provider for:

• Salvage operations

• Turn key towage / transport / handling operations

Tonnage provider, also solution/ project provider for:

• All engineering related to barges. In house design

• Turn key transportation projects

• Load out and launching

• Dry docking operations

• Float over

BMS solution/ project provider for:

• SURF (subsea, umbilicals, risers and flowlines)

• IRM (inspection, repair and maintenance) of platforms

• Floater moves and installations

• Also use of 3rd party vessels

7

As

se

ts

De

sc

rip

tio

n/o

pera

tio

ns

1 2 3

3 Boa Offshore Financials

Contents

8

2 Boa Offshore update and overview

4 Boa Offshore Business segments

5 Market Outlook

1 Boa Offshore summary

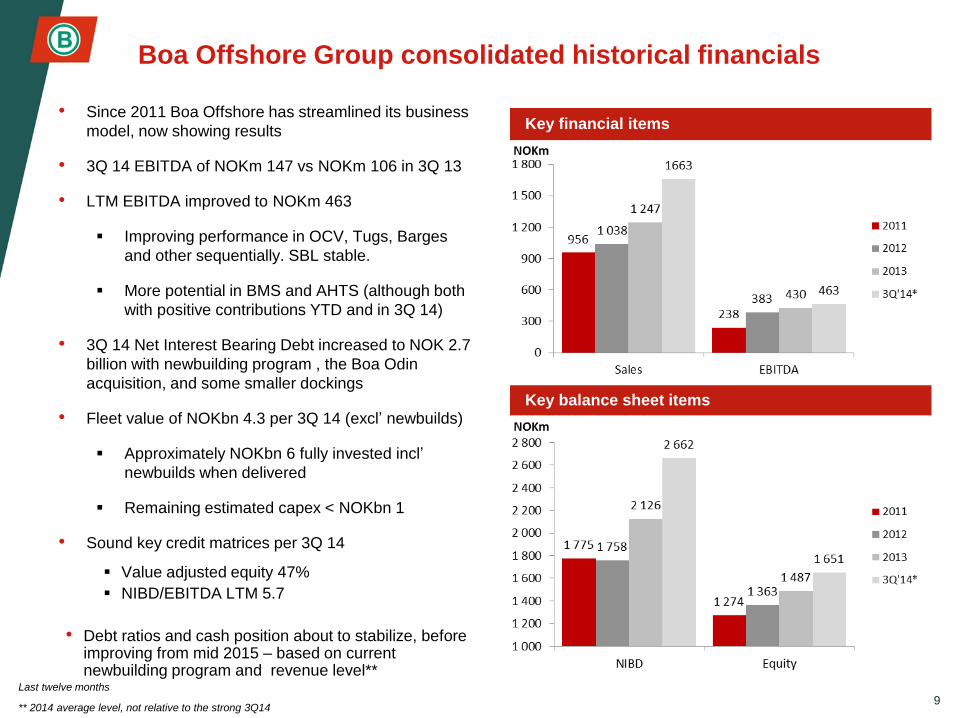

Boa Offshore Group consolidated historical financials

• Since 2011 Boa Offshore has streamlined its business

model, now showing results

• 3Q 14 EBITDA of NOKm 147 vs NOKm 106 in 3Q 13

• LTM EBITDA improved to NOKm 463

Improving performance in OCV, Tugs, Barges

and other sequentially. SBL stable.

More potential in BMS and AHTS (although both

with positive contributions YTD and in 3Q 14)

• 3Q 14 Net Interest Bearing Debt increased to NOK 2.7

billion with newbuilding program , the Boa Odin

acquisition, and some smaller dockings

• Fleet value of NOKbn 4.3 per 3Q 14 (excl’ newbuilds)

Approximately NOKbn 6 fully invested incl’

newbuilds when delivered

Remaining estimated capex < NOKbn 1

• Sound key credit matrices per 3Q 14

Value adjusted equity 47%

NIBD/EBITDA LTM 5.7

• Debt ratios and cash position about to stabilize, before improving from mid 2015 – based on current newbuilding program and revenue level**

9

Key financial items

Key balance sheet items

Last twelve months

** 2014 average level, not relative to the strong 3Q14

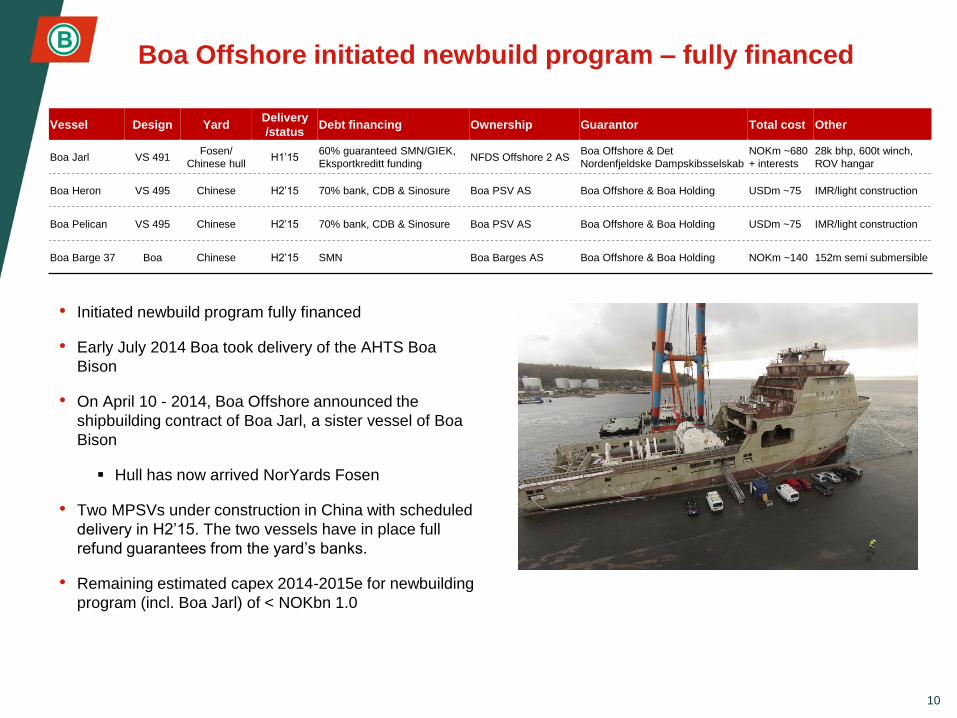

Boa Offshore initiated newbuild program – fully financed

10

• Initiated newbuild program fully financed

• Early July 2014 Boa took delivery of the AHTS Boa

Bison

• On April 10 - 2014, Boa Offshore announced the

shipbuilding contract of Boa Jarl, a sister vessel of Boa

Bison

Hull has now arrived NorYards Fosen

• Two MPSVs under construction in China with scheduled

delivery in H2’15. The two vessels have in place full

refund guarantees from the yard’s banks.

• Remaining estimated capex 2014-2015e for newbuilding

program (incl. Boa Jarl) of < NOKbn 1.0

Vessel Design Yard Delivery

/status Debt financing Ownership Guarantor Total cost Other

Boa Jarl VS 491 Fosen/

Chinese hull H1’15

60% guaranteed SMN/GIEK,

Eksportkreditt funding NFDS Offshore 2 AS

Boa Offshore & Det

Nordenfjeldske Dampskibsselskab

NOKm ~680

+ interests

28k bhp, 600t winch,

ROV hangar

Boa Heron VS 495 Chinese H2’15 70% bank, CDB & Sinosure Boa PSV AS Boa Offshore & Boa Holding USDm ~75 IMR/light construction

Boa Pelican VS 495 Chinese H2’15 70% bank, CDB & Sinosure Boa PSV AS Boa Offshore & Boa Holding USDm ~75 IMR/light construction

Boa Barge 37 Boa Chinese H2’15 SMN Boa Barges AS Boa Offshore & Boa Holding NOKm ~140 152m semi submersible

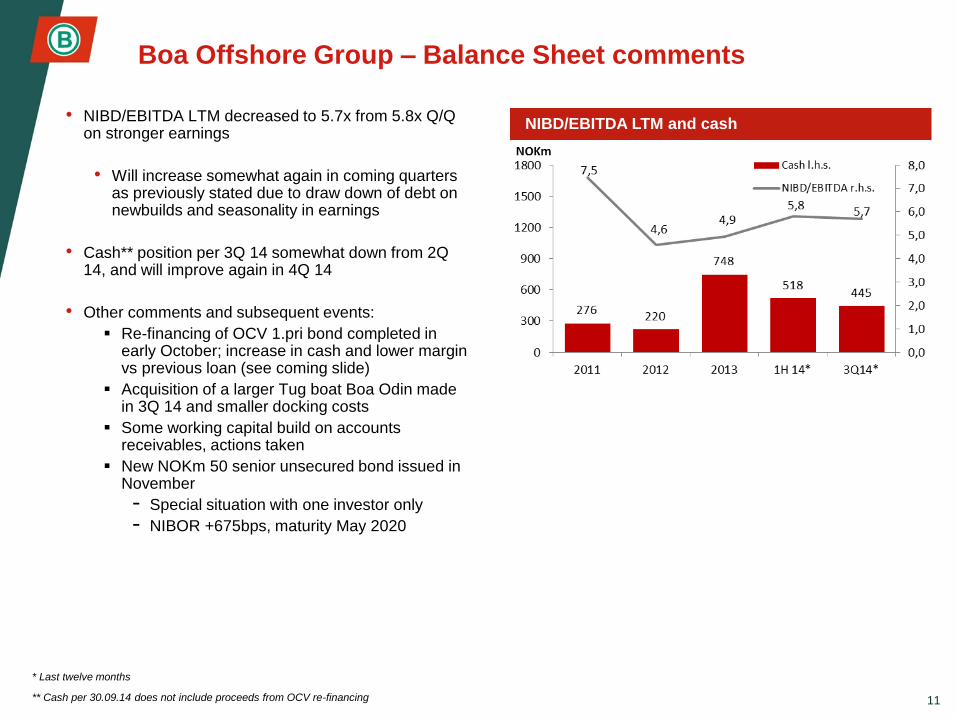

Boa Offshore Group – Balance Sheet comments

• NIBD/EBITDA LTM decreased to 5.7x from 5.8x Q/Q on stronger earnings

• Will increase somewhat again in coming quarters as previously stated due to draw down of debt on newbuilds and seasonality in earnings

• Cash** position per 3Q 14 somewhat down from 2Q 14, and will improve again in 4Q 14

• Other comments and subsequent events:

Re-financing of OCV 1.pri bond completed in early October; increase in cash and lower margin vs previous loan (see coming slide)

Acquisition of a larger Tug boat Boa Odin made in 3Q 14 and smaller docking costs

Some working capital build on accounts receivables, actions taken

New NOKm 50 senior unsecured bond issued in November

- Special situation with one investor only

- NIBOR +675bps, maturity May 2020

11

NIBD/EBITDA LTM and cash

* Last twelve months

** Cash per 30.09.14 does not include proceeds from OCV re-financing

3 Boa Offshore Financials

Contents

12

2 Boa Offshore update and overview

4 Boa Offshore Business segments

5 Market Outlook

1 Boa Offshore summary

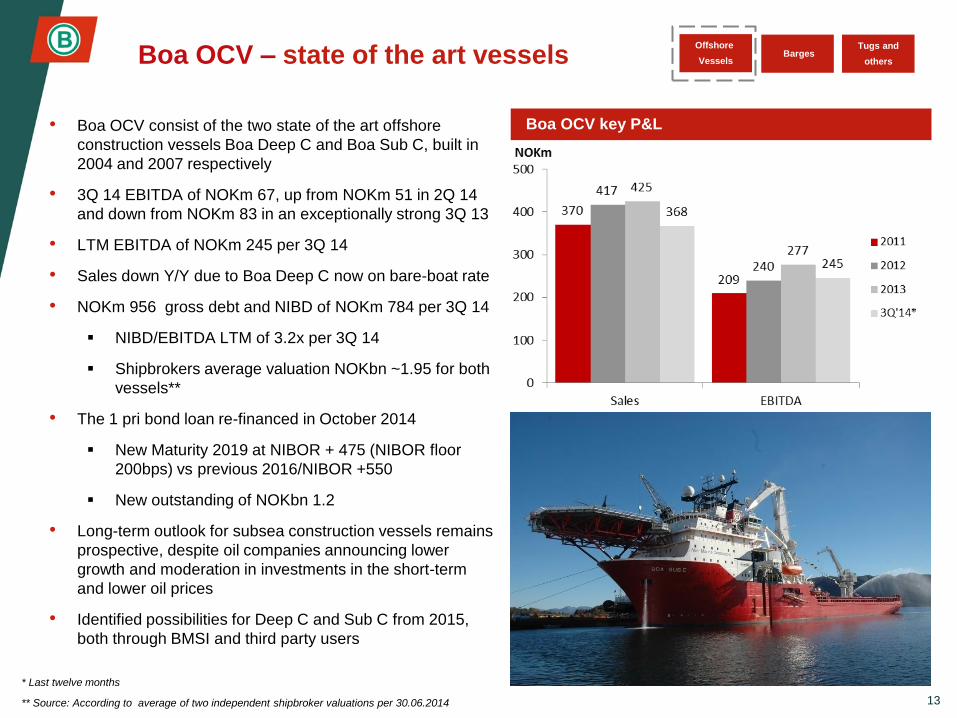

Boa OCV – state of the art vessels

• Boa OCV consist of the two state of the art offshore

construction vessels Boa Deep C and Boa Sub C, built in

2004 and 2007 respectively

• 3Q 14 EBITDA of NOKm 67, up from NOKm 51 in 2Q 14

and down from NOKm 83 in an exceptionally strong 3Q 13

• LTM EBITDA of NOKm 245 per 3Q 14

• Sales down Y/Y due to Boa Deep C now on bare-boat rate

• NOKm 956 gross debt and NIBD of NOKm 784 per 3Q 14

NIBD/EBITDA LTM of 3.2x per 3Q 14

Shipbrokers average valuation NOKbn ~1.95 for both

vessels**

• The 1 pri bond loan re-financed in October 2014

New Maturity 2019 at NIBOR + 475 (NIBOR floor

200bps) vs previous 2016/NIBOR +550

New outstanding of NOKbn 1.2

• Long-term outlook for subsea construction vessels remains

prospective, despite oil companies announcing lower

growth and moderation in investments in the short-term

and lower oil prices

• Identified possibilities for Deep C and Sub C from 2015,

both through BMSI and third party users

13

Boa OCV key P&L

Tugs and

others Barges

Offshore

Vessels

* Last twelve months

** Source: According to average of two independent shipbroker valuations per 30.06.2014

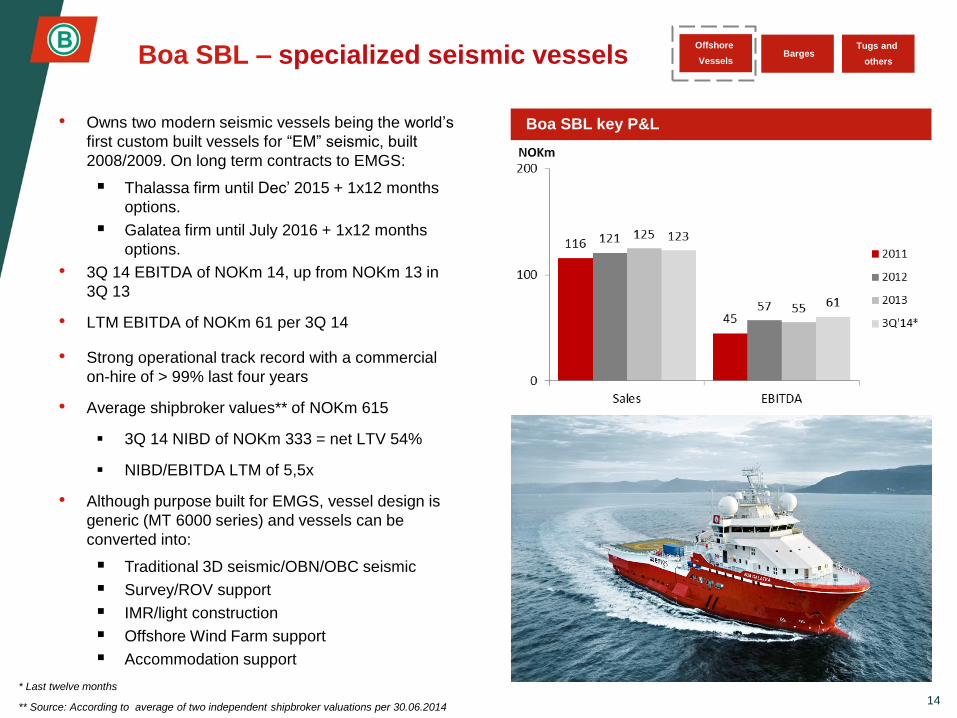

Boa SBL – specialized seismic vessels

• Owns two modern seismic vessels being the world’s

first custom built vessels for “EM” seismic, built

2008/2009. On long term contracts to EMGS:

Thalassa firm until Dec’ 2015 + 1x12 months

options.

Galatea firm until July 2016 + 1x12 months

options.

• 3Q 14 EBITDA of NOKm 14, up from NOKm 13 in

3Q 13

• LTM EBITDA of NOKm 61 per 3Q 14

• Strong operational track record with a commercial

on-hire of > 99% last four years

• Average shipbroker values** of NOKm 615

3Q 14 NIBD of NOKm 333 = net LTV 54%

NIBD/EBITDA LTM of 5,5x

• Although purpose built for EMGS, vessel design is

generic (MT 6000 series) and vessels can be

converted into:

Traditional 3D seismic/OBN/OBC seismic

Survey/ROV support

IMR/light construction

Offshore Wind Farm support

Accommodation support

Boa SBL key P&L

14

Tugs and

others Barges

Offshore

Vessels

* Last twelve months

** Source: According to average of two independent shipbroker valuations per 30.06.2014

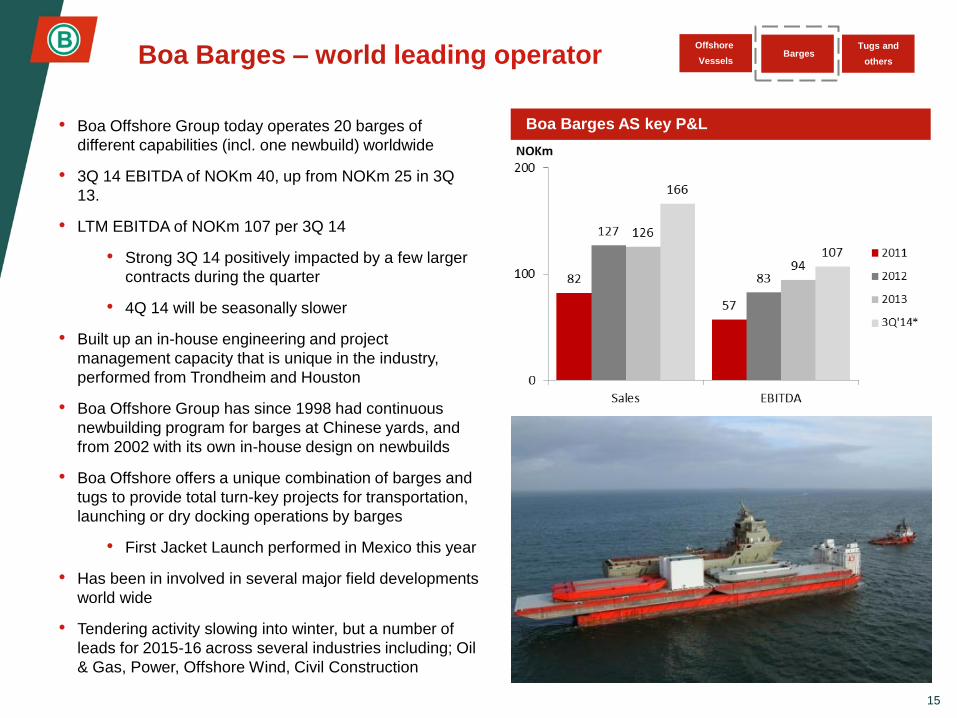

Boa Barges – world leading operator

• Boa Offshore Group today operates 20 barges of

different capabilities (incl. one newbuild) worldwide

• 3Q 14 EBITDA of NOKm 40, up from NOKm 25 in 3Q

13.

• LTM EBITDA of NOKm 107 per 3Q 14

• Strong 3Q 14 positively impacted by a few larger

contracts during the quarter

• 4Q 14 will be seasonally slower

• Built up an in-house engineering and project

management capacity that is unique in the industry,

performed from Trondheim and Houston

• Boa Offshore Group has since 1998 had continuous

newbuilding program for barges at Chinese yards, and

from 2002 with its own in-house design on newbuilds

• Boa Offshore offers a unique combination of barges and

tugs to provide total turn-key projects for transportation,

launching or dry docking operations by barges

• First Jacket Launch performed in Mexico this year

• Has been in involved in several major field developments

world wide

• Tendering activity slowing into winter, but a number of

leads for 2015-16 across several industries including; Oil

& Gas, Power, Offshore Wind, Civil Construction

15

Tugs and

others Barges

Offshore

Vessels

Boa Barges AS key P&L

Tugs and others

16

Tugs and

others Barges

Offshore

Vessels

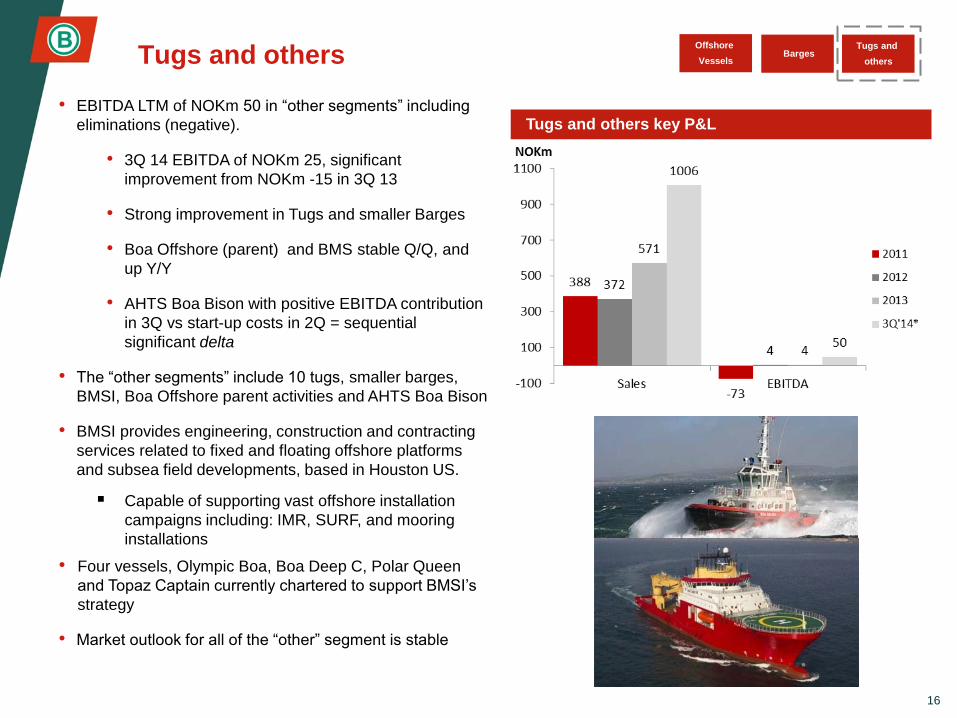

• EBITDA LTM of NOKm 50 in “other segments” including

eliminations (negative).

• 3Q 14 EBITDA of NOKm 25, significant

improvement from NOKm -15 in 3Q 13

• Strong improvement in Tugs and smaller Barges

• Boa Offshore (parent) and BMS stable Q/Q, and

up Y/Y

• AHTS Boa Bison with positive EBITDA contribution

in 3Q vs start-up costs in 2Q = sequential

significant delta

• The “other segments” include 10 tugs, smaller barges,

BMSI, Boa Offshore parent activities and AHTS Boa Bison

• BMSI provides engineering, construction and contracting

services related to fixed and floating offshore platforms

and subsea field developments, based in Houston US.

Capable of supporting vast offshore installation

campaigns including: IMR, SURF, and mooring

installations

• Four vessels, Olympic Boa, Boa Deep C, Polar Queen

and Topaz Captain currently chartered to support BMSI’s

strategy

• Market outlook for all of the “other” segment is stable

Tugs and others key P&L

3 Boa Offshore Financials

Contents

17

2 Boa Offshore update and overview

4 Boa Offshore Business segments

5 Market Outlook

1 Boa Offshore summary

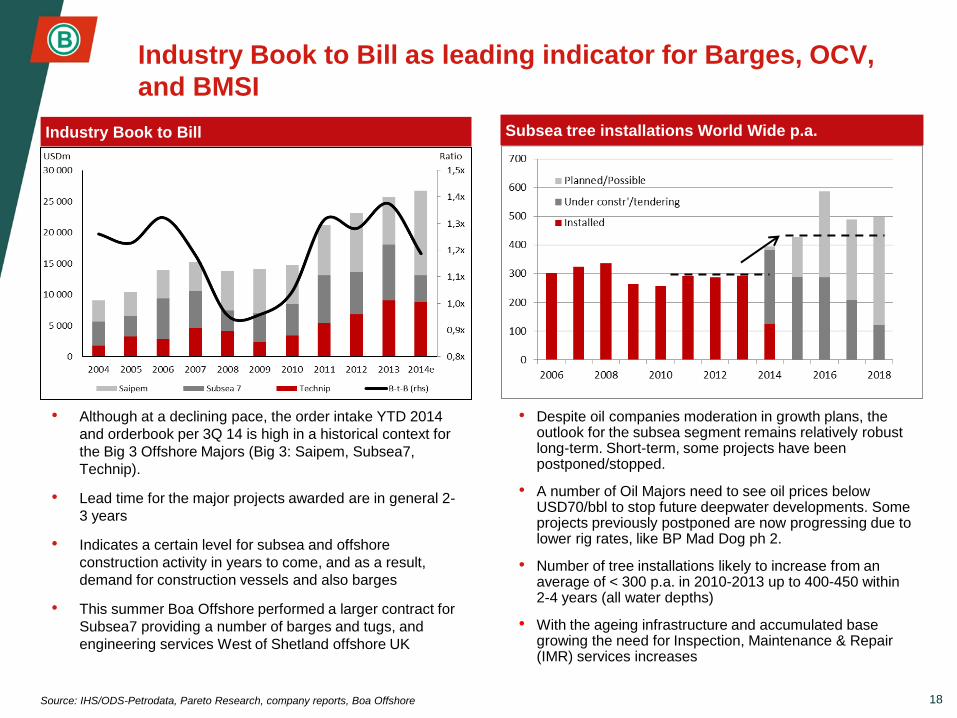

Industry Book to Bill as leading indicator for Barges, OCV,

and BMSI

Industry Book to Bill

18 Source: IHS/ODS-Petrodata, Pareto Research, company reports, Boa Offshore

• Although at a declining pace, the order intake YTD 2014

and orderbook per 3Q 14 is high in a historical context for

the Big 3 Offshore Majors (Big 3: Saipem, Subsea7,

Technip).

• Lead time for the major projects awarded are in general 2-

3 years

• Indicates a certain level for subsea and offshore

construction activity in years to come, and as a result,

demand for construction vessels and also barges

• This summer Boa Offshore performed a larger contract for

Subsea7 providing a number of barges and tugs, and

engineering services West of Shetland offshore UK

Subsea tree installations World Wide p.a.

• Despite oil companies moderation in growth plans, the outlook for the subsea segment remains relatively robust long-term. Short-term, some projects have been postponed/stopped.

• A number of Oil Majors need to see oil prices below USD70/bbl to stop future deepwater developments. Some projects previously postponed are now progressing due to lower rig rates, like BP Mad Dog ph 2.

• Number of tree installations likely to increase from an average of < 300 p.a. in 2010-2013 up to 400-450 within 2-4 years (all water depths)

• With the ageing infrastructure and accumulated base growing the need for Inspection, Maintenance & Repair (IMR) services increases

19 Source: ODS/IHS, Boa Offshore

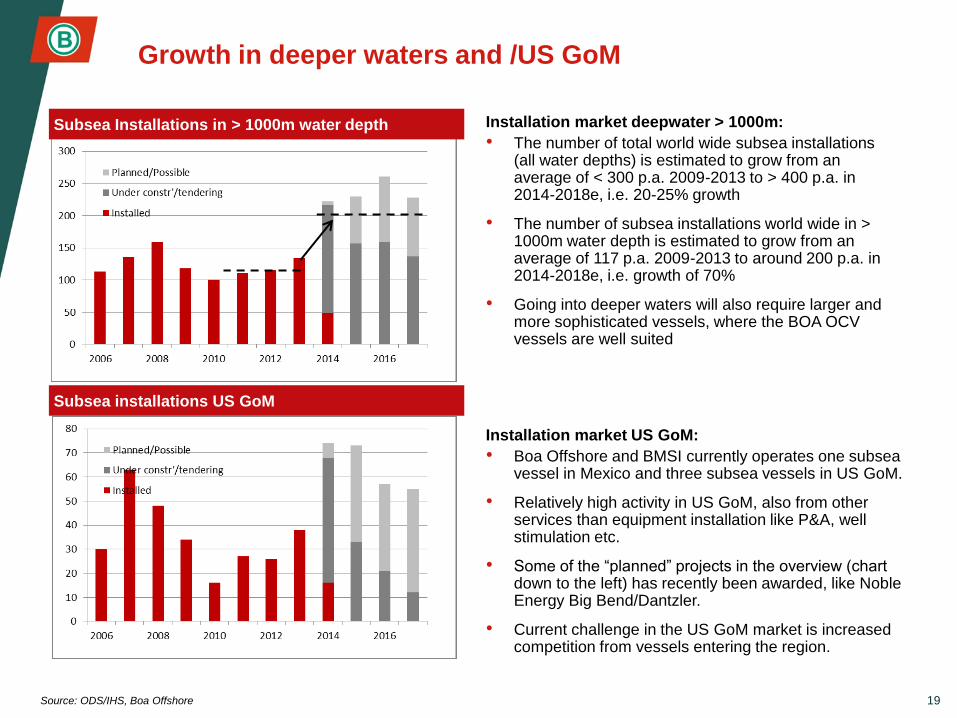

Subsea installations US GoM

Installation market deepwater > 1000m:

• The number of total world wide subsea installations (all water depths) is estimated to grow from an average of < 300 p.a. 2009-2013 to > 400 p.a. in 2014-2018e, i.e. 20-25% growth

• The number of subsea installations world wide in > 1000m water depth is estimated to grow from an average of 117 p.a. 2009-2013 to around 200 p.a. in 2014-2018e, i.e. growth of 70%

• Going into deeper waters will also require larger and more sophisticated vessels, where the BOA OCV vessels are well suited

Subsea Installations in > 1000m water depth

Growth in deeper waters and /US GoM

Installation market US GoM:

• Boa Offshore and BMSI currently operates one subsea vessel in Mexico and three subsea vessels in US GoM.

• Relatively high activity in US GoM, also from other services than equipment installation like P&A, well stimulation etc.

• Some of the “planned” projects in the overview (chart down to the left) has recently been awarded, like Noble Energy Big Bend/Dantzler.

• Current challenge in the US GoM market is increased competition from vessels entering the region.

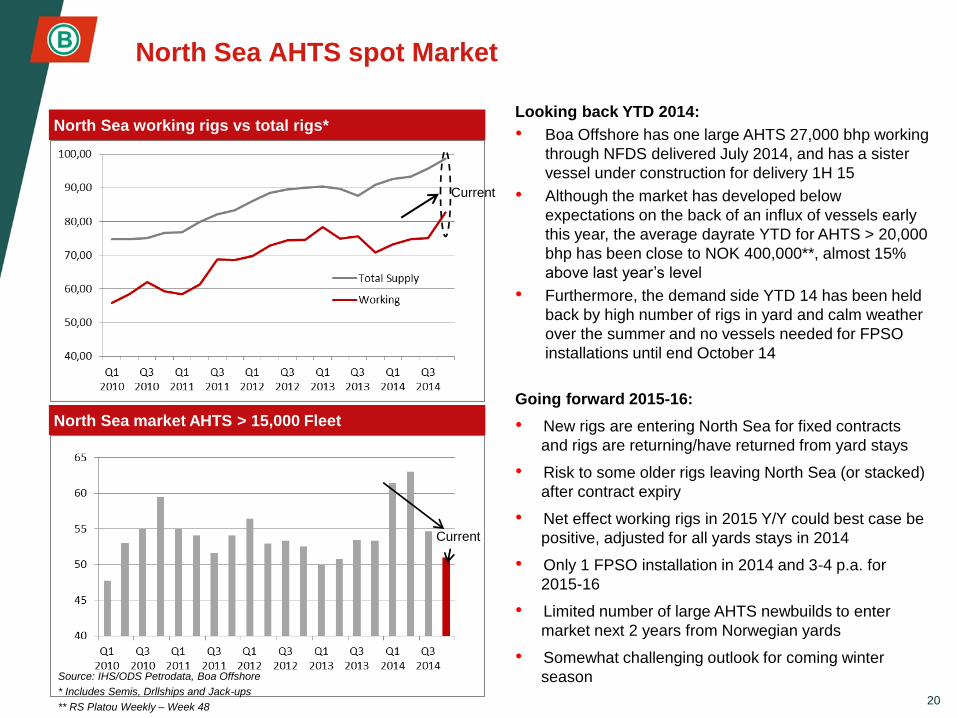

North Sea working rigs vs total rigs*

North Sea AHTS spot Market

Looking back YTD 2014:

• Boa Offshore has one large AHTS 27,000 bhp working

through NFDS delivered July 2014, and has a sister

vessel under construction for delivery 1H 15

• Although the market has developed below

expectations on the back of an influx of vessels early

this year, the average dayrate YTD for AHTS > 20,000

bhp has been close to NOK 400,000**, almost 15%

above last year’s level

• Furthermore, the demand side YTD 14 has been held

back by high number of rigs in yard and calm weather

over the summer and no vessels needed for FPSO

installations until end October 14

Going forward 2015-16:

• New rigs are entering North Sea for fixed contracts

and rigs are returning/have returned from yard stays

• Risk to some older rigs leaving North Sea (or stacked)

after contract expiry

• Net effect working rigs in 2015 Y/Y could best case be

positive, adjusted for all yards stays in 2014

• Only 1 FPSO installation in 2014 and 3-4 p.a. for

2015-16

• Limited number of large AHTS newbuilds to enter

market next 2 years from Norwegian yards

• Somewhat challenging outlook for coming winter

season

20

North Sea market AHTS > 15,000 Fleet

Current

Current

Source: IHS/ODS Petrodata, Boa Offshore

* Includes Semis, Drllships and Jack-ups

** RS Platou Weekly – Week 48