BO Asset finance and leasing (Final) - PwC€¦ · Asset finance and leasing Clarence Leung...

37

Asset finance and leasing www.pwc.com Clarence Leung Director, PwC Hong Kong Brian Leonard Partner, PwC Ireland Lim Maan Huey Partner, PwC Singapore

Transcript of BO Asset finance and leasing (Final) - PwC€¦ · Asset finance and leasing Clarence Leung...

Asset finance and leasing

www.pwc.com

Clarence LeungDirector, PwC Hong KongBrian LeonardPartner, PwC IrelandLim Maan HueyPartner, PwC Singapore

PwC

1. Introduction

2

Lim Maan HueyPartner, PwC Singapore+65 6236 [email protected]

Clarence LeungDirector, PwC Hong Kong+852 2289 [email protected]

Brian LeonardPartner, PwC Ireland+353 1 792 [email protected]

Global Tax Symposium – Asia 2015

PwC

Agenda

1. Developments and updates

2. BEPS recent developments

3. BEPS impacts – network discussion

Global Tax Symposium – Asia 20153

PwC

1.1 Developments and updates – Hong Kong / China

4Global Tax Symposium – Asia 2015

PwC

Latest developments

HONG KONG

5Global Tax Symposium – Asia 2015

PwC

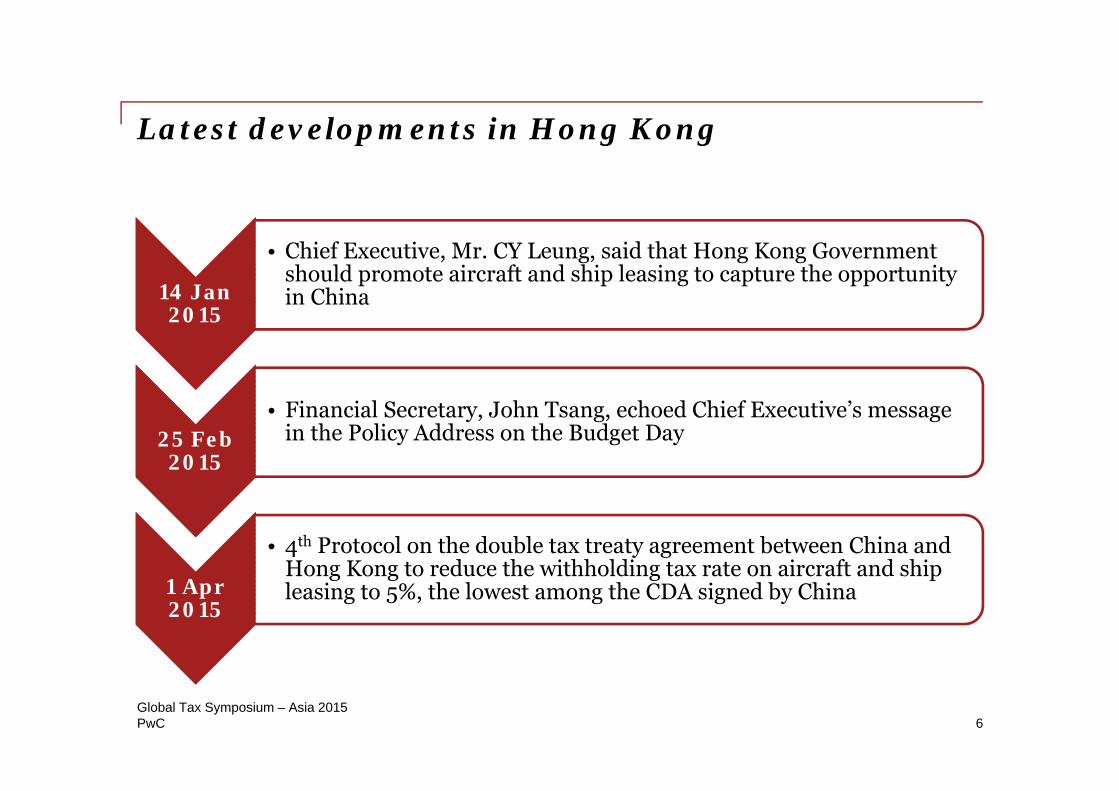

Latest developments in Hong Kong

14 Jan 14 Jan 2015

• Chief Executive, Mr. CY Leung, said that Hong Kong Government should promote aircraft and ship leasing to capture the opportunity in China

25 Feb 25 Feb 2015

• Financial Secretary, John Tsang, echoed Chief Executive’s message in the Policy Address on the Budget Day

Apr 1 Apr 2015

• 4th Protocol on the double tax treaty agreement between China and Hong Kong to reduce the withholding tax rate on aircraft and ship leasing to 5%, the lowest among the CDA signed by China

6Global Tax Symposium – Asia 2015

PwC

Reduced withholding tax on aircraft and shipping rentals

• Hong Kong signed the Fourth Protocol to the Arrangement for the Avoidance of Double Taxation and Prevention of Fiscal Evasion with respect to Taxes on Income with the PRC

• Reduced PRC withholding tax on lease rentals from 7% to cap of 5%

• Hong Kong will be the jurisdiction with the lowest withholding tax applied by rentals paid by PRC lessees, followed by Singapore and Ireland of 6% withholding tax

• Boosts Hong Kong’s development as an asset leasing hub

7Global Tax Symposium – Asia 2015

PwC

Latest developments

CHINA

8Global Tax Symposium – Asia 2015

PwC

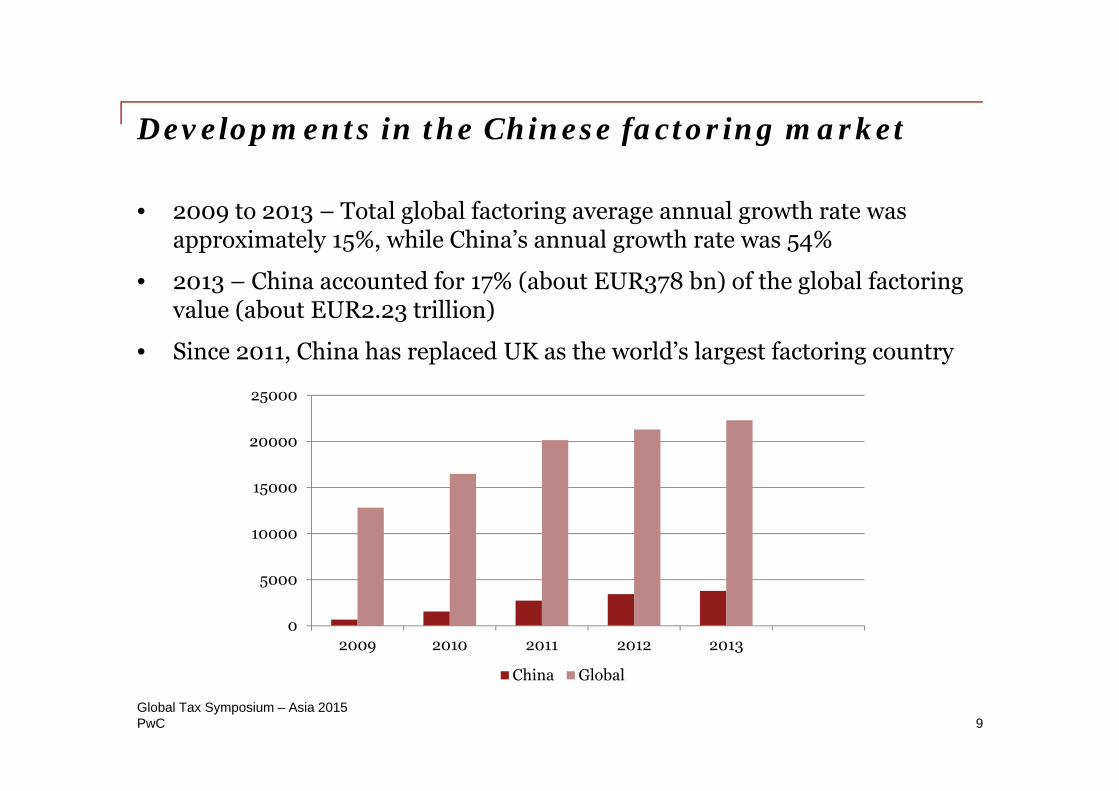

Developments in the Chinese factoring market

• 2009 to 2013 – Total global factoring average annual growth rate was approximately 15%, while China’s annual growth rate was 54%

• 2013 – China accounted for 17% (about EUR378 bn) of the global factoring value (about EUR2.23 trillion)

• Since 2011, China has replaced UK as the world’s largest factoring country

9

0

5000

10000

15000

20000

25000

2009 2010 2011 2012 2013

China Global

Global Tax Symposium – Asia 2015

PwC

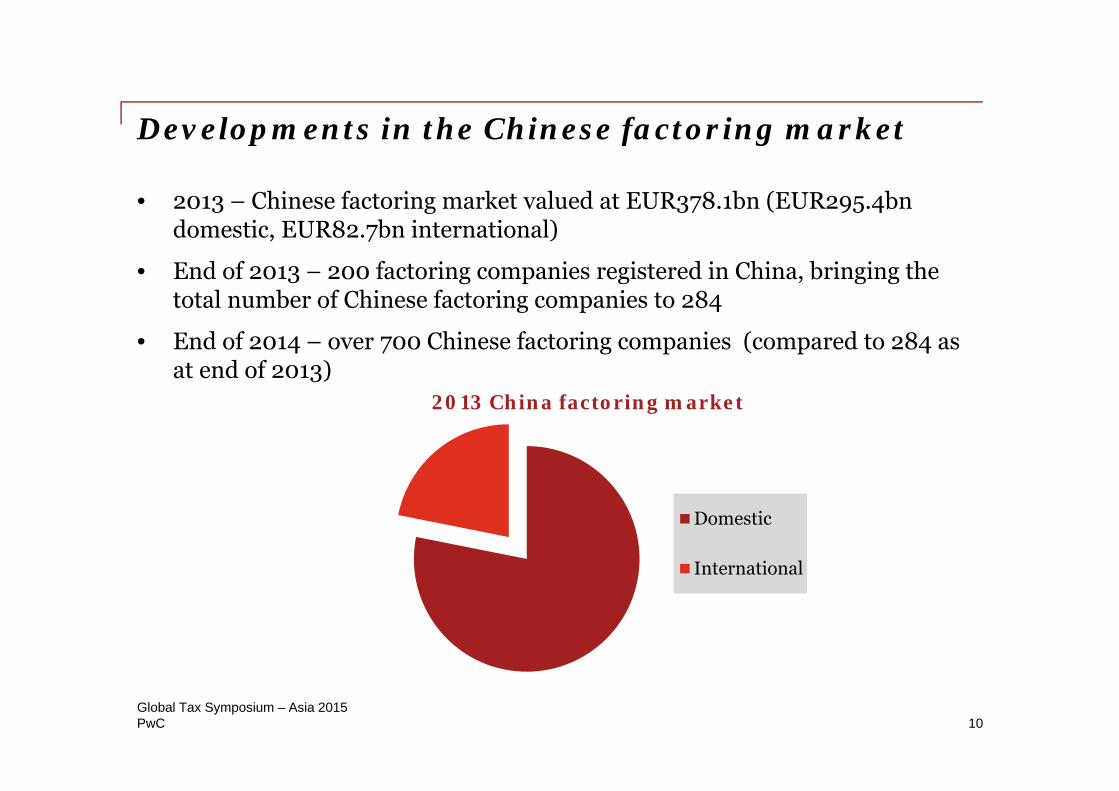

Developments in the Chinese factoring market

• 2013 – Chinese factoring market valued at EUR378.1bn (EUR295.4bn domestic, EUR82.7bn international)

• End of 2013 – 200 factoring companies registered in China, bringing the total number of Chinese factoring companies to 284

• End of 2014 – over 700 Chinese factoring companies (compared to 284 as at end of 2013)

10

2013 China factoring market

Domestic

International

Global Tax Symposium – Asia 2015

PwC

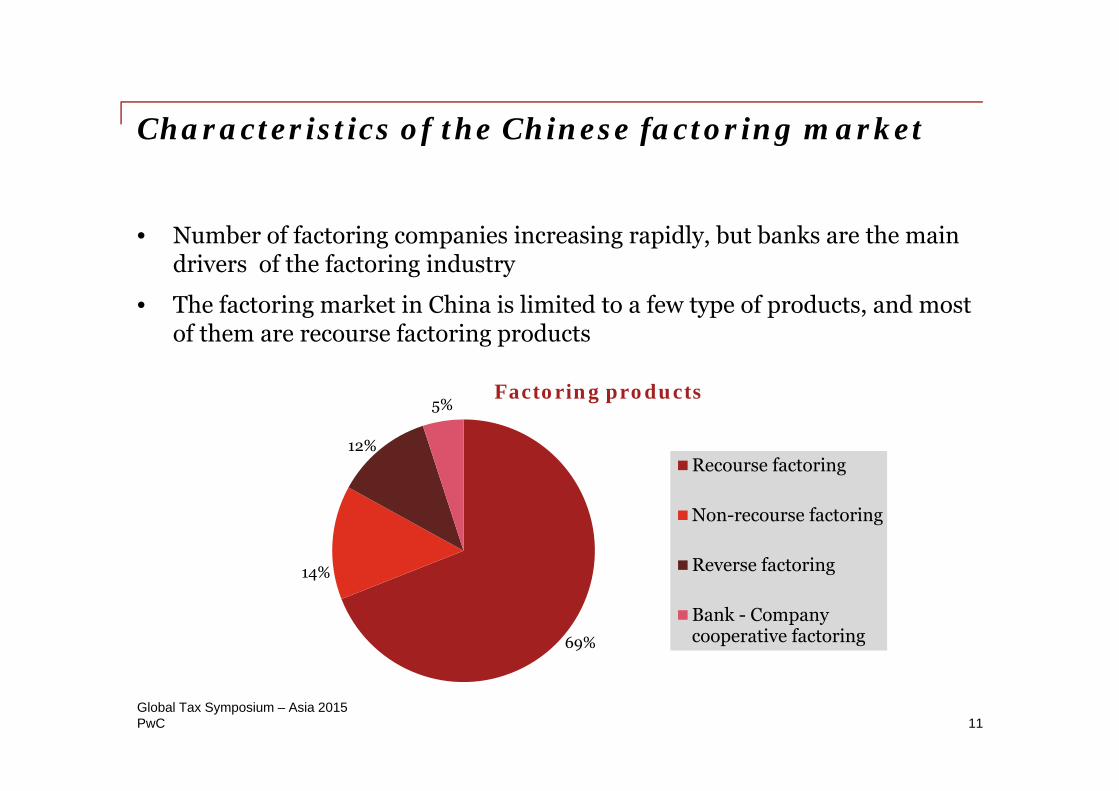

Characteristics of the Chinese factoring market

• Number of factoring companies increasing rapidly, but banks are the main drivers of the factoring industry

• The factoring market in China is limited to a few type of products, and most of them are recourse factoring products

11

69%

14%

12%

5%Factoring products

Recourse factoring

Non-recourse factoring

Reverse factoring

Bank - Companycooperative factoring

Global Tax Symposium – Asia 2015

PwC 12

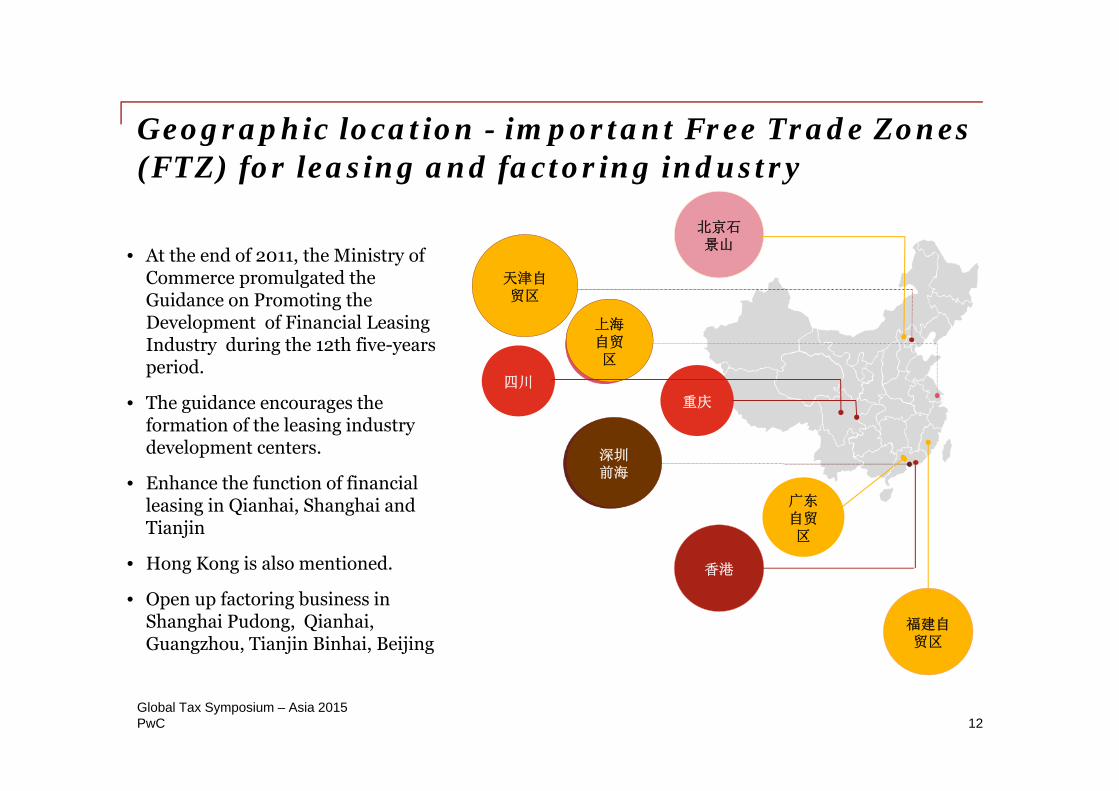

• At the end of 2011, the Ministry of Commerce promulgated the Guidance on Promoting the Development of Financial Leasing Industry during the 12th five-years period.

• The guidance encourages the formation of the leasing industry development centers.

• Enhance the function of financial leasing in Qianhai, Shanghai and Tianjin

• Hong Kong is also mentioned.

• Open up factoring business in Shanghai Pudong, Qianhai, Guangzhou, Tianjin Binhai, Beijing

Geographic location - important Free Trade Zones (FTZ) for leasing and factoring industry

香港

天津自贸区

上海自贸区

深圳前海

福建自贸区

广东自贸区

北京石景山

重庆

四川

Global Tax Symposium – Asia 2015

PwC

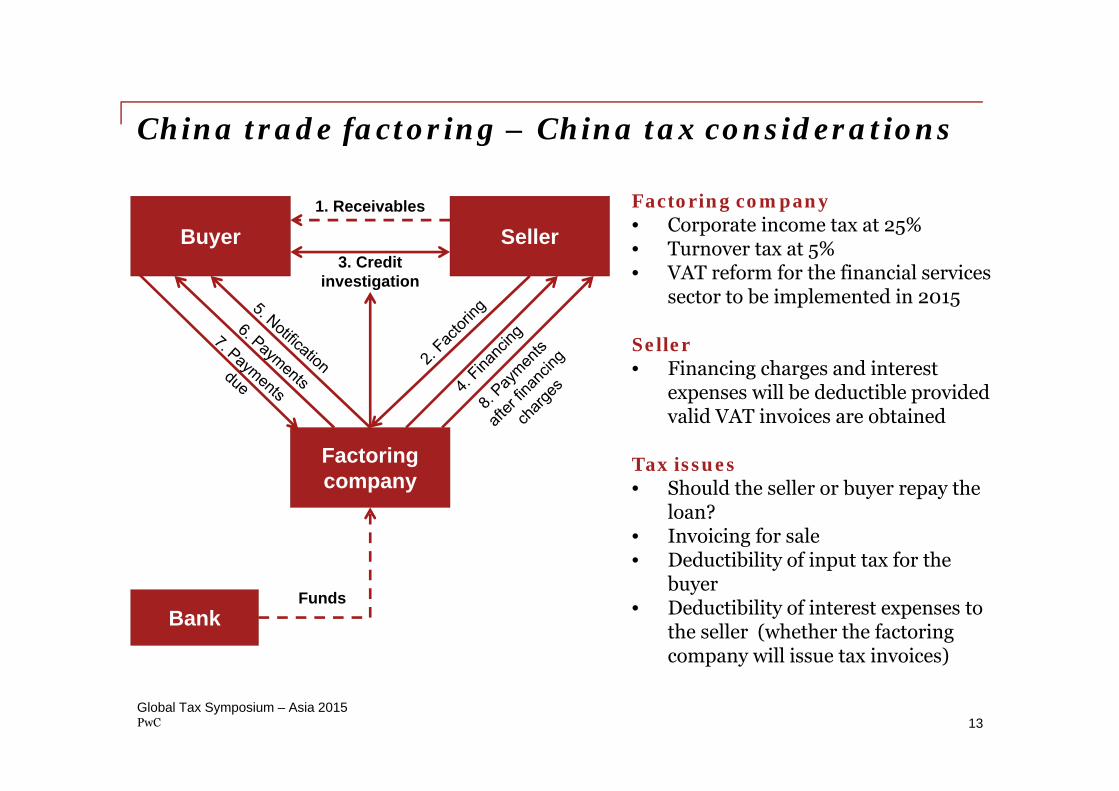

China trade factoring – China tax considerations

Factoring company• Corporate income tax at 25%• Turnover tax at 5%• VAT reform for the financial services

sector to be implemented in 2015

Seller• Financing charges and interest

expenses will be deductible provided valid VAT invoices are obtained

Tax issues• Should the seller or buyer repay the

loan?• Invoicing for sale• Deductibility of input tax for the

buyer• Deductibility of interest expenses to

the seller (whether the factoring company will issue tax invoices)

13

Bank

Factoring company

Funds

Buyer Seller3. Credit

investigation

1. Receivables

Global Tax Symposium – Asia 2015

PwC

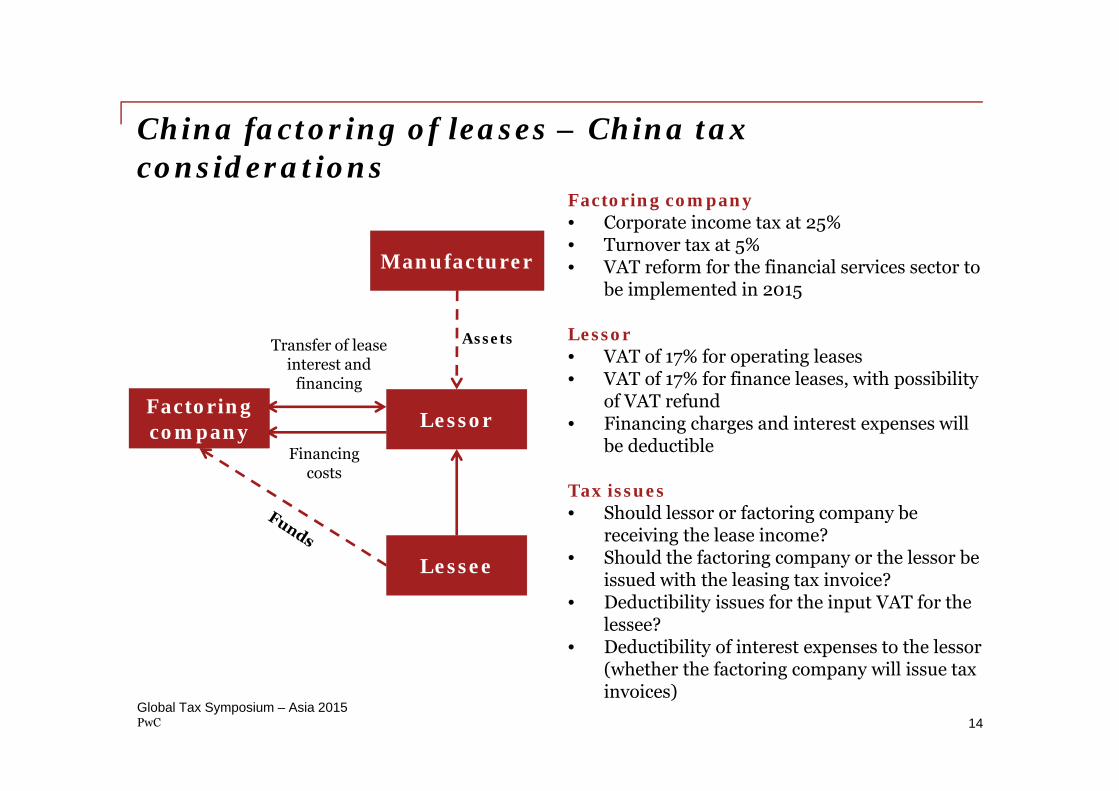

China factoring of leases – China tax considerations

Factoring company• Corporate income tax at 25%• Turnover tax at 5%• VAT reform for the financial services sector to

be implemented in 2015

Lessor• VAT of 17% for operating leases• VAT of 17% for finance leases, with possibility

of VAT refund• Financing charges and interest expenses will

be deductible

Tax issues• Should lessor or factoring company be

receiving the lease income?• Should the factoring company or the lessor be

issued with the leasing tax invoice?• Deductibility issues for the input VAT for the

lessee?• Deductibility of interest expenses to the lessor

(whether the factoring company will issue tax invoices)

14

Lessee

Transfer of lease interest and

financing

Financing costs

LessorFactoring company

Manufacturer

Assets

Global Tax Symposium – Asia 2015

PwC

1.2 Developments and updates –Ireland

15Global Tax Symposium – Asia 2015

PwC

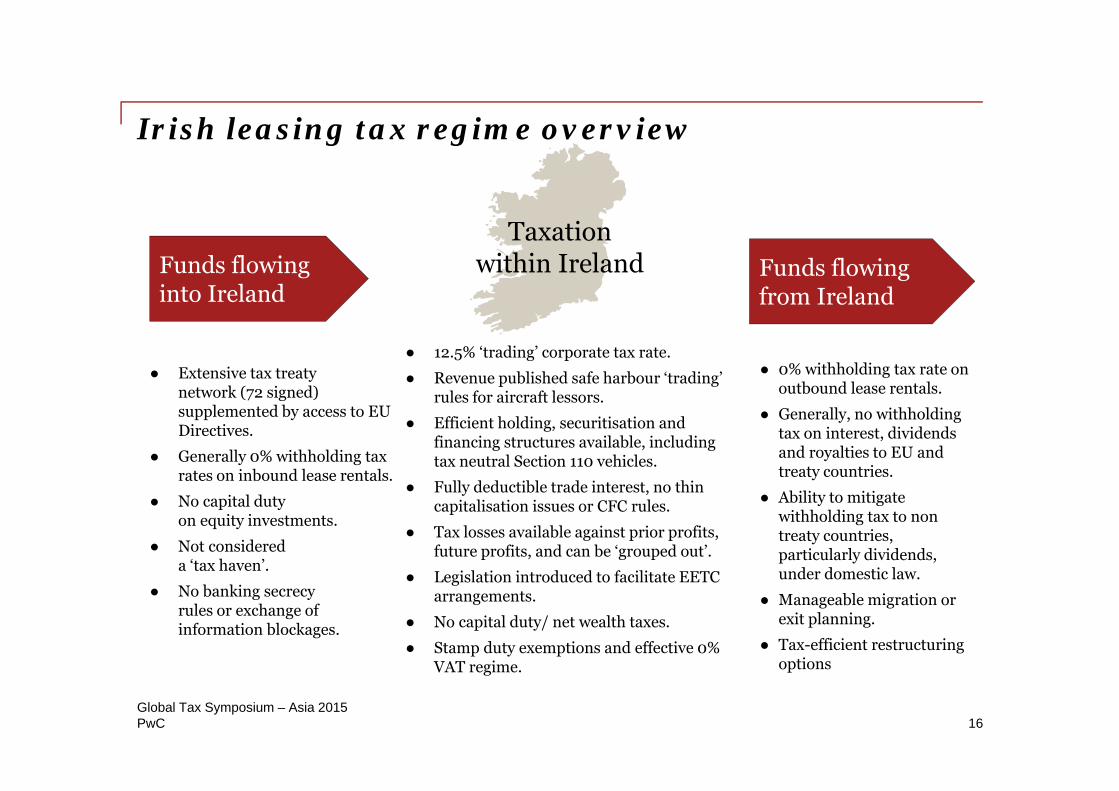

Irish leasing tax regime overview

16

Funds flowing from Ireland

Funds flowing into Ireland

● Extensive tax treaty network (72 signed) supplemented by access to EU Directives.

● Generally 0% withholding tax rates on inbound lease rentals.

● No capital duty on equity investments.

● Not considered a ‘tax haven’.

● No banking secrecy rules or exchange of information blockages.

Taxation within Ireland

● 12.5% ‘trading’ corporate tax rate.

● Revenue published safe harbour ‘trading’ rules for aircraft lessors.

● Efficient holding, securitisation and financing structures available, including tax neutral Section 110 vehicles.

● Fully deductible trade interest, no thin capitalisation issues or CFC rules.

● Tax losses available against prior profits, future profits, and can be ‘grouped out’.

● Legislation introduced to facilitate EETC arrangements.

● No capital duty/ net wealth taxes.

● Stamp duty exemptions and effective 0% VAT regime.

● 0% withholding tax rate on outbound lease rentals.

● Generally, no withholding tax on interest, dividends and royalties to EU and treaty countries.

● Ability to mitigate withholding tax to non treaty countries, particularly dividends, under domestic law.

● Manageable migration or exit planning.

● Tax-efficient restructuring options

Global Tax Symposium – Asia 2015

PwC

Section 110 company

17Global Tax Symposium – Asia 2015

What is a Section 110 company• An Irish Special Purpose Vehicle (SPV) can be funded by way of external debt and/or

internal debt/’equity’. The SPV will use these funds to acquire assets (including aircraft/engines) . The internal debt/equity generally takes the form of a profit participation loan (PPL) issued by the SPV. This PPL will be the mechanism used to extract surplus cash and/or taxable profits from the SPV.

• Takes the form of a normal Irish company. Flexibility in corporate structure -can be formed as limited or unlimited company, private or public.

• A Section 110 company must elect into the regime. To do so a number of conditions must be satisfied. The main conditions require that the company should (1) be tax resident in Ireland, (2) carry on a business of acquiring, holding or managing qualifying assets (can include the leasing of aircraft, engines, etc.) and (3) holds qualifying assets with a market value of not less than EUR10m on the day on which the assets are first acquired.

PwC

Section 110 company

18Global Tax Symposium – Asia 2015

Taxation of a Section 110 company

• Section 110 companies are taxed on their profits at the higher rate of Irish corporation tax of 25%.

• Taxable profits are calculated under the rules applicable to normal trading companies. This means that tax deductions are allowable for normal trading expenses such as trading interest, broker fees, management fees, etc. In addition, a deduction is allowed for profit participating interest.

• Certain anti-avoidance provisions which restrict deductibility of interest paid need to be considered.

• Small taxable spread (typically EUR1,000/EUR5,000 annually) left at the level of the Section 110 company each year (the PPL is the mechanism used to achieve the small spread).

• Section 110 companies are entitled to tax depreciation/capital allowances where the usual prerequisite conditions are satisfied.

• Section 110 companies benefit from Ireland’s DTA network and also EU Directives in respect of inbound flows of income or gains.

• Any tax losses incurred by the Section 110 may be carried forward against future taxable profits but cannot be carried back against the profits of an earlier accounting period or relieved against the profits of any other group company.

PwC

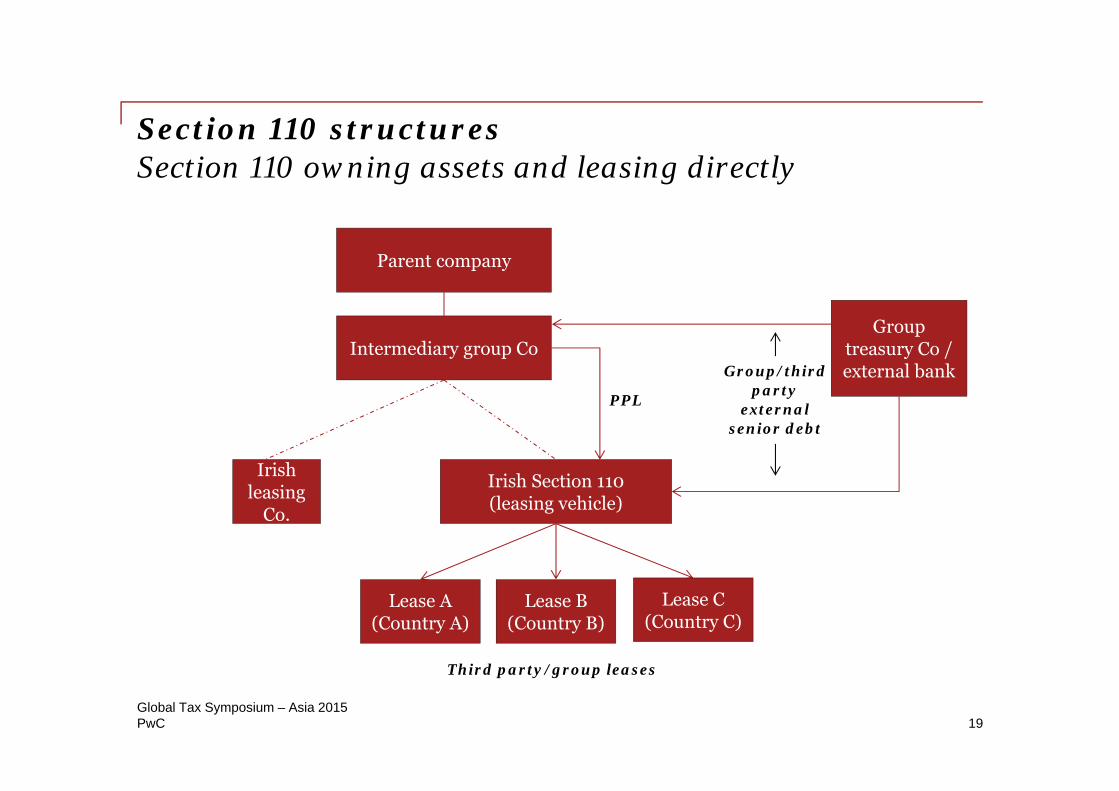

Section 110 structuresSection 110 owning assets and leasing directly

19

Parent company

Irish Section 110(leasing vehicle)

Irish leasing

Co.

PPL

Third party/group leases

Lease A(Country A)

Lease B(Country B)

Lease C(Country C)

Group treasury Co / external bankGroup/third

party external

senior debt

Intermediary group Co

Global Tax Symposium – Asia 2015

PwC

PwC Ireland treaty submission/ treaty updatesTax Director Network (1/2)

20Global Tax Symposium – Asia 2015

• PwC Ireland established the Aviation Leasing Tax Director Network in 2014 . The network comprises senior tax and finance professionals of the largest global aircraft lessors (based in Ireland and abroad) as well as major engine, helicopter and OEM lessors.

• The network was established to share Irish and international industry tax developments with a view to representing the industry at relevant governmental and OECD level where appropriate through round table discussions.

• While Ireland’s double tax treaty continues to expand, (see further below), the network made a submission to the Irish Revenue with regard to specific double tax treaties which would be beneficial for the aircraft leasing industry in Ireland.

PwC

PwC Ireland treaty submission/ treaty updatesTax Director Network (2/2)

21Global Tax Symposium – Asia 2015

• The submission was made to the Irish Revenue on 6 March 2015 and outlined a list of double tax treaties which the network believes require renegotiation (Japan, Australia and Malaysia).

• Also included in this submission was a list of territories with which Ireland does not currently have a double tax treaty but whose leasing business is steadily increasing and therefore Irish lessors would greatly benefit from double tax treaties with these countries (Indonesia, Brazil, Kazakhstan, Argentina, Nigeria, Taiwan and Mongolia).

• PwC Ireland had a follow up meeting with the Irish Revenue in relation to the submission.

PwC

PwC Ireland treaty submission/ treaty updatesTreaty network recent developments

22Global Tax Symposium – Asia 2015

• Ireland has signed comprehensive double taxation agreements with 72 countries, of which 68 are in effect, which continues to expand.

• New agreements have been signed with Botswana, Thailand, Ukraine, Ethiopia, Zambia and Pakistan.

• Treaty discussions have commenced recently with Kazakhstan.

• A new agreement with Turkmenistan is expected to be signed shortly.

• Negotiations are ongoing for new treaties with Azerbaijan, Jordan and Ghana.

PwC

Domestic legislative and policy updates

23Global Tax Symposium – Asia 2015

Employment Tax – Special Assignee Relief Programme (SARP)• Introduced in 2012 and extended to 2017.

• Removal of relief threshold amount of EUR500,000.

• Requirement not to be resident elsewhere removed.

• Relaxation for the requirement to perform all of their duties in Ireland as well as reduction in previous employment from 12 months to 6 months.

Employment Tax – Foreign Earnings Deduction (FED)• Extended to 2017, allows a deduction of up to EUR35,000 per annum for employees

who spend a minimum 40 days outside Ireland (reduced from 60 days).

• Qualifying countries extended to include Chile, Indonesia, Japan, Malaysia, Saudi Arabia, Singapore, United Arab Emirates and more.

PwC

Domestic legislative and policy updates

24Global Tax Symposium – Asia 2015

Transfer Pricing • TPCR (Irish Revenue Transfer Pricing Compliance Review) previously introduced

however Irish Revenue now conducting field Audits.

• Domestic legislation in line with international standards.

National Aviation Policy• Ireland has also published a draft national aviation policy, which specifically

endorses the aircraft leasing industry.• Evidence of continued support from governmental and regulatory authorities.

PwC

1.3 Developments and updates –Singapore

25Global Tax Symposium – Asia 2015

PwC

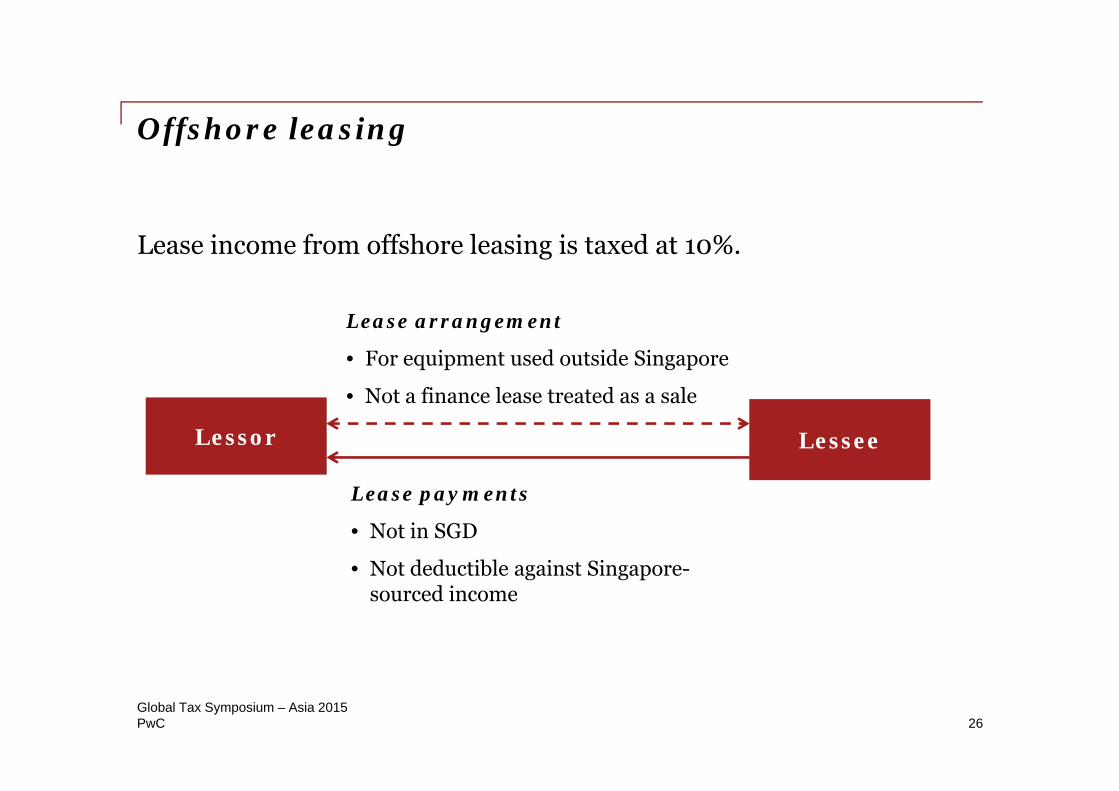

Offshore leasing

26

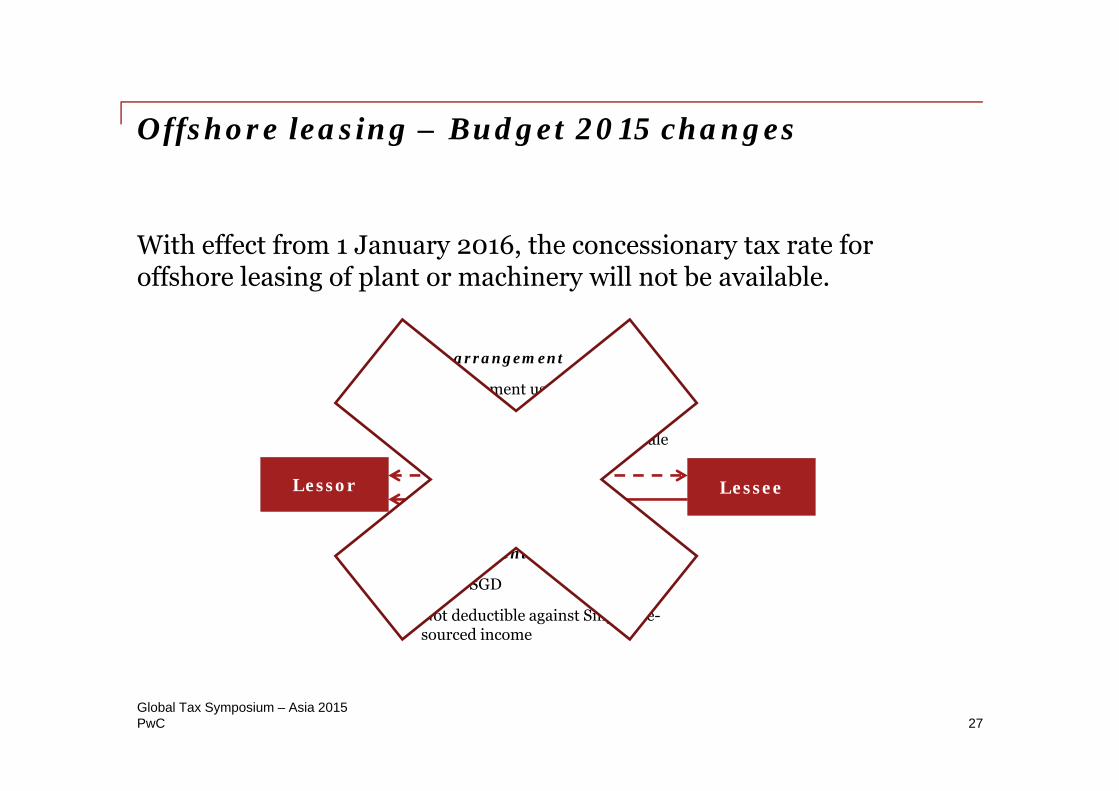

Lessee

Lease arrangement

• For equipment used outside Singapore

• Not a finance lease treated as a sale

Lessor

Lease payments

• Not in SGD

• Not deductible against Singapore-sourced income

Lease income from offshore leasing is taxed at 10%.

Global Tax Symposium – Asia 2015

PwC

Offshore leasing – Budget 2015 changes

27

Lessee

Lease arrangement

• For equipment used outside Singapore

• Not a finance lease treated as a sale

Lessor

Lease payments

• Not in SGD

• Not deductible against Singapore-sourced income

With effect from 1 January 2016, the concessionary tax rate for offshore leasing of plant or machinery will not be available.

Global Tax Symposium – Asia 2015

PwC

Maritime sector – tax concessions

28

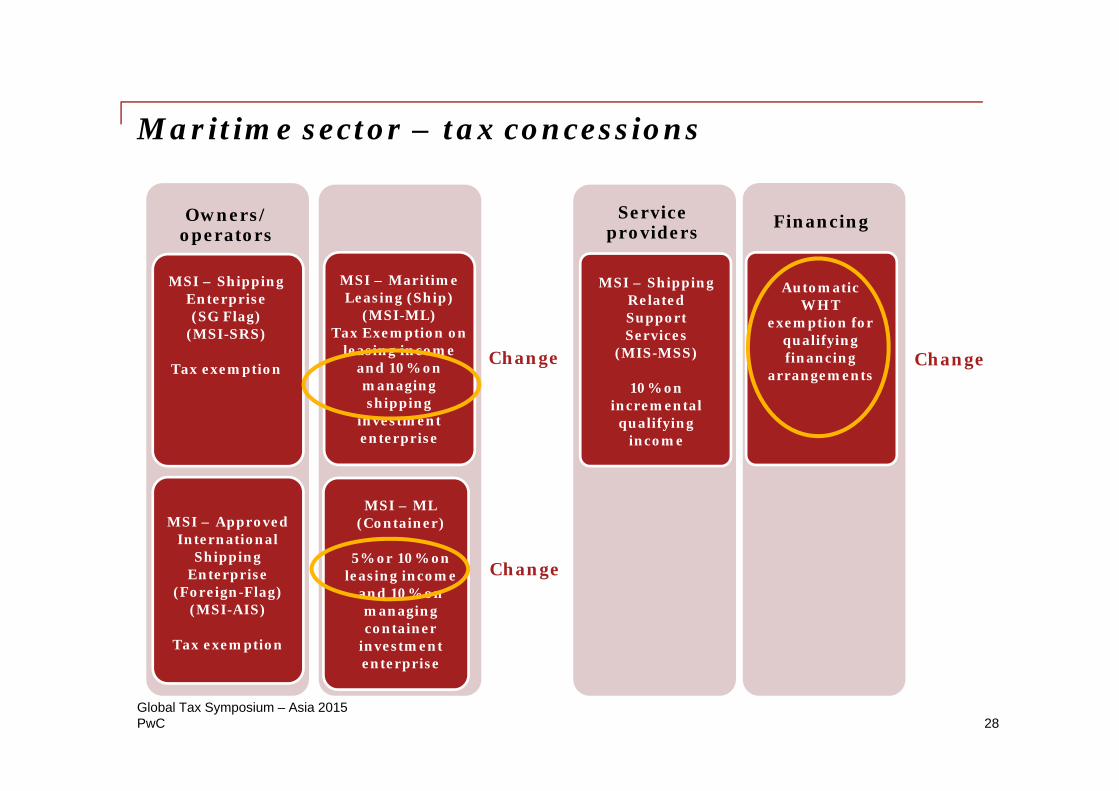

Owners/ operators

MSI – Shipping Enterprise (SG Flag)

(MSI-SRS)

Tax exemption

MSI – Approved International

Shipping Enterprise

(Foreign-Flag)(MSI-AIS)

Tax exemption

MSI – Maritime Leasing (Ship)

(MSI-ML)Tax Exemption on

leasing income and 10% on managing shipping

investment enterprise

MSI – ML (Container)

5% or 10% on leasing income

and 10% on managing container

investment enterprise

MSI – Shipping Related Support Services

(MIS-MSS)

10% on incremental

qualifyingincome

Automatic WHT

exemption for qualifying financing

arrangements

Financing

ChangeChange

Change

Service providers

Global Tax Symposium – Asia 2015

PwC

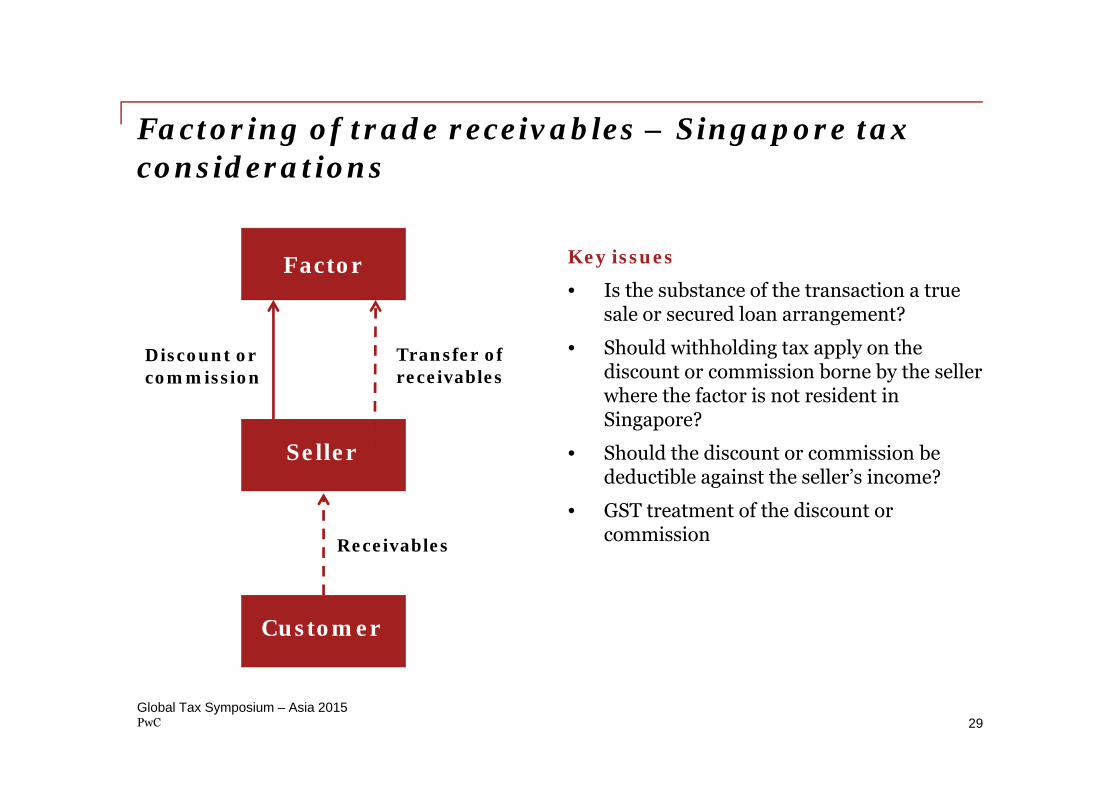

Factoring of trade receivables – Singapore tax considerations

Key issues

• Is the substance of the transaction a true sale or secured loan arrangement?

• Should withholding tax apply on the discount or commission borne by the seller where the factor is not resident in Singapore?

• Should the discount or commission be deductible against the seller’s income?

• GST treatment of the discount or commission

29

Factor

Seller

Customer

Receivables

Transfer of receivables

Discount or commission

Global Tax Symposium – Asia 2015

PwC

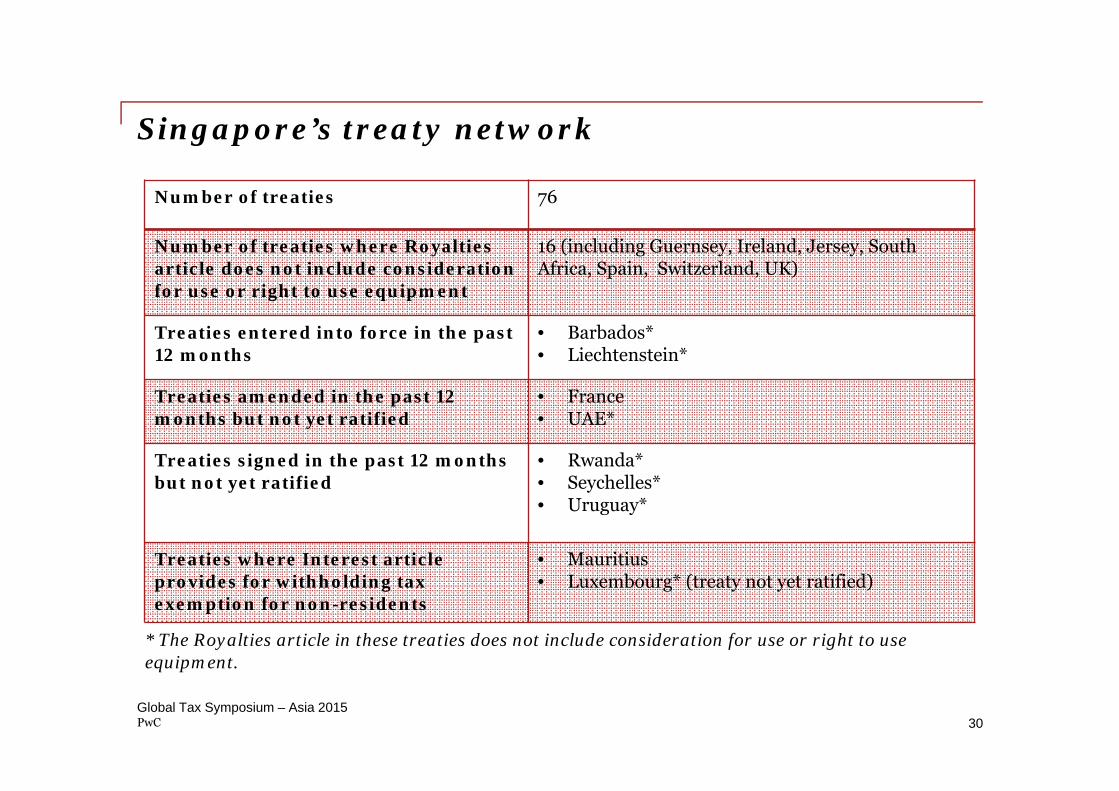

Singapore’s treaty network

30

Number of treaties 76

Number of treaties where Royalties article does not include consideration for use or right to use equipment

16 (including Guernsey, Ireland, Jersey, South Africa, Spain, Switzerland, UK)

Treaties entered into force in the past 12 months

• Barbados*• Liechtenstein*

Treaties amended in the past 12 months but not yet ratified

• France• UAE*

Treaties signed in the past 12 months but not yet ratified

• Rwanda*• Seychelles*• Uruguay*

Treaties where Interest article provides for withholding tax exemption for non-residents

• Mauritius• Luxembourg* (treaty not yet ratified)

* The Royalties article in these treaties does not include consideration for use or right to use equipment.

Global Tax Symposium – Asia 2015

PwC

2. BEPS recent developments

31Global Tax Symposium – Asia 2015

PwC

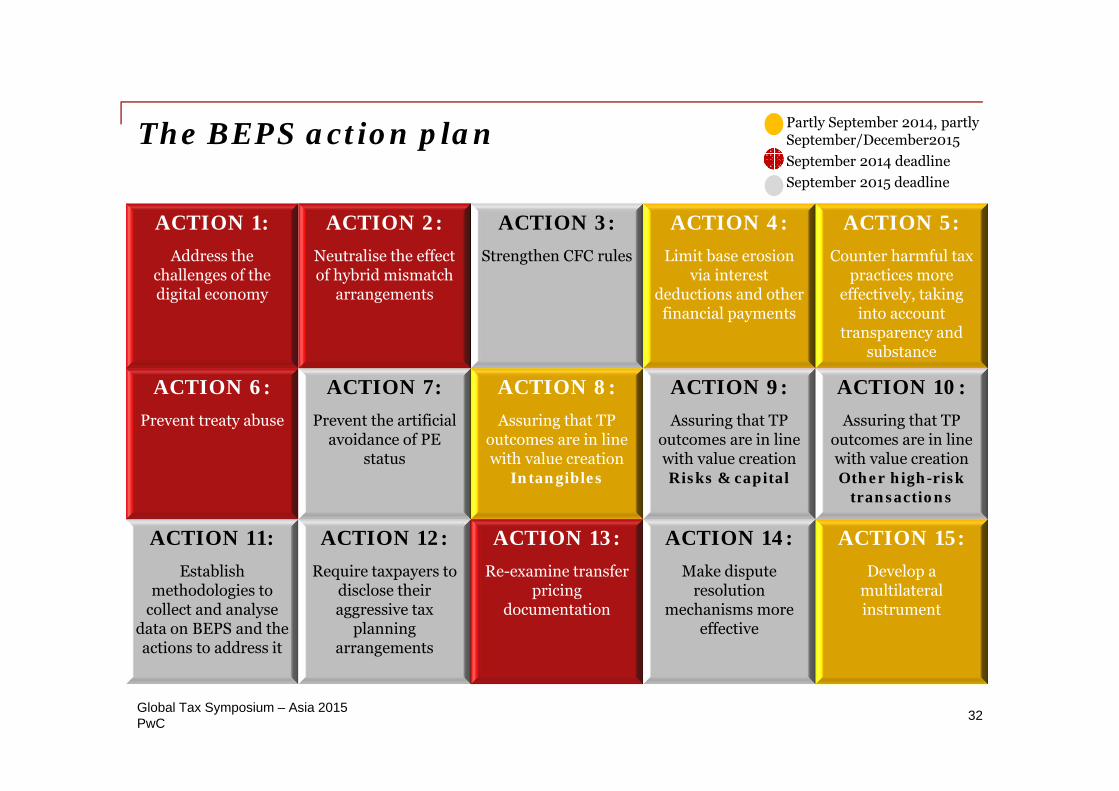

The BEPS action plan

ACTION 1:Address the

challenges of the digital economy

ACTION 2:Neutralise the effect of hybrid mismatch

arrangements

ACTION 3:Strengthen CFC rules

ACTION 4:Limit base erosion

via interest deductions and other

financial payments

ACTION 5:Counter harmful tax

practices more effectively, taking

into account transparency and

substance

ACTION 6:Prevent treaty abuse

ACTION 7:Prevent the artificial

avoidance of PE status

ACTION 8:Assuring that TP

outcomes are in line with value creation

Intangibles

ACTION 9:Assuring that TP

outcomes are in line with value creation Risks & capital

ACTION 10:Assuring that TP

outcomes are in line with value creation Other high-risk

transactions

ACTION 11:Establish

methodologies to collect and analyse

data on BEPS and the actions to address it

ACTION 12:Require taxpayers to

disclose their aggressive tax

planning arrangements

ACTION 13:Re-examine transfer

pricing documentation

ACTION 14:Make dispute

resolutionmechanisms more

effective

ACTION 15:Develop a

multilateral instrument

September 2014 deadlineSeptember 2015 deadline

Partly September 2014, partly September/December2015

32Global Tax Symposium – Asia 2015

PwC

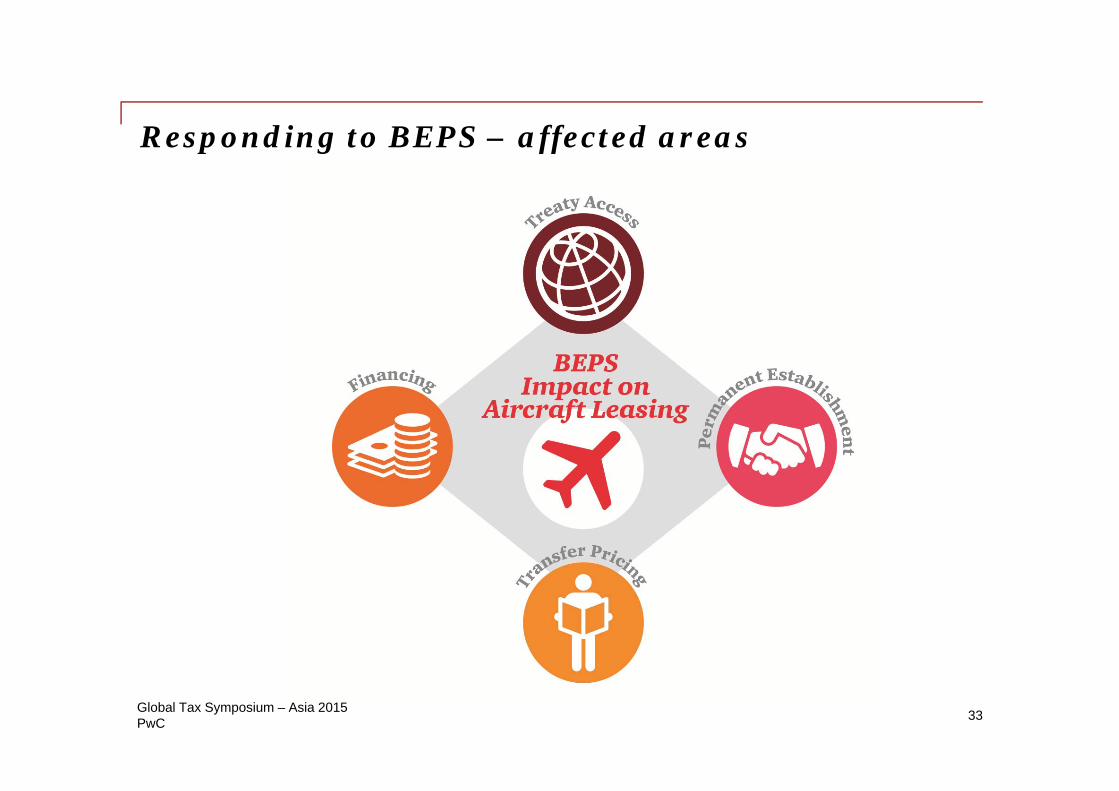

Responding to BEPS – affected areas

33Global Tax Symposium – Asia 2015

PwC

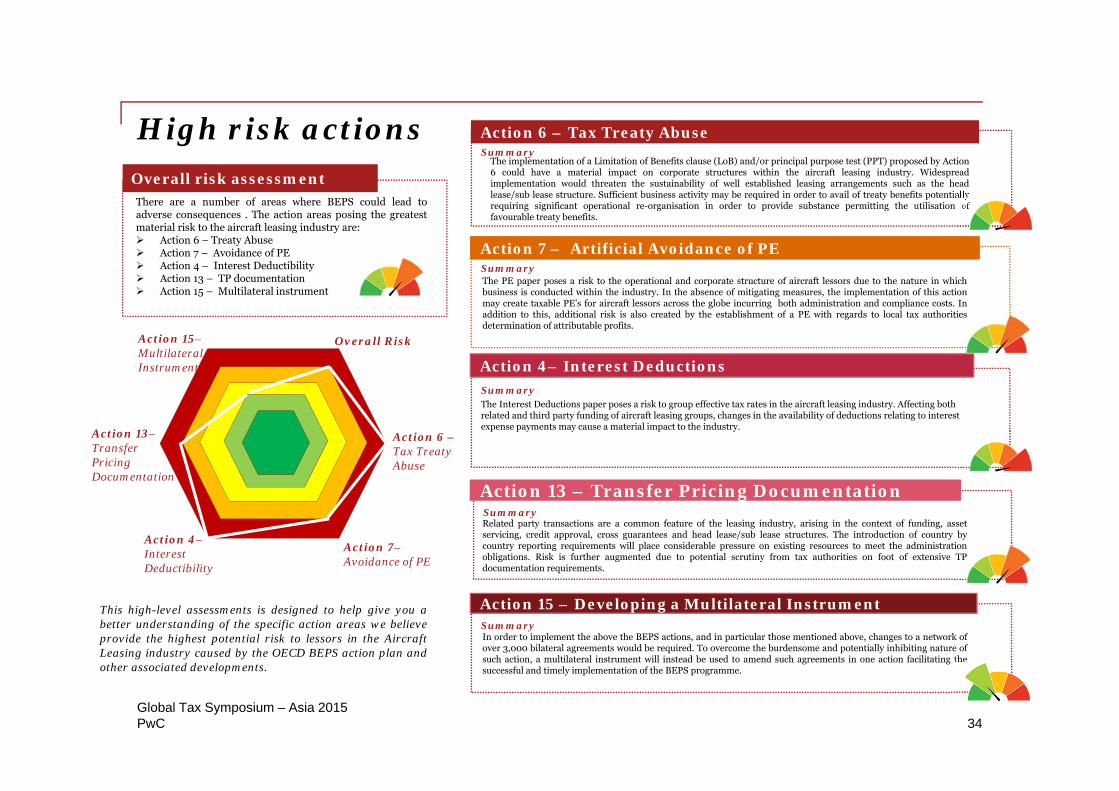

High risk actions

This high-level assessments is designed to help give you abetter understanding of the specific action areas we believeprovide the highest potential risk to lessors in the AircraftLeasing industry caused by the OECD BEPS action plan andother associated developments.

Summary

Action 6 – Tax Treaty Abuse

Action 13–Transfer Pricing Documentation

Overall Risk

Summary

Action 4– Interest Deductions

Overall risk assessmentThere are a number of areas where BEPS could lead toadverse consequences . The action areas posing the greatestmaterial risk to the aircraft leasing industry are: Action 6 – Treaty Abuse Action 7 – Avoidance of PE Action 4 – Interest Deductibility Action 13 – TP documentation Action 15 – Multilateral instrument

Action 6 –Tax Treaty Abuse

The implementation of a Limitation of Benefits clause (LoB) and/or principal purpose test (PPT) proposed by Action6 could have a material impact on corporate structures within the aircraft leasing industry. Widespreadimplementation would threaten the sustainability of well established leasing arrangements such as the headlease/sub lease structure. Sufficient business activity may be required in order to avail of treaty benefits potentiallyrequiring significant operational re-organisation in order to provide substance permitting the utilisation offavourable treaty benefits.

Summary

Action 7 – Artificial Avoidance of PE

Summary

Action 13 – Transfer Pricing Documentation

Action 7–Avoidance of PE

Action 4–Interest Deductibility

Action 15–Multilateral Instrument

The PE paper poses a risk to the operational and corporate structure of aircraft lessors due to the nature in whichbusiness is conducted within the industry. In the absence of mitigating measures, the implementation of this actionmay create taxable PE’s for aircraft lessors across the globe incurring both administration and compliance costs. Inaddition to this, additional risk is also created by the establishment of a PE with regards to local tax authoritiesdetermination of attributable profits.

The Interest Deductions paper poses a risk to group effective tax rates in the aircraft leasing industry. Affecting both related and third party funding of aircraft leasing groups, changes in the availability of deductions relating to interest expense payments may cause a material impact to the industry.

Related party transactions are a common feature of the leasing industry, arising in the context of funding, assetservicing, credit approval, cross guarantees and head lease/sub lease structures. The introduction of country bycountry reporting requirements will place considerable pressure on existing resources to meet the administrationobligations. Risk is further augmented due to potential scrutiny from tax authorities on foot of extensive TPdocumentation requirements.

Summary

Action 15 – Developing a Multilateral Instrument

In order to implement the above the BEPS actions, and in particular those mentioned above, changes to a network ofover 3,000 bilateral agreements would be required. To overcome the burdensome and potentially inhibiting nature ofsuch action, a multilateral instrument will instead be used to amend such agreements in one action facilitating thesuccessful and timely implementation of the BEPS programme.

34Global Tax Symposium – Asia 2015

PwC

3. BEPS impact – network discussion

35Global Tax Symposium – Asia 2015

PwC

Key considerations

36Global Tax Symposium – Asia 2015

• Final submissions/ representation on PE and Treaty Actions.

• Unilateral developments influenced by BEPS Agenda.

• Likely impact on corporate structure and business model.

• Questions for all:

- Have government / tax authorities in your country been influenced by BEPS Actions to date / have they introduced any unilateral legislation or commented on BEPS?

- Has there been a response by any of the lessors /lessees in your jurisdiction?

- Are you considering ways to mitigate the potential effect of these developments or are you still adopting a wait and see approach?

Thank you.

The information contained in this presentation is of a general nature only. It is not meant to be comprehensive and does not constitute the rendering of legal, tax or other professional advice or service by PricewaterhouseCoopers Ltd. ("PwC"). PwC has no obligation to update the information as law and practices change. The application and impact of laws can vary widely based on the specific facts involved. Before taking any action, please ensure that you obtain advice specific to your circumstances from your usual PwC client service team or your other advisers.

The materials contained in this presentation were assembled in May 2015 and were based on the law enforceable and information available at that time.

© 2015 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.