BMW GROUP M AUTOMOBILES ARE THE VERY SPORTY AND DYNAMIC END OF OUR MODEL RANGE. PRODUCTS BMW Group...

40

June 2016 BMW GROUP INVESTOR PRESENTATION

Transcript of BMW GROUP M AUTOMOBILES ARE THE VERY SPORTY AND DYNAMIC END OF OUR MODEL RANGE. PRODUCTS BMW Group...

June 2016

BMW GROUPINVESTOR PRESENTATION

STRATEGY NUMBER ONE > NEXT

BMW Group Investor Presentation, June 2016 Page 2

Premium brand strategy2001/

2003

Strategy Number ONE 2007

FORWARD-LOOKING STRATEGIES LEADING TO A SUCCESSFUL CORPORATE DEVELOPMENT SINCE 2001.

2016

BMW Group Investor Presentation, June 2016 Page 3

STRATEGIC APPROACH

> Brands & Design

We are leading the BMW Group into a new era:

We leverage innovative technologies, digitalization

and sustainability to deliver unique customer experiences.

> Products

> Technologies

> Customer Experience & Services

> Digitalization

> Profitability

VISION

We are Number ONE.

We inspire people on the move:

We shape tomorrow‘s individual

premium mobility.COMPETITIVE

ADVANTAGE

We unite excitement, responsibility and

success: We have the most emotional

products and attractive

services.

CORPORATE CULTURE

We create the future:

We combine operational

excellence and fresh

thinking.

BMW Group Investor Presentation, June 2016 Page 4

LEADERSHIP DRIVEN BY ASPIRATIONAL BRAND PORTFOLIO AND HIGHLY EMOTIONAL PRODUCTS. BRANDS & DESIGN

Design

BMW Group Investor Presentation, June 2016

Premium Brands

Luxury

Dynamic Efficient

Compact/Small

Now

Target group

Page 5

ATTRACTIVE PREMIUM BRANDS PROVIDE THE BASISFOR A FURTHER EXPANSION OF THE PRODUCT PORTFOLIO. BRANDS & DESIGN

BMW Group Investor Presentation, June 2016 Page 6

SIXTH GENERATION OF BMW 7 SERIES:THE NEW BENCHMARK IN THE LUXURY SEGMENT. PRODUCTS

Page 7

BMW Group Investor Presentation, June 2016 Page 8

KEEPING THE LEAD – FURTHER EXPANSION OF THE X-PORTFOLIO PLANNED UNTIL 2020. PRODUCTS

BMW X1

BMW X5

BMW X3

BMW X6

BMW X4

BMW X7

BMW M AUTOMOBILES ARE THE VERY SPORTY AND DYNAMIC END OF OUR MODEL RANGE. PRODUCTS

BMW Group Investor Presentation, June 2016

BRAND SHAPER BMW M4 GTS

BMW M235i Coupé

BMW M2 Coupé

BMW 228i Coupé

AN EXAMPLE:

M AUTOMOBILES

M PERFORMANCE

AUTOMOBILES

TOP MODEL

CORE BRAND

Page 9

CORE BRAND MODEL

WITH M SPORT PACKAGE

BMW 420i Coupé with

M sport package

iPERFORMANCE AND BMW i –BALANCING THE PRODUCT PORTFOLIO . PRODUCTS

BMW Group Investor Presentation, June 2016

DYNAMIC EFFICIENT

M Core Models

High

Performance

M Performance

Performance

Champions

Core Models PHEVs

Electrified

Efficiency

Champions

BEVs

Visionary

Mobility

The interplay of BMW M and BMW i enhances competitive differentiation

(representation of the scope of the BMW brand).

BMW brand framework for product portfolio

Page 10

SEVEN ELECTRIFIED BMW MODELS:FURTHER MODELS TO COME. PRODUCTS

BMW X5 xDrive40eiPerformance

BMW 740eiPerformance

BMW 225xeiPerformance

BMW 330eiPerformance

BMW i3 BMW i8

BMW 530Le

BMW Group Investor Presentation, June 2016 Page 11

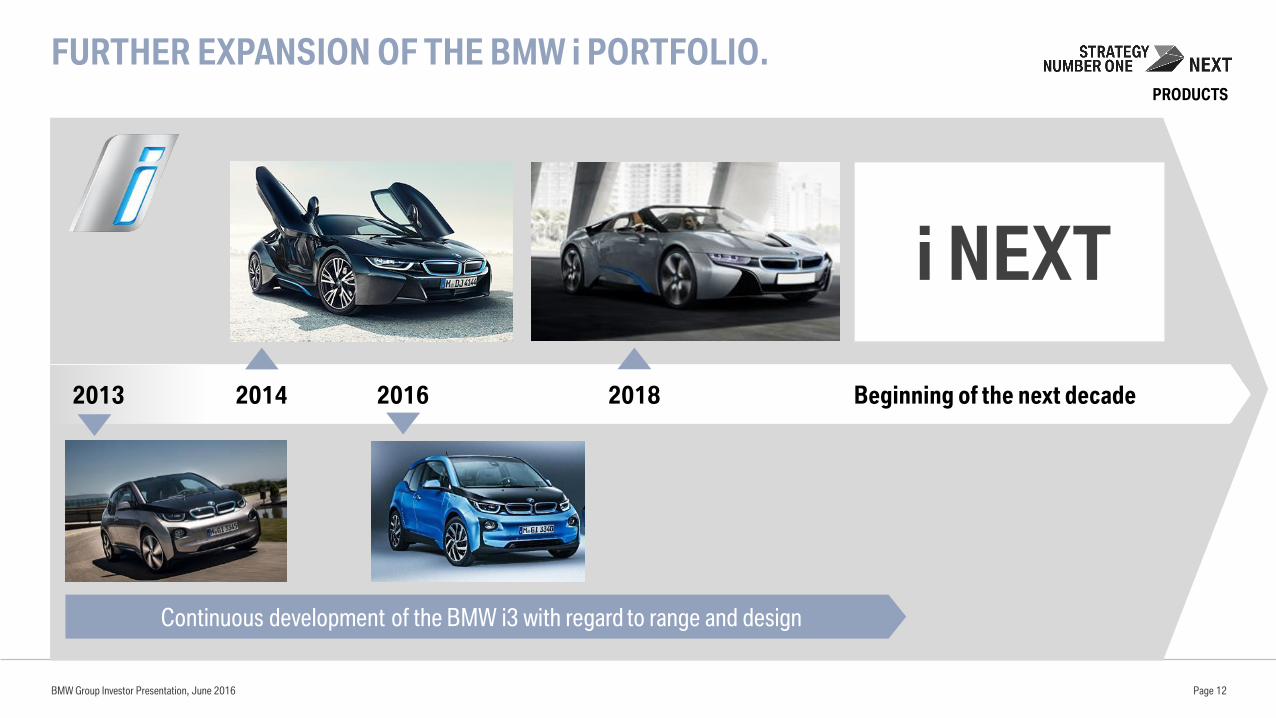

FURTHER EXPANSION OF THE BMW i PORTFOLIO.PRODUCTS

2018 Beginning of the next decade20142013

Continuous development of the BMW i3 with regard to range and design

2016

BMW Group Investor Presentation, June 2016 Page 12

i NEXT

PROJECT i 2.0:THE BMW i NEXT IS THE FUTURE OF MOBILITY.

Artificial Intelligence

Interior of the future

Highly automated driving

Autonomous

driving

Electrification

Lightweight

construction

New sportiness

Purpose-built

Sustainability

Connectivity

BMW Group Investor Presentation, June 2016 Page 13

TECHNOLOGIES

BMW i NEXT

ENSURING OUR POSITION AS TECHNOLOGY LEADER.

Technology and innovation leader

EfficientDynamics

NEXTHydrogen

Artificial Intelligence

Autonomous driving

Connectivity

TECHNOLOGIES

Future focus:Powertrain technologies

Future focus:Digitalization

BMW Group Investor Presentation, June 2016 Page 14

THE NEXT STEPS ARE HIGHLY AND FULLY AUTONOMOUS DRIVING.

BMW Group Investor Presentation, June 2016

TECHNOLOGIES

Take over request(“Eyes-off”)

3 – High-Automation 4 – Full-Automation

General awareness

No take over request(“Mind-off”)

5 – Autonomous

No driver

0 – Driver Only

No active

assistance system

1 – Assistance

Early

warning systems

such as cruise

control/ speed

assistant

(“Feet-off”)

2 – Semi-Automation

Traffic control

(e.g. congestion

assistant)

(“Hands-off”)

Awareness for

take over

Human MachineTransition of responsibility

TODAY

Page 15

MASTERING THE BASIC TECHNOLOGIES IS THE FIRST STEP FOR HIGHLY AUTOMATED DRIVING.

Intelligent

autonomous vehicle

Regulatory

requirements

Sensor systems Artificial Intelligence

Digital maps / HERE Digital reality model

BMW Group Investor Presentation, June 2016 Page 16

TECHNOLOGIES

LEVERAGING POTENTIAL OF DIGITALIZATION ANDCONNECTIVITY. CUSTOMER EXPERIENCE & SERVICES

BMW Connected

Mobility Cloud

BMW Group Investor Presentation, June 2016 Page 17

INTELLIGENT AND INNOVATIVE PRODUCTION -DIGITIZATION CREATES NEW POTENTIAL.

BMW Group Investor Presentation, June 2016

DIGITALIZATION

Laminate or Metal

Serial Production

and Rapid Prototyping

New Individualization

Internet-of-Things

Architecture

Data Management for Planning

and Control

Cyber Security

Autonomous Transport Systems

Global Supply Chain

Visibility and Control

Integrated Supplier Networks

Collaborative Robot Systems

Context-sensitive Worker

Support Systems

Reorganization of Work

46

810

1214

1618

0

2

4

6

8

10

12

14

16

125

130

135

1404

68

1012

1416

18

0

2

4

6

8

10

12

14

16

125

130

135

140

Data and Analytics Smart Logistics Innovative Automation Additive Manufacturing

Page 18

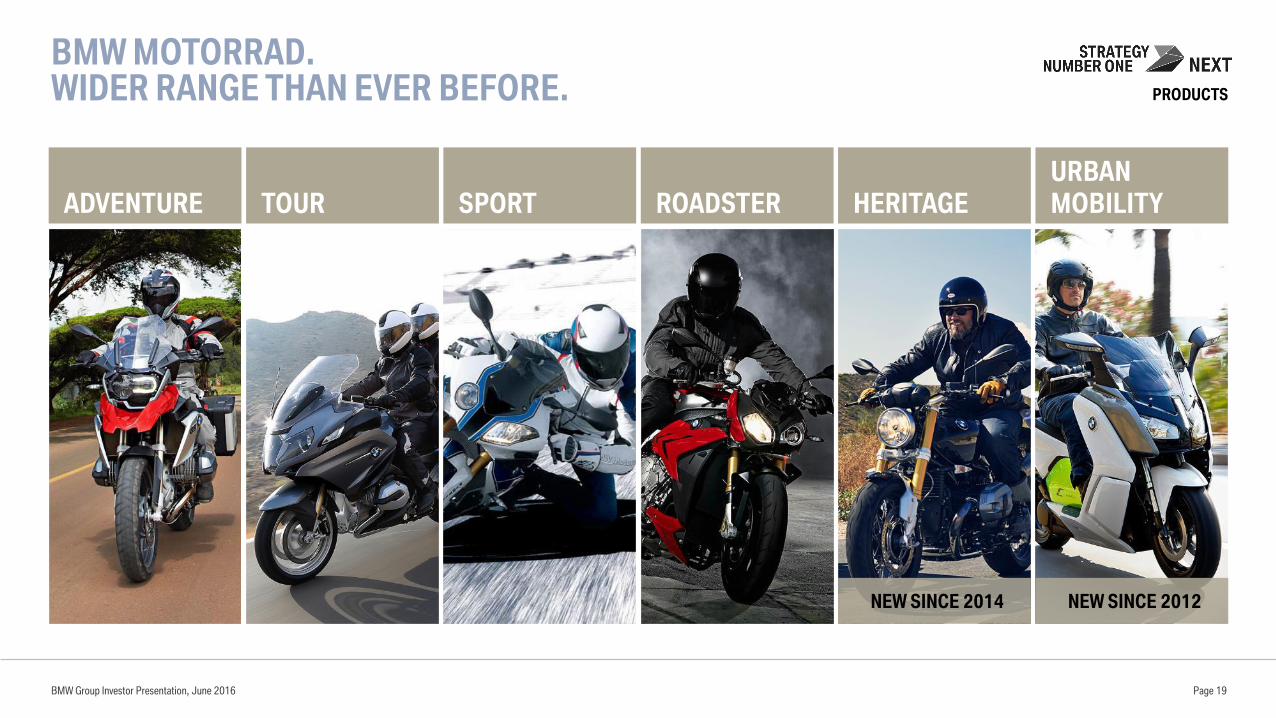

BMW MOTORRAD.WIDER RANGE THAN EVER BEFORE.

BMW Group Investor Presentation, June 2016

ADVENTURE TOUR SPORT ROADSTER HERITAGE

URBAN

MOBILITY

Page 19

NEW SINCE 2014 NEW SINCE 2012

PRODUCTS

MAINTAINING THE AUTOMOTIVE EBIT MARGIN IN THE CORRIDOR OF 8-10% DESPITE ONGOING CHALLENGES. PROFITABILITY

8 %

10 %

Ongoing efficiency

measures to compensate

the cost burden

Future costs Volatility

Market and

competitive

environment

Regulatory

requirements

Expansion & optimization

product portfolio

Reduction of

material costs

New technologies/

equipment options

Retail sales growth

Autos and Motorcycles

Benefits from

digitalizationEfficiency

measuresBMW Group Investor Presentation, June 2016 Page 20

FINANCIAL TARGETS 2020: SUSTAINABLE GROWTH AND SOLID PROFITABILITY DESPITE CHALLENGES. PROFITABILITY

BMW Group Investor Presentation, June 2016

BMW Group

EBT margin (from 2017)

Investment ratio*

Research and development ratio

Payout ratio

Automotive Segment

EBIT margin

Free Cashflow

Motorcycles Segment

Sales volume

EBIT margin (from 2017)

Financial Services Segment

Return on Equity

* Investments in property, plant and equipment and other intangible assets (without capitalized development costs).

Page 21

2015

10.0%

4.2%

5.6%

32.9%

9.2%

5.4 bn €

136,963 units

9.1%

20.2%

2020

>10%

<5.0%

5.0 - 5.5%

30 - 40%

8 -10%

>3 bn €

> 200,000 units

8 -10%

>18%

BMW GROUP

BUSINESS UPDATE

BMW Group Investor Presentation, June 2016 Page 22

SOLID START INTO THE NEW BUSINESS YEAR.BMW GROUP SALES FIGURES YTD MAY 2016.

935,288 + 5.0%

797,457 + 5.0%

136,617 + 5.2%

1,214 - 14.4%

65,761 +4.5%

BMW Group Investor Presentation, June 2016 Page 23

Americas

180,099 units

Europe

432,545 units

+10.3%

Mainland China

202,344 units

Asia (w/o) China

& Rest of World

120,300 units

-7.9%

19% 46%

+6.3%

22% 13%

+6.6%

BMW GROUP AUTOMOTIVE: BALANCED SALES DISTRIBUTION AND SOLID YTD MAY 2016 GROWTH OF +5.0%.

BMW Group Investor Presentation, June 2016 Rolls Royce is included in “Rest of World”, YTD May 2016 (figures may not add to 100% due to rounding) Page 24

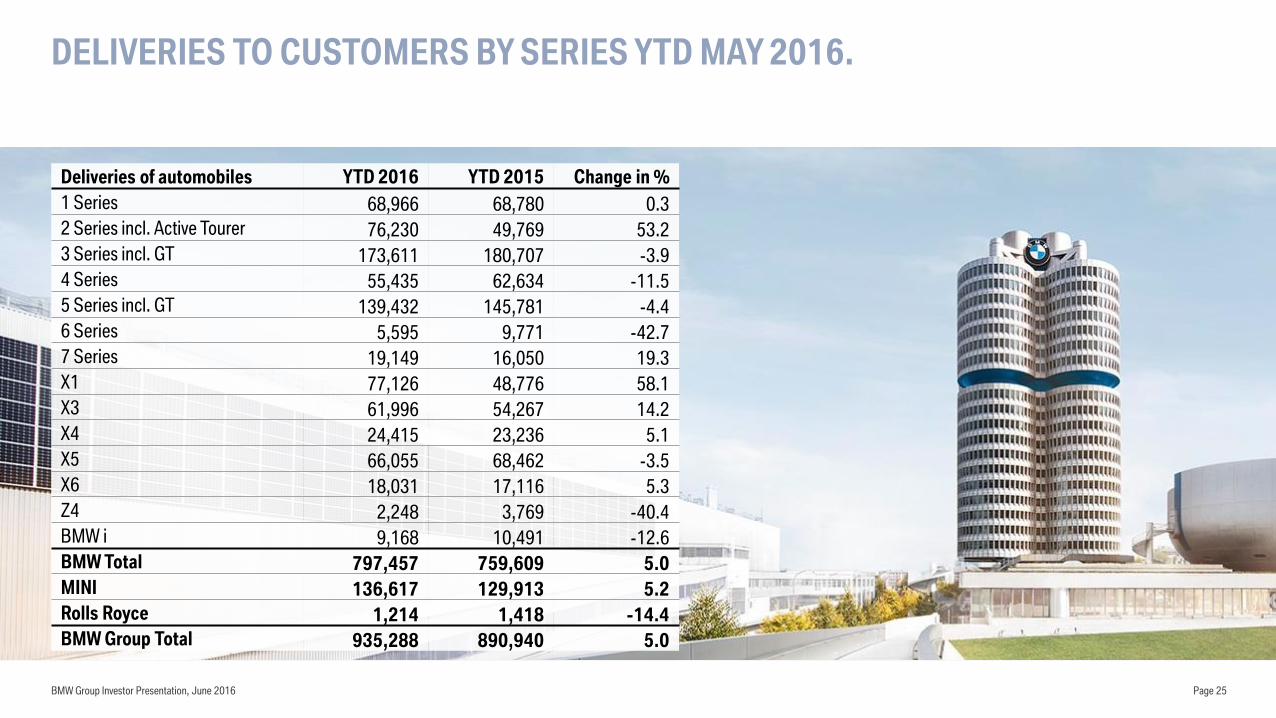

DELIVERIES TO CUSTOMERS BY SERIES YTD MAY 2016.

BMW Group Investor Presentation, June 2016 Page 25

Deliveries of automobiles YTD 2016 YTD 2015 Change in %

1 Series 68,966 68,780 0.3

2 Series incl. Active Tourer 76,230 49,769 53.2

3 Series incl. GT 173,611 180,707 -3.9

4 Series 55,435 62,634 -11.5

5 Series incl. GT 139,432 145,781 -4.4

6 Series 5,595 9,771 -42.7

7 Series 19,149 16,050 19.3

X1 77,126 48,776 58.1

X3 61,996 54,267 14.2

X4 24,415 23,236 5.1

X5 66,055 68,462 -3.5

X6 18,031 17,116 5.3

Z4 2,248 3,769 -40.4

BMW i 9,168 10,491 -12.6

BMW Total 797,457 759,609 5.0

MINI 136,617 129,913 5.2

Rolls Royce 1,214 1,418 -14.4

BMW Group Total 935,288 890,940 5.0

BMW GROUP AUTOMOTIVE MAJOR MARKETS. DELIVERIES TO CUSTOMERS YTD MAY 2016.

BMW Group Investor Presentation, June 2016 Page 26

Deliveries of automobiles YTD 2016 YTD 2015 Change in %

Europe 432,545 392,185 10.3

thereof Germany 1) 125,290 116,295 7.7

Great Britain 92,837 85,167 9.0

France 35,002 31,179 12.3

Italy 33,584 29,407 14.2

Americas 180,099 195,485 -7.9

thereof USA 144,811 160,533 -9.8

Asia 293,188 276,055 6.2

thereof China Mainland 202,344 190,427 6.3

thereof BBA retail sales 127,640 118,466 7.7

Japan 28,200 26,508 6.4

Rest of the World 2) 29,456 27,215 8.2

Total 935,288 890,940 5.0

1) Registrations 2) Rolls-Royce sales are included in “Rest of the World”

BMW AND MINI RETAIL DEVELOPMENT IN MAINLAND CHINA YTD MAY 2016.

BMW Group Investor Presentation, June 2016 Page 27

62% 59% 53% 48% 32% 61%41% 43%

Share of JV Sales

51% 61%

13.8 21.0 30.7 46.8

115.3138.2

185.3 192.2 180.1 181.7

72.0 74.722.6

30.635.2

43.7

53.7

94.4

141.2

198.5

275.9 282.0

118.5 127.6

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 YTD 2015 YTD 2016

Import JV Sales

36.451.6

65.890.5

169.0

232.6

326.4

in ‘000 units

390.7

456.0 463.7

+41.8 %

+27.5 %+37.5 %

+86.7 %

+37.6 %

+40.3 %

+19.7 %

+16.7 %+1.7%

202.3

62%

Source: BMW Group Retail data, YTD May 2016

63%

190.4

+6.3%

25.8

21.0

11.9

10.19.3 9.0 8.6 8.5 7.4

4.6

2.41.2

0

5

10

15

20

25

30

Germany UnitedKingdom

Italy USA Turkey France S. Korea Russia China Japan Brazil India

PREMIUM SEGMENT SHARE OF TOTAL MARKET 2015.

BMW Group Investor Presentation, June 2016 Page 28

in %

World Average: 8.9%

Source: Global Insight 12/2015

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2015 2016 2017 2018 2019 2020

*BRIKT refers to Brazil, Russia, India, South Korea and Turkey Source: Global Insight 04/2016

GLOBAL ANNUAL PREMIUM SEGMENT SALES ARE EXPECTED TO GROW TO 9.0 MN UNITS BY 2020.

BMW Group Investor Presentation, June 2016 Page 29

China, CAGR +5.5%

Japan, CAGR +0.4%

North America, CAGR +2.3%

Western Europe, CAGR +1.3%

Rest of World, CAGR +4.6%

BRIKT*, CAGR +5.2%

Region (‘000 units) 2015 2020 Chg.

World 7,749 9,012 16%

Res t of World 605 759 25%

BRIKT* 475 612 29%

China (Mainland) 1,793 2,345 31%

Japan 225 229 2%

North America 1,944 2,173 12%

Wes tern Europe 2,707 2,894 7%

BMW GROUP – Q1-2016: GOOD START IN THE FIRST THREE MONTHS OF 2016, WITH A RECORD FIRST-QUARTER SALES VOLUME PERFORMANCE.

BMW Group Investor Presentation, June 2016 Page 30

BMW Group Q1-2016 Q1-2015 Change in %

Earnings before tax – Group (in m€) 2,368 2,269 +4.4

EBT margin (in %) – Group 11.4 10.8 -

Automotive Segment

Automotive sales (units) 557,605 526,669 +5.9

Earnings before interest and tax (EBIT) (in m€) 1,763 1,794 -1.7

EBIT margin (in %) 9.4 9.5 -

Net financial assets (m€) 17,511 15,037 +16.5

Motorcycles Segment

Sales (units) 33,788 31,370 +7.7

Earnings before interest and tax (EBIT) (in m€) 94 115 -18.3

EBIT margin (in %) 16.2 20.3 -

Financial Services

Earnings before tax (EBT) (in m€) 570 559 +2.0

Penetration rate (in %) 46.1 44.9 -

Credit loss ratio (in %) 0.29 0.33 -

EBIT MARGIN DEVELOPMENT AUTOMOTIVE SEGMENT.TARGET PROFITABILITY OF 8-10%.

BMW Group Investor Presentation, June 2016

EBIT margin development automotive segment

[in %]

Page 31

Target corridor:

8-10 %

* 2013 figures have been adjusted in accordance with IAS 8.

6.4 6.4

1.4

-0.6

8.0

11.8

10.8

9.4 9.69.2 9.5 9.4

2006 2007 2008 2009 2010 2011 2012 2013* 2014 2015 Q1-2015Q1-2016

FREE CASH FLOW AUTOMOTIVE SEGMENT.TARGET OF >3BN EURO ANNUALLY.

BMW Group Investor Presentation, June 2016 Page 32

* Definition: Free cash flow corresponds to the cash inflow from operating activities of the Automobiles segment less the cash outflow for investing activities of the Automobiles segment adjusted for net investment in marketable securities and term deposits. 2009 – 2015 as reported, 2007 & 2008 calculated according to above definition from reported figures. No cash flow reporting on segment level in 2006.** 2009, 2011, 2013 figures have been adjusted in accordance with IAS 8.

2,277

197

1,456

4,471

3,166

3,809

3,003

3,481

5,404

1,060

532

2006 2007 2008 2009** 2010 2011** 2012 2013** 2014 2015 Q1-2015 Q1-2016

Target:

> 3 billion

n.a.

Free Cash Flow (Automotive)*

[in m€]

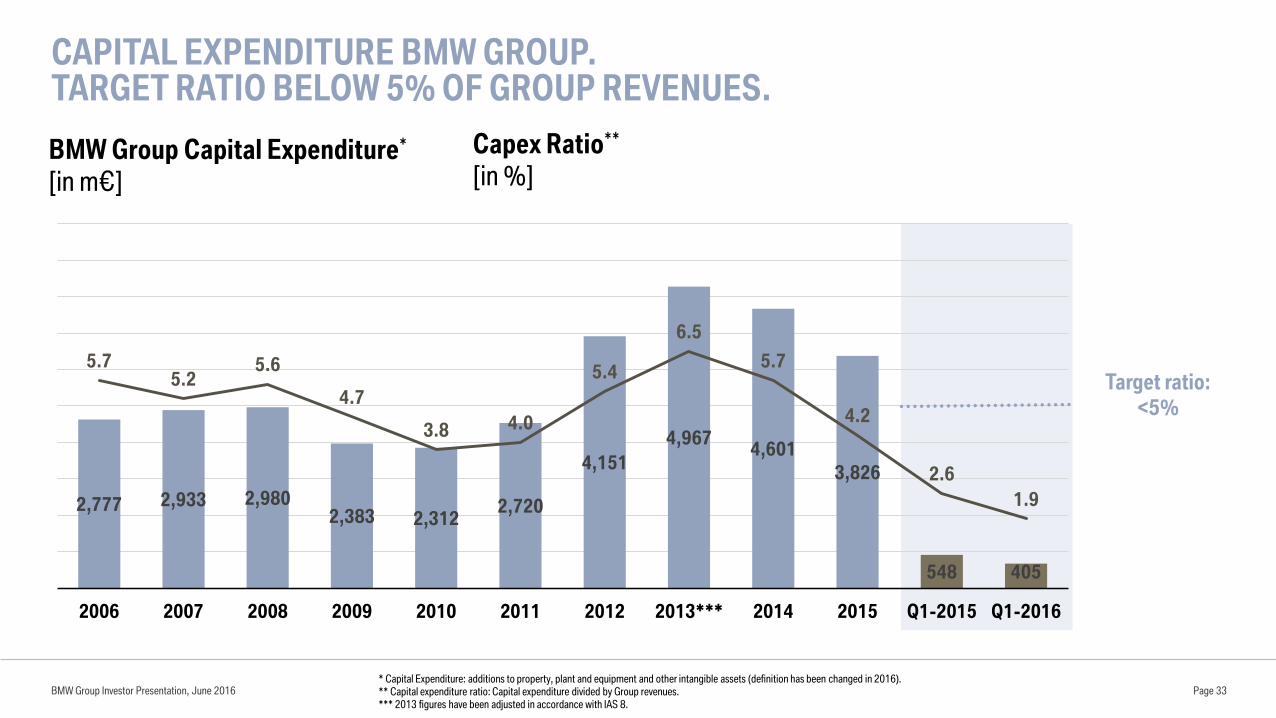

CAPITAL EXPENDITURE BMW GROUP.TARGET RATIO BELOW 5% OF GROUP REVENUES.

BMW Group Investor Presentation, June 2016

BMW Group Capital Expenditure*

[in m€]

Capex Ratio**

[in %]

* Capital Expenditure: additions to property, plant and equipment and other intangible assets (definition has been changed in 2016).** Capital expenditure ratio: Capital expenditure divided by Group revenues.*** 2013 figures have been adjusted in accordance with IAS 8.

Page 33

Target ratio:

<5%

2,777 2,933 2,9802,383 2,312

2,720

4,151

4,9674,601

3,826

548 405

5.75.2

5.6

4.7

3.8 4.0

5.4

6.5

5.7

4.2

2.6

1.9

0

1

2

3

4

5

6

7

8

9

10

0

1,000

2,000

3,000

4,000

5,000

6,000

2006 2007 2008 2009 2010 2011 2012 2013*** 2014 2015 Q1-2015 Q1-2016

OUTLOOK FOR 2016 –POSITIVE BUSINESS DEVELOPMENT EXPECTED DESPITE CHALLENGES.

BMW Group

Slight increase in EBT compared with previous year

Automotive Segment

Slight increase in deliveries and revenues compared with the previous year

EBIT margin in the target range of 8-10%

Financial Services Segment

Return on equity of at least 18%, on par with previous year

Motorcycles Segment

Slight increase in deliveries compared with the previous year

BMW Group Investor Presentation, June 2016 Page 34

BMW GROUP’S FINANCE STRATEGY COVERS THE ENTIRE AUTOMOTIVE VALUE CHAIN.

Page 35BMW Group Investor Presentation, June 2016

Research & Development Production Financial ServicesSales & Marketing

BMW GROUP CORPORATE FINANCE STRATEGY REFLECTS THE INDUSTRIAL NATURE OF THE BUSINESS

AND IS FOCUSED ON THE ENTIRE AUTOMOTIVE VALUE CHAIN.

Automotive value chain

DIVERSIFIED FUNDING MIX WITH A COMBINATION OF INDUSTRY AND BANK TYPICAL FINANCING INSTRUMENTS.

BMW Group Investor Presentation, June 2016 Page 36

CP

<1yr 1yr 2yrs 3yrs 4yrs 5yrs 7yrs 10yrs+

(EMTN) PPs Bonds

Customers deposits

Banks loans

FedFunds

BCD’s

Bank-typical

instruments

Industry-typical

instruments

ABS ABCP

*Adjusted, excluding currency and interest rate derivatives.

Funding Instruments Financial Debt as of 31.03.2016

Structured Financing3.1%

Bank Loans8.1%

SSD2.4%

Fed Funds0.5%

Brokered CD's5.7%

Customer Deposits BMW Bank

9.7%

ABS15.3%

CP6.2%

PP's12.7%

Public Bonds34.8%

Others1.6%

86.5 bn €*

BMW GROUP INVESTOR RELATIONS. CONTACTS.

BMW Group Investor Presentation, June 2016

Torsten Schüssler

Head of Investor Relations

Andreas Stöffler

Equity IR

Bernd Daser

Debt & Equity IR

Ziye Zhou

Debt & Equity IR

Patrick Neumayer

Debt & Equity IR USA

Tanja Seiler

Equity & SRI IR

http://www.bmwgroup.com/ir

IR Contact

BMW Group Investor Relations

Petuelring 130

80788 Munich

Page 37

BMW GROUP INVESTOR RELATIONS.FINANCIAL CALENDAR 2016 & 2017.

BMW Group Investor Presentation, June 2016

02.08.2016 Quarterly Report to June 2016

04.11.2016 Quarterly Report to September 2016

21.03.2017 Annual Accounts Press Conference 2017

22.03.2017 Analyst and Investor Conference 2017

04.05.2017 Quarterly Report to March 2017

11.05.2017 Annual General Meeting 2017

03.08.2017 Quarterly Report to June 2017

http://www.bmwgroup.com/ir

Page 38

BMW GROUP INVESTOR RELATIONS.ON THE ROAD H1 2016.

BMW Group Investor Presentation, June 2016

07.06.2016 J. P. Morgan European Automotive Conference London

08./09.06.2016 Unicredit Auto Credit Conference London

09.06.2016 db Access German, Swiss & Austrian Conference Berlin

13.-15.06.2016 J. P. Morgan Global China Summit Beijing

20.06.-25.06.2016 Roadshow Chicago, Toronto & Montreal

21.06.2016 DB ADAS Conference, London

22.06.2016 Roadshow Edinburgh

23.06.2016 Bank of America Merrill Lynch Future Mobility Conference, London

Page 39

DISCLAIMER.

BMW Group Investor Presentation, June 2016 Page 40

This document contains forward-looking statements that reflect BMW Group’s current views about future events. The words

“anticipate,” “assume,” “believe,” “estimate,” “expect,” “intend,” “may,” ”can,” “could,” “plan,” “project,” “should” and

similar expressions are used to identify forward-looking statements.

These statements are subject to many risks and uncertainties or may be affected by factors outside BMW Group’s control,

including adverse developments in global economic conditions resulting in a decline in demand in BMW Group’s key

markets, including China, North America and Europe; a deterioration in credit and financial markets; a shift in consumer

preferences affecting demand for BMW Group’s products; changes in the prices of fuel or raw materials; disruption of

production due to shortages of materials, labor strikes or supplier insolvencies; the effective implementation of BMW

Group’s strategic goals and targets; changes in laws, regulations and government policies, particularly those relating to

vehicle emissions, fuel economy and safety; and other risks and uncertainties, including those described under the heading

“Report on Risks and Opportunities” in BMW Group’s most recent Annual Report.

If any of these risks and uncertainties materializes or if the assumptions underlying any of BMW Group’s forward-looking

statements prove to be incorrect, actual results may be materially different from those BMW Group expresses or implies by

such statements. BMW Group does not intend or assume any obligation to update these forward-looking statements.