blue shield of california presents...blue shield of california presents: 2017 Medicare Part D...

51

blue shield of california presents: 2017 Medicare Part D product sales training 0MMDDYYYY S2468_16_231C 07252016

Transcript of blue shield of california presents...blue shield of california presents: 2017 Medicare Part D...

blue shield of california presents:

2017 Medicare Part D

product sales training

0MMDDYYYY

S2468_16_231C 07252016

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

Blue Shield Medicare Basic Plan (PDP) & Blue

Shield Medicare Enhanced Plan (PDP) Training

Disclosure

This training presentation is intended for use by licensed agents to understand the basics of both the Blue Shield Medicare Basic Plan and the Blue Shield Medicare Enhanced Plan.

When making presentations, agents must rely upon the plan’s Summary of Benefits, formulary, pharmacy directory, and other plan documentation to address the specific needs of each prospective member.

Information contained in this document regarding 2017 benefits, costs, etc. is confidential until general release to the public on October 1, 2016. Distribution to consumers, other insurers, or any other person or company is

strictly prohibited. Failure to comply with this requirement will result in the loss of appointment with Blue Shield of California on all lines of business, and may result in civil monetary judgment.

2

2017 benefits

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

2017 Blue Shield Medicare

Prescription Drug Plans (PDP)

In this section, you’ll be introduced to plan

benefits and the following plan information:

• 2017 plans:

Blue Shield Medicare Enhanced Plan

Blue Shield Medicare Basic Plan

• Enrollment periods

• How to submit Blue Shield Medicare PDP

plan applications

• Important dates

4

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

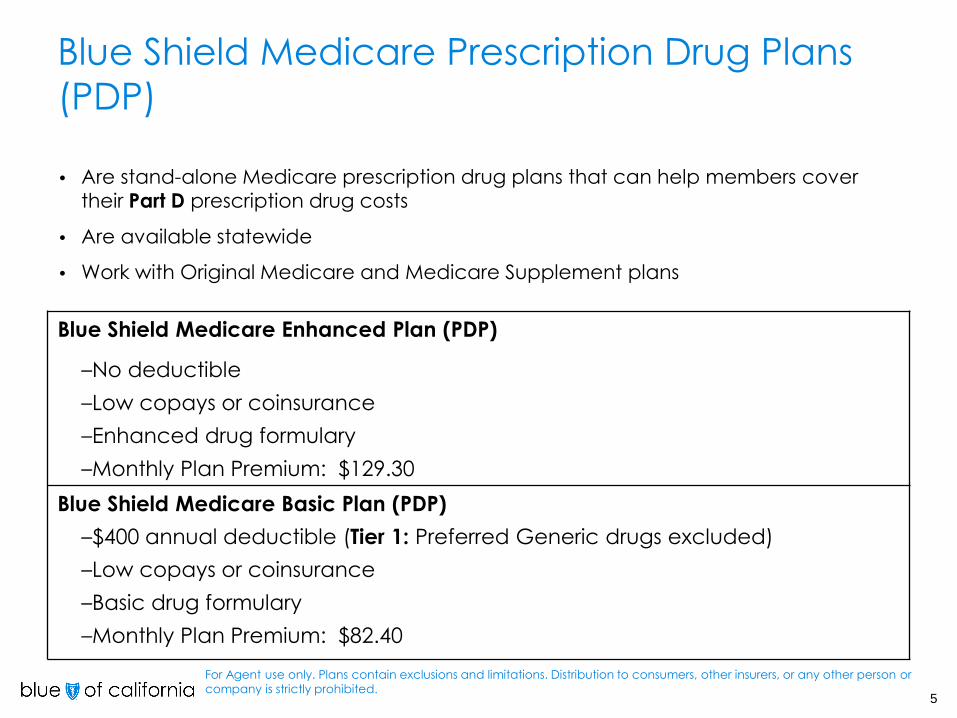

Blue Shield Medicare Prescription Drug Plans

(PDP)

• Are stand-alone Medicare prescription drug plans that can help members cover

their Part D prescription drug costs

• Are available statewide

• Work with Original Medicare and Medicare Supplement plans

5

Blue Shield Medicare Enhanced Plan (PDP)

–No deductible

–Low copays or coinsurance

–Enhanced drug formulary

–Monthly Plan Premium: $129.30

Blue Shield Medicare Basic Plan (PDP)

–$400 annual deductible (Tier 1: Preferred Generic drugs excluded)

–Low copays or coinsurance

–Basic drug formulary

–Monthly Plan Premium: $82.40

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.6

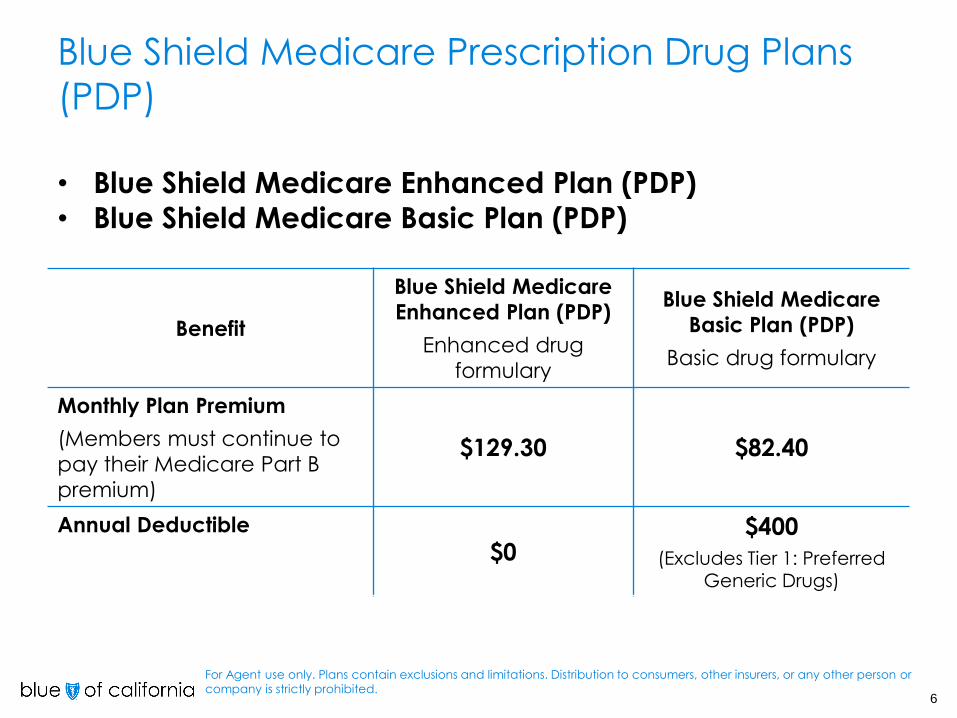

• Blue Shield Medicare Enhanced Plan (PDP)

• Blue Shield Medicare Basic Plan (PDP)

Benefit

Blue Shield Medicare

Enhanced Plan (PDP)

Enhanced drug

formulary

Blue Shield Medicare

Basic Plan (PDP)

Basic drug formulary

Monthly Plan Premium

(Members must continue to

pay their Medicare Part B

premium)

$129.30 $82.40

Annual Deductible

$0$400

(Excludes Tier 1: Preferred Generic Drugs)

Blue Shield Medicare Prescription Drug Plans

(PDP)

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.7

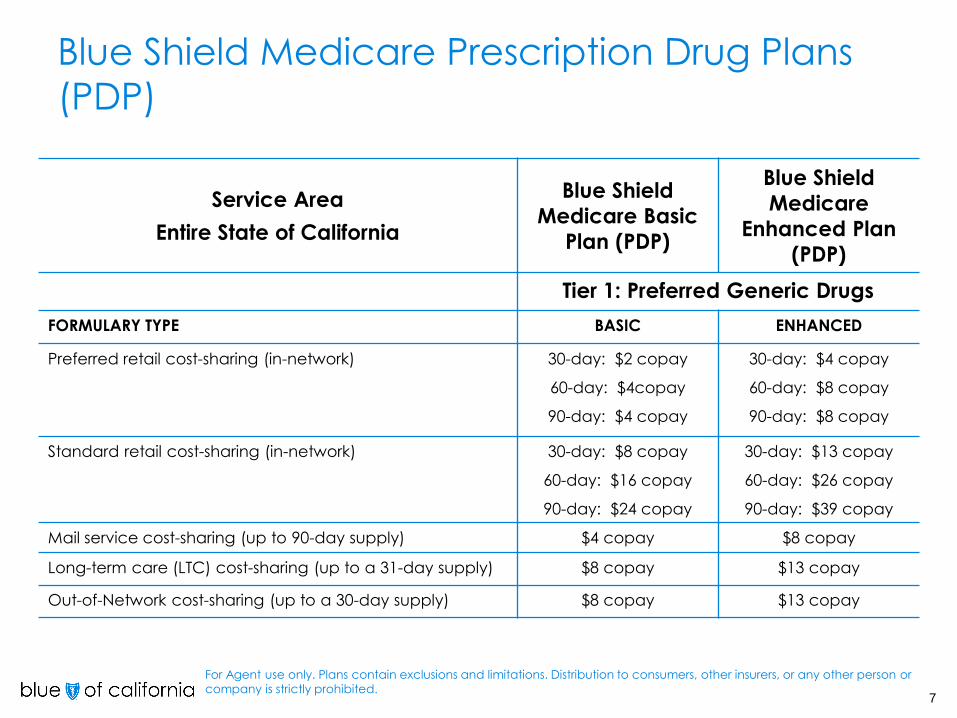

Service Area

Entire State of California

Blue Shield

Medicare Basic

Plan (PDP)

Blue Shield

Medicare

Enhanced Plan

(PDP)

Tier 1: Preferred Generic Drugs

FORMULARY TYPE BASIC ENHANCED

Preferred retail cost-sharing (in-network) 30-day: $2 copay

60-day: $4copay

90-day: $4 copay

30-day: $4 copay

60-day: $8 copay

90-day: $8 copay

Standard retail cost-sharing (in-network) 30-day: $8 copay

60-day: $16 copay

90-day: $24 copay

30-day: $13 copay

60-day: $26 copay

90-day: $39 copay

Mail service cost-sharing (up to 90-day supply) $4 copay $8 copay

Long-term care (LTC) cost-sharing (up to a 31-day supply) $8 copay $13 copay

Out-of-Network cost-sharing (up to a 30-day supply) $8 copay $13 copay

Blue Shield Medicare Prescription Drug Plans

(PDP)

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.8

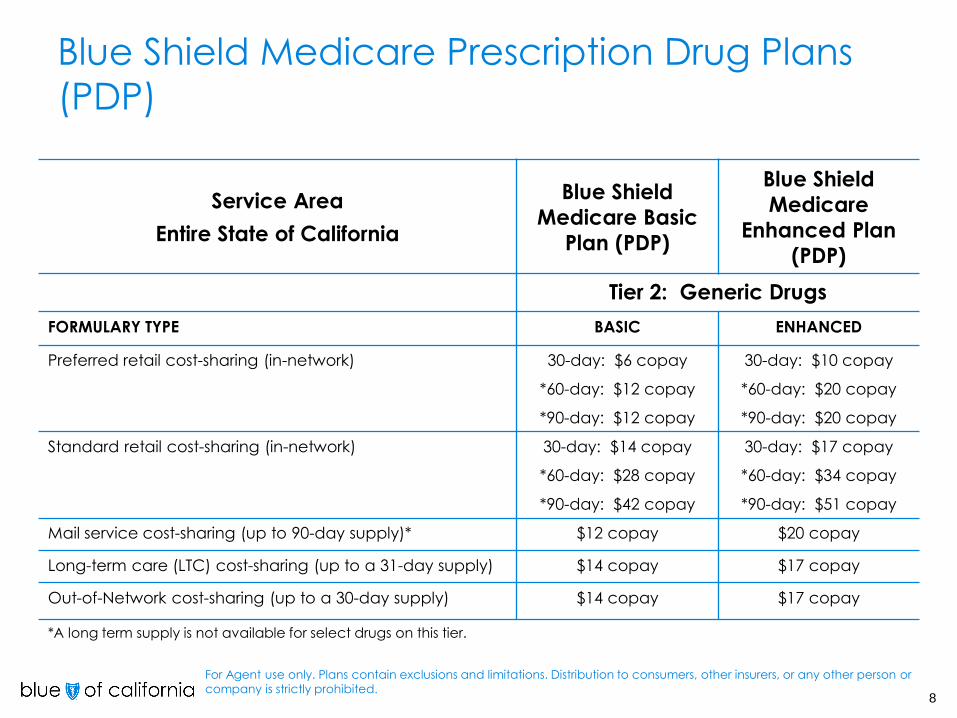

Service Area

Entire State of California

Blue Shield

Medicare Basic

Plan (PDP)

Blue Shield

Medicare

Enhanced Plan

(PDP)

Tier 2: Generic Drugs

FORMULARY TYPE BASIC ENHANCED

Preferred retail cost-sharing (in-network) 30-day: $6 copay

*60-day: $12 copay

*90-day: $12 copay

30-day: $10 copay

*60-day: $20 copay

*90-day: $20 copay

Standard retail cost-sharing (in-network) 30-day: $14 copay

*60-day: $28 copay

*90-day: $42 copay

30-day: $17 copay

*60-day: $34 copay

*90-day: $51 copay

Mail service cost-sharing (up to 90-day supply)* $12 copay $20 copay

Long-term care (LTC) cost-sharing (up to a 31-day supply) $14 copay $17 copay

Out-of-Network cost-sharing (up to a 30-day supply) $14 copay $17 copay

Blue Shield Medicare Prescription Drug Plans

(PDP)

*A long term supply is not available for select drugs on this tier.

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.9

Service Area

Entire State of California

Blue Shield

Medicare Basic

Plan (PDP)

Blue Shield

Medicare

Enhanced Plan

(PDP)

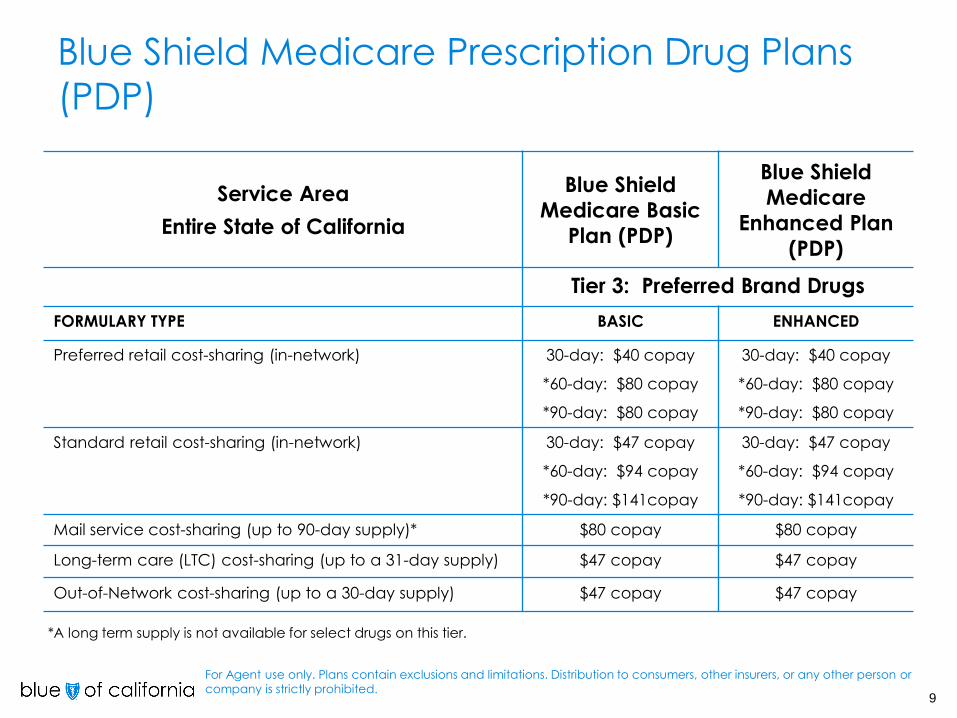

Tier 3: Preferred Brand Drugs

FORMULARY TYPE BASIC ENHANCED

Preferred retail cost-sharing (in-network) 30-day: $40 copay

*60-day: $80 copay

*90-day: $80 copay

30-day: $40 copay

*60-day: $80 copay

*90-day: $80 copay

Standard retail cost-sharing (in-network) 30-day: $47 copay

*60-day: $94 copay

*90-day: $141copay

30-day: $47 copay

*60-day: $94 copay

*90-day: $141copay

Mail service cost-sharing (up to 90-day supply)* $80 copay $80 copay

Long-term care (LTC) cost-sharing (up to a 31-day supply) $47 copay $47 copay

Out-of-Network cost-sharing (up to a 30-day supply) $47 copay $47 copay

Blue Shield Medicare Prescription Drug Plans

(PDP)

*A long term supply is not available for select drugs on this tier.

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.10

Service Area

Entire State of California

Blue Shield

Medicare Basic

Plan (PDP)

Blue Shield

Medicare

Enhanced Plan

(PDP)

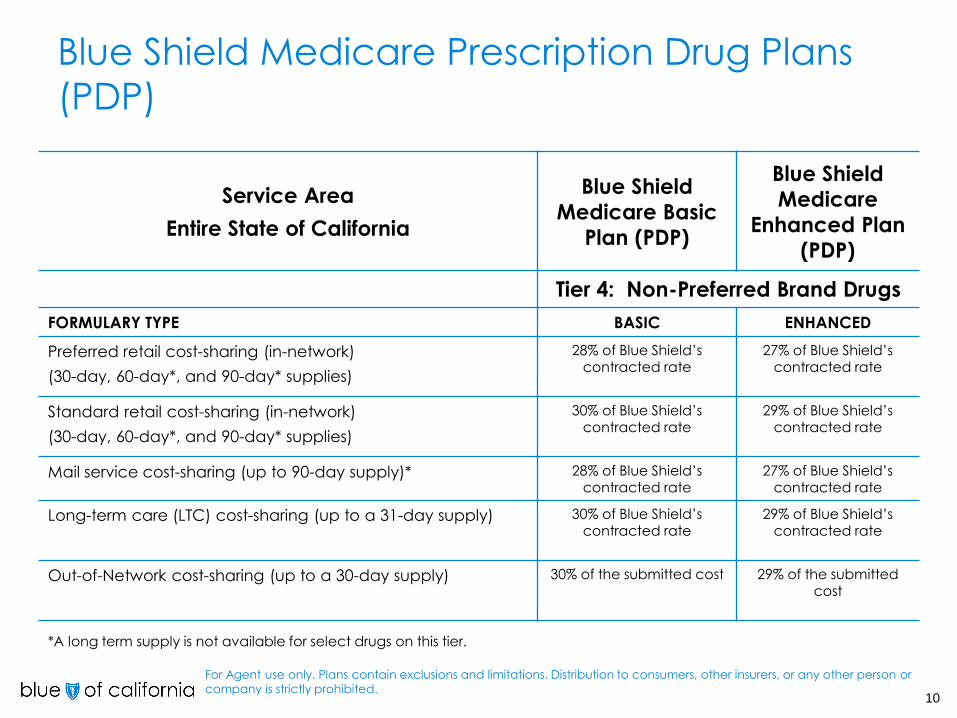

Tier 4: Non-Preferred Brand Drugs

FORMULARY TYPE BASIC ENHANCED

Preferred retail cost-sharing (in-network)

(30-day, 60-day*, and 90-day* supplies)

28% of Blue Shield’s contracted rate

27% of Blue Shield’s contracted rate

Standard retail cost-sharing (in-network)

(30-day, 60-day*, and 90-day* supplies)

30% of Blue Shield’s contracted rate

29% of Blue Shield’s contracted rate

Mail service cost-sharing (up to 90-day supply)* 28% of Blue Shield’s contracted rate

27% of Blue Shield’s contracted rate

Long-term care (LTC) cost-sharing (up to a 31-day supply) 30% of Blue Shield’s contracted rate

29% of Blue Shield’s contracted rate

Out-of-Network cost-sharing (up to a 30-day supply) 30% of the submitted cost 29% of the submitted cost

Blue Shield Medicare Prescription Drug Plans

(PDP)

*A long term supply is not available for select drugs on this tier.

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.11

Service Area

Entire State of California

Blue Shield Medicare

Basic Plan (PDP)

Blue Shield

Medicare

Enhanced Plan

(PDP)

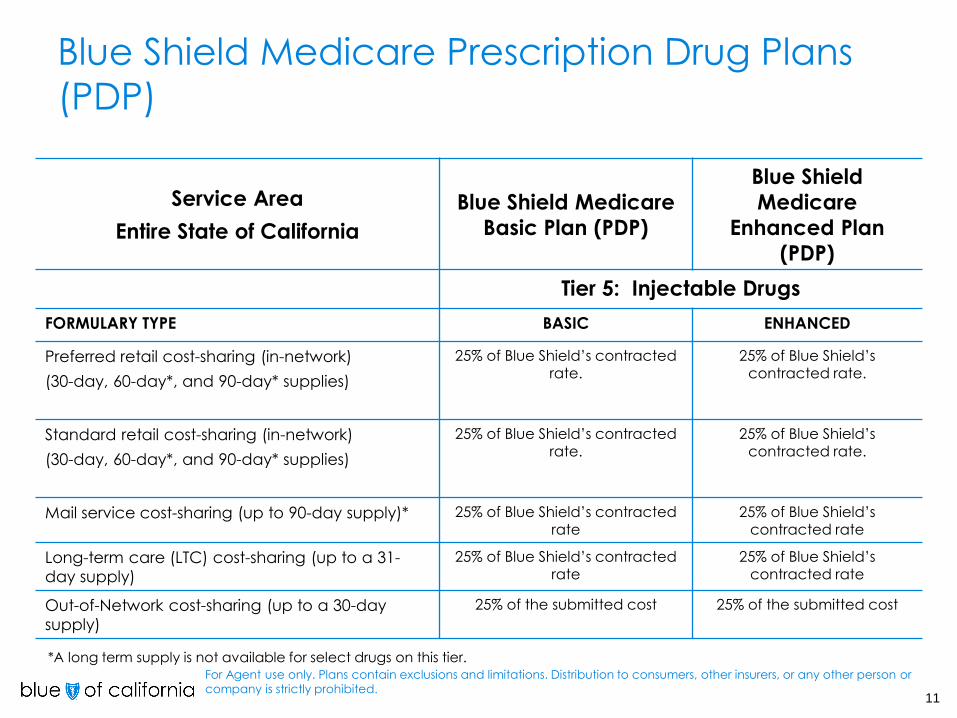

Tier 5: Injectable Drugs

FORMULARY TYPE BASIC ENHANCED

Preferred retail cost-sharing (in-network)

(30-day, 60-day*, and 90-day* supplies)

25% of Blue Shield’s contracted rate.

25% of Blue Shield’s contracted rate.

Standard retail cost-sharing (in-network)

(30-day, 60-day*, and 90-day* supplies)

25% of Blue Shield’s contracted rate.

25% of Blue Shield’s contracted rate.

Mail service cost-sharing (up to 90-day supply)* 25% of Blue Shield’s contracted

rate

25% of Blue Shield’s

contracted rate

Long-term care (LTC) cost-sharing (up to a 31-

day supply)

25% of Blue Shield’s contracted rate

25% of Blue Shield’s contracted rate

Out-of-Network cost-sharing (up to a 30-day

supply)

25% of the submitted cost 25% of the submitted cost

Blue Shield Medicare Prescription Drug Plans

(PDP)

*A long term supply is not available for select drugs on this tier.

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.12

Service Area

Entire State of California

Blue Shield Medicare

Basic Plan (PDP)

Blue Shield Medicare

Enhanced Plan (PDP)

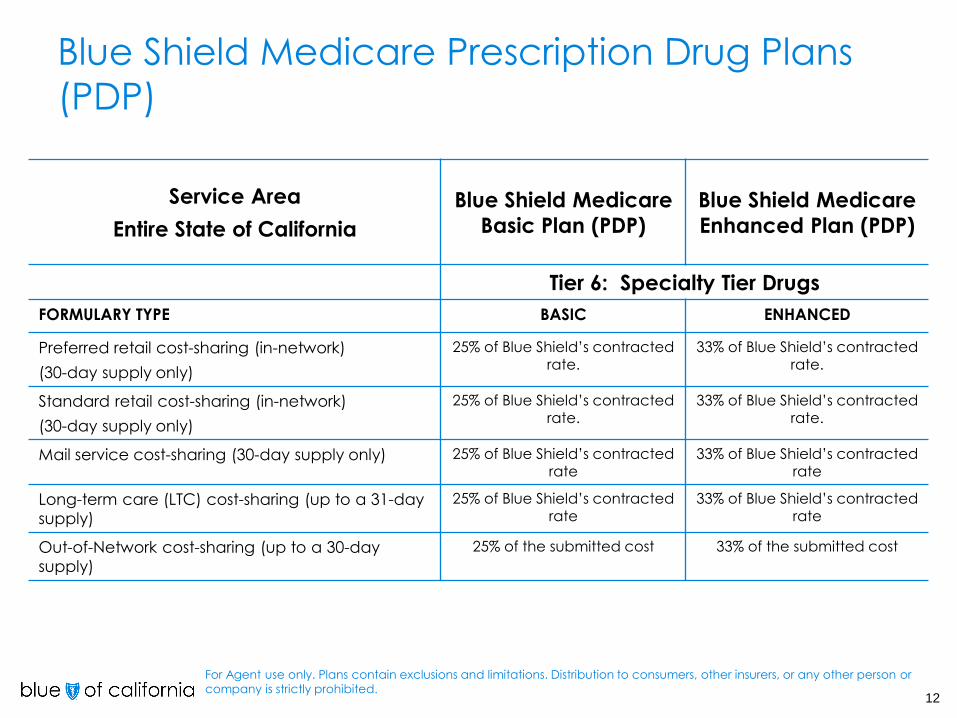

Tier 6: Specialty Tier Drugs

FORMULARY TYPE BASIC ENHANCED

Preferred retail cost-sharing (in-network)

(30-day supply only)

25% of Blue Shield’s contracted rate.

33% of Blue Shield’s contracted rate.

Standard retail cost-sharing (in-network)

(30-day supply only)

25% of Blue Shield’s contracted rate.

33% of Blue Shield’s contracted rate.

Mail service cost-sharing (30-day supply only) 25% of Blue Shield’s contracted rate

33% of Blue Shield’s contracted rate

Long-term care (LTC) cost-sharing (up to a 31-day

supply)

25% of Blue Shield’s contracted rate

33% of Blue Shield’s contracted rate

Out-of-Network cost-sharing (up to a 30-day

supply)

25% of the submitted cost 33% of the submitted cost

Blue Shield Medicare Prescription Drug Plans

(PDP)

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.13

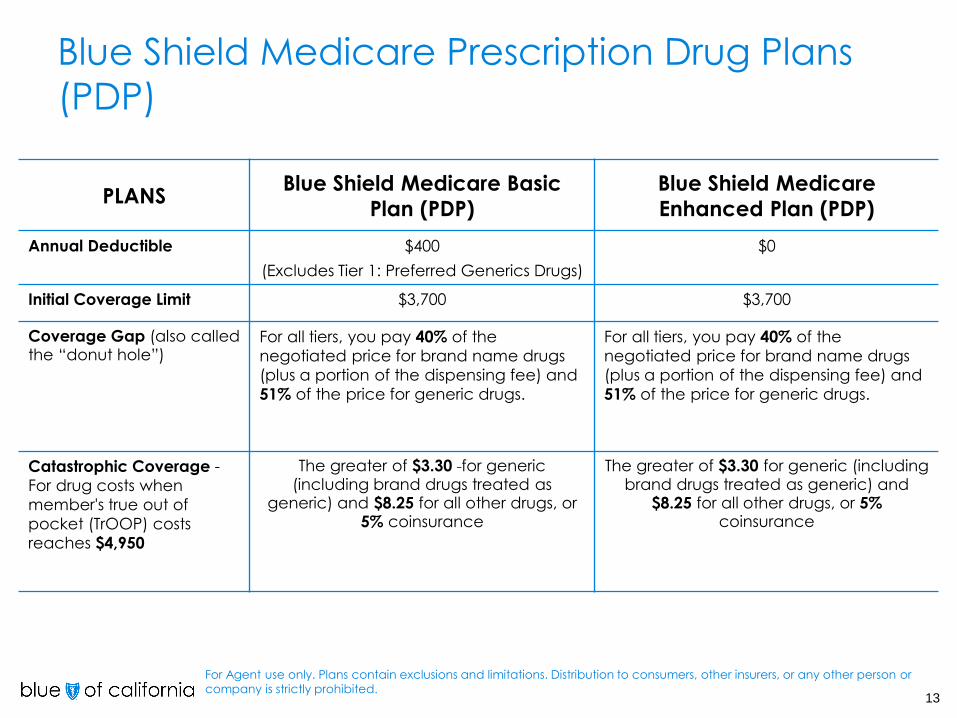

PLANSBlue Shield Medicare Basic

Plan (PDP)

Blue Shield Medicare

Enhanced Plan (PDP)

Annual Deductible $400

(Excludes Tier 1: Preferred Generics Drugs)

$0

Initial Coverage Limit $3,700 $3,700

Coverage Gap (also called the “donut hole”)

For all tiers, you pay 40% of the

negotiated price for brand name drugs

(plus a portion of the dispensing fee) and

51% of the price for generic drugs.

For all tiers, you pay 40% of the

negotiated price for brand name drugs

(plus a portion of the dispensing fee) and

51% of the price for generic drugs.

Catastrophic Coverage -

For drug costs when

member's true out of

pocket (TrOOP) costs

reaches $4,950

The greater of $3.30 for generic (including brand drugs treated as

generic) and $8.25 for all other drugs, or 5% coinsurance

The greater of $3.30 for generic (including brand drugs treated as generic) and

$8.25 for all other drugs, or 5%coinsurance

Blue Shield Medicare Prescription Drug Plans

(PDP)

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

pharmacies offering preferred cost-sharing

Our network includes pharmacies that offer standard cost-sharing and pharmacies that offer preferred cost-sharing. A member may go to either type of network pharmacy to receive covered prescription drugs.

A member may pay less when obtaining their covered prescriptions through our network pharmacies that offer preferred cost-sharing. These include:

• CVS Pharmacy (CVS Pharmacies at Target stores)

• Safeway and Vons pharmacies

• Albertsons, Sav-on, and Osco pharmacies

• Costco pharmacies*

*Member does not have to be a Costco member to use Costco Pharmacies.

Three-month supply cost-sharing also applies

to Blue Shield’s mail service pharmacy.

14

sales and marketing

standards

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

in this lesson

You’ll be introduced to the rules for selling and marketing Medicare Prescription Drug plans, including:

Who can sell Blue Shield Medicare products

What the marketing material guidelines are

How sales and marketing issues are handled and how they affect brokers and sales staff.

16

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

selling for blue shield

How can brokers or agents sell to Medicare beneficiaries on our behalf?

With these stipulations:

1) The broker/agent must be trained & tested annually on Medicare rules,

regulations, and on details specific to the plan products that they sell.

- You must pass Blue Shield’s product certification, as well as AHIP certification, each year.

2) You must be currently appointed to Blue Shield or endorsed by an Agency

that is appointed to Blue Shield.

- Blue Shield will de-appoint any agent for contract violations or fraud.

3) The broker/agent must be compliant.

- You must follow all CMS rules on marketing and sales. You may be “secret

shopped” by CMS or Blue Shield to ensure compliance.

- You must respond to any allegations made against you by any Blue Shield

beneficiary that you sign up.

4) The broker/agent must maintain current state licensure.

- You must show a copy of current license if asked by a beneficiary.

5) The broker/agent must remain free and clear from any sanctions that would

prevent them from participating in a federal program.

17

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

CMS marketing materials highlights

Sales staff, including brokers, must use only Blue Shield and CMS-approved materials, including flyers and call scripts.

Third-party websites operated by agencies/agents that market and/or contain information about Blue Shield PDP and/or MAPD products must meet applicable CY 2017 CMS Medicare Marketing Guidelines. Websites must be submitted to Blue Shield for review and approval.

Materials must be:

− pre-approved,

− printed with relevant approval/tracking codes, and

− printed in (minimum) 12-point Times New Roman or equivalent font

18

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

CMS marketing materials highlights (con’t)

Marketing Materials/Phone Numbers:

Materials that include an agent/broker’s phone number should clearly indicate, “calling agent/broker number will direct an individual to a licensed agent/broker.”

If an agent/broker’s phone number is listed, then the plan sponsor’s customer service phone and TTY numbers should also be included, as well as the plan hours of operation.

19

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

CMS sales & educational event highlights

Sales Events:

Full enrollment kits MUST be provided if enrollment applications are distributed during a Sales Event.

All formal and informal sales events must be filed with CMS prior to

advertising the event or seven (7) calendar days prior to the event’s scheduled date, whichever is earlier.

Agents may not require beneficiaries to provide any contact information as a prerequisite for attending the event.

Agents may not use personal contact information obtained to notify

individuals of raffle or drawing winnings for any other purpose.

Any sign-in sheets should clearly indicate that completion of any contact information is optional.

Educational Events:

• Educational events for prospective enrollees may not include any sales activities including the distribution of marketing materials or the distribution/collection of plan applications or materials, or setting up individual sales appointments.

• Business cards may only be provided when asked for by beneficiary.(Refer to CY 2017 CMS Medicare Marketing Guidelines section 70 for more details.)

20

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

CMS contact, appointment highlights

Phone Contacts:

Prohibited telephonic activities include, but are not limited to, the following:

• Calls to beneficiaries who attended a sales event, unless the beneficiary

gave express permission at the event for a follow-up call (the Plan/Part D Sponsor must have documentation of permission to be contacted).

• Calls based on referrals - if an individual would like to refer a friend or relative to an agent or Plan/Part D Sponsor, the agent or Plan/Part D Sponsor may provide contact information such as a business card that the individual may give to a friend or relative. Otherwise, as instructed in section 30.8 of the CY 2017 CMS Medicare Marketing Guidelines, a referred individual needs to contact the plan or agent/broker directly.

Personal/Individual Appointments:

• The Plan/Part D Sponsor must document the scope of the agreement 48 hours prior to the appointment, when practicable.

• “Walk-ins” require a signed scope of appointment before discussing Medicare Advantage or PDP plans AND must indicate “walk-in” on form.

21

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

CMS record retention requirements

All plan sponsors and contracted downstream entities must abide by CMS rules and regulations regarding record retention by retaining documents (i.e., books, records and documents, etc.) for a period of ten (10) years.

Plan sponsors are responsible for ensuring that any marketing materials developed on behalf of the plan or by third party or delegated entitiesadhere to CMS record retention requirements. Any records that should be retained as a result of direction from the Department of Justice should be kept by plan sponsors and their affiliates.

22

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

how do violations affect agents?

Violations of CMS sales and marketing standards will be investigated and may result in disciplinary action.

Allegations from beneficiaries against agents will be investigated and may result in disciplinary action.

Direct violations of CMS-prohibited practices may result in termination of Blue Shield sales associates or brokers and agents, along with reporting to CMS and the state licensing board for possible further disciplinary action, up to and including loss of license.

23

coverage determinations,

exceptions, grievances and

appeals

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

in this lesson

In this lesson you’ll be introduced to how to file:

• Coverage Determinations and Exceptions

• Appeals

• Grievances

25

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

what is a coverage determination?

Coverage Determination

Medicare Prescription Drug Plan members have the right to get a written

explanation called a “coverage determination”.

A coverage determination is the first decision made by Blue Shield about the drug coverage, including:

• whether a particular drug is covered;

• whether the member has met all the requirements for getting a requested drug;

• how much they are required to pay for a drug;

• whether to make an exception to a plan rule when it’s requested.

26

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

what is an exception?

Exceptions

There are several types of exceptions that the member, the member’s representative or the member’s provider/prescriber can request:

• Members can ask Blue Shield to cover a prescription even if it is not on the formulary.

• Members can ask Blue Shield to waive coverage restrictions or limits on a prescription.

― For example, for certain drugs, Blue Shield limits the amount of the drug that

is covered. If a member’s prescription has a quantity limit, he or she can ask

to waive the limit.

• Members can ask Blue Shield for a tier exception to provide a higher level of coverage for a prescription.

― For example, if a prescription is usually considered a Tier 3 drug, a member

can ask the Plan to cover it as a Tier 2 drug instead. This would lower the

copayment amount that the member pays for the drug.

Formulary exceptions are not guaranteed, and should not be presented to

prospects as such.

27

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

formulary exceptions (con’t)

Formulary Exceptions

• Physician support is required for

exceptions.

• Generally, Blue Shield will only approve a

member’s request for an exception if the

alternative drugs included on the Plan’s

formulary or the lower tier drug would not

be as effective in treating the member’s

condition and/or would cause the

member to have adverse medical effects.

• When the Plan approves an exception

request, the approval is valid for the

remainder of the plan year, as long as the

doctor continues to prescribe the drug

and it continues to be safe and effective

for treating the member’s condition.

• If Blue Shield denies an exception request,

the member has the right to appeal the

decision.

28

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

filing coverage determinations & exceptions

• The request for a coverage determination or exception can be requested by the member, their doctor or other prescriber, or their designated representative.

• It can be filed as a standard or an expedited request.

– The standard request requires a plan decision within 72 hours of receipt of

request.

– The expedited request requires a plan decision within 24 hours of receipt of

request.

• Coverage determinations and exception requests can be filed in writing or by calling Blue Shield.

• There may be times when the member disagrees with a coverage determination or payment decision made by Blue Shield. They then have the right to file an appeal.

29

Blue Shield must grant an expedited review if the doctor or other prescriber tells us

that the member’s life or health may be at risk by waiting for a standard request.

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

excluded drugs

The following categories of drugs are not covered (“excluded”) by the Plan:

• Non-prescription drugs (or over-the-counter drugs)

• Drugs used for treatment of anorexia, weight loss, or weight gain

• Drugs used to promote fertility

• Drugs used for cosmetic purposes or to promote hair growth

• Drugs used for the symptomatic relief of cough and colds

• Prescription vitamins and mineral products, except prenatal vitamins and fluoride preparations

• Outpatient drugs for which the manufacturer seeks to require that associated tests or monitoring services be purchased exclusively from the manufacturer as a condition of sale

• Drugs such as Viagra, Cialis, Levitra, and Caverject, when used for the treatment of sexual or erectile dysfunction

• The plan's Part D drug coverage cannot cover a drug that would be covered under Medicare Part A or Part B.

• The plan cannot cover a drug purchased outside the U.S. and its territories.

• The plan usually cannot cover off-label use (use of the drug other than those indicated on a drug's label as approved by the Food & Drug Administration), except when the use is supported by certain reference books.

30

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

appeals

• An appeal is defined as: Any of the procedures that deal with the review of

adverse coverage determinations made by the Part D plan sponsor on the

benefits under a Part D plan the enrollee believes he or she is entitled to receive,

including a delay in providing or approving the drug coverage (when a delay

would adversely affect the health of the enrollee), or on any amounts the enrollee

must pay for the drug coverage, as defined in 42 CFR 423.566(b). These

procedures include redeterminations by the Part D plan sponsor, reconsiderations

by the independent review entity (IRE), Administrative Law Judge (ALJ) hearings,

reviews by the Medicare Appeals Council (MAC), and judicial reviews.

• A member, or his/her authorized representative or provider, must forward the

request for an appeal within 60 calendar days of the date of the denial notice.

• The request can be made by phone or in writing (for an expedited request) or in

writing only (for a standard request).

• Plan response times, from receipt of appeal are:

― Standard appeal - 7 calendar days.

― Expedited appeal - 72 hours.

31

Instruct members to call Member Services to reach representatives trained to

guide members through the grievance and appeals process.

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

appeals process

• Initial decision or organization determination

This is the starting point. If the initial decision is to deny the request (in whole

or in part), then an appeal can be made.

• There are FIVE levels of appeals:

1) Appeal or request for reconsideration

2) Independent Review Entity (IRE) contracted by CMS

3) Administrative Law Judge Hearing (the amount in controversy must meet a minimum standard as defined by CMS)

4) Medicare Appeals Council (MAC) Review

5) Judicial Review (the amount in controversy must meet a minimum standard as defined by CMS)

The appeals must be made in this

order.

32

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

grievances

A grievance is any complaint, other than one that involves a request for an initial determination or an appeal. Some examples of when a member might file a grievance are:

― Blue Shield did not respond to a coverage determination or appeal within the required timeframe.

― The member has to wait too long for a prescription.

― Blue Shield is sending materials that were not asked for by the member and/or are not related to the Part D drug plan.

• The grievance must be filed within 60 calendar days of the date of the event.

• A member, or his/her representative, can file a grievance in writing or verbally by calling Blue Shield Medicare Rx Plan Member Services.

• Grievances must be handled within 30 calendar days of receipt by plan.

• If the complaint relates to Blue Shield’s refusal to expedite a coverage determination or redetermination and the member hasn’t already purchased the drug, Blue Shield must respond within 24 hours of receipt of the grievance.

33

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

submitting online enrollment forms

You may submit your enrollment forms either by fax, mail, or online. The fax and

mail information is located right at the top of the enrollment form.

We encourage you to submit enrollments online.

• Faster. Online submissions are received by us immediately. No need to wait

for the mail.

• More accurate. The online enrollment form makes it clear which elements of

the application are required, and won’t let you move forward if you haven’t

completed them.

• Fewer pends. Because the online enrollments are more accurate, there is

less of a chance of your enrollment being pended because of missing

information.

• Easier. You can immediately receive an email with confirmation that the

enrollment has been submitted, with tracking number, so you can track its

progress.

Please contact your Regional Sales Manager, or Producer Services, for more

information about our online enrollment tool if you’re not already familiar with it.

34

Blue Shield’s MAPD, PDP and Medicare Supplement enrollment forms are

all available for easy online completion & submission!

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

enrollment form requirements

• A separate enrollment form must be completed for each Medicare beneficiary.

• All enrollment form fields must be completed.

– If the field does not apply, such as a request for an email address, mark N/A.

• The Sales Agent/Broker may complete or accept enrollment forms with future effective dates ONLY for beneficiaries who are “Aging In” (i.e., turning 65 years old within the next three months).

• Sales Agents/Brokers must see the beneficiary’s red, white and blue Medicare card to verify the spelling of the beneficiary’s name and Part A and Part B effective dates, and to indicate these on the enrollment form.

– The name on the enrollment form should be written exactly as it appears on

the Medicare card, even if the spelling is incorrect.

35

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

enrollment form requirements, continued

• The Medicare identification number (which is usually the Social Security number with an alpha character at the end) should be written on the enrollment form exactly as it appears on the red, white and blue Medicare card.

• It is critical that Sales Agents/Brokers ensure that all enrollment form fields are completed.

36

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

enrollment form requirements, continued

• Each Medicare beneficiary or authorized representative must sign and date his or her own enrollment form (e.g., a spouse cannot sign for a husband/wife).

• Sales Agents/Brokers must submit to Blue Shield all completed enrollment forms within 24 hours of the agent’s signature date.

– During the last week of an enrollment period, all enrollment forms must be turned in on a daily basis.

• Sales Agents/Brokers should have the Medicare beneficiary initial any mistakes or changes on an enrollment form at the point of sale.

• An agent/broker may make corrections to a completed application prior to submitting, as long as the agent/broker initials and dates the change, and provided that it isn’t correcting the beneficiary’s signature or date of signature.

• The member’s effective date of coverage will be the first day of the month following the month in which the completed enrollment form is received, depending on the receipt date in the Blue Shield office or by the Sales Agent/Broker.

– The date of receipt is the day the Sales Agent/Broker receives, signs, and dates the enrollment form.

– Upon receiving an enrollment request, Blue Shield must provide one of the following to the member within 10 calendar days:

• Acknowledgement notice;

• Request for additional information; or

• Notice of denial

37

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

pre-enrollment packet

The following documents are included in the pre-enrollment packet to help the Medicare beneficiary make an informed choice:

• Summary of Benefits (containing both PDP plans)

• Application Instructions

• Enrollment Form

• Abridged Formulary (List of Covered Drugs) – Comprehensive Formulary available by request through Member Services

• Medicare Star rating information

• Multi-language insert

38

PDFs of Materials are available in Spanish upon request

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

welcome kit

A Welcome Kit (post-enrollment package) is mailed to the member after the enrollment form is processed and confirmation is received from CMS.

Welcome Kits for Blue Shield’s Medicare Prescription Drug Plans includes:

• Cover letter

• Evidence of Coverage (comprehensive plan description including written explanation of the Plan’s process for exception requests, appeals and grievances)

• Pharmacy Directory Flyer (instructs on how to obtain a pharmacy directory)

• Mail Service Pharmacy Brochure and form

39

A plan ID card is mailed separately to the member prior to their

effective date, or within 10 days, whichever is later.

2017 Agent/Broker

Compensation Training

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

in this module

You will be introduced to Agent/Broker compensation including:

Compensation plan definition and types

Regulations for employed agents

Compensation payment guidelines

Compensation recovery requirements

41

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

general rules regarding compensation

• Plans/Part D Sponsors may not pay agents/brokers who have not been trained and tested annually on Medicare rules, regulations, and on details specific to the plan products they sell.

• Plans/Part D Sponsors may not pay compensation to agents/brokers not meeting licensure/appointment requirements or those that have been terminated for cause.

• When a Plan/Part D Sponsor and/or a contracted independent agent/broker terminates the contract, any future payment of existing business will be governed by the terms of the contract.

• Agents/brokers/TMOs must be trained and tested annually in order to receive renewal commissions on their active book of business.

42

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

compensation applicability & definitions

All compensation requirements contained in this section apply to independent agents/brokers. Employed and captive agents/brokers who only sell for one Plan/Part D Sponsor are exempt from compensation requirements. All other marketing and sales requirements must be met.

Compensation includes monetary or non-monetary remuneration of any kind relating to the sale or renewal of a policy including, but not limited to, commissions, bonuses, gifts, prizes, awards, and referral/finder’s fees.

Compensation DOES NOT include:

• The payment of fees to comply with State appointment laws

• Training

• Certification

• Testing costs

• Reimbursement for mileage to, and from, appointments with beneficiaries

• Reimbursement for actual costs associated with beneficiary sales appointments

such as venue rent, snacks, and materials

43

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

compensation applicability & definitions

Initial Compensation: Initial compensation may be paid at or below the fair market value (FMV) cut-off amounts published by CMS annually.

Renewal Compensation: Renewal compensation may be paid for each enrollment in Year 2 and beyond, up to fifty (50) percent of the current FMV published by CMS annually.

A “like plan type” enrollment includes:• A PDP to another PDP

• An MA, MA-PD, or MMP to another MA, MA-PD, or MMP

• A Section 1876 cost plan to another Section 1876 cost plan

An “unlike plan type” enrollment includes: • An MA or MA-PD plan to a PDP or Section 1876 cost plan

• A PDP to a section 1876 cost plan or an MA (or MA-PD) plan

• A Section 1876 cost plan to an MA (or MA-PD) plan or PDP

NOTE: For dual enrollments (e.g., enrollment in an MA-only plan and a stand-alone PDP), the compensation rules apply independently to each plan. However, when dual enrollments are replaced by an enrollment in a single plan, compensation is paid based on the MA movement (e.g., movement from an MA-only plan and PDP to an MA-PD plan would be compensated at the renewal compensation amount for the MA to MA-PD “like plan type” move).

44

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

compensation payment requirements

• Plans/Part D sponsors must notify CMS of their compensation schedule by the date specified each year

• Plans/Part D Sponsors must establish a compensation structure for new and replacement enrollments and renewals effective in a given plan year that must be available upon CMS request for audits, investigations, and to resolve complaints. Compensation structures must be in place by October 1 each year.

• The compensation year is January 1 through December 31 of each year. Payments must be calculated based on the January through December enrollment year. Payments may not be based on enrollment years (rolling basis) other than January through December. For example, if a beneficiary’s enrollment is effective on September 1, then the initial year for that beneficiary ends on December 31, even though the beneficiary has only been in the plan for four (4) months. In January of the next year, the plan would begin paying renewal payments to the agent who assisted this beneficiary.

• Plans/Part D Sponsors may only pay compensation for the current year enrollment. Payment may not be paid until January 1 and must be paid in full by December 31 of the enrollment year. Plans/Part D sponsors may pay compensation annually, quarterly, monthly, or utilizing other schedules.

45

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

compensation payment requirementsInitial Compensation is paid under the following scenarios:

• The beneficiary’s first year of enrollment in any plan;

• A beneficiary moves from an employer group plan to a non-employer group

plan;

• A beneficiary changes plans during their initial enrollment year; or

• A beneficiary makes an “unlike plan change.”

Initial Compensation must be pro-rated when:

• A beneficiary enrolls in an “unlike plan type,” during their renewal year; or

• A beneficiary changes plans during their initial enrollment year.

Renewal compensation may be paid to agents/brokers under the following three

scenarios:

• Following the initial year compensation;

• A beneficiary enrolls in a new “like plan” within the same Parent Organization or

between two different Parent Organizations; or

• A beneficiary enrolled in an MMP switches to an MA plan or an MA-PD plan

(and vice versa).

Renewal Compensation must always be pro-rated.

46

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

compensation payment requirements

• When a beneficiary enrolls in a plan and has no prior plan history (as indicated on the MARX agent/broker compensation report), Plans/Part D Sponsors may pay the full year initial compensation amount or a pro-rated amount based on the number of months the beneficiary is enrolled

• When the beneficiary changes plans during the initial year, the Plan/Part D Sponsor must pay the agent/broker at a pro-rated initial year rate, based on the number of months the beneficiary is enrolled. For example, if an initial beneficiary changes from one Parent Organization to another

Parent Organization in May, the new Parent Organization must pay 8/12ths of the initial compensation.

• Referral/Finder’s fees paid to agents and brokers, including independent, employed, and captive agents and brokers, may not exceed $100 ($25 for PDPs). This amount is not reasonably expected to provide enough financial incentive for an agent or broker to recommend or enroll a beneficiary into a plan that is not the most appropriate for the beneficiary’s needs

• Referral/finder’s fees paid to all agents and brokers must be part of total compensation and must not to exceed FMV for that contract year.

47

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

compensation recovery requirements

• Plans/Part D Sponsors must recover compensation payments from agents/brokers under two circumstances: 1) when a beneficiary disenrolls from a plan within the first three months of enrollment (rapid disenrollment), and 2) any other time a beneficiary is not enrolled in a plan.

Rapid Disenrollment

• Rapid disenrollment applies when an enrollee moves from one Parent Organization to another Parent Organization, or when a enrollee moves from one plan to another plan within the same Parent Organization

• Rapid disenrollment compensation recovery does not apply when a beneficiary enrolls in a plan effective October 1, November 1, or December 1, and subsequently uses the Annual Election Period to make changes to their current plan for an effective date of January 1 of the following year during the Annual Election Period. If, however, a

beneficiary enrolls for October 1, November 1 or December 1 and disenrolls from the plan (unrelated to the AEP), the Plan/Part D Sponsor should recover compensation based on the rapid disenrollment.

• Rapid disenrollment compensation recovery does not apply when CMS determines that recoupment is not in the best interests of the Medicare program. Such situations include when a beneficiary disenrolls within the first three months for any of the following reasons:

• Other creditable coverage

• Moving into or out of an institution;

• Gains/drops employer/union sponsored coverage;

• CMS sanction against the plan/contract violation; (continued on next page)

48

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

Compensation Recovery Requirements (Rapid

Disenrollment, Continued)

• Plan terminations and non-renewals;

• In order to coordinate with Part D enrollment periods;

• In order to coordinate with a State Pharmaceutical Assistance Program;

• Becoming dually eligible for both Medicare and Medicaid;

• Qualifying for another plan based on special needs;

• Becoming LIS eligible;

• Qualifying for another plan based on a chronic condition;

• Due to an auto, facilitated, or passive enrollment;

• Death;

• Moves out of the service area;

• Non-payment of premium;

• Loss of entitlement;

• Retroactive notice of Medicare entitlement; or

• When moving to a plan with a 5-star rating or from an Low Performing Icon (LPI) plan

into a higher rated plan.

49

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

• Plans/Part D Sponsors must recover a pro-rated amount of initial compensation when an enrollee disenrolls

from a plan. The amount recovered must be equal to the number of months not enrolled. For example, an

enrollee ages in effective April 1. The enrollee disenrolls effective September 30 of the same year. The plan

initially paid a full initial compensation. Since the enrollee disenrolled (not a rapid disenrollment), the

Plan/Part D Sponsor must recover from the agent or broker 6/12ths of the initial compensation (January

through March and October through December).

• Plans/Part D Sponsors must recover a pro-rated amount of renewal compensation when an enrollee

disenrolls from a plan. This amount must be equal to the number of months not enrolled. For example, a

renewal enrollee disenrolls effective February 28. The Plan/Part D Sponsor must recover from the agent or

broker 10/12ths of the renewal payment if the renewal payment had been paid for the entire 12-month

period.

• Plans/Part D Sponsors have the option to pay the agent or broker either full or pro-rated compensation for

initial enrollments that are effective later than January 1 and the enrollees have no prior plan history.

However, if the Plan/Part D Sponsor pays a full initial compensation and the enrollee disenrolls during the

contract year, the Plan/Part D Sponsor must recoup a pro-rated amount for all months the beneficiary is not

enrolled, regardless of whether it is a change from one Parent Organization to another Parent Organization

or from one PBP in one organization to another PBP within the same organization. This would include months

prior to the enrollment. For example, a beneficiary ages into Medicare and elects an MA-PD plan (Plan A),

effective April 1. The beneficiary moves and is eligible for a special enrollment period. The beneficiary elects

a new MA-PD (Plan B), effective November 1. Plan A must recoup 5/12ths of the initial compensation

(January through March and November through December) to account for the months the beneficiary was

not enrolled in Plan A. Since the beneficiary had prior plan history when enrolled in Plan B, Plan B may only

pay a pro-rated initial compensation equal to 2/12ths (November through December).

• Plans/Part D Sponsors must recover from the agent or broker a pro-rated amount of compensation when

there is a “like plan change” from an MA or MA-PD to MMP. Compensation is not to be paid for the months

the enrollee is in the MMP for that compensation cycle year. For example, a renewal enrollee makes a “like

plan type” change from an MA to MMP effective July 1 of the compensation cycle year. The MA Plan must

recover 6/12ths of the renewal payment.

other compensation recovery

50

For Agent use only. Plans contain exclusions and limitations. Distribution to consumers, other insurers, or any other person or

company is strictly prohibited.

module complete!

Congratulations!

You’ve completed the Medicare Part D Training for Certification.

What’s next?

• Take the quiz to receive your certification.

• When you complete your exam, you will receive your score immediately.

• You must pass the quiz with a score of at least 85%. If you do not

receive a passing score, you can retake the exam up to a maximum of 5 times to pass.

51