Biotech News 2010 Story

5

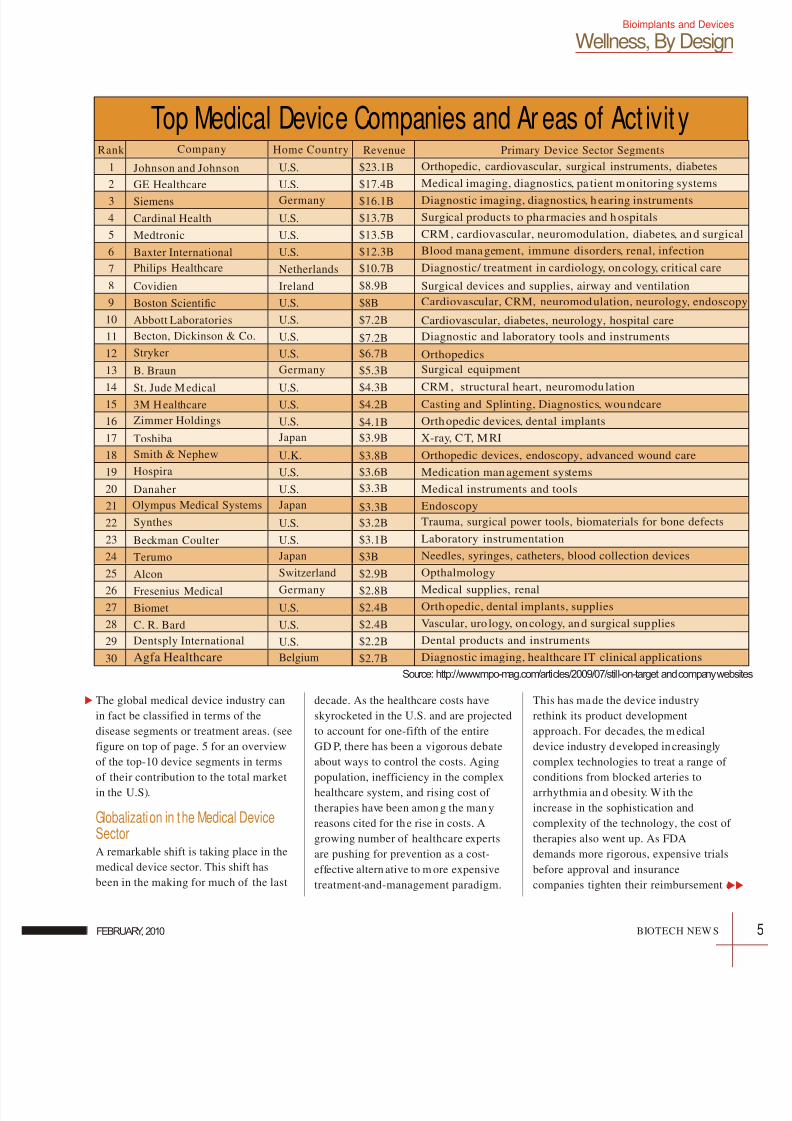

B ioimplants and devices sector, also known as the medical device sector, is a key part of the healthcare industry worldwide. The sector covers a wide spectrum of devices including diagnostics, imaging, dental, surgical, ocular, wound care, orthopedic and cardiovascular devices. Although the $250- billi on medical d evice sector is substantially smaller than the $750-bil lion pharmaceutical industry, it is growing 6- 8% annually compared to 2-4% growth rate of the global pharmaceutical market. The faster growth in the device sector is driven in large part due to the substantial clinical needs that have remained unadd ress ed by drugs. The growth is s ubstantially higher over 10% in the emerging markets as they become increasingly affluent and adopt technologies widely accepted in the developed markets. As the pharmaceutical industry growth slows down, larg e healthcare compan ies looking for growth have increasingly turned their attention to medical devices. In fact, 2009 saw a number of large mergers and acquisitions in the device sector, despite the global economic slump. Medical device sector, much like the pharmaceutical industry, is dominated by some very large players who h ave market leadership in a num ber of segments within the sector. While these large companies have internal product development teams, the thou sands of start-ups funded by venture capital form the backbone of device innovation, contributi ng a m ajority of new products in the m arket. The entrepreneurial culture of the device industry is widely recognized and well-supported by all the stakeholders in the medical device eco- system, including large device compa nies, investors , inventors, clinici ans, vendor s and service providers, Structure of and Evolution within the Medical Device Se ct or academia, and the gove rnment. M ost of these start-ups are acquired by large companies afte r the concept or the technology has been validated through animal and early clinical trials. Large companies then take over the later stages of product devel opment, perform mo re extensiv e clinical trials, seek regulator y approval and insurance coverage, and carry out product comm ercialization. Substantial capabilities of large companies in these areas built through heavy investment of resources create a barrier to entry for any new entrant. The select few companies that do grow to become a m id-size enterprise (say , > $100 million in sales) often get acquired in large acquisition dea ls . Leading device companies are active i n mu ltiple therapeutic areas (see table on p age 4 for a list of largest gl obal medical device companies and their device sale s fig ures. Ma ny o f th ese also have substantial presence in the pharmaceutical indu stry) . Bioimplants and Devices Wellness, By Design Anurag Mairal 4 BIOTECH NEWS VOLUME 5 NO . 1 | Anur ag Mai r al is Associate Director, Program Development, Stanford-India Biodesign, Stanford University , U S A Ph D (E-mail: [email protected]) COVER STORY

-

Upload

kaushik-sarkar -

Category

Documents

-

view

222 -

download

0

Transcript of Biotech News 2010 Story

8/8/2019 Biotech News 2010 Story

http://slidepdf.com/reader/full/biotech-news-2010-story 1/5

8/8/2019 Biotech News 2010 Story

http://slidepdf.com/reader/full/biotech-news-2010-story 2/5

8/8/2019 Biotech News 2010 Story

http://slidepdf.com/reader/full/biotech-news-2010-story 3/5

8/8/2019 Biotech News 2010 Story

http://slidepdf.com/reader/full/biotech-news-2010-story 4/5

8/8/2019 Biotech News 2010 Story

http://slidepdf.com/reader/full/biotech-news-2010-story 5/5