Biotech in Europe: Scaling Innovation

111

CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of McKinsey & Company is strictly prohibited Barcelona, May 20-21 2019 McKinsey report | Bio€quity Europe conference Biotech in Europe: Scaling Innovation

Transcript of Biotech in Europe: Scaling Innovation

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

Barcelona, May 20-21 2019

McKinsey report | Bio€quity Europe conference

Biotech in Europe: Scaling Innovation

McKinsey & Company 2

Biotech in Europe: Scaling innovationExecutive summary

Introduction

Biotech is entering its next S-curve of growth, as the industry moves into the next decade. Gene therapies, stem cell treatments, antisense, siRNA and CAR-T are just some of today’s driving forces. Even more innovative science and technology is on the horizon.

Across a fragmented landscape, the maturing biotech space in Europe needs to achieve greater scale in the innovation it is creating, and deliver on the promise of the golden age of biotech.

In this context, this report investigates the path forward for the region, and we attempt to answer three fundamental questions:

1. What makes the European biotech space uniquely attractive?

2. What financing is required to fuel growth?

3. Looking forward, how can biotech leaders and investors succeed?

1. What makes the European biotech space uniquely attractive?

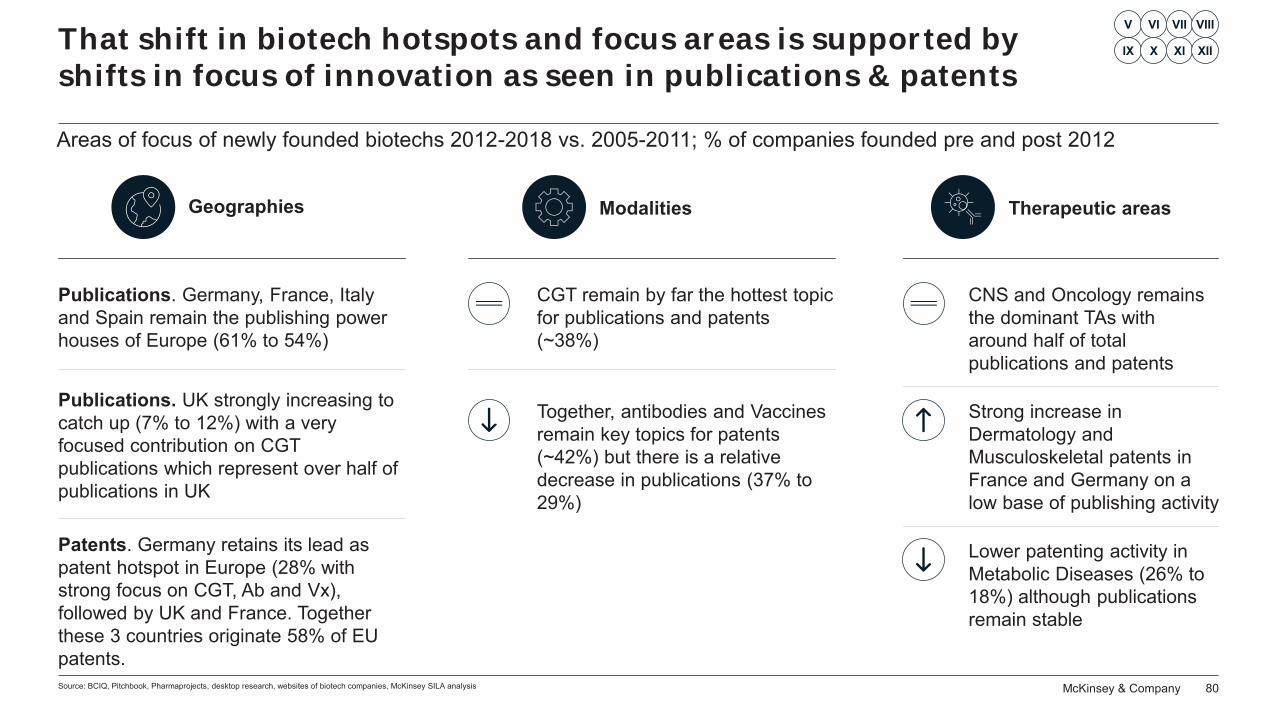

Hotspots, across a fragmented landscape. The biotech landscape in Europe is complex. Hundreds of companies, multiple countries, different paths toinnovation and financing and, of course, different geographies. To “see” through the complexity, ~1000 European biotech companies were identifiedand naturally clustered with a purpose-built methodology. This clusteringallowed for the mapping of biotech hotspots, in terms of geography,modalities and therapeutic areas clusters. This mapping reveals trending hotspot shifts, across the region, over time. It provides insight into thedirection the industry is taking in the future. For example, the UK has been disproportionately accelerating across technologies and disease areas, becoming home to 35% of all new biotechs since 2012. In fact, the trend of Europe moving at “two speeds” is accelerating. While “Service provision” still represents the largest modality focus in most countries, Cell and Gene Therapy (CGT) and mmunotherapies are the fastest growing – now close toone third of companies absorbing 40% of investment. In turn,

Oncology and CNS absorbing about half of the investment overth period.

World-class science and innovation in Europe. Europe is home to 32% of the top 50 life sciences universities, and holds a similar level of publication in top 10 journals vs. the US. Its leadership in science development means it leads both the US and China in terms of publications. Publication topics of focus are largely similar across regions. However, that innovation

McKinsey & Company 3

Biotech in Europe: Scaling innovationExecutive summary (continued)

strength does not yet translate fully to patents or new medicines. For example, in terms of patent origination, the US and, more recently China are 3x to 9x more productive respectively. Further down the innovation chain, European biotechs have contributed 13% of biotech-originated FDA new drug approvals in 2017-18, which is 6 lower than those from USbiotechs. Looking forward, however, there is potential: European biotechs overall benefit from 5 less investment versus US counterparts andshow more promise in emerging topics, driving 32% of all projects in Ph3or registration for products based on technology such as antisense, viral vectors, or siRNA. On an indexed base, we estimate Early Innovation (based on publications and patents) to be 0.73 versus the US, while Late Innovation (based on drug approvals and innovative candidates) is down to 0.41.

Top innovation & talent. Biotech experts, from Europe and beyond, consider the overall level of innovation and the quality of R&D talent inEurope very high, close to US levels and well above China. However, on such scaled assessment, there is a perceived limitation in the availability of specific profiles and the ability to attract and retain it. There is a perceived lack of both biotech-specific experience and entrepreneurial spirit around the biotech ecosystem in Europe. That adds to the challenge of financing.

2. Is financing where it need to be?

“Good value” for European biotechs. The average deal size has grown to~USD 165m average in 2018. While still around 40% lower than the higher-priced US deals, this represents a growth of 20% per annum since 2012. Inaddition, the return profile in Europe has a somewhat advantageous shape. Pre-money valuations are ~30% lower than in the US and the operational costlevels are often lower (estimated 60% of US cost in terms of structure or talent).

Financing for European biotechs is maturing. Available venture capital isestimated to have tripled to USD 2.3 bn in 2018. In the last seven years, stronger European VC funds have emerged and have doubled in average size. Most experts agree that sufficient financing is now available for early-stage private venture rounds. As business models evolve in the region, deal types are diversifying beyond pure licensing, now 35% of deals in 2018 versus up to 80% in 2012. While there is growing appetite to build late-stage plays, especially when focused on niche therapies, the US still holds a higher number of deals with higher mean value (Europe is 42% lower). This is driven by the stronger focus on business acquisitions and direct investment inthe US.

The (late-stage) financing gap v the US remains, and continues to grow.Despite the positive dynamic , the private venture financing gap versus USbiotechs is growing and now stands at almost 5 . This gap is especiallynotable when raising larger amounts in late-stage rivate venture financing

McKinsey & Company 4

Biotech in Europe: Scaling innovationExecutive summary (continued)

rounds or on public markets. This is exacerbated at country level, asthe ratios between early and late financing are highly variable acrossEurope. On public markets, IPOs are 3 larger on Nasdaq than onEuropean ex ges. As a result, European biotechs increasingly look tothe US for their growth capital: almost 30% of private venture investmentnow originates from the US, and since 2012 almost one in three Europeanbiotechs filing for an IPO have done so directly on US exchanges onsimilar terms to their US counterparts. In addition, over 95 % of total follow-on offerings by European biotechs have been on US exchanges, not European ones. Looking east, few European biotechs appear equipped toexplore investment in and from China, despite an increase in the appetite of those investors for Europe for the next 2-3 years.

3. Looking forward: How can leaders and investors succeed?

Overall, Europe remains an opportunity as a less mature biotech ecosystem than the one found in the US. Despite the increasing financing gap, attractive opportunities await those who focus on cultivating them. Europe has strong innovation fundamentals, and talent pools. It is less ‘over-fished’ than the US, while boasting access to sufficient early-stagefinancing. It has strong signs of success and “doing more with less”. To capitali e, biotech leaders and investors need to excel in 3 dimensions:

Think global and build global competitiveness. Developdifferentiated and globally competitive products to secure marketaccess in an evolving ‘future state’. Focus on defined perimeters towin big.

Prepare for success. Carefully stage when/how exactly to go tofinancial markets. Attract entrepreneurial and biotech experience,credibility, non-Europe exposure and networks. Be flexible in workingwith talent

From the East to the West. Adopt a clear path to US financing early-on. Build a board and syndicates geared to larger private rounds anda potential IPO. As Chinese investor sentiment turns, look ast forraising capital and forming partnerships.

McKinsey & Company 5MMMMMMMMccccMMMMMMMMMMMMMMMMccMMMMMMMMcMMMMMMMMMcMMMMMMcMMcMcMMMMMcMMMMMMMMMMMMMMMMMMMMMMMMMMMMMMMMMMMMMMccKiKKiKiKiiiiiinnnnnnnnnnnnnsnssnsnsnssnsnnssssnnnnnsnsnnnnsnsnsnnnnssnsssssnnnsssnsssnnsssssssssnssseeeeeeeyeyeyeyeyyyyyyeeyeeeeeeeeeeyyeeeeeeeeeeeeeyeeyeeeeeeeeyyeeyeeeeeeeeeyeeeee &&&& CCCCCCCCCCCCCCCCCCCCCCCCCCCCCCComomomomomomomomomommommmmmmomoomomommommmommmomooomooomommmommmmmmooo papapapappp nynnynynynynnnynynnnnnynnnnnnnnnnnnnnnnnnnnnnnnnnnyynnnnnnnnnnnnnnnnnnnynnnnnnnnnnynnnnnnnynnnnynnnnnnnynnnnnnnnnnnnnnnnn 555555555555555555555555555555555555555555555555555555555555555

Three questions on scaling Biotech Innovation in Europe

01

What makes the European biotech space

uniquely attractive?

03

Looking forward: How can leaders and investors succeed?

02

Is financing where it needs to be?

McKinsey & Company 6

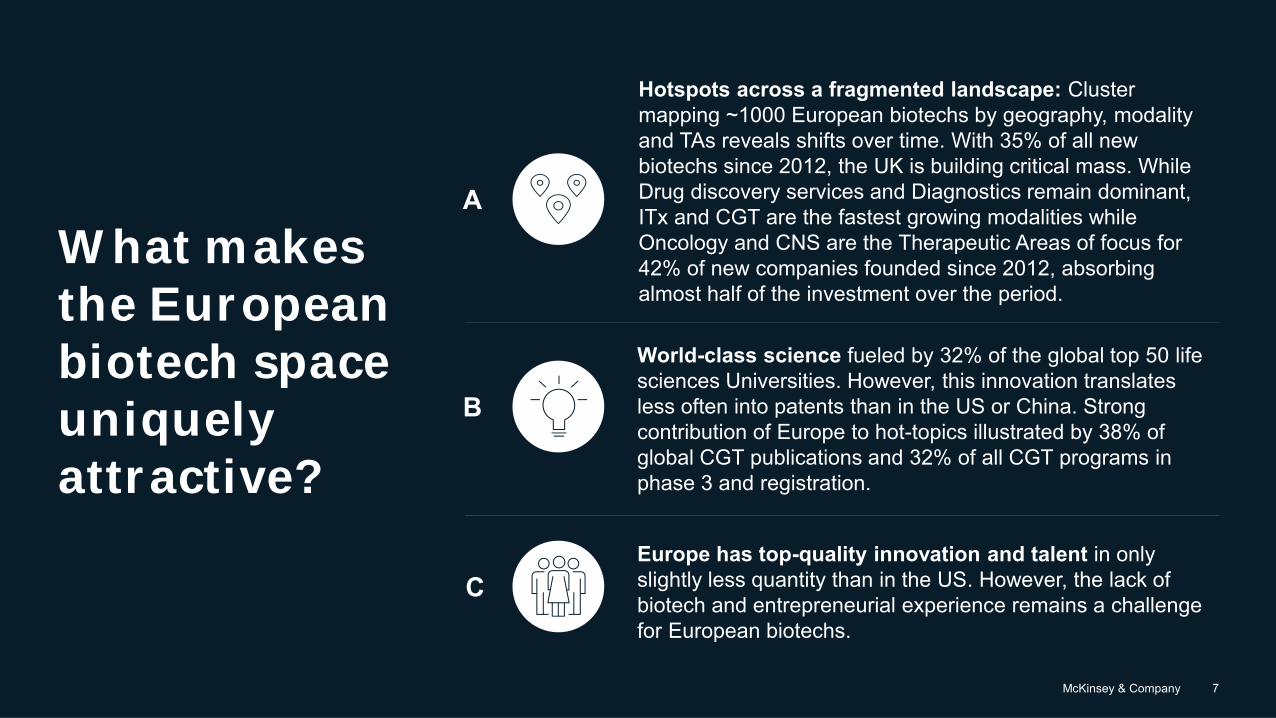

What makes the European biotech space uniquely attractive?

A. Hotspots across a fragmented landscape

B. World-class science

C. Top innovation and talent

01

McKinsey & Company 7

What makes the European biotech space uniquely attractive?

B

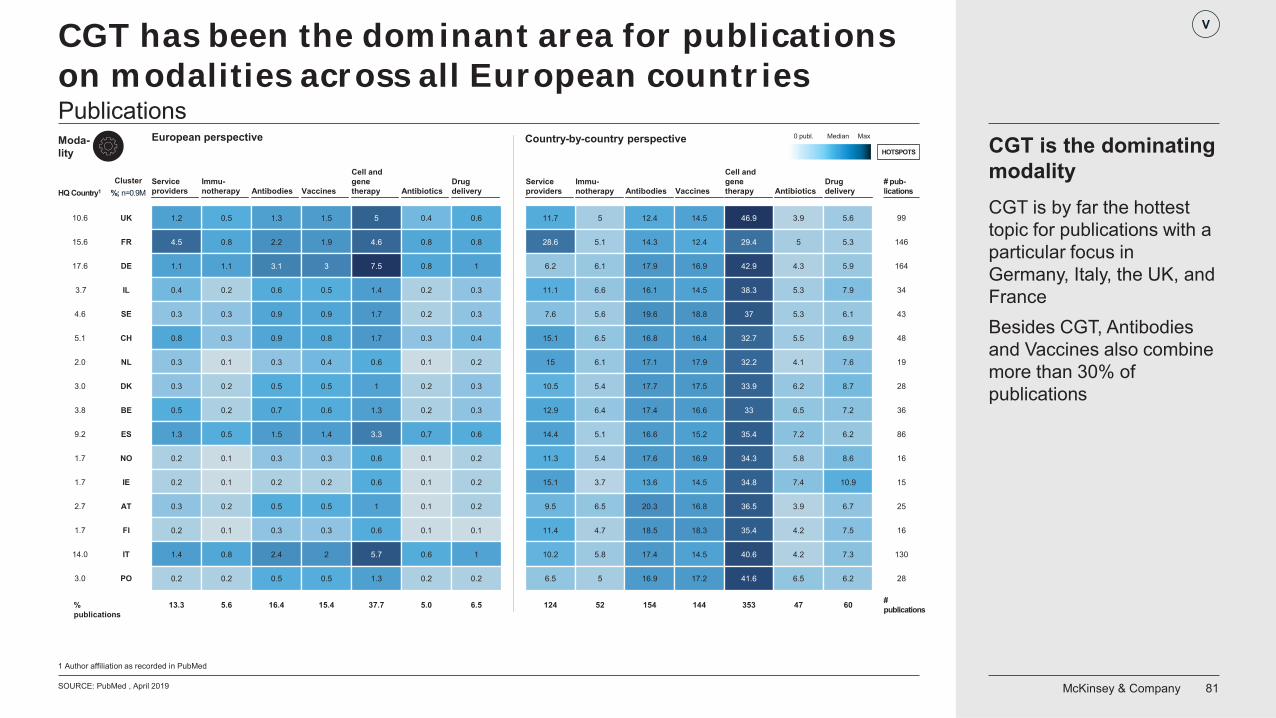

World-class science fueled by 32% of the global top 50 life sciences Universities. However, this innovation translates less often into patents than in the US or China. Strong contribution of Europe to hot-topics illustrated by 38% of global CGT publications and 32% of all CGT programs in phase 3 and registration.

CEurope has top-quality innovation and talent in only slightly less quantity than in the US. However, the lack of biotech and entrepreneurial experience remains a challenge for European biotechs.

A

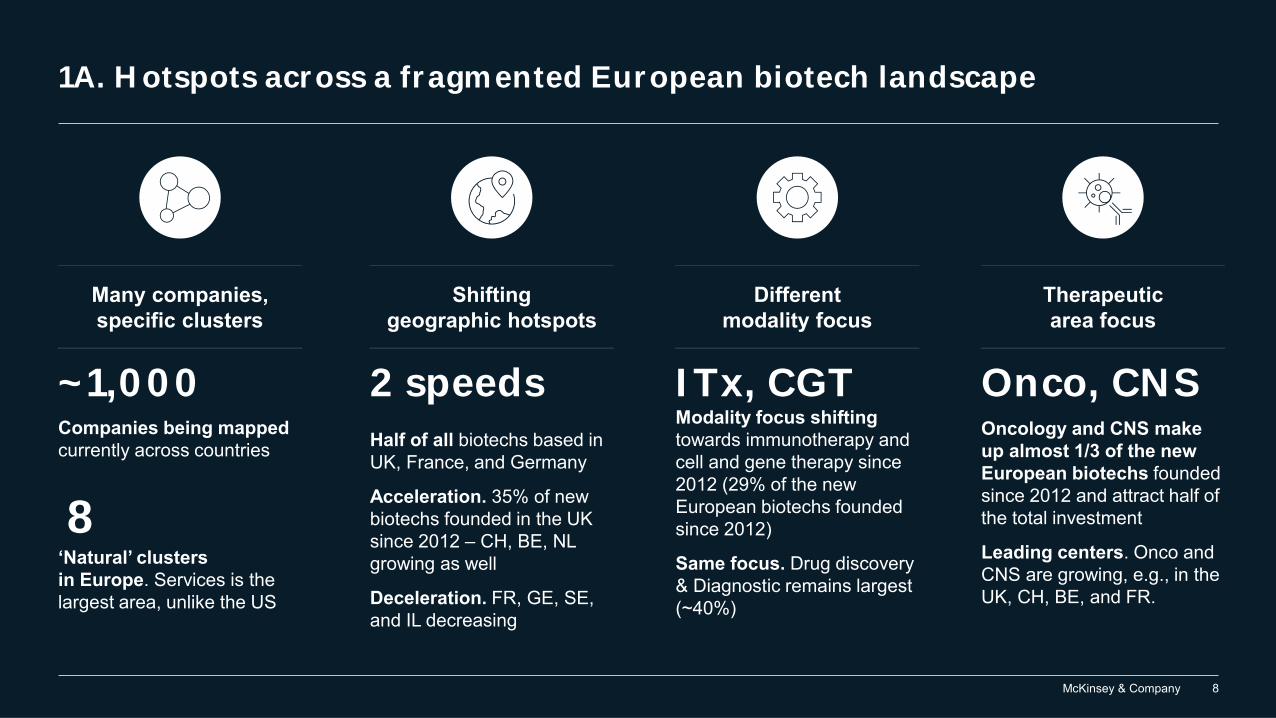

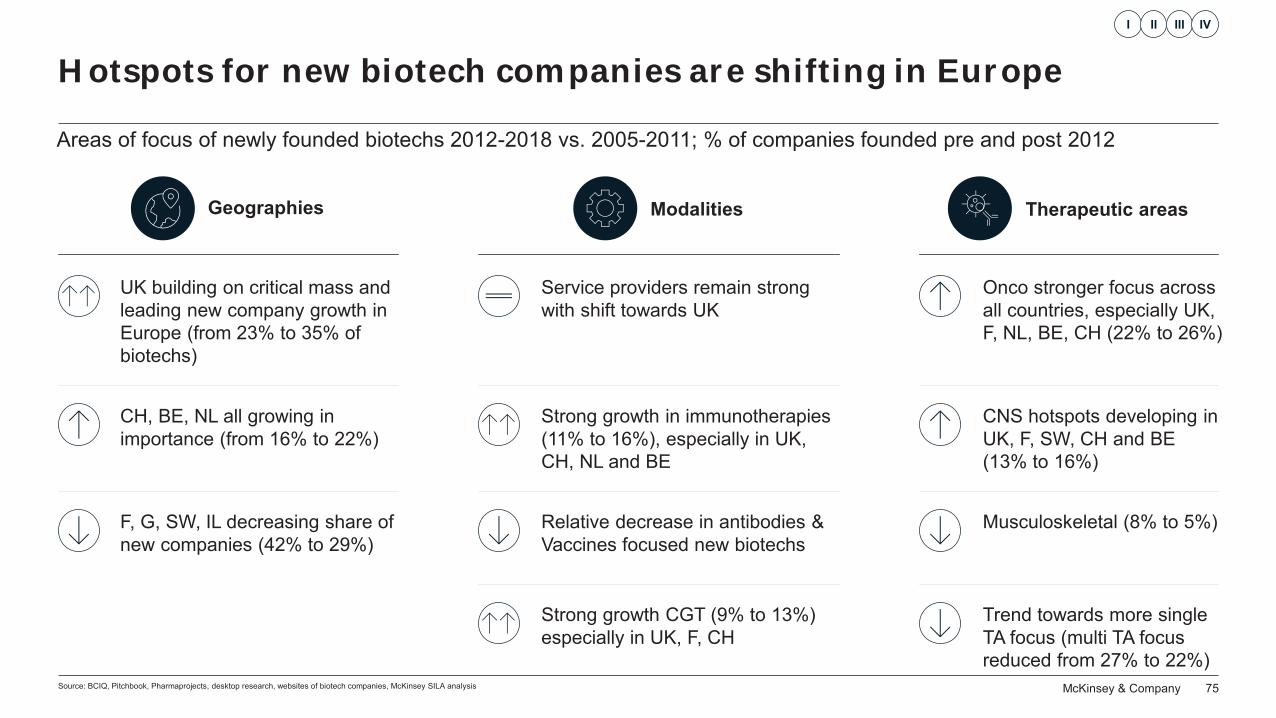

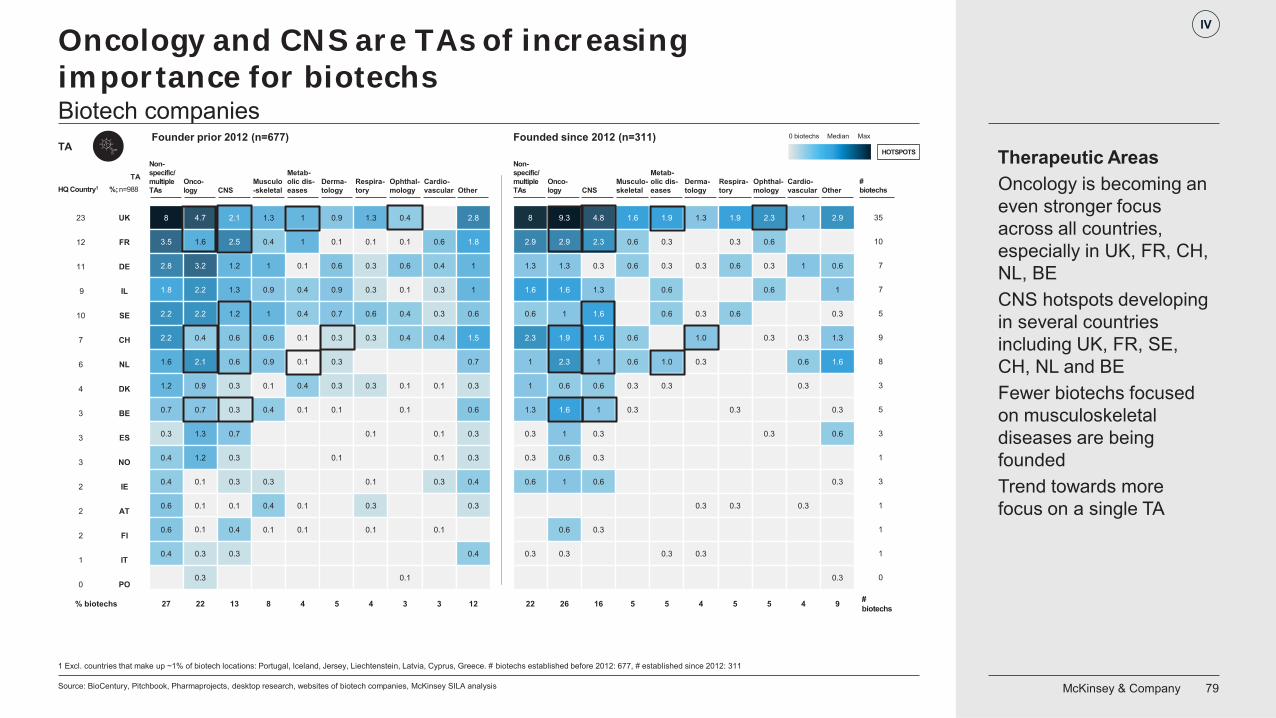

Hotspots across a fragmented landscape: Cluster mapping ~1000 European biotechs by geography, modality and TAs reveals shifts over time. With 35% of all new biotechs since 2012, the UK is building critical mass. While Drug discovery services and Diagnostics remain dominant, ITx and CGT are the fastest growing modalities while Oncology and CNS are the Therapeutic Areas of focus for 42% of new companies founded since 2012, absorbing almost half of the investment over the period.

McKinsey & Company 8

1A. Hotspots across a fragmented European biotech landscape

2 speeds

Shifting geographic hotspots

Half of all biotechs based in UK, France, and Germany

Acceleration. 35% of new biotechs founded in the UK since 2012 – CH, BE, NL growing as well

Deceleration. FR, GE, SE, and IL decreasing

~1,000

Many companies, specific clusters

8

Companies being mappedcurrently across countries

‘Natural’ clusters in Europe. Services is the largest area, unlike the US

Modality focus shifting towards immunotherapy and cell and gene therapy since 2012 (29% of the new European biotechs founded since 2012)

Same focus. Drug discovery & Diagnostic remains largest (~40%)

ITx, CGT

Different modality focus

Therapeutic area focus

Onco, CNSOncology and CNS make up almost 1/3 of the new European biotechs founded since 2012 and attract half of the total investment

Leading centers. Onco and CNS are growing, e.g., in the UK, CH, BE, and FR.

McKinsey & Company 9

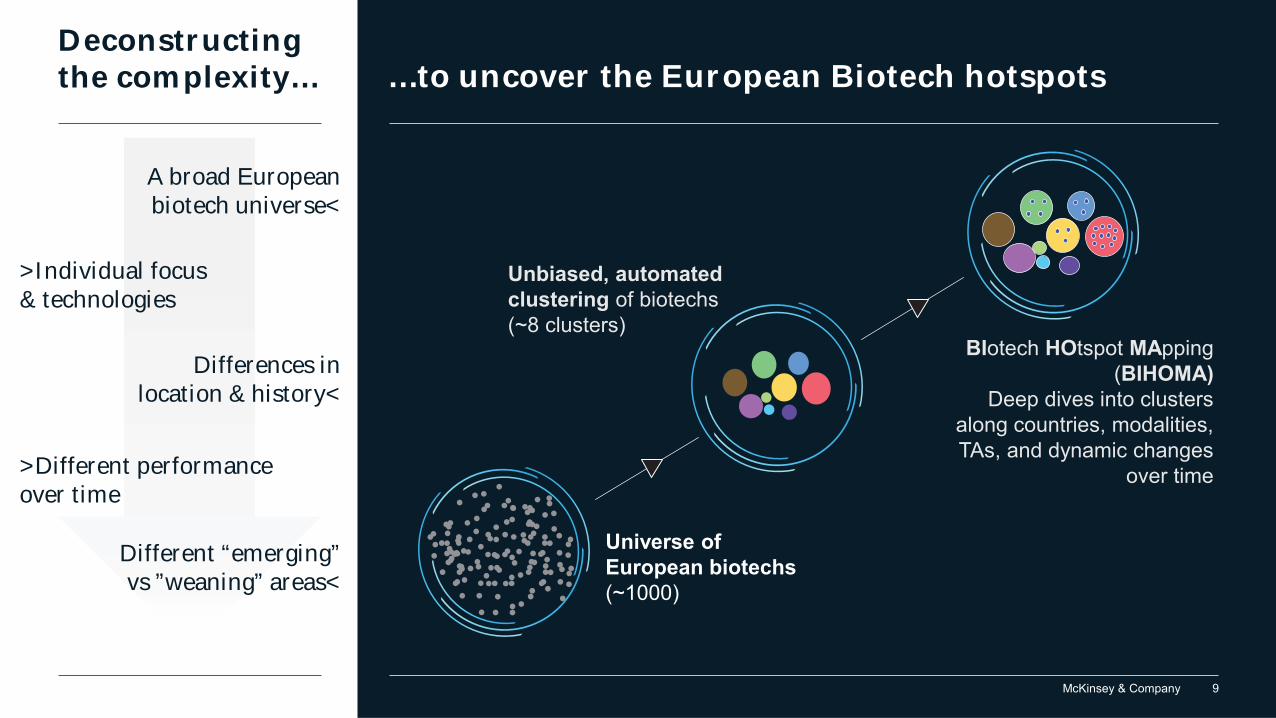

Deconstructing the complexity… …to uncover the European Biotech hotspots

A broad European biotech universe<

>Individual focus& technologies

Differences in location & history<

>Different performanceover time

Different “emerging” vs ”weaning” areas<

Universe of European biotechs (~1000)

Unbiased, automated clustering of biotechs (~8 clusters)

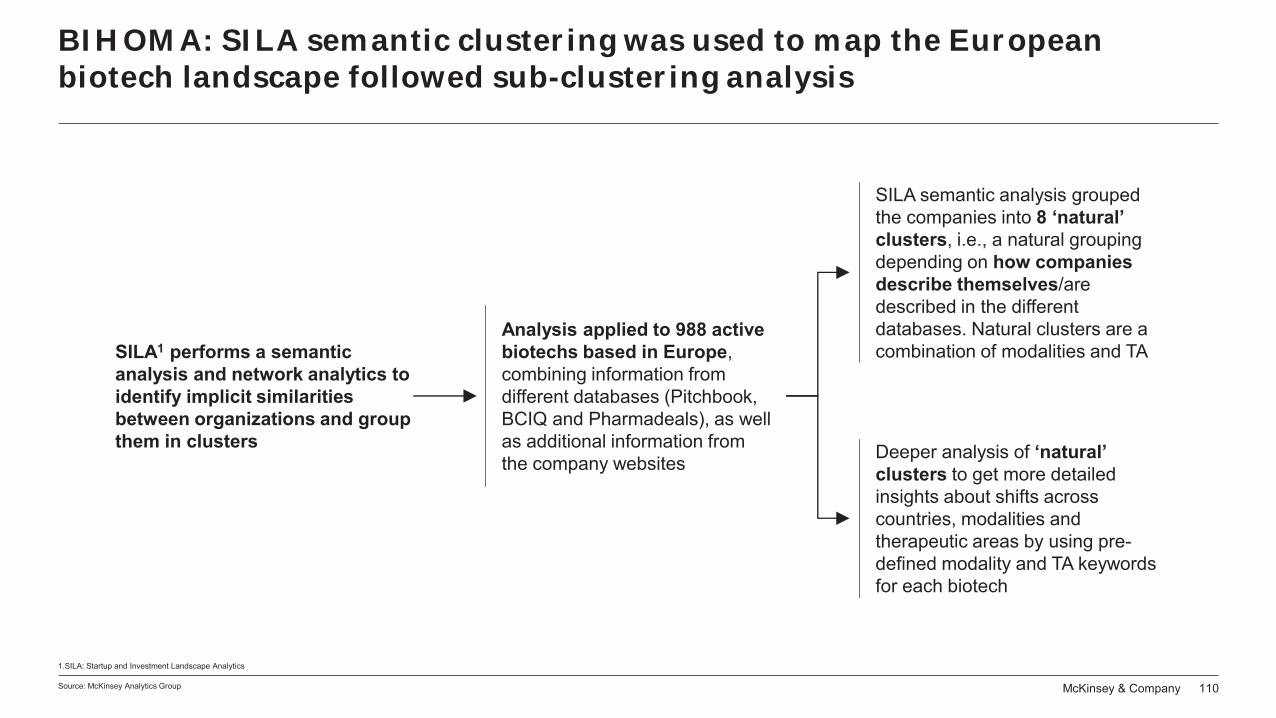

BIotech HOtspot MApping(BIHOMA)

Deep dives into clusters along countries, modalities, TAs, and dynamic changes

over time

McKinsey & Company 10Source: Startup and Investment Landscape Analytics, Pitchbook February 2019, BCIQ February/March 2019

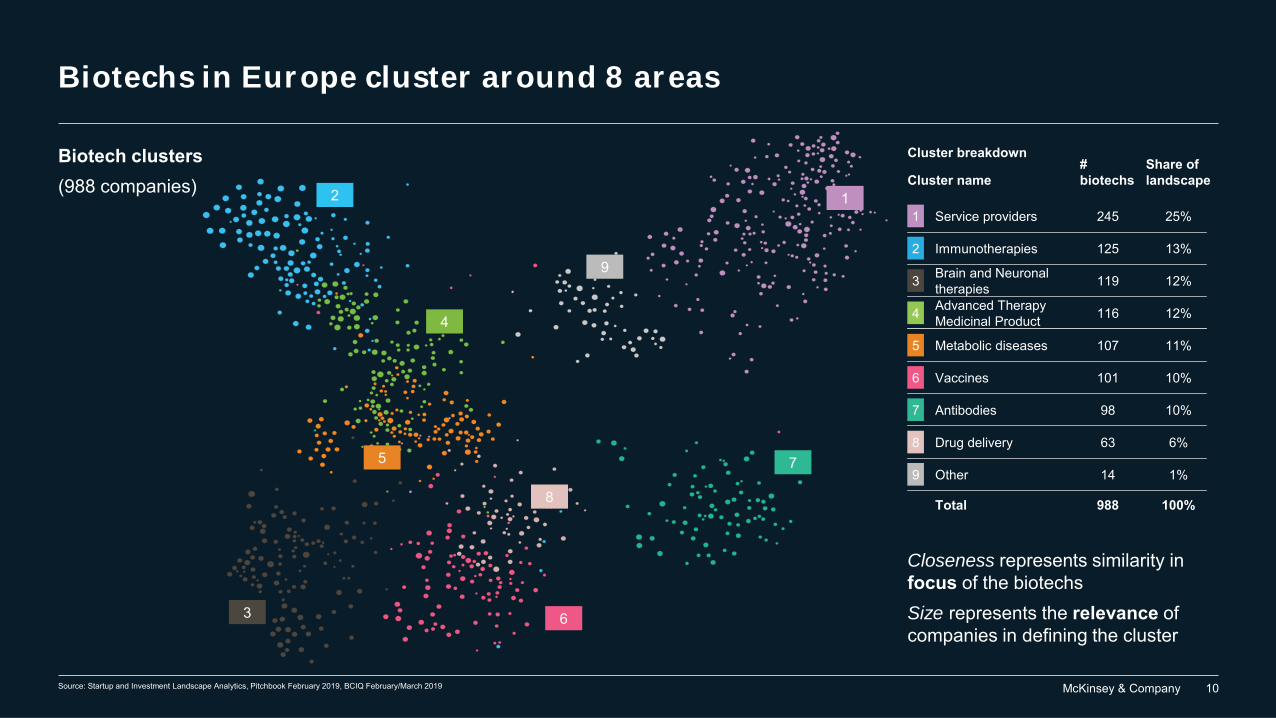

Biotech clusters (988 companies)

Closeness represents similarity in focus of the biotechsSize represents the relevance of companies in defining the cluster

Cluster breakdown

4 Advanced Therapy Medicinal Product 116 12%

5 Metabolic diseases 107 11%

6 Vaccines 101 10%

Total 988 100%

7 Antibodies 98 10%

8 Drug delivery 63 6%

9 Other 14 1%

3 Brain and Neuronal therapies 119 12%

2 Immunotherapies 125 13%

Service providers 245 25%1

# biotechs

Share of landscapeCluster name

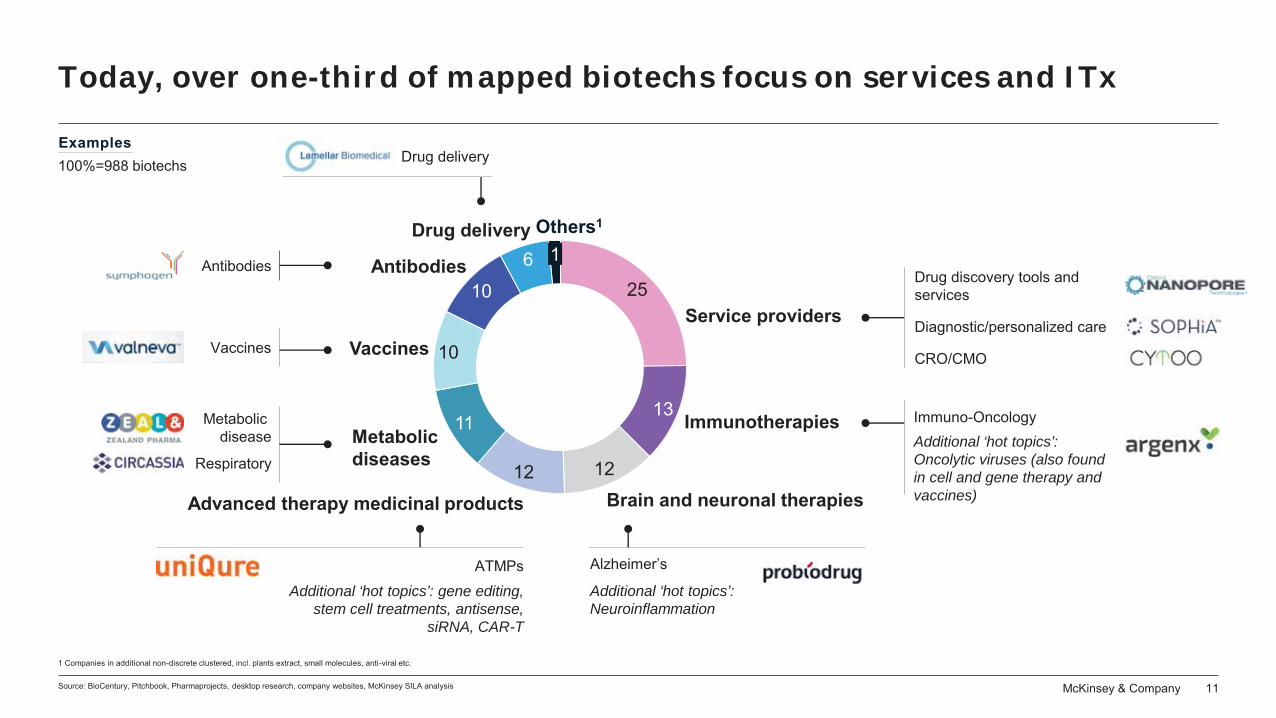

Biotechs in Europe cluster around 8 areas

4

75

1

3 6

2

8

9

McKinsey & Company 11

Drug delivery

25

13

1212

11

10

106

Drug delivery

Metabolic diseases

Advanced therapy medicinal products

Service providers

Others1

Immunotherapies

Brain and neuronal therapies

Vaccines

Antibodies 1

Today, over one-third of mapped biotechs focus on services and ITx

Source: BioCentury, Pitchbook, Pharmaprojects, desktop research, company websites, McKinsey SILA analysis

1 Companies in additional non-discrete clustered, incl. plants extract, small molecules, anti-viral etc.

Vaccines

Antibodies

Metabolic disease

Respiratory

ATMPsAdditional ‘hot topics’: gene editing,

stem cell treatments, antisense, siRNA, CAR-T

Alzheimer’s

Additional ‘hot topics’: Neuroinflammation

Diagnostic/personalized care

Drug discovery tools and services

CRO/CMO

Immuno-OncologyAdditional ‘hot topics’: Oncolytic viruses (also found in cell and gene therapy and vaccines)

Examples100%=988 biotechs

McKinsey & Company 12

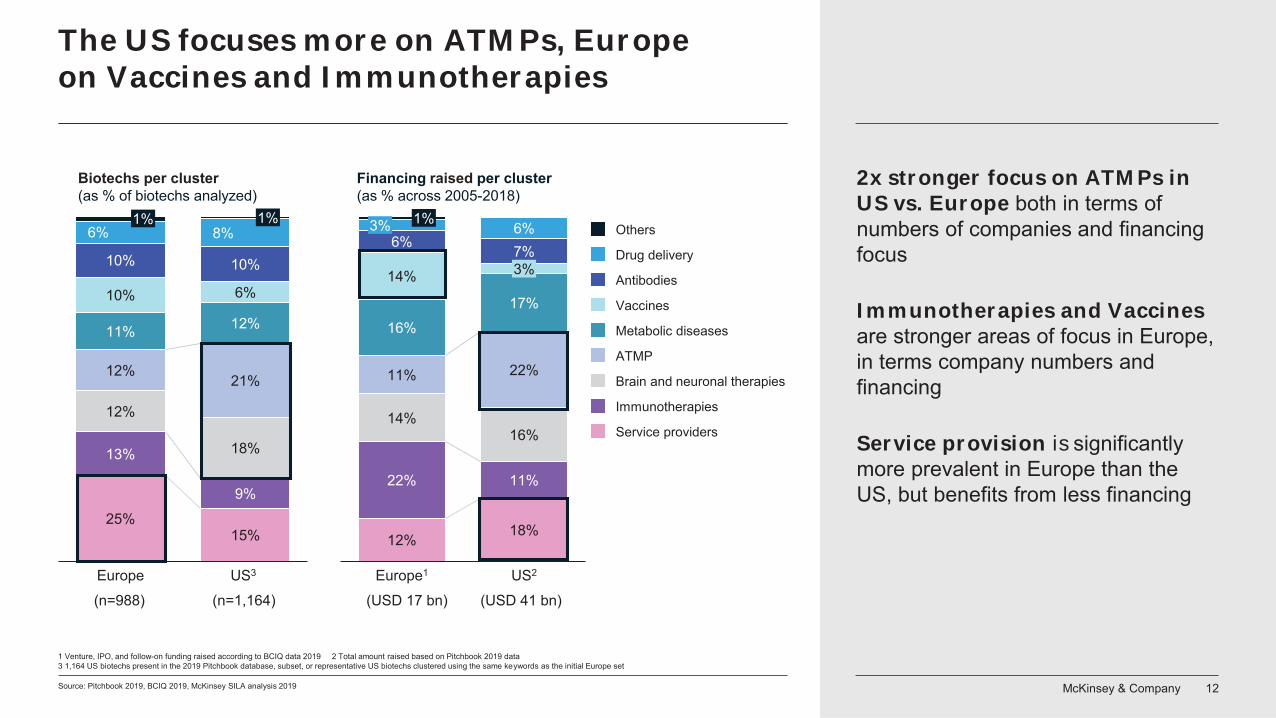

The US focuses more on ATMPs, Europeon Vaccines and Immunotherapies

Source: Pitchbook 2019, BCIQ 2019, McKinsey SILA analysis 2019

25%15%

13%

9%

12%

18%

12%21%

11% 12%

10% 6%

10% 10%

6% 8%1%

Biotechs per cluster(as % of biotechs analyzed)

1%

US3Europe

Vaccines

Others

Drug delivery

Antibodies

Metabolic diseases

ATMP

Brain and neuronal therapies

Immunotherapies

Service providers

12% 18%

22% 11%

14%16%

11% 22%

16%17%

14%

6% 7%6%

3%

Financing raised per cluster(as % across 2005-2018)

US2

3% 1%

Europe1

(n=988) (n=1,164) (USD 17 bn) (USD 41 bn)

1 Venture, IPO, and follow-on funding raised according to BCIQ data 2019 2 Total amount raised based on Pitchbook 2019 data 3 1,164 US biotechs present in the 2019 Pitchbook database, subset, or representative US biotechs clustered using the same keywords as the initial Europe set

2x stronger focus on ATMPs in US vs. Europe both in terms of numbers of companies and financing focus

Immunotherapies and Vaccines are stronger areas of focus in Europe, in terms company numbers and financing

Service provision is significantly more prevalent in Europe than the US, but benefits from less financing

McKinsey & Company 13McKinsey & Company 13

Next–level clustering provides more detailed insights in hotspots

One level deeper look of the 8 European clusters to get more detailed insights about shifts in hot locations and hot topics across geographies, modalities, and therapeutic areas

Modality

Geography

T A

Unbiased automated clustering

BIotech HOtspot MAppingBIHOMA

McKinsey & Company 14

10.3 12.2 9.9 11.8 9.9 8.030.5 5.7 1.5

23.2 13.4 9.8 13.4 15.2 12.5 6.3 3.6 2.7

30.6 15.3 9.2 9.2 8.2 9.2 7.1

13.1 16.7 15.5

11.2

7.1 8.3 14.3 15.5 8.3 1.2

20.7 8.5 15.9 7.3 12.2 12.2 9.8 11.0 2.4

21.1 6.6 21.1 13.2 7.9 7.9 11.8 7.9 2.6

27.5 11.6 5.8 21.7 8.7 2.9 15.9 5.8

10.5 21.1 5.3 15.8 13.2 10.5 15.8 2.6 5.3

29.7 13.5 8.1 13.5 13.5 8.1 10.8 2.7

32.1 10.7 14.3 7.1 7.1 14.3 7.1 7.1

19.0 47.6 4.8 14.3 9.5 4.8

22.7 9.1 9.1 9.1 13.6 13.6 9.1 13.6

17.6 5.9 5.9 23.5 23.5 11.8 11.8

26.7 13.3 20.0 6.7 13.3 13.3 6.7

7.1 14.3 28.6 7.1 7.1 28.6 7.1

50.0 25.0 25.0

2.7 3.2 2.6 3.1 2.6 2.18.1 1.5 0.4

2.6 1.5 1.1 1.5 1.7 1.4 0.7 0.4 0.3

3.0 1.5 0.9 0.9 0.8 0.9 0.7

1.1 1.4 1.3

1.1

0.6 0.7 1.2 1.3 0.7 0.1

1.7 0.7 1.3 0.6 1.0 1.0 0.8 0.9 0.2

1.6 0.5 1.6 1.0 0.6 0.6 0.9 0.6 0.2

1.9 0.8 0.4 1.5 0.6 0.2 1.1 0.4

0.4 0.8 0.2 0.6 0.5 0.4 0.6 0.1 0.2

1.1 0.5 0.3 0.5 0.5 0.3 0.4 0.1

0.9 0.3 0.4 0.2 0.2 0.4 0.2 0.2

0.4 1.0 0.1 0.3 0.2 0.1

0.5 0.2 0.2 0.2 0.3 0.3 0.2 0.3

0.3 0.1 0.1 0.4 0.4 0.2 0.2

0.4 0.2 0.3 0.1 0.2 0.2 0.1

0.1 0.2 0.4 0.1 0.1 0.4 0.1

0.2 0.1 0.1

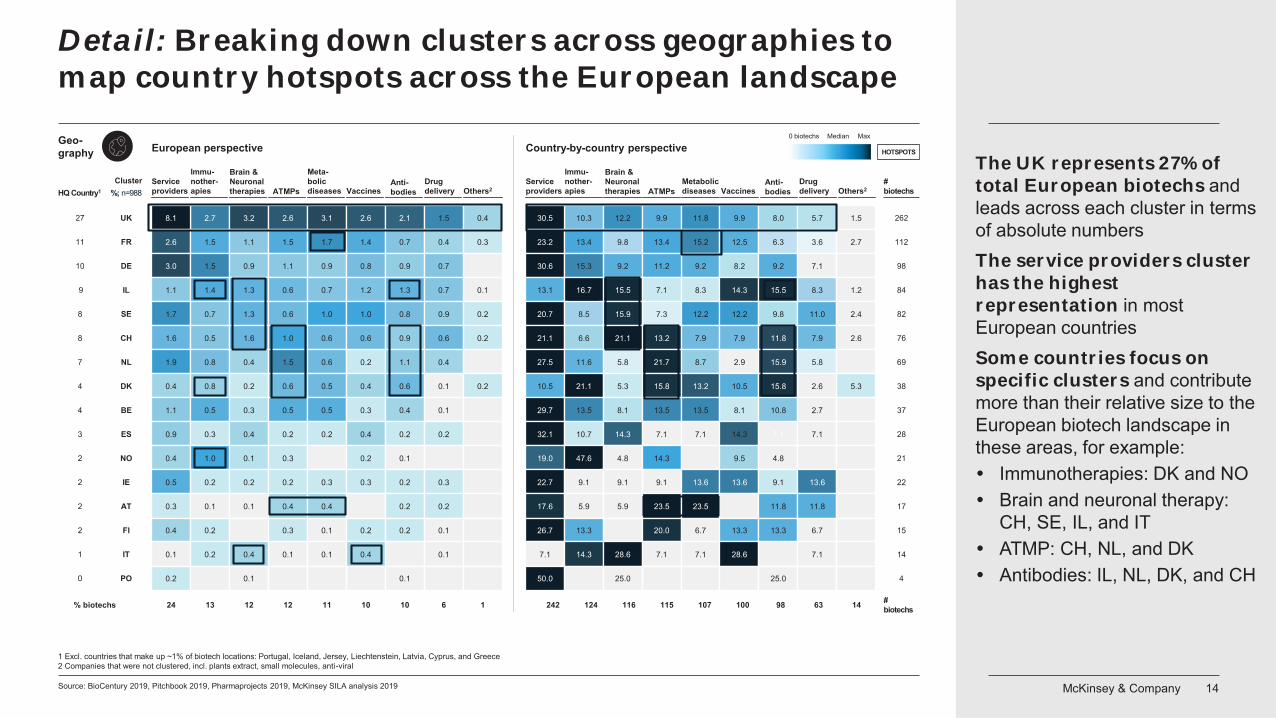

Detail: Breaking down clusters across geographies to map country hotspots across the European landscape

Source: BioCentury 2019, Pitchbook 2019, Pharmaprojects 2019, McKinsey SILA analysis 2019

Cluster

HOTSPOTS

Immu-nother-apies ATMPs

Brain & Neuronal therapies

Meta-bolicdiseases Vaccines

Anti-bodies

Drug delivery Others2

Service providers

Immu-nother-apies

Metabolic diseases Vaccines

Anti-bodies

Drug delivery Others2

Service providers

Country-by-country perspective

HQ Country1

27

11

10

9

8

8

7

4

4

3

2

2

2

2

1

0

%; n=988

UK

FR

DE

IL

SE

CH

NL

DK

BE

ES

NO

IE

AT

FI

IT

PO

24 13 12 12 11 10 10 6 1

European perspective

% biotechs 242 124 116 115 107 100 98 63 14 #biotechs

1 Excl. countries that make up ~1% of biotech locations: Portugal, Iceland, Jersey, Liechtenstein, Latvia, Cyprus, and Greece2 Companies that were not clustered, incl. plants extract, small molecules, anti-viral

#biotechs

262

112

98

84

82

76

69

38

37

28

21

22

17

15

14

4

Max0 biotechs MedianGeo-graphy

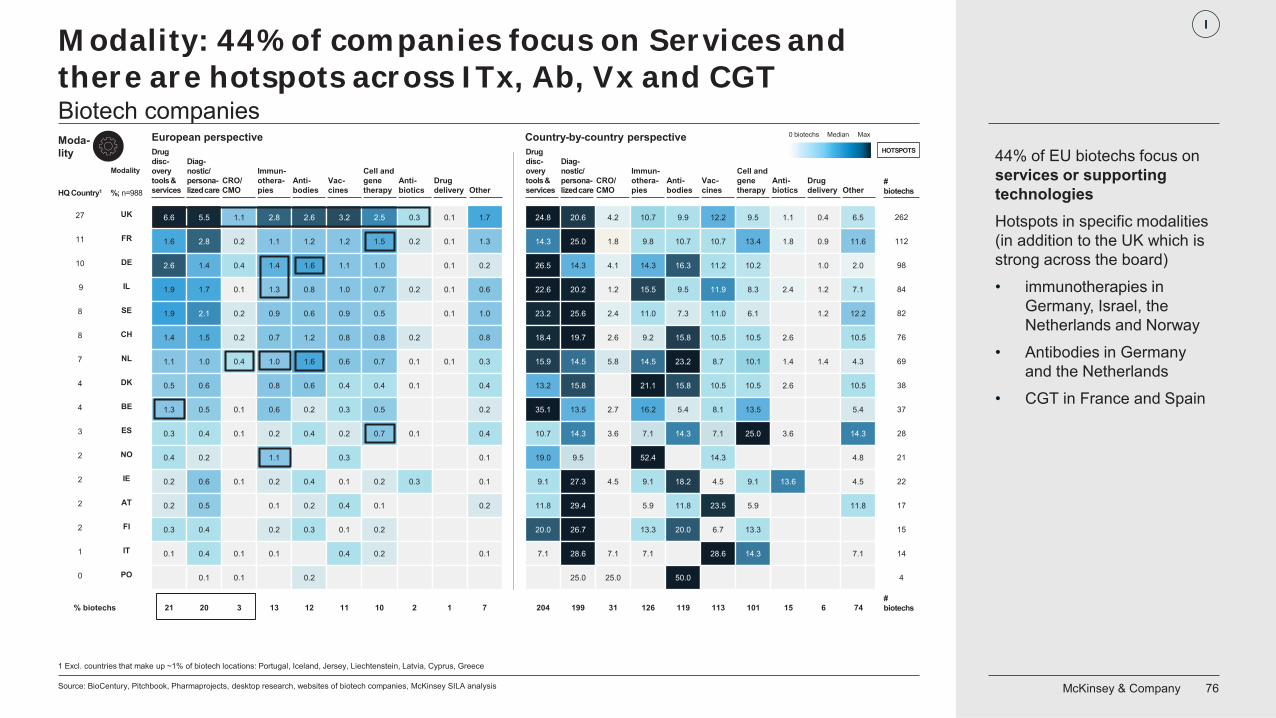

The UK represents 27% of total European biotechs andleads across each cluster in terms of absolute numbersThe service providers cluster has the highest representation in most European countriesSome countries focus on specific clusters and contribute more than their relative size to the European biotech landscape in these areas, for example:

Immunotherapies: DK and NOBrain and neuronal therapy:CH, SE, IL, and ITATMP: CH, NL, and DKAntibodies: IL, NL, DK, and CH

ATMPs

Brain & Neuronal therapies

McKinsey & Company 15

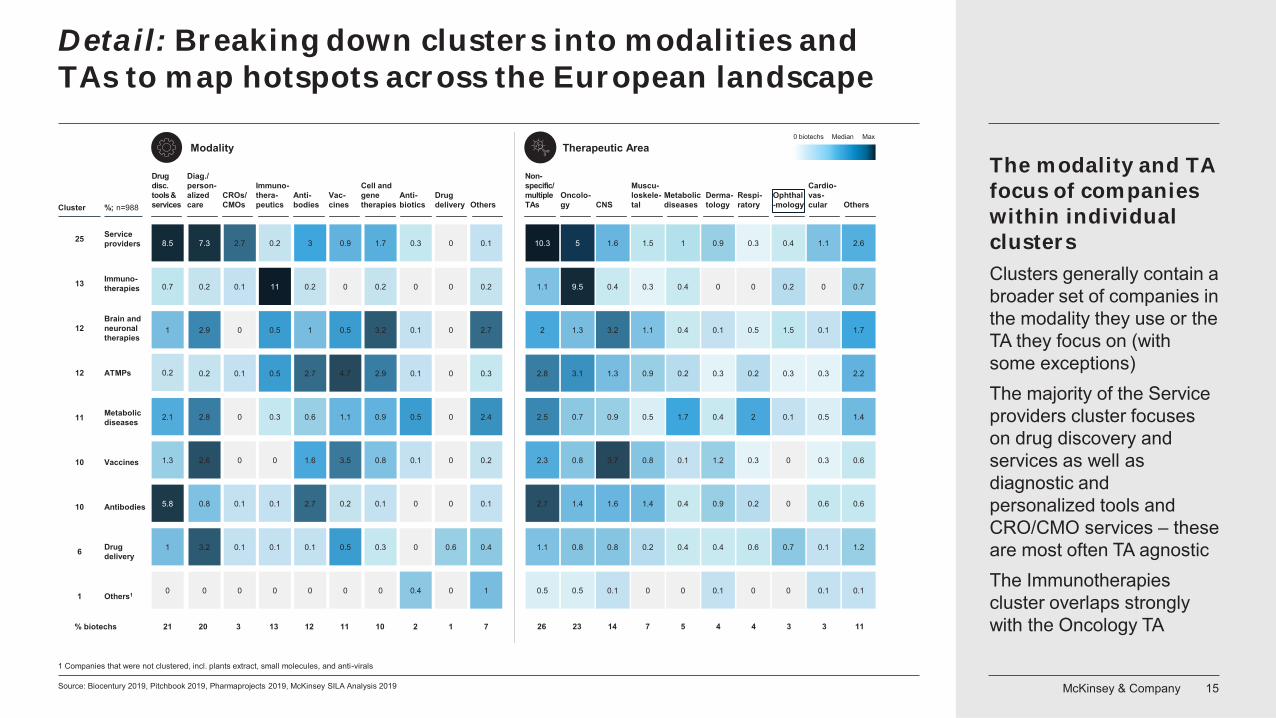

Detail: Breaking down clusters into modalities and TAs to map hotspots across the European landscape

Source: Biocentury 2019, Pitchbook 2019, Pharmaprojects 2019, McKinsey SILA Analysis 2019

Therapeutic AreaModality

1 Companies that were not clustered, incl. plants extract, small molecules, and anti-virals

Max0 biotechs Median

0.7

0.2

1

2.1

1.3

5.8

1

8.5

0

0.2

0.2

2.9

2.8

2.6

0.8

3.2

7.3

0

0.1

0.1

0

0

0

0.1

0.1

2.7

0

11

0.5

0.5

0.3

0

0.1

0.1

0.2

0

0.2

2.7

1

0.6

1.6

2.7

0.1

3

0

0

4.7

0.5

1.1

3.5

0.2

0.5

0.9

0

0.2

2.9

3.2

0.9

0.8

0.1

0.3

1.7

0

0

0.1

0.1

0.5

0.1

0

0

0.3

0.4

0

0

0

0

0

0

0.6

0

0

0.2

0.3

2.7

2.4

0.2

0.1

0.4

0.1

1

Drug disc. tools & services

Diag./ person-alizedcare

CROs/ CMOs

Immuno-thera-peutics

Anti-bodies

Vac-cines

Cell and gene therapies

Anti-biotics

Drug delivery Others

Non-specific/multiple TAs

Oncolo-gy CNS

Muscu-loskele-tal

Metabolic diseases

Derma-tology

Respi-ratory

Ophthal-mology

Cardio-vas-cular Others

1.1

2.8

2

2.5

2.3

2.7

1.1

10.3

0.5

9.5

3.1

1.3

0.7

0.8

1.4

0.8

5

0.5

0.4

1.3

3.2

0.9

3.7

1.6

0.8

1.6

0.1

0.3

0.9

1.1

0.5

0.8

1.4

0.2

1.5

0

0.4

0.2

0.4

1.7

0.1

0.4

0.4

1

0

0

0.3

0.1

0.4

1.2

0.9

0.4

0.9

0.1

0

0.2

0.5

2

0.3

0.2

0.6

0.3

0

0.2

0.3

1.5

0.1

0

0

0.7

0.4

0

0

0.3

0.1

0.5

0.3

0.6

0.1

1.1

0.1

0.7

2.2

1.7

1.4

0.6

0.6

1.2

2.6

0.1

Cluster

13

12

12

11

10

10

6

25

1

%; n=988

Drug delivery

Others1

Vaccines

Antibodies

Immuno-therapies

Brain and neuronal therapies

ATMPs

Metabolic diseases

Service providers

26 23 14 7 5 4 4 3 3 1121 20 3 13 12 11 10 2 1 7% biotechs

The modality and TA focus of companies within individual clustersClusters generally contain a broader set of companies in the modality they use or the TA they focus on (with some exceptions)The majority of the Service providers cluster focuses on drug discovery and services as well as diagnostic and personalized tools and CRO/CMO services – these are most often TA agnosticThe Immunotherapies cluster overlaps strongly with the Oncology TA

McKinsey & Company 16Sources: PubMed April 2019; BioCentury 2019, Pitchbook 2019, Pharmaprojects 2019, McKinsey SILA analysis 2019

23

12 119 10

7 64 3 3 3 2 2 2 1

35

107 7

5

9 8

35

31

31 1 1 0 0

% of biotechs since 2012 (n=311)% of biotechs prior to 2012 (n=677)

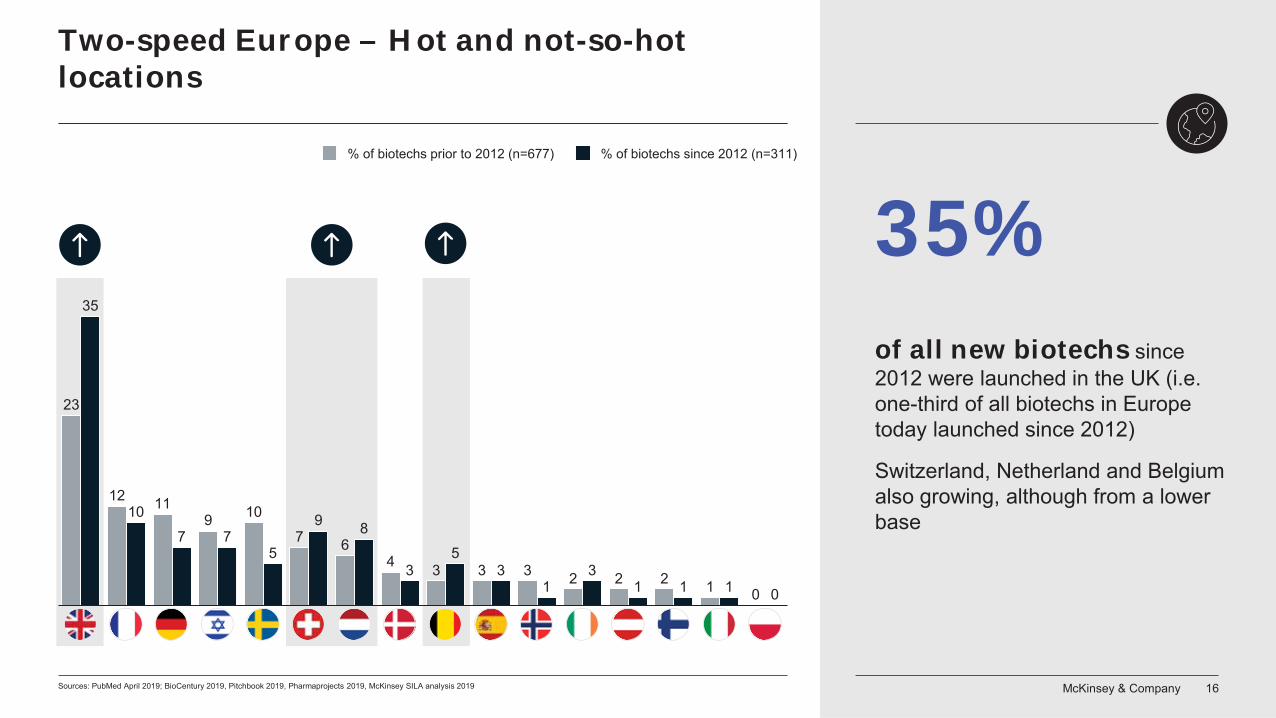

Two-speed Europe – Hot and not-so-hot locations

of all new biotechs since2012 were launched in the UK (i.e. one-third of all biotechs in Europe today launched since 2012)

Switzerland, Netherland and Belgium also growing, although from a lower base

35%

McKinsey & Company 17

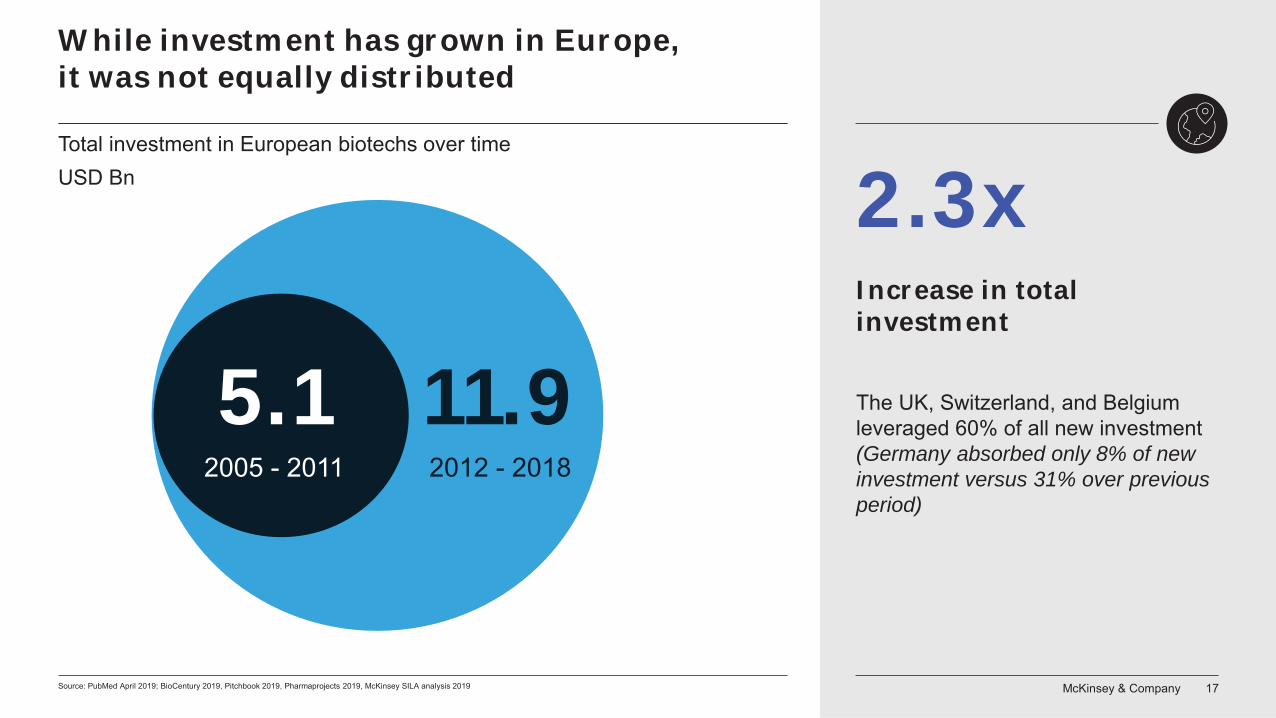

While investment has grown in Europe, it was not equally distributed

Source: PubMed April 2019; BioCentury 2019, Pitchbook 2019, Pharmaprojects 2019, McKinsey SILA analysis 2019

Total investment in European biotechs over timeUSD Bn

5.12005 - 2011

11.92012 - 2018

The UK, Switzerland, and Belgium leveraged 60% of all new investment (Germany absorbed only 8% of new investment versus 31% over previous period)

2.3xIncrease in total investment

McKinsey & Company 18

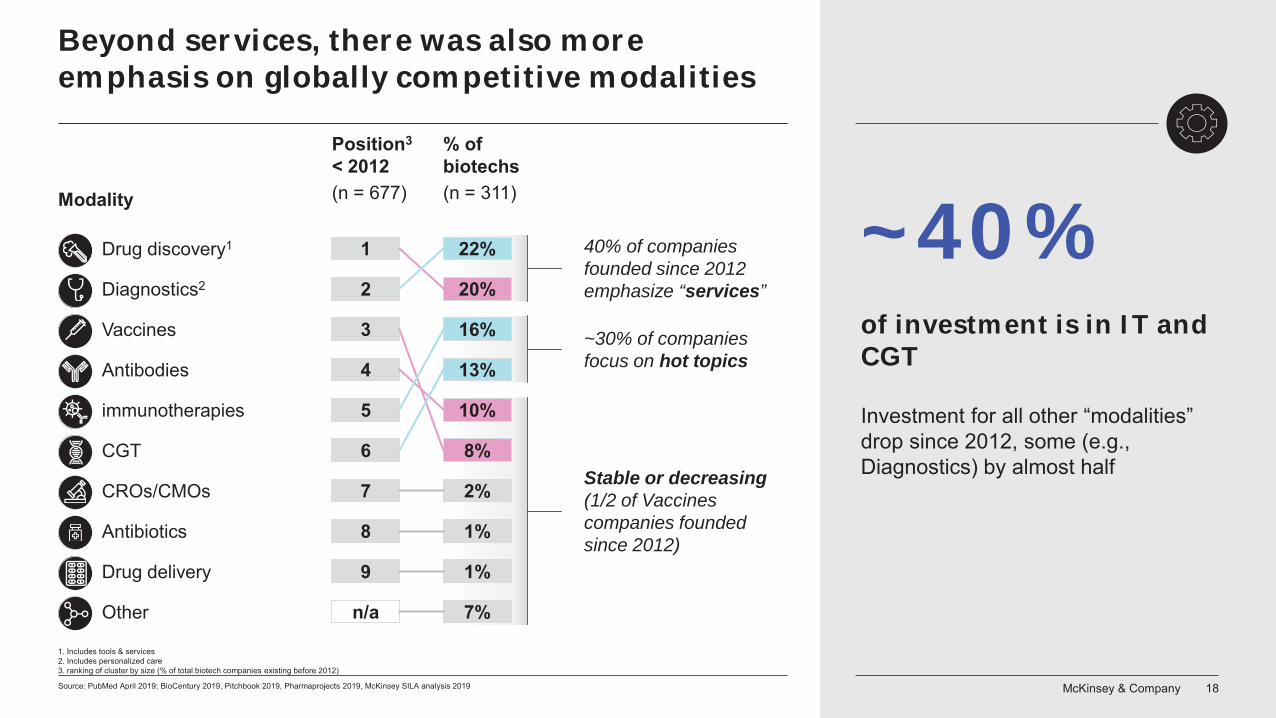

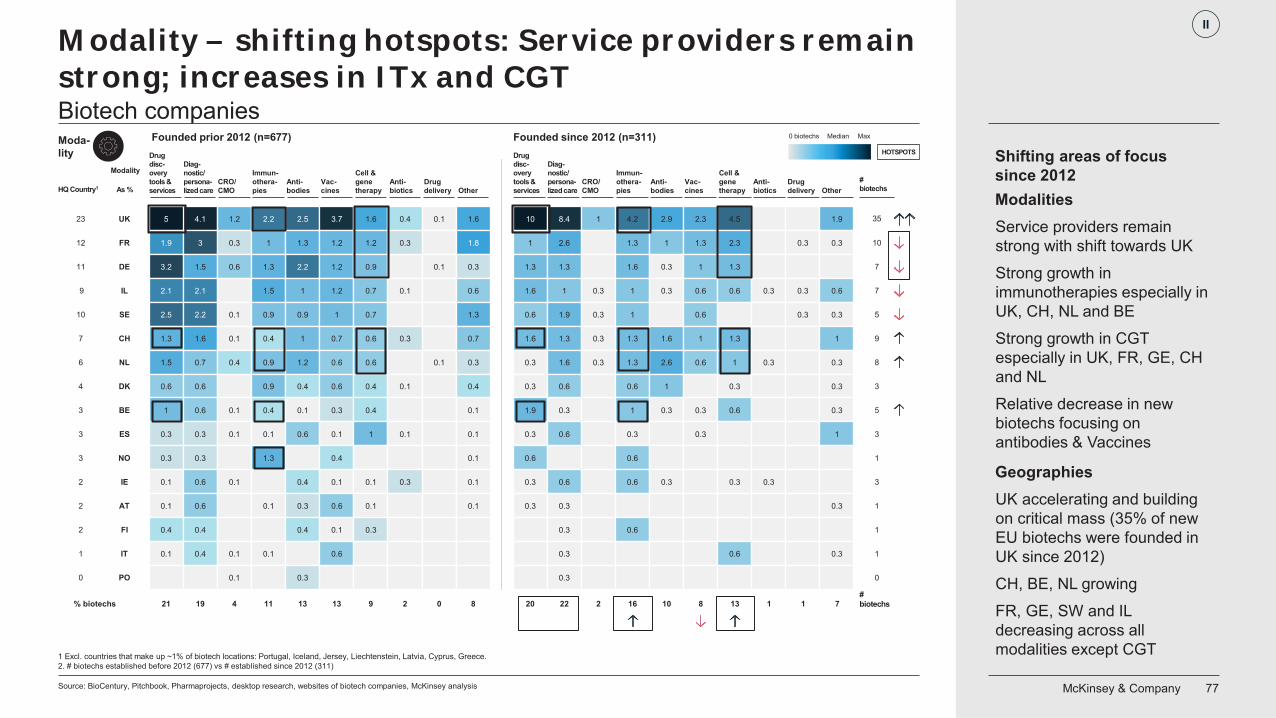

Beyond services, there was also more emphasis on globally competitive modalities

Source: PubMed April 2019; BioCentury 2019, Pitchbook 2019, Pharmaprojects 2019, McKinsey SILA analysis 2019

Modality

Position3

< 2012(n = 677)

% of biotechs(n = 311)

20%

1Drug discovery1 22%

2Diagnostics2

2%7CROs/CMOs

16%

5immunotherapies 10%

4Antibodies

8%

3Vaccines

13%

6CGT

1%8Antibiotics

1%9Drug delivery

7%n/aOther

1. Includes tools & services2. Includes personalized care3. ranking of cluster by size (% of total biotech companies existing before 2012)

40% of companies founded since 2012 emphasize “services”

Stable or decreasing (1/2 of Vaccines companies founded since 2012)

~40% of investment is in IT andCGT

Investment for all other “modalities” drop since 2012, some (e.g., Diagnostics) by almost half

~30% of companies focus on hot topics

McKinsey & Company 19

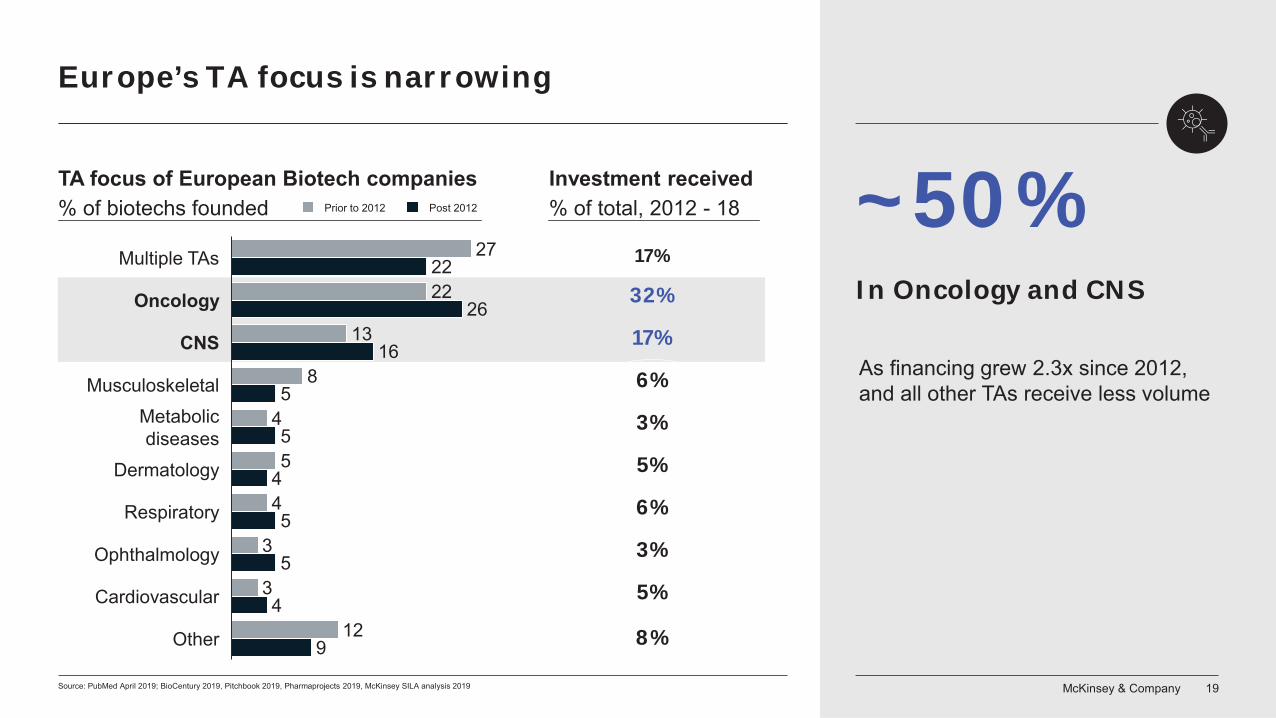

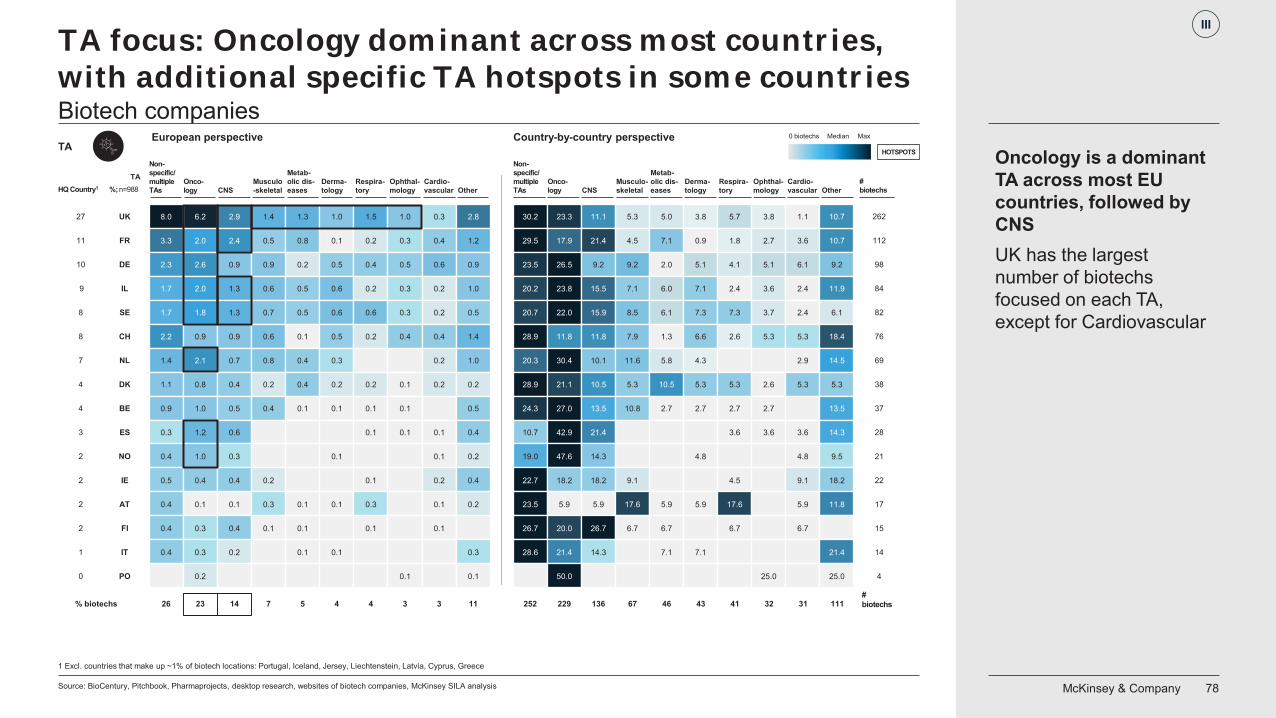

Europe’s TA focus is narrowing

Source: PubMed April 2019; BioCentury 2019, Pitchbook 2019, Pharmaprojects 2019, McKinsey SILA analysis 2019

27

22

13

8

4

5

4

3

3

12

22

26

16

5

5

4

5

5

4

9

Dermatology

Metabolicdiseases

Musculoskeletal

Multiple TAs

Cardiovascular

Oncology

CNS

Respiratory

Ophthalmology

Other

Post 2012Prior to 2012

TA focus of European Biotech companies% of biotechs founded

Investment received% of total, 2012 - 18

17%

32%

17%

6%

3%

5%

6%

3%

5%

8%

As financing grew 2.3x since 2012, and all other TAs receive less volume

~50% In Oncology and CNS

McKinsey & Company 20Source: PubMed April 2019; BioCentury 2019, Pitchbook 2019, Pharmaprojects 2019, McKinsey SILA analysis 2019

23

12

11

9

10

7

6

4

3

3

3

2

2

2

1

35

10

7

7

5

9

8

3

5

3

1

3

1

1

1

Denmark

Sweden

UK

Netherlands

France

0

Switzerland

Germany

Israel

Belgium

Austria

Spain

Norway

Ireland

Finland

Italy

Poland 0

% of biotechs prior 2012 (n=677) % of biotechs since 2012 (n=311)

21

19

4

11

13

14

9

2

8

20

22

2

16

10

8

13

1

1

7

Diagnostic/Personalized care

Drug discoveryTools and services

Vaccines

CRO/CMO

Immunotherapies

Antibodies

Cell and gene therapies

Antibiotics

Drug delivery

Other

0

27

22

13

8

4

5

4

3

3

12

22

26

16

5

5

4

5

5

4

9

Musculoskeletal

Non-specific/Multiple TAs

Respiratory

Cardiovascular

Oncology

CNS

Ophthalmology

Metabolic diseases

Dermatology

Other

Hot locations/hot topics (increasing since 2012)

By modality By TA

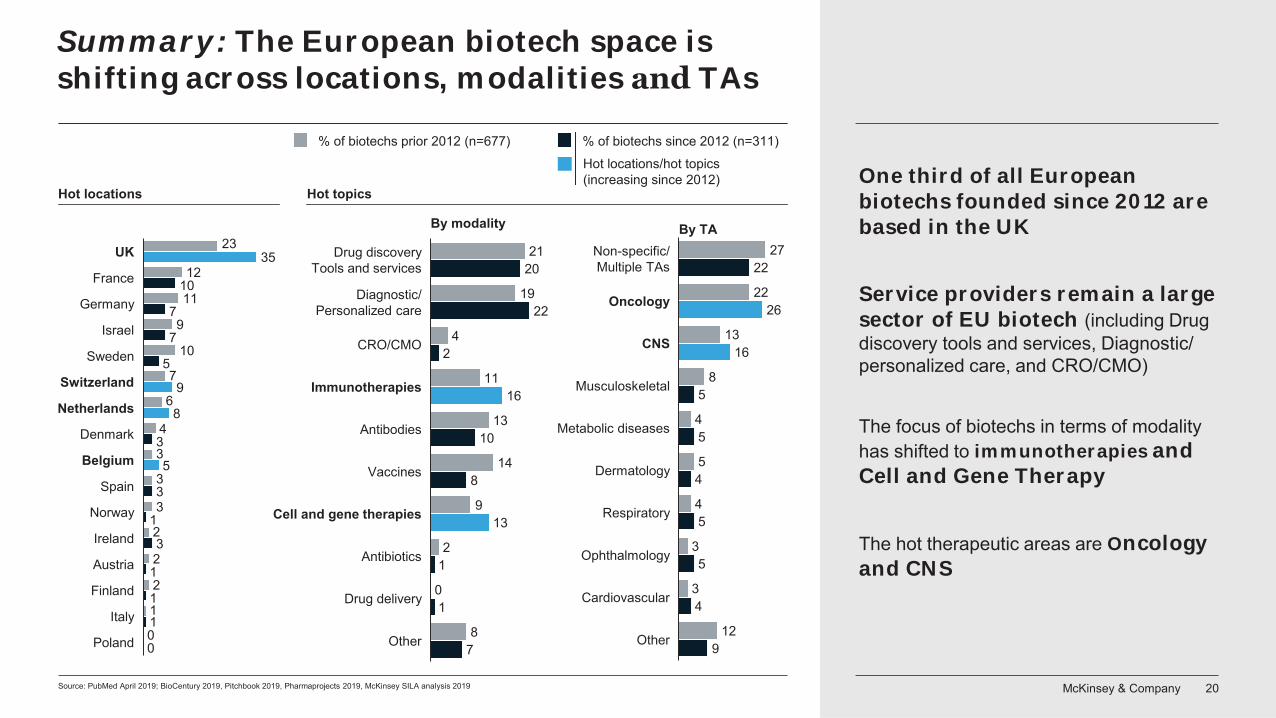

Hot topicsHot locationsOne third of all European biotechs founded since 2012 are based in the UK

Service providers remain a large sector of EU biotech (including Drug discovery tools and services, Diagnostic/ personalized care, and CRO/CMO)

The focus of biotechs in terms of modality has shifted to immunotherapies and Cell and Gene Therapy

The hot therapeutic areas are Oncologyand CNS

Summary: The European biotech space is shifting across locations, modalities TAs

McKinsey & Company 21

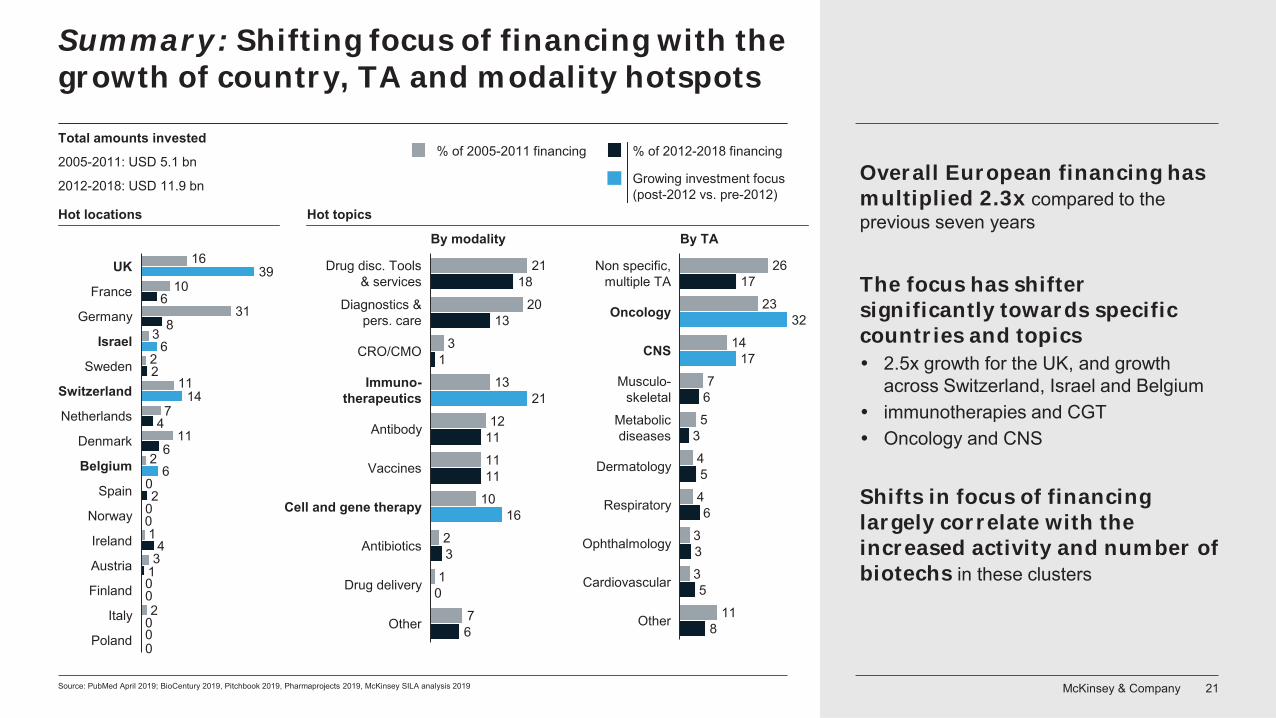

Summary: Shifting focus of financing with the growth of country, TA and modality hotspots

Source: PubMed April 2019; BioCentury 2019, Pitchbook 2019, Pharmaprojects 2019, McKinsey SILA analysis 2019

16

10

31

3

2

11

7

11

2

0

1

3

2

39

6

86

2

14

4

66

2

0

4

1

Norway

Denmark

UK

France

Germany

Israel

Ireland

Switzerland

Sweden

Netherlands

Belgium

0

Spain

Austria

Finland

Italy

Poland

0

0

000

% of 2005-2011 financing % of 2012-2018 financing

Hot locations

26

23

14

7

5

4

4

3

3

11

17

32

17

6

3

5

6

3

5

8

Musculo-skeletal

Non specific,multiple TA

Oncology

CNS

Metabolicdiseases

Dermatology

Ophthalmology

Respiratory

Cardiovascular

Other

21

20

3

13

12

11

10

2

1

7

18

13

1

21

11

11

16

3

0

6

Immuno-therapeutics

Drug disc. Tools& services

Antibiotics

Diagnostics &pers. care

Antibody

CRO/CMO

Vaccines

Cell and gene therapy

Drug delivery

Other

Total amounts invested

2005-2011: USD 5.1 bn

2012-2018: USD 11.9 bn Growing investment focus (post-2012 vs. pre-2012)

Hot topics

By modality By TA

Overall European financing has multiplied 2.3x compared to the previous seven years

The focus has shifter significantly towards specific countries and topics

2.5x growth for the UK, and growthacross Switzerland, Israel and Belgiumimmunotherapies and CGTOncology and CNS

Shifts in focus of financing largely correlate with the increased activity and number of biotechs in these clusters

McKinsey & Company 22

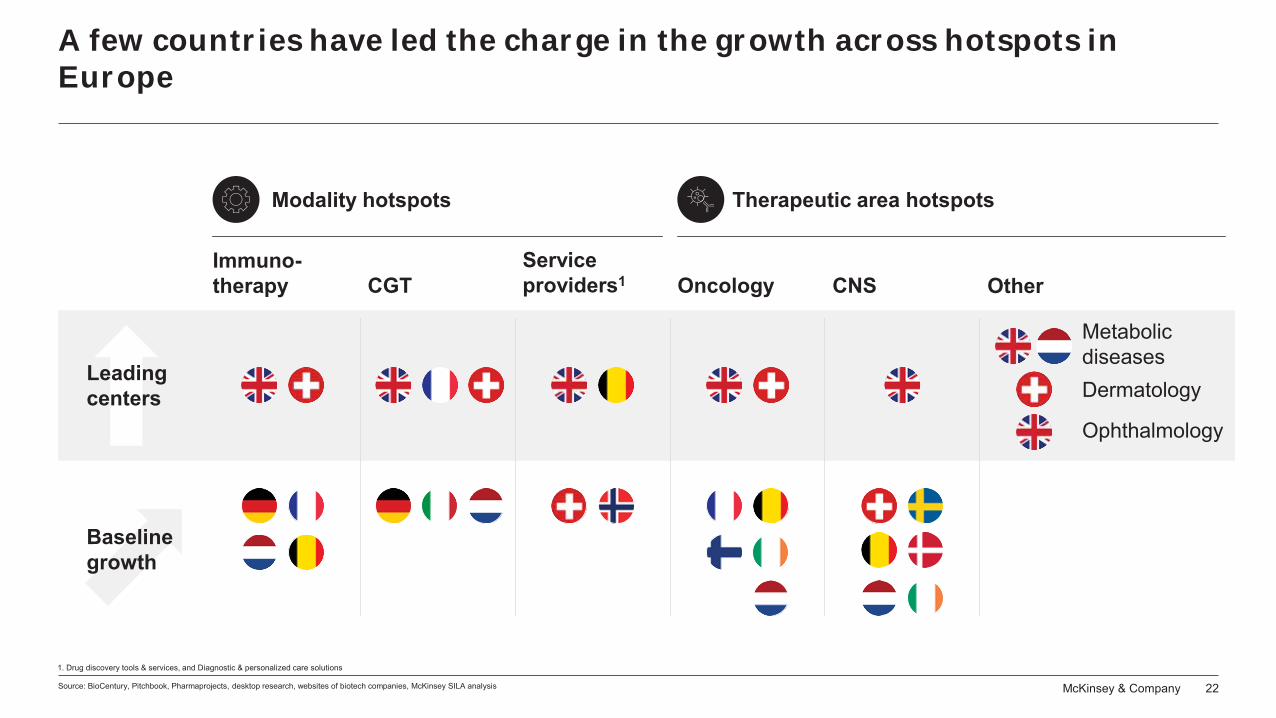

A few countries have led the charge in the growth across hotspots in Europe

1. Drug discovery tools & services, and Diagnostic & personalized care solutions

Source: BioCentury, Pitchbook, Pharmaprojects, desktop research, websites of biotech companies, McKinsey SILA analysis

Baseline growth

Leading centers

Modality hotspots Therapeutic area hotspots

Metabolic diseasesDermatology

Ophthalmology

CGTImmuno-therapy

Service providers1 CNSOncology Other

McKinsey & Company 23

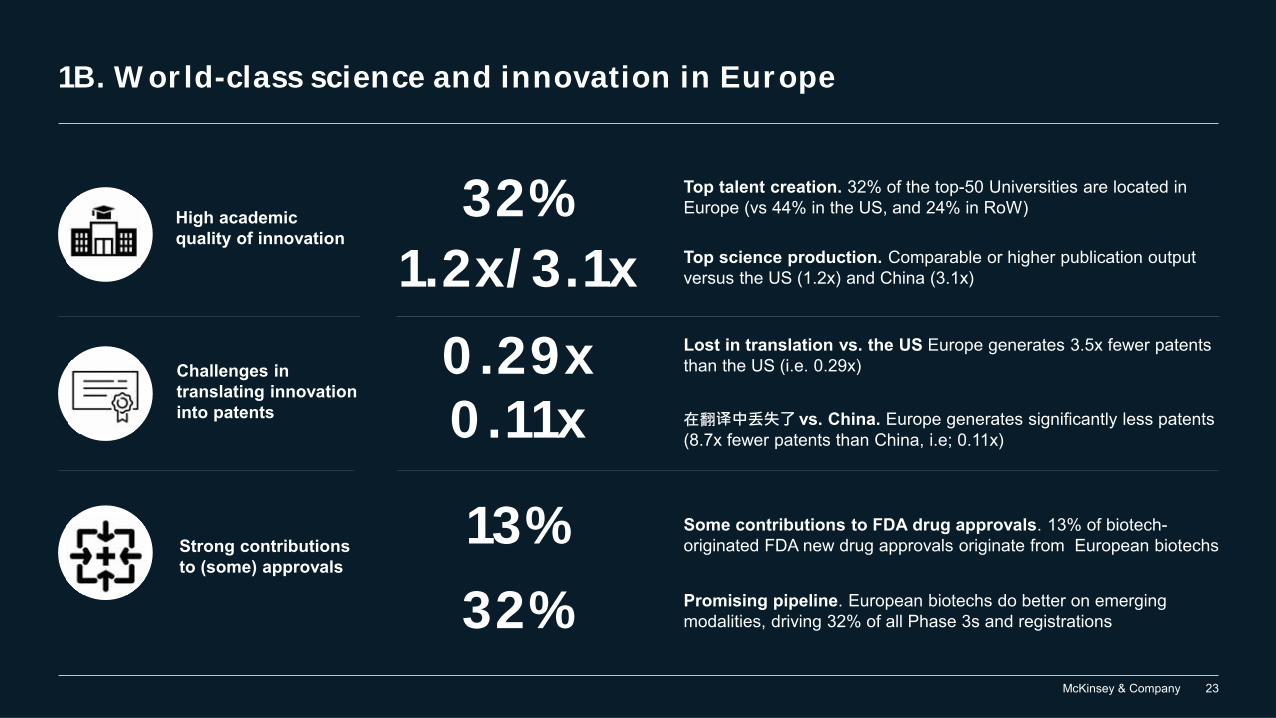

1B. World-class science and innovation in Europe

Strong contributions to (some) approvals

Challenges in translating innovation into patents

High academic quality of innovation

32%1.2x/3.1x

Top talent creation. 32% of the top-50 Universities are located in Europe (vs 44% in the US, and 24% in RoW)

Top science production. Comparable or higher publication output versus the US (1.2x) and China (3.1x)

0.29x 0.11x

Lost in translation vs. the US Europe generates 3.5x fewer patents than the US (i.e. 0.29x)

Some contributions to FDA drug approvals. 13% of biotech-originated FDA new drug approvals originate from European biotechs

Promising pipeline. European biotechs do better on emerging modalities, driving 32% of all Phase 3s and registrations

13%32%

vs. China. Europe generates significantly less patents (8.7x fewer patents than China, i.e; 0.11x)

McKinsey & Company 24Source: The Times World University rankings, CWTS Leiden Ranking 2018 – ranking of University publications (2013-2016); McKinsey Analysis

Max0 biotechs Median

10

19

2935

3940

42

37

43

47

146 69161718

202128

3032

4549

5058

11

13

22

31

27

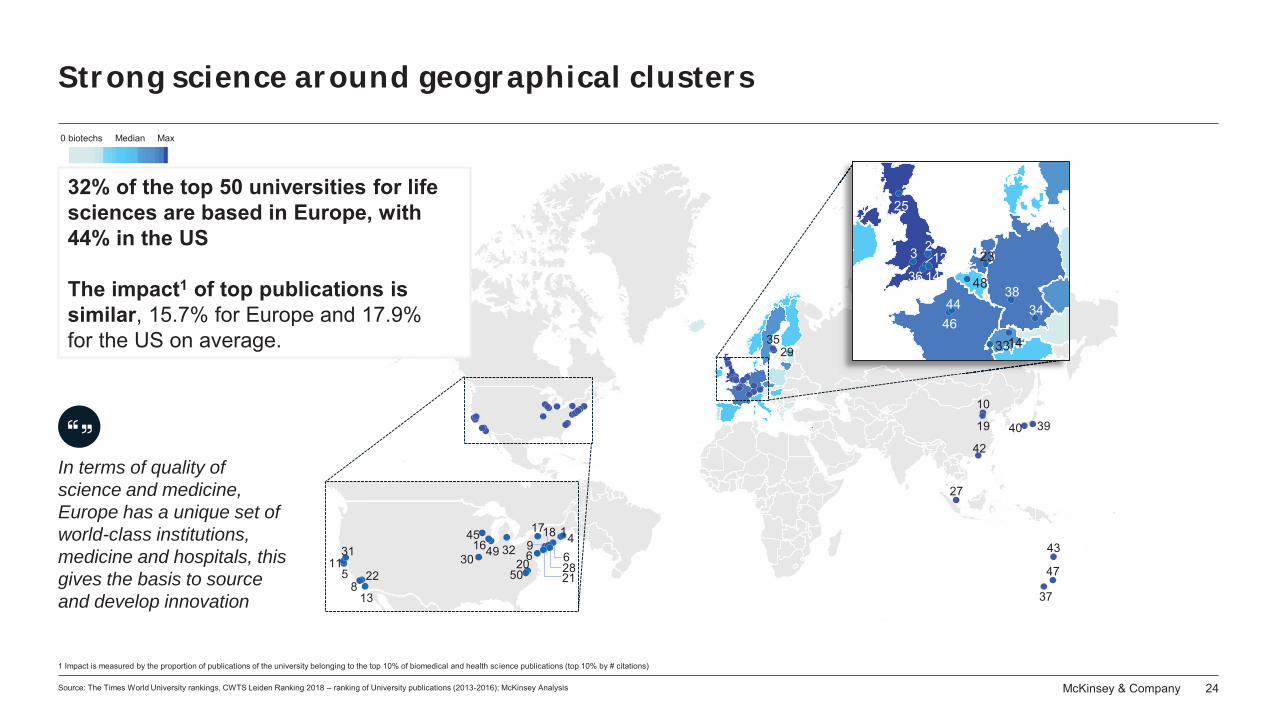

32% of the top 50 universities for life sciences are based in Europe, with 44% in the US

The impact1 of top publications issimilar, 15.7% for Europe and 17.9% for the US on average.

25

23 1236 14

34

1433

3844

46

48

23

1 Impact is measured by the proportion of publications of the university belonging to the top 10% of biomedical and health science publications (top 10% by # citations)

In terms of quality of science and medicine, Europe has a unique set of world-class institutions, medicine and hospitals, this gives the basis to source and develop innovation

Strong science around geographical clusters

McKinsey & Company 25Source: PubMed April 2019; BioCentury BCIQ 2019, Pitchbook 2019, Pharmaprojects 2019, McKinsey SILA analysis 2019

27

10

988

74

4

32

22

21

1116

18

455

234

9

2

23

214

3

Denmark

Sweden

Netherlands

UKFrance

Norway

Switzerland

IsraelGermany

BelgiumSpain

IrelandAustriaFinland

ItalyPoland

11

0

13

6

16

15

38

5

6

Immuno-therapies

Serviceproviders1

Antibiotics

Vaccines

CGT

Antibodies

Drug delivery

By modality

25

27

8

14

4

6

4

12

Dermatology

Oncology

Cardiovascular

Musculo-skeletal

CNS

Metabolicdiseases

Respiratory

By TA

Ophthalmology

% of biotechs % of publications

Hot topic

1. Services providers include Drug discovery tools and services, diagnostic and personalised care, CRO/CMO related topics

By location

Analysis of European publications since 2005, percent of biotech companies / publications

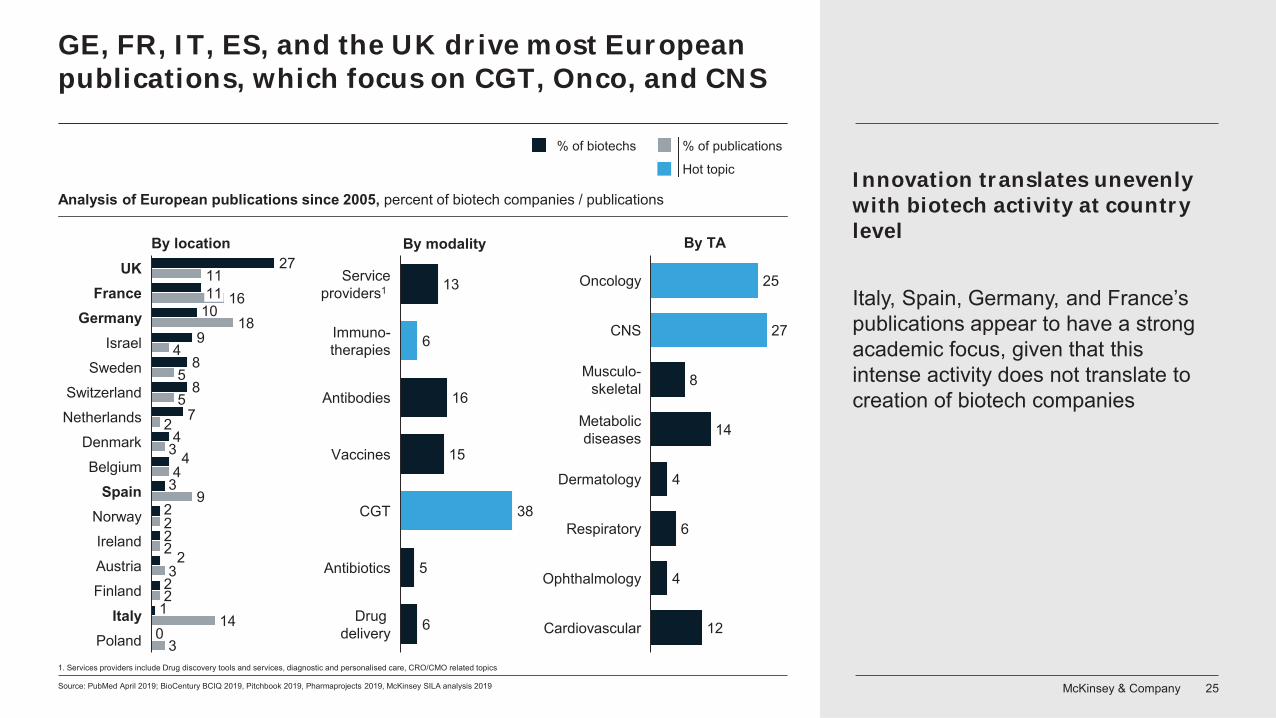

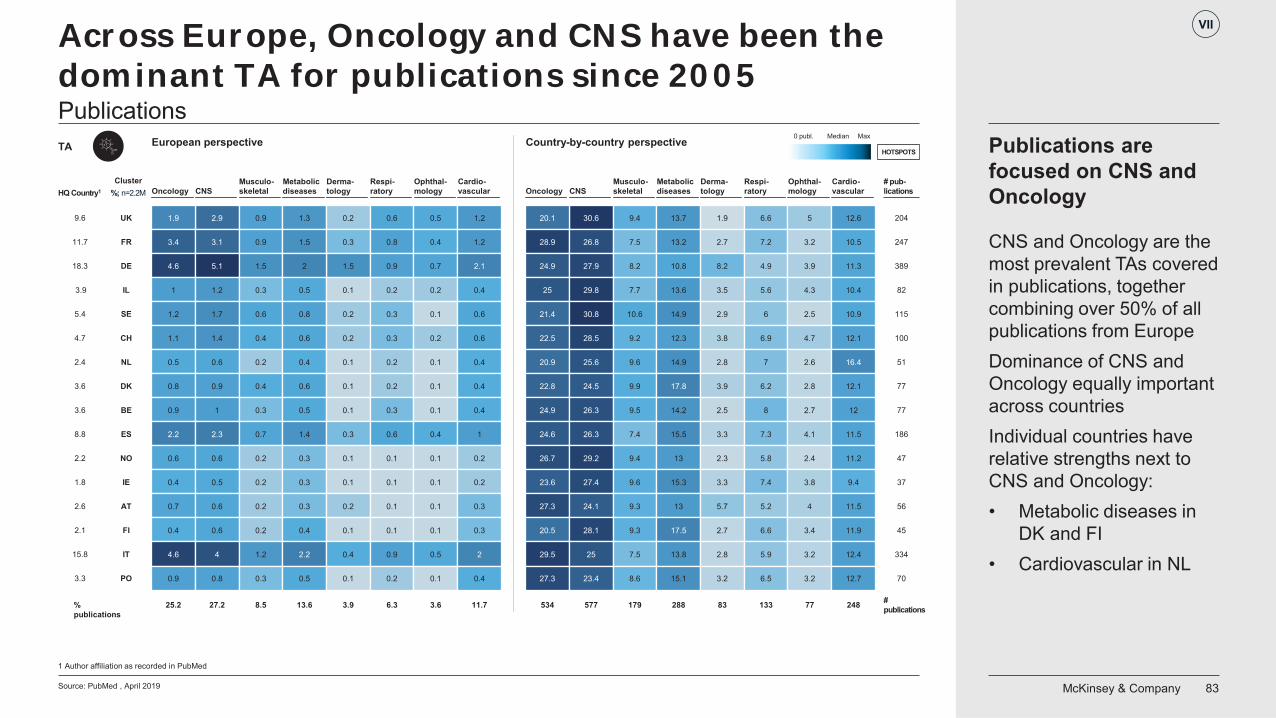

GE, FR, IT, ES, and the UK drive most European publications, which focus on CGT, Onco, and CNS

Innovation translates unevenly with biotech activity at country level

Italy, Spain, Germany, and France’s publications appear to have a strong academic focus, given that this intense activity does not translate to creation of biotech companies

McKinsey & Company 26Source: PubMed April 2019; Expert interviews 2019; McKinsey Analysis

% publications in region 2005-2018, # publications

3%

Europe

35%

21%

8%

15%

5%

8%4%

4%

US

38%

3%3%

23%7%

1,751,992

3%

20%

10%8%

11%

3%

China

33%

16%

568,737

8%

9%1,477,507

~3.1x

~1.2x

ATMP

Drug delivery

Service provider

Antibody

Vaccines

Metabolic diseases

Brain and neuronal therapies

Immunotherapies

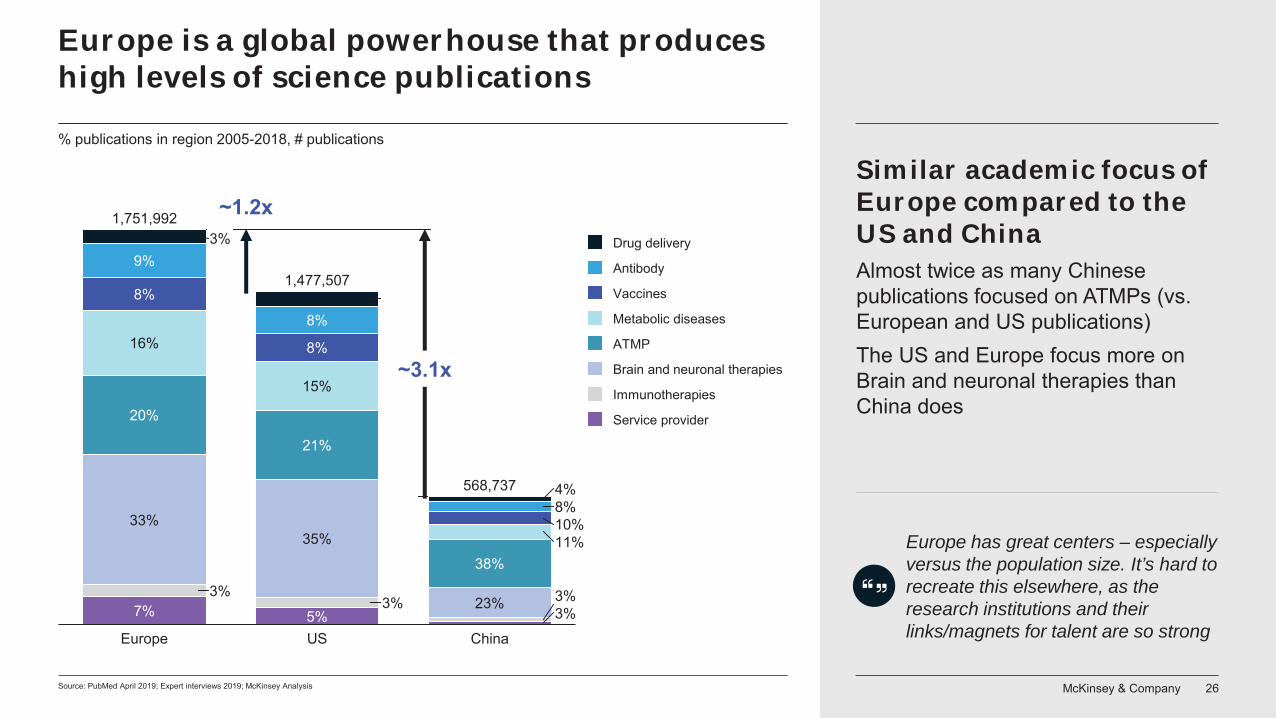

Europe has great centers – especially versus the population size. It’s hard to recreate this elsewhere, as the research institutions and their links/magnets for talent are so strong

Similar academic focus of Europe compared to the US and ChinaAlmost twice as many Chinese publications focused on ATMPs (vs. European and US publications)The US and Europe focus more on Brain and neuronal therapies than China does

Europe is a global powerhouse that produces high levels of science publications

McKinsey & Company 27Source: Innography database, March 2019 (incl. European Patent Office, Chinese patent office and United States Patent and Trademark Office). To identify patents, keywords were used. Please see keywords in backup; McKinsey Analysis

Patent registrations by region# patents registered, only 1st registration region counted (‘000)

0

12

6

4

8

10

20

14

16

18

2

22

200506 08 09 10 11 12 13 14 15 16 17201807

~ 0.29x

~ 0.11x

United States China Europe

United States

Europe1

CAGR2005-11

25% 25%

7% 18%

52% 46%China

CAGR2012-18

1 Excluding Russia

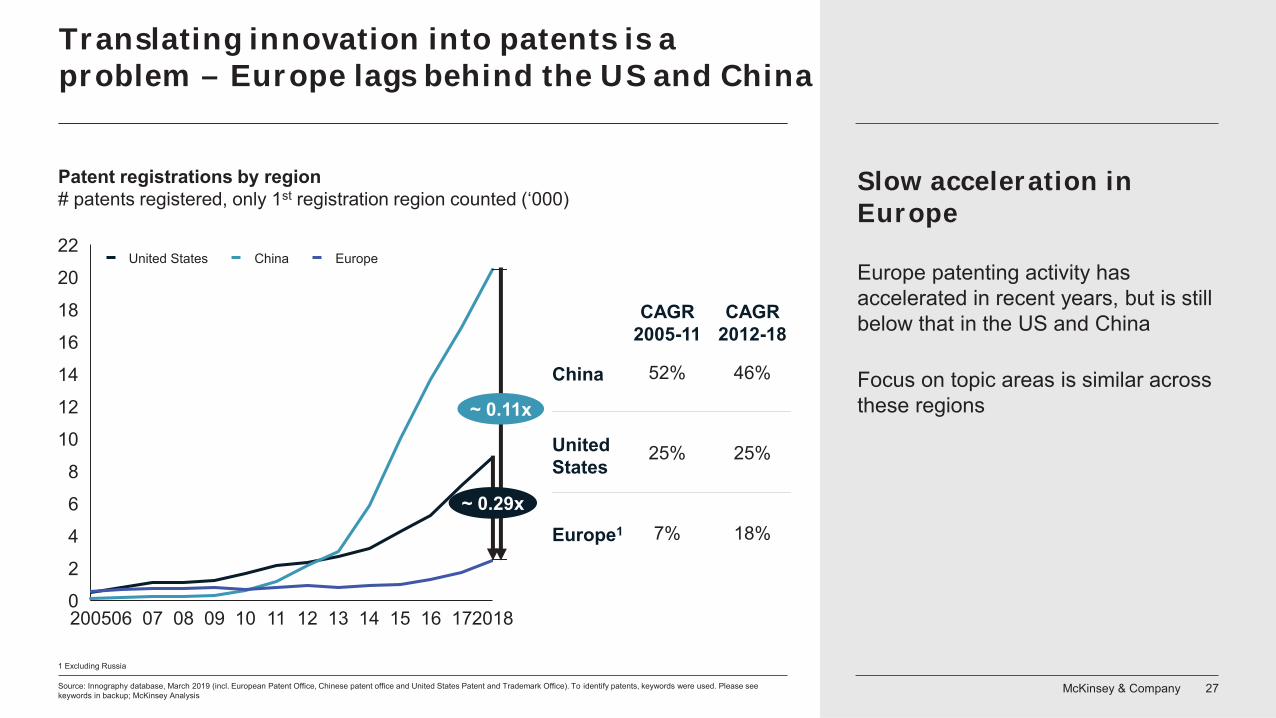

Translating innovation into patents is a problem – Europe lags behind the US and China

Slow acceleration in Europe

Europe patenting activity has accelerated in recent years, but is still below that in the US and China

Focus on topic areas is similar across these regions

McKinsey & Company 28

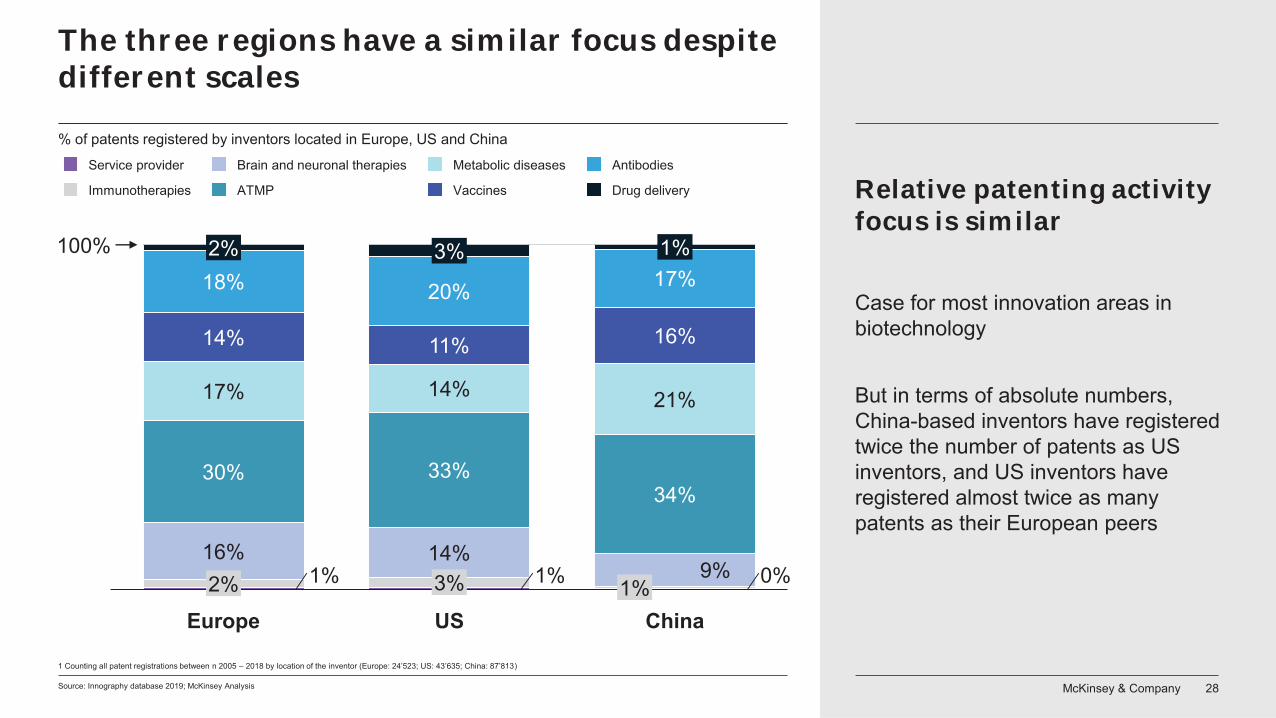

The three regions have a similar focus despite different scales

Source: Innography database 2019; McKinsey Analysis

1% 1% 0%16% 14%

9%

30% 33%34%

17% 14% 21%

14% 11% 16%

18% 20% 17%3%2%

2%

USEurope3% 1%

1%

China

100%

Brain and neuronal therapiesService provider

Immunotherapies

Metabolic diseases

ATMP Vaccines

Antibodies

Drug delivery

1 Counting all patent registrations between n 2005 – 2018 by location of the inventor (Europe: 24’523; US: 43’635; China: 87’813)

% of patents registered by inventors located in Europe, US and China

Relative patenting activity focus is similar

Case for most innovation areas in biotechnology

But in terms of absolute numbers, China-based inventors have registered twice the number of patents as US inventors, and US inventors have registered almost twice as many patents as their European peers

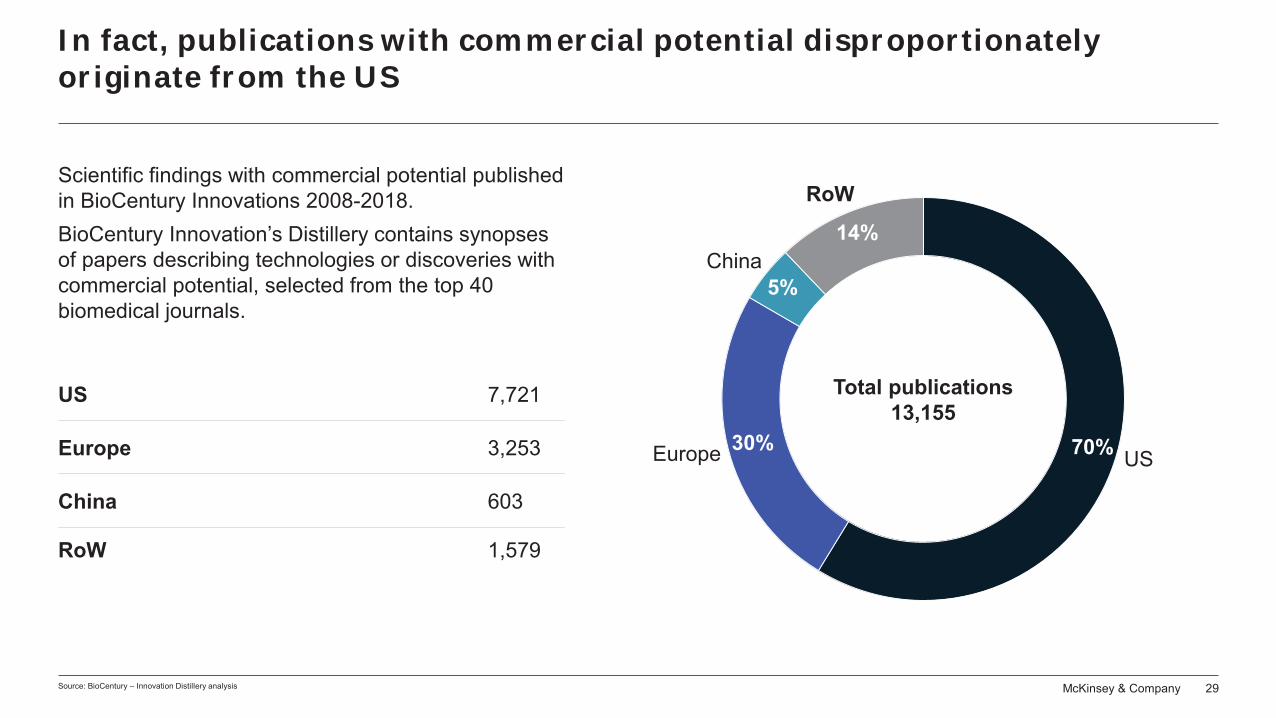

McKinsey & Company 29Source: BioCentury – Innovation Distillery analysis

Scientific findings with commercial potential published in BioCentury Innovations 2008-2018. BioCentury Innovation’s Distillery contains synopses of papers describing technologies or discoveries with commercial potential, selected from the top 40 biomedical journals.

China 603

RoW 1,579

Europe 3,253

US 7,721

70%30%

5%

14%

RoW

Europe US

China

Total publications13,155

In fact, publications with commercial potential disproportionately originate from the US

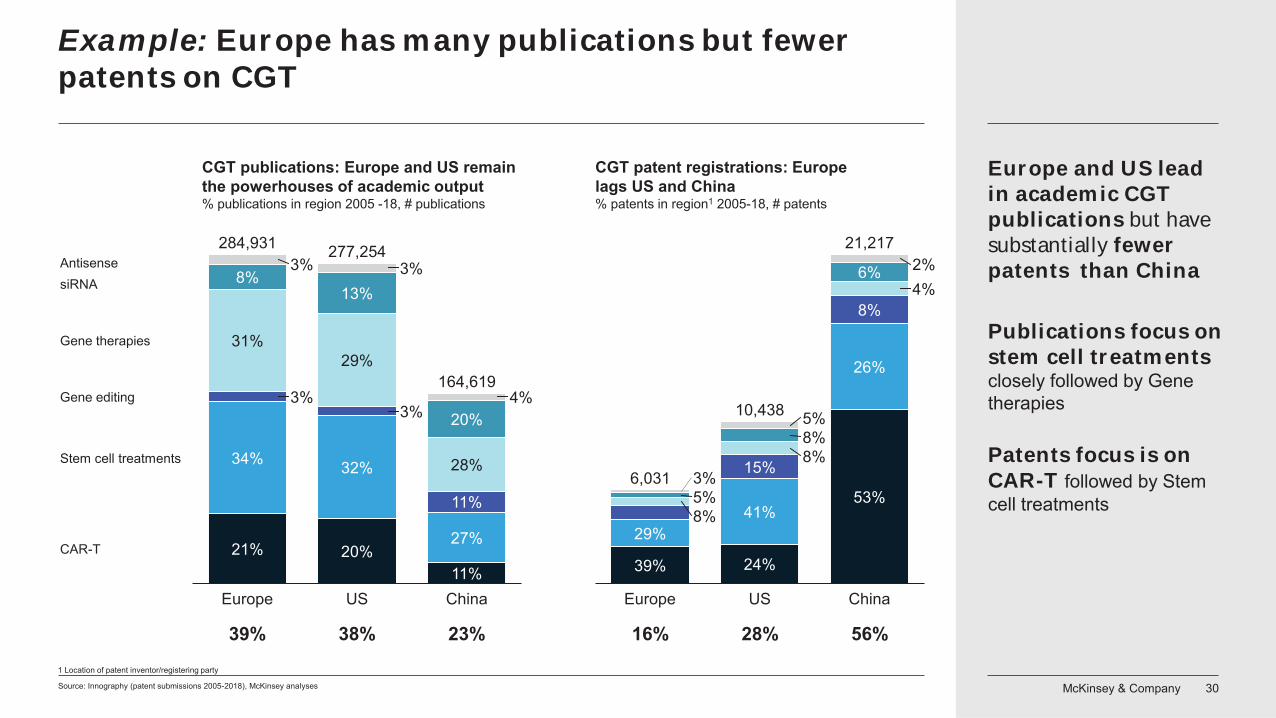

McKinsey & Company 30Source: Innography (patent submissions 2005-2018), McKinsey analyses

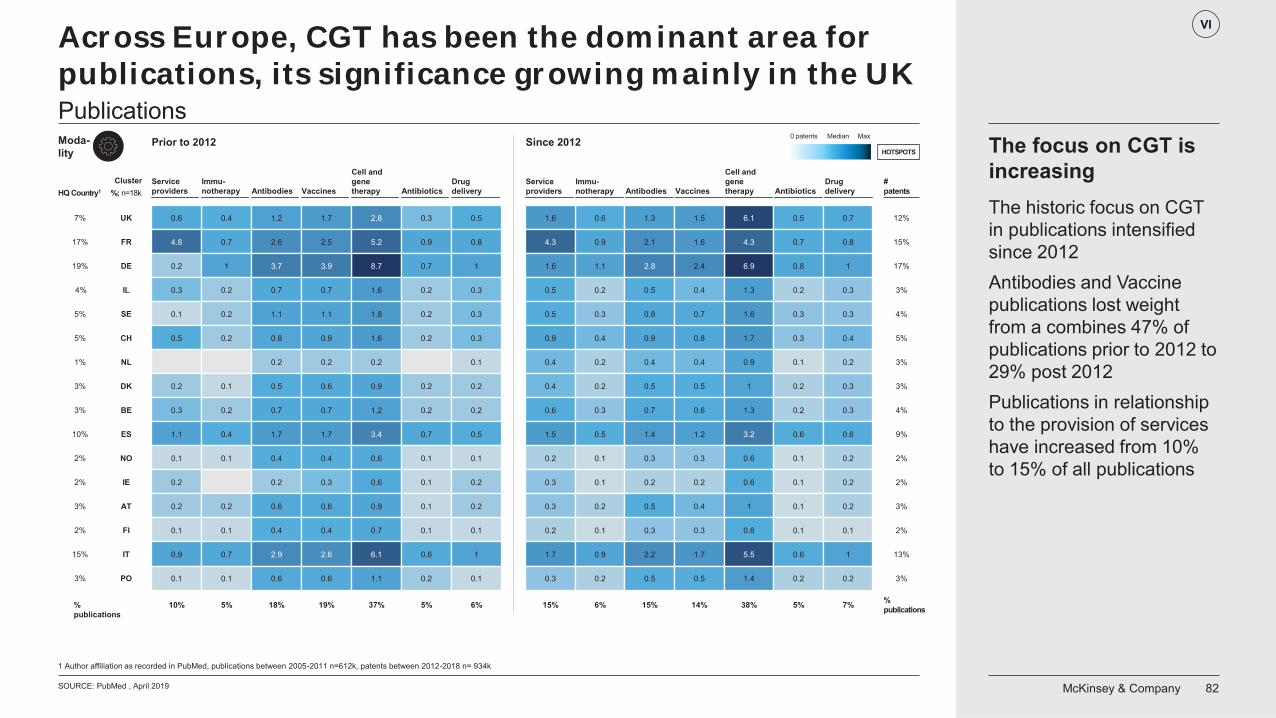

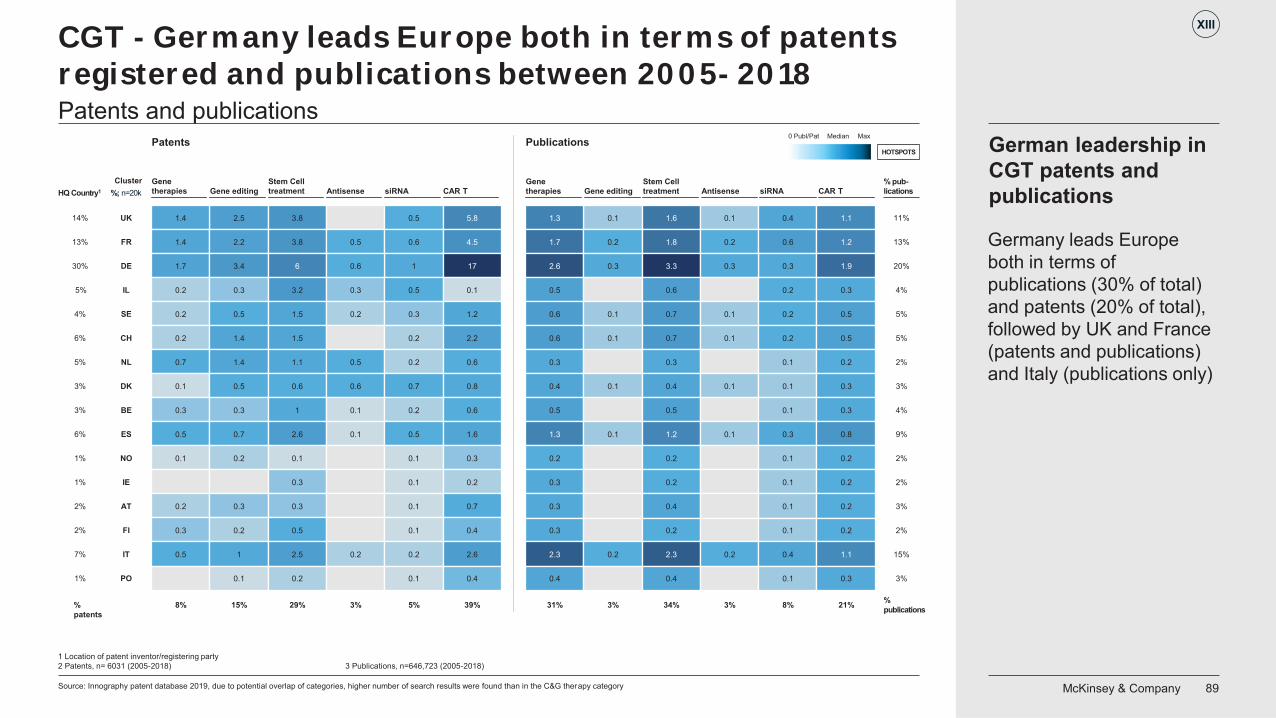

CGT publications: Europe and US remain the powerhouses of academic output% publications in region 2005 -18, # publications

CGT patent registrations: Europe lags US and China% patents in region1 2005-18, # patents

China

8%

39%

5%

29%

26%

3%

Europe

10,438

8%5%

8%15%

41%

24%

US

6%4%

8%

53%

2%

6,031

21,217

21%

4%164,619

8%

34%

31%

3%

3%

Europe

13%

29%

32%

20%CAR-T

siRNA3%

US

20%

28%

11%

27%

11%

3%

China

Gene therapies

Gene editing

284,931

Stem cell treatments

Antisense277,254

1 Location of patent inventor/registering party

39% 38% 23% 16% 28% 56%

Example: Europe has many publications but fewer patents on CGT

Europe and US lead in academic CGT publications but have substantially fewer patents than China

Patents focus is on CAR-T followed by Stem cell treatments

Publications focus on stem cell treatments closely followed by Gene therapies

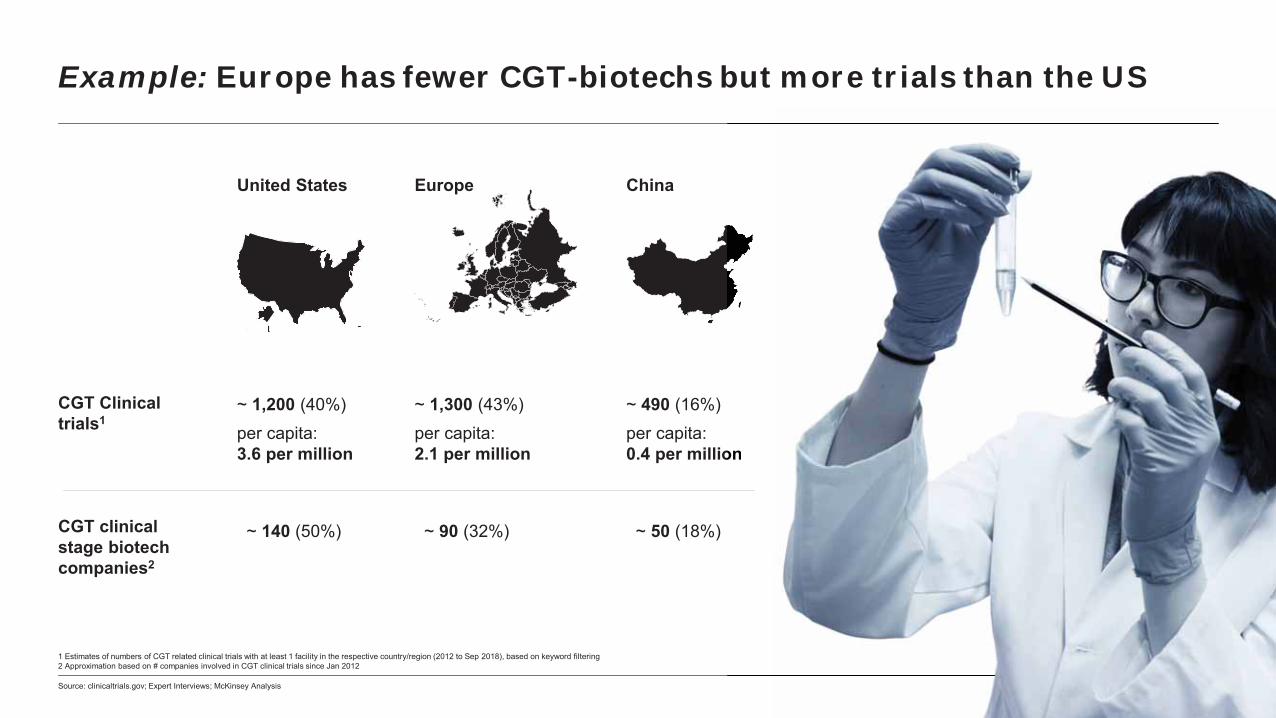

McKinsey & Company 31Source: clinicaltrials.gov; Expert Interviews; McKinsey Analysis

~ 1,200 (40%)per capita: 3.6 per million

United States

~ 1,300 (43%)per capita: 2.1 per million

Europe

~ 490 (16%)per capita: 0.4 per million

China

1 Estimates of numbers of CGT related clinical trials with at least 1 facility in the respective country/region (2012 to Sep 2018), based on keyword filtering 2 Approximation based on # companies involved in CGT clinical trials since Jan 2012

MMcMcMcMcMcMcMcMcKiKKiKiK nnsnsnnsnsn eyeyeyeyey &&&&&& CCCCCCCCCCComomomommomomomomomoommmppapapapap nynyyynny 31311

on

~ 140 (50%) ~ 90 (32%) ~ 50 (18%)

CGT Clinical trials1

CGT clinical stage biotech companies2

Example: Europe has fewer CGT-biotechs but more trials than the US

McKinsey & Company 32Source: Innography patent database 2019; BioCentury 2019, Pitchbook 2019, Pharmaprojects 2019, McKinsey SILA analysis 2019

2711

10

988

74

43

2

222

1619

24

54

733

25

1111

6

1

Switzerland

Germany

UKFrance

IsraelSweden

Netherlands

Norway

DenmarkBelgium

Spain

IrelandAustriaFinland

ItalyPoland

10

1

3

24

19

39

13

2

Antibodies

Serviceproviders2

Antibiotics

Immuno-therapies

CGT

Vaccines

By modality

Drug delivery

28

20

7

20

10

4

6

6Cardiovascular

Musculo-skeletal

Oncology

Metabolicdiseases

Respiratory

CNS

Ophthalmology

Dermatology

By TA

% of biotechs % of patents

1. Global patents from EU based inventor or registering party2. Services providers include Drug discovery tools and services, diagnostic and personalised care, CRO/CMO related topics

By location

Hot topic

Analysis of Europe patent inventors since 20051, percent of biotech companies / patents

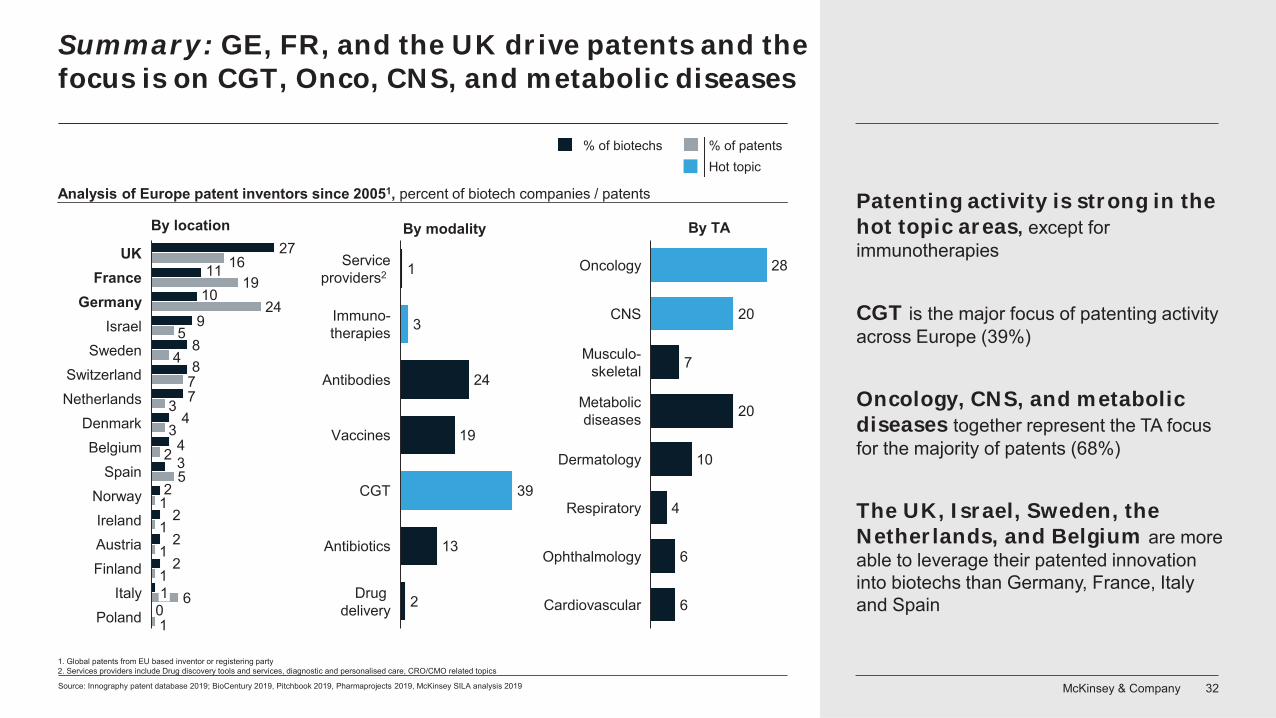

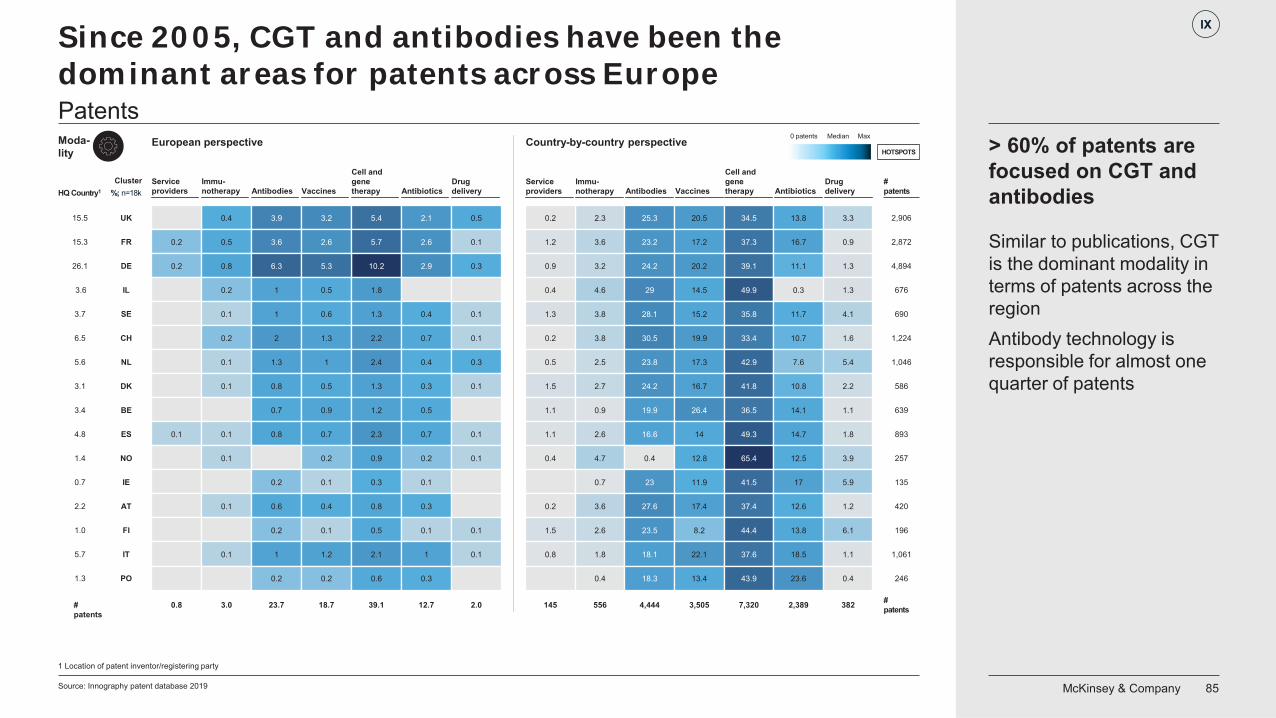

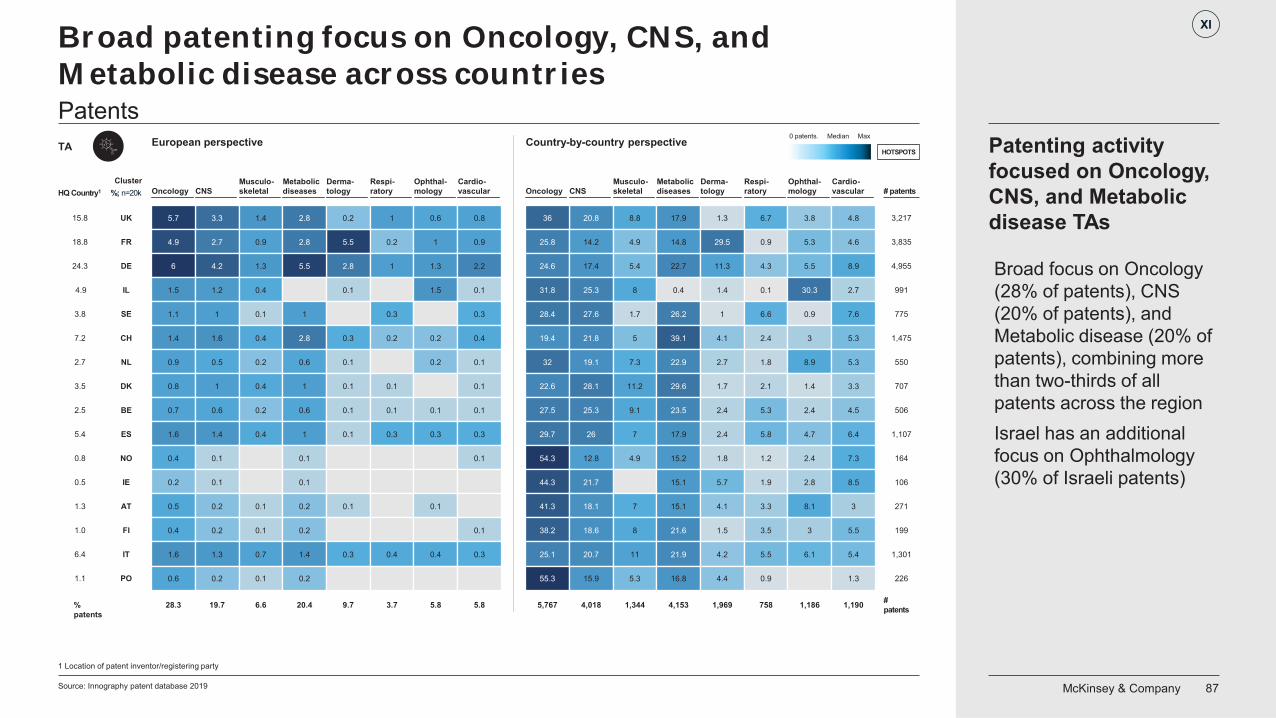

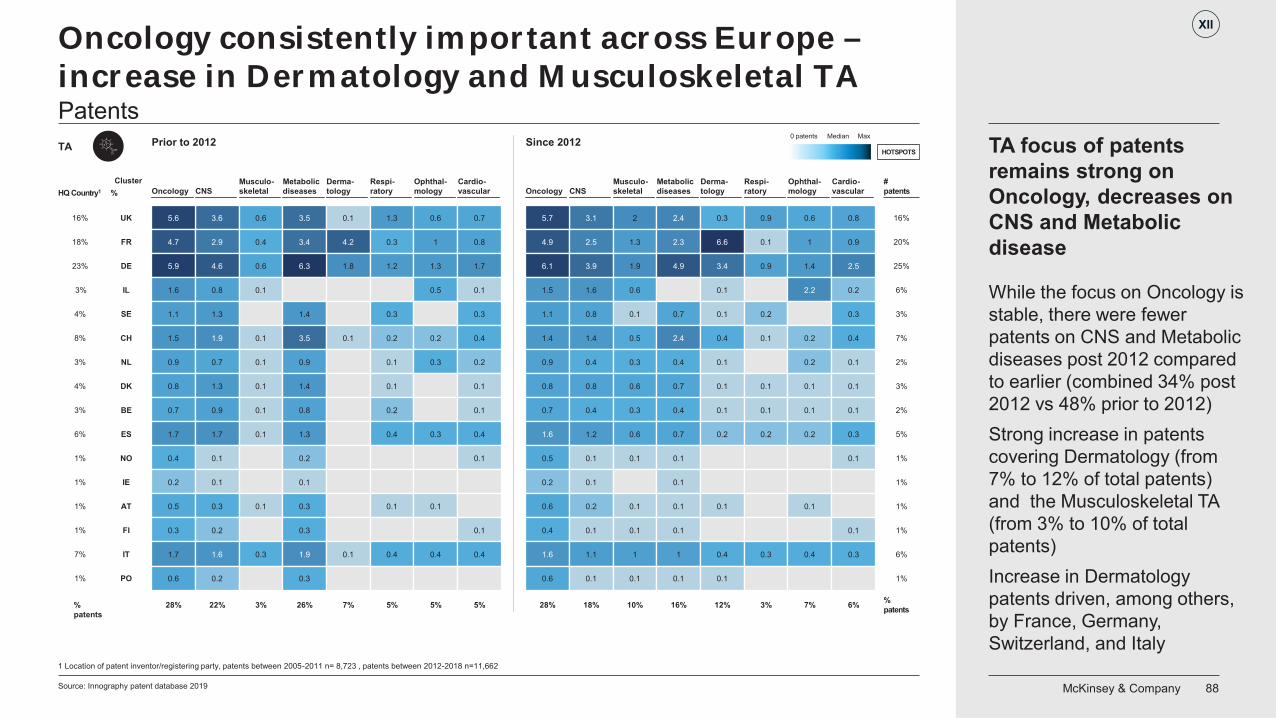

Summary: GE, FR, and the UK drive patents and the focus is on CGT, Onco, CNS, and metabolic diseases

Patenting activity is strong in the hot topic areas, except for immunotherapies

CGT is the major focus of patenting activity across Europe (39%)

Oncology, CNS, and metabolic diseases together represent the TA focus for the majority of patents (68%)

The UK, Israel, Sweden, the Netherlands, and Belgium are more able to leverage their patented innovation into biotechs than Germany, France, Italy and Spain

McKinsey & Company 33

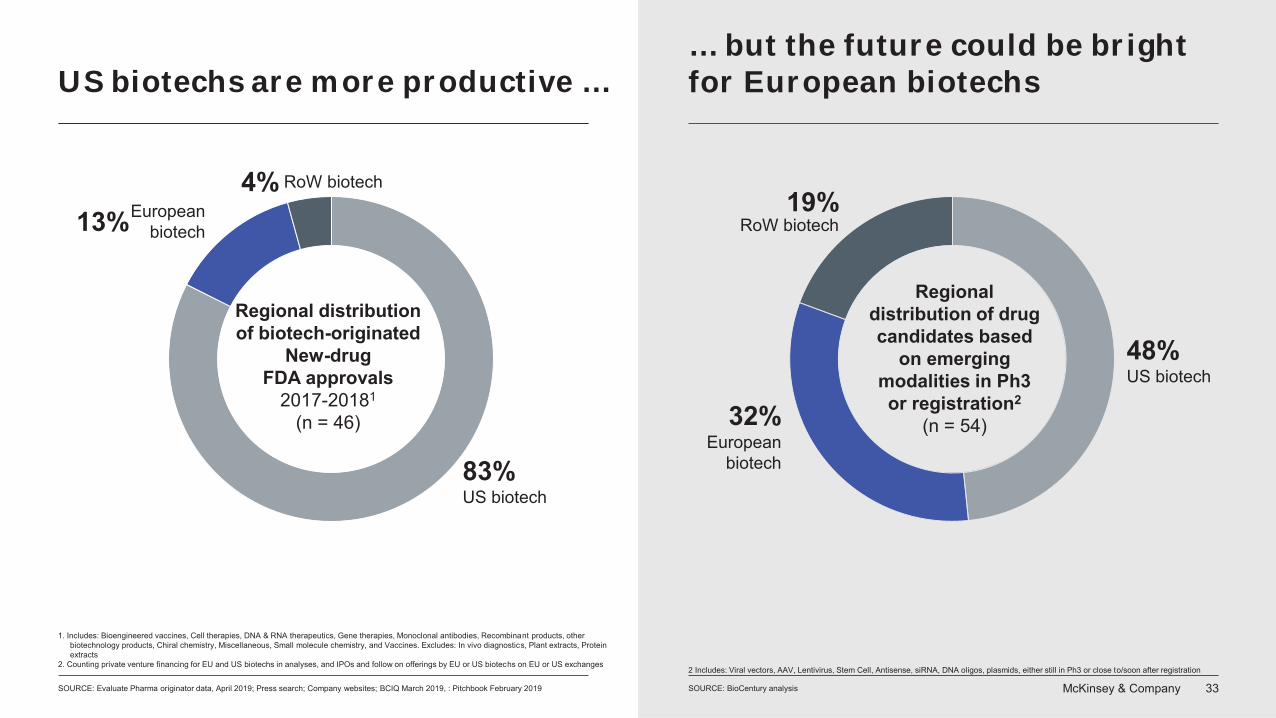

US biotechs are more productive …… but the future could be bright for European biotechs

SOURCE: Evaluate Pharma originator data, April 2019; Press search; Company websites; BCIQ March 2019, : Pitchbook February 2019

Regional distributionof biotech-originated

New-drug FDA approvals

2017-20181

(n = 46)

1. Includes: Bioengineered vaccines, Cell therapies, DNA & RNA therapeutics, Gene therapies, Monoclonal antibodies, Recombinant products, other biotechnology products, Chiral chemistry, Miscellaneous, Small molecule chemistry, and Vaccines. Excludes: In vivo diagnostics, Plant extracts, Proteinextracts

2. Counting private venture financing for EU and US biotechs in analyses, and IPOs and follow on offerings by EU or US biotechs on EU or US exchanges

SOURCE: BioCentury analysis

Regional distribution of drug candidates based

on emerging modalities in Ph3 or registration2

(n = 54)

2 Includes: Viral vectors, AAV, Lentivirus, Stem Cell, Antisense, siRNA, DNA oligos, plasmids, either still in Ph3 or close to/soon after registration

US biotech83%

Europeanbiotech13%

RoW biotech4%RoW biotech

Europeanbiotech

US biotech48%

32%

19%

McKinsey & Company 34

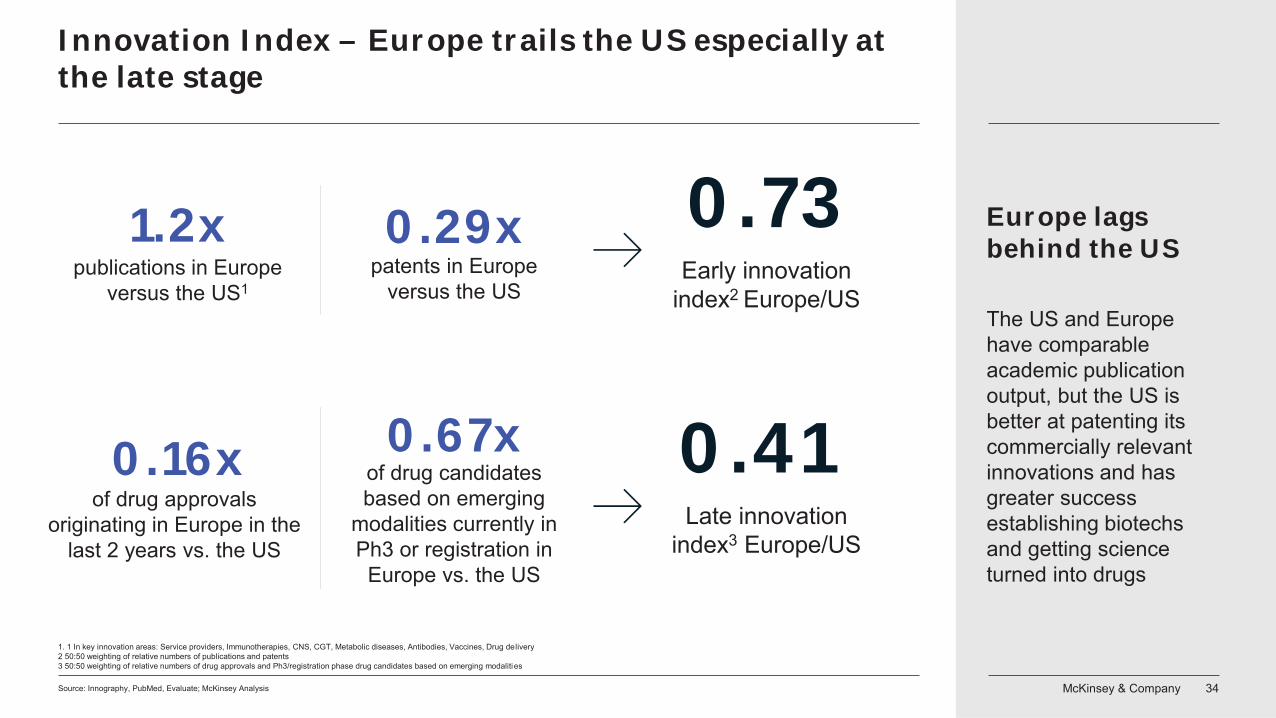

Innovation Index – Europe trails the US especially at the late stage

1. 1 In key innovation areas: Service providers, Immunotherapies, CNS, CGT, Metabolic diseases, Antibodies, Vaccines, Drug delivery2 50:50 weighting of relative numbers of publications and patents3 50:50 weighting of relative numbers of drug approvals and Ph3/registration phase drug candidates based on emerging modalities

Europe lags behind the US

The US and Europe have comparable academic publication output, but the US is better at patenting its commercially relevant innovations and has greater success establishing biotechs and getting science turned into drugs

Source: Innography, PubMed, Evaluate; McKinsey Analysis

publications in Europe versus the US1

1.2x 0.29xpatents in Europe

versus the US

0.73Early innovation

index2 Europe/US

of drug approvals originating in Europe in the

last 2 years vs. the US

0.16x 0.67xof drug candidates based on emerging

modalities currently in Ph3 or registration in

Europe vs. the US

0.41Late innovation

index3 Europe/US

McKinsey & Company 35

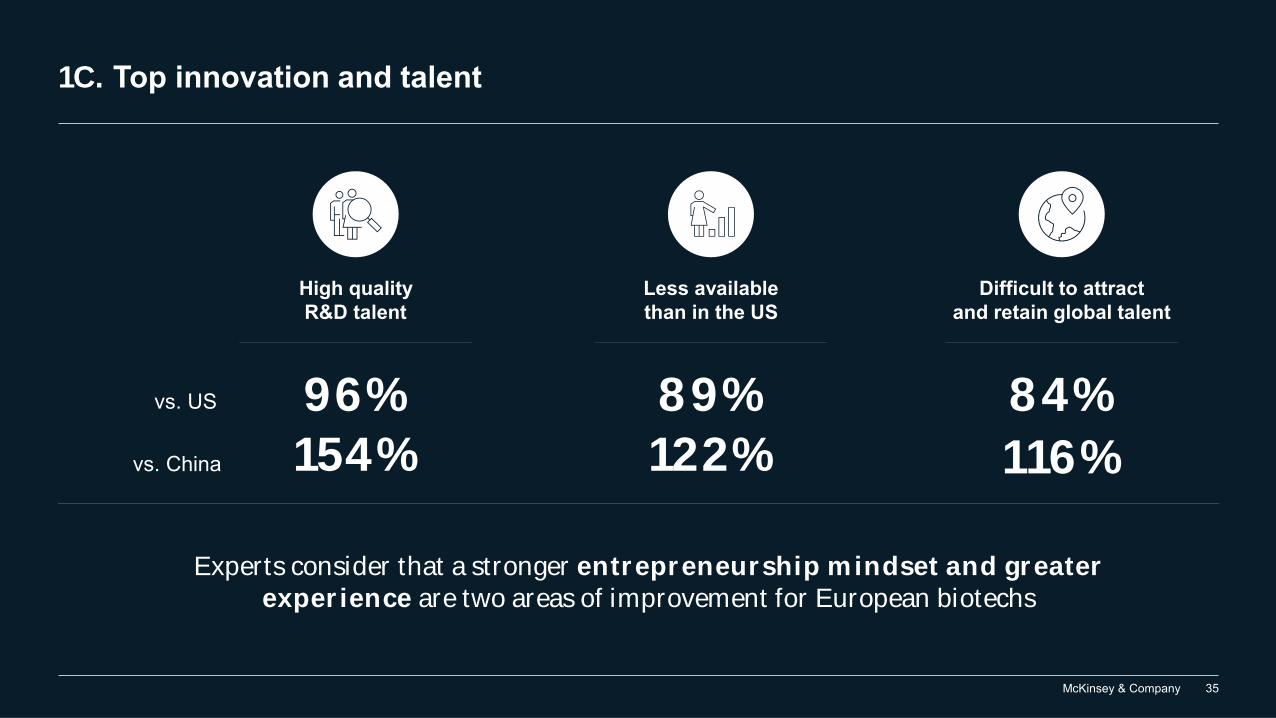

1C. Top innovation and talent

Less available than in the US

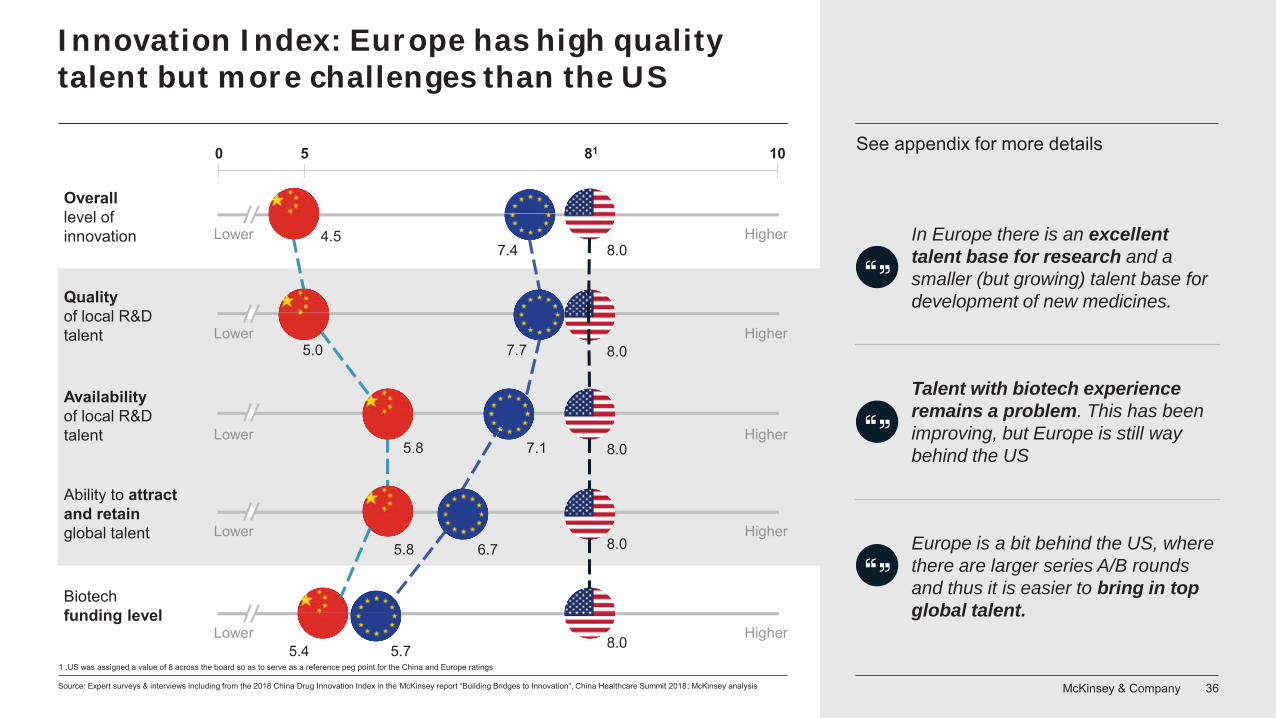

High quality R&D talent

Difficult to attract and retain global talent

89%122%

96%154%

84%116%

vs. US

vs. China

Experts consider that a stronger entrepreneurship mindset and greater experience are two areas of improvement for European biotechs

McKinsey & Company 36Source: Expert surveys & interviews including from the 2018 China Drug Innovation Index in the McKinsey report “Building Bridges to Innovation”, China Healthcare Summit 2018; McKinsey analysis

In Europe there is an excellent talent base for research and a smaller (but growing) talent base for development of new medicines.

Europe is a bit behind the US, where there are larger series A/B rounds and thus it is easier to bring in top global talent.

Talent with biotech experience remains a problem. This has been improving, but Europe is still way behind the US

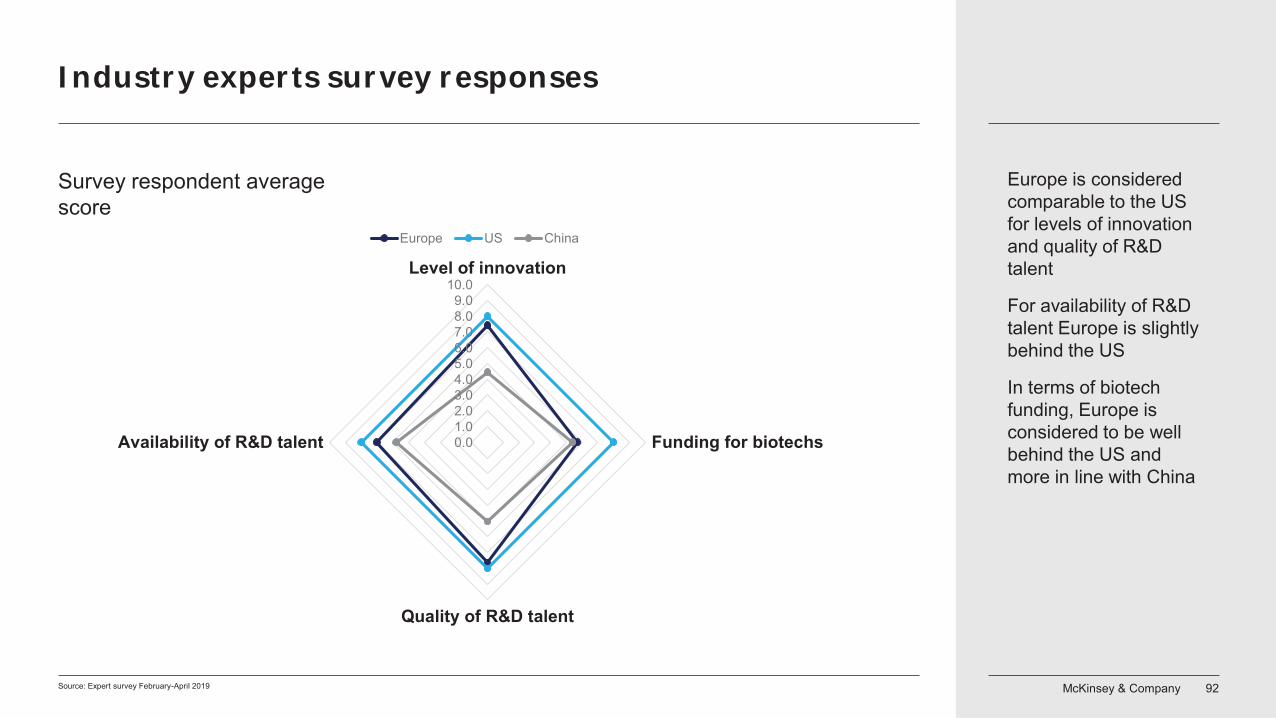

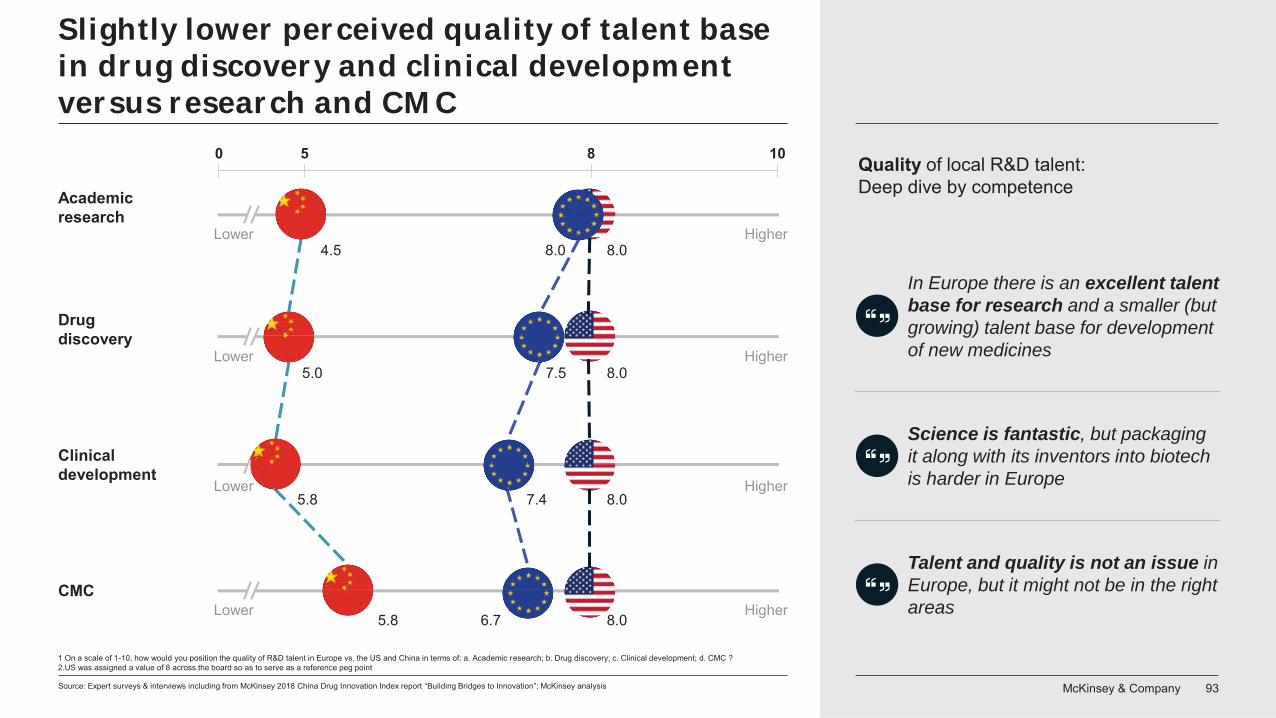

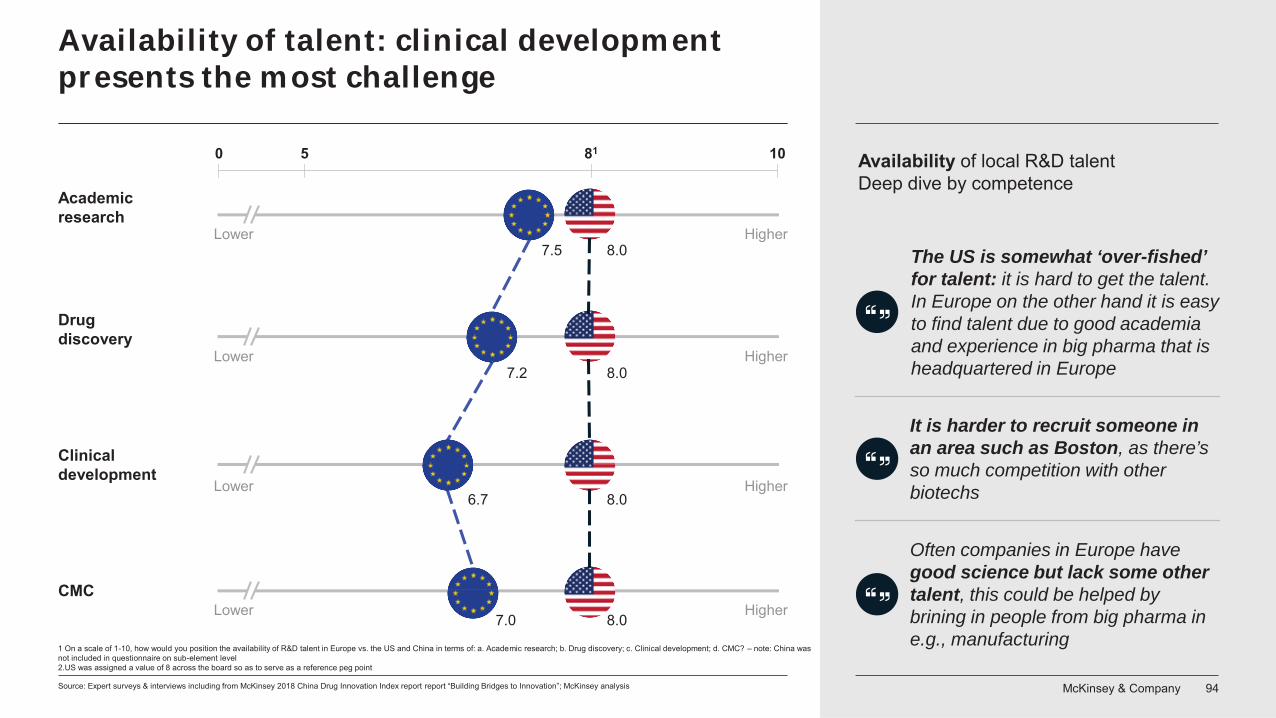

Innovation Index: Europe has high quality talent but more challenges than the US

0 105

Overalllevel of innovation HigherLower 4.5

7.4

Quality of local R&D talent Lower Higher

5.0 7.7

Availability of local R&D talent HigherLower

5.8 7.1

Ability to attract and retain global talent HigherLower

5.8 6.7

Biotech funding level

HigherLower5.4 5.7

81

8.0

8.0

8.0

8.0

1 .US was assigned a value of 8 across the board so as to serve as a reference peg point for the China and Europe ratings

8.0

See appendix for more details

McKinsey & Company 37Source: Expert interviews 2019, McKinsey cross-industry experts (McKinsey Org Practice)

Some industry experts interviewed said that, while Europe has great talent, its overall lack of experience in biotech remains a challenge

Almost one- third of industry experts interviewed pointed out that a lack of a more entrepreneurial mindset creates challenges for European biotech

In Europe it’s a big challenge to find experienced talent with business development experience

Europe is well positioned in terms of talent but talent with biotech experience remains a problem

In Europe, it is hard to get talent with rare disease and oncology experience

The quality of talent is not an issue in Europe. The question is whether it is in the right areas; maybe it is not. Has the talent been in biotechs before? Have they done lab work?

A word of caution for Europe

McKinsey & Company 38

Is financing where it needs to be?

02

A. “Good value” in European biotechs

B. Financing for European biotech is maturing

C. Gap versus US biotechs keeps growing

McKinsey & Company 39

Is financing where it needs to be?

02 A

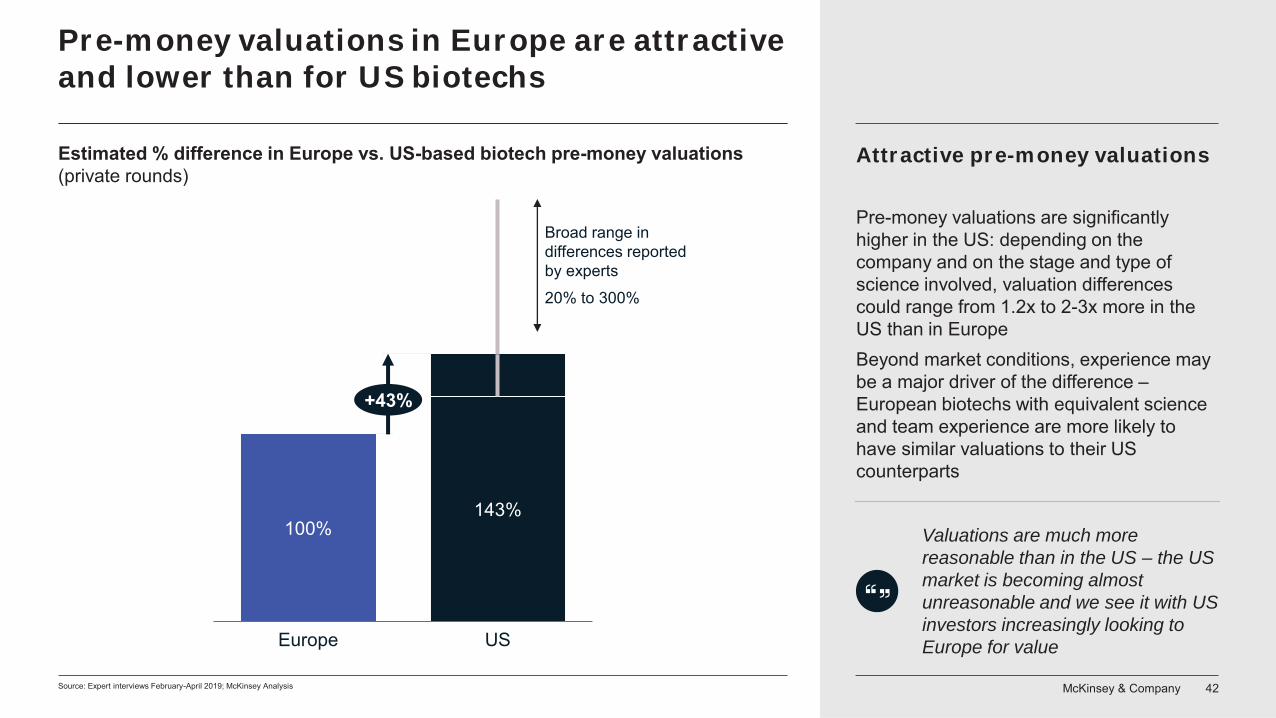

“Good value” to be found in Europe for VC investors or as a pharma partner looking for assets given lower pre-money valuations (~30%) and cheaper pharma deals which, although increasing in value, remain at roughly half the levels seen for US biotechs

B

Financing for European biotech has matured over the last 7 years especially for early-stage rounds: tripling of venture financing, doubling of European VC fund sizes, and more investments from the US The business model of European biotechs is also evolving with diversifying deal types beyond pure licensing (now only 35% of total deals) and a growing appetite to build late-stage plays

C

The financing gap vs. US biotechs is growing despite this positive dynamic, and now stands at 5x for private funding. Public markets are not deep enough: IPOs in Europe are 3x lower than those that European biotechs can secure on US markets and 95% of all follow-on offerings raised by European biotechs has been on US exchanges. As a result, European biotechs increasingly look to the US for growth capital

McKinsey & Company 40

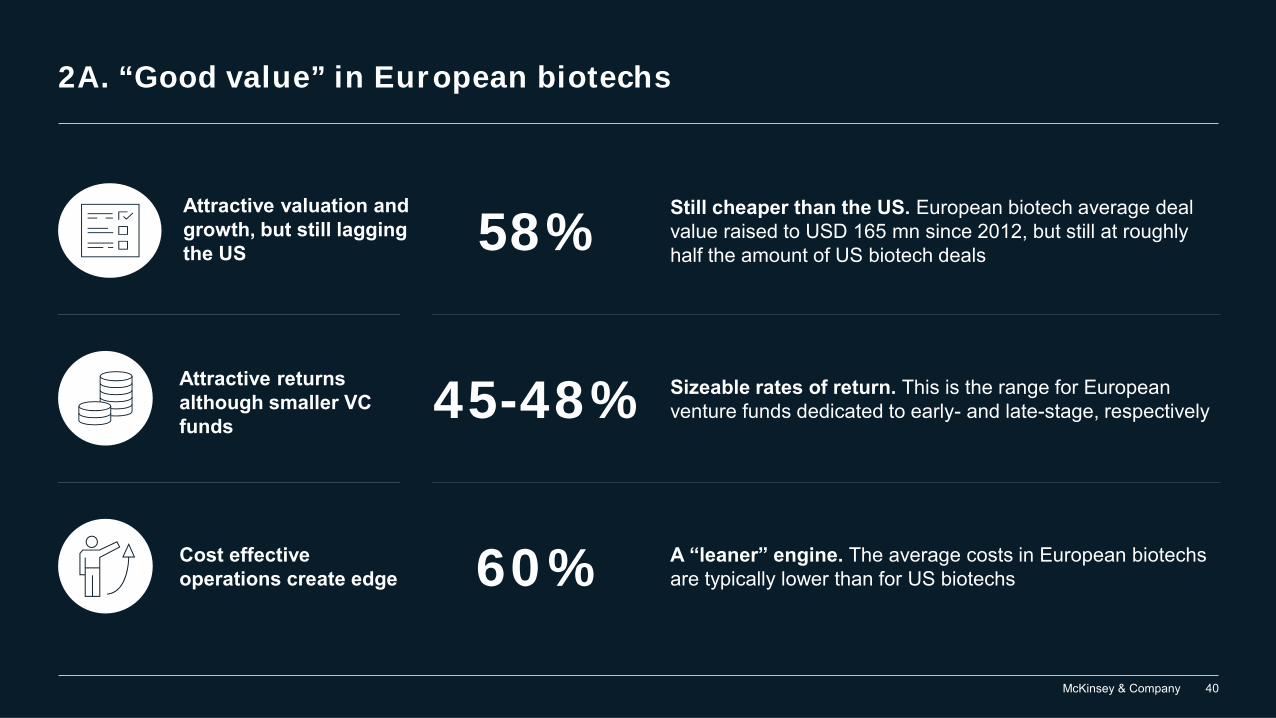

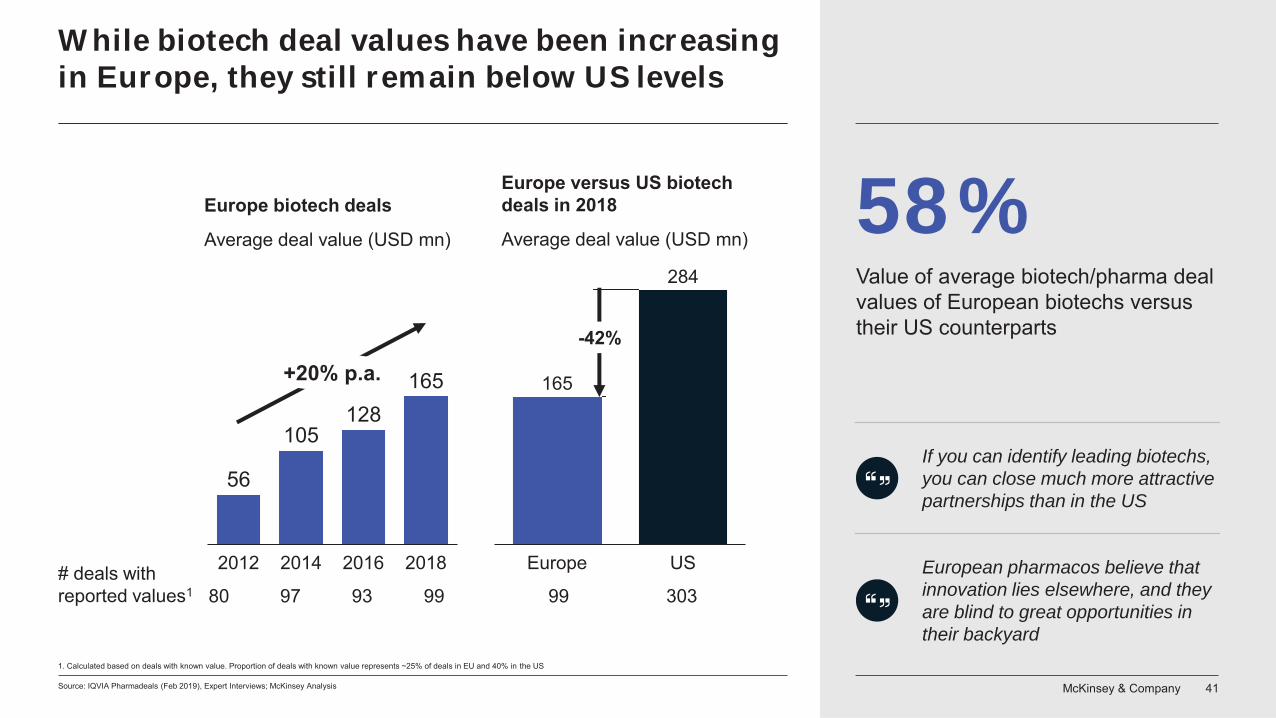

2A. “Good value” in European biotechs

58%Still cheaper than the US. European biotech average deal value raised to USD 165 mn since 2012, but still at roughly half the amount of US biotech deals

Attractive valuation and growth, but still lagging the US

Attractive returns although smaller VC funds

45-48% Sizeable rates of return. This is the range for European venture funds dedicated to early- and late-stage, respectively

Cost effective operations create edge

A “leaner” engine. The average costs in European biotechsare typically lower than for US biotechs60%

McKinsey & Company 41

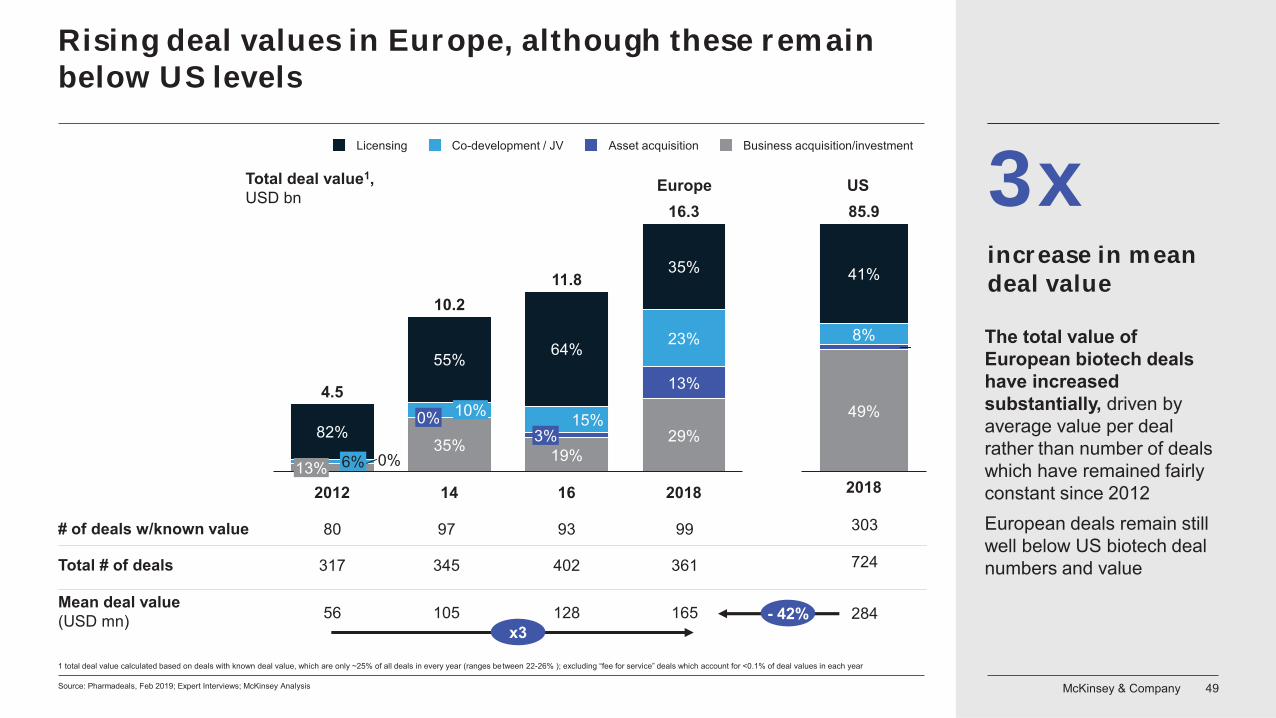

While biotech deal values have been increasing in Europe, they still remain below US levels

Source: IQVIA Pharmadeals (Feb 2019), Expert Interviews; McKinsey Analysis

Europe biotech deals

Average deal value (USD mn)

# deals with reported values1 80 97 93 99

165

284

Europe US

-42%

Europe versus US biotech deals in 2018

Average deal value (USD mn)

56

105128

165

20182012 2014 2016

+20% p.a.

99 303

1. Calculated based on deals with known value. Proportion of deals with known value represents ~25% of deals in EU and 40% in the US

58%

European pharmacos believe that innovation lies elsewhere, and they are blind to great opportunities in their backyard

If you can identify leading biotechs, you can close much more attractive partnerships than in the US

Value of average biotech/pharma deal values of European biotechs versus their US counterparts

McKinsey & Company 42

Pre-money valuations in Europe are attractive and lower than for US biotechs

Source: Expert interviews February-April 2019; McKinsey Analysis

USEurope

100%143%

+43%

Broad range in differences reported by experts 20% to 300%

Estimated % difference in Europe vs. US-based biotech pre-money valuations (private rounds)

Attractive pre-money valuations

Pre-money valuations are significantly higher in the US: depending on the company and on the stage and type of science involved, valuation differences could range from 1.2x to 2-3x more in the US than in EuropeBeyond market conditions, experience may be a major driver of the difference –European biotechs with equivalent science and team experience are more likely to have similar valuations to their US counterparts

Valuations are much more reasonable than in the US – the US market is becoming almost unreasonable and we see it with US investors increasingly looking to Europe for value

McKinsey & Company 43

Europe also has attractive returns for VCs, although the investment footprint is smaller

Source: Preqin (March 2019), includes funds with a core focus on Healthcare that reported performance in 2017 or 2018 and with geographic scope on Europe or North America.

Venture fund reported rates of return, mean net IRR (%)

45%

28%

Europe US Europe US

48%

17%

Late-stage/generalEarly-stage

Total size of funds (USD bn)

0.2 2.6 2.5 20.7 Valuations are much more reasonable than in the US – US investors increasingly looking to Europe for value

Upfront investment

Institutional funding, 80bn from H2020

Valuations, up to 3x more in the US

Better efficiency, 60% of US in structure, talent cost

Several factors contribute to the strong returns of VC funds that invest in European biotechs

McKinsey & Company 44Source: Expert survey 2019; Expert interviews 2019; McKinsey Analysis

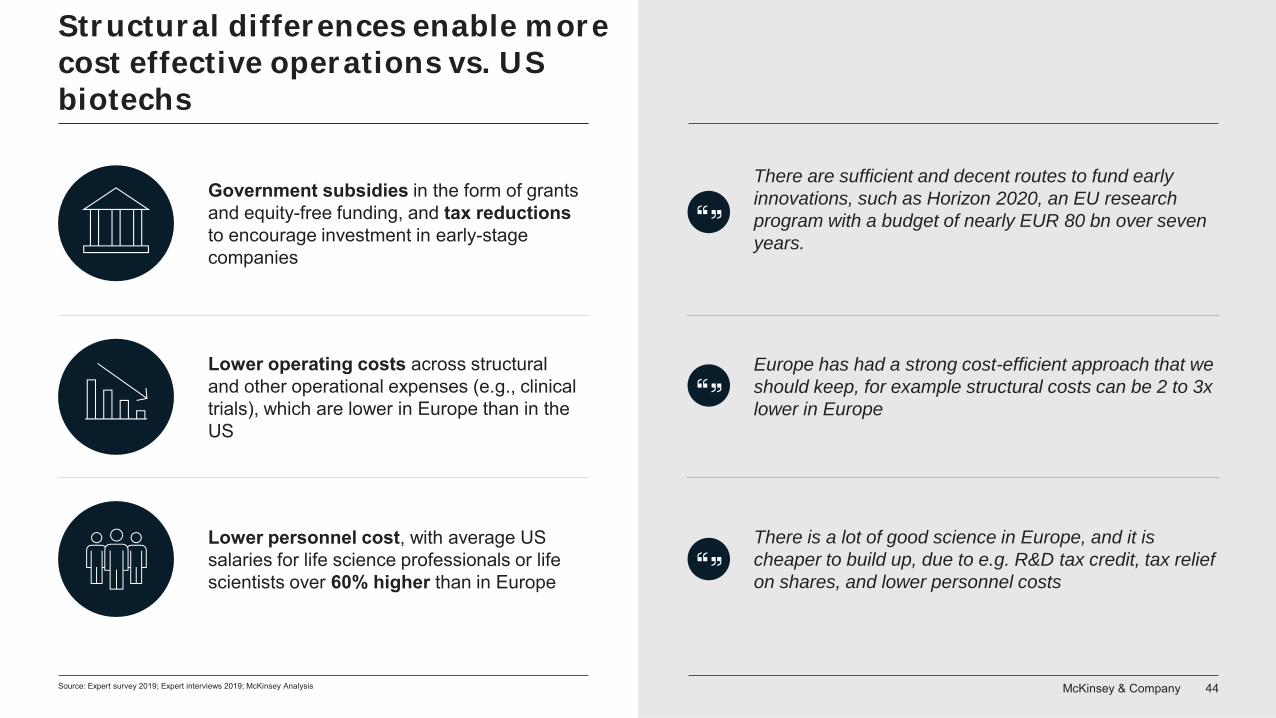

Structural differences enable more cost effective operations vs. US biotechs

Europe has had a strong cost-efficient approach that we should keep, for example structural costs can be 2 to 3x lower in Europe

There is a lot of good science in Europe, and it is cheaper to build up, due to e.g. R&D tax credit, tax relief on shares, and lower personnel costs

There are sufficient and decent routes to fund early innovations, such as Horizon 2020, an EU research program with a budget of nearly EUR 80 bn over seven years.

Government subsidies in the form of grants and equity-free funding, and tax reductions to encourage investment in early-stage companies

Lower operating costs across structural and other operational expenses (e.g., clinical trials), which are lower in Europe than in the US

Lower personnel cost, with average US salaries for life science professionals or life scientists over 60% higher than in Europe

McKinsey & Company 45

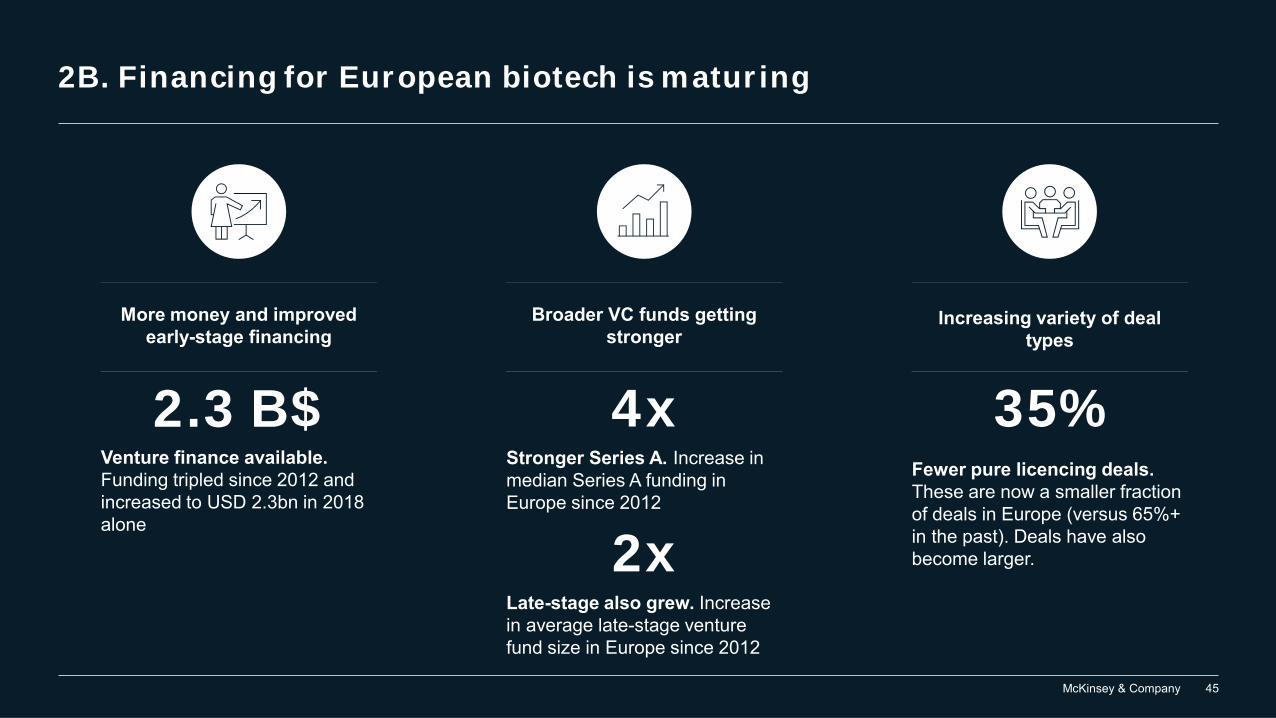

2B. Financing for European biotech is maturing

More money and improved early-stage financing

Venture finance available. Funding tripled since 2012 and increased to USD 2.3bn in 2018 alone

Broader VC funds getting stronger

2xLate-stage also grew. Increase in average late-stage venture fund size in Europe since 2012

4xStronger Series A. Increase in median Series A funding in Europe since 2012

Increasing variety of deal types

35%Fewer pure licencing deals.These are now a smaller fraction of deals in Europe (versus 65%+ in the past). Deals have also become larger.

2.3 B$

McKinsey & Company 46

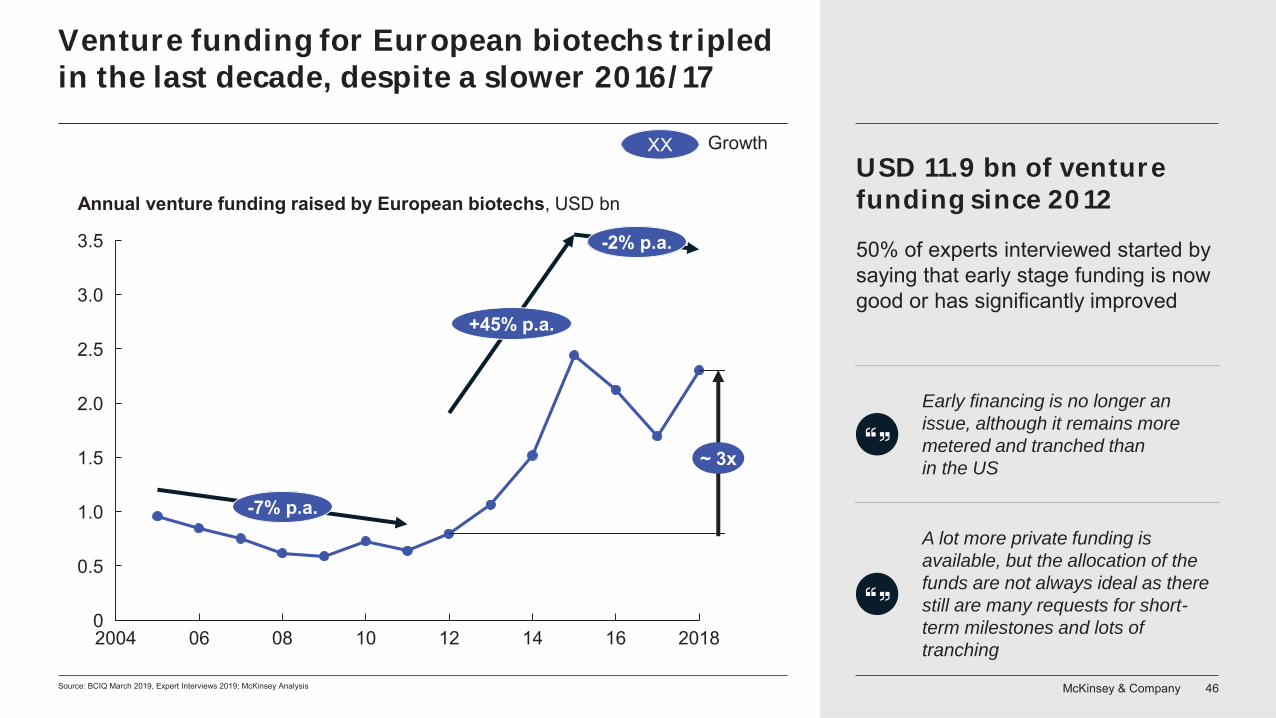

Venture funding for European biotechs tripled in the last decade, despite a slower 2016/17

Source: BCIQ March 2019, Expert Interviews 2019; McKinsey Analysis

2.0

2.5

2004 10

3.5

06 08 12 14 16 2018

3.0

0

0.5

1.0

1.5

Annual venture funding raised by European biotechs, USD bn

~ 3x

-7% p.a.

+45% p.a.

-2% p.a. 50% of experts interviewed started by saying that early stage funding is now good or has significantly improved

Early financing is no longer an issue, although it remains more metered and tranched than in the US

A lot more private funding is available, but the allocation of the funds are not always ideal as there still are many requests for short-term milestones and lots of tranching

USD 11.9 bn of venture funding since 2012

XX Growth

McKinsey & Company 47

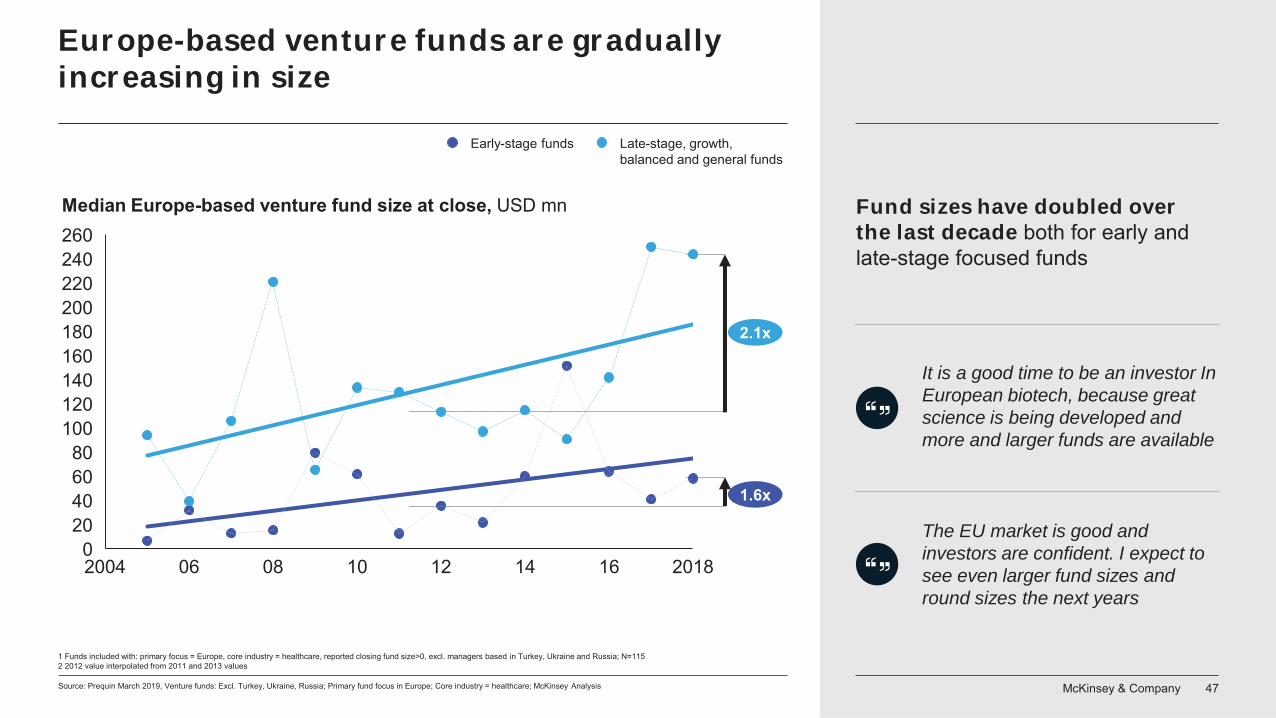

Europe-based venture funds are gradually increasing in size

Source: Prequin March 2019, Venture funds: Excl. Turkey, Ukraine, Russia; Primary fund focus in Europe; Core industry = healthcare; McKinsey Analysis

12 2018102004 0806 140

16

200

120

20406080

100

140160180

240220

260

Early-stage funds Late-stage, growth,balanced and general funds

Median Europe-based venture fund size at close, USD mn Fund sizes have doubled over the last decade both for early and late-stage focused funds

1 Funds included with: primary focus = Europe, core industry = healthcare, reported closing fund size>0, excl. managers based in Turkey, Ukraine and Russia; N=1152 2012 value interpolated from 2011 and 2013 values

2.1x

1.6x

It is a good time to be an investor In European biotech, because great science is being developed and more and larger funds are available

The EU market is good and investors are confident. I expect to see even larger fund sizes and round sizes the next years

McKinsey & Company 48

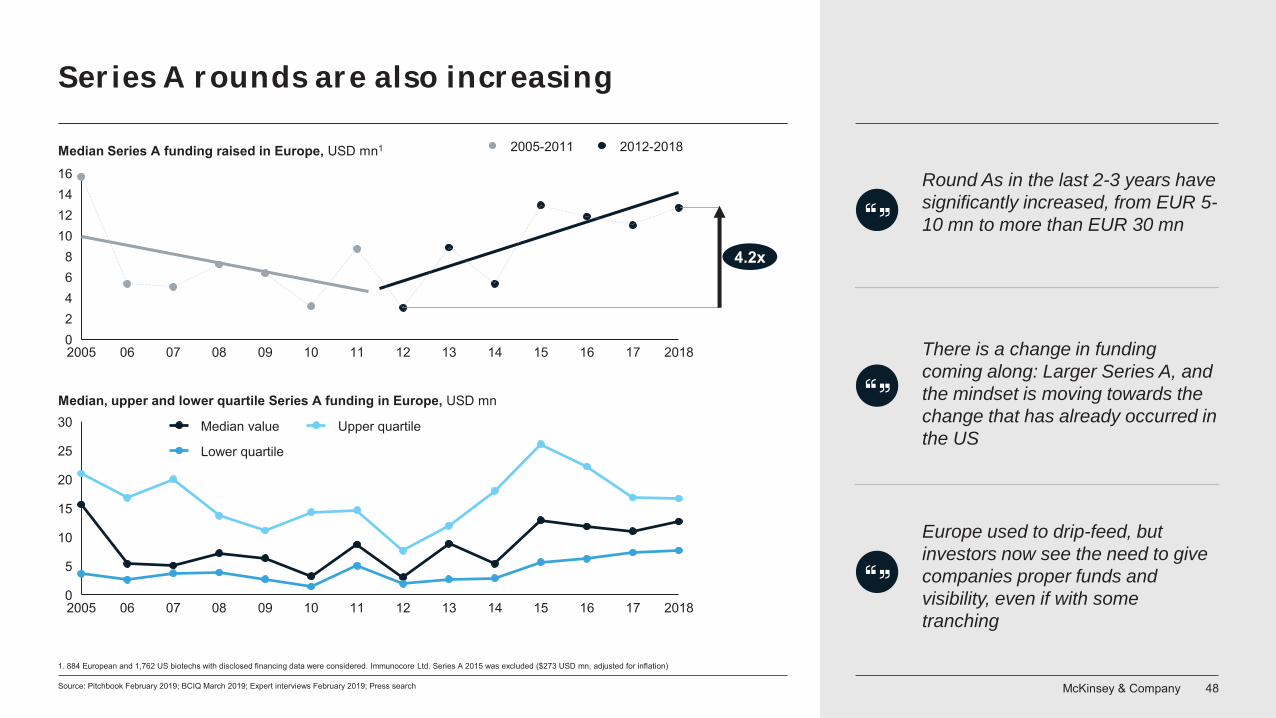

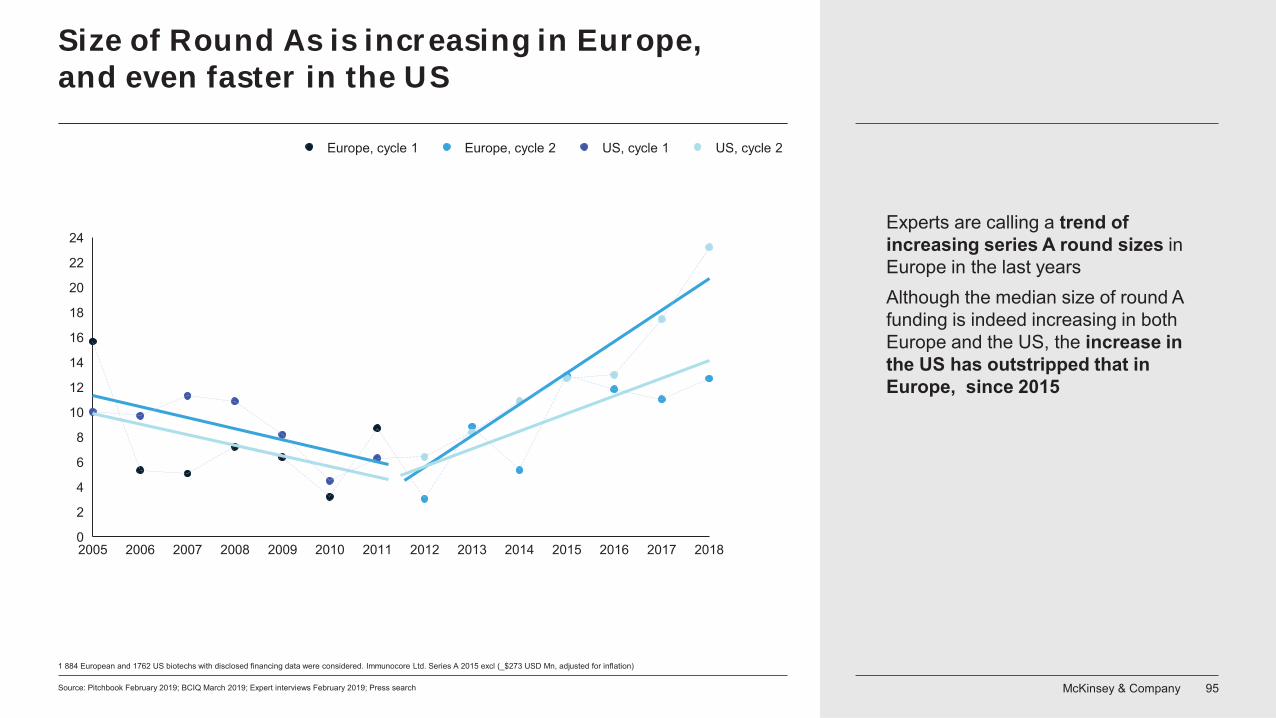

Series A rounds are also increasing

Source: Pitchbook February 2019; BCIQ March 2019; Expert interviews February 2019; Press search

07 142005

20

5

060

08 201809 12 1710 11 13 15 16

10

15

25

30

2005 09 11 1306 1207 08 10 14 15 16 17 201802468

10121416

2005-2011 2012-2018

Median value

Lower quartile

Upper quartile

1. 884 European and 1,762 US biotechs with disclosed financing data were considered. Immunocore Ltd. Series A 2015 was excluded ($273 USD mn, adjusted for inflation)

4.2x

Round As in the last 2-3 years have significantly increased, from EUR 5-10 mn to more than EUR 30 mn

There is a change in funding coming along: Larger Series A, and the mindset is moving towards the change that has already occurred in the US

Europe used to drip-feed, but investors now see the need to give companies proper funds and visibility, even if with some tranching

Median Series A funding raised in Europe, USD mn1

Median, upper and lower quartile Series A funding in Europe, USD mn

McKinsey & Company 49

82%

0%6%13%2012 2018

10%0%

55%

35%

14

64%

15%3%

19%

16

35%

23%

13%

29%

4.5

10.211.8

16.3

Rising deal values in Europe, although these remain below US levels

80 97 93 99# of deals w/known value

1 total deal value calculated based on deals with known deal value, which are only ~25% of all deals in every year (ranges between 22-26% ); excluding “fee for service” deals which account for <0.1% of deal values in each year

Source: Pharmadeals, Feb 2019; Expert Interviews; McKinsey Analysis

Total deal value1, USD bn

Licensing Co-development / JV Asset acquisition Business acquisition/investment

Europe

41%

8%

85.9

2%

49%

2018

US

317 345 402 361Total # of deals 724

303

increase in mean deal value

3x

56 105 128 165 284Mean deal value (USD mn) - 42%

x3

The total value of European biotech deals have increased substantially, driven by average value per deal rather than number of dealswhich have remained fairly constant since 2012European deals remain still well below US biotech deal numbers and value

McKinsey & Company 50

4

16

14

12

10

18

8

6

0

2

55%

29%

13%

82%

14

3%6%

10.2

35%0%

2012

10%0%

64%

15%

19%

16

35%

23%

13%

2018

4.5

11.8

16.3

Mean deal value (USD mn) 56 105 128 165

317 345 402 361Total # of deals

Total deal value1, USD Bn

Licensing Business acquisition/investmentCo-development / JV Asset acquisition

xx CAGR 2012-2018

80 97 93 99# of deals w/known value

8%

57%

43%

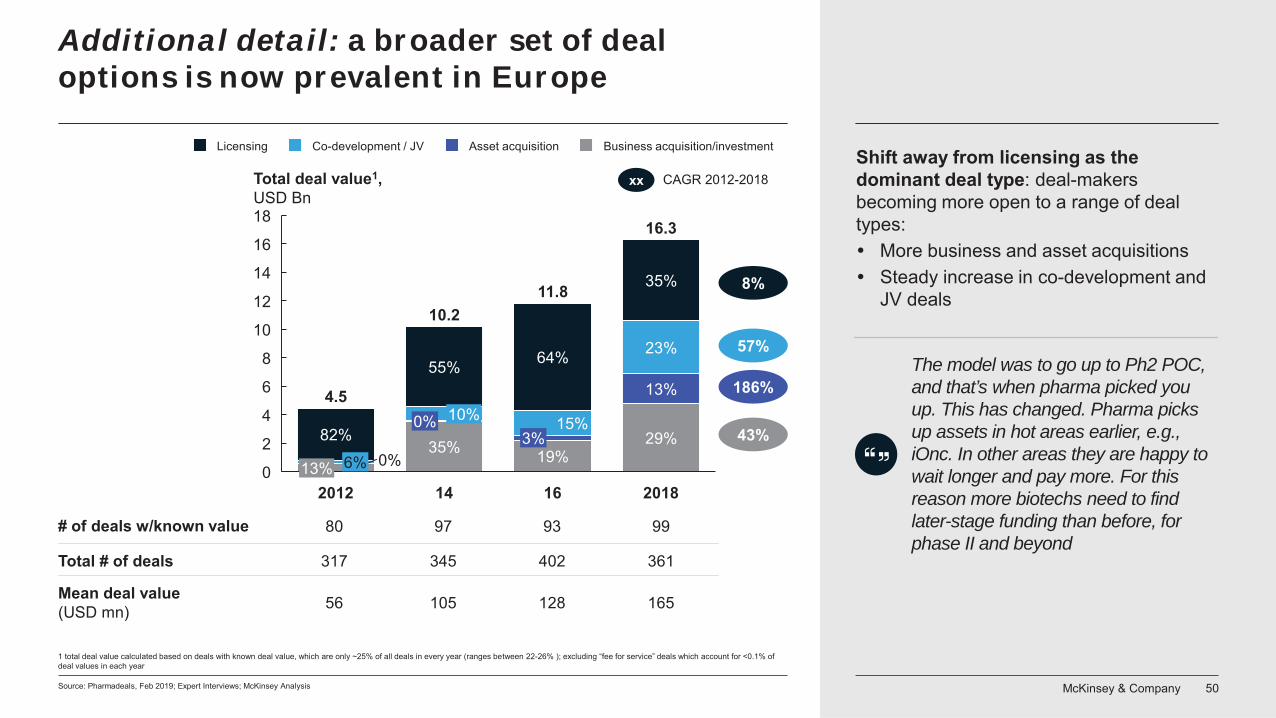

186%The model was to go up to Ph2 POC, and that’s when pharma picked you up. This has changed. Pharma picks up assets in hot areas earlier, e.g., iOnc. In other areas they are happy to wait longer and pay more. For this reason more biotechs need to find later-stage funding than before, for phase II and beyond

1 total deal value calculated based on deals with known deal value, which are only ~25% of all deals in every year (ranges between 22-26% ); excluding “fee for service” deals which account for <0.1% of deal values in each year

Shift away from licensing as the dominant deal type: deal-makers becoming more open to a range of deal types:

More business and asset acquisitionsSteady increase in co-development and JV deals

Additional detail: a broader set of deal options is now prevalent in Europe

Source: Pharmadeals, Feb 2019; Expert Interviews; McKinsey Analysis

McKinsey & Company 51

2.90.8

4.0

1.3

1.0

2.6

4.2 5.0

3.9

12

4

0

8

2

6

10

5.6

142012

0.6

11.8

0.516 2018

2.9

6.5

4.1x

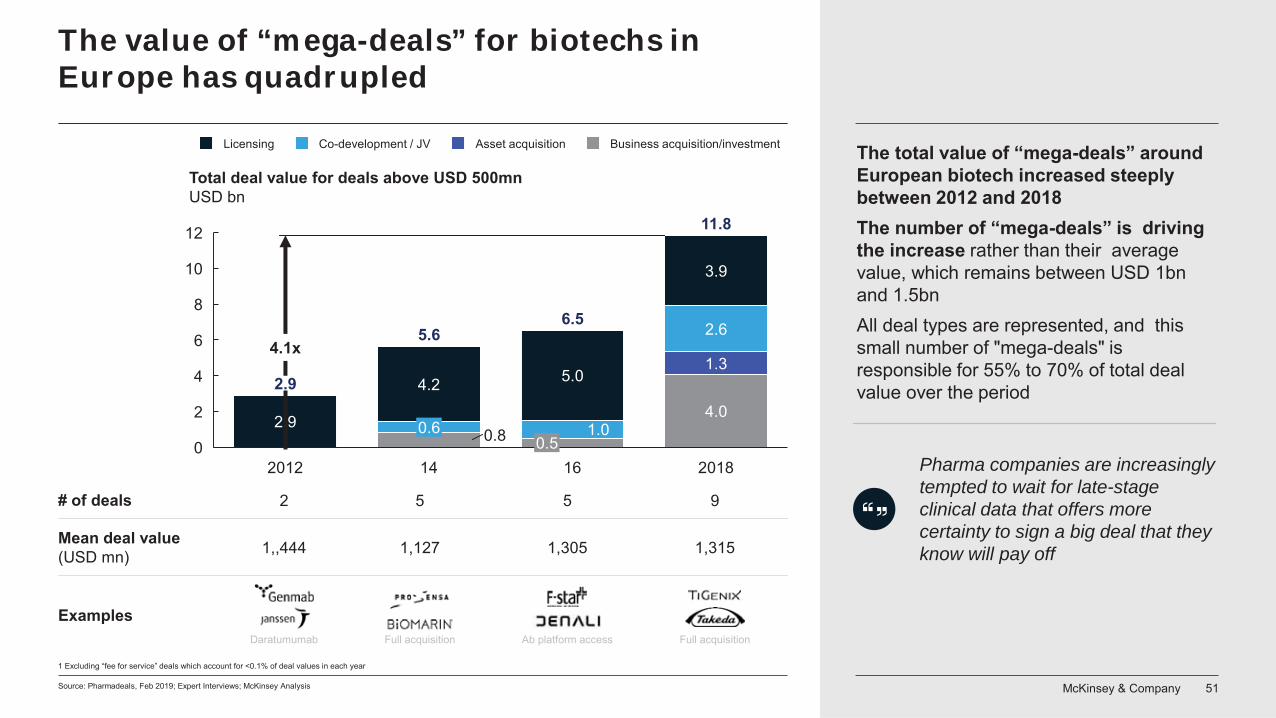

The value of “mega-deals” for biotechs in Europe has quadrupled

Licensing Co-development / JV Business acquisition/investmentAsset acquisition

Total deal value for deals above USD 500mn USD bn

1 Excluding “fee for service” deals which account for <0.1% of deal values in each year

Pharma companies are increasingly tempted to wait for late-stage clinical data that offers more certainty to sign a big deal that they know will pay off

The total value of “mega-deals” around European biotech increased steeply between 2012 and 2018The number of “mega-deals” is driving the increase rather than their average value, which remains between USD 1bn and 1.5bnAll deal types are represented, and this small number of "mega-deals" is responsible for 55% to 70% of total deal value over the period

Mean deal value (USD mn) 1,,444 1,127 1,305 1,315

# of deals 2 5 5 9

ExamplesDaratumumab Full acquisition Ab platform access Full acquisition

Source: Pharmadeals, Feb 2019; Expert Interviews; McKinsey Analysis

McKinsey & Company 52

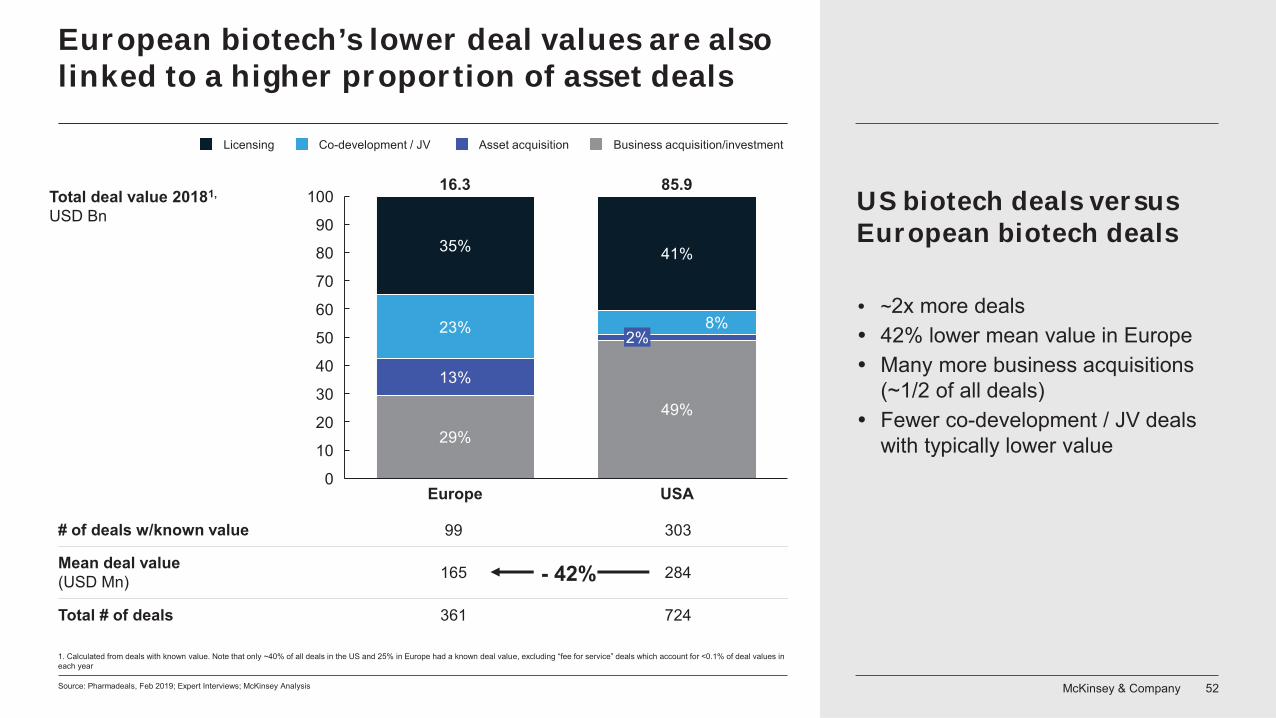

European biotech’s lower deal values are also linked to a higher proportion of asset deals

29%

49%

13%

23% 8%

35% 41%

0

20

10

30

60

50

40

70

80

90

100Total deal value 20181,

USD Bn

Europe

2%

USA

16.3 85.9

Business acquisition/investmentLicensing Co-development / JV Asset acquisition

Total # of deals 361 724

# of deals w/known value 99 303

Mean deal value (USD Mn) 165 284- 42%

US biotech deals versus European biotech deals

~2x more deals42% lower mean value in EuropeMany more business acquisitions (~1/2 of all deals)Fewer co-development / JV deals with typically lower value

1. Calculated from deals with known value. Note that only ~40% of all deals in the US and 25% in Europe had a known deal value, excluding “fee for service” deals which account for <0.1% of deal values in each year

Source: Pharmadeals, Feb 2019; Expert Interviews; McKinsey Analysis

McKinsey & Company 53

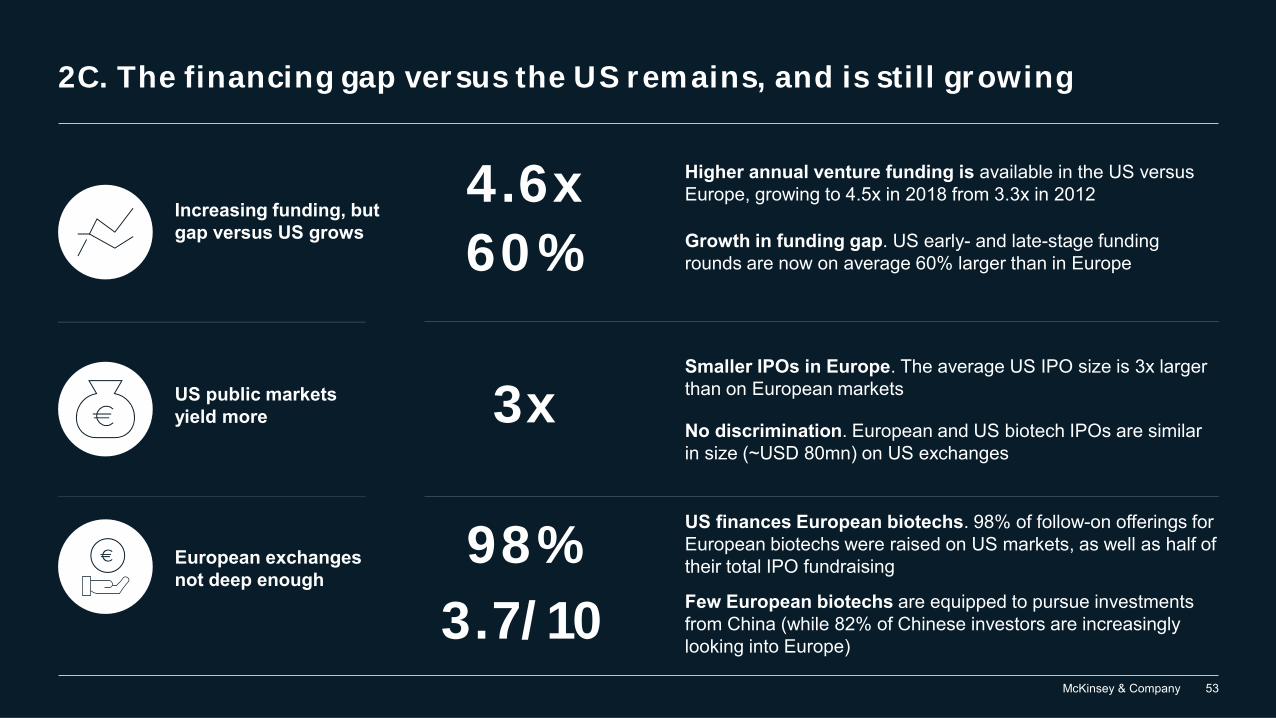

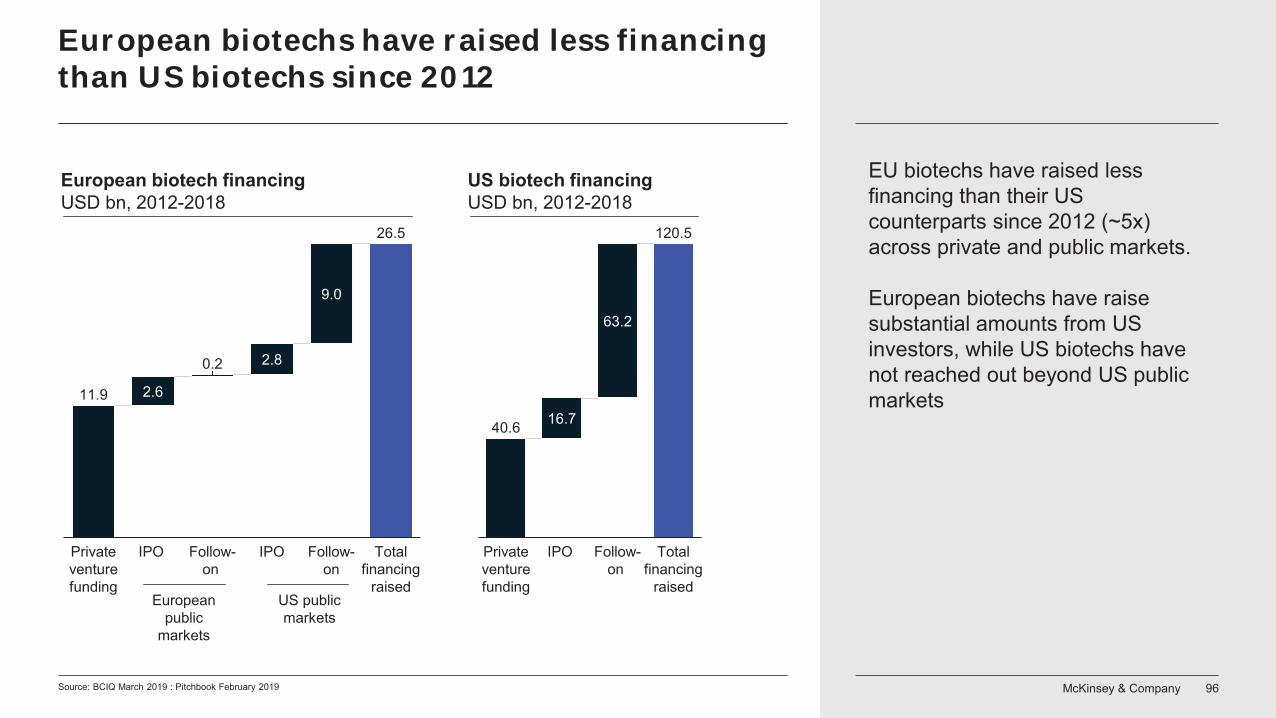

2C. The financing gap versus the US remains, and is still growing

European exchanges not deep enough

US finances European biotechs. 98% of follow-on offerings for European biotechs were raised on US markets, as well as half of their total IPO fundraising 98%

3.7/10

US public markets yield more

Smaller IPOs in Europe. The average US IPO size is 3x larger than on European markets3xNo discrimination. European and US biotech IPOs are similar in size (~USD 80mn) on US exchanges

Higher annual venture funding is available in the US versus Europe, growing to 4.5x in 2018 from 3.3x in 20124.6x

60% Growth in funding gap. US early- and late-stage funding rounds are now on average 60% larger than in Europe

Increasing funding, but gap versus US grows

Few European biotechs are equipped to pursue investments from China (while 82% of Chinese investors are increasingly looking into Europe)

McKinsey & Company 54

082005 06 07 20181709 10

2

11 12

4

15 1613

3

141

~ 4x

~ 3x

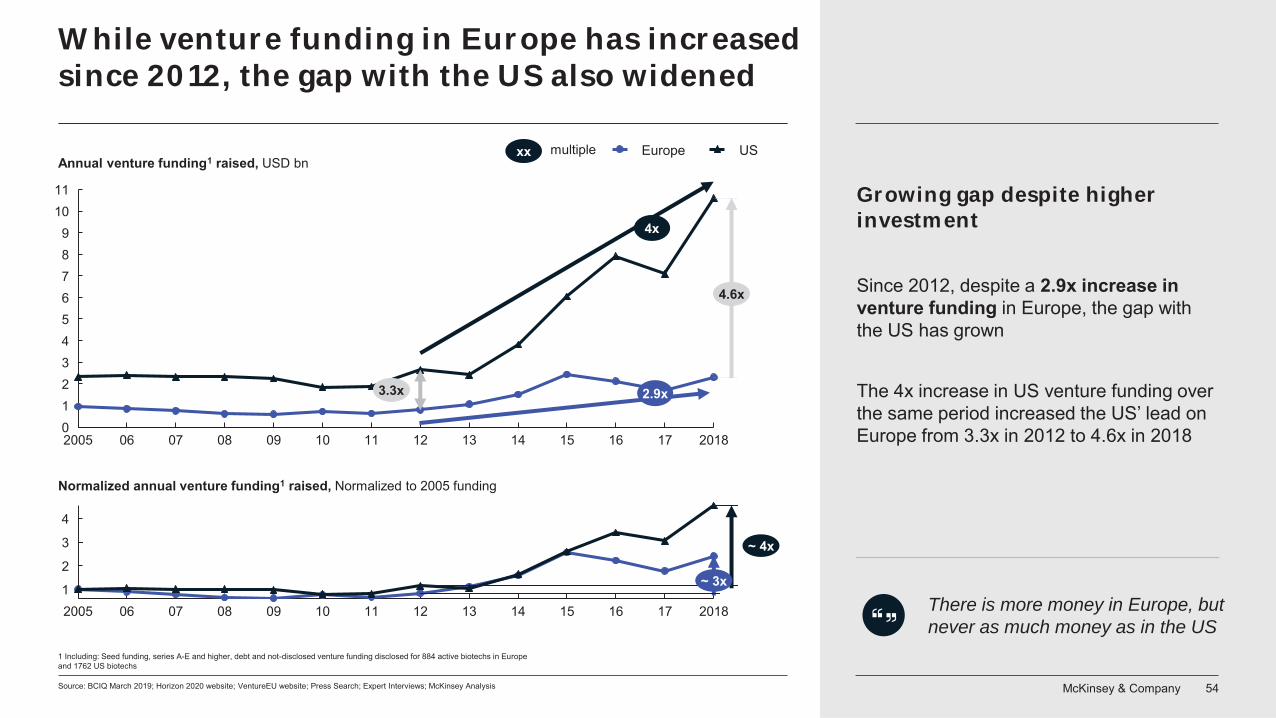

While venture funding in Europe has increased since 2012, the gap with the US also widened

Source: BCIQ March 2019; Horizon 2020 website; VentureEU website; Press Search; Expert Interviews; McKinsey Analysis

Normalized annual venture funding1 raised, Normalized to 2005 funding

Annual venture funding1 raised, USD bn

07 08 1409 10

4

11 1312

9

15 16 17

6

2018062005

123

5

7

0

1011

8

4.6x

3.3x

Europe US

1 Including: Seed funding, series A-E and higher, debt and not-disclosed venture funding disclosed for 884 active biotechs in Europe and 1762 US biotechs

xx multiple

Growing gap despite higher investment

Since 2012, despite a 2.9x increase in venture funding in Europe, the gap with the US has grown

The 4x increase in US venture funding over the same period increased the US’ lead on Europe from 3.3x in 2012 to 4.6x in 2018

There is more money in Europe, but never as much money as in the US

2.9x

4x

McKinsey & Company 55

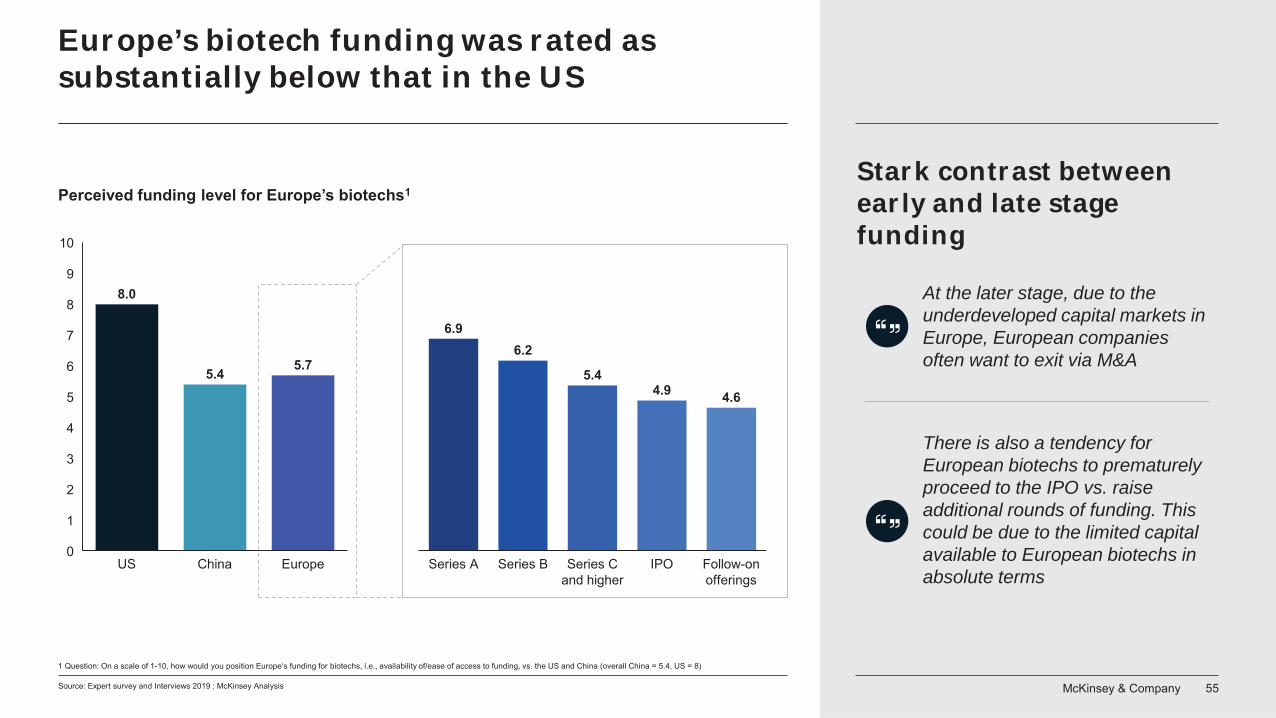

6.96.2

5.44.9 4.6

Series C and higher

Series A Follow-on offerings

Series B IPO

Source: Expert survey and Interviews 2019 ; McKinsey Analysis

8.0

5.4 5.7

9

2

1

0

3

4

5

6

7

8

10

ChinaUS Europe

Perceived funding level for Europe’s biotechs1Stark contrast between early and late stage funding

1 Question: On a scale of 1-10, how would you position Europe‘s funding for biotechs, i.e., availability of/ease of access to funding, vs. the US and China (overall China = 5.4, US = 8)

At the later stage, due to the underdeveloped capital markets in Europe, European companies often want to exit via M&A

There is also a tendency for European biotechs to prematurely proceed to the IPO vs. raise additional rounds of funding. This could be due to the limited capital available to European biotechs in absolute terms

Europe’s biotech funding was rated as substantially below that in the US

McKinsey & Company 56

The comparison of the venture funding round size in Europe and the US echoes the expert survey result, showing a larger gap in late-stage rounds

Source: Pitchbook February 2019; BCIQ March 2019; Expert interviews February 2019; Press search

441 412 31 150

Mean venture funding for European and US biotechs since 20051

USD mn, # financing roundsXXx # biotechs

146 171 312 781 157 493 81 264 40 112 13 39 3 21

4

Venture (Series A

financing)3

3

Venture (Seed

financing)

Venture (Series B financing)

Venture (Series C financing)

Venture (Series D financing)

Venture (Beyond series E)

Venture (Series E financing)

1419

2525 28 2633

2331

47

13

61

Europe US

1018

10

Venture (Debt)

28

Venture (Not disclosed)

1. 884 European and 1762 US biotechs with disclosed financing data were considered2. Assuming 800 USD Mn raised by Roivant Sciences is spread across seed, series A and series B financing in the ratio of current seed: A:B financing3. Excl. Immunocore Ltd. 20154. weighted average taking into account number of rounds per lead

Mean early-stage venture funding4

Europe2: USD 15 mnUS: USD 20 mn x1.3

Mean late-stage venture funding4

Europe: USD 25 mnUS: USD 35 mn x1.4

Additional venture funding typesUSD mn, # financing rounds

McKinsey & Company 57

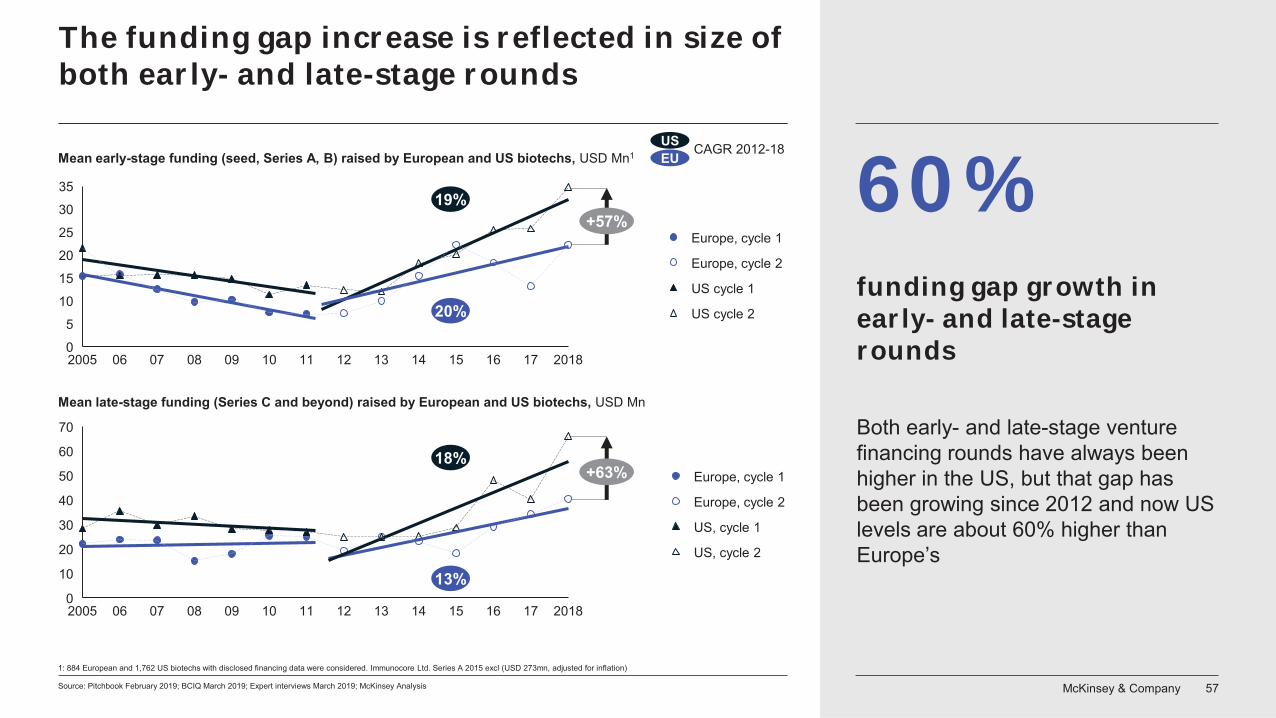

The funding gap increase is reflected in size of both early- and late-stage rounds

Source: Pitchbook February 2019; BCIQ March 2019; Expert interviews March 2019; McKinsey Analysis

10

20

2005 1206 07 0908 11 13 14 15 16

70

50

17 20180

10

30

40

60

12112005 07

15

060

1008 09 13 14 1615 17 2018

5

10

20

25

30

35

Europe, cycle 1

US cycle 1

Europe, cycle 2

US cycle 2

Europe, cycle 1

Europe, cycle 2

US, cycle 1

US, cycle 2

19%

20%

13%

18%

Mean early-stage funding (seed, Series A, B) raised by European and US biotechs, USD Mn1

Mean late-stage funding (Series C and beyond) raised by European and US biotechs, USD Mn

+57%

CAGR 2012-18USEU

+63%

1: 884 European and 1,762 US biotechs with disclosed financing data were considered. Immunocore Ltd. Series A 2015 excl (USD 273mn, adjusted for inflation)

funding gap growth in early- and late-stage rounds

Both early- and late-stage venture financing rounds have always been higher in the US, but that gap has been growing since 2012 and now US levels are about 60% higher than Europe’s

60%

McKinsey & Company 58

3.37.7

1.2 2.74.7

0.52.4

6.7

1.0 1.53.8 2.6

0

5

10

Ratio of early- to late-stage funding2

2.7: Europe avrg.1.9: US avrg.

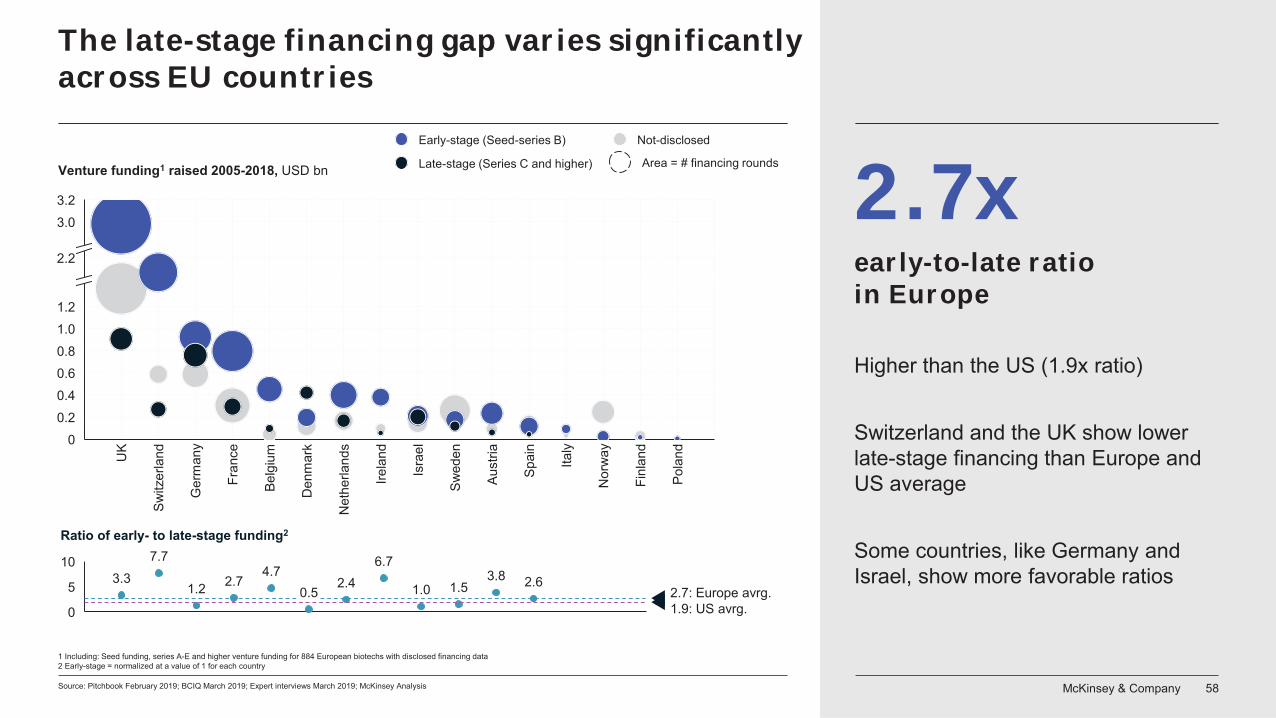

The late-stage financing gap varies significantly across EU countries

Source: Pitchbook February 2019; BCIQ March 2019; Expert interviews March 2019; McKinsey Analysis

Irela

nd

1.0

2.2

3.03.2

UK

Switz

erla

nd

0.6

1.2

Net

herla

nds

Pola

nd

Finl

and

Aust

ria

Den

mar

k

Belg

ium

Italy

Nor

way

Ger

man

y

Fran

ce

0

0.8

0.20.4

Isra

el

Spai

n

Swed

en

Area = # financing rounds

Early-stage (Seed-series B) Not-disclosed

Late-stage (Series C and higher)

1 Including: Seed funding, series A-E and higher venture funding for 884 European biotechs with disclosed financing data2 Early-stage = normalized at a value of 1 for each country

Venture funding1 raised 2005-2018, USD bn 2.7x early-to-late ratio in Europe

Higher than the US (1.9x ratio)

Switzerland and the UK show lower late-stage financing than Europe and US average

Some countries, like Germany and Israel, show more favorable ratios

McKinsey & Company 59

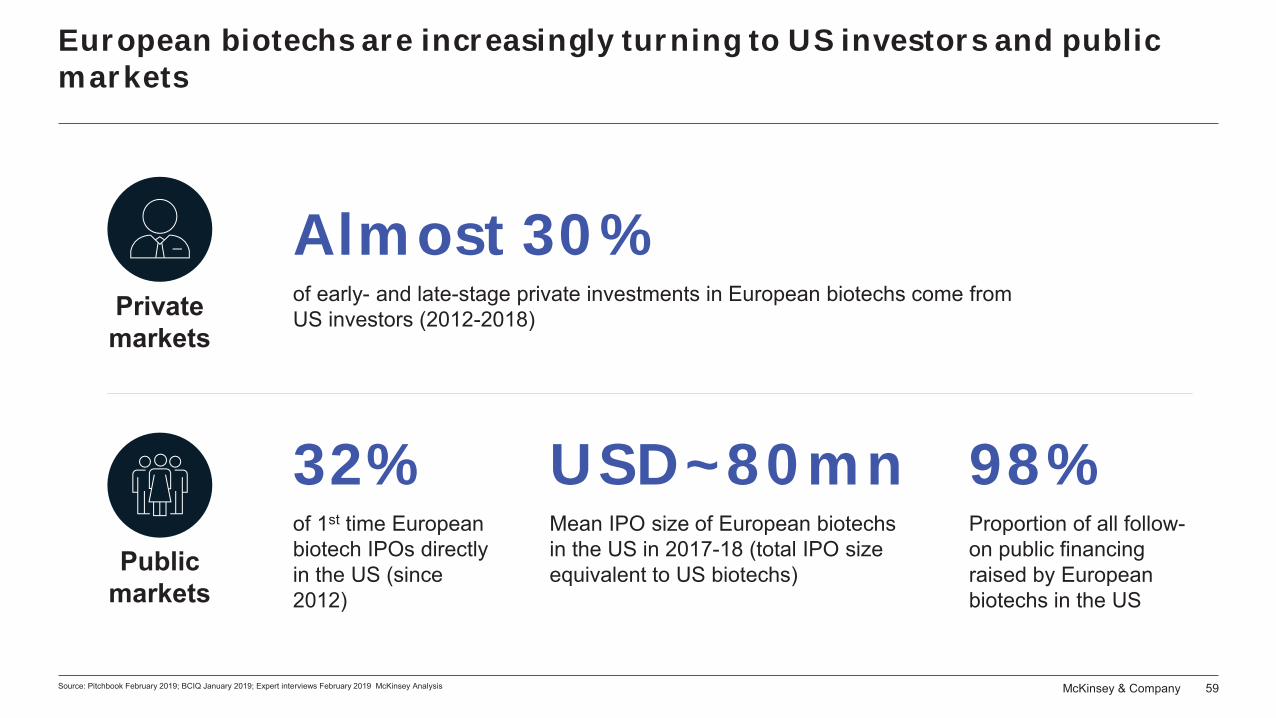

European biotechs are increasingly turning to US investors and public markets

Almost 30%of early- and late-stage private investments in European biotechs come from US investors (2012-2018) Private

markets

98%Proportion of all follow-on public financing raised by European biotechs in the US

USD~80mnMean IPO size of European biotechs in the US in 2017-18 (total IPO size equivalent to US biotechs)

32%of 1st time European biotech IPOs directly in the US (since 2012)

Public markets

Source: Pitchbook February 2019; BCIQ January 2019; Expert interviews February 2019 McKinsey Analysis

McKinsey & Company 60

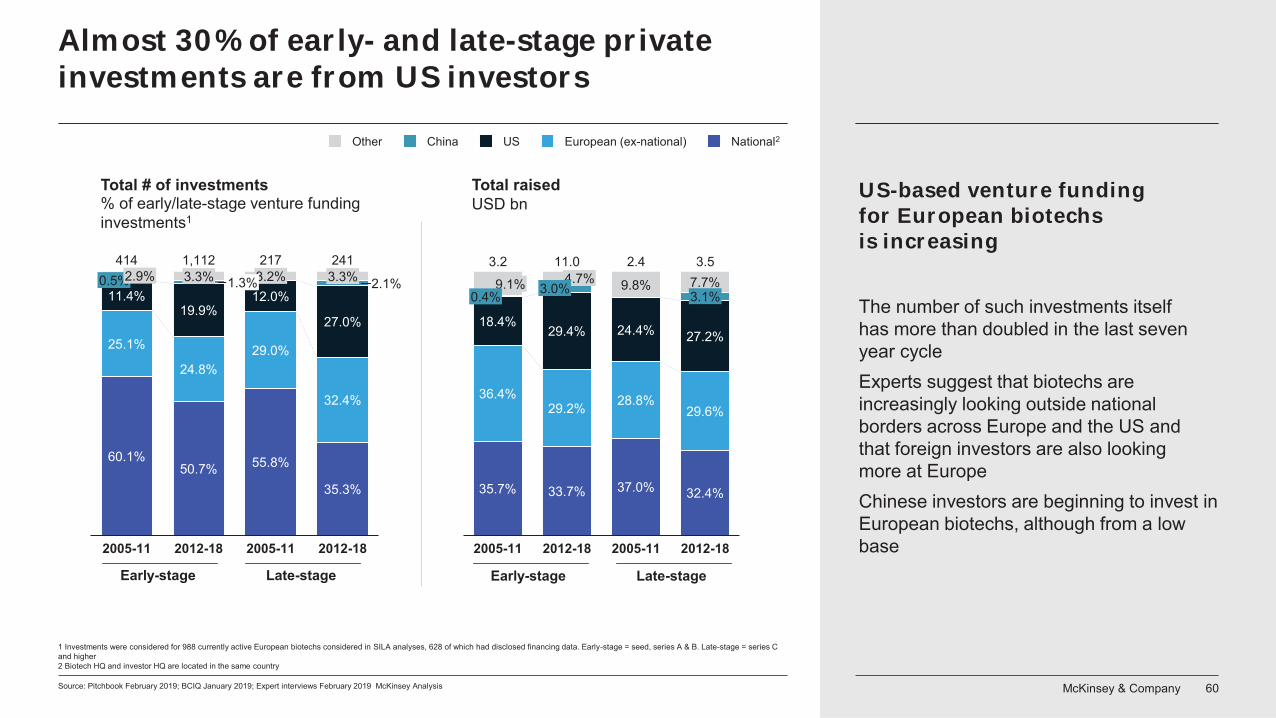

Almost 30% of early- and late-stage private investments are from US investors

Source: Pitchbook February 2019; BCIQ January 2019; Expert interviews February 2019 McKinsey Analysis

60.1%50.7% 55.8%

35.3%

25.1%

24.8%29.0%

32.4%

11.4%19.9%

12.0%

27.0%

2.1%0.5%2.9%

2005-11

3.3%241

3.2%1.3%

2012-18 2005-11

3.3%

2012-18

414 1,112 217

Other National2China US European (ex-national)

% of early/late-stage venture funding investments1

35.7% 33.7% 37.0% 32.4%

36.4%29.2% 28.8%

29.6%

18.4%29.4% 24.4% 27.2%

9.8% 7.7%3.1%

2012-182005-11

9.1% 4.7%0.4% 3.0%

2005-11 2012-18

3.2 2.411.0 3.5

Total raised USD bn

1 Investments were considered for 988 currently active European biotechs considered in SILA analyses, 628 of which had disclosed financing data. Early-stage = seed, series A & B. Late-stage = series C and higher2 Biotech HQ and investor HQ are located in the same country

Total # of investments US-based venture funding for European biotechsis increasing

The number of such investments itself has more than doubled in the last seven year cycleExperts suggest that biotechs are increasingly looking outside national borders across Europe and the US and that foreign investors are also looking more at EuropeChinese investors are beginning to invest in European biotechs, although from a low base

Early-stage Late-stage Early-stage Late-stage

McKinsey & Company 61

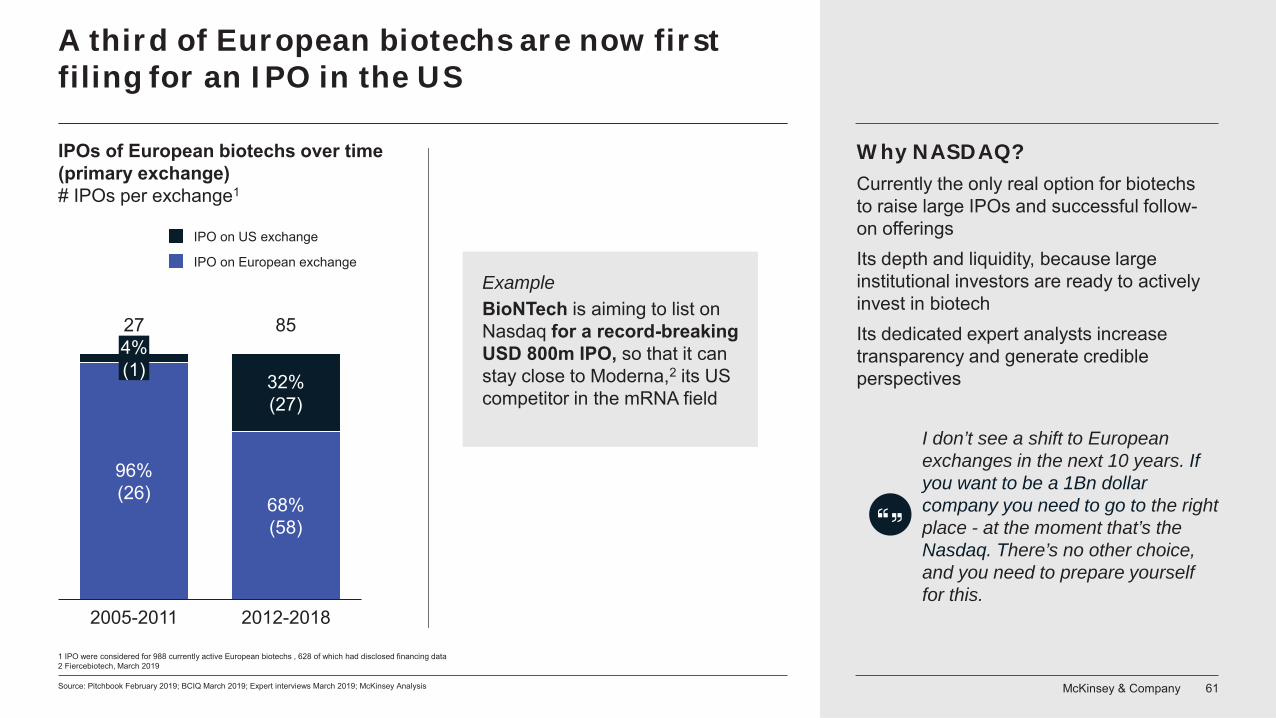

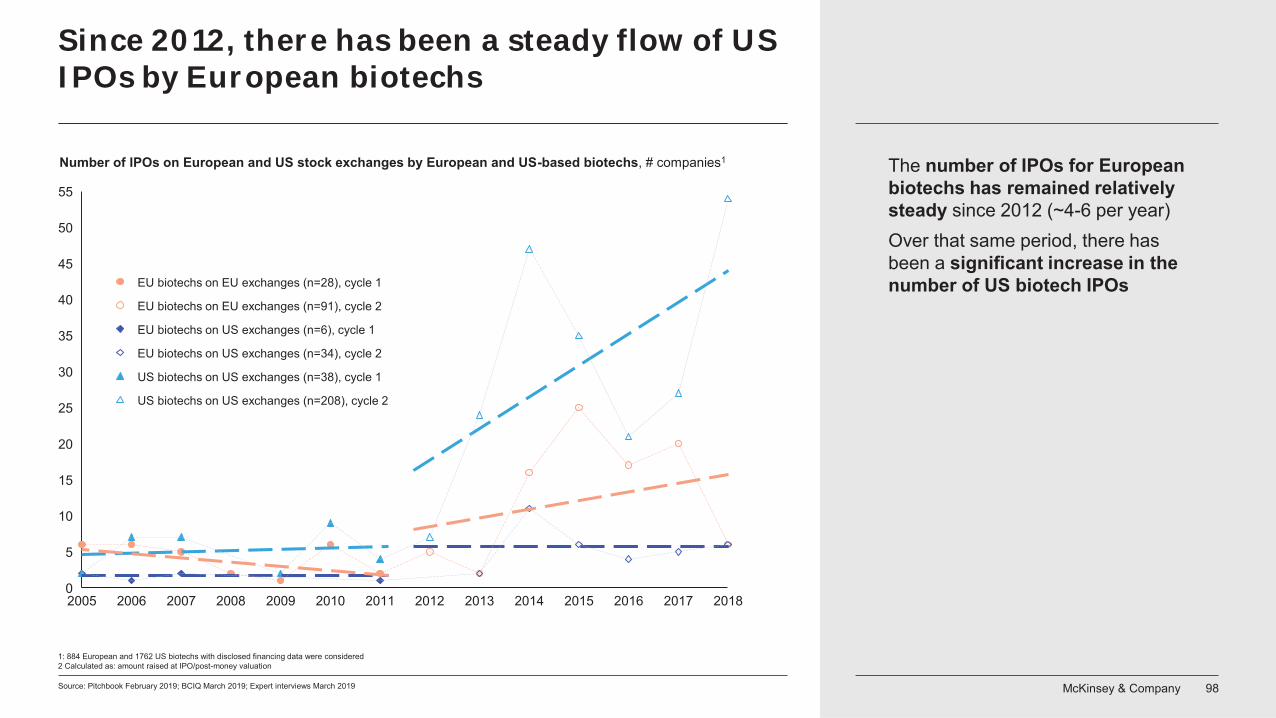

A third of European biotechs are now first filing for an IPO in the US

Source: Pitchbook February 2019; BCIQ March 2019; Expert interviews March 2019; McKinsey Analysis

1 IPO were considered for 988 currently active European biotechs , 628 of which had disclosed financing data2 Fiercebiotech, March 2019

IPOs of European biotechs over time(primary exchange)# IPOs per exchange1

854%(1)

96%(26)

2005-2011

68%(58)

32%(27)

2012-2018

27

IPO on US exchange

IPO on European exchangeExampleBioNTech is aiming to list on Nasdaq for a record-breaking USD 800m IPO, so that it can stay close to Moderna,2 its US competitor in the mRNA field

Why NASDAQ?Currently the only real option for biotechsto raise large IPOs and successful follow-on offeringsIts depth and liquidity, because largeinstitutional investors are ready to actively invest in biotechIts dedicated expert analysts increase transparency and generate credible perspectives

I don’t see a shift to European exchanges in the next 10 years. If you want to be a 1Bn dollar company you need to go to the right place - at the moment that’s the Nasdaq. There’s no other choice, and you need to prepare yourself for this.

McKinsey & Company 62

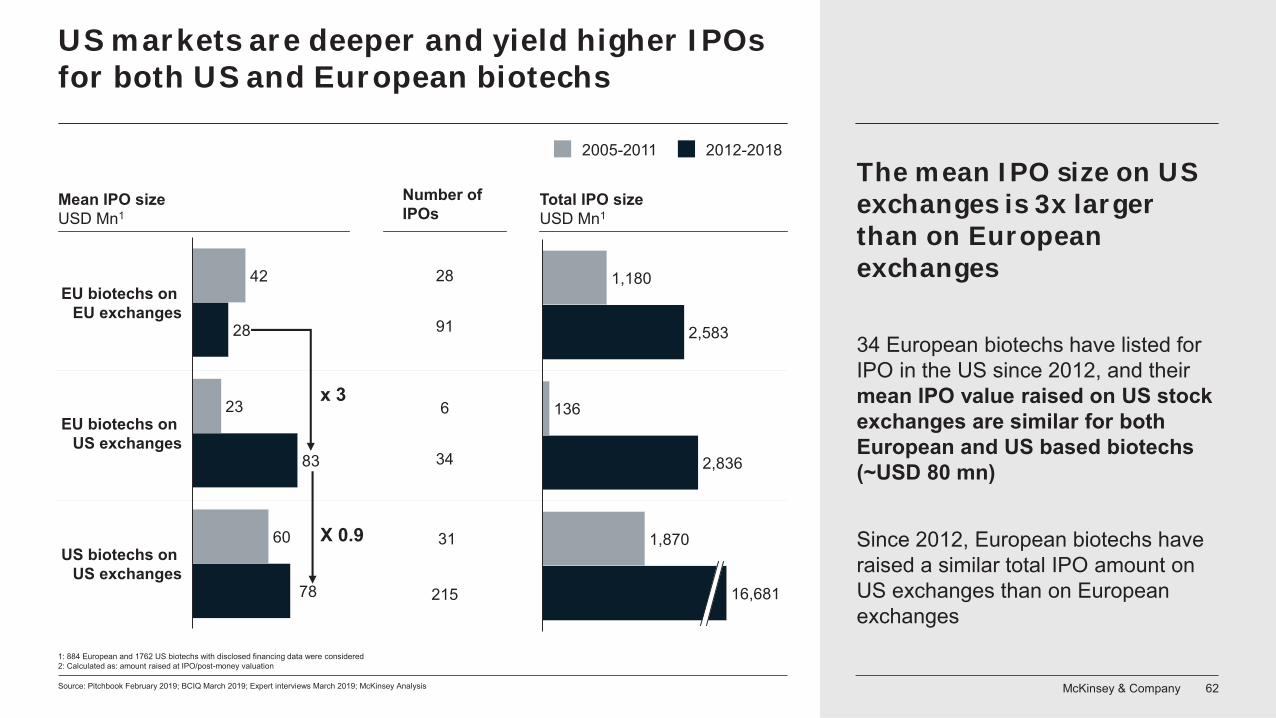

US markets are deeper and yield higher IPOs for both US and European biotechs

Source: Pitchbook February 2019; BCIQ March 2019; Expert interviews March 2019; McKinsey Analysis

EU biotechs on EU exchanges

23EU biotechs on

US exchanges

US biotechs on US exchanges

83

42

28

60

78

2005-2011 2012-2018

1: 884 European and 1762 US biotechs with disclosed financing data were considered2: Calculated as: amount raised at IPO/post-money valuation

1,870

2,583

1,180

136

2,836

16,681

Mean IPO size USD Mn1

Total IPO size USD Mn1

x 3

X 0.9

28

91

6

34

31

215

Number of IPOs

The mean IPO size on US exchanges is 3x larger than on European exchanges

34 European biotechs have listed for IPO in the US since 2012, and their mean IPO value raised on US stock exchanges are similar for both European and US based biotechs (~USD 80 mn)

Since 2012, European biotechs have raised a similar total IPO amount on US exchanges than on European exchanges

McKinsey & Company 63

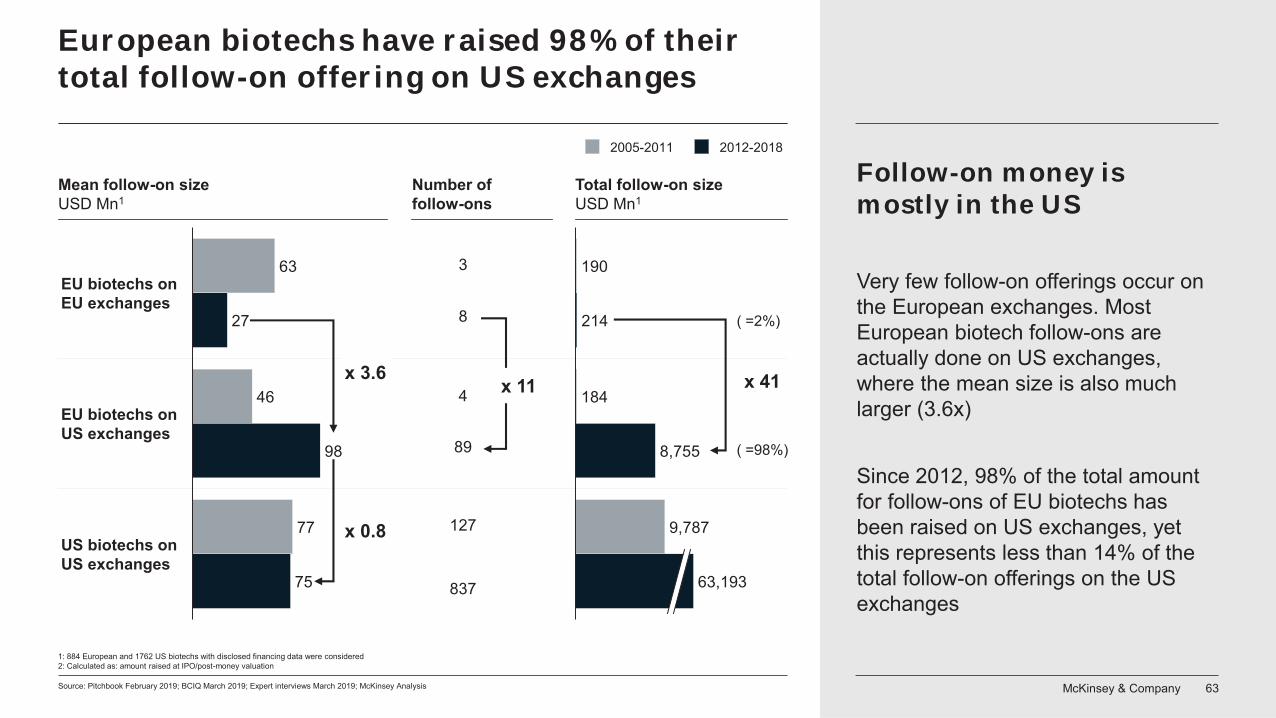

European biotechs have raised 98% of their total follow-on offering on US exchanges

Source: Pitchbook February 2019; BCIQ March 2019; Expert interviews March 2019; McKinsey Analysis

1: 884 European and 1762 US biotechs with disclosed financing data were considered2: Calculated as: amount raised at IPO/post-money valuation

EU biotechs on EU exchanges

98

US biotechs on US exchanges

EU biotechs on US exchanges

75

63

27

46

77

Mean follow-on size USD Mn1

2005-2011 2012-2018

9,787

184

214

8,755

190

63,193

Total follow-on size USD Mn1

Follow-on money is mostly in the US

Very few follow-on offerings occur on the European exchanges. Most European biotech follow-ons are actually done on US exchanges, where the mean size is also much larger (3.6x)

Since 2012, 98% of the total amount for follow-ons of EU biotechs has been raised on US exchanges, yet this represents less than 14% of the total follow-on offerings on the US exchanges

x 41

x 0.8

8

4

89

127

837

Number of follow-ons

3

x 11x 3.6

( =2%)

( =98%)

McKinsey & Company 64

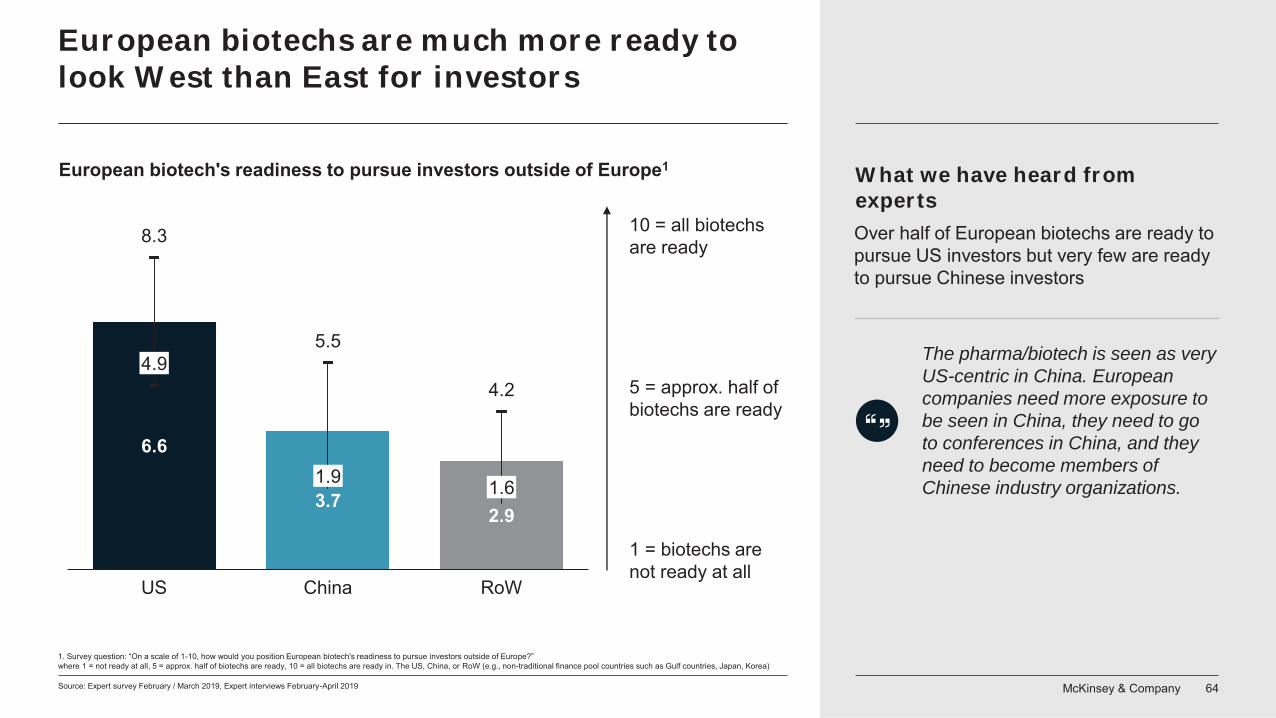

European biotechs are much more ready to look West than East for investors

Source: Expert survey February / March 2019, Expert interviews February-April 2019

1. Survey question: “On a scale of 1-10, how would you position European biotech's readiness to pursue investors outside of Europe?”where 1 = not ready at all, 5 = approx. half of biotechs are ready, 10 = all biotechs are ready in. The US, China, or RoW (e.g., non-traditional finance pool countries such as Gulf countries, Japan, Korea)

6.6

8.3

5.5

4.2

ChinaUS

4.9

1.93.7

2.91.6

RoW

10 = all biotechs are ready

5 = approx. half of biotechs are ready

1 = biotechs are not ready at all

What we have heard from experts

The pharma/biotech is seen as very US-centric in China. European companies need more exposure to be seen in China, they need to go to conferences in China, and they need to become members of Chinese industry organizations.

Over half of European biotechs are ready to pursue US investors but very few are ready to pursue Chinese investors

European biotech's readiness to pursue investors outside of Europe1

McKinsey & Company 65

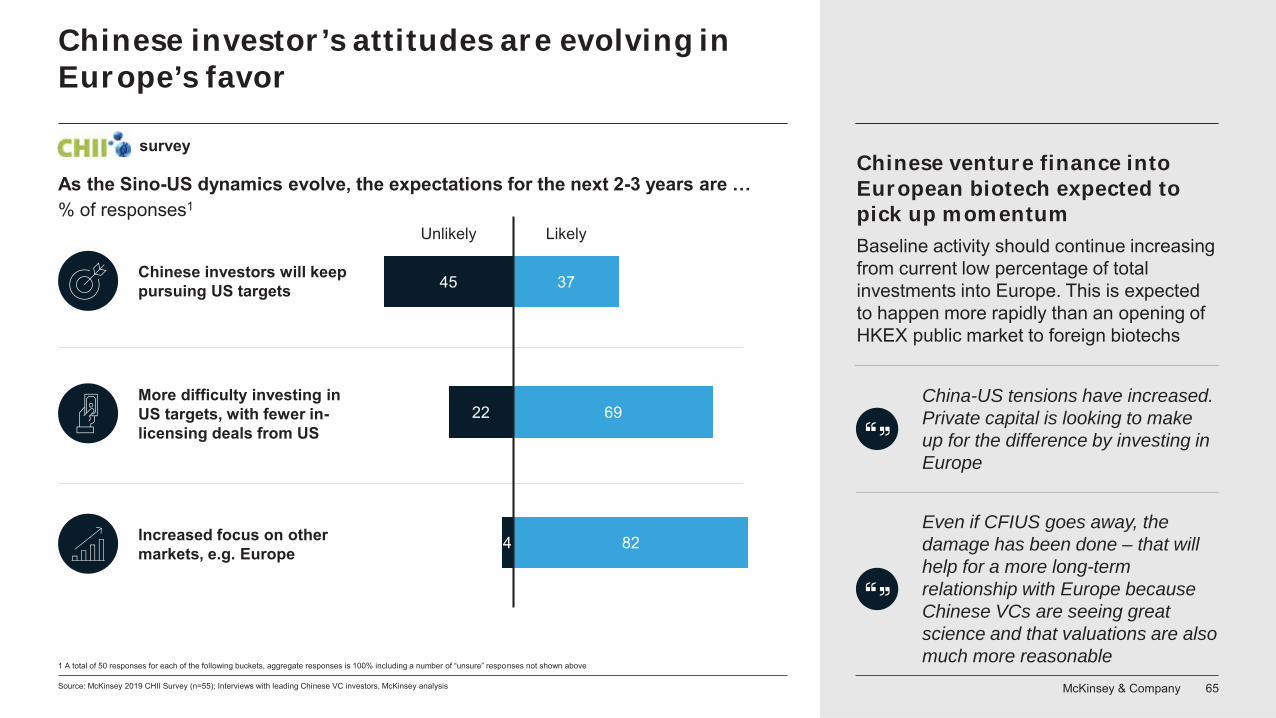

Chinese investor’s attitudes are evolving in Europe’s favor

1 A total of 50 responses for each of the following buckets, aggregate responses is 100% including a number of “unsure” responses not shown above

survey

As the Sino-US dynamics evolve, the expectations for the next 2-3 years are …% of responses1

China-US tensions have increased. Private capital is looking to make up for the difference by investing in Europe

Even if CFIUS goes away, the damage has been done – that will help for a more long-term relationship with Europe because Chinese VCs are seeing great science and that valuations are also much more reasonable

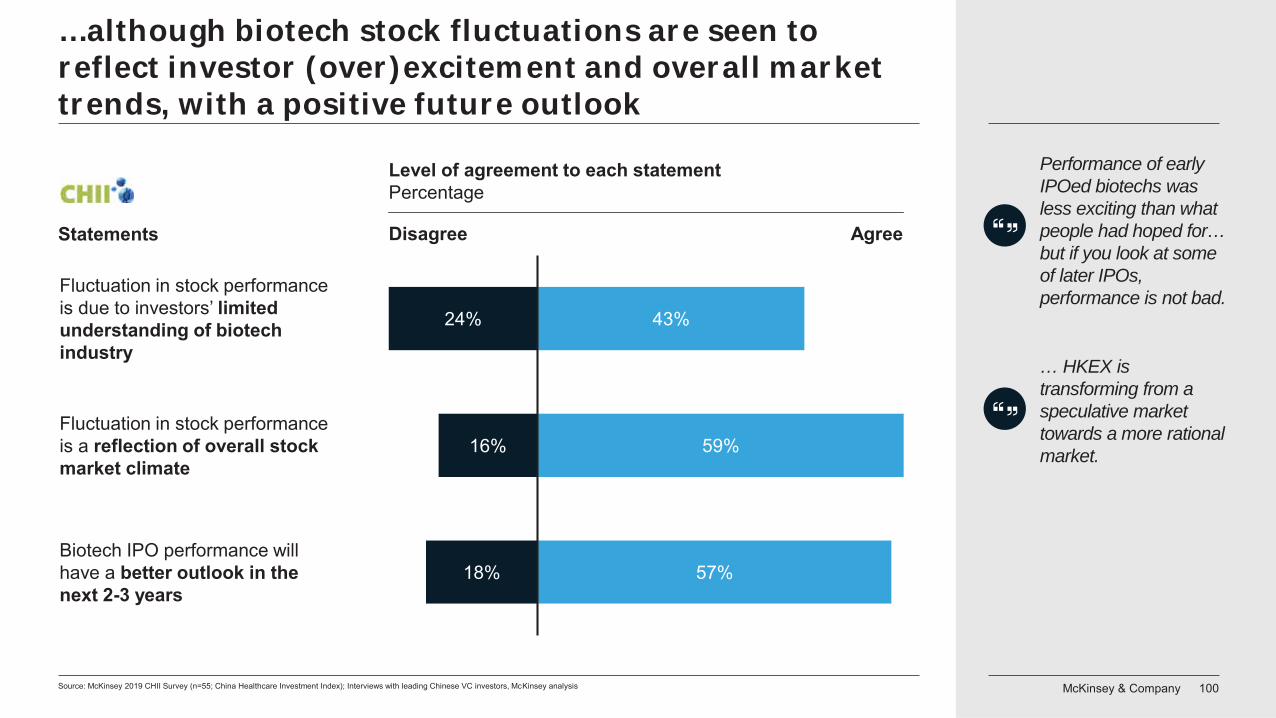

Chinese venture finance into European biotech expected to pick up momentumBaseline activity should continue increasing from current low percentage of total investments into Europe. This is expected to happen more rapidly than an opening of HKEX public market to foreign biotechs

Source: McKinsey 2019 CHII Survey (n=55); Interviews with leading Chinese VC investors, McKinsey analysis

Chinese investors will keep pursuing US targets

More difficulty investing in US targets, with fewer in-licensing deals from US

Increased focus on other markets, e.g. Europe

45

22

4

37

69

82

Unlikely Likely

McKinsey & Company 66

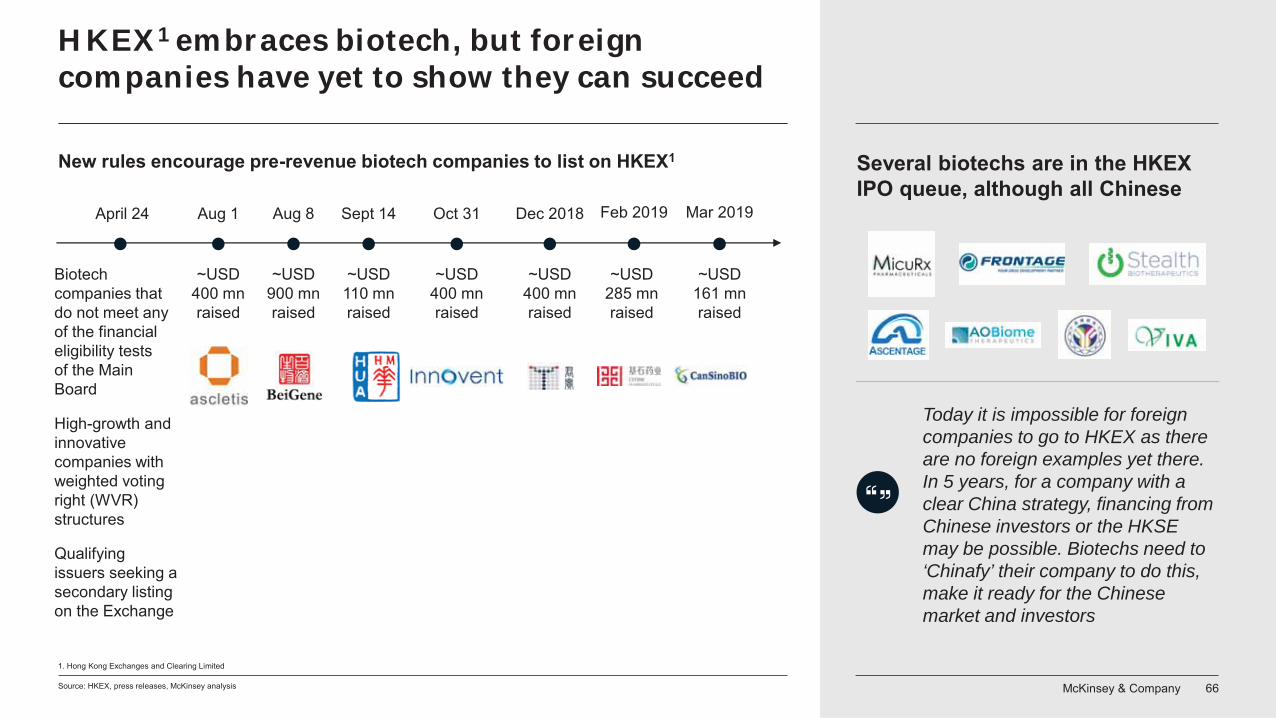

HKEX1 embraces biotech, but foreign companies have yet to show they can succeed

Source: HKEX, press releases, McKinsey analysis

1. Hong Kong Exchanges and Clearing Limited

New rules encourage pre-revenue biotech companies to list on HKEX1

Biotech companies that do not meet any of the financial eligibility tests of the Main Board

High-growth and innovative companies with weighted voting right (WVR) structures

Qualifying issuers seeking a secondary listing on the Exchange

April 24

~USD 400 mnraised

Dec 2018

~USD 285 mnraised

Feb 2019

~USD 161 mnraised

Mar 2019Aug 1

~USD 400 mnraised

Aug 8

~USD 900 mnraised

~USD 110 mnraised

Sept 14 Oct 31

~USD 400 mnraised

Today it is impossible for foreign companies to go to HKEX as there are no foreign examples yet there. In 5 years, for a company with a clear China strategy, financing from Chinese investors or the HKSE may be possible. Biotechs need to ‘Chinafy’ their company to do this, make it ready for the Chinese market and investors

Several biotechs are in the HKEX IPO queue, although all Chinese

McKinsey & Company 67

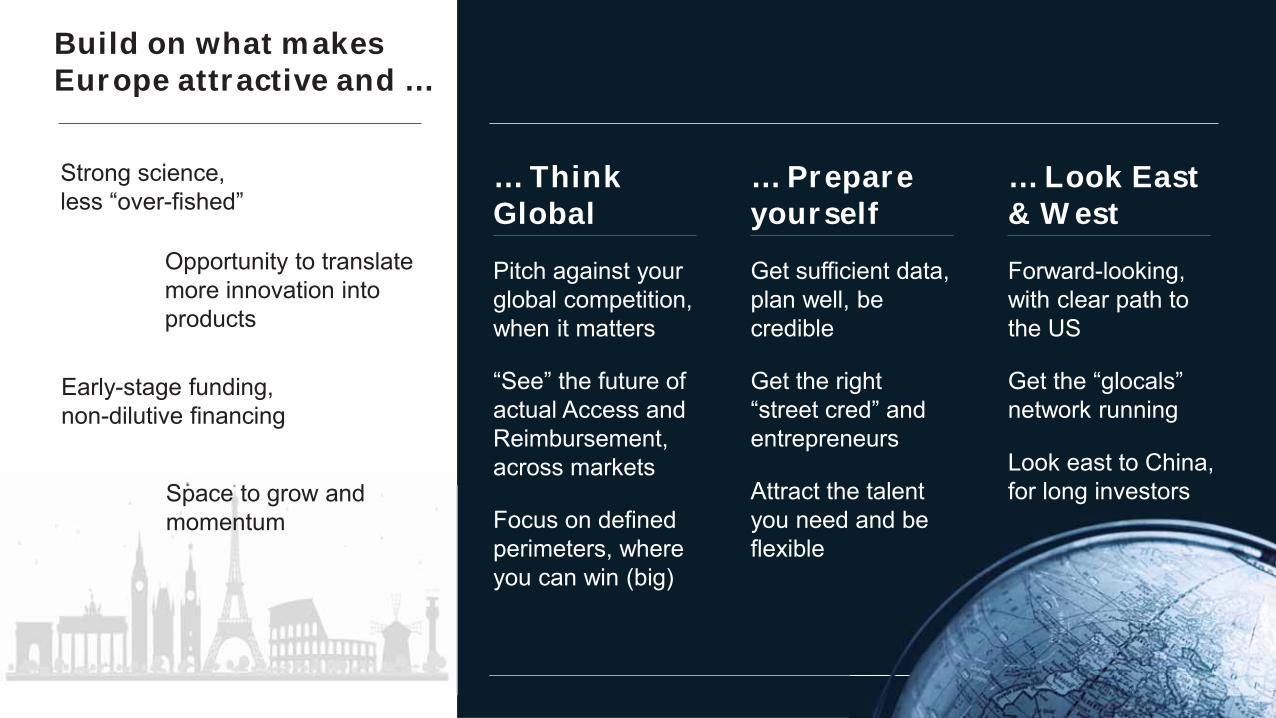

Looking forward: How can leaders and investors succeed?

A. Build your global competitiveness

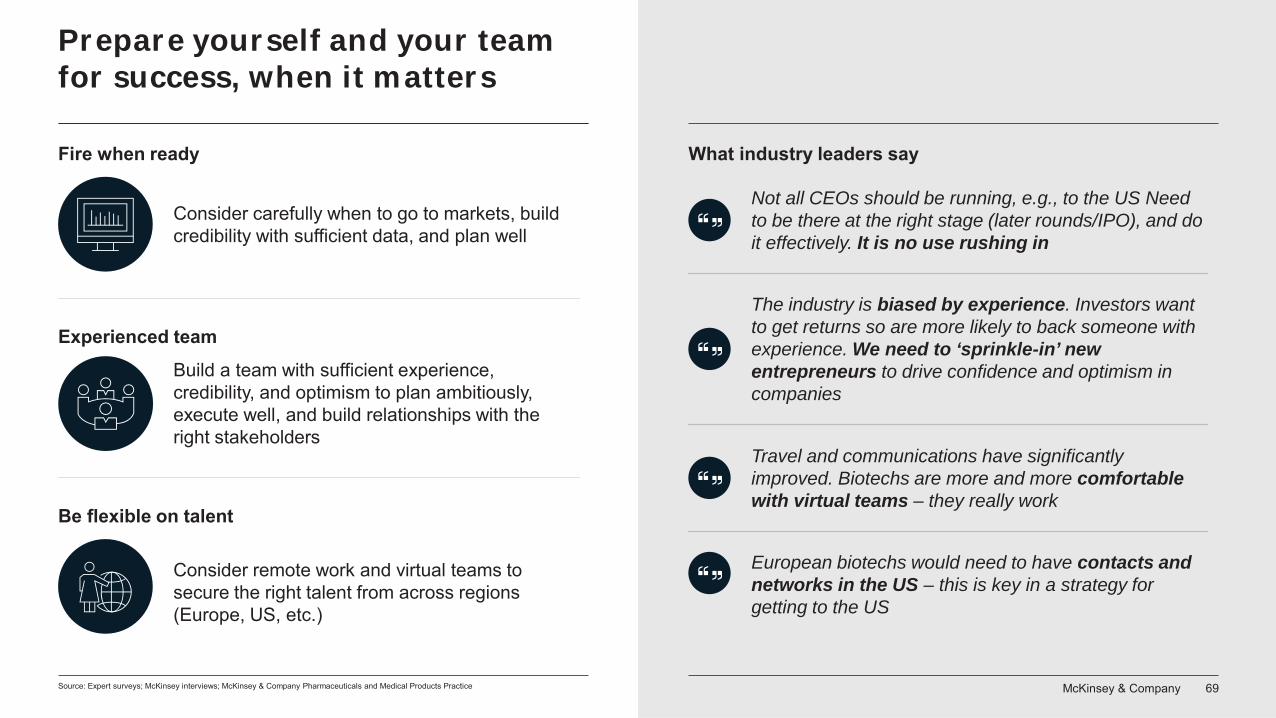

B. Prepare for success

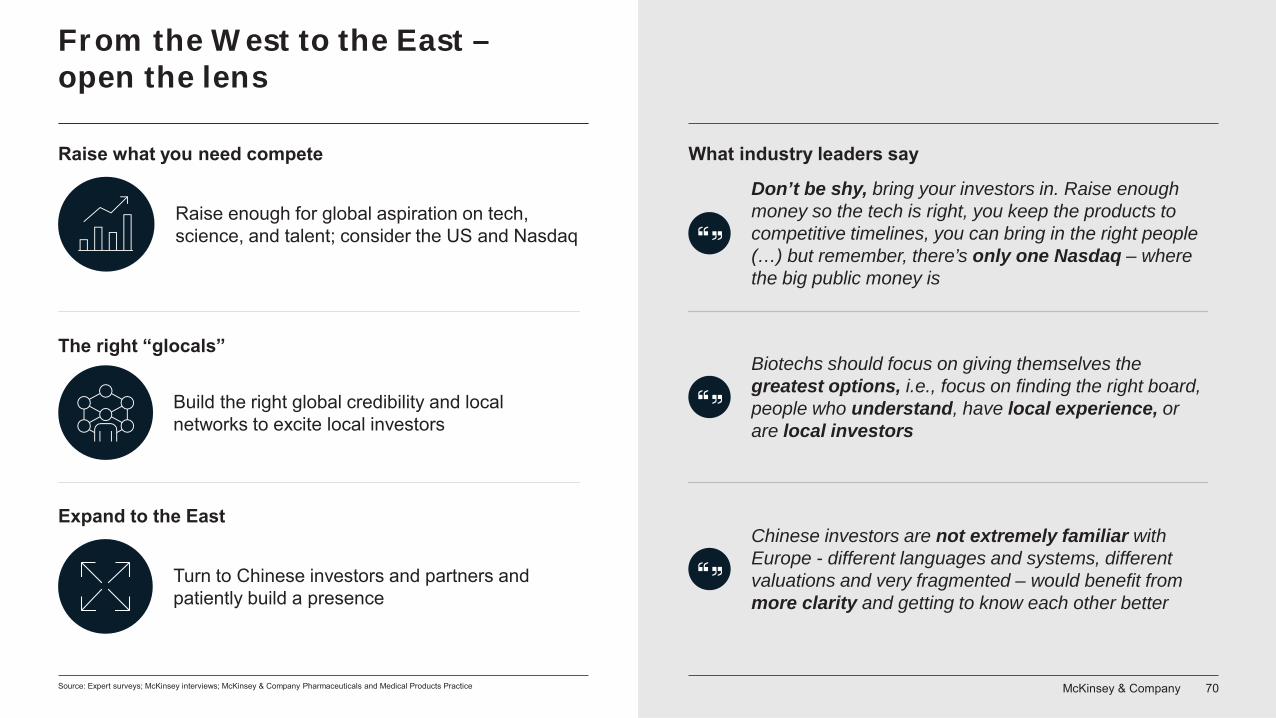

C. From East to West – open the lens

03

McKinsey & Company 68Source: Expert surveys; McKinsey interviews; McKinsey & Company Pharmaceuticals and Medical Products Practice

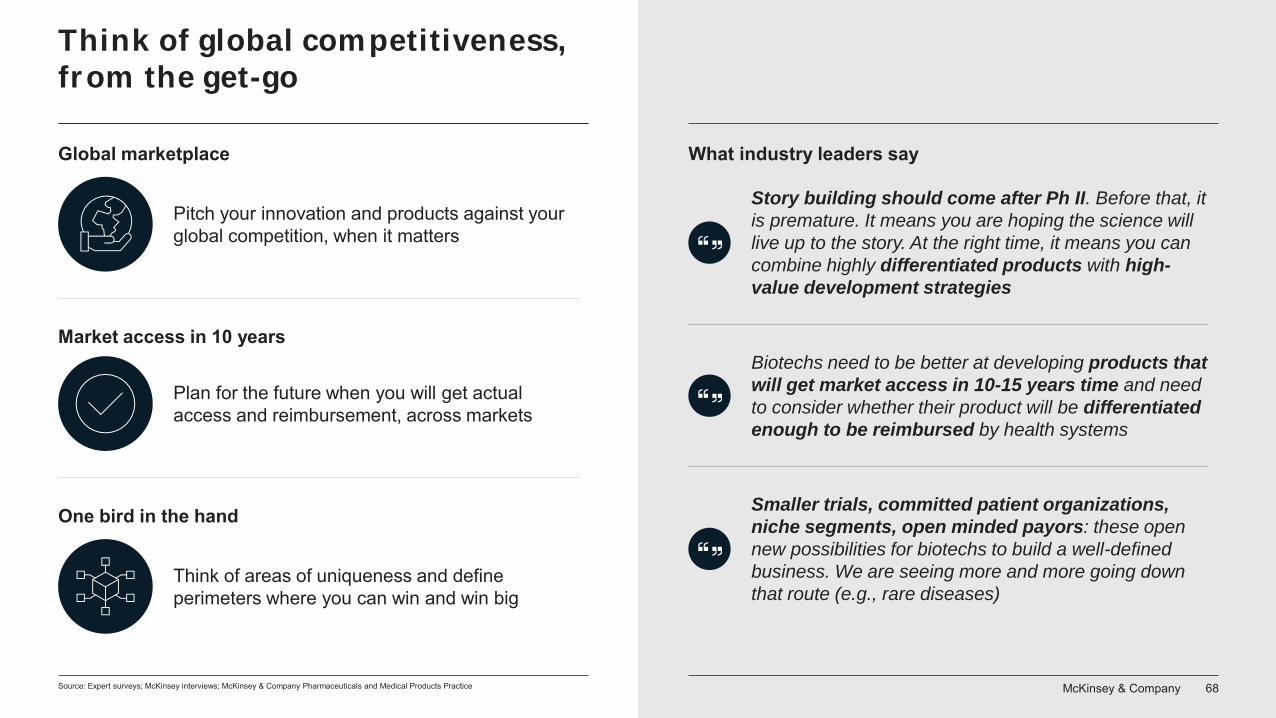

Think of global competitiveness, from the get-go

One bird in the hand

Global marketplace