European Union and No. IDBTN191 United States Biofuel Mandates

Biofuel Biofuel OutlookOutlook

Terrence Higgins

EIA: August 1, 2012

I: Global Overview

II: Focus on Americas

A. Brazilian Ethanol Supply

Outline

All rights reserved (2012)

B. U.S. Biofuel

1. RFS Requirements

2. Ethanol Limitations

3. Advanced Biofuel

Global Outlook

Africa:

Countries beginning

to set mandatesAsia Pacific:

High variance

in blend levels

Europe:

RED implementation, sustainability

and GHG savings

North America:

RFS2, LCFS, intermediate blends

Biofuel Mandates in 2012

Source: Hart Energy’s Global Biofuels Center, June 2012

Latin America: More

countries push for

mid- and higher

level ethanol blends Ethanol

Biodiesel

Ethanol & Biodiesel

Partial or No known biofuels program

Middle East:

Ethanol &

jatropha

R&D projects;

algae

Current Mandates in Asia

NORTHKOREA

JAPANSOUTHKOREA

CHINA

MONGOLIA

PAKISTAN

BHUTAN

BANGLADESHINDIA

Hong KongMacau

TaiwanNEPAL

E5 Nationwide

except selected

states

B2

B2

E10 in 10

provinces

E10, B2

Source: Hart Energy’s Global Biofuels Center, July 2012

SRILANKA

MALAYSIA

BRUNEI

CAMBODIA

THAILAND

VIETNAMLAOS

BURMA

PHILIPPINES

SINGAPORE

INDONESIA

Nationwide mandate

Partial mandate

E10 (or E5) available on market

ETBE - blended gasoline

Key:B5

E3, B2.5

B5

20

30

40

50

60

70

Billion Liters

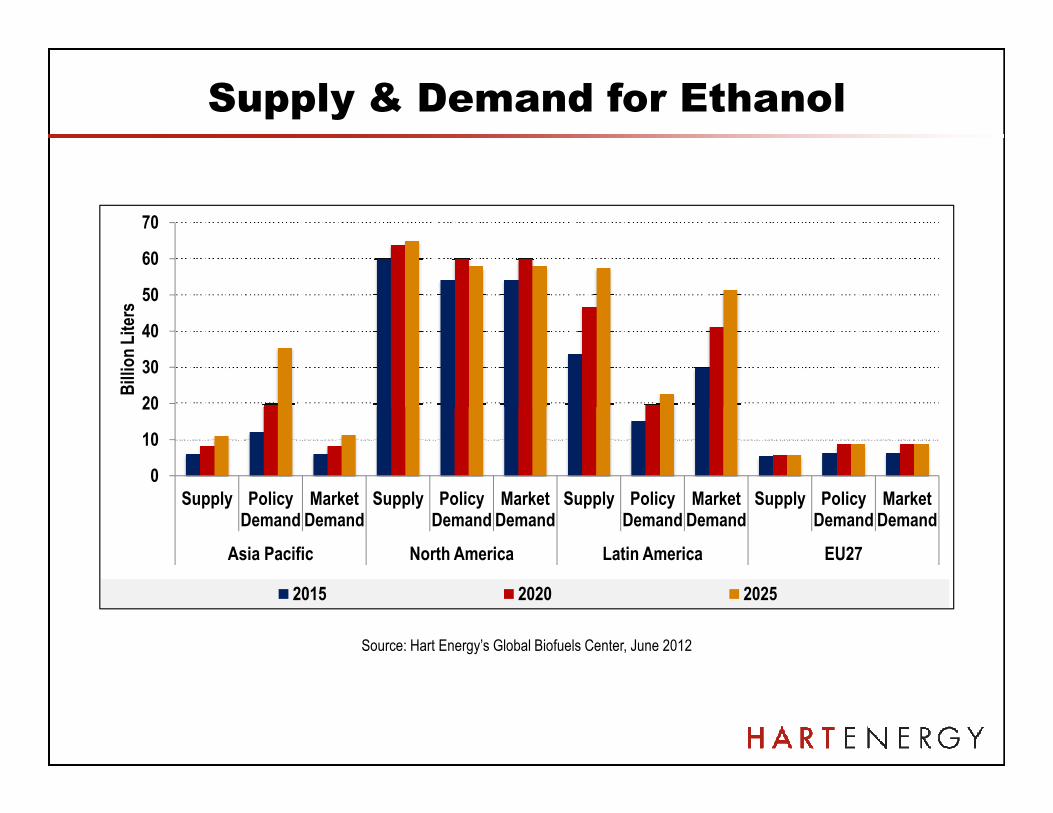

Supply & Demand for Ethanol

0

10

20

Supply Policy Demand

Market Demand

Supply Policy Demand

Market Demand

Supply Policy Demand

Market Demand

Supply Policy Demand

Market Demand

Asia Pacific North America Latin America EU27

2015 2020 2025

Source: Hart Energy’s Global Biofuels Center, June 2012

10

15

20

25

30

Billion Liters

Supply & Demand for Biodiesel

0

5

Supply Policy Demand

Market Demand

Supply Policy Demand

Market Demand

Supply Policy Demand

Market Demand

Supply Policy Demand

Market Demand

Asia Pacific North America Latin America EU27

2015 2020 2025

Source: Hart Energy’s Global Biofuels Center, June 2012

� Global biofuel will increase by 70% by 2020 and nearly double by

2025

� In 2020 88% of demand in North America, Latin America and Europe

U.S. and Brazil will account for ¾ of ethanol.

� Ethanol: Strongest growth from U.S. and Brazil

Global Trends

Biodiesel: Strongest growth from EU

� By 2020 biofuel potential to reach 7% of gasoline plus road diesel

demand

� Difficulty meeting far reaching program goals in EU and U.S.

� EU competition for Brazilian sugar cane ethanol

Focus on the Americas

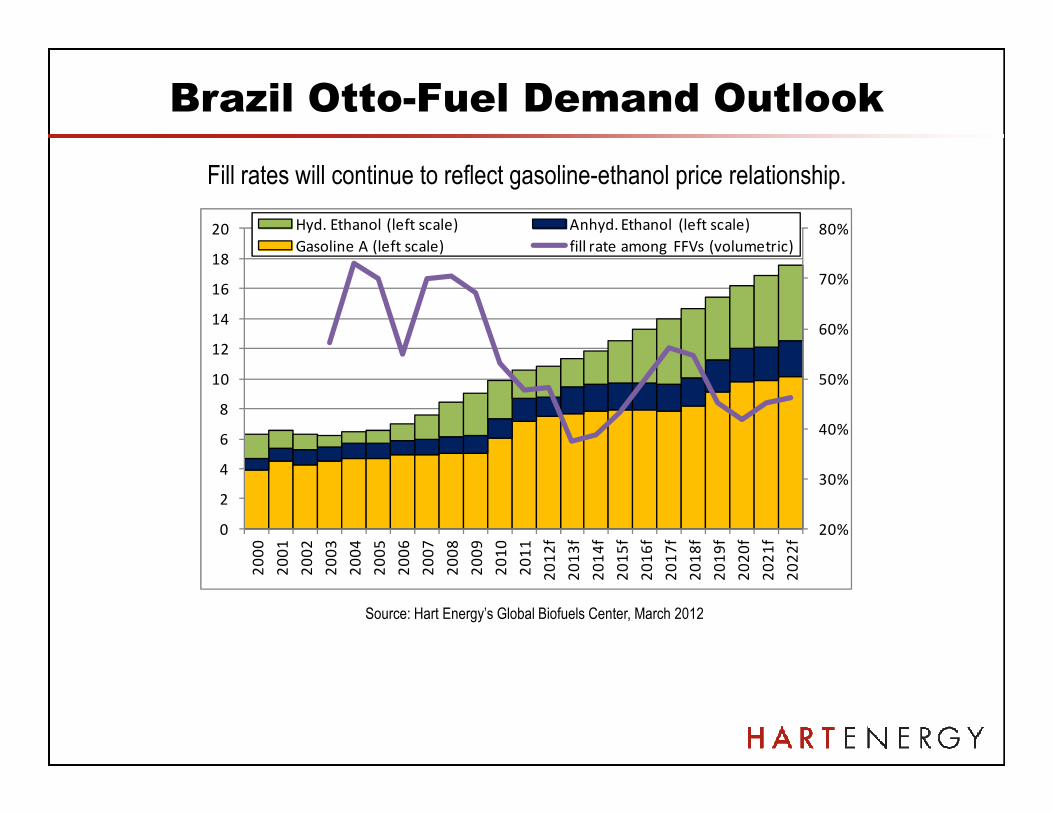

Brazil Otto-Fuel Demand Outlook

Fill rates will continue to reflect gasoline-ethanol price relationship.

50%

60%

70%

80%

8

10

12

14

16

18

20 Hyd. Ethanol (left scale) Anhyd. Ethanol (left scale)

Gasoline A (left scale) fill rate among FFVs (volumetric)

20%

30%

40%

0

2

4

6

8

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

f

20

13

f

20

14

f

20

15

f

20

16

f

20

17

f

20

18

f

20

19

f

20

20

f

20

21

f

20

22

f

Source: Hart Energy’s Global Biofuels Center, March 2012

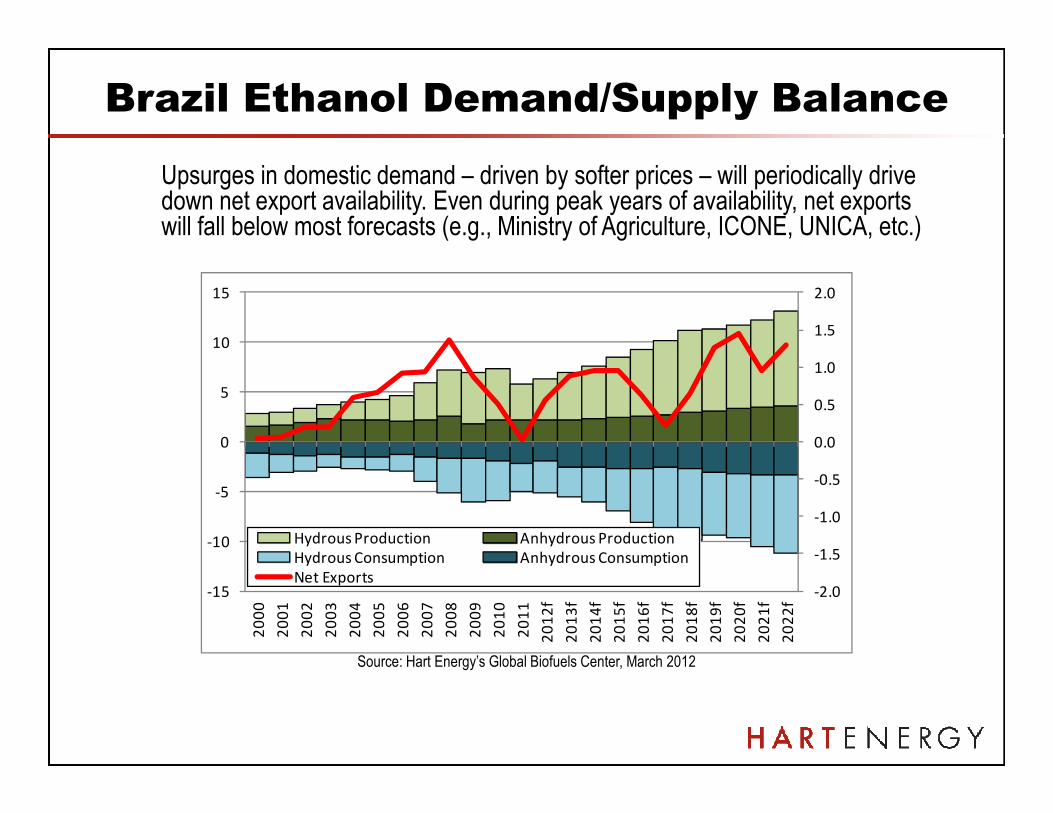

Brazil Ethanol Demand/Supply Balance

Upsurges in domestic demand – driven by softer prices – will periodically drive down net export availability. Even during peak years of availability, net exports will fall below most forecasts (e.g., Ministry of Agriculture, ICONE, UNICA, etc.)

0.5

1.0

1.5

2.0

5

10

15

-2.0

-1.5

-1.0

-0.5

0.0

0.5

-15

-10

-5

0

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

f

20

13

f

20

14

f

20

15

f

20

16

f

20

17

f

20

18

f

20

19

f

20

20

f

20

21

f

20

22

f

Hydrous Production Anhydrous Production

Hydrous Consumption Anhydrous Consumption

Net Exports

Source: Hart Energy’s Global Biofuels Center, March 2012

“RFS2” Program Requirements

15.0

20.0

25.0

30.0

35.0

40.0

Billions of Gallons

EPACT 2007

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Biomass-Based Diesel 0.5 0.7 0.8 1.0 1.0 1.0 1.0 1.0 1.0 1.0 1.0 1.0 1.0 1.0

Advanced Biofuels (Sugar) 0.1 0.2 0.3 0.5 0.8 1.0 1.5 2.0 2.5 3.0 3.5 3.5 3.5 4.0

Cellulosic Biofuels 0.1 0.25 0.5 1.0 1.8 3.0 4.25 5.5 7.0 8.5 10.5 13.5 16.0

Renewable Fuel (Corn Ethanol) 4.0 4.7 9.0 10.5 12.0 12.6 13.2 13.8 14.4 15.0 15.0 15.0 15.0 15.0 15.0 15.0 15.0

RFS1 Requirements 4.0 4.7 5.4 6.1 6.8 7.4 7.5 7.6 7.7 7.8 7.9 7.9 8.1 8.3 8.4 8.5 8.6

Total New RFS Requirement 4.0 4.7 9.0 11.1 13.0 14.0 15.2 16.6 18.2 20.5 22.3 24.0 26.0 28.0 30.0 33.0 36.0

0.0

5.0

10.0

Billions of Gallons

US Ethanol Blend Wall Scenario

E10

E15 (winter only)

2011 2012 2013 2014 2015 2022

* E15 used in Model Year 2001+

E15 (summer only)

2016 2017 2018 2019 2020 2021

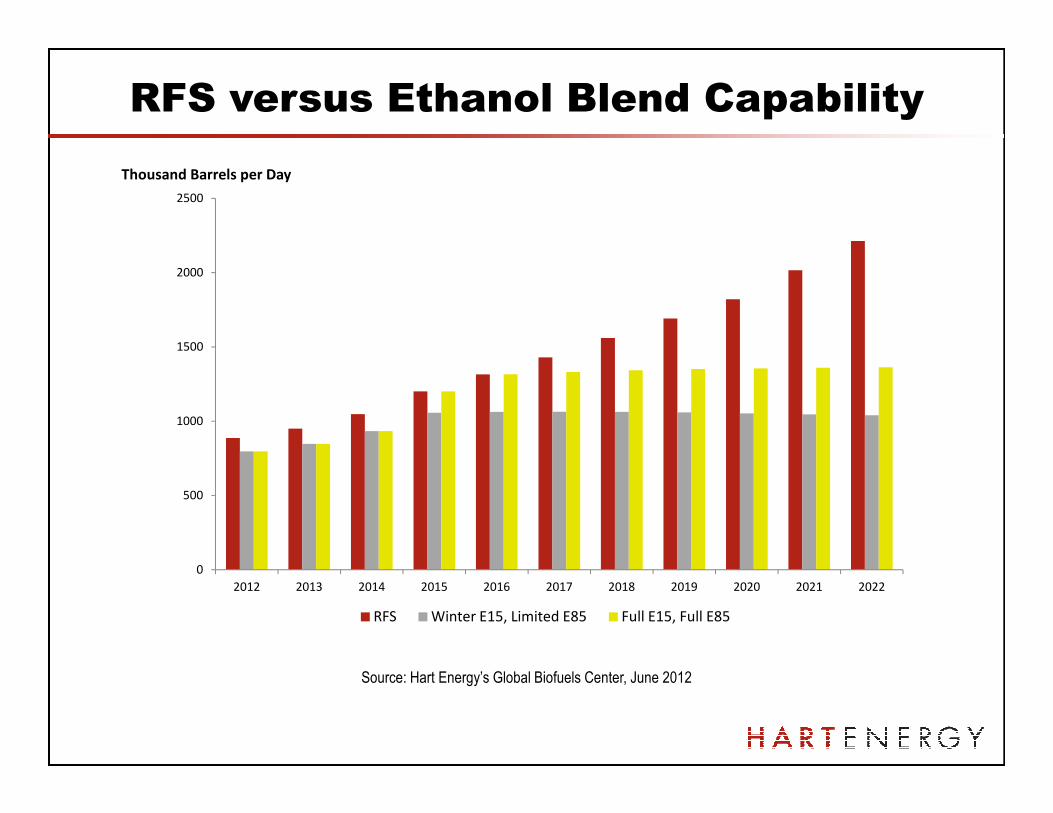

RFS versus Ethanol Blend Capability

1500

2000

2500

Thousand Barrels per Day

Source: Hart Energy’s Global Biofuels Center, June 2012

0

500

1000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

RFS Winter E15, Limited E85 Full E15, Full E85

25 operating next generation biofuels

pilot/demo plants in the U.S.

� 18 cellulosic ethanol plants with capacities ranging from 1,600 gallons per

year to 1.5 million gallons per year

� 5 FT or HVO renewable diesel plants: undisclosed to 0.07 gallons per year to

5 million gallons per year

Next Generation Operating Capacity

� 2 for biogasoline or biojet

2 operating commercial plants in the U.S.

� Gevo: 18 million gallons per year of butanol

� Dynamic Fuels: 18 million gallons per year of HVO renewable diesel

Projects with Cellulosic Feedstock

100

150

200

250

300

350

Million Gallons Per Year

Capacities of Operating and Proposed Projects with Cellulosic Feedstock

0

50

100

Operating 2012 Including Proposed

Million Gallons Per Year

Source: U.S. & Brazil Ethanol Outlook to 2022, April 2012

Biobutanol Cellulosic Ethanol

FT Liquids / Hydrocarbons, Jet fuel Hydrogenated vegetable oil / animal fat

Synthetic gasoline

� Continued growth from Brazil, but exports will fall below

expectations

� E10 blend wall concerns, E15 only limited solution

� E15 and higher blending constraints and limited E85 use will keep

ethanol below RFS requirements

� RFS faces fundamental challenges

Americas Biofuel Trends

� RFS faces fundamental challenges

� Blend wall

� Shortage of cellulosic biofuel

� Slow commercialization of advanced biofuel technologies

� Near term limits on sugarcane ethanol imports

� Changes to RFS2 likely

� Advanced biofuels costly and limited, but offer improved

opportunity for incremental biofuel introduction

� Drop in fuel advantages over ethanol

Outlook and Conclusions

� Drop in fuel advantages over ethanol

Thank You! / Questions?Terry Higgins, +1 703 .891.4815, [email protected]