Big Fish in a Small Pond: CEO Compensation, Corporate ...€¦ · Big Fish in a Small Pond: CEO...

38

Big Fish in a Small Pond: CEO Compensation, Corporate Governance, and Equilibrium Matching Zhan Li * September, 2016 Abstract We model a firm-CEO matching market in a cash flow diversion environment where mon- itoring CEOs is costly. In such market, positive assortative matching between firm size and CEO talent fails under negative economic shock; CEO compensation increases in CEO talent irrespective of how CEOs match with firms; corporate governance is affected by aggregate market characteristics such as CEO talent scarcity and equilibrium matching pattern. Our model explains why CEO turnover is driven by exogenous economic shock, and suggests a robustness rule for empirical applications based on PAM, as well as other empirical and policy implications. Keywords: CEO Compensation, Corporate Governance, Equilibrium Matching Pattern JEL Classification: G34, J33, D82 * This paper is based on my Ph.D. thesis. I am extremely grateful for the guidance and support from my thesis advisor Hector Chade. I am grateful for comments and help from Natalia Kovrijnykh and Galina Vereshchagina. I thank suggestions and comments from Alejandro Manelli, Tom Bates, Ilona Babenko, Yuri Tserlukevich, Andrei Kovrijnykh, Manish Pandey, Stefan Dodds, Soham Baksi, Wenbiao Cai and other seminar participants at Arizona State University, University of Winnipeg, and Greater China Area Finance Conference. All errors are mine . Address for correspondence: Zhan Li, Faculty of Business and Economics, University of Winnipeg, Office: 4BC09, Phone: 204.786.9833, Email: [email protected]. Website: http://zhan.li 1

Transcript of Big Fish in a Small Pond: CEO Compensation, Corporate ...€¦ · Big Fish in a Small Pond: CEO...

Big Fish in a Small Pond: CEO Compensation,Corporate Governance, and Equilibrium Matching

Zhan Li∗

September, 2016

Abstract

We model a firm-CEO matching market in a cash flow diversion environment where mon-

itoring CEOs is costly. In such market, positive assortative matching between firm size and

CEO talent fails under negative economic shock; CEO compensation increases in CEO talent

irrespective of how CEOs match with firms; corporate governance is affected by aggregate

market characteristics such as CEO talent scarcity and equilibrium matching pattern. Our

model explains why CEO turnover is driven by exogenous economic shock, and suggests a

robustness rule for empirical applications based on PAM, as well as other empirical and policy

implications.

Keywords: CEO Compensation, Corporate Governance, Equilibrium Matching Pattern

JEL Classification: G34, J33, D82

∗This paper is based on my Ph.D. thesis. I am extremely grateful for the guidance and support from my thesisadvisor Hector Chade. I am grateful for comments and help from Natalia Kovrijnykh and Galina Vereshchagina.I thank suggestions and comments from Alejandro Manelli, Tom Bates, Ilona Babenko, Yuri Tserlukevich, AndreiKovrijnykh, Manish Pandey, Stefan Dodds, Soham Baksi, Wenbiao Cai and other seminar participants at ArizonaState University, University of Winnipeg, and Greater China Area Finance Conference. All errors are mine . Addressfor correspondence: Zhan Li, Faculty of Business and Economics, University of Winnipeg, Office: 4BC09, Phone:204.786.9833, Email: [email protected]. Website: http://zhan.li

1

1 Introduction

CEO labor market plays an increasingly central role in allocating CEOs to firms. Understand-ing economic forces that affect such allocation process is thus important. Extant literature showsthat when there is complementarity between CEO talent and firm size (marginal product of CEOtalent is higher in a larger firm), competitive market allocates CEOs into firms according to posi-tive assortative matching (PAM): the largest firm matches with the most talented CEO, the secondlargest firm matches with the second most talented CEO, so on and so forth. Based on PAM,previous literature has obtained novel empirical results on CEO turnover, CEO compensation, andcorporate governance.

However, PAM, which serves as the foundation for the above research, merits a further exami-nation. Understandably, we can not expect PAM holds in the CEO labor market because it requiresa perfect monotonic relationship between firm size and CEO talent, which is apparently too strong.This paper considers a more general case: we ask to what extent can PAM hold and what can weknow about CEO turnover, compensation, and corporate governance when it fails.

To this end, we examine equilibrium matching pattern by embedding a cash flow diversionmodel into a two-sided matching market. In such market, firms have different size and CEOs havedifferent talent. There are two stages in our model. In the first stage, firms match with CEOssimultaneously by anticipating the second stage payoffs resulting from optimal contract. In thesecond stage, a matched pair of firm and CEO generate cash flow by a stochastic complementarytechnology: it is a product of firm size and CEO talent with some probability and zero otherwise.The distribution of the cash flow is exogenously given, known to all firms and CEOs, and affectedby an aggregate observable economic shock: the probability of zero cash flow is higher under anegative economic shock and lower under a positive economic shock. The realization of the cashflow is only known to the CEO, who submits a report to the firm. The CEO thus can divert thefirm’s cash flow by falsifying a report. The firm sets CEO compensation and pays a cost to auditthe CEO’s report to prevent her from diverting cash flow.

We show that despite of the complementarity between firm size and CEO talent, PAM failswhen negative economic shock is large or marginal cost of monitoring is high, and it fails firstamong small firms and low-talent CEOs. This generates three implications: first, PAM betweenfirm size and CEO talent is not a taken-as-granted result under complementary technology; second,since PAM is more likely to fail among smaller firms and their CEOs, it is more robust to use a

2

sample of large firms when PAM is assumed in empirical applications; third, PAM is also morerobust with recent data if marginal cost of monitoring is lower due to advancement in auditingtechnology.

The failure of PAM under negative economic shock is easy to understand by considering thetradeoff between higher CEO productivity and more expensive monitoring at a larger firm. Whena large firm competes against a small firm for a high talent CEO, the large firm has both advantageand disadvantage in such competition. The CEO has higher marginal product at the large firmdue to complementary production technology, thus the large firm tends to outbid the small firm.However, since cash flow subject to diversion is higher at the large firm, the large firm monitors theCEO more intensively, which increases its monitoring cost, and thus tends to underbid the smallfirm. Under negative economic shock, advantage of the large firm decreases because marginalproduct from CEO talent decreases faster in the large firm, and disadvantage increases becausemonitoring cost decreases slower at the large firm. When the negative economic shock is largeenough, PAM fails and the high talent CEO matches with the small firm, i.e., “big fish in a smallpond”.

The change in equilibrium matching pattern is equivalent to CEO turnover in our model. Ka-plan and Minton (2006) and Jenter and Kanaan (2015) show that CEOs are more likely to bedismissed after negative economic shock. However, if CEO turnover is determined by optimalcontract (Holmstrom, 1982; Gibbons and Murphy, 1990), observable economic shock, which isoutside of CEOs’ control, should be filtered out in firms’ decision on CEO dismissal. Our paperthus explains why economic shock can drive CEO turnover by considering how economic shockaffects firms’ ability in competing for CEO talent in a matching market. Eisfeldt and Kuhnen(2013) also consider CEO turnover in a matching market. Unlike our model, their paper abstractsaway agency problems and considers CEOs’ multidimensional types. CEO turnover in their pa-per is driven by firms’ demand for different types of talent under different economic conditions.Our paper thus complements Eisfeldt and Kuhnen (2013) in understanding CEO turnover in thematching market.

The second part of our paper discusses how the failure of PAM affects CEO compensationand corporate governance. For tractability, we treat different matching patterns as exogenous,which is only made possible if we have shown that matching patterns other than PAM can occurin equilibrium. Unlike previous literature on CEO compensation and corporate governance in thefirm-CEO matching market which relies on PAM, our solution applies to any matching pattern.

3

We show that irrespective of equilibrium matching pattern, CEO compensation satisfies mono-

tonicity and equal treatment. Monotonicity means CEO compensation is strictly increasing inCEO talent and equal treatment means CEOs of the same talent matching with firms of differentsize have the same compensation. This implies CEO compensation increases in firm size if andonly if CEO talent increases in firm size cross-sectionally, i.e., PAM holds.

The above result is important for empirical research from at least two aspects. First, sinceCEO compensation increases in CEO talent, the matching pattern between CEO compensationand firm size identifies the matching pattern between CEO talent and firm size. We can thusrecover market matching pattern from compensation data despite of the difficulty in measuringCEO talent. Second, it shows Gabaix and Landier (2008)’s predication that CEO compensationincreases in firm size cross-sectionally is true if and only if PAM holds. We know that PAM ismore likely to hold with a sample of large firms or more recent data. Thus Gabaix and Landier(2008)’s cross-sectional prediction is more robust with a sample of large firms or more recent data.This explains why Gabaix and Landier (2008) only include top 1000 firms in total market value intheir sample. 1 It also explains why Frydman and Saks (2010) cannot replicate Gabaix and Landier(2008)’s cross-sectional results for the sample period from 1936 to 1975: PAM may have failed inthat early sample period.

Next, we show that corporate governance is affected by aggregate market characteristics such asequilibrium matching pattern and the scarcity of CEO talent. Under PAM, larger firms have weakercorporate governance than smaller firms when CEO talent is scarce enough, and under negativeassortative matching (NAM), larger firms always have stronger corporate governance than smallerfirms. 2 This result is easy to understand by noting that compensation and corporate governanceare substitutes for a firm to incentivize its CEO for truthful reporting. Under NAM, larger firmsmatch with less talented CEOs, who have lower compensation than more talented CEOs, thuslarger firms impose stronger corporate governance than smaller firms. Under PAM, larger firmsmatch with more talented CEOs, and when scarcity of CEO talent drives CEO compensation up(due to competition for CEO talent), larger firms can incentivize their CEOs with weaker corporategovernance.

The above result holds even when it is costless to monitoring CEOs. This implies that the

1Gabaix and Landier (2008)’s sample choice is based on statistics. They resort to extreme value theory for com-puting CEO talent, which is only applicable to large firms.

2Negative assortative matching means the largest firm matches with the least talented CEO, the second largest firmmatches with the second least talented CEO, so on and so forth.

4

effectiveness of policies in enhancing corporate governance, by reducing monitoring cost suchas increasing board independence, is constrained by talent scarcity and market matching pattern.Thus it is impossible to impose a universally perfect corporate governance among all firms bygovernment regulations.

Our main contribution is that we show agency problem can affect how market allocates CEOs tofirms, by demonstrating that in a unidimensional matching framework, PAM between firm size andCEO talent is not a robust result when agency problem is present. Tervio (2008) and Gabaix andLandier (2008) establish PAM as the equilibrium matching pattern by assuming unidimensionaltype of CEOs and firms (talent and size) and symmetric information. Edmans and Gabaix (2011)show that PAM between firm size and talent is not robust when multidimensional type is consideredand the failure of PAM causes market inefficiency. Our paper differs from Edmans and Gabaix(2011) from two aspects: first, multidimensionality of types doesn’t drive matching pattern in ourpaper; second, our paper focuses on how matching pattern affects CEO turnover, compensation,and corporate governance instead of efficiency.

Our second contribution is that we provide a finer matching pattern than previous literatureby showing that when PAM fails, it may only fail on a subset of smaller firms and their CEOs.This contributes to the literature both methodologically and empirically. Methodologically, mostmatching literature only discusses two extreme matching patterns: PAM or NAM. And we fill thegap by showing that when PAM fails, it can exist for a subset of larger firms and more talentedCEOs. Our result establishes a qualitative criteria for empirical analysis: when PAM is assumed, asample of large firms generates a more robust result. This is important because empirical researchon CEO labor market often features a toy model to generate PAM, which might leave out importantdetails and generate PAM as the equilibrium when in fact it is not.

This paper proceeds as follows. Section 2 solves the model, and presents results on equilib-rium matching pattern and CEO turnover. Section 3 discusses CEO compensation and corporategovernance under different matching patterns. Section 4 discusses model implications. Section 5concludes.

2 Model

We consider a two sided matching market with firms of different size and CEOs of differenttalent. The set of firms is I and the set of CEOs is J, where I = J = [0,1]. A firm i ∈ I has sizes(i) ∈ R+ and s(i) is strictly increasing in i. A CEO j ∈ J has talent a( j) ∈ R+ and a( j) is strictly

5

increasing and differentiable in j. We call i the rank of the firm and j the rank of the CEO. Allfirms’ size and CEOs’ talent are observable, which is a standard assumption in matching literature.

There are two stages in our model. In the first stage, firms match with CEOs simultaneously.In the second stage, each matched firm-CEO pair engage in production. At the end of the secondstage, the firm will be liquidated and the proceeds from production will be divided between thefirm and the CEO. We call the first stage as matching stage and the second stage as productionstage.

Formally, a matching is a one to one mapping µ : I → J, where firm i ∈ I matches with CEOµ(i) ∈ J and CEO j ∈ J matches with firm µ−1( j) ∈ I. An equilibrium in the firm-CEO matchingmarket is given by a stable outcome: no firm or CEO will prefer to form a new pair by breakingcurrent match. We formally define equilibrium as follows:Definition 1. An equilibrium for the firm-CEO matching market consists of a matching functionµ : I → J, a firm profit function π : I → R+, and a CEO wage function w : J → R+ such that forany i, j ∈ [0,1]

i. Payoffs π(i),w( j) are feasible for j = µ(i)ii. There doesn’t exist a pair of payoffs π ′

(i),w′( j) such that π ′

(i) > π(i),w′( j) > w( j) and

j = µ(i)

Part i. states that the matching is feasible. Part ii. states that the matching is stable, whichrequires that any unmatched pair will not get a strictly higher payoffs by matching with each other.

When i = µ(i),∀i ∈ I, firms and CEOs of the same rank match with each other. We call suchmatching pattern as positive assortative matching (PAM). Apparently, PAM requires a positivemonotonic relationship between ranks of all firms and CEOs. When i= µ(1− i),∀i∈ I, the highestranked firm matches with the lowest ranked CEO, the second highest ranked firm matches withthe second lowest ranked CEO, so on and so forth. We call such matching pattern as negativeassortative matching (NAM), which requires a negative monotonic relationship between ranks ofall firms and CEOs.

We will start from the production stage and solve the optimal contract between a firm and itsCEO. Technically, we will solve the optimal contract by considering a costly state verificationproblem with binary state and random verification, which is a simplified version of Border andSobel (1987). Later, we embed this costly state verification model into the first stage matchingmodel and solve the equilibrium matching pattern.

6

2.1 Production Stage

In production stage, a firm with size s and a CEO with talent a engage in production. Both s anda are observable. Output is either qH = sa under high state “H” or qL = 0 under low state “L”.The probability of qH = sa is p, which is a measure of firm’s profitability and only affected byobservable economic shock: p increases under positive economic shock and high output is morelikely; p decreases under negative economic shock and high output is less likely.

Apparently, the firm’s expected output is psa, which shows that the (expected) marginal productof CEO talent is increasing in firm size, thus firm’s production technology exists complementarityin firm size and CEO talent. Intuitively, in a larger firm, the impact of CEO talent is larger and thusmarginal product of CEO talent is higher.

The distribution of output is known to both parties, but the realization is only observable tothe CEO. Upon observing the output, the CEO sends a report r ∈ {qH ,qL} and a payment equalto r to the firm. The firm monitors the CEO by committing to audit the report with probability gr

after receiving the CEO’s report r. The firm always finds out the true output once it audits.3 Whenthere is auditing, CEO compensation is wor, which depends on both the report r ∈ {qH ,qL} andthe audited output o ∈ {qH ,qL}; when there is no auditing, CEO compensation is wr, which onlydepends on her report. Apparently, when o = r, the CEO reports truthfully and there is no cashflow diversion. When o = r, the CEO falsifies a report, and diverted cash flow is the differencebetween the reported output and true output. The set of CEO compensation can be denoted as{wHH ,wH ,wHL,wLL,wL,wLH}.

The firm needs to pay an audit cost of kgr. Since auditing is the only way to monitor theCEO, we also call kgr as monitoring cost. The parameter k measures the marginal cost of auditing(monitoring). Auditing is costly for the firm for two reasons: the firm may need to setup a costlyinformation system to streamline the auditing process or the CEO imposes a penalty on the firm inthe event of auditing because of managerial entrenchment.

By revelation principle, we consider truth-telling equilibrium in which the CEO prefers tellingthe truth to falsifying the report. We consider the incentive compatibility condition when realizedoutput is qH = sa. If the CEO reports truthfully, CEO compensation is wH with probability 1−gH

when there is no auditing and wHH with probability gH when there is auditing. The expectedwage is thus (1− gH)wH + gHwHH . If the CEO submits a false report, there is no auditing with

3Equivalently, we can assume the firm always audits the CEO’s report and the probability of discovering true outputis gr.

7

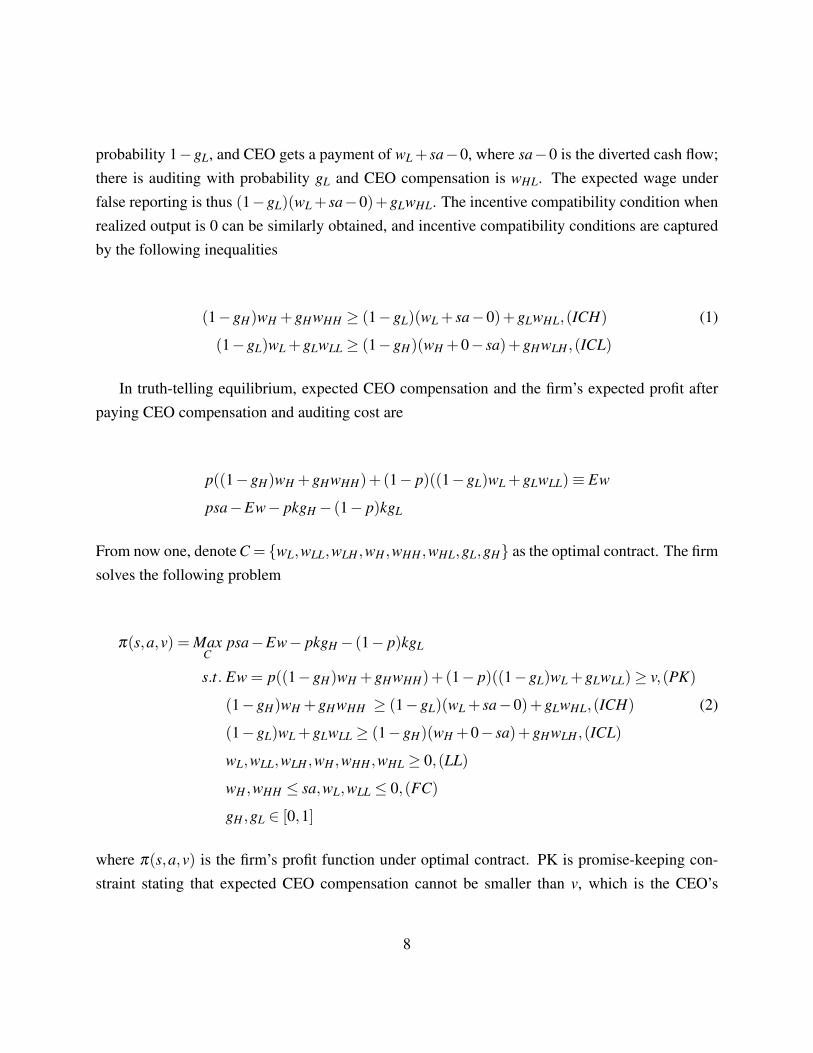

probability 1−gL, and CEO gets a payment of wL + sa−0, where sa−0 is the diverted cash flow;there is auditing with probability gL and CEO compensation is wHL. The expected wage underfalse reporting is thus (1−gL)(wL + sa−0)+gLwHL. The incentive compatibility condition whenrealized output is 0 can be similarly obtained, and incentive compatibility conditions are capturedby the following inequalities

(1−gH)wH +gHwHH ≥ (1−gL)(wL + sa−0)+gLwHL,(ICH) (1)

(1−gL)wL +gLwLL ≥ (1−gH)(wH +0− sa)+gHwLH ,(ICL)

In truth-telling equilibrium, expected CEO compensation and the firm’s expected profit afterpaying CEO compensation and auditing cost are

p((1−gH)wH +gHwHH)+(1− p)((1−gL)wL +gLwLL)≡ Ew

psa−Ew− pkgH − (1− p)kgL

From now one, denote C = {wL,wLL,wLH ,wH ,wHH ,wHL,gL,gH} as the optimal contract. The firmsolves the following problem

π(s,a,v) = MaxC

psa−Ew− pkgH − (1− p)kgL

s.t. Ew = p((1−gH)wH +gHwHH)+(1− p)((1−gL)wL +gLwLL)≥ v,(PK)

(1−gH)wH +gHwHH ≥ (1−gL)(wL + sa−0)+gLwHL,(ICH) (2)

(1−gL)wL +gLwLL ≥ (1−gH)(wH +0− sa)+gHwLH ,(ICL)

wL,wLL,wLH ,wH ,wHH ,wHL ≥ 0,(LL)

wH ,wHH ≤ sa,wL,wLL ≤ 0,(FC)

gH ,gL ∈ [0,1]

where π(s,a,v) is the firm’s profit function under optimal contract. PK is promise-keeping con-straint stating that expected CEO compensation cannot be smaller than v, which is the CEO’s

8

outside option. Limited liability constraint (LL) states that the firm cannot pay the CEO a strictlynegative wage. Feasibility constraint (LL) states that CEO compensation is smaller than the output.Optimal contract is given by the following proposition:

Proposition 1. At the optimal solution to the firm’s problem,

i. The firm pays CEO wH = vp ,wL = 0. Thus expected CEO compensation pwH +(1− p)wL is

equal to the CEO’s outside option v.

ii. The firm audits the CEO’s report with probabilities gL = 1− vpsa ,gH = 0. Thus both the

probabilities of auditing and monitoring cost (1− p)kgL + pkgH are increasing in firm size and

decreasing in expected CEO compensation.

Proposition 1 shows that auditing probabilities are state-dependent. By gL > gH = 0, the firmaudits the CEO with a strictly positive probability after receiving a report of low output and doesnot audit otherwise, intuitively, this is because the CEO can only divert cash flow by reporting alow output when the true output is high.

Substituting wH = vp into gL yields wH =(1−gL)sa. 1−gL can be considered as pay-performance

sensitivity (Jensen and Murphy, 1990), which measures change in CEO compensation associatedwith one dollar change in firm output. The optimal contract states that pay-performance sensitivityand CEO compensation decrease with monitoring, which is in accordance with recent empiricalevidence (e.g., Fahlenbrach (2009)).

It’s easy to understand why the auditing probability gL is strictly increasing in firm size s.Intuitively, there are more stakes on the table for appropriation at a larger firm, the firm thusmonitors the CEO with a higher probability of auditing to prevent her from diverting cash flow.gL is also strictly decreasing in expected CEO compensation v. This is because the firm can detercash flow diversion either by more intensive monitoring or a higher CEO compensation. The firmuse less intensive monitoring when CEO compensation is higher in order to save monitoring cost.4

This implies the following corollary:

Corollary 1. CEO compensation and monitoring are substitutes in preventing cash flow diversion

4The optimal contract shows that auditing probabilities are independent of the marginal cost of auditing k. Math-ematically, it is because optimal contract can be pinned down exactly by incentive compatibility and promise-keepingconstraint, which are both independent of k. However, we will show v is endogenously determined in matching equi-librium and a function of parameter k. Auditing probabilities are thus functions of k through their dependence onv.

9

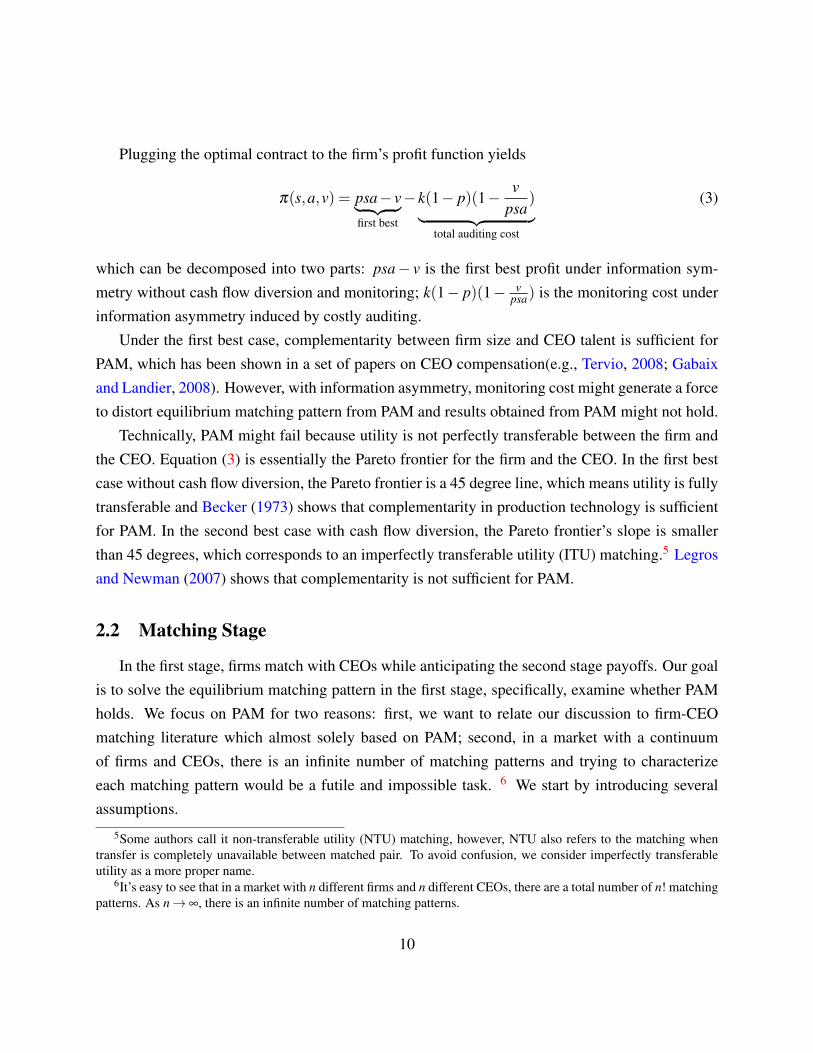

Plugging the optimal contract to the firm’s profit function yields

π(s,a,v) = psa− v︸ ︷︷ ︸first best

− k(1− p)(1− vpsa

)︸ ︷︷ ︸total auditing cost

(3)

which can be decomposed into two parts: psa− v is the first best profit under information sym-metry without cash flow diversion and monitoring; k(1− p)(1− v

psa) is the monitoring cost underinformation asymmetry induced by costly auditing.

Under the first best case, complementarity between firm size and CEO talent is sufficient forPAM, which has been shown in a set of papers on CEO compensation(e.g., Tervio, 2008; Gabaixand Landier, 2008). However, with information asymmetry, monitoring cost might generate a forceto distort equilibrium matching pattern from PAM and results obtained from PAM might not hold.

Technically, PAM might fail because utility is not perfectly transferable between the firm andthe CEO. Equation (3) is essentially the Pareto frontier for the firm and the CEO. In the first bestcase without cash flow diversion, the Pareto frontier is a 45 degree line, which means utility is fullytransferable and Becker (1973) shows that complementarity in production technology is sufficientfor PAM. In the second best case with cash flow diversion, the Pareto frontier’s slope is smallerthan 45 degrees, which corresponds to an imperfectly transferable utility (ITU) matching.5 Legrosand Newman (2007) shows that complementarity is not sufficient for PAM.

2.2 Matching Stage

In the first stage, firms match with CEOs while anticipating the second stage payoffs. Our goalis to solve the equilibrium matching pattern in the first stage, specifically, examine whether PAMholds. We focus on PAM for two reasons: first, we want to relate our discussion to firm-CEOmatching literature which almost solely based on PAM; second, in a market with a continuumof firms and CEOs, there is an infinite number of matching patterns and trying to characterizeeach matching pattern would be a futile and impossible task. 6 We start by introducing severalassumptions.

5Some authors call it non-transferable utility (NTU) matching, however, NTU also refers to the matching whentransfer is completely unavailable between matched pair. To avoid confusion, we consider imperfectly transferableutility as a more proper name.

6It’s easy to see that in a market with n different firms and n different CEOs, there are a total number of n! matchingpatterns. As n → ∞, there is an infinite number of matching patterns.

10

Assumption 1. All firms have the same marginal cost of auditing k.

There are two reasons for this simplification: first, this paper focuses on the effect of economicshock on equilibrium matching pattern. Adding heterogeneity in k will add another factor to affectequilibrium matching pattern which is not the focus of this paper and complicates intuition; sec-ond, firms will have two-dimensional types (s,k) if they have different size and marginal cost ofauditing. The model then turns into a multidimensional matching, on which little is known.7

Assumption 2. Firm profitability satisfies p > p = 1s0a0

k +1

Here s0 and a0 are the smallest firm’s size and the least talented CEO’s talent. The aboveassumption guarantees that p is large enough and k is small enough such that the smallest firm’sparticipation constraint can be satisfied even it matches with the least talented CEO. In fact, allfirms will prefer to match with any CEO than staying unmatched and all firms’ participation con-straints can be satisfied if Assumption 2 holds.8

We also assume all CEOs’ autarky payoffs are normalized to zero, which is a standard as-sumption in matching literature. Denote v0 as the least talented CEO’s compensation, we have thefollowing assumption:

Assumption 3. The least talented CEO is paid by her autarky payoff, thus v0 = 0

The above assumption vastly simplifies our analysis. The main results in this paper will quali-tatively be the same under a weaker assumption: the least talented CEO’s autarky payoff is strictlylarger than but not far away from zero. Assumption 3 is also in accordance with the empiricalliterature, which has shown that the lowest paid CEOs have much lower compensation than thehighest paid ones.

We now turn to examine how equilibrium matching pattern is affected by firms’ profitabilityp. We first show that in the CEO market with information frictions and monitoring cost, comple-mentarity between CEO talent and firm size is not sufficient for PAM, which fails when p is smallenough. We then obtain a finer equilibrium matching pattern by showing that even if PAM fails, itcan still be the equilibrium matching pattern for larger firms and more talented CEOs, by showingthat there exits a cutoff rank above which there is PAM and below which there is a failure of PAM.

7Edmans and Gabaix (2011) use a multidimensional matching model which cleverly converts several firm typesinto a single firm type, therefor, they are essentially dealing with a unidimensional matching model.

8A firm with size s has a profit of π(s,a,v) = (psa− (1− p)k)gL if it match with a CEO of talent a. The firmprefers to match with the CEO rather than stay unmatched if p > 1

sak +1 ,∀s,a, which can be satisfied if p > 1

s0a0k +1

.

11

Proposition 2. Denote p = 1s0a0

k +1and p = 1

s0a02k +1

i. There is positive assortative matching (PAM) between firm size and CEO talent among all

firms and CEOs if and only if p ≤ p ≤ 1ii. For p< p< p , there exists a cutoff rank i= {i : p= 1

s0ai2k +1

} such that PAM is the equilibrium

matching pattern between firms and CEOs with ranks higher than i, and PAM fails for firms and

CEO with ranks lower than i

Overall, Proposition 2 shows that equilibrium matching pattern is affected by firm profitabilityp, which is affected by economic shock. Part i. shows that PAM fails when firm profitability islower than a threshold. Part ii. shows that there is “PAM on top”: when PAM cannot hold for allfirms and CEOs, it will first fail for smaller firms and lower talented CEOs, but still hold for largerfirms and more talented CEOs above that cutoff rank.

The intuition is that firm size generates both advantage and disadvantage for the firm in com-peting for CEO talent due to the tradeoff between higher CEO productivity and more expensivemonitoring at a larger firm. The relative strength of such advantage and disadvantage is affectedby firm profitability p, which thus becomes the driving force of equilibrium matching pattern.

The advantage of size is induced by higher marginal product from CEO talent in a larger firmbecause of the complementary production technology. A larger firm thus tends to outbid a smallerfirm for CEO talent due to higher matching surplus. The disadvantage of size results from moreintensive monitoring at a larger firm because there are more stakes on the table for the CEO toappropriate. A larger firm thus tends to underbid a smaller firm for CEO talent due to highermonitoring cost. As firm profitability p decreases, a larger firm’s advantage decreases becausemarginal product from CEO talent decreases faster in a larger firm; its disadvantage increasesbecause monitoring cost decreases slower at a larger firm when both firms impose less monitoring,as there are fewer stakes on the table for appropriation when profitability p decreases. When p

is small enough, disadvantage outweighs advantage, a larger firm underbids a smaller firm, and asmaller firm matches with a more talented CEO.

For smaller firms, p tends to have larger effect in shaping matching pattern because smallerfirms are more sensitive to changes in p. Thus when PAM fails, it fail first between smaller firmsand their CEOs, which is the “PAM on top” result shown in Part ii.

There are two more things worth pointing out. First, when p = 1s0a0

2k +1, there might exist other

matching patterns which are not PAM but generate the same firm profit and CEO compensation asPAM, i.e., are pay-off equivalent to PAM (Legros and Newman, 2007). Second, the cutoff value

12

1s0a0

2k +1is distribution-free and unrelated to size of firms and talent of CEOs other than the bottom

firm and CEO.Next, we show how the marginal cost of monitoring k affects equilibrium matching pattern.

From Proposition 2, both p and i increase when the marginal cost of monitoring increases. ByProposition 2, as p grows larger, PAM is less likely for all firms and CEOs, and as i grows larger,there are fewer firms and CEOs on which PAM holds. The comparative statics result below isobvious.

Proposition 3. (Comparative Statics) When the marginal cost of monitoring k increases, PAM is

less likely. Or formally, p and i are strictly increasing in k

The intuition still relies on the understanding that size brings both advantage and disadvantageto a firm due to the tradeoff between higher CEO productivity and more expensive monitoringat a larger firm. As we have shown, the advantage of a larger firm is that it has higher marginalproduct from CEO talent, which generates higher matching surplus and the firm tends to outbid asmaller firm for CEO talent; the disadvantage of a larger firm is that it has larger monitoring cost,which reduces matching surplus and the firm tends to underbid a smaller firm. As the marginalcost of monitoring k increases, a larger firm’s advantage remains the same, since it is a resultof production technology, however, its disadvantage increases. And when k is large enough, thedisadvantage outweighs the advantage, a larger firm underbids a smaller firm, PAM will eventuallyfail.

2.3 CEO Turnover

Empirical research has shown that CEO turnover is affected by observable economic and industryshock (e.g., Kaplan and Minton 2006; Jenter and Kanaan 2015). This is a puzzling result be-cause observable shock is outside of CEOs’ control and should be filtered out in firms’ decision ofretaining or firing CEOs, thus should not affect CEO turnover.

Our result on equilibrium matching pattern provides an explanation to the above finding onCEO turnover. Proposition 2 shows that economic shock can change equilibrium matching pat-tern through its effect on firm profitability p. When equilibrium matching pattern changes, thereare firms and CEOs breaking their current match and rematching with each other. Thus in ourmodel, CEO turnover is equivalent to a change in equilibrium matching pattern. Proposition 2 thusexplains why CEO turnover is affected by economic shock.

13

To further understand how economic shock affects CEO turnover, we consider two specialcases. The first is negative economic shock under PAM and positive economic shock when PAMfails. The second is a small market with two firms and two CEOs. For the first case, the followingcorollary characterizes the relationship between CEO turnover and economic shock:

Corollary 2. (CEO Turnover) Assume p < p1 < p ≤ p2 ≤ 1 and denote i = {i : p1 =1

s0ai2k +1

}i. When profitability decreases from p2 to p1 under a negative economic shock, CEO turnover

only happens among firms and CEOs with ranks lower than i, where less talented CEOs match

with larger firms and more talented CEOs match with smaller firms.

ii. When profitability increases from p1 to p2 under a positive economic shock, CEO turnover

only happens among firms and CEOs with ranks lower than i and more talented CEOs match with

larger firms and less talented CEOs match with smaller firms.

The above corollary shows that CEO turnover is more frequent among smaller firms or wheneconomy is more volatile with more economic shocks. Note that CEO turnover in our model is notdriven by firms’ updated belief of CEO talent from performance signals (Hermalin and Weisbach,1998) or firms’ demand for different types of CEO talent upon economic shock( Eisfeldt and Kuh-nen, 2013). Thus the above result is obtained without resorting to firms’ incomplete informationon CEO talent or the multiple dimensional nature of CEO talent.

Now we consider the second case: a small market with only two firms and two CEOs. Wedenote firm size as s0 and s1 with s0 < s1 and CEO talent as a0 and a1 with a0 < a1. Thus firm 1is the large firm and CEO 1 is the high talent CEO. Apparently, in such market there are only twoequilibrium matching patterns: either firm 1 matches with CEO 1 and firm 0 matches with CEO0 or firm 1 matches with CEO 0 and firm 0 matches with CEO 1. We denote the former as “1-1,0-0” matching and the latter as “1-0, 0-1” matching. CEO turnover is induced by change between“1-1, 0-0” and “1-0, 0-1” matching.

Both firms are competing for the high talent CEO by submitting bids to her and the firm witha higher bid will match with her. This corresponds to a scenario where firms compete for a CEOby sending out wage offers, and the CEO chooses to work for the firm with the highest wage offer.For firm i ∈ {0,1}, denote its maximum bid for CEO 1 as bi, then bi can be solved from

π(si,a1,bi)≥ π(si,a0,0) (4)

i.e., maximum bid is the wage paid to CEO 1 when firm i is indifferent from matching with her

14

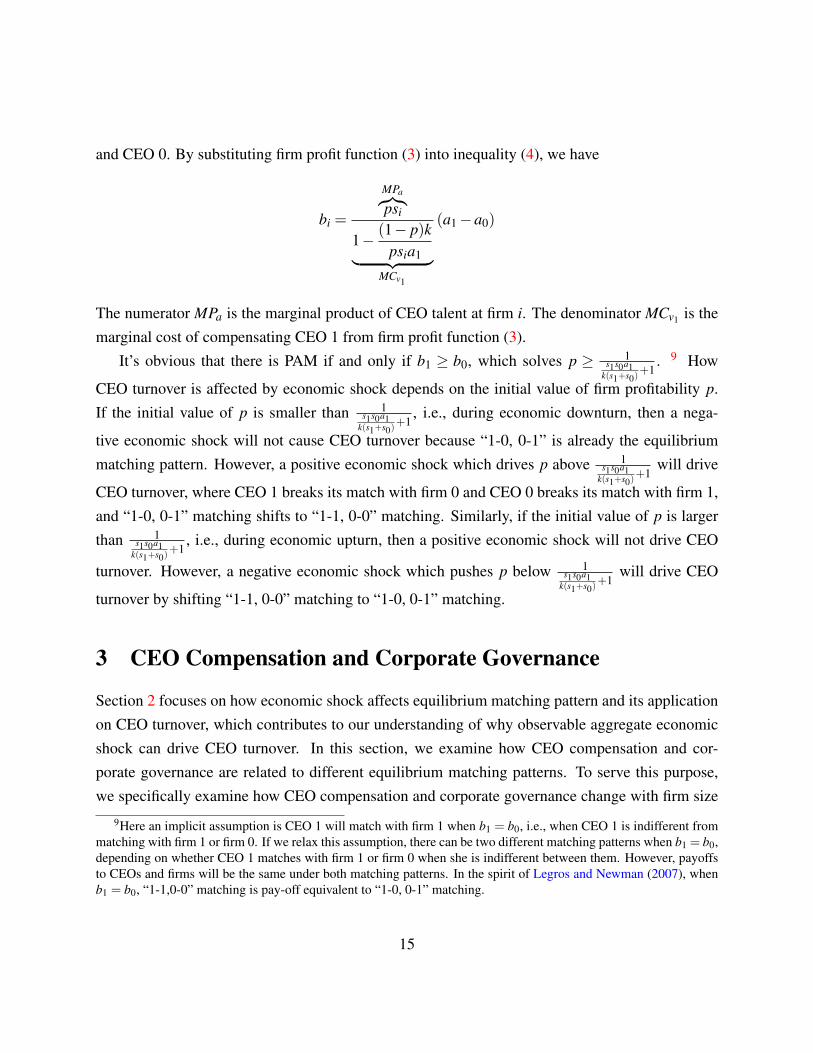

and CEO 0. By substituting firm profit function (3) into inequality (4), we have

bi =

MPa︷︸︸︷psi

1− (1− p)kpsia1︸ ︷︷ ︸

MCv1

(a1 −a0)

The numerator MPa is the marginal product of CEO talent at firm i. The denominator MCv1 is themarginal cost of compensating CEO 1 from firm profit function (3).

It’s obvious that there is PAM if and only if b1 ≥ b0, which solves p ≥ 1s1s0a1

k(s1+s0)+1

. 9 How

CEO turnover is affected by economic shock depends on the initial value of firm profitability p.If the initial value of p is smaller than 1

s1s0a1k(s1+s0)

+1, i.e., during economic downturn, then a nega-

tive economic shock will not cause CEO turnover because “1-0, 0-1” is already the equilibriummatching pattern. However, a positive economic shock which drives p above 1

s1s0a1k(s1+s0)

+1will drive

CEO turnover, where CEO 1 breaks its match with firm 0 and CEO 0 breaks its match with firm 1,and “1-0, 0-1” matching shifts to “1-1, 0-0” matching. Similarly, if the initial value of p is largerthan 1

s1s0a1k(s1+s0)

+1, i.e., during economic upturn, then a positive economic shock will not drive CEO

turnover. However, a negative economic shock which pushes p below 1s1s0a1

k(s1+s0)+1

will drive CEO

turnover by shifting “1-1, 0-0” matching to “1-0, 0-1” matching.

3 CEO Compensation and Corporate Governance

Section 2 focuses on how economic shock affects equilibrium matching pattern and its applicationon CEO turnover, which contributes to our understanding of why observable aggregate economicshock can drive CEO turnover. In this section, we examine how CEO compensation and cor-porate governance are related to different equilibrium matching patterns. To serve this purpose,we specifically examine how CEO compensation and corporate governance change with firm size

9Here an implicit assumption is CEO 1 will match with firm 1 when b1 = b0, i.e., when CEO 1 is indifferent frommatching with firm 1 or firm 0. If we relax this assumption, there can be two different matching patterns when b1 = b0,depending on whether CEO 1 matches with firm 1 or firm 0 when she is indifferent between them. However, payoffsto CEOs and firms will be the same under both matching patterns. In the spirit of Legros and Newman (2007), whenb1 = b0, “1-1,0-0” matching is pay-off equivalent to “1-0, 0-1” matching.

15

cross-sectionally in the CEO market.To simplify our discussion, we take different equilibrium matching patterns as exogenously

given. It’s worth noting that we can assume this because we have shown equilibrium matchingpattern other than PAM can emerge. In this regard, Section 2 provides a theoretical premise forour discussion on CEO compensation and corporate governance.

3.1 CEO Compensation

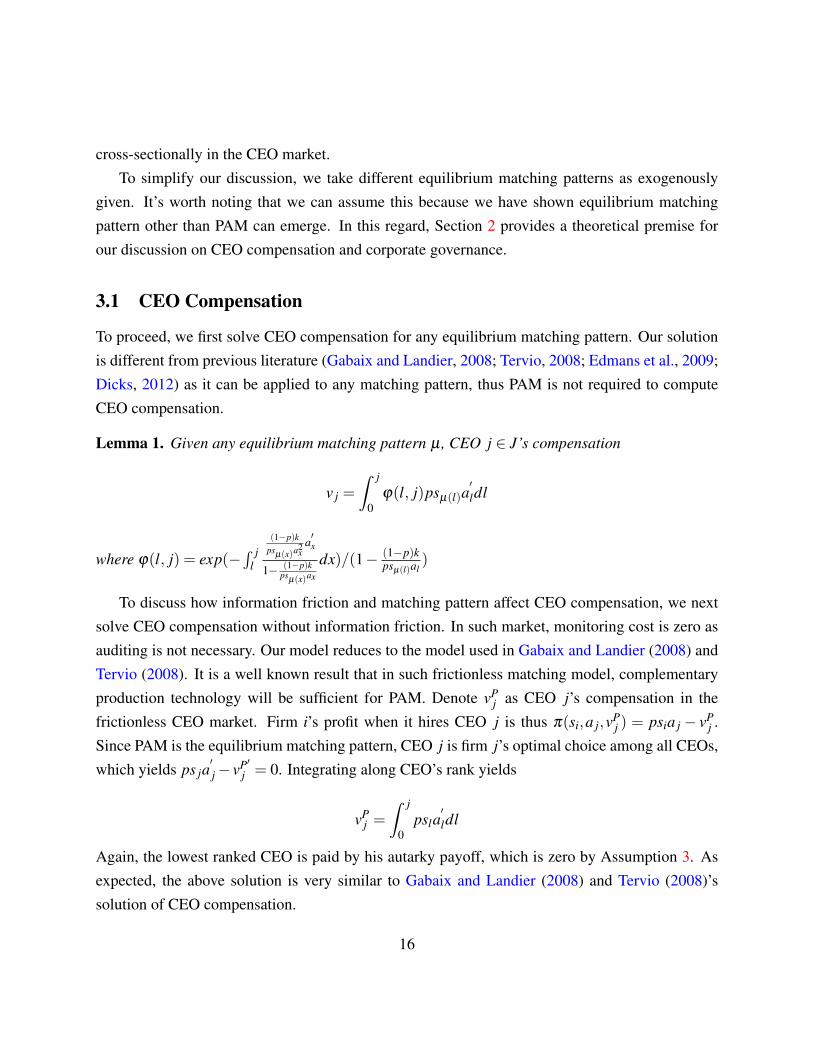

To proceed, we first solve CEO compensation for any equilibrium matching pattern. Our solutionis different from previous literature (Gabaix and Landier, 2008; Tervio, 2008; Edmans et al., 2009;Dicks, 2012) as it can be applied to any matching pattern, thus PAM is not required to computeCEO compensation.

Lemma 1. Given any equilibrium matching pattern µ , CEO j ∈ J’s compensation

v j =

ˆ j

0φ(l, j)psµ(l)a

′ldl

where φ(l, j) = exp(−´ j

l

(1−p)kpsµ(x)a2x

a′x

1− (1−p)kpsµ(x)ax

dx)/(1− (1−p)kpsµ(l)al

)

To discuss how information friction and matching pattern affect CEO compensation, we nextsolve CEO compensation without information friction. In such market, monitoring cost is zero asauditing is not necessary. Our model reduces to the model used in Gabaix and Landier (2008) andTervio (2008). It is a well known result that in such frictionless matching model, complementaryproduction technology will be sufficient for PAM. Denote vP

j as CEO j’s compensation in thefrictionless CEO market. Firm i’s profit when it hires CEO j is thus π(si,a j,vP

j ) = psia j − vPj .

Since PAM is the equilibrium matching pattern, CEO j is firm j’s optimal choice among all CEOs,which yields ps ja

′j − vP′

j = 0. Integrating along CEO’s rank yields

vPj =

ˆ j

0psla

′ldl

Again, the lowest ranked CEO is paid by his autarky payoff, which is zero by Assumption 3. Asexpected, the above solution is very similar to Gabaix and Landier (2008) and Tervio (2008)’ssolution of CEO compensation.

16

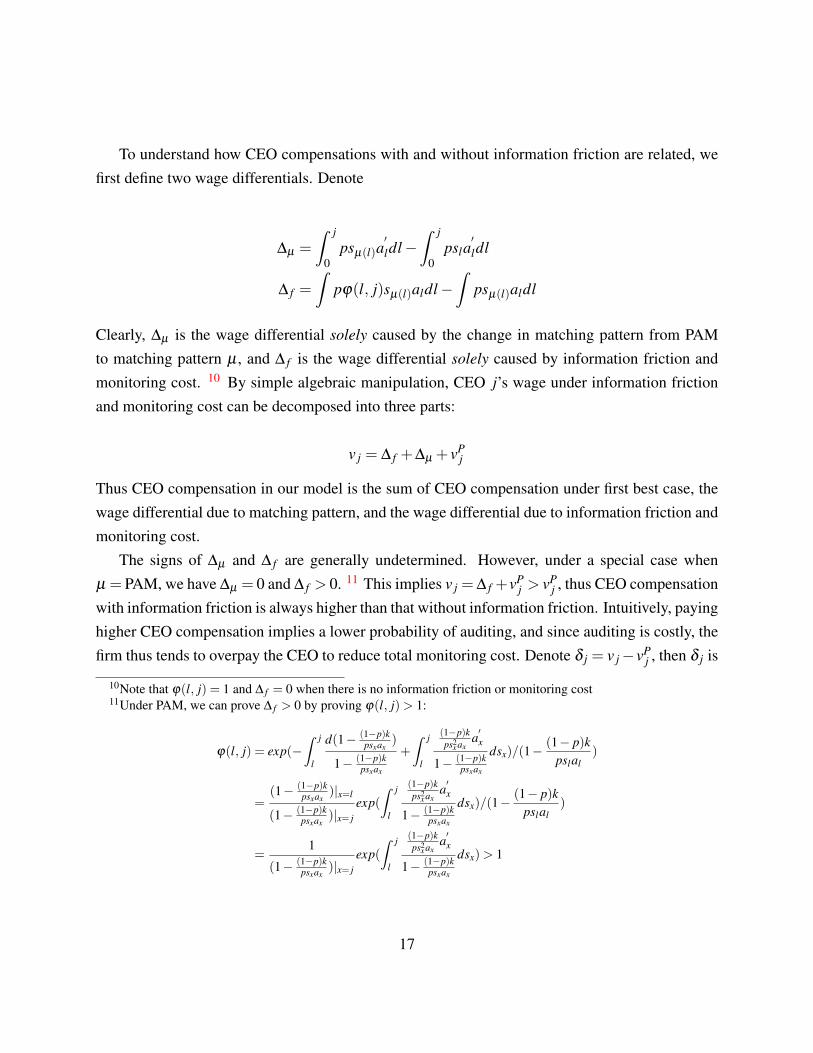

To understand how CEO compensations with and without information friction are related, wefirst define two wage differentials. Denote

∆µ =

ˆ j

0psµ(l)a

′ldl −

ˆ j

0psla

′ldl

∆ f =

ˆpφ(l, j)sµ(l)aldl −

ˆpsµ(l)aldl

Clearly, ∆µ is the wage differential solely caused by the change in matching pattern from PAMto matching pattern µ , and ∆ f is the wage differential solely caused by information friction andmonitoring cost. 10 By simple algebraic manipulation, CEO j’s wage under information frictionand monitoring cost can be decomposed into three parts:

v j = ∆ f +∆µ + vPj

Thus CEO compensation in our model is the sum of CEO compensation under first best case, thewage differential due to matching pattern, and the wage differential due to information friction andmonitoring cost.

The signs of ∆µ and ∆ f are generally undetermined. However, under a special case whenµ = PAM, we have ∆µ = 0 and ∆ f > 0. 11 This implies v j =∆ f +vP

j > vPj , thus CEO compensation

with information friction is always higher than that without information friction. Intuitively, payinghigher CEO compensation implies a lower probability of auditing, and since auditing is costly, thefirm thus tends to overpay the CEO to reduce total monitoring cost. Denote δ j = v j −vP

j , then δ j is

10Note that φ(l, j) = 1 and ∆ f = 0 when there is no information friction or monitoring cost11Under PAM, we can prove ∆ f > 0 by proving φ(l, j)> 1:

φ(l, j) = exp(−ˆ j

l

d(1− (1−p)kpsxax

)

1− (1−p)kpsxax

+

ˆ j

l

(1−p)kps2

x axa′x

1− (1−p)kpsxax

dsx)/(1−(1− p)k

pslal)

=(1− (1−p)k

psxax)|x=l

(1− (1−p)kpsxax

)|x= jexp(ˆ j

l

(1−p)kps2

x axa′x

1− (1−p)kpsxax

dsx)/(1−(1− p)k

pslal)

=1

(1− (1−p)kpsxax

)|x= jexp(ˆ j

l

(1−p)kps2

x axa′x

1− (1−p)kpsxax

dsx)> 1

17

the increase in CEO compensation due to her informational advantage over the firm, we thus call

δ j informational rent. Simple algebra yields v j∂ j −

vPj

∂ j =δ j∂ j > 0 if k = 0, which implies that more

talented CEOs extract higher information rent.The next proposition shows that CEO compensation is an increasing function of CEO talent

irrespective of matching pattern.

Proposition 4. Under any equilibrium matching pattern, CEO compensation satisfies:

i. Monotonicity: CEO compensation is strictly increasing in CEO talent

ii. Equal treatment: CEOs of the same talent matching with firms of different size have the

same compensation

The above proposition holds for any matching pattern, thus a less talented CEO working fora larger firm will not get a higher compensation than a more talented CEO working for a smallerfirm. This is easy to understand. A CEO at a larger firm is more productive due to complementaritybetween firm size and CEO talent, however, the CEO cannot command a higher compensation thana CEO with the same or higher talent but works at a smaller firm. Otherwise, both the larger firmand the more talented CEO can be better off by matching with each other, as long as the largerfirm pays the more talented CEO a wage higher than her current wage but smaller than the wagepaid to the less talented CEO. It’s worth mentioning that the argument here relies on an implicitassumption in firm-CEO matching literature: CEO talent is perfectly transferable among differentfirms. Understanding how transferability would affect firm-CEO matching market remains aninteresting direction for future research.

Empirically, Falato et al. (2015) and Albuquerque et al. (2013) show that CEO compensation ispositively related to CEO talent.12 They obtain their result without specifying or testing matchingpattern, thus their paper indirectly supports the theoretical result presented in Proposition 4.

3.2 Corporate Governance

Firms are often criticized by regulators, shareholders and the public for failing to impose adequatecorporate governance to protect shareholder value. One explanation is that firms are reluctant to

12Falato et al. (2015) use reputational, career, and educational credentials as proxies for CEO talent. Albuquerqueet al. (2013) use the firms’s historical abnormal stock and accounting performance, the market value of the firms thatthe CEO managed in the past, and the number of times the CEO is referred to in the business press as proxies for CEOtalent.

18

monitor their CEOs due to managerial power (Bebchuk, 2009). 13 In this section, we providean alternative explanation which shows that some firms will optimally choose a weaker corporategovernance than others when facing a fierce competition for scarce CEO talent.

From now on, we denote firm i’s probability of auditing under low state as gi, this is withoutloss of generality because each firm’s probability of auditing under high state is always zero ac-cording to Proposition 1. We call gi as firm i’s corporate governance. 14 By Proposition 1, givenequilibrium matching pattern µ , corporate governance at firm i is

gi = 1−vµ(i)

psiaµ(i)

where vµ(i) is CEO µ(i)’s compensation, given by Lemma 1. The above equation shows that cor-porate governance is strictly decreasing in CEO compensation, which is a function of equilibriummatching pattern µ .

To proceed, we first introduce several definitions. Assume µ(i) is continuously differentiableon I. For firm i, if ∂ µ(i)

∂ i > 0, then PAM holds for firms in the neighborhood of firm i (and CEOs inthe neighborhood of CEO µ(i)). Thus we say there is local PAM at firm i if ∂ µ(i)

∂ i > 0. Similarly,we say there is local NAM at firm i if ∂ µ(i)

∂ i < 0. We denote the density functions for firm sizeand CEO talent as f (s) and t(a), and we assume both are strictly positive for any s and a. Undermatching µ , for a firm with size si, the CEO matching with the firm has talent aµ(i). Apparently,the smaller t(aµ(i)) is compared with f (si), then scarcer talent aµ(i) is. Thus the ratio of density

functionst(aµ(i))

f (si)measures relative scarcity of CEO talent for firm i under matching µ .

The following proposition shows that corporate governance can decrease in firm size cross-sectionally if CEO talent is relatively scarce, and equilibrium matching pattern affects how corpo-rate governance changes with firm size.

Proposition 5. (Corporate Governance and Talent Density) Given equilibrium matching pattern

µi. Corporate governance decreases with firm size if CEO talent is relatively scarce under local

13We show in appendix B that our results won’t change when board of directors monitor CEOs.14We acknowledge that corporate governance is a multi-dimensional measure (Shleifer and Vishny, 1997; Zingales,

1998; Gillan and Starks, 1998), thus our model only attempts to capture one very specific but important aspect ofcorporate governance, which is how intensely a firm monitors its CEO.

19

PAM. Formally, for firm i ∈ I, ∂gi∂ i < 0 if ∂ µ(i)

∂ i > 0 andt(aµ(i))

f (si)is sufficiently small

ii. Corporate governance increases with firm size under local NAM. Formally, for firm i ∈ I,∂gi∂ i > 0 if ∂ µ(i)

∂ i < 0

The above proposition shows that firm-level corporate governance is a function of market char-acteristics such as relative scarcity of CEO talent and equilibrium matching pattern. Specifically,Part i. shows that corporate governance can not only be weaker in some firms, but also weaker in alarge firm than in a small firm, despite that corporate governance appears to be more important ina large firm as more stakes are on the table susceptible to CEO’s appropriation. Part ii. shows thatcorporate governance increases in firm size under local NAM regardless of the scarcity of CEOtalent.

The intuition relies on the understanding that corporate governance and CEO compensationare substitutes to prevent CEOs from committing fraud and diverting cash flow. Under local PAM,larger firms match with CEOs of higher talent and smaller firms match with CEOs of lower talent.CEOs of higher talent are paid with higher compensation (Proposition 4) than CEOs of lowertalent, and because corporate governance and CEO compensation are substitutes, larger firms tendto have weaker corporate governance than smaller firms. On the other hand, a larger firm tends tohave stronger corporate governance because more assets are subject to CEO’s appropriation. Whentalent is scarce, CEO compensation will be sufficiently high due to competition and the effect fromcompensation to lower governance outweighs the effect from firm size to increase governance, thuscorporate governance decreases with firm size. On the other hand, under local NAM, larger firmsmatch with CEOs of lower talent, who are paid with a lower compensation, and the effect fromCEO compensation and firm size both make a larger firm impose a stronger corporate governancethan a smaller firm.

Apparently, in the above proposition we treat equilibrium matching pattern as given and dis-cuss how distributions of CEO talent and firm size affect the cross-sectional pattern of corporategovernance. An implicit assumption is thus equilibrium matching pattern is not affected by dis-tributions. This assumption can be satisfied because our results on equilibrium matching patternin Proposition 2 are distribution-free, meaning that they hold for any distributions of firm size andCEO talent. 15

Next, we provide an example to illustrate the relationship between corporate governance and15Technically, we use Legros and Newman (2007) to prove Proposition 2, and Legros and Newman (2007)’s major

results on PAM and NAM are distribution-free.

20

scarcity of CEO talent under PAM. When PAM is the equilibrium matching pattern, corporate

governance at firm i is gi = 1−´ i

0 φ(l,i)sla′ldl

siaiwith φ(l, i) = exp[−

´ il

(1−p)kpsxa2x

a′x

1− (1−p)kpsxax

dx]/(1− (1−p)kpslal

). We

consider two extreme cases. First, all firms have the same size s and CEOs have different talent(thus CEO talent is relatively scarce). It’s easy to show that φ(l, i) = 1

1− (1−p)kpsai

, and corporate

governance at firm i is gi = 1−1− a0

ai

1− (1−p)kpsai

. Simple algebra shows that gi is decreasing in ai. 16 In this

case, corporate governance is weaker for a firm matching with a more talented CEO even thoughall firms are the same ex ante. Second, CEO talent is in sufficient supply: all CEOs have the sametalent a, and all firms have different size. Proposition 4 implies CEOs with the same talent are paidwith the same wage, which can be denoted as v, then gi = 1− v

sia. In this case, since there is no

scarcity of CEO talent, corporate governance is increasing in firm size.The following corollary shows that the result between corporate governance and talent scarcity

is robust even when monitoring CEO is costless.

Corollary 3. When it’s costless to monitor CEOs, corporate governance can decrease in firm size

if CEO talent is relatively scarce

Further more, as we increase the marginal cost of monitoring from 0 to a certain threshold,PAM continues to be the equilibrium matching pattern by Proposition 2. Under PAM, corpo-

rate governance at firm i is gi = 1−´ i

0 φ(l,i)sla′ldl

siaiwith φ(l, i) = exp[−

´ il

(1−p)kpsxa2x

a′x

1− (1−p)kpsxax

dx]/(1− (1−p)kpslal

).

Simple algebra shows that as k increases, φ(l, i) increases, thus all firms will have lower corpo-rate governance. This shows that corporate governance for all firms will be weaker if monitoring ismore costly. However, cross-sectionally, some firms facing more fierce competition for CEO talentwill impose a weaker corporate governance than other firms facing weaker competition, no matterhow small the monitoring cost is. The above corollary thus implies that it’s incorrect to contributeweak corporate governance at some firms solely to monitoring cost caused by CEO power.

16 ∂gi∂ai

= ps(ai ps+k(p−1))2 (k (1− p)−a0 ps) and by k ≤ ps0a0

2(1−p) , we have k (1− p)−a0 ps ≤ ps0a02(1−p) (1− p)−a0 ps < 0,

thus ∂gi∂ai

< 0,∀i ∈ [0,1]

21

4 Implications

4.1 Robustness of PAM and Related Empirical Applications

Previous research on CEO labor market (e.g., Gabaix and Landier, 2008; Tervio, 2008; Dicks,2012) uses firm-CEO matching framework to provide new insights on CEO compensation, corpo-rate governance, and shareholder value. One salient feature of this matching approach is that itrelies on PAM between firm size and CEO talent. However, there is clearly a lack of empirical evi-dence on the matching pattern of CEO market, thus it’s nearly impossible to answer whether PAMholds empirically, let alone how far is the actual matching pattern differs from PAM if it does nothold. PAM, without a careful examination, might be an artifact from oversimplified models whichneglect realistic but important economic forces, and empirical results relying on PAM can be spu-rious. Our paper shows that with cash flow diversion and costly monitoring, equilibrium matchingpattern can be distorted from PAM, thus PAM is not a “taken as given” result, nor implied bycomplementary production technology.

Further more, part ii. of Proposition 2 shows that PAM is more likely among larger firms andmore talented CEOs. This implies that empirical applications relying on PAM are more robustwith a sample of large firms. Comparative statics results in Proposition 3 state that PAM is morelikely when marginal cost of monitoring is smaller. Monitoring cost can be considered either asfirm’s expense spent on accounting information system or directors’ disutility from monitoring theCEO because of lack of independence, as shown in Appendix B. This implies when it’s cheaperto monitor the CEO, or board is more independent, PAM is more likely and empirical tests basedon PAM are more robust. Nowadays, technology advance makes it cheaper to deploy accountinginformation system, and corporate boards indeed grow more independent due to listing rules andlaws such as SOX Act enacted in 2002, we thus expect PAM is more likely in recent years’ data.We summarize the above arguments in the following implication:

Impication 1. Empirical applications relying on PAM are more robust with a sample of large firms

or more recent data.

4.2 Robustness of Gabaix and Landier (2008)

In this section, we discuss the robustness of a particular empirical application base on PAM, whichis from Gabaix and Landier (2008)’s seminal paper on CEO compensation. Based on PAM solved

22

from a frictionless firm-CEO matching model, they predict that CEO compensation increases infirm size in cross-sectional data. However, this prediction can not hold in our cash flow diversionenvironment if equilibrium matching pattern is distorted from PAM. Proposition 4 shows that CEOcompensation is always increasing in CEO talent, thus CEO compensation increases in firm sizeif and only if CEO talent increases in firm size, i.e., PAM holds. And Implication 1 shows thatPAM is more robust with a sample of large firms or more recent data. We thus have the followingimplication:

Impication 2. Gabaix and Landier (2008)’s cross-sectional prediction that CEO compensation

increases in firm size

i. holds if and only if PAM holds

ii. is more robust with with a sample of large firms or more recent data.

Gabaix and Landier (2008) only include “large firms”, i.e., top 500 and 1000 companies in totalfirm value in their empirical analysis. This choice is based on statistics rather than the validity ofPAM: they obtain CEO talent by extreme value theory, thus their results are applicable for “talentat the top”, which restricts their sample choice to large firms. Implication 2 thus resonates to theirempirical approach from a different perspective.

Frydman and Saks (2010) are unable to replicate Gabaix and Landier (2008)’s cross-sectionalresult for the sample period from 1936 to 1975, which is quite earlier than Gabaix and Landier(2008)’s sample period of 1992-2004. Implication 2 provides an explanation to this nonreplicabil-ity: it’s possible that Gabaix and Landier (2008)’s cross-sectional prediction on CEO compensationis less robust when tested with early years’ data as PAM was less likely to hold.

The result that CEO compensation does not increase in firm size if PAM fails seemingly con-tradicts with vast empirical findings of positive correlation between CEO compensation and firmsize (e.g., Lewellen et al. (1968); Cosh (1975); Rosen (1982); Murphy (1985); Baker et al. (1988);Kostiuk (1990); Barro and Barro (1990); Joskow et al. (1993); Rose and Shepard (1997); Gabaixand Landier (2008); Frydman and Saks (2010)). Without empirically testing the matching patternof CEO market, this “contradiction” can be reconciled from two aspects. First, it’s possible thatPAM is indeed the equilibrium matching pattern in the CEO market, thus CEO compensation is anincreasing function of firm size. This generates a positive correlation between firm size and CEOcompensation which is compatible with empirical findings. Second, it’s possible that PAM failsbut there is still positive correlation between CEO compensation and firm size. This is because

23

correlation measures linear relationship, and PAM corresponds to monotonic relationship. Mathe-matically, PAM implies positive correlation, however, a failure of PAM will not imply a failure ofpositive correlation. Thus positive correlation between CEO compensation and firm size will notcontradict with the statement that CEO compensation does not increase in firm size when PAMfails.

4.3 Measuring Equilibrium Matching Pattern

Even though PAM serves as the foundation for a number of empirical applications, there aren’tany empirical evidences to show whether PAM holds in CEO labor market or not. One possiblereason for the lack of empirical evidence is the difficulty in measuring CEO talent. Recent empir-ical corporate finance literature tries to resolve this measurement problem by using various proxyvariables.17 However, due to the unobservable nature of CEO talent, the above proxies undoubt-edly suffer from measurement errors, which makes testing matching pattern between firm size andCEO talent questionable as we are not sure how it can be affected by such errors.

Proposition 4 shows that CEO compensation increases with CEO talent. Thus the ranks of CEOtalent is equivalent to the ranks of CEO compensation, which implies even though we cannot ob-serve CEO talent directly, we can obtain the ranks of CEO talent by ranking CEOs’ compensation.We thus have the following implication:

Impication 3. The matching pattern between CEO talent and firm size is equal to the matching

pattern between CEO compensation and firm size.

Matching pattern between CEO compensation and firm size can be measured by the monotonicrelationship between them, using rank coefficient (e.g., Spearman’s ρ or Kendall’s τ). The aboveimplication states that in order to find out the market matching pattern, we only need to use CEOcompensation data instead of measuring CEO talent. This is useful because CEO compensation ismuch easier and more accurate to measure.

17For example, Cole and Mehran (2010) use CEO’s educational attainment, and Falato et al. (2015) use mediacoverage, age of first job as CEO, and undergraduate school ranking as proxies for CEO talent.

24

4.4 Endogeneity in CEO Compensation Research

To answer how corporate governance affects CEO compensation (e.g., Core et al. (1999), Fahlen-brach (2009)), empiricists regress CEO compensation on proxies of corporate governance, whichgenerally results in negative and significant coefficients. The empirical results suggest that weakercorporate governance causes higher CEO compensation.

However, our paper shows that the above approach might suffer from reverse causality issue asCEO compensation can affect corporate governance. Lemma 1 shows that CEO compensation isdetermined by a competitive market equilibrium and when firms contract with CEOs, the firm opti-mally chooses its corporate governance by taking CEO compensation into consideration, as shownin Proposition 1. Essentially, because corporate governance and CEO compensation are substi-tutes, if competitive market determines a higher CEO compensation, the firm will just optimallychoose a weaker corporate governance. We summarize our findings in the following implication:

Impication 4. To answer how corporate governance affects CEO compensation, we need to ad-

dress the reverse causality issue

Thus in order to establish clear identification, we could use exogenous shocks on corporategovernance and see how CEO compensation is affected. This has been done in the literature onhow corporate governance affects firm performance. The above implication shows that a similarendogeneity issue has to be addressed if we want to answer how corporate governance affects CEOcompensation.

4.5 Regulating Board Independence

For the Securities and Exchange Commission (SEC), the policy to strengthen corporate gover-nance is often about increasing board independence. After several highly publicized accountingscandals (e.g., Enron, Tyco, and Worldcom), starting from October 31, 2004, the SEC requiredfirms listed on NYSE and NASDAQ to have a completely independent audit committee. On Jan-uary 11, 2013, the SEC approved new listing requirements proposed by NYSE and NASDAQ toincrease compensation committee independence.

As we have shown in Appendix B, cost of monitoring is smaller when board is more indepen-dent. Increasing board independence would be effective in strengthening corporate governance for

25

all firms, which has been discussed in Section 3.2. However, it’s less effective in solving the cross-sectional variations in corporate governance, i.e., some firms have weaker corporate governancethan others. This is evident in Corollary 3, which shows that even when it’s costless to moni-tor CEOs (such as with completely independent boards), we cannot eliminate the fact that somefirms have weaker corporate governance than others due to competition for scarce CEO talent. Tosummarize,

Impication 5. The effect of increasing board independence to strengthen corporate governance is

constrained by the competition for CEO talent. Thus a universally perfect corporate governance

for all firms is impossible through regulations and laws.

5 Conclusion

This paper models a two-sided matching market with CEOs of different talent and firms of differentsize where CEOs have more information than firms and monitoring CEOs is costly. We find thatpositive assortative matching (PAM) between firm size and CEO talent can fail under negativeeconomic shock or higher cost of monitoring; the failure of PAM is more likely to occur amongsmaller firms and less talented CEOs. This result is driven by how economic shock and cost ofmonitoring affect the tradeoff between more productive CEO and more expensive monitoring at alarger firm. It implies empirical applications based on PAM are more robust with a sample of largefirms, and explains why observable economic shock affects CEO turnover.

Treating different matching patterns as given, we further discuss CEO compensation and cor-porate governance. We find that cross-sectionally, CEO compensation strictly increases in CEOtalent irrespective of equilibrium matching pattern. This implies that Gabaix and Landier (2008)’scross-sectional prediction that CEO compensation increases with firm size cannot hold if PAMfails, and the monotonic relationship between CEO compensation and firm size can identify thematching pattern between firm size and CEO talent. Corporate governance is affected by aggre-gate market characteristics such as CEO talent scarcity and matching pattern. When CEO talentis sufficiently scarce, larger firms can have weaker corporate governance than smaller firms underPAM. This result holds even when imposing corporate governance is costless to the firm.

In our paper, information friction between firms and CEOs plays an important role in equi-librium matching pattern, CEO compensation and corporate governance. For simplicity, we leave

26

search friction unexplored. However, it has been shown in matching literature that search frictionhas important implications on equilibrium matching pattern. A further direction of research onfrictional CEO market is thus to examine how search friction and search intermediaries, such asexecutive headhunters and compensation consultants, can affect the matching between firms andCEOs, CEO compensation, and corporate governance.

27

A Appendix

A.1 Proof to Proposition 1

Proof. We first simplify the incentive compatibility constraints ICL and ICH. The inequalities in(1) are as weak as possible when wHL,wLH are made as small as possible, which under limitedliability is achieved by setting wHL = wLH = 0. Limited liability and feasibility constraints underlow state imply wL = wLL = 0. Feasibility constraint under high output implies wH + 0− sa ≤ 0,thus ICL can be satisfied. We can simplify incentive compatibility conditions as

(1−gH)wH +gHwHH ≥ (1−gL)sa,(ICH)

By wL = wLL = wHL = wLH = 0, expected CEO compensation is p((1− gH)wH + gHwHH).The firm’s problem can be simplified as:

π(s,a,v) = MaxgH ,gL,wH

p(sa− (1−gH)wH −gHwHH)− (1− p)kgL − pkgH

s.t. p((1−gH)wH +gHwHH)≥ v

(1−gH)wH +gHwHH ≥ (1−gL)(sa−0) (5)

0 ≤ wH ≤ sa

gL,gH ∈ [0,1]

Because auditing is costly, the firm sets gH = 0 to minimize auditing cost. The firm’s problem canbe further simplified as

π(s,a,v) = MaxgL,wH

p(sa−wH)− (1− p)kgL

s.t. pwH ≥ v

wH ≥ (1−gL)(sa−0) (6)

gL ∈ [0,1]

It’s easy to see both the incentive constraint and promise-keeping constraint are binding, whichsolves:

28

gL = 1− vpsa

,wH =vp

A.2 Proof to Proposition 2

We first provide the necessary condition for negative assortative matching (NAM) among any twopairs of firms and CEOs, which will be used in proving Proposition 2. Here NAM refers to thematching pattern that a high talent CEO matches with a small firm and a low talent CEO matcheswith a large firm.

Lemma 2. For firms with rank i, i′and CEOs with rank j, j

′where i > i

′and j > j

′, i matches with

j′and i

′matches with j only if p

1−p ≤ ks

i′a j+ k

sia j.

Proof. NAM is the equilibrium matching pattern only if firm i prefers CEO j′

to CEO j, and firmi′prefers CEO j to CEO j

′, thus the following inequalities must hold:

psia j′ − [1− k1− ppsia j′

]v j′ ≥ psia j − [1− k1− ppsia j

]v j

psi′a j − [1− k1− ppsi′a j

]v j ≥ psi′a j′ − [1− k1− ppsi′a j′

]v j′

which are equivalent to

psia j − psia j′ +[1− k 1−ppsia j′

]v j′

1− k 1−ppsia j

≤ v j ≤psi′a j − psi′a j′ +[1− k 1−p

psi′ a j′

]v j′

1− k 1−pps

i′ a j

which implies the following

p1− p

≤ k(1

si′a j+

1sia j

−v j′

psia jsi′a j′)≤ k

si′a j+

ksia j

Now, we prove Proposition 2

29

Proof. We start from Part i.. We use the sufficient and necessary condition for PAM from Chadeet al. (2016), which states that PAM is the equilibrium matching pattern if and only if πsvπa −πsaπv ≥ 0,∀s,a, where πsv is the cross-partial of firm profit function (3) on s and v. 18 πa,πsa,πv

can be similarly defined. Simple algebra yields the sufficient and necessary condition:

p2s2a2 +(2kp2 −2kp)sa+ k(1− p)v ≥ 0,∀s,a (7)

The above inequality must hold for the lowest ranked firm and CEO, i.e., for (s,a,v)= (s0,a0,v0),thus (7) implies

p2s20a2

0 +(2kp2 −2kp)s0a0 + k(1− p)v0 ≥ 0 (8)

On the other hand, it’s easy to see that the left hand side of (7) is increasing in sa and v, thus (8)implies (7) because sa ≥ s0a0 and v ≥ v0. Note that v ≥ v0 according to Proposition 4. Thus (8)and (7) are equivalent.

By Assumption 3, the lowest ranked CEO’s compensation v0 = 0. Substituting v0 = 0 to (8)yields the sufficient and necessary condition of PAM:

p2s20a2

0 +(2kp2 −2kp)s0a0 ≥ 0 (9)

which is equivalent to

p ≥ 12 s0a0

k +1(10)

Now we prove Part ii. in two steps. Step 1, we assume firms and CEOs with ranks in [0, i) donot participate in the matching market and we prove there is PAM on [i,1]. In step 2, we add firmsand CEOs with ranks in [0, i) back into the matching market and show that any firm or CEO in[0, i) will not match with any CEO or firm in [i,1]. Step 1 an step 2 conclude our proof.

Step 1. When firms and CEOs with ranks in [0, i) do not participate in the matching market,similar to the proof in Part i., there is PAM on [i,1] if we can show that for any firm and CEO on[i,1], with size s and talent a

−2(1− p)k

ppa−1s−1 + p+

(1− p)kp

s−2a−2v ≥ 0

18Interested reader can refer to page 12 and 13 of Chade et al. (2016).

30

Because s ≥ si and a ≥ ai and v ≥ 0 for firms and CEOs on [i,1], the above inequality can besatisfied if

−2(1− p)k

ppai

−1s−1i + p ≥ 0

Substitute p = 2s0ai

k +2to the above inequality, −2 (1−p)k

p pai−1s−1

i + p = p(1− s0si) ≥ 0, thus the

condition for PAM can be satisfied.Step 2. We prove if firms and CEOs with ranks in [0, i) participate in the matching market, any

firm or CEO in [i,1] will not match with any firm or CEO in [0, i). We prove it by contradiction.Without loss of generality, we assume there exists a firm i ∈ [i,1] and a CEO j

′ ∈ [0, i) such thatfirm i matches with CEO j

′. Because firms and CEOs on [i,1] have the same measure and all firms

and CEOs will be matched in equilibrium, there must exist a firm i′ ∈ [0, i) and a CEO j ∈ [i,1]

such that j and i′match with each other.

It’s easy to see that i > i′

and j > j′, then there is NAM between CEOs j, j

′and firms i, i

′.

Because i > i′ ≥ 0 and j ≥ i, we have si > si′ ≥ s0 and a j ≥ ai, thus 2

s0ai> 1

si′ a j

+ 1sia j

. And by

i = {i : p = 1s0ai2k +1

}, we have p1−p = 2k

s0ai, thus

p1− p

=2k

s0ai>

ksi′a j

+k

sia j

which violates the necessary condition for NAM according to Lemma 2.

A.3 Proof to Lemma 1

Proof. We denote CEO j’s equilibrium wage as v j under matching µ . Then firm i’s profit if it hiresCEO j is

π(si,a j,v j) = psia j − (1− p)k− [1− (1− p)kpsia j

]v j

31

For matching pattern µ , CEO j matches with firm µ( j). Because CEO j is the optimal choice forfirm µ( j), the following first order condition must be satisfied:

∂π(si,a j,v j)

∂ j|i=µ( j) = psµ( j)a

′j − [1− (1− p)k

psµ( j)a j]v

′j −

(1− p)kpsµ( j)a j2

a′jv j = 0

By rearrange the above equality, we have the following first order differential equation:

v′j +

(1−p)kpsµ( j)a j2

a′j

[1− (1−p)kpsµ( j)a j

]v j =

psµ( j)a′j

[1− (1−p)kpsµ( j)a j

]

which solves v j =´ j

0 φ(l, j)psµ(l)a′ldl with φ(l, j) = exp(−

´ jl

(1−p)kpsµ(x)a2x

a′x

1− (1−p)kpsµ(x)ax

dx)/(1− (1−p)kpsµ(l)al

) by not-

ing that v0 = 0.

A.4 Proof to Proposition 4

Proof. By Lemma 1, v j =´ j

0 φ(l, j)psµ(l)a′ldl. For j > j

′, we have

v( j′)− v( j) =

ˆ j′

0φ(l, j)psµ(l)a

′ldl −

ˆ j

0φ(l, j)psµ(l)a

′ldl

=

ˆ j′

jφ(l, j)psµ(l)a

′ldl > 0

The strict inequality > follows because a( j) is strictly increasing in j. By proof in Lemma 1,

v′j = [psµ( j)a j −

(1− p)kpsµ( j)a j

v j]a′ja

−1j

1− (1−p)kpsµ( j)a j

when a′j = 0, v j

∂ j = 0. The result here holds for any equilibrium matching pattern µ and specifically,not affected by the size of the firm with which CEO j matches with.

32

A.5 Proof to Proposition 5

Proof. Under matching µ , CEO µ(i) matches with firm i, and by the first order condition derivedin Section A.3, we have

v′j = [psµ( j)a j −

(1− p)kpsµ( j)a j

v j]a′ja

−1j

1− (1−p)kpsµ( j)a j

Note that gi = 1− vµ(i)psiaµ(i)

, we have

∂gi

∂ i=−

v′µ(i)µ

′(i)psiaµ(i)− p

(s′iaµ(i)+ s ja

′µ(i)µ

′(i)

)vµ(i)(

psiaµ(i))2

By substituting v′µ(i) into ∂gi

∂ i , we have ∂gi∂ i =

Ais′i−Bia

′µ(i)µ

′(i)

(psiaµ(i))2 with Ai = paµ(i)vµ(i) and Bi = [

psiaµ(i)−vµ(i)

1− (1−p)kpsiaµ(i)

]psi.

It’s easy to see that Ai ∈ [0, ps1a1] and Bi ∈ [0, ps1a1

1− (1−p)kps0a0

ps1], where [a0,a1] and [s0,s1] are supports

for talent and size distributions respectively. Thus both Ai and Bi are bounded functions of i on[0,1] for matching pattern µ .

Denote F(.),T (.) as the distribution functions and f (.) and t(.) as the density functions forfirm size and CEO talent. Then the size of firm i is si = F−1(i), thus s

′i =

1F ′

(si)= 1

f (si). Similarly,

a′µ(i) =

1t(aµ(i))

. Therefore, we have

∂gi

∂ i=

Aif (si)

− Biµ′(i)

t(aµ(i))

(psiaµ(i))2

When µ ′(i)< 0, it’s easy to see that ∂gi

∂ i > 0. When µ ′(i)> 0, if f (si) is sufficiently close to zero

and t(aM(i)) is sufficiently large, then ∂gi∂ i > 0; if f (si) is sufficiently large and t(aM(i)) is close to

zero or M′(i) is sufficiently large , then ∂gi

∂ i < 0.

A.6 Proof to Corollary 3

Proof. First, as k = 0, we have shown that PAM is the equilibrium matching pattern from Section

3, and gi = 1−´ i

0 sla′ldl

siaiunder PAM, and its derivative with respect to i is

33

∂gi

∂ i=−

sia′i (siai)−

´ i0 sla

′ldl

(s′iai + sia

′i

)(siai)

2

=−sia

′i (siai)−

´ i0 sla

′ldl

(s′iai + sia

′i

)(siai)

2

=−si

1t(ai)

(siai)−´ i

0 sla′ldl

(1

f (si)ai + si

1t(ai)

)(siai)

2

=−si (siai)−

´ i0 sla

′ldl

(t(ai)f (si)

ai + si

)(siai)

21

t(ai)

Thus when t(ai)f (si)

is small enough, ∂gi∂ i < 0.

B When Board of Directors Monitor the CEO

In our model, firms directly interact with CEOs. However, it’s easy to extend our model to amore realistic setting where board of directors serve the fiduciary duty to hire, compensate, andmonitor CEOs. It turns out that our results hold with the following two assumptions: first, boardof directors act as a single decision maker, thus there is no strategic interaction among directors orsubcommittees; second, expected utility for board of directors under truth-telling equilibrium hasthe following form:

u = p[α(sa− (1−gH)wH −gHwHH)− cgH ]+ (1− p)[α(0− (1−gL)wL −gLwLL)− cgL]

where the parameter α measures the incentive of the board tied to firm’s cash flow after payingCEO compensation and c is the marginal cost of auditing. Auditing the CEO can be costly to boardof directors due to the board’s lack of independence. 19 Hermalin and Weisbach (1998) suggestthat a board member’s career is often tied to the CEO and the board thus suffers from disutilitywhen it dissents the CEO.

19Board independence can be measured as percentage of independent directors among all directors. Independentdirectors are board members who do not have any obvious relationship with the firm or its CEO that would potentiallygive rise to a conflict of interest.

34

Denote k = cα as the normalized marginal cost of auditing. A simple monotone transformation

yields

u′= p[sa− (1−gH)wH −gHwHH − kgH ]+ (1− p)[0− (1−gL)wL −gLwLL − kgL]

which is the same as the firm profit function. The board solve the same contracting problem as thefirm, which results in the same indirect utility function as Equation 3. In a matching model, theindirect utility function is decisive in determining matching pattern and payoffs. Thus introducingboard of directors will not change our results and model implications.

When a board has higher stock ownership or higher reputational concerns, its interests are morealigned with shareholders, thus α is larger. Monitoring is also less costly when the board becomesmore independent. The normalized marginal cost of monitoring k is lower if board of directors aremore independent, have higher stock ownership or reputational concerns.

35

References

Albuquerque, Ana M, Gus De Franco, and Rodrigo S Verdi (2013), “Peer choice in ceo compen-sation.” Journal of Financial Economics, 108, 160–181.

Baker, George P, Michael C Jensen, and Kevin J Murphy (1988), “Compensation and incentives:Practice vs. theory.” The journal of Finance, 43, 593–616.

Barro, Jason R and Robert J Barro (1990), “Pay, performance, and turnover of bank ceos.” Journal

of Labor Economics, 448–481.

Bebchuk, Lucian A (2009), Pay without performance: The unfulfilled promise of executive com-

pensation. Harvard University Press.

Becker, Gary S (1973), “A theory of marriage: Part i.” The Journal of Political Economy, 813–846.