Bfp 2 Q09 Outlook

14

Brighton Financial Planning, Inc. Brighton Financial Planning, Inc. Brighton Financial Planning, Inc. Economic and Financial Market Review 2 nd Quarter 2009 John P. Middleton, CFA, CAIA [email protected] www.brightonfinancial.com www.brightonperspective.typepad.com

-

Upload

john-middleton -

Category

Documents

-

view

358 -

download

2

description

Brighton Financial Planning, Inc. 2nd Quarter Review

Transcript of Bfp 2 Q09 Outlook

Brighton FinancialPlanning, Inc.Brighton FinancialPlanning, Inc.

Brighton Financial Planning, Inc.

Economic and Financial Market Review2nd Quarter 2009

John P. Middleton, CFA, CAIA

www.brightonfinancial.com

www.brightonperspective.typepad.com

Brighton FinancialPlanning, Inc.

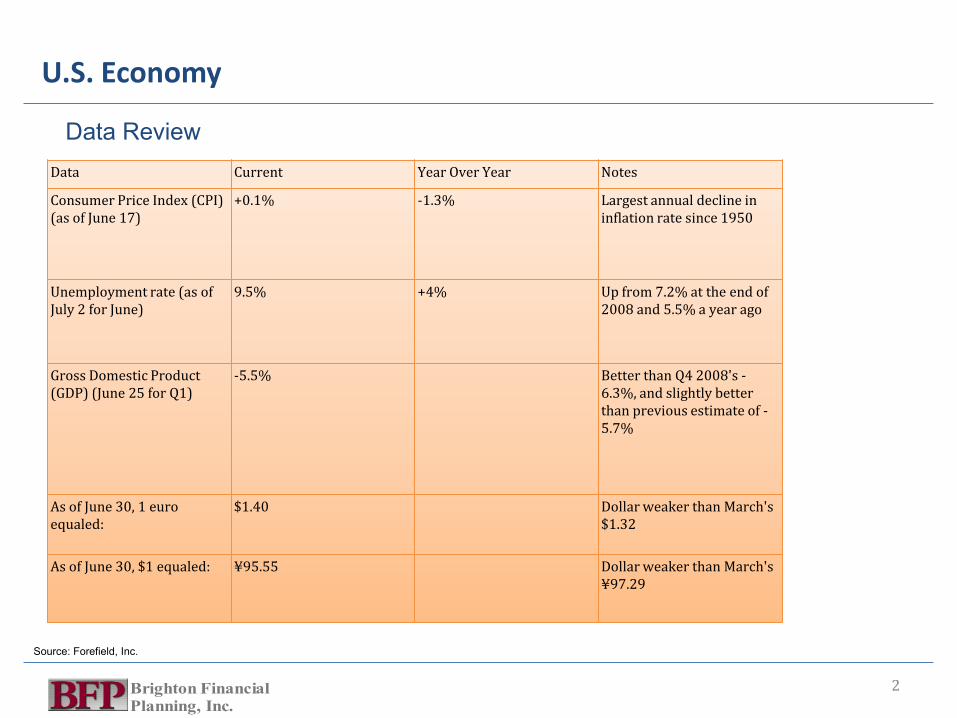

U.S. Economy

2

Data Current Year Over Year Notes

Consumer Price Index (CPI) (as of June 17)

+0.1% -1.3% Largest annual decline in inflation rate since 1950

Unemployment rate (as of July 2 for June)

9.5% +4% Up from 7.2% at the end of 2008 and 5.5% a year ago

Gross Domestic Product (GDP) (June 25 for Q1)

-5.5% Better than Q4 2008's -6.3%, and slightly better than previous estimate of -5.7%

As of June 30, 1 euro equaled:

$1.40 Dollar weaker than March's $1.32

As of June 30, $1 equaled: ¥95.55 Dollar weaker than March's ¥97.29

Data Review

Source: Forefield, Inc.

Brighton FinancialPlanning, Inc.

Brighton Financial Planning, Inc.

• U.S. Economy

– GDP growth likely to remain negative for the 2nd quarter

• Key negative driver for last 2 quarters has been Corporate Investment

• Personal consumption still accounts for 70% of GDP

• Consumers are struggling to maintain current income

3

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

19

47

-I

19

49

-I

19

51

-I

19

53

-I

19

55

-I

19

57

-I

19

59

-I

19

61

-I

19

63

-I

19

65

-I

19

67

-I

19

69

-I

19

71

-I

19

73

-I

19

75

-I

19

77

-I

19

79

-I

19

81

-I

19

83

-I

19

85

-I

19

87

-I

19

89

-I

19

91

-I

19

93

-I

19

95

-I

19

97

-I

19

99

-I

20

01

-I

20

03

-I

20

05

-I

20

07

-I

Rolling 12 month change in Personal Income

Rolling 12 month change in Personal Income

Source: Bureau of Economic Analysis

Brighton FinancialPlanning, Inc.

U.S. Economy

• Consumers and Corporations are not spending

• Consumers and Corporations are de-leveraging their balance sheets

– Result is higher savings and less spending

– Which leads to decline in GDP

– Government spending is up significantly but is not wealth-creating long-term

4

0500

1000150020002500

19

47

-I

19

49

-III

19

52

-I

19

54

-III

19

57

-I

19

59

-III

19

62

-I

19

64

-III

19

67

-I

19

69

-III

19

72

-I

19

74

-III

19

77

-I

19

79

-III

19

82

-I

19

84

-III

19

87

-I

19

89

-III

19

92

-I

19

94

-III

19

97

-I

19

99

-III

20

02

-I

20

04

-III

20

07

-I

Gross Private Domestic Investment (in billions)

Gross Private Domestic Investment

Source: Bureau of Economic Analysis

Brighton FinancialPlanning, Inc.

U.S. Economy

• Conclusions

– GDP growth should continue to be anemic for the near future

• 2/3rds of GDP is consumer driven and consumers are not spending

– Unemployment remains high with most growth in government jobs

– High leverage + unemployment is not good

– Consumers know this and are cutting back spending and paying down debt

• Corporations are not investing in capital

– Recovery should be driven by new capital spending

– As companies invest in new capital, employment will pick up

• Government is attempting to pick up the slack

– Not success yet and questionable as to whether it will be at all

– Can create other issues such as inflation

– Inflation and higher tax risks remains

• Government spending can be inflationary

– Unlikely to be curtailed as economy recovers

– Increase in money supply and velocity + devalued dollar create inflationary pressures

– Higher spending needs means higher income needs

5

Source: Bureau of Economic Analysis

Brighton FinancialPlanning, Inc.

Global Economy

• Global economy very dependent on U.S. economy

– U.S. is leading consumer of global supply

– However, emerging markets have suffered less than developed markets

– And, the IMF forecasts continued improvement in emerging markets

– But, decline in U.S. consumption must be offset somewhere

• Either higher consumption x U.S.

• Or reduction in supply

6

0.00

20,000.00

40,000.00

60,000.00

80,000.00

100,000.00

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

est

20

10

est

20

11

est

20

12

est

20

13

est

20

14

est

GDP (PPP adjusted)

World Advanced economies Emerging and developing economies

Source: Bureau of Economic Analysis

Brighton FinancialPlanning, Inc.

Global Economy

• Developed Markets have struggled much like the U.S.

• U.S. and EU (primary components of Advanced Economies)

– Ran government net deficits for much of the last 15 years

– Have increased government expenditures to combat global recession

• Emerging Markets ran surplus during early part of this decade

– Have increased spending but only deficit forecast to remain under 4%

– Suggests economic improvement will be easier and more quickly achieved

7

-10

-5

0

5

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

est

20

10

est

General Government Balance % of GDP

Advanced economies

European Union

Newly industrialized Asian economies

Source: Bureau of Economic Analysis

Brighton FinancialPlanning, Inc.

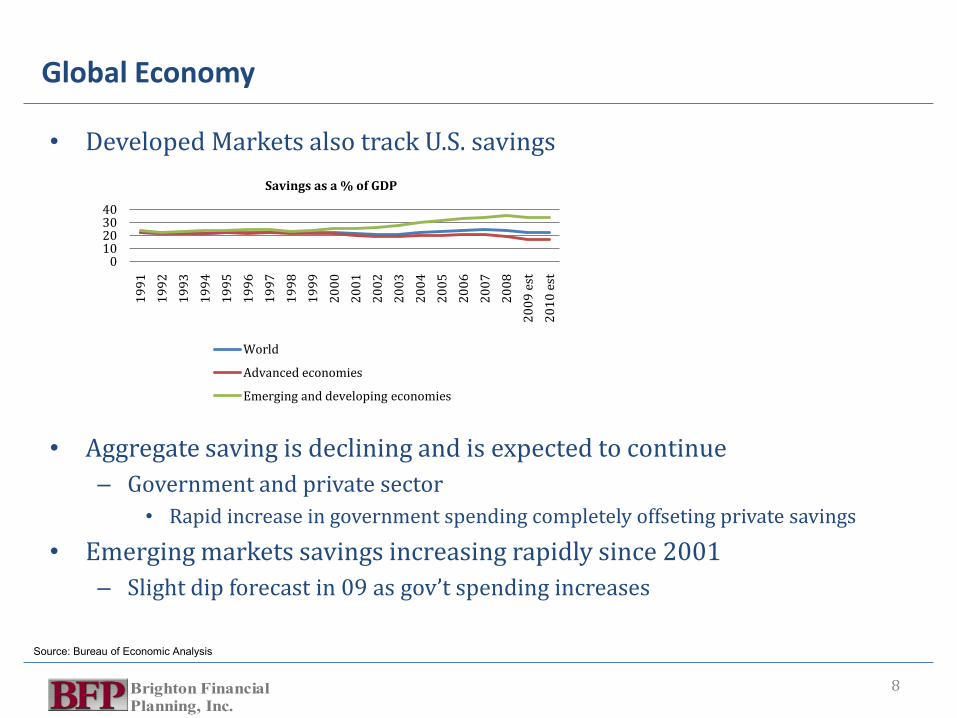

Global Economy

• Developed Markets also track U.S. savings

• Aggregate saving is declining and is expected to continue

– Government and private sector

• Rapid increase in government spending completely offseting private savings

• Emerging markets savings increasing rapidly since 2001

– Slight dip forecast in 09 as gov’t spending increases

8

010203040

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

est

20

10

est

Savings as a % of GDP

World

Advanced economies

Emerging and developing economies

Source: Bureau of Economic Analysis

Brighton FinancialPlanning, Inc.

Global Economy

• Developed markets investment flat

• Investment is key contributor to GDP improvement

– Private investment, particularly corporate capital spending will drive growth

• Emerging markets investment has improved steadily over last 6 years

– And is forecast to continue to remain well above developed markets

9

010203040

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

est

20

10

est

Investment as % of GDP

World

Advanced economies

Emerging and developing economies

Source: Bureau of Economic Analysis

Brighton FinancialPlanning, Inc.

Global Economy

• Conclusions

– Developed markets are struggling just as much as U.S.

• Are highly dependent on U.S. for goods and services

• Must replace U.S. demand and/or services

• Many don’t have the infrastructure to quickly offset that decline

– Emerging markets are also weak, BUT

• Had healthier balance sheets entering the recession

• Haven’t increased government spending above investment and savings

• Are more dependent on commodities consumption

– Driven by China and India currently

• Should recover more quickly than developed markets (including U.S)

10

Brighton FinancialPlanning, Inc.

Financial Markets Performance

11

Market/Index June 30 Quarterly Change

Year Over Year

DJIA 8447.00 +11.0% -25.6%

NASDAQ 1835.04 +20.0% -20.0%

S&P 500 919.32 +15.2% -28.2%

Russell 2000 508.28 +20.2% -26.3%

Global Dow 1629.31 +20.9% -34.0%

Fed. Funds .25% 0 -175 bps

2-year Treasuries 1.11% +30 bps -152 bps

10-year Treasuries

3.53% +82 bps -46 bps

Crude Oil (per barrel)

$69.82 +44% -50.1%

Spot Gold (per oz.)

$928.50 +.8% +.4%

• Equity markets rallied strongly

• Smaller cap, lower quality stocks led

• International equity participated

• All remain significantly down for 12 mos.

• Fed Funds cut sharply to combat

recession

• Short-term Treasuries have been the safe

haven for investors

• Oil rallied but well off last summer’s highs

• Gold and other precious metals have held

value

Source: Forefield, Inc.

Brighton FinancialPlanning, Inc.

Equity Markets

• Earnings continue to deteriorate

– S&P is now forecasting a trailing twelve month loss for period ending 9/30

– Trailing “As Reported” P/E at all-time high

12

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

12

/31

/19

36

9/3

0/1

94

0

6/3

0/1

94

4

3/3

1/1

94

8

12

/31

/19

51

09

/30

/19

55

06

/30

/19

59

03

/31

/19

63

12

/31

/19

66

09

/30

/19

70

06

/30

/19

74

03

/31

/19

78

12

/31

/19

81

09

/30

/19

85

06

/30

/19

89

03

/31

/19

93

12

/31

/19

96

09

/30

/20

00

06

/30

/20

04

03

/31

/20

08

12 MO P/E

Historic Average P/E

Rolling 5YR Ave P/E

Brighton FinancialPlanning, Inc.

Equity Markets

• Conclusions

– P/E ratios tend to trend higher as the economy emerges from recession

– S&P forecasts 2009 earnings at $29.97 per share

– Applying a P/E of 30 (trend forecast) suggests ending S&P 500 Index value of 899.10

– S&P forecasts 2010 earnings at $37.26 per share

– Applying the same P/E suggests ending S&P 500 Index value of 1,117.80

– However, P/E tends to peak 6 to 9 months after recession end

– Thus, more likely to be around 24, so S&P 500 at end of 2010 forecast = 908

13

Brighton FinancialPlanning, Inc.

Looking Ahead

• Weak U.S. economy will gradually improve over the next 18 months

• Global economy will track U.S. but with stronger recovery in EM

• Inflation remains a risk as stimulus spending enters an improving economy

• Equity markets remain flat to slightly positive as lack of leverage suggests any improvement will match earnings growth

• Fixed income markets offer mixed bag – higher inflation is not good but credit dislocation beginning in 2008 hasn’t completely resolved itself

– Inflation hedges – TIPS, Bank Loans may offer opportunities

• Emerging markets and commodities may offer better returns over next 2 years

– EM equity and fixed income

– Commodities producers, oil and gas (MLPs)

14