Beverage at c store

21

Refreshing Drinks 8/28/2014

Transcript of Beverage at c store

Refreshing Drinks8/28/2014

convenience stores (C-stores) are 800 to 5,000 square-feet, carry 500 to 1,500 SKUs and include stores that may or may not sell gasoline and offer fast food services.

Defining Convenience Stores :

*Source: Hartman Group

Positive outlook for convenience stores

Total convenience store retail sales reached $127 billion in 2013, and are expected to increase by 16% by 2018, to reach $147 billion due to new offerings and the growing Hispanic population that is likely to support c-stores.

* Source: Mintel

Total US convenience store sales and fan chart forecast, with best and worst cases, at current prices, 2008-18

Growing Hispanic population will benefit convenience stores

The total number of Hispanics in the US is expected to increase by 12% over the next five years. All age groups are projected to grow by more than 5% with those aged 55+ increasing the most. As the number of Hispanics throughout the country rises, it will certainly impact convenience stores since Hispanics are more likely than non-Hispanics to visit convenience stores, and tend to buy items across more categories. As such, this segments’ growth will have a positive impact on convenience stores.

* source: Mintel/US Census Bureau, interim population projections released 2012 and annual population estimates

US Hispanic population, 2009-19

Most visit c-stores to get gas, buy food/drink• Consumers who have visited gas station or road based convenience stores in the last three

months have done so primarily to get gasoline. Among those who have visited any convenience store in the last three months, most have done so to buy food/drink items.

• Seeing as more than half of all respondents indicate buying food/drink as a primary reason for visiting, c-stores have an opportunity to cross-promote other categories while shoppers are in stores buying food and/or drink.

“Thinking about your visits to convenience stores in the last three months, what were the primary reasons for your visits?”

* Source: Mintel

• 1,639 internet users aged 18+ who have visited convenience stores in the last three months• To get gasoline: 1,469 internet users aged 18+ who have visited convenience stores in the last three months and gas

station or road based convenience stores • To buy tobacco products: 1,611 internet users aged 19+ who have visited convenience stores in the last three months

Reasons for visiting convenience stores, January 2014

Pre-packaged food and drink commonly purchased c-store items

• Pre-packaged food and pre-packaged drinks see the most commonly purchased items by convenience store shoppers who have bought food/foodservice items at c-stores in the last three months. These items can be used for immediate consumption or saved to be consumed later

• Alcoholic beverages have been purchased by nearly one quarter of those (21+) who have shopped at a c-store in the last 12 months. Convenience stores typically offer a selection of alcohol and some, such as 7-Eleven, are improving their alcohol selection with the introduction of premium wines.

“You mentioned you have purchased food/drink and/or other items at convenience stores in the last three months. Which of the following items have you purchased?”

*Source: Mintel

• 1,050 internet users aged 18+ who have bought food items and/or visited the restaurant at convenience stores in the last three months

• Alcoholic beverage purchases: 986 internet users aged 21+ who have bought food items and/or visited the restaurant at convenience stores in the last three months

Items purchased at convenience stores, January 2014

Based

Consumers are moving toward a “Wellness Culture” Healthier Foods & Beverages are part of a holistic,

mainstream solution

Consumers seek healthier options at c-stores

• Nearly two thirds of consumers would like convenience stores to carry more healthy foods. While some c-stores are making inroads in this area, (such as 7-Eleven, ampm), they still have room to improve. C-stores walk a fine line between continuing to offer some of the unhealthy items that many of their core customers desire, while also appealing to more health-conscious consumers.

• Despite agreeing that c-stores should offer healthier choices, more than half of consumers say they allow themselves to indulge in unhealthy food/drinks from convenience stores.

“Thinking about convenience stores, please indicate how much you agree or disagree with each statement.” (Any agree)

*Source: Mintel1,638 internet users aged 18+ who have visited convenience stores in the last three months

Attitudes toward healthy food items at convenience stores, January 2014

Based

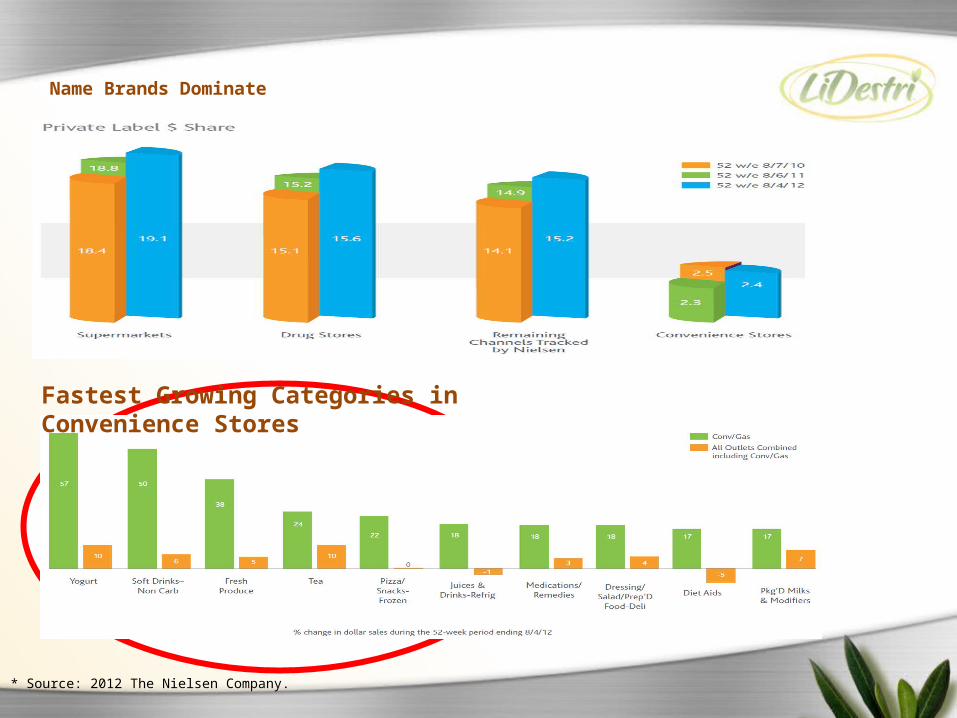

Name Brands Dominate

* Source: 2012 The Nielsen Company.

Fastest Growing Categories in Convenience Stores

Evolving ‘convenience’ landscape: Can traditional c-stores adapt?

•The latest 7-Eleven prototype is a huge departure for not only the retailer, but c-stores in general. A new store design, open layout and revamped assortment, including fresh & healthy, reflect a definite attempt to attract a different shopper type – including more females, young shoppers and the health-conscious.

•Select 7-Eleven units have been adding instore Amazon collection lockers, making order pick-up easy for busy consumers. For 7-Eleven, it brings extra traffic into stores – which hopefully translates into add-on sales.

Adapt, or be left in the dust. Traditional c-store retailers must adapt to survive the competitive onslaught ahead.

*Source: Planet Retail

Private Brand Trend – Organic

•Organic differentiates Private Brands vs. National Brands

•Both Shelf Stable and Refrigerated segments can provide opportunities

•15% of Consumers report purchasing Juice based on “Organic” as an attribute

•As retailers launch Private Brand Organic/Natural brands, Juice is often one of the first categories to be developed

Private Brand Trend – RTD Tea and Lemonade Leadership •In Refrigerated Tea, Private Brand is 13.2% of Dollars, and 15.8% of Units, with room to grow vs. regional brands which are PB placeholders

•Both Shelf Stable and Refrigerated Teas and Lemonades can provide solutions as consumers migrate to perceived healthier beverages from Carbonated Soft Drinks

•Private Brands can offer shoppers innovation and value vs. national brands in these growing segments

The issues: 57% of c-store shoppers think that most convenience stores are pretty much the same; 61% think that c-stores should offer more healthy foods; more than 40% are satisfied with the quality of convenience stores’ private label food and beverages.

The implications:Offering healthier foods will appeal to health conscious consumers, particularly fresh foods that can be eaten on the go. C-stores can leverage their own private label food and drinks when promoting healthier options since many feel private label c-store products are on par with national brands.

What can c-stores do to encourage more visits?

*Source: Mintel

* Source: Category Management Handbook 2012

NEXT FEW SLIDES ARE BASED ON GLOBALLY -WHAT’S GOING ON IN TRENDSDirectional purpose only

Core Beverage TrendsHealthier Carbonated Beverages

•National/Regional brands area beginning to challenge Private Brand leadership in Sparkling Water in reaction to consumers migrating from Carbonated Soft Drinks to healthier sparkling beverages •Many successful low/no calorie national brand s have launched and have also introduced line extensions •All Natural/No Sweetener versions are emerging

Naturally Healthy/Functional •Beverage blends with healthy options like Coconut Water, Tea or Milk Alternatives provide unique and trendy variety •Naturally occurring antioxidants in tea drive segment growth •Sugars associated with Juice/Lemonade can be overlooked for freshness, health benefits, refreshment •Fiber, Protein and Vitamins continue to be on trend

Minimally Processed/Fresh/Organic

•Unflavored Bottled Water continues to grow •Clean ingredient decks appeal to consumers seeking “Real”, “Fresh” alternatives •Organic is becoming established in Juices

Orange and apple remain the most prominent ingredients An analysis of the most-used flavors in new juice and smoothie products between 2012 and 2013 shows that while traditional orange and apple remain most common, more unusual flavors are gaining traction. Pomegranate, considered a "superfruit" due to its high antioxidant properties, has gained in rank, highlighting the influence the Health and Wellness megatrend is having on flavor innovation. Other unusual flavors such as pear, guava, and coconut also feature in the top 20.

New and unusual flavors are gaining traction in juice and smoothie innovation

Source: Datamonitor Consumer's Product Launch Analytics; Additional image: Projectfreshcraftjuice.com, accessed June 2014; *Excludes blended flavors, arrows indicate positioning relative to 2011-12 period.

Exotic flavors and fruit and vegetable juice pairings should be a key focus of juice and smoothie innovation

Source: Datamonitor Consumer’s Product Launch Analytics

Focus innovation on positive health benefits

Source: Datamonitor Consumer’s Product Launch Analytics

Develop personalized products to meet the differing nutritional needs of consumer groups

Source: Datamonitor Consumer’s Product Launch Analytics

Evolving Landscapes Consumer demand is often driven by contrasting needs and motivations across different consumer

groups

Source: Datamonitor Consumer’s Product Launch Analytics

Easy & Affordable

Private label products appeal because as they deliver on both price and quality

Source: Datamonitor Consumer’s Product Launch Analytics