Betting Against Beta - Top1000Funds.com on High Beta is Low Alpha: All Asset Classes 0.00 Source:...

16

Betting Against Beta Prepared for the Fiduciary Investors Symposium, Beijing 2011 Lasse H. Pedersen New York University, Copenhagen Business School, CEPR, NBER, and AQR Capital Management

Transcript of Betting Against Beta - Top1000Funds.com on High Beta is Low Alpha: All Asset Classes 0.00 Source:...

Betting Against Beta

Prepared for the Fiduciary Investors Symposium, Beijing 2011

Lasse H. Pedersen

New York University, Copenhagen Business School, CEPR, NBER, and

AQR Capital Management

Betting Against Beta: Motivation

Traditional porfolios (including the market portfolio) dominated by

– Risky asset classes

• Equities

– Risky securities within each asset class

• Equity portfolios dominated by risky stocks

• Bond portfolios dominated by long-term bonds

What is the risk-adjusted return of the assets that dominate the portfolio risk?

– Low!

Three research questions:

1. Why? Theoretical justification?

2. How general is this finding empirically?

3. What are the implications for investors?

Lasse H. Pedersen

2

Betting Against Beta: Research Papers

“Capital market equilibrium with restricted borrowing,” Fischer Black (1972)

“The Capital Asset Pricing Model: Some Empirical Tests,” Black, Jensen, and Scholes (1972)

“Betting Against Beta” by Andrea Frazzini and Lasse Pedersen (2010)

“Leverage Aversion and Risk Parity” by Cliff Asness, Andrea Frazzini, and L. Pedersen (2011)

“Embedded Leverage” by Andrea Frazzini and Lasse Pedersen (2011)

Theory - Why?

Investors like high returns, but often cannot or will not use leverage

Rather than using leverage, they overweight risky securities

– Pushing up their price

– Lowering their expected return

Lasse H. Pedersen

4

Theory: High Beta is Low Alpha

Proposition. [Black-Frazzini-Pedersen] When some investors face leverage constraints, the

required return is:

where the risk premium is , and ψ is the average Lagrange multiplier measuring

the tightness of funding constraints. A security’s alpha with respect to the market decreases in the

security’s market beta:

Sources: Fischer Black (1972), and Andrea Frazzini and Lasse H. Pedersen (2010) “Betting Against Beta”

5

1

s f s

t t t t tE r r

1

M f

t t t tE r r

(1 )s s

t t t

Expected

return

β

Standard

CAPM

Margin

CAPM

rf

α

α

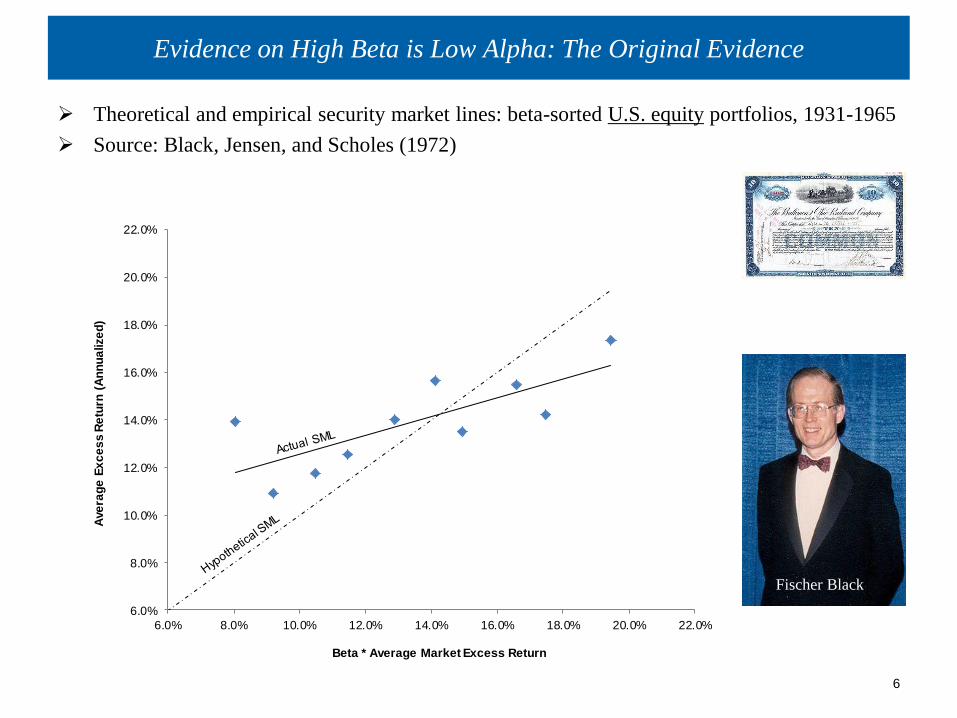

Evidence on High Beta is Low Alpha: The Original Evidence

Theoretical and empirical security market lines: beta-sorted U.S. equity portfolios, 1931-1965

Source: Black, Jensen, and Scholes (1972)

6

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0% 20.0% 22.0%

Ave

rag

e E

xc

es

s R

etu

rn (

An

nu

alize

d)

Beta * Average Market Excess Return

Fischer Black

Evidence on High Beta is Low Alpha: Updated Equity Sample

Theoretical and empirical security market lines: beta-sorted U.S. equity portfolios, 1926-2010

Source: Andrea Frazzini and Lasse H. Pedersen (2010)

7

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

4.0% 5.0% 6.0% 7.0% 8.0% 9.0% 10.0% 11.0% 12.0% 13.0% 14.0%

Ave

rag

e E

xc

es

s R

etu

rn (

An

nu

alize

d)

Beta * Average Market Excess Return

Evidence on High Beta is Low Alpha: Bonds

Theoretical and empirical security market lines: beta-sorted bond portfolios, 1952-2010

Source: Andrea Frazzini and Lasse H. Pedersen (2010)

8

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5%

Ave

rag

e E

xc

es

s R

etu

rn (

An

nu

alize

d)

Beta * Average Market Excess Return

Evidence on High Beta is Low Alpha: Across Asset Classes

9

Theoretical and empirical security market lines: Evidence across asset classes

Source: Cliff Asness, Andrea Frazzini, and Lasse H. Pedersen (2011)

“Leverage Aversion and Risk Parity”

Theory: High Beta is Low Alpha

Proposition. [Black-Frazzini-Pedersen] When some investors face leverage constraints, the

required return is:

where the risk premium is , and ψ is the average Lagrange multiplier, measuring

the tightness of funding constraints. A security’s alpha with respect to the market decreases in the

security’s market beta:

Sources: Fischer Black (1972), and Andrea Frazzini and Lasse H. Pedersen (2010) “Betting Against Beta”

10

1

s f s

t t t t tE r r

1

M f

t t t tE r r

(1 )s s

t t t

Expected

return

β

Standard

CAPM

Margin

CAPM

rf

α

α

Evidence on High Beta is Low Alpha: All Asset Classes

Source: “Betting Against Beta,” Andrea Frazzini and Lasse Heje Pedersen (2010)

11

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

0.50

P1(low

beta)

P2 P3 P4 P5 P6 P7 P8 P9 P10(high

beta)

Alp

ha

US Stocks

-0.70

-0.60

-0.50

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

P1(low

beta)

P2 P3 P4 P5 P6 P7 P8 P9 P10(high

beta)

Alp

ha

International Stocks

-0.08

-0.06

-0.04

-0.02

0.00

0.02

0.04

1 to 12months

13 to24

25 to36

37 to48

49 to60

61 to120

> 120

Alp

ha

Treasury

-0.08

-0.06

-0.04

-0.02

0.00

0.02

0.04

0.06

1-3 years 3-5 year 5-10 years 7-10 years

Alp

ha

Credit Indices

-0.05

-0.04

-0.03

-0.02

-0.01

0.00

0.01

0.02

0.03

0.04

1-3 years 3-5 year 5-10 years 7-10 yearsA

lph

a

Credit - CDS

-1.20

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

Alp

ha

Credit - Corporate

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

Low beta High beta

Alp

ha

Equity Indices

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

Low beta High beta

Alp

ha

Commodities

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

0.18

0.20

Low beta High beta

Alp

ha

FX

-0.01

-0.01

0.00

0.01

0.01

0.02

0.02

0.03

0.03

Low beta High beta

Alp

ha

Country Bonds

Theory: Betting Against Beta

Define a betting against beta portfolio as:

Proposition. [Frazzini and Pedersen, Prop. 2] The expected return of a betting against beta

portfolio is positive:

12

1 1 1

1 1BAB L f H f

t t tL H

t t

r r r r r

1 0H L

BAB t tt t tL H

t t

E r

Expected

return

β

Long

Short

rf

Evidence on Betting Against Beta

Lasse H. Pedersen

13

-0.2

0

0.2

0.4

0.6

0.8

1

US

sto

cks

AU

S

AU

T

BE

L

CA

N

CH

E

DE

U

DN

K

ES

P

FIN

FR

A

GB

R

HK

G

ITA

JPN

NL

D

NO

R

NZ

L

SG

P

SW

E

Glo

bal S

tocks

(all

)

Cre

dit

Ind

ices

Corp

ora

te B

onds

Cre

dit

Hedged (

CD

S)

Tre

asu

ries

Equit

y Indic

es

Cou

ntr

y B

on

ds

Fore

ign E

change

Com

modit

ies

Sharpe ratio of betting against beta portfolios:

Source: “Betting Against Beta,” Andrea Frazzini and Lasse Heje Pedersen (2010)

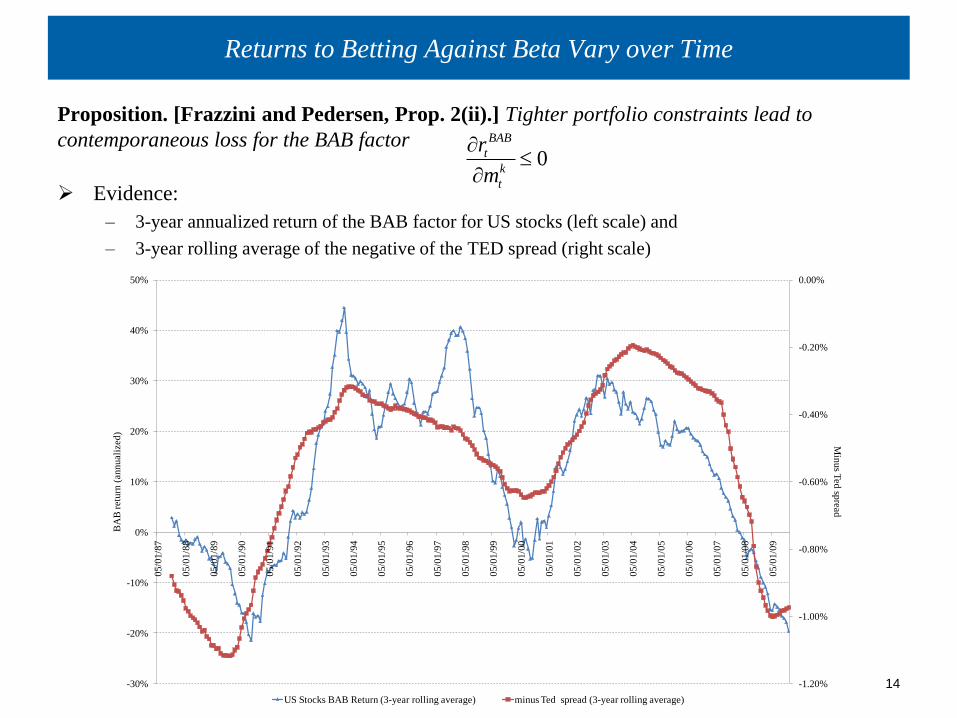

Returns to Betting Against Beta Vary over Time

Proposition. [Frazzini and Pedersen, Prop. 2(ii).] Tighter portfolio constraints lead to

contemporaneous loss for the BAB factor

Evidence:

– 3-year annualized return of the BAB factor for US stocks (left scale) and

– 3-year rolling average of the negative of the TED spread (right scale)

Lasse H. Pedersen

14 -1.20%

-1.00%

-0.80%

-0.60%

-0.40%

-0.20%

0.00%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

05/0

1/8

7

05

/01

/88

05

/01

/89

05/0

1/9

0

05

/01

/91

05

/01

/92

05

/01

/93

05/0

1/9

4

05

/01

/95

05

/01

/96

05/0

1/9

7

05

/01

/98

05

/01

/99

05/0

1/0

0

05

/01

/01

05

/01

/02

05/0

1/0

3

05/0

1/0

4

05

/01

/05

05

/01

/06

05/0

1/0

7

05

/01

/08

05

/01

/09

Min

us T

ed sp

read

BA

B r

etu

rn (

annuali

zed)

US Stocks BAB Return (3-year rolling average) minus Ted spread (3-year rolling average)

0BAB

t

k

t

r

m

Who Bets Against Beta and Who Does the Reverse: Buffett vs. Retail

Proposition. [Frazzini and Pedersen, Prop. 4.] Constrained investors hold high-beta assets

while unconstrained investors hold low-beta assets and possibly apply leverage.

Evidence from equity positions:

Source: “Betting Against Beta,” Andrea Frazzini and Lasse Heje Pedersen (2010)

15

Panel Investor Method

Beta

t-statistics

(H0: beta=1) Beta

t-statistics

(H0: beta=1)

A) Investors Likely to be Constrained

A.1) Mutual Funds Value weighted 1980 - 2009 1.04 13.14 1.08 11.96

Mutual Funds Equal weighted 1980 - 2009 1.06 15.35 1.12 4.08

A.2) Individual Investors Value weighted 1991 - 1996 1.04 18.14 1.09 2.60

Individual Investors Equal weighted 1991 - 1996 1.05 16.03 1.08 1.17

B) Investors who use Leverage

B.1) Private Equity (All) Value weighted 1963 - 2009 0.96 -2.67

Private Equity (All) Equal weighted 1963 - 2009 0.92 -5.40

Private Equity (LBO, MBO) Value weighted 1963 - 2009 0.83 -4.01

Private Equity (LBO, MBO) Equal weighted 1963 - 2009 0.83 -4.02

B.2) Berkshire Hathaway Value weighted 1980 - 2009 0.90 -10.73 0.78 -5.53

Berkshire Hathaway Equal weighted 1980 - 2009 0.90 -13.33 0.83 -5.29

Sample

Period

Ex Ante Beta

of Positions

Realized Beta

of Positions

Conclusion: Implications for Investors

Low beta = high alpha: Investors can exploit this to get a higher Sharpe ratio

– Without leverage if the return target is modest

– With high expected return if they are willing to use leverage

– But remember that leverage requires dynamic trading and may have other risks

Implications for asset allocation:

• Overweight safer asset classes

• Consider a risk-parity approach:

• Diversify by risk: Allocate capital to equalize risk contribution across asset classes

Implications for equity investment:

• Defensive equity:

• Overweight low-beta stocks

• Overweight quality stocks

• Betting against beta:

• Long low-beta stocks, short high-beta stocks

Lasse H. Pedersen