Best Practices

22

PRESENTATION FOR HARVEY MUDD ALUMNI BEST PRACTICES FROM INSIDE A PROFESSIONAL FINANCIAL ADVISORY FIRM March 23, 2012 Proud Bird Restaurant

-

Upload

ahmad-mostafa -

Category

Documents

-

view

10 -

download

0

description

practices

Transcript of Best Practices

PRESENTATION FOR HARVEY MUDD ALUMNI

BEST PRACTICES FROM INSIDE A PROFESSIONAL FINANCIAL ADVISORY FIRM March 23, 2012 Proud Bird Restaurant

Potpourri of Topics

• Estate planning • Umbrella liability • Education planning • Mortgage payoff • Charitable Giving

• Advisory landscape • Tax loss harvesting • Retirement

spending • Investing • Your questions

Estate Planning

• This is first because it’s important • Under current federal law couples can pass

on $10M without paying estate tax • So why do you need to worry about this? • It’s about control of assets, not tax savings • Probate is time consuming and expensive

– California probate is running 18 months – Statutory fee on $1M assets is $23,000

Estate Planning (cont.)

• Standard package includes – Revocable living trust – Pour-over wills – Healthcare powers of attorney – Financial powers of attorney

• Guardians for children are listed in wills • Selecting trustees/executors and ultimate

beneficiaries often proves difficult • Cost: $1,500 to $3,500 (non-blended

family)

Umbrella Liability Insurance

• A question about umbrella liability insurance appears on the Certified Financial PlannerTM certification test every year

• Is in addition to your homeowners and auto policies (i.e., an umbrella over)

• Provides additional coverage against large claims and lawsuits

• Very affordable – $1M coverage about $200

Education Planning • 529 college savings

plans recommended – Contributions grow tax-

free if used for college – Opportunity to front-

load with five year contribution

– Each state runs a plan – Shop based on

investment choices • Be careful with

custodial (UTMA) accounts

Mortgage Payoff

• Should I pay off my home mortgage loan? • The portfolio leverage answer:

– Assume taxable (i.e., accessible) investment portfolio earning 8% per year

– Assume interest rate 4.5%; tax bracket 37% combined (28% fed + 9% CA)

– After-tax cost of loan = (4.5%)(1-.37) = 2.8% – Return difference: 8% - 2.8% = 5.2%

• Limited by income available for debt service

Charitable Giving • Donor-advised funds

can be a good option • Income tax deduction

in year of contribution • Make donations from

the fund any time • Assets leave your

estate but you retain control

• Used to reduce tax in high income years

Advisory Landscape

• Proliferation of credentials – CFP, CFA, CIMA, CPA, EA, ChFC, CLU, CMFC, PFS,

RIA, AAMS, CDFA, etc. • Growth in client-centered, advice-driven

model versus traditional product sales model – Independent firms vs. Wall Street firms

• Fiduciary standards debate

• Advisors are employees

• Products and services limited, often proprietary

• Sales culture, product-centric business model

• Advisors/reps are NASD Series 7 licensed to sell financial products

• Paid by commission and fees which can create conflicts of interest

• Advisors not fiduciaries (not obligated to act in client’s best interest)

Fully Affiliated Supervised Independent Fully Independent

Brokerage Firm: (e.g. Smith Barney, Merrill Lynch, UBS, Morgan Stanley)

Independent Broker/Dealer (IBD): (e.g. LPL, Royal Alliance)

• Advisors are independent contractors

• Products and services limited to IBD offerings

• Mixed culture, products and advice

• Advisors/reps are NASD Series 7 licensed to sell financial products

• Paid by commission and fees which can create conflicts of interest

• Advisors not fiduciaries (not obligated to act in client’s best interest)

• Advisors are self-employed/partners

• Broadest product access and most sophisticated service offerings

• Client-centered, advice driven business model

• Advisors are NASD Series 65/66 licensed to provide investment advice

• Advice for fee compensation reduces conflicts of interest

• Fiduciaries by law, required to act in client’s best interest

Registered Investment Advisor (RIA): (e.g. Parkworth Wealth Mgmt., Inc.)

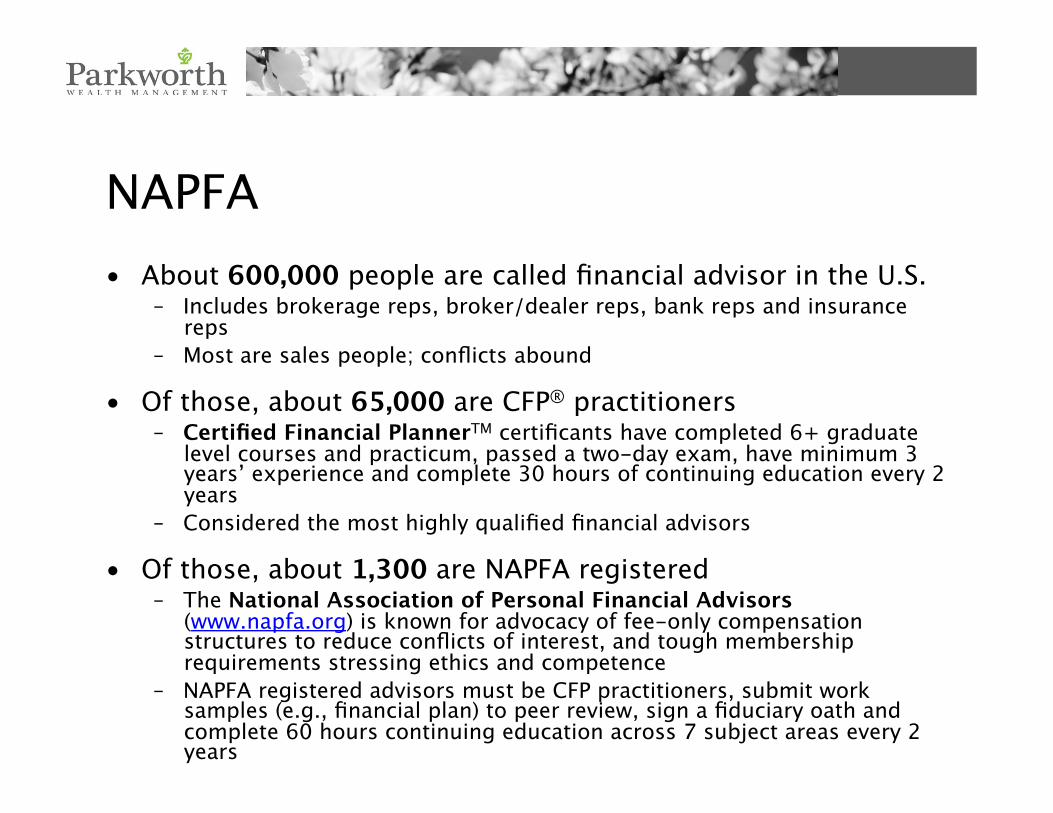

NAPFA • About 600,000 people are called financial advisor in the U.S.

– Includes brokerage reps, broker/dealer reps, bank reps and insurance reps

– Most are sales people; conflicts abound

• Of those, about 65,000 are CFP® practitioners – Certified Financial PlannerTM certificants have completed 6+ graduate

level courses and practicum, passed a two-day exam, have minimum 3 years’ experience and complete 30 hours of continuing education every 2 years

– Considered the most highly qualified financial advisors

• Of those, about 1,300 are NAPFA registered – The National Association of Personal Financial Advisors

(www.napfa.org) is known for advocacy of fee-only compensation structures to reduce conflicts of interest, and tough membership requirements stressing ethics and competence

– NAPFA registered advisors must be CFP practitioners, submit work samples (e.g., financial plan) to peer review, sign a fiduciary oath and complete 60 hours continuing education across 7 subject areas every 2 years

• High transparency • Low fees • ERISA 3(38) fiduciary advisors • Independent registered investment

advisory firm managed plans • Plan sponsor/participant driven

• Non-fiduciary consultants • Insurance company and large

brokerage firm managed plans • Lack of transparency • Unnecessarily high fees • Conflicts of interest

Changing 401(k) Marketplace

Tax Loss Harvesting • Technique to reduce and defer capital gains taxes

generated by taxable portfolios • Involves selling an investment at a loss, buying

back a similar investment and holding for 30 days, then selling that investment and buying back the original investment

• Result is a capital loss that can be used to offset capital gains in that year or carried forward to use in future years

Retirement Spending • For the first time in human

history, mass population is scheduled to be retired nearly as long as they worked

• Retirement portfolios will need to keep working hard

• Sustainable withdrawal rates while maintaining principal are in 3%-5% range

• A glimpse at the future: Stanford and Yale endowments are pioneering spending rules using a “low-pass filter” to smooth spending

Stanford Spending Rule:

[w1 * (s * (1+i))] + [w2 * (r * m)]

w1 = 60% w2 = 40% s = last year’s spending i = inflation r = policy spending rate m = last year’s market value

Randomness of Returns Highest Return

Lowest Return

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 36.94 28.58 66.41 31.04 40.59 7.62 74.48 35.14 34.54 35.97 39.78 8.83 79.02 34.59 9.37

33.75 23.11 33.01 8.96 18.04 5.11 69.18 33.16 24.13 32.99 8.16 6.60 70.19 29.53 3.38

33.36 11.95 30.16 8.28 12.35 3.82 66.79 32.11 22.63 32.59 8.04 4.75 51.48 28.07 2.31

25.79 10.24 28.41 7.33 8.44 3.58 60.25 30.58 15.10 27.54 6.35 -37.00 47.81 20.79 2.11

19.66 9.69 21.51 4.01 7.28 3.39 57.81 27.33 13.82 26.32 6.31 -38.64 47.02 20.17 0.57

7.27 8.41 21.04 -2.01 6.44 -2.85 56.28 25.95 9.70 21.87 6.24 -39.20 44.83 19.30 -5.38

7.12 7.75 6.99 -3.08 -2.37 -6.00 36.43 19.15 5.61 21.70 5.95 -42.54 37.51 19.20 -10.78

5.93 5.91 4.37 -6.40 -2.71 -11.72 36.18 17.74 4.91 17.08 5.49 -44.49 28.46 15.06 -15.12

0.39 -2.33 4.04 -9.10 -6.48 -13.84 28.69 10.88 4.45 15.80 -2.61 -45.12 26.46 13.32 -15.59

-11.59 -10.04 3.55 -12.26 -11.89 -19.87 2.04 2.65 3.08 4.32 -12.24 -47.11 2.29 3.73 -17.05

-14.55 -17.01 1.90 -12.26 -15.41 -22.10 1.95 1.35 2.36 4.09 -17.55 -53.14 0.80 1.99 -18.17

-15.12 -25.34 -2.58 -30.61 -16.75 -30.28 1.47 0.83 1.34 3.75 -18.38 -53.18 0.19 0.83 -19.90

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 US Large Cap 33.36 28.58 21.04 -9.10 -11.89 -22.10 28.69 10.88 4.91 15.80 5.49 -37.00 26.46 15.06 2.11

US Large Cap Value 33.75 11.95 6.99 -6.40 -2.71 -30.28 36.43 17.74 9.70 21.87 -12.24 -53.14 37.51 20.17 -19.90 US Small Cap 25.79 -2.33 28.41 -12.26 18.04 -19.87 57.81 19.15 5.61 17.08 -2.61 -38.64 47.02 29.53 -5.38

US Small Cap Value 36.94 -10.04 4.37 -3.08 40.59 -11.72 74.48 27.33 4.45 21.70 -18.38 -44.49 70.19 34.59 -10.78 US Real Estate 19.66 -17.01 -2.58 31.04 12.35 3.58 36.18 33.16 13.82 35.97 -17.55 -39.20 28.46 28.07 9.37

International Large Cap Value 0.39 23.11 33.01 4.01 -15.41 -13.84 69.18 30.58 15.10 32.99 6.35 -45.12 51.48 13.32 -17.05 International Small Cap -14.55 10.24 30.16 -12.26 -16.75 -2.85 60.25 32.11 22.63 26.32 8.04 -47.11 44.83 20.79 -15.59

International Small Cap Value -15.12 9.69 21.51 -2.01 -6.48 3.82 66.79 35.14 24.13 27.54 6.24 -42.54 47.81 19.30 -15.12 Emerging Markets -11.59 -25.34 66.41 -30.61 -2.37 -6.00 56.28 25.95 34.54 32.59 39.78 -53.18 79.02 19.20 -18.17

One-Year US Fixed 5.93 5.91 4.04 7.33 7.28 3.39 1.47 0.83 2.36 4.32 5.95 4.75 0.80 0.83 0.57 Five-Year US Government

Fixed 7.12 7.75 1.90 8.96 8.44 7.62 2.04 1.35 1.34 3.75 8.16 8.83 0.19 3.73 3.38 Five-Year Global Fixed 7.27 8.41 3.55 8.28 6.44 5.11 1.95 2.65 3.08 4.09 6.31 6.60 2.29 1.99 2.31

• The vast majority of the variation in returns is due to risk factor exposure

• After fees, traditional management typically reduces returns

sensitivity to market [market return minus T-bills]

sensitivity to size [small stocksminus big stocks]

sensitivity to BtM [value stocksminus growth]

randomerror e(t)

++ + +=average expected return [minus T-bills]

average excess return

THE MODEL TELLS THE DIFFERENCE BETWEEN INVESTING AND SPECULATING

Priced Risk • Positive expected return • Systematic • Economic • Long-term • Investing

Unpriced Risk • Noise • Random • Short-term • Speculating.

Structured Exposure to Factors

Unexplained Variation

• Market • Size • Value/Growth

Structure Determines Performance

• Equity Market (complete value-weighted universe of stocks) Stocks tend to have higher expected returns than fixed income over time.

• Company Size (measured by market capitalization) Small company stocks tend to have higher expected returns than large company stocks over time.

• Company Price (measured by ratio of company book value to market equity) Lower-priced “value” stocks tend to have higher expected returns than higher-priced “growth” stocks over time.

Value

Large

Small

Growth

Increased Risk Exposure and Expected Return

Total Stock Market

Decreased Risk Exposure and

Expected Return

Three Dimensions of Stock Returns around the World

Risk and Return are Related

US Large Value

S&P 500

US Large

Growth

US Small Value

CRSP 6-10

US Small

Growth Intl.

Value Intl.

Small MSCI EAFE

Intl. Growth

Emg. Markets

Value

Emg. Markets

Small

Emg. Markets “Market”

Emg. Markets Growth

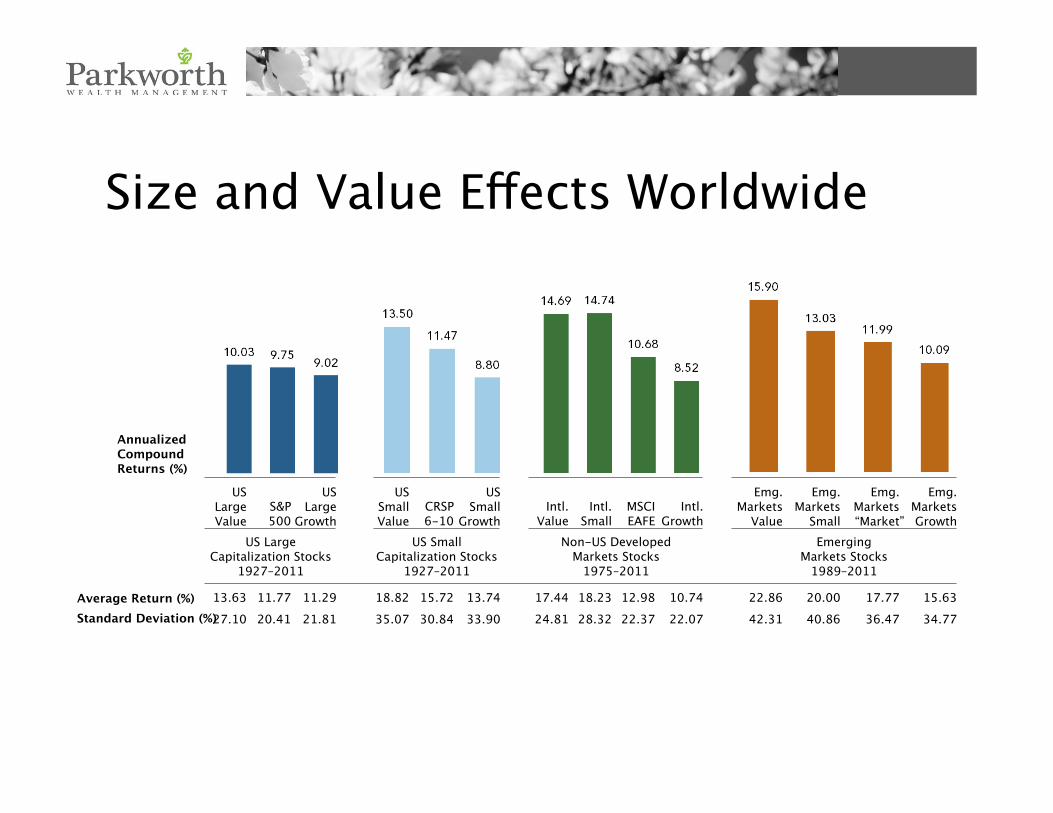

US Large Capitalization Stocks

1927–2011

US Small Capitalization Stocks

1927–2011

Non-US Developed Markets Stocks

1975–2011

Emerging Markets Stocks

1989–2011

13.63 11.77 11.29 18.82 15.72 13.74 17.44 18.23 12.98 10.74 22.86 20.00 17.77 15.63 27.10 20.41 21.81 35.07 30.84 33.90 24.81 28.32 22.37 22.07 42.31 40.86 36.47 34.77

Average Return (%) Standard Deviation (%)

Annualized Compound Returns (%)

Size and Value Effects Worldwide

The Failure of Active ManagementPercentage of Active Public Equity Funds That Failed to Beat the Index Five Years as of June 2011

US Large Cap

US Mid Cap

US Small Cap

Global International

International Small

Emerging Markets

% of

Act

ive

Fund

s Th

at F

aile

d

to O

utpe

rfor

m B

ench

mar

k

Equity Fund Category

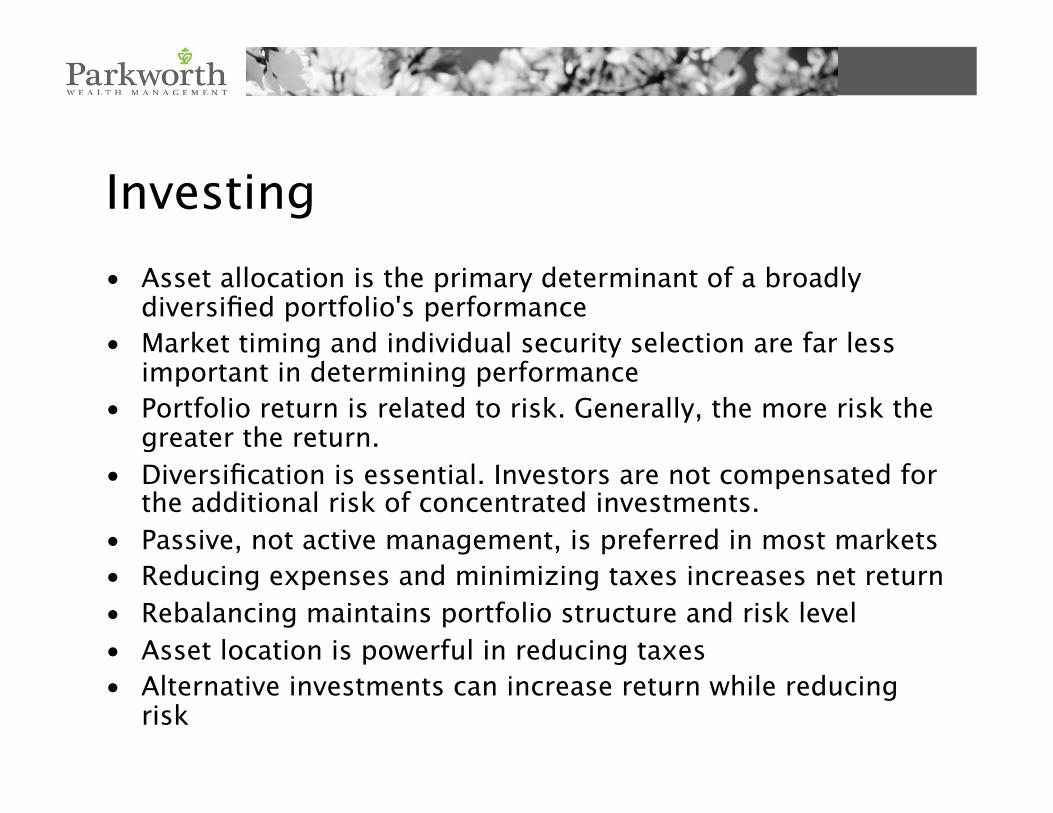

Investing • Asset allocation is the primary determinant of a broadly

diversified portfolio's performance • Market timing and individual security selection are far less

important in determining performance • Portfolio return is related to risk. Generally, the more risk the

greater the return. • Diversification is essential. Investors are not compensated for

the additional risk of concentrated investments. • Passive, not active management, is preferred in most markets • Reducing expenses and minimizing taxes increases net return • Rebalancing maintains portfolio structure and risk level • Asset location is powerful in reducing taxes • Alternative investments can increase return while reducing

risk

Bull and Bear MarketsS&P 500 Index (USD)Daily Returns: January 1, 1926–December 31, 2011

220%

-13%

-85%

20%

-16% -39%

119%

87%

27%

-15% -10%

-13%

100%

44%

-53%

25%

40%

-13% -14%

26%

-25%

22%

-11%

23%

-33%

83%

-11%

99%

-26%

19%

-11% -16%

26%

53%

91%

-13%

121%

-11%

26%

-13%

18%

69%

-21% -11%

44%

-27%

15%

96%

-11%

59%

-27%

-10% -21%

-32%

56%

-12%

38%

-45%

22%

-13%

50%

-13%

38%

-15%

27%

-13%

26%

-10%

21%

-16%

48%

-20%

78%

-11%

156%

-33%

73%

-10%

16%

-19%

303%

-12%

37% 50%

-19% -12%

23%

-11%

13%

-47%

21%

-14%

113%

03/09/2009 -55%

12/31/2011

-11% 1%

Average Duration Bull Market: 413 Days Bear Market: 220 Days

Average Return Bull Market: 58% Bear Market: -21%