Best Ideas Financials 2016 Long Final - Jonathan Casteleyn, Analyst

10

2016/2017 U.S. Financials Jonathan Casteleyn, CFA, CMT - Analyst

description

Best Ideas Long only portfolio in Financials from Jonathan Casteleyn

Transcript of Best Ideas Financials 2016 Long Final - Jonathan Casteleyn, Analyst

2016/2017

U.S. Financials Jonathan Casteleyn, CFA, CMT - Analyst

LONGS Market Cap ($MM)

Dividend Yield Short Interest (% of Float)

Sell Side Sentiment

Fundamental Factor

Rationale Risk Units

Visa (V) $184,000 0.60% 3.8% 80% Positive Quality The Networks perform best late cycle and this defensive business is one of the few groups we like

3

Bank of America (BAC) $168,250 0.25% 1.0% 46% Positive Value Book value of $20 at a 10% normalized ROE is $2 in EPS – Street is at $1.30

3

Mastercard (MA) $110,000 0.66% 1.1% 79% Positive Quality The Networks perform best late cycle and International networks grow faster than U.S.

3

Goldman Sachs (GS) $78,000 1.3% 1.9% 21% Positive Quality Like GS as a Pair with short MS with higher operating leverage at GS and better exposure to M&A

2

Allianz SE (ALV) $67,000 3.6% 0.5% 51% Positive Value PIMCO outflows are waning and performance is improving – great time to own this value insurer with a dividend yield

3

Capital One (COF) $48,200 1.4% 1.3% 72% Positive Value Still cheap at 10x earnings in one of the few growing U.S. loan categories

1

CME Group (CME) $29,000 2.1% 2.1% 31% Positive Quality Prime beneficiary of renewed volatility in the US – good pair against short ICE

3

Invesco (IVZ) $16,697 2.6% 1.6% 53% Positive Quality Improving distribution – UK retail fears well discounted

2

FNF Group (FNF) $10,000 2.3% 2.1% 77% Positive Quality Great way to invest in housing theme - great mgmt and buying back lots of stock - Black Knight worth $10 per share

3

NASDAQ OMX (NDAQ) $6,700 1.5% 5.3% 61% Positive Value 40% of market share trades off exchange which will change

3

eTrade (ETFC) $6,500 0.0% 3.8% 60% Positive Momentum A potential takeout candidate with US retail back – loan book is improving

1

Och Ziff (OZM) $6,300 6.8% 1.6% 66% Positive Yield Alts have a massive tailwind with Pension reallocation – 10% fully loaded dividend yield too

2

Legg Mason (LM) $6,000 1.2% 7.0% 26% Positive Value Pension reallocation helps them with still high short interest and low sell side sentiment in this stock

3

Zions Bancorp (ZION) $5,537 0.5% 6.4% 24% Positive Value Regional banks can grow their loan segments with the big banks in the penalty box – ZION still under book value

3

Federated Investors (FII) $3,400 3.0% 9.0% 15% Positive Value My EPS opportunity is 15% above the Street and sentiment is way too low

2

KB Homes (KBH) $1,400 0.6% 19.7% 25% Positive Value PHS is turning up which should pull housing equities with it. KBH is a value name out of favor

2

Beazer Homes (BZH) $500 0.0% 17.6% 30% Positive Value PHS is turning up which should pull housing equities with it.

2

Market Thesis: After a volatile 2015 with our call for the market to be “down a little” looking prescient,

we are now calling for a more substantial equity market decline in 2016. Late cycle indicators are

flashing more brightly and with the Federal Reserve “boxed” in for a rate hike in the New Year, the

effectiveness of quantitative easing will now reverse. U.S. corporate earnings have tripped into

recession with the second consecutive quarter of negative growth in the current 3Q15 earnings season.

The Street however is not heeding this warning and is still modeling mid-single digit corporate earnings

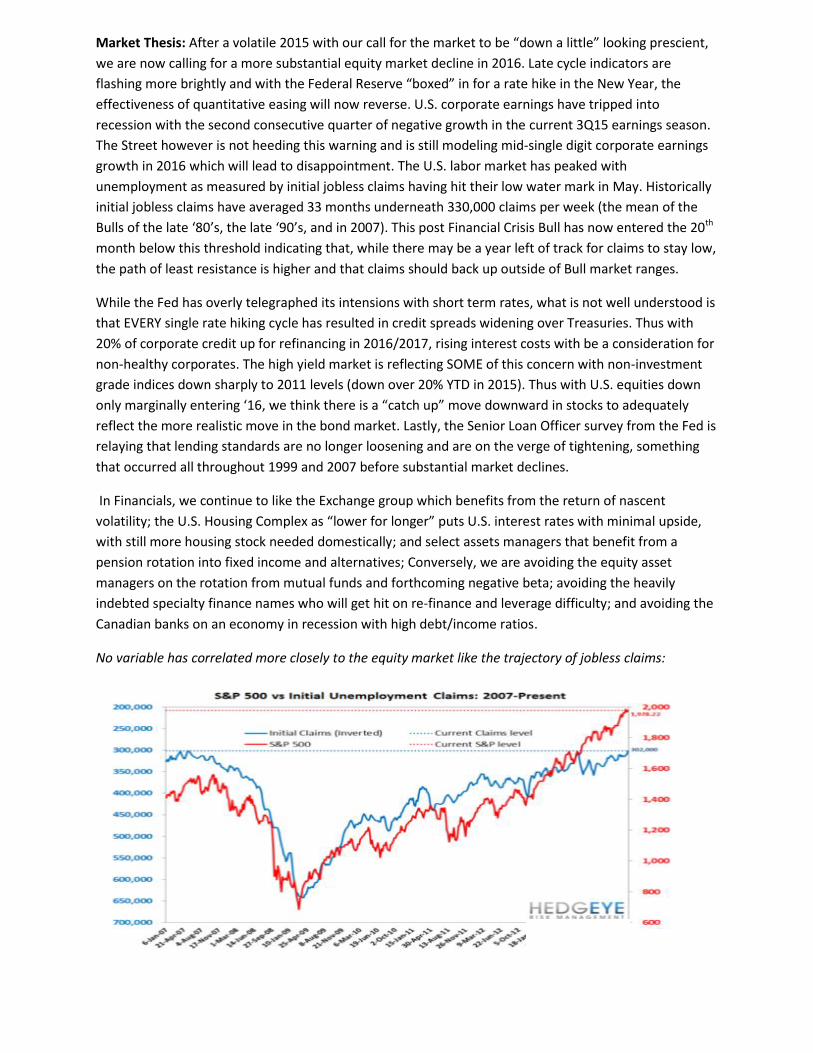

growth in 2016 which will lead to disappointment. The U.S. labor market has peaked with

unemployment as measured by initial jobless claims having hit their low water mark in May. Historically

initial jobless claims have averaged 33 months underneath 330,000 claims per week (the mean of the

Bulls of the late ‘80’s, the late ‘90’s, and in 2007). This post Financial Crisis Bull has now entered the 20th

month below this threshold indicating that, while there may be a year left of track for claims to stay low,

the path of least resistance is higher and that claims should back up outside of Bull market ranges.

While the Fed has overly telegraphed its intensions with short term rates, what is not well understood is

that EVERY single rate hiking cycle has resulted in credit spreads widening over Treasuries. Thus with

20% of corporate credit up for refinancing in 2016/2017, rising interest costs with be a consideration for

non-healthy corporates. The high yield market is reflecting SOME of this concern with non-investment

grade indices down sharply to 2011 levels (down over 20% YTD in 2015). Thus with U.S. equities down

only marginally entering ‘16, we think there is a “catch up” move downward in stocks to adequately

reflect the more realistic move in the bond market. Lastly, the Senior Loan Officer survey from the Fed is

relaying that lending standards are no longer loosening and are on the verge of tightening, something

that occurred all throughout 1999 and 2007 before substantial market declines.

In Financials, we continue to like the Exchange group which benefits from the return of nascent

volatility; the U.S. Housing Complex as “lower for longer” puts U.S. interest rates with minimal upside,

with still more housing stock needed domestically; and select assets managers that benefit from a

pension rotation into fixed income and alternatives; Conversely, we are avoiding the equity asset

managers on the rotation from mutual funds and forthcoming negative beta; avoiding the heavily

indebted specialty finance names who will get hit on re-finance and leverage difficulty; and avoiding the

Canadian banks on an economy in recession with high debt/income ratios.

No variable has correlated more closely to the equity market like the trajectory of jobless claims:

…and the year-over-year improvement in jobless claims peaked in May and is now converging towards

zero:

…and Bull Market levels below 330,000 per week is getting long in the tooth now eclipsing over 20

months:

During the start of the past 7 rate hiking cycles, high yield spreads over Treasuries have widen EVERY

single time between 200-2,000 basis points (yellow line – right hand scale)

The Fed’s Senior Loan Officer Survey has been leading/concident with the trajectory of the Financials

sector. C&I lending standards peaked (loosened most) in 2014 and are on the verge of tightening which

they did all throughout 1999 and 2007:

Corporate earnings are entering a recession in 3Q15 with then an unrealistic recovery to mid single digit

growth in 2016 (some of this will be “comping the negative comp”):

And some thing has to give with High Yield prices at 2011 levels with U.S. equities only marginally off

their highs (either high yield prices rise and equities make new highs or equities need a “catch up” trade

downward):

A recent Barron’s contributor outlined that 20% of corporate credit needs to be refinanced in 2016/2017

which means widening credit spreads matter:

Late Cycle Financial subgroup outperformers include Fin Tech, Exchanges, and Credit Card companies.

Convesely, the Debt Collectors, Mortgage Finance, and Auto Insurers perform poorly:

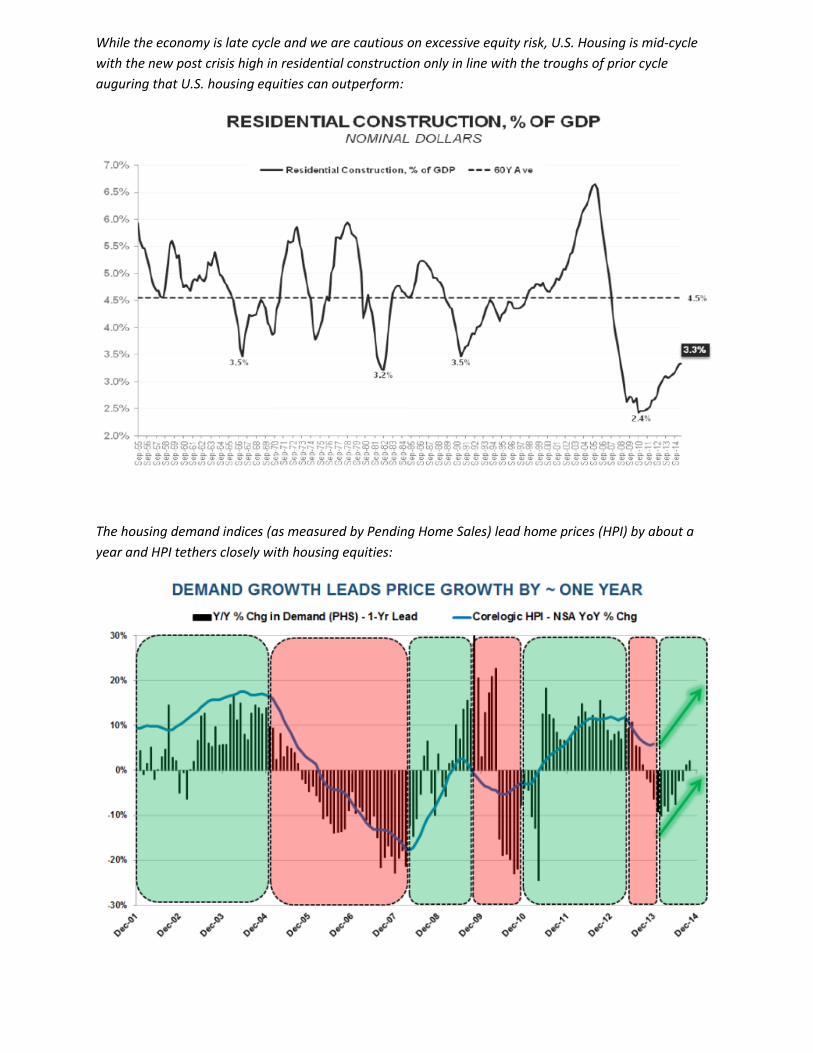

While the economy is late cycle and we are cautious on excessive equity risk, U.S. Housing is mid-cycle

with the new post crisis high in residential construction only in line with the troughs of prior cycle

auguring that U.S. housing equities can outperform:

The housing demand indices (as measured by Pending Home Sales) lead home prices (HPI) by about a

year and HPI tethers closely with housing equities:

And U.S. HPI is positively inflecting again which will push U.S. Housing equities higher:

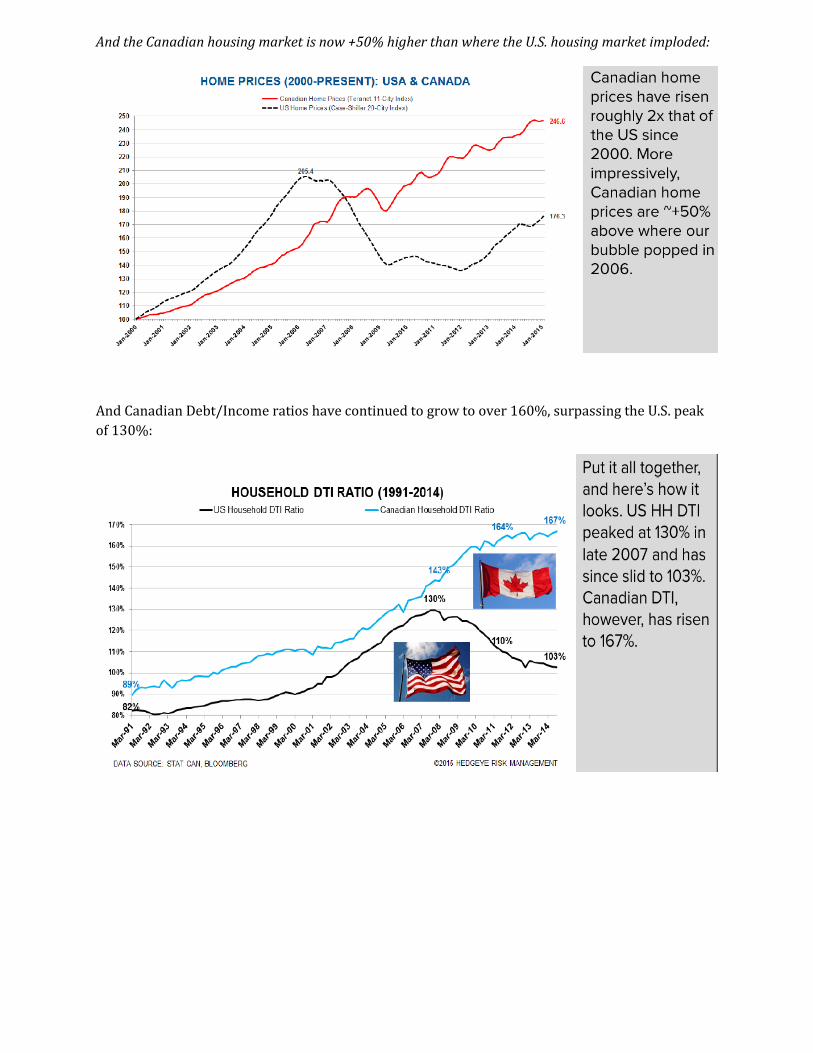

The landscape North of the Border is in an inverse state with high leverage in the system and

Canadian banks now posing a risk to the economy:

And the Canadian housing market is now +50% higher than where the U.S. housing market imploded:

And Canadian Debt/Income ratios have continued to grow to over 160%, surpassing the U.S. peak

of 130%: