Benchmarking and Best Practices Survey Results BRD ...

12

1 2013-2014 BREWERS’ RESOURCE DIRECTORY BREWERS’ RESOURCE DIRECTORY BRD 2013-2014 BENCHMARKING AND BESTPRACTICES SURVEY RESULTS BREWERS ASSOCIATION MEMBERS-ONLY EXCLUSIVE CONTENT • BREWERS ASSOCIATION MEMBERS-ONLY EXCLUSIVE CONTENT • BREWERS ASSOCIATION MEMBERS-ONLY EXCLUSIVE CONTENT • BREWERS ASSOCIATION MEMBERS The Brewers Association (BA) conducted a comprehensive survey of America’s craft brewers to establish and share industry benchmarks and best practices. This survey was developed in response to BA member requests for hard data that they could use to measure their businesses and in turn make them more efficient and successful. 2012 survey questions were revised slightly from the 2010 edition; importantly, the 2012 survey now includes the BA salary survey as well. Results were compiled and aggregated by BA staff. The results provide a valuable set of tools specific to America’s small and independent craft brewers. This section contains the highlights of the 2012 survey and newly a sampling of the BA salary survey results. Remaining data and more detailed in-depth salary information will be available in the Members-Only section of BrewersAssociation.org. Thank you to all who participated and may you find value in these results to help you grow with the industry. This is, indeed, an exciting time to be part of the craft beer community! Sincerely, Paul Gatza Brewers Association Kristi Switzer Brewers Publications Chris Swersey Technical Brewing Projects Coordinator

Transcript of Benchmarking and Best Practices Survey Results BRD ...

12013-2014 Brewers’ resource Directory

BREWERS’ RESOURCE DIRECTORYBRD2013-2014

BENCHMARKING AND BESTPRACTICES

SURVEY RESULTS• BREWERS ASSOCIATION MEMBERS-ONLY EXCLUSIVE CONTENT • BREWERS ASSOCIATION MEMBERS-ONLY EXCLUSIVE CONTENT • BREWERS ASSOCIATION MEMBERS-ONLY EXCLUSIVE CONTENT • BREWERS ASSOCIATION MEMBERS-ONLY EXCLUSIVE CONTENT

BREWERSASSOCIATION.ORG 107

Benchmarking and Best Practices Survey Results

BENCHMARKING AND BESTPRACTICES SURVEY RESULTS

The Brewers Association (BA) conducted a comprehensive survey of America’s craft brewers to establish and share industry benchmarks and best

practices. This survey was developed in response to BA member requests for hard data that they could use to measure their businesses and in turn make

them more efficient and successful.

2012 survey questions were revised slightly from the 2010 edition; importantly, the 2012 survey now includes the BA salary survey as well. Results were

compiled and aggregated by BA staff. The results provide a valuable set of tools specific to America’s small and independent craft brewers.

This section contains the highlights of the 2012 survey and newly a sampling of the BA salary survey results. Remaining data and more detailed in-depth

salary information will be available in the Members-Only section of BrewersAssociation.org.

Thank you to all who participated and may you find value in these results to help you grow with the industry. This is, indeed, an exciting time to be part of

the craft beer community!

Sincerely,

Paul Gatza

Brewers Association

Kristi Switzer

Brewers Publications

Chris Swersey

Technical Brewing Projects Coordinator

Benchmarking and Best Practices Survey Results

22013-2014 Brewers’ resource Directory

Benchmarking and Best Practices Survey Results

108 2013-2014 BREWERS’ RESOURCE DIRECTORY

Key

Anonymity The Brewers Association places great value on the anonymity of survey respondents. Many survey questions were of

a highly sensitive nature. Not all respondents chose to answer all questions. The answers to questions with very low

participation rates are shown with less detail (for example, not broken down by region, or not organized by company

size), or may be shown on a per barrel basis (based on 2011 reported production) in order to protect the identity of

the companies that answered these questions. The answer u/r (“unreported”), indicates an answer that is not provided

in order to protect the anonymity of survey respondents.

Bonus For purposes of this survey, “Bonus” includes all non-wage compensation such as bonus, profit sharing, commissions,

tips, etc.

Brewery Production For purposes of this survey, these are Brewmaster/Head Brewers, Shift Brewers, Cellarmen, QA/QC/Sensory, Lab and

Employees R&D employees.

Brewpub The Brewers Association defines a brewpub as follows: A restaurant-brewery that sells 25% or more of its company-

owned production onsite. The beer is brewed primarily for sale in the restaurant and bar. The beer is often dispensed

directly from the brewery’s storage tanks. Where allowed by law, brewpubs often sell beer “to go” and/or distribute to

off site accounts.

Brewpub Sizes Brewpubs were grouped based on their reported 2011 production figures in US Barrels. Groups were chosen in order

to even out the number of responses within each size group. Many answers to survey questions are published on a

per barrel basis, making identification of individual respondents impossible. Brewpubs with more than one location

were given the option of answering questions in aggregate form, or based on average value per store values. Unless

otherwise noted, survey answers are reported on a per store basis.

Full-Time Employee For purposes of this survey, full-time employees are those working >30 hours per week or salaried. Full-time employee

compensation reported as hourly wages was converted to a yearly figure by multiplying the reported hourly wage by

1,560 (52*30).

Max The largest value among all responses

Mean The “average” value of survey responses to a given question. The total of all responses given, divided by the number

of responses

Median The “middle” response. An equal number of larger and smaller values were given as responses

Min The smallest value among all responses

Mode The most common answer to a question

Non-Production, Sales For purposes of this survey, these are Owners/Proprietors, Professional Services (Accounting, Legal, Engineering,

and Marketing Employees other), Administrative, Sustainability, HR, PR, other, Marketing/Advertising/Sales Managers or Staff, Material

Ordering/Order Fulfillment/Warehouse/Logistics/Maintenance/All Others

Part-Time Employee For purposes of this survey, full-time employees are those working <30 hours per week or salaried. Part-time employee

compensation reported as hourly wages was converted to a yearly figure by multiplying the reported hourly wage by

780 (52*15).

Production Brewery A production brewery, contract brewing company or alternating proprietorship that is not a brewpub.

Production Brewery Sizes Production breweries were grouped based on their reported 2011 total production figures in US Barrels. Group

volume breaks were chosen in order to roughly even out the number of responses within each size group. The largest

category of production breweries (with 2011 production >50,000 US Barrels) contained the smallest number of

responses. In order to maintain the confidentiality of individual respondents, answers within this group are often

published as an entire group, with less detail than other groups. Many answers to survey questions are published on

a per barrel basis, making identification of individual respondents impossible. All production brewery respondents

entered their information in aggregate form.

Respondents The survey included US craft brewers as defined by the Brewers Association. Datasets that did not include 2011

production data were removed. 288 total datasets were included in the analysis.

Benchmarking and Best Practices Survey Results

32013-2014 Brewers’ resource DirectoryBREWERSASSOCIATION.ORG 109

Benchmarking and Best Practices Survey Results

Midwest Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota, Wisconsin

Mountain West Arizona, Colorado, Nevada, New Mexico, Utah, Wyoming

Northeast Connecticut, Delaware, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island, Vermont, Virginia, Wash-ington DC, West Virginia

Paci�c California, Hawaii

Paci�c NW Alaska, Idaho, Montana, Oregon, Washington

South Arkansas, Florida, Georgia, Kentucky, Louisiana, Mississippi, North Carolina, Oklahoma, South Carolina, Tennessee, Texas

Regions For the purposes of this survey, states were assigned to generally accepted definitions of regions, with a few exceptions that allowed

for more even numbers of responses among the regions. Regions are usually tabulated alphabetically.

Midwest Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota, Wisconsin

Mountain West Arizona, Colorado, Nevada, New Mexico, Utah, Wyoming

Northeast Connecticut, Delaware, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island,

Vermont, Virginia, Washington DC, West Virginia

Pacific California, Hawaii

Pacific NW Alaska, Idaho, Montana, Oregon, Washington

South Alabama, Arkansas, Florida, Georgia, Kentucky, Louisiana, Mississippi, North Carolina, Oklahoma, South Carolina, Tennessee, Texas

Restaurant Employees For purposes of these survey, these are grouped as Chefs/Kitchen Managers (back-of-house), Wait Staff and Bar Managers

(front-of-house), Cooks, Dishwashers, other (back-of-house), Wait Staff, Bar Staff, Bussers, Host-Greeters, other (front-of-

house).

Salary/Hourly Wages For purposes of this survey, salary/hourly wages consists of base compensation paid to employees, not including bonus, profit

sharing, comissions, tips, etc.

42013-2014 Brewers’ resource Directory

Benchmarking and Best Practices Survey Results

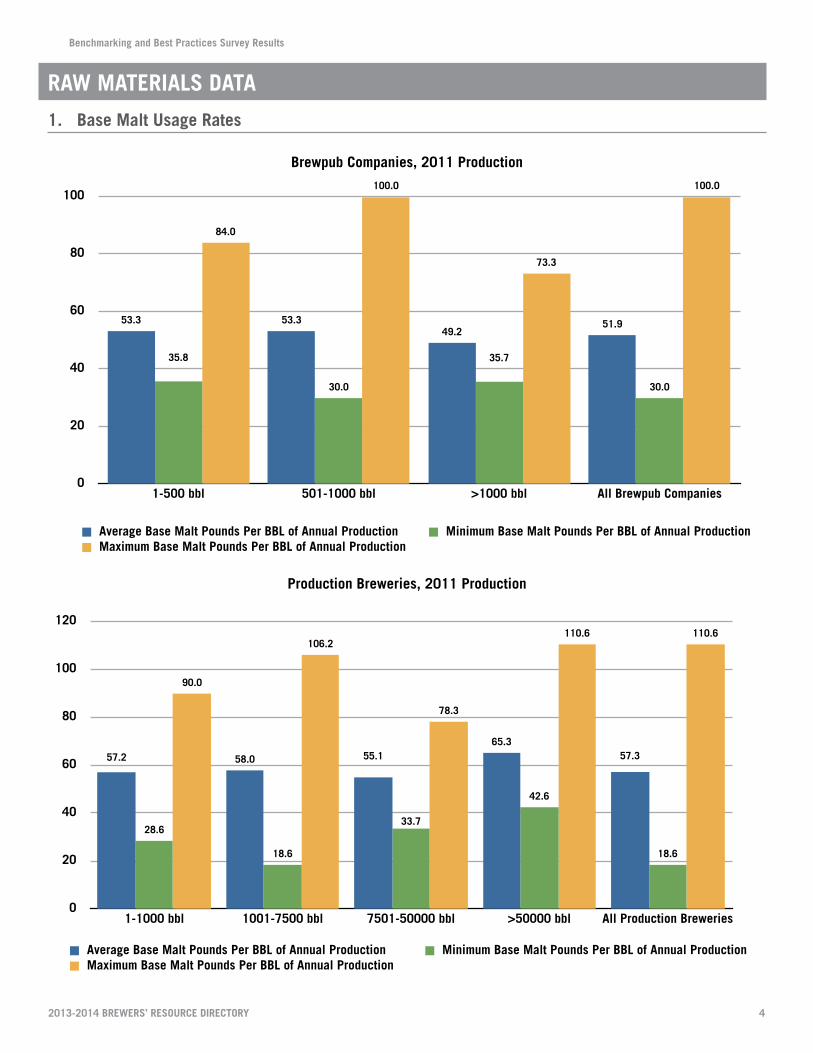

Raw MateRialS Data

1. Base Malt Usage Rates

Brewpub Companies, 2011 Production

0

20

40

60

80

100

1-500 bbl 501-1000 bbl >1000 bbl All Brewpub Companies

100.0

73.3

100.0

84.0

30.0

35.7

30.0

35.8

51.949.2

53.353.3

Average Base Malt Pounds Per BBL of Annual Production Minimum Base Malt Pounds Per BBL of Annual ProductionMaximum Base Malt Pounds Per BBL of Annual Production

Production Breweries, 2011 Production

0%

20%

40%

60%

80%

100%

Multiple Brewing Shifts Multiple Packaging Shifts

27%

63%

82%

100%

46%

100%

17%

69%

5%10%

1-1000 bbl 1001-7500 bbl 7501-50000 bbl >50000 bbl All Production Breweries

0

20

40

60

80

100

120

1-1000 bbl 1001-7500 bbl 7501-50000 bbl >50000 bbl All Production Breweries

110.6110.6

78.3

106.2

90.0

18.6

42.6

33.7

18.6

28.6

57.365.3

55.158.057.2

Average Base Malt Pounds Per BBL of Annual Production Minimum Base Malt Pounds Per BBL of Annual ProductionMaximum Base Malt Pounds Per BBL of Annual Production

Benchmarking and Best Practices Survey Results

52013-2014 Brewers’ resource Directory

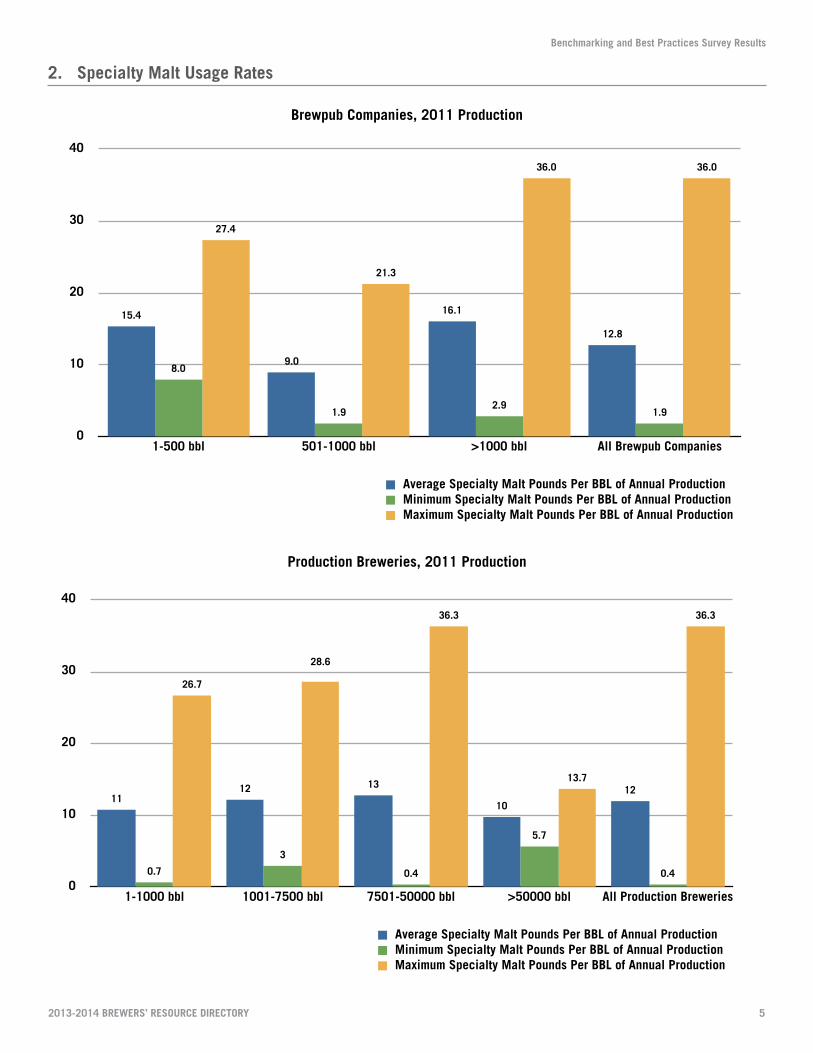

2. Specialty Malt Usage Rates

Brewpub Companies, 2011 Production

0

10

20

30

40

1-500 bbl 501-1000 bbl >1000 bbl All Brewpub Companies

36.036.0

21.3

27.4

1.92.9

1.9

8.0

12.8

16.1

9.0

15.4

Average Specialty Malt Pounds Per BBL of Annual ProductionMinimum Specialty Malt Pounds Per BBL of Annual ProductionMaximum Specialty Malt Pounds Per BBL of Annual Production

Production Breweries, 2011 Production

0%

20%

40%

60%

80%

100%

Multiple Brewing Shifts Multiple Packaging Shifts

27%

63%

82%

100%

46%

100%

17%

69%

5%10%

1-1000 bbl 1001-7500 bbl 7501-50000 bbl >50000 bbl All Production Breweries

0

10

20

30

40

1-1000 bbl 1001-7500 bbl 7501-50000 bbl >50000 bbl All Production Breweries

36.3

13.7

36.3

28.6

26.7

0.4

5.7

0.4

3

0.7

12

10

131211

Average Specialty Malt Pounds Per BBL of Annual ProductionMinimum Specialty Malt Pounds Per BBL of Annual ProductionMaximum Specialty Malt Pounds Per BBL of Annual Production

Benchmarking and Best Practices Survey Results

62013-2014 Brewers’ resource Directory

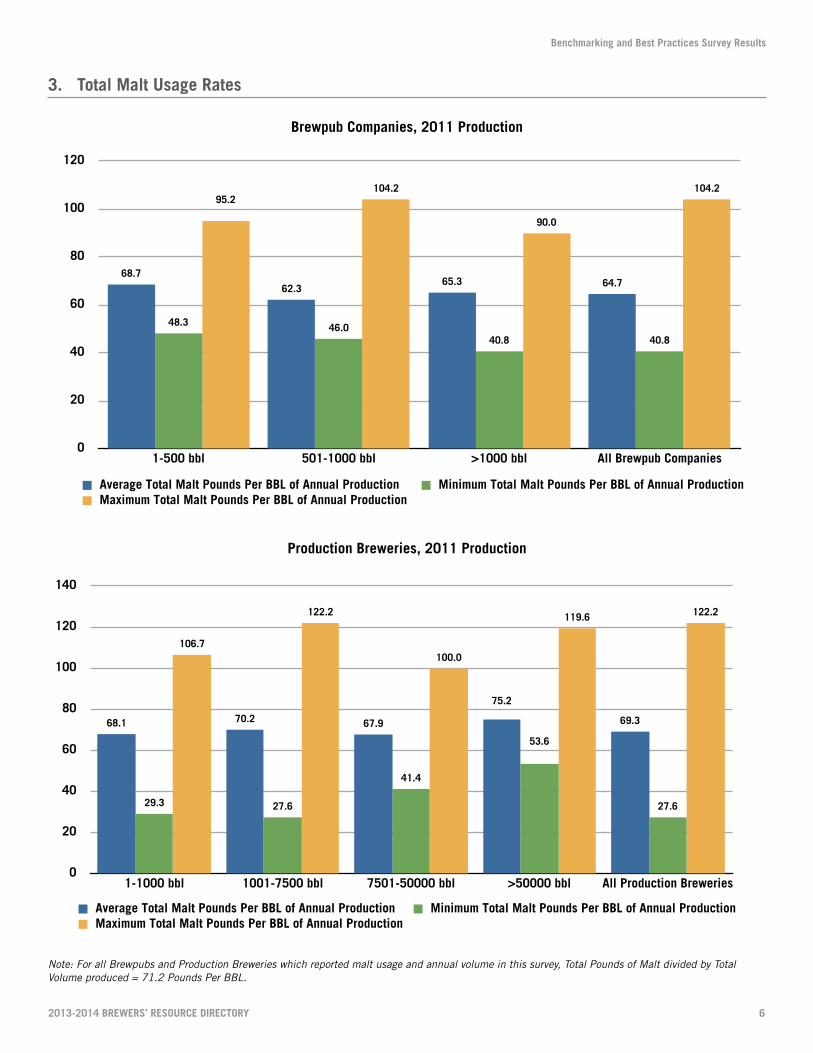

3. total Malt Usage Rates

Brewpub Companies, 2011 Production

0

20

40

60

80

100

120

1-500 bbl 501-1000 bbl >1000 bbl All Brewpub Companies

104.2

90.0

104.295.2

40.840.846.048.3

64.765.362.3

68.7

Average Total Malt Pounds Per BBL of Annual Production Minimum Total Malt Pounds Per BBL of Annual ProductionMaximum Total Malt Pounds Per BBL of Annual Production

Production Breweries, 2011 Production

0%

20%

40%

60%

80%

100%

Multiple Brewing Shifts Multiple Packaging Shifts

27%

63%

82%

100%

46%

100%

17%

69%

5%10%

1-1000 bbl 1001-7500 bbl 7501-50000 bbl >50000 bbl All Production Breweries

0

20

40

60

80

100

120

140

1-1000 bbl 1001-7500 bbl 7501-50000 bbl >50000 bbl All Production Breweries

122.2119.6

100.0

122.2

106.7

27.6

53.6

41.4

27.629.3

69.3

75.2

67.970.268.1

Average Total Malt Pounds Per BBL of Annual Production Minimum Total Malt Pounds Per BBL of Annual ProductionMaximum Total Malt Pounds Per BBL of Annual Production

Note: For all Brewpubs and Production Breweries which reported malt usage and annual volume in this survey, Total Pounds of Malt divided by Total Volume produced = 71.2 Pounds Per BBL.

Benchmarking and Best Practices Survey Results

72013-2014 Brewers’ resource Directory

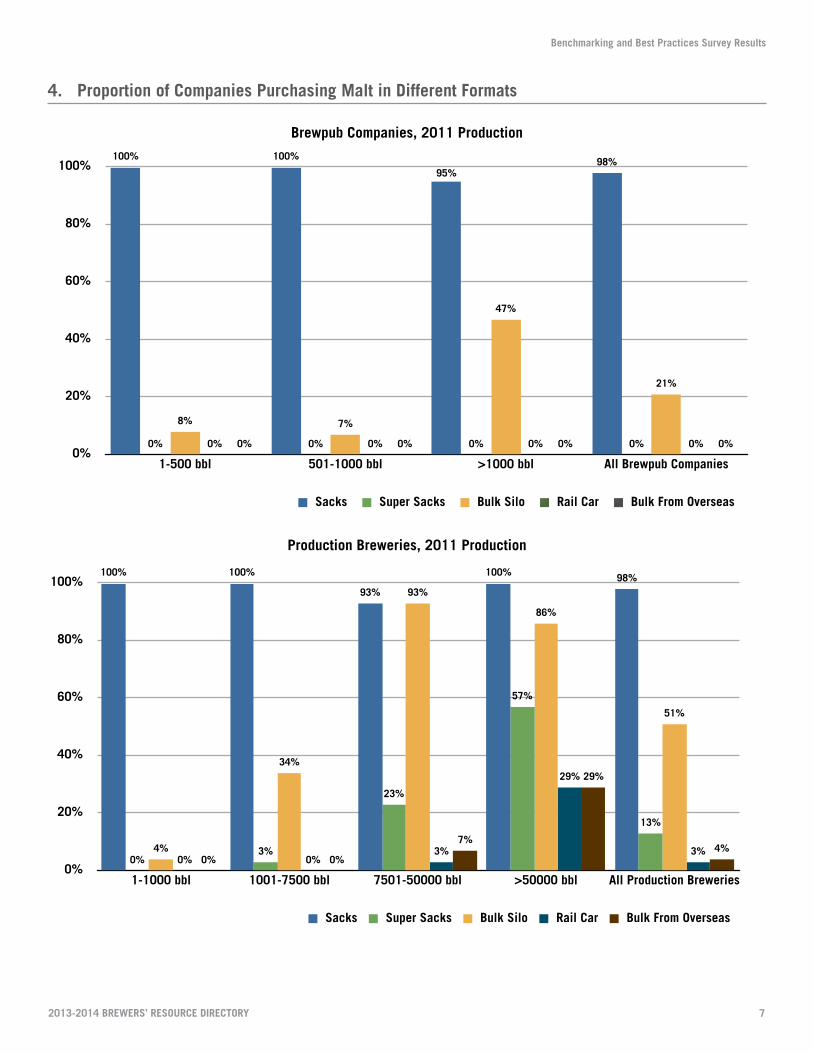

4. Proportion of Companies Purchasing Malt in Different Formats

Brewpub Companies, 2011 Production

0%

20%

40%

60%

80%

100%

1-500 bbl 501-1000 bbl >1000 bbl All Brewpub Companies

0%0%0%0% 0%0%0%0%

21%

47%

7%8%

0%0%0%0%

98%95%

100%100%

Sacks Super Sacks Bulk Silo Rail Car Bulk From Overseas

Production Breweries, 2011 Production

0%

20%

40%

60%

80%

100%

Multiple Brewing Shifts Multiple Packaging Shifts

27%

63%

82%

100%

46%

100%

17%

69%

5%10%

1-1000 bbl 1001-7500 bbl 7501-50000 bbl >50000 bbl All Production Breweries

0%

20%

40%

60%

80%

100%

1-1000 bbl 1001-7500 bbl 7501-50000 bbl >50000 bbl All Production Breweries

4%

29%

7%

0%0%3%

29%

3%0%0%

51%

86%

93%

34%

4%

13%

57%

23%

3%0%

98%100%

93%

100%100%

Sacks Super Sacks Bulk Silo Rail Car Bulk From Overseas

Benchmarking and Best Practices Survey Results

82013-2014 Brewers’ resource Directory

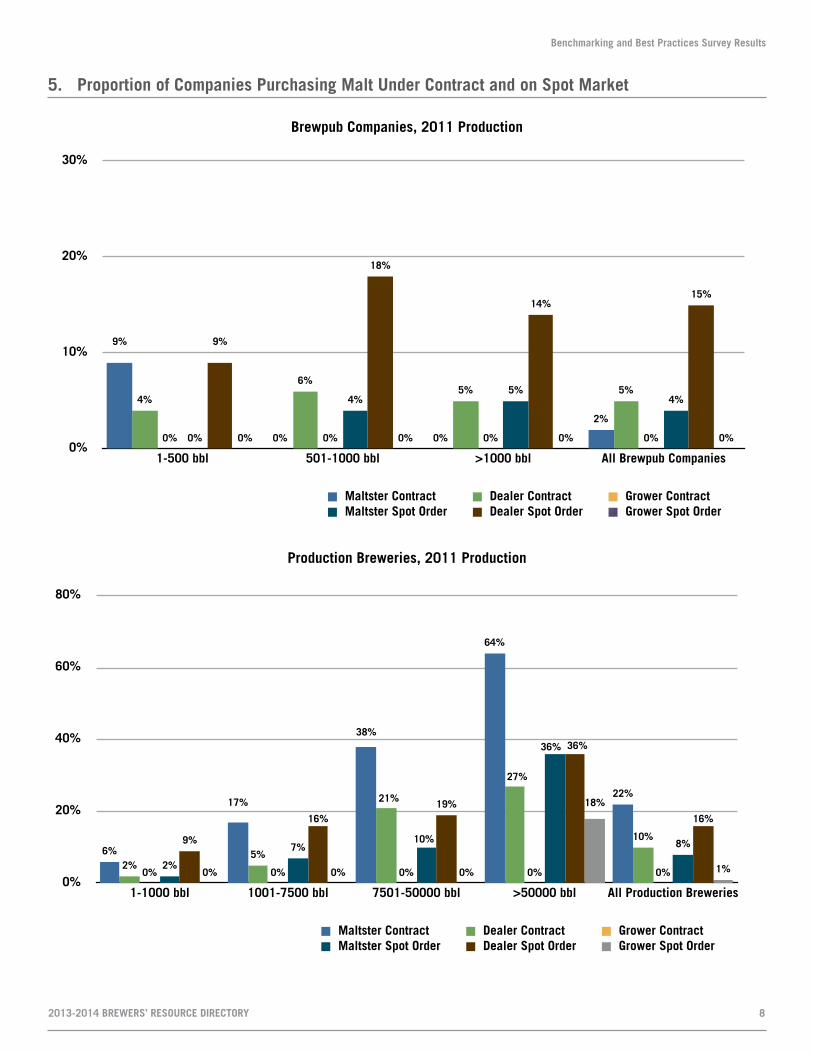

5. Proportion of Companies Purchasing Malt Under Contract and on Spot Market

Brewpub Companies, 2011 Production

0%

10%

20%

30%

1-500 bbl 501-1000 bbl >1000 bbl All Brewpub Companies

0%0%0%0%

15%14%

18%

9%

4%5%

4%

0% 0%0%0%0%

5%5%6%

4%

2%

0%0%

9%

Maltster Contract Dealer Contract Grower ContractMaltster Spot Order Dealer Spot Order Grower Spot Order

Production Breweries, 2011 Production

0%

20%

40%

60%

80%

100%

Multiple Brewing Shifts Multiple Packaging Shifts

27%

63%

82%

100%

46%

100%

17%

69%

5%10%

1-1000 bbl 1001-7500 bbl 7501-50000 bbl >50000 bbl All Production Breweries

0%

20%

40%

60%

80%

1-1000 bbl 1001-7500 bbl 7501-50000 bbl >50000 bbl All Production Breweries

1%

18%

0%0%0%

16%

36%

19%16%

9% 8%

36%

10%7%

2%0%0%0%0%0%

10%

27%

21%

5%2%

22%

64%

38%

17%

6%

Maltster Contract Dealer Contract Grower ContractMaltster Spot Order Dealer Spot Order Grower Spot Order

Benchmarking and Best Practices Survey Results

92013-2014 Brewers’ resource Directory

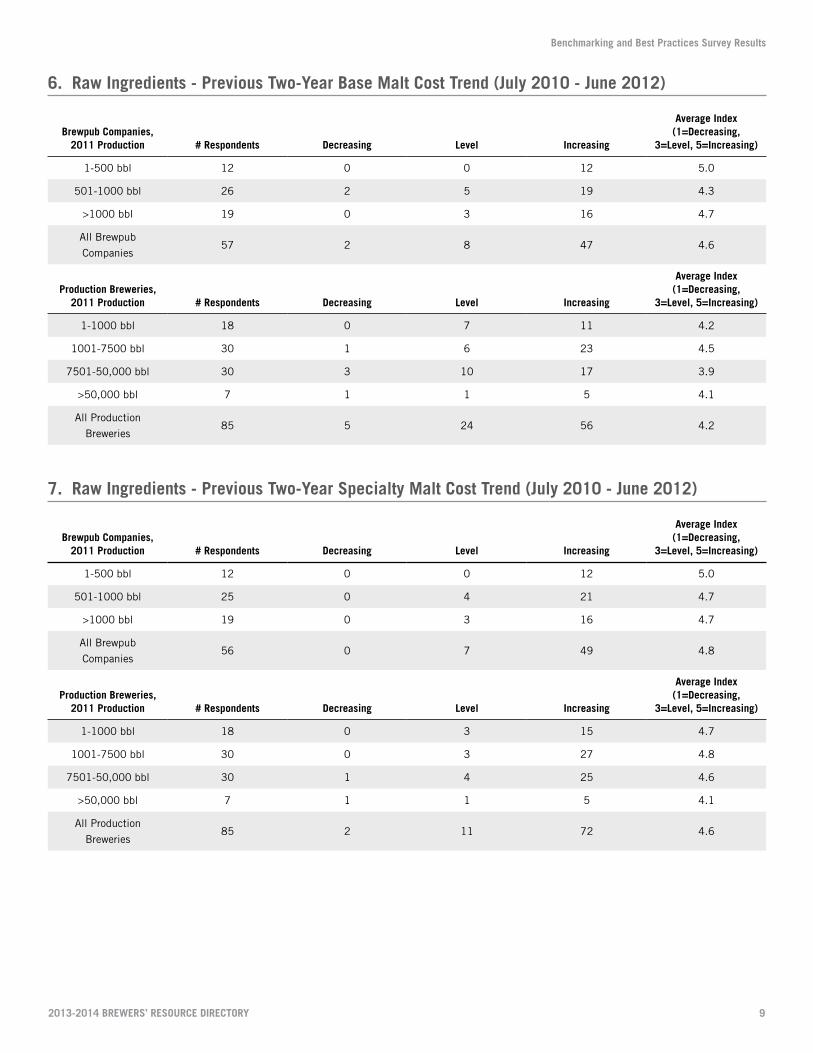

6. Raw ingredients - Previous two-Year Base Malt Cost trend (July 2010 - June 2012)

Brewpub Companies, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-500 bbl 12 0 0 12 5.0

501-1000 bbl 26 2 5 19 4.3

>1000 bbl 19 0 3 16 4.7

All Brewpub

Companies57 2 8 47 4.6

Production Breweries, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-1000 bbl 18 0 7 11 4.2

1001-7500 bbl 30 1 6 23 4.5

7501-50,000 bbl 30 3 10 17 3.9

>50,000 bbl 7 1 1 5 4.1

All Production

Breweries85 5 24 56 4.2

7. Raw ingredients - Previous two-Year Specialty Malt Cost trend (July 2010 - June 2012)

Brewpub Companies, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-500 bbl 12 0 0 12 5.0

501-1000 bbl 25 0 4 21 4.7

>1000 bbl 19 0 3 16 4.7

All Brewpub

Companies56 0 7 49 4.8

Production Breweries, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-1000 bbl 18 0 3 15 4.7

1001-7500 bbl 30 0 3 27 4.8

7501-50,000 bbl 30 1 4 25 4.6

>50,000 bbl 7 1 1 5 4.1

All Production

Breweries85 2 11 72 4.6

Benchmarking and Best Practices Survey Results

102013-2014 Brewers’ resource Directory

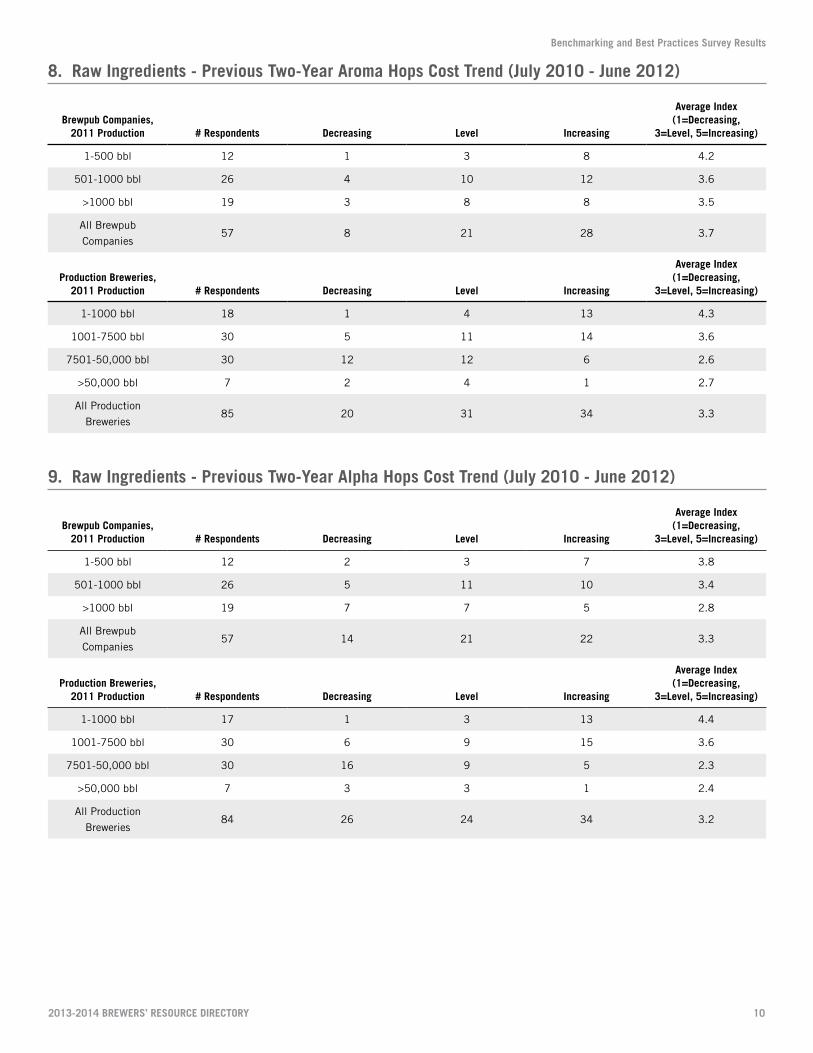

8. Raw ingredients - Previous two-Year aroma Hops Cost trend (July 2010 - June 2012)

Brewpub Companies, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-500 bbl 12 1 3 8 4.2

501-1000 bbl 26 4 10 12 3.6

>1000 bbl 19 3 8 8 3.5

All Brewpub

Companies57 8 21 28 3.7

Production Breweries, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-1000 bbl 18 1 4 13 4.3

1001-7500 bbl 30 5 11 14 3.6

7501-50,000 bbl 30 12 12 6 2.6

>50,000 bbl 7 2 4 1 2.7

All Production

Breweries85 20 31 34 3.3

9. Raw ingredients - Previous two-Year alpha Hops Cost trend (July 2010 - June 2012)

Brewpub Companies, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-500 bbl 12 2 3 7 3.8

501-1000 bbl 26 5 11 10 3.4

>1000 bbl 19 7 7 5 2.8

All Brewpub

Companies57 14 21 22 3.3

Production Breweries, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-1000 bbl 17 1 3 13 4.4

1001-7500 bbl 30 6 9 15 3.6

7501-50,000 bbl 30 16 9 5 2.3

>50,000 bbl 7 3 3 1 2.4

All Production

Breweries84 26 24 34 3.2

Benchmarking and Best Practices Survey Results

112013-2014 Brewers’ resource Directory

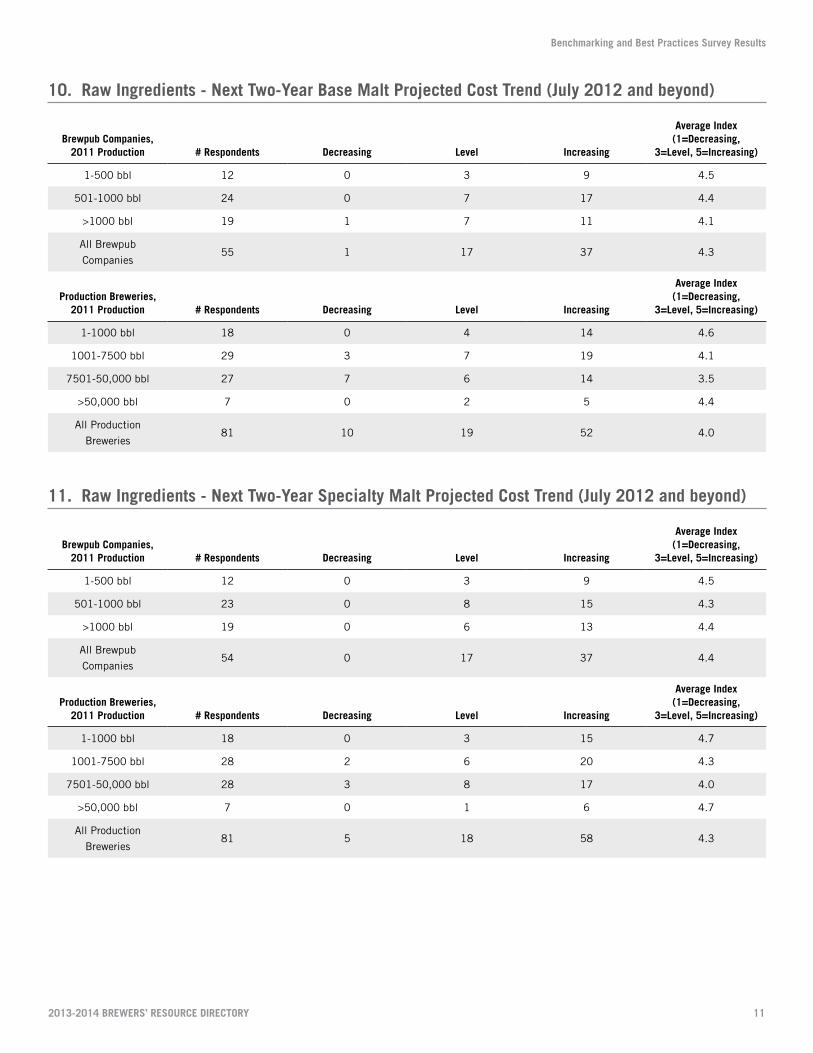

10. Raw ingredients - Next two-Year Base Malt Projected Cost trend (July 2012 and beyond)

Brewpub Companies, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-500 bbl 12 0 3 9 4.5

501-1000 bbl 24 0 7 17 4.4

>1000 bbl 19 1 7 11 4.1

All Brewpub

Companies55 1 17 37 4.3

Production Breweries, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-1000 bbl 18 0 4 14 4.6

1001-7500 bbl 29 3 7 19 4.1

7501-50,000 bbl 27 7 6 14 3.5

>50,000 bbl 7 0 2 5 4.4

All Production

Breweries81 10 19 52 4.0

11. Raw ingredients - Next two-Year Specialty Malt Projected Cost trend (July 2012 and beyond)

Brewpub Companies, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-500 bbl 12 0 3 9 4.5

501-1000 bbl 23 0 8 15 4.3

>1000 bbl 19 0 6 13 4.4

All Brewpub

Companies54 0 17 37 4.4

Production Breweries, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-1000 bbl 18 0 3 15 4.7

1001-7500 bbl 28 2 6 20 4.3

7501-50,000 bbl 28 3 8 17 4.0

>50,000 bbl 7 0 1 6 4.7

All Production

Breweries81 5 18 58 4.3

Benchmarking and Best Practices Survey Results

12

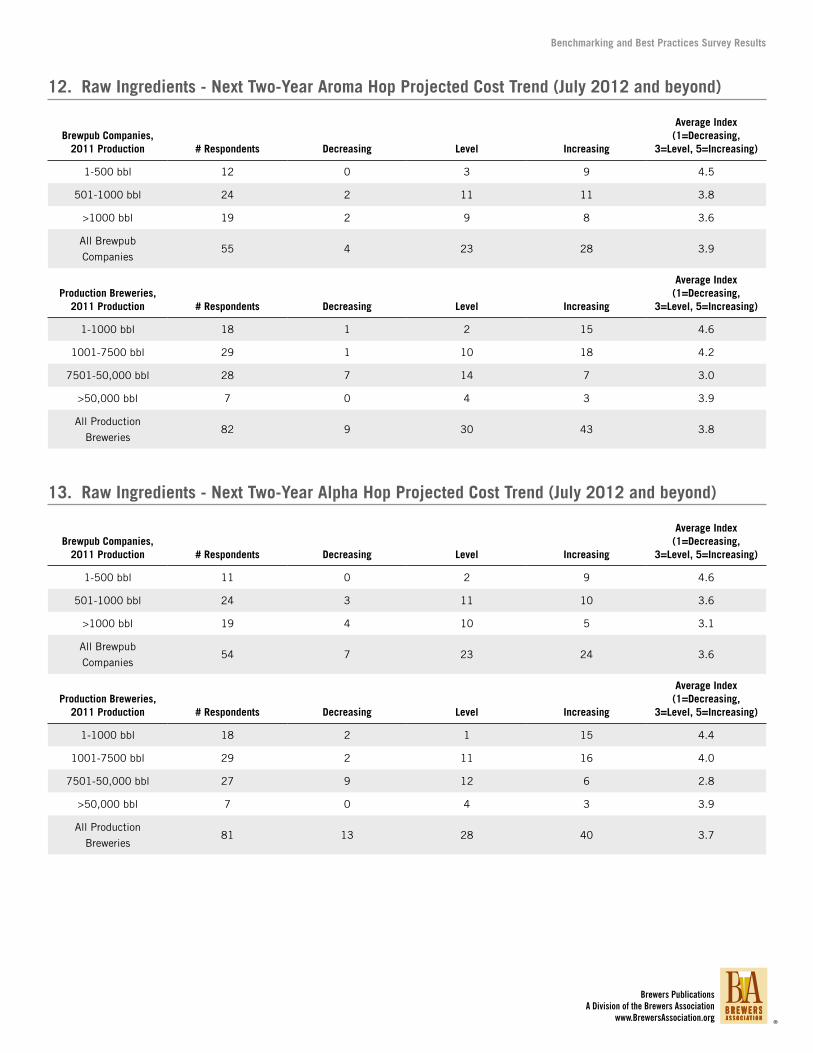

12. Raw ingredients - Next two-Year aroma Hop Projected Cost trend (July 2012 and beyond)

Brewpub Companies, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-500 bbl 12 0 3 9 4.5

501-1000 bbl 24 2 11 11 3.8

>1000 bbl 19 2 9 8 3.6

All Brewpub

Companies55 4 23 28 3.9

Production Breweries, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-1000 bbl 18 1 2 15 4.6

1001-7500 bbl 29 1 10 18 4.2

7501-50,000 bbl 28 7 14 7 3.0

>50,000 bbl 7 0 4 3 3.9

All Production

Breweries82 9 30 43 3.8

13. Raw ingredients - Next two-Year alpha Hop Projected Cost trend (July 2012 and beyond)

Brewpub Companies, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-500 bbl 11 0 2 9 4.6

501-1000 bbl 24 3 11 10 3.6

>1000 bbl 19 4 10 5 3.1

All Brewpub

Companies54 7 23 24 3.6

Production Breweries, 2011 Production # Respondents Decreasing level increasing

average index (1=Decreasing,

3=level, 5=increasing)

1-1000 bbl 18 2 1 15 4.4

1001-7500 bbl 29 2 11 16 4.0

7501-50,000 bbl 27 9 12 6 2.8

>50,000 bbl 7 0 4 3 3.9

All Production

Breweries81 13 28 40 3.7

Brewers PublicationsA Division of the Brewers Association

www.BrewersAssociation.org ®