BellSouth: A Competitive Force

81

BellSouth: A Competitive Force Analyst Briefing New York, NY November 10, 2003

Transcript of BellSouth: A Competitive Force

BellSouth: A Competitive ForceAnalyst Briefing

New York, NYNovember 10, 2003

Safe Harbor

In addition to historical information, this briefing may contain forward-looking statements regarding events and financial trends. Factors that could affect future results and could cause actual results to differ materially from those expressed or implied in the forward-looking statements include: (i) a change in economic conditions in domestic or international markets where we operate or have material investments which would affect demand for our services; (ii) currency devaluations and continued economic weakness in certain international markets in which we operate or have material investments; (iii) the intensity of competitive activity and its resulting impact on pricing strategies and new product offerings; (iv) higher than anticipated cash requirements for investments, new business initiatives and acquisitions; (v) unfavorable regulatory actions and (vi) those factors contained in the Company’s periodic reports filed with the SEC. The forward-looking information in this presentation is given as of this date only, and BellSouth assumes no duty to update this information.

This presentation may also contain certain non-GAAP financial measures. The most directly comparable GAAP financial measures, and a full reconciliation of non-GAAP to GAAP financial information, are provided on the Company's investor relations website, www.bellsouth.com/investor.

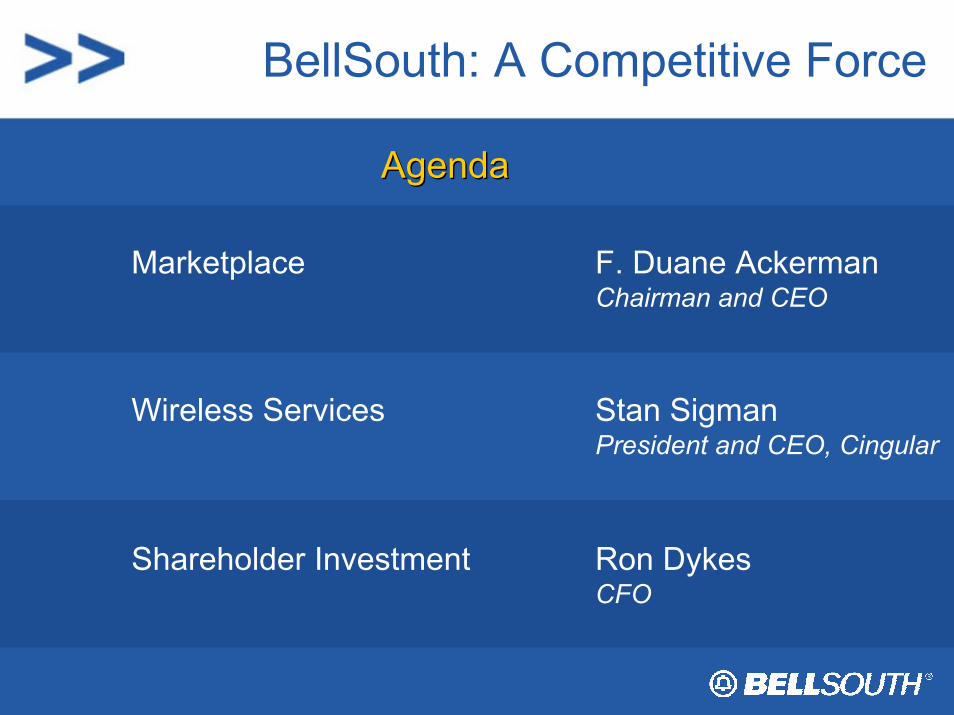

BellSouth: A Competitive Force

AgendaAgenda

Ron DykesCFO

Shareholder Investment

Stan SigmanPresident and CEO, Cingular

Wireless Services

F. Duane AckermanChairman and CEO

Marketplace

BellSouth: A Competitive ForceIn the Marketplace

F. Duane Ackerman, Chairman and CEO

A Competitive Force – Agenda

• Finishing strong in 2003

• Pursuing policy reform

• Focusing on the marketplace

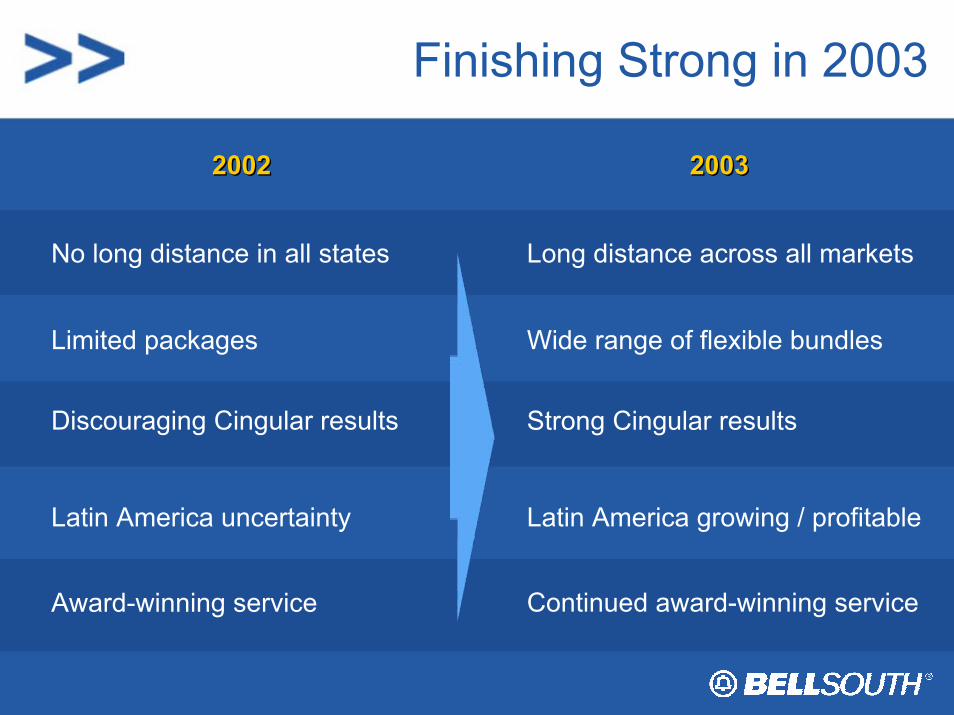

Finishing Strong in 2003

20022002

Discouraging Cingular results

No long distance in all states

Limited packages

Latin America uncertainty

Award-winning service

20032003

Strong Cingular results

Long distance across all markets

Wide range of flexible bundles

Latin America growing / profitable

Continued award-winning service

A Competitive Force – Agenda

• Finishing strong in 2003

• Pursuing policy reform

• Focusing on the marketplace

Pursuing Policy Reform

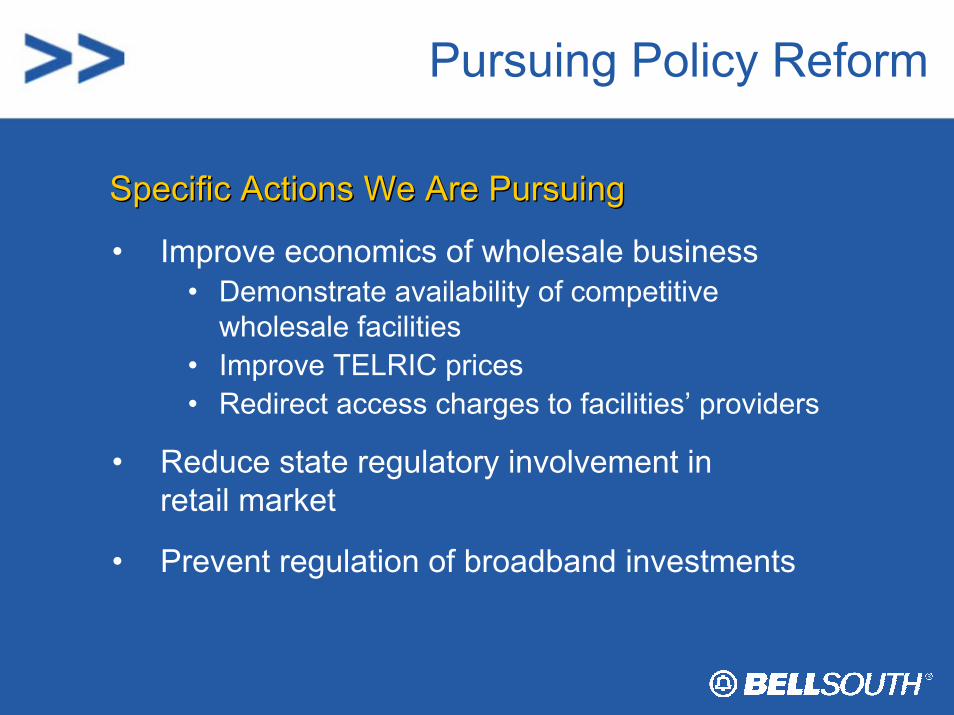

Specific Actions We Are PursuingSpecific Actions We Are Pursuing

• Improve economics of wholesale business• Demonstrate availability of competitive

wholesale facilities• Improve TELRIC prices• Redirect access charges to facilities’ providers

• Reduce state regulatory involvement in retail market

• Prevent regulation of broadband investments

A Competitive Force – Agenda

• Finishing strong in 2003

• Pursuing policy reform

• Focusing on the marketplace– Communications Group

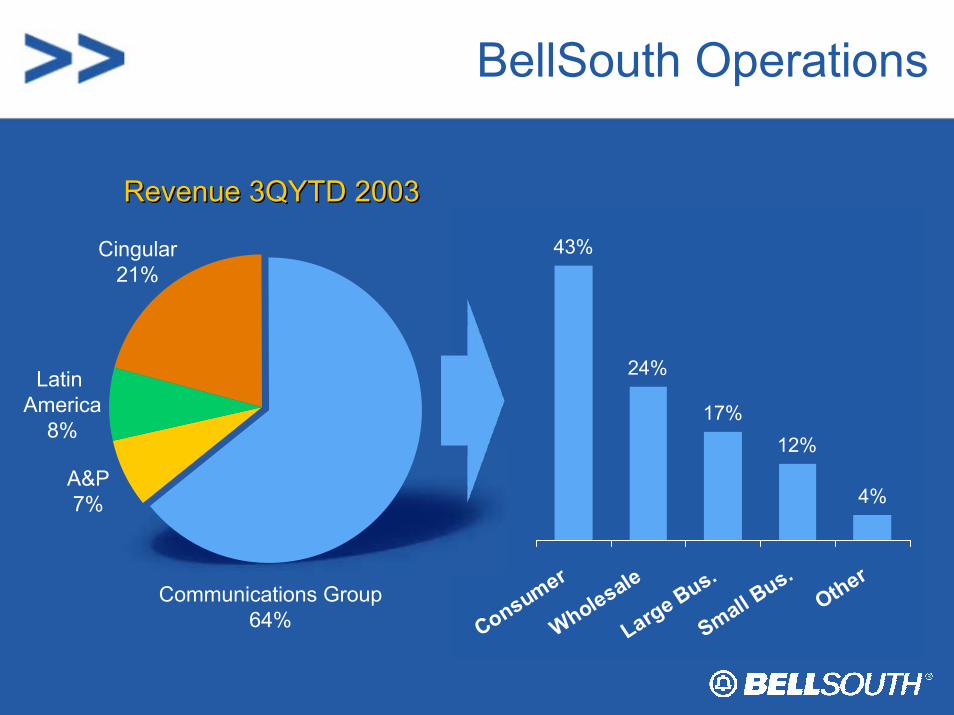

BellSouth Operations

43%

24%

17%12%

4%

Consumer

Wholesale

Large Bus.

Small Bus.

OtherCommunications Group

64%

Cingular21%

Latin America

8%

A&P 7%

Revenue 3QYTD 2003Revenue 3QYTD 2003

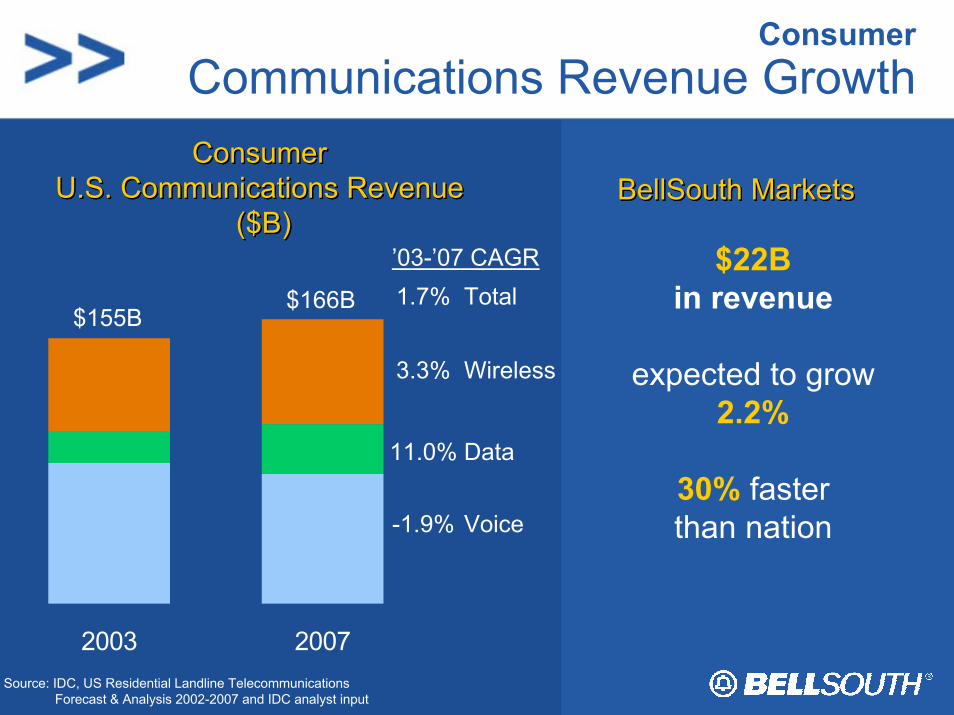

ConsumerCommunications Revenue Growth

Source: IDC, US Residential Landline Telecommunications Forecast & Analysis 2002-2007 and IDC analyst input

Consumer U.S. Communications Revenue

($B)

Consumer Consumer U.S. Communications RevenueU.S. Communications Revenue

($B)($B)’03-’07 CAGR

Wireless

2003 2007

$155B$166B

3.3%

-1.9% Voice

1.7% Total

11.0% Data

$22Bin revenue

expected to grow2.2%

30% faster than nation

BellSouth MarketsBellSouth MarketsBellSouth Markets

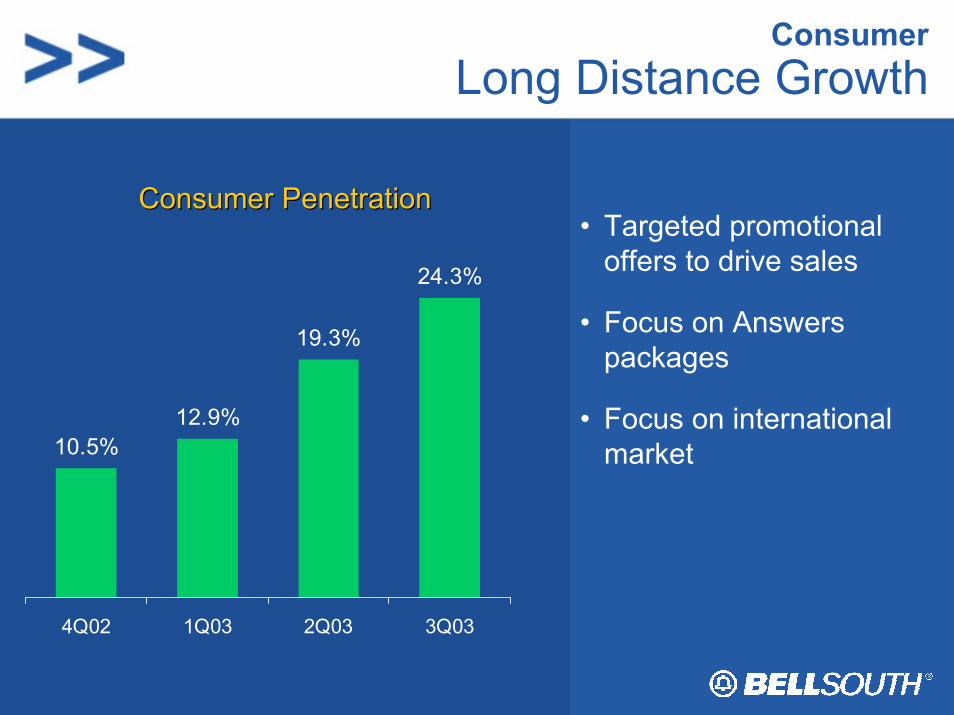

ConsumerLong Distance Growth

• Targeted promotional offers to drive sales

• Focus on Answers packages

• Focus on international market10.5%

12.9%

19.3%

24.3%

4Q02 1Q03 2Q03 3Q03

Consumer PenetrationConsumer Penetration

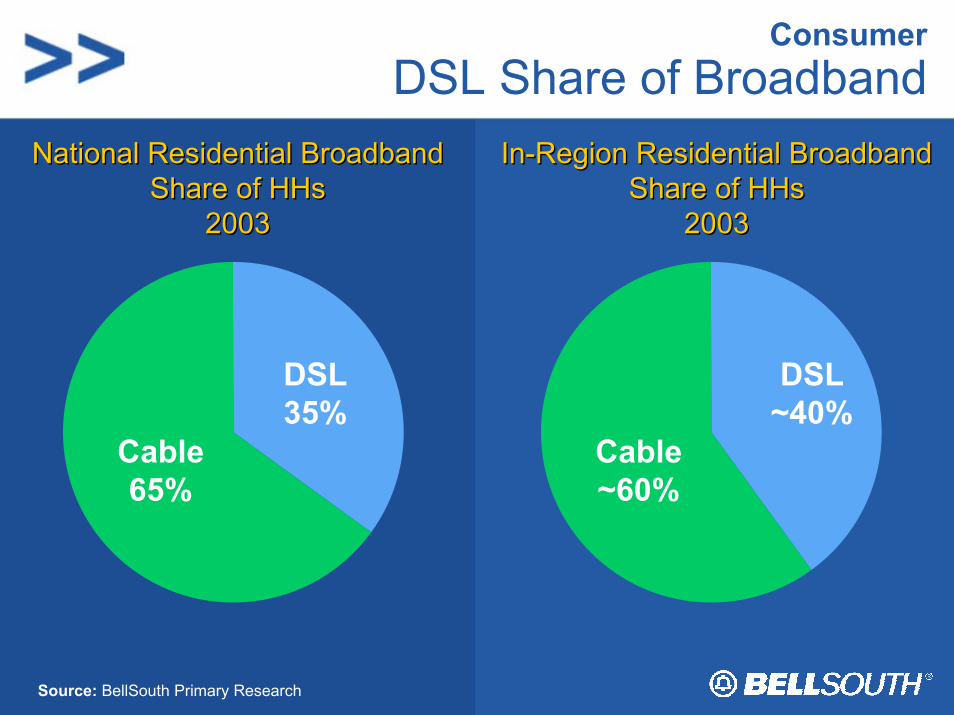

ConsumerDSL Share of Broadband

Source: BellSouth Primary Research

National Residential Broadband Share of HHs

2003

National Residential Broadband Share of HHs

2003

Cable65%

DSL35%

In-Region Residential Broadband Share of HHs

2003

In-Region Residential Broadband Share of HHs

2003

Cable~60%

DSL~40%

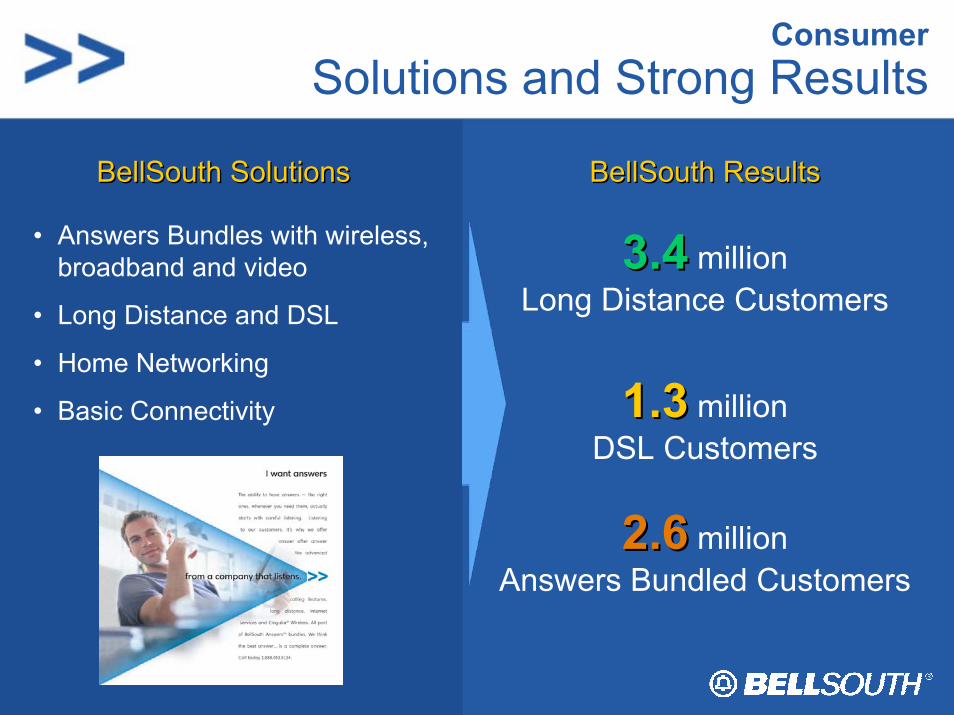

ConsumerSolutions and Strong Results

• Answers Bundles with wireless, broadband and video

• Long Distance and DSL

• Home Networking

• Basic Connectivity

BellSouth SolutionsBellSouth Solutions

2.62.6 millionAnswers Bundled Customers

BellSouth ResultsBellSouth Results

3.43.4 millionLong Distance Customers

1.31.3 millionDSL Customers

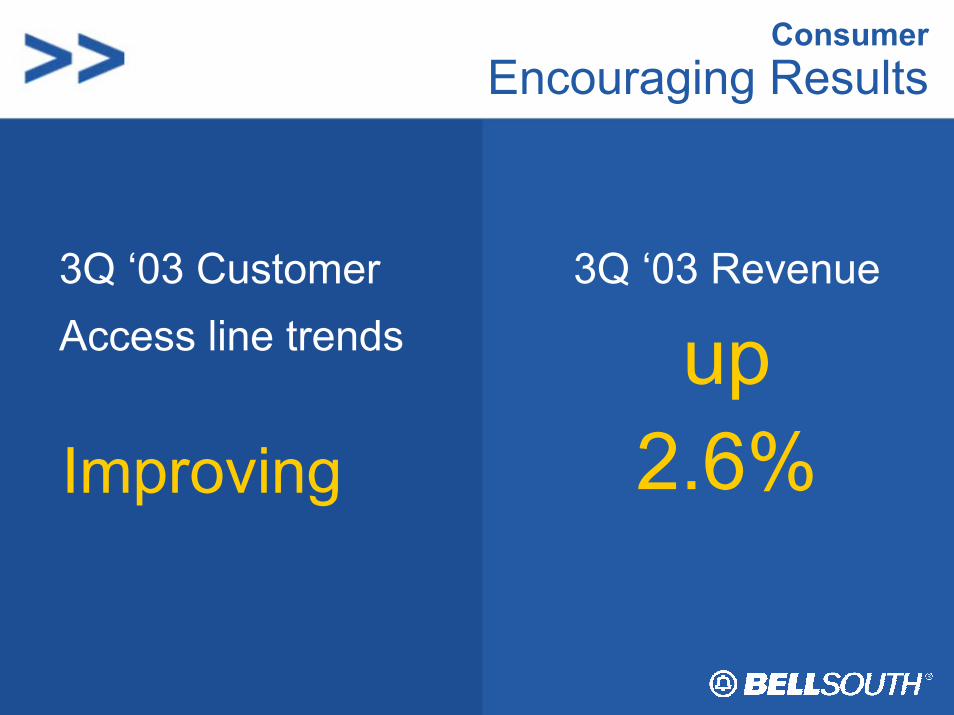

Consumer Encouraging Results

3Q ‘03 CustomerAccess line trends

Improving

3Q ‘03 Revenue

up2.6%

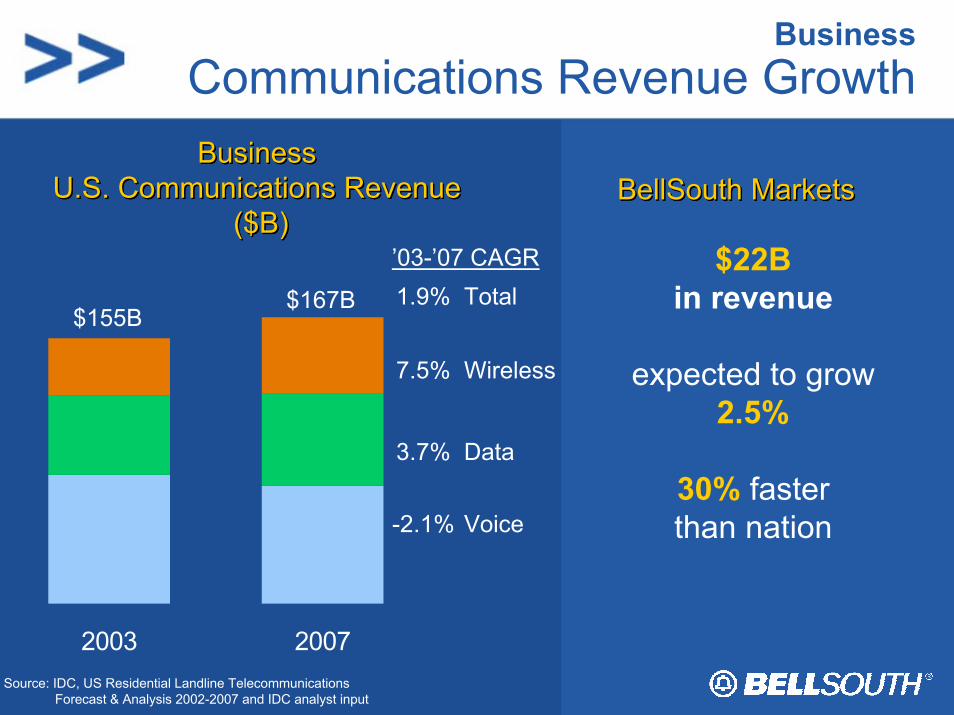

BusinessCommunications Revenue GrowthBusiness

U.S. Communications Revenue($B)

BusinessBusinessU.S. Communications RevenueU.S. Communications Revenue

($B)($B)

2003 2007Source: IDC, US Residential Landline Telecommunications

Forecast & Analysis 2002-2007 and IDC analyst input

’03-’07 CAGR

Wireless

$155B$167B

7.5%

-2.1% Voice

1.9% Total

3.7% Data

$22Bin revenue

expected to grow2.5%

30% faster than nation

BellSouth MarketsBellSouth MarketsBellSouth Markets

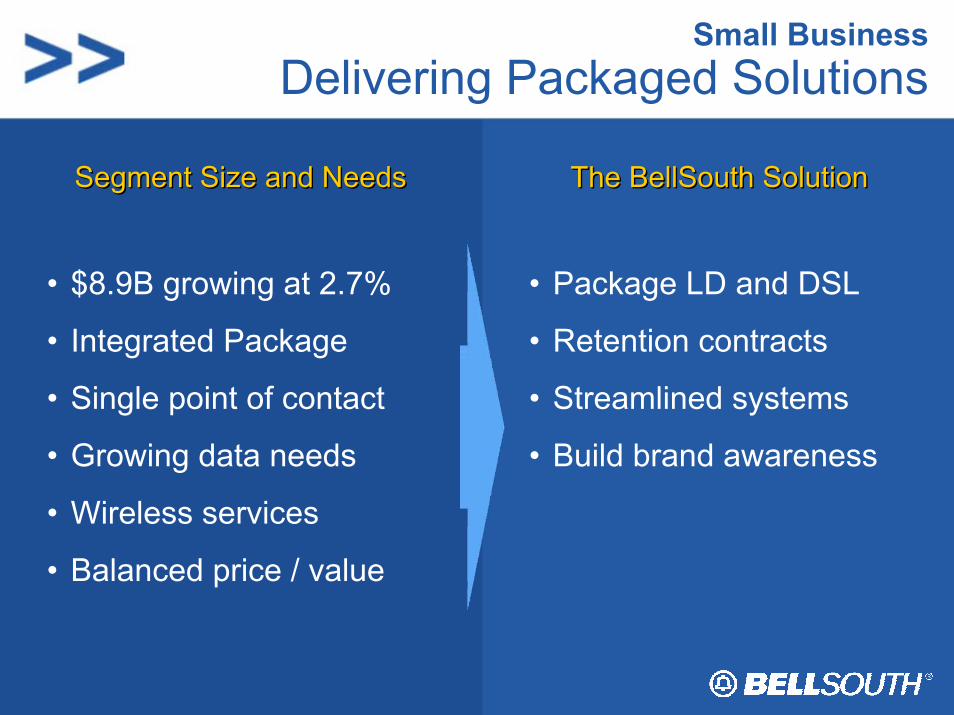

Small BusinessDelivering Packaged Solutions

• $8.9B growing at 2.7%

• Integrated Package

• Single point of contact

• Growing data needs

• Wireless services

• Balanced price / value

• Package LD and DSL

• Retention contracts

• Streamlined systems

• Build brand awareness

Segment Size and NeedsSegment Size and Needs The BellSouth SolutionThe BellSouth Solution

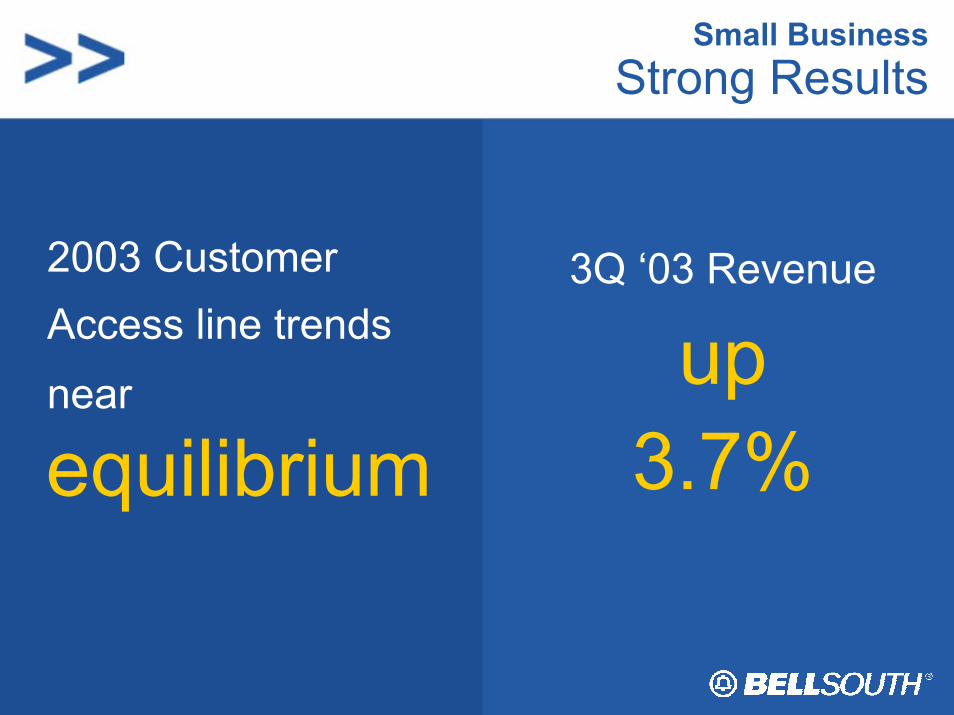

Small BusinessStrong Results

2003 CustomerAccess line trendsnear

equilibrium

3Q ‘03 Revenue

up3.7%

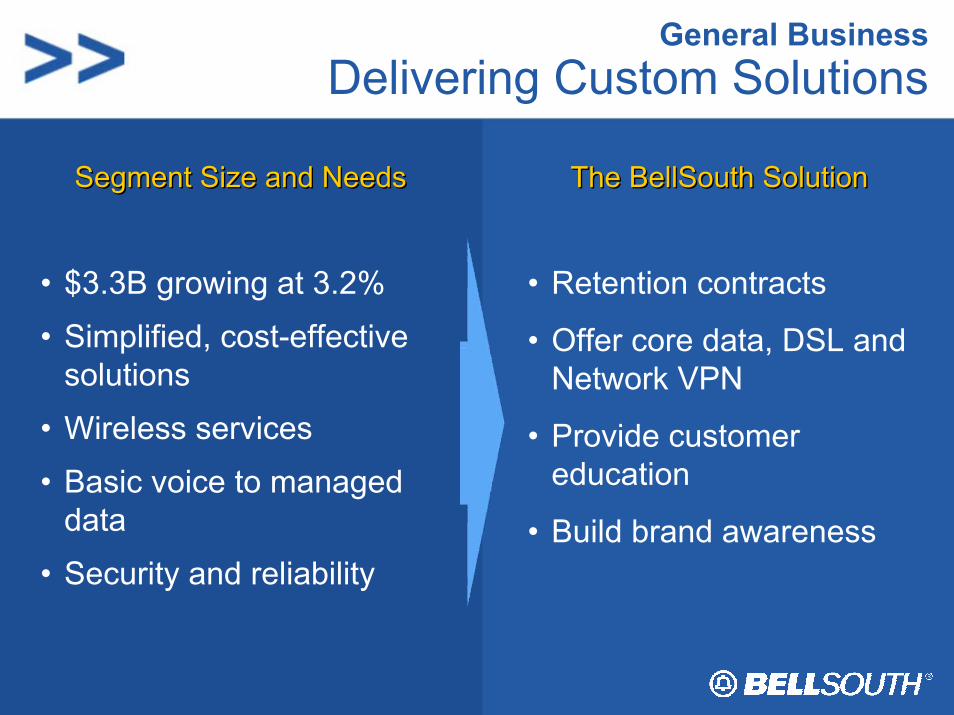

General BusinessDelivering Custom Solutions

Segment Size and NeedsSegment Size and Needs The BellSouth SolutionThe BellSouth Solution

• $3.3B growing at 3.2%

• Simplified, cost-effective solutions

• Wireless services

• Basic voice to managed data

• Security and reliability

• Retention contracts

• Offer core data, DSL and Network VPN

• Provide customer education

• Build brand awareness

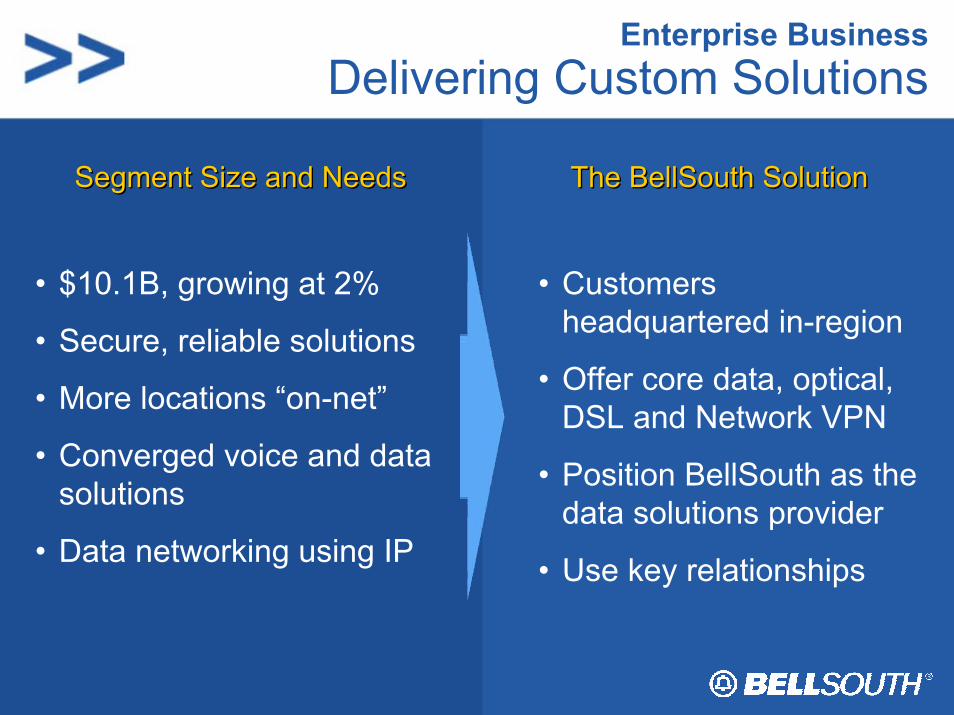

Enterprise BusinessDelivering Custom Solutions

• $10.1B, growing at 2%

• Secure, reliable solutions

• More locations “on-net”

• Converged voice and data solutions

• Data networking using IP

• Customers headquartered in-region

• Offer core data, optical, DSL and Network VPN

• Position BellSouth as the data solutions provider

• Use key relationships

Segment Size and NeedsSegment Size and Needs The BellSouth SolutionThe BellSouth Solution

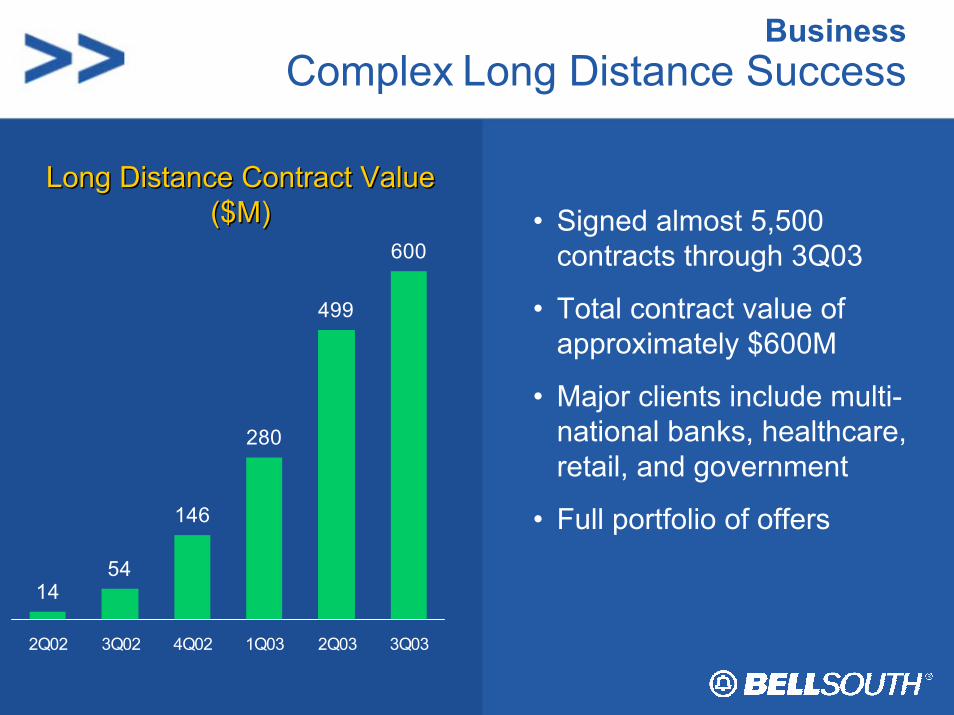

BusinessComplex Long Distance Success

1454

146

280

499

600

2Q02 3Q02 4Q02 1Q03 2Q03 3Q03

Long Distance Contract Value($M)

Long Distance Contract Value($M) • Signed almost 5,500

contracts through 3Q03

• Total contract value of approximately $600M

• Major clients include multi-national banks, healthcare, retail, and government

• Full portfolio of offers

Lead with Service

Continue to Win AwardsContinue to Win Awards

#110 years in

a row!American Customer Satisfaction Index

American Customer Satisfaction Index

J.D. Power & AssociatesJ.D. Power & Associates

#1Local, LD,

High Speed, Business

• Emphasize The Customer Rules!

• Improve consumer office access

• Improve rep / tech satisfaction

• Focus on end-to-end process

Continue to Deliver Industry-Leading Service

Continue to Deliver Industry-Leading Service

Communications GroupKey Initiatives

• Lead with service

• Pursue public policy reform

• Drive growth, retention and reacquisition

A Competitive Force – Agenda

• Finishing strong in 2003

• Pursuing policy reform

• Focusing on the marketplace– Cingular

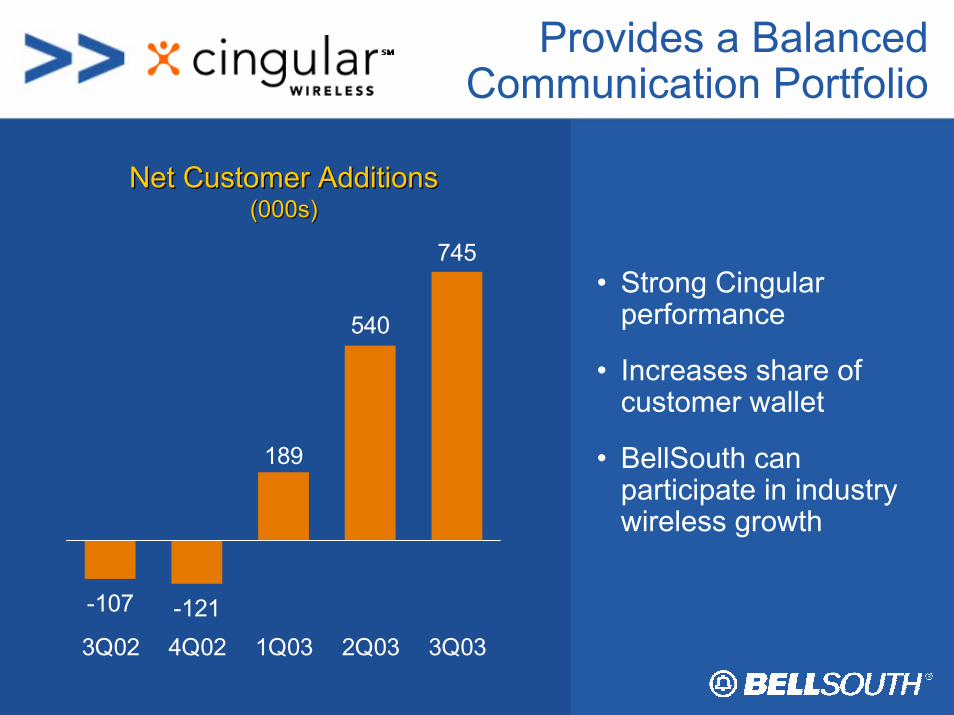

Provides a BalancedCommunication Portfolio

• Strong Cingularperformance

• Increases share of customer wallet

• BellSouth can participate in industry wireless growth

-107 -121

189

540

745

3Q02 4Q02 1Q03 2Q03 3Q03

Net Customer AdditionsNet Customer Additions(000s)(000s)

A Competitive Force – Agenda

• Finishing strong in 2003

• Pursuing policy reform

• Focusing on the marketplace– Latin America

Latin AmericaKey Strategies

• Grow customer base

• Grow revenues

• Improve profitability– Positive Cash Flow– Positive Net Income

Latin AmericaTargeted Marketing Strategies

Buying Power: $248BBuying Power: $248B

HH Income: $35,440HH Income: $35,440

176M 176M POPsPOPs

21M 21M POPsPOPs

Buying Power: $305BBuying Power: $305B

HH Income: $6,946HH Income: $6,946

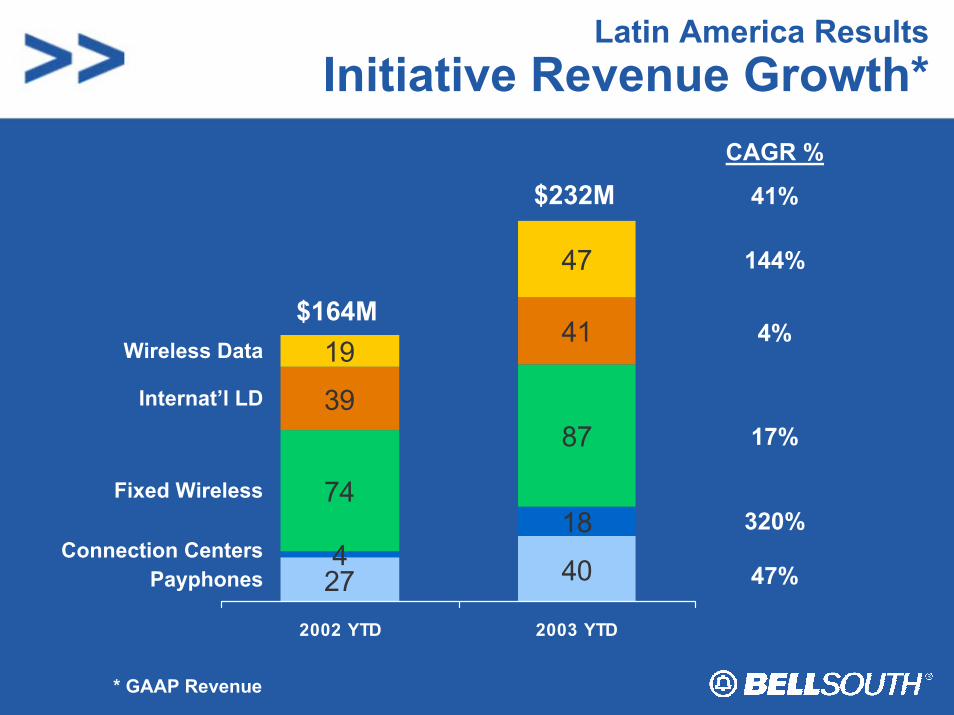

Latin America ResultsInitiative Revenue Growth*

CAGR %

41%

144%

4%

17%

320%

47%27 40418

74

8739

4119

47

2002 YTD 2003 YTD

PayphonesConnection Centers

Fixed Wireless

Internat’l LD

Wireless Data

$164M

$232M

* GAAP Revenue

Key Takeaways

Reformed public policy

+ Upside Opportunities

Top-line revenue growth

Progress at Cingular and Latin

Latin America

Cingular Wireless: A Competitive Force

Stan Sigman, President and CEO

Cingular’s Focus for Success

• Maximize growth & profit

• Integration with Wireline

• Leverage GSM conversion– EDGE capability

• Capitalize on wireless number portability

Three Key Steps

1 Sales & marketing reorganization

2 Improve marketing message

3 Leveraging affiliation with parent companies

1. Sales & Marketing Reorganization

ResultsResultsWhat We DidWhat We Did

• Focus on local markets– responsibility and

accountability– 22 market leaders

• Driving more traffic to stores

• Higher sales

2. Improve Marketing Message

Provides a meaningful reasonto choose Cingular

3. Leverage Affiliation with Parents

PART OF THE FAMILY

• New branding will highlight our strengths– Coverage– Reliability– Service– Trust

Three Key Steps

1 Sales & marketing reorganization

2 Improve marketing message

3 Leveraging affiliation with parent companies

The results are showing. . .

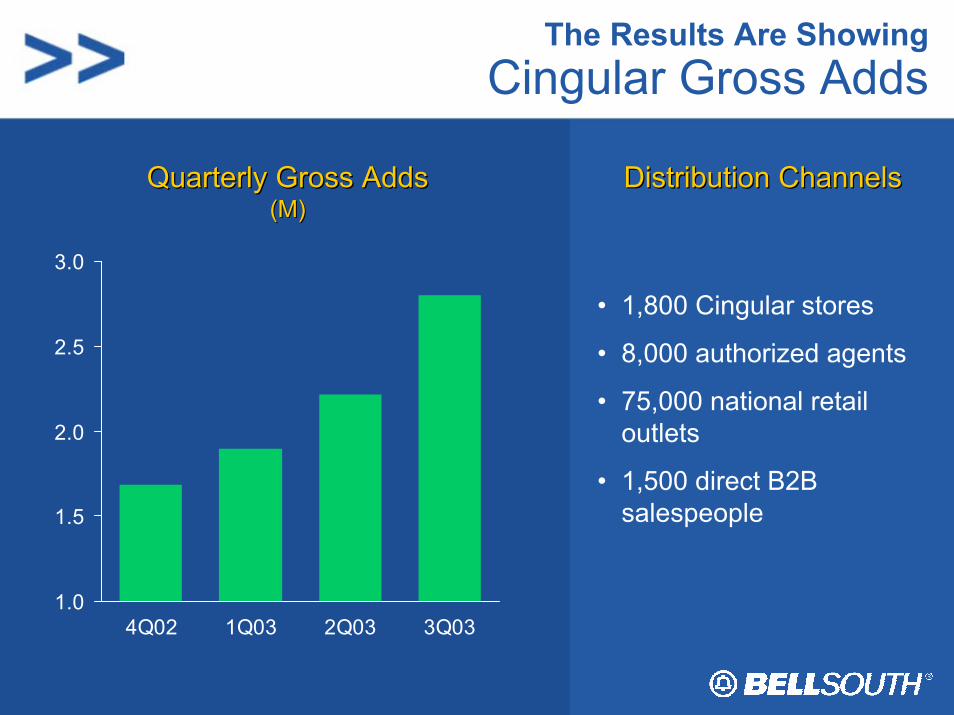

The Results Are ShowingCingular Gross Adds

1.0

1.5

2.0

2.5

3.0

4Q02 1Q03 2Q03 3Q03

• 1,800 Cingular stores

• 8,000 authorized agents

• 75,000 national retail outlets

• 1,500 direct B2B salespeople

Quarterly Gross AddsQuarterly Gross Adds(M)(M)

Distribution ChannelsDistribution Channels

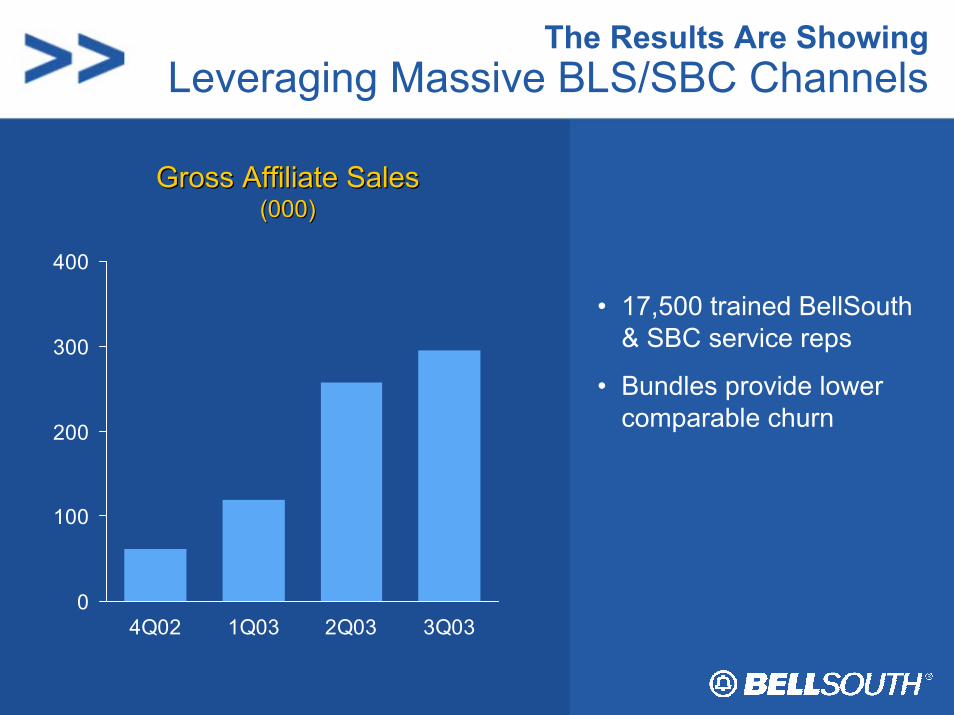

The Results Are ShowingLeveraging Massive BLS/SBC Channels

0

100

200

300

400

4Q02 1Q03 2Q03 3Q03

Gross Affiliate SalesGross Affiliate Sales(000)(000)

• 17,500 trained BellSouth & SBC service reps

• Bundles provide lower comparable churn

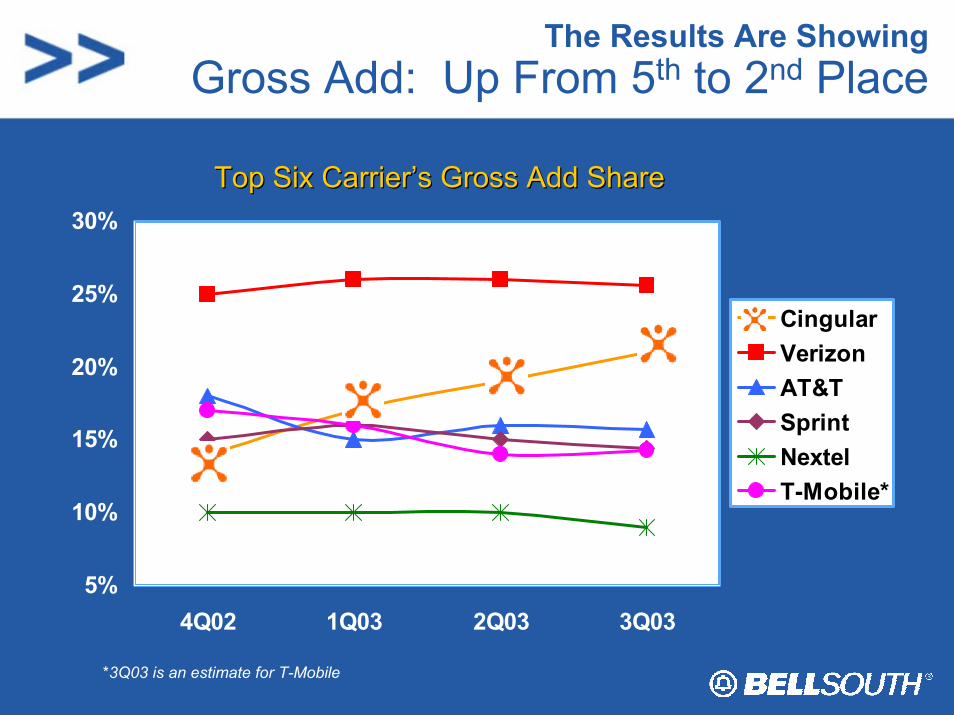

The Results Are ShowingGross Add: Up From 5th to 2nd Place

Top Six Carrier’s Gross Add ShareTop Six Carrier’s Gross Add Share

5%

10%

15%

20%

25%

30%

4Q02 1Q03 2Q03 3Q03

CingularVerizonAT&TSprintNextelT-Mobile*

*3Q03 is an estimate for T-Mobile

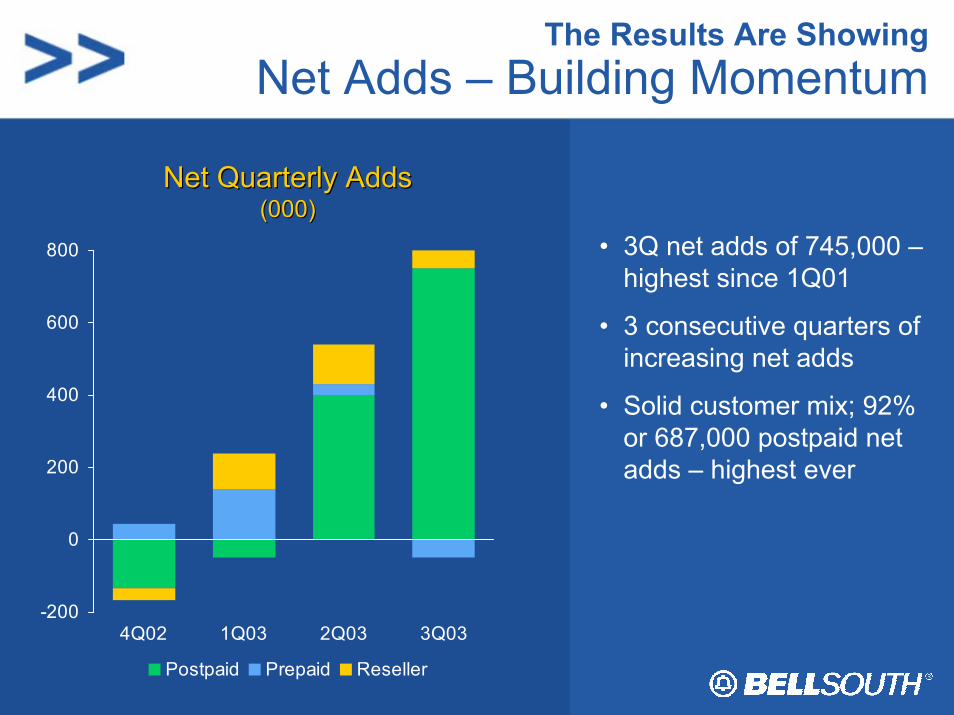

The Results Are ShowingNet Adds – Building Momentum

-200

0

200

400

600

800

4Q02 1Q03 2Q03 3Q03

Postpaid Prepaid Reseller

• 3Q net adds of 745,000 –highest since 1Q01

• 3 consecutive quarters of increasing net adds

• Solid customer mix; 92% or 687,000 postpaid net adds – highest ever

Net Quarterly AddsNet Quarterly Adds(000)(000)

The Three “R’s”

Revenue intensity – ARPU

SuccessReturn on operations

Rate of penetration

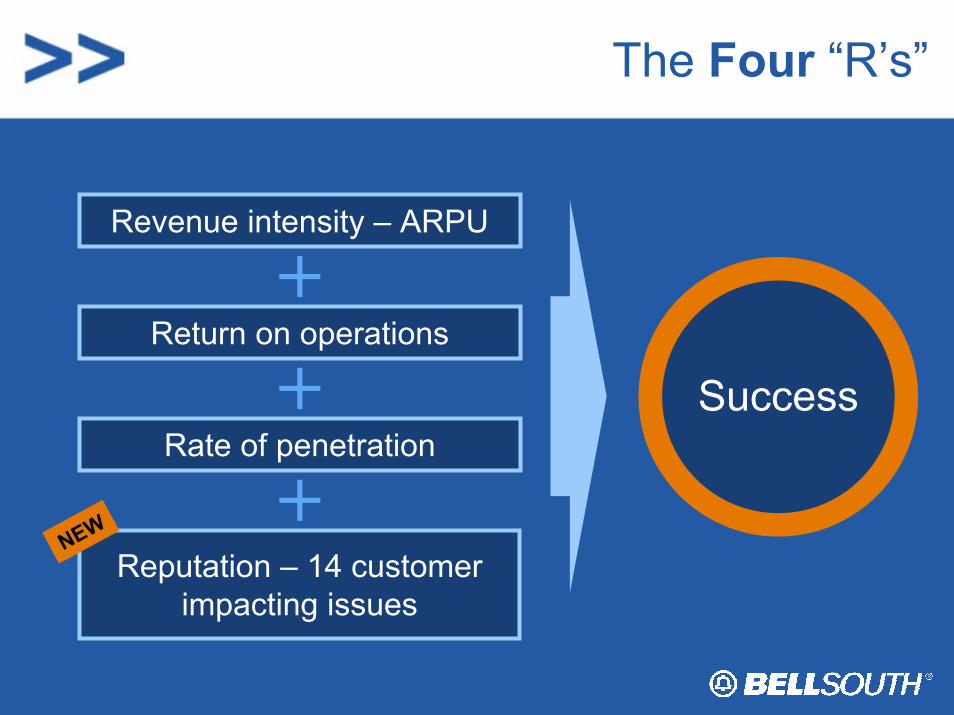

The Four “R’s”

Revenue intensity – ARPU

SuccessReturn on operations

Rate of penetration

Reputation – 14 customerimpacting issues

NEW

Cingular’s Focus for Success

• Maximize growth & profit

• Integration with Wireline

• Leverage GSM conversion– EDGE capability

• Capitalize on wireless number portability

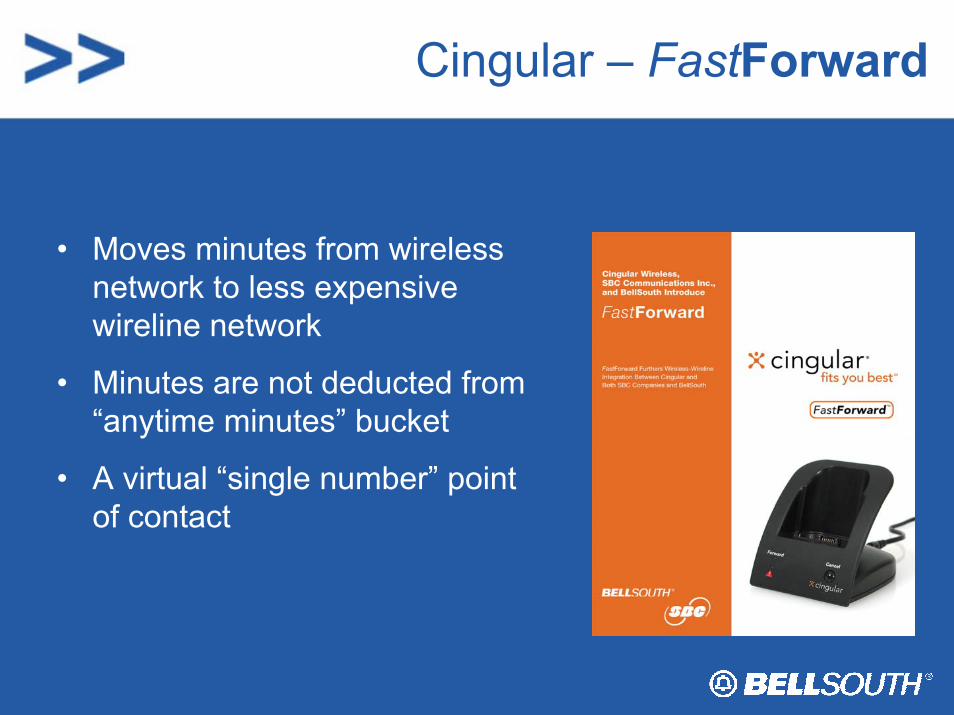

Cingular – FastForward

• Moves minutes from wireless network to less expensive wireline network

• Minutes are not deducted from “anytime minutes” bucket

• A virtual “single number” point of contact

Cingular’s Focus for Success

• Maximize growth & profit

• Integration with Wireline

• Leverage GSM conversion– EDGE capability

• Capitalize on wireless number portability

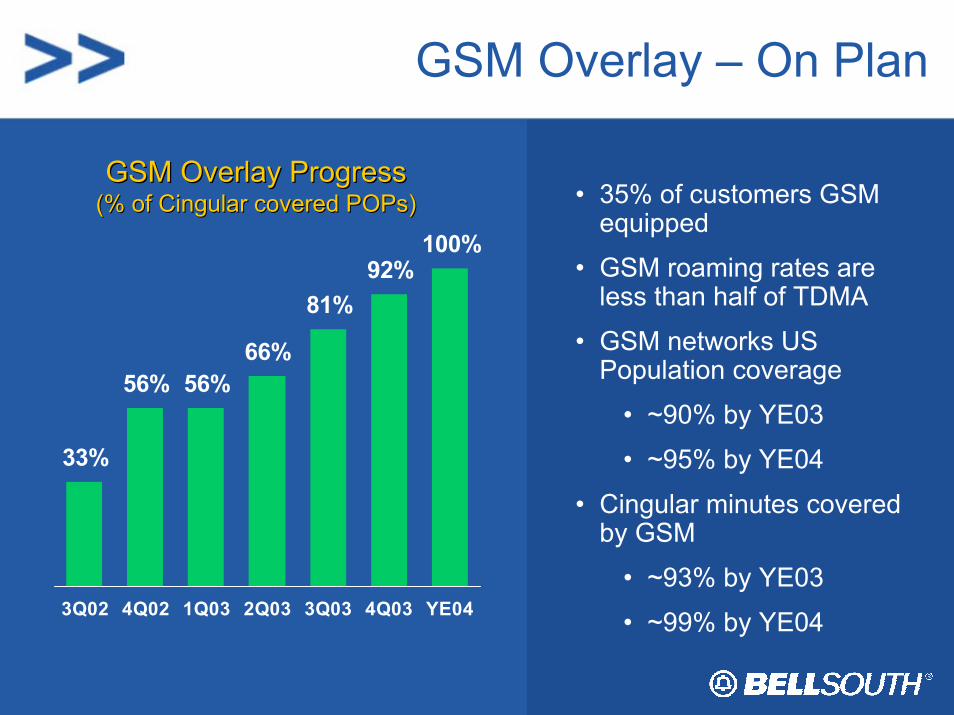

GSM Overlay – On Plan

• 35% of customers GSM equipped

• GSM roaming rates are less than half of TDMA

• GSM networks US Population coverage

• ~90% by YE03

• ~95% by YE04

• Cingular minutes covered by GSM

• ~93% by YE03

• ~99% by YE04

33%

56% 56%66%

81%92%

100%

3Q02 4Q02 1Q03 2Q03 3Q03 4Q03 YE04

GSM Overlay ProgressGSM Overlay Progress(% of (% of CingularCingular covered covered POPsPOPs))

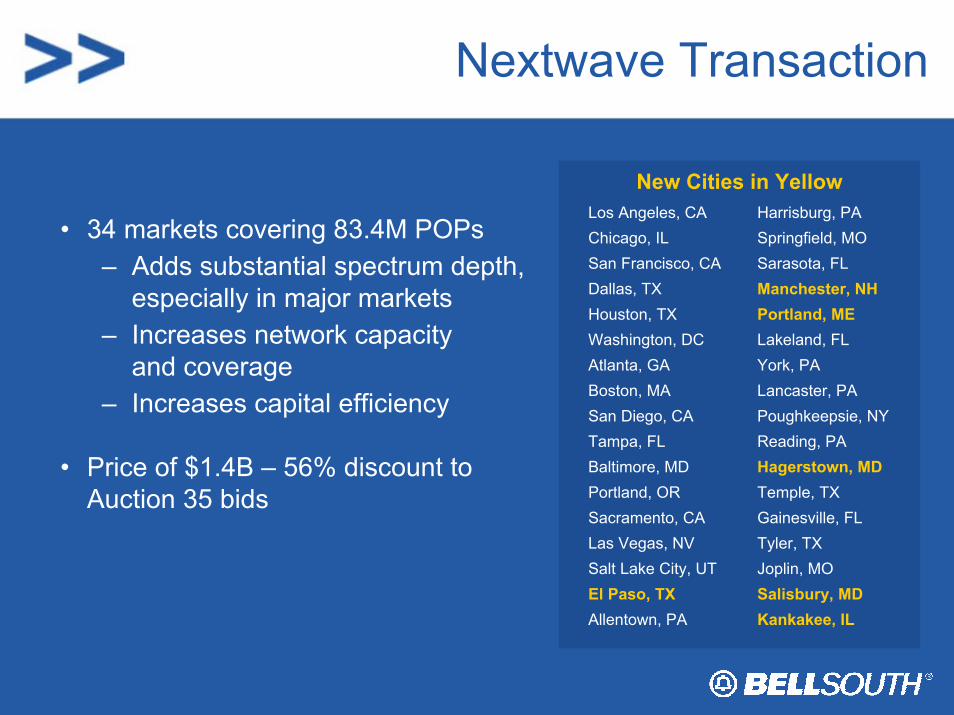

Nextwave Transaction

Kankakee, ILAllentown, PASalisbury, MDEl Paso, TXJoplin, MOSalt Lake City, UTTyler, TXLas Vegas, NVGainesville, FLSacramento, CATemple, TXPortland, ORHagerstown, MDBaltimore, MDReading, PATampa, FLPoughkeepsie, NYSan Diego, CALancaster, PABoston, MAYork, PAAtlanta, GALakeland, FLWashington, DCPortland, MEHouston, TXManchester, NHDallas, TXSarasota, FLSan Francisco, CASpringfield, MOChicago, ILHarrisburg, PALos Angeles, CA

New Cities in Yellow

• 34 markets covering 83.4M POPs – Adds substantial spectrum depth,

especially in major markets– Increases network capacity

and coverage– Increases capital efficiency

• Price of $1.4B – 56% discount to Auction 35 bids

Cingular’s Focus for Success

• Maximize growth & profit

• Integration with Wireline

• Leverage GSM conversion– EDGE capability

• Capitalize on wireless number portability

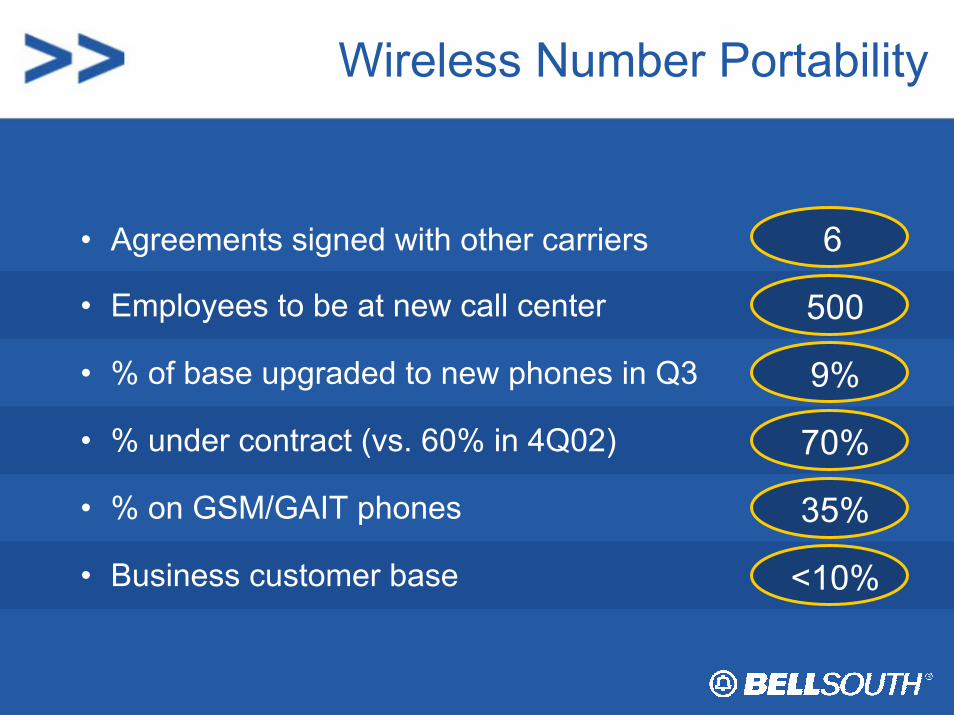

Wireless Number Portability

6• Agreements signed with other carriers

• Employees to be at new call center 500

• % under contract (vs. 60% in 4Q02) 70%

9%• % of base upgraded to new phones in Q3

• Business customer base <10%

35%• % on GSM/GAIT phones

In SummaryMoving Forward – Rapidly

Continue to grow the business and bottom line

Grow and enhance the GSM network

More integration with BellSouth and SBC

Progress towards best in class results

“All footprints point forward.”

Cingular Wireless: A Competitive Force

Stan Sigman, President and CEO

BellSouth: A Competitive ForceAnalyst Briefing

New York, NYNovember 10, 2003

Meeting Break Will resume shortly

BellSouth: A Competitive ForceRon Dykes, CFO

Topics for Discussion

• Key Operating and Financial Trends – 2003– Communications Group– Cingular Wireless– Latin America– Advertising & Publishing– BellSouth

• Business Financial Trends – 2004

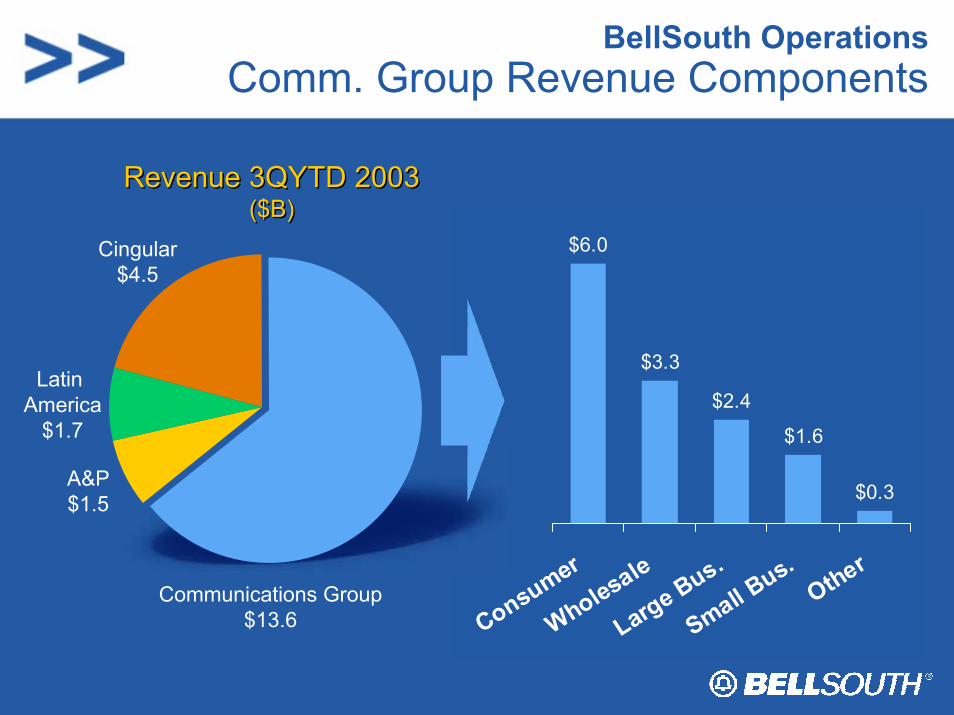

BellSouth OperationsComm. Group Revenue Components

$6.0

$3.3

$2.4

$1.6

$0.3

Consumer

Wholesale

Large Bus.

Small Bus.

OtherCommunications Group

$13.6

Cingular$4.5

Latin America

$1.7

A&P $1.5

Revenue 3QYTD 2003($B)

Revenue 3QYTD 2003($B)

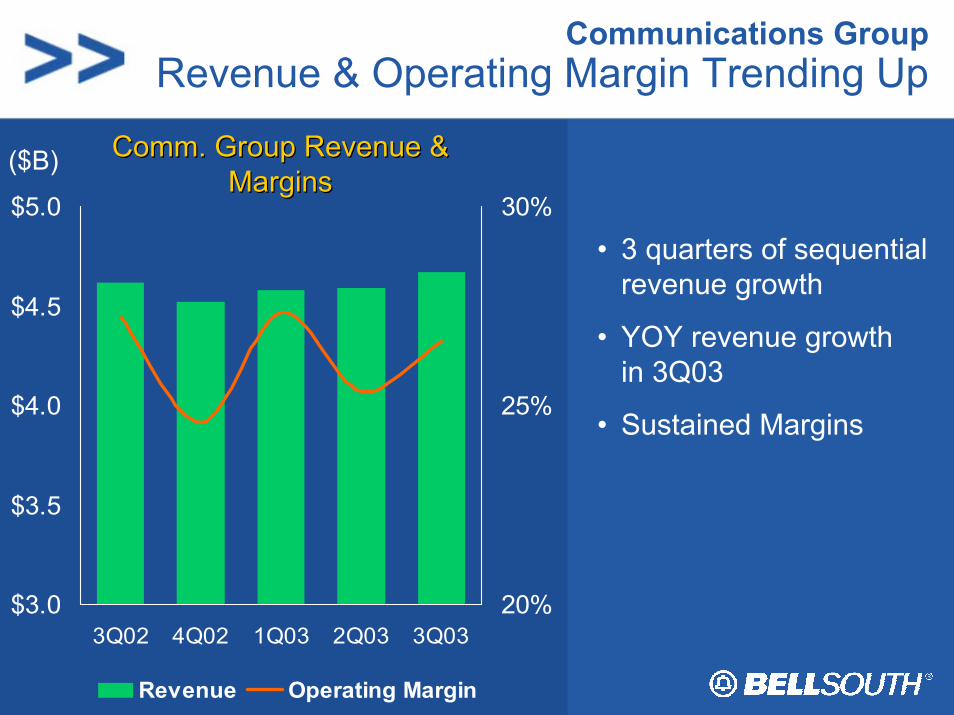

Communications GroupRevenue & Operating Margin Trending Up

Comm. Group Revenue & Comm. Group Revenue & MarginsMargins

• 3 quarters of sequential revenue growth

• YOY revenue growth in 3Q03

• Sustained Margins

$3.0

$3.5

$4.0

$4.5

$5.0

3Q02 4Q02 1Q03 2Q03 3Q0320%

25%

30%

Revenue Operating Margin

($B)

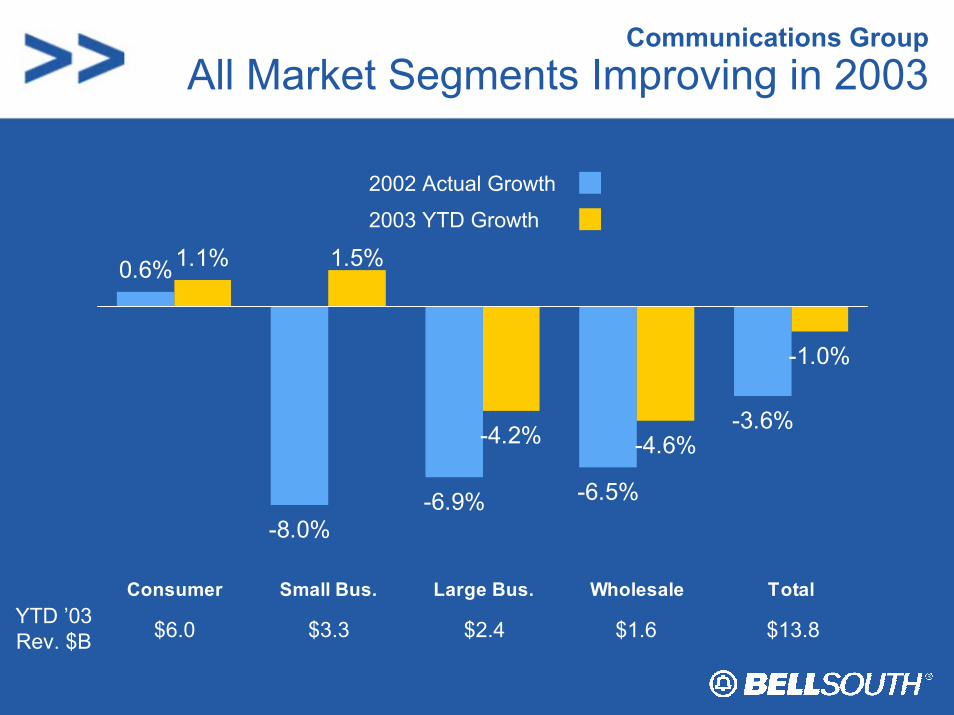

Communications GroupAll Market Segments Improving in 2003

0.6%

-8.0%-6.9% -6.5%

-3.6%

1.1% 1.5%

-4.2% -4.6%

-1.0%

Consumer Small Bus. Large Bus. Wholesale TotalYTD ’03Rev. $B $6.0 $3.3 $2.4 $1.6 $13.8

2002 Actual Growth

2003 YTD Growth

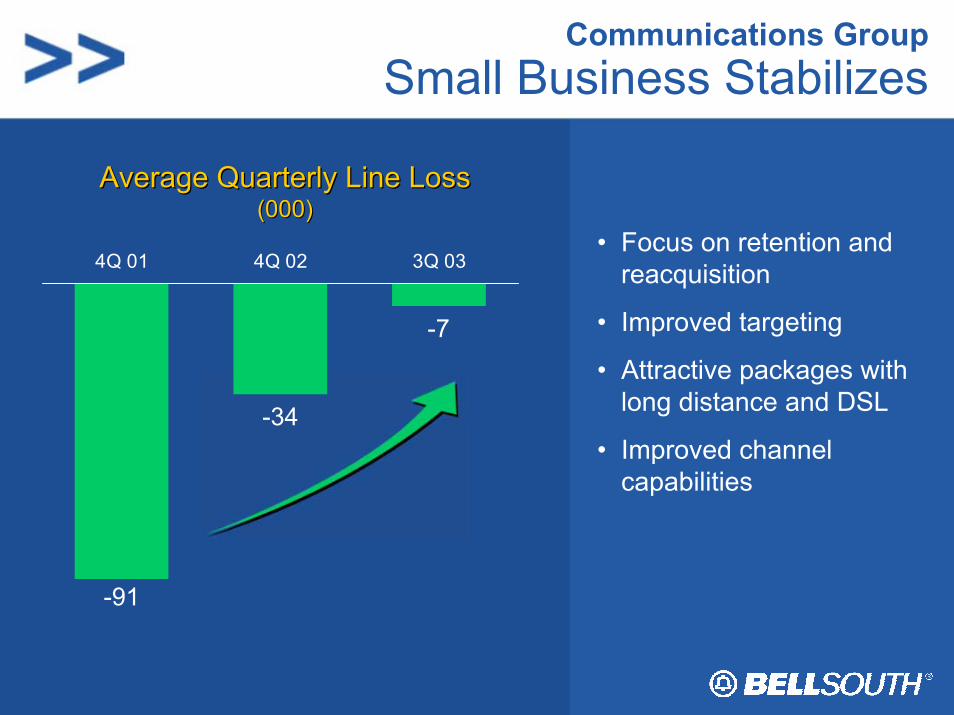

Communications GroupSmall Business Stabilizes

-91

-7

-34

4Q 01 4Q 02 3Q 03• Focus on retention and

reacquisition

• Improved targeting

• Attractive packages with long distance and DSL

• Improved channel capabilities

Average Quarterly Line LossAverage Quarterly Line Loss(000)(000)

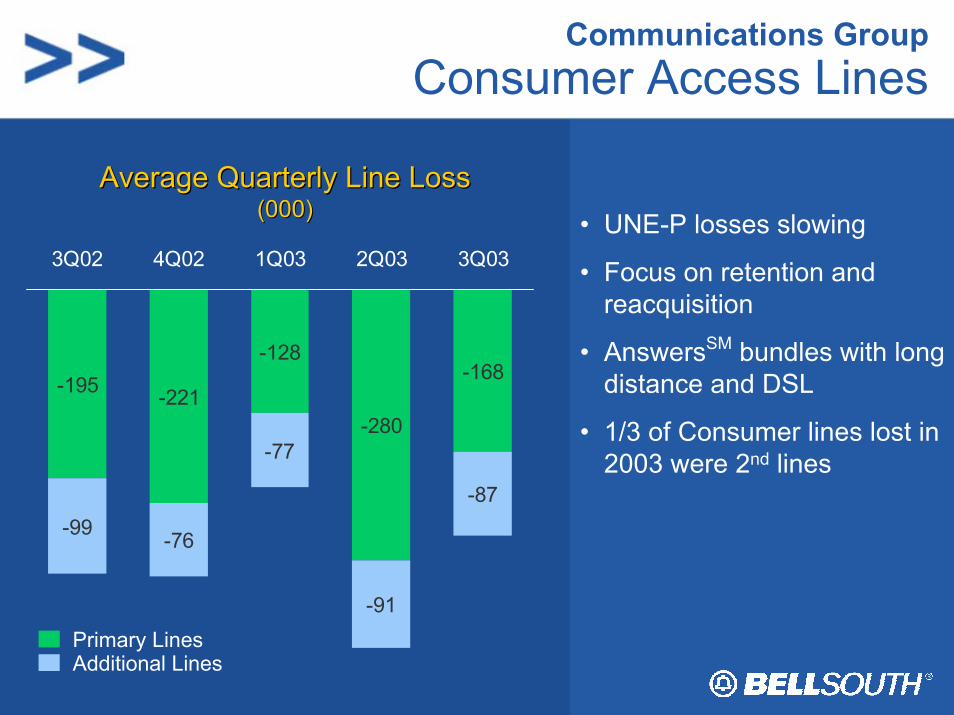

Communications GroupConsumer Access Lines

• UNE-P losses slowing

• Focus on retention and reacquisition

• AnswersSM bundles with long distance and DSL

• 1/3 of Consumer lines lost in 2003 were 2nd lines

-195 -221

-128

-280

-168

-99 -76

-77

-91

-87

3Q02 4Q02 1Q03 2Q03 3Q03

Average Quarterly Line LossAverage Quarterly Line Loss(000)(000)

Primary Lines Additional Lines

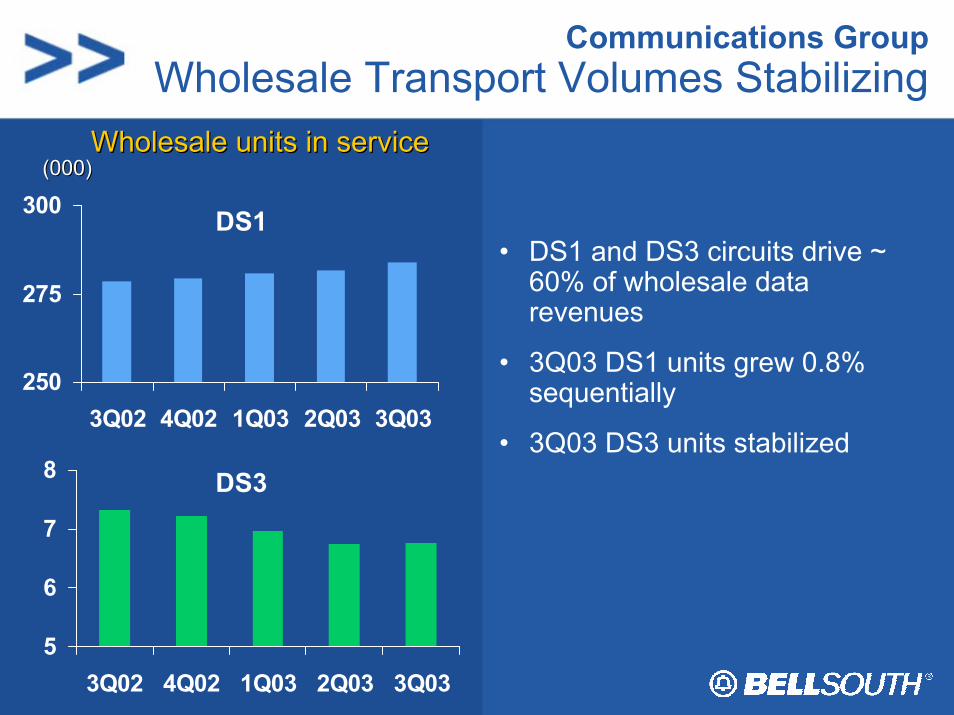

Communications GroupWholesale Transport Volumes Stabilizing

• DS1 and DS3 circuits drive ~ 60% of wholesale data revenues

• 3Q03 DS1 units grew 0.8% sequentially

• 3Q03 DS3 units stabilized

Wholesale units in serviceWholesale units in service

5

6

7

8

3Q02 4Q02 1Q03 2Q03 3Q03

250

275

300

3Q02 4Q02 1Q03 2Q03 3Q03

(000)(000)

DS1

DS3

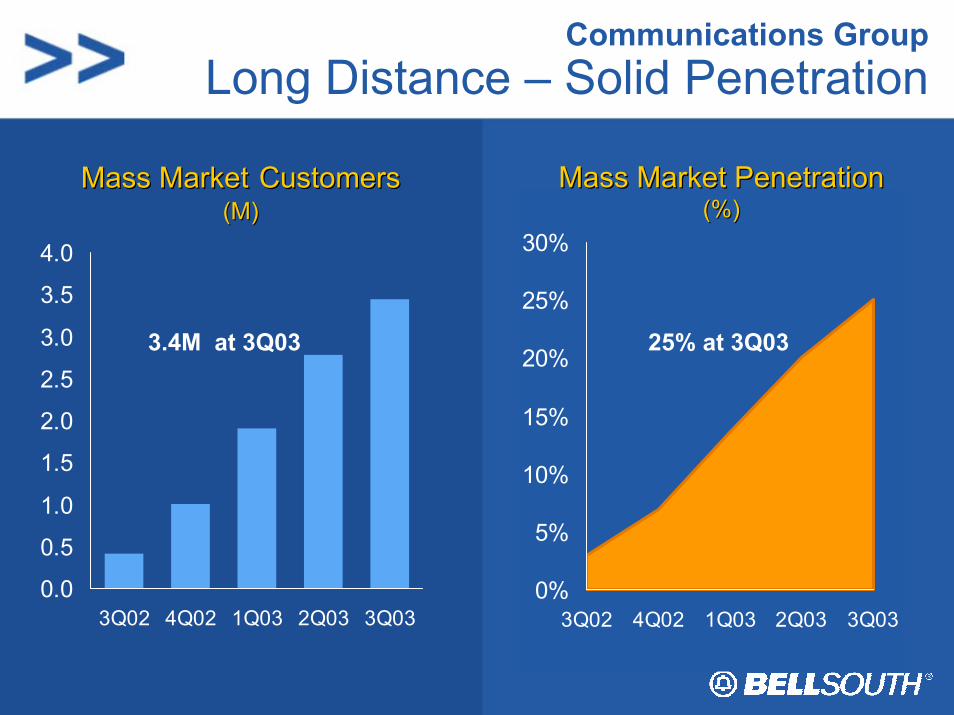

Communications GroupLong Distance – Solid Penetration

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

3Q02 4Q02 1Q03 2Q03 3Q03

Mass MarketMass Market CustomersCustomers(M)(M)

3.4M at 3Q03

0%

5%

10%

15%

20%

25%

30%

3Q02 4Q02 1Q03 2Q03 3Q03

Mass Market PenetrationMass Market Penetration(%)(%)

25% at 3Q03

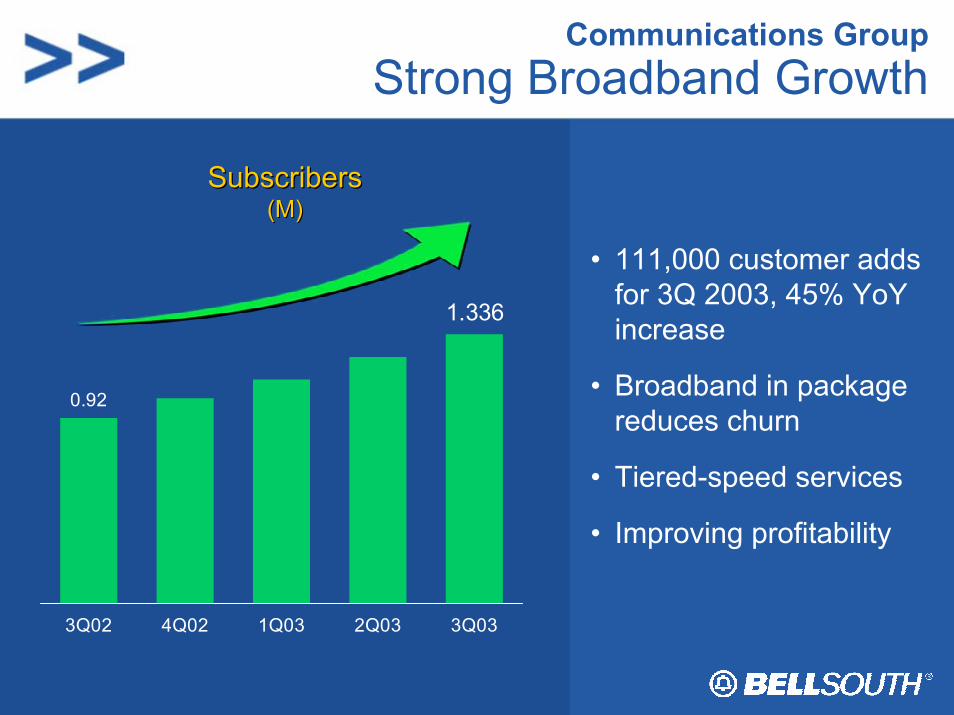

Communications GroupStrong Broadband Growth

• 111,000 customer adds for 3Q 2003, 45% YoYincrease

• Broadband in package reduces churn

• Tiered-speed services

• Improving profitability

0.92

1.336

3Q02 4Q02 1Q03 2Q03 3Q03

SubscribersSubscribers(M)(M)

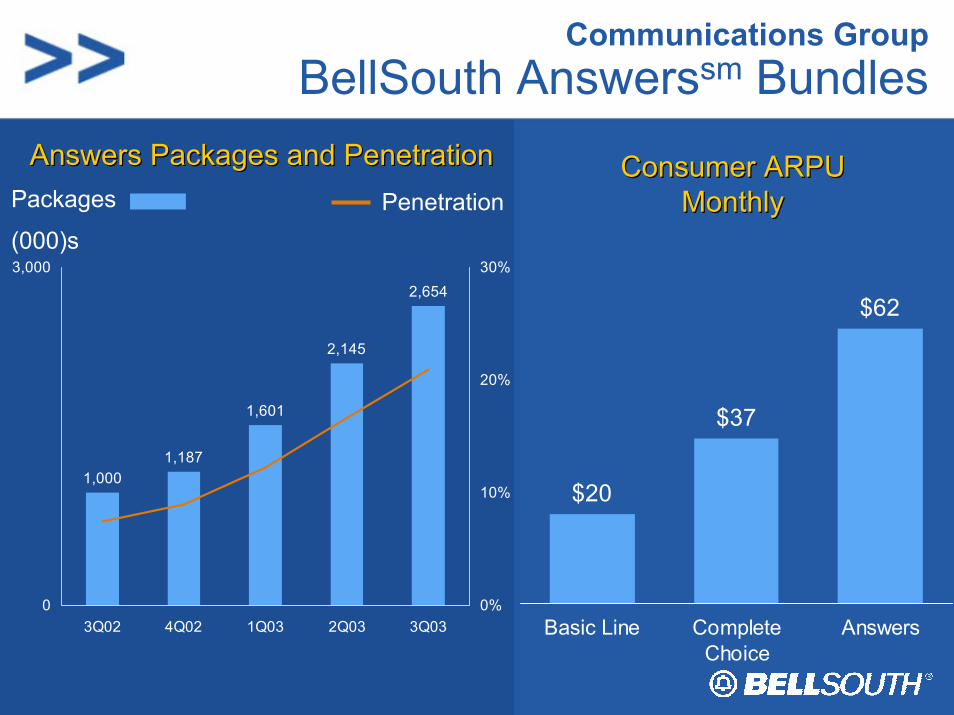

Communications GroupBellSouth Answerssm Bundles

Answers Packages and PenetrationAnswers Packages and Penetration

1,0001,187

1,601

2,145

2,654

0

3,000

3Q02 4Q02 1Q03 2Q03 3Q030%

10%

20%

30%

Packages

(000)sPenetration

$20

$37

$62

Basic Line CompleteChoice

Answers

Consumer ARPUConsumer ARPUMonthlyMonthly

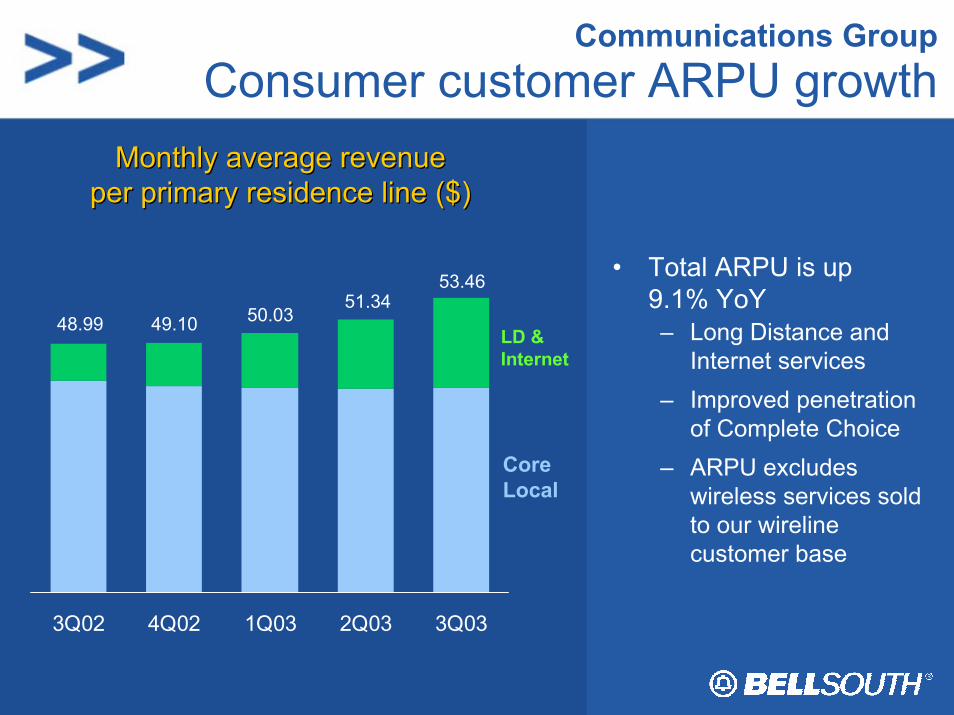

Communications GroupConsumer customer ARPU growth

3Q02 4Q02 1Q03 2Q03 3Q03

Monthly average revenueMonthly average revenueper primary residence line ($)per primary residence line ($)

• Total ARPU is up 9.1% YoY– Long Distance and

Internet services– Improved penetration

of Complete Choice– ARPU excludes

wireless services sold to our wirelinecustomer base

Core Local

LD & Internet

48.99 49.10 50.0351.34

53.46

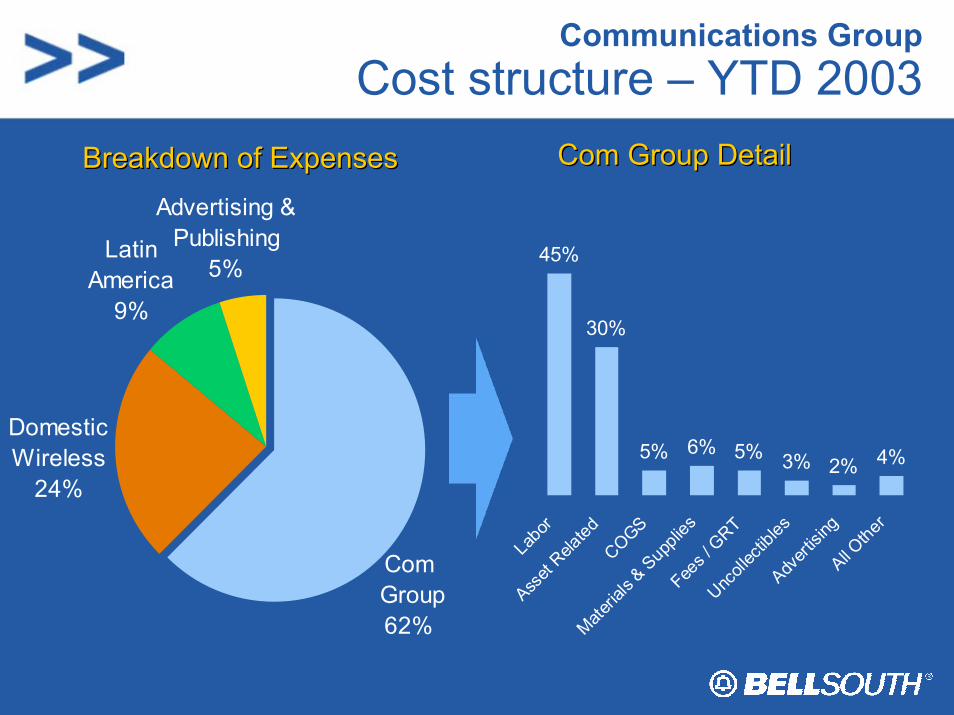

Communications GroupCost structure – YTD 2003

Com Group DetailCom Group DetailBreakdown of ExpensesBreakdown of Expenses

Domestic Wireless

24%

Latin America

9%

Advertising & Publishing

5%

Com Group62%

45%

30%

6% 5% 3% 2% 4%5%La

bor

Asset

Related

COGS

Materia

ls & S

uppli

esFee

s / G

RTUnc

ollec

tibles

Advert

ising

All Othe

r

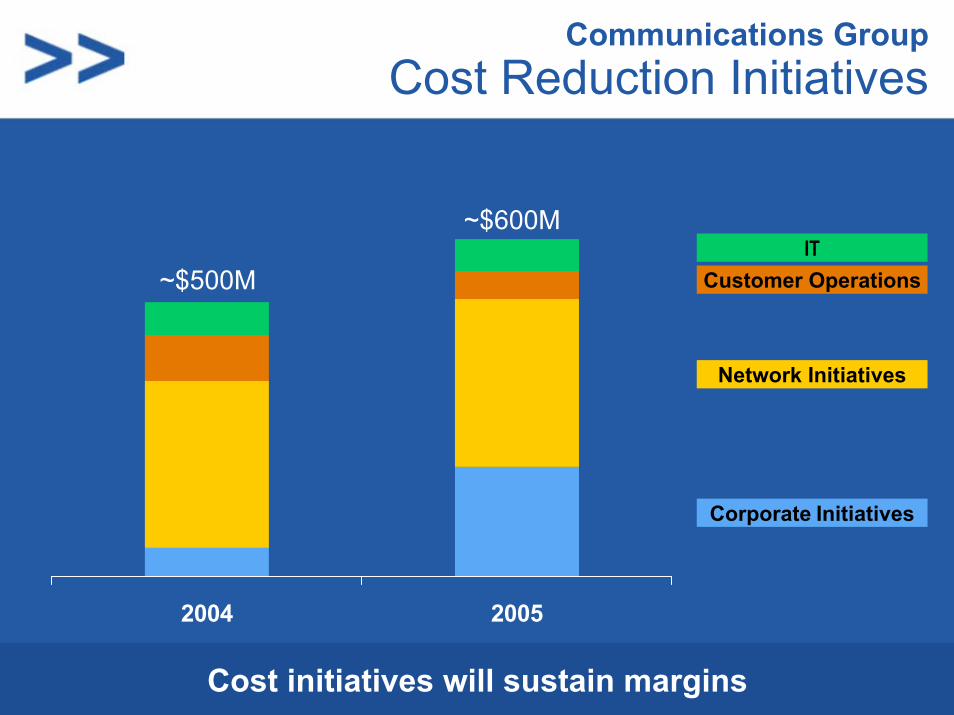

Communications GroupCost Reduction Initiatives

2004 2005

~$600M

~$500M

Corporate Initiatives

Network Initiatives

Customer OperationsIT

Cost initiatives will sustain margins

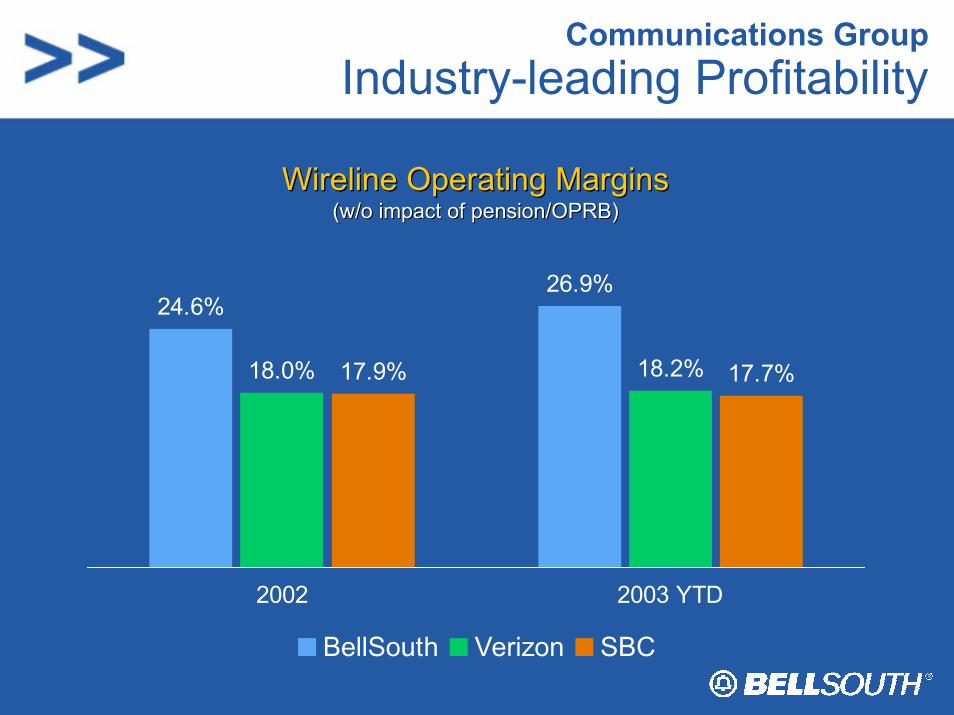

Communications GroupIndustry-leading Profitability

24.6%26.9%

18.0% 18.2%17.9% 17.7%

2002 2003 YTD

BellSouth Verizon SBC

WirelineWireline Operating MarginsOperating Margins(w/o impact of pension/OPRB)(w/o impact of pension/OPRB)

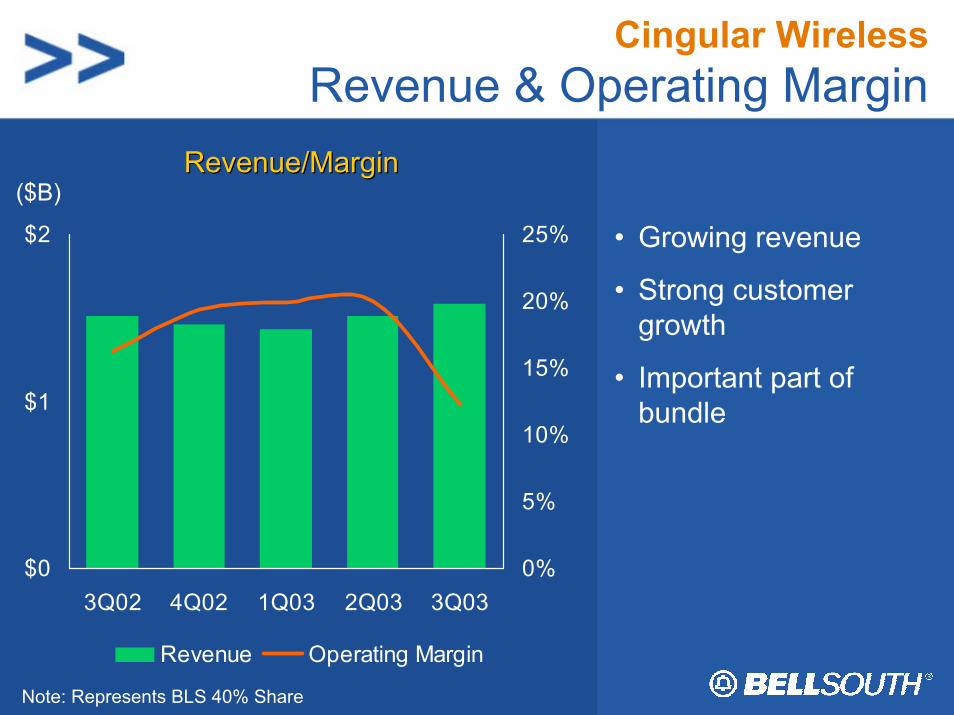

Cingular WirelessRevenue & Operating Margin

$0

$1

$2

3Q02 4Q02 1Q03 2Q03 3Q030%

5%

10%

15%

20%

25%

Revenue Operating Margin

Note: Represents BLS 40% Share

• Growing revenue

• Strong customer growth

• Important part of bundle

Revenue/MarginRevenue/Margin($B)

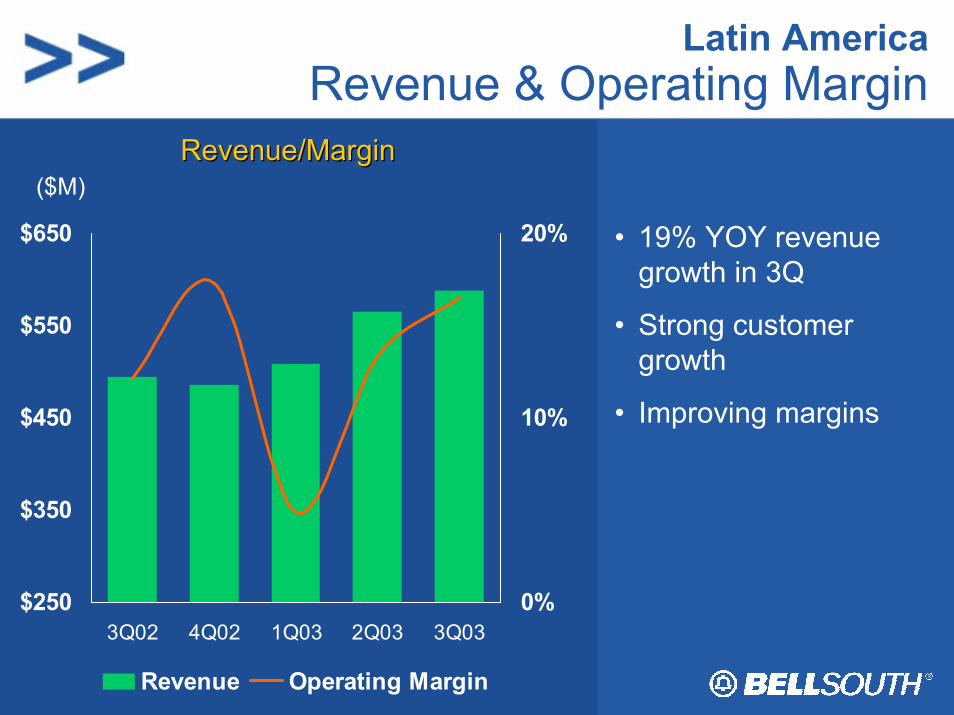

Latin America Revenue & Operating Margin

$250

$350

$450

$550

$650

3Q02 4Q02 1Q03 2Q03 3Q030%

10%

20%

Revenue Operating Margin

• 19% YOY revenue growth in 3Q

• Strong customer growth

• Improving margins

Revenue/MarginRevenue/Margin($M)

Advertising & PublishingRevenue & Operating Margin

$200

$300

$400

$500

$600

3Q02 4Q02 1Q03 2Q03 3Q0310%

20%

30%

40%

50%

Revenue Operating Margin

• Stable margins

• Strong cash flow

• Competition increasing

• Lags economic recovery

Revenue/MarginRevenue/Margin($M)

BellSouth TotalRevenue & Operating Margin

$5.5

$6.5

$7.5

3Q02 4Q02 1Q03 2Q03 3Q030%

10%

20%

30%

Revenue Operating Margin

• Revenue growth

• New wireline services continue to be strong

• Improving wireless growth

Revenue/MarginRevenue/Margin($B)

BellSouth TotalCapital Expenditures

Total BellSouthTotal BellSouth

CapexCapex Capex: Revenue RatioCapex: Revenue Ratio

$0.0

$0.6

$1.2

3Q02 4Q02 1Q03 2Q03 3Q030%

10%

20%

30%

($B)

BellSouth TotalHealthy Cash Flow

Operating Free Cash FlowOperating Free Cash Flow

2000 2001 2002 2003YTD

$4.5B

$2.0B$1.6B

$4.8B

Topics for Discussion

• Key Operating and Financial Trends – 2003– Communications Group– Cingular Wireless– Latin America– Advertising & Publishing– BellSouth Overall

• Business Financial Trends – 2004

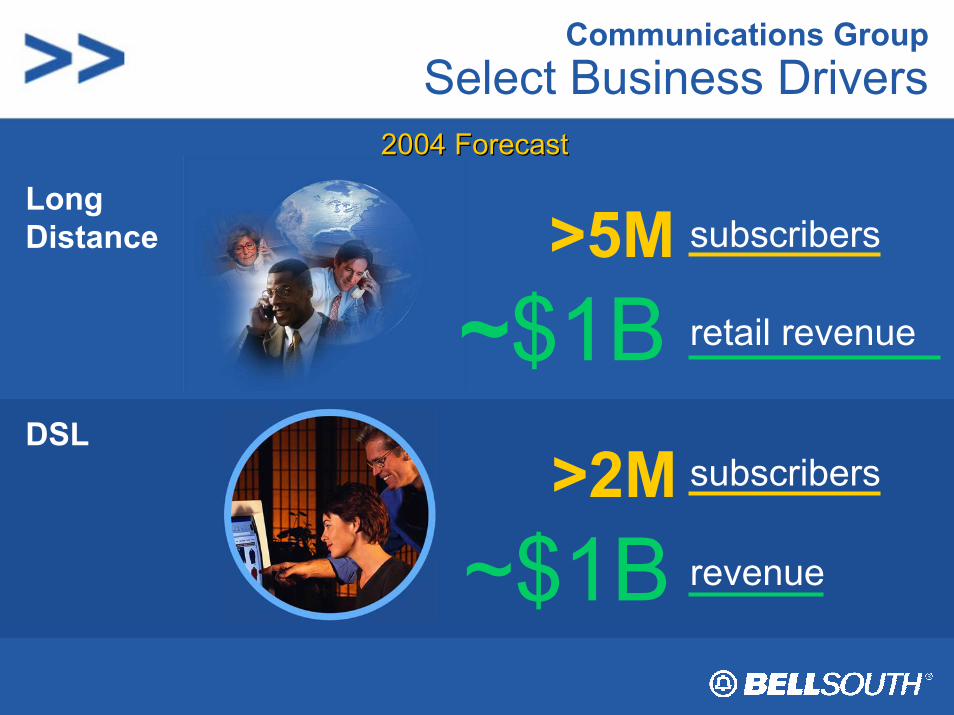

Communications GroupSelect Business Drivers

>5M subscribers

2004 Forecast2004 Forecast

~$1B retail revenue

Long Distance

DSL>2M subscribers

~$1B revenue

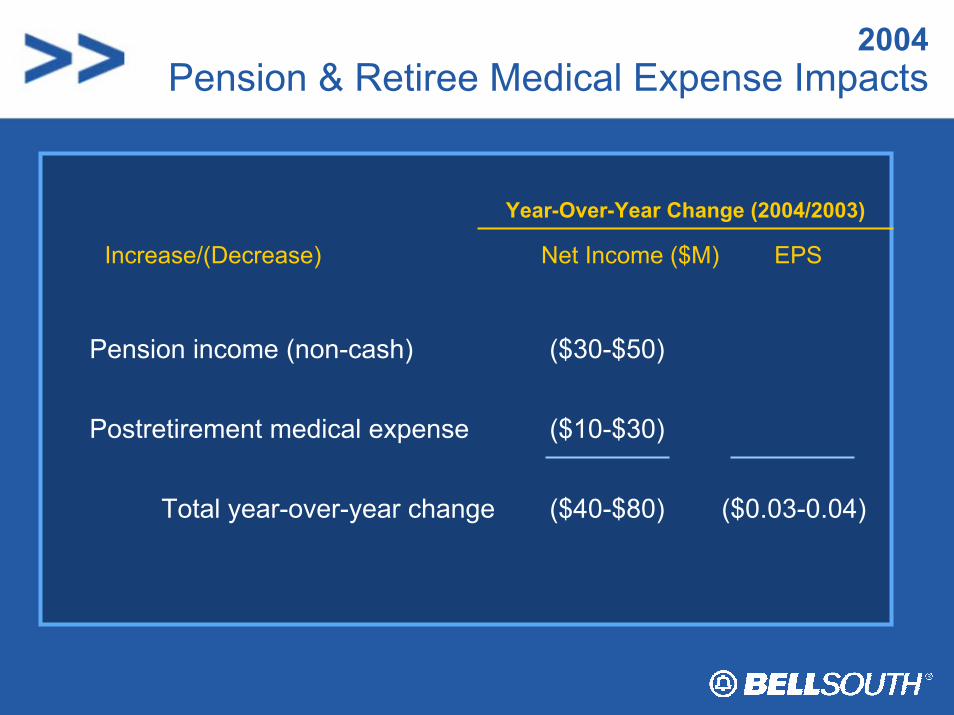

2004Pension & Retiree Medical Expense Impacts

Pension income (non-cash)

Postretirement medical expense

Total year-over-year change

Increase/(Decrease) Net Income ($M) EPS

Year-Over-Year Change (2004/2003)

($30-$50)

($10-$30)

($40-$80) ($0.03-0.04)

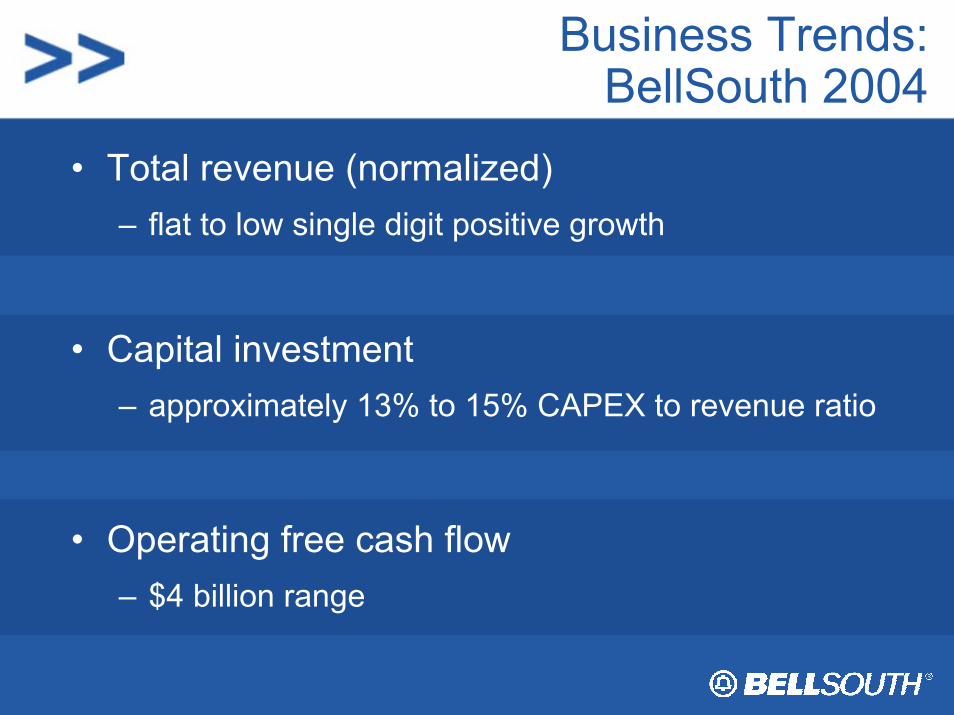

Business Trends:BellSouth 2004

• Total revenue (normalized)– flat to low single digit positive growth

• Capital investment– approximately 13% to 15% CAPEX to revenue ratio

• Operating free cash flow– $4 billion range

BellSouth – Demonstrating Leadership

Performance improving– strong margins

Cingular growth

Latin America growing and profitable

Strong cash flow

BellSouth: A Competitive ForceRon Dykes, CFO

BellSouth: A Competitive ForceAnalyst Briefing

New York, NYNovember 10, 2003