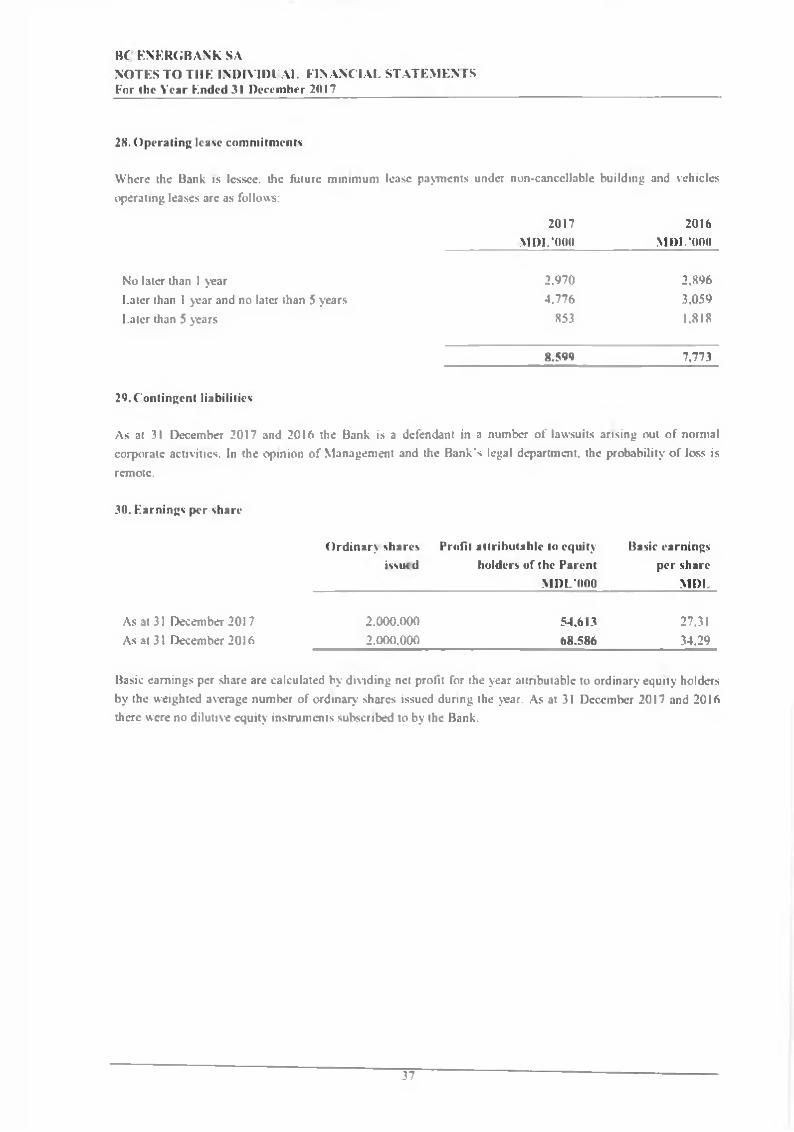

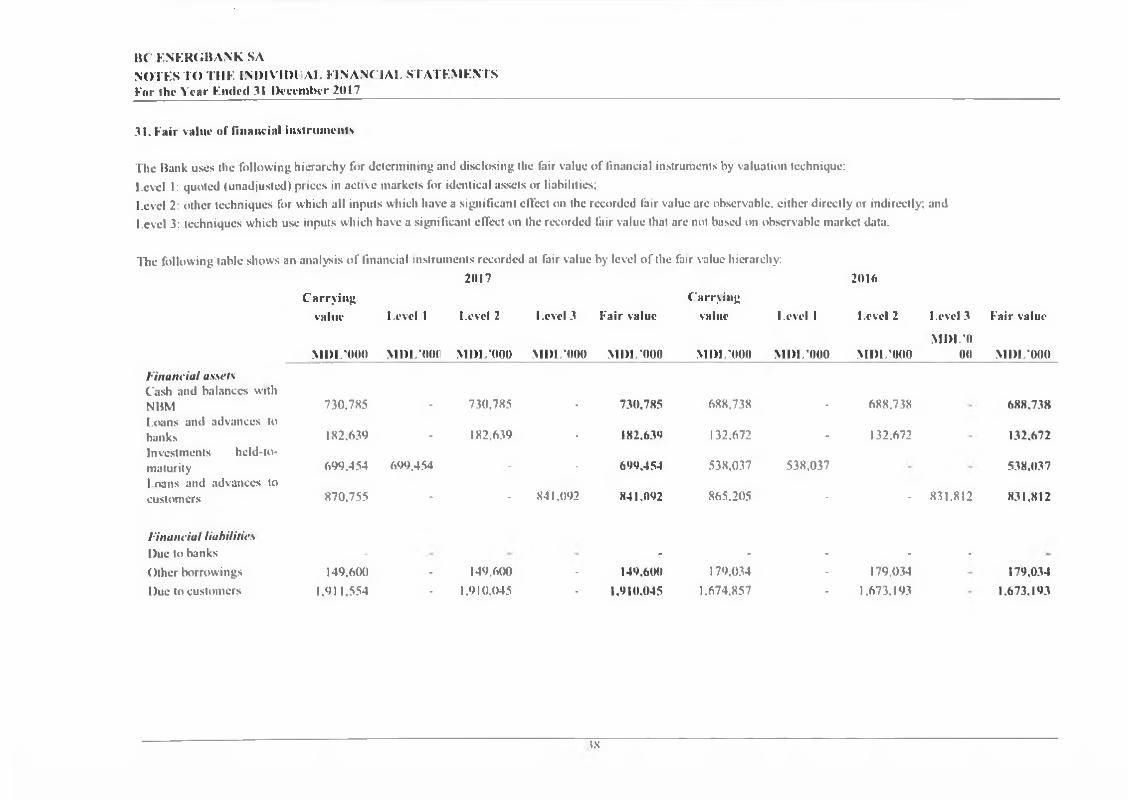

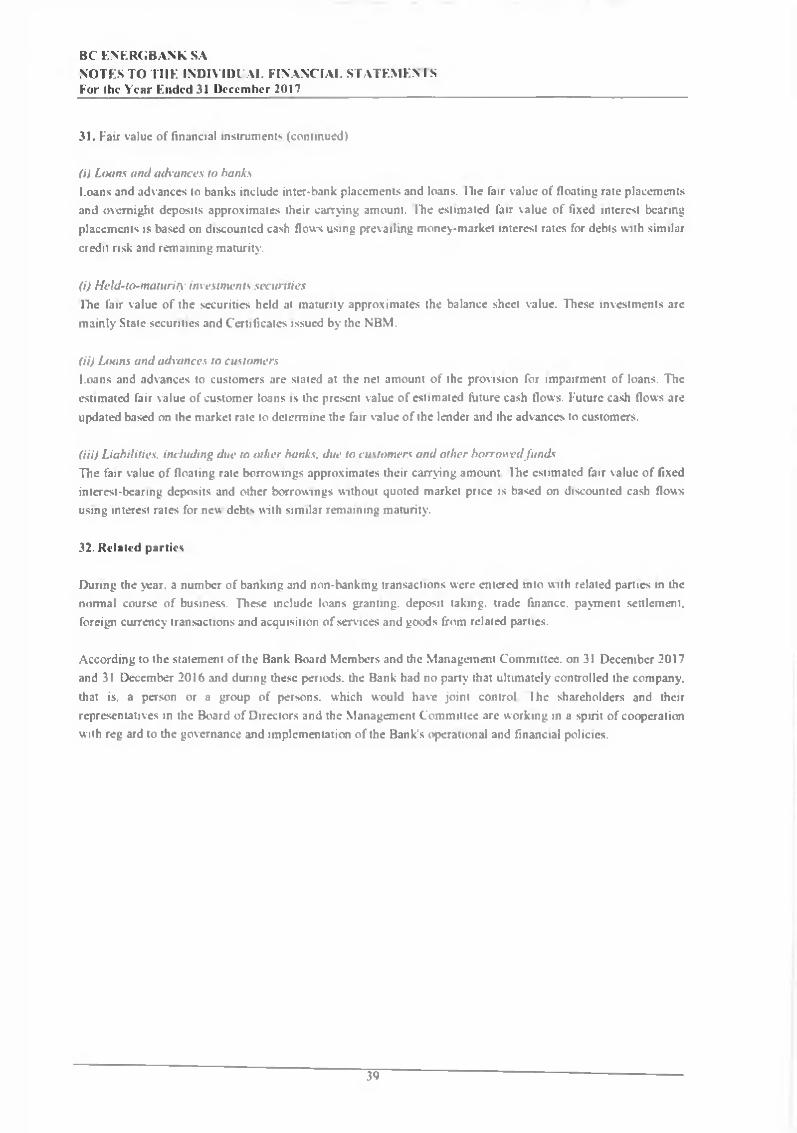

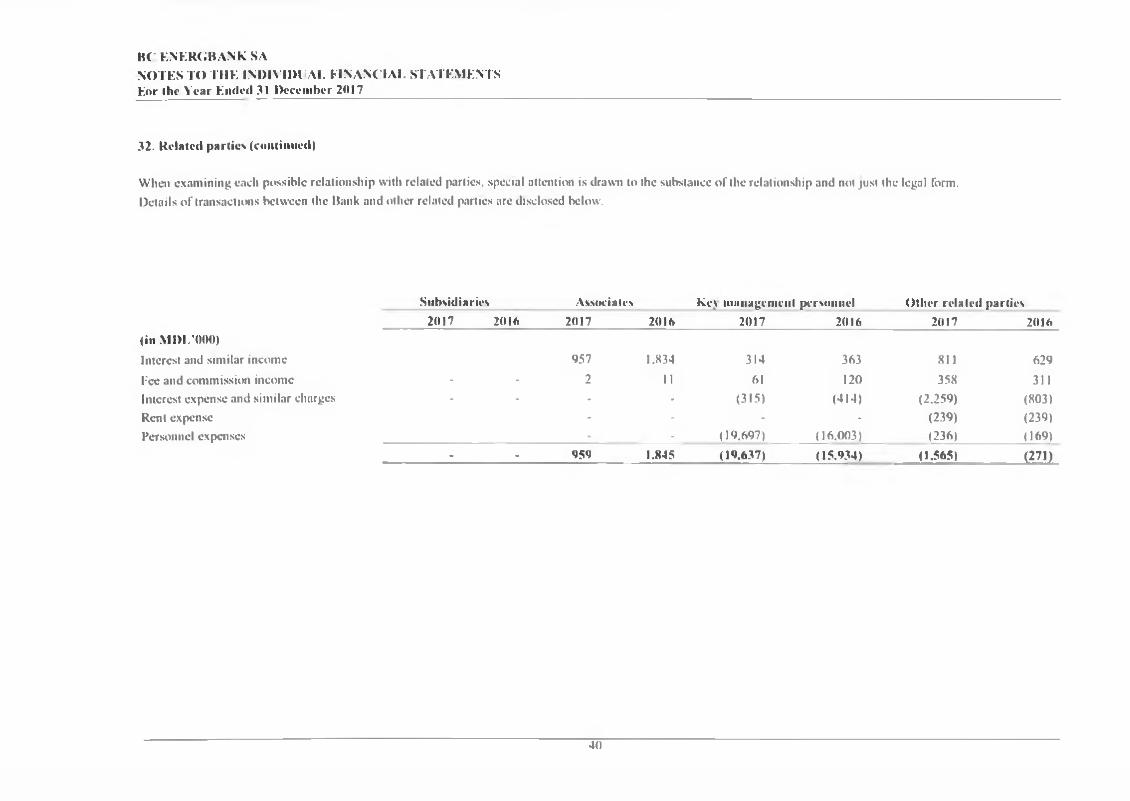

BC ENERGBANK SA INDIVIDUAL STATEMENT OF FINANCIAL...

61

BC ENERGBANK SA INDIVIDUAL STATEMENT OF FINANCIAL POSITION As at 31 Deeeniber 2017 ______ Note 2017 2016 MDI.*000 MDL’000 ASSETS Cash and balances with National Bank 3 730.785 688.738 C'urrent accounts and deposits with banks 4 182,639 132.672 Financial investments, debi securities held to matunty 5 699.454 538.037 Loans. net 6 870.755 865.205 Financial investments. cquity securities available-for-sale 7 2.733 3.331 Intangiblc assets 8 3.823 1.969 Property and equipment 9 131.183 130.808 C'urrent incomc tax asset 1.427 855 Other assets 10 52,614 53.811 Total assets 2.675.413 2.415.426 LIAB1LITIES Due to customers 11 1.911.554 1.674.857 Other borrowings 12 149.600 179.034 Other liabihties 13 15.503 17.219 Defcrred tax liabilitics 14 3.348 2.923 Total liabilitics 2.080.005 1.874.033 Shareholders' equity Ordinary shares 15 100.000 100.000 Property revaluation reserve 15.368 15.966 Other reserv es 16 152.940 147.111 Retaincd eamings 327.100 278.316 Total shareholders' equity 595,408 541.393 Total liabilities and shareholders* equity 2.675.413 2.415.426 The accompanying notes arc an integral pan of these financial statements. The financial statements were authorized for issue on 04 April 2018 by the Executives of the Bank represented by: C'hicf Accountant Mr. Sergiu Slobcxlean I

Transcript of BC ENERGBANK SA INDIVIDUAL STATEMENT OF FINANCIAL...

BC ENERGBANK SAINDIVIDUAL STATEMENT OF FINANCIAL POSITIONAs at 31 Deeeniber 2017 ______

Note 2017 2016M DI.*000 MDL’000

ASSETSCash and balances with National Bank 3 730.785 688.738

C'urrent accounts and deposits with banks 4 182,639 132.672

Financial investments, debi securities held to matunty 5 699.454 538.037

Loans. net 6 870.755 865.205

Financial investments. cquity securities available-for-sale 7 2.733 3.331

Intangiblc assets 8 3.823 1.969

Property and equipment 9 131.183 130.808

C'urrent incomc tax asset 1.427 855

Other assets 10 52,614 53.811

Total assets 2.675.413 2.415.426

LIAB1LITIESDue to customers 11 1.911.554 1.674.857

Other borrowings 12 149.600 179.034

Other liabihties 13 15.503 17.219

Defcrred tax liabilitics 14 3.348 2.923

Total liabilitics 2.080.005 1.874.033

Shareholders' equityOrdinary shares 15 100.000 100.000Property revaluation reserve 15.368 15.966Other reserv es 16 152.940 147.111Retaincd eamings 327.100 278.316

Total shareholders' equity 595,408 541.393

Total liabilities and shareholders* equity 2.675.413 2.415.426

The accompanying notes arc an integral pan o f these financial statements.

The financial statements were authorized for issue on 04 April 2018 by the Executives o f the Bank representedby:

C'hicf Accountant Mr. Sergiu Slobcxlean

I

BC ENERGBANK SAINDIVIDUAL STATEMENT OF COMPREHENSIVE INCOMEFor the Year Fnded 31 December 2017

Note 2017M DL’000

2016 M DL'000

Intercst and similar income Inter est expense and similar charges

2020

159.550(61.478)

184.863(78.242)

Noi intercst and similar income 98.072 106.621

Fee and commission income Fee and commission expense

2121

55.792(10.767)

50.421(9.390)

Net fee and commission income 45.025 41,031

Financial income. net Othcr operating expenses. net

2123

46.3701.511

50.2921.723

Total operating income 190,978 199,667

Impairment o f loansImpairment o f receivablcs and othcr assets

6 (9.765)(5,220)

(7.152)(13.099)

Net operating income 175,993 179.416

Pcrsonncl expensesGeneral and administrative expensesDcpreciation and amortization

2425

8 .9

(73.489)(36,295)

(6.044)

(68.311)(30.784)

(5.507)Total operating expenses (115.828) (104.602)

Profit before lax 60.165 74.814

Income tax expense 14 (5,552) _ (6.228)Profit for the year 54,613 68.586

Other comprehensive income

Impairment o f financial assets (598) .

Other comprehensive income (598) -

Total comprehensive income for the year 54.015 68.586

Eamings per share (MDL per sliarc) 30 27,31 34.29

The accompanying notes arc an integral pan o f these individual financial statements.

The individual financial statements were authonzed for issue on 04 April 2018 by the Executives o f the Bank represented by:

President

Mr. Iurii Vasilachi

Chief Accountant

Mr. Sergiu Slobodean

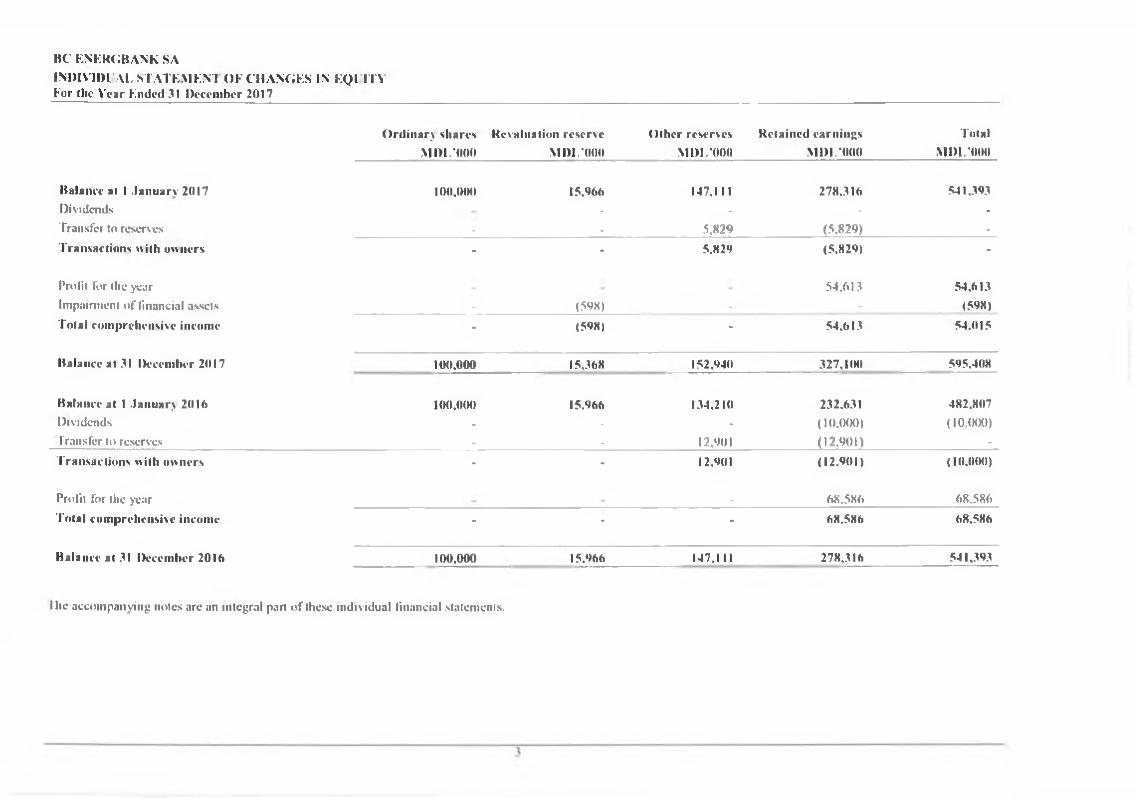

b c e n f k g b a n k s a

INDIVIDUAL STATEMENT OF C'HANCiES IN EQUITYFor ihc Year Fndcd 31 Dcccmbcr 2017

O rd in a ry shares Kevaliialion reserve O ther reserves K ctaincd earn ings TotalM 1)1/000 M D I.'000 M D L'000 M D I.*000 M DL'000

Balancc al 1 .1 anuarv 2017 100,000 15.966 147.111 278.316 541.393Dividends - - - -

Transfer to reserves _ . 5.829 (5.829) -

Transactions with owners - - 5.829 (5.829) -

Profit for the year 54.613 54.613Impairment o f financial assets . (598) - - (598)

Total com prehensive income - (598) - 54.613 54.015

Balancc al 31 Dcccmbcr 2017 100,000 15.368 152.940 327.100 595.408

Balancc at 1 J a n u a r) 2016 100.000 15.^66 134.210 232.631 482.807Dividends • - - (10.000) (10.000)Transfer tu reserves . - 12,901 (12.901) -

T ransactions with o n n ers - - 12.901 (12.901) (10.000)

Prolit for the year . 68.586 68,586

Total com prehensive income - - - 68.586 68.586

Balancc at 31 Dcccmbcr 2016 100,000 15,*>66 147.111 278.316 541,393

Ihe accompanying notes arc an integral part o f these individual financial statements.

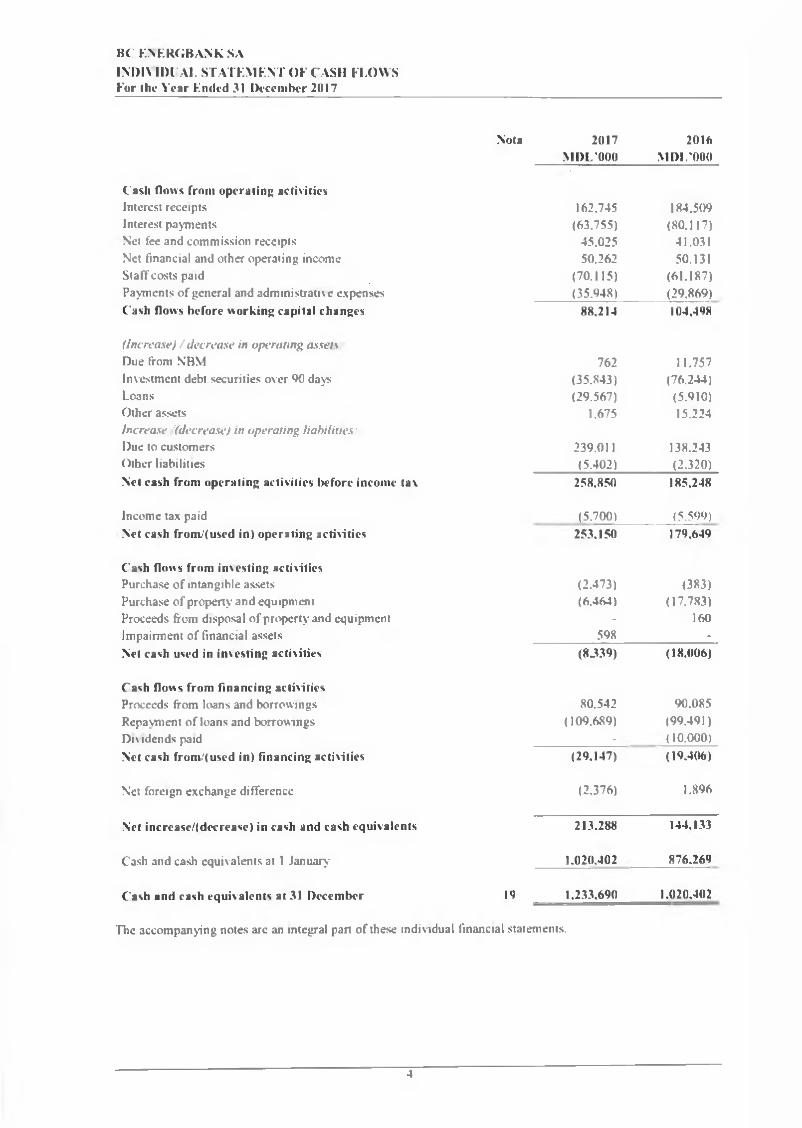

BC ENERGBANK SA

INDIV IDUAL STATEMENT OF CASH FLOWSFor the Y'ear Ended 31 December 2017

Nota 2017 2016MDL’000 MDL *000

Cash flows from operating activiticsInterest receipts 162.745 184.509Interest payments (63.755) (80.117)Net fee and commission receipts 45.025 41.031Net financial and other operating income 50.262 50.131StalTcosts paid (70.115) (61.187)Payments o f general and administrative expenses (35.948) (29,869)Cash flows before working capital changcs 88,214 104,498

(Increase) / decrease in operating assetsDue from NBM 762 11.757Investment deht securities over 90 days (35.843) (76.244)Loans (29.567) (5.910)Other assets 1.675 15.224Increase /(dec re ase) in operating liahilities:Due to customers 239.011 138.243Other liabilities (5.402) (2.320)Net cash from operating activitics beforc income tax 258.850 185,248

Income tax paid (5.700) (5.599)Net cash from/(used in) operating activitics 253.150 179,649

Cash flows from investing activiticsPurchase o f intangible assets (2.473) (383)Purchase o f property and equipment (6.464) (17,783)Proceeds from disposal o f property and equipment - 160Impairment o f Financial assets 598 -Net cash uscd in investing activitics (8339) (18.006)

Cash flows from financing activiticsProceeds from loans and borrovvings 80.542 ‘>0.085Repayment o f loans and borrowings (109.689) (99.491)Div idends paid - (10.000)Net cash from/(uscd in) financing activitics (29,147) (19.406)

Net foreign exchange differencc (2,376) 1.896

Ncl incrcase/(dccreasc) in cash and cash cquivalcnts 213,288 144.133

Cash and cash cquivalents at 1 January 1.020.402 876.269

Cash and cash cquivalcnts at 31 December 19 1.233.690 1.020.402

The accompanying notes arc an integral part o f these individual financial statements.

4

BC ENERGBANK SANOTES TO THE INDIVID!'Al. FINANCIAL STATEMENTSFor (hc Year Fndcd 31 Dcccmbcr 2017

1. General information about Bank

BC' Fnergbank SA ("the Bank” ) was cstablishcd in the Republic o f Moldova on 16 January 1997 as a closed joint stock company. The Bank is principally engaged m retail banking opcrations in the Republic o f Moldova. The Bank opera tes through its head oflice located in Chisinau. 22 branches (22 branches as at 31 December 2016) and 43 agencies (43 agencies as at 31 Dcccmbcr 2016) located throughout the country. At the end o f 2017 the Bank possessed a license granted by the National Bank o f Moldova, which allows the Bank to bc engaged in

all banking activities.

The number o f employces employed by the Bank as at 31 December 2017 was 594 (593 as at 31 December 2016).

The registered oftice o f the Bank is located at 23 3 I ighina Street. Chisinau. Republic o f Moldova.

As Bank's opcrations do not have sigmficantly dilTerent nsks and retums and considering the regulatory environment. the nature o f its serviccs. the business process. as well as the types o f customers for the products and service> and the methods used to provide the services are homogenous for all Bank’s activities. the Bank operates as a smgle business segment unit and its activities arc cxclusivelv cam ed out in the Republic of Moldova.

fhc Board o f Directors formulatcs policics for die operation o f the Bank and supervises thcir implcmcntation. Ilie Board is composed o f 7 members appc>inted by the General Meeting o f Shareholders.

As at 31 December 2017 the Board o f Directors comprised the following members:

- Mr. Vladimir Tonciuc. C'hairman o f the Board:- Mr.Valeriu Usatu. Fnergoimpex. Mcmbcr o f the Board:- Mr.Mihail Pop. Mcmber of the Board.- Mrs. Natalia Cecctova. Gamaiun SRI . Member o f the Board:- Mrs.Maximenco Galina. Mcmbcr o f the Board:- Mrs. Natal ia Covanji. Member o f the Board:- Mr. Ghcnnadi Dimov. Member o f the Board.

ITiesc financial statements were authorised for issue on 04 Apnl 2018 by the Executives o f the Bank represented by the Prcsidcnt and the C'hief Accountant.

2. Accounting policics

2.1 Basis of preparation

Statement of compliance

The individual financial statements o f the Bank have been prepared in accordance with International Financial Rcponing Standards (IFRS) as issued by the International Accounting Standards Board (IASB).

Basis of measurement

I hc individual financial statements have been prepared under the histonc cost convention. except for land and buildings. invcstment propenies and a\ailablc-for-sale assets that have been measured at fair value.

5

BC ENERGBANK SANOTES TO T1IE INDIVIDUAL FINANCIAL STATEMENTSFor the Year Ended 31 December 2017

2. Accotiiiling policics (con(inued)

2.1 Basis of preparation (con(inued)

Funcţional and presentation currcnc)The individual financial statements are presented in Moldovan lei (“MDI "). which is also us funcţional currency and the currency o f the country m which the Bank operates. All financial In fo rm a t io n presented in MDL has bccn rounded to the nearest thousands. except when otherwise indicated.

2.2 Significant accounting judgments and estimates

ITie Bank makes estimates and assumptions that affect the reported amounts o f assets and liabilities within the next financial year. Estimates and judgements are continually evaluated and are based on historical experience and other factors. including expcctations of futurc events that arc belicvcd to bc rcasonablc under the circumstances.

(i) Impairment losses on loans and advancesThe Bank reviews its loan portfolios to assess impairment at least on a monthly basis. In determining whether an impairment loss should be recorded in the income statement. the Bank makes judgements as to whether thcrc is anv observable data indicating that thcrc is a measurable decrease in the estimated futurc cash flows from a portfolio o f loans before the decrease can be identitied with an individual loan in that portfolio. This evidence may include observable data indicating that thcrc has bccn an adverse changc in the paymcnt status o f borrowcrs in a Bank. or naţional or local economie conditions that correlate with defaults on assets in the Bank. Management uses estimates based on historical loss experience for assets with credit risk characteristics and objective evidence o f impairment similar to those in the portfolio when scheduling its future cash flows. The mcthodology and assumptions uscd for estimatmg both the amount and timing o f future cash flows are reviewed regularly to reduce any differences between loss estimates and actual loss experience.

Where the final outcome o f these factors is difi'crcnt from the amounts that were initially rccordcd. such differences could materially impact the provision for loan impairment in the period in which such detenmnation is made.

(ii) Going concernHie Bank’s management has made an assessment o f the Bank's ability to continuc as a going concern and is satisfied that the Bank has the rcsourccs to continuc in busmess for the foreseeable future. Furthermore, the management is not aware o f any material unccrtainties that may cast sigmficant doubi upon the Bank's ability to continue as a going concern. Thereforc. the financial statements continue to be prepared on the going concern

basis.

(iii) Fair value o f financial InstrumentsThe fair value o f financial instruments that are not traded in an active market is determmed by using valuaiion techniques. The management uses its judgment to select the valuation method and make assumptions that arc mainly based on market conditions existing at each balance sheet date.

6

BC ENF.RGBANK SANOTES TO MIE INDIVIDl AL FINANCIAL STATEMENTSFor ihc Year Fndcd 31 Dcccmbcr 2017

2. Accounting policics (continucd)

2.3 t'hangc in accounting policics

The accounting policics adopted arc consistcnt with those o f the previous financial year. The adopt ion o f new standards and interpretations eflective for the Bank from I January 2017 did not have any impact on the accounting policies. financial position or performance o f the Bank.

2.4 Significant accounting policics

The principal accounting policics apphed in the preparation o f these financial statements are set out helow.

a. Forcign currcncy translation

Foreign currency transactions arc translatcd into the funcţional currency using the exchangc rates prcvailing at the dates o f the transactions Foreign exchangc gains and losses resulting from the settlcmcnt o f such transactions and from the translation at year-end exchangc rates o f monetary assets and liabilitics denonunated in foreign currencies are recognized in the income statement.

Changes in the fair \a lue o f monetar, sccurities denommatcd in foreign currcncy classified as available for sale are analysed between translation dift'erences resulting from changes in the amortised cost o f the sccurity and other changes in the carrying amount o f the security. Translation differences related to changes in the amortised cost are recognized in profit or loss. and other changes in the carrying amount are recognized in equity.

Translation diffcrences on non-monetarv nems. such as equity investments classified as available-for-sa le financial assets, are includcd in the fair valuc reserve in equity The year-end and average rates for the year were:

____________2017_______________________ 2(U6___________t ’SD Euro LSI) Euro

Average for the period 18.4902 20.8282 19.9238 22.0548Year end 17.1002 20.4099 19.9814 20.8895

b. Financial assetsThe Bank classifics its financial assets in the following catcgones: loans and receivables, held-to-maturitv investments and available-for-sale financial assets. Management determincs the classification o f its investments at iniţial recognition.

(i) Loans and receivuhlesLoans and receivables arc non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. other than: (a) those that the entity intends to sell immediately or in the shorl term. which are classified as held for trading. and those that the entity upon mmal recognition designates as at lair valuc through profit or loss; (b) those that the entity upon iniţial recognition designates as available for sale: or (c) those for which the holder may not recover substantially all o f its iniţial investment. other tlian because of credit detenoration.

(ii) Held-to-maturityHeld-to-maturity investments are non-derivative financial assets with fixed or determinable payments and fixed maturities that the Bank’s management has the positive intention and ability to hold to maturity. If the Bank were to sell other than an insignificant amount o f held-to-maturity assets, the entirc category would be tainted and reclassified as available-for-salc.

(iii) A vailuhle-for-salcAvailable-for-sale investments are those intended to be held for an indefinite period o f time. which may be sold in response to nccds for liquidity or chango in interest rates. exchangc rates or equity prices. State securities are

7

BC ENERGBANK SANOTES I O THE INDIVIDUAL FINANCIAL STATEMENTSFor ihe Year Ended 31 December 2017

2. Accounting policics (continiied)

2.4 Significant accounting policics (continiied)

(iii) A vailable-for-sale (continiied) also included in this category.

h. Financial assetsRegular way purchascs and salcs o f financial assets at fair valuc through profit and loss, hcld-to-maturity and available-for-sale are recognized on trade-date the date on which the Bank commits to purchase or sell theasset.

Financial assets are initially recognized at fair value plus transaction costs for all financial assets not carried at fair value through profit or loss. Financial assets cam ed at fair value through profit and loss are initially recognized at fair value. and transaction costs arc expensed in the income statement. Financial assets are derecognized when the rights to receivc cash flows from the financial assets have expired or where the Bank has transferred substantially all risks and rewards o f ownership. Financial Iiabilities are derecognized when they are extinguished. that is. when the obligation is dischargcd. cancclled or expired.

Available-for-salc financial assets and financial assets at fair valuc through profit or loss are subsequentlv carried at fair value. I.oans and receivables and held-to-maturity investmenis are carried at amortized cost usmg the effective interest method. Gains and losscs arising from changes in the fair value o f the 'financial assets at fair value through profit or loss’ category are included in the income statement in the period in which they arise. Gains and losscs arising from changes in the fair value o f available-for-sale financial assets arc recognized directiv in cquitv. until the financial asset is derecognized or impaired. At this tirne. the cumulative gain or loss previously recognized in equity is recognized in profit or loss.

However. tnterest calculated using the effective interest method and foreign currency gains and losses on monetary assets classilied as available for sale are recognized in the income statement. Dividends on available- for-salc equity instrumente are recognized in the income statement when the entity’s right to receivc payment îs cstablishcd.

The fair values o f quoted investments in active markets are based on current bid prices. or if no such price is available. the last traded price on such day. If the market for a financial asset îs not active (and for unlisted securitics). the Bank cstablishes fair value by using valuation techniques. These include the use o f recent arm 's lcngth transactions. discounted cash flow analysis, option pricing models and other valuation techniques commonlv uscd by market participants.

c. Investments in associatesAn associate is an entity in which the Bank has significant înlluence and which is neither a subsidiary nor a joint venture. In the separate financial statements o f the Bank. investments in associatcs are cam ed at cost less

impairment losses.

d. Offsetting financial instrumentsFinancial assets and Iiabilities are offset and the net amount reported in the balancc sheet when there îs a legally enforccable right to set ofTthe rccognized amounts and there is an intention to settle on a net basis. or reali/e the

asset and settle the liability simultaneously.

8

BC ENERCBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor the Vear Fndcd 31 Dcccmbcr 2017

2. Accounting policics (continucd)

2.4 Significant accounting policics (continucd)

c. Intcrest income and expenseIn ter est income an d expense for all in tcrest bcaring financial Instrum ents, except for those c lassified as held for trading or designated at fair valuc through profit or loss. are rccognized in the income statement for all Instrum en ts m easu red at amortised cost using the eflcctive intcrest method.

Tlie effective interest method îs a method o f calculating the amortised cost of a financial asset or a financial liability and o f allocating the intcrest income or intcrest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments or reccipts through the expected Iile o f the financial instrument or. when appropriate. a shorter period to the net canying amount o f the financial asset or financial liability. When calculating the effective interest rate. the Bank estimates cash flows considermg all contractual tenns o f the financial instrument but does not consider future credit losses. The calculation includcs all fees and commissions paid or rcceived bctween parties to the contract that are an integral part of the effective interest rate. transaction costs and all other premiums or discounts.

Once a financial asset or a Bank of financial assets has been written down as a rcsult o f an impairment loss. interest income îs rccognized using the rate o f interest used to discount the future cash fiows for the purposc o f mcasuring the impairment loss.

f. Fee and comniission incomeFees and commissions are generally recogni^ed on an accrual basis when the scrvice has been provided. Loan commitment fees for loans that arc likclv to be drawn down are deferred (togeiher with related dircct costs) and rccognized as an adjustment to the cffcctive interest rate on the loan. Commission and fccs ansing from ncgotiating. or participating in the negotiation of. a transaction for a third partv such as the arrangement o f the acquisition of shares or other securities or the purchase or sale of businesses are rccognized on complction of the underlying transaction. Portfolio and other management advisory and sem ee fees are rccognized based on the applicable service contracts. usually on a time-apportion basis.

g. Sale and repurchase agreementsSecurities sold subiect to repurchase agreements (‘repos’) arc classified in the financial statements as available- for-sale securities (treasury bills) and the counter partv liability is included in amounts duc to banks or customers. as appropriate Securities purchased under agreements to rescll (‘reverse repos-) are rccorded as loans and advanccs to other banks or customcrs. as appropriate. The differencc bctween sale and repurchase price is treated as interest and accrued over the life o f the agreements using the effective interest method.

Securities held by the Bank as collateral for lending activities with financial institutions arc not rccognized in the financial statements. unless these arc sold to third parties. in which casc the purchase and sale are recorded with the gain or loss included in tradmg mcome. The obligation to retum them is recorded at fair value as a trading liability.

h. Derccognition

The Bank derecognises a financial asset when the contractual rights to the cash flows from the asset expire, or ît transfers the rights to receive the contractual cash flows on the financial asset in a transaction m which substantially all the risks and rcwards o f ownership o f the financial asset are transferred Any interest in transferred financial assets that is crcated or retained by the Bank is recognised as a separate asset or liability.

On derccognition o f a financial asset. the differencc bctwccn the carrying amount o f the asset (or the carrying amount allocated to the portion ol the asset transferred). and the sum o f (i) the consideration received (including any newr asset obtained less any new liability assumed) and (ii) any cumulative gam or loss that had been

9

BC ENERGBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor Ihe Year Ended 31 December 2017

2. Accounting policics (continucd)

2.4 Significant accountin" policics (continucd)

h. Derecognition (continucd)

recogni/cd in othcr comprehensive income îs recognized in profit or loss.

The Bank derccogmses a financial liabilitv when its contractual obligations are discharged or cancelled or expire.

The Bank enters into transactions whercby it transfers assets rccognised on its statement o f financial position. but retains either all risks and rewards o l'the transferred assets or a portion o f them. I f all or substantially all risks and rewards are rctaincd. then the transferred assets are not dcrccognised from the statement o f financial position. Transfers o f assets with retention o f all or substantially all risks and rewards include, for example, securities lending and repurchase transactions.

The rights and obligations rctaincd in the transfer arc rccognised scparatcly as assets and Iiabilities as appropriate. In transfers where control over the asset is retained. the Bank continues to recognise the asset to the extent o f its continuing involvement. determined by the extern to which it is exposed to changes in the valuc of the transferred asset.

i. Impairment of Financial assets

(i) Assets carried ut amortized costs

The Bank's asscsscs at each balance sheet date whether there is objective evidence that a financial asset or Bank o f financial assets îs impaircd. A financial asset or a Bank o f financial assets is impaired and impairment losses are incurred if. and only if, there is objective evidence o f impairment as a result o f one or more events that occurrcd after the iniţial rccognition o f the asset (a 'loss cveni*) and that loss event (or events) has an impact on the estimated futurc cash flows o f the financial asset or Bank o f financial assets that can be reliably estimated.

The criteria that the Bank uses to determine that there îs objective evidence o f an impairment loss include:

• Delinqucncy in contractual payments o f principal or interest;• Cash tlow difficulties experienced by the borrowcr (for example. equity ratio. net income pcrcentage o f sales):• Breach o f loan covcnants or conditions:• Imtiation o f bankruptcy proceedings;• Deterioration o f the borrower’s competitive position:• Deterioration in the value o f collateral; and• Downgrading bclow investment grade levcl.

Ihe estimated period between a loss occu rrin g and its Identification is determ ined by th e Bank m anagem ent for each identified portfolio. In general, the periods vary from 6m onths to 12 months.

10

BC ENERGBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor the Year Fuded 31 December 2017

2. Accounting policies (continued)

2.4 Significant accounting policies (continued)

i. Impairment of financial assets (continued)The Bank iirst assesses whether objective evidence o f impairment exists individually for financial assets that are individually sigmficant. and thcrcaftcr indi\idually or collectively for financial assets that are not individually significant. If the Bank determines that no objective evidence o f impairment exists for an individually assessed financial asset. whether significant or not. it mcludes the asset in a Bank o f financial assets with similar credit nsk characteristics and collectively assesses them for impairment. Assets that are individually assessed for impairment and for which an impairment loss is or connnues to be recogm/.cd arc not included in a collective assessment o f impairment.

The amount o f the loss is measured as the difference between the asset's carrying amount and the present value o f estimated future cash flows (excluding future credit losses that have not been incurred) discounted at the financial asset's original effective interest rate. The carrying amount o f the asset is rcduced through the usc o f an allowance account and the amount o f the loss is rccognized in the income statement. If a loan or held-to-maturity investment has a variable interest rate. the discount rate for measunng any impairment loss is the currcnt effective interest rate determined under the contract.

rhe calculation o f the present valuc o f the estimated future cash flows o f a collateralizcd financial asset rcflccts the cash flows that may result from foreclosurc less costs for obtaining and selling the collateral. whether or not forcclosure is probable.

For the purposes o f a collective evaluadon o f impairment. financial assets are Banked on the basis o f similar credit nsk characteristics (i e., on the basis o f the Bank * grading proccss that considers asset type. industry. geographical location. collateral type. past-due status and other relevant factors). Those characteristics are relev ant to the estimation o f future cash flows for Banks o f such assets by being indicative o f the debtors* ability to pay all amounts due according to the contractual terms o f the assets bcing evaluated.

Future cash flows in a Bank o f financial assets that are collectively evaluated for impairment are estimated on the basis o f the contractual cash flows o f the asset* in the Bank and histoncal loss expcricnce for assets w ith credit nsk characteristics similar to those in the Bank. Histoncal loss experienţe is adjusted on the basis of currcnt observable data to reflect the effects o f current conditions that did not affect the period on which the histoncal loss expcricnce is based and to remove the effects o f conditions in the historica! period that do not exist currently.

Estimates o f changes in future cash flow s for Banks o f assets should reflect and be directionally consistent with changes in related observable data from period to period (for example. changes in unemployment rates. property priccs. paymcnt status. or other factors indicative o f changes in the probability o f losses in the Bank and their magnitude). ITj c methodology and assumptions used for estimating future cash flows arc reviewed regularly by the Bank to reduce any differences between loss estimates and actual loss experiencc. When a loan îs uncollectible. it is wntten off agamst the related provision for loan impairment. Such loans are written ofTafter all the necessary procedures have been completcd and the amount of the loss has been determined.

If in a subsequent period, the amount o f the impairment loss decrcascs and the decrease can be related objectively to an event occurnng afier the impairment was rccognized (such as an improvement in the debtor’s credit rating). the previously rccognized impairment loss is reversed by adjusting tlic allowance account. rhe amount o f the rcversal is rccognized in the income statement in impairment cliangc for credit losses.

11

BC ENERGBANK SANOTES TO T1IE INDIVIDUAL FINANCIAL STATEMENTSFor Ihe* Year Ended 31 December 2017

2. Accounting policics (continiied)

2.4 Signifîcant accounting policics (continiied)

i. Impairment of financial assets (continiied)

fii) Assets carried at fa ir valueThe Bank assesses at each balancc sheet date whether thcrc is objective evidence that a financial asset or a Bank o f financial assets is impaircd. In the case o f equity investments classified as available-for-sale. a signifîcant or prolongcd decline in the fair valuc o f the security below its cost is considered in determining whether the assets are impaircd. I f any such evidence exists for available-for- sale financial assets. the cumulative loss measured as the difYcrcnce bctwccn the acquisition cost and the current fair value. less any impairment loss on that financial asset previously recognized in profit or loss is removed from equity and recognized in the income statement. If. in a subsequent period, the fair value o f a debt instrument classified as available for sale increases and the increase can bc objectivcly related to an event occurring after the impairment loss was recognized in profil or loss. the impairment loss is reversed through the income statement.

fiii) Renegotiated loansWhcre possible. the Bank seeks to restructurc loans rather than to take possession of collateral. This may involve extending the payment arrangements and the agreement of new loan conditions. Oncc the terms have bccn renegotiated any impairment is measured using the original Effective Interest Rate (“EIR") as calculatcd before the modilîcation o f terms and the loan îs no longer considered past due. Management continuously reviews renegotiated loans to ensure that all criteria are met and that future payments arc likcly to occur. The loans continue to be subject to an individual or collective impairment assessment. calculated using the loan's original effective interest rate.

j. Impairment of non - financial assetsAssets that have an indefinite useful life are not subject to amortization and are tested annually for impairment. Assets that arc subjcct to amortization are revicwed for impairment whcncvcr events or changes in circumstances indicate that the carrying amount may not be reco\erable. An impairment loss is recognized for the amount by which the asset’s carrying amount exceeds its recovcrable amount. The recoverable amount is the higher of an asset’s fair valuc less costs to sell and value in usc. For the purposcs o f asscssmg impairment. assets are Banked at the lowcst levels for which there are separately identifiablc cash flows (cash-gcnerating units). Non-financial assets othcr than goodwill that sufTered impairment are reviewed for possible reversal o f the impairment at each reporting date.

k. Cash and cash cquivalcntsFor the purposes o f the cash flow statement. cash and cash cquivalcnts comprise balances with less than three months’ maturity o f the assets at acquisition dates including: cash. non-restricted balances with National Bank of Moldova, treasury bills. NBM certificates, amounts due from other banks and amounts duc from quick payment

systems.

I. Intangihlc assetsAcquired computer software licenscs are capitalized on the basis o f the costs incurred to acquire and bring to usc the specific software. These costs are amortized on the basis o f the expccted useful lives (three to five years)

using the straight-line method.

Costs associatcd with developing or maintainmg computer software programs are recognized as an expense as

incurred.

12

BC ENERGBANK SANOTES TO THE INDIM Dl Al. FINANCIAL STATEMENTSFor tiu* Year Fndcd 31 December 2017

2. Accounting policics (continucd)

2.4 Significant accounting policies (continued)

ni. Property and ecpiipmentBuildings arc stated at revalued amounts. being tts fair value at the date o f re valuation. Icss accumulated deprcciation and Icss pro vis ion for impairment. where required. Other property and equipmcnt is stated at histoncal cost Icss depreciation. Histoncal cost includcs expenditure that is directiv attributable to the acquisition o f the items.

Land is not depreciated Depreciation on other assets is calculatcd using the straight-linc method to allocatc their cost to thcir rcsidual values over their estimated useful lives, as follows:

Asset t y p e _________________ ___________________________Ani

Buildings 25-75Fumiture and cquipmcnt 2-20Motor vehicles 7-10Other 5-20

Assets under construction arc not dcprcciatcd until thcrc arc brought in usc.

The assets* rcsidual valuc and useful lives are reviewed. and adjusted if appropriate, at each balancc shect date. Assets that arc subjcct to amortization arc reviewed for impairment whenever events or changes in circumstances indicate that the eanym g amount may not bc recoverable. An asset's carrying amount is written down immcdiatcly to its rccoverable amount if the asset’s carrying amount is greater than its estimated recoverable amount. The recoverable amount is the higher of the asset's fair value less costs to sell and valuc in

Gains and losses on disposal o f property, plant and equipmcnt are determined by rcfcrcncc to thcir carrying amount. These are included in their operatmg expenses in the meome statements.

n. Invcstnient propertyProperty held for long-tcrm rentai yields or for capital appreciation or both. which is not occupied by the Bank is classified as mvestment propeny.Invcstnient property compriscs frcehold land. Investment property is cam ed at fair value. Fair value is based on active market prices. adjusted. if necessarv. for any diffcrcnce in the nature. location or condition o f the spccific asset. If this Information is not available. the Bank uses alternative valuation method such as salcs comparison method by comparing similar or substitute propertics sold in the market with subject property. These valuations are reviewed annually by Directors.If an investment property bccomes owner-occupicd. it is reclassified as property, plant and cquipmcnt and its fair value at the date o f reclassification bccomes its cost for accounting purposcs o f subsequent rccording. Propeny that is being constructed or developed for ftiture usc as investment propeny is classified as property. plant and equipment and stated at cost until construction or development is complete, at which time it is reclassified and subscquently accountcd for as investment propeny .

If an item of property. plant and equipmcnt bccomes an investment property because its usc has changed, any differencc resulting between the carrying amount and the fair valuc o f this item at the date o f transfer is rccognised in equity as a revaluation o f propeny . plant and cquipmcnt under IAS 16. Howcvcr. if a fair valuc gain reverses a previous impairment loss. the gain is rccognised in the incomc statement. Upon the disposal o f such investment property. any surplus prcviously recorded in equity is transferred to retained camings: the transfer is not made through the income statement.

13

BCENERGBANKSANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor Ihe Year Ended 31 December 2017

2. Accounting policics (continucd)

2.4 Signifîcant accounting policics (continiied)

0. LeascsThe determination o f whether an arrangement is a lease or it contains a lease, is based on the substance o f the arrangement and requires an assessment o f whether the fulfilment o f the arrangement is dependent on the usc o f a specific asset or assets and the arrangement conveys a right to use the asset.

Bank as a tessee

1.ease which does not transfer to the Bank substantially all the risks and benefits incidental to ownership o f the leased item arc operating leascs. Operating lease payments arc rccognised as an expense in the income statement on a straight line basis over the lease term.

Bank as a lessorI.eases where the Bank does not transfer substantially all the risk and benefits o f ownership o f the asset are classified as operating leases. Iniţial direct costs incurred in negotiating operating leascs arc added to the carrying amount o f the leased asset and recogntsed over the lease term on the same basis as rentai income.

p. Defined contrihution planThe Bank. in the normal course o f business makes payments to the Moldovan State funds on behalf o f its employees for pension, hcalth carc and unemploymcnt benefit. All cmployecs o f the Bank arc members o f the State pension plan.

The Bank does not operate any other pension scheme and. consequently. has no further obli gat ion in respect of pensions. The Bank does not operate any othcr defined benefit plan or post-rctirement benefit plan. The Bank has no obligation to provide further services to current or former employees.

q. ProvisionsProvisions and legal claims are recognized when the Bank has a present legal or constructive obligation to transfer economic benefits as a result o f past events. It is probable that an outllow o f rcsourccs will be required to settle the obligation and the amount has bccn reliably estimated.

Where there are a number of similar obligations. the likelihood that an outflow will be required in settlcmcnt îs detennined by considcring the class o f obligations as a wholc. A provision is rccogni/cd even if the likelihood of an outflow with respect to any one item included in the same class of obligations may be small.

Provisions are measured at the present value o f the expenditures expected to be required to settle the obligation using a pre-lax rate that reflects current market assessmcnts o f the time value o f money and the risks specific to the obligation. The increase in the provision due to passage o f time is recognized as interest expense.

r. Financial guarantee contractsFinancial guarantee contracts are contracts that rcquire the issuer to make spccificd payments to rcimburse the holder for a loss it incurs because a spccificd debtor fails to make payments when due. in accordance with the terms o f a debt instrument. Such financial guarantees are given to banks. financial institutions and othcr bodies on behalf o f customcrs to secure loans, overdrafts and other banking facilities.

14

BC ENERGBANK SANOTES TO TIIE INDIVIDUAL FINANCIAL STATEMENTSFor du* Year Fndcd 31 December 2017

2. Accounting policies (con(inucd)

2.4 Significant accounting policies (continued)

r. Financial guarantee contracts (continued)

Financial guarantccs are mitially recogni/ed in the financial statements at fair valuc on the date the guarantee was given. Subsequent to iniţial recognition. the bank’s liabilitics under such guarantccs arc measured at the higher o f the iniţial measurcment. less amortization calculated to recogmse in the incomc statement the fee income eanied on a straight line basis over the life o f the guarantee and the besi estimate of the expenditure requircd to settle any financial obligation arising at the balancc shcet date. These estimates are determined based on experienţe o f similar transactions and history o f past losses. supplemcnted by the judgment of Management. Any incrcase in the liability relating to guarantccs îs taken to the income statement under other operating expenses.

s. TaxationIncome tax payable on profits. based on the applicable Moldovan tax law is rccognized as an expense in the period in wbich profits arise. The tax effects o f incomc tax losses available for carry forward are rccognized as an asset when it is probable that future taxable profits will be available agamst which these losses can be utilised.

Deferred income tax is provided m tuli. using the liability method. on temporary differences arising between the tax bases o f assets and liabilitics and their carrying amounts in the financial statements. Deferred income tax is determined using tax rates (and laws) that have been enacted or subsiantially enactcd by the balance sheet date and are expected to apply when the related deferred incomc tax asset is realized or the deferred incomc tax liability is settled.

The principal temporary difterences arise from depreciation o f equipm cnt provisions for loans and advances to customers. other assets and other liabilitics. The rates enacted or substantivelv enacted at the balance sheet date arc used to determine deferred income tax. However, the deferred income tax is not accounted for if it arises from iniţial recognition o f an asset or liability in a transaction other than a business combination that at the time o f the transaction afîects ncither accounting nor taxable profit nor loss.

Deferred tax assets are rccognized where it îs probable that future taxable profit will bc available agamst which the temporary differences can be utilised

t. BorrowingsBorrowings are rccognised mitially at fair value. being their issuc procceds (fair value o f consideration received) net o f transaction costs meurred. Subsequentlv borrowings are stated at amortised cost and any diffcrence between net procceds and the redemption value is recognized in the income statement over the period o f the borrowings using the effective interest method.

u. DividendsDividends are not accounted for until they have been approved at the Annual General Mccting.

15

BC ENERGBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor the Year Ended 31 December 2017

2. Accounting policics (continiied)

2.4 Signifîcant accounting policics (continucd)

v. Assets for resaleAssets for resale includc forccloscd col lateral on non-performing loans. They are classified as assets held for sale as thcir carrying amount is to be recovered principally through a sale transaction and a sale is considered highly probable. T*hey are siated at the lower o f carrying amount and fair value less costs to sell if their carrying amount is to be recovered principally through a sale transaction radier than through continuing use. rhe Bank considers impairment both at the time o f classification as assets for resale as well as in subsequent

periods. At the time o f rccognition as assets for resale. any impairment loss is rccognised in profit or loss unlcss the asset had bccn measured at revalue d amount in accordance with IAS 16 or IAS 38, in which case the impairment is treated as a revaluation decrease.In the subsequent periods. any impairment loss is calculatcd based on the differencc bctwecn the adjusted carrying amounts of the asset and fair value less costs to sell. Any impairment loss that arises is recognised in profit or loss. even for assets that previously carried at rcvalucd amounts.

2.5 New and revised standards that are effective for anuual periods bcginning on or after 1 Januar> 2017

A number o f new and revised standards are effective for annual periods beginning on or after 1 January 2017. These amendmcnts had no material effect on the financial statements for any period presented and therefore were not presented.

Dic Bank has implemented the following standards. amendmcnts to existing standards and interpretatlons i^sued by the International Accounting Standards Board (IASB) that are applicable for the current period:

IAS 12 Reeognition of Deferred l ax Assets for l nreali/cd I.osses (Amendiuents).

Tlie objective o f these amendmcnts is to clarify the requirements for deferred tax accounting when an asset is measured at fair value and the fair value is less than the amount o f the tax base o f the asset. Changes were not applicable to the Bank and. respectively. they had no effect on the financial position.

IAS 7: Disclosure Iniţiative ( Amendmcnts).

The objective o f these changes is to provide information that enables users o f financial statements to evaluate changes in terms o f Iiabilities resultmg from financing activ itics. including the changes both from cash flows and the non-cash items. Specific changes need the provision of a table o f reconciliat ion between the iniţial and final balances o f debts resultmg from financing activitics. including changes in cash flows from financing activity, changes arising from obtaining or losing control o f subsidiaries or other segments. the effect o f changes in exchange rates. changes m fair value and other types o f changes. These changes did not have a signifîcant impact on the Bank's financial statements.

2.6 Standards, amendmcnts and interpretations to existing standards that are not vet effective and have

not been adopted early b \ the Bank

At the date o f authorisation o f these financial statements. certam new standards. and amendmcnts to existing standards have bccn published by the IASB that are not vet effective. and have not been adopted earlv by the B. Information on those expected to be relevant to the Bank's financial statements is provided bclow.

Management anticipatcs that all relevant pronounccments will be adopted in the Bank’s accounting policies for the first period bcginning after the effective date o f the pronouncement.

16

BC ENERGBANK SANOTES TO THE INDIVIDUAL FIN ANCIAL STATEMENTSFor ihc Year Fndcd 31 December 2017

2. Accounting policies (continucd)

2.6 Standards. aniendments aiul interpretations to existing standards that are not yel effective and have not been adopted earlv by the Bank (continued)

New standards. interpretations and amendments not either adopted or listed below arc not expected to have a material impact on the Bank's individual financial statements.

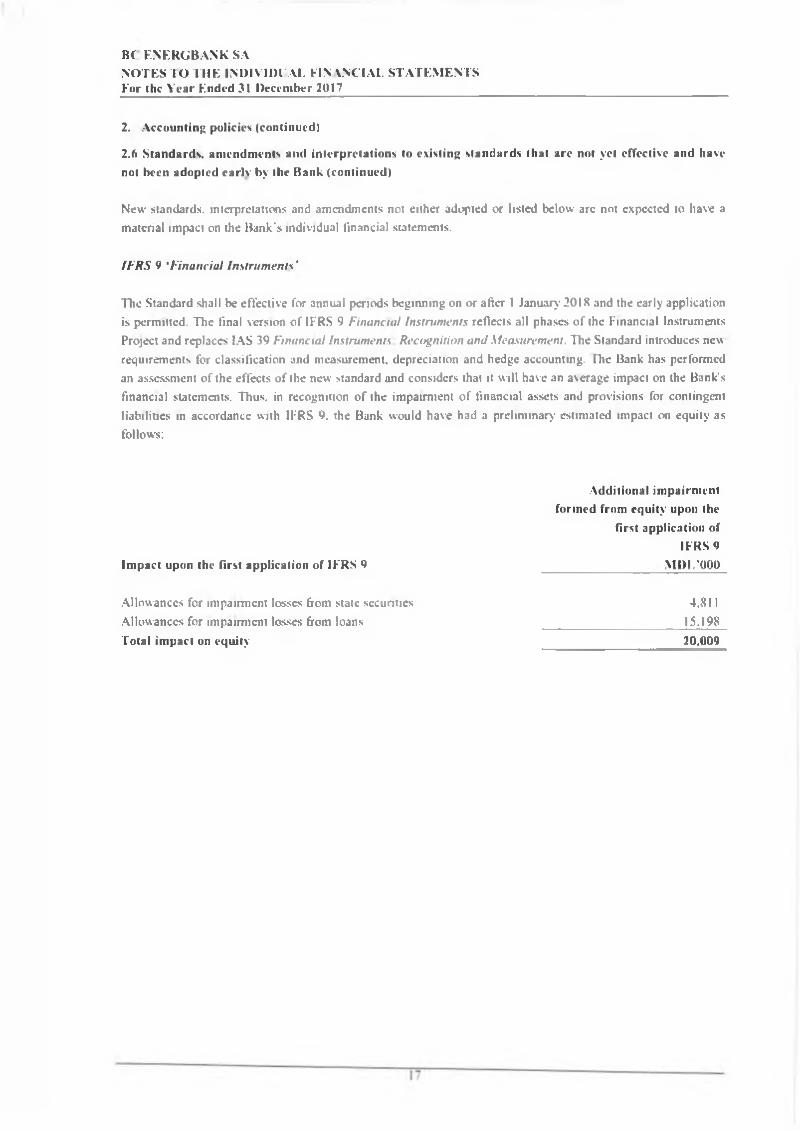

IFRS 9 ‘Financial Instruments'

The Standard shall be effective for annual periods beginning on or after 1 January 2018 and the early application is permitted. The final version o f IFRS 9 Financial Instruments reflects all phases o f the Financial Instruments Project and replaces IAS 39 Financial Instruments Recognition and Measurement. The Standard introduces neu requirements for classification and measurement. depreciation and hedge accounting. rhe Bank has performed an assessment o f the effects of the new standard and considers that it will have an average impact on the Bank’s financial statements. Thus. in recognition o f the impairment o f financial assets and provisions for contingent liabilitics in accordance with IFRS 9. the Bank would have had a prehminary estimated impact on equity as follows:

Additional impairment forined from equity upon the

First application of IFRS 9

Impact upon the first application of IFRS 9 __________ MDL'000

Allowances for impairment losses from state securities Allowances for impairment losses from loans Total impact on equity

4.81115.19820.009

BC ENERGBANK SANOTES TO THE INDIVIDl'AL FINANCIAL STATEMENTSFor Ihe Year Furieri 31 December 2017

2. Accounting policics (continucd)

2.6 Standards. amendments and intcrprclations to existing standards that arc not vet effective and have not been adopted early by the Bank (continucd)

IFRS 15 Revenuefrom Contracts with Customers

The Standard becomes cffcctive for annual periods bcginning on or after I January 2018. II RS 15 establishes a five-step model that will apply to revenues arising from a contract with a client (with limited exceptions), regardless the type o f transaction or industry. The requirements o f the Standard will also apply to the rccognition and measurement o f gains and losses on the sale o f certam non-financial assets that arc not the result o f the entity’s ordinary activitics (cg sale o f tangiblc and mtangiblc assets).

An extensive disclosure o f information. including disaggregation o f total revenuc. in format ion on execution obligations. changes in assets and Iiabilities between periods and keyjudgm ents and estimates. will be provided. The Bank does not consider that these amendmcnts will have a material elTcct on the Bank's financial statements.

Clarifications shall be applied for annual periods begmning on or after I January 2018 and early application is permitted. Tlie purpose o f the clarifications is to clcar the lASB's intentions when elaborating the requirements o f IFRS 15 Revenite from contracts with customers. in particular the accounting for the identilication of performancc obligations. modifymg the formulation o f the principie o f "distinctly identifiable” assets. o f the considerations regarding the trustee and principal, including the fact that an entity acts as a trustec or a principal, as well as the application o f the control and licensing pnnciplc. providing additional guidancc on the accounting o f intellectual property and royaltics. ITic clarifications also provide additional practicai solutions available to cntitics that either apply IFRS 15 completely retrospcctivcly or choose to applv the modified retrospective approach. The management has estimated that the cffcct o f these clarifications on the financial statements will be insignificant.

IF R S 16 Leascs

ITic Standard becomes effective for annual periods bcginning on or after I January 2019. II RS 16 sets out the pnnciples for recognizing. cvaluating. presenting and describing providing Information about the leascs o f the two partics to a contract, namcly the client ("lessee") and the provider ("Icssor"). The new standard requircs lessees to recognize the majority o f leases in the financial statements. I.essees will have a single accounting model for all contracts. with some exceptions. Lessor’s account remains significantly unchangcd. Ihe management has estimated that the effect o f these changes on the financial statements will bc insignificant.

IFRS 2: Clussificution unJ Measurement o f Shure-bused Payment Transactions (amendments).

The amendmcnts become effectivc for annual periods bcginning on or after 1 January 2018 and early application is permitted. The amendments provide for requirements for accounting the effccts o f the necessary conditions for vesting and the effects o f the vesting rights on the valuation o f cash-settlcd share-based payment transactions. sharc-based payment transactions with the net sctilement featurc o f the source taxation as well as for changes to the terms and conditions applicable to sharc-based payment that change the classification o f the transaction from the cash settlcment transaction to the equity settlement transaction. The management has estimated that these changes will not have an cfî'cct on the financial statements.

IA S 40: Transfers o f Investment Property (Amendment).

Fhc amendmcnts become effective for annual periods begmning on or after 1 January- 2018 and early application is permitted. Changes clarify when an entity nccds to transfer real estatc. including real

18

BC ENERGBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor ihc Year Ended 31 December 2017

2. Accounting policics (continucd)

2.6 Standards, amcndmcnts and interpretations to existing standards that are not vet effective and liavc not been adopted cari) by the Bank (continued)

estate under construction or development, into or out o f investment property. The amendmcnt foresees that a changc in usc occurs when the property nieets or no loager meets the definition o f investment property and there is cvidcnce o f change in use. A simple change of management's intennon to use a building does not provide evidence o f a change in use. The management has estimated that these changes will not have a significant impact on the financial statements.

IFRS 9: Prepayment Features with Xcgative Compcnsation (Amendment).

The amendment shall becom e effec tive for annual periods beginning on or after 1 January 2019 and the early application is permitted. rhe changc allows for financial assets with prepayment characteristics that allow or require either a partv to a contract either to pay or reccive reasonable compensation for early termination o f the contract (so that from the perspective o f the asset holder u is possible to exist "negative compensation") are measured at amortized cost or at fair value through other comprehensive income. The management has estimated that the effect o f these changes on the financial statements will bc insignificant.

IFRIC Interpretation 22: Foreign Currency Transactions and Advance Consideration.

fhe interpretation shall become effective for annual periods beginning on or after I January 2018 and early application is permitted. Interpretation clarifies how transactions are recorded that include the receipt or payment o f foreign currency advances. Interpretation covers foreign currency transactions for which the entity recogmzes a non-monctary asset or a non-monetary liability arising from the payment or receipt o f an advance amount before the entity recognizes the asset. expense or income. The Interpretation provides that. in determining the exchangc rate. the transaction date is the date o f iniţial recognition o f the non-cash asset paid in advance or the deferred income debt If there arc multiple payments or receipts made in advance. then the entity must determine a transaction date for each payment or cash advance. The management has estimated that the effect o f these changes on the financial statements will be insignificant.

IFRIC Interpretation 23: l ’ncertainty over Income Tax Treatment

Interpretation bccomes effective for annual periods beginning on or after 1 January 2019 and early application is permitted. The Interpretation addresses accounting o f incomc tax when tax treatment involves a degree o f unccrtainty that affects the application o f IAS 12. The interpretation provides guidance on how certam tax treatments are analyzed individually or collectively. tax audits. the appropriate method that refiects the unccrtainty and accounting for changes in events and circumstanccs. The management has estimated that the effect o f these changes on the financial statements will be insignificant.

The IASB has issued IFRS Annual Improvements * Cycle 2015-2017. which is a collection o f changes to IFRSs. Amendments enter into forcc for annual periods beginning on or after January 1. 2019. early application being permitted. The management has estimated that the effect o f these changes on the financial statements will be insignificant.

IA S 12 Income Taxes.

Ilic amendments clarify that the effects on the incomc tax on financial instrument payments classified as equity must be rccognized in the manner in which transactions or past events that gcncraied distributable profit were rccognized.

19

BC ENERGBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor ihe Year Ended 31 December 2017

2. Accounting policics (continucd)

2.6 Standards. amendments and interpretations to existing standards that are not vet effective and have noi bccn adopted early by the Bank (continucd)

IA S 23 Borrawing Costs.

I he amendments clarify paragraph 14 o f the Standard, which states that when a qualifving asset is available for its intended use or sale. and some o f the specific loans relatcd to the qualifving asset reniain outstanding at that time, the loan must be included in the funds that an entity leascs. in general. The Bank has dccidcd not to apply these standards. amendments and interpretations before the effective date on which they become effective.

20

BC ENERGBANK SANOTES TO THE INDIN IDI AL FINANCIAL STATEMENTSFor the Year Ended 31 December 2017

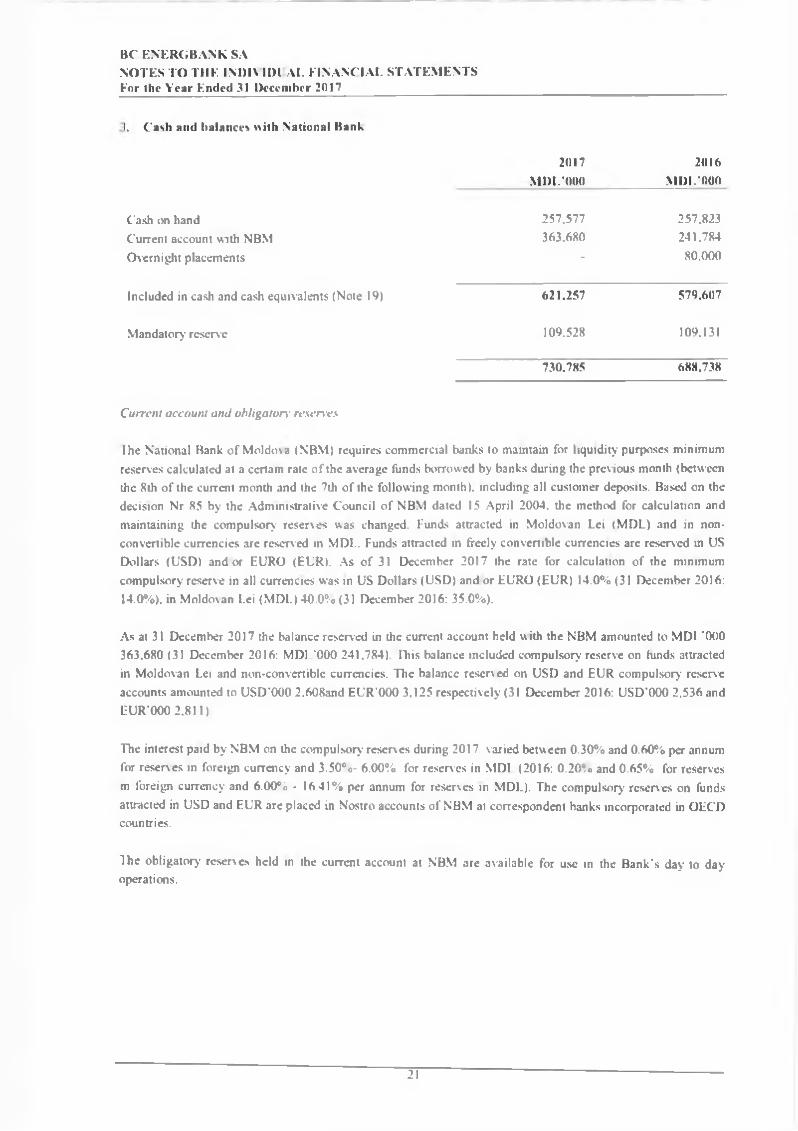

l. Cash aud balances with National Bank

2017 2016MDL'000 M DI.*000

Cash on liand 257.577 257.823

Current account with NBM 363.680 241,784

Overnight placements - 80.000

Included in cash and cash equivalents (Note 19) 621,257 579,607

Mandatory reserve 109.528 109.131

730,785 688,738

Current account and obligatory resenes

I he National Bank o f Moldov a (NBM) rcquircs commcrcial banks to maintain for liquidity purposes minimum reserves calculatcd at a certam rate o f the average funds borrovved by banks during the previous month (between the 8th o f the current month and the 7th o f the following month). including all custoiner deposits. Based on the decision Nr 85 by the Administrative Council o f NBM dated 15 April 2004. the method for calculation and maintaining the compulsory reserves was changed. Funds attractcd in Moldovan Lei (MDL) and in non* convertible currencies are reserved in MDL. Funds attracted in freely convertible currencies are reserved in US Dollars (USD) and or EURO (EUR). As o f 31 Dccember 2017 the rate for calculation of the minimum compulsory reserve in all currencies was in US Dollars (USD) and or EURO (EUR) 14.0% (31 December 2016: 14.0%), in Moldovan Lei (MDL) 40.0% (31 December 2016: 35.0%).

As at 31 December 2017 the balancc reserved in the current account hcld w ith the NBM amounted to MDL '000 363.680 (31 December 2016: MDI *000 241.784). lliis balance included compulsory reserve on funds attracted in Moldovan Lei and non-convertiblc currencies. The balancc reserved on USD and EUR compulsory- reserve accounts amounted to USD’000 2.608and EUR’000 3.125 respecţi vel y (31 December 2016: USD’000 2,536 and EUR'000 2.811)

The interest paid by NBM on the compulsory reserves during 2017 varied between 0.30% and 0.60% per annum for resenes in foreign currency and 3.50°o- 6.00% for reserves in MDI (2016: 0.20?o and 0.65% for reserves m foreign currency and 6.00% - 16.41% per annum for reserves in MDL). The compulsory reserves on funds attracted in USD and EUR arc placcd in Nostro accounts of NBM at correspondent banks mcorporated in OECD countries.

Ih e obligator)' reserves held in the current account at NBM arc available for use in the Bank’s day to day operalions.

21

BC ENERGBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor the Year Ended 31 December 2017

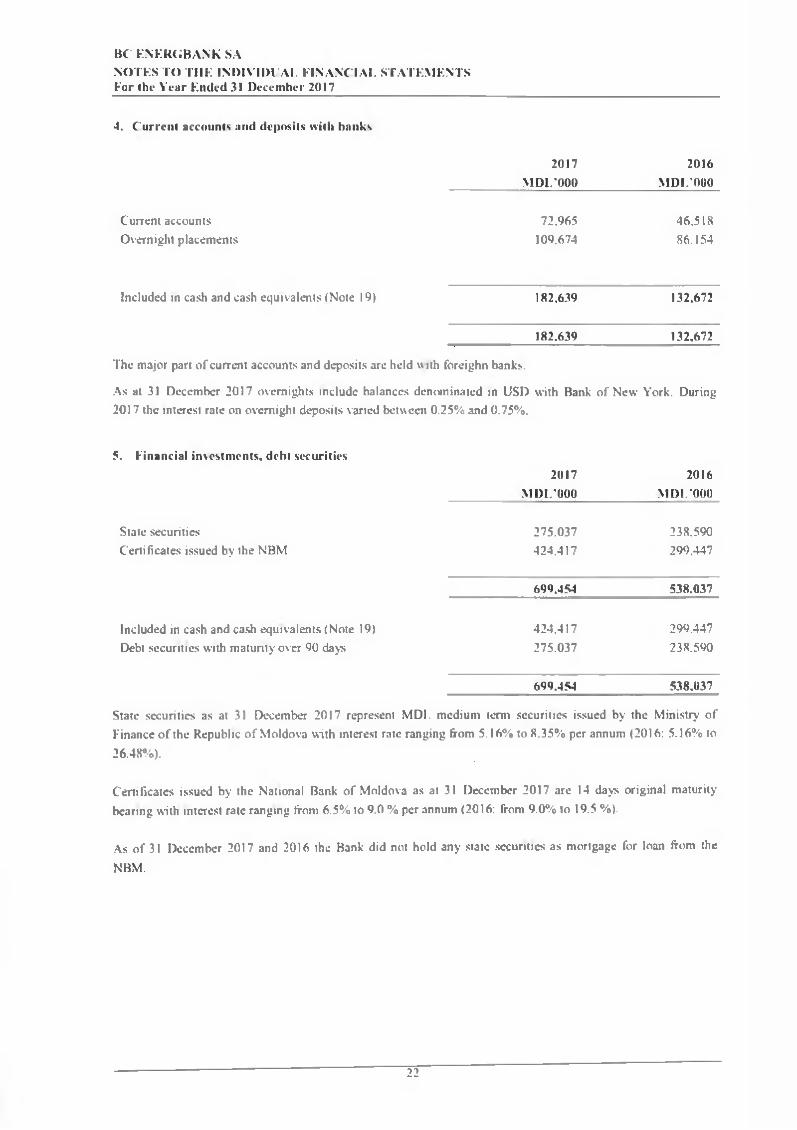

4. Cur reni accounts and deposits with banks

2017 2016M DL’000 M D l/000

C'urrent accounts Overnight placements

72.965109.674

46,51886.154

Included in cash and cash equivalents (Note 19) 182,639 132.672

182.639 132,672

The major part o f current accounts and deposits are held w ith foreighn banks.

As at 31 December 2017 overnights include balances denominated in USD 2017 the interest rate on overnight deposits var ied between 0.25% and 0.75%.

with Bank o f New York. During

5. Einancial investments, debt securities2017

M D I/0002016

MDL'000

State securitiesCertificates issued by the NBM

275.037424.417

238.590299.447

699.454 538.037

Included in cash and cash equivalents (Note 19) Debt securities with maturity over 90 days

424.417275.037

299.447238.590

699.454 538,037

State securities as at 31 December 2017 represent MDI. medium tenn securities issued by the Ministry o f Finance o f the Republic o f Moldova with interest rate ranging from 5.16% to 8.35% per annum (2016: 5.16% to

26.48%).

Certificates issued by the National Bank o f Moldova as at 31 December 2017 are 14 days original maturity bcaring with interest rate ranging from 6.5% to 9.0 % per annum (2016: from 9.0% to 19.5 %).

As o f 31 December 2017 and 2016 the Bank did not hold any state securities as mortgage for loan from the

NBM.

22

BC ENERGBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor the Year Ended 31 December 2017

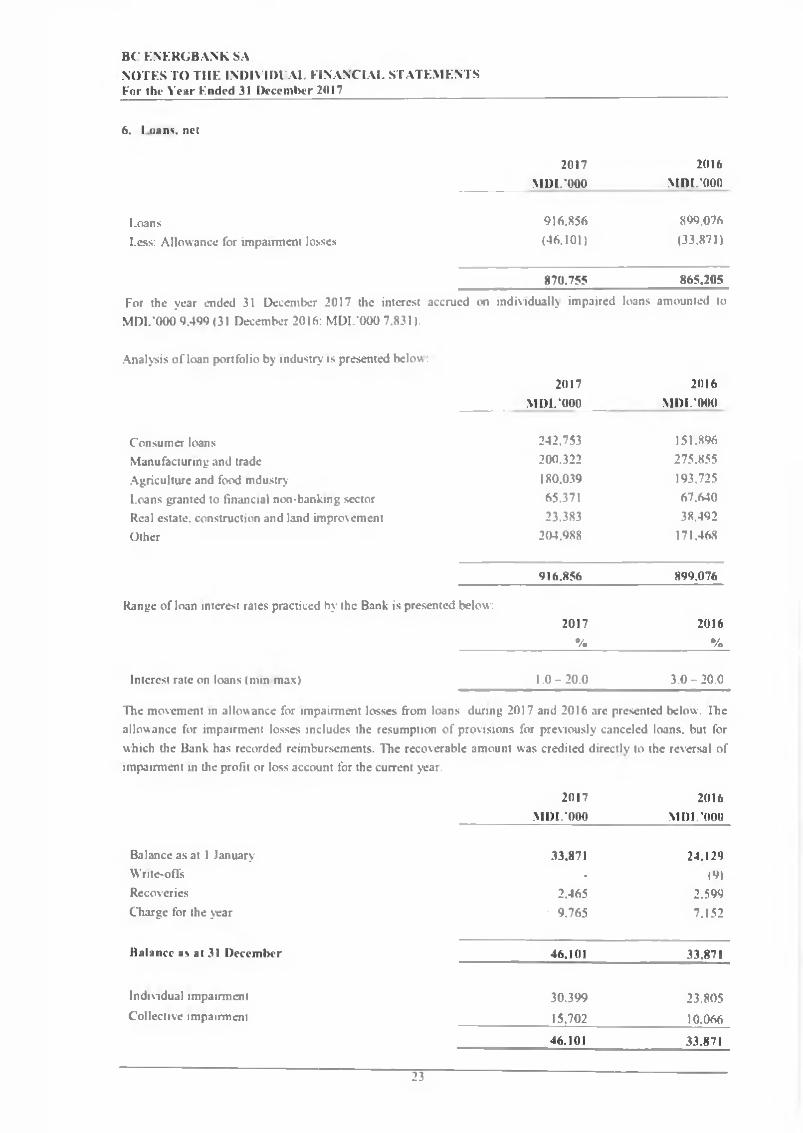

6. l oans. net

2017 2016

-------------- MDL'000 M DL’000

I.oans 916.856 899.076

Less: Allowance for impairment losses (46.101) (33.871)

870.755 865,205

For the year ended 31 December 2017 the interest accrucd on individuali) impaired loans amounted toMDL'000 9.499 <31 December 2016: MDL’000 7.831).

Analysis o f loan portfolio by mdustry is presented bel o u :

2017 2016

-------------- M DL’000 MDL’000

Consumer loans 242.753 151.896

Manufacturing and trade 200.322 275.855

Agriculture and food mdustry 180.039 193.725

Loans granted to financial non-banking sector 65.371 67.640

Real estate. construction and land improvement 23.383 38.492

Other 204.988 171.468

916.856 899.076

Range o f loan interest rates practiced by the Bank is presented below:2017 2016

•/. %

Interest rate on loans (nun max) 1 .0 -2 0 .0 3 .0 -2 0 .0

The movement in allowance for impairment losses from loans during 2017 and 2016 arc presented below. Ibcallowance for impairment losses includcs the resumption o f provisions for previously canccled loans. but forwhich the Bank has recorded reimbursements. The recoverable amount was credited directiv to the reversal ofimpairment in the profit or loss account for the current year.

2017 2016M DL’000 MDL’000

Balancc as at 1 January 33.871 24.129Wnte-offs - (9)Recoverics 2.465 2.599Charge for the year 9.765 7.152

Balancc as at 31 December 46.101 33.871

Individual impairment 30.399 23,805Collective impairment 15.702 10.066

46.101 33,871

23

HC ENERGBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor the Year Ended 31 December 2017

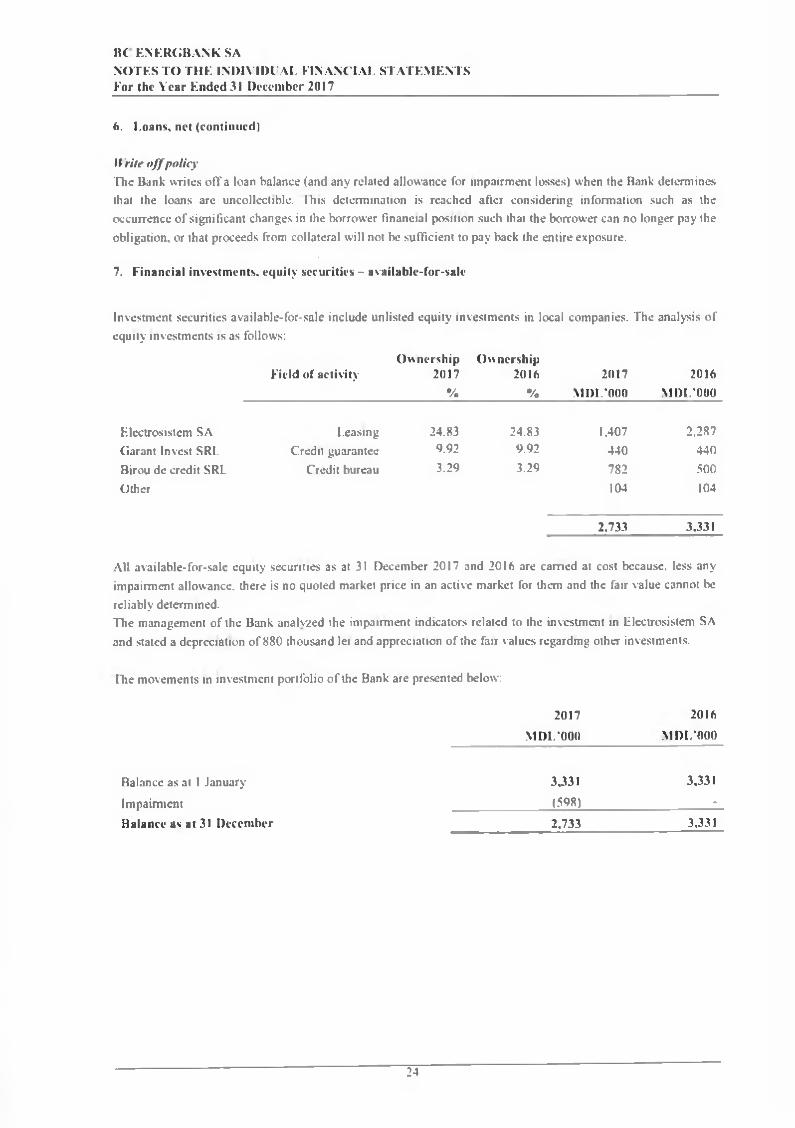

6. Loans, net (continucd)

It ’rite offpolicyThe Bank writes oflfa loan balance (and any related allowance for impairment losses) when the Bank determines that the loans arc uncollcctiblc. Ihis dctcrmination is rcachcd after considering information such as the occurrence o f significant changes in the borrower financial position such that the borrower can no longer pay the obligation, or that proceeds from collateral will not be sufficient to pay back the entire exposure.

7. Financial investments, equity securities - available-for-sale

Investment securities available-for-sale include unlisted equity investments in local companies. The analysis o f equity investments is as follows:

Field of activityOw nership

2017%

Ownership2016

%2017

MDL‘0002016

MDL'000

Electrosistem SA Leasing 24.83 24.83 1.407 2.287

Garant Invcst SRL Credit guarantee 9.92 9.92 440 440

Birou de credit SRL Credit bureau 3.29 3.29 782 500

Other 104 104

2,733 3,331

All available-for-sale equity securities as at 31 December 2017 and 2016 are camed at cost bccausc. less any impairment allowance. there is no quoted market price in an active market for them and the fair value cannot be rcliably determined.The management o f the Bank analv/ed the impairment indicators related to the investment in Llectrosistem SA and stated a depreciation o f 880 thousand lei and appreciation o f the fair va lues regardmg other investments.

rhe movements in investment portfolio o f the Bank are presented below:

2017 2016

MDL'000 MDL'000

Balancc as at I January 3,331 3,331

Impairment (598) -

Balance as at 31 December 2,733 3,331

24

BC ENERGBANK SANOTES TO THE INDIVIDl'AL FINANCIAL STATEMENTSFor Ihe Year Ended 31 December 2017

!. Iniangible assets

2017 M DL'000

2016 MDL *000

CosiBalance as at 1 January 9.340 9.547

Additions 2.473 383

Disposals (35) (590)

Balance as at 31 December 11,778 9.340

Accumulatcd deprecialionBalance as at 1 January 7J71 7.121

Charge for the year 619 840

Disposals (35) (590)

Balance as al 31 December 7,955 7.371

Net book value

At 3 1 December 3.823 1,969

The iniangible assets represent computer software and workstation licenses.

As at 31 December 2017 the cost o f fully amortized intangible assets amounted to MDL*000 5.780 (as at 31 December 2016 M DL’000 5.293).

BC ENERCiBANK SANOTES TO TIIK IN D IM D l Al.FINANCIAL STATEMENTSFor the Year Ended 31 Dcccmbcr 2017

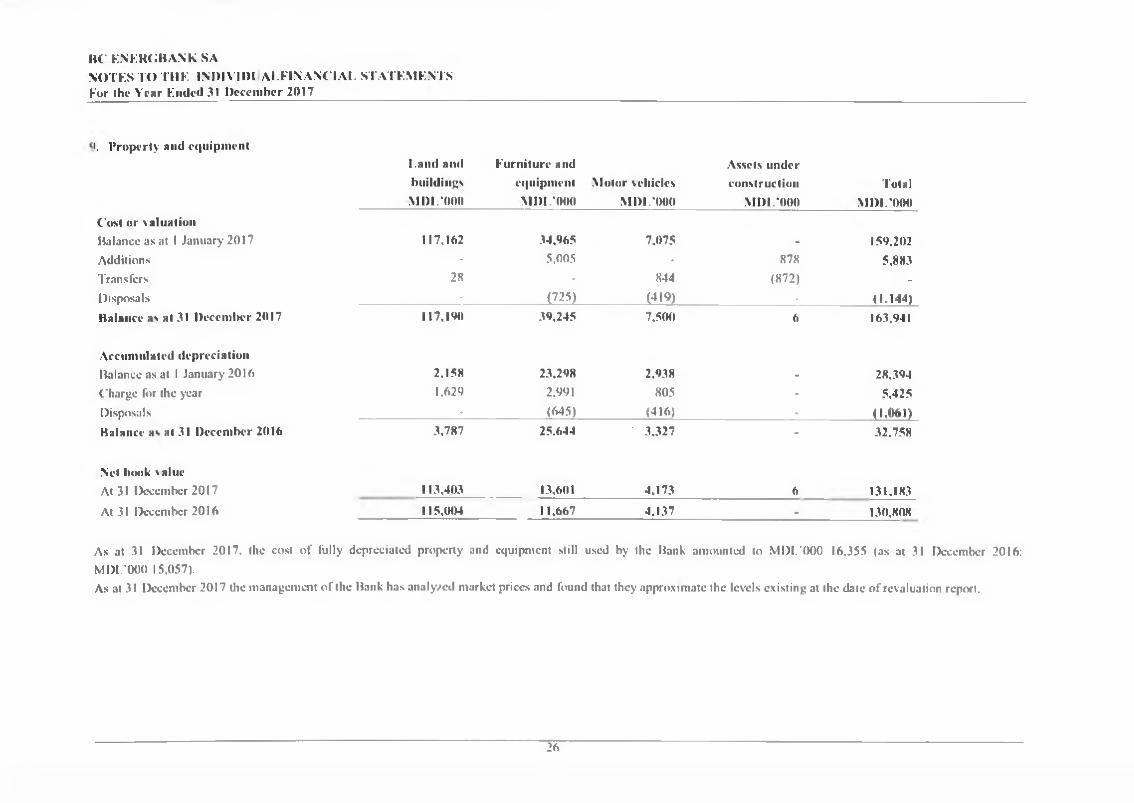

i. Property and cquipmcntLand aiul buildings

MDL'000

Furniturc and cquipment MDL'000

Motor vehides MDL'000

Assets under construction

MDL'000Total

M DL'000Cost or valuationBalancc as at 1 January 2017 117,162 34.965 7,075 - 159.202Additions - 5,005 - 878 5,883Transfcrs 28 - 844 (872) -

Disposals - (725) (419) . (1.144)Balance as al 31 December 2017 117,190 39,245 7,500 6 163.941

Accumulated depreciationBalance as at 1 January 2016 2,158 23,298 2.938 - 28.394Chargc for the year 1.629 2,991 805 - 5.425Disposals - (645) (416) . (1,061)Balancc as at 31 December 2016 3,787 25.644 3.327 - 32.758

Net book \alucAt 31 December 2017 113.403 13,601 4.173 6 131.183

At 31 December 2016 115,004 11.667 4.137 - 130,808

As at 31 Deceinbcr 2017, the cost o f fully depreciated property and equipmcnt still used by the Bank amountcd to MDI.'OOO 16,355 (as at 31 Dcccmbcr 2016: MDL'000 15.057).As at 31 Dcccmbcr 2017 the management o f the Bank has analy/ed market priccs and found that they approximatc the levels existing at the date o f rcvaluation report.

26

BCENERGBANK SA

NOTES TO THE INDIVIIHIAI. FINANCIAL STATEMENTSFor tiu* Year Ended 31 December 2017

9. Property and e(|iiipment (continucd)

Terenuri şi Clădiri MDL *000

Mobilier şi echipamente M DI.*000

AutovehiculeM DL’000

Active iu curs dc execuţie MDL *000

lo ia lM DI.'000

Cost or valuationBalancc as at 1 January 2016 104.127 32,891 5.737 399 143.154Additions 177 2.659 - 15.299 18.135Transfers 13.183 335 1.981 (15.499) -Kcclassi ficat ion - - - (122) (122)Disposals (325) (920) (643.) (77) <1.965)Balance as at 31 December 2016 117.162 34,965 7,075 - 159.202

Accumulatcd depreciationBalancc as at 1 January 2016 718 21.635 2,703 - 25.056Charge for Ihe year 1.440 2.547 680 - 4.667Disposals . (884) (445) - (1.329)

Balance as al 31 December 2016 2.158 23.298 2,938 - 28,394

Net book valueAt 31 December 2016 115.004 11.667 4,137 - 130,808

At 31 December 2015 103,409 11.256 3,034 399 118,098

BC ENERGBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor Ihe Year Ended 31 December 2017

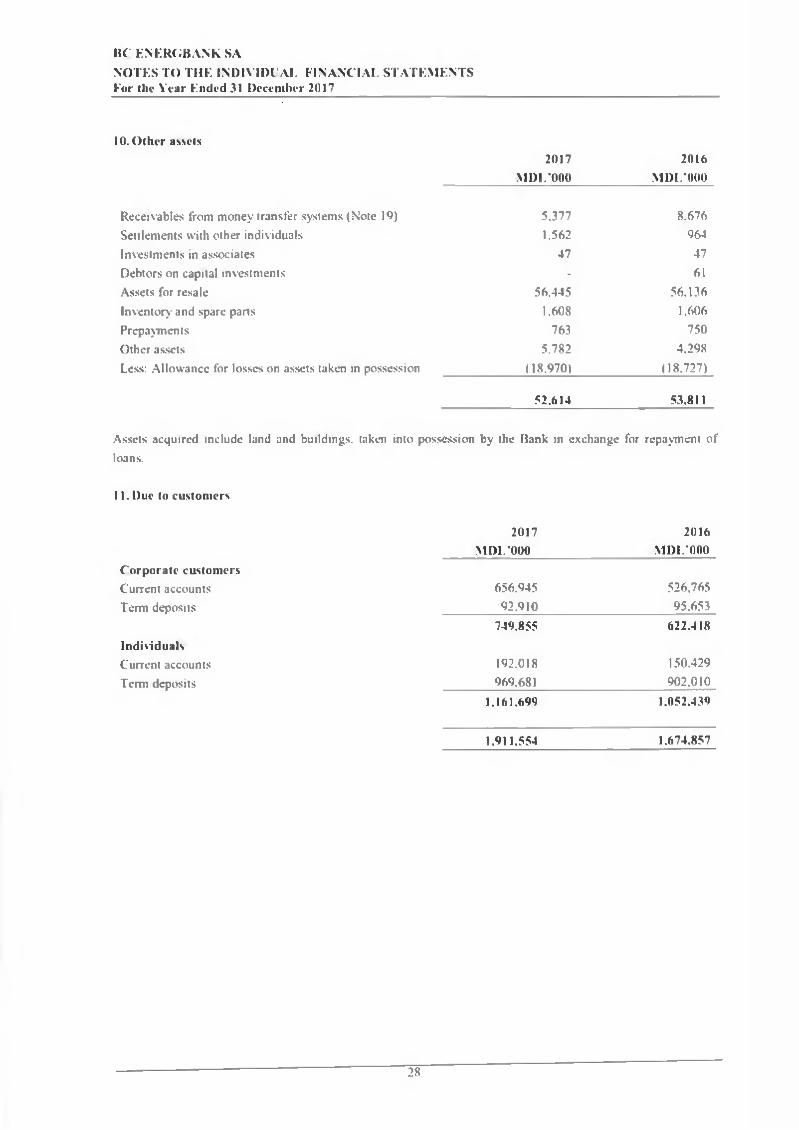

10. Olher assets2017 2016

MDL’000 M DL’000

Receivables from money transfer systems (Note 19) 5,377 8.676

Settlements with other individuals 1.562 964

Investments in associates 47 47

Debtors on capital investments - 61Assets for resale 56.445 56.136Inventory and spare paris 1.608 1.606Prcpayments 763 750

Other assets 5.782 4.298

Lcss: Allowance for losses on assets taken in possession (18.970) (18.727)

52.614 53.811

Assets acquired include land and buildings. taken into possession by the Bank in exchange for repayment of loans.

11. Due to customers

2017 2016

Corporale customersMDL’000 MDL‘000

Currcnt accounts 656.945 526,765Term deposits 92.910 95.653

Individual*749.855 622.418

Currcnt accounts 192.018 150.429

Temi deposits 969.681 902.010

1.161,699 1.052.439

1.911.554 1.674.857

28

BC ENERGBANK SANOTES TO I UE INDIN 11)1 AL FINANCIAL STATEMENTSFor the Year Ended 31 Dcccmbcr 2017

11. Duc Iu customers (cuniiuiicd)

The annual interes! rates paid by the Bank for the MDI and FCY deposits o f individuals and companies ranged as follows:

2017 2016MDL Valuta MDI. Valută

% % % % % % % %

min MaX

min max min max min max

Persoane juridice

Demand deposits 0.00 5.00 0.00 2.00 0.00 5.00 0.10 1.50

Ierni deposits up to 3 nionths 0.00 3.00 0.00 0.05 0.00 10.00 0.00 0.05

Term deposits >3 monihs< 1 year 0.00 7.00 0.00 1.50 0.00 16.00 0.00 2.10

Tenii deposits over 1 vear 0.00 8.00 0.00 1.90 0.00 8.50 0.00 3.00

Individual*

Demand deposits 0.00 6.80 0.00 0.20 0.00 0.00 0.00 0.00

Terni deposits up to 3 months 0.00 2.30 0.00 0.10 0.00 17.25 0.00 0.10

Temi deposits >3 months< 1 vear 0.00 7.00 0.00 1.80 0.00 18.00 0.00 2.00

Temi deposits over I year

12. Other borrowings

0.00 8.30 0.00 3.00 0.00 18.50

2017

0.00 2.70

201iInterest rate,

% MDL‘000 MDL’000

BorrowingsRISP loans with lloating rate due 2.03-6.5 48.809 70.131FIDA loans with floating rate due 2.04-6.5 36.141 56.408PAC loans with lloating rate due 2.03-6.5 6.668 10.496KFW loans with floating rate due 1.93-6.5 228 4.411Filiera Vinului loans w ith lloating rate due 1.01-6.5 23.054 26.720Livada Moldovei 0.9 33.035 8.927Interest accrued 1.665 1.941

149.600 179.034

Dunng 2017 and 2016 the Bank didn’t ha\e any defaults o f principal, interest or other breaches o f contractual terms.

29

BC ENERGBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor the Vear Ended 31 December 2017

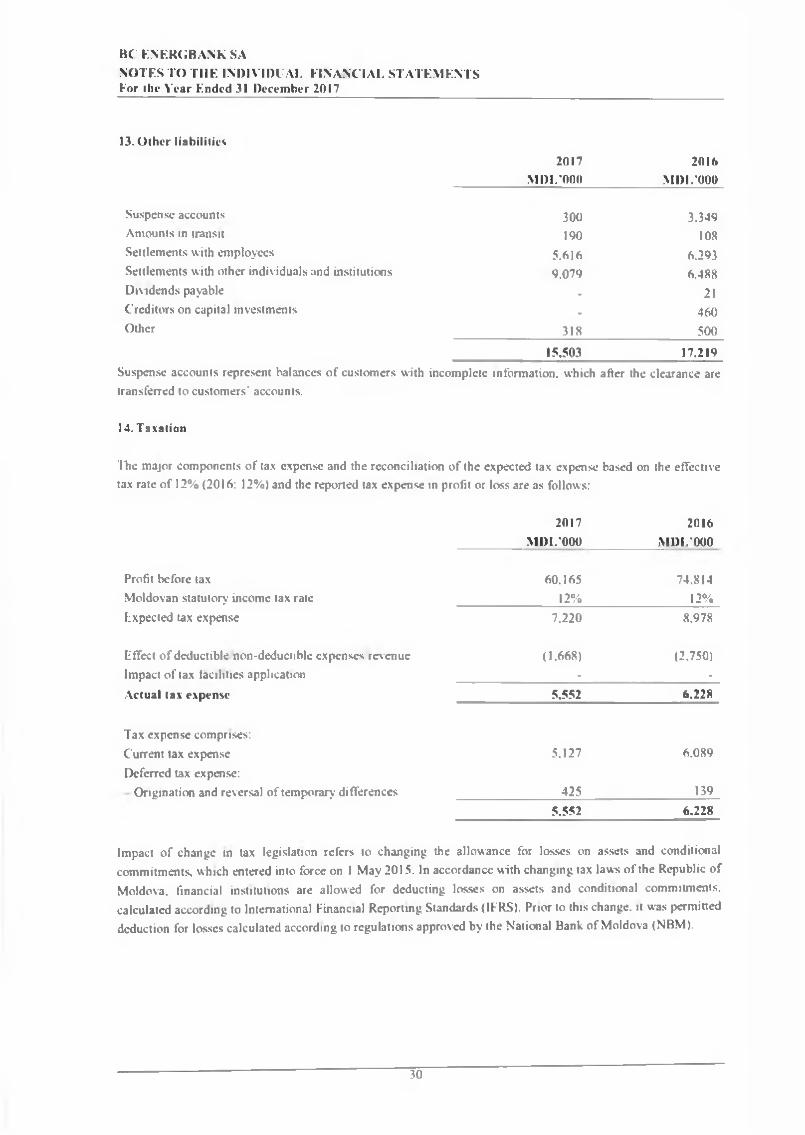

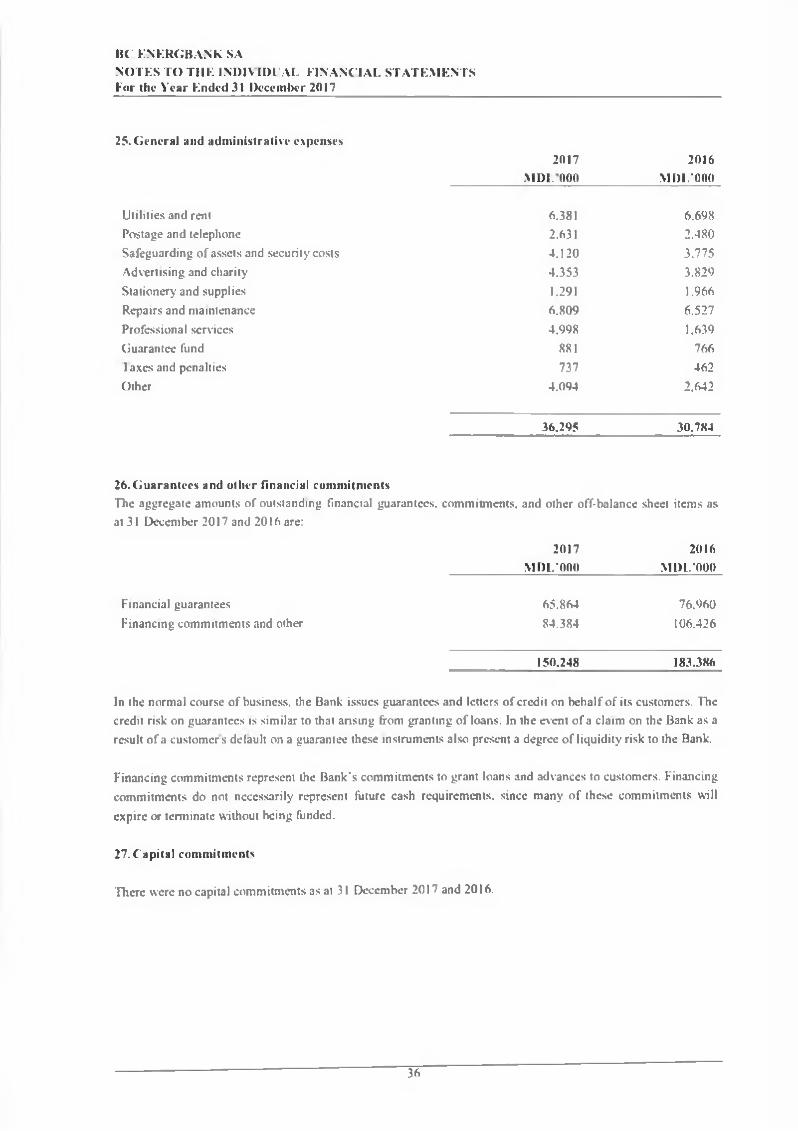

13. Other Iiabilities

2017 2016MDL'*000 M DL’000

Suspcnsc accounts 300 3.349Amounts in transit 190 108Settlements with employees 5.616 6.293Settlements with other individuals and institutions 9.079 6.488Dividends payable . 21Crcditors on capital investments . 460Othcr 318 500

15,503 17.219

Suspcnsc accounts represent balances o f customcrs with incomplctc Information, which after the clcarance are transferred to customers' accounts.

14. Taxation

The major components o f tax expense and the reconciliation o f the expected tax expense based on the effectivetax rate o f 12% (2016: 12%) and the reported tax expense in profit or loss are as follows:

2017 2016M DL'000 MDL'000

Profit before tax 60.165 74.814Moldovan statutory income tax rate 12% 12%Expected tax expense 7.220 8.978

Effect o f deductible non-dcductible expenses revenue (1.668) (2.750)Impact o f tax lacilities application - -Actual tax expense 5.552 6,228

Tax expense comprises:Current tax expense Deferred tax expense:

5.127 6.089

Origination and reversal o f temporary differences 425 139

5,552 6.228

Impact o f change in tax legislation refers to changing the allowance for losscs on assets and condiţional commitments, which entered into forcc on I May 2015. In accordance with changing tax laws o f the Republic o f Moldova, financial institutions are allowed for dcducting losses on assets and condiţional commitnicnts. calculatcd according to International Financial Reporting Standards (IFRS). Prior to this change. it was permitted deduction for losscs calculatcd according to rcgulations approvcd by the National Bank o f Moldova (NBM).

30

BC ENERGBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor Ihe Year Ended 31 December 2017

14. Taxation (continued)

Deferred taxes arising from temporary diffcrcnccs are summarized as follows:

Recogni/ed inDeferred tax assets (liabilides) 1 January 2(117 profit and loss 31 December 2017

M DL'000 MDL'000 MDL'000

AssetsProperty and equipment (3.678) (344) (4.022)

IiabilitiesOther Iiabilities 755 (81) 674

(2.923) (425) (3.348)

Rccognised as:Deferred tax assel Deferred tax liahility

Deferred tax assets (Iiabilities)

(2.923)

1 January 2016 MDL'000

(425)

Reeogni/ed in profit and loss

MDL'000

(3.348)

31 December 2016 MDL'000

AssetsProperty and equipment (3.347) (331) (3.678)

IiabilitiesOthcr Iiabilities 563 192 755

(2.784) (139) (2.923)

Rccognised as:Deferred tax asset - - -

Deferred tax liahility (2.784) <«*> (2.923)

Deferred tax was calculatcd by applying the 2017 standard tax rate o f 12% (2016 standard tax rate o f 12%).

31

BC ENERGBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor the Year Ended 31 December 2017

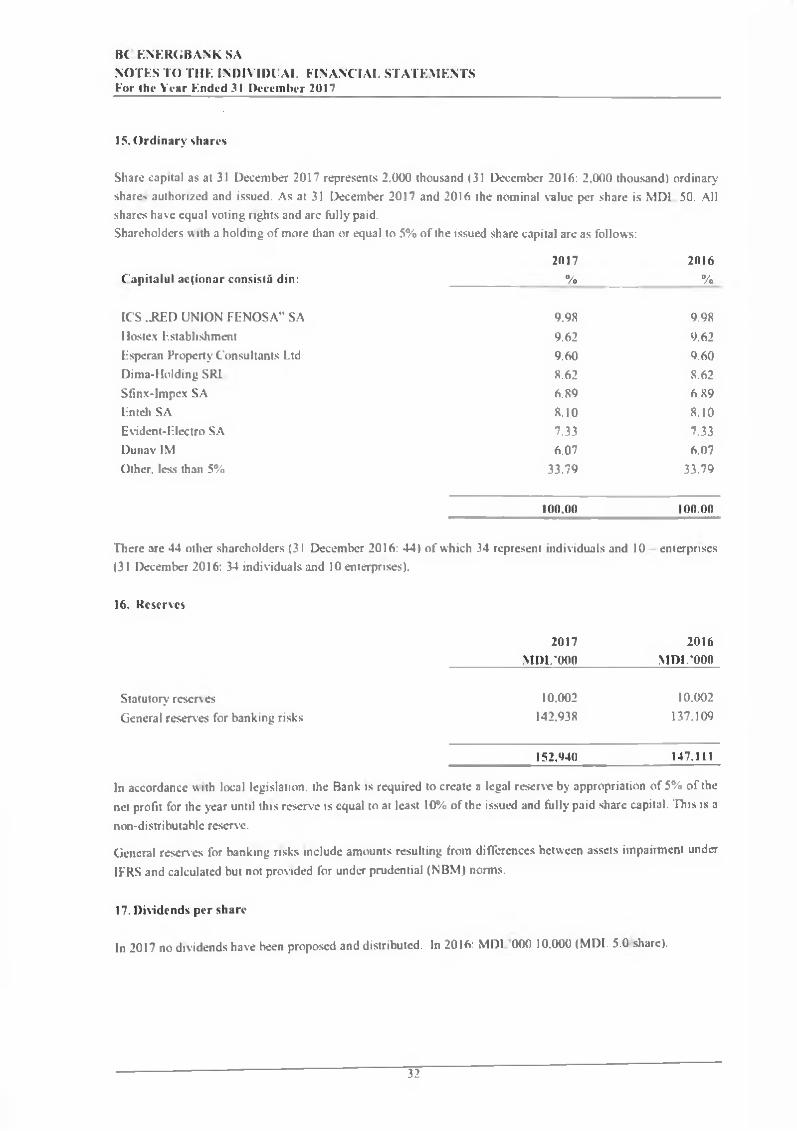

15. Ordinary shares

Share capital as at 31 December 2017 represenis 2.000 thousand (31 Dcccmbcr 2016: 2,000 thousand) ordinary shares authorized and issued. As at 31 December 2017 and 2016 the nominal valuc per share is MDI 50. All shares have equal voting rights and arc fiiUy paid.Shareholders w ith a holding o f more than or equal to 5% o f the issued share capital arc as follows:

2017 2016Capitalul aefionar consistă din: % %

ICS ..RED UNION FENOSA" SA 9.98 9.98I lostex Establishment 9.62 9.62Esperan Property Consultants I.td 9.60 9.60Dima-Holding SRL 8.62 8.62Sfinx-Impcx SA 6.89 6.89Lntch SA 8.10 8.10Evident-Hlcctro SA 7.33 7.33Dunav IM 6.07 6.07Other. Icss than 5% 33.79 33.79

100.00 100.00

There are 44 other shareholders (31 Deccmbcr 2016: 44) o f which 34 represent individuals and 10 enterpriscs (31 December 2016: 34 individuals and 10 enterprises).

16. Reserves

2017 2016M DL'000 MDL’000

Statutory reserv es 10.002 10.002

General reserves for banking risks 142.938 137.109

152.940 147.111

In accordance with local legislation. the Bank is rcquired to create a legal reserve by appropriation of 5% o f the net profit for the year until this reserve is equal to at least 10% o f the issued and fully paid share capital. This îs a

non-distributablc reserve.

General reserves for banking nsks include amounts resulting from differences between assets impairment under

IFRS and calculated but not provided for under prudcntial (NBM) norms.

17. Dividends per share

In 2017 no dividends have been proposed and disiributed. In 2016: MDI 000 10.000 (MDI. 5.0 share).

32

BC ENERGBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor the Year Ended 31 December 2017

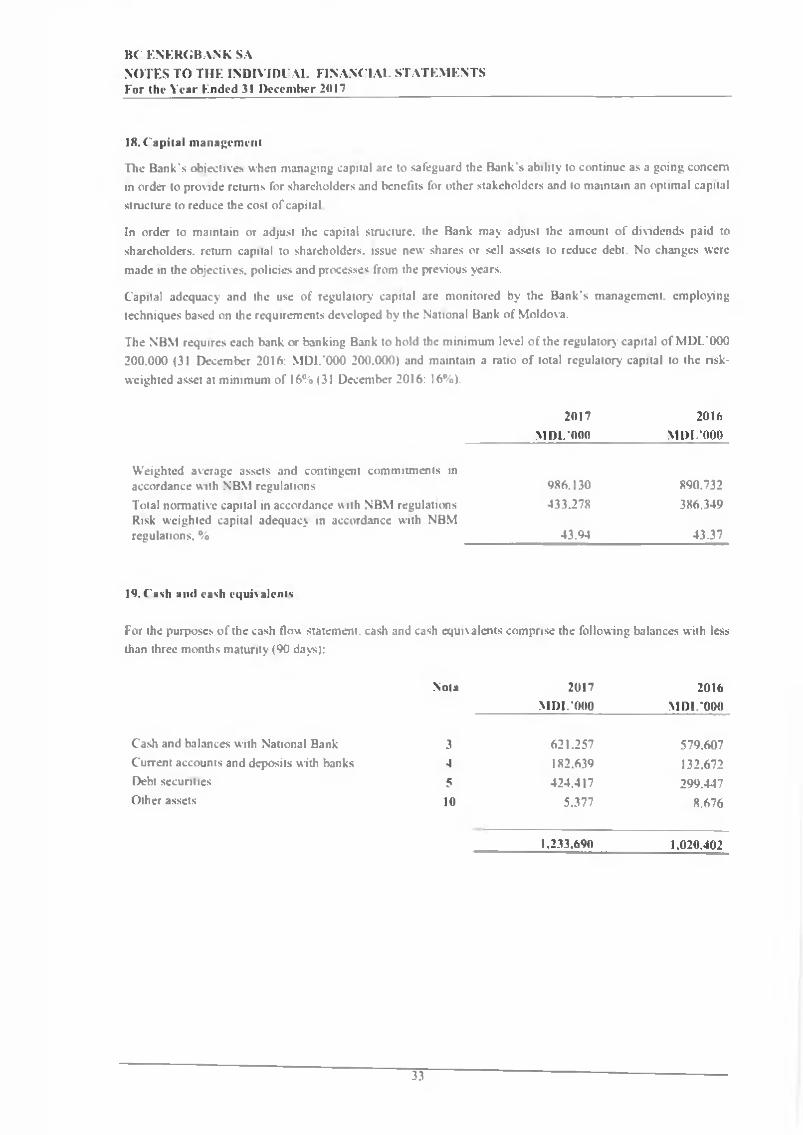

18. Capital management

The Bank’s obiective* when managing capital arc to safeguard the Bank's ability to continuc as a going concern in order to provide rctums for shareholdcrs and benefits for other stakcholdcrs and to maintain an optimal capital structure to reduce the cost o f capital

In order to maintain or adjust the capital structure. the Bank may adjust the amount o f dividends paid to shareholdcrs. retum capital to shareholders. issue new shares or sell assets to reduce debt. No changes were made in the objectives. policics and processes from the previous years.

Capital adcquacy and the use o f regulatory capital are monitored by the Bank's management, cmploying techniques based on the requirements dcvcloped by the National Bank of Moldova.

The NBM requires each bank or banking Bank to hold the minimum Icvel o f the regulator)' capital o f MDL’000 200.000 (31 December 2016: MDL'000 200.000) and maintain a ratio o f total regulatory capital to the nsk- weighted asset at minimum o f 16% (31 December 2016: 16%).

2017 2016M DL’000 MDL'000

Weighted average assets and contingent commitments in accordance with NBM rcgulations 986.130 890.732Total normative capital in accordance with NBM rcgulations Risk weighted capital adequacy in accordance with NBM regulations. %

433.278

43.94

386,349

43.37

19. Cash aiul cash equhalcnts

For the purposcs o f the cash tlow statement. cash and cash cquivalcnts comprise the following balances with lessthan three months maturity (90 days):

Nota 2017MDL'000

2016MDL'000

Cash and balances with National Bank 3 621.257 579.607Current accounts and deposits with banks 4 182.639 132.672Debt securit ies 5 424.417 299.447Other assets 10 5.377 8.676

1.233.690 1.020.402

33

BC ENERGBANK SANOTES TO THE INDIVIDUAL FINANCIAL STATEMENTSFor the Year Ended 31 December 2017

20. Intcrest and similar incomc and expense

2017 2016M DL'000 MDL'000

Intcrest and similar incomeLoans and advances to customers 95.588 100.365Available-for-sale held to matunty investments 43.711 59.229Loans and advances to banks 20.251 25.269

159,550 184.863Interest expense and similar charges Deposits from individuals (47.167) (65.696)Deposits from corporatc clicnts (7.173) (5.232)Deposits and loans from banks (260) (35)Other borrowings (6.878) (7.279)

(61,478) (78,242)

Net interest incomc 98,072 106.621

21. Net fee and commission income

2017 2016M DL’000 MDL'000

Fee and commission incomeProcessing o f payments by clicnts 49.028 44.256

Commission on guarantees and letters o f credit 1.298 1.352Transactions with debit cards 2.150 1.757

Other 3.316 3.056

55,792 50,421

Fee and commission expense Commissions on debit card serviccs (6.229) (5,006)

Payment transactions (4.308) (3.887)

Other (230) (497)

(10,767) (9.390)

Net fee and commission incomc 45.025 41.031