Bayesian estimation of a DSGE model for the Portuguese...

165

Universidade T ´ ecnica de Lisboa Instituto Superior de Economia e Gest ˜ ao Mestrado em Econometria Aplicada e Previs˜ao Bayesian estimation of a DSGE model for the Portuguese economy Vanda Almeida Departamento de Estudos Econ´omicos, Banco de Portugal [email protected] Orientador: Maximiano Pinheiro Jur´ ı: Artur Silva Lopes (Presidente), Maximiano Pinheiro (Vogal), Lu´ ıs Catela Nunes (Vogal) Junho 2009 1

-

Upload

nguyenkiet -

Category

Documents

-

view

256 -

download

8

Transcript of Bayesian estimation of a DSGE model for the Portuguese...

Universidade Tecnica de Lisboa

Instituto Superior de Economia e Gestao

Mestrado em Econometria Aplicada e Previsao

Bayesian estimation of a DSGE model for

the Portuguese economy

Vanda Almeida

Departamento de Estudos Economicos, Banco de Portugal

Orientador: Maximiano Pinheiro

Jurı: Artur Silva Lopes (Presidente), Maximiano Pinheiro (Vogal), Luıs Catela Nunes (Vogal)

Junho 2009

1

Abstract

We present a New-Keynesian DSGE model for a small open economy integrated in a

monetary union and estimate it for the Portuguese economy, using a Bayesian approach.

We obtain estimates for some key structural parameters and perform a set of exercises that

explore the model’s empirical properties and the results’ robustness. A survey on the main

events and literature associated with DSGE models is also provided, as well as a comprehen-

sive discussion of Bayesian estimation and model comparison techniques. The model features

five types of economic agents namely households, firms, aggregators, the rest of the world

and the government, and includes a number of shocks and frictions, which have proven to

enable a closer matching of the short-run properties of the data and a more realistic short-

term adjustment to shocks. It is assumed from the outset that monetary policy is defined by

the union’s central bank and that the domestic economy’s size is negligible, relative to the

union’s one, and therefore its specific economic fluctuations have no influence on the union’s

macroeconomic aggregates and monetary policy. A risk-premium is considered, to allow for

deviations of the domestic economy’s interest rate from the union’s one. Furthermore it is

assumed that all trade and financial flows are performed with countries belonging to the

union, which implies that the nominal exchange rate is irrevocably set to unity.

Keywords: DSGE; econometric modelling; Bayesian; estimation; small-open economy.

JEL codes: C10, C11, C13, E10, E12, E17, E27, E30, E37.

1

Acknowledgements

I would like to thank my advisor Maximiano Pinheiro for his guidance and support throughout

the research and writing of this dissertation. I am also grateful to Jesper Linde, Malin Adolfson

and Rafael Wouters for providing me with valuable materials on their own research, and to

Wouter Den Haan whose clarifications on specific topics were of great use. Helpful insights

were also gained from the lectures given at the 2008 Dynare Summer School by Michel Juillard,

Stephane Adjemian, Wouter Den Haan and Sebastien Villemot and at the 7th EABCN by

Lawrence Christiano and Matthias Kehrig. Special thanks go to my fellow workers Ricardo

Felix, Gabriela Castro and Jose Maria for their important support and contribution to the

success of this research and to Banco de Portugal for providing financial support and access to

a world of data and materials. Finally, I wish to express my deep gratitude to my friends for

their patience and encouragement throughout this process and to my parents for giving me the

possibility of pursuing the best during my student career.

2

Measurement with theory appears to have its merits

DeJong, Ingram and Whiteman (2000)

3

Contents

1 Introduction 6

2 Motivation and background 8

3 On the construction, solution and Bayesian estimation of a DSGE model 16

3.1 Model construction and solution . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

3.2 Likelihood function . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

3.3 Prior distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

3.4 Posterior distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

3.5 Evaluation of the estimation results . . . . . . . . . . . . . . . . . . . . . . . . . 32

3.6 Main properties of Bayesian estimation and model comparison . . . . . . . . . . 39

4 A DSGE model for a small open economy in a monetary union 40

4.1 Households . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

4.2 Firms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

4.3 Aggregators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

4.4 Rest of the world . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

4.5 Government . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

4.6 Aggregation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

4.7 Market clearing conditions and useful identities . . . . . . . . . . . . . . . . . . . 59

4.8 Shocks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

5 Estimation of the model for the Portuguese economy 61

5.1 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

5.2 Calibration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

5.3 Priors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

5.4 Estimation results and evaluation . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

6 Conclusions and directions for further work 69

References 71

Tables 77

4

Figures 81

Appendices 88

A Derivation of the model’s equations 88

A.1 Households . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

A.2 Firms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

A.2.1 Intermediate good firms . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

A.2.2 Final good firms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

A.3 Aggregators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98

A.4 Rest of the world . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99

A.5 Government . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100

A.6 Aggregation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100

A.7 Market clearing conditions and useful identities . . . . . . . . . . . . . . . . . . . 105

A.8 Shocks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

A.9 The model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

A.10 The steady-state model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 114

A.11 The log-linearised model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123

B Dynare code 145

C Additional figures 151

5

1 Introduction

The modelling of macroeconomic fluctuations has changed dramatically over the last thirty

years. When traditional large-scale macroeconometric models used in the 1960s and 1970s came

under severe critiques, the need for a new paradigm emerged and became the main concern of

macroeconomists. In their seminal paper, Kydland and Prescott (1982) provided an answer by

proposing a new type of model, where private agents had an optimising behaviour, benefiting

from rational expectations and acting in a Dynamic Stochastic General Equilibrium (DSGE)

framework. The article was in the genesis of a new way of studying macroeconomic fluctuations,

the so-called Real Business Cycle (RBC) approach to macroeconomic modelling, which became

one of the main toolboxes of macroeconomic research over the 1980s.

Although RBC models provided a fundamental methodological contribution, they soon

proved to be insufficient, especially for policy analysis in central banks and other policy in-

stitutions, giving rise to a new debate in the field of macroeconomics. A new school of thought

emerged from the debate, in the 1990s, the so-called New-Keynesian Macroeconomics. Although

sharing the basic RBC structure, this new approach viewed the sources and mechanisms of busi-

ness cycles in a very distinct way, introducing a wide set of new assumptions into DSGE models,

which proved to be extremely successful among both the academia and applied economists.

In parallel with developments on the theoretical ground, major advances were also accom-

plished with respect to the econometric apparatus associated with DSGE models. Bayesian

techniques emerged as the most promising tools to estimate and quantitatively evaluate these

models, bearing important advantages when compared to the other available methods both from

an economic and statistical point of view, especially for medium to large-scale models.

The development of a deeper econometric framework surrounding DSGE models has made

them attractive not only because of their theoretical consistency but also because of their data

explanatory power. Many studies have documented the empirical possibilities and usefulness of

these models, even when compared with more traditional econometric tools like Vector Autore-

gressions (VAR), Vector Error Correction Models (VECM), Bayesian Vector Autoregressions

(BVAR), among others. Some reference examples are Smets and Wouters (2003), Fernandez-

Villaverde and Rubio-Ramirez (2004), Del Negro, Schorfheide, Smets and Wouters (2005), Adolf-

son, Laseen, Linde and Villani (2005), Juillard, Kamenik, Kumhof and Laxton (2006) and

Adolfson, Linde and Villani (2007).

6

The combination of a strong theoretical framework with a good empirical fit has turned

New-Keynesian DSGE models into one of the most attractive tools for modern macroeconomic

modelling and has led to their widespread use. They are considered to be a privileged vehicle

for economists to structure their thinking and understand the functioning of the economy, being

used for a number of purposes, from policy analysis to welfare measurement, identification of

shocks, scenario analysis and forecasting exercises. They are the object of attention not only

in the academia but also in a number of policy-making institutions such as the International

Monetary Fund (IMF), the Bank of Sweden, the Bank of Finland, the European Central Bank

(ECB), the Federal Reserve (FED) or the European Commission.

New-Keynesian DSGE modelling and estimation is therefore one of the most interesting

and promising fields in modern macroeconometric research, from which no country should be

left out. In the case of Portugal, some exercises have already been performed using DSGE

models, namely: Pereira and Rodrigues (2000), where an analysis of the impact of a tax reform

package is performed, using a calibrated New-Keynesian model; Fagan, Gaspar and Pereira

(2004), where the macroeconomic effects of structural changes are investigated, using a calibrated

New-Keynesian model; Silvano (2006) where business cycle movements are studied using an

RBC model estimated with Generalised Method of Moments techniques; and Almeida, Castro

and Felix (2008), where the effects of increasing competition in the nontradable goods and

labour markets are inspectioned, using a calibrated large-scale New-Keynesian model. To our

knowledge, no attempt has however been made to estimate a New-Keynesian DSGE model for

the Portuguese economy.

In this article, we hope to contribute to fill this gap by developing a New-Keynesian DSGE

model, incorporating the main assumptions that have proven to be crucial to take these models

to the data, and estimating it with Portuguese data, using Bayesian techniques. We obtain

estimates for some key structural parameters of the Portuguese economy and perform a set of

exercises that explore the model’s empirical properties and the results’ robustness. A survey

on the main events and literature associated with DSGE models is also provided, as well as a

comprehensive discussion on the estimation and model comparison techniques used in the study.

The model is greatly inspired in the works of Smets and Wouters (2003), Adolfson, Laseen,

Linde and Villani (2007) and Almeida et al. (2008). It is a New-Keynesian DSGE model for

a small open economy, integrated in a monetary union, featuring five types of economic agents

namely households, firms, aggregators, the rest of the world and the government. It includes a

7

number of shocks and frictions, which have proven to enable a closer matching of the short-run

properties of the data and a more realistic short-term adjustment to shocks. It is assumed

from the outset that monetary policy is totally defined by the union’s central bank and that

the domestic economy’s size is negligible, relative to the union’s one, and therefore its specific

economic fluctuations have no influence on the union’s macroeconomic aggregates and monetary

policy. A risk-premium is considered to allow for deviations of the domestic economy’s interest

rate from the union’s one. Furthermore, for simplification, it is assumed that all trade and

financial flows are performed with countries belonging to the union, which implies that the

nominal exchange rate is irrevocably set to unity.

The remainder of the dissertation is organised as follows: in section 2 we motivate the

study and provide some references of background literature; in section 3 we explain the main

methodological aspects related to the study; in section 4 we present our model; in section 5,

we estimate the model for the Portuguese economy, presenting some data and methodological

considerations, and the estimation results and evaluation; and finally, in section 6, we wrap up

our main conclusions and discuss some possible extensions of our work.

2 Motivation and background

In this section, we provide a description of the main events and literature related to the de-

velopment and estimation of DSGE models, that inspired our study and legitimate our options

concerning both the model features and the methods used when taking it to the data.

The failure of traditional macroeconometric models

During the 1960s and 1970s, large-scale macroeconometric models in the tradition of the ”Cowles

Commission” were the main tool available for applied macroeconomic analysis1. These models

were composed by dozens or even hundreds of equations linking variables of interest to explana-

tory factors, such as economic policy variables, and while the choice of which variables to include

in each equation was guided by economic theory, the coefficients assigned to each variable were

mostly determined on purely empirical grounds, based on historical data.1The ”Cowles Commission for Research in Economics” is an economic research institute founded by the

businessman and economist Alfred Cowles in 1932. As its motto ”science is measurement” indicates, the CowlesCommission was dedicated to the pursuit of linking economic theory to mathematics and statistics, leading to anintense study and development of econometrics. Their work in this field became famous for its concentration onthe estimation of large simultaneous equations models, founded in a priori economic theory.

8

In the late 1970s and early 1980s, these models came under sharp criticism. On the empir-

ical side, they were confronted with the appearance of stagflation, i.e. the combination of high

unemployment with high inflation, which was incompatible with the traditional Phillips curve

included in these models, according to which unemployment and inflation were negatively corre-

lated. It was necessary to accept that this was not a stable relation, something that traditional

macroeconometric models were poorly equipped to deal with. Another strong criticism on the

empirical side came from Sims (1980), who questioned the usual practice of making some vari-

ables exogenous, i.e. determined ”outside” the model. This was an ad-hoc assumption, which

excluded meaningful feedback mechanisms between the variables included in the models.

But the main critique was on the theoretical side and came from Lucas (1976) when he

developed an argument that became known as the ”Lucas critique”. Lucas pointed out that the

empirical puzzle of stagflation was just a reflection of a more general theoretical problem. He

noted that agents behaved according to a dynamic optimisation approach and formed rational

expectations. This meant that they maximised welfare over their entire lifetime, taking into

account not only the past and present economic conditions but also their prospects about the

future, using all relevant available information, and that although they could not fully predict

the future, they were able to construct expectations that were not systematically biased. There-

fore, if agents anticipated any change in the economic environment, like a change in economic

policy, they would immediately incorporate those expectations in their decision problems, pos-

sibly changing both their current and future behaviours. Being exclusively based on the past,

traditional models could not account for the role of expectations on the behaviour of economic

agents and consequently they lacked an important piece of the functioning of the economy. They

simply assumed that the relationships between economic variables that were valid in a certain

context would be able to explain developments in the economy even if the underlying con-

text changed, without taking into account that the anticipation of those changes by the agents

could alter the way they reacted, and this way invalidate the previously estimated relationships.

Therefore, to correctly predict the effects of new policies, models would have to cope with the

role of expectations in economic agents’ decisions.

Rise and fall of RBC models

As a response to these critiques, economists of the 1980s departed from the old paradigm to

a different type of macroeconomic models, whose genesis can be found in the seminal work by

9

Kydland and Prescott (1982). In this article, decisions of economic agents were modelled in a

structural micro founded way, in a DSGE framework, taking into account their expectations on

all future developments. The model economy was perfectly competitive and frictionless, with

prices and quantities immediately adjusting to their long-run, optimal, levels after a shock had

hit the economy. Fluctuations were exclusively generated by the agents’ reactions to random

technology shocks continuously hitting the economy, which intended to describe business cycles

simply as the efficient response of rational optimising agents to a real exogenous shock.

Besides theoretically appealing by its consistency and microfoundations the model proved to

be able to replicate a number of stylised business cycle facts, being largely adopted by macroe-

conomists, who introduced several sophistications to the initial model over the years. This

became known as the RBC approach to macroeconomic modelling, and has been recognised as

one of the most important advances in modern macroeconomics, by firmly establishing DSGE

models as the new paradigm of macroeconomic theory.

Despite their important methodological contribution and initial empirical success, RBC mod-

els soon came under criticism. The main issue was that, with completely flexible prices, any

change in the nominal interest rate (whether chosen directly by the central bank or induced by

changes in the money supply) was always matched by one-for-one changes in inflation, leaving

the real interest rate unchanged. This meant that any action by the monetary authority would

have no impact on real variables and therefore there was no role for monetary policy, a result

that was at odds with the widely held belief (certainly among central bankers) in the power

of that policy to influence the real side of the economy in the short run. Furthermore, since

cyclical fluctuations were the optimal response of the economy to shocks, stabilisation policies

were not necessary and could even be counterproductive, as they would divert the economy from

its optimal response. This was in sharp contrast with the Keynesian view that the troughs of

the economic cycle were mainly due to an inefficiently low utilisation of resources, which could

be brought to an end by means of economic policies aimed at expanding aggregate demand. In

addition, the primary role attributed to technology shocks in explaining economic fluctuations

was at odds with the traditional view of technology shocks as a source of long-term growth, unre-

lated to business cycles, which were to a large extent considered a demand-driven phenomenon.

Finally, the ability of RBC models to match the empirical evidence began to be questioned, as

they were not able to reproduce some important stylised facts. All these issues determined that

although RBC models had a strong influence in the academia, they had a very limited impact

10

on central banks and other policy-making institutions, which continued to rely on large-scale

macroeconometric models despite their acknowledged shortcomings.

NKM as the new road ahead

The insufficiencies of RBC models began to be overcome in the 1990s when economists, while

keeping the RBC main structure, started to introduce some new assumptions in the models giving

birth to a new school of thought, the so-called New-Keynesian Macroeconomics (NKM). This

school shared the RBC approach belief that macroeconomics needed rigorous microfoundations,

also using DSGE models as their main instrument but rationalised the business cycle in a

substantially different way. They considered that the economy was not perfectly flexible nor

perfectly competitive and that instead it was subject to a variety of imperfections and rigidities,

with these being the key elements to understand the dynamics of the real world. Based on this

view, NKM economists introduced monopolistic competition and various types of nominal and

real rigidities, as well as a broader set of random disturbances. Some notable examples are:

the introduction of sticky prices, following previous studies like Calvo (1983), which allowed

for price inertia, breaking the strong RBC assumption of money neutrality; capital adjustment

costs following King (1991), which allowed models to capture the liquidity effect ; and demand

shocks as in Rotemberg and Woodford (1995).

These new assumptions, besides generating a meaningful role for monetary and other eco-

nomic policies, proved to be extremely successful in capturing some of the salient features of

macroeconomic time series that RBC models previously missed. A new window opened up for

DSGE models. They began to be used not only by academics but also by applied researchers

and central bankers. A vast range of literature was produced dedicated to the improvement

of DSGE models, with a wide set of new assumptions being put forward and capable of be-

ing introduced in a tractable way. Some recent developments were: the extension of nominal

stickiness to wages, following Erceg, Henderson and Levin (2000), which have been shown to

play an important role in explaining inflation and output dynamics; the introduction of con-

sumption habits in the utility function, following previous work by Abel (1990), which helped in

capturing consumption persistency; price and wage indexation and the inclusion of investment

adjustment costs, as in Christiano, Eichenbaum and Evans (2005), which have improved the

ability of the models to capture the inflation persistence present in the data and enhanced the

ability of models to capture investment dynamics.

11

Econometrics gathers with economic theory

In parallel with these theoretical developments, major advances were accomplished with respect

to the econometric apparatus associated with DSGE models. In fact, numerous econometric pro-

cedures have been proposed to parameterise and evaluate DSGE models which, as suggested by

Geweke (2006), can be categorised according to a ”weak” or ”strong” econometric interpretation

of DSGE models.

Under the ”weak” interpretation, a DSGE model mimics the world only along a carefully

specified set of dimensions. Parameters are chosen such that selected features given by the model

match as closely as possible those observed in the data. This approach is behind calibration,

the method originally proposed by Kydland and Prescott (1982), which simply attributes values

to the parameters, based on information from previous studies and common knowledge, such

that the model is able to replicate some selected moments of the data. Another approach

that fits in the ”weak” interpretation is the Generalised Method of Moments (GMM), used

for e.g. in Christiano and Eichenbaum (1990), where parameters are chosen in a way that

selected equilibrium equations are verified, as precisely as possible. In addition, there is the

method adopted in Christiano et al. (2005), where a subset of the parameters is estimated by

minimising the difference between estimated impulse response functions (IRFs) to a monetary

policy shock in an identified VAR and those based on the DSGE model.

In contrast, the ”strong” econometric interpretation of DSGE models takes the whole set of

implications of the model into account, attempting to obtain estimates that are able to provide

a full characterisation of the observed data series. These methods are called full-information

methods, as they embody all the characteristics and implications of the model in the estima-

tion process while, by an analogous reasoning, the ones lying in the ”weak” interpretation are

called limited-information methods. There are basically two methods that fit into the ”strong”

interpretation category, Classical and Bayesian Maximum Likelihood Estimation (MLE). Both

methods rely on the specification of a probabilistic structure for the model, which enables the

construction of a function, the likelihood function, that expresses the probability of observing

a given dataset as a function of the parameters of the underlying model. The likelihood can

be computed for different combinations of parameters, in order to find the combination that

produces the maximum value for the likelihood, i.e. that makes the data set (that we know to

be true) ”more likely”. In Classical MLE, parameter estimates are directly obtained from this

process, being simply the values found to produce the maximum value of the likelihood. This

12

method has been applied by a number of authors to estimate the parameters of DSGE models,

such as Kim (2000) and Ireland (2001). In Bayesian MLE, an additional function is considered,

the prior, representing the a-priori probability that the researcher attributes to different possible

values of the parameters, before observing the data, based on previous studies or on his per-

sonal beliefs. The information from the prior is then combined with the information from the

likelihood and the resulting function can then be maximised, with respect to the parameters,

in a similar way as previously described, until the combination of parameters estimates that

produces the highest value for the objective function is found, i.e. the combination that makes

both the data set and the imposed a-priori beliefs to be ”more likely”. The application of these

techniques to the estimation of a DSGE model was firstly done by DeJong et al. (2000) and

has since then been adopted by several researchers as is the case of Smets and Wouters (2003),

Adolfson et al. (2005), Rabanal and Rubio-Ramırez (2005), Adolfson, Laseen, Linde and Villani

(2007), and Christoffel, Coenen and Warne (2008).

Bayesian techniques stand out

When comparing the two econometric interpretations of a DSGE model, although both have

advantages and disadvantages, the superiority of the ”strong” interpretation is clear, both from

an economic and statistical point of view. On the economic side, it is appealing since parameters

estimates are obtained employing all the restrictions implied by the model, allowing for a more

consistent characterisation of the data generation process. On the statistical side, efficiency is

enhanced by the use of all available information. Furthermore, while the computational burden

associated with full-information methods may have been a problem in the past, computational

methods have dramatically improved over the last years, so that even large-scale models can be

solved quite efficiently.

Within the two full-information methods we have referred, Bayesian estimation is clearly

the one that has gathered more supporters. Classical MLE has proven to be feasible only for

systems of relatively small size and not for the large-scale models that have been used recently.

The main issue has to do with identification problems. In the words of Canova (2007a) ”One

crucial but often neglected condition needed for any methodology to deliver sensible estimates

and meaningful inference is the one of identifiability: the objective function must have a unique

minimum and should display ”enough” curvature in all relevant dimensions”. In models with

a large amount of parameters to estimate it is hard to obtain correct information about all the

13

parameters from the data, which implies that quite often two problems arise: the likelihood is

flat in large subsets of the parameters space, i.e. different values of the parameters lead to the

same joint distribution for the observed data, making the maximisation of the likelihood a very

hard (and sometimes impossible) task; or the likelihood peaks in ”strange areas”, producing

estimates that are at odds with additional information that the researcher may have, the so-

called ”dilemma of absurd parameter estimates”. In Bayesian inference, the likelihood function

is ”reweighted” by the prior which produces a function with more curvature that is able to avoid,

or at least minimise, both the ”flatness” and ”dilemma of absurd parameter estimates” problems.

This way, Bayesian MLE is better equipped to deal with identification problems, although it

is not able to avoid them 2. Furthermore, it is important to note that, being highly stylised,

DSGE models are necessarily misspecified, with some elements of its structure being sometimes

at odds with the data. In Classical MLE, the outcome of the overall estimation process is highly

sensitive to the estimated value of each parameter meaning that if one or more parameters are

poorly supported by the data, leading to a bad estimate, this may strongly affect the results

for all the parameters of the model. In Bayesian MLE this problem is minimised, since the

estimation of each parameter does not embody a particular value for the other parameters being

estimated, but instead, it takes a whole distribution into account for each parameter, which

encompasses a wide range of possible estimates. In addition, the Bayesian approach allows one

to formally incorporate the use of a-priori information, coming either from previous studies or

simply reflecting the subjective opinions of the researcher, through the specification of prior

probability density functions for the parameters, while Classical estimation cannot incorporate

even the most non-controversial prior information. Also, the Bayesian approach provides a

natural framework for model evaluation and comparison, through the computation of posterior

odds ratios3. These have Classical analogues in likelihood ratios, but go beyond the comparison

of two parameter vectors of greatest likelihood to involve information about other possible values

by comparing weighted-average values of likelihoods, with weights given by the priors. Finally,

another important advantage of Bayesian methods is the fact that they automatically produce

probability distributions for the model’s parameters, IRFs, forecasts, and all the other quantities

given by the model, and thereby directly provide a measure of the uncertainty associated with

model-based analysis and forecasting.2For a discussion of identification problems in DSGE models see Canova (2007a) and Iskrev (2009).3This concept will be defined further on in Section 3.

14

A large scope of application

The development of a deeper econometric framework surrounding DSGE models has considerably

enlarged their scope of application. They are now attractive not only because of their theoretical

consistency but also because the most recent vintages, estimated with Bayesian techniques, have

made big a progress on the empirical front. Indeed, they have proven to fit economic data quite

reasonably and to compare well and in many cases outperform more traditional tools such as

VARs, VECMs, BVARs, random walks, among others. These findings can be found in many

reference studies such as Smets and Wouters (2003), Fernandez-Villaverde and Rubio-Ramirez

(2004), Del Negro et al. (2005), Juillard et al. (2006) and Adolfson, Linde and Villani (2007).

An important milestone in this evolution was the development of Dynare, a pre-processor

and a collection of publically available Matlab routines, specifically developed for the solution,

simulation and estimation of DSGE models4. It has enabled an easier access to quantitative

DSGE modelling and is by now the software adopted by a large fraction of macroeconomists

working with DSGE models.

The possibility of combining a strong theoretical framework with a good explanatory power of

empirical evidence has turned New-Keynesian DSGE models into one of the most attractive tools

for modern macroeconomic modelling and has led to their widespread use. They are considered

to be the state of the art vehicle for economists to structure their thinking, understand the

functioning of the economy and are used for a number of purposes, from policy analysis to welfare

measurement, identification of shocks, scenario analysis and forecasting exercises. They are

capable of performing basically all empirical exercises that previous macroeconometric models

performed but have the advantage of being strongly founded on economic theory, in contrast

with the more statistical nature of previous models. They are the object of attention not only in

the academia but also in a number of policy-making institutions, such as central banks, which

has brought the later closer to academic research and knowledge. In fact, DSGE models are

seen as an outstanding vehicle of cross-fertilisation between the more theoretical ground of the

academia and the more empirically oriented world of central banks and other institutions alike.

Some prominent examples of organisms using these models are: the IMF whose model, presented

in Kumhof and Laxton (2007), has been used for e.g. to analyse the effects of fiscal policy on the

US economy; the Bank of Sweden who has used its model, described in Adolfson, Laseen, Linde4For more information on Dynare, and access to its materials, please refer to the website

http://www.cepremap.cnrs.fr/dynare/. A reference manual is provided by Griffoli (2007).

15

and Villani (2007), both for policy analysis and forecasting; the Bank of Finland with the AINO

model, that can be seen in Kilponen and Ripatti (2006), which besides being applied to the

study of many relevant issues of the Finnish economy, like ageing and demographics, is already

the official forecasting model of Finland’s central bank; and the ECB with the New Area Wide

Model, exposed in Christoffel et al. (2008), which is being used for a wide range of purposes.

For what has been exposed, New-Keynesian DSGE models and their estimation is certainly

one of the most interesting and promising fields in modern macroeconometric research, from

which no country should be left out. In the case of Portugal, some exercises have already been

performed using DSGE models, namely: Pereira and Rodrigues (2000), where an analysis of the

impact of a tax reform package is performed, using a calibrated New-Keynesian model; Fagan

et al. (2004), where the macroeconomic effects of structural changes are investigated, using a

calibrated New-Keynesian model; Silvano (2006) where business cycle movements are studied

using an RBC model estimated with GMM; and Almeida et al. (2008), where the effects of

increasing competition in the nontradable goods and labour markets are inspectioned, using a

calibrated large-scale New-Keynesian model. However, to our knowledge, no attempt has yet

been made to estimate a New-Keynesian DSGE model using Portuguese data. We therefore

consider this to be not only a legitimate but also necessary task, which has led to the conduct

of the present study.

3 On the construction, solution and Bayesian estimation of a

DSGE model

We now provide an overview of the main methodological aspects of our work. It is not our

intention to give an extensive description of the ”formal world” of DSGE models but to present

and justify the main choices and procedures inherent to our research, providing a (as much as

possible) comprehensive understanding of what is ”behind the scenes” of our results 5.

3.1 Model construction and solution

The construction of a DSGE model starts with the specification of the characteristics of the

economy one wishes to model, its environment, its agents, their preferences, technologies and

constraints, and of a set of structural shocks to which the economy is subject. The objectives5We focus, in particular, on the methods applied by Dynare since this is the software we have chosen to adopt.

16

of each agent are then presented, usually involving dynamic optimisation problems for private

agents and policy rules for the fiscal and monetary authorities. Solving the problems of the op-

timising agents with the Lagrange multipliers method one obtains a set of first order conditions,

defining those agents’ decision rules. The equations obtained from this process are then subject

to aggregation procedures, to obtain a set of equations describing the behaviour of economic

agents as a whole, i.e. at the macroeconomic level instead of the microeconomic level from which

we departed. Furthermore, a set of market clearing conditions is specified, to ensure that all the

markets in the economy are in equilibrium in each and every period.

Combining the agents’ behavioural equations, policy rules and constraints (at the aggregate

level) with the market clearing conditions and the shock processes one obtains a set of equations

expressing the endogenous variables of the model at each period as a function of its past, present

and expected future path, of the set of parameters quantifying the relations between variables,

and of the structural exogenous innovations hitting the economy in each period. These equations,

defining our DSGE model, are the starting point of a set of operations which in the end allow

for the computation of a stable, unique, solution to the model. Below, we provide a description

of the main steps needed to achieve this.

Stationarising the model

The first step is rendering all the variables in the model stationary, with a well defined steady-

state to which they return after the economy has been hit by one or more temporary shocks. For

a model like ours, which comprises a unit-root technology shock and inflation in the steady-state,

the following transformations are needed: all non-stationary real variables have to be scaled by

the level of technology; all nominal variables have to be scaled by the numeraire of the economy;

the consumption lagrange multiplier has to be multiplied by the technology level.

Some issues should be referred at this point, although they will probably become more evident

after the model has been presented. First, variables are scaled with the technology level and

numeraire price level of the period in which they are decided and therefore, all predetermined

variables such as the capital stock are scaled with the lagged values of technology and/or price.

Second, being assumed to grow in line with productivity (which grows with technology), the

nominal wage rate needs to be scaled by both the price and technology levels. Finally, foreign

real variables are scaled by the foreign technology level, not the domestic one.

17

Writing the model in a general form

Having obtained the set of equations defining the stationary model, they can be put into the

following matrix general form:

Et {f (yt+1, yt, yt−1, et+1, et)} = 1 (1)

where yt is a vector containing the (stationary) endogenous variables (i.e. variables generated

”inside” the model, explained by the model equations), 1 is a vector of 1’s and et is a vector

containing the structural exogenous innovations (i.e. variables generated ”outside” the model),

which are assumed to be Gaussian white noise processes, satisfying the following properties:

E(et) = 0; E(ete′t) = Σe; E(ete

′s) = 0 t 6= s; et ∼ N(0, Σe)

We want to find the solution of the model, i.e. obtain the path for the endogenous variables,

in every period, that is conformable with our model’s structure and assumptions. To do this,

we need to express the endogenous variables at any given period as a function of the available

information set. This can be formalised recurring to a categorisation of the endogenous variables

into predetermined (or state) and non-predetermined (or forward-looking) variables. The former

are variables that at t are already determined, i.e. totally known at the end of t− 1, while the

later are variables that are only known at t. We want to express the forward-looking endogenous

variables at t as a function of the available information set composed by the predetermined

endogenous variables and the innovations occurring in that period. Formally, we wish to obtain

a function g(.), called the policy function, such that:

yt = g (yt−1, et) (2)

Now note that from (2) we can write:

yt+1 = g (yt, et+1) = g (g (yt−1, et) , et+1) (3)

Substituting (2) and (3) in (1) we can rewrite the model as:

Et {f (g (g (yt−1, et) , et+1) , g (yt−1, et) , yt−1, et+1, et)} = 1 (4)

18

Ideally, we would be able to obtain the solution of our model directly from analytical ma-

nipulation of this system of equations. The problem is that they are usually highly non-linear,

which makes the task of finding the exact expression for g(.) a very difficult one, if not impos-

sible. In general, this is not achievable and researchers typically try to obtain a satisfactory

approximation using numerical methods. We focus on a strategy that is commonly used and

corresponds to the one applied by Dynare.

Computing the steady-state of the model

Start by computing the steady-state of the model, which corresponds to the situation in which

there are no innovations and variables loose their time subscript, implying that variables assume

a constant value in every period that verify (1) and (2). Denoting the steady-state value of yt

by y, and using (1) and (2), the steady-state of the model can then be represented by:

f (y, y, y, 0, 0) = 1 (5)

y = g (y, 0) (6)

Approximating the model with a log-linearisation

Having computed the steady-state, each equation of (1) is approximated by the expected value

of a first order Taylor expansion of its logarithm around the steady-state6. As a result, a ”new”

set of equations is obtained defining an approximate linear model whose endogenous variables

correspond to the percentage deviations of the original variables from their steady-state. Using

these equations, (1) and (2) can then be approximated by the following system:

Et {fy+1yt+1 + fyyt + fy−1yt−1 + fe+1et+1 + feet} = 0 (7)

yt = gy−1yt−1 + geet (8)

6For any function f(x1t , x

2t ) a first order Taylor expansion of the logarithm of f(.) around the steady-state

(x1, x2) is given by:

ln f(x1t , x

2t ) ' ln f(x1, x2) +

1

f(x1, x2)

(∂f(x1

t , x2t )

∂x1t

(x1, x2)(x1

t − x1) +∂f(x1

t , x2t )

∂x2t

(x1, x2)(x2

t − x2))

=

= ln f(x1, x2) +1

f(x1, x2)

(∂f(x1

t , x2t )

∂x1t

(x1, x2)x1x1t +

∂f(x1t , x

2t )

∂x2t

(x1, x2)x2x2t

)

where xit =

xit−xi

xi is the percentage deviation of variable xit (with i = 1, 2) from the steady-state. Naturally, this

can be extended to functions with any number of arguments.

19

where fy+1, fy and fy−1 are the matrix derivatives of f(.) with respect to yt+1, yt and yt−1,

respectively, evaluated in the steady-state; fe+1 and fe are the matrix derivatives of f(.) with

respect to et+1 and et, respectively, evaluated in the steady-state; gy−1 is the derivative of g(.)

with respect to yt−1, evaluated in the steady-state; ge is the derivative of g(.) with respect to et,

evaluated in the steady-state; yt+1, yt and yt−1 are vectors containing the percentage deviations

of the original endogenous variables from their steady-state at times t+1, t and t−1, respectively.

Equation (7) constitutes the general form of the approximate linear model and equation

(8) expresses the corresponding endogenous forward-looking variables as a function of the en-

dogenous state variables and the innovations, which is the analogous of (2) for the approximate

log-linear model. It is characterised by an approximate linear policy function dependent on

matrices gy−1 and ge, which are a function of the deep, structural and policy parameters of

the model, but whose exact composition is yet unknown. gy−1 and ge are called the feedback

and feedforward matrices, respectively. The feedback matrix characterises the impact of the

endogenous state variables on the endogenous forward-looking variables, while the feedforward

matrix characterises the impact of the innovations on the endogenous forward-looking variables.

Once we have obtained the behaviour of the endogenous variables of the approximate linear

model, we can easily recover the values of the original endogenous variables by simply multiplying

their deviations from the steady-state by the corresponding steady-state value and adding this

steady-state value to the obtained result, i.e. for any variable yit:

yit = yi + yiyi

t (9)

Therefore, as long as we can solve the approximate linear model, i.e. obtain gy−1 and ge

that characterise its policy function, given in (8), we will be able to obtain an (approximate)

solution for our original model, by using (9) and the previously computed steady-state. And we

are in fact capable of finding gy−1 and ge by applying some by now well-known techniques for

solving Linear Rational Expectations (LRE) models.

Solving the approximate linear model

To find gy−1 and ge, a series of complex algebraic procedures are needed, which we will present

here in only rough terms, since a detailed explanation is considered to be beyond the scope of

20

our study7. We start by using (8) to write:

yt+1 = gy−1yt + geet+1 = gy−1 (gy−1yt−1 + geet) + geet+1 =

= gy−1gy−1yt−1 + gy−1geet + geet+1 (10)

Using (8) and (10) we can rewrite (7) as:

Et {fy+1 (gy−1gy−1yt−1 + gy−1geet + geet+1) + fy (gy−1yt−1 + geet)+

+fy−1yt−1 + fe+1et+1 + feet} = 0 ⇔

⇔ (fy+1gy−1gy−1 + fygy−1 + fy−1) yt−1 + (fy+1gy−1ge + fyge + fe) et = 0 (11)

This equation has to hold for any yt−1 and any et and therefore each parentheses must be

null. Thus the matrices gy−1 and ge that we seek must satisfy:

fy+1gy−1gy−1 + fygy−1 + fy−1 = 0 (12)

fy+1gy−1ge + fyge + fe = 0 (13)

Now note that equation (11) can be rearranged in the following way:

fy+1gy−1gy−1yt−1 + fygy−1yt−1 + fy−1yt−1 + fy+1gy−1geet + fygeet + feet = 0 ⇔

⇔ fy+1gy−1 (gy−1yt−1 + geet) + (fygy−1 + fy−1) yt−1 + (fyge + fe) et = 0 ⇔

⇔ fy+1gy−1yt + (fygy−1 + fy−1) yt−1 + (fyge + fe) et = 0 (14)

We can then write our approximate linear model, characterised by (8) and (14) in the fol-

lowing matrix representation:

Axt+1 = Bxt + Cet (15)

where:

A =

0 fy+1

I 0

B =

−fy−1 −fy

0 I

xt =

yt−1

gy−1yt−1

C =

− (fyge + fe)

ge

7To obtain a detailed exposition of this subject, please refer to Klein (2000) and Sims (2002).

21

We now have a representation of our approximate linear model as a first order linear stochas-

tic difference equation, defined for endogenous variables xt and characterised by matrices A, B,

and C, that contain reduced form parameters, which are a function of the deep parameters of

our original model. There are multiple solutions to this system but we are only interested in

finding a unique stable one, since we want our variables to always return to the steady-state

after a shock and have a unique, identified, trajectory. Following Blanchard and Kahn (1980)

this occurs if the system’s number of eigenvalues larger than one, called explosive, is equal to the

number of non-predetermined variables included in the system. To find the eigenvalues of the

system, we first apply a generalised Schur decomposition to matrices A and B, which produces:

A = QTZ

B = QSZ

where T and S are upper triangular matrices and Q and Z are unitary matrices.

We can then compute the generalised eigenvalues of (A,B), that solve the generalised eigen-

value problem λAx = Bx, where λ is the vector of generalised eigenvalues. The ith generalised

eigenvalue λi is computed as the ratio of the diagonal elements of S to those of T , i.e. (using

subscripts to denote matrix elements) λi = SiiTii . Having done, this, the Blanchard-Kahn con-

dition can then easily be checked. If the condition is satisfied, we can proceed in finding the

model solution. Let the matrices (Q,T, Z, S) be rearranged in a way that the pairs (Tii, Sii) are

organised such that λi is increasing in i, moving from left to right, which allows us to isolate

the unstable part of the system from the remaining part. We can then rewrite our system as:

QTZxt+1 = QSZxt + Cet ⇔ Q−1QTZxt+1 = Q−1QSZxt + Q−1Cet ⇔

⇔ TZxt+1 = SZxt + wt ⇔

⇔

T11 T12

0 T22

Z11 Z12

Z21 Z22

xt+1 =

S11 S12

0 S22

Z11 Z12

Z21 Z22

xt +

w1,t

w2,t

⇔

⇔

T11 T12

0 T22

z1,t+1

z2,t+1

=

S11 S12

0 S22

z1,t

z2,t

+

w1,t

w2,t

where T22 and S22 are the block matrices whose diagonal elements produce λi > 1, i.e. the

22

matrices containing the unstable part of the system, z2,t = [Z21 Z22] xt and wt = Q−1Cet.

Then, using the lower block of this system, we can write a sub-system containing all the explosive

generalised eigenvalues:

T22z2,t+1 = S22z2,t + w2,t (16)

Solving for z2,t yields:

z2,t = Pz2,t+1 − S−122 w2,t (17)

where P = S−122 T22. Performing recursive substitution for z2,t+1, z2,t+2,..., we obtain:

z2,t = P(Pz2,t+2 − S−1

22 w2,t+1

)− S−122 w2,t =

= P 2z2,t+2 − PS−122 w2,t+1 − S−1

22 w2,t =

= P 2(Pz2,t+3 − S−1

22 w2,t+2

)− PS−122 w2,t+1 − S−1

22 w2,t =

= P 3z2,t+3 − P 2S−122 w2,t+2 − PS−1

22 w2,t+1 − S−122 w2,t =

= P iz2,t+i −∞∑

i=0

P iS−122 w2,t+i (18)

Now note that P−1 = T−122 S22 is a diagonal matrix containing the system’s explosive eigenvalues

and therefore its inverse, P , is also a diagonal matrix containing the inverse of those eigenvalues.

Therefore P t converges to zero as t increases, implying:

P iz2,t+i = 0 (19)

Therefore, z2,t can be written as:

z2,t = −∞∑

i=1

P i−1S−122 w2,t+i (20)

This means that z2,t can be expressed solely as a function of future shocks whose expected

value at t is zero implying:

z2,t = 0 ⇔[

Z21 Z22

]xt = 0 ⇔

[Z21 Z22

]

yt

gy−1yt

= 0 ⇔

23

⇔ Z21yt + Z22gy−1yt = (Z21 + Z22gy−1) yt = 0

Since this must be valid for any yt, it must be that:

Z21 + Z22gy−1 = 0 (21)

Then, as long as matrix Z22 is invertible, we can write:

gy−1 = −Z−122 Z21 (22)

Therefore, if the Blanchard-Kahn condition and a rank condition on Z22 are satisfied, we

can find a matrix gy−1, given by (22), that produces a unique, stable, solution for our model.

Having recovered gy−1, recovering ge is then straightforward from equation (13):

fy+1gy−1ge + fyge + fe = 0 ⇔ ge = − (fy+1gy−1 + fy)−1 fe (23)

We can then finally obtain our model solution by replacing the obtained gy−1 and ge in (8):

yt = gy−1yt−1 + geet (24)

This equation constitutes the reduced form representation of our DSGE model, which has

the same form of a VAR model. The crucial difference is that while the DSGE model imposes

restrictions on the coefficient matrices gy−1 and ge that relate directly to the economic structure

of the model, the VAR literature imposes identifying restrictions that do not come directly from

an explicit model.

Having found the form of matrices gy−1 and ge we simply have to define some initial condi-

tions for the endogenous variables, y0, and obtain values for the model parameters, to be able to

use the model for all types of ”computational experiments”. For reasons that will become clear

in the next subsection, we impose the assumption that the initial conditions are drawn from a

Normal distribution.

Note that since the endogenous variables are expressed as percentage deviations of the orig-

inal variables from the steady-state, the results of the simulations have to be interpreted ac-

cordingly. Furthermore, it is important to be aware that the performed approximation is only a

local one, around the steady-state, and therefore experiments should not deviate the economy

24

considerably from the steady-state, since in this case the approximation will no longer be valid.

Our approach to finding parameters estimates relies on the Bayesian MLE methodology and

therefore the next subsections focus on the procedures associated with it.

3.2 Likelihood function

Using a MLE approach, we first need to obtain the likelihood function. The likelihood corre-

sponds to the joint density of all variables in the data sample, conditional on the structure and

parameters of our model.

To obtain it, we first need to establish a relation between the data and the model. We do

this by considering that the measured variables can be explained partly by the model’s variables

and partly by some factors that the model is unable to measure, which we call measurement

errors. This can be formalised through the following equation:

y∗t = F yt + Gut (25)

where y∗t represents the vector of observed variables, F is a matrix establishing the link between

the model’s endogenous variables and the data, ut stands for the vector of measurement errors

and G consists of a matrix defining the role of measurement errors in each observed variable.

The measurement errors are assumed to be Gaussian white noise processes, such that:

E(ut) = 0; E(utu′t) = Σu; E(utu

′s) = 0 t 6= s; ut ∼ N(0,Σu)

If the number of innovations in the model is higher than the number of observed variables,

the inclusion of measurement errors is optional. If, however, this is not the case, one must include

at least as many measurement errors as the difference between the number of innovations and

observed variables. Otherwise, the system will suffer from a singularity problem.

Denoting matrices gy−1 and ge in (24) by D and E, respectively, and combining this equation

with (25) we can write the following system:

yt = Dyt−1 + Eet (26)

y∗t = F yt + Gut (27)

where y0, et and ut satisfy the already mentioned properties.

25

Now note that since the model innovations, et, the initial conditions, y0, and the measurement

errors ut are all normally distributed, it must be that yt and y∗t are also normally distributed.

Denoting the whole data sample by y∗, we can then write the log-likelihood function as:

L(y∗|y∗, Σy∗) = −Tn

2log 2π − 1

2log |Σy∗ | − 1

2(y∗ − y∗)′Σy∗

−1 (y∗ − y∗) (28)

where n is the number of observed variables, T is the number of periods in the sample, y∗ is the

expected value of y∗ and Σy∗ is its variance-covariance matrix.

The computation of (28) requires the use of the entire data sample at once, which is a quite

complicated task. An alternative, more convenient, format of the likelihood can be obtained

using a predictor error decomposition, which produces the following:

L(y∗|θ) = −Tn

2log 2π − 1

2

T∑t=1

log |Σy∗ t|t−1| −12

T∑t=1

(y∗t − y∗t|t−1

)′Σy∗ t|t−1

−1(y∗t − y∗t|t−1

)(29)

where y∗t|t−1 is a predictor of y∗t using information up to t − 1, Σy∗ t|t−1 is a predictor of the

variance-covariance matrix of y∗t using information up to t−1, and θ is a vector of parameters on

which y∗t|t−1 and Σy∗ t|t−1 depend. Note that, contrary to (28), (29) can be computed recursively,

since it only involves the one step ahead forecasts of y∗t and Σy∗ . These can be easily computed

through the use of the Kalman filter8.

To understand how, start by noting that the system described by equations (26) and (27)

can be viewed as a linear state space system, where the former is the transition (or state)

equation, and the latter is the measurement (or observation) equation. For a system of this

type, the Kalman filter provides an assessment of the conditional probability associated with

time t observations, given the history of past observations, producing optimal one step-ahead

forecasts of both y∗t and Σy∗ . Starting in period t, the procedure applied by the filter can

basically be described in the following steps:

1. For t = 1, set initial values for a one-step ahead forecast of time t states, yt|t−1, and

respective forecast error variance-covariance matrix, Σyt|t−1.

2. Compute a one-step ahead forecast of time t data, y∗t|t−1, and respective variance-covariance

matrix, Σy∗ t|t−1, as:

y∗t|t−1 = E (y∗t |t− 1) = E ((F yt + Gut) |t− 1) = F yt|t−1 (30)

8A thorough overview of the Kalman filter, is provided in Welch and Bishop (2001) and Canova (2007b).

26

Σy∗ t|t−1 = E(y∗t − y∗t|t−1

)(y∗t − y∗t|t−1

)′= E

(F yt + Gut − F yt|t−1

)×

× (F yt + Gut − F yt|t−1

)′ = E(F

(yt − yt|t−1

)+ Gut

)×

×((

yt − yt|t−1

)′F ′ + u′tG

′)

= FE(yt − yt|t−1

) (yt − yt|t−1

)′F ′+

+ GE(utu

′t

)G′ = FΣy

t|t−1F′ + GΣuG′ (31)

3. Having observed time t data, compute the corresponding likelihood as:

L(y∗t |θ) = −n

2log 2π − 1

2log |Σy∗ t|t−1| −

12

(y∗t − y∗t|t−1

)′Σy∗ t|t−1

−1(y∗t − y∗t|t−1

)(32)

4. Update forecasts of time t states, yt|t, and respective variance-covariance matrix, Σyt|t, as:

yt|t = yt|t−1 + Σyt|t−1F

′Σy∗ t|t−1−1

(y∗t − y∗t|t−1

)(33)

Σyt|t = Σy

t|t−1 − Σyt|t−1F

′Σy∗ t|t−1−1FΣy

t|t−1 (34)

5. Compute an one-step ahead forecast of time t + 1 states, yt+1|t, and respective variance-

covariance matrix, Σyt+1|t, as:

yt+1|t = E (yt+1|t) = E ((Dyt + Eet+1) |t) = Dyt|t (35)

Σyt+1|t = E

(yt+1 − yt+1|t

) (yt+1 − yt+1|t

)′ = E(Dyt + Eet+1 −Dyt|t

)(Dyt+

+Eet+1 −Dyt|t)′ = E

(D

(yt − yt|t

)+ Eet+1

) ((yt − yt|t

)′D′ + e′t+1E

′)

=

= DE((

yt − yt|t) (

yt − yt|t)′)

D′ + EE(et+1e

′t+1

)E′ = DΣy

t|tD′ + EΣeE

′ =

= D(Σy

t|t−1 − Σyt|t−1F

′Σy∗ t|t−1−1FΣy

t|t−1

)D′ + EΣeE

′ (36)

6. Iterate on steps 2-5 for t = 2, 3, 4, ..., T .

As long as the initial conditions, the model innovations and the measurement errors are all

normally distributed, the estimated y∗t|t−1 and Σy∗ t|t−1 are the optimal forecasts of y∗t and Σy∗ .

This way, we are able to recursively express the likelihood of each observation, period by

period, which when replaced in (29) provide us the expression for the likelihood of the whole

data sample. Notice that the obtained forecasts are a function of matrices F , G and Σu, which

we know, and of matrices D, E and Σe, which are functions of the structural parameters of

27

our original model, that we intend to estimate. Therefore, the likelihood function we obtain is

simply a function of the original model’s parameters, which is exactly what we intended.

3.3 Prior distributions

The next step is the specification of prior distributions for the parameters we want to estimate,

p(θ), which is where the Bayesian component of the estimation process starts. Each prior is a

probability density function of a parameter, constituting a formal way of specifying probabilities

to each value that the parameter can assume, based on past studies or/and occurrences or simply

reflecting subjective views of the researcher. Either way, it is basically a representation of belief

in the context of the model under analysis, being constructed without any reference to the

data set contained in the estimation sample constituting an additional, independent, source of

information on the model’s parameters.

The specification of a prior starts with the selection of the most adequate functional form for

the distribution. This can be done on the basis of a number of criteria, with some of the most

common ones being: inverse gamma distribution for parameters bounded to be positive; beta

distribution for parameters bounded between zero and one; normal distribution for parameters

that are not bounded.

It is then necessary to choose values for the parameters defining each of the distributions,

which are usually measures of location (e.g. mode and mean) and dispersion (e.g. standard de-

viation and probability intervals). For this, parameters are usually grouped into two categories:

parameters for which we have relatively strong a priori convictions, which comprises the model’s

core structural parameters; and parameters for which we are quite uncertain about, which in-

cludes the parameters that characterise the stochastic shocks. Priors for the parameters in the

first category are based on our reading of existing empirical evidence and their implications for

macroeconomic dynamics. For parameters in the second category, although we can also recur to

existing studies, the strategy is mainly to set priors with reasonable means and a density with

a large support so that the distribution can cover a considerable range of parameter values, i.e.,

priors that are only weakly informative.

Since the prior is generated from well-known densities, its computation is straightforward.

28

3.4 Posterior distributions

Having derived the likelihood and specified the priors, we can then estimate the posterior distri-

bution. The posterior represents the probabilities assigned to different values of the parameters

after observing the data. It basically constitutes an update of the probabilities given by the

prior, based on the additional information provided by the variables in our sample. To express

formally how the posterior relates to the likelihood and the priors we apply the well-known

Bayes theorem to the two random events θ and y∗, which produces:

p (θ|y∗) =p (θ, y∗)p (y∗)

(37)

p (y∗|θ) =p (θ, y∗)

p (θ)⇔ p (θ, y∗) = p (y∗|θ) p (θ) (38)

where p (θ|y∗) is the density of the parameters conditional on the data (the posterior), p (θ, y∗)

is the joint density of the parameters and the data, p (y∗|θ) is the density of the data conditional

on the parameters (the likelihood), p (θ) is the unconditional density of the parameters (the

prior) and p (y∗) is the marginal density of the data (this concept will be further explored in the

next subsection). Replacing (38) in (37):

p (θ|y∗) =p (y∗|θ) p (θ)

p (y∗)(39)

Now note that p (y∗) does not depend on the parameters and therefore, in what concerns

the estimation of the parameters, can be treated as a constant, enabling us to write:

p (θ|y∗) ∝ p (y∗|θ) p (θ) = K (θ|y∗) (40)

where K (θ|y∗) is the posterior kernel, which is proportional to the posterior by the factor p (y∗).

Taking logs:

lnK (θ|y∗) = ln p (y∗|θ) + ln p (θ) = L(y∗|θ) + ln p (θ) (41)

Assuming that priors are independently distributed, this equation may be calculated as:

lnK (θ|y∗) = L(y∗|θ) +∑ג

x=1

ln p (θx) (42)

29

where ג is the number of parameters being estimated. This is the equation that will allow us to

estimate the posteriors. It is however analytically intractable, since it is a nonlinear complicated

function of the parameters contained in θ, and therefore the analysis has to be performed with

numerical methods.

We start by maximizing (42) with respect to θ to obtain an estimate for the mode of the

posterior distribution, θm, and for the Hessian matrix evaluated at the mode, H(θm) (note that

the maximum of p (θ|y∗) will be the same as the maximum of K (θ|y∗)). This is carried out using

an optimisation routine (csmiwell) developed by Christopher Sims.

We then use a Monte-Carlo Markov-Chain (MCMC) sampling method, specifically the

Metropolis-Hastings (MH) algorithm, to simulate the posterior distributions. The general idea

of the algorithm is to generate a Markov-Chain that represents a sequence of possible parameter

estimates, in a way that the whole domain of the parameter space is explored, and then use the

frequencies associated with each estimate to build an histogram that mimics the posterior dis-

tribution. To do so, the algorithm starts by specifying a ”candidate” (or jumping) distribution,

from which several parameter estimates are drawn and then poses an ”acceptance-rejection”

rule according to which some of the generated estimates are kept and some are not. To pick

the ”candidate” distribution, the algorithm builds on the fact that under fairly general regu-

larity conditions, the posterior will be asymptotically normal, and uses the mode and Hessian

obtained from the maximisation of the posterior kernel to define the mean and variance. The

variance is built as the inverse of the Hessian multiplied by a constant, called the scale factor,

which is a crucial parameter, since it determines the acceptance ratio, i.e. the percentage of

estimates generated from the jumping distribution that are kept to construct the posterior. In

the words of An and Schorfheide (2007), the algorithm ”constructs a Gaussian approximation

around the posterior mode and uses a scaled version of the asymptotic covariance matrix as

the covariance matrix for the proposal distribution. This allows for an efficient exploration of

the posterior distribution at least in the neighborhood of the mode”. More precisely, the MH

algorithm implements the following steps:

1. Consider a jumping distribution for the model’s parameters given by:

J(θ∗|θt−1

)= N

(θt−1, cΣθm

)(43)

where θt−1 is the distributions’s jumping mean, whose initial value is set to the previously

30

estimated posterior mode, Σθm is the variance of the distribution, computed as the inverse

of the previously estimated Hessian matrix, and c is a scale factor.

2. Draw a proposal new estimate θ∗ from the distribution.

3. Compute r, the ratio of the posterior kernel evaluated at the new proposal estimate over

the posterior kernel evaluated at the previous proposal estimate:

r =K (θ∗|y∗)K (θt−1|y∗) (44)

4. Accept or discard θ∗ as the new estimate according to the following rule:

θt =

θ∗ with probability min(r,1)

θt−1 otherwise

5. If θ∗ is accepted update the mean of the distribution, otherwise keep the previous one.

6. Loop on steps 2-5.

7. Having done enough loops, use the accepted draws to built an histogram.

It is important to understand the intuition behind this mechanism. When r > 1 we will

definitely keep θ∗ since it produces a higher value for the posterior than θt−1, i.e., given our

sample, it is more likely to have θ∗ than θt−1. When 0 ≤ r ≤ 1, the proposal estimate produces

a lower value for the posterior. However, we will not discard this estimate immediately, we will

accept it with probability r and reject it with probability 1− r. The point is that to be able to

visit the entire domain of the posterior distribution, we should not be too quick to simply throw

out the candidate giving a lower value of the posterior kernel, because it might be the case that

the candidate allows us to leave a local maximum and travel towards the global maximum. As

clearly said in Griffoli (2007) ”the idea is to allow the search to turn away from taking a small

step up and instead take a few small steps down in the hope of being able to take a big step up

in the near future”. This will produce a sample of diversified parameter estimates, where highly

likely values are represented by multiple occurrences, forming the center of the distribution, but

less likely values are also considered, forming the tails of the distribution.

A fundamental part of this procedure is the variance of the jumping distribution and in

particular the scale factor. If the variance is too small, the acceptance rate, i.e. the fraction of

31

draws that are accepted, will be too high and the Markov chain will not be able to do a good

job in visiting the entire distribution, and will probably get ”stuck” around a local maximum.

However, if the variance is too high, the acceptance rate will be too small and the chain will

spend much time visiting the tails of the distribution and will have difficulty in finding the

maximum. Therefore, c will be crucial to ”fine-tune” the variance of the jumping distribution,

such that the acceptance rate is neither too big nor to small. Another important aspect is the

number of iterations performed by the algorithm. The bigger the number, the smoother will be

the histogram, since each ”bucket” of the histogram will have less and less weight in the overall

distribution, and the closer will be the histogram to the desired theoretical distribution.

This way, we are able to obtain an approximation of the posterior distributions, characterised

by the usual measures of location (mode, mean) and dispersion (standard deviation, percentiles),

which provide not only point estimates of the parameters of the model but also a measure of

the uncertainty surrounding those estimates.

Beyond the calculation of posterior moments and distributions themselves, one can use these

results for a number of applications, which explore the model’s theoretical and empirical impli-

cations in an informative way. Some of the most common and relevant ones are: forecasting,

where departing from an initial state the future behaviour of the endogenous variables is pre-

dicted; historical decomposition, where the historical evolution of the observed variables, used

in the estimation, can be decomposed into the contributions of the structural shocks considered

in the model and the lagged effect of the initial state, allowing one to conclude on the main

driving forces behind the economy’s behaviour; IRFs, which corresponded to estimates of the

effect of each shock on the endogenous variables; forecast-error-variance decompositions, which

decompose the variance of the error in forecasting the endogenous variables into the contribu-

tions of the variance of each shock; counterfactual scenarios, where the consequences of assuming

a difference in some feature of the model are explored. For all these applications, we can obtain

not only point estimates, but also confidence intervals, by simply using the draws produced by

the MH algorithm.

3.5 Evaluation of the estimation results

A crucial part of the process of estimating a model is the conduction of an evaluation of its

results. In the case of a DSGE model, estimated with a Bayesian approach, this can be done

in a number of ways, using both techniques that are common to other estimation methods and

32

techniques that are exclusively used in a Bayesian context. We consider three broad classes of

aspects that can be inspectioned in order to assess the quality of the estimated model: validation

of the estimation procedures and results, ability of the model to fit the data’s characteristics

and comparison with alternative models.

Checking the estimation diagnosis and results

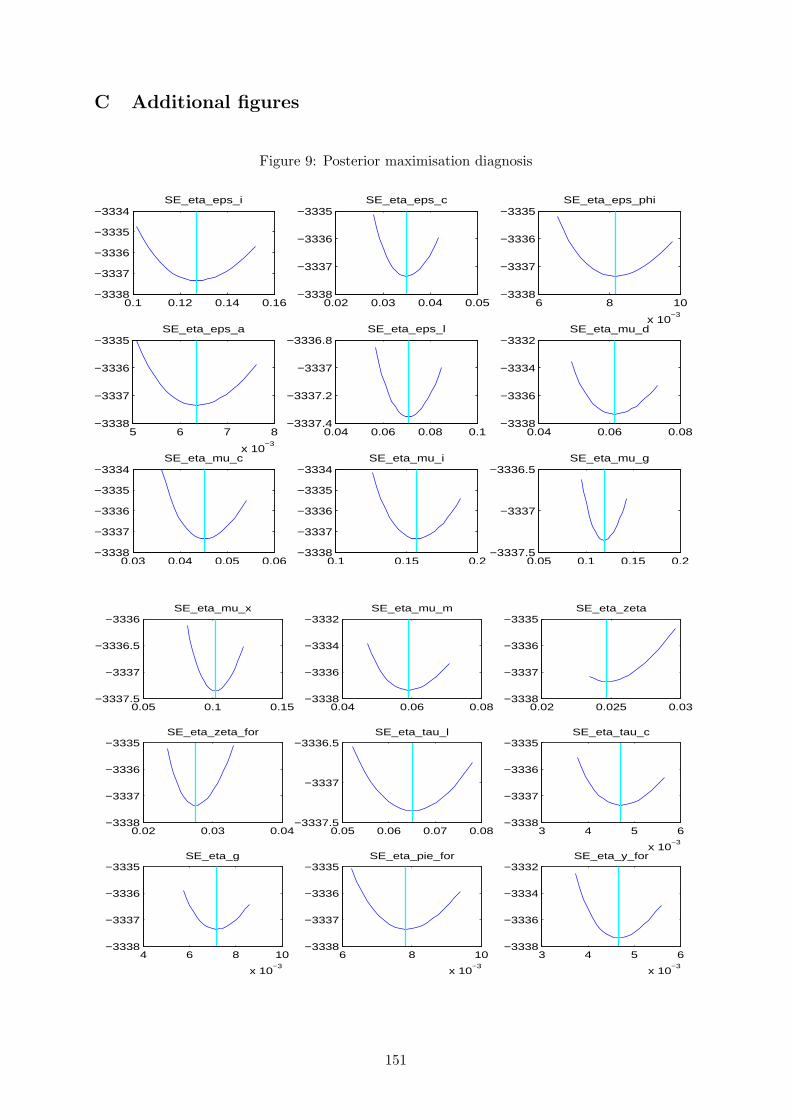

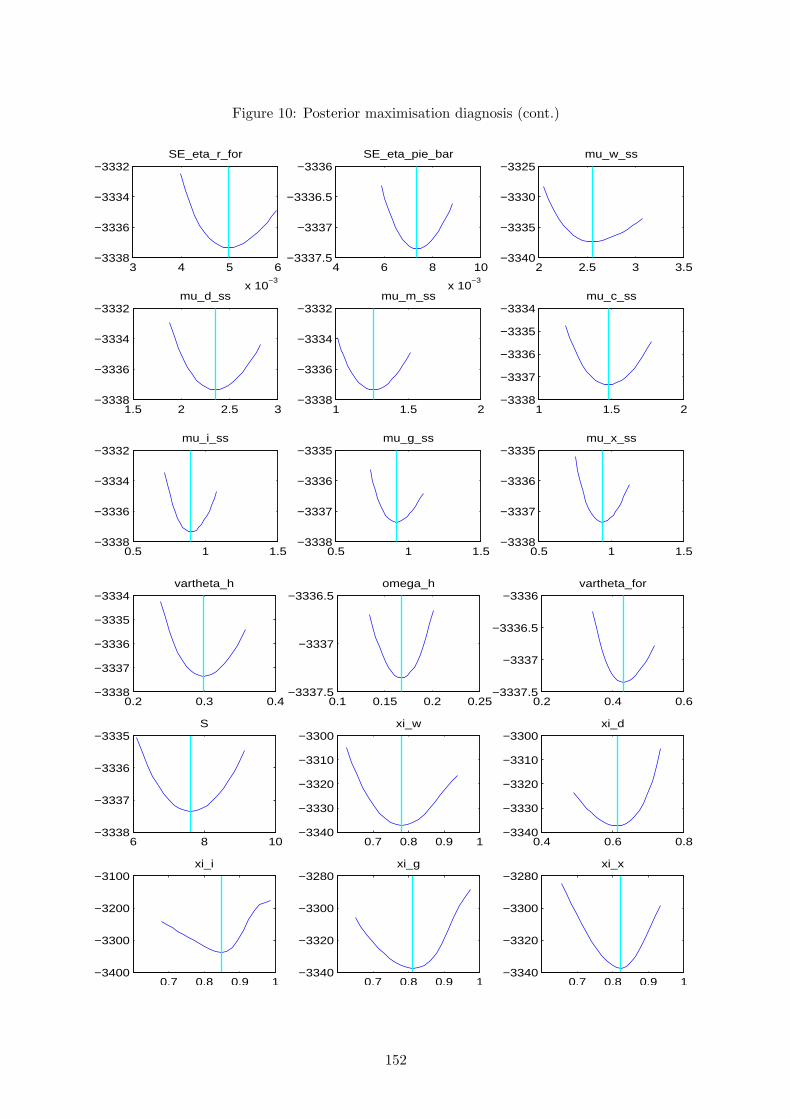

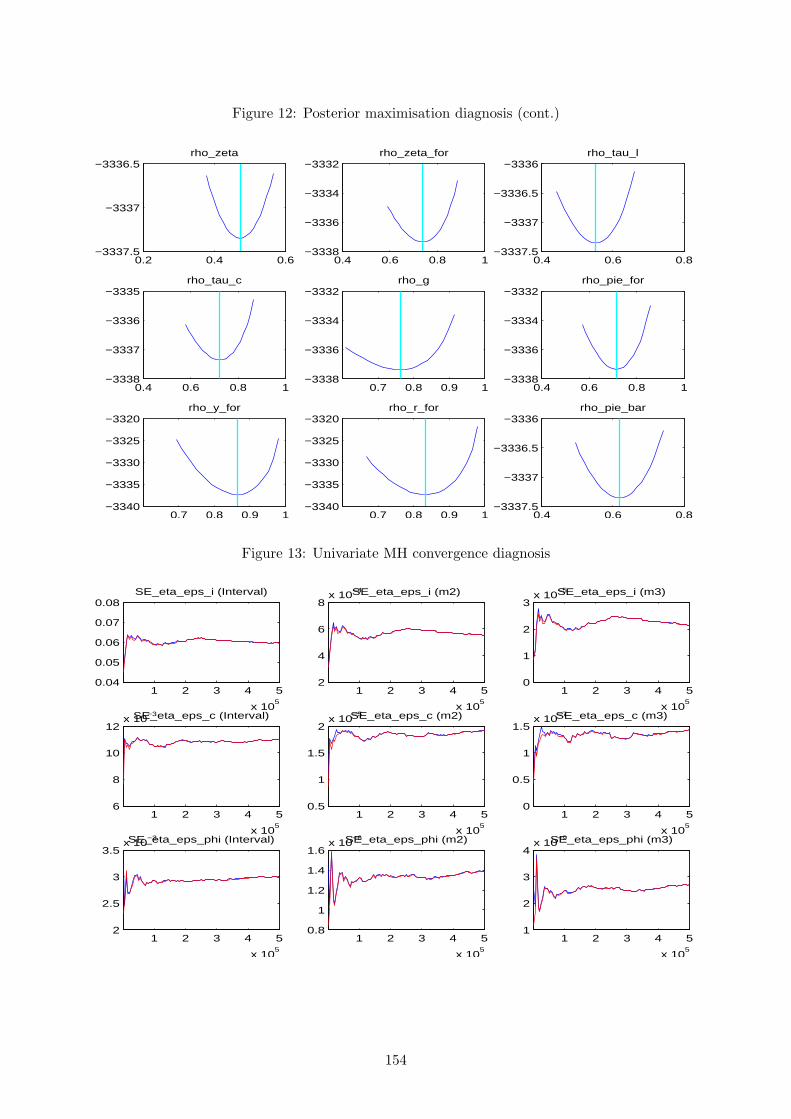

The first thing to check is the quality of the posterior kernel numerical maximisation. We do

this by plotting the minus of the posterior kernel for values around the computed mode, for each

estimated parameter in turn. If the estimated mode is not at the trough (bottom minus) of the

distribution, there is a clear sign that the numerical procedure is having a hard time finding the

optimum. This can be related to poor priors or to identification problems.

Secondly, if one concludes that the numerical procedure is working well, then the parameters

mode and standard deviation estimates can be inspectioned. They should be plausible both

from a statistical and an economic point of view. For this, comparison with previous studies

and evidence from micro data can be of extreme usefulness.

Thirdly, if the estimates seem to be reasonable, they can be considered as good initial values

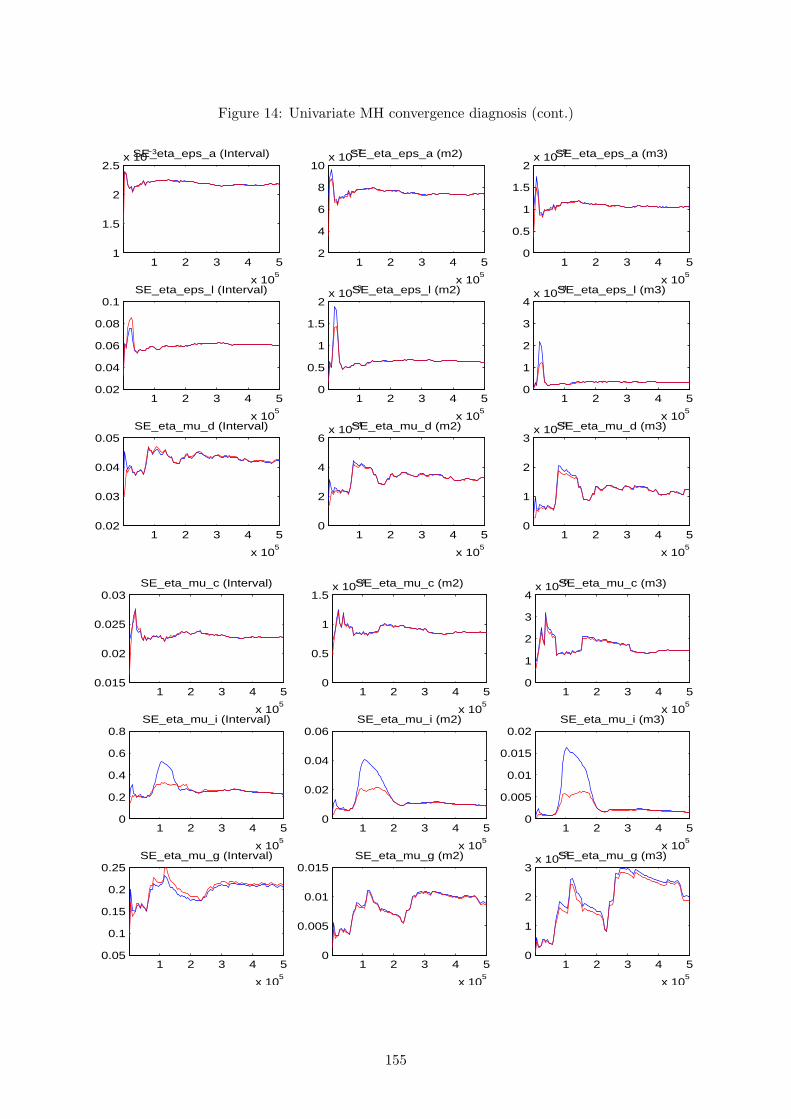

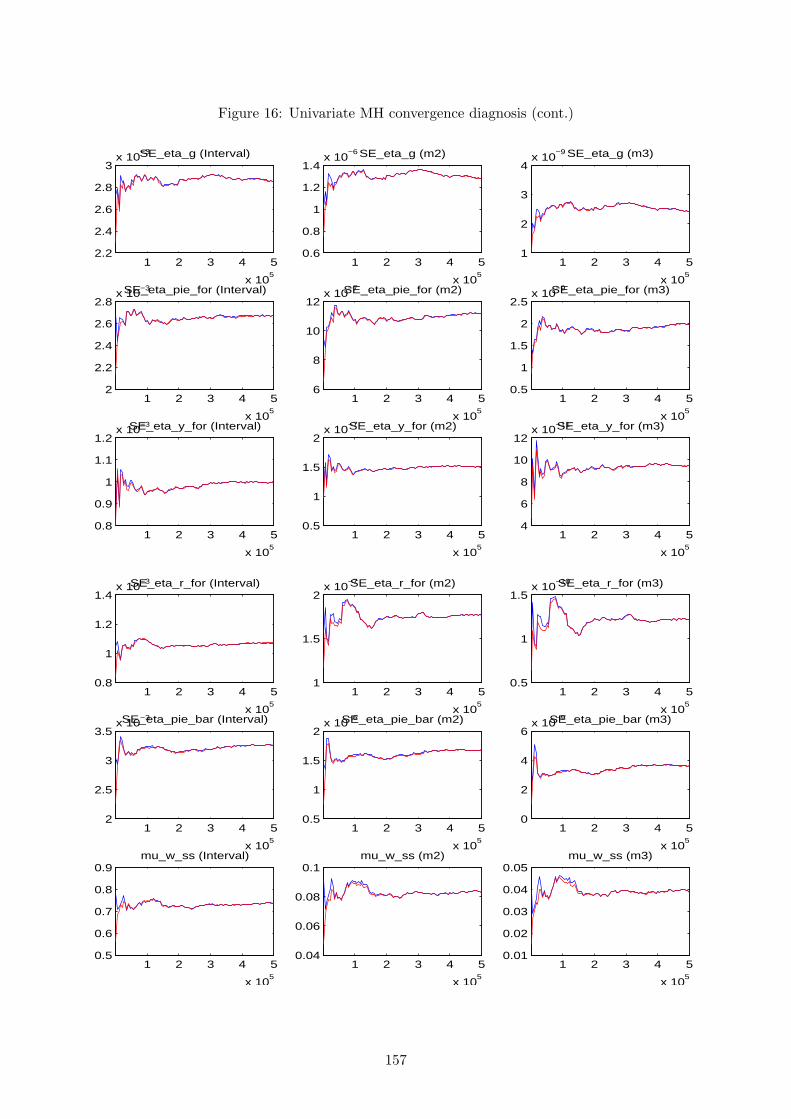

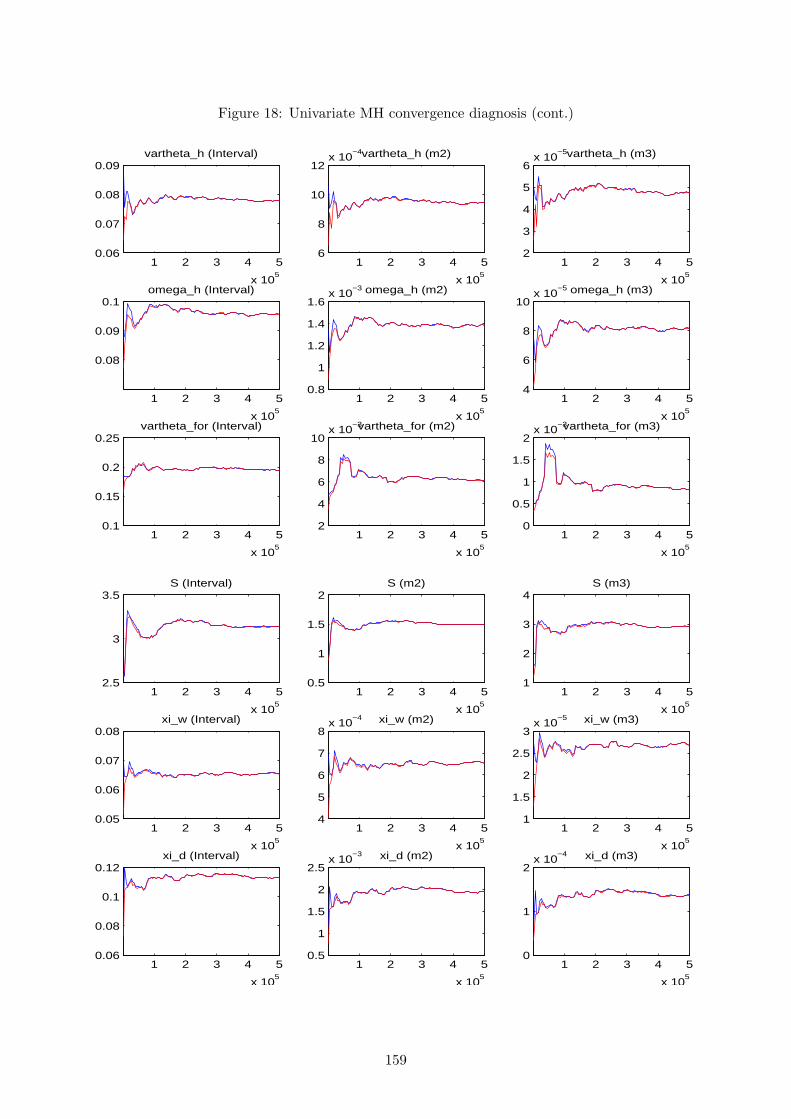

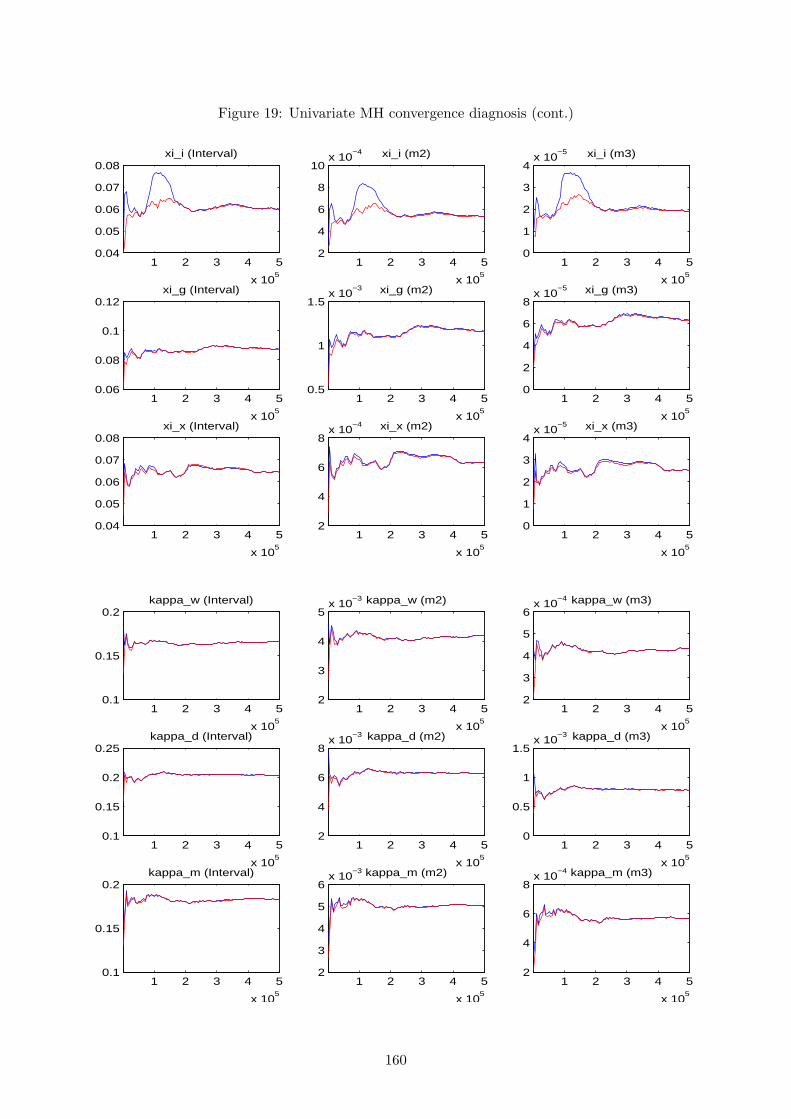

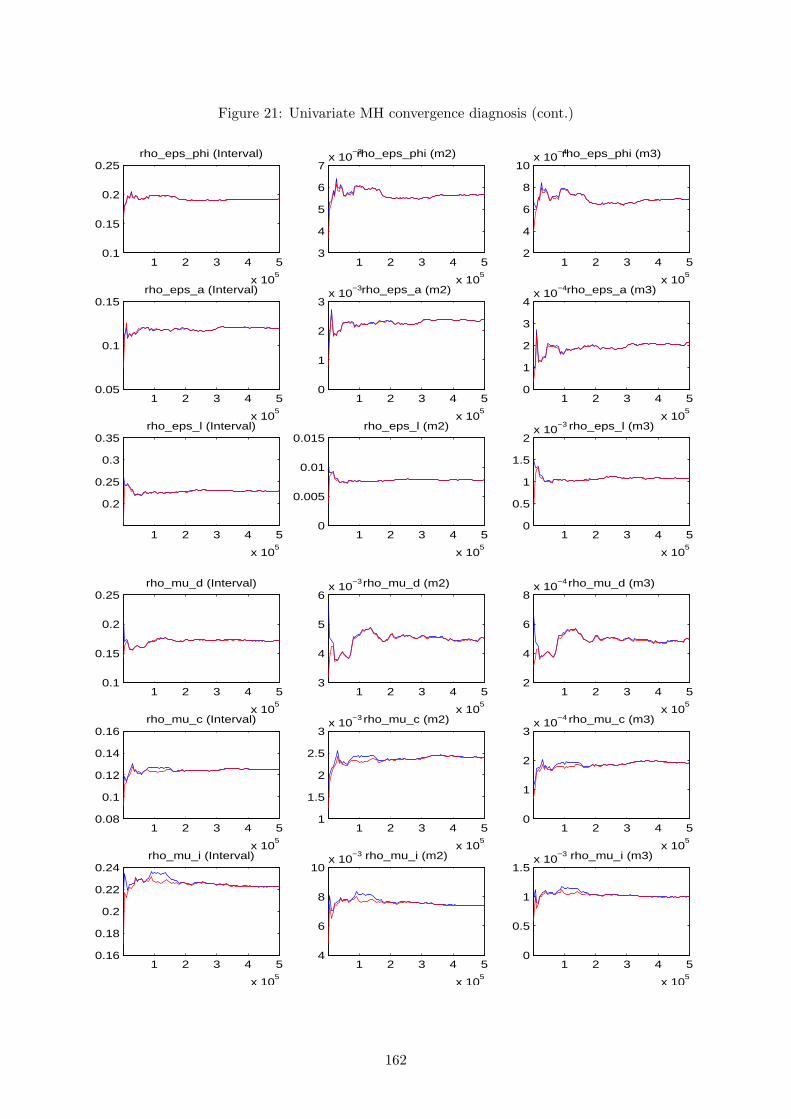

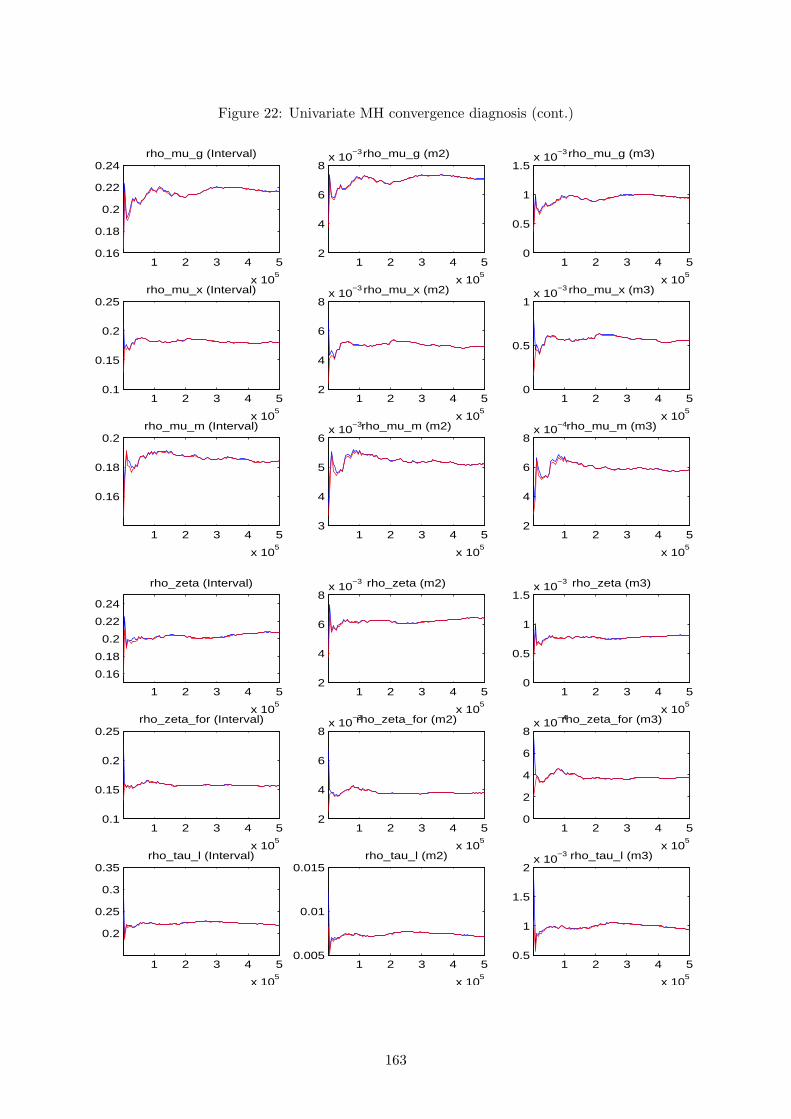

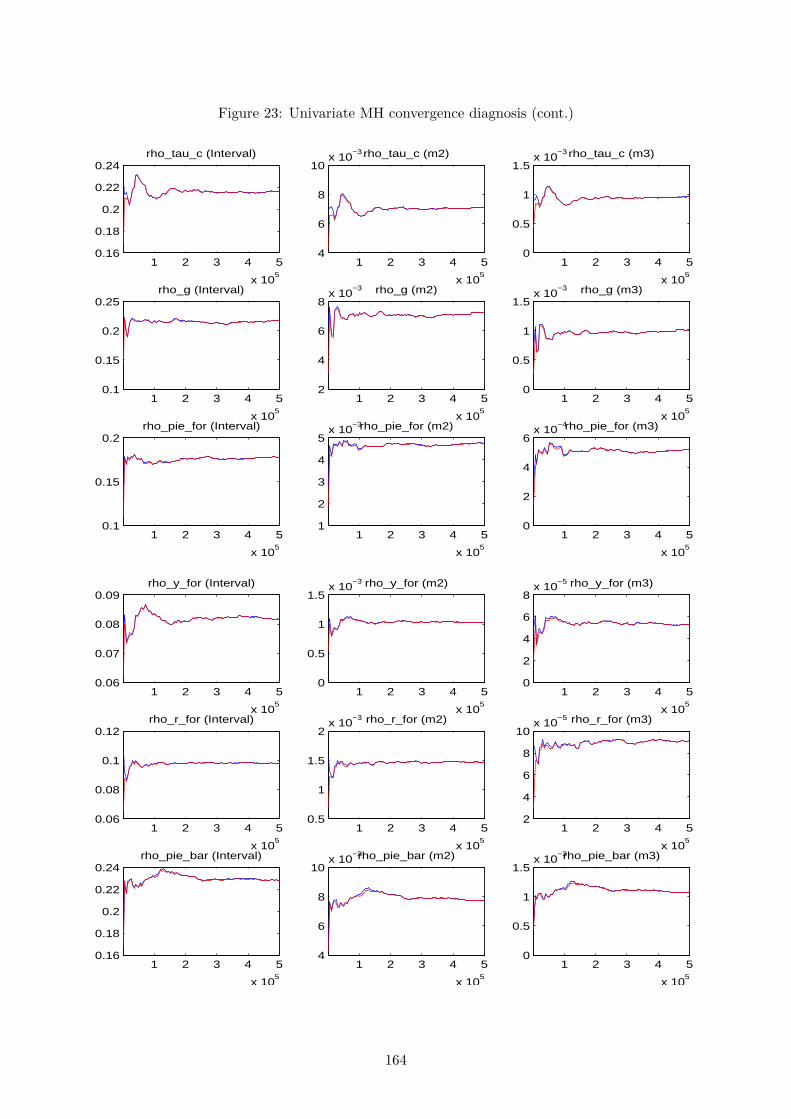

for the MH algorithm and, therefore, we can proceed by examining its convergence properties.

This is the main source of feedback to gain confidence or spot a problem with the results. To

obtain it, one should conduct several distinct runs of MH simulations, with each one starting

at a different initial value, and for each run perform a large number of draws. If convergence

is achieved, and the optimiser did not get stuck in an odd area of the parameter subspace, two

things should happen: results within each run’s iterations should be similar; results between

different runs should be close. When convergence is not achieved, the problem is usually related

to poor priors or to an insufficient number of MH iterations.

Fourthly, it is necessary to inspect the simulated posterior distribution and confront it with

both the prior distribution and the posterior mode obtained by the maximisation of the posterior

kernel. First, the posterior distributions should be approximately normal. Second, the prior

and posterior should not be excessively different nor excessively similar. If they are very far

from each other, this may indicate that the priors are imposing erroneous restrictions on the

data. If they are too similar, results are probably being mostly led by the prior and only

marginally by the data. In fact, informative posterior distributions can be obtained even when

the parameters are not identified in the data, if a tight enough prior distribution is specified. The

33

posteriors will appear to be well behaved only because the prior has selected a particular region

of the parameter space. While the prior should be used to exclude regions of the parameter

space that are unreasonable from an economic point of view, it should also be made reasonably