Basic-level Module - iaisweb.org · D. Legal Framework ... Note to learners Welcome to module 14:...

67

ICP 14: Preventive and Corrective Measures of the Supervisor Basic-level Module A Core Curriculum for Insurance Supervisors

Transcript of Basic-level Module - iaisweb.org · D. Legal Framework ... Note to learners Welcome to module 14:...

ICP 14: Preventive andCorrective Measuresof the Supervisor

Basic-level Module

A Core Curriculum for Insurance Supervisors

Copyright © 2006 International Association of Insurance Supervisors (IAIS).All rights reserved.

The material in this module is copyrighted. It may be used for training by competent organizations with permission. Please contact the IAIS to seek permission.

This module was prepared by Lawrie Savage, who is a former superintendent of insurance for the government of Ontario (1991–95) and is currently president of Lawrie Savage and Associates. He has 37 years of experience in the Canadian insurance sector and, in addition to his work with Ontario, was with the Canadian financial supervisory authority, OSFI, for 19 years. For the last eight years of his tenure with OSFI, he was in charge of non-life insurance supervision for Canada. He has also been chief executive officer of a Canadian life insurance company and vice chairman of a non-life insurer.

The module was reviewed by Pilar González de Frutos, a specialist in both sides of insurance supervision, is president of the Spanish Insurers Association. Prior to that, she was head of Spanish insurance supervision for six years. She earned her law degree at the Autonomous University in Madrid (Spain). She also has broad experience at the international level as a member of the International Association of Insurance Supervisors (IAIS), Asociación de Su-pervisores de Seguros de América Latina (ASSAL), Comité Européen des Assurances (CEA), and Federación Interamericana de Empresas de Seguros FIDES.

iii

Contents

About the Core Curriculum . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . v

Note to learners . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vii

Pretest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .ix

A. Introduction: Prevention and Correction in the Supervisory Process . . . . . . . . . . . 1

B. Understanding Key Terms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

C. Importance of ICP 14 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

D. Legal Framework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

E. The Application of Preventive and Corrective Measures in a Transparent,Consistent, and Effective Manner . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

F. Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

G. References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Appendix I. ICP 14 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

Insurance Supervision Core Curriculum

iv

Appendix II. Ladder of Intervention Followed by the Office of theSuperintendent of Financial Institutions Canada (OSFI) . . . . . . . . . . . . . . . . . . . . . . . . 42

Appendix III. Discussion of Case Studies and Possible Supervisory Strategies . . . . . 46

Appendix IV. Answer key . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

Figures

Figure 1: Original Situation in Which Two Brothers Own Company Aand Company B . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24Figure 2: Follow-up Situation in Which Mother Owns Corporation B . . . . . . . . . . . . 25

Case StudiesCase Study 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5Case Study 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14Case Study 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24Case Study 4 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26Case Study 5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

v

About theCore Curriculum

A financially sound insurance sector contributes to economic growth and well-being by supporting the management of risk, allocation of resources, and mobilization of long-term savings. The insurance core principles (ICPs), developed by the International As-sociation of Insurance Supervisors (IAIS), are key international standards relevant for sound financial systems.

Effective implementation of the ICPs requires skilled and knowledgeable insurance supervisors. Recognizing this need, the World Bank and the IAIS partnered in 2002 to develop a “core curriculum” for insurance supervisors. The Core Curriculum Project, funded and supported by various sources, accelerates the learning process of both new and experienced supervisors. The ICPs provide the structure for the core curriculum, which consists of a set of modules that summarize the most relevant aspects of each topic, focus on the practical application of supervisory concepts, and cross-reference existing literature.

The core curriculum is designed to help those studying it to:

• Recognize the risks that arise from insurance operations• Know the techniques and tools used by private and public sector professionals

to identify, measure, and manage these risks• Operate effectively within a supervisory organization• Understand the ICPs and other IAIS principles, standards, and guidance• Recommend techniques and tools to help a particular jurisdiction observe the

ICPs and other IAIS principles, standards, and guidance• Identify the constraints and identify and prioritize supervisory techniques and

tools to best manage the existing risks in light of these constraints.

vii

Note to learners

Welcome to module 14: preventive and corrective measures of the supervisor!This is a basic-level module on preventive and corrective measures that does not

require specific prior knowledge of this topic. The module should be useful to either a new insurance supervisor or an experienced supervisor who has not dealt extensively with the topic—or is simply seeking to refresh and update knowledge.

Start by reviewing the objectives, which will give you an idea of what a person will learn as a result of studying the module, and answer the questions in the pretest to help gauge your prior knowledge of the topic. Then proceed to study the module either on an independent, self-study basis or in the context of a seminar or workshop. The amount of time required to study the module on a self-study basis will vary but it is recommended that it be addressed over a short time, broken into separate sessions on parts if desired.

To help you engage and involve yourself in the topic, we have interspersed the module with a number of hands-on activities for you to complete. These are intended to provide a checkpoint from time to time so that you can absorb and understand the material more readily. You are encouraged to complete each of these activities before proceeding with the next section of the module. You will also find questions dealing with the local situation and related to practices in your jurisdiction. These are intended to help you apply the material in this module to your local circumstances. If you are working with others on this module, develop the answers through discussion and co-operative work methods.

As a result of studying the material in this module, you will be able to do the fol-lowing:

Insurance Supervision Core Curriculum

viii

1. Describe measures that a supervisory authority might take to help prevent breaches of legislation and regulations from occurring

2. Describe the instruments available to supervisory authorities to enable timely preventive and corrective measures to be taken if an insurer fails to operate in a manner that is consistent with sound business practices or regulatory require-ments

3. Identify the costs and the benefits of early intervention4. Describe possible triggers for supervisory intervention and illustrate how they

can be arranged in a supervisory ladder, so that more serious breaches result in more intrusive intervention

5. Select an appropriate form of communication between the supervisory author-ity and an insurer, in response to a particular type of supervisory concern

6. Justify the imposition of timetables in plans of corrective action7. Describe the oversight required once a plan of corrective action has been agreed

on8. Summarize the requirements of ICP 14.

ix

Pretest

Before studying this module on preventive and corrective measures, answer the follow-ing questions. The questions are designed to help you gauge your existing knowledge of this topic. An answer key is presented in appendix IV at the end of the module.

For each of the following questions, circle the response that is correct or most relevant.

1. Asupervisoryauthoritybelievesthereisahighprobabilitythatarecentlylicensedinsurerisnotcomplyingwiththelegislationandregulations.Whichofthefollowingpreventivemeasuresmightthesupervisoryauthoritytakefirst?

a. Takeawaytheinsurer’slicense

b.Meetwiththeboardofdirectorstoexplainthereasonfortheconcerns

c. Seeklegalactionthroughthecourtsfornoncompliance

d.Requestabusinessplansoastobeabletoassesslikelyfuturerisk

e.Retainaninternationalauditingfirmtocarryoutaninvestigation

f. Performanonsiteinspection

g. Amendthelegislationandregulations.

Insurance Supervision Core Curriculum

x

2. Whichofthefollowingisnot anadvantageofusingasupervisoryladderorsimilarschemeforassessingrisk?

a. Ithelpstoensureconsistencyinthewayrisksareassessed

b. Itenablesstaffofthesupervisoryauthoritytoresolveconcernswithouttheinvolvementoftheauthority’sseniormanagement

c. Ithelpstoensurethatinsurersunderstandhowriskswillbeassessedandcangovernthemselvesaccordingly

d. Itservesasa“gameplan”thatpoliticianscanapproveinadvance,sotheywillnotbesurprisedwhenthesupervisoryauthorityrecommendsaparticularcourseofactiontodealwithasituationofconcern.

3. Inadditiontothesupervisoryladderandtheladderofintervention,whichofthefollowingcanhelptoensurethatinsurersarebeingdealtwithinaconsistentmanner?

a. Apolicyandproceduresmanual

b.Aregulationthatprescribespenaltiesforthelatefilingofregulatoryreturns

c. Aconsumerombudsman.

4. Categorizethefollowingpreventiveandcorrectivemeasuresintothreegroupsbasedontheorderinwhichtheyarelikelytobeapplied—inotherwords,earlymeasures,mid-termmeasures,andlate-termmeasures:

a. Assessthefitnessandproprietyofofficersanddirectors

b.Withdrawtheinsurer’slicense

c. Increasethefrequencyoffinancialreporting

d.Requireabusinessplan

e.Conductapublichearingintotheinsurer’saffairs

f. Performaroutineonsiteinspection

g. Reviewtheannualfinancialregulatoryreturnfiledbytheinsurer

h.Restricttheinsurer’svolumeofbusinessbyputtingaconditioninitslicense.

5. Whichofthefollowingarebenefitsthatreviewinganinsurer’sbusinessplanmightprovidetoasupervisor?

a. Itindicateswhattheinsurerplanstodointhefuture,enablingthesupervisortoconsidertherisksinvolvedandwhethertheinsureriswellpositionedtomanagetheserisks

ICP 14: Preventive and Corrective Measures of the Supervisor

xi

b. Itenablesthesupervisoryauthoritytoscheduleitsonsiteinspectionatatimethatwillbeconvenienttotheinsurer

c. Itprovidesinsightintomanagement’sabilitytoprepareawell-thought-outandcoherentplan

d. Itprovidesinsightintomanagement’sabilitytocontrolitsoperationsandachieveitsstatedgoals

e. Itbetterpreparesthesupervisortoadvisetheinsurer’smanagementonmattersofbusinessstrategy

f. Alloftheabove,exceptforaandc

g. Alloftheabove,exceptforbande

h.Alloftheabove.

6. Threeoftheactionslistedbelowarefeaturesofrisk-basedsupervision.Whichofthefollowingactionsisnot necessarilyassociatedwithrisk-basedsupervision?

a. Basingsupervisoryactivitiesontheperceivedrisklevelofeachinsurer

b.Assessinginsurersonthebasisofrisk

c. Reviewingfinancialstatementsandcalculatingearly-warningtestratios

d.Usingasupervisoryladderorsomeothermechanismtoassessriskinaconsistentmanner.

7. Whichofthefollowingareimportantcriteriawithregardtotheeffectivenessofsanctionsfornoncompliance?

a. Theapplicationofsanctionsmustrequirecourtaction

b.Thepenaltiesmustbesignificantenoughtobeameaningfuldeterrent

c. Sanctionsagainstindividualsmustinvolveimprisonment

d.Thepenaltiesmustactuallybeenforced,notmerelystatedinthelaw

e.Bothaandb

f. Bothaandc

g. Bothbandd.

Insurance Supervision Core Curriculum

xii

8. Asupervisoryauthorityfindsthataninsurerhasinvestedaconsiderableproportionofitsfundsinrealestate.Whichofthefollowingpreventiveorcorrectivemeasuresshouldbeappliedfirst?

a. Requiretheinsurertofileamoredetailedlistingofitsinvestments

b.Requiretheinsurertoreduceitsvolumeofbusiness

c. Requirethatthelargestpropertiesbevaluedbyanaccreditedappraiserandadjusttheinsurer’ssolvencycalculationtoreflectanyovervaluation

d.Putaconditionontheinsurer’slicense,requiringthatitdisposeofsomeoftherealestatewithinaprescribedperiodoftime.

9. Aninsurerisnotmeetingtheminimumsolvencytest,andthesupervisoryauthorityhasjustrequiredthattheinsurerobtainatleast$5millionofadditionalcapitalassoonaspossible,butdefinitelywithinthenext90days.Atthispoint,whichofthefollowingpreventiveorcorrectivemeasuresshouldthesupervisoryauthoritybeconsidering?

a. Requiretheinsurertofilemonthlyfinancialstatements

b.Requiretheinsurertoprovideabusinessplan

c. Preparetowithdrawtheinsurer’slicense

d.Placeaconditionintheinsurer’slicenseindicatingthatthelicensewillexpirein90daysunlessitisrenewedbythesupervisoryauthority

e.Retainanauditfirmtocarryoutaspecialauditoftheinsurer.

10.Totalgeneral(non-life)insurancepremiumsinaparticularjurisdictiongrew4percentlastyear.Thepremiumgrowthratesof95percentofthegeneralinsurersfellwithinarangeof−10percentand+10percent.However,onegeneralinsurerhadapremiumgrowthrateof49percent.Whichofthefollowingpreventiveorcorrectivemeasureswouldthesupervisoryauthoritybemostlikelytoconsiderwithregardtothisinsurer?

a. Requiretheinsurertofileabusinessplanthatshowsexpectedfuturegrowthratesbylineofbusinessandtheexpectedgeographicdistributionofnewbusiness

b. Imposeaconditionontheinsurer’slicensetolimititsrateofgrowthinthecurrentyeartoalevelthatappearstobereasonablerelativetotheavailabilityofcapitalandtheinsurer’sabilitytounderwriteandprocessbusiness

ICP 14: Preventive and Corrective Measures of the Supervisor

xiii

c. Limittheinsurer’slicensesothatitwillexpirein180days,withtheintentionthatthelicensewillberenewediftheinsurerhasreduceditsrateofgrowthtoanacceptablelevelinthemeantime

d.Requiretheinsurertopostadepositwiththesupervisoryauthority,sothatfundswillbeavailabletoprotectthepublicifthecompanyisunabletomeetitsobligations.

1

ICP 14: Preventive and CorrectiveMeasures of the Supervisor

Basic-level Module

A. Introduction: Prevention and Correction in the Supervisory Process

The objective of insurance supervision is to build and maintain public confidence in the financial system of the country (1) by avoiding undue monetary loss to policyholders as a result of insolvency and (2) by working to ensure fair treatment of policyholders in accordance with the terms of their contracts. To achieve these objectives, the supervisor administers the provisions of the insurance law in a professional manner, recommends such revisions to the legal structure as may be necessary to deal with changing circum-stances, and works with insurers to foster the adoption of sound business and financial practices.

The supervisor and the supervisory system must strike a balance between an overly conservative approach based on extensive and restrictive regulation and, at the other extreme, a permissive approach that allows excessive risk taking by insurers. The conser-vative approach could protect policyholders from loss but may lead to high costs (which are borne by policyholders and therefore discourage them from purchasing insurance products) and tend to stifle innovation within the industry. Such a system would not foster development of a vibrant insurance industry capable of stimulating the country’s economy. The overly permissive approach could foster entrepreneurial behavior that may lead to an increase in the number of failures and undermine the credibility of the entire sector. Ideally, insurance products are available and affordable within a competi-tive industry that provides fair treatment to consumers.

An important prerequisite for this type of environment is a supervisory agency that has the legal power to take action in a timely and effective manner when insurer actions

Insurance Supervision Core Curriculum

�

or situations demand it and that exercises those powers in a way that is most likely to achieve system objectives.1

Insurance core principle (ICP) 14, as its explanatory note mentions, is concerned with this area of preventive and corrective action:

Where insurers fail to meet supervisory requirements or where their continued solvency comes into question, the supervisory authority must intervene to protect policyholders. To do so, the supervisory authority needs to have the legal and op-erational capacity to bring about timely corrective action. Depending on the nature of the problem detected, a graduated response may be required. In instances where the detected problem is relatively minor, informal action such as an oral or written communication to management may be sufficient. In other instances, more formal action may be necessary.

ICP 14 further requires that:

The supervisory authority takes preventive and corrective measures that are timely, suitable, and necessary to achieve the objectives of insurance supervision.

While the International Association of Insurance Supervisors (IAIS) does not set out any formal definition of the terms preventive and corrective, this module defines preventive measures as actions that seek to reduce risk or avoid situations likely to weaken the insurer’s position with respect to policyholders. In the case of preventive measures, the supervisor will generally take a proactive mode of response. Corrective measures are defined as measures that seek to improve an existing situation.

When the system is working as it should, the supervisor will seldom have to rely on the formal application of these measures. Desirable supervisory objectives tend to coincide with the objectives of responsible managers, boards of directors, and share-holders—that is, the company will generate a satisfactory return on equity and develop a strong franchise with the public. From a supervisory perspective, the best results typi-cally are achieved when supervisors and company managers work together to ensure that risk is properly managed to protect the public interest.

Supervisors who frame their comments on companies’ operations in terms that are both constructive and knowledgeable soon gain the respect of industry members. In addition, when the supervisor is backed up by broad legal authority to impose correc-tive and preventive measures of the types outlined in this module—and those measures are applied in a determined manner when the situation requires them—over time, it

1. Kumar, Chuppe, and Perttunen (1997) describes the regulatory framework adopted in some mature-market economies, and regulatory issues arising in some emerging markets. Part 2 of the paper examines in detail the regulation and supervision of non-bank activities and institutions, primarily in the United States, but also in many emerging markets. Das, Quintyn, and Chenard (2004) provides empirical evidence that the quality of regulatory governance and governance practices adopted by financial system regulators and supervisors matters for financial system soundness.

ICP 14: Preventive and Corrective Measures of the Supervisor

�

typically becomes less and less necessary to draw on the formal authorities contained in the law. In other words, when these conditions exist, moral suasion, rather than the application of the law per se, often is the normal basis of supervision.

Insurance Supervision Core Curriculum

4

B. Understanding Key Terms

The essential criteria elaborate ICP 14 as follows:

• The supervisory authority has available and makes use of adequate instruments to enable timely preventive and corrective measures if an insurer fails to oper-ate in a manner that is consistent with sound business practices or regulatory requirements [essential criterion a].

• The supervisory authority has the capacity and standing to communicate with insurers, and insurers comply with such communications, to ensure that rela-tively minor preventive or corrective measures are taken [essential criterion c].

• The supervisory authority initiates measures designed to prevent a breach of the legislation from occurring and promptly and effectively deals with noncompli-ance with regulations that could put policyholders at risk or impinge on any other of the authority’s objectives [essential criterion e].

Several key phrases in the criteria are important for the concept of preventive and corrective measures: adequate instruments; capacity and standing; timely, suitable, and necessary measures; and measures to prevent a breach from occurring.

Complete this exercise by referring to the wording of ICP 14. The following questions are intended to stimulate discussion. If you are working with oth-ers on this module, develop the answers through discussion and cooperative work methods.

1. Whatdoyouunderstandthetermadequateinstrumentstomean?

2. Whatdoyouunderstandthetermtimelymeasurestomean?

3. Discussyourunderstandingofthetermcapacityandstanding.

4. ConsiderwhatismeantbysuitablewithinthecontextofICP14.Whatcriteriamightbeappliedtodeterminewhetherameasureissuitableornot?

5. Suggestsomecriteriaorfactorsthatyouwoulduseindeterminingwhethercertainsupervisorymeasuresareorarenot“necessary.”

6. Whatconceptisevokedbytheideaofpreventingabreachofthelegislationfromoccurring?

Q1

ICP 14: Preventive and Corrective Measures of the Supervisor

�

The supervisor must have the legal authority within the su-pervisory framework to carry out corrective measures, as required. Specific types of legal authorities are discussed later in the module. In addition to the country’s actual insurance law, adequate instru-ments include written policies and procedures for the supervisory agency and an internal corporate governance system designed to ensure that the agency continues to function in an objective and professional manner.

The supervisor must have ca-pacity and standing, and this means the ability to recruit and maintain a human resource base with the experience and training required to assess risks within the insurance industry and to discuss those risks in a constructive manner with industry personnel. This implies that the salaries of supervisory staff have to be reasonably comparable to those of similar positions in the industry. If the supervi-sory staff do not have credibility with the industry, it will be difficult, if not impossible, to meet supervisory objectives in general and to conform with ICP 14 in particular. Credibility is also a function of making timely, suitable, and necessary decisions in a professional and transparent manner.

Situations can change rapidly in the insurance business, and timely measures are essential. If supervisors are to have a reasonable chance of obtaining the desired re-sults from various preventive and corrective measures, it is necessary to formulate plans and to carry them out within a time frame that is appropriate to the situation. For example, if it is clear that a company is insolvent, then rapid intervention by the supervisor provides the best chance of minimizing the depletion of assets and maxi-mizing the resources available to protect policyholder interests. Timely action is also an important factor in maintaining credibility with the industry. Supervisory mea-sures that are long delayed are likely to be ineffective not only because the situation has changed over time but also because they are less likely to be taken seriously by industry members. Government agencies are often criticized for their indecisiveness and slowness to act; the insurance supervisor must work to ensure that these stereo-types are not applicable to its operations.2

2. Andrews and Josefsson (2003) emphasize the system costs of regulatory forbearance and argue in favor of prompt closure when circumstances dictate.

An onsite inspection report for alife insurer contains the followinginformation:

Duringtheinspectionofthiscompany,which is one of the larger companiesin the marketplace, we noted the in-troduction of three new products inthepastyear.Eachoftheseproductsisquitecomplex.Wealsonoted that,although the systems department in-dicates that the internal software forprocessingthisbusinesswillbeonline“very soon,” sales of these productsarenowaccountingforalmost25per-centofthecompany’sbusiness.

Case Study 1

Insurance Supervision Core Curriculum

�

In maintaining the credibility of the supervisory system, preventive and corrective measures must be perceived by industry members and other observers as meaningful and appropriate to the circumstances. This module discusses some of the methodolo-gies that supervisors can employ to ensure that the measures being proposed are suit-able to the circumstances.

On occasion, it is necessary for the insurance supervisor to take tough measures to enforce the law, both to ensure continued respect for the legislative process and to safeguard the public interest. The supervisor, who holds strong powers, is responsible for using those powers judiciously and wisely and for using them when the situation requires it.

The task of the supervisor includes more than just reacting to problems. It includes a degree of proactive attentiveness with the goal of preventing problems from arising in the first instance by working with company management and boards of directors to reduce risk when it exceeds desirable levels. This is one of the key concepts underlying the risk-based approach to supervision. See case study 1 for an example of preventive action.

Complete this exercise by referring to the wording of ICP 14. The following questions are intended to stimulate discussion. If you are working with oth-ers on this module, develop the answers through discussion and cooperative work methods.

1. Doyoufeelthatyourownjurisdictionhasadequateinstrumentstoachieveitsobjectives?Ifnot,whataresomeimportantchangesthatyouwouldliketoseeandhowwouldtheyimprovethesituation?

2. Whatdoyouunderstandthetermtimelymeasurestomean?Doestimelyalwaysmeanthesamething?

3. Doyouseeaconnectionbetweentheneedfortimelymeasuresandtheneedforcapacityandstanding?

4. Howdoyouratetheimportanceofcapacityandstandingfromasupervisoryperspective?

5. Suggestsomewaysinwhichthecapacityandstandingofasupervisoryagencymightbeimproved.

6. Providesomeexamplesofhowabreachofthelegislationmightbeprevented.

Q2

ICP 14: Preventive and Corrective Measures of the Supervisor

�

Answer the following questions with regard to the information in case study 1.

1. Listanyconcernsyoumighthavewiththissituation.

2. Whatdoyouseeasthetimingforaction?

3. Discusssomeapproachestopreventionandcorrectionthatmightbefollowedinacaselikethis.

Q3

Insurance Supervision Core Curriculum

�

C. Importance of ICP 14

In a perfect world, it would not be necessary to think about remedial measures in insur-ance supervision or elsewhere. But when dealing with insurance companies, the stakes are high, and there is a unique potential for abuse. These companies amass substantial amounts of funds from the public to pay for services that will not be rendered until some future date, sometimes many years in the future. Unscrupulous insurers could exploit this state of affairs by using the funds to the advantage of their managers and shareholders rather than carefully preserving the amounts required to discharge pres-ent and future obligations.

International experience clearly underlines the need to have well-trained supervi-sors who are backed by comprehensive legal structures that provide the powers neces-sary to safeguard the public interest.

In addition to the need to protect the public interest directly, there is also a more indirect reason for ICP 14. Over the past 15 years or so, there have been significant improvements in banking supervision. Major inconsistencies between bank supervi-sion and insurance supervision are likely to give rise to what is termed regulatory arbitrage. For example, if in a country the laws of bank supervision are up to date and enforced by well-trained banking supervisors, but insurance supervision is largely absent, the maximum volume of financial transactions will tend to migrate to the less-supervised sector. When a transaction can be structured through an insurance company rather than a bank, this will be done. In the absence of monitoring and oversight, risk levels can become so high that the insurance sector may collapse. In some cases, this has given rise to a domino effect in which the entire financial sector, including the banking sector, has had to be restructured. This has occurred at great cost to the countries involved.

In most countries, the banking sector is now subject to modern supervisory re-quirements, including strong powers for the supervisor to take remedial actions to pro-tect the public and the country’s financial system. In order to avoid the problem of regulatory arbitrage, insurance supervisors must have corresponding powers.

In countries that have only recently been creating democratic institutions and im-posing modern standards of justice, the ability to implement powerful corrective and preventive measures may be even more important than in developed countries. In these types of emerging-market situations, financial entrepreneurs have not had a long pe-riod of experience in which to gain an understanding and appreciation of the need to protect the public interest and to maintain the integrity of their financial institutions. (Developed countries also have companies and individuals who lack this appreciation!) Accordingly, emerging-market countries may have an even greater need for supervisors who have authority, confidence to use it in a timely and decisive way, and ongoing sup-port of their ministers and other politicians.

ICP 14: Preventive and Corrective Measures of the Supervisor

�

D. Legal Framework

In order to have a sufficiently broad selection of preventive and corrective measures, it is important for the insurance law to include basic powers that:

• Enable the supervisor to monitor and understand developments in insurance companies and in the industry so that decisions can be made concerning when and what type of specific corrective measures may be required

• Can be exercised with varying degrees of intensity and represent important components of a program of preventive and corrective measures.

These basic powers fall into two specific categories. First, there are the fundamen-tal powers that one expects to find in almost any supervisory regime. These include the power to carry out onsite inspections, to request financial information, and to im-pose solvency requirements. A second category of supervisory powers includes more specialized authorities that complement the fundamental powers. These supplementary powers enhance the supervisor’s ability to protect the public interest.

This part of the module provides a catalogue of supervisory powers and explains their potential role as supervisory tools that can be used to reduce risk and to address existing problems. A later section focuses more specifically on techniques that can be used to apply the measures in a consistent manner and in ways that best fit the circum-stances.

The following questions are intended to stimulate discussion. If you are work-ing with others on this module, develop the answers through discussion and cooperative work methods.

1. Inyourview,whatarethefivemostimportantpowersrequiredbyaninsurancesupervisor?Ineachcase,explainwhyyouconsiderthepowertobecriticaltoachievingsupervisoryobjectives.

2. Howdoyouassesstherelativeimportanceofonsiteandoffsiteinspection(thatis,themonitoringandfinancialanalysisofinsurers’financialandoperationalresults)?

3. Discusstheroleofminimuminitialcapitalrequirementsandminimumsolvencyrequirementsinmeetingsupervisorygoals.Inyourview,whataretheessentialdifferencesbetweenthesetwoconcepts?

4. Providesomeexamplesofsupervisorypowersthatarenotamongthe“fivemostimportant”youhavelistedinquestion1andexplainwhyeachoftheseisalsoimportantandunderwhatcircumstancesthismightbethecase.

Q4

Insurance Supervision Core Curriculum

10

Fundamental powers

Certain fundamental powers should be present in every supervisory regime. They in-clude fit and proper requirements, the power to obtain well-designed annual supervi-sory filings and supplementary filings, the power to carry out onsite inspections, the power to inspect business plans, the power to enforce minimum capital and solvency requirements, the power to withdraw a business license, and the power to impose sanc-tions and penalties for noncompliance. This section deals with each of these in turn.

Fit and proper requirements

Given their fiduciary powers and access to policyholder funds, it is critical that senior managers and directors of insurance companies be persons of integrity. This being the case, the supervisor must be able to block access to insurers or remove senior managers, directors, or shareholders, where documented criminal or other behavior would render the persons or corporations not fit and proper for the purposes of operating, directing, or controlling an insurance com-pany. In keeping with the need to maintain transparent procedures, the supervisor should establish publicly accessible criteria describ-ing what constitutes (or at least provide examples of) situations or experience that do not meet fit and proper standards.3

The power to block a person from accepting a position or to remove someone from a position is a significant power and must be used judiciously. Nevertheless, it is a power that the supervisor must have in order to protect the public interest and to ensure that criminal elements do not gain positions of power within the country’s financial institutions. The very existence of this power in the law is likely to mandate against the need to actually exercise it. This is because persons with clearly undesirable records will know that they “need not ap-ply” because they will be disqualified on fit and proper grounds. ICP 7 on suitability of persons addresses fit and proper requirements more generally, while several of the essential criteria under ICP 15 on enforcement and sanctions describe remedies that should be available to deal with problems in this area.

3. IAIS (2000) describes fit and proper principles and how supervisors may apply them to individuals and corporations. Australian Prudential Regulation Authority (2004) explains how fit and proper requirements should be applied to pension trustees in Australia. The site also presents other material and information describing how the fit and proper requirements should be applied in that country. See also Risk Institute (n.d.).

Integrity

Basicallyitisallaboutpeople.Nosuper-

visorysystemwillproducegoodresultsif

theindustryincludesunscrupulousper-

sonswholackintegrityandarespectfor

thelaw.

ICP 14: Preventive and Corrective Measures of the Supervisor

11

power to obtain well-designed annual supervisory Filings and supplementary Filings

Supervisors cannot assess the financial positions of insurers nor make well-considered supervisory decisions if they do not have timely, accurate, and meaningful information from the supervised insurers. In addition to complete audited financial statements and their corresponding notes, the information package that companies must submit to the supervisory authority should be sufficiently complete to enable calculation of all the standard early warning ratios and the company’s solvency position. Nonfinan-cial material, such as information about the company’s reinsurance arrangements, shareholders and related parties, off-bal-ance-sheet items, and number of staff, is also invaluable for supervisory purposes and should be part of the formal reporting requirements. ICP 12 on reporting to supervisors and offsite monitoring provides fur-ther guidance on supervisory information requirements.

Supervisors normally require a major filing on an annual basis as well as supple-mentary filings during the year. In today’s world of electronic information and comput-erized systems within companies, there should be no compelling reason why the filings should not be submitted to the supervisor within 90 days of the end of the period to which they pertain. Some jurisdictions provide a slightly longer period to professional reinsurers because they have to obtain some of their information from their client in-surers. Remember, insurance company management also needs timely and accurate information to guide the company’s decisionmaking.

In addition to the power to obtain periodic information, the supervisor should also have the legal power to impose more frequent reporting and to revise the content of reporting when particular risks need to be monitored.

It is in this sense that financial reporting requirements often comprise an impor-tant part of a program of preventive and corrective measures. When the supervisor becomes aware of heightened areas of risk, in addition to any other measures that may be taken, it is often considered prudent to require more frequent reporting, often with more detailed information being provided about the area of concern.

For example, suppose that a general insurance company has allowed its investment portfolio to become considerably overexposed to investments in high-risk, speculative common stock investments, many of which are not listed on any stock exchange. Such assets would be a poor match for short-term liabilities, high-liquidity needs, and vola-tile underwriting results, all of which are typically associated with a general insurer’s underlying policy liabilities. The company may have promised the supervisor that most of these investments will be disposed of in the near future. In such a case, the supervisor may want to require, in addition to the normal statutory filings, detailed monthly infor-mation with regard to the investment portfolio so that the issue of high investment risk

Supervisory Assessments

Supervisoryassessmentsanddecision-

makingmustbebasedonaccurateand

timelyinformation.

Insurance Supervision Core Curriculum

1�

can be monitored closely. If improvements do not take place fast enough, the supervisor may require additional measures.

Over the last few years, a growing number of supervisory agencies have found it beneficial to supplement historical financial information with information based on financial modeling, often referred to as stress testing or dynamic capital adequacy test-ing. One weakness of pure financial data is that they can only reflect what happened in the past. However, by using actuarially sound stochastic models (models that can incorporate many possible outcomes on a probabilistic basis), analysts can forecast a company’s future solvency position. Initially, this approach required each company to develop a model that corresponded to its unique mix of product characteristics and, by extension, to possess either a highly sophisticated in-house actuarial group or to have access to significant consulting resources. Over the last few years, however, generic soft-ware has become widely available that permits models to be developed on a much more cost-effective basis.

Thus stress testing is becoming more accepted as a powerful tool, not only as a pre-ventive measure for the supervisor but, even more important, as a way for management and boards of directors to gain considerable insight regarding the impact on future solvency of various economic and business scenarios.

power to carry out onsite inspections

The onsite inspection is a fundamental requirement for supervisors. Onsite inspectors are the eyes and ears of the supervisory agency. Financial information is crucial for the supervisor, but it represents a look into the past. Except when used as a basis for model-ing, at best it shows what was happening during the period in question. By comparison, the onsite inspection produces a direct assessment by staff members of what is hap-pening in the company at the pres-ent time. Also very important, it enables inspectors to discuss with senior management their plans for the coming periods and to consid-er the amount of risk that the com-pany may be exposed to in these future periods. For example, a vigorous expansion plan would alert the supervisor to a possible need for heightened monitoring of the insurer in the upcoming periods and for a careful examination of the adequacy of the company’s internal financial controls, including underwriting, claims handling, and accounting.

The very fact that onsite inspections are going to take place serves as a preventive measure because, when people understand that their activities are going to be subject to onsite review, they tend to work hard on what they know will be of interest to the in-spectors. In addition, by identifying weaknesses and bringing them to management’s at-

Onsite Inspections

Onsiteinspectorsaretheeyesandears

ofthesupervisoryagency.

ICP 14: Preventive and Corrective Measures of the Supervisor

1�

tention, onsite inspections encourage management to take direct preventive measures. Although not a corrective measure per se, onsite inspections typically give rise to cor-rective measures that are instituted in response to specific problems noted during the onsite work.

An important trend in recent years is for supervisors to adopt what is generally referred to as risk-based supervision.4 Risk-based supervision monitors areas of risk in insurers and focuses supervisory resources on the higher-risk companies, aiming to re-duce risk in cases where it exceeds prudent levels. The supervisor considers that one of the main responsibilities of senior management and the board is to manage and mitigate risk by means of internal policies and procedures and high standards of corporate gover-nance. The supervisor uses agreed techniques and measures to assess risk in a consistent manner across companies and over time. The methods of assessing risk must be fully transparent so that the insurers can be satisfied that they are addressing the proper ar-eas of their operations. Risk-based supervision relies on both preventive and corrective measures to reduce risks. Even when a problem has materialized, one may still think in terms of risk reduction in the sense that measures will be applied in order to reduce the risk of continued deterioration.

A risk-based supervisor is always evaluating the insurer in terms of the risk in-herent in the various activities being carried out and the systems in place to control and mitigate those risks. This approach contrasts with the more traditional approach of having onsite inspectors verify data and check for compliance, primarily as a means of finding problems.

It may be more efficient and effective to prevent problems from occurring—by reducing risk before it reaches critical levels—than to attempt to fix problems after they occur. In other words, in some situations, it may be more efficient to use a risk-based approach rather than a more traditional compliance-based approach. A similar issue

4. Sparrow (2000) discusses the evolving concept of risk-based supervision and the need for the supervisor to have sufficient discretion to craft specific solutions to unique problems. Moore (1995) offers a more general look at management of orga-nizations in the public sector and techniques for creating value. Based on analysis of actual situations, the Committee of the Conference of Insurance Supervisory Services (2002) describes the risks facing insurance firms in the European Union and evaluates how supervisors might respond to them.

Answer the questions with reference to the information in case study 2. If you are working with others on this module, develop answers through discus-sion and cooperative work methods.

1. IsthesituationofABCLifeInsuranceCompanyhighrisk,mediumrisk,orlowrisk?

2. Whatarethemainrisks?

3. Deviseasupervisorystrategyhighlightingthemainpreventiveandcorrectivemeasuresthatyoumightinitiate.

Q5

Insurance Supervision Core Curriculum

14

arises in public health care, where measures to keep the population healthy are thought to be more cost-efficient than medical assistance after the individual becomes sick.

There are many specific situations where increased frequency and scope of onsite inspection provide the supervisor with better intelligence on emerging risks and the additional steps that may need to be taken to ensure that they do not become unman-ageable (see case study 2).

Priortocommencinganonsiteinspection,

thesupervisoralwaysmeetswiththeinde-

pendentauditoroftheinsurertodiscuss

thecompany’ssituation,anyissuesthat

mayhavebeenraisedwiththecompany,

andanyoutstandingconcernsthatthe

auditormayhave.Membersoftheinspec-

tionteamalsoreviewtheauditor’sworking

papersinordertounderstandtheareas

offocus,theteststhathavebeencarried

out,andsoon.Thisnotonlyprovidesthe

inspectionteamwithmanyusefulinsights

intothecompany’sinternalcontrolsys-

temsandotheraspectsofitsfinancialre-

portingsystembutalsoenablestheteam

toavoidduplicationofworkthathasbeen

carriedoutbytheauditor.

AspartoftheauditreviewofABCLifeIn-

suranceCompany,theinspectorreviews

themanagementletter(thelettertheau-

ditorsendstothecompanysummarizing

issuesfortheinsurer’sattentionpriorto

signingoffontheaudit).Thelettercon-

tainsthefollowingparagraph:

Wenotethatduringtheyearthecom-

panymadealoanof$25milliontoa

manufacturingcompanythatiscon-

trolledbythemajorshareholderofyour

company.Wehavebeenunabletofind

anydocumentationtosupporttheloan

ortorecordthedetailsofanycollateral

thatmayhavebeentakenassecurity.

Inviewofthefactthattheloanamount

isconsiderablyinexcessofthecompa-

ny’sequitybase,wewouldliketohave

yourassurance,priortooursigning

offonthefinancials,thatappropriate

documentationwillbeprovidedforthe

filesassoonascanconvenientlybear-

ranged.

Thereviewersareunabletofindanyevi-

denceintheauditor’sfiletoindicatethat

thecompanyhasprovidedtherequested

documentation.

Theauditfirmistheauditorforallthecom-

paniesintheshareholdergroup,including

ABCLifeandthemanufacturingfirmre-

ferredtointheletter.

Duringtheonsiteinspection,italsobe-

comesapparentthatthecompanyhas

recentlyretainedanewactuarywhohas

discernedthatthebasisonwhichthepre-

vioustechnicalprovisionswereestablished

wasundulyconservativeandthat,under

differentassumptions,theamountofsuch

provisionswouldbereducedbyapproxi-

mately20percent,orcloseto$15million.

Theyear-endfinancialstatementsreflect

thenewassumptionsbutdonotaddress

thechangeinactuarialbasesyearover

year.

Case Study 2

ICP 14: Preventive and Corrective Measures of the Supervisor

1�

Increased frequency and intensity of the onsite inspection work can also be a preventive or corrective measure. For example, where a company’s financial posi-tion has reached a critically depleted level or where there is evidence of fraudulent behavior on the part of the insurer, supervisors may place inspectors on the company premises on a more or less continuous basis. These inspectors monitor developments closely in a particular area, and their presence encourages appropriate actions by management.

More information regarding onsite inspections can be found in the module on ICP 13.

power to inspect business plans

The insurance law should provide the supervisor with the authority to obtain, on a timely basis, any information required to assess the financial position and risk profile of the insurer and to assess the company’s treatment of policyholders. A particularly important document in this regard is the business plan of the insurer, which is a crucial piece of information for the supervisor. First of all, it enables the supervisor to assess the risk inherent in the company’s plans for the coming periods. For example, if the busi-ness plan indicates that the company is go-ing to develop a complex new product and also commence writing business in three new jurisdictions within the coming year, then the upcoming period is judged to be of inherently higher risk than normal. The supervisor will therefore look for internal controls, budgets, management resources, board oversight, and other factors that the company should have in place to mitigate and manage the risks involved in this business plan.

The insurer’s business plan also enables the supervisor to assess the ability of a company to deal with issues that have been raised. For example, suppose that the most recent financial filing shows that the company has been sustaining unacceptably poor underwriting results. An onsite inspection has confirmed that the company’s results in virtually all of its lines of business are significantly more unprofitable than those of companies in its peer group. In a case like this, a useful supervisory tactic is to request the company to file a business plan demonstrating the steps it will take, and over what period of time, to improve its underwriting experience. The business plan then pro-vides a base case against which the company’s performance can be monitored. Should it become evident that the plan is not bringing about the required improvement, the supervisor can follow up with the company to discuss what changes are required.

Another benefit of this approach is that the business plan itself can provide con-siderable insight into the depth of management within the company. An unrealistic,

Assessing Viability

Ultimately,supervisionisaboutunder-

standingthesupervisedcompaniesand

assessingtheirviability.

Insurance Supervision Core Curriculum

1�

poorly thought out plan says much about the management of the company and alerts the supervisor to additional risk, which can lead to closer monitoring and more active intervention.

A supervisory requirement to file revised or more detailed business plans can be an important corrective or preventive measure.

power to set minimum capital requirements and minimum solvency requirements

Holding a license to transact the business of insurance is a privilege, not a right. When consumers pay their premiums, they are in effect paying for the protection afforded by the financial strength of the insurer and its reinsurers. It is reasonable to require every insurer to maintain capital and surplus at all times at least equal to an agreed level.5 Because insured risks are not proportional to the level of development

of the local economy, the minimum ac-ceptable level of capital and surplus tends to be roughly comparable from one juris-diction to another; typically, it is not less than about $3 million. Often a somewhat higher minimum is mandated for life in-surance compared to general insurance

because the start-up expenses are usually higher for a life insurer than for a general insurer and because the profits on life insurance products, even for established insur-ers, often do not emerge until several years after policies are issued.

Minimum capital requirements are important when a company is commencing busi-ness, but as the company grows and its liability base becomes much larger, the minimum capital requirement has increasingly less relevance. For example, when a company has been operating for only a short period of time, an equity base of $3 million provides a sub-stantial margin of safety for the small number of policyholders, who may represent only a few hundred thousand dollars of policy liabilities. However, when the same company has grown to have thousands of policyholders and has technical provisions of, say, $100 mil-lion, an equity base of only $3 million provides virtually no margin of comfort.

Therefore, it is crucial to have a minimum solvency requirement that is proportional to the liability base of the company. There are many ways of accomplishing this goal, but every company must maintain a margin of assets over liabilities that will be sufficient to protect policyholders and provide enough time for the supervisor and management to implement measures and steer the company back onto a safe course before an actual insolvency results. ICP 23 on capital adequacy and solvency, and related IAIS papers, provide more information on these issues.

5. Das, Davies, and Podpiera (2003) examine the causes of financial failures in insurance companies and conclude that ad-equate solvency requirements are the critical factor. The paper then considers the merits of risk-based capital requirements versus so-called “fixed-ratio” approaches to minimum solvency.

Equity Base

Theonlythinganinsurerhastosellisthe

securityofferedbyitsequitybase.

ICP 14: Preventive and Corrective Measures of the Supervisor

1�

In the context of preventive and corrective measures, a helpful supervisory power is the legal authority to prescribe higher solvency margins or higher initial capital require-ments in particular cases. Some types of business are inherently more risky than other types (for example, financial guarantee insurance and the insuring of commercial mort-gages against default), and if a company begins to focus on a particular high-risk type of coverage, it may be appropriate to require additional solvency margins. In the case of a

The following questions are intended to stimulate discussion. If you are work-ing with others on this module, develop the answers through discussion and cooperative work methods.

1. Basicallyitisallaboutpeople.Nosupervisorysystemwillproducegoodresultsiftheindustryincludesunscrupulouspersonswholackintegrityandrespectforthelaw.Whatcanthesupervisordotokeepbadpeopleoutofthebusiness?

2. Supervisoryassessmentsanddecisionmakingmustbebasedonaccurateandtimelyinformation.Discusssomeofthesupervisoryproblemsthatwilloccurwhensuchinformationisnotavailable.

3. Notallsupervisoryagenciescarryoutonsiteinspections.Whydoyouthinkthisisthecase?Whatdoyouseeasthevulnerabilitiesforsuchasupervisoryagency?

4. Ultimately,supervisionisaboutunderstandingthesupervisedcompaniesandassessingtheirviability.Inthiscontext,whatdoyouseeasvalueaddedinreviewinginsurerbusinessplans?

5. Ithasbeensaidthattheonlythinganinsurerhastosellisthesecurityofferedbyitsequitybase.Discusswhyyouwouldeitheragreeordisagreewiththisstatement.Whataretheimplicationsofthisstatementforminimumcapitalrequirementsandminimumsolvencyrequirements?

6. Thewithdrawalofacompany’slicenseissometimesputoffanddeferreduntil,whenitfinallyoccurs,the“centsonthedollar”figureavailabletopolicyholdershasbecomequitesmall.Whataresomeofthereasonsforthisphenomenon?Doyouthinktheexistenceofaninsuranceconsumerprotectionplan(similartodepositinsurance)wouldhaveanimpactinthisregard?

7. Ultimately,managersandshareholdershavetobelievethattheywillbepunishediftheydonotfollowthelaw.Discussthecurrentsanctionsandpenaltiesprovidedforinyourlegislation.Doyoubelievetheyhavetherequireddeterrenteffect?

Q6

Insurance Supervision Core Curriculum

1�

company that chooses to operate at a higher level of risk, perhaps as a conscious decision not to mitigate or manage certain aspects of risk, it is reasonable for the supervisor to require a higher margin of solvency than for other companies with lower risk profiles. Many countries are now adopting so-called risk-based capital requirements, which make this sort of adjustment on a formula basis.

The main preventive or corrective impact of minimum capital requirements and solvency requirements is that they allow the supervisor to mandate the injection of ad-ditional capital when a company is not complying with the provisions.

power to withdraw a company’s license

Withdrawal of a company’s license is the ultimate corrective measure and is only in-voked if the insurer is deemed unable to meet its obligations to the public. While the threat of license withdrawal may have some deterrent effect, this measure is only adopted after the time for constructive action has expired.

As highlighted by ICP 14, es-sential criterion b, it is beneficial to have a range of preventive and corrective measures that can be ap-plied in an escalating manner as a situation becomes more serious, with withdrawal of a company’s license being at the end of the line. These types of measures are discussed in the section on supplementary powers.

power to impose sanctions and penalties

An important form of supervisory intervention involves the imposition of penalties, either directly by the supervisor or through the court system, for failure to comply with provisions of the law. It is critically important that penalties be sufficient to motivate compliance and that they be imposed when there are significant instances of noncom-pliance. ICP 15 on enforcement and sanctions addresses these is-sues more fully.

There is no room within the financial system for rogue players who are inclined to ignore laws that have been carefully designed

License Withdrawal

Thewithdrawalofacompany’slicense

issometimesputoffanddeferreduntil,

whenitfinallyoccurs,the“centsonthe

dollar”figureavailabletopolicyholders

hasbecomequitesmall.

Punishment

Ultimately,managersandshareholders

havetobelievetheywillbepunishedif

theydonotfollowthelaw.

ICP 14: Preventive and Corrective Measures of the Supervisor

1�

to protect the public interest. Substantial fines and even the possibility of jail terms, cutting through the corporate veil to directors where they have been personally neg-ligent (or worse) in carrying out their fiduciary responsibilities, should be the order of the day. Other components of the core curriculum deal with corporate governance. Suffice it to say here that, in today’s world, directors and senior managers should be expected to do everything reasonably possible to ensure that their institutions oper-ate in accordance with sound business and financial practices. When they do not, they should be sanctioned in a meaningful way.

The imposition of significant numbers of financial and other penalties that are minor in nature and apply to relatively small transgressions of the law generally is not an effective method of supervision. In this type of situation, the supervisor spends too much time levying and collecting fines, most of which will have little or no impact on the behavior of the insurers because the amounts of the fines are tiny relative to their resources. In addition, most of the so-called violations do not materially threaten the public interest. Later on, this module outlines an effective supervisory approach for dealing with a company that is guilty of many relatively minor instances of noncom-pliance.

Supplementary powers

Supplementary powers are not always part of the supervisory regime, but they are desir-able because they enable the supervisor to draw on a broader range of preventive and corrective measures for dealing with the wide variety of situations that may arise.

imposition oF license conditions and requirements For undertakings

When financial problems are developing or risks are increasing and the reasons for the difficulties can be accurately diagnosed, the supervisor might, as an initial response, re-quire an insurer to file a business plan showing how it is going to change its operations so as to remedy the identified problems. Sometimes, however, a business plan is poorly thought out or, if well thought out, is not followed, and in these cases the situation will continue to deteriorate.

In such instances, a powerful supervisory tool is the power to impose conditions on the insurer’s license or require it to provide a written undertaking with regard to making changes in its operations. Overly rapid expansion is a common cause of fi-nancial difficulties and provides a good example of where this power may be used to advantage.

A well-accepted international insurance ratio for general insurers is the ratio of net premiums written to capital and surplus, often known as the risk ratio. It is generally ac-cepted that this ratio should not exceed about 2.5 to 1, and it can be shown mathemati-

Insurance Supervision Core Curriculum

�0

cally why this is so. Therefore, if an insurer has an equity base of $10 million, then its volume of net premiums written should not exceed about $25 million. If, however, the insurer writes net premiums at a rate of $35 million a year, the supervisor could impose a license condition (or require a written undertaking) to the effect that, in the upcoming 12 months, net premiums cannot exceed $25 million.

The power can also be used with regard to other aspects of insurer operations. For example, the insurer could be prevented from transacting business in new jurisdic-tions without first obtaining supervisory approval. Or a maximum volume could be prescribed for a particular line of business or product. For example, this power has been used to prevent an insurer from investing in any securities being promoted by an invest-ment brokerage firm that was a member of the same corporate group as the insurer.

Where a specific operational aspect or combination of aspects is deemed respon-sible for an unacceptable level of risk in an insurer, and where the company has not demonstrated a willingness to correct the problem, a license condition or undertaking may lower risk to more appropriate levels.

To reduce the possibility that the insurer will not follow the license condition or undertaking, a provision in the law should state that noncompliance with a license con-dition or undertaking constitutes noncompliance with the insurance law. ICP 15 calls for strong penalties for failure to comply with the law.

special audits with power For supervisor to require costs to be covered by the

insurer

Even in developed countries, the insurance supervisor rarely has a budget sufficient to draw on the virtually unlimited range of professional resources available to an insur-ance company. When supervisory staff members raise what they believe to be a serious issue, the insurer not only may use its own experts but also may hire professional ac-counting, actuarial, legal, and other resources to challenge the supervisor’s findings.

This is not an undesirable situation. On the one hand, the supervisor’s assessment may not be correct, and the insurer’s staff and professional consultants may be in a position to demonstrate this fact. On the other hand, the supervisory assessment may be correct, but officers of the supervisory agency may not have the same degree of cred-ibility as the high-profile professionals the insurer is able to retain, particularly if the evidence has to be presented in a court of law. In addition, before moving forward, the supervisor may want to have an outside professional opinion to confirm the views of his or her officers with regard to the issue in question.

To level the playing field regarding this disparity in resources, a useful legal power is for the supervisor to be able to retain any outside experts needed to carry out special audits, actuarial reviews, or other assessments and to be able to require the insurer in-volved to bear the expense. This does not mean that the insurer will always be required to bear the costs; it does mean that the supervisor can require this to be done, de-

ICP 14: Preventive and Corrective Measures of the Supervisor

�1

pending on the circumstances. This power is especially important in emerging-market countries, where the disparity between supervisory resources and insurance company resources may be particularly significant.

power to appraise assets and to adjust liabilities

Major issues for supervisors often involve the deliberate overvaluation of assets and the undervaluation of liabilities. Real estate is an especially common asset valuation prob-lem as it is relatively easy for insurers to obtain inflated appraisals if they are willing to pay the required fee. On the liability side, the problem is with the technical provisions: for general insurers, it is the outstanding claims, and for life insurers, it is the actuarial liabilities.

It is desirable that the supervisor have the power to obtain professional evaluations of both assets and liabilities and to revalue those items as necessary. ICP 20, essential criterion e, states that the supervisory authority should be able to require technical pro-visions to be increased if they are not suffi-cient. An additional desirable power is the corresponding ability to revalue assets to reflect economic reality. In order to avoid lengthy negotiations with the insurer’s au-dit firm and others, a useful approach is to give the supervisor the authority to revalue items, as necessary, by adjusting the values that are used when calculating the company’s minimum solvency position under the in-surance law. In this way, the supervisor can adjust the basic calculation used to assess the financial health of the insurer without requiring that all the financial statements be restated (which affects the bonuses paid to executives, the figures that the auditor and board have signed off on in the financial statements, and so forth); it also does not re-quire the auditor to agree or disagree with the changes.

As with special audits, the supervisor should have the authority to bill the cost of any special valuations of assets or liabilities to the insurer involved.

limited time horizon For license

There are differing practices with regard to the renewal of licenses. Some jurisdictions prefer to issue an annual license and require renewal each year, typically with payment of a fee. Other jurisdictions favor the issuance of a license with no specific expiration date, although there may still be an annual license fee that is payable to the govern-ment.

Balance Sheet

Assessingthebalancesheetofaninsurer

isacriticaldimensionofprotectingthe

public.

Insurance Supervision Core Curriculum

��

Issuing a “license outstanding until revoked” may be the more efficient approach. Supervisory resources are always scarce, and an annual renewal of all licenses can be relatively time-consuming and labor intensive. These resources can generally be better employed in other supervisory activities. If the supervisory regime is well designed and carried out, risk assessment and appropriate action should be continuous activities rather than concentrated into a particular “renewal period” each year. (An annual re-newal is not in keeping with a risk-based approach because it involves the expenditure of supervisory resources across the board rather than on the basis of risk.)

But whether the license is annual or indefinite, the supervisor should have the power to insert, at any time, a specific expiry date in it. This can be particularly useful when an insurer requires additional equity to support its operations. In this situation, it is common for the insurer to report to the supervisor that an investor is “close” to making a significant investment. Time passes, but the investor continues to carry out due diligence without making an investment. Then the investor dis-appears, but a new potential inves-tor arrives on the scene, and again this person is reportedly “close” to making a significant investment. This process can continue over an extended period. Naturally, the su-pervisor does not want to take ac-tion that will scare away a potential investor, but the company’s posi-tion continues to deteriorate, and no new funds are being injected into the company.

In this type of situation, it can often be helpful for the supervisor to be able to issue a new license, which, for example, expires 30 days from the date of issue. This emphasizes the supervisor’s position that the matter requires urgent action and that, if additional equity is not forthcoming, the company will have to cease doing business. The knowledge that either the money must be in the company within 30 days or the company’s license will expire tends to “clarify the minds” of shareholders and strongly underlines the need to get serious about putting in the required equity.

The deadline for an expiring license also disciplines the supervisor. In too many instances, supervisors, realizing the large amount of work, pressure, and resources that may arise from a decision to withdraw an insurer’s license, put off making a decision even though the situation is continuing to deteriorate. Much time can elapse with no action being taken. Ultimately, something must be done, and the policyholders may be much worse off than they would be if action had been initiated at an earlier date.

Of course, the law should also enable the supervisor to extend a license for ad-ditional periods in case the company really is about to close a deal with new investors just when the prescribed period is about to expire. However, any extensions should be for short periods of time and rarely repeated; otherwise the provision loses its power to motivate shareholder action.

Licenses

Tellingacompanythatitslicensewillbe

withdrawnifitdoesnotmeetcertaincon-

ditionsmaygivealessemphaticmessage

thanissuinganewlicensethatwillexpire

onaprescribeddateiftheconditions

havenotbeenmet.

ICP 14: Preventive and Corrective Measures of the Supervisor

��

power to conduct a public hearing into an insurer’s activities

The power to conduct a public hearing into an insurer’s activities is not commonly found in insurance laws, but in some cases it has been beneficial in safeguarding the position of policyholders.

Basically, the law merely indicates that, where the supervisor considers it to be in the public interest to do so, the supervisor may arrange to hold a public hearing into any aspect of an insurer’s affairs. Representatives of the insurer, expert witnesses, and others could be called to testify before the insurance superintendent or commis-sioner in a public forum and under oath with regard to any aspect of the insurer’s operations.

As shown in case study 3, the ability to call a public hearing can be a powerful tool in persuading shareholders to “do the right thing” in cases where the company is technically in compliance with the law but clearly is violating its spirit.

power to require a deposit From insurers

In some situations, it can be beneficial for the supervisor to have the authority to require a deposit from an insurer, in an amount to be determined by the supervisor. Again based on experience, as seen in case study 4, if the supervisor believes there is a danger that securities could disappear from an insurer, as a result of theft or other illegal activi-ties, the ability to require the insurer to post a substantial deposit can help to protect the interests of policyholders.

As with the power to hold a public hearing, this power will not be required often, but it can be used effectively when needed.

Requiring every insurer to post a deposit with the supervisor as a condition of holding a license may not be the most efficient or effective means of proceeding. On the one hand, the amounts of such deposits are not likely to be of major benefit to poli-cyholders in the event of the insolvency of the insurer because the liability base of an insurer will normally be much greater than the amount of the deposit posted. On the other hand, the supervisory agency is likely to expend scarce resources (administering the deposits, accounting for the deposits, and so on) for a purpose that may not signifi-cantly help it to meet supervisory objectives.

Getting Around the Law

Somecompaniesareverygoodat“get-

tingaroundthelaw.”

Insurance Supervision Core Curriculum

�4

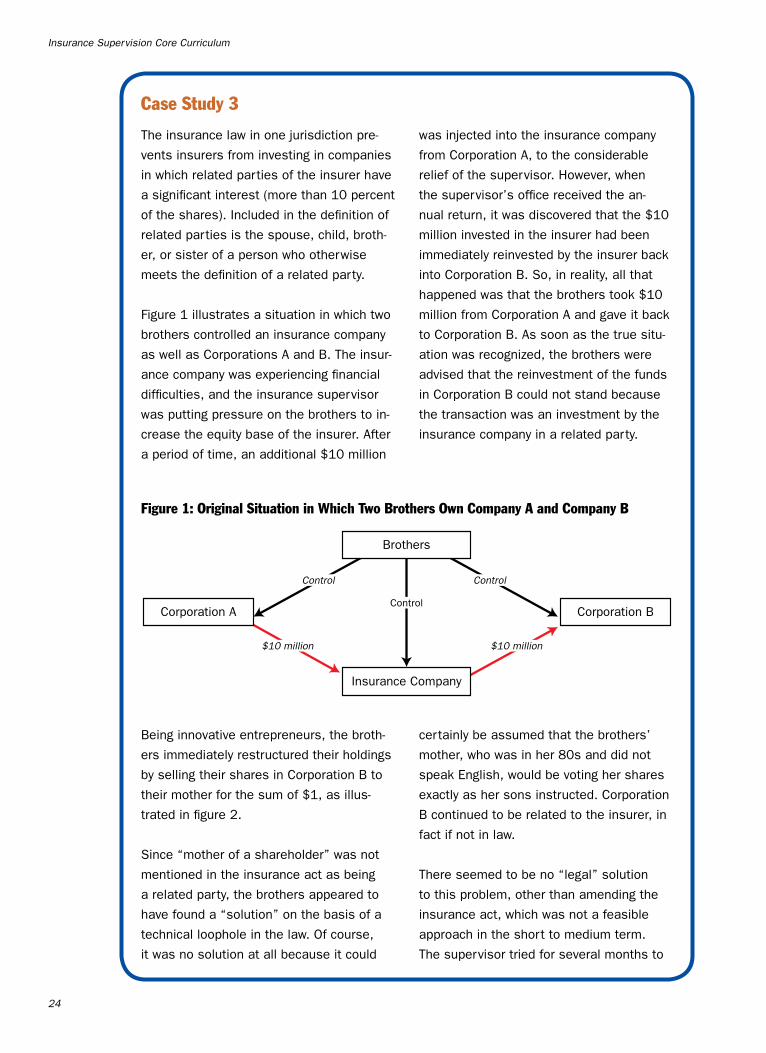

Theinsurancelawinonejurisdictionpre-

ventsinsurersfrominvestingincompanies

inwhichrelatedpartiesoftheinsurerhave

asignificantinterest(morethan10percent

oftheshares).Includedinthedefinitionof

relatedpartiesisthespouse,child,broth-

er,orsisterofapersonwhootherwise

meetsthedefinitionofarelatedparty.

Figure1illustratesasituationinwhichtwo

brotherscontrolledaninsurancecompany

aswellasCorporationsAandB.Theinsur-

ancecompanywasexperiencingfinancial

difficulties,andtheinsurancesupervisor

wasputtingpressureonthebrotherstoin-

creasetheequitybaseoftheinsurer.After

aperiodoftime,anadditional$10million

wasinjectedintotheinsurancecompany

fromCorporationA,totheconsiderable

reliefofthesupervisor.However,when

thesupervisor’sofficereceivedthean-

nualreturn,itwasdiscoveredthatthe$10

millioninvestedintheinsurerhadbeen

immediatelyreinvestedbytheinsurerback

intoCorporationB.So,inreality,allthat

happenedwasthatthebrotherstook$10

millionfromCorporationAandgaveitback

toCorporationB.Assoonasthetruesitu-

ationwasrecognized,thebrotherswere

advisedthatthereinvestmentofthefunds

inCorporationBcouldnotstandbecause

thetransactionwasaninvestmentbythe

insurancecompanyinarelatedparty.

Case Study 3

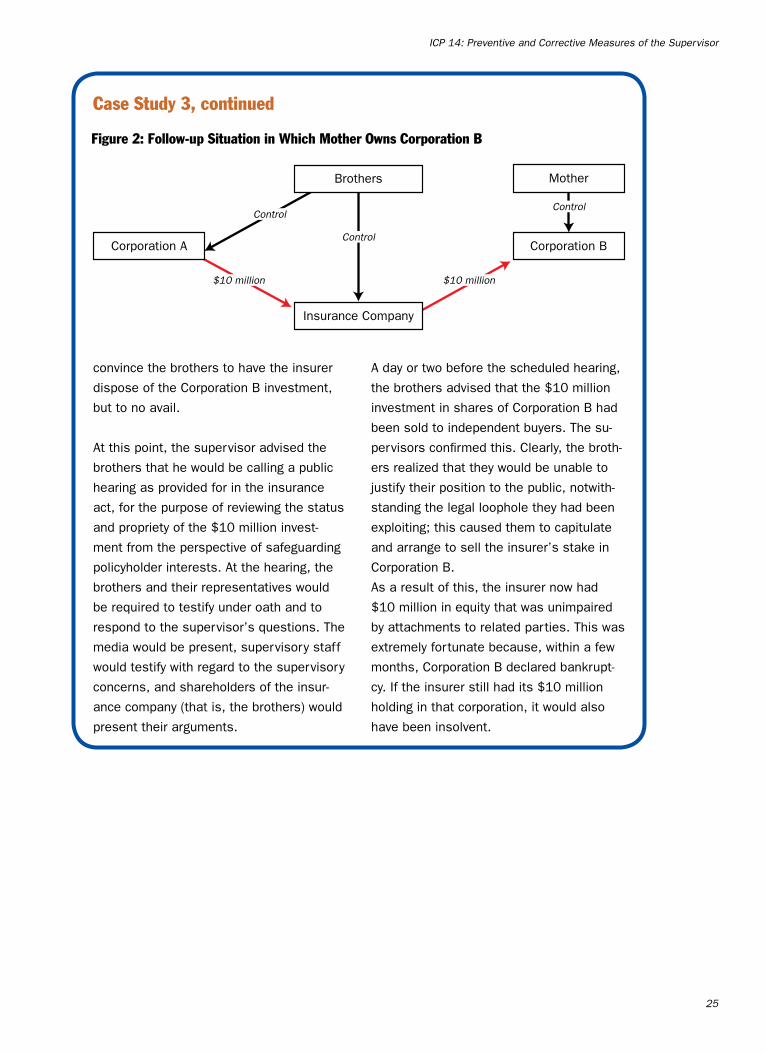

Beinginnovativeentrepreneurs,thebroth-

ersimmediatelyrestructuredtheirholdings

bysellingtheirsharesinCorporationBto

theirmotherforthesumof$1,asillus-

tratedinfigure2.

Since“motherofashareholder”wasnot

mentionedintheinsuranceactasbeing

arelatedparty,thebrothersappearedto

havefounda“solution”onthebasisofa

technicalloopholeinthelaw.Ofcourse,

itwasnosolutionatallbecauseitcould

certainlybeassumedthatthebrothers’

mother,whowasinher80sanddidnot

speakEnglish,wouldbevotinghershares

exactlyashersonsinstructed.Corporation

Bcontinuedtoberelatedtotheinsurer,in

factifnotinlaw.

Thereseemedtobeno“legal”solution

tothisproblem,otherthanamendingthe

insuranceact,whichwasnotafeasible

approachintheshorttomediumterm.

Thesupervisortriedforseveralmonthsto

Corporation B

Insurance Company

Brothers

Control

$10 million $10 million

Corporation A

Control

Control

Figure 1: Original Situation in Which Two Brothers Own Company A and Company B

ICP 14: Preventive and Corrective Measures of the Supervisor

��

convincethebrotherstohavetheinsurer

disposeoftheCorporationBinvestment,

buttonoavail.

Atthispoint,thesupervisoradvisedthe

brothersthathewouldbecallingapublic

hearingasprovidedforintheinsurance

act,forthepurposeofreviewingthestatus

andproprietyofthe$10millioninvest-

mentfromtheperspectiveofsafeguarding

policyholderinterests.Atthehearing,the

brothersandtheirrepresentativeswould

berequiredtotestifyunderoathandto

respondtothesupervisor’squestions.The

mediawouldbepresent,supervisorystaff

wouldtestifywithregardtothesupervisory

concerns,andshareholdersoftheinsur-

ancecompany(thatis,thebrothers)would

presenttheirarguments.

Adayortwobeforethescheduledhearing,

thebrothersadvisedthatthe$10million

investmentinsharesofCorporationBhad

beensoldtoindependentbuyers.Thesu-

pervisorsconfirmedthis.Clearly,thebroth-

ersrealizedthattheywouldbeunableto

justifytheirpositiontothepublic,notwith-

standingthelegalloopholetheyhadbeen

exploiting;thiscausedthemtocapitulate

andarrangetoselltheinsurer’sstakein

CorporationB.

Asaresultofthis,theinsurernowhad

$10millioninequitythatwasunimpaired

byattachmentstorelatedparties.Thiswas

extremelyfortunatebecause,withinafew

months,CorporationBdeclaredbankrupt-

cy.Iftheinsurerstillhadits$10million

holdinginthatcorporation,itwouldalso

havebeeninsolvent.

Case Study 3, continued

Control

Corporation B

Insurance Company

Brothers

Control

$10 million $10 million

Corporation AControl

Mother

Figure 2: Follow-up Situation in Which Mother Owns Corporation B

Insurance Supervision Core Curriculum

��

Thesupervisorhadevidencethatthechief

executiveofficer(CEO)ofaninsurerwas

stealingfromthecompany.Itwasgoing

totakesometimeforthesupervisorto

buildasufficientcaseagainsttheCEOfor

presentationinacourtoflaw.Inthemean-

time,thesupervisorwasabletorequire

theinsurertopostadepositofsecurities,

consistingofvirtuallyallthecompany’s

investments.Thedepositwasunderthe

controlofthesupervisor,soitcouldnotbe

misappropriatedbytheCEO.Thisaction

ensuredthat,whileevidencewasbeing