BASIC FINANCIAL RATIO ANALYSIS AND IMPLICATION · · 2016-11-23include the following types of...

85

1 BASIC FINANCIAL RATIO ANALYSIS AND IMPLICATION Dr. Eden Chow Hang Seng Management College 19 November 2016 © Hong Kong Institute of Certified Public Accountants, 2016. All rights reserved.

-

Upload

vuongkhanh -

Category

Documents

-

view

215 -

download

1

Transcript of BASIC FINANCIAL RATIO ANALYSIS AND IMPLICATION · · 2016-11-23include the following types of...

1

BASIC FINANCIAL RATIO

ANALYSIS AND IMPLICATION Dr. Eden Chow Hang Seng Management College 19 November 2016

© Hong Kong Institute of Certified Public Accountants, 2016. All rights reserved.

Annual reports as a communication tool

• Annual reports are the top sources of information for shareholders, lenders and potential investors etc.

• Annual reports provide information about the company from company visions, goals and strategies to financial information.

• Substance over form(實質重於形式) – Information users should make his / her financial decisions based on the substance of the annual reports, i.e. audited financial statements.

• Annual reports can be easily found in the internet.

2

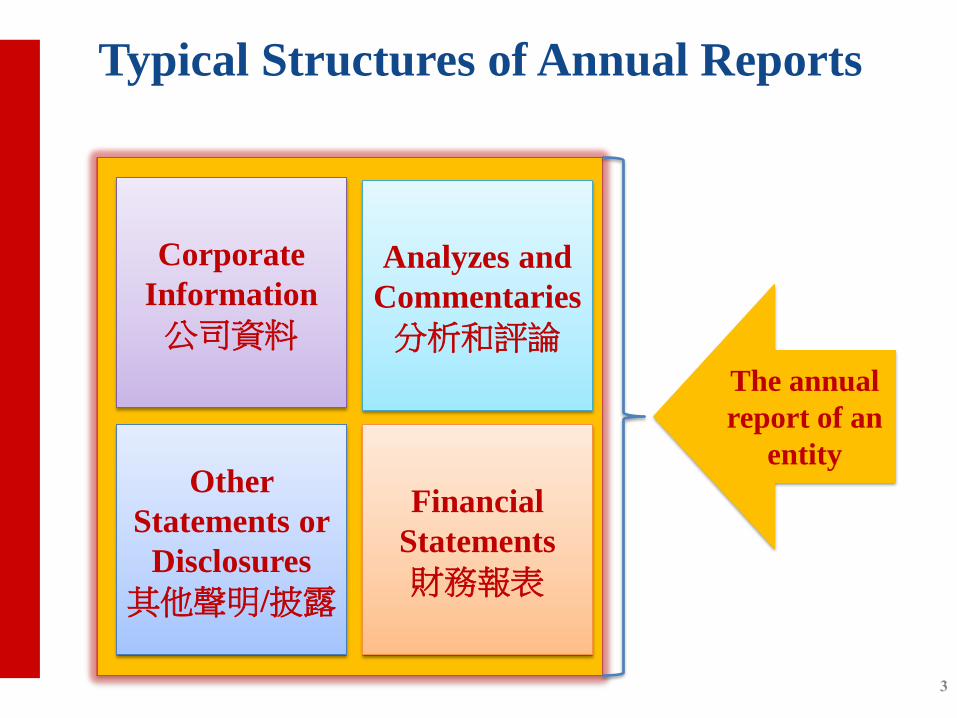

Typical Structures of Annual Reports

3

The annual

report of an

entity

Corporate

Information

公司資料

Analyzes and

Commentaries

分析和評論

Other

Statements or

Disclosures

其他聲明/披露

Financial

Statements

財務報表

Corporate Information

4

The following corporate information is

provided in an annual report:

• Short history of company

• Members of board of directors and

key management personnel

• Organization structure

• Awards and accolades

• Key markets and products

• Operating statistics and financial

highlights

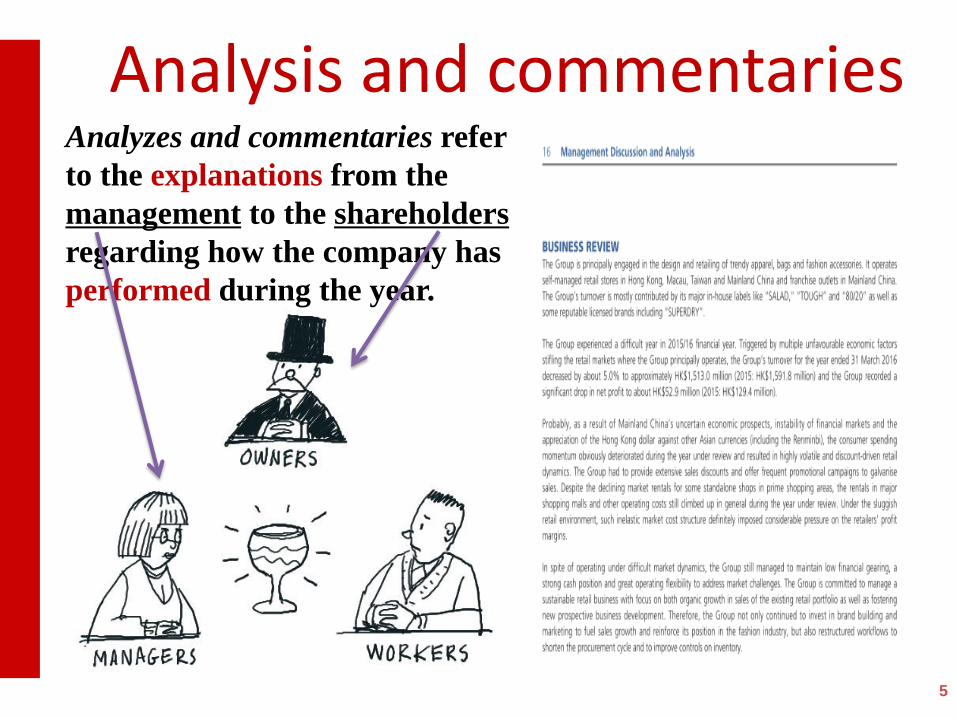

Analysis and commentaries

5

Analyzes and commentaries refer

to the explanations from the

management to the shareholders

regarding how the company has

performed during the year.

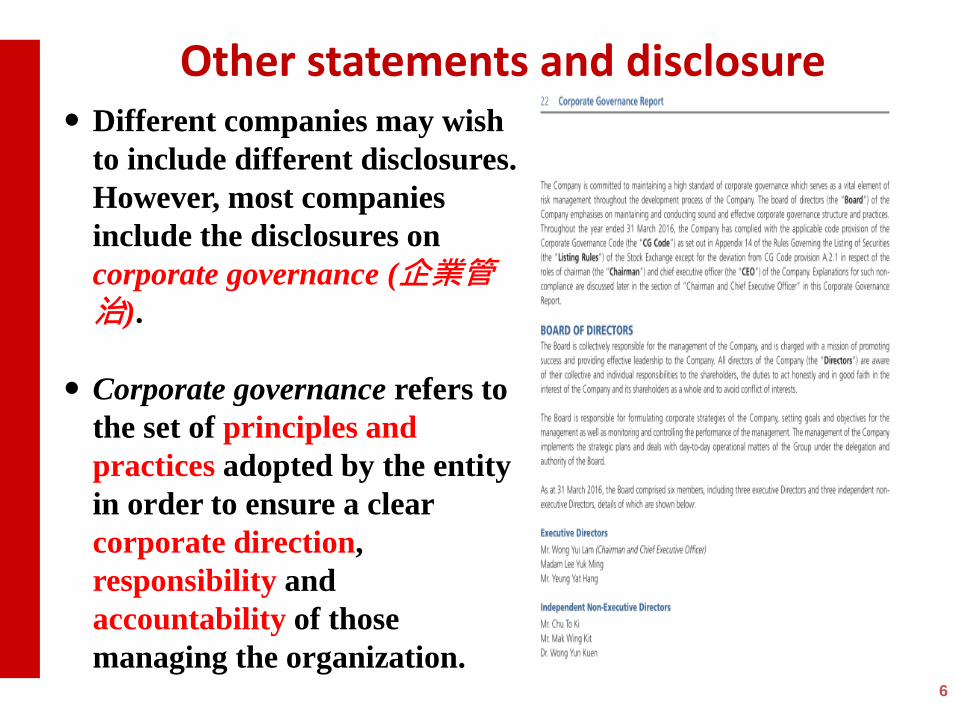

Other statements and disclosure

6

Different companies may wish

to include different disclosures.

However, most companies

include the disclosures on

corporate governance (企業管治).

Corporate governance refers to

the set of principles and

practices adopted by the entity

in order to ensure a clear

corporate direction,

responsibility and

accountability of those

managing the organization.

Financial Statements

It usually begins with the

acknowledgement ( 確 認 ) by

directors and management that they are

responsible for the financial statements.

It is then followed by the auditor’s report

(審計報告) and the full set of

financial statements.

7

8

Contents

• Financial Highlights

• Corporate Information

• Information for Inventors

• Chairman’s Statement

• Management Discussion and

Analysis

• Directors and Senior

Management

• Corporate Governance Report

• Report of the Directors

• Independent Auditors’ Report

• Audited Financial Statements

• Consolidated Statement of Profit

or Loss and Other

Comprehensive Income

• Consolidated Statement of

Financial Position

• Consolidated Statement of

Changes in Equity

• Consolidated Statement of Cash

Flows

• Notes to Financial Statements

• Five Year Financial Summary

9

COMPONENTS OF ANNUAL REPORT 企業年報的構成要素

• Chairman’s Statement 主席報告

• Management Discussion and

Analysis

管理層討論及分析

• Independent Auditor’s Report 獨立核數師報告

• Consolidated Financial

Statements

綜合財務報表

• Notes to the Consolidated

Financial statements

綜合財務報表附註

10

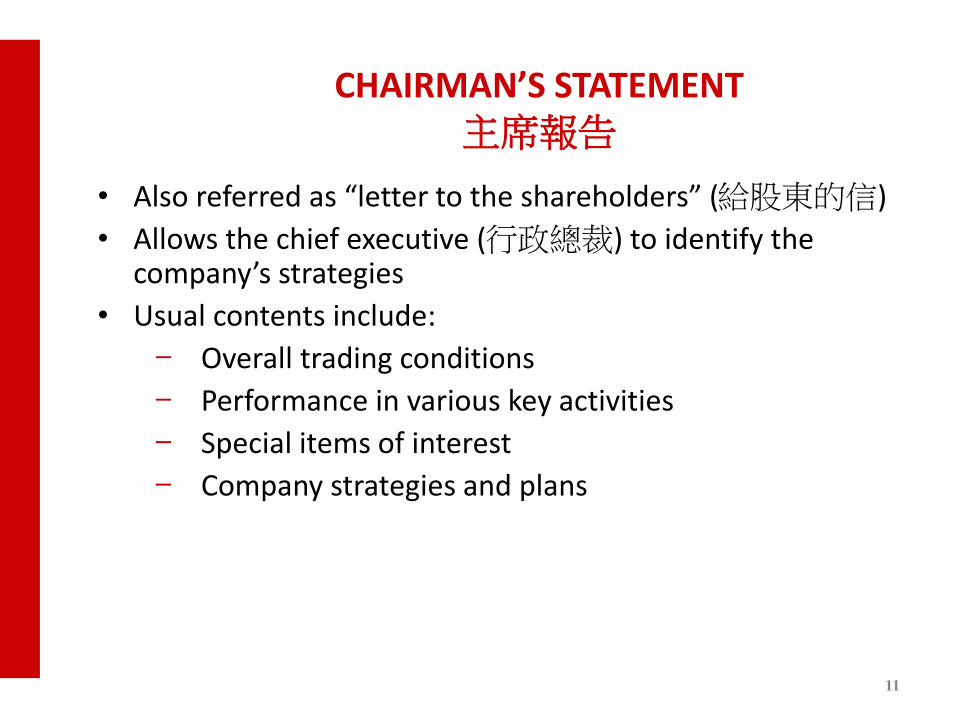

CHAIRMAN’S STATEMENT 主席報告

11

CHAIRMAN’S STATEMENT 主席報告

• Also referred as “letter to the shareholders” (給股東的信)

• Allows the chief executive (行政總裁) to identify the company’s strategies

• Usual contents include:

− Overall trading conditions

− Performance in various key activities

− Special items of interest

− Company strategies and plans

12

MANAGEMENT DISCUSSION AND ANALYSIS

管理層討論及分析

13

MANAGEMENT DISCUSSION AND ANALYSIS 管理層討論及分析

• One of the most important components of the annual report

• Discuss the organization's (組織) past performance

• Makes explicit (詳盡) how successful leadership has been at achieving the corporate strategies

• Points to the company’s future strategic focus

14

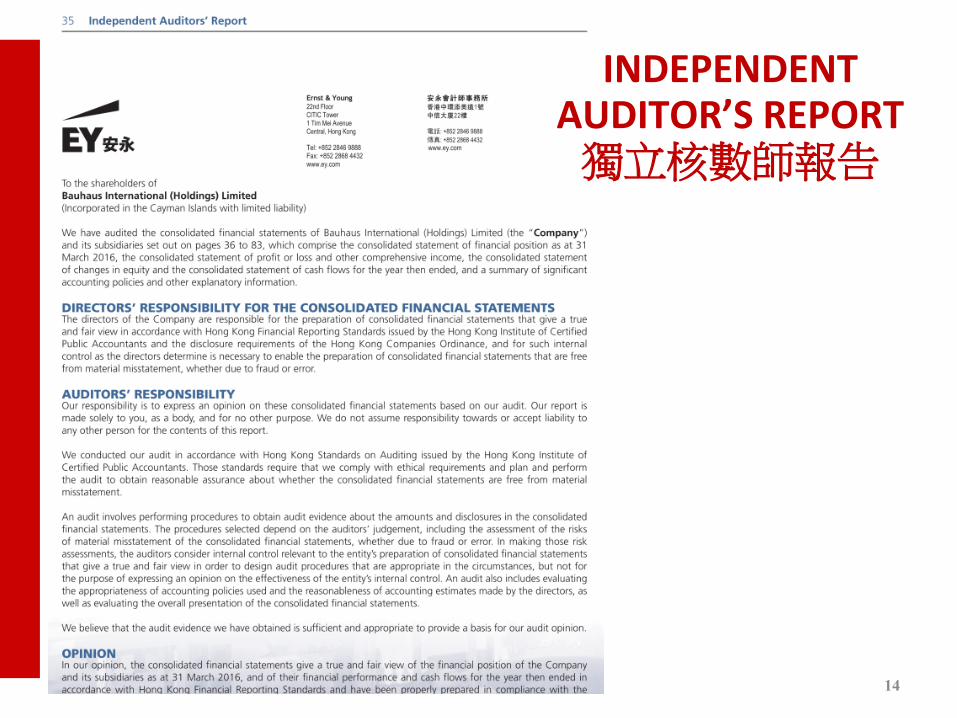

INDEPENDENT AUDITOR’S REPORT 獨立核數師報告

15

INDEPENDENT AUDITOR’S REPORT 獨立核數師報告

• New Companies Ordinance (新公司條例) Section 406

• Confirmation of Management Responsibility

• Declaration (聲明) of Process and Procedures

• Announcement of Audit Opinions (核數評價)

• Clean/ Unqualified Report (無保留意見)

• Qualified Report (保留意見)

• Adverse Opinion (否定意見)

• Disclaimer of Opinion (不發表意見)

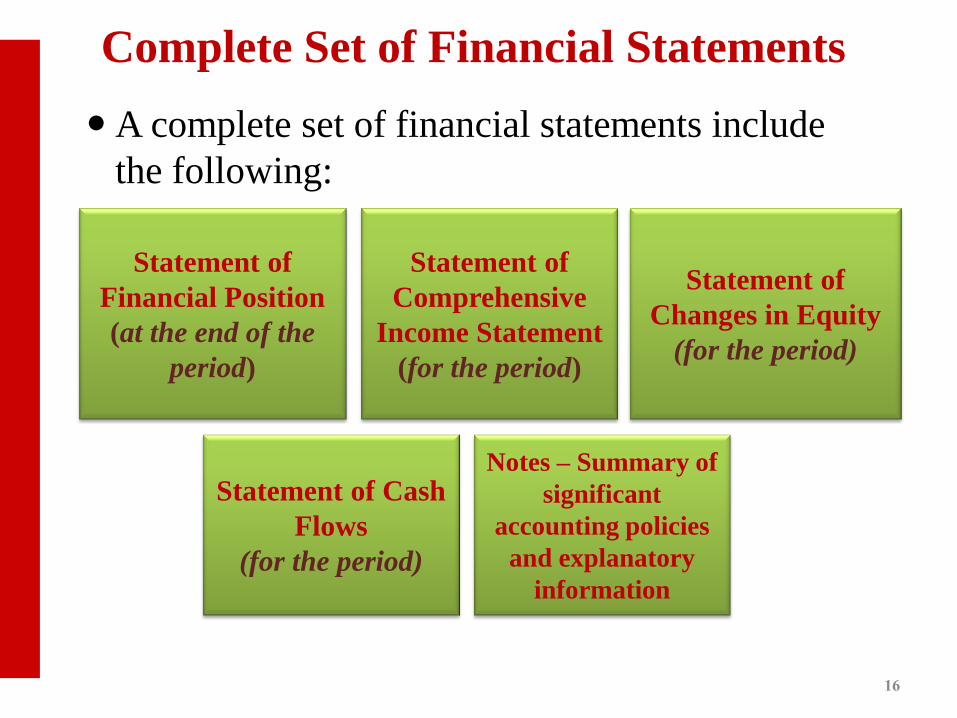

Complete Set of Financial Statements

A complete set of financial statements include

the following:

16

Statement of

Financial Position

(at the end of the

period)

Statement of

Comprehensive

Income Statement

(for the period)

Statement of

Changes in Equity

(for the period)

Statement of Cash

Flows

(for the period)

Notes – Summary of

significant

accounting policies

and explanatory

information

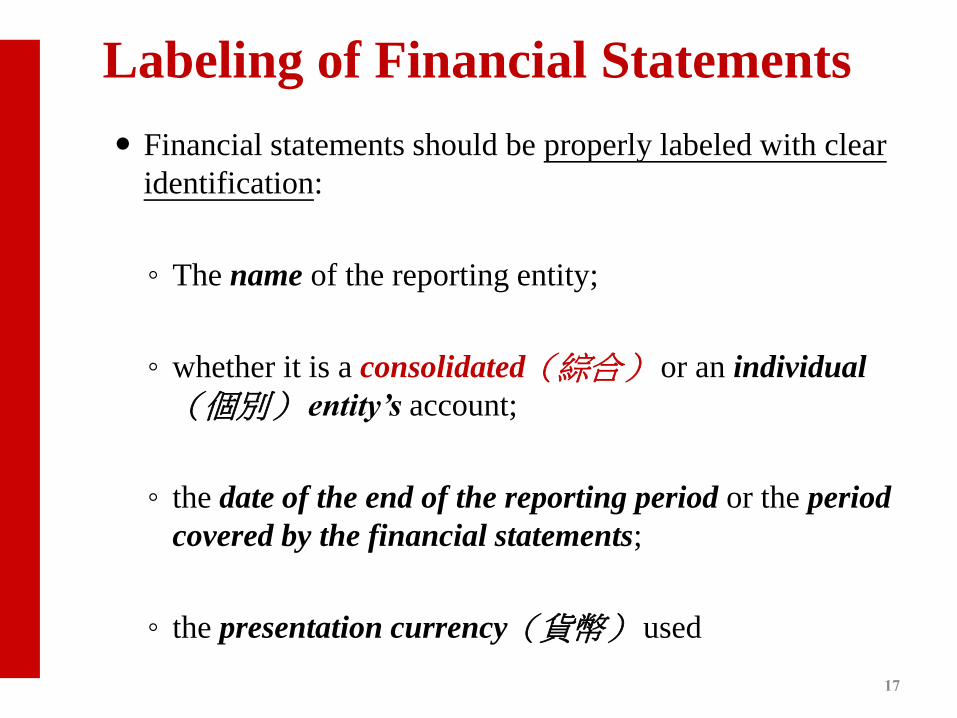

Labeling of Financial Statements

Financial statements should be properly labeled with clear

identification:

◦ The name of the reporting entity;

◦ whether it is a consolidated(綜合) or an individual

(個別) entity’s account;

◦ the date of the end of the reporting period or the period

covered by the financial statements;

◦ the presentation currency(貨幣) used

17

18

CONSOLIDATED FINANCIAL STATEMENTS

19

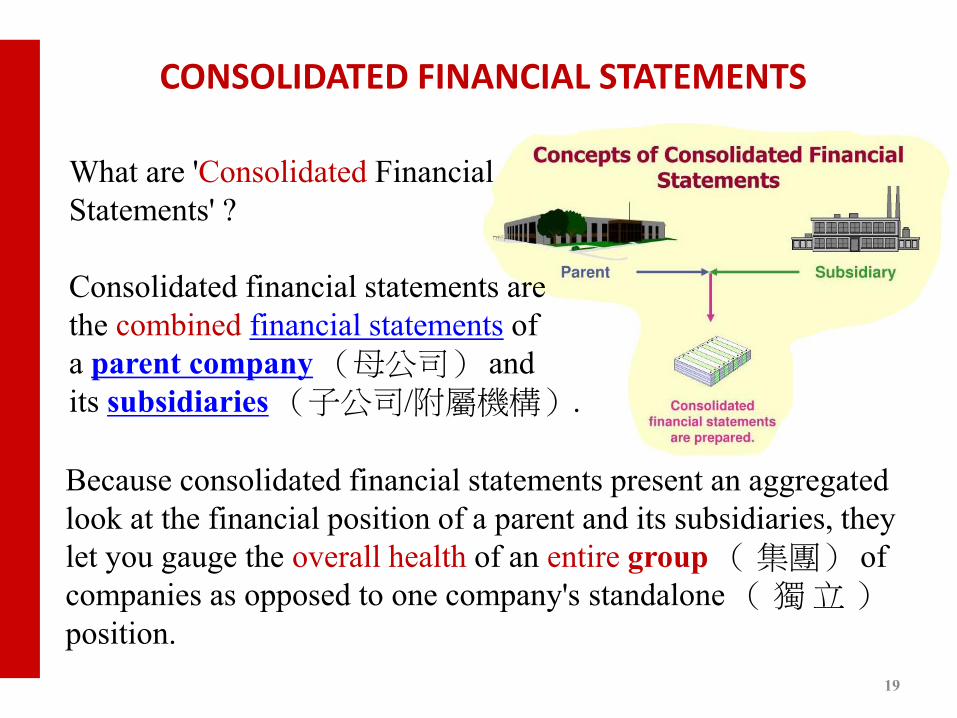

What are 'Consolidated Financial

Statements' ?

Consolidated financial statements are

the combined financial statements of

a parent company (母公司) and

its subsidiaries (子公司/附屬機構).

Because consolidated financial statements present an aggregated

look at the financial position of a parent and its subsidiaries, they

let you gauge the overall health of an entire group ( 集團) of

companies as opposed to one company's standalone ( 獨 立 )

position.

20

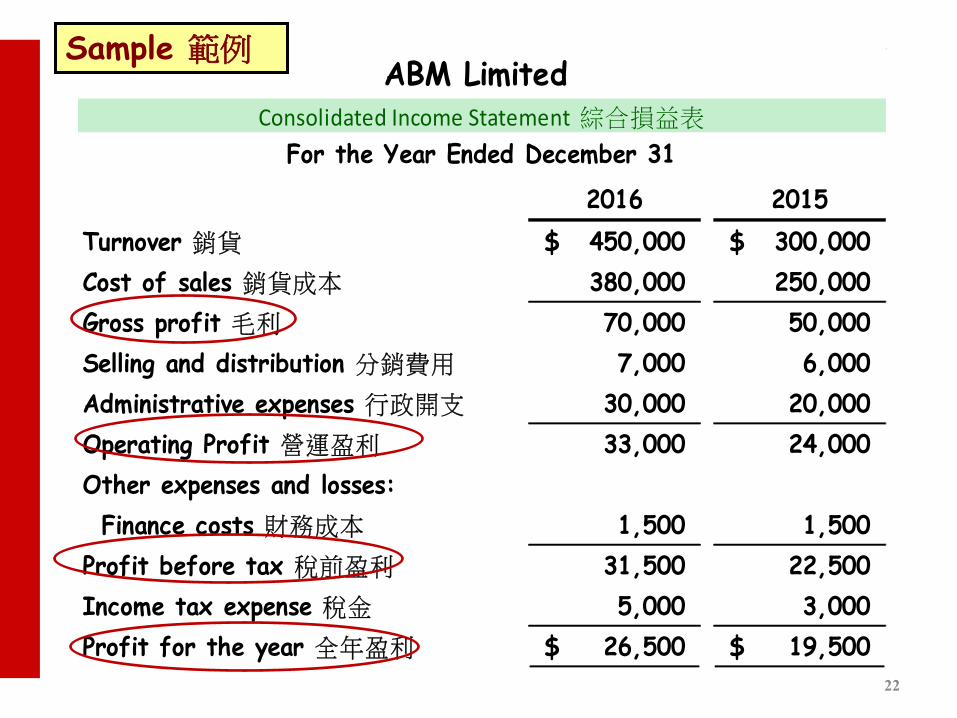

CONSOLIDATED INCOME STATEMENT

綜合損益表

21

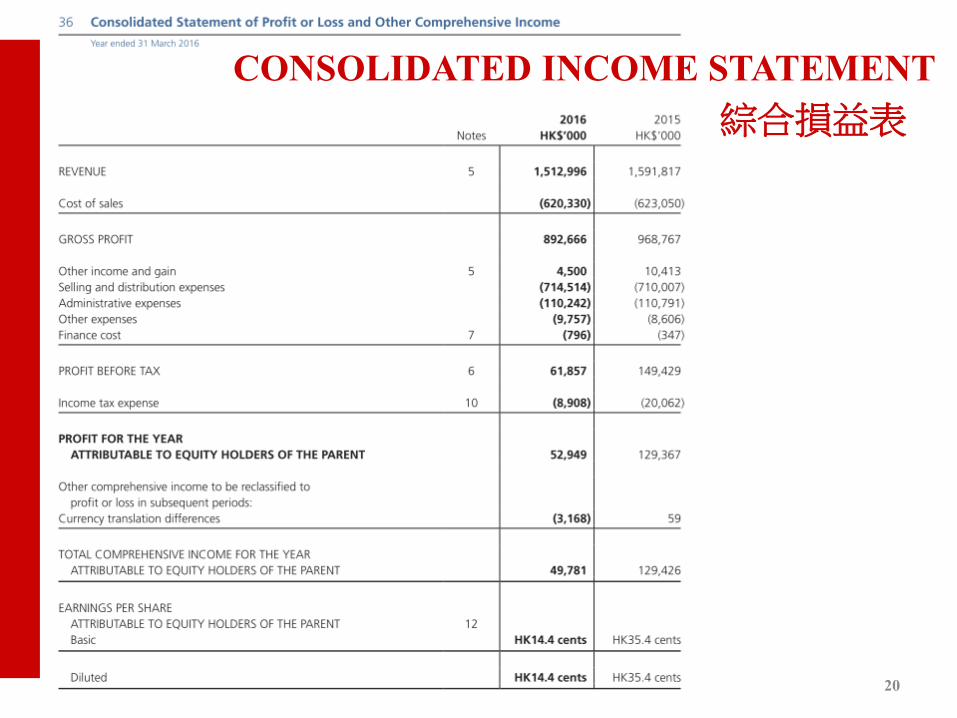

CONSOLIDATED INCOME STATEMENT/

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

綜合損益表

Function of Expense Method (按開支功能歸類)

• Classifies expenses according to their functions as cost of sales, selling and distribution costs, or administrative expenses

• This method can provide more relevant information to users, but allocating costs to functions may require arbitrary allocations and involve considerable judgment

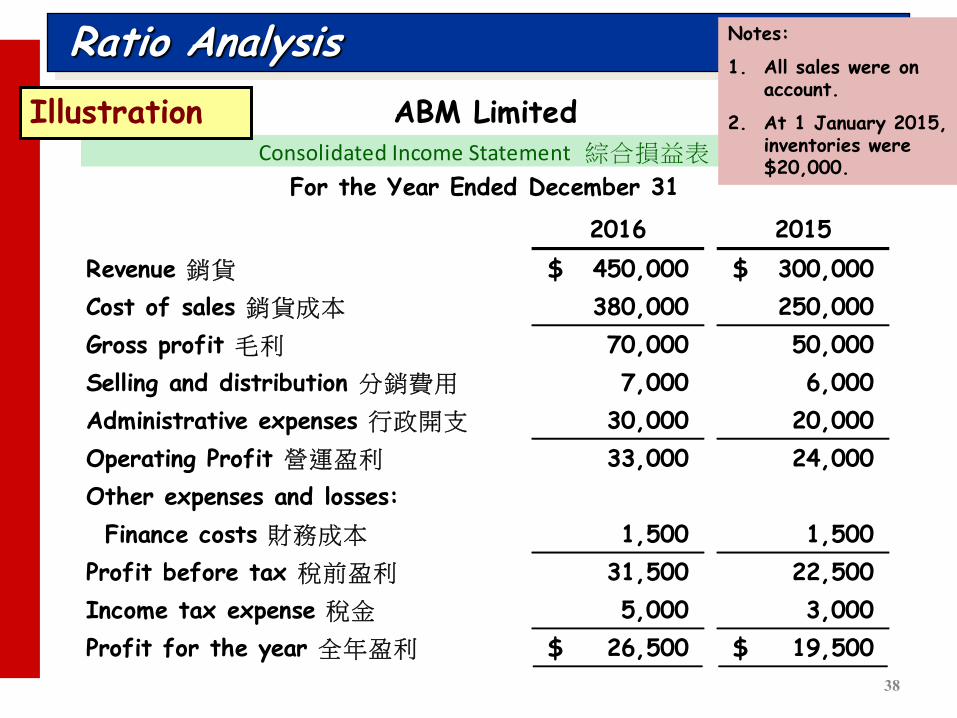

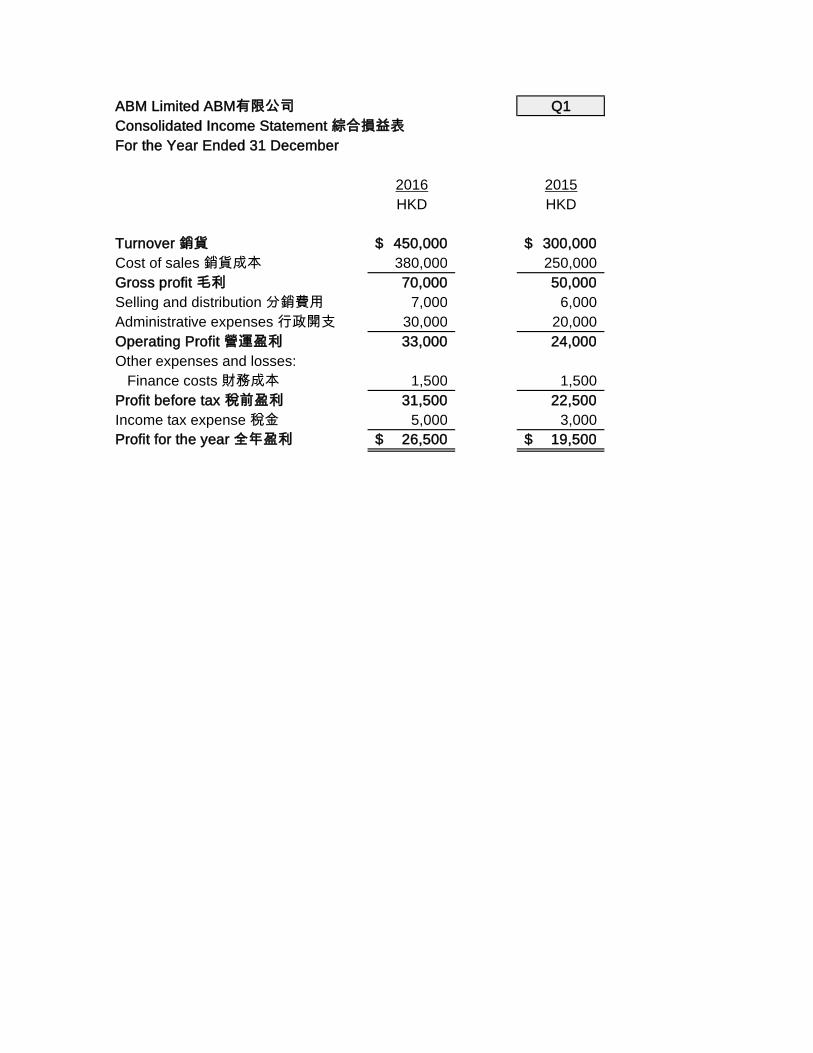

2016 2015

Turnover 銷貨 450,000$ 300,000$

Cost of sales 銷貨成本 380,000 250,000

Gross profit 毛利 70,000 50,000

Selling and distribution 分銷費用 7,000 6,000

Administrative expenses 行政開支 30,000 20,000

Operating Profit 營運盈利 33,000 24,000

Other expenses and losses:

Finance costs 財務成本 1,500 1,500

Profit before tax 稅前盈利 31,500 22,500

Income tax expense 稅金 5,000 3,000

Profit for the year 全年盈利 26,500$ 19,500$

ABM Limited Consolidated Income Statement 綜合損益表

For the Year Ended December 31

Sample 範例

22

23

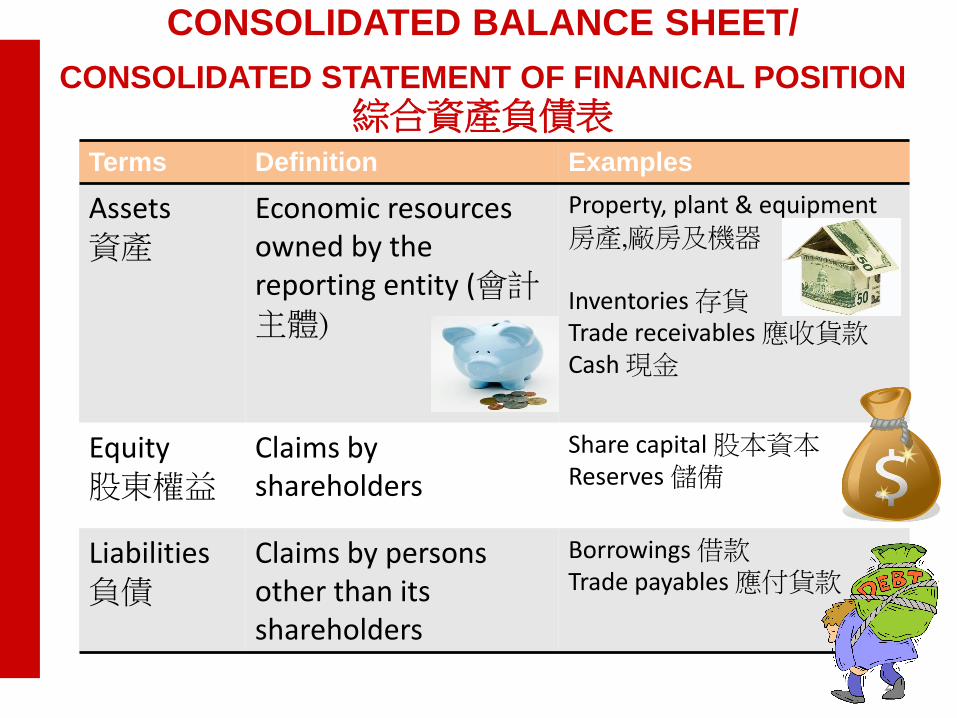

CONSOLIDATED BALANCE SHEET 綜合資產負債表

Assets

資產 Liabilities 負債

Equity 股本

Resources = Sources

Resources used

in the business

營商資源

Resources supplied by

creditors and owners

股東及債權人提供

CONSOLIDATED STATEMENT OF FINANCIAL POSITION/

CONSOLIDATED BALANCE SHEET

綜合資產負債表 資源 來源

24

CONSOLIDATED BALANCE SHEET/

CONSOLIDATED STATEMENT OF FINANICAL POSITION

綜合資產負債表

Terms Definition Examples

Assets 資產

Economic resources owned by the reporting entity (會計主體)

Property, plant & equipment 房產,廠房及機器 Inventories 存貨 Trade receivables 應收貨款 Cash 現金

Equity 股東權益

Claims by shareholders

Share capital 股本資本 Reserves 儲備

Liabilities 負債

Claims by persons other than its shareholders

Borrowings 借款 Trade payables 應付貨款

25

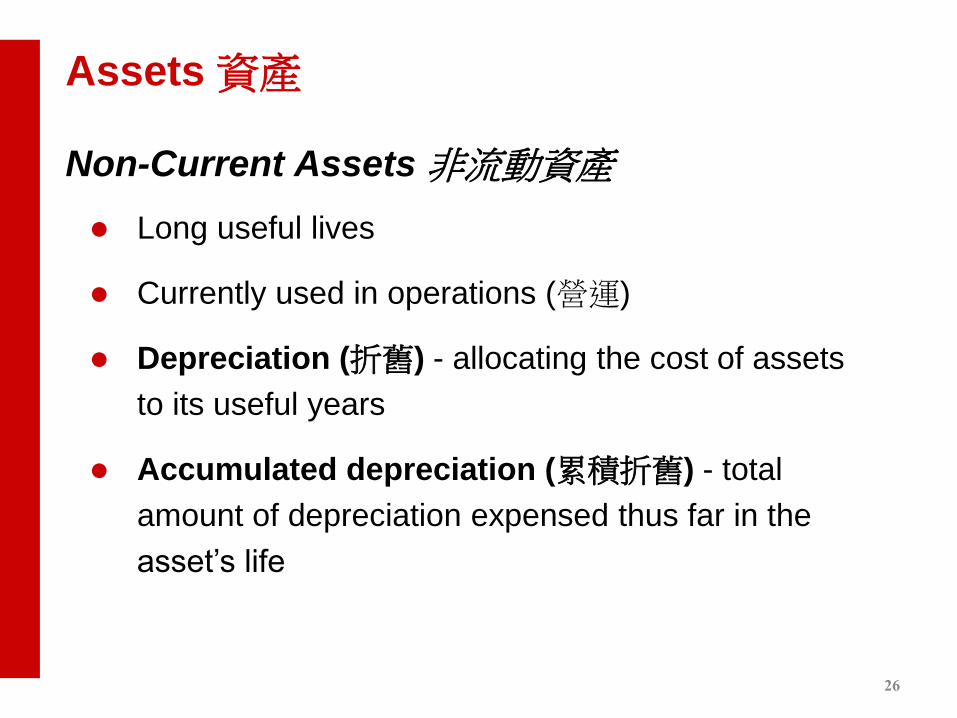

Long useful lives

Currently used in operations (營運)

Depreciation (折舊) - allocating the cost of assets

to its useful years

Accumulated depreciation (累積折舊) - total

amount of depreciation expensed thus far in the

asset’s life

Non-Current Assets 非流動資產

Assets 資產

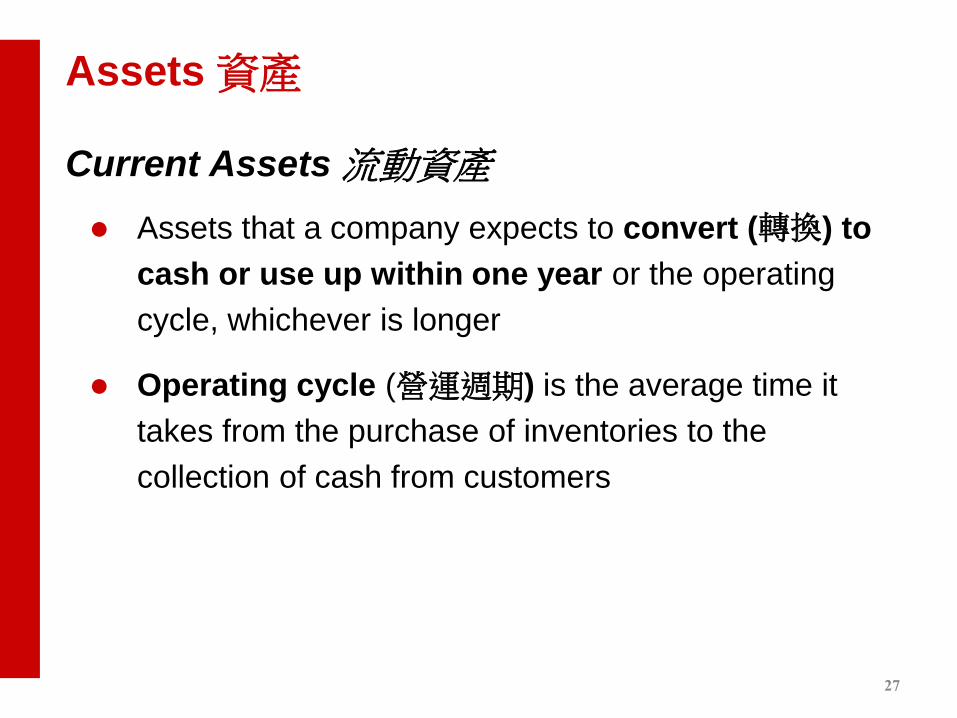

26

Assets that a company expects to convert (轉換) to

cash or use up within one year or the operating

cycle, whichever is longer

Operating cycle (營運週期) is the average time it

takes from the purchase of inventories to the

collection of cash from customers

Current Assets 流動資產

Assets 資產

27

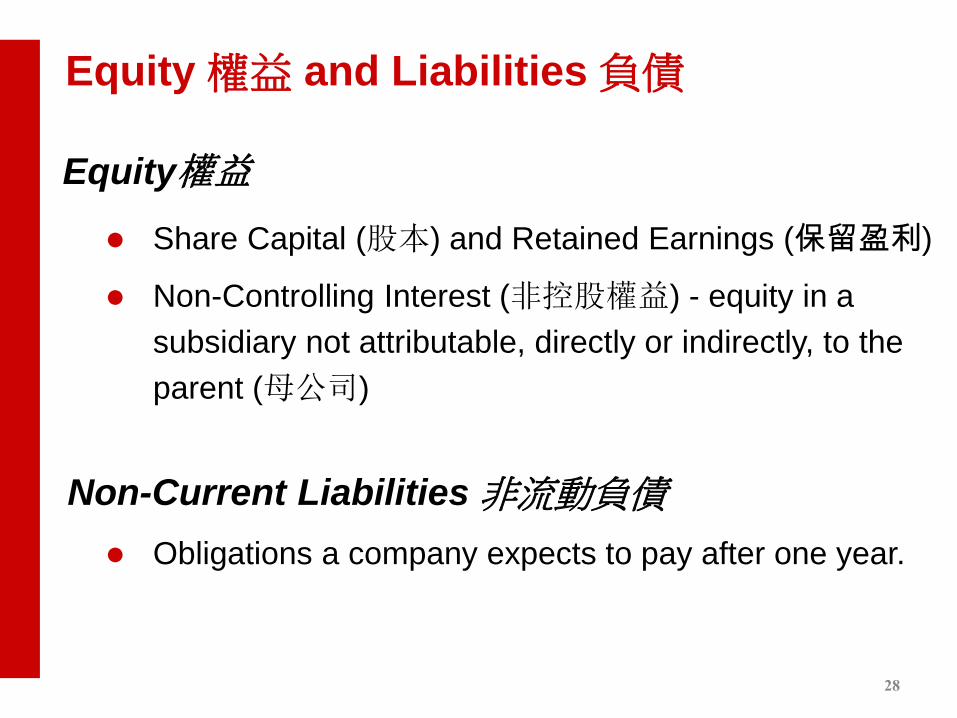

Obligations a company expects to pay after one year.

Non-Current Liabilities 非流動負債

Equity 權益 and Liabilities 負債

Equity權益

Share Capital (股本) and Retained Earnings (保留盈利)

Non-Controlling Interest (非控股權益) - equity in a

subsidiary not attributable, directly or indirectly, to the

parent (母公司)

28

Obligations (負債) a company is to pay within the

coming year or its operating cycle, whichever is

longer

Liquidity (流動性) - ability to pay obligations

expected to be due within the next year

Current Liabilities 流動負債

Equity 權益 and Liabilities 負債

29

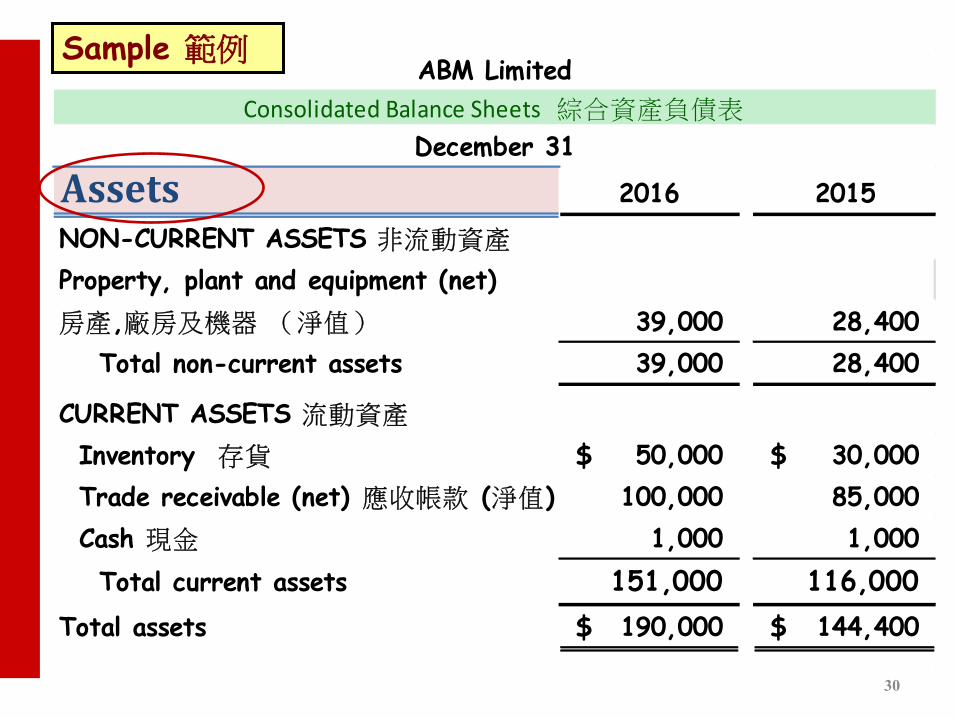

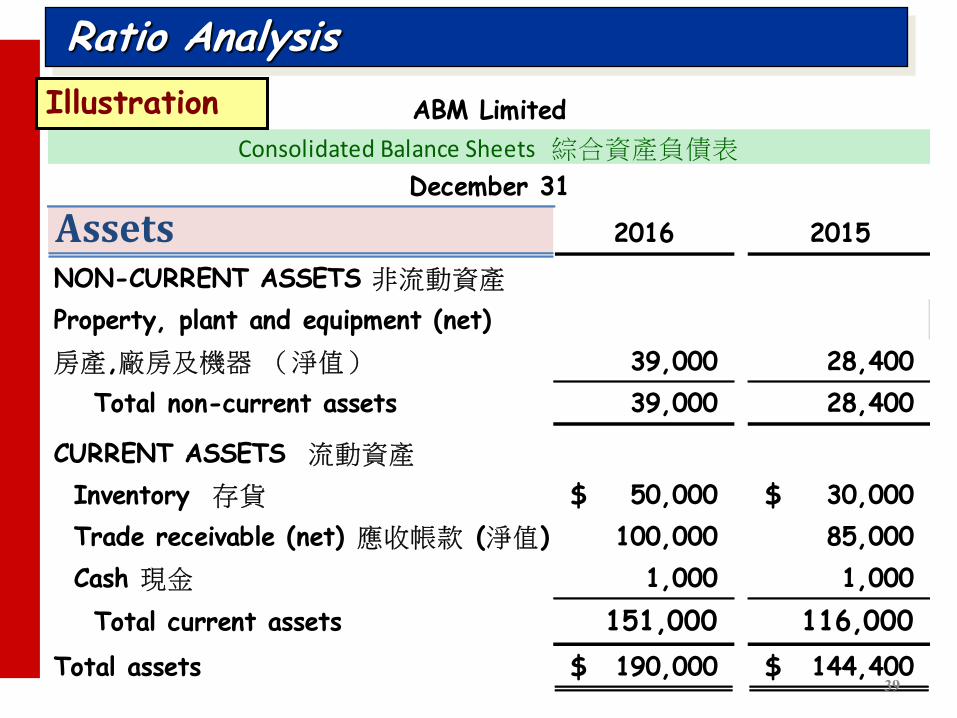

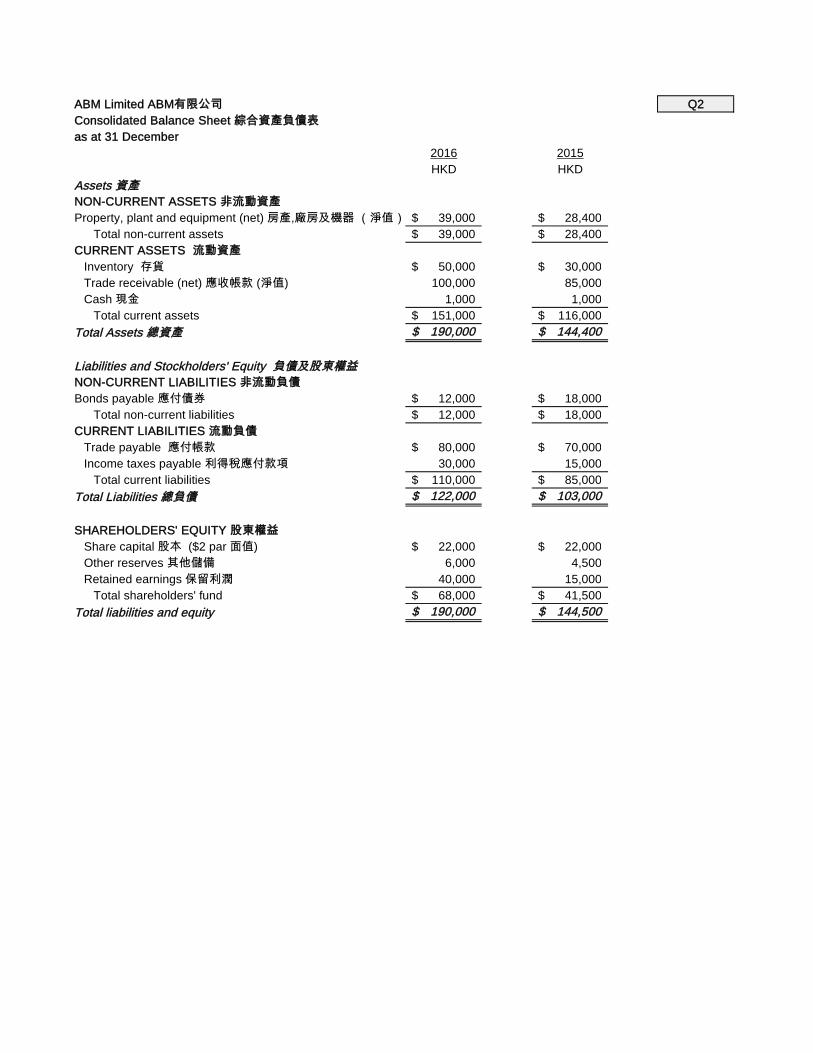

Assets 2016 2015

NON-CURRENT ASSETS 非流動資產

Property, plant and equipment (net)

房產,廠房及機器 (淨值) 39,000 28,400

Total non-current assets 39,000 28,400

CURRENT ASSETS 流動資產

Inventory 存貨 50,000$ 30,000$

Trade receivable (net) 應收帳款 (淨值) 100,000 85,000

Cash 現金 1,000 1,000

Total current assets 151,000 116,000

Total assets 190,000$ 144,400$

ABM Limited

Consolidated Balance Sheets 綜合資產負債表

December 31

Sample 範例

30

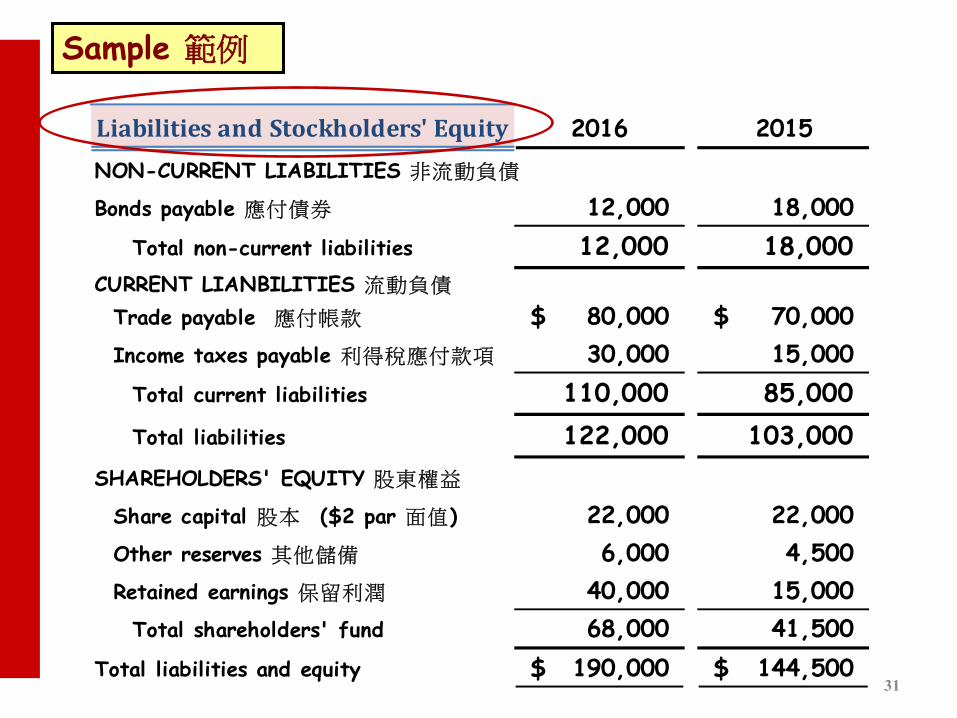

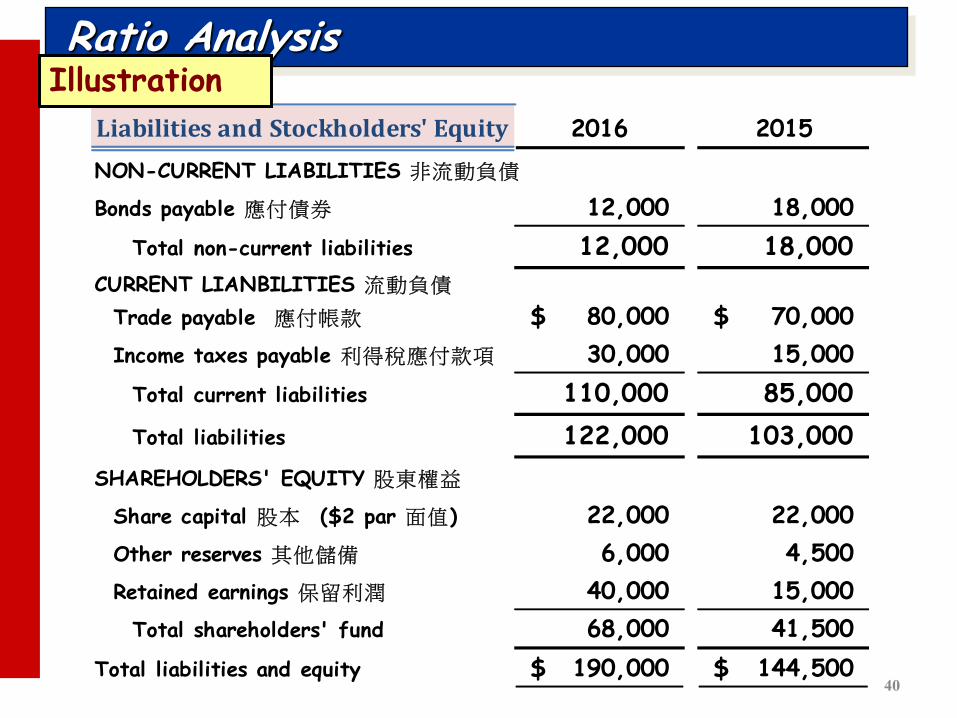

Liabilities and Stockholders' Equity 2016 2015

NON-CURRENT LIABILITIES 非流動負債

Bonds payable 應付債券 12,000 18,000

Total non-current liabilities 12,000 18,000

CURRENT LIANBILITIES 流動負債

Trade payable 應付帳款 80,000$ 70,000$

Income taxes payable 利得稅應付款項 30,000 15,000

Total current liabilities 110,000 85,000

Total liabilities 122,000 103,000

SHAREHOLDERS' EQUITY 股東權益

Share capital 股本 ($2 par 面值) 22,000 22,000

Other reserves 其他儲備 6,000 4,500

Retained earnings 保留利潤 40,000 15,000

Total shareholders' fund 68,000 41,500

Total liabilities and equity 190,000$ 144,500$

Sample 範例

31

32

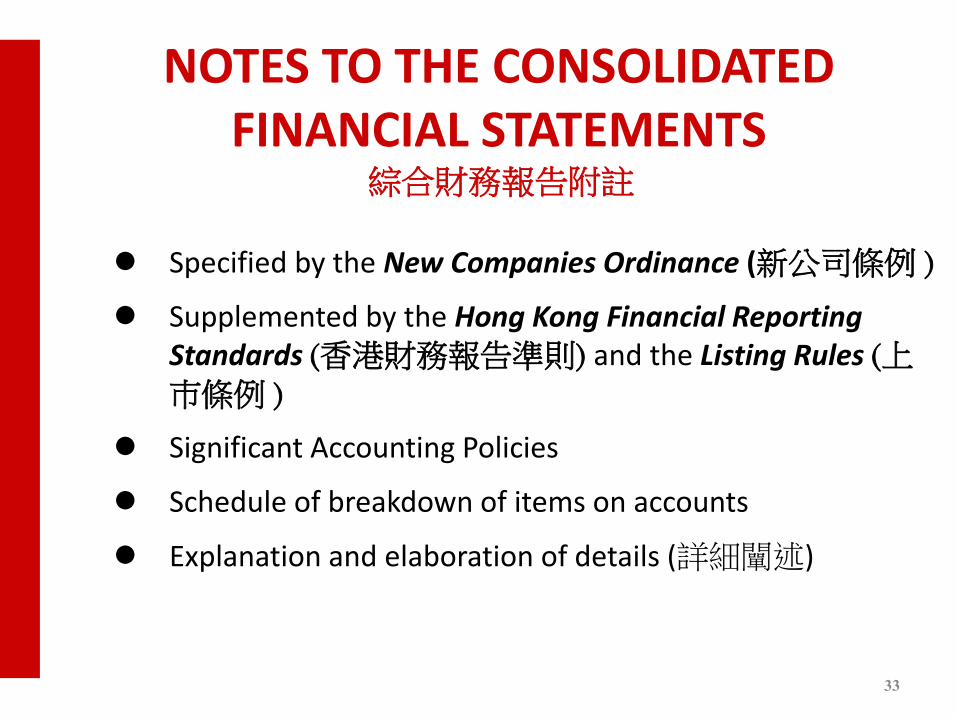

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 綜合財務報告附註

33

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

綜合財務報告附註

Specified by the New Companies Ordinance (新公司條例 )

Supplemented by the Hong Kong Financial Reporting Standards (香港財務報告準則) and the Listing Rules (上巿條例 )

Significant Accounting Policies

Schedule of breakdown of items on accounts

Explanation and elaboration of details (詳細闡述)

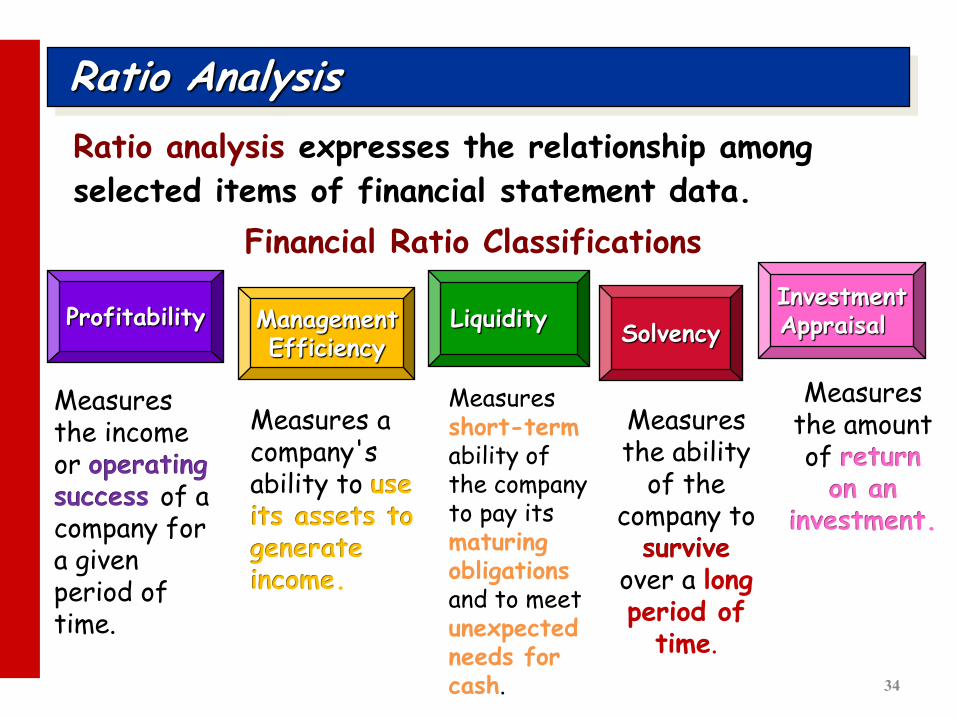

Ratio Analysis

Ratio analysis expresses the relationship among

selected items of financial statement data.

Liquidity Profitability Solvency

Measures short-term ability of the company to pay its maturing obligations and to meet unexpected needs for cash.

Financial Ratio Classifications

Measures the income or operating success of a company for a given period of time.

Measures the ability

of the company to

survive over a long period of

time.

Measures a company's ability to use its assets to generate income.

Management Efficiency

Investment Appraisal

Measures the amount of return

on an investment.

34

Ratio Analysis

The discussion of ratios will

include the following types of

comparisons.

A single ratio by itself is not very meaningful.

2015 2016

35

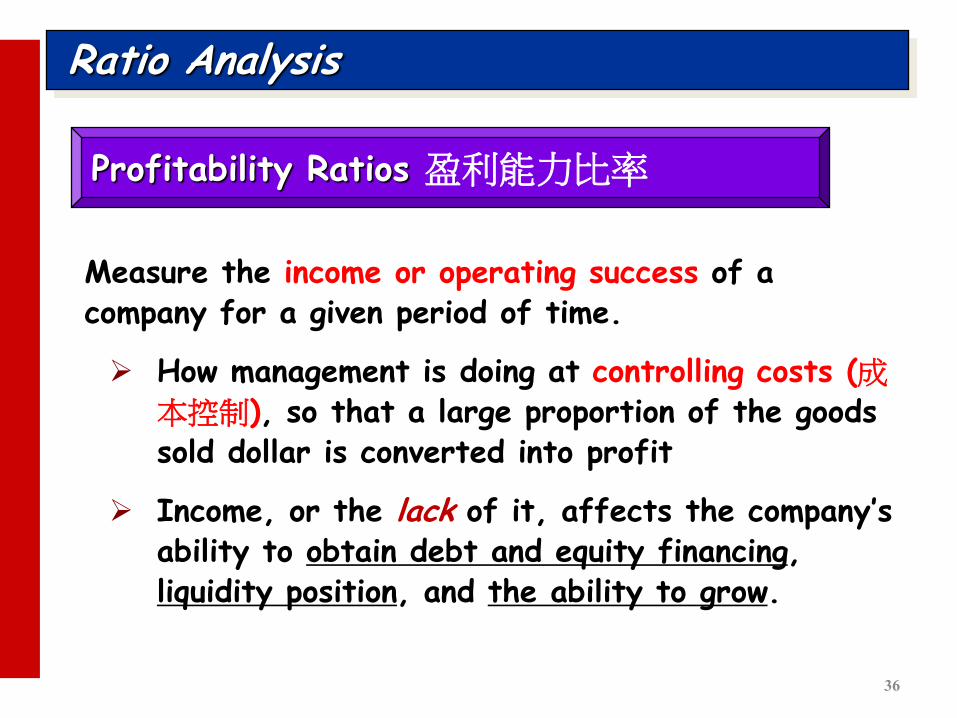

Ratio Analysis

Profitability Ratios 盈利能力比率

Measure the income or operating success of a company for a given period of time.

How management is doing at controlling costs (成本控制), so that a large proportion of the goods sold dollar is converted into profit

Income, or the lack of it, affects the company’s ability to obtain debt and equity financing, liquidity position, and the ability to grow.

36

37

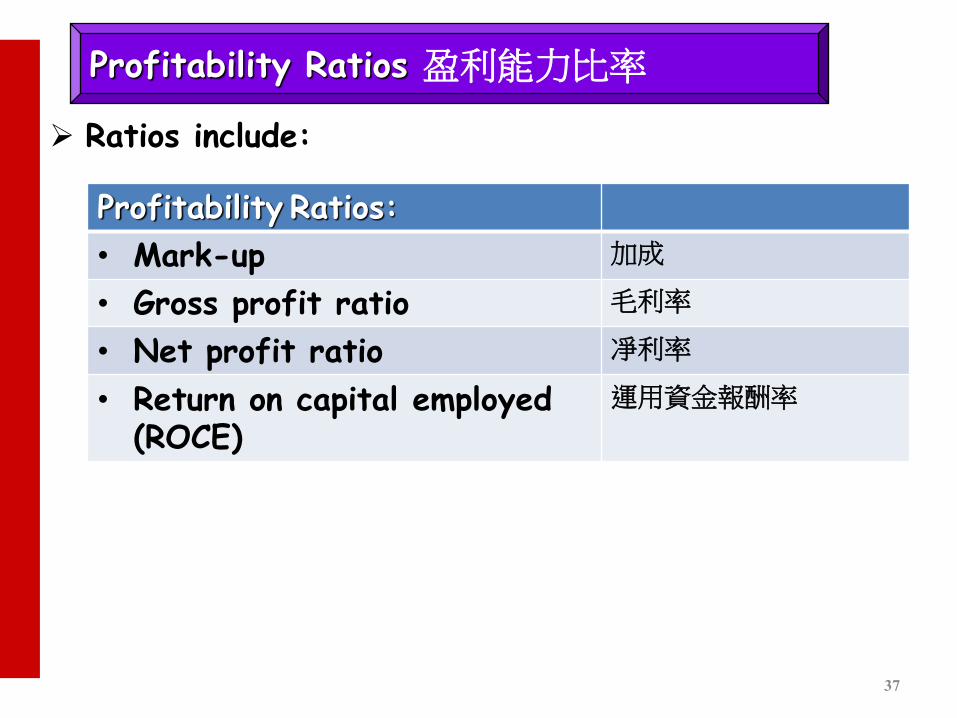

PROFITABILITY RATIOS 盈利能力比率

Ratios include:

Profitability Ratios:

• Mark-up 加成

• Gross profit ratio 毛利率

• Net profit ratio 凈利率

• Return on capital employed (ROCE)

運用資金報酬率

Profitability Ratios 盈利能力比率

2016 2015

Revenue 銷貨 450,000$ 300,000$

Cost of sales 銷貨成本 380,000 250,000

Gross profit 毛利 70,000 50,000

Selling and distribution 分銷費用 7,000 6,000

Administrative expenses 行政開支 30,000 20,000

Operating Profit 營運盈利 33,000 24,000

Other expenses and losses:

Finance costs 財務成本 1,500 1,500

Profit before tax 稅前盈利 31,500 22,500

Income tax expense 稅金 5,000 3,000

Profit for the year 全年盈利 26,500$ 19,500$

ABM LimitedConsolidated Income Statement 綜合損益表

For the Year Ended December 31

Ratio Analysis Notes:

1. All sales were on account.

2. At 1 January 2015, inventories were $20,000.

Illustration

38

Ratio Analysis

Assets 2016 2015

NON-CURRENT ASSETS 非流動資產

Property, plant and equipment (net)

房產,廠房及機器 (淨值) 39,000 28,400

Total non-current assets 39,000 28,400

CURRENT ASSETS 流動資產

Inventory 存貨 50,000$ 30,000$

Trade receivable (net) 應收帳款 (淨值) 100,000 85,000

Cash 現金 1,000 1,000

Total current assets 151,000 116,000

Total assets 190,000$ 144,400$

ABM Limited

Consolidated Balance Sheets 綜合資產負債表

December 31

Illustration

39

Ratio Analysis

Liabilities and Stockholders' Equity 2016 2015

NON-CURRENT LIABILITIES 非流動負債

Bonds payable 應付債券 12,000 18,000

Total non-current liabilities 12,000 18,000

CURRENT LIANBILITIES 流動負債

Trade payable 應付帳款 80,000$ 70,000$

Income taxes payable 利得稅應付款項 30,000 15,000

Total current liabilities 110,000 85,000

Total liabilities 122,000 103,000

SHAREHOLDERS' EQUITY 股東權益

Share capital 股本 ($2 par 面值) 22,000 22,000

Other reserves 其他儲備 6,000 4,500

Retained earnings 保留利潤 40,000 15,000

Total shareholders' fund 68,000 41,500

Total liabilities and equity 190,000$ 144,500$

Illustration

40

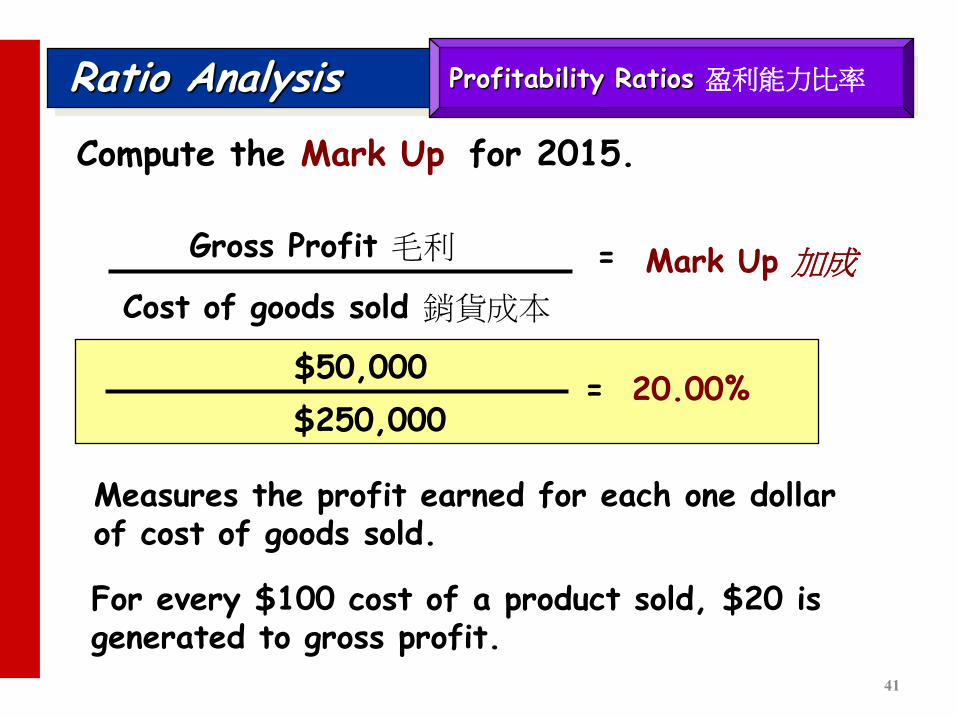

Ratio Analysis

Compute the Mark Up for 2015.

Measures the profit earned for each one dollar of cost of goods sold.

$50,000

$250,000 = 20.00%

Gross Profit 毛利

Cost of goods sold 銷貨成本

Mark Up 加成 =

Profitability Ratios 盈利能力比率

For every $100 cost of a product sold, $20 is generated to gross profit.

41

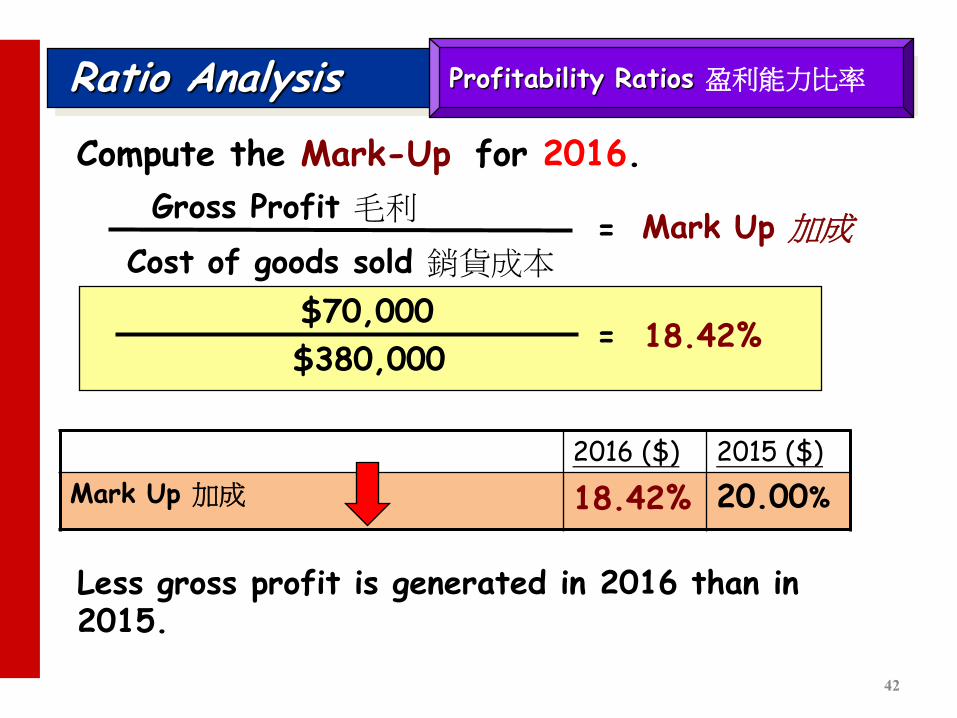

Ratio Analysis

Compute the Mark-Up for 2016.

$70,000

$380,000 = 18.42%

Gross Profit 毛利

Cost of goods sold 銷貨成本 Mark Up 加成 =

2016 ($) 2015 ($)

Mark Up 加成 20.00%

18.42%

Profitability Ratios 盈利能力比率

Less gross profit is generated in 2016 than in 2015.

42

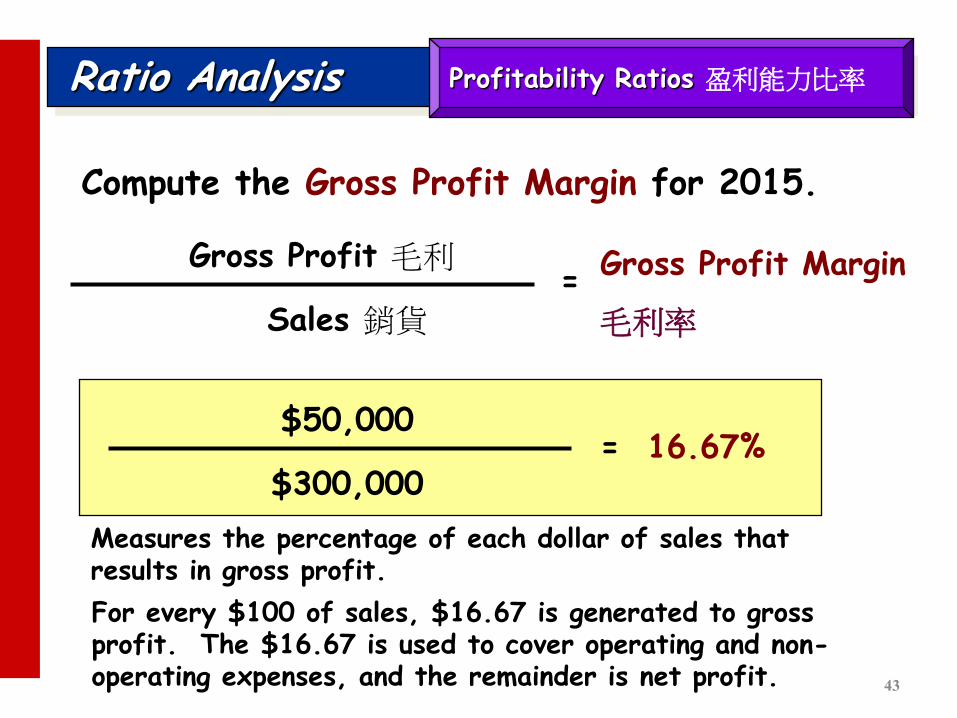

Ratio Analysis

Compute the Gross Profit Margin for 2015.

Measures the percentage of each dollar of sales that results in gross profit.

$50,000

$300,000 = 16.67%

Gross Profit 毛利

Sales 銷貨

Gross Profit Margin

毛利率 =

Profitability Ratios 盈利能力比率

For every $100 of sales, $16.67 is generated to gross profit. The $16.67 is used to cover operating and non- operating expenses, and the remainder is net profit. 43

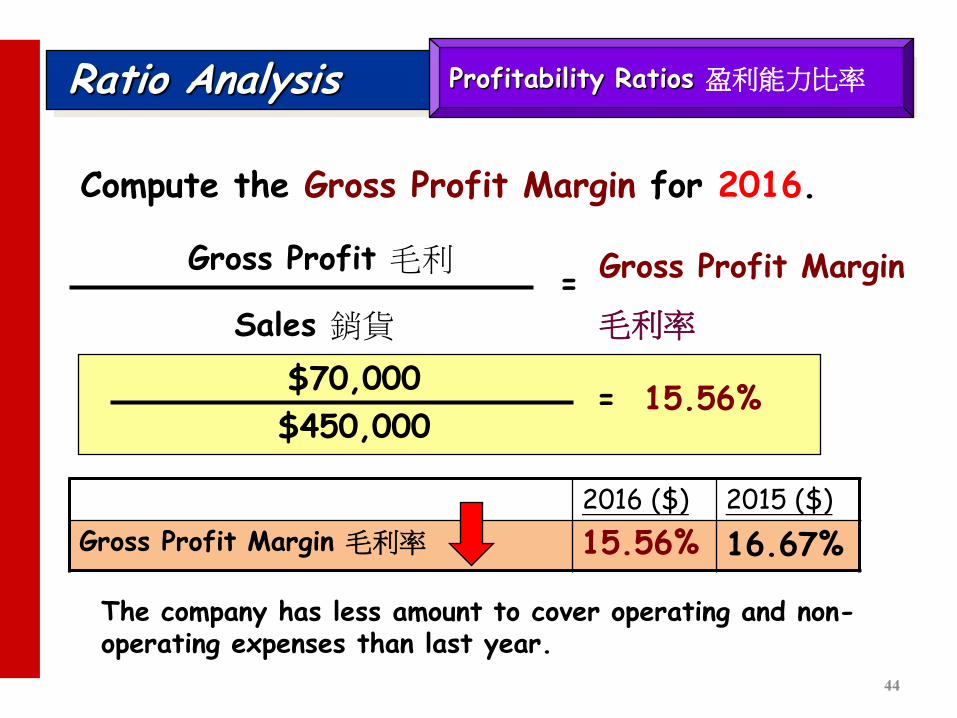

Ratio Analysis

Compute the Gross Profit Margin for 2016.

$70,000

$450,000 = 15.56%

Gross Profit 毛利

Sales 銷貨

Gross Profit Margin

毛利率 =

2016 ($) 2015 ($)

Gross Profit Margin 毛利率 16.67% 15.56%

Profitability Ratios 盈利能力比率

The company has less amount to cover operating and non- operating expenses than last year.

44

Ratio Analysis

Compute the Net Profit Margin for 2015.

Measures the percentage of each dollar of sales that results in net income.

$22,500

$300,000 = 7.50%

Net Profit before tax 稅前淨利

Sales 銷貨

Net Profit Margin

凈利率 =

Profitability Ratios 盈利能力比率

For every $100 of sales, $7.50 is generated to operating profit.

45

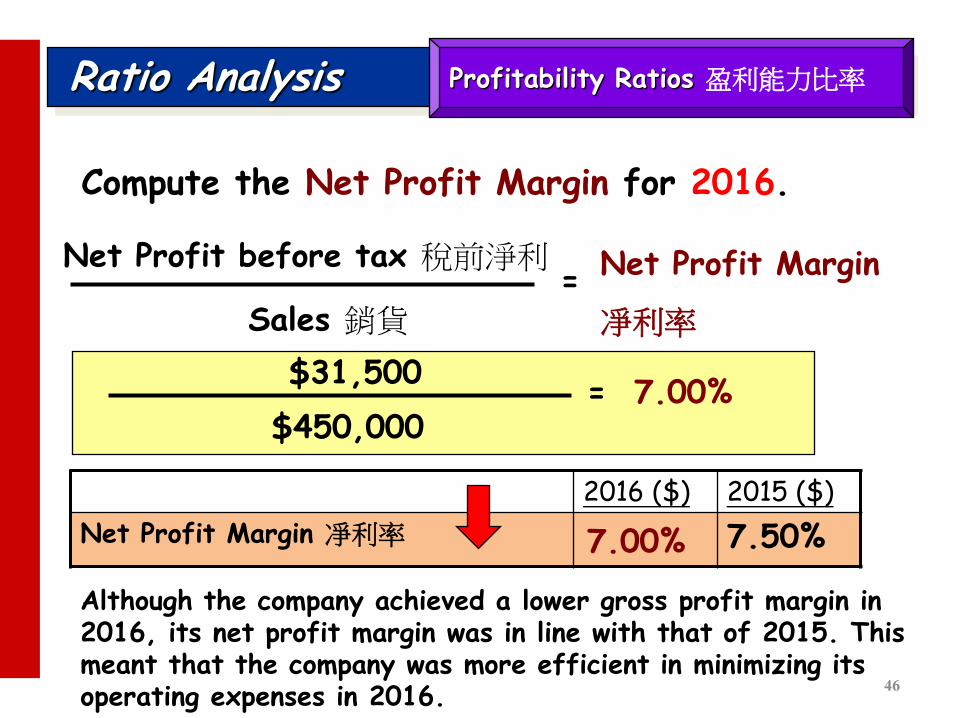

Ratio Analysis

Compute the Net Profit Margin for 2016.

$31,500

$450,000 = 7.00%

Net Profit before tax 稅前淨利

Sales 銷貨

Net Profit Margin

凈利率 =

2016 ($) 2015 ($)

Net Profit Margin 凈利率 7.50% 7.00%

Profitability Ratios 盈利能力比率

Although the company achieved a lower gross profit margin in 2016, its net profit margin was in line with that of 2015. This meant that the company was more efficient in minimizing its operating expenses in 2016.

46

Ratio Analysis

Compute the Return on Capital Employed (ROCE) for 2015.

$24,000

($41,500 + $18,000) = 40.34%

Profit before interest and tax 利息及稅前淨利 Return on Capital Employed

運用資金報酬率

= Capital Employed 運用資金

Rate of return based on the book value of long term capital investment made in the business.

Equity 股本 + Non-current liabilities 非流動負債

Operating Profit 營運盈利

Profitability Ratios 盈利能力比率

For every $100 of long term capital investment made in the business, $40.34 is operating profit generated for the year. 47

Ratio Analysis

Compute the Return on Capital Employed (ROCE) for 2016.

$33,000

($68,000 + $12,000) = 41.25%

Profit before interest and tax 利息及稅前淨利 Return on Capital Employed

運用資金報酬率

= Capital Employed 運用資金

2016 ($) 2015 ($)

ROCE 運用資金報酬率 40.34% 41.25%

Profitability Ratios 盈利能力比率

Much more income is earned in 2016 base on the book value of long term capital investment made in the business.

48

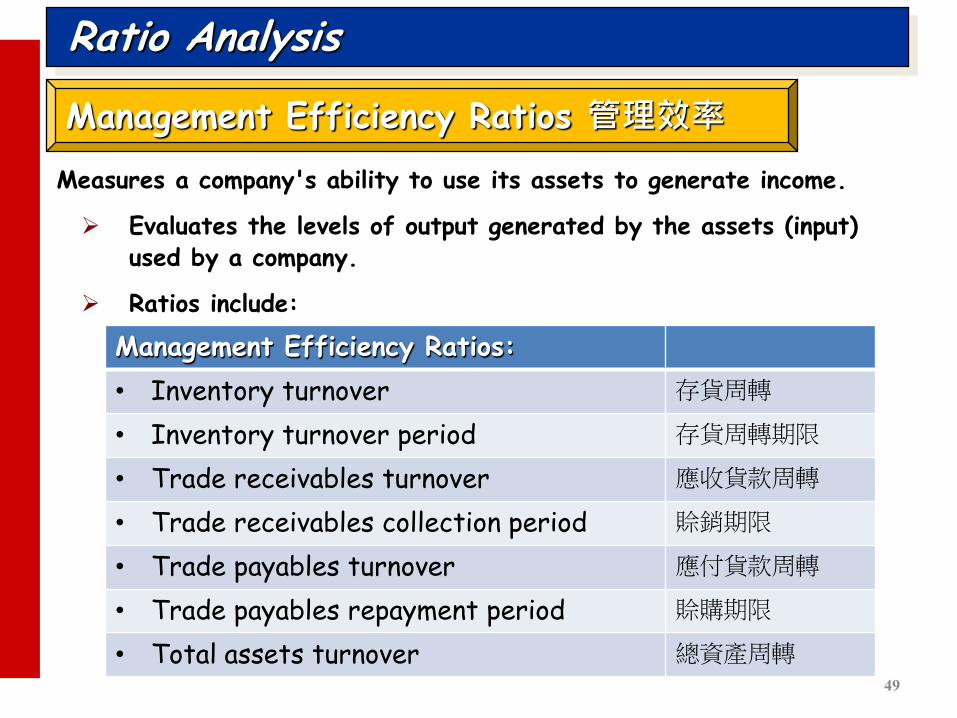

Ratio Analysis

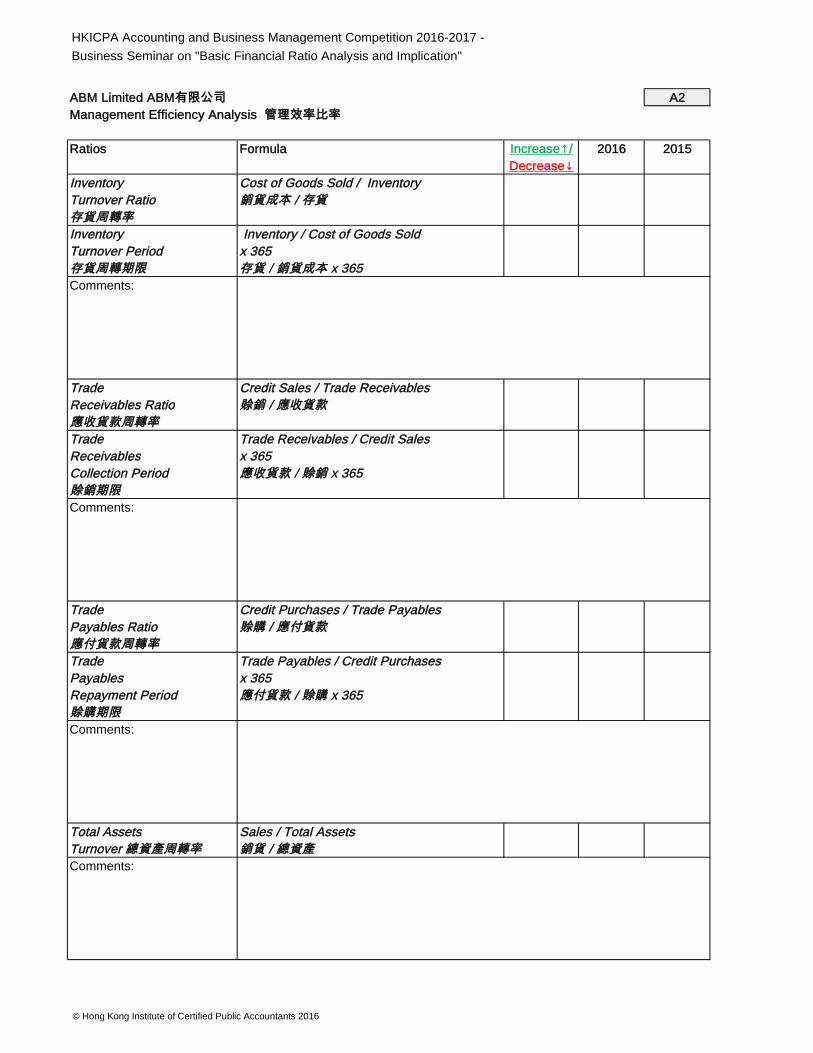

Measures a company's ability to use its assets to generate income.

Evaluates the levels of output generated by the assets (input) used by a company.

Ratios include:

Management Efficiency Ratios 管理效率

Management Efficiency Ratios:

• Inventory turnover 存貨周轉

• Inventory turnover period 存貨周轉期限

• Trade receivables turnover 應收貨款周轉

• Trade receivables collection period 賒銷期限

• Trade payables turnover 應付貨款周轉

• Trade payables repayment period 賒購期限

• Total assets turnover 總資產周轉 49

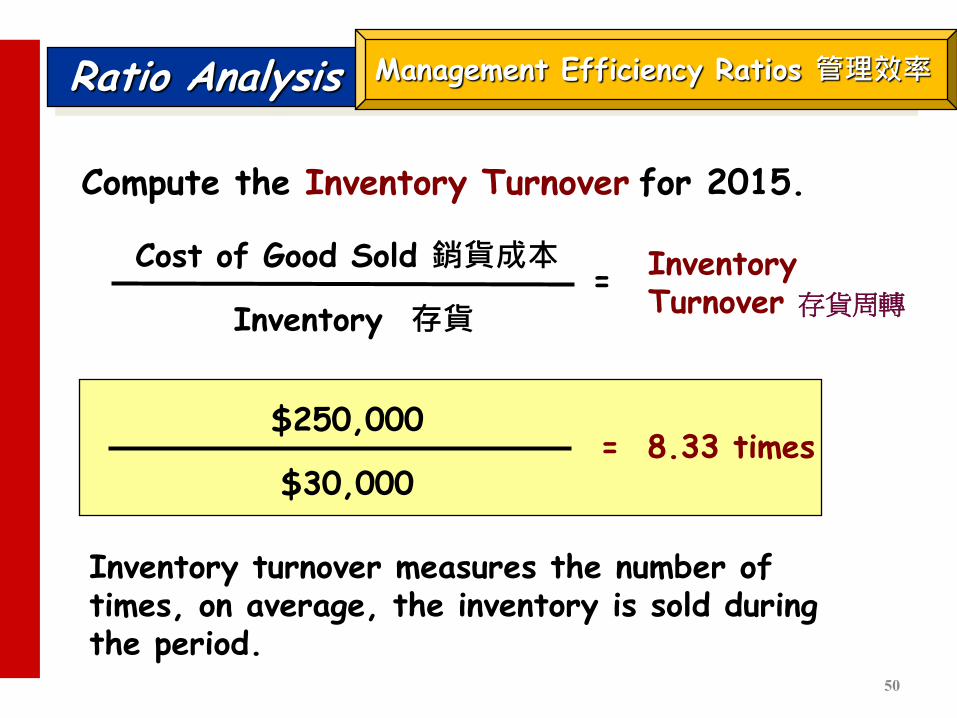

Ratio Analysis

Compute the Inventory Turnover for 2015.

Inventory turnover measures the number of times, on average, the inventory is sold during the period.

$250,000

$30,000 = 8.33 times

Cost of Good Sold 銷貨成本

Inventory 存貨

Inventory Turnover 存貨周轉

=

Management Efficiency Ratios 管理效率

50

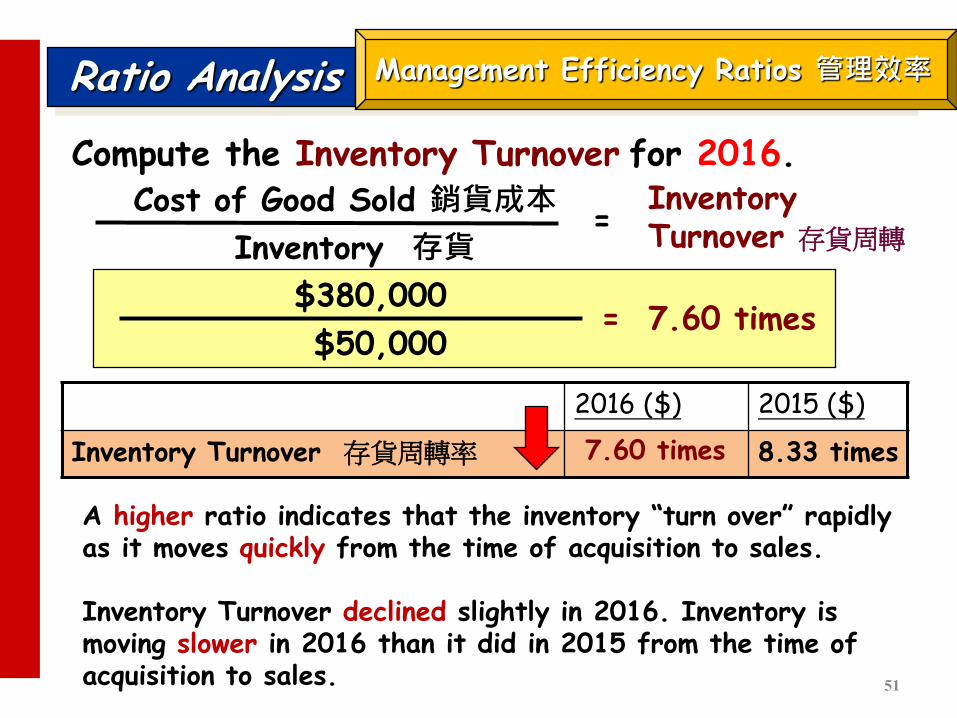

Ratio Analysis

Compute the Inventory Turnover for 2016.

$380,000

$50,000 = 7.60 times

Cost of Good Sold 銷貨成本

Inventory 存貨

Inventory Turnover 存貨周轉

=

2016 ($) 2015 ($)

Inventory Turnover 存貨周轉率 8.33 times

51

7.60 times

Management Efficiency Ratios 管理效率

A higher ratio indicates that the inventory “turn over” rapidly as it moves quickly from the time of acquisition to sales. Inventory Turnover declined slightly in 2016. Inventory is moving slower in 2016 than it did in 2015 from the time of acquisition to sales.

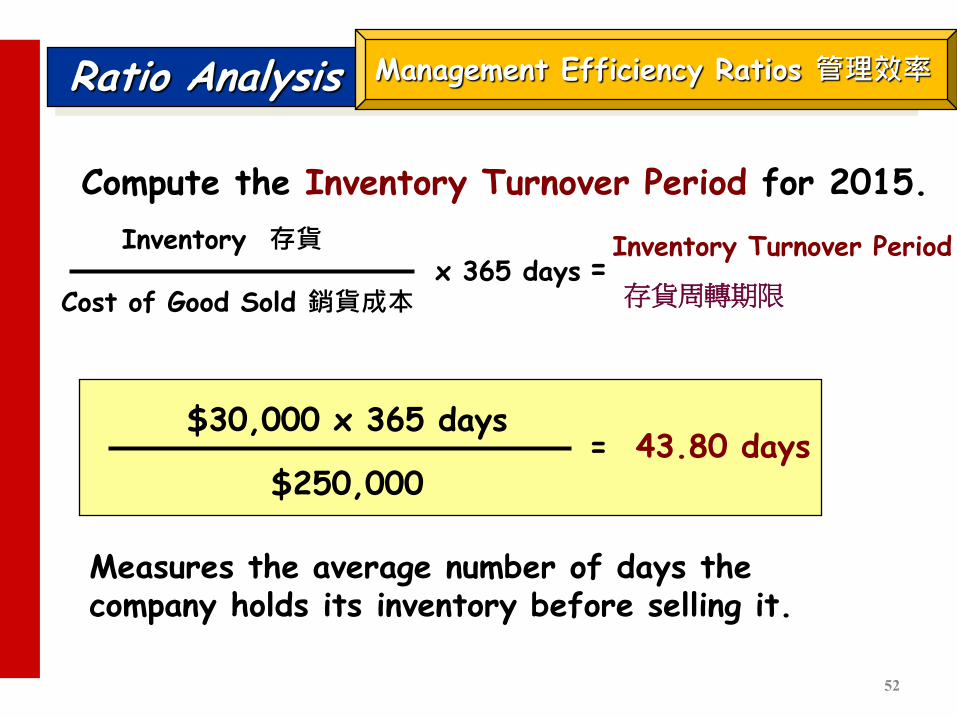

Ratio Analysis

Compute the Inventory Turnover Period for 2015.

Measures the average number of days the company holds its inventory before selling it.

$30,000 x 365 days

$250,000 = 43.80 days

Cost of Good Sold 銷貨成本

Inventory 存貨 = x 365 days

Inventory Turnover Period

存貨周轉期限

Management Efficiency Ratios 管理效率

52

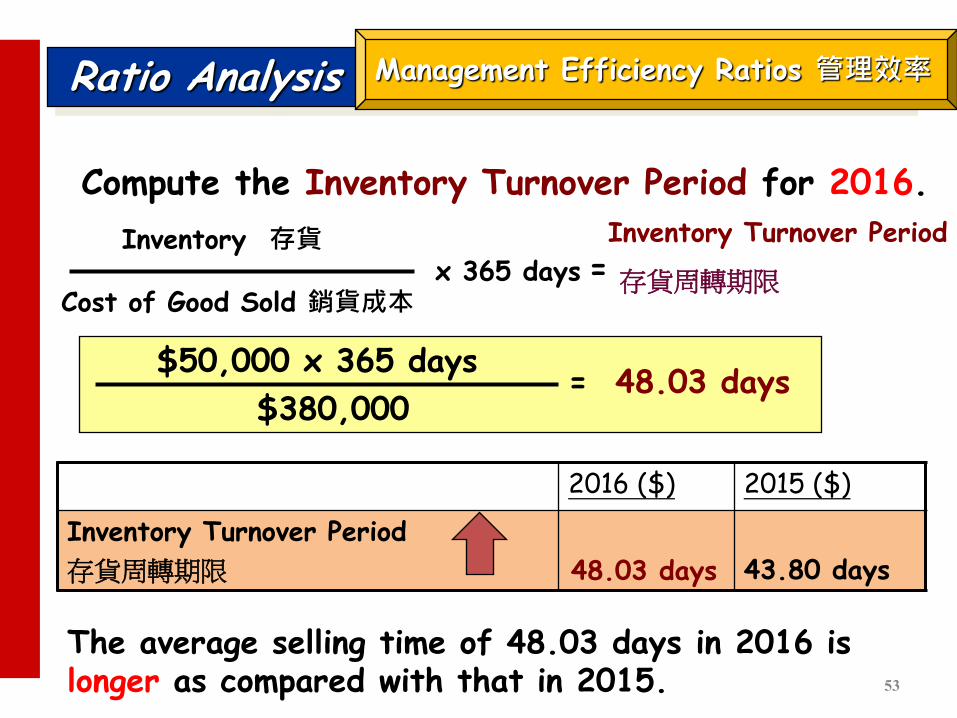

Ratio Analysis

Compute the Inventory Turnover Period for 2016.

$50,000 x 365 days

$380,000 = 48.03 days

Cost of Good Sold 銷貨成本

Inventory 存貨 Inventory Turnover Period

存貨周轉期限

= x 365 days

2016 ($) 2015 ($)

Inventory Turnover Period

存貨周轉期限

43.80 days

53

48.03 days

Management Efficiency Ratios 管理效率

The average selling time of 48.03 days in 2016 is longer as compared with that in 2015.

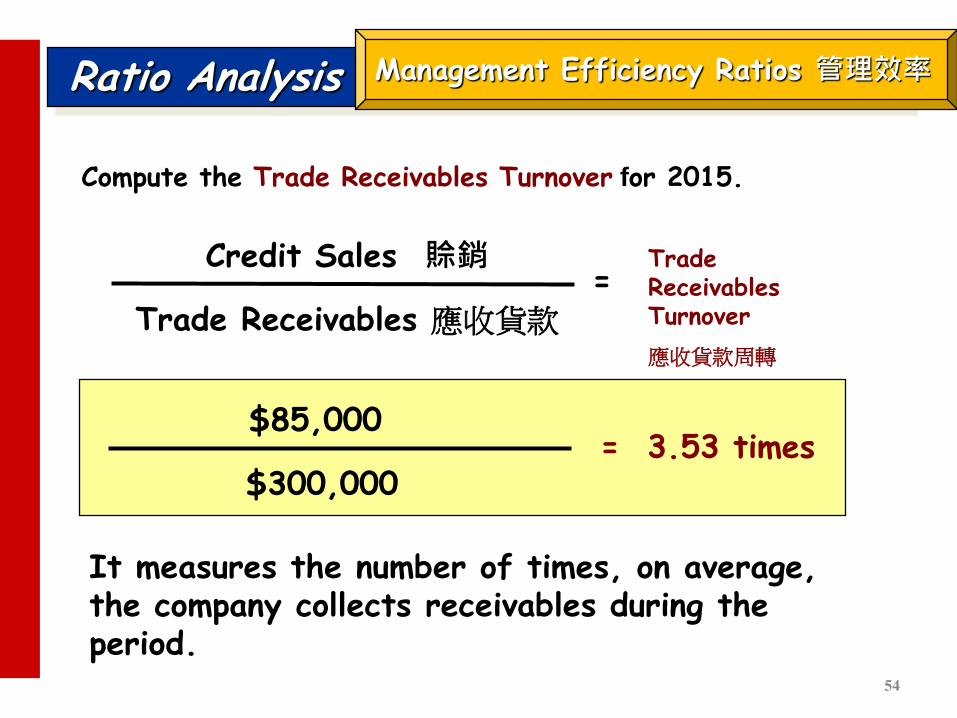

Ratio Analysis

Compute the Trade Receivables Turnover for 2015.

It measures the number of times, on average, the company collects receivables during the period.

$85,000

$300,000 = 3.53 times

Credit Sales 賒銷

Trade Receivables 應收貨款

Trade Receivables Turnover

應收貨款周轉

=

Management Efficiency Ratios 管理效率

54

Ratio Analysis

Compute the Trade Receivables Turnover for 2016.

$100,000

$450,000 = 4.50 times

Credit Sales 賒銷

Trade Receivables 應收貨款

Trade Receivables Turnover

應收貨款周轉

=

2016 ($) 2015 ($)

Trade Receivables Ratio

應收貨款周轉

3.53 times

55

4.50 times

Management Efficiency Ratios 管理效率

Trade Receivables Turnover improved in 2016.

Ratio Analysis

Compute the Trade Receivables Collection Period for 2015.

It assesses the effectiveness of a company’s credit and collection policies.

This ratio means that receivables are collected on average every 103.42 days.

$85,000 x 365 days

$300,000 = 103.42 days

Credit Sales 賒銷

Trade Receivables 應收貨款 Trade Receivables Collection Period

賒銷期限

= x 365 days

Management Efficiency Ratios 管理效率

56

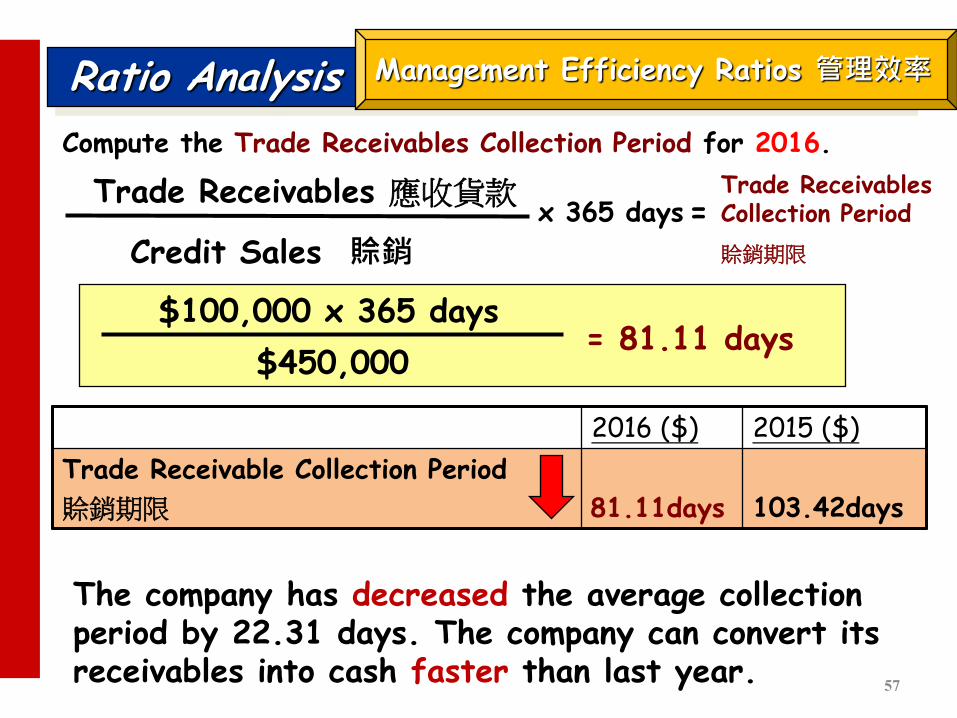

Ratio Analysis

Compute the Trade Receivables Collection Period for 2016.

$100,000 x 365 days

$450,000 = 81.11 days

Credit Sales 賒銷

Trade Receivables 應收貨款 Trade Receivables Collection Period

賒銷期限

= x 365 days

2016 ($) 2015 ($)

Trade Receivable Collection Period

賒銷期限

103.42days

57

81.11days

Management Efficiency Ratios 管理效率

The company has decreased the average collection period by 22.31 days. The company can convert its receivables into cash faster than last year.

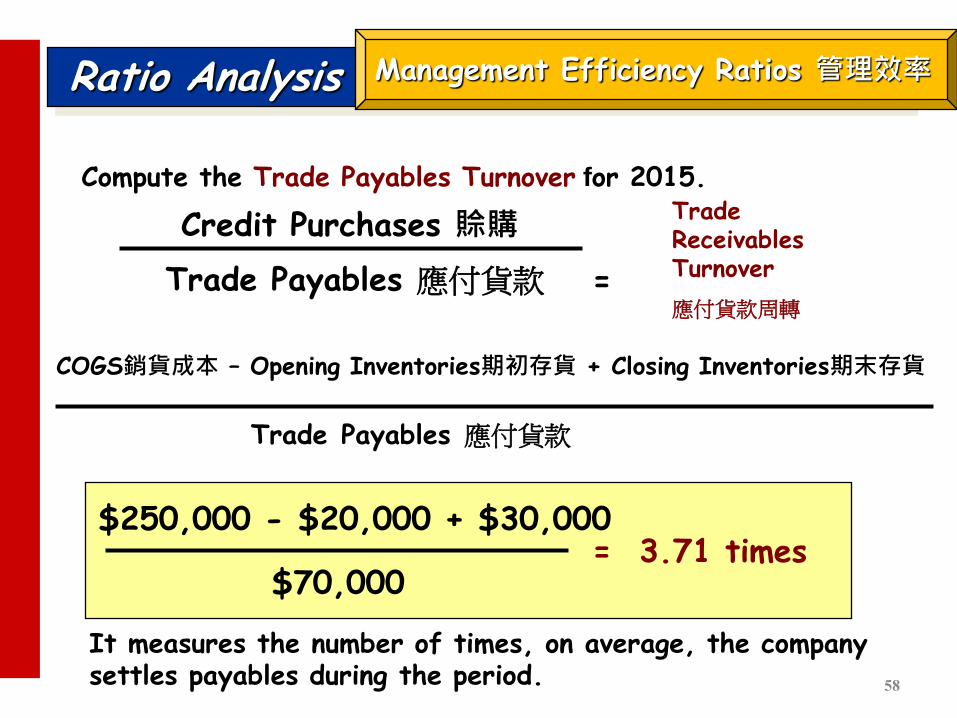

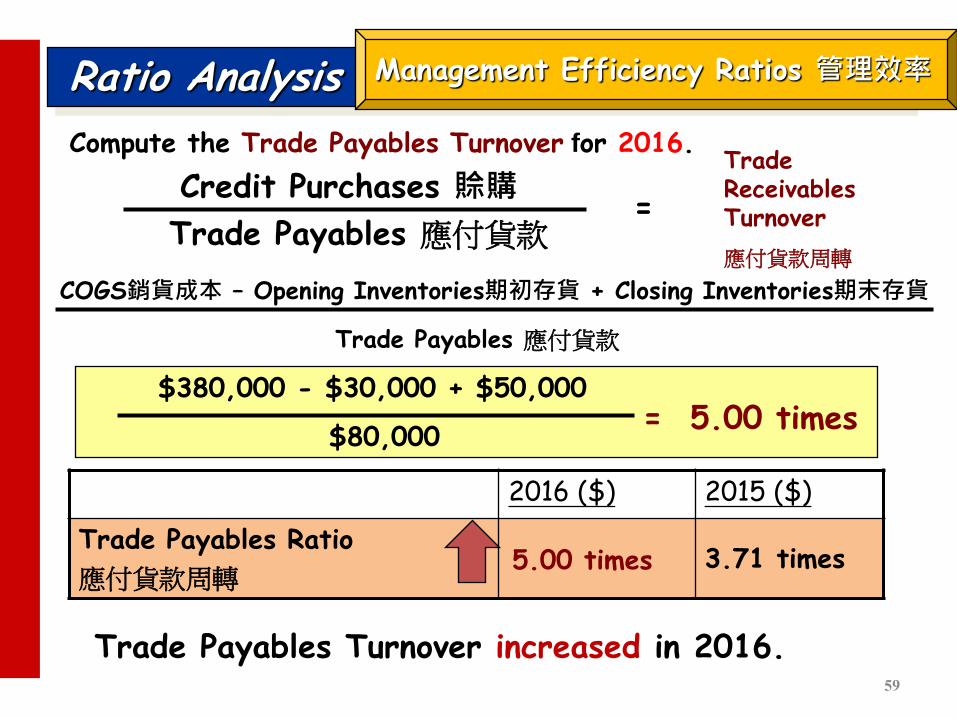

Ratio Analysis

Compute the Trade Payables Turnover for 2015.

It measures the number of times, on average, the company settles payables during the period.

$250,000 - $20,000 + $30,000

$70,000 = 3.71 times

Credit Purchases 賒購

Trade Payables 應付貨款

Trade Receivables Turnover

應付貨款周轉

=

Trade Payables 應付貨款

COGS銷貨成本 – Opening Inventories期初存貨 + Closing Inventories期末存貨

Management Efficiency Ratios 管理效率

58

Ratio Analysis

Compute the Trade Payables Turnover for 2016.

$380,000 - $30,000 + $50,000

$80,000 = 5.00 times

Credit Purchases 賒購

Trade Payables 應付貨款

Trade Receivables Turnover

應付貨款周轉

=

Trade Payables 應付貨款

COGS銷貨成本 – Opening Inventories期初存貨 + Closing Inventories期末存貨

2016 ($) 2015 ($)

Trade Payables Ratio

應付貨款周轉 3.71 times

59

5.00 times

Management Efficiency Ratios 管理效率

Trade Payables Turnover increased in 2016.

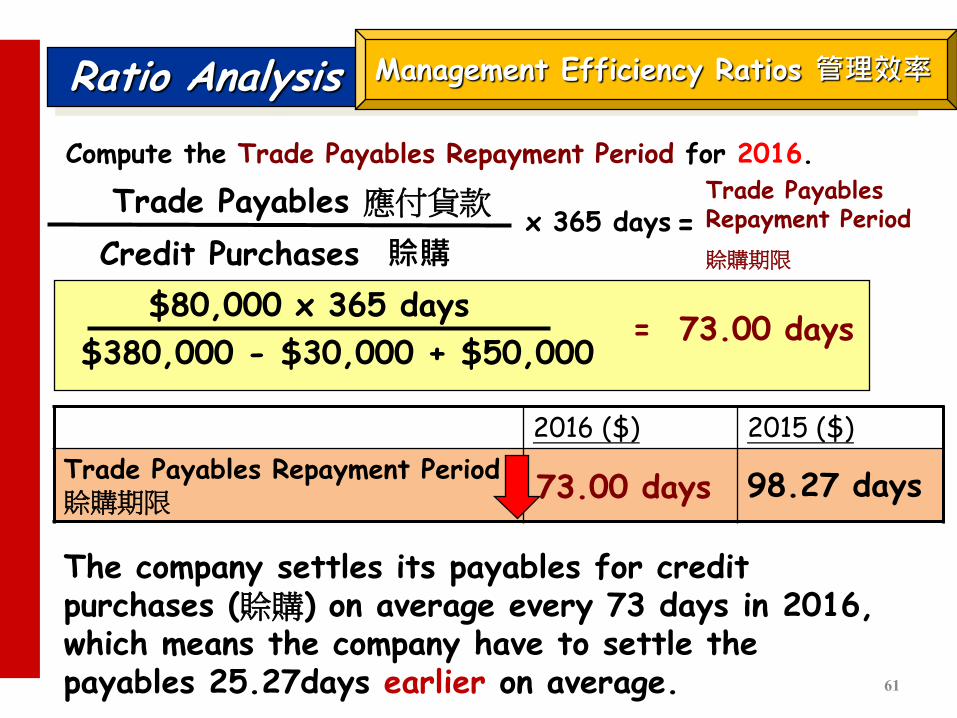

Ratio Analysis

Compute the Trade Payables Repayment Period for 2015.

$70,000 x 365 days = 98.27 days

Credit Purchases 賒購

Trade Payables 應付貨款 Trade Payables Repayment Period

賒購期限

= x 365 days

$250,000 - $20,000 + $30,000

Indicates average length of time in days within which a company must pay for its credit purchases (賒購). This means that payables are settled on average every 98.27 days.

Management Efficiency Ratios 管理效率

60

Ratio Analysis

Compute the Trade Payables Repayment Period for 2016.

$80,000 x 365 days = 73.00 days

Credit Purchases 賒購

Trade Payables 應付貨款 Trade Payables Repayment Period

賒購期限

= x 365 days

$380,000 - $30,000 + $50,000

2016 ($) 2015 ($)

Trade Payables Repayment Period 賒購期限 98.27 days

61

73.00 days

Management Efficiency Ratios 管理效率

The company settles its payables for credit purchases (賒購) on average every 73 days in 2016, which means the company have to settle the payables 25.27days earlier on average.

Ratio Analysis

Whether these days are good or bad depend on the company goals.

A company may have long trade receivables period by granting customers long credit period in order to gain market share.

Credit period enjoyed by the company enables more liquid funds for operations;

Management Efficiency Ratios 管理效率

62

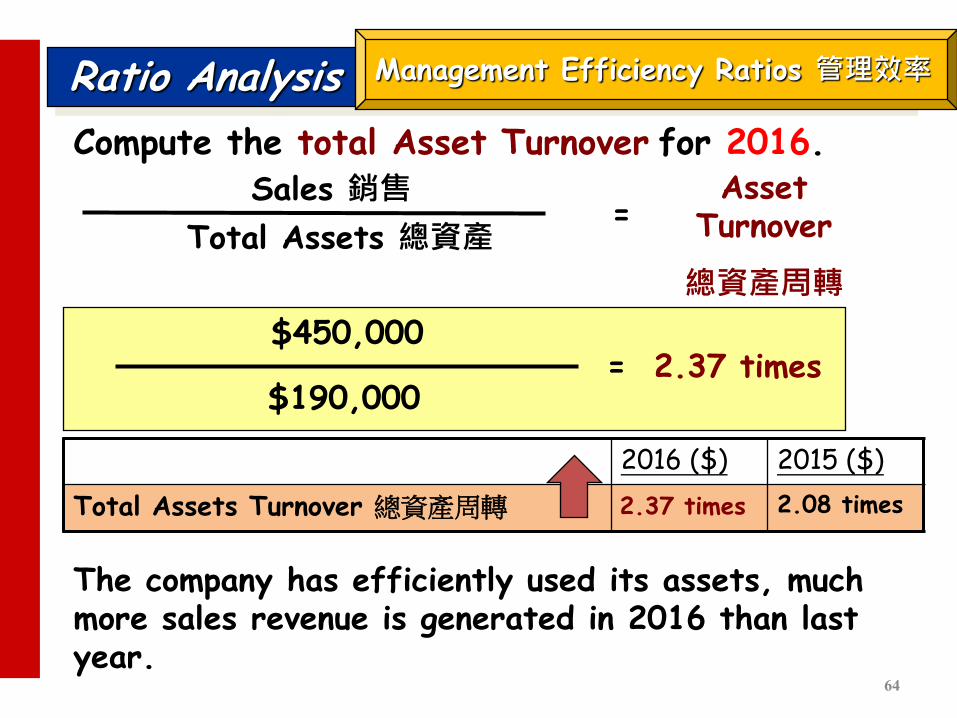

Ratio Analysis

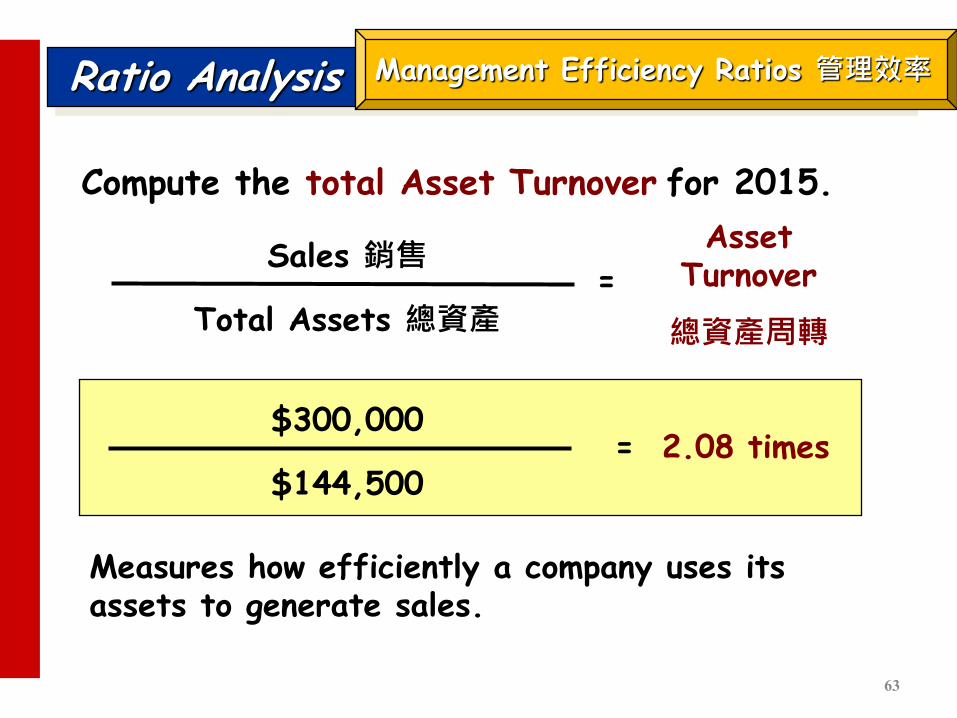

Compute the total Asset Turnover for 2015.

Measures how efficiently a company uses its assets to generate sales.

$300,000

$144,500 = 2.08 times

= Sales 銷售

Total Assets 總資產

Asset Turnover

總資產周轉

Management Efficiency Ratios 管理效率

63

Ratio Analysis

Compute the total Asset Turnover for 2016.

$450,000

$190,000 = 2.37 times

Sales 銷售

Total Assets 總資產

Asset Turnover

總資產周轉

=

2016 ($) 2015 ($)

Total Assets Turnover 總資產周轉 2.08 times 2.37 times

Management Efficiency Ratios 管理效率

The company has efficiently used its assets, much more sales revenue is generated in 2016 than last year.

64

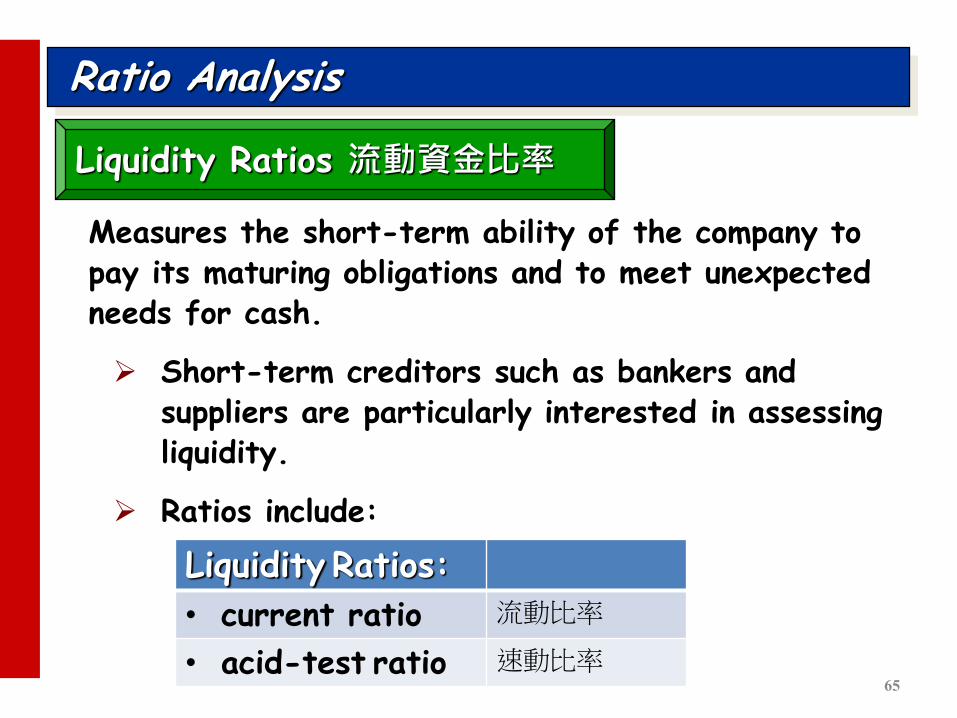

Ratio Analysis

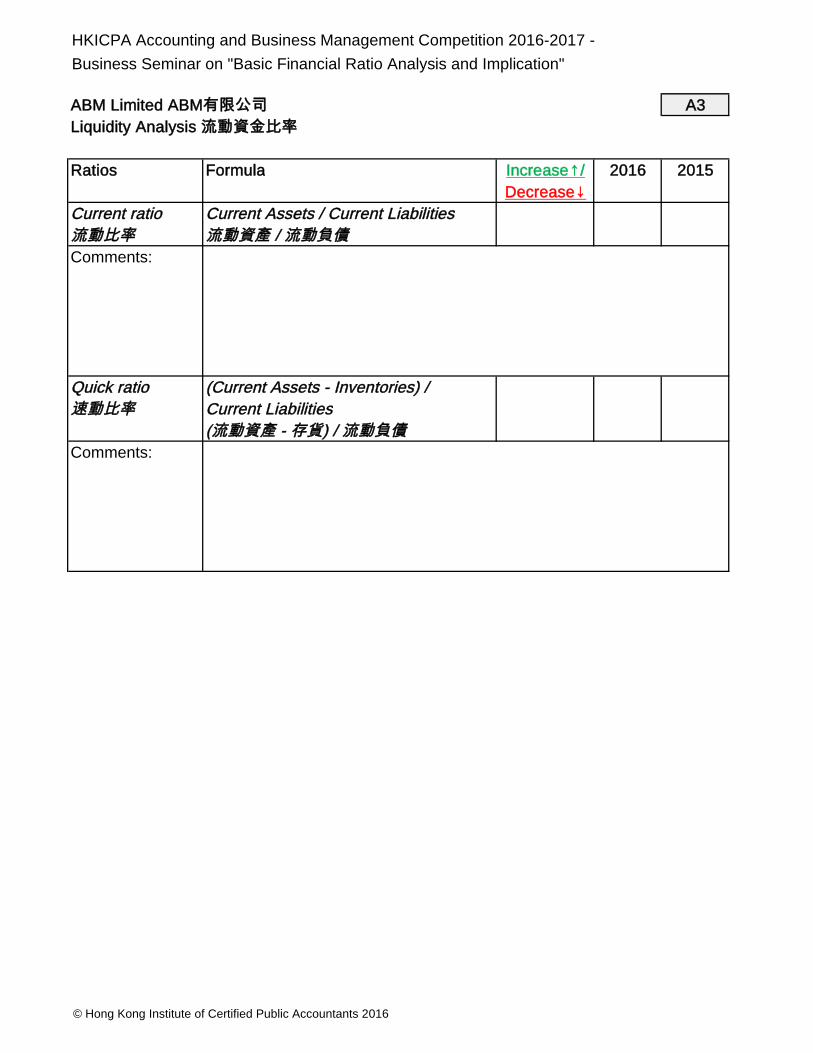

Measures the short-term ability of the company to pay its maturing obligations and to meet unexpected needs for cash.

Short-term creditors such as bankers and suppliers are particularly interested in assessing liquidity.

Ratios include:

Liquidity Ratios:

• current ratio 流動比率

• acid-test ratio 速動比率

Liquidity Ratios 流動資金比率

65

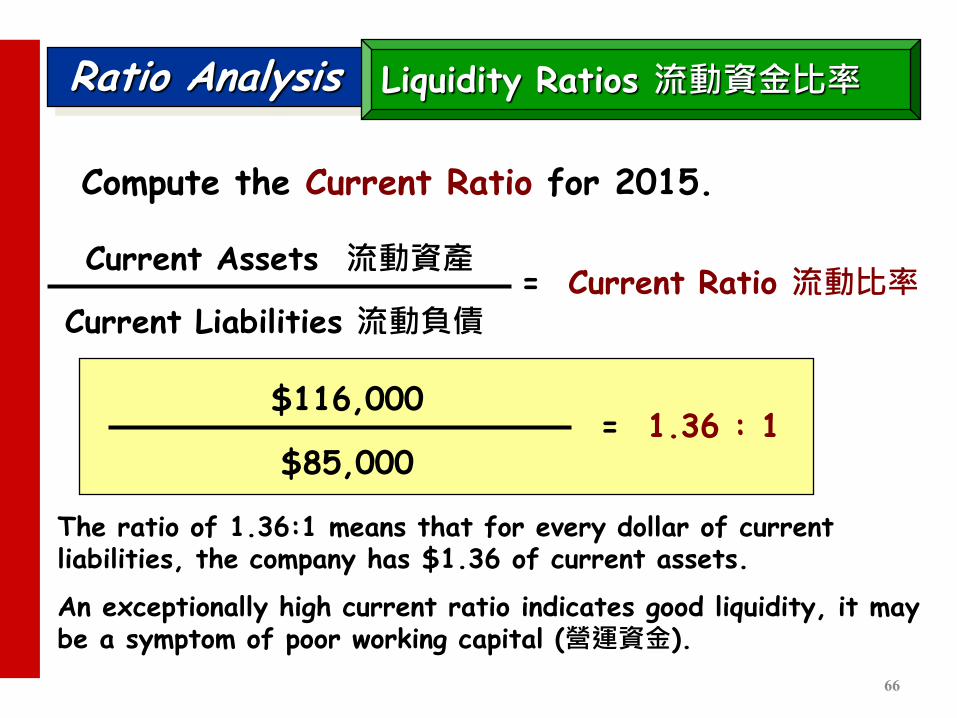

Ratio Analysis

Compute the Current Ratio for 2015.

The ratio of 1.36:1 means that for every dollar of current liabilities, the company has $1.36 of current assets.

An exceptionally high current ratio indicates good liquidity, it may be a symptom of poor working capital (營運資金).

Current Assets 流動資產

Current Liabilities 流動負債 = Current Ratio 流動比率

$116,000

$85,000 = 1.36 : 1

Liquidity Ratios 流動資金比率

66

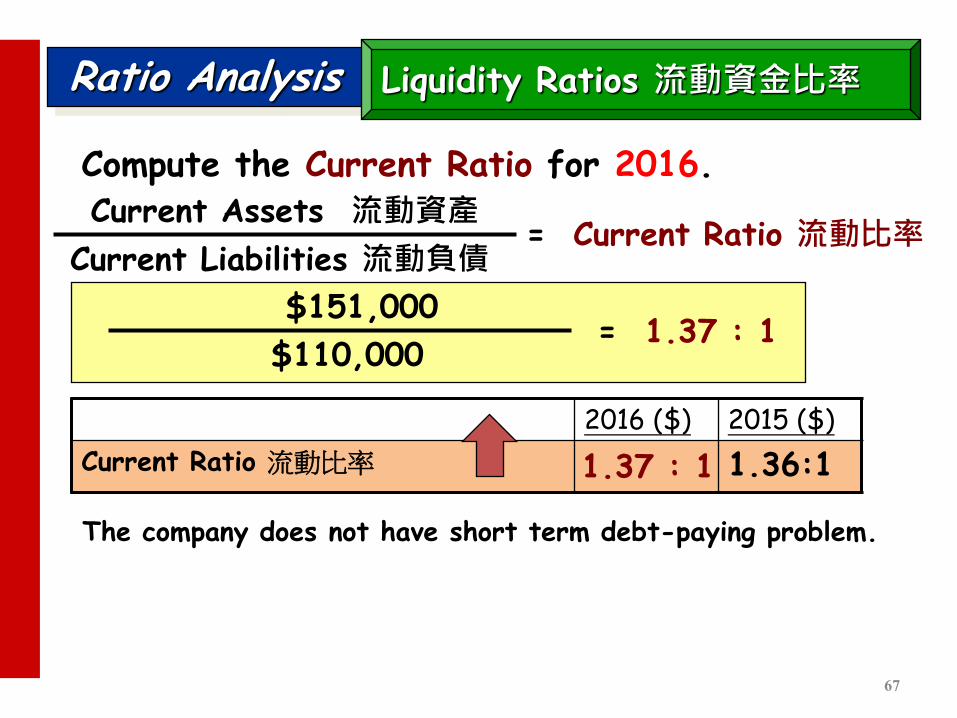

Ratio Analysis

Compute the Current Ratio for 2016. Current Assets 流動資產

Current Liabilities 流動負債 = Current Ratio 流動比率

$151,000

$110,000 = 1.37 : 1

2016 ($) 2015 ($)

Current Ratio 流動比率 1.36:1 1.37 : 1

Liquidity Ratios 流動資金比率

The company does not have short term debt-paying problem.

67

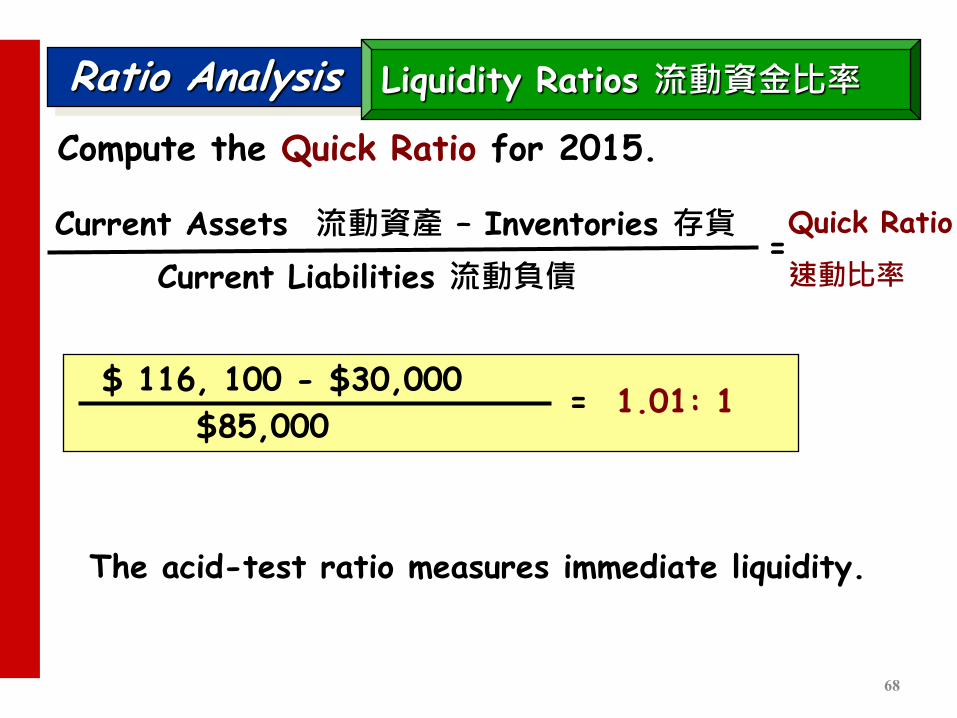

Ratio Analysis

Compute the Quick Ratio for 2015.

The acid-test ratio measures immediate liquidity.

Current Liabilities 流動負債

Quick Ratio

速動比率

$ 116, 100 - $30,000

$85,000 = 1.01: 1

= Current Assets 流動資產 – Inventories 存貨

Liquidity Ratios 流動資金比率

68

Ratio Analysis

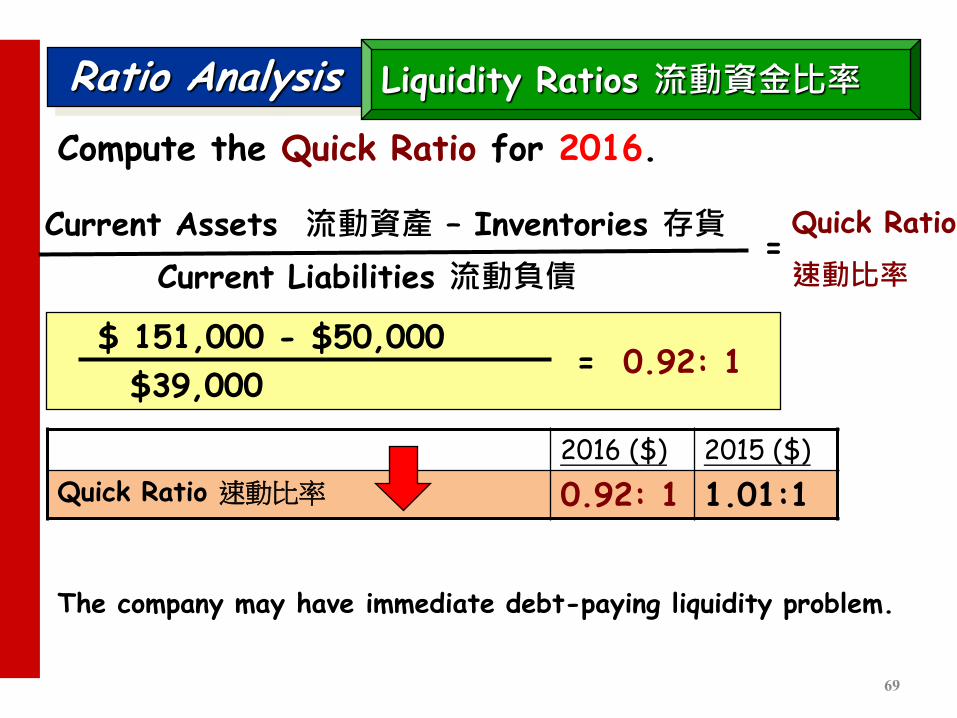

Compute the Quick Ratio for 2016.

Current Liabilities 流動負債

Quick Ratio

速動比率

$ 151,000 - $50,000

$39,000 = 0.92: 1

= Current Assets 流動資產 – Inventories 存貨

2016 ($) 2015 ($)

Quick Ratio 速動比率 1.01:1 0.92: 1

Liquidity Ratios 流動資金比率

The company may have immediate debt-paying liquidity problem.

69

Ratio Analysis

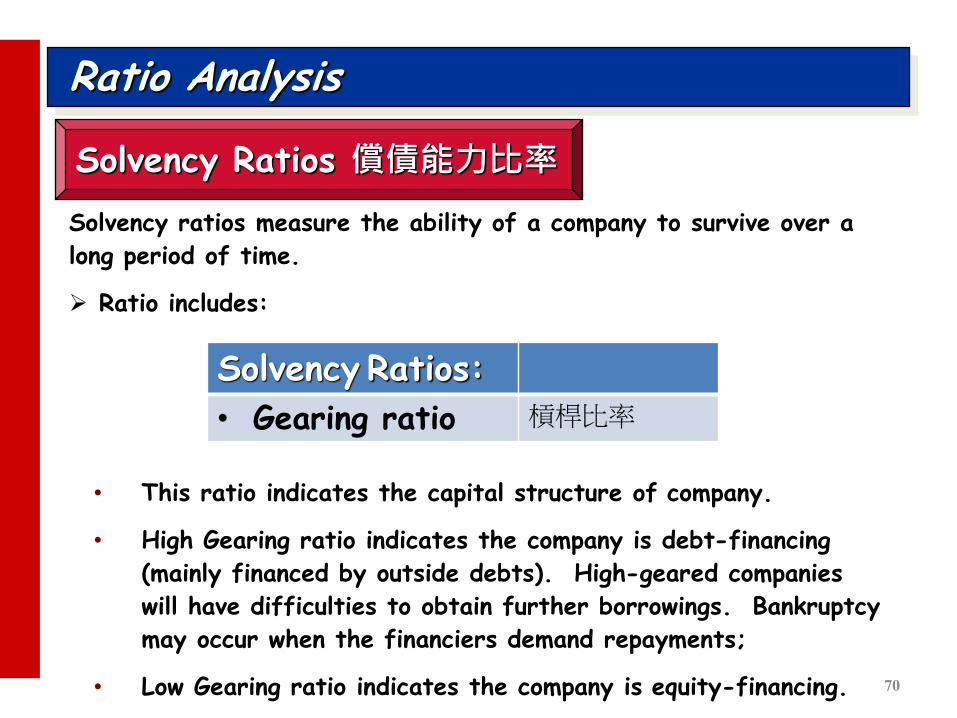

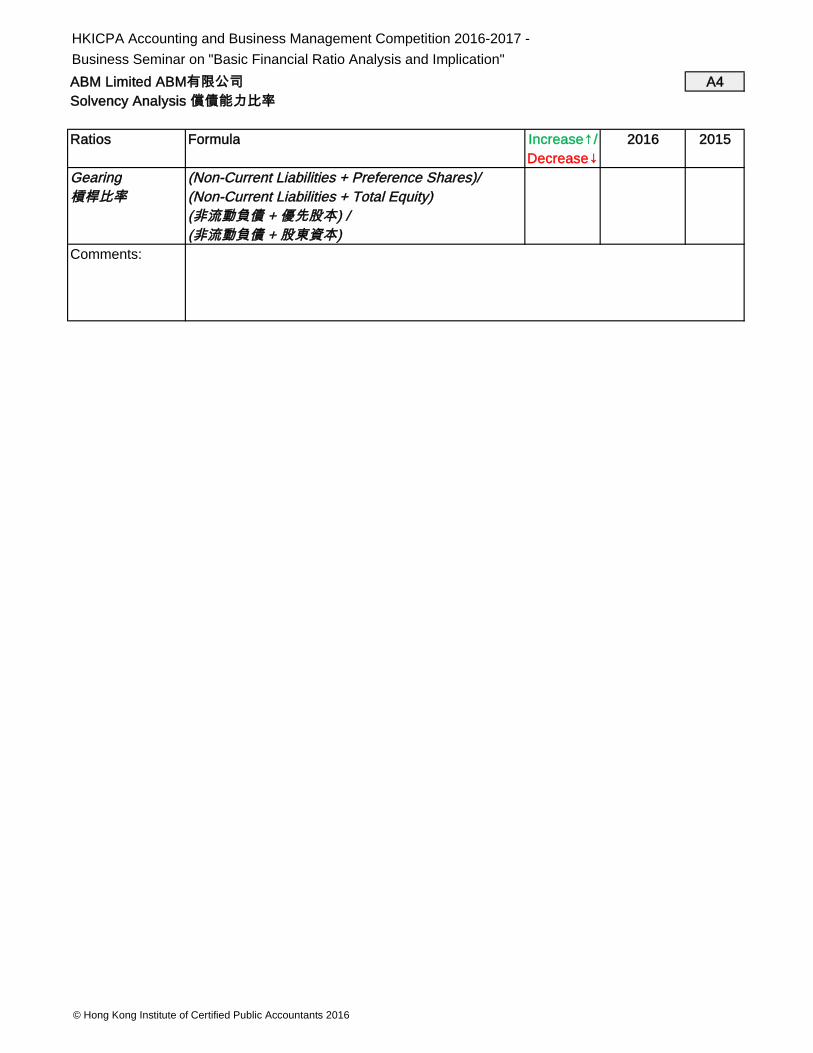

Solvency Ratios 償債能力比率

Solvency ratios measure the ability of a company to survive over a

long period of time.

Ratio includes:

• This ratio indicates the capital structure of company.

• High Gearing ratio indicates the company is debt-financing

(mainly financed by outside debts). High-geared companies

will have difficulties to obtain further borrowings. Bankruptcy

may occur when the financiers demand repayments;

• Low Gearing ratio indicates the company is equity-financing.

Solvency Ratios:

• Gearing ratio 槓桿比率

70

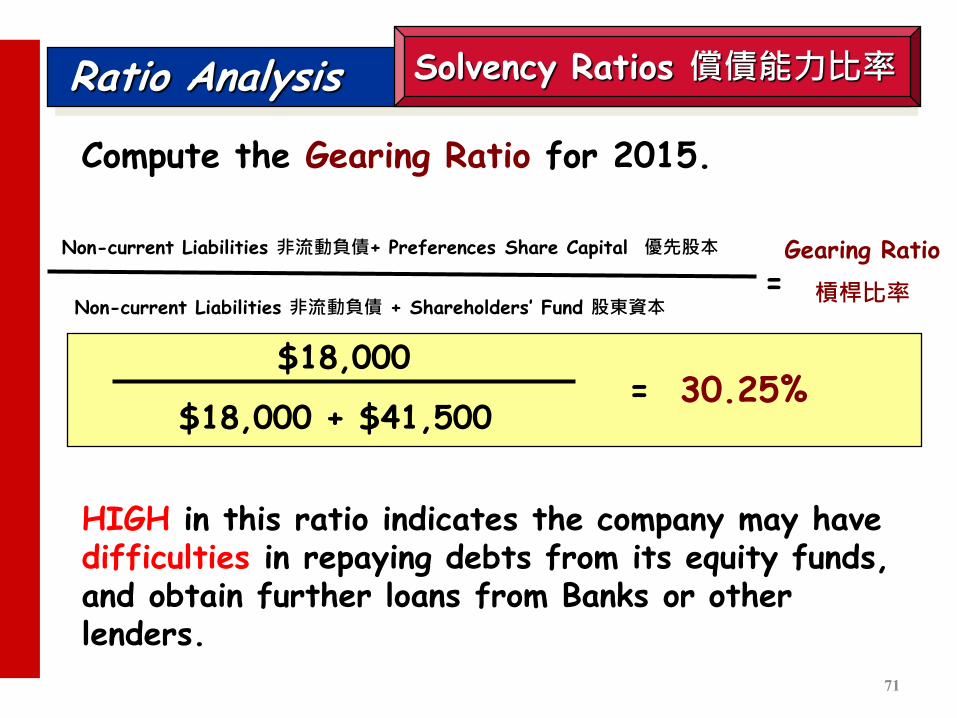

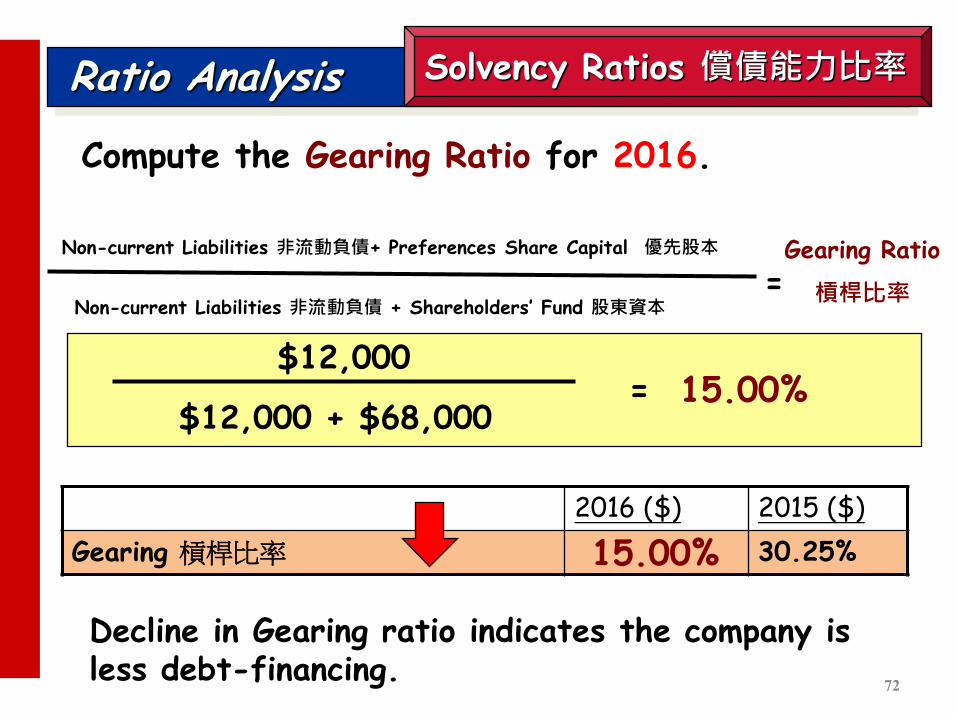

Ratio Analysis

Compute the Gearing Ratio for 2015.

HIGH in this ratio indicates the company may have difficulties in repaying debts from its equity funds, and obtain further loans from Banks or other lenders.

$18,000

$18,000 + $41,500 = 30.25%

Non-current Liabilities 非流動負債+ Preferences Share Capital 優先股本 Gearing Ratio

槓桿比率 = Non-current Liabilities 非流動負債 + Shareholders’ Fund 股東資本

Solvency Ratios 償債能力比率

71

Ratio Analysis

Compute the Gearing Ratio for 2016.

$12,000

$12,000 + $68,000 = 15.00%

Non-current Liabilities 非流動負債+ Preferences Share Capital 優先股本 Gearing Ratio

槓桿比率 = Non-current Liabilities 非流動負債 + Shareholders’ Fund 股東資本

2016 ($) 2015 ($)

Gearing 槓桿比率 30.25%

72

15.00%

Solvency Ratios 償債能力比率

Decline in Gearing ratio indicates the company is less debt-financing.

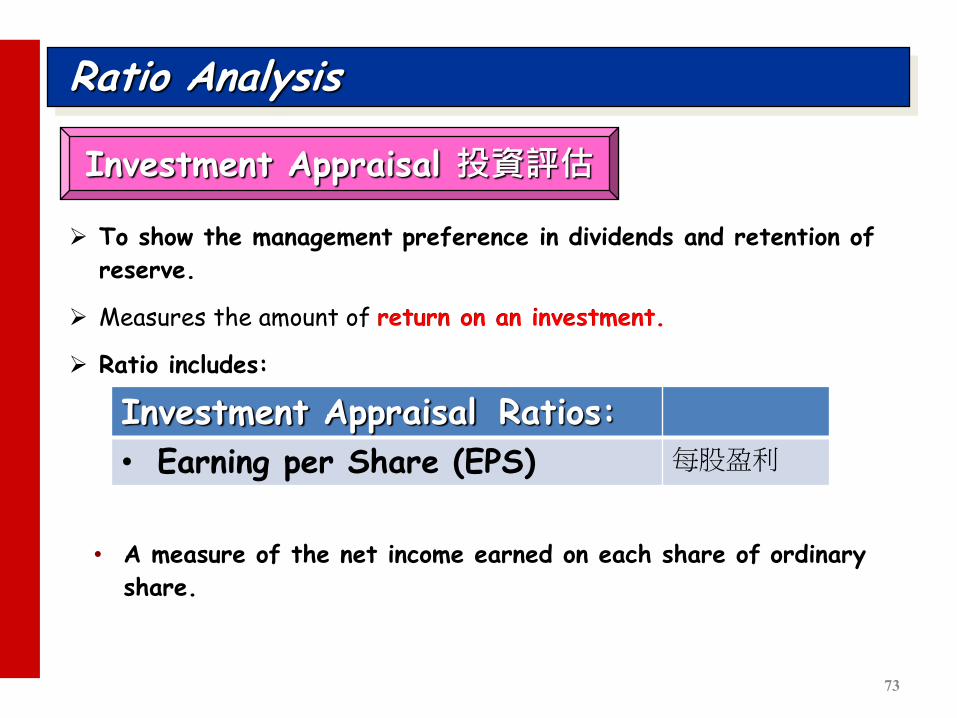

Ratio Analysis

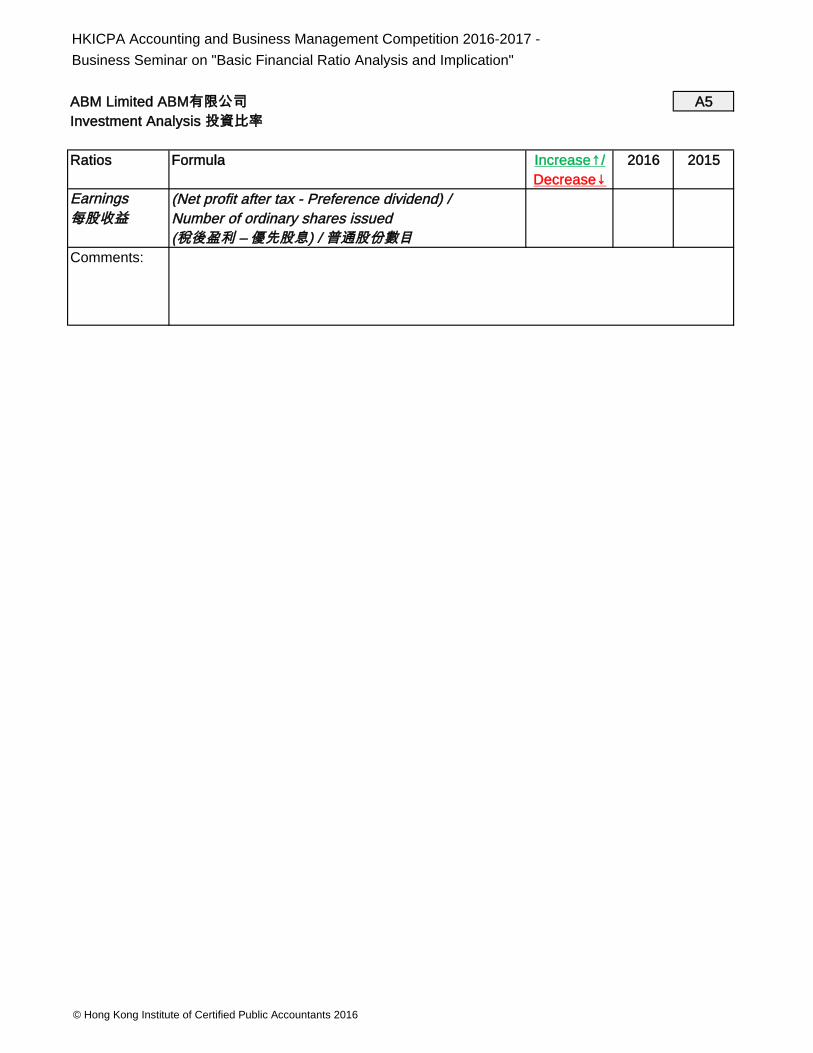

To show the management preference in dividends and retention of

reserve.

Measures the amount of return on an investment.

Ratio includes:

• A measure of the net income earned on each share of ordinary

share.

Investment Appraisal Ratios:

• Earning per Share (EPS) 每股盈利

Investment Appraisal 投資評估

73

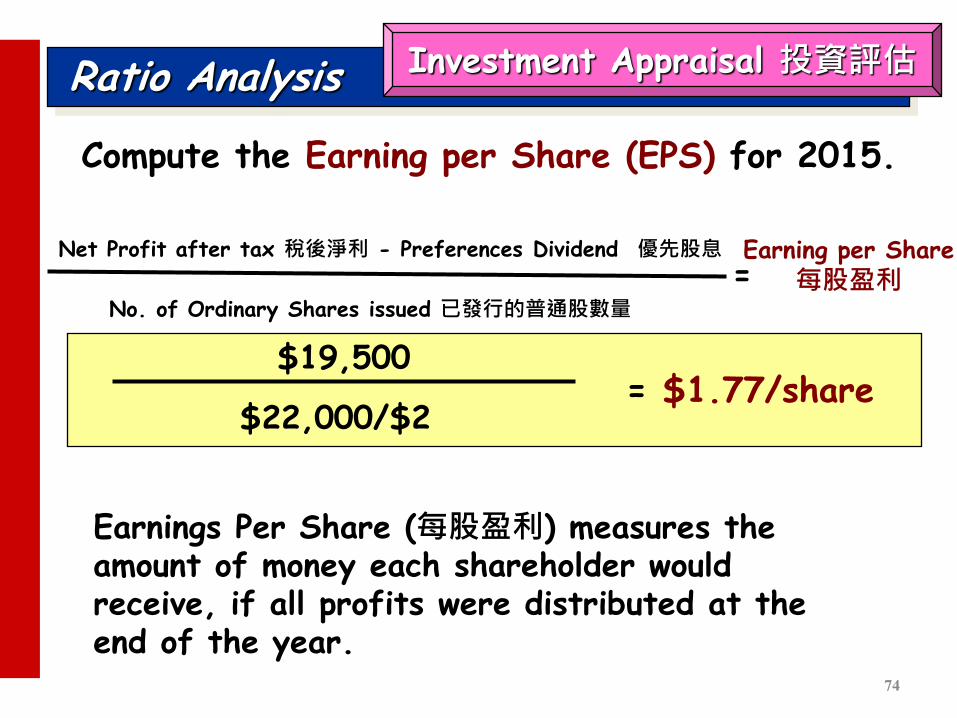

Ratio Analysis

Compute the Earning per Share (EPS) for 2015.

$19,500

$22,000/$2 = $1.77/share

Net Profit after tax 稅後淨利 - Preferences Dividend 優先股息 Earning per Share每股盈利 =

No. of Ordinary Shares issued 已發行的普通股數量

Earnings Per Share (每股盈利) measures the amount of money each shareholder would receive, if all profits were distributed at the end of the year.

Investment Appraisal 投資評估

74

Ratio Analysis

Compute the Earning per Share (EPS) for 2016.

$26,500

$22,000/$2 = $2.41/share

Net Profit after tax 稅後淨利 - Preferences Dividend 優先股息 Earning per Share每股盈利 =

No. of Ordinary Shares issued 已發行的普通股數量

2016 ($) 2015 ($)

Earnings Per Share 每股盈利 $1.77/share

75

$2.41/share

Investment Appraisal 投資評估

Much more net income is generated from each issued ordinary share in 2016 than last year.

76

Importance of Relative Financial Ratios

• In order to make sense of a ratio, we must compare it with some appropriate benchmarks (合適基準)

• Examine a company’s performance relative to:

• Aggregate economy (經濟情況)

• Its industry (行業)

• Its major competitors (競爭對手) within the industry

• Its own past performance (過往表現)

77

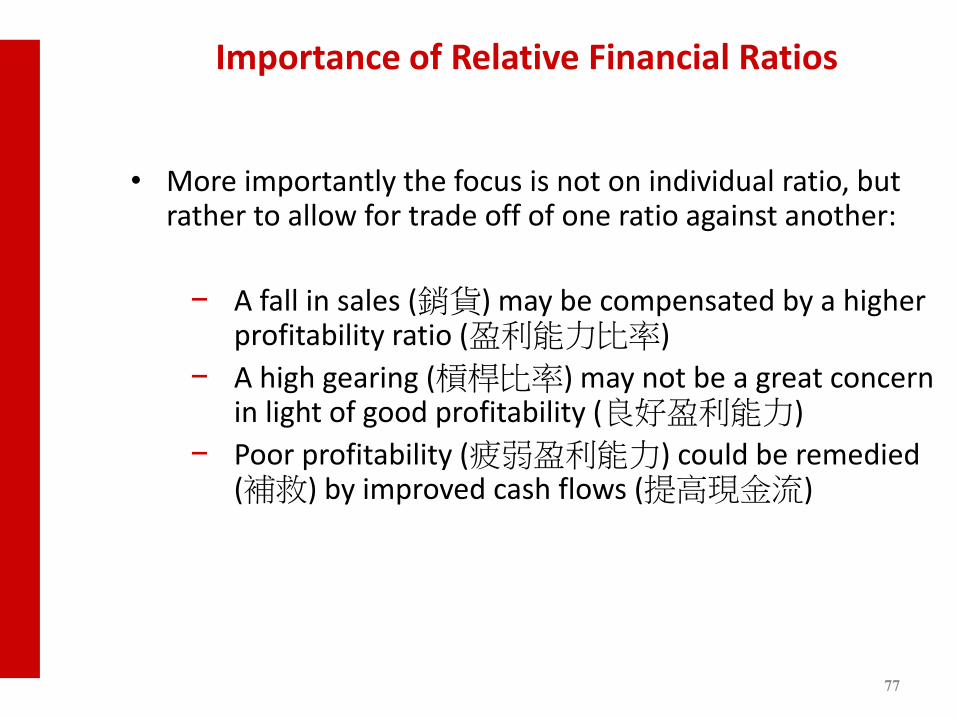

Importance of Relative Financial Ratios

• More importantly the focus is not on individual ratio, but rather to allow for trade off of one ratio against another:

− A fall in sales (銷貨) may be compensated by a higher profitability ratio (盈利能力比率)

− A high gearing (槓桿比率) may not be a great concern in light of good profitability (良好盈利能力)

− Poor profitability (疲弱盈利能力) could be remedied (補救) by improved cash flows (提高現金流)

78

ABM Limited ABM Q1Consolidated Income StatementFor the Year Ended 31 December

2016 2015HKD HKD

Turnover 450,000$ 300,000$Cost of sales 380,000 250,000Gross profit 70,000 50,000Selling and distribution 7,000 6,000Administrative expenses 30,000 20,000Operating Profit 33,000 24,000Other expenses and losses:

Finance costs 1,500 1,500Profit before tax 31,500 22,500Income tax expense 5,000 3,000Profit for the year 26,500$ 19,500$

ABM Limited ABM Q2Consolidated Balance Sheetas at 31 December

2016 2015 2014HKD HKD HKD

AssetsNON-CURRENT ASSETSProperty, plant and equipment (net) 39,000$ 28,400$ 20,000

Total non-current assets 39,000$ 28,400$ 20,000$CURRENT ASSETS

Inventory 50,000$ 30,000$ 20,000Trade receivable (net) ( ) 100,000 85,000 81,000Cash 1,000 1,000 4,000

Total current assets 151,000$ 116,000$ 105,000$Total Assets 190,000$ 144,400$ 125,000$

Liabilities and Stockholders' EquityNON-CURRENT LIABILITIESBonds payable 12,000$ 18,000$ 10,000

Total non-current liabilities 12,000$ 18,000$ 10,000$CURRENT LIABILITIES

Trade payable 80,000$ 70,000$ 60,000Income taxes payable 30,000 15,000 12,000

Total current liabilities 110,000$ 85,000$ 72,000$Total Liabilities 122,000$ 103,000$ 82,000$

SHAREHOLDERS' EQUITYShare capital ($2 par ) 22,000$ 22,000$ 20,000$Other reserves 6,000 4,500 3,000Retained earnings 40,000 15,000 20,000$

Total shareholders' fund 68,000$ 41,500$ 43,000$Total liabilities and equity 190,000$ 144,500$ 125,000$

Capital Emplyed 80,000$ 59,500$ 53,000$Avverage Capital Employed 69,750$ 56,250$

HKICPA Accounting and Business Management Competition 2016-2017 -Business Seminar on "Basic Financial Ratio Analysis and Implication"

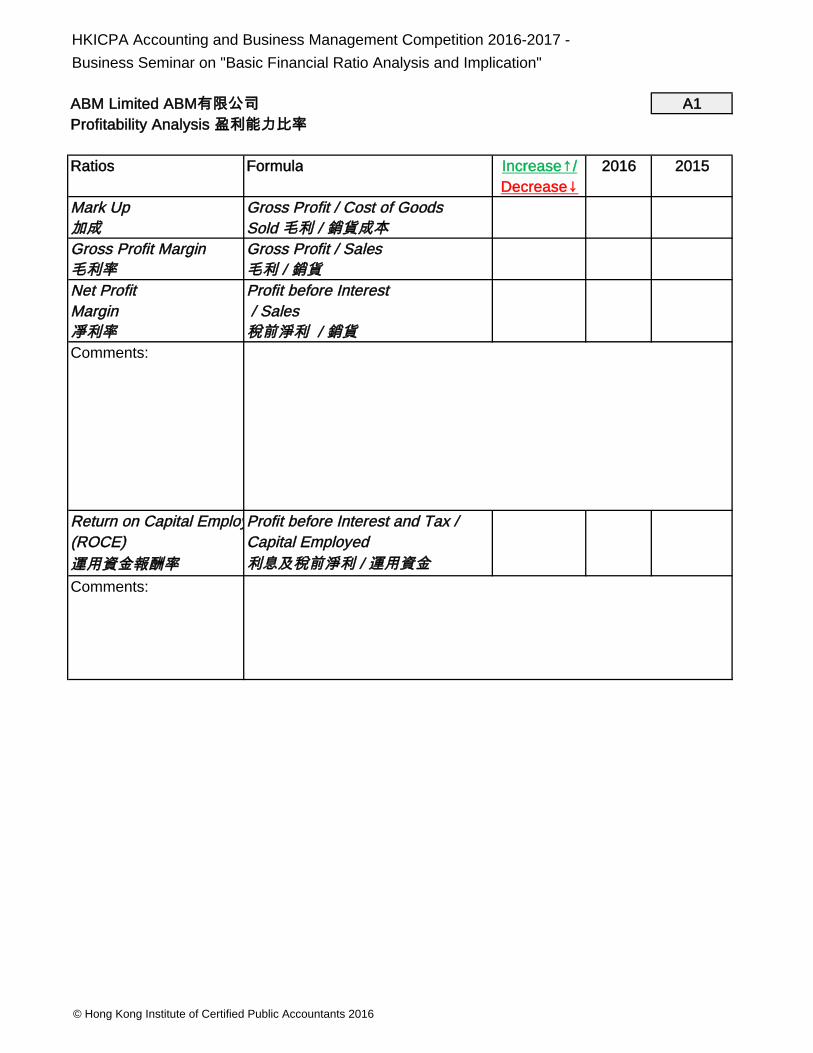

ABM Limited ABM A1Profitability Analysis

Ratios Formula Increase / 2016 2015Decrease

Mark Up Gross Profit / Cost of GoodsSold /

Gross Profit Margin Gross Profit / Sales /

Net Profit Profit before InterestMargin / Sales

/ Comments:

Return on Capital EmployedProfit before Interest and Tax /(ROCE) Capital Employed

Comments: /

© Hong Kong Institute of Certified Public Accountants 2016

HKICPA Accounting and Business Management Competition 2016-2017 -Business Seminar on "Basic Financial Ratio Analysis and Implication"

ABM Limited ABM A2Management Efficiency Analysis

Ratios Formula Increase / 2016 2015Decrease

Inventory Cost of Goods Sold / InventoryTurnover Ratio /

Inventory Inventory / Cost of Goods SoldTurnover Period x 365

/ x 365Comments:

Trade Credit Sales / Trade ReceivablesReceivables Ratio /

Trade Trade Receivables / Credit SalesReceivables x 365Collection Period / x 365

Comments:

Trade Credit Purchases / Trade PayablesPayables Ratio /

Trade Trade Payables / Credit PurchasesPayables x 365Repayment Period / x 365

Comments:

Total Assets Sales / Total AssetsTurnover / Comments:

© Hong Kong Institute of Certified Public Accountants 2016

HKICPA Accounting and Business Management Competition 2016-2017 -Business Seminar on "Basic Financial Ratio Analysis and Implication"

ABM Limited ABM A3Liquidity Analysis

Ratios Formula Increase / 2016 2015Decrease

Current ratio Current Assets / Current Liabilities /

Comments:

Quick ratio (Current Assets - Inventories) / 0.92 1.01Current Liabilities

- ) / Comments:

© Hong Kong Institute of Certified Public Accountants 2016

HKICPA Accounting and Business Management Competition 2016-2017 -Business Seminar on "Basic Financial Ratio Analysis and Implication"ABM Limited ABM A4Solvency Analysis

Ratios Formula Increase / 2016 2015Decrease

Gearing (Non-Current Liabilities + Preference Shares)/ 15.00% 30.25%(Non-Current Liabilities + Total Equity)

+ ) / + )

Comments:The Gearing Ratio ( ) also reflected the companyhas decreased its reliance on debt in the current year.

© Hong Kong Institute of Certified Public Accountants 2016

HKICPA Accounting and Business Management Competition 2016-2017 -Business Seminar on "Basic Financial Ratio Analysis and Implication"

ABM Limited ABM A5Investment Analysis

Ratios Formula Increase / 2016 2015Decrease

(Net profit after tax - Preference dividend) /Number of ordinary shares issued

– ) / Comments:

Earnings

© Hong Kong Institute of Certified Public Accountants 2016

![Basel 3 & Implication[1]](https://static.fdocuments.in/doc/165x107/577d1e721a28ab4e1e8e9042/basel-3-implication1.jpg)