BASIC DATA - Citibank · Chile’s robust domestic fundamentals and political and institutional...

30

C H I L E

Transcript of BASIC DATA - Citibank · Chile’s robust domestic fundamentals and political and institutional...

C H I L E

C H I L E

180

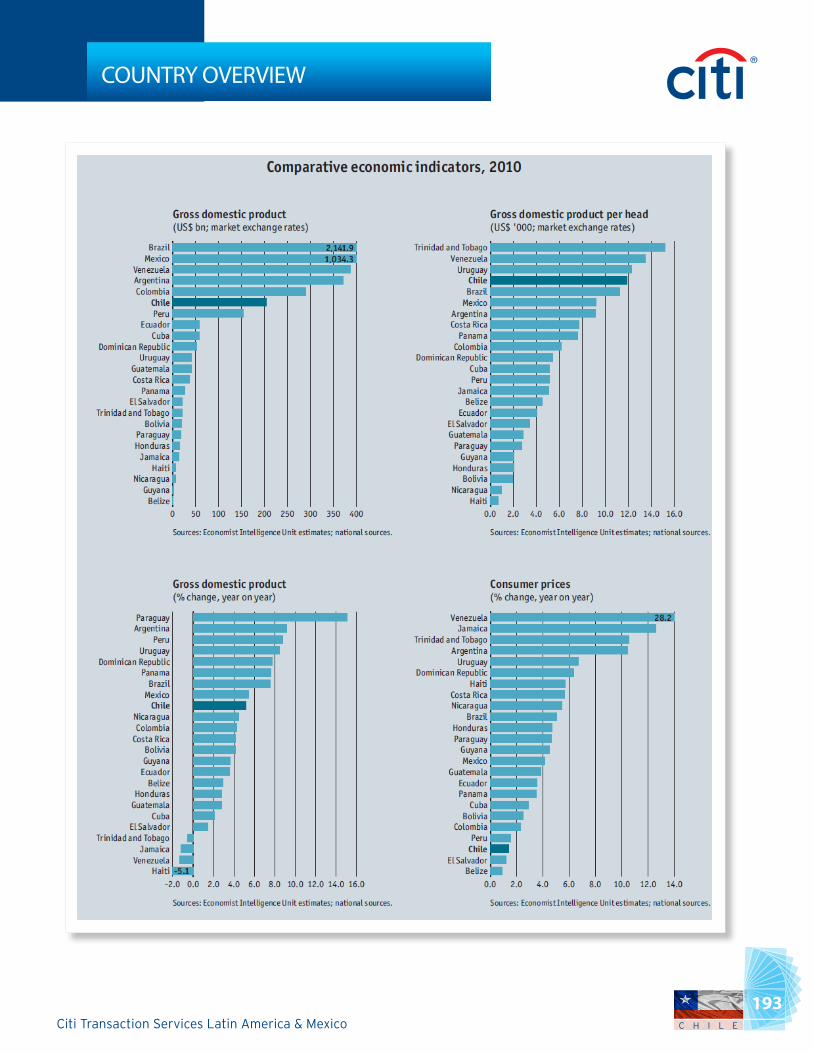

COUNTRY OVERVIEW

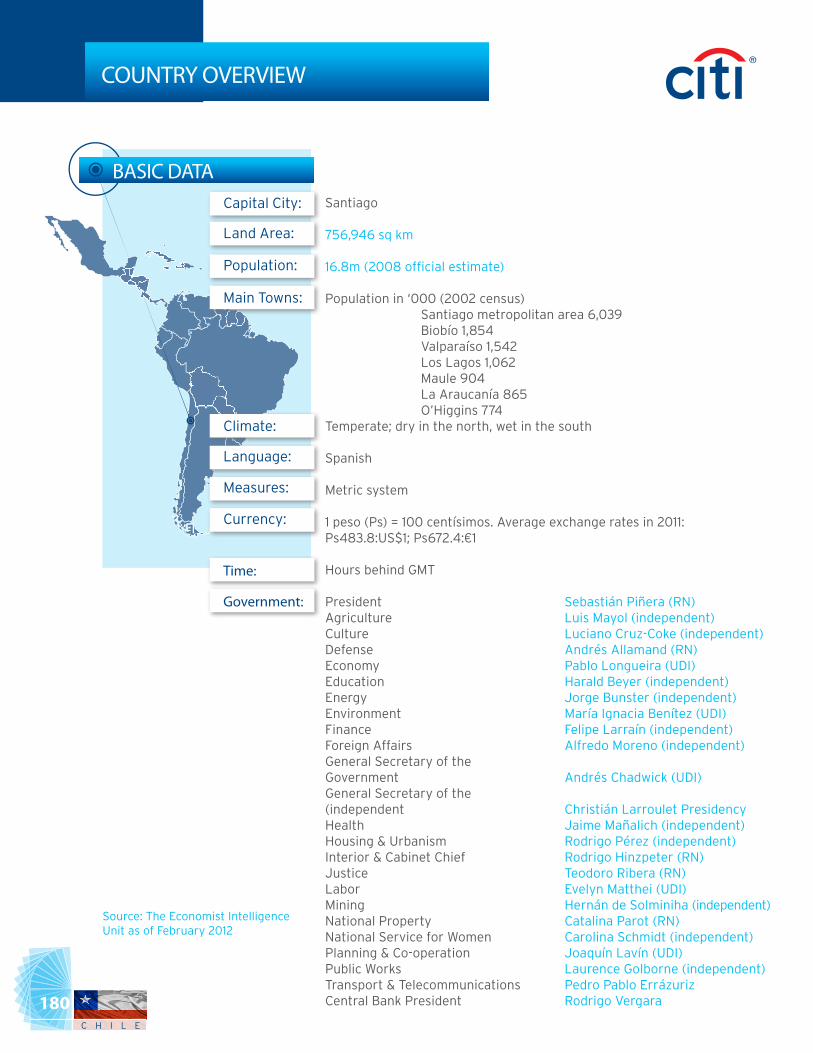

BASIC DATACapital City:

Land Area:

Population:

Main Towns:

Climate:

Language:

Measures:

Currency:

Time:

Government:

Santiago

756,946 sq km

16.8m (2008 official estimate)

Population in ‘000 (2002 census) Santiago metropolitan area 6,039 Biobío 1,854 Valparaíso 1,542 Los Lagos 1,062 Maule 904 La Araucanía 865 O’Higgins 774Temperate; dry in the north, wet in the south

Spanish

Metric system

1 peso (Ps) = 100 centísimos. Average exchange rates in 2011: Ps483.8:US$1; Ps672.4:€1

Hours behind GMT

President Sebastián Piñera (RN)Agriculture Luis Mayol (independent)Culture Luciano Cruz-Coke (independent)Defense Andrés Allamand (RN)Economy Pablo Longueira (UDI)Education Harald Beyer (independent)Energy Jorge Bunster (independent)Environment María Ignacia Benítez (UDI)Finance Felipe Larraín (independent)Foreign Affairs Alfredo Moreno (independent) General Secretary of the Government Andrés Chadwick (UDI)General Secretary of the (independent Christián Larroulet PresidencyHealth Jaime Mañalich (independent)Housing & Urbanism Rodrigo Pérez (independent)Interior & Cabinet Chief Rodrigo Hinzpeter (RN)Justice Teodoro Ribera (RN)Labor Evelyn Matthei (UDI)Mining Hernán de Solminiha (independent)National Property Catalina Parot (RN)National Service for Women Carolina Schmidt (independent)Planning & Co-operation Joaquín Lavín (UDI)Public Works Laurence Golborne (independent)Transport & Telecommunications Pedro Pablo ErrázurizCentral Bank President Rodrigo Vergara

Source: The Economist Intelligence Unit as of February 2012

C H I L E

181Citi Transaction Services Latin America & Mexico

B. POLITICAL STRUCTURE

Official Name Republic of Chile

Form of Government Presidential system, based on 1980 ConstitutionThe Executive The president, elected for a period of four years, is head of state and appoints the cabinet

National Legislature Bicameral legislature (Congress): a Senate (the upper house) comprising 38 members elected for eight years and partly renewed every four years; and a Chamber of Deputies (the lower house), with 120 members who are all elected every four years

Legal System The 21 Supreme Court judges are appointed by the president from lists submitted by the Supreme Court, and confirmed by a two-thirds majority in the upper house; 16 regional courts of appeal and members of the lower courts are appointed by the Supreme Court

National Elections October 2012 (municipal); November 2013 (presidential and congressional)

National Government Sebastián Piñera of the Renovación Nacional (RN) heads the Coalición por el Cambio coalition; he took office as president on March 11th 2010

Main Political Organizations Government: Coalición por el Cambio, comprising the Renovación Nacional (RN) and the Unión Demócrata Independiente (UDI); Chile Primero (CH1). Opposition: Concertación de Partidos por la Democrática (Concertación) coalition, comprising the Partido Demócrata Cristiano (PDC), the Partido Radical Social Demócrata (PRSD), the Partido Socialista (PS) and the Partido por la Democracia (PPD); Partido Comunista (PC); Partido Regionalista Independiente (PRI)

COUNTRY OVERVIEW

C H I L E

182

C. POLITICAL OUTLOOK 2012 – 2016

Despite an end to the student demonstrations and strikes that paralyzed the education system during the second half of 2011, the popularity of the president, Sebastián Piñera, of the centre-right Coalición por el Cambio (Coalición), remains critically low and could endanger his ability to push through a reform agenda focused on improving structural limitations to growth. It will also leave the government vulnerable to pressure from centre-left opposition, the Concertación de Partidos por la Democracia (Concertación), as well as more right-wing elements within Mr. Piñera’s own coalition, particularly now that both sides have begun gearing up for the 2013 presidential and legislative elections. The education crisis, in particular, has highlighted the difficulties in achieving major structural reforms, as neither coalition appeared willing to undertake a major overhaul of the highly decentralized and privately funded education system (which remains a legacy of the of the Pinochet-era), contrary to the demands of students. The government did, however, achieve success in accepting only modest concessions, such as increasing the size of the education budget for 2012. However, in the absence of a deeper reform, dissatisfaction with the system will linger throughout the outlook period, raising the possibility of further protests. This outbreak of unrest comes against the backdrop of one of the most politically stable systems in the region, with a two-coalition structure that has been characterized in the past two decades by a pragmatic and co-operative approach to politics, and a consensus to promote a pro-market, business-friendly environment.

Notwithstanding the education-related disturbances, the risk of severe political and social instability is low. Both coalitions are prone to internal friction, owing to the different degrees of radicalism between their constituent parties, but a breakdown of the two-coalition system is highly unlikely in the short term. Nevertheless, some changes in party arrangements (such as realignments or secessions by smaller fringe parties) may emerge if differences become irremediable. Overall, strong democratic institutions and a low risk of social unrest will ensure that political disputes do not get out of hand, but low popularity, tense relations with the opposition, and growing apathy towards the political class as a whole could lead to a more difficult environment for effective governance and more conflictive inter-coalition relations than what has been usual in the past. This could complicate Mr. Piñera’s efforts in pushing forward more contentious reforms in key sectors, such as energy and the labor market, during the second half of his term. Mr. Piñera will seek to maintain solid trade relations and avoid diplomatic disputes with other Latin American countries, in particular those with whom underlying tensions persist, such as Argentina (owing to natural-gas supply issues) and Bolivia (owing to a long-standing territorial dispute). Trade and investment links

COUNTRY OVERVIEW

C H I L E

183Citi Transaction Services Latin America & Mexico

with Peru will remain strong, despite an unresolved dispute regarding a maritime border. Beyond the region, Mr. Piñera is expected to continue to broaden and deepen trade links to support export-led economic development, which includes fostering closer integration among Pacific economies, both in the region (Mexico, Peru and Colombia) and abroad, such as through the Trans-Pacific Partnership (TPP) and additional free-trade agreements (FTAs) with Asian countries such as Malaysia and Vietnam.

D. ECONOMIC PERFORMANCE

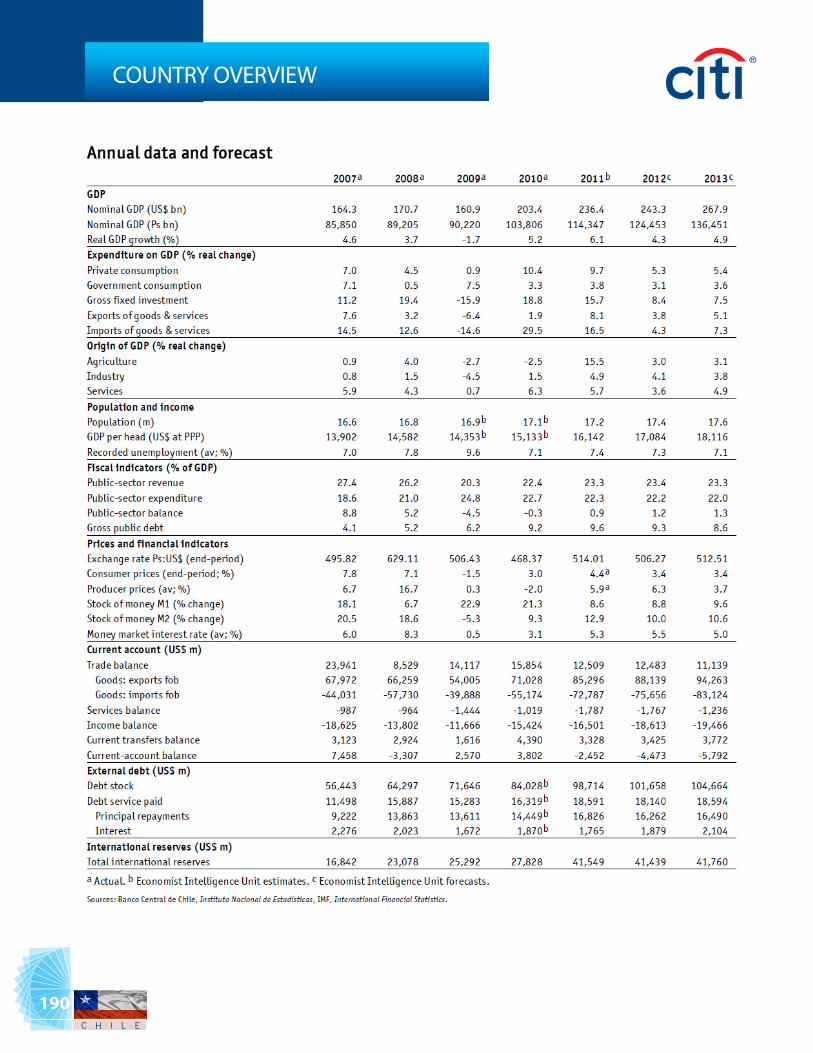

Monthly economic activity grew at just 4% year on year in November, the second lowest rate in 2011, although in seasonally adjusted terms growth came in strong at 0.8% compared with October. Overall, domestic demand growth is trending lower owing to a darkening global scenario, but remains resilient on the back of a rise in real wages and employment levels. Retail sales increased at a brisk pace of 8.5%, which was the result of a 13.1% rise in sales of durable goods and 7.5% in non-durables. Construction activity also remained strong, fuelled in part by the continuing process of reconstruction of homes and infrastructure from the February 2010 earthquake. Construction activity rose by 9.5% year on year in October, and 8.4% in the first ten months of 2011. according to the monthly index of construction activity compiled by the local construction chamber, the Cámara Chilena de la Construcción (CChC).

However, on a more negative note, mining output continued to slide owing to declining ore grades. There is a massive investment effort underway to increase mining capacity, but new projects will only come on stream by 2013.

With investment at record levels, job creation has been highly dynamic under the current administration, resulting in a rise of nearly 600,000 in the number of people in employment in the 21 months to November 2011. This reduced average annual unemployment to 7.2% in 2011, the lowest rate of the past 13 years, and helped to raise real wages by 2.3% per year in 2010-11. This will probably be reflected in lower poverty levels and an improvement of the country’s income distribution in the national socio-economic characterization survey (CASEN) currently being carried, and whose results are due to be published in the second quarter of 2012. The previous survey, released in 2010, had been unduly influenced by the 2009 recession, which showed a spike in both poverty and inequality, despite a gradual reduction over the course of the last decade.

COUNTRY OVERVIEW

C H I L E

184

COUNTRY OVERVIEW

E. ECONOMIC FORECAST

Chilean capital markets slumped badly in the second half of 2011, in line with global developments, reversing the gains from a buoyant first half but still ending on a positive note from non-trading activity. In 2011, the Bolsa de Comercio de Santiago (BCS, the Santiago Stock Exchange) handled initial public offerings (IPOs) and capital increases totaling US$7.5bn, 4% more than in 2010, despite the cancellation of two major IPOs that Agrosuper (food) and Ingevec (construction) had scheduled for the second half of the year. The paucity in these operations is expected to persist for at least the first half of 2012 while global conditions remain sour. Mergers and acquisitions reached US$13.3bn in 2011, doubling the US$6.7bn recorded in 2010. The rise in mergers and acquisitions was mostly explained by the controversial sale of a 25% stake in Anglo American Sur (formerly known as La Disputada de las Condes) by Anglo American, a UK-based mining company, to Mitsubishi (Japan) for US$5.4bn. This was supposed to prevent the acquiring by the state copper corporation, Codelco, of a 49% stake in Anglo American Sur in the course of January, as it is entitled by the contract signed by Anglo American when it acquired La Disputada. Overall, the BCS’s market capitalization fell by 16.1% in US-dollar terms (11.3% in local currency) as of November 2011, while the IGPA, Chile’s main composite index, fell by 12.4% during the year as a whole.

C H I L E

185Citi Transaction Services Latin America & Mexico

COUNTRY OVERVIEW

Foreign direct investment (FDI) projects authorized by the Ministry of the Economy totaled US$13.8bn (around 6% of estimated GDP) in 2011.4% above the 2010 figure and a new record. This was mostly explained by investments in mining ventures, which reached US$9.7bn or 70.1% of the total. Barrick (Canada) was by far the main investor company getting approval for a US$4.4bn participation in the Cerro Casale gold and copper mining project, and US$800m to develop the Zaldívar copper mine. Kinross, another Canadian mining company, will also participate in Cerro Casale (for which it got approval for a US$1.5bn investment), and Sumimoto Metal Mining (Japan) presented a US$1bn project to acquire a 45% stake in the Sierra Gorda copper and molybdenum mine.

The services sector accounted for 16.7% of authorized investments in 2011, including a US$788m venture by ZS Insurance America, a company incorporated in Spain, in which Zurich Financial Services (Switzerland) holds 51% ownership and Banco Santander (Spain) 49%.to acquire 100% of a Chilean insurance company, Santander Seguros de Vida, in November. Utilities (electricity, gas and water) accounted for 5.9% of authorized investments, transport and communications 3.3%, industry 2.8% and other sectors 1.2%. The government is now focusing its efforts on attracting foreign investment from Asia, particularly from China, which along with Hong Kong, accounted for less than 1% (US$1.2bn) of the total stock of FDI in 2010.

C H I L E

186

COUNTRY OVERVIEW

Economic Growth

Chile’s robust domestic fundamentals and political and institutional stability will be supportive of growth in 2012-16, although strong headwinds from a weak global outlook place short-term risks on the downside. Following an exceptionally good year in 2011 (for which we estimate a GDP growth rate of 6.1%), growth will moderate to 4.3% in 2012, as currently buoyant consumption and investment return to normal levels, and statistical carryover effects from the 2010 earthquake disappear. Growth will then pick up to an average of 4.8% during 2013-16, close to Chile’s trend level. The government’s 6% growth target to be achieved by the end of its term thus appears unlikely, but current rates will still be sufficient to encourage rising incomes and sustained job creation. However, income (and regional) inequality will remain a major socioeconomic concern, which will also prevent a more rapid expansion of the middle class and become a source of social tension. Chileans will nevertheless continue to enjoy the highest standard of living as well as income (in purchasing power terms) in Latin America throughout the forecast period. Our forecast, particularly in the shorter term, is subject to risks emerging from a global slowdown, since Chile’s highly open economy is heavily dependent on external demand, as well as on commodity prices of its main export, copper, which in recent months have fallen from their early-2011 peak. Closer synchronization of the business cycle with China in recent years means that recession in the US or Europe would have only a moderate adverse impact, insofar as Chinese demand remains resilient, although a more dramatic shock, such as a euro zone break-up (to which our baseline forecast attaches a 40% probability) would carry significant spillover risks. Overall, domestic demand will drive growth throughout the forecast period, deriving from a surge in public and private investment, but also from robust levels of private consumption from an increasingly affluent consumer base (benefiting from rising real wages and ready access to credit). The strength of domestic demand will sustain import volume growth, which will outpace growth in export volumes (particularly during the reconstruction phase). As a result, the contribution of net trade to GDP growth will be negative in 2012-16.

On the supply side, public and private reconstruction-related investment will provide a major boost to the construction sector, which suffered a steep slump during the 2009 recession. The mining and energy sectors will also benefit from projects to expand capacity, with copper mining particularly well placed to meet demand from a rapidly urbanizing China. Agriculture, Chile’s second largest source of exports, is expected to grow rapidly in 2012-16, supported by solid global demand for foodstuffs and the privileged market access afforded by Chile’s large network of FTAs. It will also benefit from a revival of the lucrative salmon industry, after a virus outbreak ravaged stocks in 2007-10. The manufacturing sector is small, since Chile imports the bulk of its consumer and investment goods, but it will post solid rates of growth owing to its agro industry component. The services sector will continue to record steady growth in the outlook period, driven by well-established and advanced retail, shipping and transport sectors, a growing tourism sector, and the major role of Chile as a regional hub for business and financial services.

C H I L E

187Citi Transaction Services Latin America & Mexico

COUNTRY OVERVIEW

Inflation

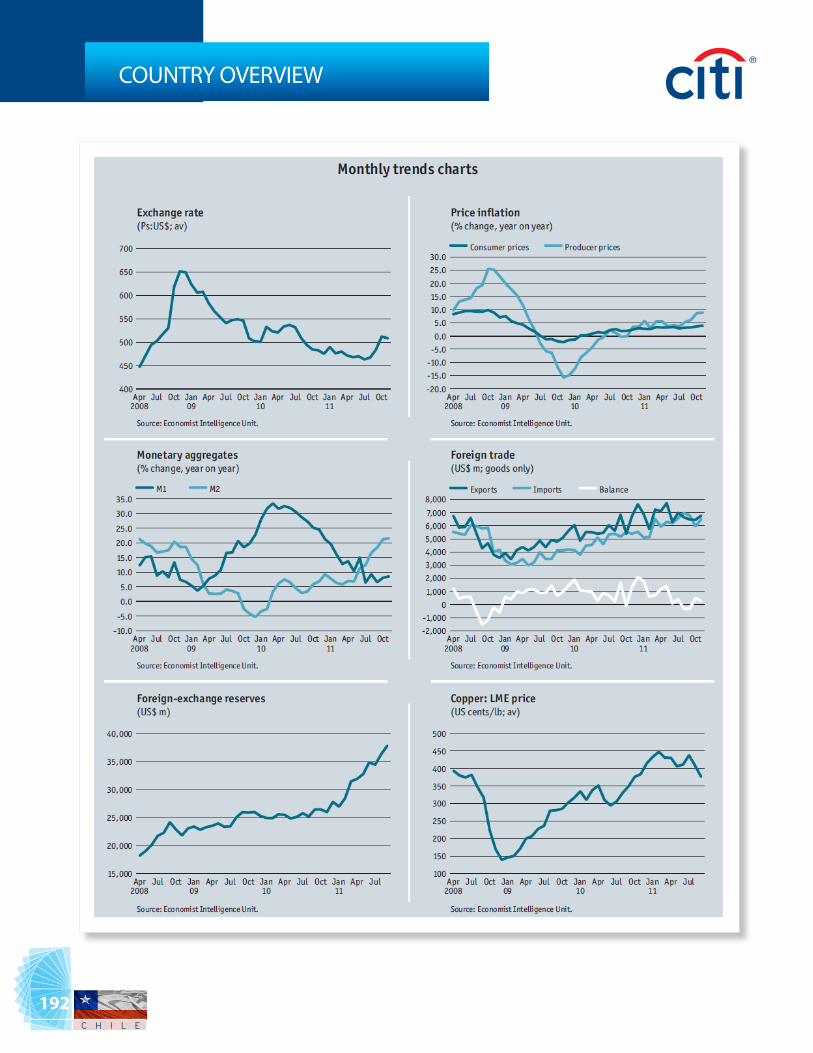

Consumer price inflation (CPI) ended 2011 at 4.4%, above the BCC’s target range of 2-4%, although average inflation was only 3.3%. Despite this sudden increase (attributed partly to a weaker base of comparison), the monetary authorities should be able to contain inflationary pressure throughout the outlook period. We expect a moderation of year-end inflation to 3.4% in 2012, and inflation to average 3.3% throughout 2013-16. As global prices abate, domestic demand will become the main driver of inflation, but there is little evidence of overheating and pressure will be limited by the policy rate, which is now close to its neutral stance (and now unlikely to be cut in the near term). Furthermore, we expect the labor market to remain relatively tight in the absence of major labor reform, thereby keeping real wage growth stable. Domestic risks can emerge from the vulnerability of the national energy grid to climatic shocks (predominantly droughts), which could result in energy-price hikes.

Exchange Rates

The peso continues to trade above Ps510:US$1 as of early January, a considerably weaker level compared with the levels seen before the August- September global sell-off of emerging market currencies. In the short term, risk aversion caused by euro zone financial woes will put a premium on US-dollar assets, making it unlikely that the peso will strengthen significantly, at Ps513:US$1 at end-2013 it will still be weaker than in mid-2011 when it hovered slightly above Ps460:US$1. As a result, we do not expect the BCC to

C H I L E

188

COUNTRY OVERVIEW

renew its programme of US-dollar purchases, which was intended to weaken the peso. this programme ended in mid-December after buying up its planned US$12bn in dollar reserves. In the longer term, our forecasts envision a weaker peso in nominal terms, reaching Ps526.5:US$1 by end-2016, as a result of a widening current-account deficit. However, with the prospects of weaker growth in the US and Europe, the modest nominal weakening envisioned by 2016 will not be sufficient to redress the peso’s gradual strengthening in real terms, by 2016, we expect the peso to have appreciated by as much as 9% compared with the average for the previous decade.

External Sector

After recording an estimated deficit of 1% of GDP in 2011, Chile’s current account balance will deteriorate over the outlook period, reaching a deficit of 3% of GDP by 2016. Chile will maintain a large, but shrinking, trade surplus throughout 2012-16, in part because it benefits from its extensive FTA network, as well as other high-growth markets, such as China. The latter is also the main source of demand for Chile’s copper exports, which are set to remain high by historical comparison (notwithstanding a recent slump in prices). Over one-half of Chile’s exports go to Asia and Latin America, thereby providing ample sources of growing external demand. However, earthquake reconstruction will help to fuel growth in imports (particularly intermediate and capital goods) during the early part of the forecast period, and rising household consumption, boosted by booming domestic demand, will also help to drive imports of consumer goods. Chile will continue to run a large structural deficit on the income account, reflecting large profit repatriations from multinationals. These will remain the main contributors to Chile’s current-account deficit but will increasingly be offset by an expanding base of outward investments, as well as the return on foreign reserves invested in the two sovereign wealth funds. The services and transfers balances will remain the smallest components of the current account, reaching -0.2% and 1.4% of GDP, respectively, by 2016. On the capital account, Chile has had little difficulty in attracting foreign investment and we expect this trend to continue throughout the forecast period. Inward foreign direct investment (FDI) reached US$11.1bn in the first nine months of 2011, while portfolio inflows came in at US$6.7bn in the same period, both figures were among the highest nine-month levels on record, despite a 64.5% year-on-year drop in portfolio flows in the third quarter. Speculative inflows remain a threat while interest rate differentials exist, although episodes of risk aversion could occasionally lead to capital flight instead. However, as a whole, the high levels of debt and equity investment are a reflection of Chile’s open and relatively deep financial system. Access to voluntary capital will also be facilitated by the strong credit ratings of the sovereign and the corporate sector. Foreign-exchange reserves, boosted by the recent currency-market intervention, will jump to US$59.1bn by 2016 (from US$36.8bn in September 2011), offering a cushion of close to five months of import cover.

C H I L E

189Citi Transaction Services Latin America & Mexico

COUNTRY OVERVIEW

C H I L E

190

COUNTRY OVERVIEW

C H I L E

191Citi Transaction Services Latin America & Mexico

COUNTRY OVERVIEW

C H I L E

192

COUNTRY OVERVIEW

C H I L E

193Citi Transaction Services Latin America & Mexico

COUNTRY OVERVIEW

C H I L E

194

BANKING SYSTEM

A. BANKS IN CHILE

The Chilean banking system operates in a stable macroeconomic environment and is closely supervised by a credible regulatory regime. The banking system has so far withstood the recent turmoil in global financial markets, as the country’s banks are well-capitalised and have traditionally maintained a high quality loan portfolio. The sector has consolidated over the last decade, resulting from the gradual liberalization of the financial-services sector. There were 24 banks operating in Chile in December 2011, down from 40 in 1992.

There were 12 domestically-owned banking groups operating in Chile as of December 2010. The top ten domestic banks in terms of assets held 61.0% of the banking sector total assets and the top three domestic banks.Banco de Chile, BancoEstado and Banco de Crédito e Inversiones held a market share of 46.5% at end-December 2010.

B. CITIBANK IN CHILE

Banco de Chile acquired Citibank local franchise in 2007 and during 2008 both banks were merged with a partnership between Banco de Chile and Citigroup Inc. The alliance broaden the scope of financial services that we offer to our customers through the addition of global financial services and other benefits to our local retail customers conducting transactions outside Chile. Similarly, this alliance enabled us to enhance our relationship with multinational companies operating in Chile. As a result of this partnership, we entered into a global connectivity agreement (the “Global Connectivity Agreement”), which has supported the creation of (i) an international personal banking unit, responsible for optimizing access to financial services outside Chile to our local retail customers, (ii) a global transactional services unit, responsible for executing local and international cash management services, as well as custody and foreign trade assistance, to our wholesale customers, and (iii) an enhanced investment banking unit, responsible for providing financial advisory services and access to global capital markets to our Chilean corporate customers

Currently Banco de Chile has 441 branches including the following cities.

Location of Branches:• Santiago• Arica• Iquique• Calama• Antofagasta• Copiapó

C H I L E

195Citi Transaction Services Latin America & Mexico

• Vallenar• La Serena• Coquimbo• Ovalle• San Felipe• La Ligue• Quillota• Quilpue• Valparaíso• Viña del Mar• Melipilla• La Calera• Los Andes• Villa Alemana• San Antonio• Buin• Rancagua• Rengo• San Fernando• Curicó• Talca• San Carlos• Linares• Chillán• Talcahuano• Concepión • Coronel• Los Angeles• Victoria• Angol• Temuco• Villarrica• Loncoche• Valdivia• Osorno• La Unión• Puerto Varas• Puerto Montt• Coyhaique• Castro and Punta ArenasServices Offered to Citibank Clients:

• Liquidity Management / Domestic & International Account Structures• Information Management• Payables Management• Receivables Management• FX Management• Trade Services, Trade Finance• Regional Implementation• Customer Service• Commercial Cards Offering: Local Issuance Capabilities• Securities and Funds Services

BANKING SYSTEM

C H I L E

196

A. CLEARING HOUSE

There are several types of payment clearing systems in Chile. Checks clearing takes place in five regional clearinghouses authorized by the Central Bank of Chile (Banco Central de Chile). Cheks are presented daily at the clearinghouses, which report amounts due to the central bank. These net amounts are settled on the next business day (through accounts held at the central bank). There is also a privately run Automatic Clearing House (Centro de Compensación Automatizado.CCA) that settles payments between 15 participating banks. The central bank also manages the Real Time Gross Settlement System (Sistema de Liquidación Bruta en Tiempo Real.LBTR), which allows banks to settle payments immediately via their accounts at the central bank. The system allows invoicing and payments to be settled electronically in real time. To facilitate liquidation of operations through the LBTR, the central bank gives participants access to an .intraday liquidity facility., which offers financing by the hour and operates through the purchase of repo instruments over the course of the day. The LBTR system and the liquidity facility ensure that payments are settled smoothly and safely.

CLEARING SYSTEM

C H I L E

197Citi Transaction Services Latin America & Mexico

FOREIGN EXCHANGE CONTROLS

A. FOREIGN EXCHANGE REGULATION

The Central Bank of Chile (Banco Central de Chile) eliminated all remaining exchange controls in April 2001 (via changes to Chapter XIV of Title I of the Compendium of Foreign Exchange Regulations). Investment and monetary flows to or from Chile are no longer subject to any official restrictions. Importers and exporters are only required to report their transactions to the central bank for statistical purposes.

B. TAXES

Income Tax

Corporate income is assessed in two stages. When taxable income is accrued, it is liable for first-category tax (impuesto de primera categoría) of 18,5%. In the second stage, if profits are distributed, the distributed amount is liable for a 35% additional tax (impuesto adicional), for which the first-category tax serves as a credit.

Withholding Tax

Payments of royalties or fees to entities or individuals not domiciled in Chile are subject to a 30% withholding tax, unless these entities are located in a country with which Chile has a tax treaty. Only commercial commissions are exempt. There are a few services for which withholding taxes are lower, such as insurance contracts (subject to a 22% withholding tax), technical assistance (20%), leasing (20%) and fees to non-residents for port or shipping services (5%). Where customs duties are deferred, payments for leasing imported capital goods are subject to a 1.75% tax on each payment.

Stamp Tax

Law 20,326 of January 2009 created several tax incentives and temporarily eliminated the 1.2% stamp tax during 2009. It halved the stamp tax to 0.6%, from January 1st to June 30th 2010.

C H I L E

198

TRADE REGULATIONS

A. IMPORT AND EXPORT REGULATIONS

Foreign exchange is readily available for imports and importers can purchase spot exchange before the payment date. Imports on deferred-payment terms (cobertura diferida).for example, on credit terms exceeding 360 days no longer require prior central-bank authorization.

There are no restrictions on export leads and lags. Importers may pay in advance. They must buy the required foreign currency in the banking system no more than 360 working days after the payment deadline indicated in the import report.

B. REGIONAL TRADING ASSOCIATIONS

ALADI

MERCOSUR

APEC

EC

C. BILATERAL AGREEMENTS

At the moment Chilean economy has many bilateral agreements working with different countries of the world. The list is long and is increasing continuously.

C H I L E

199Citi Transaction Services Latin America & Mexico

A. TREASURY BONDS

The Treasury places discountable promissory notes with financial institutions and investors via auction; these have maturities of 30.365 days on the primary market. Terms on the secondary market vary. The stockmarket calculates a daily internal rate of median return (tasa interna de retorno.TIR) to measure the market yield for Treasury and Central Bank of Chile (Banco Central de Chile) bonds.

B. COMMERCIAL PAPER

The market for short-term unsecured promissory notes was hindered for some time owing to the stamp tax on debt instruments (impuesto de timbres y estampillas) that was applicable to each commercial paper (CP) issue. Law 19,768, of November 6th 2001, established that the 1.2% tax may apply only once. An entity may then place as many CP issues as it likes over the course of ten years. Law 20,326 of January 2009 temporarily eliminated the stamp tax for 2009 (and halved it to 0.6% for the first half of 2010) in an effort to stimulate investment and financial sector activity.

Law 20,190, a capital-market reform law known as MK2, was enacted on June 5th 2007. It included changes to Law 18,876, which regulates the custody of securities. It enabled CP to be issued electronically and included more flexible norms for private pension-fund investments in CP.

Tax consequences. Interest received - technically a capital gain over the initially discounted price - from CP issues is tax exempt. Issuing companies may deduct from taxable corporate income the interest payments and costs associated with their offerings.

INVESTMENT OPPORTUNITIES

C H I L E

200

INVESTMENT OPPORTUNITIES

C. CORPORATE BONDS

Before issuing bonds on the local market, a company must register the issue with the SVS and present a risk classification from two local rating agencies. Corporate bonds enjoy an important advantage over public-sector bonds, in that the interest they generate is tax exempt. They also offer higher yields. Rates for medium and long-term private bond issues tend to be 0.5.2.5 percentage points higher than for medium- or long-term bonds issued by the Central Bank of Chile (bonos banco central en unidades de fomento.BCUs).

D. STOCK MARKET

Spot and Forward Market

Growing cross-border trade and investment flows, as well as the liberalization of Chile’s foreign-exchange controls, helped to deepen the spot and forward markets in recent years, with most trades conducted with the US dollar. The ongoing global economic crisis has limited these advances in the short-term. The depreciated value of the peso, coupled with market uncertainty in the United States, has curbed activity in the market.

C H I L E

201Citi Transaction Services Latin America & Mexico

CASH MANAGEMENT SERVICES

A. GENERAL BUSINESS TERMS AND CONDITIONS

Cash Account Services allow the entity to manage and dispose of tools to help your daily management run in a timely and efficient manner.

Services available

• Cash Pooling (TBA, Zero Balance)• SWIFT MT940 message• Digital Library

Benefits

• Manage the cash flow of the company• Increase your level of automation• Facilitate operations reflecting a decrease in administrative costs• Allows to define account’s daughters• Collecting accounts• Paying bills accounts• Different accounts belonging to the holding• Management of Subsidiaries belonging to the enterprise

B. CITIBANK’S ACCOUNTS SERVICES SOLUTIONS IN CHILE

Non-Resident Client Account USD or CLP

• Min. Balance Requirement: None• Maintenance Fee: Commercial terms and conditions agreed• Overdraft subject to available o/d credit facility

Legal Documentation

• Incorporation of the company and its amendments• Public deed detailing current powers of attorney and the way in which they act.• Identity Card Copy or Passport of each of the signers • Copy of Tax Identification Number (RUT) granted by Servicio de Impuestos Internos from Chile. (SII)• Account request form

CITI SOLUTIONS AND SERVICES

C H I L E

202

• Commercial account conditions• If the mentioned documents are in English Client must send a Legal Opinion From a Law Firm in the country of jurisdiction that indicates: i) Entity is still in existence ii) attorneys-in-fact iii) powers of these attorneys-in-fact iv) limitations of the attorneys-in-fact• Foreign entities that are not locally registered to do business in Chile must appoint a Local Legal Representative holding Power of Attorney. This Local Legal Representative is entitled to obtain the company RUT in from the Internal Revenue Service.• Each foreign and public legal document submitted must be consularized by the Chilean Consulate in the Country of Jurisdiction

C. ABOUT CONTRACTS

DDA Local Contract

Account opening agreement, which must sign the proxy, that open the account. It is mandatory to attach an original photo in color and record the fingerprint of each one of them. ADDA Local Contract is an account opening agreement which must be signed by the proxy opening the account.

Communication via email and key system telephone (TPIN)

Contract for access to information through telephone banking.It should contain the data from each of those recorded as those who consult the help desk (Fonobank) required fields are: full name, ruth, telephone, e-mail.

Register of Signatures

Record the signature of each of the proxies and each of the accounts that are being requested.

Authorization to make banking transactions

Document that allows you to specify the persons authorized to represent the administrative burden on the company, making removal of information or documentation the Bank of Chile.

CITI SOLUTIONS AND SERVICES

C H I L E

203Citi Transaction Services Latin America & Mexico

Electronic Banking Agreement

CitiDirect enabling contract

Request for Current Account Opening

This is a form letter which should indicate name, business address, business or activity, telephone, ruth company.

Communication by facsimile (FAX)Authorization letter for manual transfer.

Local Payments

**Subject to payment of fees contained in the contract**

D. CITIBANK’S PAYMENT SOLUTIONS IN CHILE

Cross Border Payments

Funds Transfers - International wire transfers or check issuances may be made in USD or other currencies available through WorldLink SM. Clients may fund these transfers through their local:

• Citidirect • Worldlink

Local Payments

Funds Transfer Services will allow the company to manage transfers of funds and have tools to help your daily management in a timely and efficient. Services available are:

• High value payments (HVPS).• Delivery versus payment (DVP).

Currency: EUR – USD – CLP

CITI SOLUTIONS AND SERVICES

C H I L E

204

CITICONNECT

Electronic payment service given a solution for payment of services to third parties by an electronic platform one by one,

• PreviRed (AFP ISAPRES, INP)• Internal Revenue Service (SII)• Servipag• Treasury of the Republic (TGR)

CITI SOLUTIONS AND SERVICES

C H I L E

205Citi Transaction Services Latin America & Mexico

MARKET GUIDE FOR TREASURY

Allowed —No materialrestrictions

Operating Accounts1,2 Non-Residents ResidentsOnshore local currencyOnshore foreign currencyOffshore local currency Offshore foreign currency

Overdrafts Non-Residents ResidentsOnshore local currencyOnshore foreign currency

Interest-Bearing Accounts3,4 Non-Residents Residents Onshore local currency operating accountsOnshore foreign currency operating accounts

Time Deposits5,6 Non-Residents ResidentsOnshore local currencyOnshore foreign currency

Domestic Notional Pooling7 Non-Resident to Resident Residents OnlyOnshore local currencyOnshore foreign currency

Inter-company Lending Non-Resident to Resident Resident to Non-residentOnshore local currencyOnshore foreign currency

Non-Residents Only Residents OnlyOnshore local currencyOnshore foreign currency

FX Convertibility/Transferability• Local Currency is freely convertible domestically only• Transactions must be within the boundaries of what is defined by the Compendium of Foreign Exchange Regulations of the Central Bank of Chile, basically limited to foreign trade (broadly defined), investments, loans and derivatives. Straight opening and usage of CLP accounts that are not associated to these activities is not allowed. There are general information duties to be complied by non-residents

Allowed —Straightforwardregulations,approval orlicense

Allowed —Challengingregulatoryapproval orlicense

Allowed —Subject to acomplex setof rules

StrictlyProhibited

C H I L E

206

MARKET GUIDE FOR TREASURY

Central Bank and Other Regulatory Requirements• Foreign investors must obtain or be granted a local tax ID and report all of their• activities to the Central Bank of Chile

Tax and Transfer Pricing Considerations• Corporate tax 17% (2009 tax year)• Arms-length transfer pricing is required for any inter-company arrangement• Other Payment and Clearing Consideration for Treasury• No major restrictions on netting• No major restrictions on non residents making pay-on-behalf-of residents• All cross-borders transfers are restricted by our Central Bank, since each one has to have a Central Bank code

For more information, please visit www.transactionservices.citi.com.

Notes:1 CLP accounts for non-residents are not allowed to be overdrawn2 There are practical and regulatory limitations that do not allow opening of any offshore CLP accounts3 A 4% withholding tax is levied on bank interest recieved by non-residents without a permanent establishment in Chile4 Normally (except for 2009) a Stamp Duty is applied on all forms of interest-bearing deposits; this is of 0.1% per month or fraction of month with a cap of 1.2% and resident entities and individuals are exempt of such duties5 A 4% withholding tax is levied on bank interest received by non-residents without a permanent establishment in Chile6 Normally (except for 2009) a Stamp Duty is applied on all forms of interest-bearing deposits; this is of 0.1% per month or fraction of month with a cap of 1.2% and resident entities and individuals are exempt of such duties7 Notional pool strongly rests on the bank’s ability to enforce its right to set off balances in one account versus over drafts in another account across legal entities

C H I L E

207Citi Transaction Services Latin America & Mexico

CONTACT INFORMATION

Sales Heads

Industry Sector Heads

Carolina JuanTreasury and Trade Solutions Client Sales ManagementLatin America & Mexico HeadCiti Transaction ServicesEmail: [email protected]: + 57 (316) 743 - 9347Of. Phone: +57 (1) 639 - 4026

Industrials SectorInes Vargas BarreraEmail: [email protected]: +52 (181) 8366 - 5190Of. Phone: +52 (81) 1226 - 8525

Branding, Consumer and Healthcare SectorOscar MazzaEmail: [email protected]: +1 (305) 588 - 9396Of. Phone: +1 (305) 347 - 1336

Technology, Media and Telecom SectorGabriel KirestianEmail: [email protected]: +54 (911) 3301 - 4826Of. Phone: +54 (11) 4329 - 1516

Energy, Power and Chemicals SectorPeter LangshawEmail: [email protected]: +55 (11) 6183 - 6958Of. Phone: +55 (11) 6183 - 6958

Public SectorJorg PaascheEmail: [email protected]: +52 (1) 55 5453 - 0103Of. Phone: +52 (55) 2226 - 6020Based: Mexico DF, Mexico

Non Bank FI Sector (NFBI)Ricardo DessyEmail: [email protected]: +54 (911) 6641 - 9752Of. Phone: +54 (11) 4329 - 1471Based: Buenos Aires, Argentina

BrazilAdoniro CestariEmail: [email protected]: +55 (11) 7130 - 9447Of. Phone: +55 (11) 4009 - 7838Based: Sao Paulo, Brazil

Central AmericaEvelin MadridEmail: [email protected]: + 506 8701 - 4529Of. Phone: +506 2588 - 7541Based: San Jose, Costa Rica

MexicoMiguel YtuarteEmail: [email protected]: +52 (1) 55 4088 - 2284Of. Phone: +5255 (1226) 8895Based: Mexico DF, Mexico

Andean RegionCarolina JuanEmail: [email protected]: + 57 (316) 743 - 9347Of. Phone: +57 (1) 639 - 4026Based: Bogota, Colombia

ArgentinaAdrian ScosceiraEmail: [email protected]: +54 (911) 5674 - 6966Of. Phone: +54 (11) 4329 - 1194Based: Buenos Aires, Argentina

Citi Transaction Serviceswww.transactionservices.citi.com

© 2012 Citibank, N.A. All rights reserved. Citi and Arc Design is a trademark and service mark of Citigroup Inc., used and registered throughout the world. All other trademarks are the property of their respective owners.