Presentatie Jacques Pijl - Mediafacts Nationale Uitgeefdag 2014

Basic concepts of Basic concepts of

Eurosystem´s Operational Eurosystem´s Operational

Monetary Policy Framework Monetary Policy Framework

and Experiences with the operational and Experiences with the operational frameworkframework

Hans PijlHans Pijl

Division Financial Markets Division Financial Markets

Department Treasury and MonitoringDepartment Treasury and Monitoring

Basic concepts of Basic concepts of

Eurosystem´s Operational Eurosystem´s Operational

Monetary Policy Framework Monetary Policy Framework

and Experiences with the operational and Experiences with the operational frameworkframework

Hans PijlHans Pijl

Division Financial Markets Division Financial Markets

Department Treasury and MonitoringDepartment Treasury and Monitoring

Basic concepts of Basic concepts of

Eurosystem´s Operational Eurosystem´s Operational

Monetary Policy Framework Monetary Policy Framework

Basic concepts of Basic concepts of

Eurosystem´s Operational Eurosystem´s Operational

Monetary Policy Framework Monetary Policy Framework

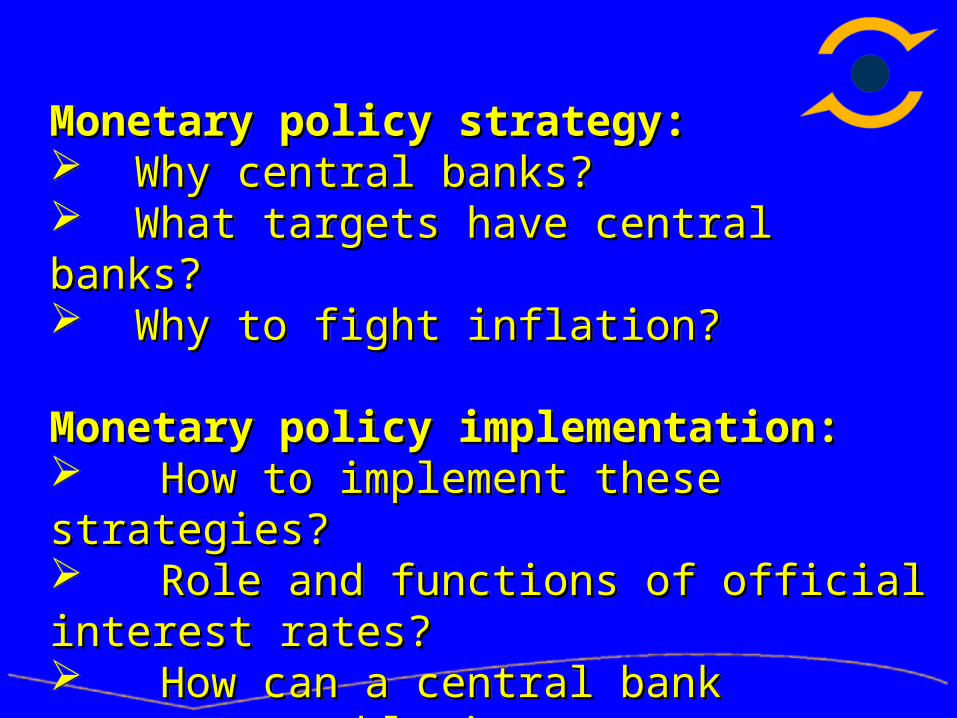

Monetary policy strategy:Monetary policy strategy: Why central banks?Why central banks? What targets have central banks?What targets have central banks? Why to fight inflation?Why to fight inflation?

Monetary policy implementation:Monetary policy implementation: How to implement these strategies?How to implement these strategies? Role and functions of official interest rates?Role and functions of official interest rates? How can a central bank generate stable interest How can a central bank generate stable interest rate movements?rate movements?

Monetary policy strategy:Monetary policy strategy: Why central banks?Why central banks? What targets have central banks?What targets have central banks? Why to fight inflation?Why to fight inflation?

Monetary policy implementation:Monetary policy implementation: How to implement these strategies?How to implement these strategies? Role and functions of official interest rates?Role and functions of official interest rates? How can a central bank generate stable interest How can a central bank generate stable interest rate movements?rate movements?

Monetary policy strategy:Monetary policy strategy:

The monetary strategy determines which money

market interest rate level is required to maintain

price stability.

Monetary policy implementation:Monetary policy implementation:

The operational framework determines how to

achieve this interest rate level using the available

monetary instruments.

Transmission of monetary policy Transmission of monetary policy and instrumentsand instruments

Instruments → Operational Target → Intermediate target → Policy objective

Official interest rates year-on-yearMonetarye aggregrates increase

Reverse requirements M3 Harmonised Index Euro area money market of Consumer Pirces (HICP)

Open markt operations interes rate Other financial, reel close to 2% (EONIA rate) and nominal indictors for euro area

Standing Facilities over the medium term

Exchange rate

Functions of the operational framework

Eurosystem sets and stabilises interest rates inthe short term money market in two ways:

Signalling its monetary policy stance to the money market

Managing the liquidity situation in the money market

How to set (money market) interest rates?How to set (money market) interest rates?

Step 1: determine official interest ratesStep 1: determine official interest rates

Step 2: make banks dependent on credit by the ECBStep 2: make banks dependent on credit by the ECB

Step 3: extend credit to banks with the appropriateStep 3: extend credit to banks with the appropriate interest rateinterest rate

Step 4: design framework to stabilise very Step 4: design framework to stabilise very short-term interest ratesshort-term interest rates

How to set (money market) interest rates?How to set (money market) interest rates?

Step 1: determine official interest ratesStep 1: determine official interest rates

Step 2: make banks dependent on credit by the ECBStep 2: make banks dependent on credit by the ECB

Step 3: extend credit to banks with the appropriateStep 3: extend credit to banks with the appropriate interest rateinterest rate

Step 4: design framework to stabilise very Step 4: design framework to stabilise very short-term interest ratesshort-term interest rates

Main monetary policy instruments:Main monetary policy instruments:

Minimum reserve requirementsMinimum reserve requirements Credit extension to banks viaCredit extension to banks via

Open Market OperationsOpen Market Operations Main refinancing operationsMain refinancing operations Long-term refinancing operationsLong-term refinancing operations Fine-tuning operations Fine-tuning operations Structural operations Structural operations

Standing facilitiesStanding facilities Marginal lending facilityMarginal lending facility Deposit facilityDeposit facility

Main monetary policy instruments:Main monetary policy instruments:

Minimum reserve requirementsMinimum reserve requirements Credit extension to banks viaCredit extension to banks via

Open Market OperationsOpen Market Operations Main refinancing operationsMain refinancing operations Long-term refinancing operationsLong-term refinancing operations Fine-tuning operations Fine-tuning operations Structural operations Structural operations

Standing facilitiesStanding facilities Marginal lending facilityMarginal lending facility Deposit facilityDeposit facility

Minimum reserve requirements:Minimum reserve requirements:

During a reserve maintenance period banks have During a reserve maintenance period banks have on average to maintain a certain percentage of on average to maintain a certain percentage of certain banks’ balance sheet items (2%) on an certain banks’ balance sheet items (2%) on an account at the central banksaccount at the central banks

Create / increase money market shortage Create / increase money market shortage (counterparties vis a vis Eurosystem)(counterparties vis a vis Eurosystem)

Averaging feature helps stabilising overnight andAveraging feature helps stabilising overnight and intraday money market ratesintraday money market rates

Minimum reserve requirements:Minimum reserve requirements:

During a reserve maintenance period banks have During a reserve maintenance period banks have on average to maintain a certain percentage of on average to maintain a certain percentage of certain banks’ balance sheet items (2%) on an certain banks’ balance sheet items (2%) on an account at the central banksaccount at the central banks

Create / increase money market shortage Create / increase money market shortage (counterparties vis a vis Eurosystem)(counterparties vis a vis Eurosystem)

Averaging feature helps stabilising overnight andAveraging feature helps stabilising overnight and intraday money market ratesintraday money market rates

Minimum reserve requirements:Minimum reserve requirements:

Interest paid over required reservesInterest paid over required reserves

Excess reserves not remunerated, giving incentive Excess reserves not remunerated, giving incentive to go to the market to go to the market

Penalty in case of non-compliancePenalty in case of non-compliance

Banks with large payment flows prefer large Banks with large payment flows prefer large reserve requirementsreserve requirements

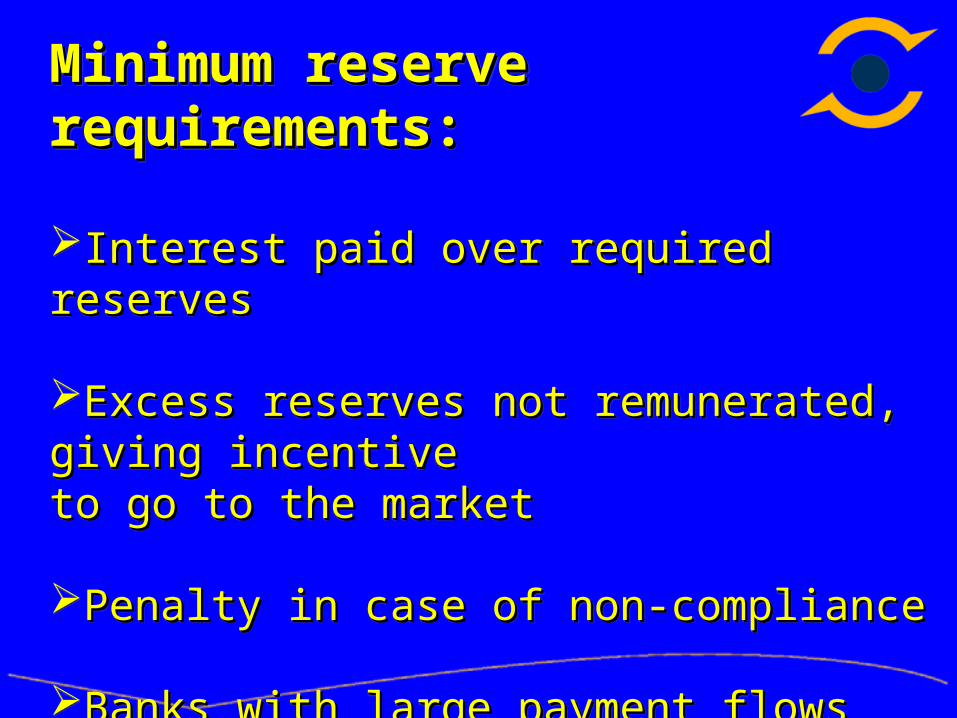

Minimum reserve requirements:Minimum reserve requirements:

Interest paid over required reservesInterest paid over required reserves

Excess reserves not remunerated, giving incentive Excess reserves not remunerated, giving incentive to go to the market to go to the market

Penalty in case of non-compliancePenalty in case of non-compliance

Banks with large payment flows prefer large Banks with large payment flows prefer large reserve requirementsreserve requirements

Open marktoperations:Open marktoperations:

Main refinancing operations (MROs)Main refinancing operations (MROs)about 70% of total credit extensionabout 70% of total credit extension

Long term refinancing transactions (LTROs)Long term refinancing transactions (LTROs)about 30% of total credit extensionabout 30% of total credit extension

Fine-tuning operations (FTOs) Fine-tuning operations (FTOs) nowadays last day of the reserve maintenance nowadays last day of the reserve maintenance

periodperiodStructural operations Structural operations

Open marktoperations:Open marktoperations:

Main refinancing operations (MROs)Main refinancing operations (MROs)about 70% of total credit extensionabout 70% of total credit extension

Long term refinancing transactions (LTROs)Long term refinancing transactions (LTROs)about 30% of total credit extensionabout 30% of total credit extension

Fine-tuning operations (FTOs) Fine-tuning operations (FTOs) nowadays last day of the reserve maintenance nowadays last day of the reserve maintenance

periodperiodStructural operations Structural operations

Main refinancing operations (MROs):Main refinancing operations (MROs):

Liquidity providingLiquidity providing

Conducted on a weekly basisConducted on a weekly basis

One week maturity One week maturity

Reverse transactionsReverse transactions

Main refinancing operations (MROs):Main refinancing operations (MROs):

Liquidity providingLiquidity providing

Conducted on a weekly basisConducted on a weekly basis

One week maturity One week maturity

Reverse transactionsReverse transactions

Main refinancing operations (MROs):Main refinancing operations (MROs):

Open for all banks with a minimum reserve Open for all banks with a minimum reserve requirement (cf US system of primary dealers)requirement (cf US system of primary dealers)

Interest rate on MROs is main ECB interest rateInterest rate on MROs is main ECB interest rate

Main source credit extension EurosystemMain source credit extension Eurosystem

Variable rate tender (opposite to fixed rate tender)Variable rate tender (opposite to fixed rate tender)

Marginal rate few base points above min. bidrateMarginal rate few base points above min. bidrate

Main refinancing operations (MROs):Main refinancing operations (MROs):

Open for all banks with a minimum reserve Open for all banks with a minimum reserve requirement (cf US system of primary dealers)requirement (cf US system of primary dealers)

Interest rate on MROs is main ECB interest rateInterest rate on MROs is main ECB interest rate

Main source credit extension EurosystemMain source credit extension Eurosystem

Variable rate tender (opposite to fixed rate tender)Variable rate tender (opposite to fixed rate tender)

Marginal rate few base points above min. bidrateMarginal rate few base points above min. bidrate

Long term refinancing transactions Long term refinancing transactions (LTROs):(LTROs):

Liquidity providingLiquidity providing

Monthly auction via variable rate tenderMonthly auction via variable rate tender

Three month maturity Three month maturity

Long term refinancing transactions Long term refinancing transactions (LTROs):(LTROs):

Liquidity providingLiquidity providing

Monthly auction via variable rate tenderMonthly auction via variable rate tender

Three month maturity Three month maturity

Long term refinancing transactions Long term refinancing transactions (LTROs):(LTROs):

Reverse transactionsReverse transactions

Pre-announced 50 billion euro size eachPre-announced 50 billion euro size each

Particularly designed for smaller banksParticularly designed for smaller banks

Amount allotted is sufficient to balance supply Amount allotted is sufficient to balance supply and demandand demand

Long term refinancing transactions Long term refinancing transactions (LTROs):(LTROs):

Reverse transactionsReverse transactions

Pre-announced 50 billion euro size eachPre-announced 50 billion euro size each

Particularly designed for smaller banksParticularly designed for smaller banks

Amount allotted is sufficient to balance supply Amount allotted is sufficient to balance supply and demandand demand

Fine-tuning operations (FTOs):Fine-tuning operations (FTOs):

Smooth out effects on interest rates of unexpectedSmooth out effects on interest rates of unexpectedliquidity fluctuationsliquidity fluctuations

Liquidity providing or liquidity absorbingLiquidity providing or liquidity absorbing

Ad hoc basis and regular basis i.e. last day of a Ad hoc basis and regular basis i.e. last day of a reserve maintenance period reserve maintenance period

Fine-tuning operations (FTOs):Fine-tuning operations (FTOs):

Smooth out effects on interest rates of unexpectedSmooth out effects on interest rates of unexpectedliquidity fluctuationsliquidity fluctuations

Liquidity providing or liquidity absorbingLiquidity providing or liquidity absorbing

Ad hoc basis and regular basis i.e. last day of a Ad hoc basis and regular basis i.e. last day of a reserve maintenance period reserve maintenance period

Fine-tuning operations (FTOs):Fine-tuning operations (FTOs):

Short-term basisShort-term basis

Tender or bilateral operationTender or bilateral operation

Selected group of fine-tuning counterpartiesSelected group of fine-tuning counterparties

Fine-tuning operations (FTOs):Fine-tuning operations (FTOs):

Short-term basisShort-term basis

Tender or bilateral operationTender or bilateral operation

Selected group of fine-tuning counterpartiesSelected group of fine-tuning counterparties

Structural operations:Structural operations:

Liquidity-providing or liquidity-absorbing

Conducted on an ad hoc basis (never used yet)

Maturity not standardised

Tender or bilateral operations

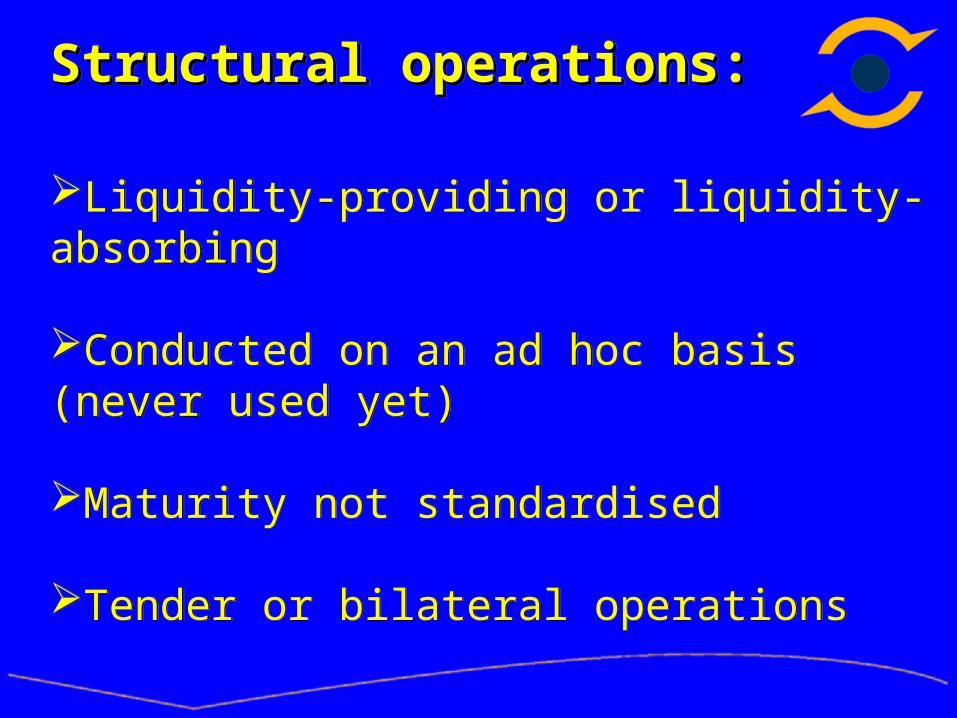

Structural operations:Structural operations:

Liquidity-providing or liquidity-absorbing

Conducted on an ad hoc basis (never used yet)

Maturity not standardised

Tender or bilateral operations

Types of open market operations:Types of open market operations:

Reverse transactions

Outright transactions

Foreign exchange swaps

Collection of fixed-term deposits

Issuance of ECB debt certificates

Types of open market operations:Types of open market operations:

Reverse transactions

Outright transactions

Foreign exchange swaps

Collection of fixed-term deposits

Issuance of ECB debt certificates

Stabilizing money market interest Stabilizing money market interest rates:rates:

Fine-tuning instrumentsFine-tuning instruments

Averaging facility on the reserve requirementsAveraging facility on the reserve requirements

Standing facilities Standing facilities

Stabilizing money market interest Stabilizing money market interest rates:rates:

Fine-tuning instrumentsFine-tuning instruments

Averaging facility on the reserve requirementsAveraging facility on the reserve requirements

Standing facilities Standing facilities

Standing facilities :Standing facilities :

Deposit facilityDeposit facility overnight liquidity absorptionovernight liquidity absorption at relatively low (official) interest at relatively low (official) interest raterate floor for market ratesfloor for market rates normally no restrictionsnormally no restrictions

Marginal lending facilityMarginal lending facilityovernight liquidity provisionovernight liquidity provision

at relatively high (official) interest at relatively high (official) interest raterate ceiling for market ratesceiling for market rates normally no restrictions except normally no restrictions except collateralcollateral

Standing facilities :Standing facilities :

Deposit facilityDeposit facility overnight liquidity absorptionovernight liquidity absorption at relatively low (official) interest at relatively low (official) interest raterate floor for market ratesfloor for market rates normally no restrictionsnormally no restrictions

Marginal lending facilityMarginal lending facilityovernight liquidity provisionovernight liquidity provision

at relatively high (official) interest at relatively high (official) interest raterate ceiling for market ratesceiling for market rates normally no restrictions except normally no restrictions except collateralcollateral

Standing facilities :Standing facilities :

General:General:Providing / absorbing liquidity at the discretion of Providing / absorbing liquidity at the discretion of banks/at the initiative of counterpartiesbanks/at the initiative of counterparties

Limiting maximum interest volatilityLimiting maximum interest volatility

Signal general stance of monetary policySignal general stance of monetary policy

Standing facilities :Standing facilities :

General:General:Providing / absorbing liquidity at the discretion of Providing / absorbing liquidity at the discretion of banks/at the initiative of counterpartiesbanks/at the initiative of counterparties

Limiting maximum interest volatilityLimiting maximum interest volatility

Signal general stance of monetary policySignal general stance of monetary policy

Standing facilities :Standing facilities :Usage only at the end of the maintenance periodonly at the end of the maintenance periodOccasionally large resource on deposit facility Occasionally large resource on deposit facility duedueto securities settlementto securities settlement

Standing facilities :Standing facilities :Usage only at the end of the maintenance periodonly at the end of the maintenance periodOccasionally large resource on deposit facility Occasionally large resource on deposit facility duedueto securities settlementto securities settlement

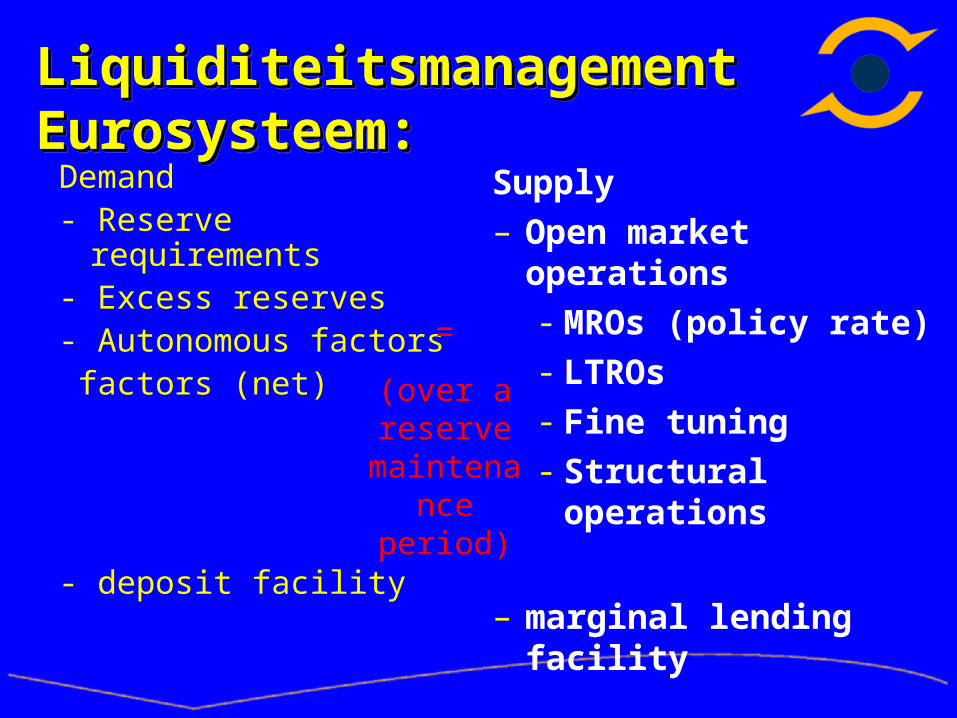

Liquiditeitsmanagement Eurosysteem:Liquiditeitsmanagement Eurosysteem:Liquiditeitsmanagement Eurosysteem:Liquiditeitsmanagement Eurosysteem:

Demand- Reserve requirements - Excess reserves- Autonomous factors factors (net)

- deposit facility

Supply– Open market operations

- MROs (policy rate)- LTROs- Fine tuning- Structural operations

– marginal lending facility

Liquiditeitsmanagement Eurosysteem:Liquiditeitsmanagement Eurosysteem:Liquiditeitsmanagement Eurosysteem:Liquiditeitsmanagement Eurosysteem:

Demand- Reserve requirements - Excess reserves- Autonomous factors factors (net)

- deposit facility

Supply– Open market operations

- MROs (policy rate)- LTROs- Fine tuning- Structural operations

– marginal lending facility

=

(over a reserve

maintenance period)

When is implementation succesfull?When is implementation succesfull?Stable and small spread between minimum bid rate Stable and small spread between minimum bid rate and EONIA rateand EONIA rate

When is implementation succesfull?When is implementation succesfull?Stable and small spread between minimum bid rate Stable and small spread between minimum bid rate and EONIA rateand EONIA rate

1

2

3

4

5

jan-06 feb-06 mrt-06 apr-06 mei-06 jun-06 jul-06 sep-06 okt-06 nov-06 dec-06 jan-07 feb-07

Minimum bidrate ECB EONIA Index Deposit rate Marginal rate

Graph 2 Official interest rates ECB and EONIA-rate

Source: Bloomberg.

-0,50

-0,40

-0,30

-0,20

-0,10

0,00

0,10

0,20

0,30

0,40

0,50

jan-06 feb-06 mrt-06 apr-06 mei-06 jun-06 jul-06 sep-06 okt-06 nov-06 dec-06 jan-07 feb-07

Graph 3 Spread minimum bid rate ECB and EONIA-rate

Source: Bloomberg.

Central Bank Balance Sheet:Central Bank Balance Sheet:Central Bank Balance Sheet:Central Bank Balance Sheet:Figure 1 Simplified Eurosystem Balance Sheet, February 2007, EUR billions

Autonomous factors Autonomous factors

Net foreign assets (A1+A2+A3-L7-L8-L9) 321,8 Banknotes in circulation (L1) 604,4Net assets denominated in euro´s (A4-L6+A7+A11.2) 266,5 Government Deposits (L5.1) 35,8

Other autonomous factors (net) * 180,7

Reserve requirements (L2.1) 183,9

Monetary Policy Instruments Monetary Policy Instruments

Main Refinancing Operation (A5.1) 286,5 Deposit Facility (L2.2) 0,0Longer Term Refinancing Operation (A5.2) 130,0

Marginal lending facility (A5.5) 0.0

1004,8 1004,8

Source: ECB Liquidity Management Data and own calculations.

Figures in brackets refer to relevant balance sheet item Balance sheet identity: Ca = OMO + ML - DF - AF* (A5.6+A6+A8+A10+A11.1+A11.3+A11.4-L2.5-L3-L5.2-L10-L12-L13-L14-L15)

Principles:Principles:

Operational efficiencyOperational efficiencyOpen market economy / hands-off approachOpen market economy / hands-off approachEqual treatment of counterpartiesEqual treatment of counterparties

Decentralisation op implementation, simplicity, Decentralisation op implementation, simplicity, transparency, continuity, safety and cost efficiency transparency, continuity, safety and cost efficiency

Principles:Principles:

Operational efficiencyOperational efficiencyOpen market economy / hands-off approachOpen market economy / hands-off approachEqual treatment of counterpartiesEqual treatment of counterparties

Decentralisation op implementation, simplicity, Decentralisation op implementation, simplicity, transparency, continuity, safety and cost efficiency transparency, continuity, safety and cost efficiency

Experiences with the operational Experiences with the operational frameworkframework

Experiences with the operational Experiences with the operational frameworkframework

Issues:Issues:I.I. Modification of Operational Framework in Modification of Operational Framework in

March 2004March 2004

II.II. Transparency of allotment policyTransparency of allotment policy

III.III. Volatility Treasury DepositVolatility Treasury Deposit

IV.IV. End of period fine-tuning operationsEnd of period fine-tuning operations

V.V. EONIA SwapsEONIA Swaps

VI.VI. Optimal size and composition open market Optimal size and composition open market operationsoperations

VII.VII.Future challenges Future challenges

Issues:Issues:I.I. Modification of Operational Framework in Modification of Operational Framework in

March 2004March 2004

II.II. Transparency of allotment policyTransparency of allotment policy

III.III. Volatility Treasury DepositVolatility Treasury Deposit

IV.IV. End of period fine-tuning operationsEnd of period fine-tuning operations

V.V. EONIA SwapsEONIA Swaps

VI.VI. Optimal size and composition open market Optimal size and composition open market operationsoperations

VII.VII.Future challenges Future challenges

I Modification of Operational I Modification of Operational Framework in March Framework in March

20042004

Several problems encountered Interest rate changes during a maintenance

period

Underbidding in tenders, because of interest rate expectations and overlapping tenders

‘Weekend’ problem in minimum reserves and use of standing facilities

I Modification of Operational I Modification of Operational Framework in March Framework in March

20042004

Several problems encountered Interest rate changes during a maintenance

period

Underbidding in tenders, because of interest rate expectations and overlapping tenders

‘Weekend’ problem in minimum reserves and use of standing facilities

I Modification of Operational I Modification of Operational Framework in March Framework in March

20042004

Solution:

Changing maintenance period from ‘Monetary

Council meeting’ to the next Monetary council.

Shortening the duration of the MRO’s to one

week

I Modification of Operational I Modification of Operational Framework in March Framework in March

20042004

Solution:

Changing maintenance period from ‘Monetary

Council meeting’ to the next Monetary council.

Shortening the duration of the MRO’s to one

week

II Transparency of allotment policyII Transparency of allotment policy

Till March 2004: only publication of forecast for autonomous factors Sometimes wrong interpretation of allotment by

the market New information about autonomous factors andexcess reserves by daily update ECB LM figures From March 2004: publication of Benchmarkallotment, before and after allotment Nowadays frontloading (more than benchmarkallotment) as lubricant to buffer micro-economicfrictions in the money market.

II Transparency of allotment policyII Transparency of allotment policy

Till March 2004: only publication of forecast for autonomous factors Sometimes wrong interpretation of allotment by

the market New information about autonomous factors andexcess reserves by daily update ECB LM figures From March 2004: publication of Benchmarkallotment, before and after allotment Nowadays frontloading (more than benchmarkallotment) as lubricant to buffer micro-economicfrictions in the money market.

III Volatility Treasury DepositIII Volatility Treasury Deposit

Large swings in treasury deposits hampered

efficient liquidity management by ECB

Measures to limit volatility

Remuneration

Arrangements (Italy)

III Volatility Treasury DepositIII Volatility Treasury Deposit

Large swings in treasury deposits hampered

efficient liquidity management by ECB

Measures to limit volatility

Remuneration

Arrangements (Italy)

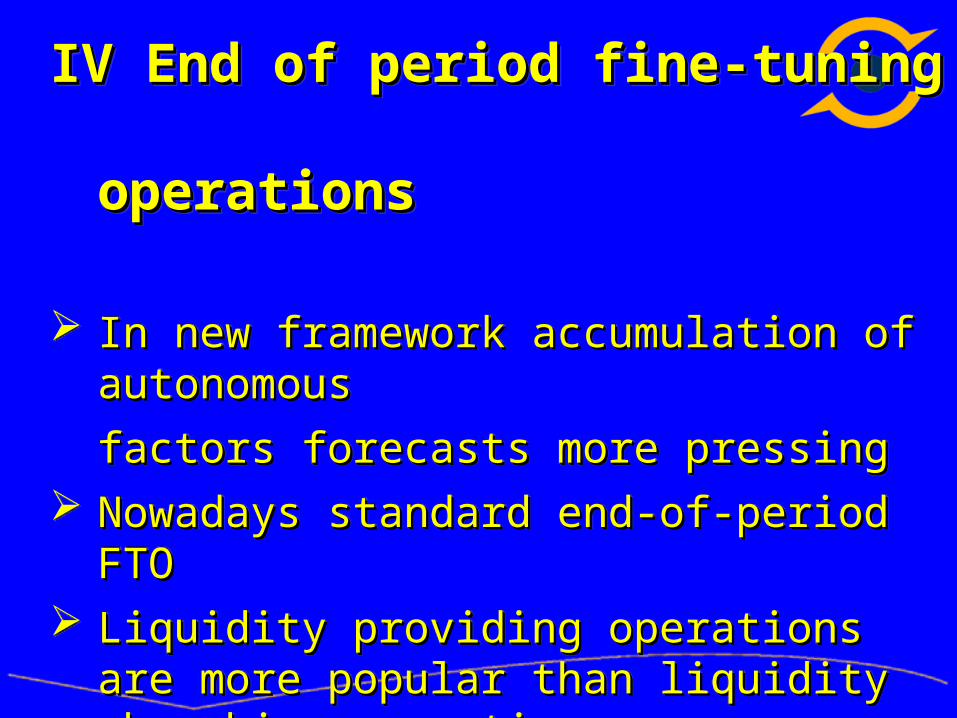

IV End of period fine-tuningIV End of period fine-tuning operationsoperations

In new framework accumulation of autonomousIn new framework accumulation of autonomous

factors forecasts more pressing factors forecasts more pressing Nowadays standard end-of-period FTO Nowadays standard end-of-period FTO Liquidity providing operations are more popular Liquidity providing operations are more popular

than liquidity absorbing operationsthan liquidity absorbing operations Reason: timing of operation, interest rate Reason: timing of operation, interest rate

operation, different specification operation, different specification

IV End of period fine-tuningIV End of period fine-tuning operationsoperations

In new framework accumulation of autonomousIn new framework accumulation of autonomous

factors forecasts more pressing factors forecasts more pressing Nowadays standard end-of-period FTO Nowadays standard end-of-period FTO Liquidity providing operations are more popular Liquidity providing operations are more popular

than liquidity absorbing operationsthan liquidity absorbing operations Reason: timing of operation, interest rate Reason: timing of operation, interest rate

operation, different specification operation, different specification

V EONIA SwapsV EONIA Swaps

Interest rate swaps from 1 week to 12 months

used for: hedging interest rate risk (transform fixed

debt into variable or reverse)arbitrage

taking positions on the curve

EONIA swap market is a very large market Sometimes spill-overs on operational target/Cashmarket

V EONIA SwapsV EONIA Swaps

Interest rate swaps from 1 week to 12 months

used for: hedging interest rate risk (transform fixed

debt into variable or reverse)arbitrage

taking positions on the curve

EONIA swap market is a very large market Sometimes spill-overs on operational target/Cashmarket

EONIA swap hedge example (1)

Credit to customer for 12 months at 3.5% Does not want to fund for 12 months, but want to

hedge interest rate risk Solution: a 12 months EONIA (payer)swap at

2.26% pay the fix (2.26%) and receive the floating

(EONIA) fund daily in the overnight market and pay the

EONIA (or less) Difference is calculated daily (compounding) and

settled at the end of the period

EONIA swap hedge example (1)

Credit to customer for 12 months at 3.5% Does not want to fund for 12 months, but want to

hedge interest rate risk Solution: a 12 months EONIA (payer)swap at

2.26% pay the fix (2.26%) and receive the floating

(EONIA) fund daily in the overnight market and pay the

EONIA (or less) Difference is calculated daily (compounding) and

settled at the end of the period

EONIA swap hedge example (2)

Issue 12 month paper to cover deficit Does not want the 12 month interest rate

exposure So conclude a 12 months EONIA (receiver)swap

at 2.24% receive the fix (2.24%) and pay EONIA

EONIA swap hedge example (2)

Issue 12 month paper to cover deficit Does not want the 12 month interest rate

exposure So conclude a 12 months EONIA (receiver)swap

at 2.24% receive the fix (2.24%) and pay EONIA

VI. Optimal size and composition openVI. Optimal size and composition open

market operationsmarket operations

VI. Optimal size and composition openVI. Optimal size and composition open

market operationsmarket operationsFigure 1 Simplified Eurosystem Balance Sheet, Figures in normal letters: February 2007, figures in brackets: June 2000, all figures in EUR billions

Autonomous factors Autonomous factors

Net foreign assets (A1+A2+A3-L7-L8-L9) 321,8 (378) Banknotes in circulation (L1) 604,4 (353)Net assets denominated in euro´s (A4-L6+A7+A11.2) 266,5 (92) Government Deposits (L5.1) 35,8 (42)

Other autonomous factors (net) * 180,7 (155,6)

Reserve requirements (L2.1) 183,9 (113,4)

Monetary Policy Instruments Monetary Policy Instruments

Main Refinancing Operation (A5.1) 286,5 (134) Deposit Facility (L2.2) 0,0 (0)Longer Term Refinancing Operation (A5.2) 130,0 (60)

Marginal lending facility (A5.5) 0.0 (0)

1004,8 (664) 1004,8 (664)

Source: ECB Liquidity Management Data and own calculations.

Figures in brackets refer to relevant balance sheet item Balance sheet identity: Ca = OMO + ML - DF - AF* (A5.6+A6+A8+A10+A11.1+A11.3+A11.4-L2.5-L3-L5.2-L10-L12-L13-L14-L15)

VI. Optimal size and composition openVI. Optimal size and composition openmarket operationsmarket operations

Implications for monetary policy Implications for monetary policy implementation?implementation?

Not convinced that current situation requiresNot convinced that current situation requires substantial changessubstantial changes Substantial reduction of reserve ratioSubstantial reduction of reserve ratio Maybe more reverse LTRO´s or structural Maybe more reverse LTRO´s or structural

operationsoperations No monetary policy outright portfolio No monetary policy outright portfolio

VI. Optimal size and composition openVI. Optimal size and composition openmarket operationsmarket operations

Implications for monetary policy Implications for monetary policy implementation?implementation?

Not convinced that current situation requiresNot convinced that current situation requires substantial changessubstantial changes Substantial reduction of reserve ratioSubstantial reduction of reserve ratio Maybe more reverse LTRO´s or structural Maybe more reverse LTRO´s or structural

operationsoperations No monetary policy outright portfolio No monetary policy outright portfolio

VII Future challenges:VII Future challenges:

a)a) the management of the volatility of short term the management of the volatility of short term interest ratesinterest rates

b)b) determining the optimal size and composition of determining the optimal size and composition of central bank balance sheetcentral bank balance sheet

c)c) the appropriate level of communication with the the appropriate level of communication with the financial marketsfinancial markets

d)d) contribute to further integration of financial contribute to further integration of financial markets by harmonising and expanding collateral markets by harmonising and expanding collateral instrumentsinstruments

VII Future challenges:VII Future challenges:

a)a) the management of the volatility of short term the management of the volatility of short term interest ratesinterest rates

b)b) determining the optimal size and composition of determining the optimal size and composition of central bank balance sheetcentral bank balance sheet

c)c) the appropriate level of communication with the the appropriate level of communication with the financial marketsfinancial markets

d)d) contribute to further integration of financial contribute to further integration of financial markets by harmonising and expanding collateral markets by harmonising and expanding collateral instrumentsinstruments

Questions ?Questions ?Questions ?Questions ?

Hans PijlHans PijlDivision Financial Markets Division Financial Markets Department Treasury and MonitoringDepartment Treasury and Monitoring

Phone number 00 31 20 524 2214 Phone number 00 31 20 524 2214