1 Introduction Basic concepts Basic concepts Terminology Terminology.

Auditing – Study Notes Chapter 2: Basic Concepts of Auditing

Page | 8

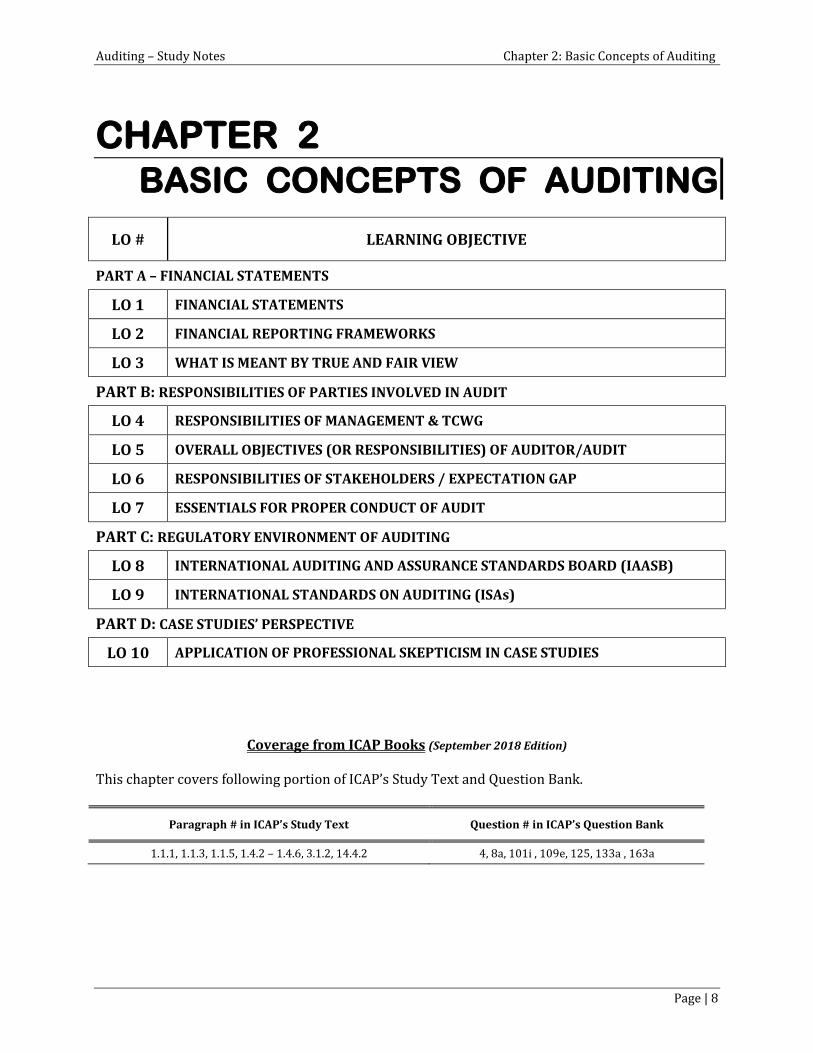

CHAPTER 2 BASIC CONCEPTS OF AUDITING

LO # LEARNING OBJECTIVE

PART A – FINANCIAL STATEMENTS

LO 1 FINANCIAL STATEMENTS

LO 2 FINANCIAL REPORTING FRAMEWORKS

LO 3 WHAT IS MEANT BY TRUE AND FAIR VIEW

PART B: RESPONSIBILITIES OF PARTIES INVOLVED IN AUDIT

LO 4 RESPONSIBILITIES OF MANAGEMENT & TCWG

LO 5 OVERALL OBJECTIVES (OR RESPONSIBILITIES) OF AUDITOR/AUDIT

LO 6 RESPONSIBILITIES OF STAKEHOLDERS / EXPECTATION GAP

LO 7 ESSENTIALS FOR PROPER CONDUCT OF AUDIT

PART C: REGULATORY ENVIRONMENT OF AUDITING

LO 8 INTERNATIONAL AUDITING AND ASSURANCE STANDARDS BOARD (IAASB)

LO 9 INTERNATIONAL STANDARDS ON AUDITING (ISAs)

PART D: CASE STUDIES’ PERSPECTIVE

LO 10 APPLICATION OF PROFESSIONAL SKEPTICISM IN CASE STUDIES

Coverage from ICAP Books (September 2018 Edition) This chapter covers following portion of ICAP’s Study Text and Question Bank.

Paragraph # in ICAP’s Study Text Question # in ICAP’s Question Bank

1.1.1, 1.1.3, 1.1.5, 1.4.2 – 1.4.6, 3.1.2, 14.4.2 4, 8a, 101i , 109e, 125, 133a , 163a

Auditing – Study Notes Chapter 2: Basic Concepts of Auditing

Page | 9

PART A – FINANCIAL STATEMENTS Auditor is required to express opinion whether financial statements have been prepared in accordance with applicable financial reporting framework (AFRF), and give true and fair view.

LO 1: FINANCIAL STATEMENTS: Financial statements means structured representation of historical (i.e. past) financial information. Components of financial statements depend on AFRF, and usually include:

1. Statement of financial position. 2. Statement of profit or loss, and Other Comprehensive income. 3. Statement of changes in equity. 4. Cash Flow Statement. 5. Notes to the financial statements, including summary of significant accounting policies and

other explanatory information.

CONCEPT REVIEW QUESTION Q. 1 What parts of a company’s annual report are covered by an audit report? (02 marks)

(ICAEW Professional Stage – September 2006)

LO 2: FINANCIAL REPORTING FRAMEWORKS: A financial reporting framework is a set of criteria used to prepare financial statements. Types of Frameworks: There are many types of frameworks e.g. :

1. General Purpose (for wide range of users), and Special Purpose (for specific users). 2. Fair presentation Framework, and Compliance Framework.

Fair Presentation Framework: Fair presentation framework is a financial reporting framework that requires compliance with requirements of the framework, and contains acknowledgment that, to achieve fair presentation, it may be necessary for management:

To provide disclosures in addition to specific requirements of framework or To depart from a requirement of framework

In Fair presentation framework, auditor expresses opinion whether:

“financial statements give true and fair view in accordance with the framework”, or “financial statements are presented fairly, in all material respects, in accordance with the

framework”. (Both phrases are equivalent) An example is International Financial Reporting Standards. Compliance Framework: Compliance framework is a financial reporting framework that requires compliance with requirements of the framework, and does not contain acknowledgements which are contained in fair presentation framework (regarding additional disclosures or departure from requirements of framework to achieve fair presentation).

Auditing – Study Notes Chapter 2: Basic Concepts of Auditing

Page | 10

In Compliance framework, auditor expresses opinion whether “financial statements are prepared, in all material respects, in accordance with the framework”. An example is Tax-basis Framework. Applicable Financial Reporting Framework (AFRF): AFRF is the financial reporting framework adopted by management and Those Charged With Governance (TCWG), in preparation of financial statements considering legal requirements, nature of entity, nature of financial statements, and purpose of financial statements. AFRF includes financial reporting standards (e.g. IFRS), and may be supplemented by law or regulation (e.g. Companies Act 2017). If AFRF is other than IFRS, jurisdiction of framework shall also be referred in opinion.

CONCEPT REVIEW QUESTION Q. 2 Differentiate between the Fair presentation framework and Compliance framework (04)

(ICAP, CAF 09 Level – Spring 2012) (ICAP’s Official Question Bank for CAF 09 – Q. # 101i)

LO 3: WHAT IS MEANT BY TRUE AND FAIR VIEW: Term “true and fair view” or “fair presentation” have no legal definition. Generally:

true means free from errors, and fair means free from undue bias in preparation or presentation of financial statements.

The phrase “True and fair view” indicates that judgment is applied in preparation of financial statements by management, and in expressing opinion by auditor.

CONCEPT REVIEW QUESTION Q. 3 Discuss the concept of fair presentation (true and fair view) in relation to the financial statements. (02)

(ICAP, CAF 09 Level – Spring 2017, Q. # 6b) (ICAP’s Official Question Bank for CAF 09 – Q. # 125)

Study Tips 1. Auditor shall accept proposed audit engagement, only if AFRF is acceptable. 2. Management means persons responsible for operational and managerial duties (e.g. CFO, CEO).

TCWG means persons responsible for Overseeing the strategic direction and Accountability (e.g. Directors).

3. As a general rule, if there is conflict between international standards and local laws then local laws will prevail. However, compliance with international standards cannot be stated unless all standards have been fully complied.

Auditing – Study Notes Chapter 2: Basic Concepts of Auditing

Page | 11

PART B – RESPONSIBILITIES OF PARTIES INVOLVED IN AUDIT

LO 4: RESPONSIBILITIES OF MANAGEMENT/TCWG: An audit is conducted on the premise that management (and where applicable TCWG) is responsible:

1. For preparation and presentation of financial statements in accordance with AFRF. This includes to identify AFRF, prepare and present financial statements in accordance with AFRF, selecting and applying appropriate accounting policies and reasonable estimates.

2. For design and implementation and operating effectiveness of such internal controls which are necessary for preparation of reliable financial statements;

3. To provide auditor with: a. all relevant information, b. additional information requested by auditor, and c. unrestricted access to persons within the entity to obtain evidence.

4. Other responsibilities include prevention and detection of fraud, and to provide written representation to auditor at end of audit.

CONCEPT REVIEW QUESTION Q. 4 Briefly highlight the management’s responsibilities relating to the financial statements? (04)

(ICAP, CAF 09 Level – Autumn 2009) (ICAP’s Official Question Bank for CAF 09 – Q. # 4a)

Q. 5 Discuss as to who is responsible to prepare financial statements. (02)

(ICAP, CAF 09 Level – Spring 2002)

LO 5: OVERALL OBJECTIVES (OR RESPONSIBILITIES) OF AUDITOR/AUDIT: The overall objectives of the auditor are:

To obtain reasonable assurance whether financial statements are free from material misstatement (whether due to error or fraud), to enable auditor to express opinion whether financial statements are prepared, in all material respects, in accordance with the AFRF,

To issue audit report on the financial statements, and communicate as required by the ISAs in accordance with the auditor’s findings

CONCEPT REVIEW QUESTION Q. 6 What is the primary/overall objective of an audit? (03)

(ICAP, CAF 09 Level – Autumn 2001) Q. 7 The purpose of an external audit and its role are not well understood. You have been asked to write some material for inclusion in your firm’s training materials dealing with these issues in the audit of large companies. Required: Draft an explanation dealing with the purpose of an external audit and its role in the audit of large companies, for the inclusion in your firm’s training materials.

(ICAP’s Official Question Bank for CAF 09 – Q. # 8a)

Auditing – Study Notes Chapter 2: Basic Concepts of Auditing

Page | 12

Q. 8 You are the audit manager of Rake Enterprises, a limited liability company. The company’s annual revenue is over Rs 100 million. Required: Compare the responsibilities of the directors and auditors regarding the published financial statements of Rake Enterprises.

(ACCA, Fundamentals Level F8 – June 2005) (ICAP’s Official Question Bank for CAF 09 – Q. # 163a)

LO 6: RESPONSIBILITIES OF STAKEHOLDERS / EXPECTATION GAP: It is the responsibility of stakeholders to understand and eliminate expectation gap so that scope of audit is not misunderstood. Expectation Gap: Expectation gap means public perception of the role and responsibilities of the external auditor is different (and is usually higher) from his statutory role and responsibilities. Some Common Misunderstandings (i.e. Expectation Gap) about Audit:

1. Auditor prepares financial statements. 2. Auditor checks 100% transactions of entity during the accounting period. 3. Auditor provides absolute assurance (i.e. he certifies or guarantees that financial statements

are correct in all respects, and can be relied for all decision making purposes). 4. Auditor is responsible to prevent and detect fraud. 5. Auditor is responsible to express opinion on internal controls. 6. Emphasis of Matter Paragraph, Other Matter Paragraph, and Material Uncertainty related to

Going Concern Paragraph are modified opinions. Consequences of Expectation Gap: It increases tendency of users to make wrong decisions on the basis of audit report, and to file legal actions against auditors on frivolous basis (i.e. without any valid basis). How to Reduce Expectation Gap: Expectation gap can be reduced by:

1. Mentioning management’s responsibilities, and auditor’s responsibilities in Engagement Letter and Auditor’s Report.

2. Expanding and improving the format of auditor’s report to clarify responsibilities of auditor. 3. Implementation of regulations to explain responsibilities of management/directors e.g.

Code of Corporate Governance by SECP. 4. Public awareness on scope of audit and responsibilities of auditor.

CONCEPT REVIEW QUESTION Q. 9 Explain the term ‘Expectation Gap’ in the context of an audit and give three examples of expectation gap. (04)

(ICAP, CAF 09 Level – Autumn 2015) (ICAP’s Official Question Bank for CAF 09 – Q. # 133a)

Auditing – Study Notes Chapter 2: Basic Concepts of Auditing

Page | 13

Q. 10 You are the audit manager of Polycrafts Limited for two years. During the audit for the year ended 30th June, 2017, the management communicated to you a misstatement identified in previous year accounting entries that was not corrected by the auditors. Management is of the view that auditor is responsible for identifying all the misstatements, whether due to fraud or error. (a) Explain the term “Expectation Gap”. (03) (b) Discuss whether you agree with the views expressed by the management. (03) (c) List down the factors due to which auditor is unable to provide absolute assurance. (05)

(PIPFA – Winter 2017) Q. 11 What is the “expectation gap” and how could it be removed or reduced by the auditing profession? (04)

(ICAP, CFAP 06 Level – Winter 1993)

LO 7: ESSENTIALS FOR PROPER CONDUCT OF AUDIT: 1. Professional Judgment:

Professional Judgment is the application of Cumulative Audit Knowledge, Experience and Training (within the context of accounting, auditing, and ethical standards), to reach an appropriate course of action or conclusion during an audit. Auditor is required apply professional judgment in planning and performing the audit.

2. Professional Skepticism:

Professional skepticism is an attitude that includes: i. a questioning mind,

ii. being alert to conditions which indicate possible misstatement (due to error or fraud), and

iii. critical assessment of audit evidence. Even if management has shown honesty and integrity in past, still auditor shall apply professional skepticism in planning and performing the audit. He shall corroborate every assertion of management, by obtaining persuasive evidence. Importance of Professional Skepticism: Professional skepticism is necessary:

To identify risk of material misstatements. To critically assess audit evidence, and To determine sufficiency and appropriateness of audit evidence.

Professional skepticism helps auditor to reduce risks of:

Overlooking unusual circumstances. Over-generalizing when drawing conclusions from audit observations. Using inappropriate assumptions in determining audit procedures, and evaluating

results. 3. Independence:

Independence means auditor should be free to perform audit procedures without any bias or influence. Auditor should be Independent of financial, personal and employment relations with client. (This concept will be discussed in detail in Chapters # 6 & 7.)

Auditing – Study Notes Chapter 2: Basic Concepts of Auditing

Page | 14

CONCEPT REVIEW QUESTION Q. 12 Briefly discuss the concept of ‘Professional skepticism’. (03)

(ICAP, CAF 09 Level – Spring 2016) (ICAP’s Official Question Bank for CAF 09 – Q. # 109e)

Q. 13 During the audit team planning meeting, a member of the audit team passed a comment that based on past experience with the client, he was confident that the management of the client was honest and there was no issue as regards management integrity or risk of fraud in the Company. The audit manager responded that the auditor should always maintain an attitude of professional skepticism throughout the audit. Required: Briefly describe ‘Audit Skepticism’ and elaborate on the response of the audit manager. (04)

(ICAP, CAF 09 Level – Autumn 2009) (ICAP’s Official Question Bank for CAF 09 – Q. # 4b)

Q. 14 Aslam is a junior member of your audit team. During an informal discussion with your team members, Aslam has inquired you about the reasons of emphasizing on professional scepticism when honesty and integrity of the management is not questionable based on prior experience. Briefly respond to the inquiry of Aslam. (03)

(ICAP, CAF 09 Level – Autumn 2019, Q. # 2a)

PART C – REGULATORY ENVIRONMENT OF AUDITING

LO 8: INTERNATIONAL AUDITING AND ASSURANCE STANDARDS BOARD: International Federation of Accountants: IFAC is the worldwide leader of audit profession. It is the global organization of professional accountants dedicated to serving the public interest. Functions/Role/Activities of IFAC: IFAC supports the development of profession in the area of ①auditing, ②ethics, ③professional education and ④public sector by following activities:

1. development of high-quality standards and guidance. 2. facilitating the adoption and implementation of standards and guidance. 3. promoting the value of professional accountants worldwide. 4. speaking out on public interest issues where professional voice is important.

Boards of IFAC: IFAC includes following four boards:

1. International Auditing and Assurance Standards Board (IAASB) 2. International Ethics Standards Board for Accountants (IESBA) 3. International Public Sector Accounting Standards Board (IPSASB) 4. International Accounting Education Standards Board (IAESB)

International Auditing and Assurance Standards Board (IAASB): IAASB is one of the boards within IFAC, and performs following activities:

1. It develops and promotes standards to be applied in providing the audit, review and related services.

2. It also provides facilitation in adoption and implementation of international standards. In doing so, IAASB enhances quality and consistency of assurance practice throughout the world.

Auditing – Study Notes Chapter 2: Basic Concepts of Auditing

Page | 15

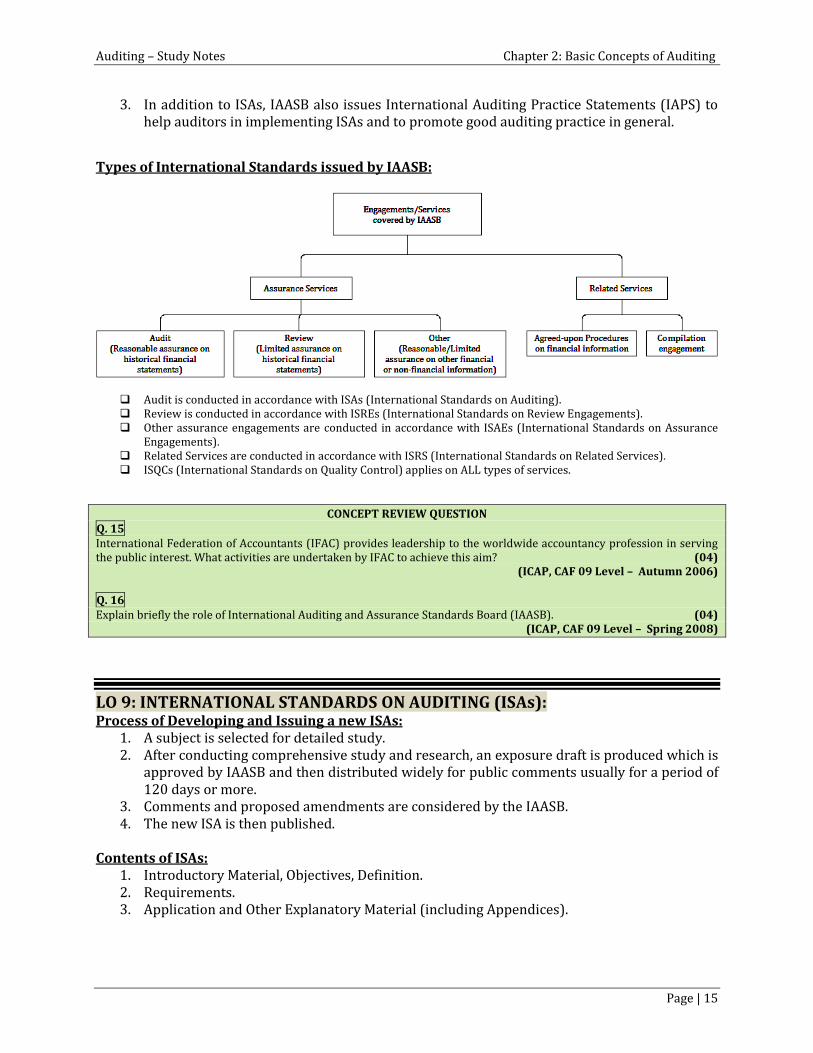

3. In addition to ISAs, IAASB also issues International Auditing Practice Statements (IAPS) to help auditors in implementing ISAs and to promote good auditing practice in general.

Types of International Standards issued by IAASB:

Audit is conducted in accordance with ISAs (International Standards on Auditing). Review is conducted in accordance with ISREs (International Standards on Review Engagements). Other assurance engagements are conducted in accordance with ISAEs (International Standards on Assurance

Engagements). Related Services are conducted in accordance with ISRS (International Standards on Related Services). ISQCs (International Standards on Quality Control) applies on ALL types of services.

CONCEPT REVIEW QUESTION Q. 15 International Federation of Accountants (IFAC) provides leadership to the worldwide accountancy profession in serving the public interest. What activities are undertaken by IFAC to achieve this aim? (04)

(ICAP, CAF 09 Level – Autumn 2006) Q. 16 Explain briefly the role of International Auditing and Assurance Standards Board (IAASB). (04)

(ICAP, CAF 09 Level – Spring 2008)

LO 9: INTERNATIONAL STANDARDS ON AUDITING (ISAs): Process of Developing and Issuing a new ISAs:

1. A subject is selected for detailed study. 2. After conducting comprehensive study and research, an exposure draft is produced which is

approved by IAASB and then distributed widely for public comments usually for a period of 120 days or more.

3. Comments and proposed amendments are considered by the IAASB. 4. The new ISA is then published.

Contents of ISAs:

1. Introductory Material, Objectives, Definition. 2. Requirements. 3. Application and Other Explanatory Material (including Appendices).

Auditing – Study Notes Chapter 2: Basic Concepts of Auditing

Page | 16

Authority/Status of ISAs: In Pakistan, audit is conducted in accordance ISAs. To obtain reasonable assurance, it is compulsory for auditors to comply with all requirements of all ISAs. Exception to follow requirements of ISA: A required procedure will not be performed if it is:

not relevant or not practicable.

However, if a procedure is not practicable, auditor shall document:

reason of departure from required procedure, and alternative procedures performed to obtain evidence/assurance.

CONCEPT REVIEW QUESTION Q. 17 International Standards on Auditing (ISAs) are issued by the International Auditing and assurance Standard Board (IAASB). In this context, explain the following: (i) The position of these standards relating to external audit process (02) (ii) The extent to which an auditor must follow ISAs. (02)

(ICMA Pakistan – Fall 2017)

Auditing – Study Notes Chapter 2: Basic Concepts of Auditing

Page | 17

PART D– CASE STUDIES’ PERSPECTIVE

LO 10: APPLICATION OF PROFESSIONAL SKEPTICISM IN CASE STUDIES: Following situations in case studies must increase your risk:

1. Intended sale of shares/business, or acquiring loan. 2. Unusual growth or decrease of sales. 3. Management’s bonuses based on financial performance. 4. Significant transactions at year end. 5. Imports and Exports. 6. Cash for Sale or purchase is received (or paid) in advance 7. Inconsistency between different sources of evidences e.g.

a. Management Vs. Lawyer b. Financial Statements Vs. Other Information c. Debtors’ Confirmation Letter Vs. Amount recorded in sales ledger. d. Amount Estimated by auditor (through Analytical procedures) Vs. Amount actually Recorded in F/S

8. Going Concern Issues e.g. increased competition, product failures, operating losses 9. Significant related party transactions. 10. Significant Income, Expenses, Assets, and Liabilities are based on estimates. 11. Identified deficiencies in internal controls (e.g. No Approval, Reconciliations or Segregation of duties). 12. Lack of competence or integrity in management or employees. 13. Valuation of inventory (Decrease in sales/demand, Long-standing inventory/increase in inventory turnover

ratio, Defective goods in inventory, Cost of production increases, or Sale price decreases, If product is malfunctioning, New products are launched by company or competitor, Contract of specialized inventory is cancelled or customer goes bankrupt, Defective goods returned by customers.)

14. Inventory is held at various locations or Inventory is held with third party or Physical count was not done at balance sheet date.

15. Additions to fixed assets (Major fixed assets purchased during the year, or Significant capital expenditures incurred during the year)

16. Revaluation of PPE. 17. Closure of a factory 18. Provision for warranty (Increase in warranty period/complains, Malfunctioning of products) 19. Onerous contracts 20. There is dispute with major debtor e.g. on defective goods (this may require provision for debtors, write-down

of inventory to NRV, and impairment of machinery). 21. There are pending litigations against company (unfair dismissal of staff, serious accident damaging environment

or injuring people, malfunctioning of product) 22. Other Risks:

a. Company deals in multiple products (Segment Reporting) b. Risk of inappropriate treatment of contingent liabilities and contingent assets. c. Restricted time schedule for audit (Audit team may not have time to obtain sufficient appropriate audit

evidence.) d. Predecessor auditor did not wish to be reappointed, or predecessor auditor expressed modified

opinion. e. Auditor is appointed this year (first year of audit)

CONCEPT REVIEW QUESTION

Q. 18 An auditor is required to maintain an attitude of ‘Professional Skepticism’ while conducting an audit of Financial Statements. Describe by giving TWO appropriate examples, the term Professional Skepticism. (04)

(PIPFA – Summer 2015)

Auditing – Study Notes Chapter 2: Basic Concepts of Auditing

Page | 18

APX 1: HINTS & COMMENTS TO CONCEPT REVIEW QUESTIONS: Q. 1 Annual report contains components of financial statements as well as other information (e.g. directors’ report). However, audit report covers 5 components of financial statements only (as in LO 1). Q. 2 Easy question, but don’t forget to give example of each framework with definition (as in LO 2). Q. 3 While describing true and fair, don’t forget to mention that this term has not been defined in law, IFRS, or ISAs (as in LO 3). Q. 4 Easy question to be reproduced from notes (as in LO 4). Q. 5 Management and TCWG. (as in LO 4) Q. 6 Easy question to be reproduced from LO 6. Q. 7 Note that question has two parts:

1. purpose of an external audit (i.e. objective of audit), (Ch. 2, LO 5)and 2. role in the audit of large companies (i.e. advantages of audit) (Ch. 1, LO 1)

You must present both parts separately giving suitable headings in your answer. Q. 8 Easy question to be reproduced from LO 4 and LO 5. Q. 9 Easy question to be reproduced from LO 6. Q. 10 (a) Easy question to be reproduced from LO 6. Although examples are not specifically required in question, however, you must also give some examples to explain the concept. (b)No. Auditor is not responsible to detect immaterial error or fraud. Further, regarding material error or fraud, auditor provides only reasonable assurance because of inherent limitations of audit. (c) This part relates to Chapter # 1 (LO 1: Inherent Limitations). Q. 11 Easy question to be reproduced from LO 6. Q. 12 Explanatory line should also be written alongwith 03 points of professional skepticism. Q. 13 Question has two parts:

1. definition of audit skepticism (i.e. professional skepticism) 2. elaboration. (Students should give some examples of situations in which it is particularly important to apply

professional skepticism. These examples are given in the LO 10). Q. 14 Refer to importance of Professional Skepticism, in LO 7 subheading “Professional Skepticism”.

Auditing – Study Notes Chapter 2: Basic Concepts of Auditing

Page | 19

Q. 15 Easy question to be reproduced from LO 8. However, students did not perform well in this question. Q. 16 Easy question to be reproduced from LO 8. However, students did not perform well in this question. Q. 17 (i) reproduce “authority/status of ISAs”. (ii) reproduce “exception to follow requirements of ISA” Many candidates could not understand in exam what was required. Q. 18 Easy question to be reproduced from notes.

APX 2: SELF ASSESSMENT QUESTIONS:

Q.1 (a) What factors are considered by management in adoption of applicable financial reporting framework (AFRF). (02) (b) Auditor has to determine whether (AFRF) is acceptable or not. What shall be auditor’s course of action if AFRS is NOT acceptable. (01)

Q.2 Briefly discuss what is meant by the term ‘true and fair view’ in the context of audit of financial statements. (03) (ICAP, CAF 09 Level – Spring 2002)

Q.3 An auditor is required to express his opinion on the true and fair view of the financial statements. What do you

understand by the term “true and fair view”? (03) (ICAP, CAF 09 Level – Spring 2001)

Q.4 Briefly discuss the term “true and fair view” in the context of an audit. (03)

(ICAP, CAF 09 Level – Spring 2004)

Q.5 Explain the meaning of ‘True and Fair’. (03)

(ICAP, CFAP 06 Level – Winter 1994)

Q.6 The external auditors are responsible to give their opinion on the truth and fairness of the financial statements of a company produced by the management. Explain what do you understand by the concept of true and fair presentation of financial statements. (05)

(ICMA Pakistan – Summer 2017)

Q.7 What are the responsibilities of management and auditor in relation to audit of financial statements. (ICAP, CAF 09 Level – Adapted)

Q.8 What is the primary objective of an audit? (02)

(ICAP, CAF 09 Level – Autumn 2001) Q.9 Define professional skepticism. (03)

(ICAP, CAF 09 Level – Spring 2001)

Q.10 State the objective of an audit of financial statements. (ACCA F8 Adapted)

Q.11 What are the principal misunderstandings made by lay users of audited financial statements that are commonly referred

to as “The Expectation Gap”? (02) (ICAEW– Professional, September 2007)

Auditing – Study Notes Chapter 2: Basic Concepts of Auditing

Page | 20

Q.12 Outline the measures adopted in the UK to address the expectation gap. (02) (ICAEW– Professional, March 2011)

Q.13 Which subsidiary board of International Federation of Accountants (IFAC) is authorized to develop and promote

International Standards on Auditing (ISAs)? State the reasons why does an auditor need to learn about the key principles and requirements of the International Standards on Auditing (ISAs)? (04 marks)

(ICMA Pakistan, Professional Level P2 – 2015 March)

Q.14 Briefly describe the meaning of professional judgment. Identify the key decisions/areas where an auditor may need to

apply professional judgment. (08) (ICAP, CAF 09 Level – Spring 2013)

Q.15 Rabia is a newly inducted trainee student in the audit firm. She thinks that auditor should conduct an audit with a

detective approach and should look only for frauds. The principal, Mr. Ahmed tells her that audit has to be conducted with an approach of professional skepticism. The principal has asked you to explain the concept of professional skepticism to Rabia. (04)

(ICAP, CAF 09 Level – Autumn 2002) Q.16 The auditor should plan and perform the audit with a certain attitude. Identify and describe this attitude with an example.

(02) (ICAP, CFAP 06 Level – Summer 1998)

Q.17 Auditors are required to plan and perform an audit with professional scepticism, to exercise professional judgement and

to comply with ethical standards. Required:

(i) Explain what is meant by ‘professional scepticism’ and why it is so important that the auditor maintains professional scepticism throughout the audit. (03)

(ii) Define ‘professional judgement’ and describe two areas where professional judgement is applied when planning an audit of financial statements. (03)

(ACCA F8 Adapted)

Q.18 What is the role of International Federation of Accountants (IFAC)? (04) (ICAP, CAF 09 Level – Autumn 2002)

Q.19 What is the IAASB?

(ACCA P7 Adapted)

Q.20 State what "IFAC" stands for. (ACCA F8 Adapted)

Q.21 State the objective of the International Auditing and Assurance Standards Board (IAASB).

(ACCA F8 Adapted)

Q.22 What is the function of IFAC? (ACCA F8 Adapted)

Q.23 Explain the status of International Standards on Auditing. (02)

(ACCA, Fundamentals Level F8 – December 2010)