Basic Accounting Concepts

18

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part. Basic Accounting Concepts Chapte r 2

-

Upload

malik-melton -

Category

Documents

-

view

128 -

download

3

description

Basic Accounting Concepts. Chapter 2. Learning Objectives. After studying this chapter, you should be able to: Describe the basic elements of a financial accounting system. Analyze, record, and summarize transactions for a corporation’s first period of operations. - PowerPoint PPT Presentation

Transcript of Basic Accounting Concepts

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Basic AccountingConcepts Chapter

2

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Learning Objectives

After studying this chapter, you should be able to:

•Describe the basic elements of a financial accounting system.

•Analyze, record, and summarize transactions for a corporation’s first period of operations.

•Prepare financial statements for a corporation’s first period of operations.

•Analyze, record, and summarize transactions for a corporation’s second period of operations.

•Prepare financial statements for a corporation’s second period of operations.

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Learning Objective 1

Describe the basic elements of a financial accounting system

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

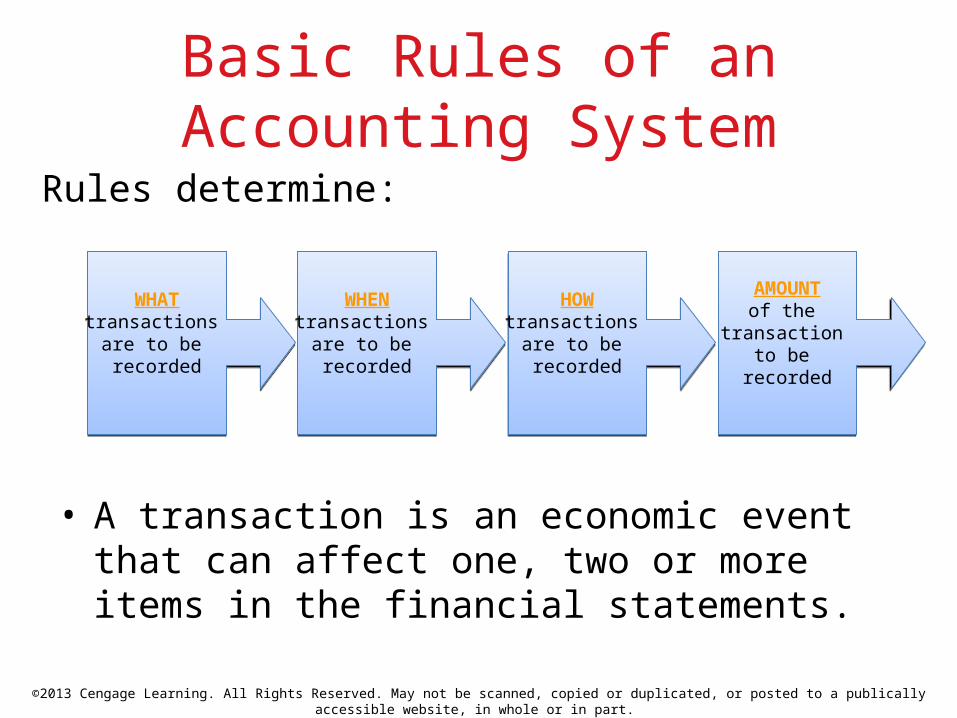

Basic Rules of an Accounting System

• A transaction is an economic event that can affect one, two or more items in the financial statements.

Rules determine:

WHATtransactions

are to be recorded

WHATtransactions

are to be recorded

WHENtransactions

are to be recorded

WHENtransactions

are to be recorded

HOWtransactions

are to be recorded

HOWtransactions

are to be recorded

AMOUNTof the

transaction to be

recorded

AMOUNTof the

transaction to be

recorded

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

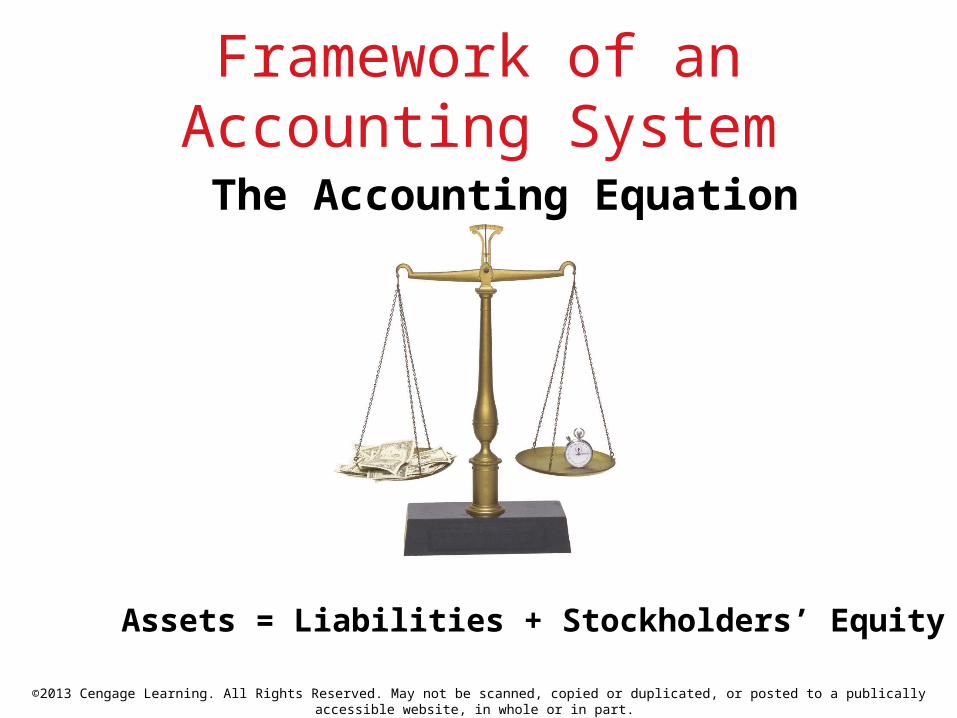

Framework of an Accounting System

Assets = Liabilities + Stockholders’ Equity

The Accounting Equation

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

• By expanding the accounting equation, transactions can be analyzed, summarized, and recorded within the integrated financial statement framework.

Integrated Financial Statement Framework: Template

Impact of transactionon cash

Impact of transactionon Income Statement

Exhibit 1: Integrated Financial Statement Framework

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Controls of an Accounting System

THE ACCOUNTING EQUATION

MUSTBALANCE

THE ACCOUNTING EQUATION

MUSTBALANCE

Ending Cash on Balance Sheet = Ending Cash on

Statement of Cash Flows

Ending Cash on Balance Sheet = Ending Cash on

Statement of Cash Flows

Net Income on Income Statement =

Net Effects of Revenues/Expenses

on Retained Earnings

Net Income on Income Statement =

Net Effects of Revenues/Expenses

on Retained Earnings

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Learning Objective 2

Analyze, record, and summarize transactions for a corporation’s first

period of operations

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

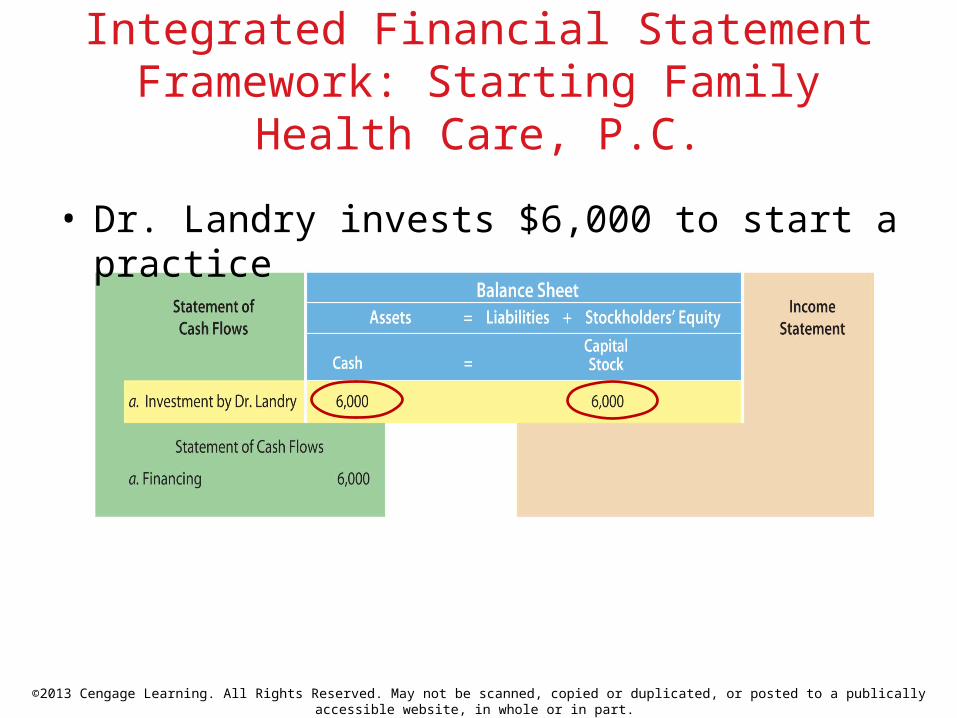

• Dr. Landry invests $6,000 to start a practice

Integrated Financial Statement Framework: Starting Family Health Care, P.C.

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

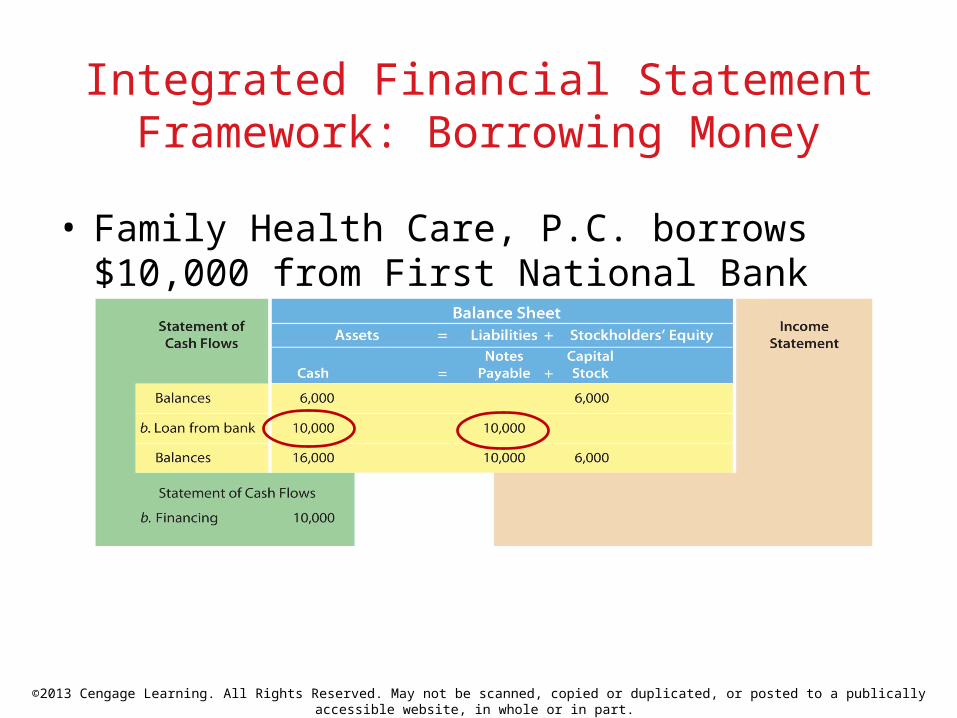

• Family Health Care, P.C. borrows $10,000 from First National Bank

Integrated Financial Statement Framework: Borrowing Money

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Integrated Financial Statement Framework: Buying Land

• Family Health Care buys land for $12,000 cash

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

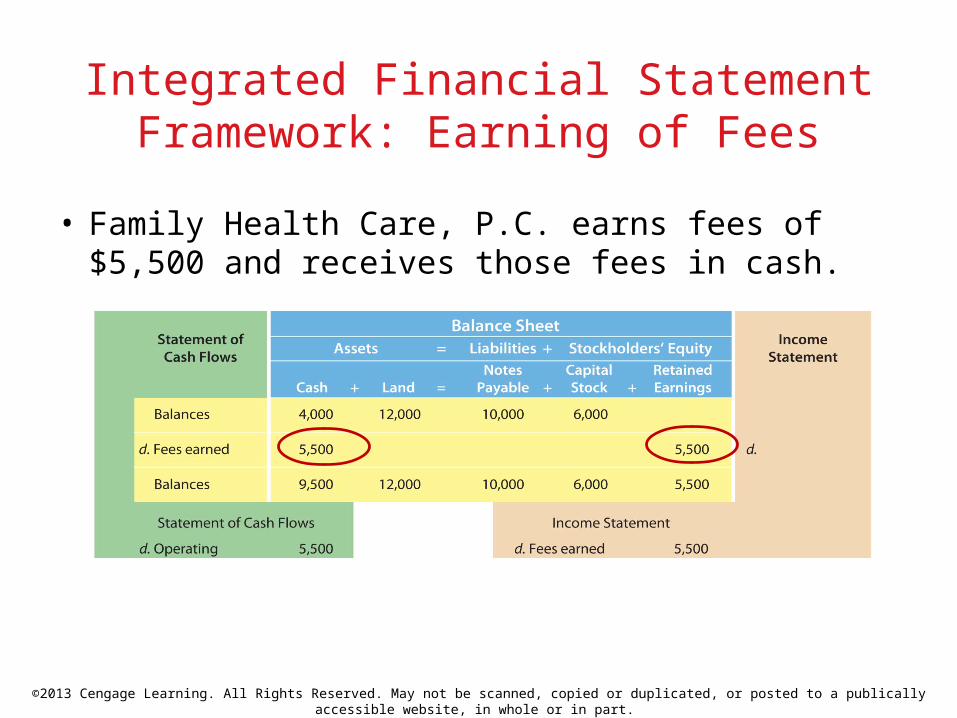

• Family Health Care, P.C. earns fees of $5,500 and receives those fees in cash.

Integrated Financial Statement Framework: Earning of Fees

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

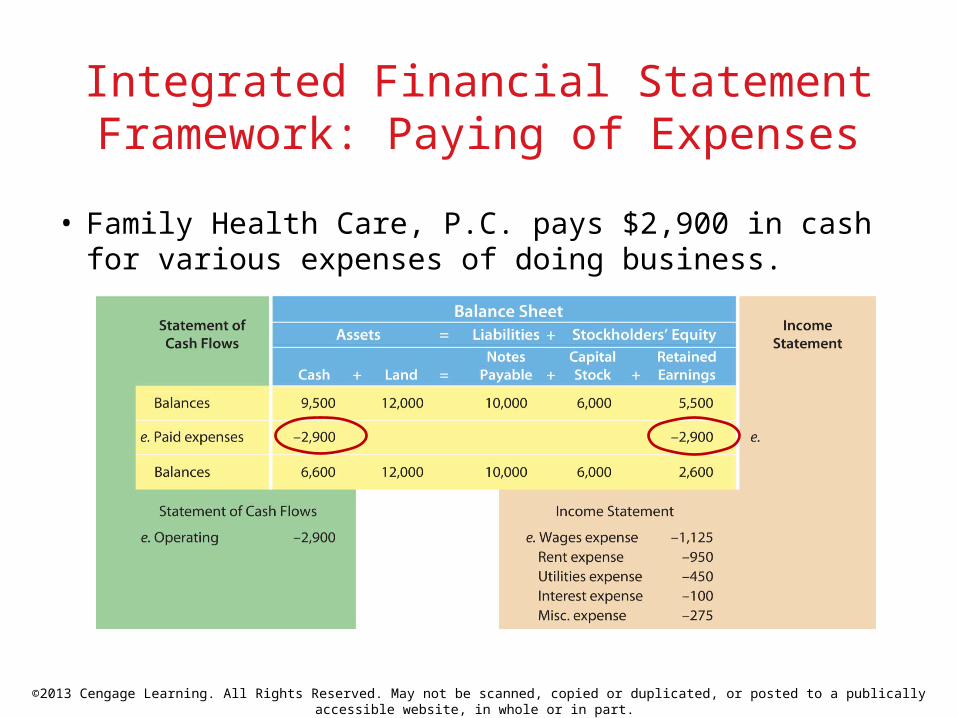

Integrated Financial Statement Framework: Paying of Expenses

• Family Health Care, P.C. pays $2,900 in cash for various expenses of doing business.

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Integrated Financial Statement Framework: Paying of Dividends

• Family Health Care, P.C. pays dividends of $1,500 to their only stockholder, Dr. Lee Landry.

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Integrated Financial Statements: Family Health Care, P.C.

Exhibit 2: Family Health Care Summary of Transactions for September

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

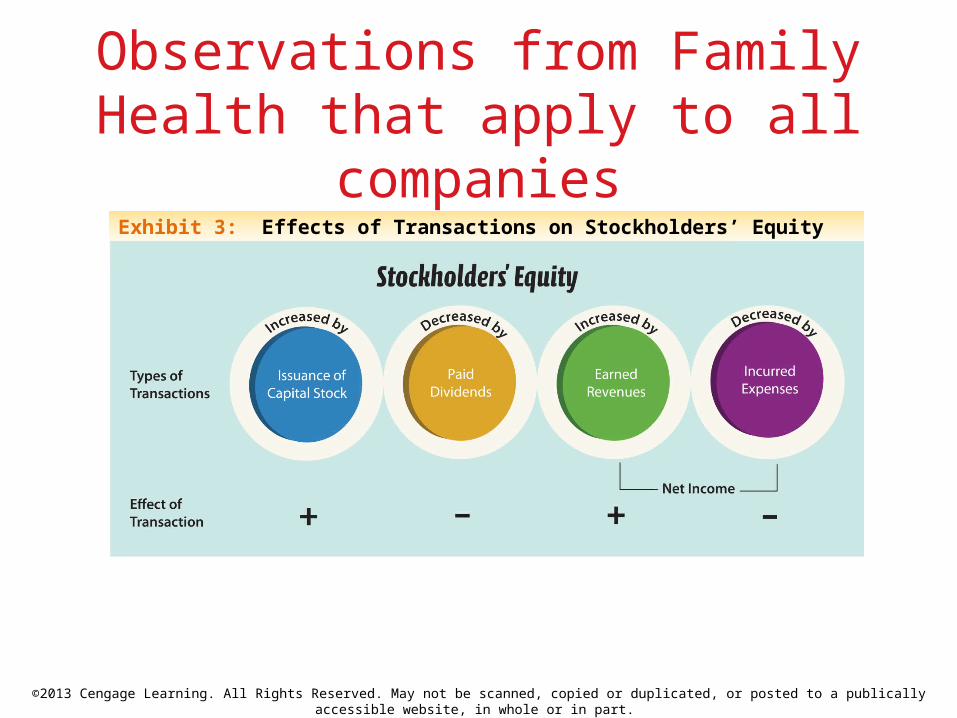

Observations from Family Health that apply to all companies

Exhibit 3: Effects of Transactions on Stockholders’ Equity

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Learning Objective 3

Prepare financial statements for a corporation’s first period of operations

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Preparation of Financial Statements

• This exhibit lists Family Health’s transactions in the order they occurred; it does not group and summarize the transactions in a meaningful manner.

Balance Sheetcomponents

Statement of Cash Flow

components

Income Statement

components

Exhibit 2: Family Health Care Summary of Transactions for September

![Basic Accounting Concepts _ GE Accounting[1]](https://static.fdocuments.in/doc/165x107/577cc8081a28aba711a203c2/basic-accounting-concepts-ge-accounting1.jpg)