BASF Roundtable Agricultural Solutions 2012

55

BASF Roundtable Agricultural Solutions, November 12, 2012 Verbund Synergies Agro Growth via Innovation Group Strategy 1 Agricultural Solutions Sustainable growth through market-driven innovations BASF Roundtable Agricultural Solutions November 12, 2012 London

-

Upload

basf -

Category

Investor Relations

-

view

1.836 -

download

0

Transcript of BASF Roundtable Agricultural Solutions 2012

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 1

Agricultural Solutions Sustainable growth through market-driven innovations

BASF Roundtable Agricultural Solutions November 12, 2012 London

BASF Roundtable Agricultural Solutions, November 12, 2012

2

Disclaimer

This presentation includes forward-looking statements that are subject to risks and uncertainties, including those pertaining to the anticipated benefits to be realized from the proposals described herein. This presentation contains a number of forward-looking statements including, in particular, statements about future events, future financial performance, plans, strategies, expectations, prospects, competitive environment, regulation and supply and demand. BASF has based these forward-looking statements on its views with respect to future events and financial performance. Actual financial performance of the entities described herein could differ materially from that projected in the forward-looking statements due to the inherent uncertainty of estimates, forecasts and projections, and financial performance may be better or worse than anticipated. Given these uncertainties, readers should not put undue reliance on any forward-looking statements.

Forward-looking statements represent estimates and assumptions only as of the date that they were made. The information contained in this presentation is subject to change without notice and BASF does not undertake any duty to update the forward-looking statements, and the estimates and assumptions associated with them, except to the extent required by applicable laws and regulations.

3

1 | Introduction Dr. Andreas Kreimeyer Member of the Board of Executive Directors 2 | BASF Crop Protection 3 | BASF Plant Biotechnology

4

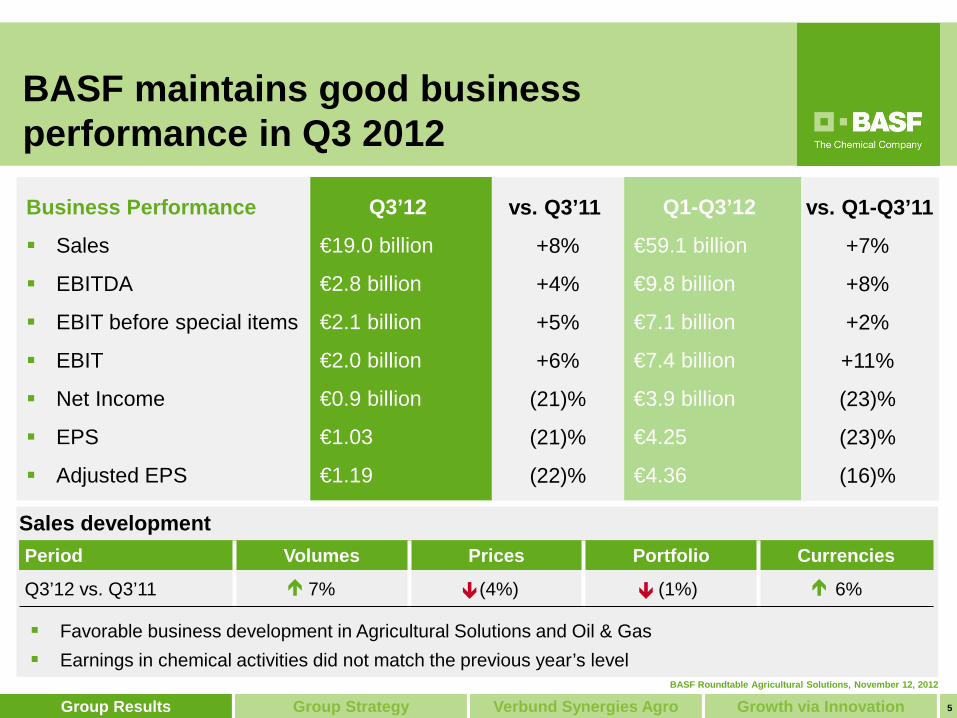

1 | BASF maintains good business performance in Q3 2012

2 | ‘We Create Chemistry’ strategy on track; Agricultural Solutions is a key contributor

3 | Agricultural Solutions offers attractive growth opportunities with strong commitment to innovation

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 5

Q1-Q3’12

€59.1 billion

€9.8 billion

€7.1 billion

€7.4 billion

€3.9 billion

€4.25

€4.36

vs. Q1-Q3’11

+7%

+8%

+2%

+11%

(23)%

(23)%

(16)%

Favorable business development in Agricultural Solutions and Oil & Gas Earnings in chemical activities did not match the previous year’s level

BASF maintains good business performance in Q3 2012

Q3’12

€19.0 billion

€2.8 billion

€2.1 billion

€2.0 billion

€0.9 billion

€1.03

€1.19

vs. Q3’11

+8%

+4%

+5%

+6%

(21)%

(21)%

(22)%

Business Performance

Sales

EBITDA

EBIT before special items

EBIT

Net Income

EPS

Adjusted EPS

Sales development Period Volumes Prices Portfolio Currencies

Q3’12 vs. Q3’11 7% (4%) (1%) 6%

Favorable business development in Agricultural Solutions and Oil & Gas Earnings in chemical activities did not match the previous year’s level

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 6

Ongoing portfolio optimization

BASF is strengthening competitiveness of Construction Chemicals in Europe

Measures include:

- Adjusting business to declining markets in Southern Europe and Great Britain

- Enhancing overall efficiency and customer focus

About 400 positions in Europe are affected

BASF to acquire Becker Underwood $1.02 billion (€785 million) purchase

price Strengthens global crop protection

business Leading global provider of

technologies for biological seed treatment

2012 (E) Sales $240 million (€185 million)

Merger control approvals pending

Acquisition of equity in 3 producing fields in Norway: Brage (32.7%), Gjøa (15%), Vega (30%)

2P reserves of ~100 million boe Rise in daily production in Norway

from 3,000 to 40,000 boepd Statoil to receive - 15% in development field Edvard

Grieg - $1.35 billion - up to additional $100 million

depending on success of Vega

Photo: Statoil

Becker Underwood Restructuring of Construction Chemicals

Asset swap with Statoil

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 7

Outlook 2012 confirmed

For the FY 2012, BASF aims to exceed the record levels of sales and EBIT before special items achieved in 2011

BASF will strive again to earn a high premium on cost of capital

Chemical activities - We do not expect demand to pick up in the fourth quarter 2012 - Therefore, 2012 EBIT before special items of chemical activities will come in below the level of the

previous year.

Outlook 2012

GDP: +2.2% (before: 2.3%)

Industrial production: +2.8% (before: 3.4%)

Chemical production: +2.9% (before: 3.5%)

US$/Euro: 1.30 (unchanged)

Oil price (US$/bbl): 110 (unchanged)

Assumptions 2012

8

1 | BASF maintains good business performance in Q3 2012

2 | ‘We Create Chemistry’ strategy on track; Agricultural Solutions is a key contributor

3 | Agricultural Solutions offers attractive growth opportunities with strong commitment to innovation

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 9

Chemistry as an enabler BASF has superior growth

opportunities: Innovation, sustainability, Emerging Markets, …

Long-term value creation, ambitious financial targets

The #1 chemical company. 2011: €73.5 billion sales, €8.4 billion EBIT bSI

#1- #3 in >75% of business, present in >200 countries

Production in 41 countries, 6 integrated Verbund sites

10 years of outperformance 16% average annual stock

performance* 15% average annual

dividend increase, >3% yield every single year**

Performance

BASF – The Chemical Company. We create chemistry for a sustainable future

Perspective

* Nov. 2002 - Oct. 2012 ** For 2002-2011

Ludwigshafen, Germany Antwerp, Belgium

Nanjing, China

Kuantan, Malaysia Geismar,

USA Freeport, USA

Verbund site

Positioning

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 10

‘We Create Chemistry’ strategy defines clear financial targets for 2015 and 2020

Grow at least 2 percentage points above chemical production

Earn a premium on cost of capital of at least €2.5 billion on average p.a.

Profitability targets Growth targets

2015

2020

Sales ~€85 billion

Sales ~€115 billion

EBITDA ~€15 billion EPS ~€7.50

Double EBITDA to ~€23 billion (compared with 2010)

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 11

Demographic challenges set the stage for the future of the chemical industry

Nine billion people in 2050 but only one earth

Resources, Environment & Climate

Food & Nutrition Quality of life

Chemistry as an enabler

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 12

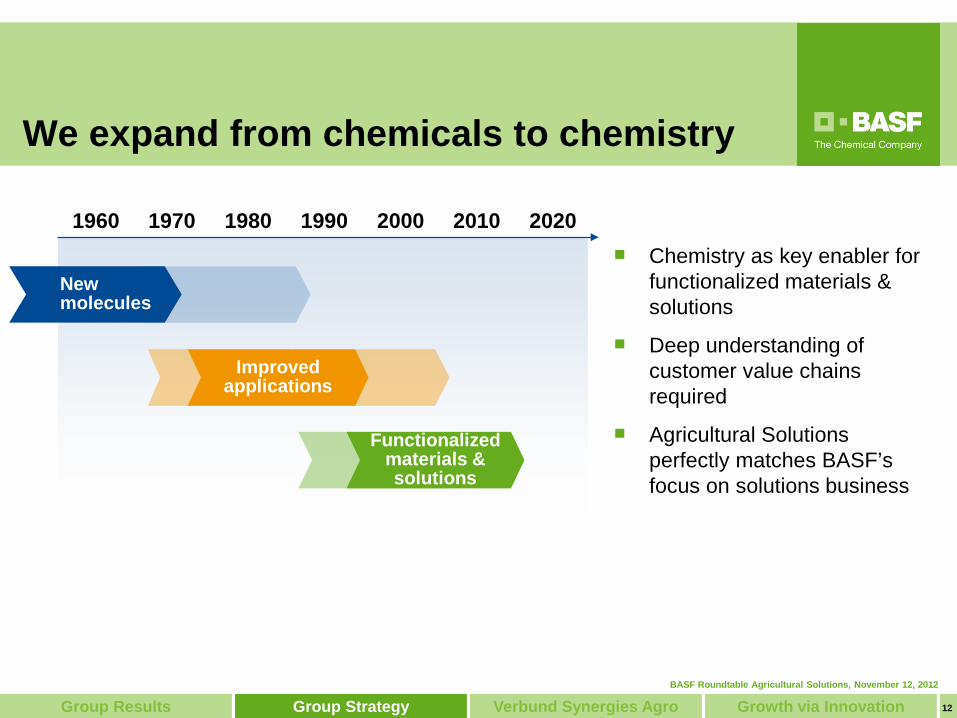

We expand from chemicals to chemistry

Chemistry as key enabler for functionalized materials & solutions

Deep understanding of customer value chains required

Agricultural Solutions perfectly matches BASF’s focus on solutions business

1960 1970 1980 1990 2000 2010 2020

New molecules

Improved applications

Functionalized materials & solutions

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 13

BASF Crop Protection’s offering goes beyond weed, disease and pest control

Commodity Prices

Sustai- nability

Risk management Exchange Rate

External factors

Frost Drought Water Nutrition Soil

Stress

Heat

Innovation beyond Crop Protection

Weeds Diseases

Natural foes

Pests

Crop Protection

Resources

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 14

BASF Plant Science – Trait Technology Partner

Growers

Concept and strengths BASF has focused on trait

technologies early on Cutting-edge technology

and trait portfolio attracts top partners (seeds, food)

Products to be marketed via our partners’ channels

Partnership business model provides high flexibility and keeps asset costs low

Trait Technology Partner

Plant Science

Trait & Seed Partners

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 15

Multiple synergies between Agricultural Solutions and BASF Verbund

Non-cyclical, adds earnings

resilience

Technological synergies through

Know-how Verbund

Agricultural Solutions

Strong contributor to BASF‘s profitable

growth

Backward- integration

and sourcing

synergies

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 16

EBIT before special items in billion €

0

0,2

0,4

0,6

0,8

1

2006 2007 2008 2009 2010 2011 2012Q1-Q3

Agricultural Solutions has increased its earnings contribution to BASF sustainably

EBIT bSI more than doubled from 2006 to 2011

New record in 2011: €810 million

FY 2011 record has been already significantly surpassed: Q1-Q3 2012: €1,004 million

Sustainably increased earnings

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 17

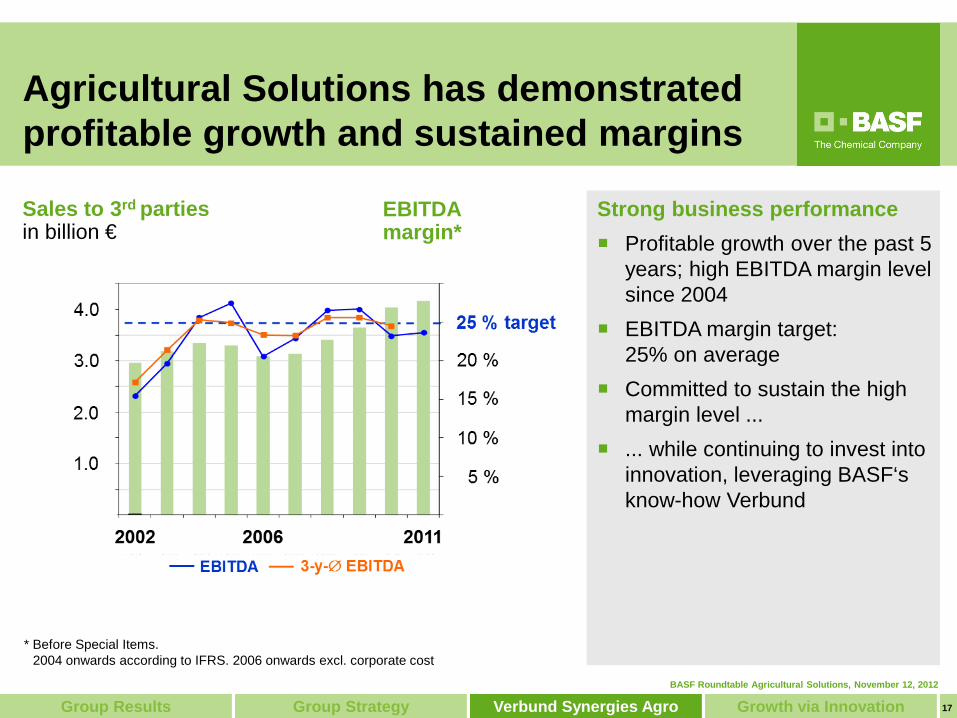

Strong business performance Profitable growth over the past 5

years; high EBITDA margin level since 2004

EBITDA margin target: 25% on average

Committed to sustain the high margin level ...

... while continuing to invest into innovation, leveraging BASF‘s know-how Verbund

* Before Special Items. 2004 onwards according to IFRS. 2006 onwards excl. corporate cost

Agricultural Solutions has demonstrated profitable growth and sustained margins

Sales to 3rd parties in billion €

EBITDA margin*

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 18

Oil & Gas Agricultural Solutions

Chemicals business

0

2

4

6

8

10

12

2002 2004 2006 2008 2010

Agricultural Solutions is adding to BASF Group’s earnings resilience

Agriculture not coupled to chemical cycle

Agricultural Solutions delivered substantial contribution even in 2009 trough

Agro adds to earnings resilience EBITDA by activity (excluding Other) in billion €

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 19

in million €

from 3rd parties 64%

Sourcing of Top-100 raw materials* (by value) in 2011

from Verbund 36%

Make or buy Verbund back-integration

– security & flexibility of supply – market-based transfer pricing – typically ~40% of the Top-100 raws come from Verbund

Sourcing synergies

– economy of scale via joint BASF procurement

Capex

– capex will increase to >€250 M/y in 2012-2016 (on average)

– insourcing of advanced intermediates

– capacity expansions

€515 million

Our growth in Crop Protection is backed by a high level of backward integration

Capex in million €/a

0 100 200

2012-2016

2007-2011

* Without a.i. tolling, formulants, packaging

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 20

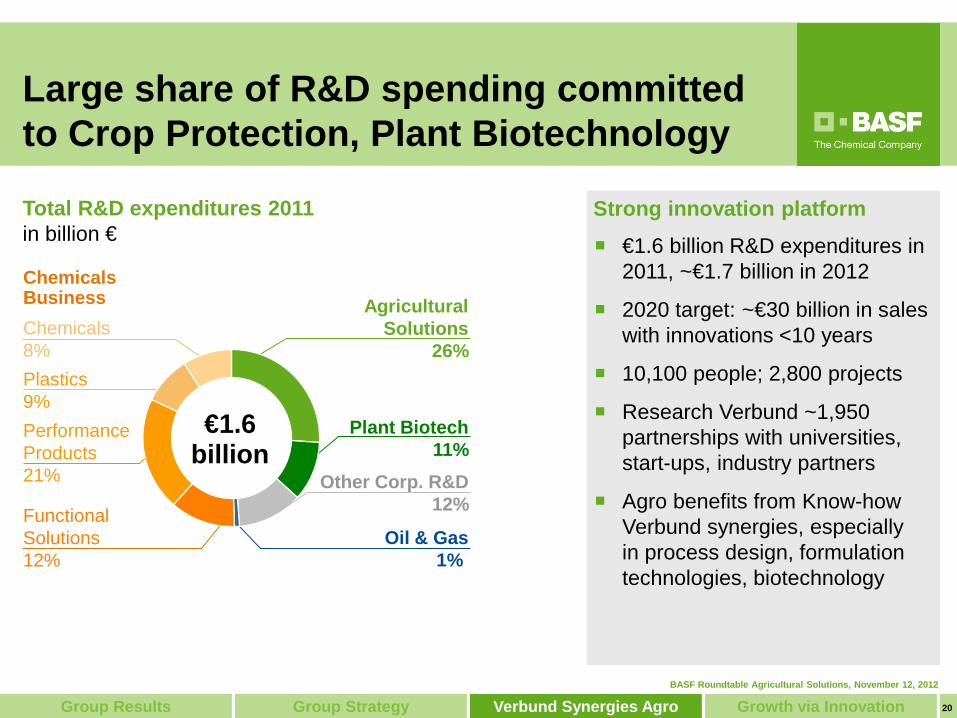

Total R&D expenditures 2011 in billion €

Large share of R&D spending committed to Crop Protection, Plant Biotechnology

€1.6 billion R&D expenditures in 2011, ~€1.7 billion in 2012

2020 target: ~€30 billion in sales with innovations <10 years

10,100 people; 2,800 projects

Research Verbund ~1,950 partnerships with universities, start-ups, industry partners

Agro benefits from Know-how Verbund synergies, especially in process design, formulation technologies, biotechnology

Functional Solutions 12%

Other Corp. R&D 12%

Chemicals 8%

Agricultural Solutions

26% Plastics

9% Performance Products 21%

Oil & Gas 1%

Chemicals Business

Plant Biotech 11%

€1.6 billion

Strong innovation platform

21

1 | BASF maintains good business performance in Q3 2012

2 | ‘We Create Chemistry’ strategy on track; Agricultural Solutions is a key contributor

3 | Agricultural Solutions offers attractive growth opportunities with strong commitment to innovation

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 22

To stimulate further growth in Agriculture, we pursue two promising Growth Fields

Resources, Environment & Climate Food & Nutrition Quality of Life

* Including growth fields still under evaluation

Consumer Goods

Chemistry as Enabler

Transportation Health & Nutrition Construction Electronics Agriculture C

usto

mer

In

dust

ries

Energy Management

Water Solutions

Wind Energy

Rare Earth Metals Recycl.

Heat Management Enzymes Plant

Biotechnology Batteries for

Mobility Lightweight Composites

Heat Management

Functional Crop Care

Medical Organic Electronics

Gro

wth

Fi

elds

*

Energy & Resources

Growth fields at different stages, >€500 million sales each expected at maturity

BASF Roundtable Agricultural Solutions, November 12, 2012

Verbund Synergies Agro Growth via Innovation Group Results Group Strategy 23

BASF Plant Science founded (1998)

Acquisition of CropDesign (2006)

Foundation of Metanomics (1998)

2010 1995 2000

BASF Plant Science founded in 1998 as a subsidiary of BASF

Strong trait technology platform was created, highly attractive to partners

Prime example: Yield & Stress collaboration with Monsanto ranks #1 in Patent Asset Index

A strong trait technology platform Patent Asset Index for Yield & Stress Traits

BASF Plant Sciences has generated a leading technology platform

0 200 400 600 800 1000 1200

DuPont

Mendel

Bayer

Ceres

BASF/ Monsanto

2010

2009

2011

Partnership with

Partnership with

Partnership with

24

Important contributions to BASF Group – profitable growth – stable earnings

Integrated in BASF Verbund – cost synergies – know-how synergies

Important role in reaching goals of our We Create Chemistry strategy – customer focused solutions offer – innovative & sustainable solutions

Agricultural Solutions is a star in our portfolio

BASF Roundtable Agricultural Solutions, November 12, 2012

1 | Introduction 2 | BASF Crop Protection Markus Heldt President, Crop Protection Division 3 | BASF Plant Biotechnology

BASF Roundtable Agricultural Solutions, November 12, 2012

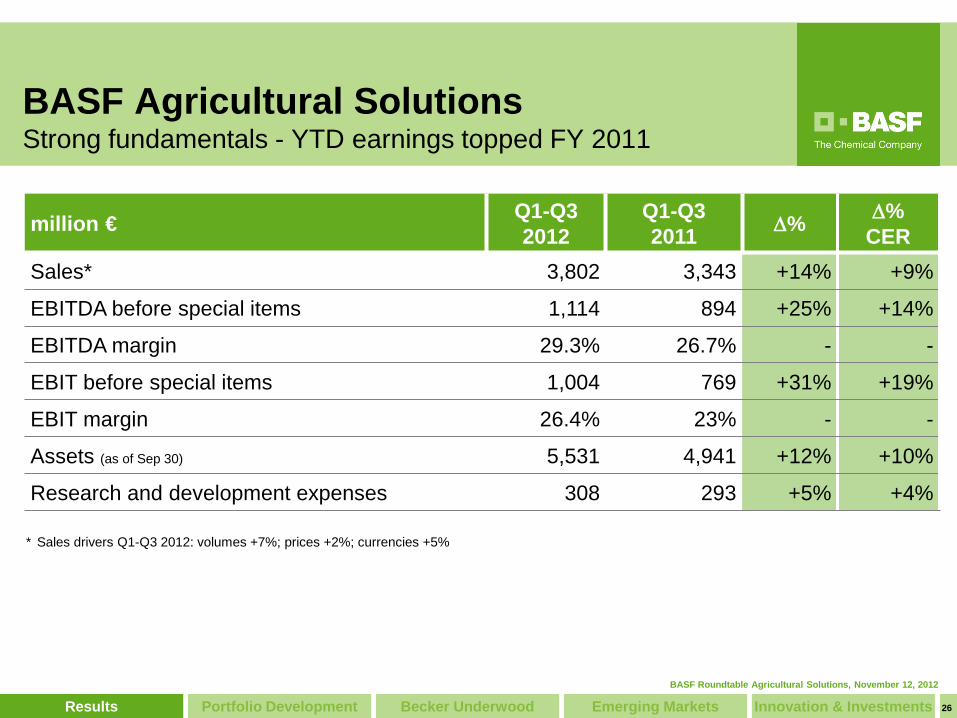

Portfolio Development Results Becker Underwood Emerging Markets Innovation & Investments 26

million € Q1-Q3 2012

Q1-Q3 2011 ∆% ∆%

CER Sales* 3,802 3,343 +14% +9%

EBITDA before special items 1,114 894 +25% +14%

EBITDA margin 29.3% 26.7% - -

EBIT before special items 1,004 769 +31% +19%

EBIT margin 26.4% 23% - -

Assets (as of Sep 30) 5,531 4,941 +12% +10%

Research and development expenses 308 293 +5% +4%

* Sales drivers Q1-Q3 2012: volumes +7%; prices +2%; currencies +5%

BASF Agricultural Solutions Strong fundamentals - YTD earnings topped FY 2011

BASF Roundtable Agricultural Solutions, November 12, 2012

Portfolio Development Results Becker Underwood Emerging Markets Innovation & Investments 27

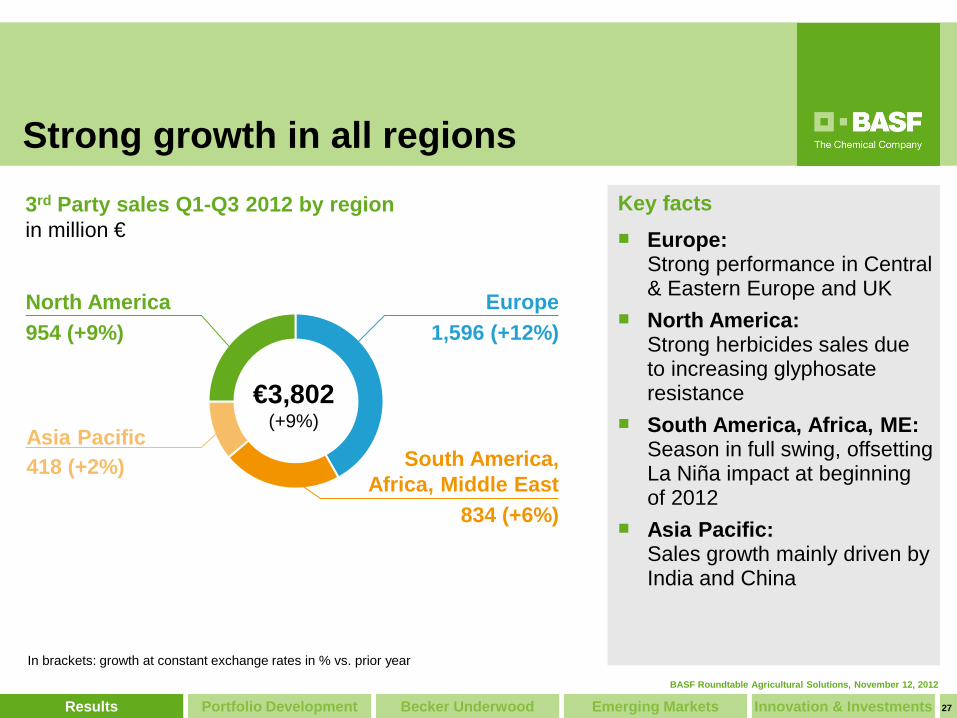

Strong growth in all regions

3rd Party sales Q1-Q3 2012 by region in million €

Key facts Europe:

Strong performance in Central & Eastern Europe and UK

North America: Strong herbicides sales due to increasing glyphosate resistance

South America, Africa, ME: Season in full swing, offsetting La Niña impact at beginning of 2012

Asia Pacific: Sales growth mainly driven by India and China

Asia Pacific 418 (+2%)

Europe 1,596 (+12%)

South America, Africa, Middle East

834 (+6%)

North America 954 (+9%)

€3,802 (+9%)

In brackets: growth at constant exchange rates in % vs. prior year

BASF Roundtable Agricultural Solutions, November 12, 2012

Portfolio Development Results Becker Underwood Emerging Markets Innovation & Investments 28

Fungicides: Strong volume growth driven by Xemium® sales in Europe, and strong Plant Health adoption in North America

Herbicides: Main drivers were Clearfield® in Europe, Kixor® in North America, IMIs in Asia.

Insecticides: Strong demand increase for Fipronil especially in Brazil (sugarcane)

Fungicides 1,624 (+6%)

Herbicides 1,395 (+13%)

Insecticides/Other 783 (+7%)

Key facts

€3,802 (+9%)

Strong growth in all indications 3rd Party sales Q1-Q3 2012 by indication in million €

In brackets: growth at constant exchange rates in % vs. prior year

BASF Roundtable Agricultural Solutions, November 12, 2012

Portfolio Development Results Becker Underwood Emerging Markets Innovation & Investments 29

Crop Protection growth story continues, €6 billion sales targeted for mid of decade

Financial Targets

€6 billion sales target expected to be reached at mid of decade due to:

– strong momentum and additional value extraction from our existing portfolio

– new product launches

– emerging market business models gaining further grip

EBITDA margin target: 25% on average

Emerging Markets* * Latin America, Eastern Europe, South Africa, Asia (w/o Japan, Australia, New Zealand) ** FCC = Functional Crop Care

Sales drivers in million €

2012E 2011

Fungicide & AgCelence

growth

Herbicide Renaissance& Innovations

FCC** & Becker

Underwood

Growth in emerging markets

New product

launches

~ 4,700 4,165

~ 6,000

~ 50%

46% 44%

2015E

BASF Roundtable Agricultural Solutions, November 12, 2012

Portfolio Development Results Becker Underwood Emerging Markets Innovation & Investments 30

Global expansion of AgCelence®

leverages our Plant Health portfolio AgCelence®

Umbrella brand for Plant Health solutions, global rollout in full swing

Plant Health effect: Improved stress tolerance, growth, crop quality

F 500® fungicide continues to be a key contributor to Plant Health business

3rd capacity expansion for F500® announced in September 2012

0

200

400

600

800

2008 2011 2015E

Asia Europe/EMA

Latin America North America

sales to third parties Sales in million €

BASF Roundtable Agricultural Solutions, November 12, 2012

Portfolio Development Results Becker Underwood Emerging Markets Innovation & Investments 31

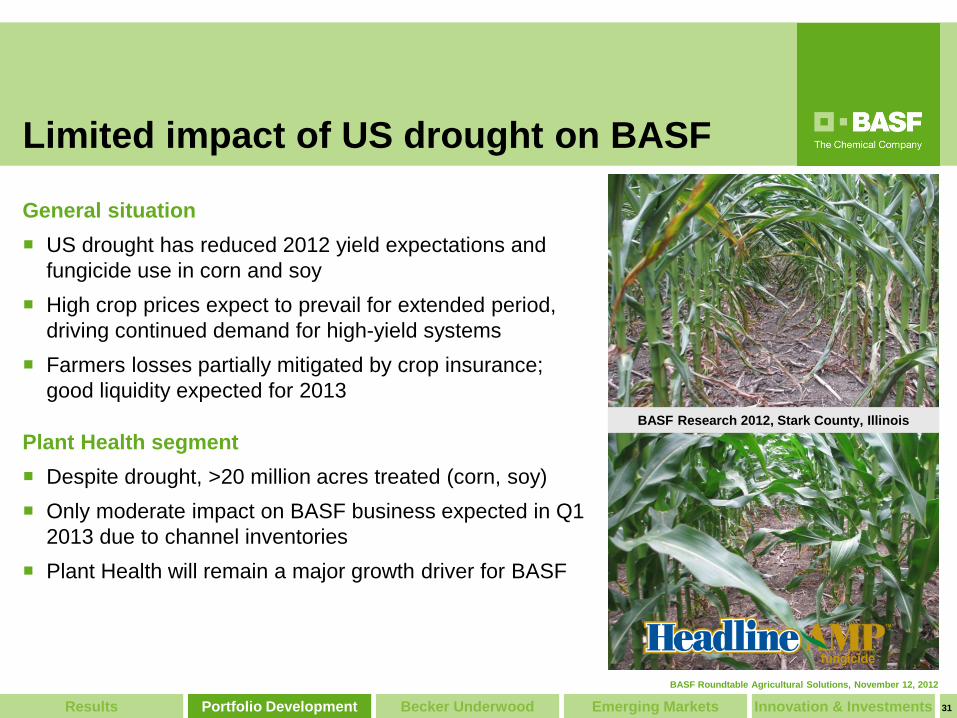

Limited impact of US drought on BASF

General situation US drought has reduced 2012 yield expectations and

fungicide use in corn and soy High crop prices expect to prevail for extended period,

driving continued demand for high-yield systems Farmers losses partially mitigated by crop insurance;

good liquidity expected for 2013

Plant Health segment Despite drought, >20 million acres treated (corn, soy) Only moderate impact on BASF business expected in Q1

2013 due to channel inventories Plant Health will remain a major growth driver for BASF

June 5th

July 2nd

June 16th

BASF Research 2012, Stark County, Illinois

BASF Roundtable Agricultural Solutions, November 12, 2012

Portfolio Development Results Becker Underwood Emerging Markets Innovation & Investments 32

Next upcoming registrations Xemium registered

New fungicide for all market segments

Strengthens BASF’s global leadership position

Successful launch Global registration proceeds in

record time. Target: >100 crops, >50 countries

Outstanding Q1-Q3 sales Initial peak sales potential:

>€200 million

Very successful Xemium® launch confirms blockbuster potential

Xemium®

BASF Roundtable Agricultural Solutions, November 12, 2012

Portfolio Development Results Becker Underwood Emerging Markets Innovation & Investments 33

Continued growth in herbicides; sales target of >€1.75 billion for 2015

Urgent need for innovation Rethinking of weed control Multiple modes of action

needed

BASF’s multi-level approach Strong herbicide pipeline Successful expansion of Kixor® Herbicide-tolerant production

systems: – Clearfield® in global launch – Cultivance® and Engenia®

(Dicamba) in approval Roundup Ready® (RR) launched by Monsanto in 1996

Increasing weed resistance to Glyphosate

Accelerating market penetration of RR system in the Americas

Engenia®

BASF launches

2010 1990 2000

Herbicide Renaissance

BASF Roundtable Agricultural Solutions, November 12, 2012

Portfolio Development Results Becker Underwood Emerging Markets Innovation & Investments 34

Acquisition of Becker Underwood supports Agricultural solutions strategy

Strategy Strengthens our traits & seed

partnerships via expanded seed treatment offering

Gives access to growth market of biological Crop Protection

Complements offering in strategic crops and countries, i.e. Americas

Opens door to combined solutions of chemical and biological crop protection

Strengthens know-how and technology platform

Becker Underwood adds value

Innovation beyond crop protection

Traits & seed partnerships

Crop protection

Agricultural Solutions

BASF Roundtable Agricultural Solutions, November 12, 2012

Portfolio Development Results Becker Underwood Emerging Markets Innovation & Investments 35

Closing of transaction expected by year end 2012

Becker Underwood will be part of Functional Crop Care, support all three pillars

Structural integration to be completed by end of 2013

Timelines

Becker Underwood further strengthens BASF’s position as solution provider

Global Business Unit Functional Crop Care (FCC)

Seed Solutions Innovations beyond Crop

Protection Biologicals

* To be part of Health & Nutrition ** Fiscal year ended September 30, 2012

Foliar Plant Health

Seed Enhancement Landscape Horticulture &

Specialty

Becker Underwood (Sales 2012E**: €185 million)

Livestock Nutrition*

BASF Roundtable Agricultural Solutions, November 12, 2012

Portfolio Development Results Becker Underwood Emerging Markets Innovation & Investments 36

Latin America: Additional resources established, new financial tools introduced

Eastern Europe: Headcount to double from 2008 - 2013

Asia: Additional investments in assets, resources planned

Africa: Crop Protection is a main driver for BASF Group’s growth in Africa

We will grow Emerging Markets sales significantly

0

100

200

300

2007 2011 2015E

Latin America

0

100

200

300

2007 2011 2015E

Eastern Europe

0

100

200

300

400

500

600

2007 2011 2015E

Asia

0

100

200

300

400

500

600

2007 2011 2015E

Africa

Emerging Market sales indexed

% %

%

>€ 3 bn. in 2015

Key drivers

BASF Roundtable Agricultural Solutions, November 12, 2012

Portfolio Development Results Becker Underwood Emerging Markets Innovation & Investments 37

We are committed to keep investing into innovation

Core of our business model: Innovative solution provider

High R&D intensity in Crop Protection (~9% of sales)

Increased R&D investments: – 2007 - 2011: € 1.8 billion – 2012 - 2016: ~€ 2.5 billion

321 329

358

390 410

2007 2008 2009 2010 2011 2012

Total R&D expenditures in million €

Commitment to innovation

BASF Roundtable Agricultural Solutions, November 12, 2012

Portfolio Development Results Becker Underwood Emerging Markets Innovation & Investments 38

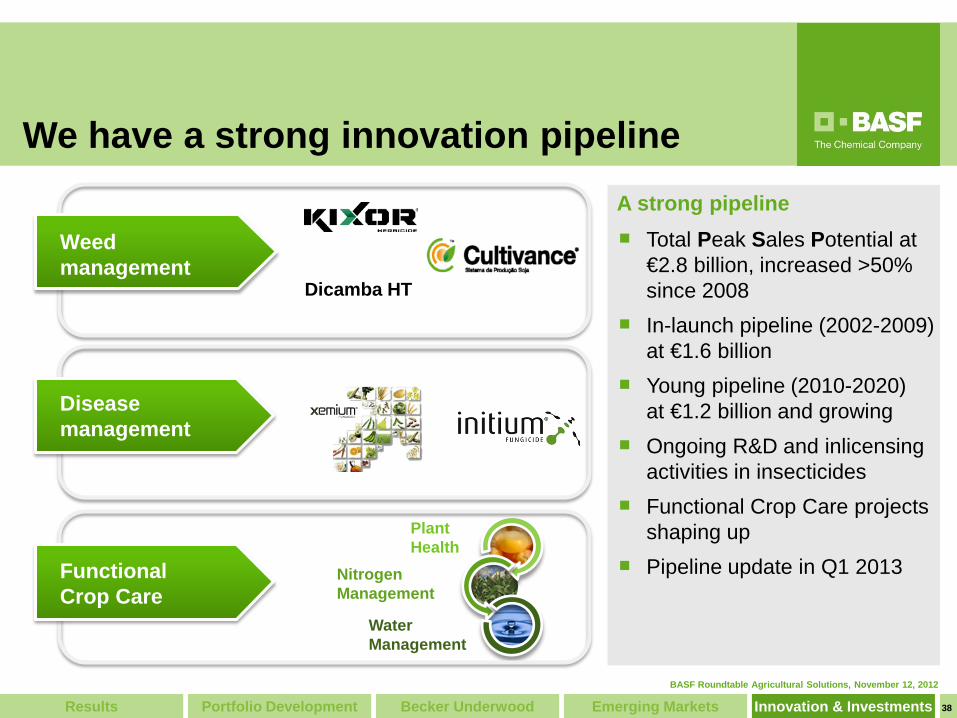

Dicamba HT

We have a strong innovation pipeline

Plant Health

Nitrogen Management

Water Management

A strong pipeline

Weed management

Total Peak Sales Potential at €2.8 billion, increased >50% since 2008

In-launch pipeline (2002-2009) at €1.6 billion

Young pipeline (2010-2020) at €1.2 billion and growing

Ongoing R&D and inlicensing activities in insecticides

Functional Crop Care projects shaping up

Pipeline update in Q1 2013

Functional Crop Care

Disease management

BASF Roundtable Agricultural Solutions, November 12, 2012

Portfolio Development Results Becker Underwood Emerging Markets Innovation & Investments 39

Capex to be further increased, following our strategy Capex 2007-2011 in billion €

€0.8 billion

Various*

Capex 2007-2011 F500®: capacity expansion Kixor® and Xemium®: new

production plants Formulation: New plants and

expansions

Planned capex 2012-2016 F500®: 3rd capacity expansion Xemium®: backward integration Dicamba: capacity expansion New formulation plants (Asia) R&D expansion (India, USA)

Key Projects (F500, Kixor, Xemium)

>€1.4 billion

Various* Key Projects (F500, Xemium, Dicamba)

* Formulation sites, research sites, infrastructure

Planned capex 2012-2016 in billion €

BASF Roundtable Agricultural Solutions, November 12, 2012

40

Summary and outlook

Positive market fundamentals expected to persist (high crop prices, accelerated technology adaption in emerging markets)

BASF is strongly positioned as solution provider

Continued profitable growth, based upon high demand for innovative solutions and strong pipeline

New sales and earnings records forecasted for 2012

Expected sales of ~€6 billion in 2015

BASF Roundtable Agricultural Solutions, November 12, 2012

41

1 | Introduction 2 | BASF Crop Protection 3 | BASF Plant Biotechnology Dr. Peter Eckes President, BASF Plant Science

BASF Roundtable Agricultural Solutions, November 12, 2012

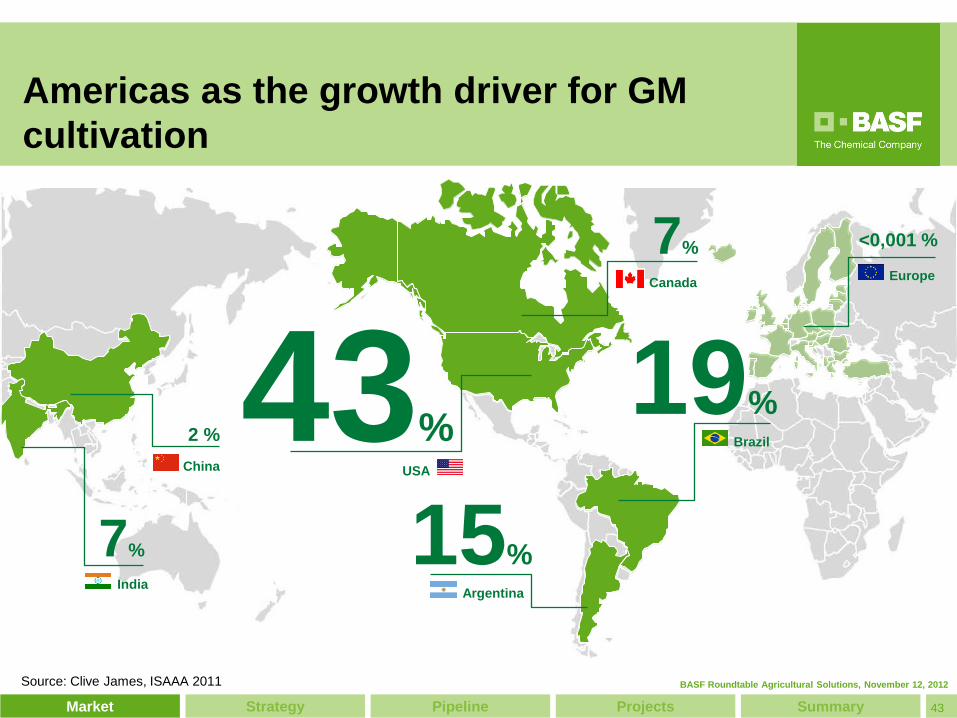

Key facts

Global GM crop area continued to grow in 2011 (8% from 2010)

Biotech crops are planted on about 11% of the cultivated land

In 2011, 16.7 million farmers grew GM crops in 29 countries

Market expected to grow to €32 billion by 2020**

Global GM crop area in million hectares; 1 ha = 2.47 acres

* CAGR 1997-2011 ** Source: Context Outlook 2010, BASF estimates;

incl. license value; major crops only; net farm value Source: ISAAA 2011

0

20

40

60

80

100

120

140

2003 1997 2006 2011 2000

160 160

Pipeline Projects Market Strategy 42 Summary

The GM success story continues

BASF Roundtable Agricultural Solutions, November 12, 2012

7%

Canada

Source: Clive James, ISAAA 2011

43% USA

19% Brazil

15% Argentina India

7%

China

2 %

<0,001 %

Europe

Americas as the growth driver for GM cultivation

Pipeline Projects Market Strategy 43 Summary

BASF Roundtable Agricultural Solutions, November 12, 2012

Situation

7%

Canada

43%

USA

<0,001 %

Europe

BASF Plant Science refocuses on strategic markets

Decision in January 2012

Active portfolio & site management

Strengthen position in North America; expand the new HQ in Research Triangle Park (NC)

Stop projects with EU market focus

Refocus activities on main markets in North and South America

Consolidate global site footprint

Trait Technology Partner Strategy remains unchanged

Pipeline Projects Market Strategy 44 Summary

BASF Roundtable Agricultural Solutions, November 12, 2012

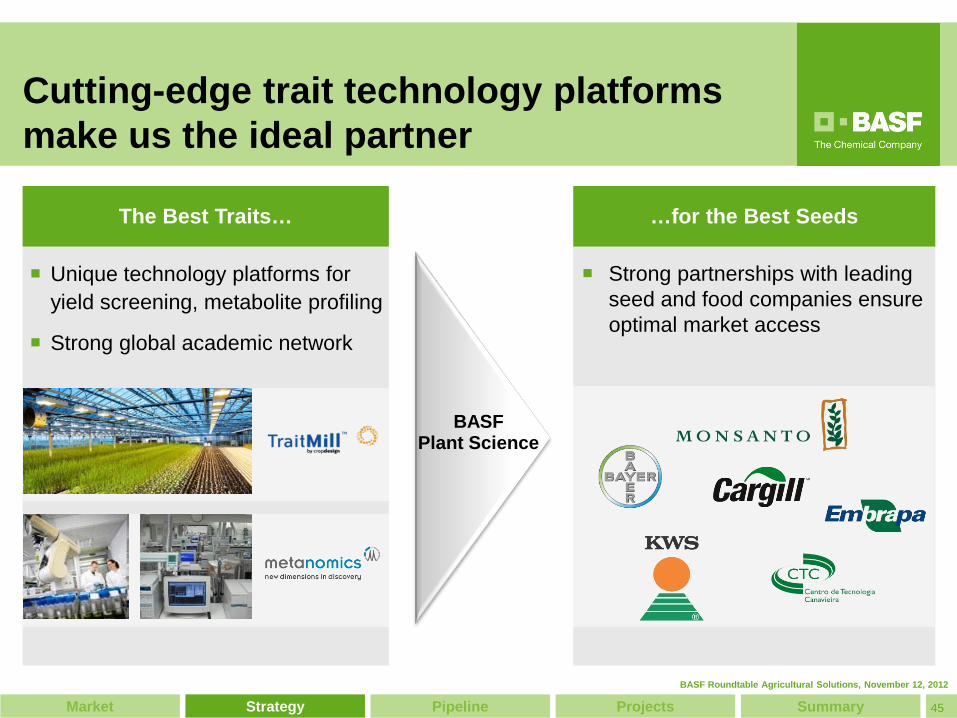

The Best Traits…

Unique technology platforms for yield screening, metabolite profiling

Strong global academic network

…for the Best Seeds

Strong partnerships with leading

seed and food companies ensure optimal market access

z

z

BASF Plant Science

Cutting-edge trait technology platforms make us the ideal partner

Pipeline Projects Market Strategy 45 Summary

BASF Roundtable Agricultural Solutions, November 12, 2012

Cutting-edge trait technology platforms fuel strong pipeline

Pipeline Projects Market Strategy 46 Summary

Business potential*

Discovery gene identification & proof of concept

Stage I proof of concept in target crops

Stage II early product development

Stage III advanced product

development

Stage IV pre-launch

Trait total development time: 10-12 years

Higher-yielding corn

Higher-yielding canola

Higher-yielding sugar cane2

Drought-tolerant cotton

Higher-yielding sugar beet3

Higher-yielding rice4

Improved nitrogen utilization in corn

Higher-yielding wheat

Yield & Stress with Monsanto1

Higher-yielding soybean 2nd Generation

Drought-tolerant corn 2nd Generation

Improved corn feed Feed Specialities Healthy fatty acids in canola5

Input Traits

Nematode resistant soybean1

Herbicide-tolerant soybean6

Fungal resistant soybean

Yield & Stress with others

Target gross trait sales before partner share in 2020***: €1.8 bn

1st Gen.

1st Gen. 250-500 M $

<250 M $

250-500 M $

<250 M $ tbd**

tbd**

tbd** <250 M $

tbd**

250-500 M $ tbd**

<250 M $

tbd**

>500 M $

250-500 M $

1 as communicated at Monsanto pipeline update in January 2012, 2 with CTC, 3 with KWS , 4 with Bayer, 5 with Cargill, 6 with Embrapa

* peak gross trait sales of last family member in country of 1st launch before partner share ** to be defined when product enters Phase II *** adjusted due to discontinuation of potato projects

BASF Roundtable Agricultural Solutions, November 12, 2012

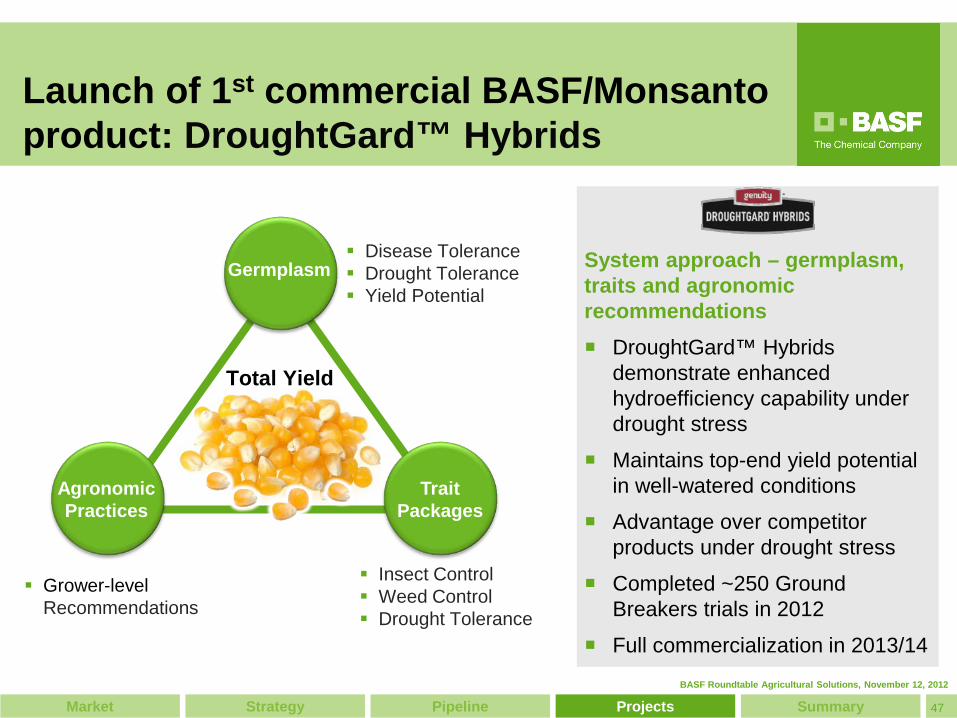

System approach – germplasm, traits and agronomic recommendations DroughtGard™ Hybrids

demonstrate enhanced hydroefficiency capability under drought stress

Maintains top-end yield potential in well-watered conditions

Advantage over competitor products under drought stress

Completed ~250 Ground Breakers trials in 2012

Full commercialization in 2013/14

Insect Control Weed Control Drought Tolerance

Grower-level Recommendations

Disease Tolerance Drought Tolerance Yield Potential

Total Yield

Germplasm

Agronomic Practices

Trait Packages

Launch of 1st commercial BASF/Monsanto product: DroughtGard™ Hybrids

Pipeline Projects Market Strategy 47 Summary

BASF Roundtable Agricultural Solutions, November 12, 2012

TX

NM OK

LA

AR

MO

IA

MN ND

SD

NE

KS CO

WY

TX

NM OK

LA

AR

MO

IA

MN ND

SD

NE

KS CO

WY

Monsanto’s Ground Breakers On-farm trial program designed to: Provide select farmers early

exposure to the latest products and agronomic systems

Support a better understanding of where, how and in which system a product will perform best

Help support commercial decisions DroughtGard™ Hybrid System ~250 Ground Breakers farmers on

thousands of acres Stewardship guidelines followed

throughout the unfolding of the regulatory approvals

Targeted for the Western Corn Belt

The DroughtGard™ Hybrid – the first and only drought management system

Pipeline Projects Market Strategy 48 Summary

BASF Roundtable Agricultural Solutions, November 12, 2012

DroughtGard Hybrids™

Drought-tolerant competitor product

The DroughtGard™ Hybrid System outperforms the competition

Pipeline Projects Market Strategy 49 Summary

BASF Roundtable Agricultural Solutions, November 12, 2012

Higher yielding rice: Biotech solutions tap an attractive and expanding market

Megatrend population increase Currently rice provides ~20% of

human caloric intake globally* Current yield increase ~0.8% p.a.

vs. future need of 1.2-1.5%* Partner strategy Market access via non-exclusive

license agreements First partnership signed with

Bayer CropScience (#1 in global hybrid rice market)

Attractive market Yield increase offers an attractive

value potential for combination of hybrid- & biotechnology

Key markets: Asia and Americas * Rice Almanac, 3rd ed., IRRI, 2002; A.J. Garris, et al., Genetics 169, 2005, 1631

Pipeline Projects Market Strategy 50 Summary

BASF Roundtable Agricultural Solutions, November 12, 2012

Transgene Reference

Seed weight (indexed)

indica

Development Discovery

japonica

Validation

indica

Higher yielding rice: First results show strength of yield trait system

0

2

4

6

TraitMill™ Indica Screen Field Trail

Pipeline Projects Market Strategy 51 Summary

BASF Roundtable Agricultural Solutions, November 12, 2012

Where do our resistance genes come from? The idea of Non-Host Resistance Soybeans, our host species, are

highly susceptible to Asian Soybean Rust (ASR)

There are plants with a natural immunity against ASR, like peanuts, chickpeas, certain clover and trefoil, etc.

Non-Host Resistance relies on taking these resistance genes and introducing them into soybean

Learning from nature enables an innovative biotech approach

Birdsfoot trefoil

Peanut

Fungal-resistant soybeans: Innovation inspired by nature

Chickpea

Low hop clover

Pipeline Projects Market Strategy 52 Summary

BASF Roundtable Agricultural Solutions, November 12, 2012

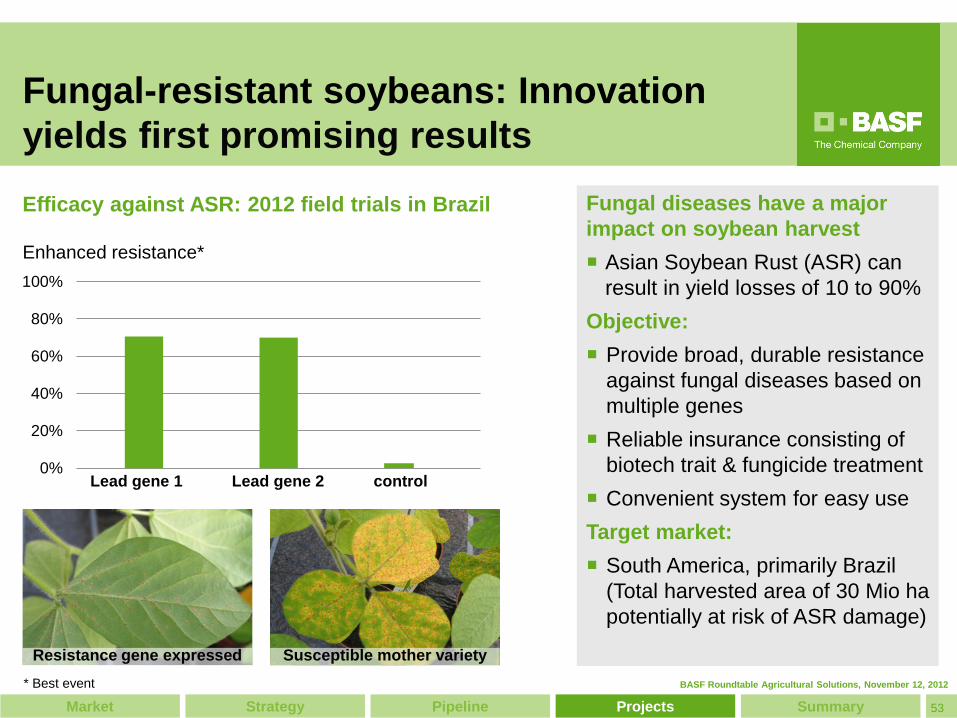

0%

20%

40%

60%

80%

100%

Enhanced resistance*

Lead gene 1 Lead gene 2 control

* Best event

Fungal-resistant soybeans: Innovation yields first promising results

Fungal diseases have a major impact on soybean harvest Asian Soybean Rust (ASR) can

result in yield losses of 10 to 90% Objective: Provide broad, durable resistance

against fungal diseases based on multiple genes

Reliable insurance consisting of biotech trait & fungicide treatment

Convenient system for easy use Target market: South America, primarily Brazil

(Total harvested area of 30 Mio ha potentially at risk of ASR damage)

Efficacy against ASR: 2012 field trials in Brazil

Resistance gene expressed Susceptible mother variety

Pipeline Projects Market Strategy 53 Summary

BASF Roundtable Agricultural Solutions, November 12, 2012

54

Refocused on key markets in Americas and Asia

Concentrate on highly attractive yield traits

Discovery platforms enable innovative gene discovery

Strong pipeline with target gross trait sales before partner share of €1.8 bn

BASF Plant Science slated to become an operating division of BASF within this decade

Summary and outlook

BASF Roundtable Agricultural Solutions, November 12, 2012