Basel Norms i, II and III

30

BASEL NORMS I, II and III

-

Upload

yashwanth-prasad -

Category

Documents

-

view

71 -

download

2

description

basel

Transcript of Basel Norms i, II and III

BASEL NORMS I, II and III

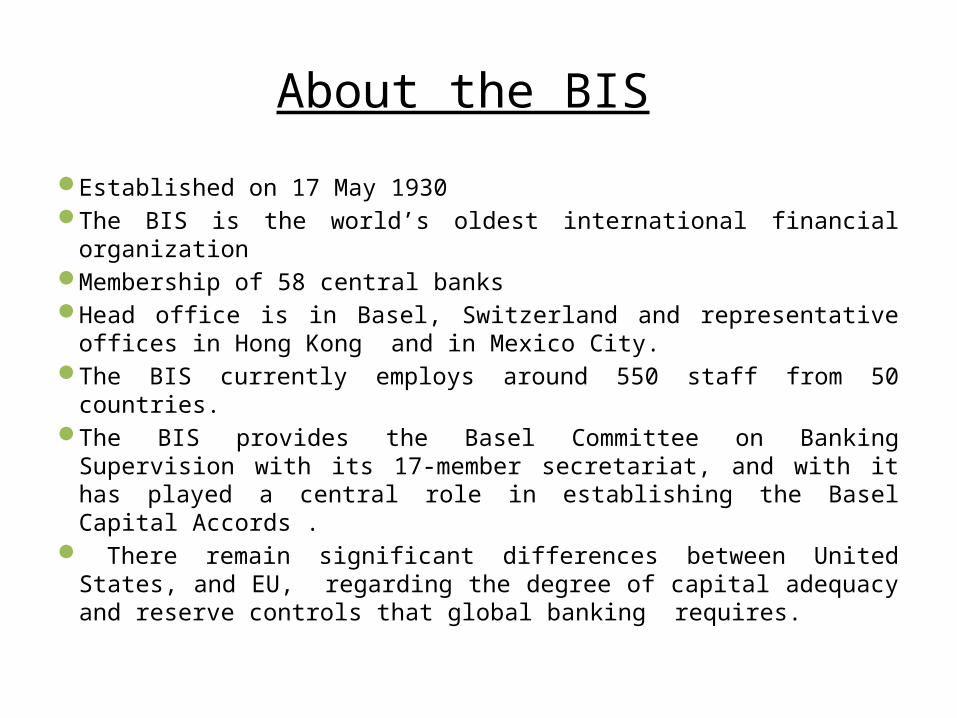

About the BIS

Established on 17 May 1930The BIS is the world’s oldest international financial organizationMembership of 58 central banksHead office is in Basel, Switzerland and representative offices in

Hong Kong and in Mexico City.The BIS currently employs around 550 staff from 50 countries.The BIS provides the Basel Committee on Banking Supervision with

its 17-member secretariat, and with it has played a central role in establishing the Basel Capital Accords .

There remain significant differences between United States, and EU, regarding the degree of capital adequacy and reserve controls that global banking requires.

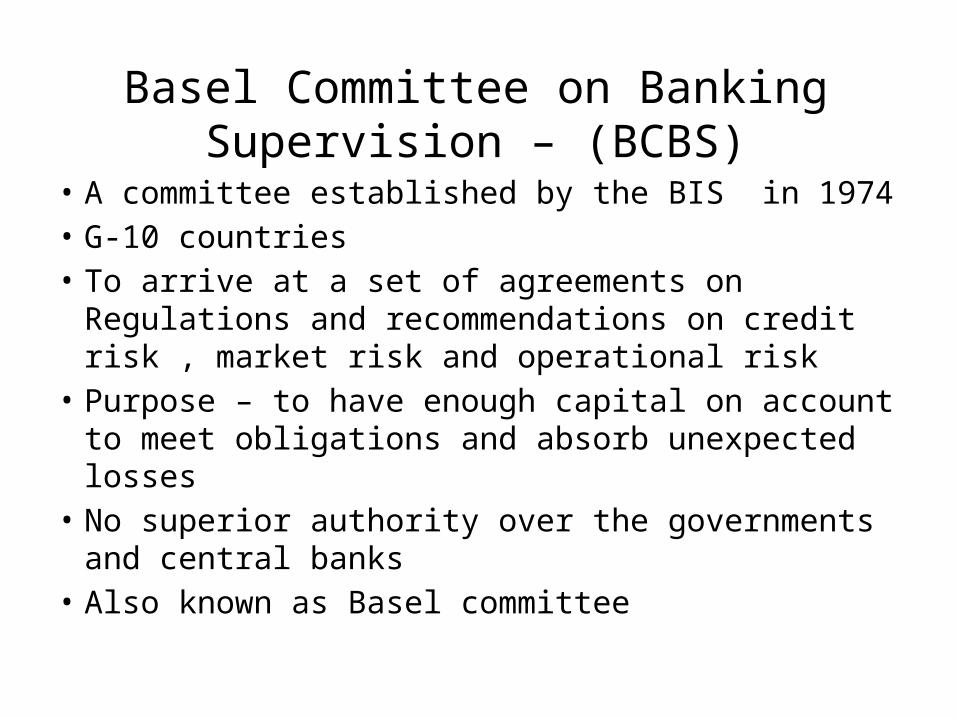

Basel Committee on Banking Supervision – (BCBS)

• A committee established by the BIS in 1974• G-10 countries• To arrive at a set of agreements on Regulations and

recommendations on credit risk , market risk and operational risk

• Purpose – to have enough capital on account to meet obligations and absorb unexpected losses

• No superior authority over the governments and central banks

• Also known as Basel committee

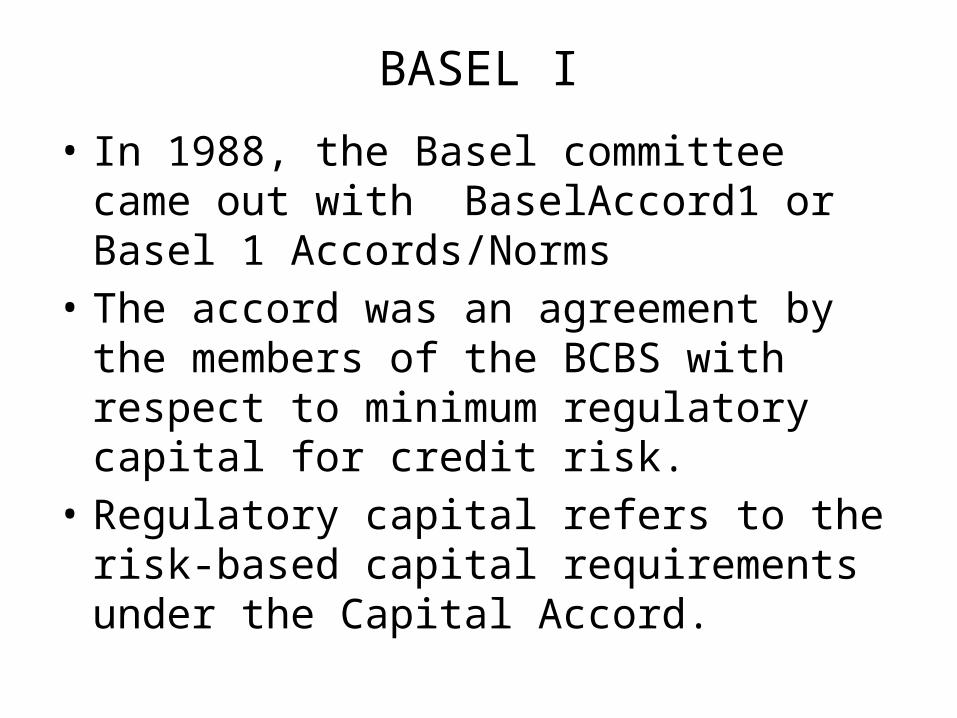

BASEL I

• In 1988, the Basel committee came out with BaselAccord1 or Basel 1 Accords/Norms

• The accord was an agreement by the members of the BCBS with respect to minimum regulatory capital for credit risk.

• Regulatory capital refers to the risk-based capital requirements under the Capital Accord.

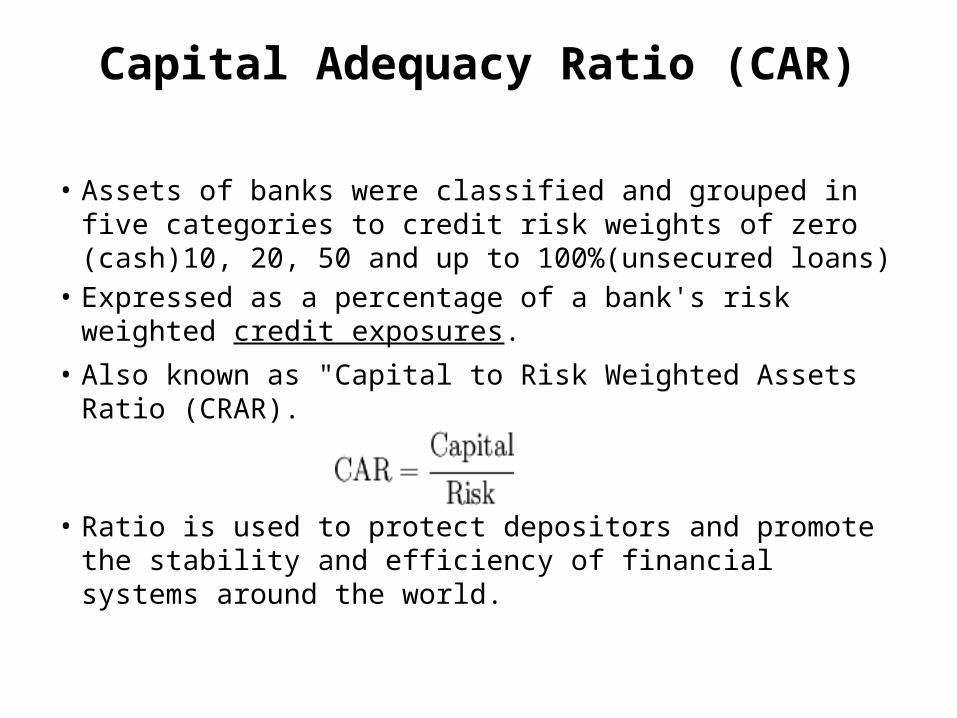

Capital Adequacy Ratio (CAR)

• Assets of banks were classified and grouped in five categories to credit risk weights of zero (cash)10, 20, 50 and up to 100%(unsecured loans)

• Expressed as a percentage of a bank's risk weighted credit exposures.

• Also known as "Capital to Risk Weighted Assets Ratio (CRAR).

• Ratio is used to protect depositors and promote the stability and efficiency of financial systems around the world.

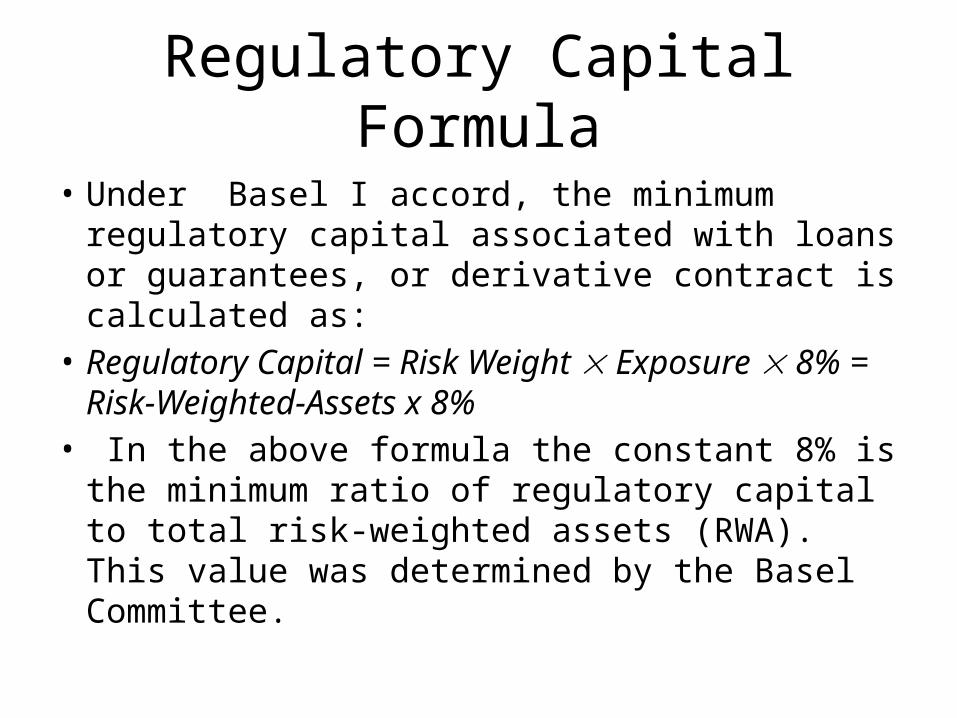

Regulatory Capital Formula

• Under Basel I accord, the minimum regulatory capital associated with loans or guarantees, or derivative contract is calculated as:

• Regulatory Capital = Risk Weight Exposure 8% = Risk-Weighted-Assets x 8%

• In the above formula the constant 8% is the minimum ratio of regulatory capital to total risk-weighted assets (RWA). This value was determined by the Basel Committee.

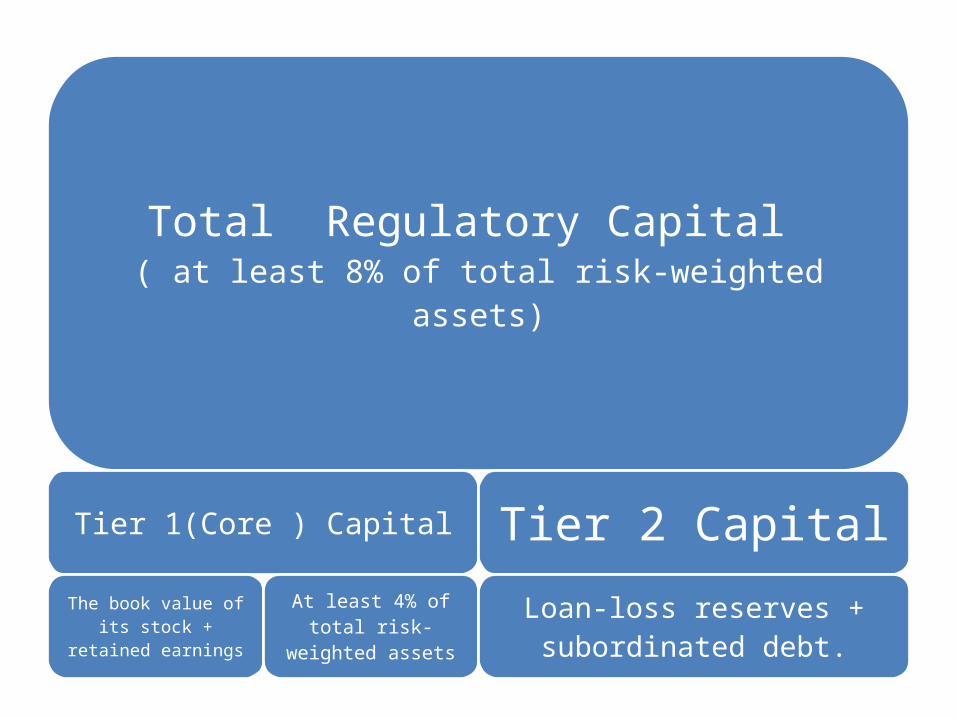

Total Regulatory Capital ( at least 8% of total risk-weighted assets)

Tier 1(Core ) CapitalThe book value of

its stock + retained earnings

At least 4% of total risk-

weighted assets

Tier 2 CapitalLoan-loss reserves + subordinated debt.

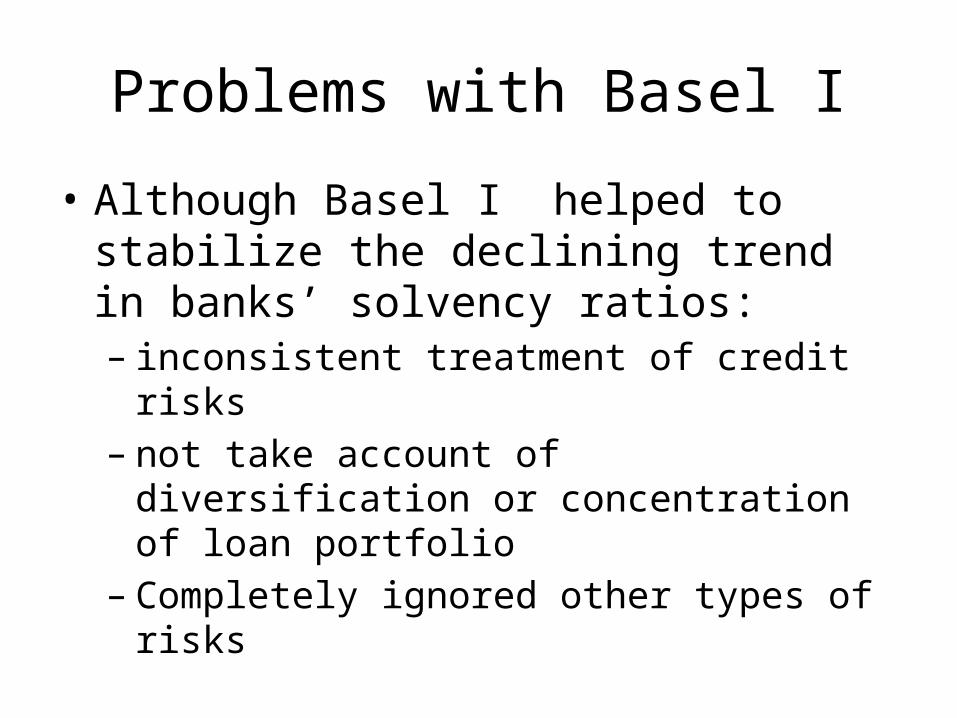

Problems with Basel I

• Although Basel I helped to stabilize the declining trend in banks’ solvency ratios:– inconsistent treatment of credit risks– not take account of diversification or

concentration of loan portfolio– Completely ignored other types of risks

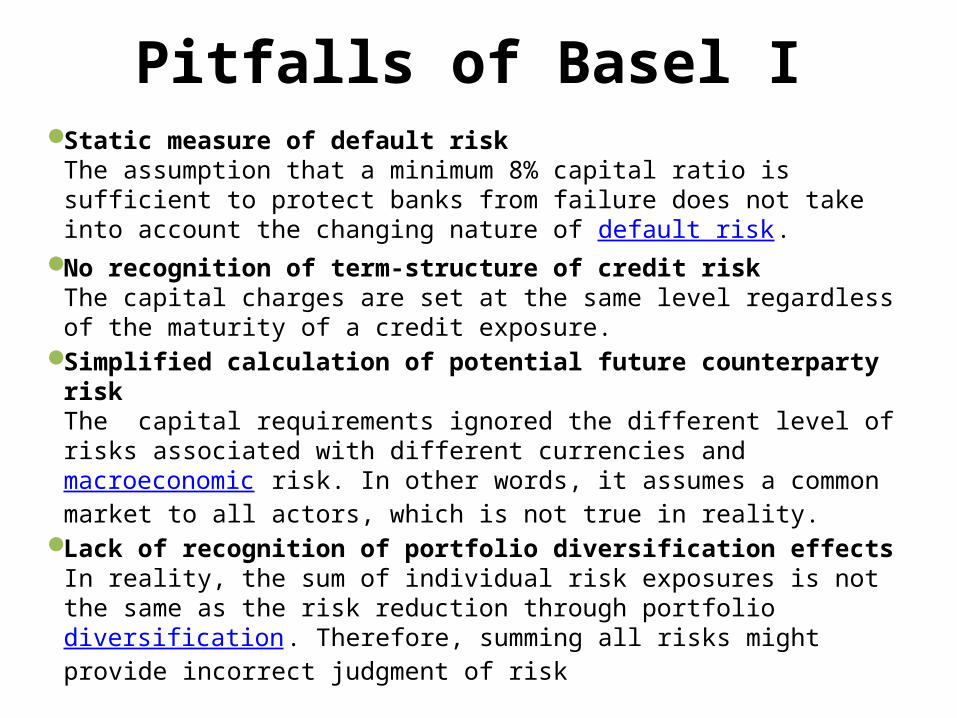

Pitfalls of Basel IStatic measure of default risk

The assumption that a minimum 8% capital ratio is sufficient to protect banks from failure does not take into account the changing nature of default risk.

No recognition of term-structure of credit risk The capital charges are set at the same level regardless of the maturity of a credit exposure.

Simplified calculation of potential future counterparty riskThe capital requirements ignored the different level of risks associated with different currencies and macroeconomic risk. In other words, it assumes a common market to all actors, which is not true in reality.

Lack of recognition of portfolio diversification effectsIn reality, the sum of individual risk exposures is not the same as the risk reduction through portfolio diversification. Therefore, summing all risks might provide incorrect judgment of risk

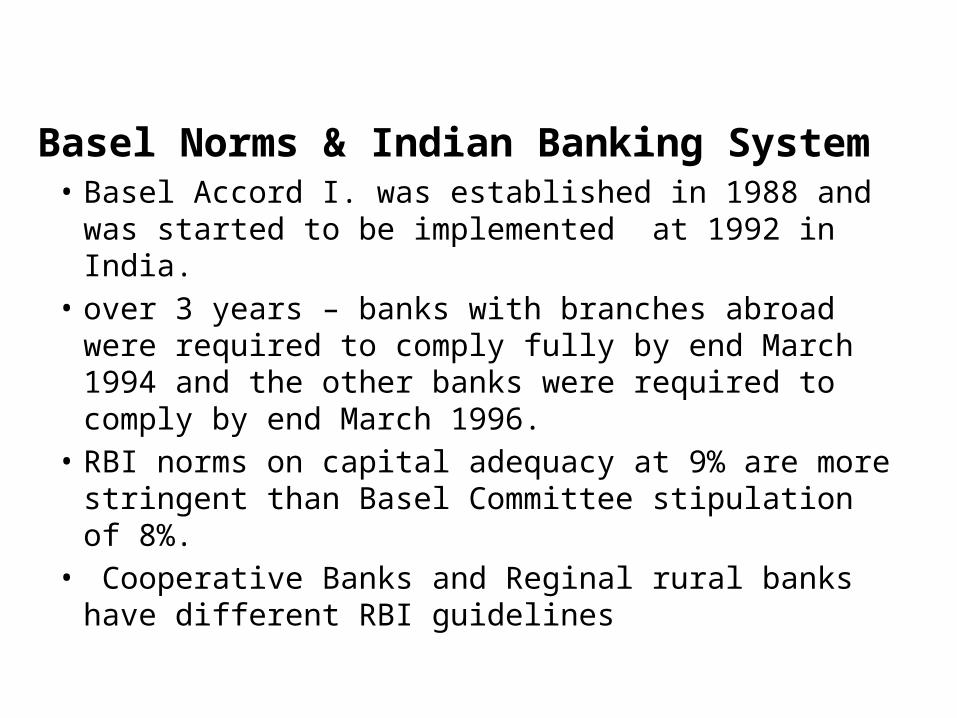

Basel Norms & Indian Banking System• Basel Accord I. was established in 1988 and was

started to be implemented at 1992 in India.• over 3 years – banks with branches abroad were

required to comply fully by end March 1994 and the other banks were required to comply by end March 1996.

• RBI norms on capital adequacy at 9% are more stringent than Basel Committee stipulation of 8%.

• Cooperative Banks and Reginal rural banks have different RBI guidelines

Conclusion

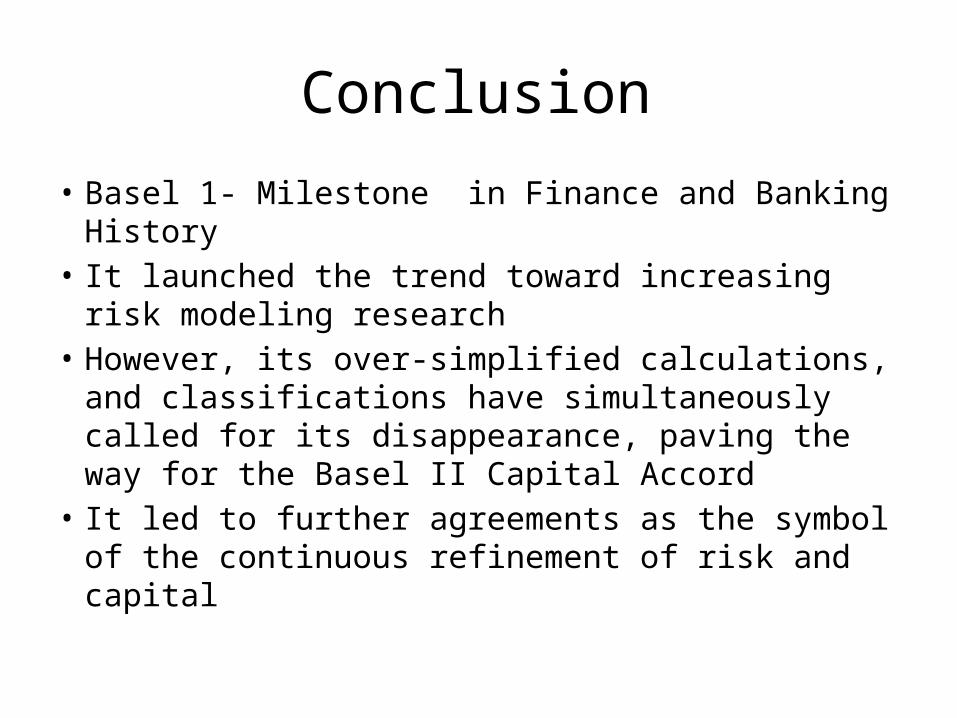

• Basel 1- Milestone in Finance and Banking History• It launched the trend toward increasing risk

modeling research• However, its over-simplified calculations, and

classifications have simultaneously called for its disappearance, paving the way for the Basel II Capital Accord

• It led to further agreements as the symbol of the continuous refinement of risk and capital

BASEL-II

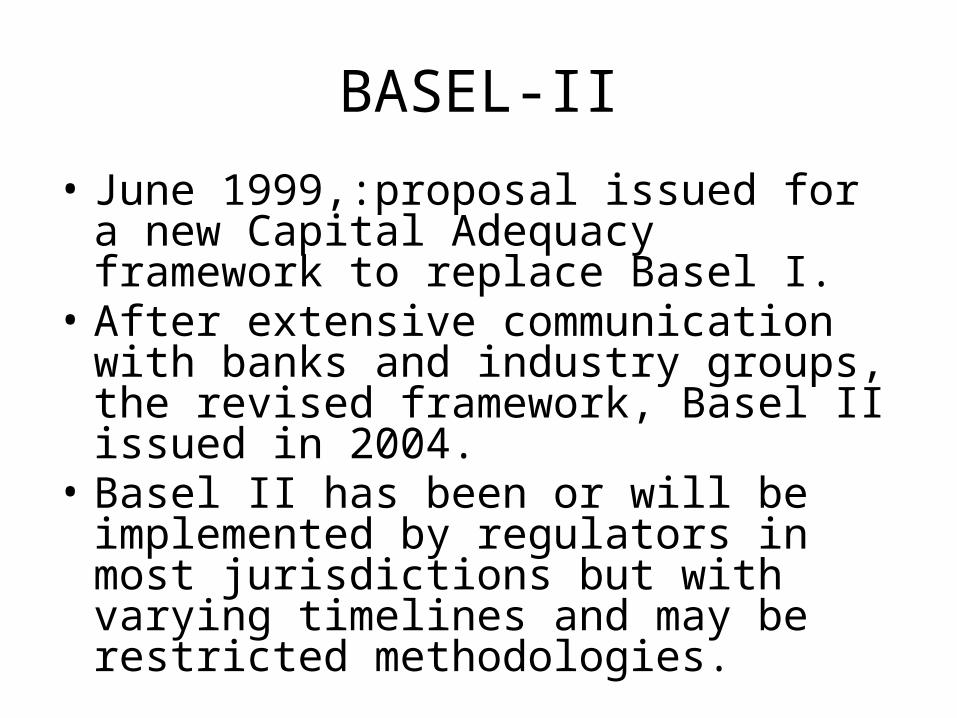

• June 1999,:proposal issued for a new Capital Adequacy framework to replace Basel I.

• After extensive communication with banks and industry groups, the revised framework, Basel II issued in 2004.

• Basel II has been or will be implemented by regulators in most jurisdictions but with varying timelines and may be restricted methodologies.

Improvements over BASEL-I

• The Basel I Capital Accord focused only on minimum regulatory capital requirements

• The Basel II Capital Accord broadens this focus by describing the supervisory process in the Basel II Capital Accord by “three pillars”:– Pillar 1 - Minimal regulatory capital requirements– Pillar 2 - Supervisory review of capital adequacy– Pillar 3 - Market discipline and disclosure.

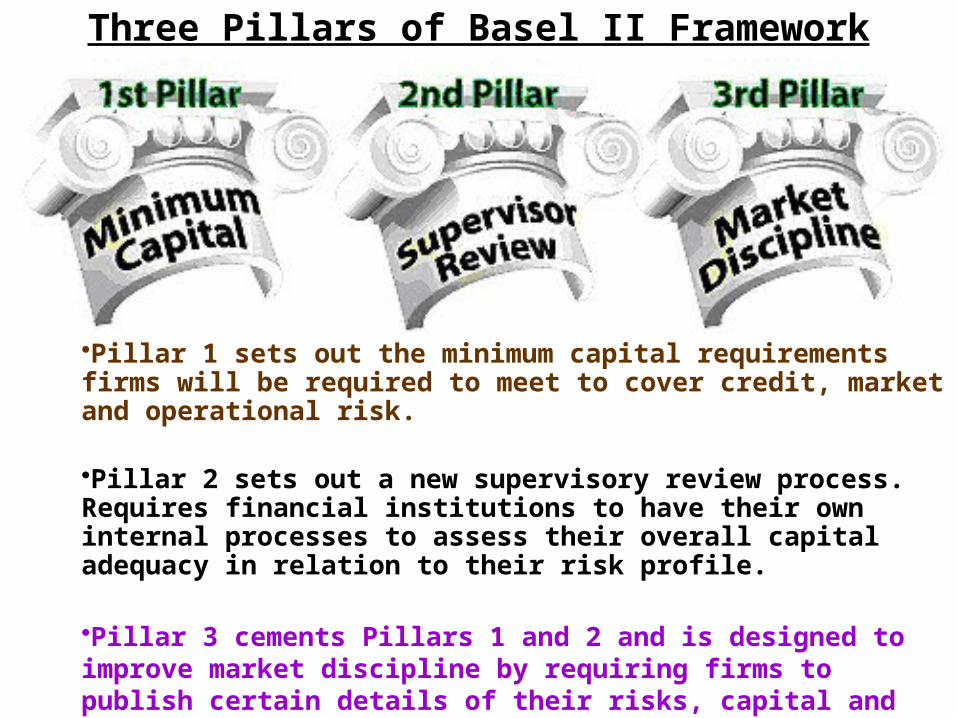

•Pillar 1 sets out the minimum capital requirements firms will be required to meet to cover credit, market and operational risk.

•Pillar 2 sets out a new supervisory review process. Requires financial institutions to have their own internal processes to assess their overall capital adequacy in relation to their risk profile.

•Pillar 3 cements Pillars 1 and 2 and is designed to improve market discipline by requiring firms to publish certain details of their risks, capital and risk management as to how senior management and the Board assess and will manage the institution's risks.

Three Pillars of Basel II Framework

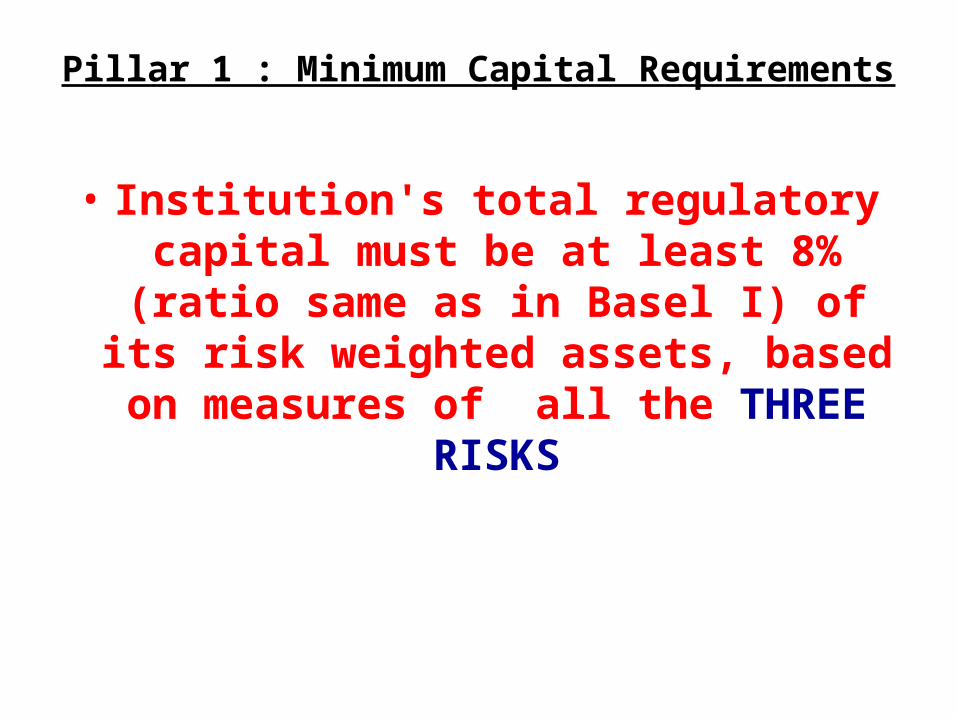

Pillar 1 : Minimum Capital Requirements

• Institution's total regulatory capital must be at least 8% (ratio same as in Basel I) of its risk

weighted assets, based on measures of all the THREE RISKS

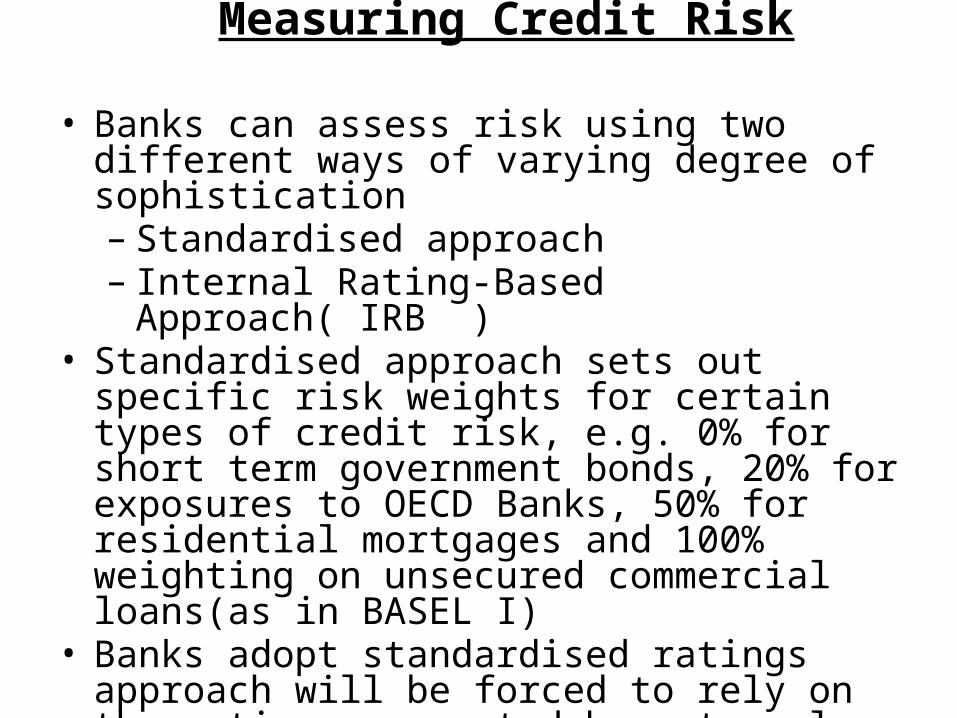

Measuring Credit Risk

• Banks can assess risk using two different ways of varying degree of sophistication– Standardised approach– Internal Rating-Based Approach( IRB )

• Standardised approach sets out specific risk weights for certain types of credit risk, e.g. 0% for short term government bonds, 20% for exposures to OECD Banks, 50% for residential mortgages and 100% weighting on unsecured commercial loans(as in BASEL I)

• Banks adopt standardised ratings approach will be forced to rely on the ratings generated by external agencies.

• Certain Banks are developing the IRB approach as a result.

Measuring operational risk

• Operational risk is risk of loss resulting from inadequate or failed internal processes, people and systems or from external events. It includes legal risk, such as exposure to fines, penalties and private settlements. It does not, however, include systemic risk.

• Three methods to measure operational risk– Basic Indicator Approach – Standardised Approach– Advanced Measurement Approach

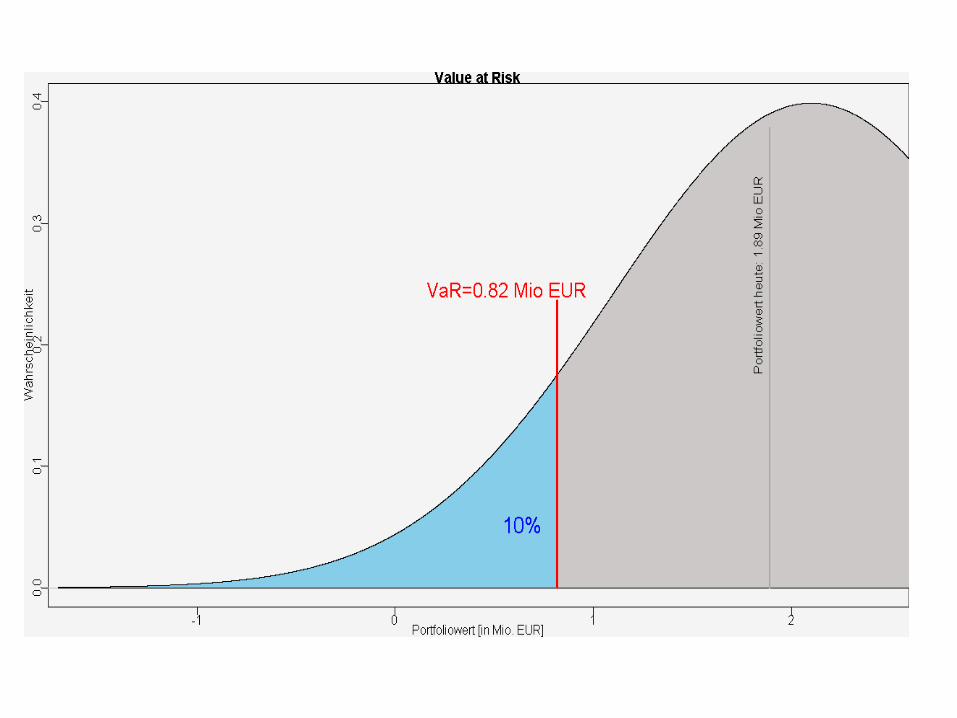

Measuring Market Risk

• Institutions may be obliged to make a series of disclosures about their risk profiles and regulatory capital procedures available to market participants, while balancing between meaningful disclosures and need to protect confidential and proprietary information. Preferred approach is VaR( Value at Risk)

Pillar 2 : Supervisory Review• Covers Supervisory Review Process, describing principles for

effective supervision.• Supervisors obliged to evaluate activities, corporate

governance, risk management and risk profiles of banks to determine whether they have to change or to allocate more capital for their risks (called Pillar 2 capital)

• Deals with regulatory response to the first pillar, giving regulators much improved 'tools' over those available to them under Basel I

• Also provides framework for dealing with all the other risks a bank may face, such as Systemic risk, pension risk, concentration risk, strategic risk, reputation risk, liquidity risk and legal risk, which the accord combines under the title of residual risk

• It gives banks a power to review their risk management system.

Pillar 3 : Market Discipline

• Covers transparency and the obligation of banks to disclose meaningful information to all stakeholders

• Clients and shareholders should have sufficient understanding of activities of banks, and the way they manage their risks

Implementation progress• Implementation has to accommodate differing cultures,

varying structural models, and complexities of public policy and existing regulation. Corporate strategy will be implemented based in part on how Basel II is ultimately interpreted by various countries' legislatures and regulators.

• The USA’s various regulators have agreed on a final approach. They have required the Internal Ratings-Based approach for the largest banks, and the standardized approach will not be available to anyone.

• In India, RBI implemented Basel II standardized norms on 31st March 2009 and is moving to internal ratings in credit and AMA norms for operational, VaR for market risks in banks.

• EU has already implemented the Accord via the EU Capital Requirements Directives. Many European banks already report capital adequacy ratios according to the new system. All credit institutions adopted it by 2008.

BASEL-III

• "Basel III is a comprehensive set of reform measures, developed by the Basel Committee on Banking Supervision, to strengthen the regulation, supervision and risk management of the banking sector".

• Thus, we can say that Basel 3 is only a continuation of effort initiated by the Basel Committee on Banking Supervision to enhance the banking regulatory framework under Basel I and Basel II.

• This latest Accord now seeks to improve the banking sector's ability to deal with financial and economic stress, improve risk management and strengthen the banks' transparency.

Objectives of Basel III measures ?

• Improve the banking sector's ability to absorb shocks arising from financial and economic stress, whatever the source

• Improve risk management and governance • Strengthen banks' transparency and disclosures. • Thus we can say that Basel III guidelines are aimed at

to improve the ability of banks to withstand periods of economic and financial stress as the new guidelines are more stringent than the earlier requirements for capital and liquidity in the banking sector.

Basel III: Three Pillars Still Standing :

• Basel III has essentially been designed to address the weaknesses that become too obvious during the 2008 financial crisis world faced.

• The intent of the Basel Committee seems to prepare the banking industry for any future economic downturns.

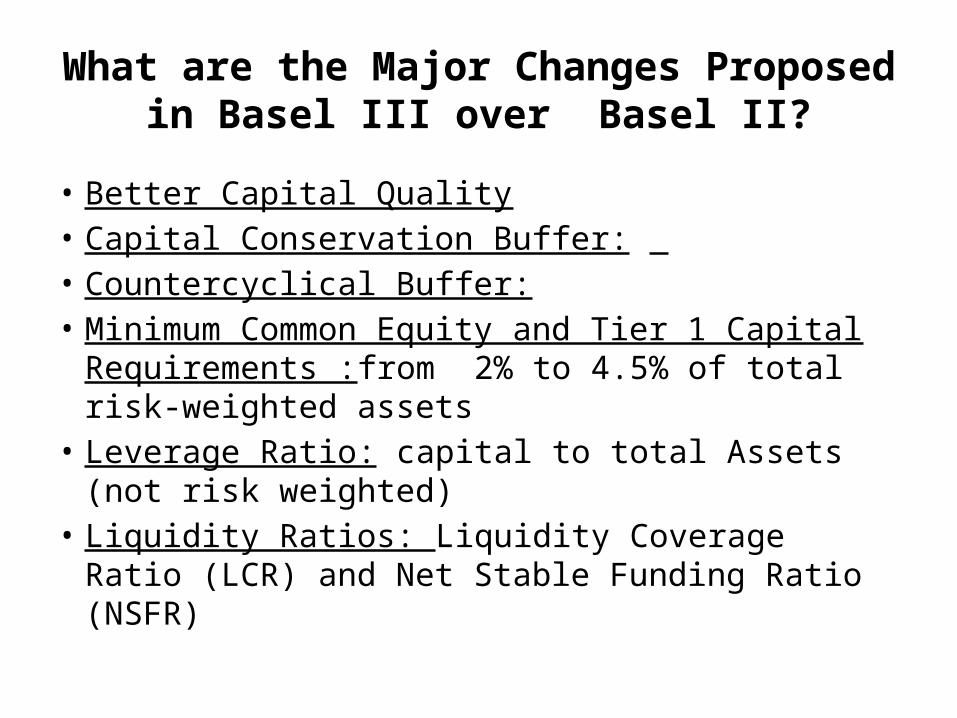

What are the Major Changes Proposed in Basel III over Basel II?

• Better Capital Quality• Capital Conservation Buffer: • Countercyclical Buffer:• Minimum Common Equity and Tier 1 Capital

Requirements :from 2% to 4.5% of total risk-weighted assets

• Leverage Ratio: capital to total Assets (not risk weighted)

• Liquidity Ratios: Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR)

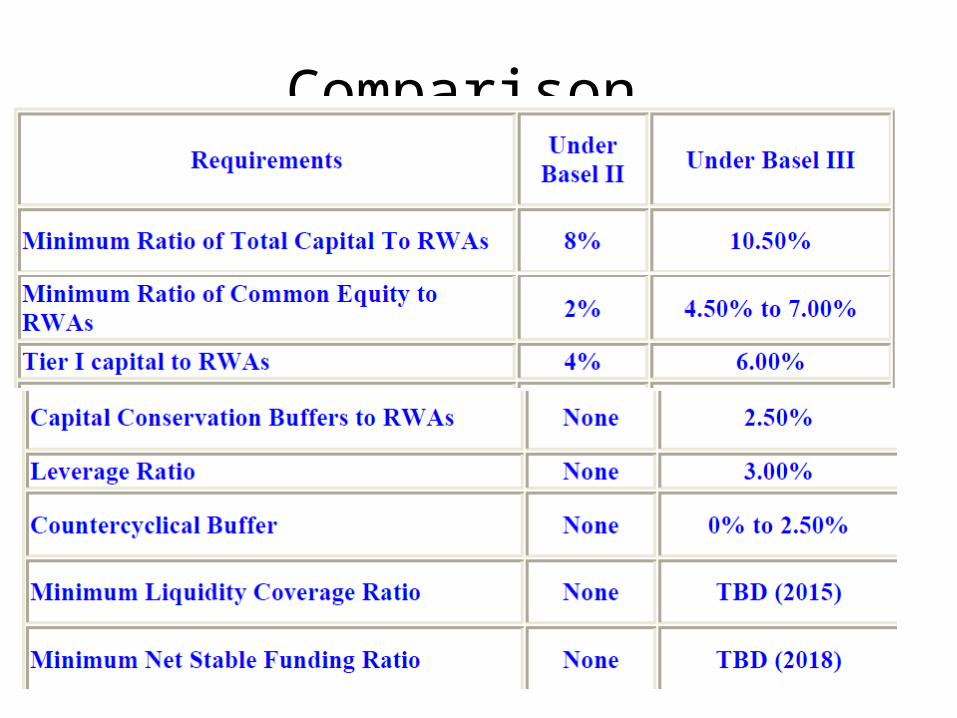

Comparison

How Basel III Requirements Will Affect Indian Banks?

• The Basel III , is to be implemented by banks in India as per the guidelines issued by RBI from time to time, will be challenging task not only for the banks but also for RBI& GOI.

• It is estimated that Indian banks will be required to raise Rs 6,00,000 crores in regulatory capital in next nine years or so i.e. by 2018-20 (The estimates vary from organisation to organisation).

• Expansion of capital to this extent will affect the returns on the equity of these banks specially public sector banks.

Exposure

• The type of instrument determines the Exposure:• For fully funded loans or bonds, the exposure is the face

amount.• For unfunded commitments : the exposure is 50% of the

commitment for undrawn commitments with maturity over 1 year and 0% of the commitment for undrawn commitments with maturity less than one year.

• For credit products (e.g. guarantees) the exposure is 100% of the notional value of the contract.

• For derivatives the exposure is determined by the equation: Replacement Costs +(Add-On Percentage Notional Principal).