Barry University and Subsidiaries - FLAuditor.gov rpts/2011...Revenues, gains, and other support:...

44

Barry University and Subsidiaries Consolidated Financial Statements as of and for the Years Ended June 30, 2011 and 2010, Supplemental Information for the Year Ended June 30, 2011, and Independent Auditors’ Reports in Accordance With Government Auditing Standards, OMB Circular A-133, and State of Florida Rules of the Auditor General, Chapter 10.650

Transcript of Barry University and Subsidiaries - FLAuditor.gov rpts/2011...Revenues, gains, and other support:...

Barry University and Subsidiaries Consolidated Financial Statements as of and for the Years Ended June 30, 2011 and 2010, Supplemental Information for the Year Ended June 30, 2011, and Independent Auditors’ Reports in Accordance With Government Auditing Standards, OMB Circular A-133, and State of Florida Rules of the Auditor General, Chapter 10.650

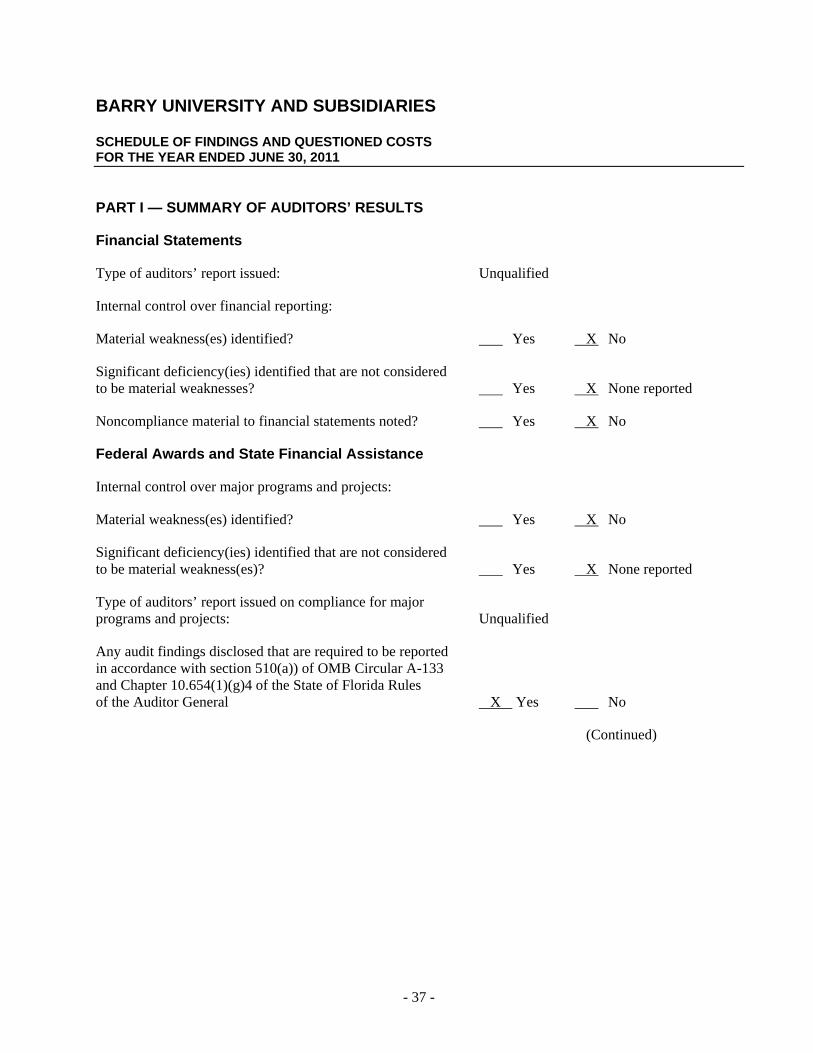

BARRY UNIVERSITY AND SUBSIDIARIES

TABLE OF CONTENTS

Page

INDEPENDENT AUDITORS’ REPORT 1–2

CONSOLIDATED FINANCIAL STATEMENTS AS OF AND FOR THE YEARS ENDED JUNE 30, 2011 AND 2010: Statements of Financial Position 3 Statements of Activities 4–5 Statements of Cash Flows 6–7 Notes to Consolidated Financial Statements 8–27

SUPPLEMENTAL SCHEDULE FOR THE YEAR ENDED JUNE 30, 2011: 28 Supplemental Schedule of Expenditures of Federal Awards and State Projects and Financial Assistance Programs 29–31 Notes to Supplemental Schedule of Expenditures of Federal Awards and State Projects and Financial Assistance Programs 32

INDEPENDENT AUDITORS’ REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED UPON AN AUDIT PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS 33–34

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE WITH REQUIREMENTS THAT COULD HAVE A DIRECT AND MATERIAL EFFECT ON EACH MAJOR FEDERAL PROGRAM AND STATE PROJECT AND FINANCIAL ASSISTANCE PROGRAM AND ON INTERNAL CONTROL OVER COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133 AND STATE OF FLORIDA RULES OF THE AUDITOR GENERAL, CHAPTER 10.650 35–36

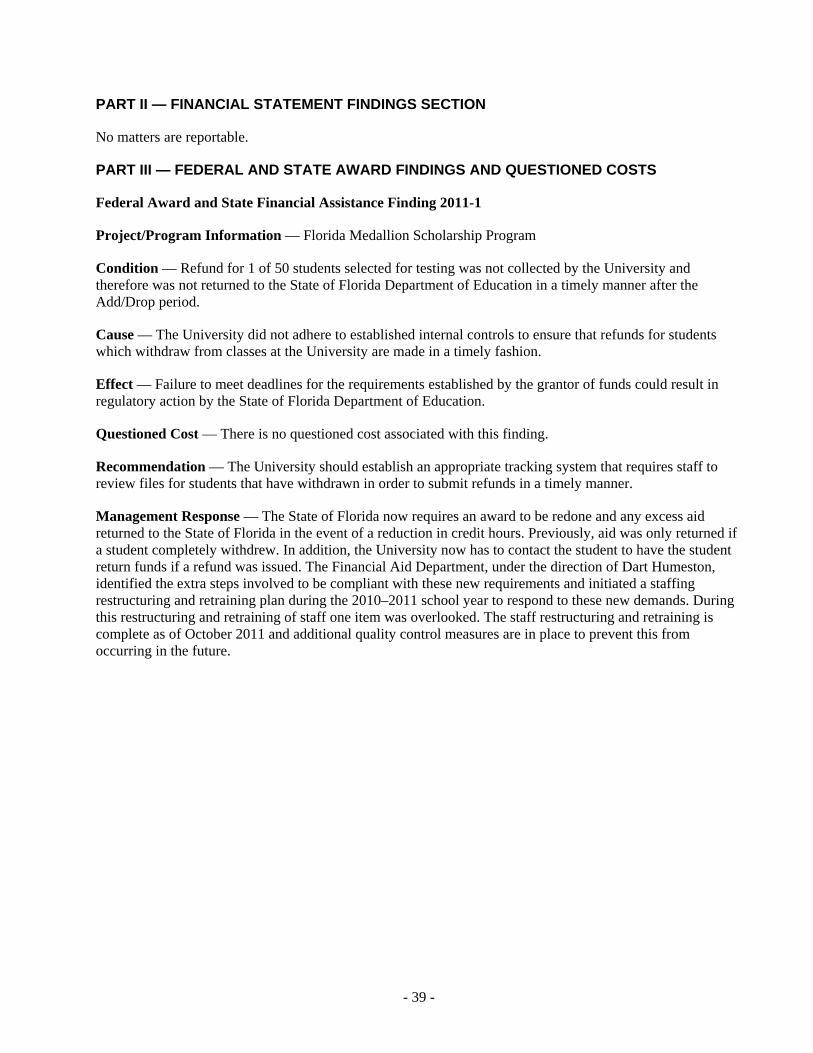

SCHEDULE OF FINDINGS AND QUESTIONED COSTS FOR THE YEAR ENDED JUNE 30, 2011 37–39

SUMMARY SCHEDULE OF PRIOR AUDIT FINDINGS 40

INDEPENDENT AUDITORS’ MANAGEMENT LETTER IN ACCORDANCE WITH THE STATE OF FLORIDA RULES OF THE AUDITOR GENERAL 41–42

INDEPENDENT AUDITORS’ REPORT

To the Audit Committee of the Board of Trustees of Barry University and Subsidiaries:

We have audited the accompanying consolidated statements of financial position of Barry University and subsidiaries (the “University”) as of June 30, 2011 and 2010, and the related consolidated statements of activities and of cash flows for the years then ended. These financial statements are the responsibility of the management of the University. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the University’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the consolidated financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall consolidated financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, such consolidated financial statements present fairly, in all material respects, the consolidated financial position of the University as of June 30, 2011 and 2010, and the consolidated changes in its net assets and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America.

Our audits were performed for the purposes of forming an opinion on the basic consolidated financial statements of the University, taken as a whole. The accompanying supplemental schedule of expenditures of federal awards and state projects and financial assistance programs for the year ended June 30, 2011, is presented for the purpose of additional analysis as required by the U.S. Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, and State of Florida Rules of the Auditor General, Chapter 10.650, State Single Audits of Nonprofit and For-Profit Organizations, and is not a required part of the basic 2011 consolidated financial statements. This supplemental schedule is the responsibility of the management of the University. Such information has been subjected to the auditing procedures applied in our audit of the basic 2011 consolidated financial statements and, in our opinion, is fairly stated in all material respects when considered in relation to the basic 2011 consolidated financial statements taken as a whole.

In accordance with Government Auditing Standards, we have also issued our report dated November 8, 2011, on our consideration of the University’s internal control over financial reporting and our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial

- 2 -

reporting and compliance and the results of that testing and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be considered in assessing the results of our audit.

November 8, 2011

- 3 -

BARRY UNIVERSITY AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF FINANCIAL POSITIONAS OF JUNE 30, 2011 AND 2010

Temporarily PermanentlyUnrestricted Restricted Restricted 2011 2010

ASSETS

CASH AND CASH EQUIVALENTS 32,776,074$ 3,064,020$ - $ 35,840,094$ 30,123,737$

RESTRICTED CASH 2,396,645 2,396,645 6,916,914

STUDENT ACCOUNTS RECEIVABLE — Net 4,885,267 4,885,267 5,384,449

CONTRIBUTIONS RECEIVABLE — Net 2,826,030 2,826,030 3,447,725

OTHER RECEIVABLES — Net 1,455,993 3,969 1,459,962 2,012,179

PREPAID EXPENSES AND OTHER ASSETS 6,966,515 1,029,245 7,995,760 7,193,838

LOANS AND NOTES RECEIVABLE — Net 3,964,958 24,016 3,988,974 3,236,660

INVESTMENTS 9,255,569 12,828,922 22,084,491 19,631,619

INVESTMENTS HELD FOR DEBT SERVICE RESERVE 3,972,854 3,972,854 2,500,674

CONTRIBUTIONS RECEIVABLE FROM TRUSTS 332,303 332,303 288,597

PROPERTY, PLANT, AND EQUIPMENT — Net 96,149,831 96,149,831 90,277,679

DUE FROM (TO) OTHER NET ASSETS 779,623 (1,081,913) 302,290 -

TOTAL 162,603,329$ 6,197,670$ 13,131,212$ 181,932,211$ 171,014,071$

LIABILITIES AND NET ASSETS

LIABILITIES: Accounts payable and accrued expenses 10,873,794$ 105,505$ - $ 10,979,299$ 9,515,939$ Student deposits 4,524,753 4,524,753 4,877,005 Deferred revenue 539,625 539,625 720,713 Other liabilities 3,832,481 3,832,481 3,348,696 Loans, mortgages, notes payable, and capital leases 60,926,909 60,926,909 62,598,424

Total liabilities 80,697,562 105,505 - 80,803,067 81,060,777

COMMITMENTS AND CONTINGENCIES (Note 12)

NET ASSETS: Unrestricted: Unrestricted — Barry University 81,509,199 81,509,199 69,926,812 Noncontrolling interest in partnership 396,568 396,568 396,535 Total unrestricted 81,905,767 - - 81,905,767 70,323,347 Temporarily restricted 6,092,165 6,092,165 6,642,797 Permanently restricted 13,131,212 13,131,212 12,987,150 Total net assets 81,905,767 6,092,165 13,131,212 101,129,144 89,953,294

TOTAL 162,603,329$ 6,197,670$ 13,131,212$ 181,932,211$ 171,014,071$

See notes to consolidated financial statements.

Total

- 4 -

BARRY UNIVERSITY AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF ACTIVITIESFOR THE YEAR ENDED JUNE 30, 2011

Temporarily PermanentlyUnrestricted Restricted Restricted Total

CHANGES IN NET ASSETS: Revenues, gains, and other support: Tuition and fees — net of $45,961,723 of financial aid and discounts 134,867,127$ - $ - $ 134,867,127$ Private gifts and grants 2,522,924 492,752 94,164 3,109,840 Government grants and contracts 5,970,804 5,970,804 Investment income 368,481 368,481 Net realized and unrealized gain on investments 2,226,809 2,226,809 Rental income from investments 724,316 724,316 Earnings of an equity method investee 113,477 113,477 Other income 4,470,648 12,359 4,483,007 Podiatric clinic practice 548,122 548,122 Auxiliary enterprises 11,466,274 11,466,274 Contributed services 118,040 118,040

Total 163,397,022 505,111 94,164 163,996,297

Net assets released from restrictions 1,005,845 (1,055,743) 49,898 Total revenues, gains, and other support 164,402,867 (550,632) 144,062 163,996,297 EXPENSES AND LOSSES: Educational and general expenses: Academic departments and programs 80,410,185 80,410,185 Grants and contracts 3,684,217 3,684,217 Academic support 12,402,751 12,402,751 Student services 16,144,252 16,144,252 Institutional support 25,604,074 25,604,074 Podiatric clinical practice 889,380 889,380

Total educational and general expenses 139,134,859 139,134,859

BarryTel expenses (including impairment loss of $3,849,786) 9,065,248 9,065,248 Auxiliary enterprises 8,521,667 8,521,667

Total expenses and losses 156,721,774 - - 156,721,774

Increase in net assets from continuing operations 7,681,093 (550,632) 144,062 7,274,523

Increase in unrestricted net assets from discontinued operations (including gain on sale of $3,529,615) 3,901,327 3,901,327

INCREASE (DECREASE) IN NET ASSETS 11,582,420 (550,632) 144,062 11,175,850

NET ASSETS — Beginning of year 70,323,347 6,642,797 12,987,150 89,953,294 NET ASSETS — End of year 81,905,767$ 6,092,165$ 13,131,212$ 101,129,144$

See notes to consolidated financial statements.

- 5 -

BARRY UNIVERSITY AND SUBSIDIARIES

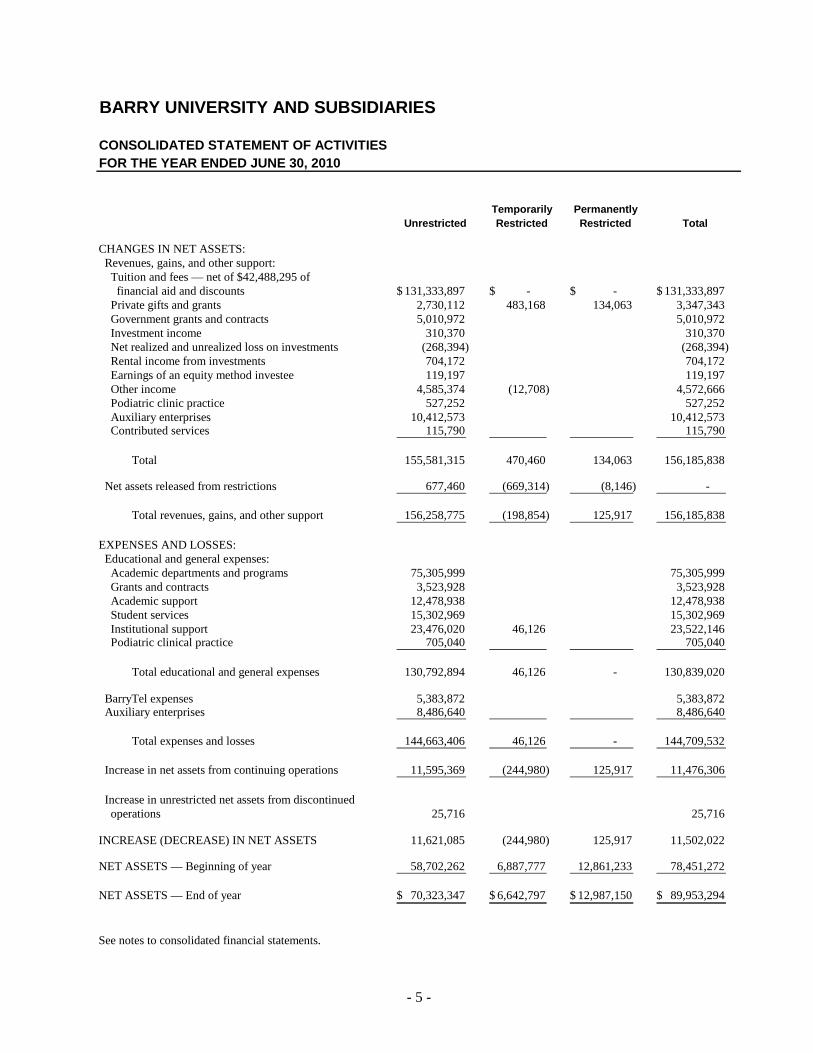

CONSOLIDATED STATEMENT OF ACTIVITIESFOR THE YEAR ENDED JUNE 30, 2010

Temporarily PermanentlyUnrestricted Restricted Restricted Total

CHANGES IN NET ASSETS: Revenues, gains, and other support: Tuition and fees — net of $42,488,295 of financial aid and discounts 131,333,897$ - $ - $ 131,333,897$ Private gifts and grants 2,730,112 483,168 134,063 3,347,343 Government grants and contracts 5,010,972 5,010,972 Investment income 310,370 310,370 Net realized and unrealized loss on investments (268,394) (268,394) Rental income from investments 704,172 704,172 Earnings of an equity method investee 119,197 119,197 Other income 4,585,374 (12,708) 4,572,666 Podiatric clinic practice 527,252 527,252 Auxiliary enterprises 10,412,573 10,412,573 Contributed services 115,790 115,790

Total 155,581,315 470,460 134,063 156,185,838

Net assets released from restrictions 677,460 (669,314) (8,146) - Total revenues, gains, and other support 156,258,775 (198,854) 125,917 156,185,838 EXPENSES AND LOSSES: Educational and general expenses: Academic departments and programs 75,305,999 75,305,999 Grants and contracts 3,523,928 3,523,928 Academic support 12,478,938 12,478,938 Student services 15,302,969 15,302,969 Institutional support 23,476,020 46,126 23,522,146 Podiatric clinical practice 705,040 705,040

Total educational and general expenses 130,792,894 46,126 - 130,839,020

BarryTel expenses 5,383,872 5,383,872 Auxiliary enterprises 8,486,640 8,486,640 Total expenses and losses 144,663,406 46,126 - 144,709,532

Increase in net assets from continuing operations 11,595,369 (244,980) 125,917 11,476,306

Increase in unrestricted net assets from discontinued operations 25,716 25,716

INCREASE (DECREASE) IN NET ASSETS 11,621,085 (244,980) 125,917 11,502,022

NET ASSETS — Beginning of year 58,702,262 6,887,777 12,861,233 78,451,272 NET ASSETS — End of year 70,323,347$ 6,642,797$ 12,987,150$ 89,953,294$

See notes to consolidated financial statements.

- 6 -

BARRY UNIVERSITY AND SUBSIDIARIES

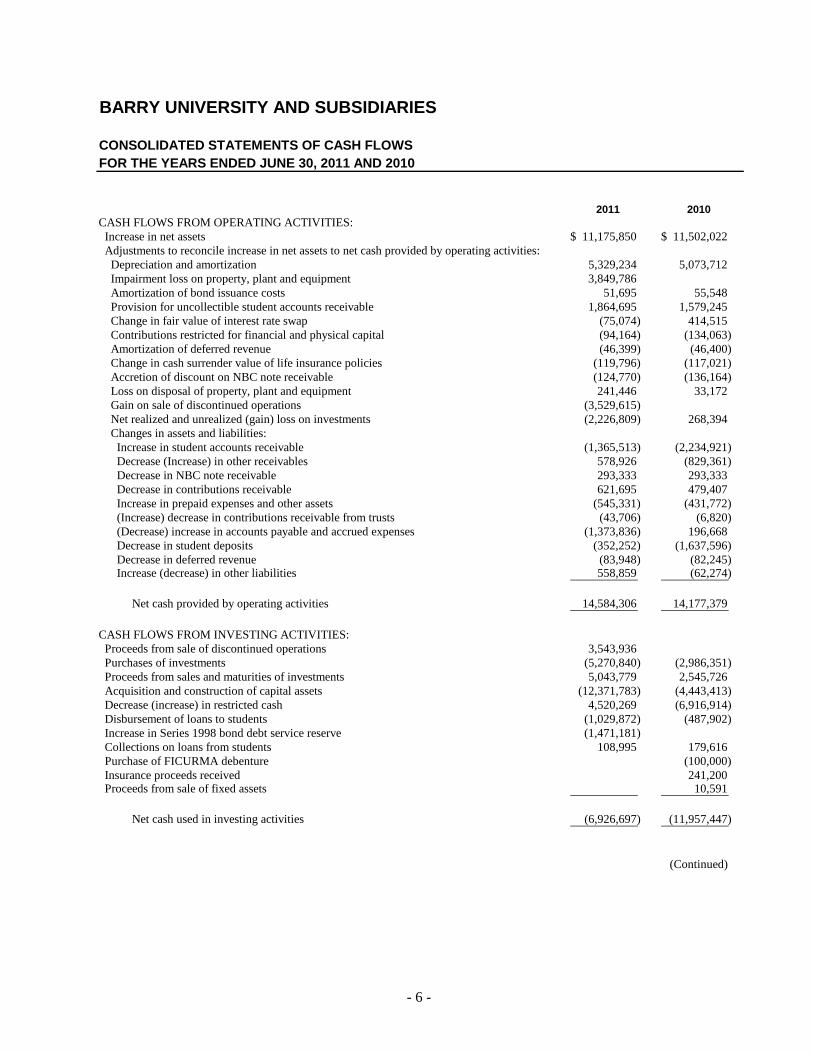

CONSOLIDATED STATEMENTS OF CASH FLOWSFOR THE YEARS ENDED JUNE 30, 2011 AND 2010

2011 2010CASH FLOWS FROM OPERATING ACTIVITIES: Increase in net assets 11,175,850$ 11,502,022$ Adjustments to reconcile increase in net assets to net cash provided by operating activities: Depreciation and amortization 5,329,234 5,073,712 Impairment loss on property, plant and equipment 3,849,786 Amortization of bond issuance costs 51,695 55,548 Provision for uncollectible student accounts receivable 1,864,695 1,579,245 Change in fair value of interest rate swap (75,074) 414,515 Contributions restricted for financial and physical capital (94,164) (134,063) Amortization of deferred revenue (46,399) (46,400) Change in cash surrender value of life insurance policies (119,796) (117,021) Accretion of discount on NBC note receivable (124,770) (136,164) Loss on disposal of property, plant and equipment 241,446 33,172 Gain on sale of discontinued operations (3,529,615) Net realized and unrealized (gain) loss on investments (2,226,809) 268,394 Changes in assets and liabilities: Increase in student accounts receivable (1,365,513) (2,234,921) Decrease (Increase) in other receivables 578,926 (829,361) Decrease in NBC note receivable 293,333 293,333 Decrease in contributions receivable 621,695 479,407 Increase in prepaid expenses and other assets (545,331) (431,772) (Increase) decrease in contributions receivable from trusts (43,706) (6,820) (Decrease) increase in accounts payable and accrued expenses (1,373,836) 196,668 Decrease in student deposits (352,252) (1,637,596) Decrease in deferred revenue (83,948) (82,245) Increase (decrease) in other liabilities 558,859 (62,274)

Net cash provided by operating activities 14,584,306 14,177,379

CASH FLOWS FROM INVESTING ACTIVITIES: Proceeds from sale of discontinued operations 3,543,936 Purchases of investments (5,270,840) (2,986,351) Proceeds from sales and maturities of investments 5,043,779 2,545,726 Acquisition and construction of capital assets (12,371,783) (4,443,413) Decrease (increase) in restricted cash 4,520,269 (6,916,914) Disbursement of loans to students (1,029,872) (487,902) Increase in Series 1998 bond debt service reserve (1,471,181) Collections on loans from students 108,995 179,616 Purchase of FICURMA debenture (100,000) Insurance proceeds received 241,200 Proceeds from sale of fixed assets 10,591

Net cash used in investing activities (6,926,697) (11,957,447)

(Continued)

- 7 -

BARRY UNIVERSITY AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWSFOR THE YEARS ENDED JUNE 30, 2011 AND 2010

2011 2010

CASH FLOWS FROM FINANCING ACTIVITIES: Contributions restricted for financial and physical capital 94,163$ 134,063$ Proceeds from issuance of indebtedness 7,000,000 Repayments of principal on notes payable (2,035,415) (1,568,004)

Net cash (used in) provided by financing activities (1,941,252) 5,566,059

NET INCREASE IN CASH AND CASH EQUIVALENTS 5,716,357 7,785,991

CASH AND CASH EQUIVALENTS — Beginning of year 30,123,737 22,337,746

CASH AND CASH EQUIVALENTS — End of year 35,840,094$ 30,123,737$

SUPPLEMENTAL DISCLOSURE — Cash paid for interest 2,936,525$ 2,900,453$

NONCASH TRANSACTIONS: Property, plant, and equipment acquired through accounts payable 2,808,096$ 448,301$

Property, plant, and equipment acquired through capital leases 349,590$ - $

Deferred programming and membership costs financed through note payable - $ 895,776$

Write-off of student accounts receivable 1,865,695$ 1,584,912$

See notes to consolidated financial statements. (Concluded)

- 8 -

BARRY UNIVERSITY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS AS OF AND FOR THE YEARS ENDED JUNE 30, 2011 AND 2010

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Organization — Founded in 1940, Barry University is a four-year Catholic university sponsored by the Dominican Sisters of Adrian, Michigan, and is governed by an independent, self-perpetuating Board of Trustees. Barry University, whose main campus is located in Miami Shores, Florida, offers more than 100 undergraduate, graduate, professional, and doctoral programs to approximately 9,000 full- and part-time students at multiple sites throughout the state of Florida.

The accompanying consolidated financial statements include Barry University and its subsidiaries, Barry Telecommunications, Inc. (“BarryTel”), and 6484 Indian Creek Limited Partnership (the “Partnership”), (collectively, the “University”). BarryTel is a wholly owned subsidiary of Barry University that operates as a not-for-profit organization. BarryTel was formed on January 24, 1997, to operate public radio and television stations in South Florida. Barry Tel’s radio license and related assets were sold during the year ended June 30, 2011. (See Note 11).

The University has a 61.64% interest as the general partner in the Partnership, with the remaining interest held by unrelated minority partners. The Partnership holds land as an investment and earns rental revenues through a ground lease arrangement.

The University holds a 35% equity investment in the South Florida Instructional Television, Inc. (SFITV), which holds licenses for educational broadband service channels. The University acquired this interest in 1985 for no initial investment. SFITV had no activity prior to fiscal year 2009.

Basis of Presentation — The consolidated financial statements are prepared on the accrual basis of accounting. Net assets, revenues, and gains or losses are classified into three categories of net assets based on the existence or absence of donor-imposed restrictions. The three net asset categories reflected in the accompanying consolidated financial statements are as follows:

Unrestricted — Net assets which are free of donor-imposed restrictions; all revenues, gains, and losses that are not changes in permanently or temporarily restricted net assets.

Temporarily Restricted — Net assets whose use by the University is limited by donor-imposed stipulations that either expire by the passage of time, or that can be fulfilled or removed by actions of the University pursuant to those stipulations.

Permanently Restricted — Net assets whose use by the University is limited by donor-imposed stipulations that neither expire with the passage of time nor can be fulfilled or otherwise removed by actions.

Use of Estimates — The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. The University considers critical accounting policies to be those that require more significant judgments and estimates in the preparation of its consolidated financial statements,

- 9 -

including valuation of accounts receivable, including student accounts, pledges, and receivables under contribution agreements and valuation of certain investments. Management relies on historical experience and on other assumptions believed to be reasonable under the circumstances in making its judgments and estimates. Actual results could differ from those estimates.

Consolidation — The accompanying consolidated financial statements present the financial position, changes in net assets, and cash flows of the University and its subsidiaries, BarryTel and the Partnership. All significant intercompany balances and transactions are eliminated in consolidation.

Subsequent Events — The University evaluated subsequent events for potential recognition and disclosure through November 8, 2011, the date the financial statements were available to be issued.

Cash and Cash Equivalents — All highly liquid cash investments with original maturities of three months or less when purchased are considered to be cash equivalents.

Restricted Cash — Restricted cash consists of cash and cash equivalents held for purposes of the construction of a law school facility.

Investments — Investments in equity securities with readily determinable fair values and all investments in debt securities are measured at fair value in the accompanying consolidated statements of financial position. As described in Note 2, the University purchased certain properties as investments, consisting of the Sinai Plaza Nursing and Rehabilitation Center (the “Nursing and Rehabilitation Center”), the residence for the University’s president, and an additional investment property that is leased to a third party, all of which are measured at fair value.

The University is not in the business of leasing property or conducting nursing home activities. Based on such, the University has determined to account for these properties as investments and value the properties at fair value, consistent with all of its other investments.

Interest and dividends are included as investment income in the accompanying consolidated statements of activities. Unrealized and realized gains and losses are recognized as changes in net assets in the accompanying consolidated statements of activities. Unless specifically identified, all investment income and unrealized and realized gains and losses are recorded in unrestricted revenues, gains, and other support.

Student Accounts Receivable — Student accounts receivable consist of amounts due from students for tuition, fees and room and board for the current term and for prior completed terms adjusted for any scholarships and certain grant funds received. Recoveries of receivables previously written off are recorded in the period received. The allowance for doubtful accounts of student accounts receivables is based on the aging of the outstanding balance and historical collection rates. The University fully reserves all outstanding balances greater than 360 days.

Loans and Notes Receivable — Loans and note receivable consist primarily of amounts loaned to students through loan programs sponsored by the federal government. This program includes the Perkins student loan program and the nursing faculty loan program. In addition the balance also includes a 15 year note obtained by BarryTel as part of a settlement with National Broadcasting Company. (See Note 10). The University fully reserves all outstanding balances greater than 360 days which they deem to be uncollectible.

- 10 -

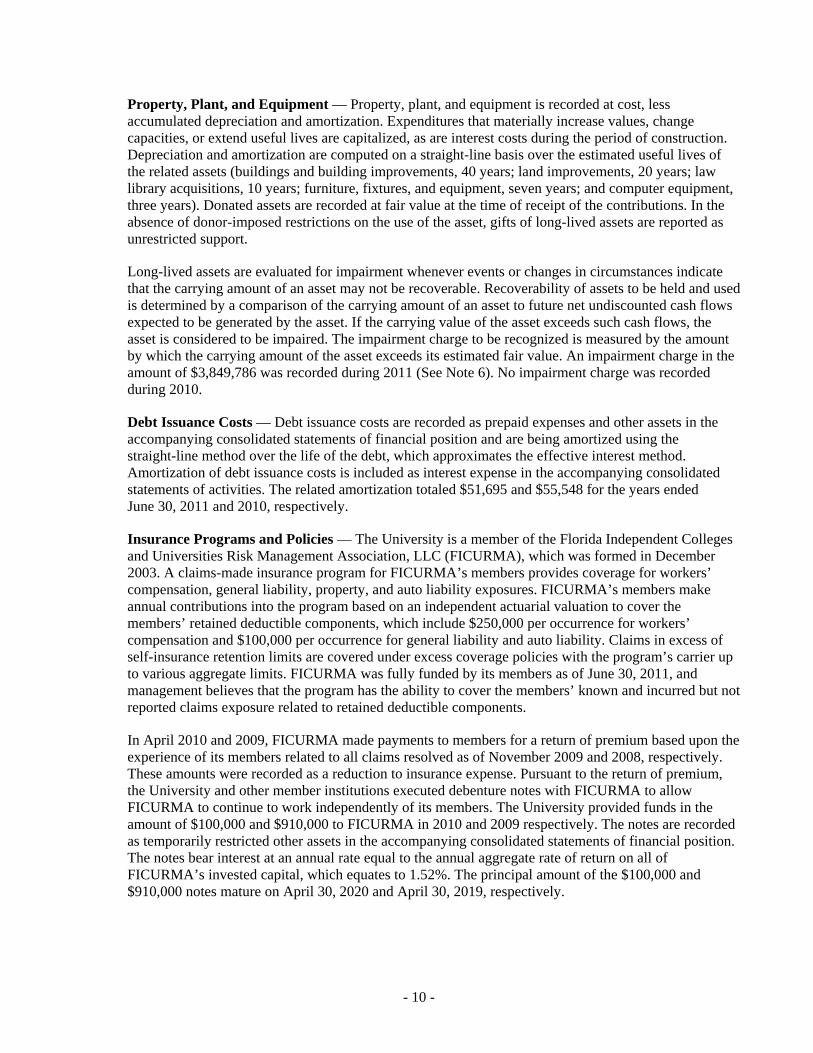

Property, Plant, and Equipment — Property, plant, and equipment is recorded at cost, less accumulated depreciation and amortization. Expenditures that materially increase values, change capacities, or extend useful lives are capitalized, as are interest costs during the period of construction. Depreciation and amortization are computed on a straight-line basis over the estimated useful lives of the related assets (buildings and building improvements, 40 years; land improvements, 20 years; law library acquisitions, 10 years; furniture, fixtures, and equipment, seven years; and computer equipment, three years). Donated assets are recorded at fair value at the time of receipt of the contributions. In the absence of donor-imposed restrictions on the use of the asset, gifts of long-lived assets are reported as unrestricted support.

Long-lived assets are evaluated for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of assets to be held and used is determined by a comparison of the carrying amount of an asset to future net undiscounted cash flows expected to be generated by the asset. If the carrying value of the asset exceeds such cash flows, the asset is considered to be impaired. The impairment charge to be recognized is measured by the amount by which the carrying amount of the asset exceeds its estimated fair value. An impairment charge in the amount of $3,849,786 was recorded during 2011 (See Note 6). No impairment charge was recorded during 2010.

Debt Issuance Costs — Debt issuance costs are recorded as prepaid expenses and other assets in the accompanying consolidated statements of financial position and are being amortized using the straight-line method over the life of the debt, which approximates the effective interest method. Amortization of debt issuance costs is included as interest expense in the accompanying consolidated statements of activities. The related amortization totaled $51,695 and $55,548 for the years ended June 30, 2011 and 2010, respectively.

Insurance Programs and Policies — The University is a member of the Florida Independent Colleges and Universities Risk Management Association, LLC (FICURMA), which was formed in December 2003. A claims-made insurance program for FICURMA’s members provides coverage for workers’ compensation, general liability, property, and auto liability exposures. FICURMA’s members make annual contributions into the program based on an independent actuarial valuation to cover the members’ retained deductible components, which include $250,000 per occurrence for workers’ compensation and $100,000 per occurrence for general liability and auto liability. Claims in excess of self-insurance retention limits are covered under excess coverage policies with the program’s carrier up to various aggregate limits. FICURMA was fully funded by its members as of June 30, 2011, and management believes that the program has the ability to cover the members’ known and incurred but not reported claims exposure related to retained deductible components.

In April 2010 and 2009, FICURMA made payments to members for a return of premium based upon the experience of its members related to all claims resolved as of November 2009 and 2008, respectively. These amounts were recorded as a reduction to insurance expense. Pursuant to the return of premium, the University and other member institutions executed debenture notes with FICURMA to allow FICURMA to continue to work independently of its members. The University provided funds in the amount of $100,000 and $910,000 to FICURMA in 2010 and 2009 respectively. The notes are recorded as temporarily restricted other assets in the accompanying consolidated statements of financial position. The notes bear interest at an annual rate equal to the annual aggregate rate of return on all of FICURMA’s invested capital, which equates to 1.52%. The principal amount of the $100,000 and $910,000 notes mature on April 30, 2020 and April 30, 2019, respectively.

- 11 -

Insurance expense related to the program totaled $2,324,107 and $2,302,510 in 2011 and 2010, respectively, and has been recorded in institutional support in the accompanying consolidated statements of activities.

The University is the owner and beneficiary of several life insurance policies with a recorded cash surrender value of $1,377,323 and $1,257,527 as of June 30, 2011 and 2010, respectively. These policies are recorded in prepaid expenses and other assets in the accompanying consolidated statements of financial position.

Tuition and Fee Revenue — The University recognizes tuition and fee revenue when persuasive evidence of an arrangement with a student exists, services have been delivered to the student, and related billings to the student are determinable and probable of collection. Amounts billed to students in advance are deferred and are recognized as revenue in the term in which the service is provided. The University has reduced its tuition and fee revenue by $45,961,723 and $42,488,295 for the years ended June 30, 2011 and 2010, respectively, to reflect University financial aid and discounts provided to assist students. Revenues and expenses related to summer sessions, which are conducted over the fiscal year end, are reported entirely within the fiscal year in which the session is predominantly conducted.

Contributions — Unconditional promises to give (pledges) are recognized as contribution revenue when the donor’s commitment is received. Pledges with payments due to the University in future periods are recorded as increases in temporarily restricted or permanently restricted net assets at the estimated present value of future cash flows net of an allowance for certain promises that are estimated as uncollectible. The discount rate used to measure the present value of the pledge receivable at the time of the gift is used throughout the life of the pledge. Amortization of the discount due to payments or changes in future payment schedules is recorded as an increase or decrease in contribution revenue and the pledge receivable balance.

Conditional promises are recorded when donor stipulations are substantially met. Conditional promises are considered to be available for general operations of the University, unless specifically restricted by the donor. The University reports gifts of cash and other assets as restricted support if they are received with donor stipulations that limit the use of the donated assets. When a donor restriction expires (that is, when a stipulated time restriction ends or the purpose of the restriction is accomplished), temporarily restricted net assets are reclassified to unrestricted net assets and reported in the accompanying consolidated statements of activities as net assets released from restrictions. Donor-restricted contributions received and collected and/or satisfied during the same year are recorded in the unrestricted net assets class.

Contributions Receivable from Trust — As of June 30, 2011 and 2010, included in contributions receivable from trust are $332,303 and $288,597, respectively, of contributions due to the University under charitable remainder trusts and gift annuities. Under these arrangements, the University is the trustee and is obligated to make periodic distributions to beneficiaries over the lifetime of the donor. The University receives the remaining assets of the trust at the time of the trust’s termination; the assets generally have donor stipulations and have been recorded as temporarily restricted net assets in the accompanying consolidated statements of financial position. A liability of $102,150 and $70,803 at June 30, 2011 and 2010, respectively, has been recorded within accounts payable and accrued expenses in the accompanying consolidated statements of financial position at the present value of the estimated future payments to be distributed over the donors’ expected lives related to these contributions.

Contributed Services — Certain religious members of the faculty and administration receive only a portion of their salary. The unpaid portion is contributed to the University for unrestricted use and is reported as unrestricted revenues and expenses.

- 12 -

Student Deposits — Student deposits consist of payments made by students before year-end for classes conducted after year-end to be recognized as revenues in future periods.

Deferred Revenue — During December 2000, the University sold its rights to future investment income for the next 20 years on amounts deposited in its Series 2000 Reserve Fund (see Notes 2 and 6), to a financial institution for proceeds totaling $928,000. In accordance with the Series 2000 Bonds (see Notes 2 and 6), the University maintains required funds in a debt service reserve fund. The University recorded the proceeds as deferred revenue and is amortizing such amount into income over 20 years. Additionally, deferred revenue as of June 30, 2011, includes funds received in advance for the University’s continuing medical education and education programs, as well as deferred program revenue from BarryTel.

Discount on Bonds — As described in Note 7, the University has entered into certain loan agreements with the Pinellas County Educational Facilities Authority (the “Authority”) related to the issuance of Revenue Refunding Bonds by the Authority in 1998, 2000, and 2007. The related bond discount totaling $263,674 and $277,982 as of June 30, 2011 and 2010, respectively, is amortized using the straight-line method over the life of the debt, which approximates the effective interest method. Bond discount amortization totaled $14,310 for the years ended June 30, 2011 and 2010, respectively.

Income Taxes — The University is a not-for-profit corporation and has been recognized as tax exempt pursuant to Section 501(c)(3) of the Internal Revenue Code (IRC). The IRC provides for taxation of unrelated business income under certain circumstances. Management has concluded that the University has no material unrelated business income.

The University follows the provisions of ASC 740, Income Taxes, and has determined that as of June 30, 2011 and 2010, the University had no material unrecognized tax benefits. The University does not expect that unrecognized tax benefits will materially increase within the next twelve months.

Derivative — The University entered into an interest rate swap agreement to manage the interest rate risk on its Series 2007 Bonds effective October 29, 2007. The fair value of the swap agreement has been recognized in the consolidated statements of financial position of the University, and it is included within other liabilities. Any changes in the fair value of the interest rate swap agreements are recorded as a component of interest expense in the consolidated statement of activities.

Fair Value of Financial Instruments — The fair values of financial instruments held by the University as June 30, 2011 and 2010, are based on a variety of factors and assumptions and may not necessarily be representative of the actual gains or losses that will be realized in the future and do not include expenses that could be incurred in an actual sale or settlement of such financial instruments. The carrying values for cash and cash equivalents, student accounts receivable, contributions receivable, other receivables, and accounts payable approximate fair values based on their short-term nature.

The University estimates the fair value of the NBC note receivable using a fair value measure based on estimated current rates for similar borrowings. The fair value of the note receivable was approximately $1,811,000 and $2,013,000 at June 30, 2011 and 2010, respectively (see Note 10).

The fair values of the University’s investments, which are the amounts reported in the statements of financial position, are based on quoted market prices, except for the investments in real estate and property which are based on market comparable values.

- 13 -

Loans, mortgage, notes payable and capital leases based on borrowing rates currently available to the University for debt with similar terms and maturities, have an estimated fair value of $77.4 million and $78.1 million as of June 30, 2011 and 2010, respectively.

Noncontrolling Interest — Noncontrolling interests presented in the consolidated statements of financial position reflect the original investment by these noncontrolling interests in the Partnership, along with their accumulated proportional share of the net earnings or losses of the Partnership, plus any contributions, less any dividend distributions. Increase in net assets attributable to noncontrolling interests in the consolidated statements of activities represents the noncontrolling portion of net income or loss that is attributable to the noncontrolling ownership interests in the Partnership.

2. INVESTMENTS

Investments and investments held for debt service as of June 30, 2011 and 2010, consist of the following:

Quoted Prices in SignificantActive Markets Other Significant

for Identical Observable UnobservableAssets Inputs Inputs

Description (Level 1) (Level 2) (Level 3) Total

Long-term certificate of deposits - $ 21,640$ - $ 21,640$ Corporate stock 8,570,250 8,570,250 Corporate bonds 10,394 10,394 Bond mutual funds 2,365,108 2,365,108 Real estate mutual funds 380,890 380,890 Commodities funds 556,183 444,799 1,000,982 U.S. government obligations 4,439,472 4,439,472 Government agency funds 146,557 146,557 Hedge funds 701,410 701,410 Land and buildings held for investment 8,165,000 8,165,000 Other investments 255,644 255,644

Total 12,018,988$ 4,916,305$ 9,122,054$ 26,057,347$

Fair Value Measurement at Reporting Date2011

Hedge Land and Buildings OtherFunds Held for Investment Investments

Beginning balance June 30, 2010 - $ 8,035,000$ 342,748$ Additions 616,385 Total realized/unrealized gains (losses) included in statement of activities 85,025 130,000 (87,104)

Ending balance June 30, 2011 701,410$ 8,165,000$ 255,644$

The amount of total gain or (losses) for the period included in changes in net assets attributable to the change in unrealized gains or losses relating to assets/liabilities still held at year-end 85,025$ 130,000$ (87,104)$

(Level 3)Significant Unobservable InputsFair Value Measurements Using

- 14 -

2010Fair Value Measurement at Reporting Date

Quoted Prices in SignificantActive Markets Other Significant

for Identical Observable UnobservableAssets Inputs Inputs

Description (Level 1) (Level 2) (Level 3) Total

Money market 165,261$ - $ - $ 165,261$ Long-term certificates of deposit 21,682 21,682 Corporate stock 6,774,234 6,774,234 Corporate bonds 10,473 10,473 Bond mutual funds 2,949,019 2,949,019 Real estate mutual funds 295,212 295,212 Commodities funds 825,113 825,113 U.S. government obligations 2,500,674 2,500,674 Government agency funds 212,877 212,877 Land and buildings held for investment 8,035,000 8,035,000 Other investments 342,748 342,748

Total 11,253,871$ 2,500,674$ 8,377,748$ 22,132,293$

Land and Buildings OtherHeld for Investment Investments

Beginning balance June 30, 2009 9,015,000$ 358,700$ Total realized/unrealized losses included in statement of activities (980,000) (15,952)

Ending balance June 30, 2010 8,035,000$ 342,748$

The amount of total gain or losses for the period included in changes in net assets attributable to the change in unrealized changes in net assets or losses relating to assets/liabilities still held at year-end (980,000)$ (15,952)$

Fair Value Measurements UsingSignificant Unobservable Inputs

(Level 3)

The University’s investments include debt and equity securities and certain other investments. Unrealized gains on these investments totaled $4,865,417 and $3,276,154 as of June 30, 2011 and 2010, respectively. The change in fair market value on these investments of $1,589,262 and $226,810 for the years ended June 30, 2011 and 2010, respectively, has been included within net realized and unrealized gains or losses on investments in the accompanying consolidated statements of activities. The University had a net gain of $708,597 for fiscal year 2011 and a net loss of $445,993 for fiscal year 2010, attributed to investments. The University incurred $71,051 of fees related to the management of the investments for the year ended June 30, 2011.

The University accounts for its investments categorized as Level 1 through the use of quoted market prices for those investments in debt and equity securities with readily determinable market values.

The University accounts for its investments categorized as Level 2 through the use of observable inputs other than quoted prices included in Level 1, such as quoted prices for similar assets and liabilities in active markets; quoted prices for identical or similar assets and liabilities in markets that are not active; or other inputs that are observable or can be corroborated by observable market data.

- 15 -

The University’s investments categorized as Level 2 consist of long term certificates of deposit, corporate bonds, commodities and US government obligations. The US government obligations are held in satisfaction of the Reserve Fund Requirement for the Series 1998 and 2000 Bonds, as described in Note 7. As of June 30, 2011 and 2010, the University had an established debt service reserve of $3,972,854 and $2,500,574 respectively. The reserve is held in U.S. government obligations. Such amount has been classified as an investment held for debt service reserve in the accompanying consolidated statements of financial position.

The University’s investments categorized as Level 3 consist of hedge funds, land and buildings held for investment and a collection of books related to theology, philosophy, religious studies, and supporting disciplines. The land and buildings held for investment include the Nursing and Rehabilitation Center, a nursing facility owned by the University and leased to a third party, the residence for the University’s president, the land investment in the Partnership, and an additional investment property leased to a third party.

The Nursing and Rehabilitation Center lease agreement is dated February 6, 1996, and amended November 6, 2000, April 8, 2003, and March 1, 2007. The lease period of the land and building expires January 31, 2021, and grants the lessee the option to renew the original term of the lease for one renewal period. The renewal period is to begin February 1, 2021, and expire January 31, 2032. The estimated fair value of the Nursing and Rehabilitation Center as of June 30, 2011 and 2010, was $6,150,000 and $6,000,000, respectively. For the years ended June 30, 2011 and 2010, the University recorded an unrealized gain on the fair value of this investment of $150,000 for fiscal year 2011 and an unrealized loss of $800,000 for fiscal year 2010. The valuation was based on an independent third-party appraisal using an income capitalization approach based on the value of the lease.

The University owns land as an investment and earns rental revenues through a ground lease arrangement as part of the Partnership. The land was valued at $1,000,000 as of June 30, 2011 and 2010. The University recorded no unrealized gain or loss on the investment for fiscal year 2011 and an unrealized loss of $80,000 on the investment for fiscal year 2010. The valuation was based on an independent third-party appraisal based on the market value of the leased fee interest.

The University acquired property designated for the University president’s residence for $529,892 as an investment in May 2004. The property was leased to the president commencing in July 2004 through June 30, 2008. In June 2008, the University acquired an additional investment property for $841,209 designated as the president’s residence. This property was valued at $575,000 and $595,000 as of June 30, 2011 and 2010, respectively. The University recorded an unrealized loss of $20,000 and $45,000 for the years ended June 30, 2011 and 2010, respectively.

The former residence is leased to a third party. This investment property is valued at $440,000 at June 30, 2011 and 2010, respectively. The University recorded an unrealized loss of $55,000 for the fiscal year ended June 30, 2010. No change in value was recorded for fiscal year ended June 30, 2011.

Valuations of both properties were based on an independent third-party appraisal using recent sales prices and other comparable properties within the geographic marketplace of the investments.

The University holds an investment in a private hedge fund. The hedge fund is valued at $701,410 as of June 30, 2011. The University recorded an unrealized gain on the investment of $85,025 for fiscal year 2011. The University estimated the fair value of the hedge funds primarily using the information provided by the fund manager and historical audited financial results of the hedge fund.

- 16 -

The components of investment return in the accompanying consolidated statements of activities for the years ended June 30, 2011 and 2010, are summarized as follows:

2011Temporarily Permanently

Unrestricted Restricted Restricted Total

Investment income: Dividends 232,041$ - $ - $ 232,041$ Interest 136,440 136,440

Total investment income 368,481 - - 368,481

Net realized and unrealized gain on investments 2,226,809 2,226,809 Rental income from investments 724,316 724,316

Total 3,319,606$ - $ - $ 3,319,606$

Temporarily PermanentlyUnrestricted Restricted Restricted Total

Investment income: Dividends 204,201$ - $ - $ 204,201$ Interest 106,169 106,169

Total investment income 310,370 - - 310,370

Net realized and unrealized loss on investments (268,394) (268,394) Rental income from investments 704,172 704,172

Total 746,148$ - $ - $ 746,148$

2010

The University has a 35% interest in SFITV and accounts for the related transactions in accordance with the equity method of accounting. The equity method of accounting dictates that an investor initially records an investment in the stock of an investee at cost, and adjusts the carrying amount of the investment to recognize the investor’s share of the earnings or losses of the investee after the date of acquisition. The University’s initial investment was nominal, and SFITV had no activity prior to fiscal year 2009.

On July 24, 2008, SFITV entered into a long-term lease with an unrelated entity, whereby the entity leases three broadband channels from SFITV through December 2016, with additional renewal options requiring Federal Communications Commission (FCC) approval. Under the terms of the lease, SFITV received a $3 million initial payment and will receive annual lease payments that escalate from $378,000 in the first year to $858,000 in the final year. Total payments that will be received under the long-term lease are $7.75 million. SFITV is recognizing the revenues earned from the long-term lease on a straight-line basis over the term of the lease. During fiscal year 2011, SFITV recognized $930,000 of revenues and presented deferred revenues of $1.39 million as of June 30, 2011. During fiscal year 2010, SFITV recognized $930,000 of revenues and presented deferred revenues of $1.96 million as of June 30, 2010. As of and for the years ended June 30, 2011 and 2010, SFITV has no assets, liabilities, or operating activities, except as described above.

- 17 -

During fiscal years 2011 and 2010, the University’s cumulative portion of SFITV’s net income amounted to approximately $922,250 and $596,750, respectively. The University has received cumulative cash distributions of approximately $1.8 million from SFITV. Such distributions are not refundable, and the University is not liable for obligations of SFITV or committed to provide financial support. As such, the University recorded $113,477 and $119,000 as earnings of an equity method investee in the accompanying consolidated statements of activities for 2011 and 2010, respectively.

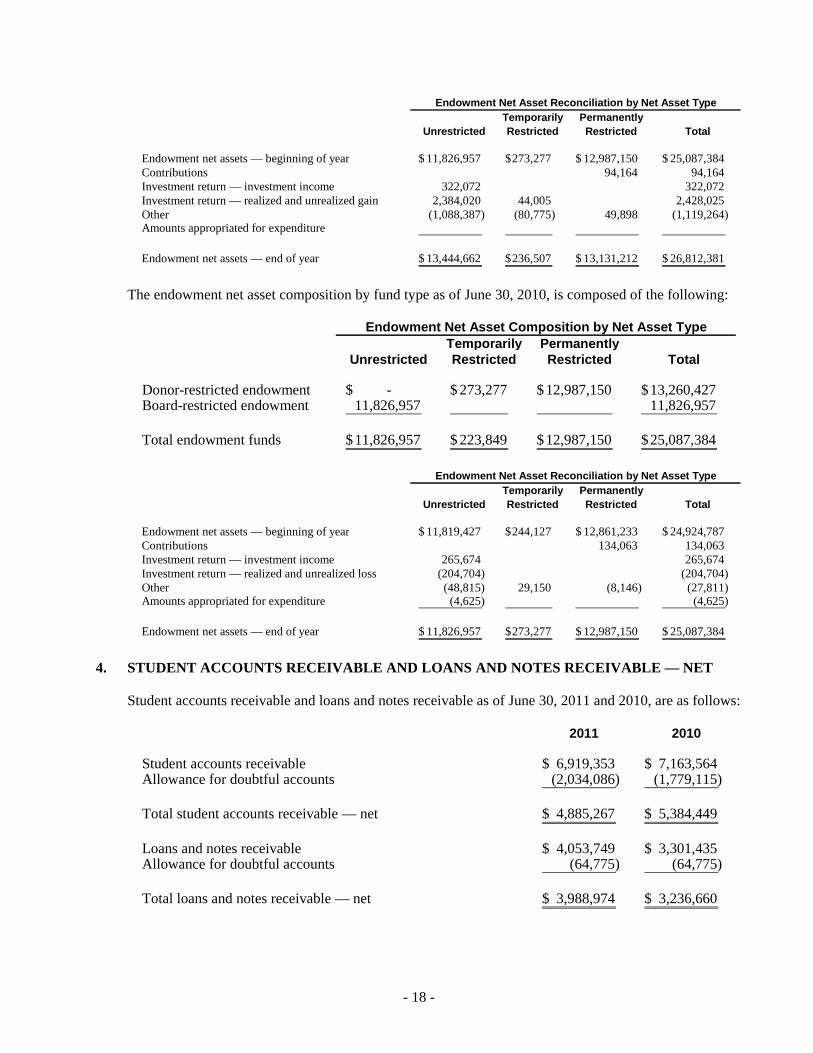

3. ENDOWMENT INVESTMENTS

Endowment investments, presented at fair value, are composed of unrestricted endowments, temporarily restricted endowments, and permanent endowments. Unrestricted endowments are restricted by the University’s board. The board can appropriate as much of the net appreciation on board-designated endowments as is prudent considering the University’s present and anticipated financial requirements, expected total return on its investments, price-level trends, and general economic conditions. Temporarily restricted endowments consist of funds limited by donor-imposed stipulations that either expire by the passage of time or that can be fulfilled or removed by actions of the University pursuant to those stipulations. Permanent endowments consist of donor-restricted funds whose use by the University is limited by donor-imposed stipulations that neither expire with the passage of time nor can be fulfilled or otherwise removed by actions of the University. As required by accounting principles generally accepted in the United States of America, net assets associated with endowment funds are classified and reported based on the existence or absence of donor-imposed restrictions.

The University requires the preservation of the original value of any donor-restricted gift, as of the gift date, absent explicit donor stipulations to the contrary. As a result, the University classifies as permanently restricted net assets the original value of gifts donated as permanent endowment. The income derived from permanent endowment investments, which is expendable to support the various programs sponsored by the University in accordance with the donor’s wishes, is classified as unrestricted or temporarily restricted net assets, in accordance with the donor’s wishes.

The University has developed an investment policy for all of its investable assets whose general purpose is to preserve the capital and purchasing power of the University and to provide sufficient investment return for current and future spending needs. The University has adopted a total return strategy that is designed to provide balance to the overall structure of the University’s investment program over a long-term period. The endowment net asset composition by fund type as of June 30, 2011, is composed of the following:

Temporarily PermanentlyUnrestricted Restricted Restricted Total

Donor-restricted endowment - $ 236,507$ 13,131,212$ 13,367,719$ Board-restricted endowment 13,444,662 13,444,662

Total endowment funds 13,444,662$ 236,507$ 13,131,212$ 26,812,381$

Endowment Net Asset Composition by Net Asset Type

- 18 -

Temporarily PermanentlyUnrestricted Restricted Restricted Total

Endowment net assets — beginning of year 11,826,957$ 273,277$ 12,987,150$ 25,087,384$Contributions 94,164 94,164 Investment return — investment income 322,072 322,072 Investment return — realized and unrealized gain 2,384,020 44,005 2,428,025 Other (1,088,387) (80,775) 49,898 (1,119,264) Amounts appropriated for expenditure

Endowment net assets — end of year 13,444,662$ 236,507$ 13,131,212$ 26,812,381$

Endowment Net Asset Reconciliation by Net Asset Type

The endowment net asset composition by fund type as of June 30, 2010, is composed of the following:

Temporarily PermanentlyUnrestricted Restricted Restricted Total

Donor-restricted endowment - $ 273,277$ 12,987,150$ 13,260,427$ Board-restricted endowment 11,826,957 11,826,957

Total endowment funds 11,826,957$ 223,849$ 12,987,150$ 25,087,384$

Endowment Net Asset Composition by Net Asset Type

Temporarily PermanentlyUnrestricted Restricted Restricted Total

Endowment net assets — beginning of year 11,819,427$ 244,127$ 12,861,233$ 24,924,787$Contributions 134,063 134,063 Investment return — investment income 265,674 265,674 Investment return — realized and unrealized loss (204,704) (204,704) Other (48,815) 29,150 (8,146) (27,811) Amounts appropriated for expenditure (4,625) (4,625)

Endowment net assets — end of year 11,826,957$ 273,277$ 12,987,150$ 25,087,384$

Endowment Net Asset Reconciliation by Net Asset Type

4. STUDENT ACCOUNTS RECEIVABLE AND LOANS AND NOTES RECEIVABLE — NET

Student accounts receivable and loans and notes receivable as of June 30, 2011 and 2010, are as follows:

2011 2010

Student accounts receivable 6,919,353$ 7,163,564$ Allowance for doubtful accounts (2,034,086) (1,779,115)

Total student accounts receivable — net 4,885,267$ 5,384,449$

Loans and notes receivable 4,053,749$ 3,301,435$ Allowance for doubtful accounts (64,775) (64,775)

Total loans and notes receivable — net 3,988,974$ 3,236,660$

- 19 -

5. CONTRIBUTIONS RECEIVABLE — NET

Outstanding pledges receivable are from various individuals, foundations, and corporations. The discounted present values of pledges receivable are computed using expected payout periods, an average risk-free interest rate in effect as of the date of the pledge, and an estimated allowance for uncollectible pledges, using specific experience factors. Contributions receivable as of June 30, 2011 and 2010, are summarized as follows:

2011 2010

Pledges due: Less than one year 263,500$ 916,000$ One year to five years 1,434,622 3,431,233 Greater than five years 1,865,988 83,988

3,564,110 4,431,221

Less unamortized discount (738,080) (495,324) Allowance for uncollectible accounts (488,172)

Total contributions receivable — net 2,826,030$ 3,447,725$

In March 2008, the University was notified that it received a bequest that consisted of interests in two perpetual trust funds. Since that time the trust funds have been subject to legal proceedings pending a final resolution. On August 18, 2011, the Surrogate’s Court of New York entered an order confirming the University’s entitlement to the interest in the perpetual trust funds. As a result, the University anticipates receiving disbursements of five percent (5%) of the average value of the funds on an annual basis plus payments in arrears to March 2008, the date of the bequest. As of June 30, 2011 no corresponding amounts have been included in the University’s consolidated financial statements.

6. PROPERTY, PLANT, AND EQUIPMENT — NET

Property, plant, and equipment as of June 30, 2011 and 2010, consists of the following:

2011 2010

Land 6,711,877$ 7,848,877$ Land improvements 4,850,947 4,649,019 Building and building improvements 108,366,457 106,590,054 Furniture, fixtures, and equipment 36,523,368 38,626,535 Law library acquisitions 6,492,717 6,492,717 Construction in progress 9,357,970 1,214,552

Total property, plant, and equipment 172,303,336 165,421,754

Less accumulated depreciation and amortization (76,153,505) (75,144,075)

Property, plant, and equipment — net 96,149,831$ 90,277,679$

- 20 -

Depreciation and amortization expense on property, plant, and equipment totaled $5,329,234 and $5,073,712 for the years ended June 30, 2011 and 2010, respectively. The estimated cost to complete for construction in progress as of June 30, 2011 and 2010, totaled $14,471,163 and $7,537,725, respectively. The increase is primarily related to the construction of a new dormitory and law school building.

On May 25, 2011 the licenses and related assets of BarryTel’s radio operations were sold to a third party. All of the related costs of property, plant and equipment asset and related accumulated depreciation were removed from the consolidated financial statements as of June 30, 2011.

BarryTel, as a result of the sale of WXEL-FM, determined that it was appropriate to assess the recoverability of the remaining property, plant, and equipment. The carrying value of BarryTel’s remaining property, plant and equipment, was compared to the amount of future net undiscounted cash flows expected to be generated by the long-lived assets. The total carrying value of the property, plant and equipment exceeded such cash flows, and were considered to be impaired. During June 2011, BarryTel performed a fair value analysis of its property, plant and equipment and concluded that the impairment of its property, plant and equipment, was necessary. The fair value of the property, plant and equipment was determined through the use of a market approach, using the current agreement to sell the remaining operations of BarryTel. (See Note 11). As a result, long-lived assets held and used with a carrying amount of $3,849,786 were impaired to their fair value of zero, resulting in an impairment charge of such amount, which is recognized in the statement of activities for the year ended June 30, 2011.

- 21 -

7. LOANS, MORTGAGE, NOTES PAYABLE, AND CAPITAL LEASES

2011 2010Loans payable: 1998 Loan Agreement with Pinellas County Educational Facilities Authority Revenue and Revenue Refunding Bonds, annual principal payments made; semiannual interest payments due each April and October through 2028; variable interest rate commencing at 5.375% and increasing to 5.5%; the effective interest rate at June 30, 2011 and 2010, was 5.31% and 5.37%, respectively 16,880,000$ 17,425,000$ 2000 Loan Agreement with Pinellas County Educational Facilities Authority Revenue Bonds, annual principal payments made; semiannual interest payments due each April and October through 2030; variable interest rate commencing at 4.7% and increasing to 6.25%; the effective interest rate at June 30, 2011 and 2010, was $5.8 % 23,045,000 23,570,000 2007 Loan Agreement with Pinellas County Educational Facilities Authority Revenue and Refunding Bonds, annual payments due each October with a variable interest rate equal to London InterBank Offered Rate (LIBOR) plus 1.50% settled monthly; the effective rate at June 30, 2011 and 2010, was 3.91%. 9,005,000 9,340,000 Less — discount on Series 2000 Bonds (220,211) (231,857) Less — discount on Series 2007 Bonds (43,463) (46,125)

Total loans payable 48,666,326 50,057,018

Mortgage, notes payable, and capital leases: Bank of America Term Loan in the amount of $7 million, subject to terms of Loan Agreement dated March 11, 2010; interest payments due monthly commencing April 5, 2010; variable interest rate equal to the LIBOR rate plus 1.65% per annum; principal balance shall be repaid in installments commencing March 5, 2011, with the full balance and interest due March 5, 2014. The effective interest rate at June 30, 2011 and 2010 was 1.84%. The loan was retired on August 2, 2011. 6,930,296 7,000,000 Bank of America Term Loan in the amount of $5.2 million, subject to terms of loan agreement dated February 24, 2009 maturing March 5, 2014; interest and principal payments due monthly, commencing June 5, 2009; variable interest equal to the LIBOR rate plus 1.650%. The effective interest rate at June 30, 2011 and 2010 was 1.84% and 2.0%. The loan was retired on August 2, 2011 4,970,617 5,083,605 Public Broadcasting Service Dues Payment Plan Agreement and Promissory Note; monthly payments commencing November 1, 2009, and ending October 1, 2010. The payment plan was paid in full in October 2010. 303,128 First American Equipment Finance Lease Agreement for NetAPP Hardware; monthly payments commencing February 1, 2009, for 36 months; effective interest rate at June 30, 2011, was 5.1% 27,309 72,974 All American Investment Financing Agreement for modular building on law school campus; monthly payments commencing June 1, 2008, for 35 months; the effective interest rate at June 30, 2010 was 8.4%. 81,699 CSI Leasing Inc. Agreement Phase II for Computer Equipment Monthly payments commencing May 2, 2011 for 360 months. Effective interest rate at June 30, 2011 was 2.0% 272,487 CSI Leasing Inc. Lease Agreement Phase I for Computer Equipment Monthly payments commencing April 1, 2011 for 36 months. Effective interest rate at June 30, 2011 was 2.5% 59,874

Total mortgage, notes payable, and capital leases 12,260,583 12,541,406

Total loans, mortgage, notes payable, and capital leases 60,926,909$ 62,598,424$

Series 1998 Bonds — On July 29, 1998, the Authority issued $22,000,000 of Pinellas County Educational Facilities Authority Revenue and Revenue Refunding Bonds, Series 1998 (“Series 1998 Bonds”). The proceeds of the sale of the Series 1998 Bonds have been loaned to the University (the “1998 Loan”) to (i) finance the costs of acquiring, constructing, and equipping certain educational facilities to be owned and operated by the University; (ii) pay in full the University’s loan with the Authority in connection with the Revenue Bonds, Series 1992A in the aggregate principal amount of $12,290,000, previously issued by the Authority for the benefit and on behalf of the University, (iii) purchase a reserve fund credit facility for deposit to the credit of the reserve fund in satisfaction of the reserve requirement for the Series 1998 Bonds; and (iv) pay certain costs of issuance of the Series 1998 Bonds.

Series 1998 Debt Service Reserve — A debt service reserve fund was established pursuant to the trust indenture under which the Series 1998 Bonds were issued to secure to secure such Bonds. At the time of issuance of the Series 1998 Bonds, the University deposited into the debt service reserve fund, a debt service reserve fund surety policy (the “Reserve Policy”) issued by ACA Financial Guaranty Corp.

- 22 -

(“ACA”) in an amount equal to the debt service reserve requirement (the “Reserve Requirement”) established by the bond indenture. The University agreed in the Loan Agreement, pursuant to which the proceeds of the Series 1998 Bonds were loaned to the University, that if the rating of ACA dropped below “A” by Moody’s Investors Service, Inc. or Fitch Ratings that the University would either substitute the Reserve Policy with a substitute policy issued by a provider satisfying the rating requirements under the Loan Agreement or to cash fund the debt service reserve fund in an amount equal to the Reserve Requirement. On June 17, 2011 the University deposited $1,471,181 into a debt service reserve fund which equaled the Reserve Requirement under the trust indenture securing the Series 1998 Bonds.

Series 2000 Bonds — On November 29, 2000, the Authority issued $27,000,000 of Pinellas County Educational Facilities Authority Revenue Bonds, Series 2000 (“Series 2000 Bonds”). The proceeds of the sale of the Series 2000 Bonds have been loaned to the University (the “2000 Loan”) to (i) finance the cost of acquiring, constructing, and equipping certain educational facilities to be owned and operated by the University, including, without limitation, to reimburse the University for a portion of such costs previously advanced by the University, (ii) make a deposit to the Series 2000 Reserve Fund in satisfaction of the Series 2000 Reserve Fund Requirement for the Series 2000 Bonds; (iii) pay a portion of the interest that was coming due on the Series 2000 Bonds through June 1, 2002; and (iv) pay certain costs of issuance of the Series 2000 Bonds.

Series 2007 Bonds — On October 24, 2007, the Authority issued $10,000,000 of Pinellas County Educational Facilities Authority Revenue and Revenue Refunding Bonds, Series 2007 (“Series 2007 Bonds”). The proceeds of the sale of the Series 2007 bonds have been loaned to the University (the “2007 Loan”) to (i) fund the construction of a building for the Institute for Community Health & Minority Medicine and related improvements of the University campus; (ii) refund a taxable loan dated May 7, 2004, from Bank of America, N.A. (the “Bank”), to the University in the original amount of $7,300,000; and (iii) pay certain costs of issuance of the Series 2007 Bonds.

Pursuant to the supplemental loan agreement between the University and the Authority, Barry University is solely responsible for all payments due under Series 2007 Bonds. The Series 2007 Bonds mature October 1, 2037. The Series 2007 Bonds are variable rate obligations secured by an irrevocable, direct pay, letter of credit issued by the Bank on behalf of the University for the benefit of bondholders, which expires on October 15, 2011. The University is responsible for reimbursing the Bank for all draws under the letter of credit. The 2007 Loan Agreement is subject to certain covenants and financial ratios specified in the Master Trust Indenture (the “Indenture”) and supplemental indenture, as amended.

In connection with the bond issue, the University entered into an interest rate swap agreement with the Bank to manage the interest rate risk on its Series 2007 Bonds in an initial notional amount of $10,000,000, effective October 29, 2007. The agreement swaps the University’s variable rate for a fixed rate of 3.9%. The notional amount declines over time and terminates on October 1, 2027. The University began making payments under the agreement on December 1, 2007. The University has recorded the fair value of the swap agreement as of June 30, 2011 and 2010, as a liability in the amount of $922,386 and $997,460, respectively, within other liabilities in its consolidated statements of financial position, and the change in fair value as interest expense within its consolidated statements of activities. The fair market value classification of the swap agreement is Level 2.

The University is required to make loan payments in amounts sufficient for the Authority to pay the principal and interest on the Series 1998, Series 2000, and Series 2007 Bonds, whether at maturity, upon acceleration, or upon redemption, and to maintain the required amount in the reserve fund established under the Indenture.

- 23 -

Debt Restrictions — Pursuant to the Indenture and supplemental loan agreement between the Authority and the University, the 1998 Loan, 2000 Loan, and 2007 Loan, include certain quantitative covenants that require the University to maintain specified financial ratios and levels of working capital, as well as certain qualitative covenants. As of June 30, 2011 and 2010, management believes that the University was in compliance with all financial and nonfinancial covenants under the terms of the Indenture.

The annual principal maturities for loans, mortgages, notes payable, and capital leases as of June 30, 2011, are as follows:

Years Ending Loans Notes CapitalJune 30 Payable Payable Leases Total

2012 1,475,000$ 331,464$ 123,863$ 1,930,327$ 2013 1,550,000 348,282 96,553 1,994,835 2014 1,640,000 11,221,165 90,914 12,952,079 2015 1,735,000 61,667 1,796,667 2016 1,830,000 1,830,000 2017 and thereafter 40,700,000 40,700,000

Total 48,930,000 11,900,911 372,997 61,203,908

Less discount on Series 2000 Bonds (220,211) (220,211) Less discount on Series 2007 Bonds (43,463) (43,463) Less amounts for interest expense (13,325) (13,325)

Total 48,666,326$ 11,900,911$ 359,672$ 60,926,909$

Interest costs expensed during fiscal years 2011 and 2010 were $2,849,512 and $2,861,784, respectively. Capitalized interest totaled $39,556 in fiscal year 2011.

Subsequent Events — On August 2, 2011, the Authority issued $38,575,000 of Pinellas County Educational Facilities Authority Revenue and Revenue Refunding Bonds, Series 2011 (“Series 2011 Bonds”). The proceeds of the sale of the Series 2011 bonds have been loaned to the University (the “2011 Loan”) to (i) finance the cost of acquisitions, construction and equipping of certain educational facilities and other capital improvements to be owned and operated by the University and to reimburse advances made by the University to pay a portion of such costs, (ii) refinance certain obligations of the University which were used to finance the acquisition, construction and improvements to certain educational facilities of the University, (iii) make a deposit in an amount equal to the Series 2011 Reserve Fund Requirement to the 2011 Reserve Fund established for the Series 2011 Bonds, (iv) pay a portion of the interest coming due on the Series 2011 Bonds through August 1, 2012, and (v) pay certain costs of issuance of the Series 2011 Bonds.

On October 1, 2011 the University refunded the par value of $6,650,000 of the Series 2000 bonds maturing on October 1, 2015 and October 1, 2020. The refunded bonds were called for redemption at a redemption price equal to 100% of the principal amount together with interest accrued to the redemption date of October 1, 2011. Upon delivery of the Series 2011 Bonds on August 2, 2011 $6,849,572 was placed in an irrevocable escrow deposit trust fund held by the bond trustee as Escrow Agent until the redemption date. This amount included $6,650,000 for principal and $199,572 of interest.

- 24 -

As referenced above, certain proceeds of the Series 2011 bond issuance were used to refinance certain existing debt. On August 2, 2011 the outstanding principal balances of $6,912,870 for the Bank of America $7 million term loan for the construction on the law school campus and $4,960,761 for the Bank of American $5.2 million term loan for the purchase of an apartment complex for student housing were repaid.

The annual principal maturities for the Series 2011 Bonds are as follows:

Years EndingJune 30

20122013 800,000$ 2014 1,105,000 2015 1,155,000 2016 1,205,000 2017 and thereafter 34,310,000

38,575,000$

8. NET ASSETS

Unrestricted net assets attributable to the controlling and noncontrolling interests as of June 30, 2011 and 2010, are as follow:

Controlling NoncontrollingUnrestricted Net Assets Total Interest Interest

Balance — June 30, 2009 58,702,262$ 58,275,167$ 427,095$

Increase in net assets 11,651,645 11,651,645 Decrease in net assets attributed to noncontrolling interest (30,560) (30,560)

Change in unrestricted net assets 11,621,085 11,651,645 (30,560)

Balance — June 30, 2010 70,323,347 69,926,812 396,535

Increase in net assets 11,582,387 11,582,387 Increase in net assets attributed to noncontrolling interest 33 33

Change in unrestricted net assets 11,582,420 11,582,387 33

Balance — June 30, 2011 81,905,767$ 81,509,199$ 396,568$

- 25 -

Temporarily restricted net assets as of June 30, 2011 and 2010, are available for the following purposes:

2011 2010

Educational and general expenses 4,177,830$ 4,648,790$Scholarships 1,819,520 1,802,955 Student loan funds 94,815 191,052

Total 6,092,165$ 6,642,797$

As of June 30, 2011 and 2010, the University has temporarily restricted net assets totaling $2,826,030 and $3,447,725, respectively, for educational and general expenses, which will be funded through outstanding pledges due in future periods.

Net assets were released from restrictions by incurring expenses satisfying the restricted purposes or by the occurrence of other events specified by donors. As described in Note 1, donor-restricted contributions whose restrictions are met in the same reporting period are reported as unrestricted support. Net assets released from restrictions by function for the years ended June 30, 2011 and 2010, were as follows:

2011 2010

Educational and general 630,370$ 322,672$Scholarships 375,475 346,642

Total 1,005,845$ 669,314$

9. RETIREMENT PLAN

The University has a defined contribution retirement annuity program (the “Retirement Plan”) for personnel. The program is administered by a third party and is funded by individual annuity contracts, with the University contributing up to 9.5% of the employee’s salary. The University’s contribution to the Retirement Plan was $4,578,118 and $4,072,780 for 2011 and 2010, respectively.

10. NATIONAL BROADCASTING COMPANY (NBC) STATIONS MANAGEMENT INC. DIGITAL TV SETTLEMENT

On May 20, 2002, BarryTel and an unrelated third party finalized a settlement with NBC, which resulted in BarryTel accepting minimal signal interference resulting from digital television construction permit applications and allowed NBC to apply for a digital television channel redesignation with the FCC.

BarryTel and NBC’s applications, along with NBC’s channel redesignation, were granted by the FCC. The FCC’s approval of the agreement was finalized on February 19, 2003.

Under the agreement, the University received or will receive the following compensation totaling $7,700,000 from NBC:

a. Six million, four hundred thousand dollars ($6,400,000) as follows:

i. Two million dollars ($2,000,000) payable upon closing, which was collected on February 19, 2003.

- 26 -

ii. Four million, four hundred thousand dollars ($4,400,000) via promissory note ($293,333 per year for 15 years starting June 1, 2004). The promissory note was recorded at its present value of $2,629,975 at June 30, 2003, and is included in receivables in the accompanying consolidated statements of financial position.

b. One million, three hundred thousand dollars ($1,300,000) of spot time and program time to be used by Barry University on the facilities of Station WTVJ, Channel 6, and Station WSCV, Channel 51, Fort Lauderdale, during the period commencing on the closing date (February 25, 2003) and ended on the fifth anniversary (February 25, 2008). The University recognized the contributed advertising spots in revenue and expense, as the spots were aired on NBC. The University has exhausted all $1.3 million of the spot and program time as of June 30, 2008.

The carrying value of the promissory note will accrete to its maturity value over the life of the note using the effective interest method. The promissory note totaled $1,576,511 and $1,745,074 as of June 30, 2011 and 2010, respectively. Interest income recorded on the promissory note totaled $124,770 and $136,164 for the years ended June 30, 2011 and 2010, respectively, and has been recorded in other income in the accompanying consolidated statements of activities.

11. SALE OF BARRYTEL’S RADIO AND TELEVISION OPERATIONS

On April 20, 2010, the University’s Board of Trustees approved a resolution to sell the licenses and related assets of BarryTel’s radio station (WXEL-FM) to an unrelated third party. On May 16, 2011, the sale of WXEL-FM was approved by the Federal Communications Commission. On May 25, 2011, the sale was completed.

The carrying value of the operating assets, liabilities and equipment of WXEL-FM was $26,709, $83,133, and $236,851, respectively. The sale of WXEL-FM was for total consideration of $3,721,407. The consideration consisted of cash of $3,543,936 and advertising of $177,471. The advertising is to be used over a three year period commencing September 2011. The sale resulted in a gain of $3,529,615 that has been recorded in the statement of activities and is included in the results from discontinued operations.

Discontinued Operations 2011 2010

Revenue and other support 2,074,022$ 2,031,809$BarryTel expenses 1,702,310 2,006,093

Increase in unrestricted net assets from discontinued operations 371,712$ 25,716$

In June 2011, the University entered into a letter of intent to sell BarryTel’s television operations to a third party. The completion of the sale is subject to approval of the State Board and the Federal Communications Commission. To date, the University has not received regulatory approval for the sale and management believes that approval is uncertain. BarryTel has not classified the net assets related to its television operations as held for sale in the accompanying statement of financial position as management does not believe that it is probable the sale will be consummated within one year.

- 27 -

12. COMMITMENTS AND CONTINGENCIES

Operating Leases — The University leases space at various locations to provide off-campus programs. The University also leases certain information technology (e.g., computers, routers, and storage) as part of a technology refresh program. BarryTel has noncancelable operating leases for its television, transmitter site, and other operating equipment.

The schedule by years of future minimum lease payments under operating leases that have initial or remaining noncancelable lease terms in excess of one year as of June 30, 2011, is as follows:

Years EndingJune 30

2012 2,516,624$2013 2,170,488 2014 1,795,443 2015 1,382,387 2016 742,027 2017 and thereafter 458,522

9,065,491$

Rent expense amounted to $2,975,263 and $3,032,634 in 2011 and 2010, respectively.

Litigation — The University is, at times, subject to threatened or filed legal action. Based upon counsel’s advice and its knowledge of these cases, management does not expect the outcome of these matters to have a material adverse effect on the University’s future financial condition, results of activities, or cash flows. However, there can be no assurances regarding the ultimate outcome of these matters.

Guarantee — On August 30, 1999, the University entered into a guarantee agreement with Educational Services of the South, Inc., wherein the University unconditionally and irrevocably guaranteed the full and timely payment of all principal of and interest on, and fees and charges with respect to, each credit-based loan for students attending the University’s law program covered under the guaranty agreement. The balances of such loans outstanding amounted to $158,263 and $238,052 in 2011 and 2010, respectively.

Grants — Barry University and BarryTel receive state and federal grant funding in support of their respective educational missions. Grants are subject to annual renewal and periodic amendment and require the fulfillment of certain conditions as set forth in each instrument of grant. Failure to fulfill the conditions could result in the return of the funds to grantors. Management believes that Barry University and BarryTel have met all conditions under their grant programs.

Certain items of BarryTel’s broadcasting equipment were purchased with federal grant funds. As a result, governmental agencies have a priority lien on such equipment for 10 years from the various dates of acquisition. Such equipment, at cost, totaled $1,812,867 and $2,768,120 as of June 30, 2011 and 2010, respectively, and is included in property, plant, and equipment in the accompanying consolidated statements of financial position. Capital expenditures for buildings and equipment made by the University with federal grant funds, at cost, totaled $5,917,556 and $5,288,725 as of June 30, 2011, and 2010, respectively, and is included in property, plant, and equipment in the accompanying consolidated statements of financial position.

* * * * * *

- 28 -

SUPPLEMENTAL SCHEDULE

- 29 -

BARRY UNIVERSITY AND SUBSIDIARIES

SUPPLEMENTAL SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS AND STATE PROJECTS AND FINANCIAL ASSISTANCE PROGRAMSYEAR ENDED JUNE 30, 2011

Pass-ThroughFederal Entity Identifying Federal

Federal Grantor/Pass-Through CFDA Number or Awards Transfers toGrantor/Program or Cluster Title Number Contract Number Expenditures Subrecipients

Student Financial Aid — Cluster: U.S. Department of Education: Academic Competitiveness Grant (ACG) 84.375 P375A0101246 200,657$ - $ National Science and Mathematics Access to Retain Talent (SMART) 87.376 P376S101246 217,000 Teacher Education Assistance for College and Higher Education (TEACH) 84.379 P379T111246 114,500 Federal Pell Grant Program 84.063 P063P101246 11,708,353 Federal Supplemental Educational Opportunity Grant (FSEOG) 84.007 P007A100857 571,269 Federal Work-Study Program 84.033 P0033A100857 1,959,760 Federal Perkins Loan Program (Note 2) 84.038 N/A 115,030 Federal Direct Student Loans (Note 2) 84.268 P268K101246 146,305,443

Total U.S. Department of Education 161,192,012 -