Barloworld Limited Limited Domicile South ... construction and motor related industries ... exposing...

9

CORPORATES CREDIT OPINION 30 June 2017 New Issue RATINGS Barloworld Limited Domicile South Africa Long Term Rating Baa3 Type LT Issuer Rating - Dom Curr Outlook Negative Please see the ratings section at the end of this report for more information. The ratings and outlook shown reflect information as of the publication date. Contacts Dion Bate 27-11-217-5472 VP-Senior Analyst [email protected] David G. Staples 971-4237-9562 MD-Corporate Finance [email protected] Barloworld Limited Update of Key Credit Factors Following Sovereign Rating Action Summary Rating Rationale The Baa3/Aa1.za issuer ratings recognise Barloworld Limited's (Barloworld) leading competitive positions in the markets it operates in and is supported by strong brand offerings and stable long term relationships with its principal suppliers. The rating also considers Barloworld’s diversified product mix and its resilient business model whereby its integrated after sales support segments are able to soften the impact from the decline in new equipment and vehicle sales during cyclical downturns. Barloworld’s credit metrics have historically been relatively stable and are supported by the company’s ongoing commitment to balanced financial policies. While adjusted debt/EBITDA of 2.2x is strongly positioned within the rating category, Barloworld’s EBIT/interest expense cover of 3.2x and operating margin of 6.8% are weakly positioned (as of the last twelve months (LTM) to 31 March 2017) leaving it susceptible to weaker operating performance and a rising interest rate environment. Ratings also consider Barloworld's good liquidity position resulting from its favourable debt maturity profile. The rating is constrained by Barloworld’s exposure to (1) the Sub-Saharan African and Russian markets, leaving it exposed to the weak economic conditions of these countries; and (2) more cyclical mining, agricultural, construction and motor related industries which are currently experiencing prolonged depressed global commodity prices and weaker local consumer environments. In addition, Barloworld is exposed to key supplier risk as most of its operations depend on its position as the principal agent for a number of high profile brands such as Caterpillar Inc. This is mitigated by its long term relationships and close strategic alignment as well as, in some cases, its fixed term contractual agreements with its principals, which we expect to continue. Credit Strengths » Leading market positions supported by strong brand offerings » Resilient operating cash flows underpinned by integrated business model and diversified product mix » Relatively stable credit metrics through the cycle underpinned by balanced financial policies » Good liquidity profile

Transcript of Barloworld Limited Limited Domicile South ... construction and motor related industries ... exposing...

CORPORATES

CREDIT OPINION30 June 2017

New Issue

RATINGS

Barloworld LimitedDomicile South Africa

Long Term Rating Baa3

Type LT Issuer Rating - DomCurr

Outlook Negative

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Contacts

Dion Bate 27-11-217-5472VP-Senior [email protected]

David G. Staples 971-4237-9562MD-Corporate [email protected]

Barloworld LimitedUpdate of Key Credit Factors Following Sovereign RatingAction

Summary Rating RationaleThe Baa3/Aa1.za issuer ratings recognise Barloworld Limited's (Barloworld) leadingcompetitive positions in the markets it operates in and is supported by strong brandofferings and stable long term relationships with its principal suppliers. The rating alsoconsiders Barloworld’s diversified product mix and its resilient business model whereby itsintegrated after sales support segments are able to soften the impact from the decline innew equipment and vehicle sales during cyclical downturns. Barloworld’s credit metrics havehistorically been relatively stable and are supported by the company’s ongoing commitmentto balanced financial policies. While adjusted debt/EBITDA of 2.2x is strongly positionedwithin the rating category, Barloworld’s EBIT/interest expense cover of 3.2x and operatingmargin of 6.8% are weakly positioned (as of the last twelve months (LTM) to 31 March2017) leaving it susceptible to weaker operating performance and a rising interest rateenvironment. Ratings also consider Barloworld's good liquidity position resulting from itsfavourable debt maturity profile.

The rating is constrained by Barloworld’s exposure to (1) the Sub-Saharan African andRussian markets, leaving it exposed to the weak economic conditions of these countries;and (2) more cyclical mining, agricultural, construction and motor related industries whichare currently experiencing prolonged depressed global commodity prices and weaker localconsumer environments. In addition, Barloworld is exposed to key supplier risk as most of itsoperations depend on its position as the principal agent for a number of high profile brandssuch as Caterpillar Inc. This is mitigated by its long term relationships and close strategicalignment as well as, in some cases, its fixed term contractual agreements with its principals,which we expect to continue.

Credit Strengths

» Leading market positions supported by strong brand offerings

» Resilient operating cash flows underpinned by integrated business model and diversifiedproduct mix

» Relatively stable credit metrics through the cycle underpinned by balanced financialpolicies

» Good liquidity profile

MOODY'S INVESTORS SERVICE CORPORATES

Credit Challenges

» High exposure to cyclical end markets tied to commodity price volatility and mining industry weakness

» Concentration to Sub-Saharan African and Russian markets currently experiencing challenging economic conditions

» Key supplier risks mitigated by long term relationships and close strategic alignment

» Debt levels and leverage susceptible to seasonal working capital demands

Rating OutlookThe negative outlook reflects Barloworld's operational concentration in South Africa (75% of Group revenues and 72% of Groupoperating profit), exposing the company to the heightened risks associated with the operating environment in South Africa. As a resultMoody’s views Barloworld's ratings as being correlated with South Africa’s long term bond rating.

Factors that Could Lead to an UpgradeWe do not expect any further upward rating action as Barloworld's rating is likely to be constrained at the same level as South Africa'sgovernment bond rating given the bulk of Barloworld's cash flows operational exposure is derived in South Africa and the rest of Africa.

Subject to the government of South Africa's bond rating, Moody's would consider an upgrade if Barloworld

» Is able to grow in size and geographic diversification, while maintaining its financial performance under challenging operatingconditions

» Adjusted debt/EBITDA were to fall below 2.0x

» EBIT / interest increases above 4.0x

» A positive and sustainable free cash flow position

Factors that Could Lead to a DowngradePressure on the ratings would develop following

» A downgrade of the government of South Africa's bond rating

» Operating performance were to weaken, to the extent there are revenue and operating margin declines translating into weakerdebt protection measures such that debt / EBITDA rises above 3.0x or its EBIT/ interest expense falls below 2.5x for an extendedperiod of time

» If the company's liquidity risk profile deteriorates

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 30 June 2017 Barloworld Limited: Update of Key Credit Factors Following Sovereign Rating Action

MOODY'S INVESTORS SERVICE CORPORATES

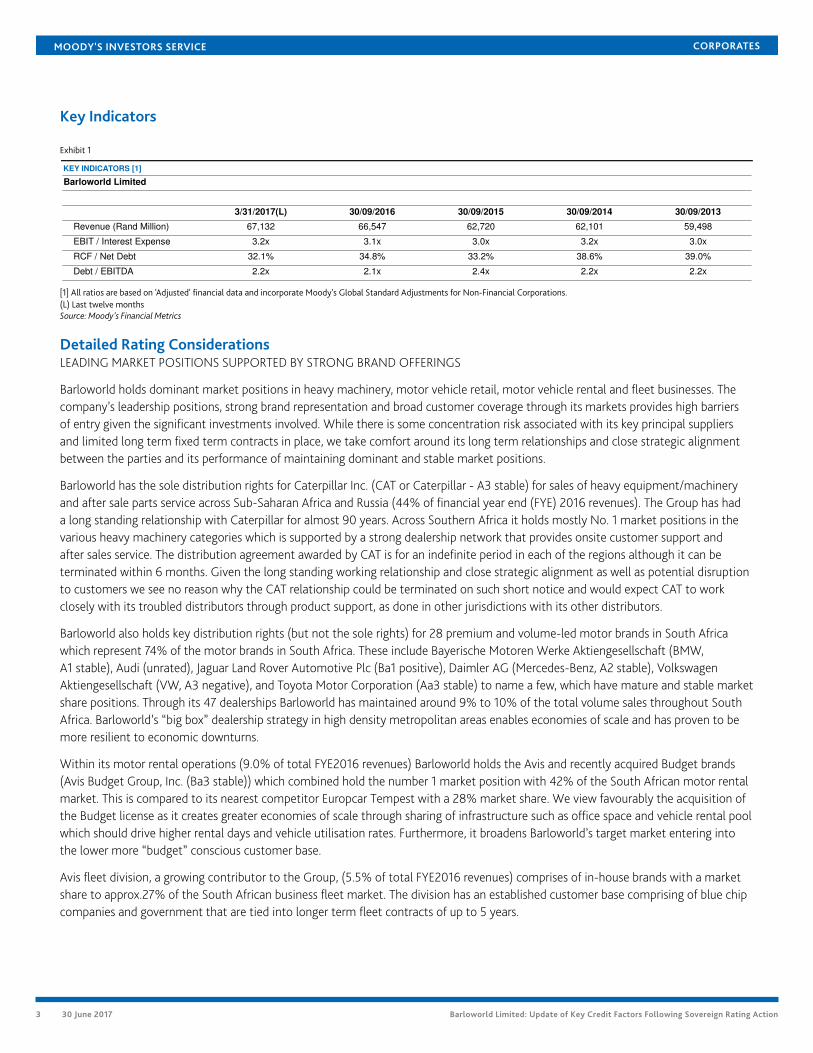

Key Indicators

Exhibit 1

KEY INDICATORS [1]

Barloworld Limited

3/31/2017(L) 30/09/2016 30/09/2015 30/09/2014 30/09/2013

Revenue (Rand Million) 67,132 66,547 62,720 62,101 59,498

EBIT / Interest Expense 3.2x 3.1x 3.0x 3.2x 3.0x

RCF / Net Debt 32.1% 34.8% 33.2% 38.6% 39.0%

Debt / EBITDA 2.2x 2.1x 2.4x 2.2x 2.2x

[1] All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations.(L) Last twelve monthsSource: Moody's Financial Metrics

Detailed Rating ConsiderationsLEADING MARKET POSITIONS SUPPORTED BY STRONG BRAND OFFERINGS

Barloworld holds dominant market positions in heavy machinery, motor vehicle retail, motor vehicle rental and fleet businesses. Thecompany’s leadership positions, strong brand representation and broad customer coverage through its markets provides high barriersof entry given the significant investments involved. While there is some concentration risk associated with its key principal suppliersand limited long term fixed term contracts in place, we take comfort around its long term relationships and close strategic alignmentbetween the parties and its performance of maintaining dominant and stable market positions.

Barloworld has the sole distribution rights for Caterpillar Inc. (CAT or Caterpillar - A3 stable) for sales of heavy equipment/machineryand after sale parts service across Sub-Saharan Africa and Russia (44% of financial year end (FYE) 2016 revenues). The Group has hada long standing relationship with Caterpillar for almost 90 years. Across Southern Africa it holds mostly No. 1 market positions in thevarious heavy machinery categories which is supported by a strong dealership network that provides onsite customer support andafter sales service. The distribution agreement awarded by CAT is for an indefinite period in each of the regions although it can beterminated within 6 months. Given the long standing working relationship and close strategic alignment as well as potential disruptionto customers we see no reason why the CAT relationship could be terminated on such short notice and would expect CAT to workclosely with its troubled distributors through product support, as done in other jurisdictions with its other distributors.

Barloworld also holds key distribution rights (but not the sole rights) for 28 premium and volume-led motor brands in South Africawhich represent 74% of the motor brands in South Africa. These include Bayerische Motoren Werke Aktiengesellschaft (BMW,A1 stable), Audi (unrated), Jaguar Land Rover Automotive Plc (Ba1 positive), Daimler AG (Mercedes-Benz, A2 stable), VolkswagenAktiengesellschaft (VW, A3 negative), and Toyota Motor Corporation (Aa3 stable) to name a few, which have mature and stable marketshare positions. Through its 47 dealerships Barloworld has maintained around 9% to 10% of the total volume sales throughout SouthAfrica. Barloworld’s “big box” dealership strategy in high density metropolitan areas enables economies of scale and has proven to bemore resilient to economic downturns.

Within its motor rental operations (9.0% of total FYE2016 revenues) Barloworld holds the Avis and recently acquired Budget brands(Avis Budget Group, Inc. (Ba3 stable)) which combined hold the number 1 market position with 42% of the South African motor rentalmarket. This is compared to its nearest competitor Europcar Tempest with a 28% market share. We view favourably the acquisition ofthe Budget license as it creates greater economies of scale through sharing of infrastructure such as office space and vehicle rental poolwhich should drive higher rental days and vehicle utilisation rates. Furthermore, it broadens Barloworld’s target market entering intothe lower more “budget” conscious customer base.

Avis fleet division, a growing contributor to the Group, (5.5% of total FYE2016 revenues) comprises of in-house brands with a marketshare to approx.27% of the South African business fleet market. The division has an established customer base comprising of blue chipcompanies and government that are tied into longer term fleet contracts of up to 5 years.

3 30 June 2017 Barloworld Limited: Update of Key Credit Factors Following Sovereign Rating Action

MOODY'S INVESTORS SERVICE CORPORATES

DIVERSIFIED OPERATIONS AGAINST HIGH EXPOSURE TO CYCLICAL END MARKETS

Barloworld business profile benefits from its diversified operations which partially offset its exposure to more cyclical end markets suchas mining, and construction industries which are currently experiencing prolonged depressed global commodity prices and weaker localbusiness environments. Its non-commodity linked business lines contribute to 56% of total revenues, offering exposure to industriesthat are less correlated to mining and construction industries, which have resulted in a more stable operating profile.

Exhibit 2

Revenue Breakdown per Division (% of total revenues before eliminations)

37.5% 41.5%47.3% 46.8% 43.8% 41.9%

9.5%8.2%

4.2% 3.1%3.2% 2.3%

35.9% 34.6% 29.4% 30.9% 32.1% 32.8%

6.7% 6.1%6.8% 7.3% 8.3% 9.0%

3.6% 3.9% 4.9% 5.0% 5.4% 5.5%

6.8% 5.8% 7.4% 7.0% 7.2% 8.6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015 2016

Equipment Handling Motor retail Car rental Fleet leasing Logistics

Source: Barloworld annual financial reports

We anticipate that Barloworld’s heavy equipment unit sales will remain under pressure largely due to the weak commodityfundamentals as miners delay projects, limit capital expenditure and lower operating costs. This is evident in Barloworld’s equipmentorder book which has been declining since the high point in FYE2012 and are currently at similar levels to the low point of FYE2009/10.The recent uptick in orders from Russia has provided some respite against the subdued demand in Southern Africa.

Barloworld’s broad customer base and commodity mix reduces its operating risk profile. Within the Equipment southern Africandivision mining represents 29% (40% FYE2015) of new Equipment revenues with construction and power contributing 52% and 15%(43% and 13% FYE2015), respectively. The top 10 customers represents key global mining operators and contribute 63% to Equipmentdivision after sales revenues, with Anglo American plc (Ba3 positive) the largest customer at 19% of after sales revenues. (machinesales by customer depend on the timing of large mining projects and will vary from period to period). From a commodity exposurewe consider its exposure to commodities to be moderately diversified with its top 3 key exposures to coal, copper and diamonds,representing 51% to total equipment revenues.

HIGH CONCENTRATION TO REGIONS WHICH ARE EXPERIENCING WEAKER ECONOMIC CONDITIONS

With close to 72.2% of revenues derived from South Africa (Baa3, negative), Barloworld is intrinsically linked to the macro-economicenvironment of South Africa. The slowdown in South Africa’s economic growth, low consumer and business confidence and policyuncertainty in the mining sector is creating a challenging operating environment. The rest of Africa contributes to 13.5% of revenuesand along with operations in Russia (Ba1, stable) and Iberia (Spain (Baa2 stable) and Portugal (Ba1 stable)) which contribute 14.3% ofFYE2016 revenues offers geographic and commodity diversification but are also facing their own challenges. We recognize Barloworld’sprudent approach to operating in weaker sovereign environments as demonstrated by limiting local currency receipts (predominatelyfor African countries outside of South Africa).

Due to the infrastructure backlog in many African countries we see the potential for strong long term demand for Barloworld’sEquipment division, however fiscal and funding challenges are likely to prevail over the short to medium term. Russia with its significantmining territory also offers long term growth opportunities.

4 30 June 2017 Barloworld Limited: Update of Key Credit Factors Following Sovereign Rating Action

MOODY'S INVESTORS SERVICE CORPORATES

Exhibit 3

Regional diversification limited to Southern Africa

71% 71%82% 85% 88% 85%

18% 19%

10% 8% 7% 7%

8% 6% 5% 7%8% 9%0%

3% 2%

0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015 2016

Southern Africa Europe Russia North America Australia

Source: Barloworld annual financial reports

Barloworld’s motor dealership new vehicle sales are under pressure from a weak consumer confidence and high consumerindebtedness. As a result we are expecting South African vehicle volumes to remain flat with greater downside risk for 2017 asconsumers delay new vehicle purchases or switch to the used vehicle market. We believe Barloworld is partially insulated given itsbroad brand offering covering premium and volume led brands as well as its access to a sizable car parc base of 2.16 million motorvehicles in South Africa which will support its after sales service and parts revenues (14% of motor trading revenues for FYE2016).

Barloworld’s Motor Retail division benefits from having greater price competitive brands relative to imported vehicle brands. This is dueto the largely locally based OEM’s (Original Equipment Manufacturers) which are partially insulated from the currency volatility of theRand.

RESILIENT OPERATING CASH FLOWS UNDERPINNED BY INTEGRATED BUSINESS MODEL

Barloworld’s operating performance has been relatively resilient through the cycles, particularly post the financial crisis of 2008.This is partly due to its exposures to different industry sectors, geographic diversification and integrated product offerings down thevalue chain. The management of its “assets” across the value chain benefits from (1) obtaining discounts/rebates from OEMs; (2)providing maintenance, parts and related services on sold equipment/vehicles; and (3) a disposal margin which is captured throughits in-house electronic disposal platform. The integrated business model down the value chain provides a strong counterbalance tothe anticipated declines in new equipment and vehicle sales, as companies attempt to extend the lifespan of machinery beyond thetraditional replacement cycle and consumers delay new vehicle purchases.

Exhibit 4

Revenues, EBITDA and margins demonstrate operational resilience through the cycle

50,10745,269

40,830

49,82353,415

59,49862,101 62,720

66,547 67,13270,100

5,366 4,952 3,981 4,859 5,620 6,343 7,196 7,761 8,435 8,759 8,622

10.7% 10.9%

9.8% 9.8%9.9% 10.7%

11.6%

12.4%12.7%

13.0%12.3%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

FYE 2008 FYE 2009 FYE 2010 FYE 2011 FYE 2012 FYE 2013 FYE 2014 FYE 2015 FYE 2016 LTM Mar 2017Moody's Forecast FYE 2017

ZA

R m

illio

n

Revenue Adjusted EBITDA EBITDA Margin

Note: FYE 2012, Barloworld’s revenues were boosted by CAT’s acquisition of Bucyrus which expanded Barloworld’s product offering and profitability.Source: Barloworld annual financial reports and Moody’s

Barloworld has maintained adjusted EBITDA margins around 10% to 11% historically, weakening to 9.8% in FYE 2010 and FYE2011,when the full effect of the financial crisis was felt, but has since improved to 13.0% as of LTM 2017 as a result of its higher marginaftermarket services contributions. We do expect performance over the next two to three years to come under pressure largely due

5 30 June 2017 Barloworld Limited: Update of Key Credit Factors Following Sovereign Rating Action

MOODY'S INVESTORS SERVICE CORPORATES

to Barloworld’s exposure to the prolonged depressed commodity cycle and weaker South African economic environment with itsexpected low growth rates (Moody’s forecast of GDP for 2017 is 0.8% and 2018 is 1.5%). We, however, remain confident that therespective operations will be able to adjust and that management will be responsive to these pressures as historically demonstratedthrough right sizing troubled operations and keeping the business focused on its core competencies. We also expect Barloworld’ssizable, higher margin aftermarket services business to continue to counterbalance the anticipated declines in new equipment andvehicle sales. Over the past 5 years after service and parts revenues in the Equipment division has increased from around 33%(FYE2012) to 53% of total Equipment division revenues.

Exhibit 5

Material Equipment after sales revenue contribution (FYE2016)

35%

53%

7%5%

New equipment Product support Used equipment Rental

Source: Barloworld FYE2016 annual financial report

In addition to leveraging off its large installed equipment/vehicle population management’s strategy over the next two to three yearswill be to optimize its operations through cost efficiencies, right sizing and pursuing growth opportunities in adjacent markets. Weanticipate these strategies will place Barloworld in a stronger position should market conditions and volumes improve given its largelyfixed cost base.

STABLE CREDIT METRICS SUPPORTED BY BALANCED FINANCIAL POLICIES

The resilience of Barloworld’s diversified business model and balanced approach to financial management policies is furtherdemonstrated through its historically stable credit metrics. Leverage, as measured by adjusted debt/EBITDA, of 2.2x is moderatelypositioned within the rating category but is susceptible to seasonal working capital funding demands to support its after salesbusinesses. We expect leverage to remain relatively stable underpinned by management’s internal target of net debt/ EBITDA of lessthan 2.5x (reported to 31 March 2017: 1.4x). Barloworld’s EBIT/interest cover of 3.2x, although weakly positioned, has historically beenaround these levels but is expected to come under pressure, particularly given the rising funding cost environment in South Africa.We anticipate overall credit metrics will remain relatively stable despite the challenges Barloworld faces in the current economicenvironment. This will be supported by our expectation that management will maintain its balanced financial policies.

6 30 June 2017 Barloworld Limited: Update of Key Credit Factors Following Sovereign Rating Action

MOODY'S INVESTORS SERVICE CORPORATES

Exhibit 6

Credit metrics have remained range bound through the cycle

2.0x

2.2x

2.4x

2.6x

2.8x

3.0x

3.2x

3.4x

FYE 2008 FYE 2009 FYE 2010 FYE 2011 FYE 2012 FYE 2013 FYE 2014 FYE 2015 FYE 2016 LTM Mar 2017 Forecast FYE 2017

(Moody's Case)

Debt/ EBITDA EBIT/ Interest expense

Source: Barloworld annual financial reports and Moody’s

Liquidity AnalysisBarloworld's liquidity as of 31 March 2017 is considered good whereby Barloworld has sufficient available committed facilities totalingZAR6.5 billion ($ 470 million) and cash of ZAR3.2 billion ($233 million) to meet debt maturities of ZAR3.0 billion ($218 million)(includes ZAR1.5 billion of drawn on-demand bank facilities), committed capital expenditure and seasonal working capital needsover the next 12 months. Barloworld has an evenly spread debt maturity profile over the next seven years but there is reliance onshort term debt (commercial paper, 365 day notice facilities and on-demand facilities) to fund its working capital needs. Barloworld'ssplit between long term and short term debt maturities was 66:34 as of 31 March 2017 and will improve as bond and bank debt arerefinanced during the year. We will continue to closely monitor Barloworld's liquidity profile, particularly given the seasonality of itsworking capital.

Barloworld has a track record of regular access to the bond and bank market and as a listed entity is able to raise equity if needed.Barloworld has good headroom under its financial covenants, which include net debt/ EBITDA of less than 3.0x (reported 31 March2017: 1.4x) and EBITDA/interest expense of greater than 3.5x (reported 31 March 2017 4.7x). We expect management to continue tooperate within its conservative financial policy framework.

Corporate ProfileBarloworld, headquartered in South Africa, is a leading distributor and after sales support provider of heavy equipment and motorvehicles for leading international brands across Sub Saharan Africa, Russia and Iberia. It also provides integrated rental, fleetmanagement, product support and logistics solutions. The core divisions of the group comprise of (1) Equipment which provides endto end solutions across the value chain on behalf Caterpillar Inc. to the mining, construction, industrial sectors; (2) Automotive whichoperates the motor retail, car rental, and fleet management services; and (3) Logistics which provide logistics management transportand supply chain optimisation.

As of LTM to 31 March 2017 Barloworld reported revenues of ZAR67.1 billion ($5.2 billion) and adjusted EBITDA of ZAR8.8 billion ($0.6billion).

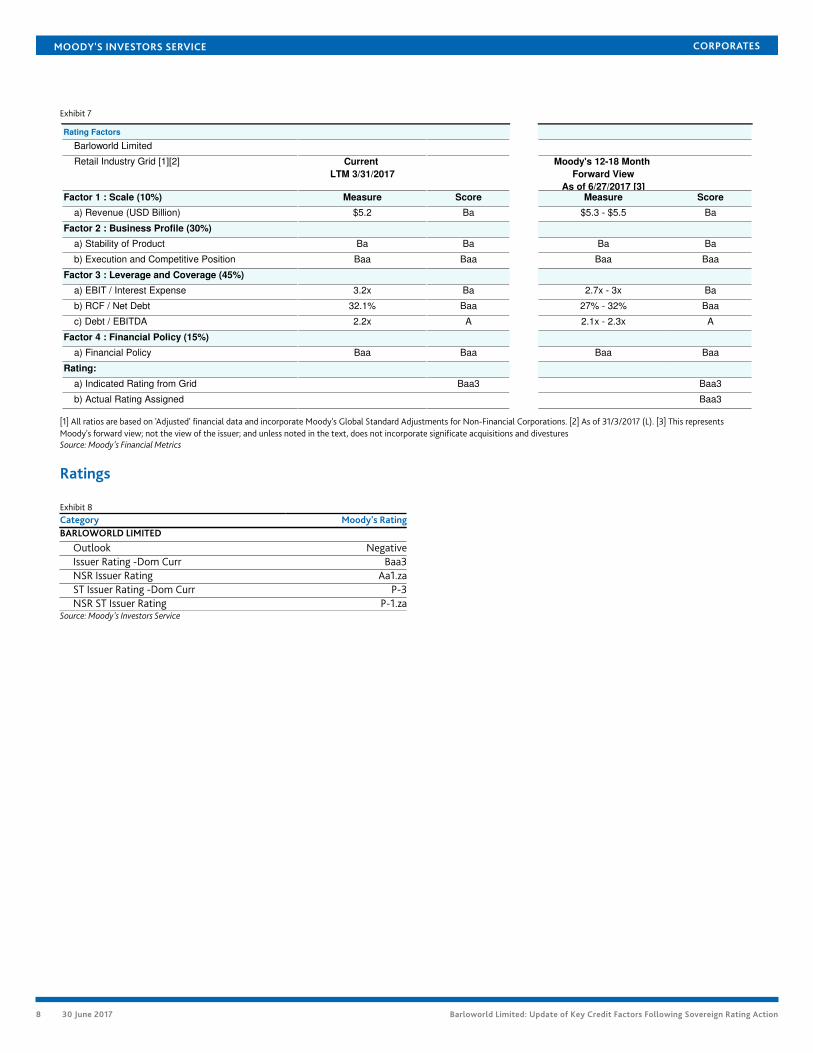

Rating Methodology and Scorecard FactorsThe principal methodology used in rating the company was Moody's Global Retail Industry Methodology (October 2015), as it capturesthe biggest portion of its businesses being the Equipment and Automotive retail and after services operations, representing 75% ofGroup revenues. We also consider the Global Manufacturing Companies Methodology (July 2014) and Equipment and TransportationRental Industry Methodology (December 2014) into our analysis. Based on the last twelve months to 31 March 2017 Barloworld'soverall performance measurements from the rating grid indicate a rating outcome equated to a Baa3. This is in line with Moody'sassigned global scale issuer rating of Baa3. On a forward 12-18 month view we expect the grid implied rating to remain at Baa3, despitesome anticipated weakness in the credit metrics.

7 30 June 2017 Barloworld Limited: Update of Key Credit Factors Following Sovereign Rating Action

MOODY'S INVESTORS SERVICE CORPORATES

Exhibit 7

Rating Factors

Barloworld Limited

Retail Industry Grid [1][2] Current

LTM 3/31/2017

Moody's 12-18 Month

Forward View

As of 6/27/2017 [3]Factor 1 : Scale (10%) Measure Score Measure Score

a) Revenue (USD Billion) $5.2 Ba $5.3 - $5.5 Ba

Factor 2 : Business Profile (30%)

a) Stability of Product Ba Ba Ba Ba

b) Execution and Competitive Position Baa Baa Baa Baa

Factor 3 : Leverage and Coverage (45%)

a) EBIT / Interest Expense 3.2x Ba 2.7x - 3x Ba

b) RCF / Net Debt 32.1% Baa 27% - 32% Baa

c) Debt / EBITDA 2.2x A 2.1x - 2.3x A

Factor 4 : Financial Policy (15%)

a) Financial Policy Baa Baa Baa Baa

Rating:

a) Indicated Rating from Grid Baa3 Baa3

b) Actual Rating Assigned Baa3

[1] All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations. [2] As of 31/3/2017 (L). [3] This representsMoody's forward view; not the view of the issuer; and unless noted in the text, does not incorporate significate acquisitions and divesturesSource: Moody's Financial Metrics

Ratings

Exhibit 8Category Moody's RatingBARLOWORLD LIMITED

Outlook NegativeIssuer Rating -Dom Curr Baa3NSR Issuer Rating Aa1.zaST Issuer Rating -Dom Curr P-3NSR ST Issuer Rating P-1.za

Source: Moody's Investors Service

8 30 June 2017 Barloworld Limited: Update of Key Credit Factors Following Sovereign Rating Action

MOODY'S INVESTORS SERVICE CORPORATES

© 2017 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGSDO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’SOPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVEMODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’SPUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOTPROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THESUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATIONAND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FORPURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1077368

9 30 June 2017 Barloworld Limited: Update of Key Credit Factors Following Sovereign Rating Action