banking ppt final123

30

-

Upload

somsubhra-mukherjee -

Category

Documents

-

view

62 -

download

2

Transcript of banking ppt final123

What is a Bank ??? It is an establishment authorized by a government to accept

deposits, pay interest, make loans, act as an intermediary in financial transaction and provide other financial services to its customers.

What is Banking ???The business conducted or services offered by bank.

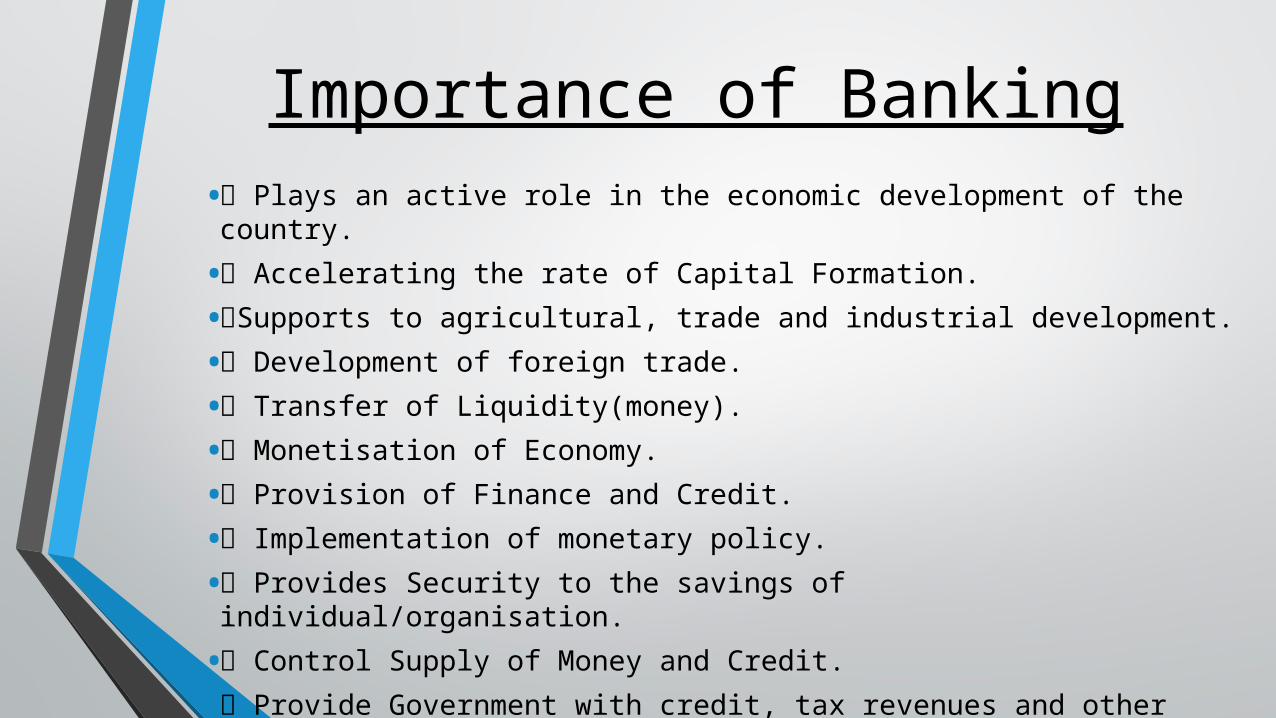

Importance of Banking

• Plays an active role in the economic development of the country.

• Accelerating the rate of Capital Formation.

• Supports to agricultural, trade and industrial development.

• Development of foreign trade.

• Transfer of Liquidity(money).

• Monetisation of Economy.

• Provision of Finance and Credit.

• Implementation of monetary policy.

• Provides Security to the savings of individual/organisation.

• Control Supply of Money and Credit.

• Provide Government with credit, tax revenues and other services.

Importance of Banking

How do we benefit from Banking???

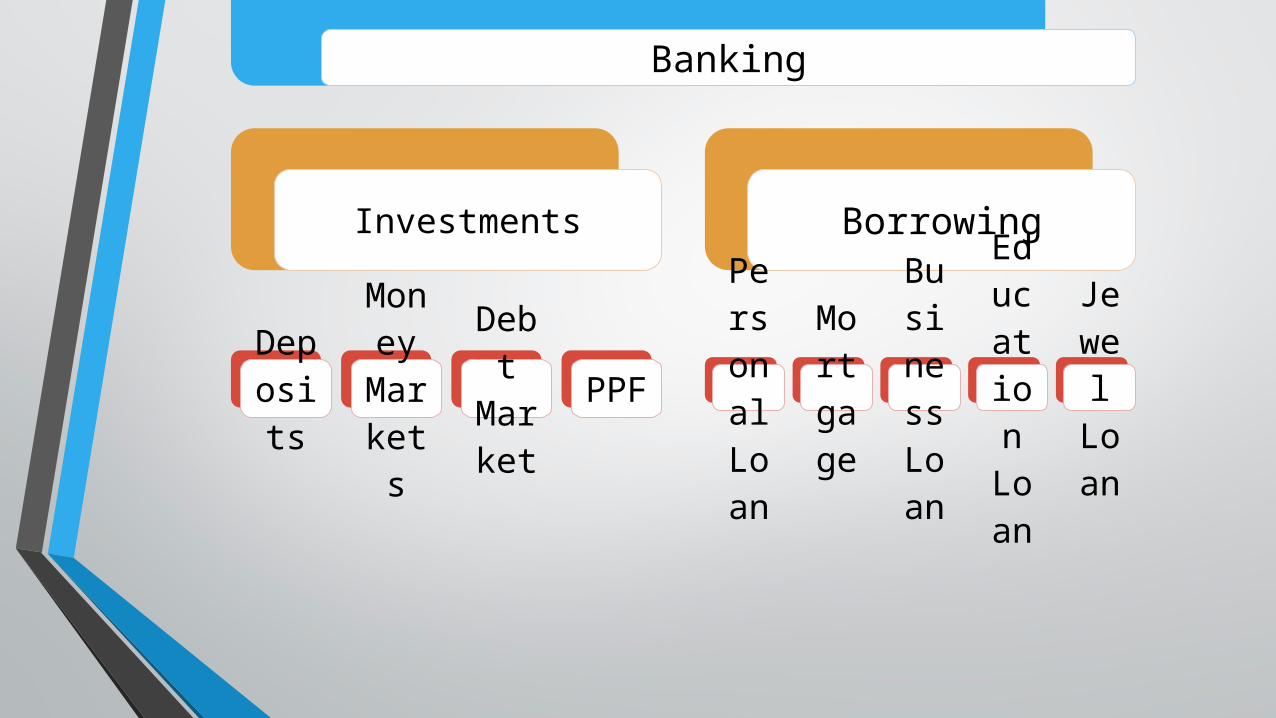

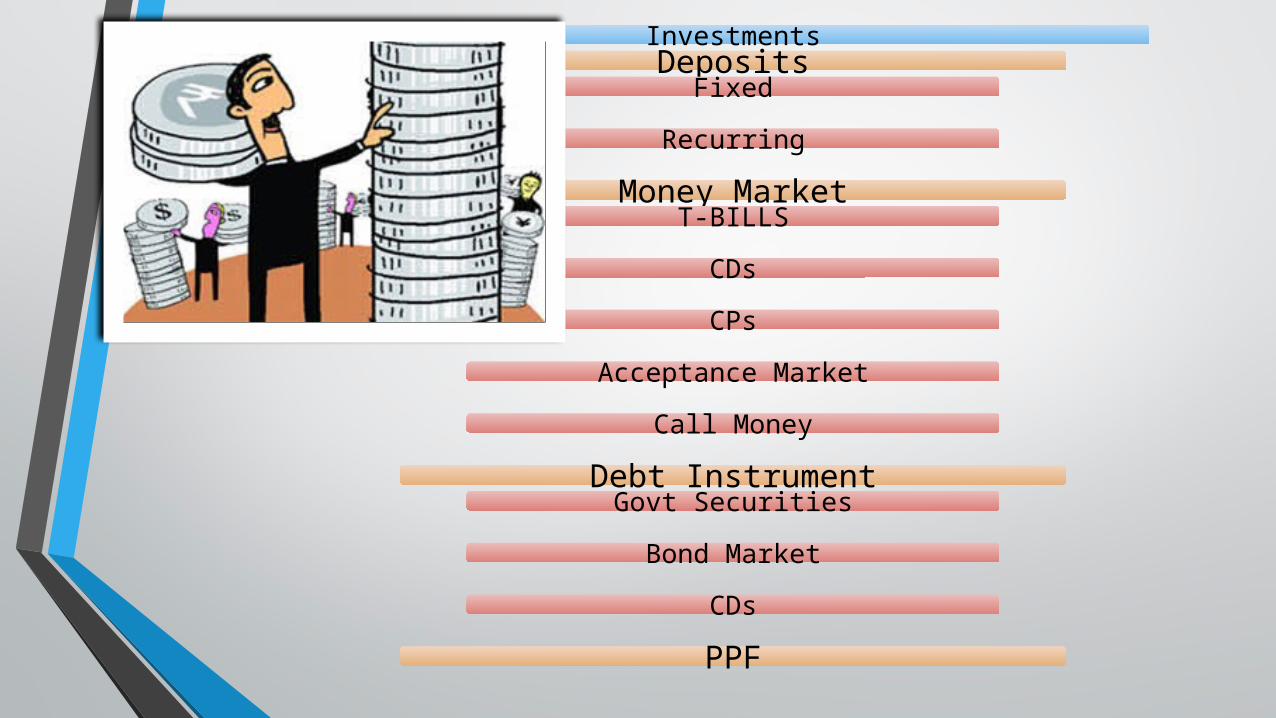

Banking

Investments

Deposits

Money Markets

Debt Market

PPF

Borrowing

Personal Loan

Mortgage

Business Loan

Education Loan

Jewel Loan

InvestmentsDeposits

Fixed

Recurring

Money MarketT-BILLS

CDs

CPs

Acceptance Market

Call Money

Debt InstrumentGovt Securities

Bond Market

CDs

PPF

Regular Fixed Deposits: In this type of FD scheme, the tenure is fixed for a period ranging 1

week to 10 years. The interest rate of each period is pre-determined, and an investor can choose to stay invested for a suitable period.

Special Fixed Deposits: In special tenure FD schemes, the fund can be invested for a

special period like 333, 399 or 555 days, and rate of interest is higher.

Tax Saving Fixed Deposits:This type of FD scheme attracts investors who want to invest for saving income tax. There is a compulsory lock-in of five years under this type, and the fund cannot be withdrawn before completion of the period.

Minimum Amount= Rs 10,000/-, Maximum Amount= Rs 1,50,000/-

Deposits

Floating Fixed DepositsUnder this scheme, an investor can opt for a market-based interest rate. The rate of interest is renewed automatically with the change in the base rate.

Recurring deposit schemeUnder this scheme, an investor can regularly deposit a fixed amount every month for a fixed tenure and at a pre-decided interest rate. The corpus keeps on growing every month towards the maturity period.

*Formulae: MV=n*p+(n(n+1)p*r/2400)

Where MV=Maturity Value, n=number of periods, p=monthly installment, r=rate%

Deposits (Contd…)

Flexi Fixed Deposits- Also known as Auto-sweep(sweep-in) and Reverse

Sweep(Sweep-out)

- Auto-Sweep is when the balance in excess of a stipulated amount is automatically transferred to an Fixed Deposit for a default term of one year. Hence, amount in excess of a fixed limit can now earn a substantially higher rate of return. It has two components Savings A/c and Current A/c.

• Reverse-Sweep is done when in case of shortfalls in the Savings account to honor any debit instruction.

• Hence in case the customer wants to withdraw more than what is deposited in the Savings account component, the bank would withdraw money from the Fixed Deposit component.

Deposits (Contd…)

• 1. By submitting Form 15G/15H

• 2. Distributing FD investment

• 3. Timing the FD

• 4. Splitting the FD

How to save TDS on Fixed Deposits???

As per RBI definition, ” The money market is a mechanism that deals with the lending and borrowing of short term funds (less than one year)”.

Money Market and its Features

Transaction have to be conducted without the help of brokers.

It is not a single homogeneous market, it comprises of several submarket like call money market, acceptance & bill market.

The component of Money Market are the commercial banks, acceptance houses & NBFC (Non-banking financial companies).

In Money Market transaction can not take place formal like stock exchange, only through oral communication, relevant document and written communication transaction can be done .

Defination:-

Features:-

Composition of Money Market

Call Money

Commercial

Paper

Acceptance Market

Treasury Bill

Certificate of Deposits

Call Money Market• Short Term Finance, Repayable on Demand with a maturity period of one to fifteen days.

• Used for INTER-BANK transactions.

• Money Lent for one day is ‘Call money’ and if exceeds one day then ‘Notice Money’. And rate of interest is known as ‘Call rate’.

• Call money is a method by which banks lend to each other to be able to maintain the CRR(Cash Reserve Ratio).

• Highly volatile, interest varies from day to day or sometimes even hour to hour.Commercial Paper(CPs)• Short term unsecured loan issued by a corporation typically

financing day to day operation.

• Much safer investment because the financial situation of a company can easily be predicted over a period.

• Only company with high credit rating issue CPs.

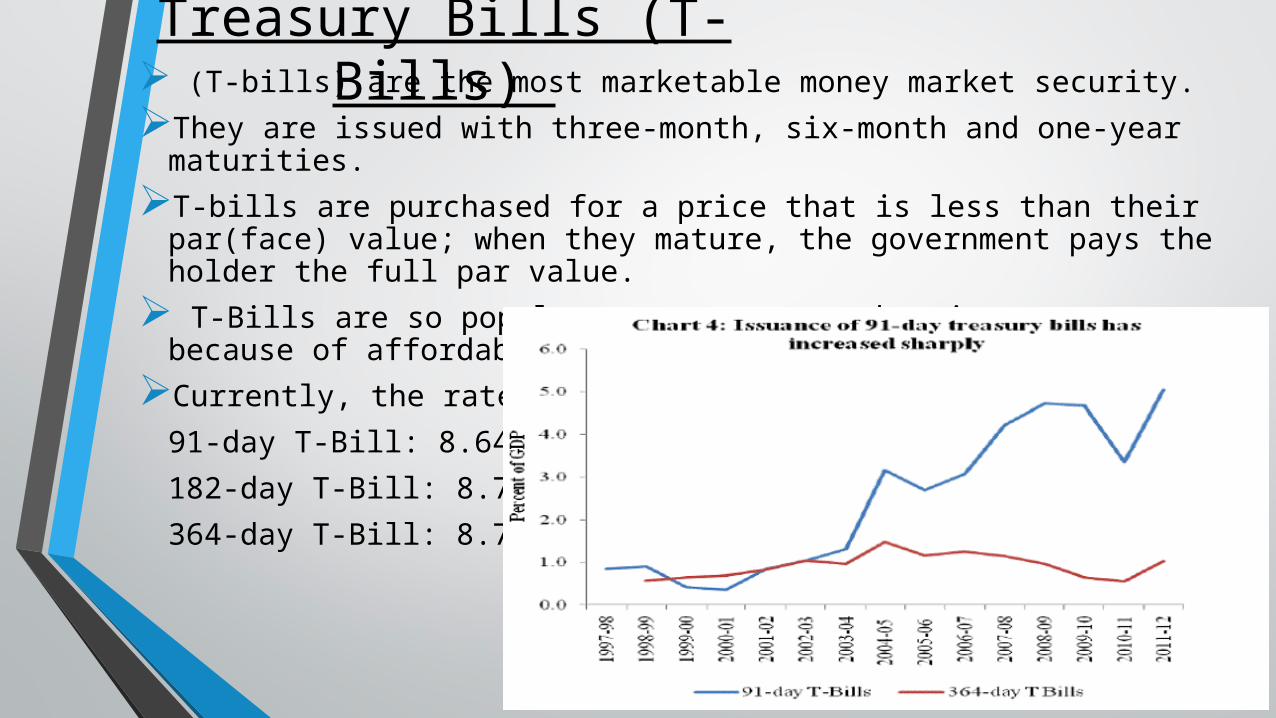

Treasury Bills (T-Bills) (T-bills) are the most marketable money market security.

They are issued with three-month, six-month and one-year maturities.

T-bills are purchased for a price that is less than their par(face) value; when they mature, the government pays the holder the full par value.

T-Bills are so popular among money market instruments because of affordability to the individual investors

Currently, the rates of T-Bills are:

91-day T-Bill: 8.6456%

182-day T-Bill: 8.7050%

364-day T-Bill: 8.7432 %

A banker’s acceptance (BA) is a short-term credit investment created by a non-financial firm

BAs are guaranteed by a bank to make payment i.e Low-Risk.Acceptances are traded at discounts from face value in the

secondary marketBA acts as a negotiable time draft for financing imports,

exports or other transactions in goods.

Banker's Acceptance

Certificate of deposit (CD)A CD is a time deposit with a bank.Like most time deposit, funds can not be withdrawn before maturity without paying a penalty.CDs have specific maturity date, interest rate and it can be issued in any denomination.The main advantage of CD is their safety.Anyone can earn more than a saving account interest.

Other Debt instruments Government Securities Market (G-Sec Market):

• It consists of central and state government securities. It means that, loans are being taken by the central and state government. It is also the most dominant category in the India debt market.

• It is the Reserve Bank of India that issues G-Secs on behalf of the Government of India.

• These securities have a maturity period of 1 to 30 years. G-Secs offer fixed interest rate, where interests are payable semi-annually. For shorter run T-BILLS.

• Includes the Money market Instruments also.

Bond Market:

• These are the bonds issued to meet financial requirements at a fixed cost and hence remove uncertainty in financial costs.

• Consists of Corporate Bond, Fixed rate bond, Floating rate bond, zero-coupon bond, Capital Indexed Bond, Bonds with call/put option.

Corporate Bonds

• These bonds come from PSUs and private corporations and are offered for an extensive range of tenures up to 15 years.

• Comparing to G-Secs, corporate bonds carry higher risks, which depend upon the corporation, the industry where the corporation is currently operating, the current market conditions, and the rating of the corporation.

Fixed Rate Bonds:

• These are bonds on which the coupon rate is fixed for the entire life of the bond. Most government bonds are issued as fixed rate bonds.

Floating Rate Bonds:

• These bonds are securities that do not have a fixed coupon rate. The coupon is re-set at pre-announced intervals (say, every 6 months, or 1 year) by adding a spread over a base rate.

• In this case so far, the base rate is the weighted average cut-off yield of the last three 364-day Treasury Bill auctions preceding the coupon re-set date, and the spread is decided through the auction.

• Floating rate bonds were first issued in India in September 1995.

Zero Coupon Bonds:

• Zero coupon bonds are bonds with no coupon payments. Like T-Bills, they are issued at a discount to the face value.

• The Government of India issued such securities in the 90s; it has not issued zero coupon bonds after that.

Capital Indexed Bonds:

• These are bonds, the principal of which is linked to an accepted index of inflation with a view to protecting the holder from inflation.

• These bonds were first issued in December 1997 for a period of 5yrs.

• The government is currently working on a fresh issuance of Inflation Indexed Bonds wherein the payment of both the coupon as well as the principal on the bonds would be linked to an Inflation Index (Wholesale Price Index).

• In the proposed structure, the principal will be indexed and the coupon will be calculated on the indexed principal. In order to provide the holders protection against actual inflation, the final WPI will be used for indexation.

Bonds with Call/Put Options:

• Bonds issued with features of optionality, wherein the issuer can have the option to buy back (call option) or the investor can have the option to sell the bond(put option) to the issuer during the currency of the bond.

• The optionality on the bond could be done after the completion of five years from the date of issue.

• Govt has the right to buy-back the bond(call option) at par value(equal to the face value), while the investor has the right to sell the bond(put option) to the government at par value at the time of any of the half-yearly coupon dates starting from July 18, 2007.

Public Provident Fund (ppf)

• PPF is a long term investment scheme floated by Govt. of INDIA.

• To encourage Savings habit and provide Tax benefits to salaried and self-employees.

• Investor can invest as minimum as Rs. 500 to maximum Rs. 1,50,000 in the PPF account in one complete financial year in one lump sum subscription or in maximum 12 transactions.

• Tenure is 15yrs, aftr the completion, investor can invest furthur for 5yrs or withdraw the amount.

• Can avail loan, mostly 70-80% of the amount paid.

• Tax Benefits on investment as well as on interest and maturity payments.

• Current Interest rate varies from 8.8%-9.5%, depending on the Banks Criteria.

Public Provident Fund (ppf)(Contd…)

Public Provident Fund (ppf)(Contd…)

Borrowing

Personal Loan

Mortgage

Business Loan

Auto Loan

Education Loan

Jewel Loan

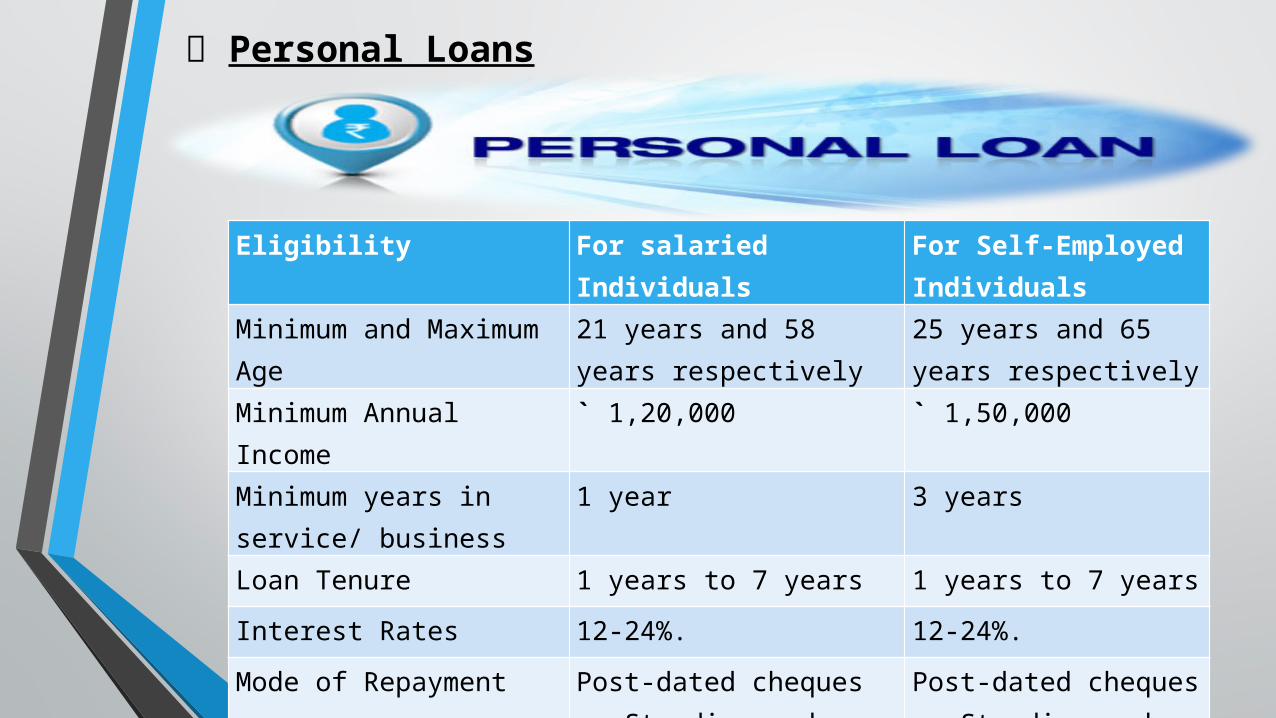

Personal Loans

Eligibility For salaried Individuals For Self-Employed Individuals

Minimum and Maximum Age 21 years and 58 years respectively

25 years and 65 years respectively

Minimum Annual Income ` 1,20,000 ` 1,50,000

Minimum years in service/ business

1 year 3 years

Loan Tenure 1 years to 7 years 1 years to 7 years

Interest Rates 12-24%. 12-24%.

Mode of Repayment Post-dated cheques or Standing orders to debit from personal A/c

Post-dated cheques or Standing orders to debit from personal A/c

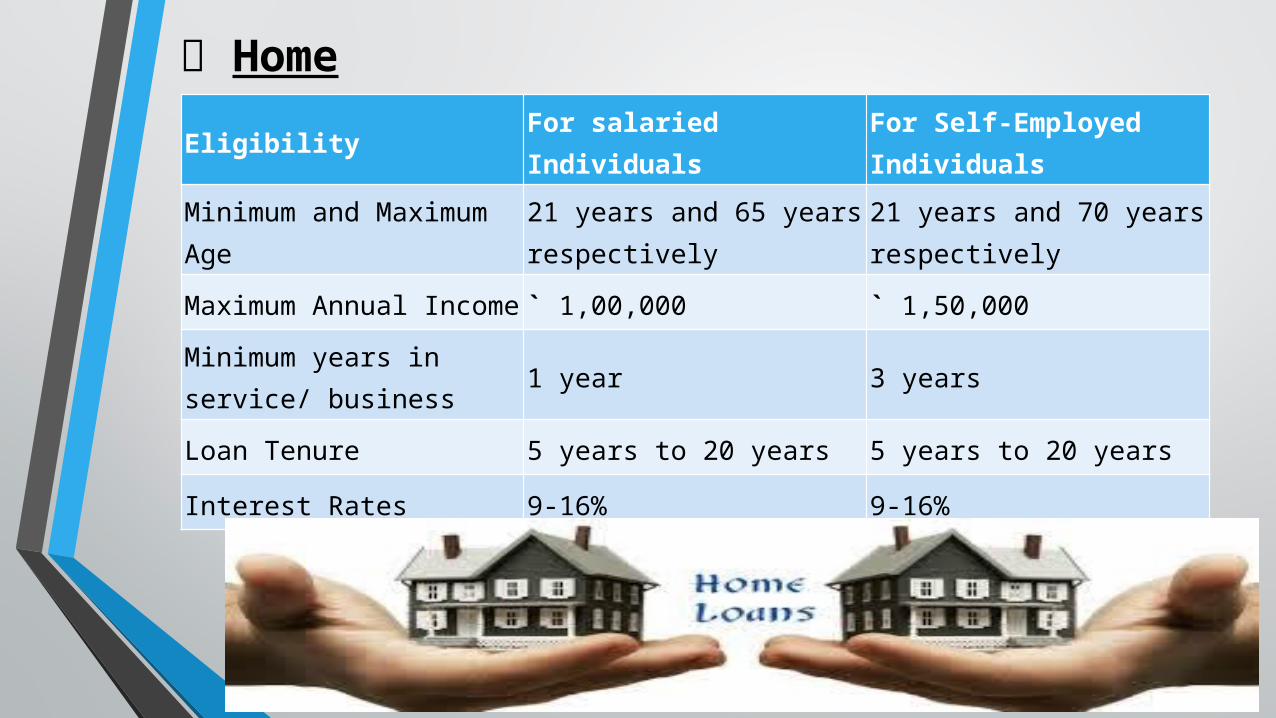

Home LoansEligibility For salaried Individuals

For Self-Employed Individuals

Minimum and Maximum Age21 years and 65 years respectively

21 years and 70 years respectively

Maximum Annual Income ` 1,00,000 ` 1,50,000

Minimum years in service/ business

1 year 3 years

Loan Tenure 5 years to 20 years 5 years to 20 years

Interest Rates 9-16% 9-16%

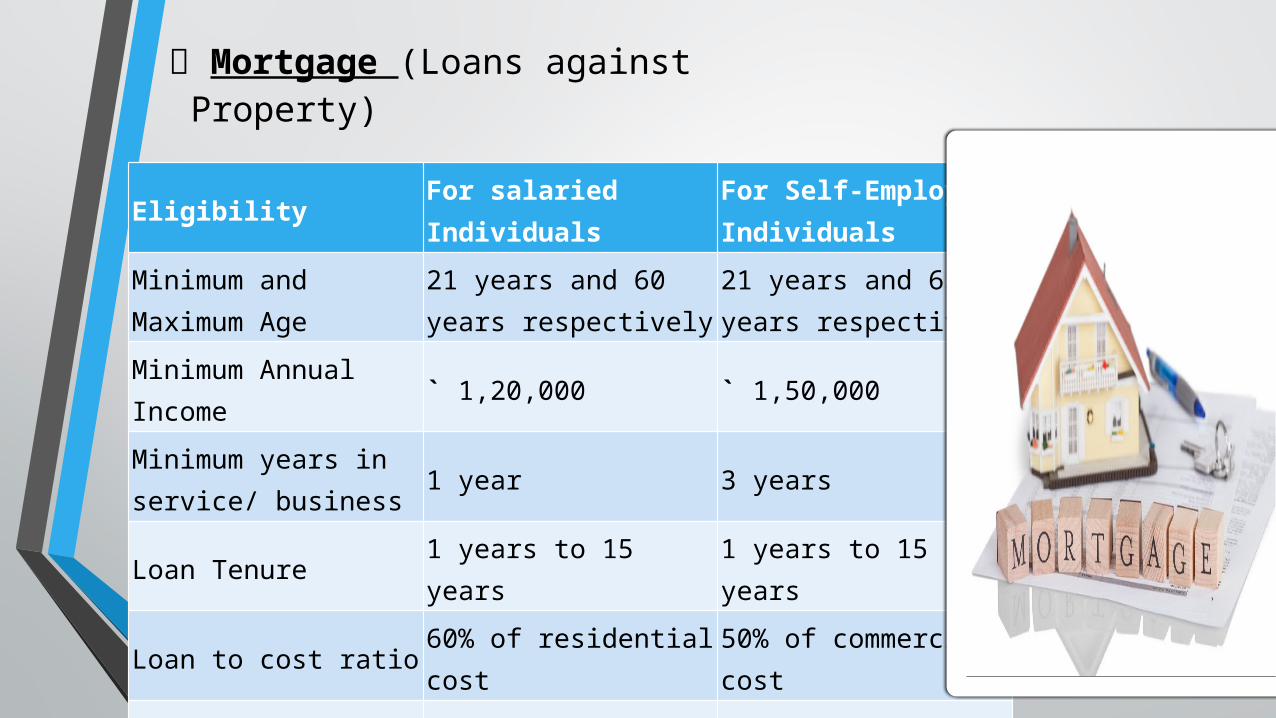

Mortgage (Loans against Property)

Eligibility For salaried IndividualsFor Self-Employed Individuals

Minimum and Maximum Age

21 years and 60 years respectively

21 years and 65 years respectively

Minimum Annual Income ` 1,20,000 ` 1,50,000

Minimum years in service/ business

1 year 3 years

Loan Tenure 1 years to 15 years 1 years to 15 years

Loan to cost ratio 60% of residential cost 50% of commercial cost

Tax Rebate NIL NIL

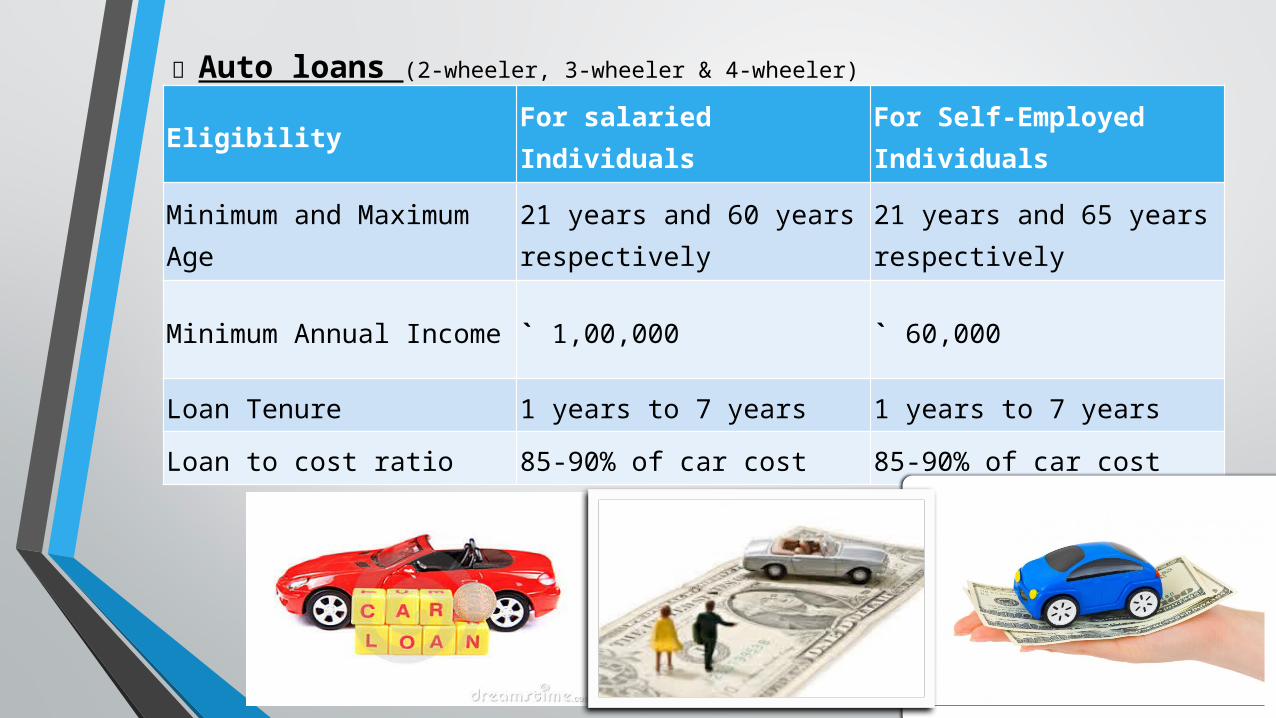

Auto loans (2-wheeler, 3-wheeler & 4-wheeler)

Eligibility For salaried IndividualsFor Self-Employed Individuals

Minimum and Maximum Age21 years and 60 years respectively

21 years and 65 years respectively

Minimum Annual Income ` 1,00,000 ` 60,000

Loan Tenure 1 years to 7 years 1 years to 7 years

Loan to cost ratio 85-90% of car cost 85-90% of car cost

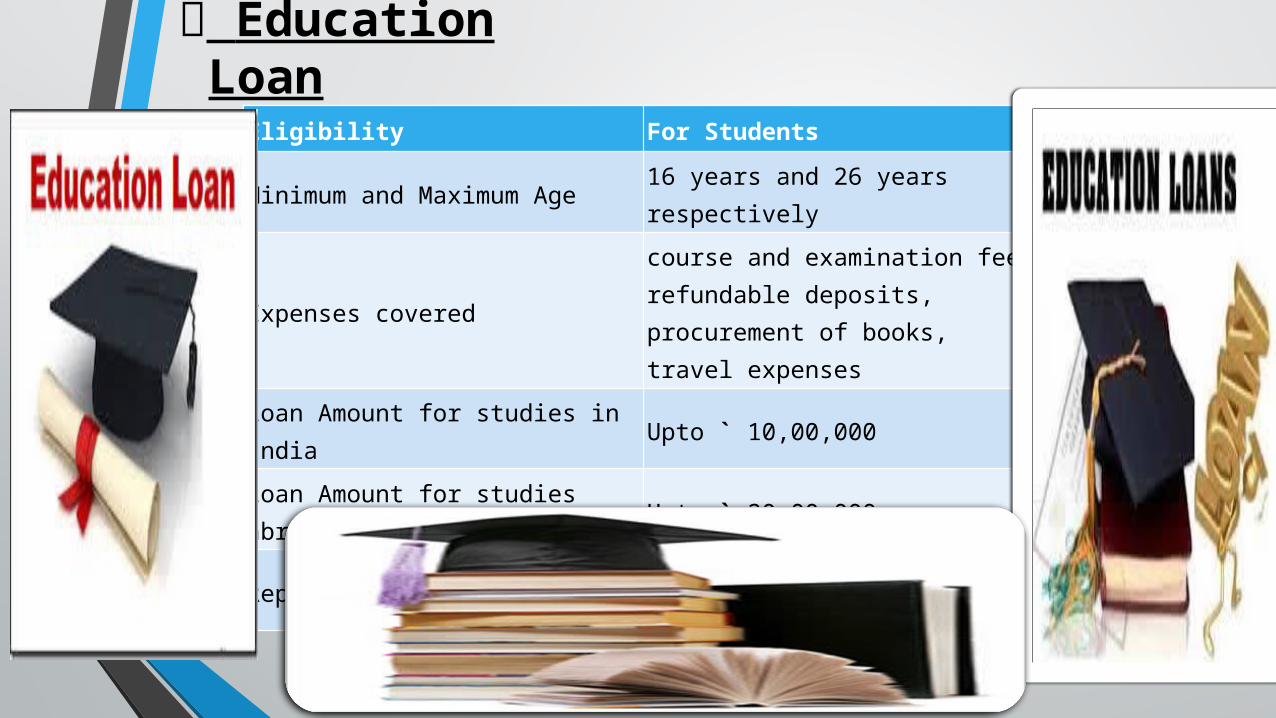

Education Loan

Eligibility For Students

Minimum and Maximum Age 16 years and 26 years respectively

Expenses coveredcourse and examination fee, refundable deposits, procurement of books, travel expenses

Loan Amount for studies in India Upto ` 10,00,000

Loan Amount for studies abroad Upto ` 20,00,000

Repayment Period5-8 years(includes 2 yrs monetary period)

Thank You