banking in retail

83

1 GENERAL INTRODUCTION BANKING IN RETAIL With a jump in the Indian economy from a manufacturing sector, that never really took off, to a nascent service sector, Banking as a whole is undergoing a change. A larger option for the consumer is getting translated into a larger demand for financial products and customization of services is fast becoming the norm than a competitive advantage. With the Retail banking sector expected to grow at a rate of 30% [Chandra Kocher, ED, ICICI Bank] players are focusing more and more on the Retail and are waking up to the potential of this sector of banking. At the same time, the banking sector as a whole is seeing structural changes in regulatory frameworks and securitization and stringent NPA norms expected to be in place by 2004 means the faster one adapts to these changing dynamics, the faster is one expected to gain the advantage. In this article, Richer try to study the reasons behind the euphemism regarding the Retail-focus of the Indian banks and try to assess how much of it is worth the attention that it is attracting. Retail banking means banking in which banking institutions undertake transactions directly with consumers, rather than corporations or other banks. Services offered include: savings and transactional accounts, mortgages, personal loans, debit cards, credit cards, and so forth. Retail lending is a part of retail banking which is conceptually similar in characteristics. POTENTIAL FOR RETAIL IN INDIA: IS SKY THE LIMIT The Indian players are bullish on the Retail business and this is not totally unfounded. There are two main reasons behind this. Firstly, it is now undeniable that the face of the Indian consumer is changing. This is reflected in a change in the urban household income pattern. The direct fallout of such a change will be the consumption patterns and hence the banking habits of Indians, which will now be skewed towards Retail products. At the same time, India compares pretty poorly with the other economies of the world that are now becoming comparable in terms of spending patterns with the opening up of our economy. For instance, while the total outstanding Retail loans in Taiwan is around 41% of GDP, the figure in India stands at less than 5%. The comparison with the West is even more staggering. Another comparison that is natural when comparing Retail sectors is the use of credit cards. Here also, the potential lies in the fact that of all the

description

projet report on banking in india.

Transcript of banking in retail

1

GENERAL INTRODUCTION

BANKING IN RETAIL

With a jump in the Indian economy from a manufacturing sector, that never really took off, to a nascent

service sector, Banking as a whole is undergoing a change. A larger option for the consumer is getting

translated into a larger demand for financial products and customization of services is fast becoming the

norm than a competitive advantage. With the Retail banking sector expected to grow at a rate of 30%

[Chandra Kocher, ED, ICICI Bank] players are focusing more and more on the Retail and are waking up

to the potential of this sector of banking. At the same time, the banking sector as a whole is seeing

structural changes in regulatory frameworks and securitization and stringent NPA norms expected to be

in place by 2004 means the faster one adapts to these changing dynamics, the faster is one expected to

gain the advantage. In this article, Richer try to study the reasons behind the euphemism regarding the

Retail-focus of the Indian banks and try to assess how much of it is worth the attention that it is

attracting. Retail banking means banking in which banking institutions undertake transactions directly

with consumers, rather than corporations or other banks. Services offered include: savings and

transactional accounts, mortgages, personal loans, debit cards, credit cards, and so forth. Retail lending

is a part of retail banking which is conceptually similar in characteristics.

POTENTIAL FOR RETAIL IN INDIA: IS SKY THE LIMIT

The Indian players are bullish on the Retail business and this is not totally unfounded. There are two

main reasons behind this. Firstly, it is now undeniable that the face of the Indian consumer is changing.

This is reflected in a change in the urban household income pattern. The direct fallout of such a change

will be the consumption patterns and hence the banking habits of Indians, which will now be skewed

towards Retail products. At the same time, India compares pretty poorly with the other economies of the

world that are now becoming comparable in terms of spending patterns with the opening up of our

economy. For instance, while the total outstanding Retail loans in Taiwan is around 41% of GDP, the

figure in India stands at less than 5%.

The comparison with the West is even more staggering. Another comparison that is natural when

comparing Retail sectors is the use of credit cards. Here also, the potential lies in the fact that of all the

2

consumer expenditure in India in 2001, less than 1% was through plastic, the corresponding US figure

standing at 18%. Going by international standards, a large portion of the Indian population is simply not

“bankable” – taking profitability into consideration. On the other hand, the financial services market is

highly over-leveraged in India. Competition is fierce, particularly from local private banks such as

HDFC and ICICI, in the business of home, car and consumer loans. There, precisely lie the pitfalls of

such explosive growth.

Competitive Analysis: The fact that the statistics reveal a huge potential also brings with it a threat that is true for any sector of

a country that is opening up. Just how competitive are our banks? Is the threat of getting drubbed by

foreign competition real? To analyze this, one needs to get into the shoes of the foreign banks. In other

words, how do they see us? Are we good takeover targets?

Going by international standards, a large portion of the Indian population is simply not “bankable” –

taking profitability into consideration. On the other hand, the financial services market is highly over-

leveraged in India. Competition is fierce, particularly from local private banks such as HDFC and ICICI,

in the business of home, car and consumer loans. There, precisely lie the pitfalls of such explosive

growth. All banks are targeting the fluffiest segment i.e. the upwardly mobile urban salaried class.

Although the players are spreading their operations into segments like self- employed and the semi-

urban rich, it is an open secret that the big city Indian yuppies form the most profitable segment. Over-

dependence on this segment is bound to bring in inflexibility in the business. There are few documents

that get the attention of product planners and marketers the way that a competitive analysis does. A good

competitive analysis is a scouting report of the actual market terrain that your company must navigate in

order to be successful. The analysis begins with a list of your company's competitors. Most of the time,

such a list is comprised of what your company considers to be its chief competitors. However, there may

be other companies that indirectly compete with yours, ones that offer products or services that are

aiming for the same customer capital.

3

What according to you would be the next big thing to happen in the Indian retail

banking sector

Outsourcing! If you are a keen observer of the market, you would notice that every sector, including big

industrial sectors like car manufacturers, have gone for outsourcing their requirements. Over a period,

those players who have gone aggressive on outsourcing have found that it saves them not only cost and

time but helps them concentrate on their core business area, a key survival necessity in these times of

economic downturns.

Industry profile The Economic Survey of India is a document presented to Parliament by the government a few days before the Union Budget. It is an analysis of the state of the economy and its prospects. Economists and analysts scan it closely because it very often reflects policy changes that will be announced in the Budget.

Economic Survey 2010-11, tabled in Parliament on February 25, had this to say about the retail sector: “Permitting FDI (foreign direct investment) in retail in a phased manner beginning with metros and incentivizing the existing retail shops to modernize could help address the concerns of farmers and consumers. FDI in retail may also help bring in technical know-how to set up efficient supply chains which could act as models of development in India retail banking sector

BANKING IN INDIA

Retail credit outstanding as on March 22, 2003, amounted to Rs 1,60,000 crore. According to one

estimate, the retail segment is expected to grow at 30-40% in the coming years.

Major Players: HDFC Bank, AXIS Bank, IDBI Bank and ICICI Bank. Banking in India in the modern

sense originated in the last decades of the 18th century. The first banks were Bank of Hindustan (1770-

1829) and The General Bank of India, established 1786 and since defunct. The largest bank, and the

oldest still in existence, is the State Bank of India, which originated in the Bank of Calcutta in June

1806, which almost immediately became the Bank of Bengal. This was one of the three presidency

banks, the other two being the Bank of Bombay and the Bank of Madras,

4

all three of which were established under charters from the British East India Company. They are

generally subject to minimum capital requirements based on an international set of capital standards,

known as the Basel Accords. Banking in its modern sense evolved in the 14th century in the rich cities

of Renaissance Italy but in many ways was a continuation of ideas and concepts of credit and

lending that had its roots in the ancient world. In the history of banking, a number of banking

dynasties have played a central role over many centuries.

What about the foreign giants

The foreign banks have identified this problem but there are certain systematic risks involved in operating in the

Retail market for them. These include regulatory restrictions that prevent them from expanding their branch

network.

So these banks often take the Direct Selling Agent (DSA) route whereby low-end jobs like sourcing or

transaction processing are outsourced to small regional layers. So now on, when you see a loan mela or a

road show showcasing the retail bouquet of an elite MNC giant, you know that a significant commission

earned out of any such booking gets ploughed back to our own economy. Perhaps, one of the biggest

impediments in foreign players leveraging the Indian markets is the absence of positive credit bureaus.

In the west the risk profile can be easily mapped to things like SSNs and this information can be

publicly traded. PAN is a step in this direction but lot more work need to be done. What has been a

positive step towards this is a negative file sharing started by a consortium of 11 banks. However, as a

McKinsey study points out actual write-offs on NPAs show a strong negative correlation with sharing of

positive information. On top of this, the spend-now-pay-later “credit culture” in India is just not picking

up.

So all for the keeping then

This will perhaps be the most wrongful inference that can be drawn from the above. We just cannot

afford to look inwards and repeat the mistakes that were the side effects of the Nationalization of the

Banking System. A growing market can never be an alibi for lack of innovation.

5

Indian banks have shown little or no interest in innovative tailor-made products. A case in point is the

successful implementation of micro-credit networks in Bangladesh. Positioning a bank as a tech-savvy

financial vendor in a country where Internet penetration is an abysmal 1.65% can only add to the over-

leveraging as pointed out earlier. The focus of the sector should remain in macroeconomic wealth

creation and not increasing the per capita indebtedness that will do little but add to the NPA burden.

Retail Banking in India has to be developed in the Indian way, notwithstanding the long queues in front

of the teller counters in the Public sector banks.

PRODUCT RANGE

PRODUCT/SERVICES PROFILE OF S.B.I

1. Current account

-CA30000

-CA70000

-CA200000

-CA500000

2. Savings account

-Silver savings account

-Gold savings account

3. FIXED DEPOSIT

4. Smart Saver

6

5. Smart Access

6. Nonresident account (different variant)

CURRENT ACCOUNTS .Current Account is primarily meant for the purpose of facilitating business transactions. current

account is one of the two primary components of the balance of payments, the other being capital

account. It is the sum of the balance of trade. The difference between a nation’s savings and its

investment. The current account is an important indicator about an economy's health. It is defined as the

sum of the balance of trade (goods and services exports less imports), net income from abroad and net

current transfers. A positive current account balance indicates that the nation is a net lender to the rest of

the world, while a negative current account balance indicates that it is a net borrower from the rest of the

world. A current account surplus increases a nation’s net foreign assets by the amount of the surplus,

and a current account deficit decreases it by that amount. The current account and the capital account are

the two main components of a nation’s balance of payments. A nation’s current account balance is

influenced by numerous factors – its trade policies, exchange rate, competitiveness, forex reserves,

inflation rate and others.

Current Accounts – Benefits The main benefit of Current Account is its high liquidity and also provides safety of funds to the

customer. Current account serves as a low cost of funds for the Bank, provides an opportunity for cross

sell and creates stickiness / engagement of the customer because of their transactional nature. One of the

compulsory requirements when starting a business is that of opening a Current Bank account. It is ideal

for carrying out day-to-day business transactions. And with more and more banks dishing out attractive

features to add customers, businesses are spoilt for choice. Facilities like 24-hour Phone-Banking, Net-

Banking, Doorstep-Banking, Instant Alert services, free Demand-Drafts/Pay-Orders are commonplace

and almost ‘by default’ these days.

7

A current account is generally best suited for managing day to day transactions, while a savings account

provides a safe and potentially profitable home for your extra cash.

Most current accounts allow you to set up automatic payments - including direct debits and standing

orders - issue cheques and provide a debit card that you can use to withdraw cash and pay for goods and

services.

CA 30

Features 1. Swift & Convenient Cheque Collections at SBI Bank Locations as well as 2500 Correspondent

Bank Locations

2. AQT/AQB Criterion for evaluating Non-Maintenance Charges

3. Doorstep Banking allowing pickup and delivery of cash and instruments

4. CMS Services

5. Corporate Net Banking with bulk upload facility

6. Flat and aggressive transaction charges for Pay Orders, Demand Drafts, RTGS, Online RTGS,

Foreign Outward Remittances (non-trade)

CA 70

Features 7. Swift & Convenient Cheque Collections at S.B.I Bank Locations as well as 2500 Correspondent

Bank Locations

8. AQT/AQB Criterion for evaluating Non-Maintenance Charges

9. Doorstep Banking allowing pickup and delivery of cash and instruments

8

10. CMS Services

11. Corporate Net Banking with bulk upload facility

12. Mobile banking availability.

Flat and aggressive transaction charges for Pay Orders, Demand Drafts, RTGS, Online RTGS, Foreign

Outward Remittances (non-trade)

CA 200

Features 13. Swift & Convenient Cheque Collections at S.B.I Bank Locations as well as 2500 Correspondent

Bank Locations

14. AQT/AQB Criterion for evaluating Non-Maintenance Charges

15. Doorstep Banking allowing pickup and delivery of cash and instruments

16. CMS Services

17. Corporate Net Banking with bulk upload facility

18. Flat and aggressive transaction charges for Pay Orders, Demand Drafts, RTGS, Online RTGS,

Foreign Outward Remittances (non-trade)

19. S.B.I Business Gold Card providing a cash withdrawal limit of Rs 1 lacs

CA 500

Features 20. Swift & Convenient Cheque Collections at S.B.I Bank Locations as well as 2500 Correspondent

Bank Locations

21. AQT/AQB Criterion for evaluating Non-Maintenance Charges

22. Free Personalized PAP Cheque Books (limits as per account variant)

9

23. Doorstep Banking allowing pickup and delivery of cash and instruments

24. CMS Services

25. Corporate Net Banking with bulk upload facility

26. Flat and aggressive transaction charges for Pay Orders, Demand Drafts, RTGS, Online RTGS,

Foreign Outward Remittances (non-trade)

27. S.B.I Business Gold Card allowing a cash withdrawal limit of Rs 1 lacs.

SAVINGS ACCOUNTS Savings Bank Accounts are meant to promote the habit of saving among the citizens while allowing

them to use their funds when required. Savings accounts are opened for purpose of personal banking

transactions. Saving accounts are accounts maintained by retail financial institutions that pay interest but

cannot be used directly as money in the narrow sense of a medium of exchange. These accounts let

customers set aside a portion of their liquid assets while earning a monetary return.

Savings Accounts – Benefits The main advantage of Savings Bank Account is its high liquidity and safety. Savings account serves as

a low cost of funds for the Bank, provides a platform for cross sell and creates stickiness / engagement

of the customer because of its transactional nature. While savings accounts aren't typically known for

their high interest rates, they do offer numerous advantages over other savings options. Consider these

savings account advantages before putting your money in a CD or other investments.

Savings accounts and money market accounts allow you to withdraw your money at any time, which is

rarely an option with CDs or long-term investment options. Savings accounts allow for unlimited

withdrawals by teller, mail or ATM, but federal regulations limit you to six telephone, electronic or

preauthorized transfers per month. Keep in mind, only three of these withdraw.

10

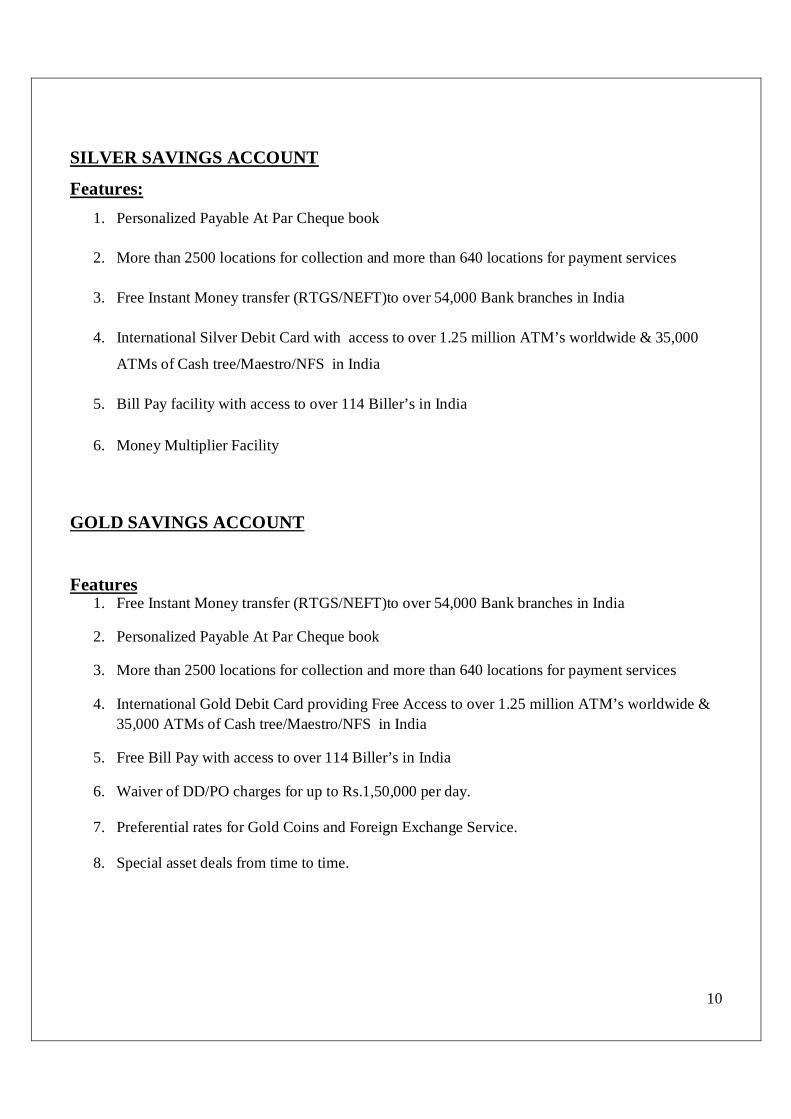

SILVER SAVINGS ACCOUNT

Features: 1. Personalized Payable At Par Cheque book

2. More than 2500 locations for collection and more than 640 locations for payment services

3. Free Instant Money transfer (RTGS/NEFT)to over 54,000 Bank branches in India

4. International Silver Debit Card with access to over 1.25 million ATM’s worldwide & 35,000

ATMs of Cash tree/Maestro/NFS in India

5. Bill Pay facility with access to over 114 Biller’s in India

6. Money Multiplier Facility

GOLD SAVINGS ACCOUNT Features

1. Free Instant Money transfer (RTGS/NEFT)to over 54,000 Bank branches in India

2. Personalized Payable At Par Cheque book

3. More than 2500 locations for collection and more than 640 locations for payment services

4. International Gold Debit Card providing Free Access to over 1.25 million ATM’s worldwide & 35,000 ATMs of Cash tree/Maestro/NFS in India

5. Free Bill Pay with access to over 114 Biller’s in India

6. Waiver of DD/PO charges for up to Rs.1,50,000 per day.

7. Preferential rates for Gold Coins and Foreign Exchange Service.

8. Special asset deals from time to time.

11

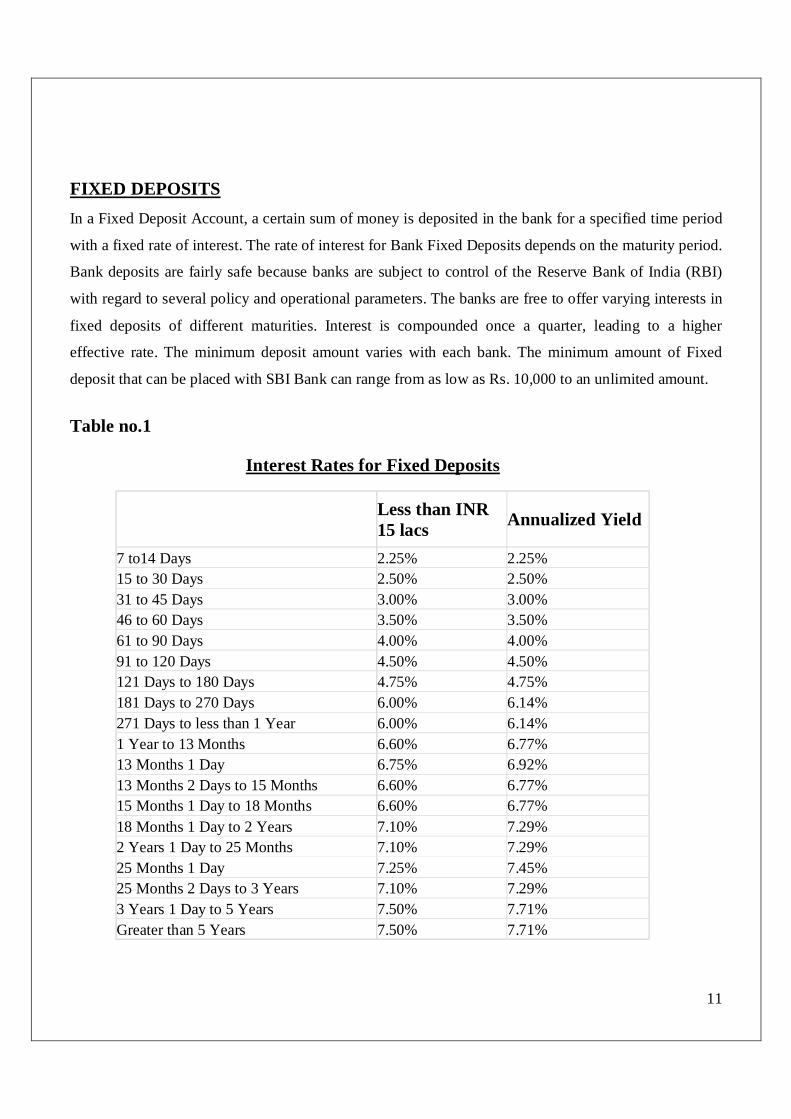

FIXED DEPOSITS In a Fixed Deposit Account, a certain sum of money is deposited in the bank for a specified time period

with a fixed rate of interest. The rate of interest for Bank Fixed Deposits depends on the maturity period.

Bank deposits are fairly safe because banks are subject to control of the Reserve Bank of India (RBI)

with regard to several policy and operational parameters. The banks are free to offer varying interests in

fixed deposits of different maturities. Interest is compounded once a quarter, leading to a higher

effective rate. The minimum deposit amount varies with each bank. The minimum amount of Fixed

deposit that can be placed with SBI Bank can range from as low as Rs. 10,000 to an unlimited amount.

Table no.1

Interest Rates for Fixed Deposits

Less than INR 15 lacs Annualized Yield

7 to14 Days 2.25% 2.25% 15 to 30 Days 2.50% 2.50% 31 to 45 Days 3.00% 3.00% 46 to 60 Days 3.50% 3.50% 61 to 90 Days 4.00% 4.00% 91 to 120 Days 4.50% 4.50% 121 Days to 180 Days 4.75% 4.75% 181 Days to 270 Days 6.00% 6.14% 271 Days to less than 1 Year 6.00% 6.14% 1 Year to 13 Months 6.60% 6.77% 13 Months 1 Day 6.75% 6.92% 13 Months 2 Days to 15 Months 6.60% 6.77% 15 Months 1 Day to 18 Months 6.60% 6.77% 18 Months 1 Day to 2 Years 7.10% 7.29% 2 Years 1 Day to 25 Months 7.10% 7.29% 25 Months 1 Day 7.25% 7.45% 25 Months 2 Days to 3 Years 7.10% 7.29% 3 Years 1 Day to 5 Years 7.50% 7.71% Greater than 5 Years 7.50% 7.71%

12

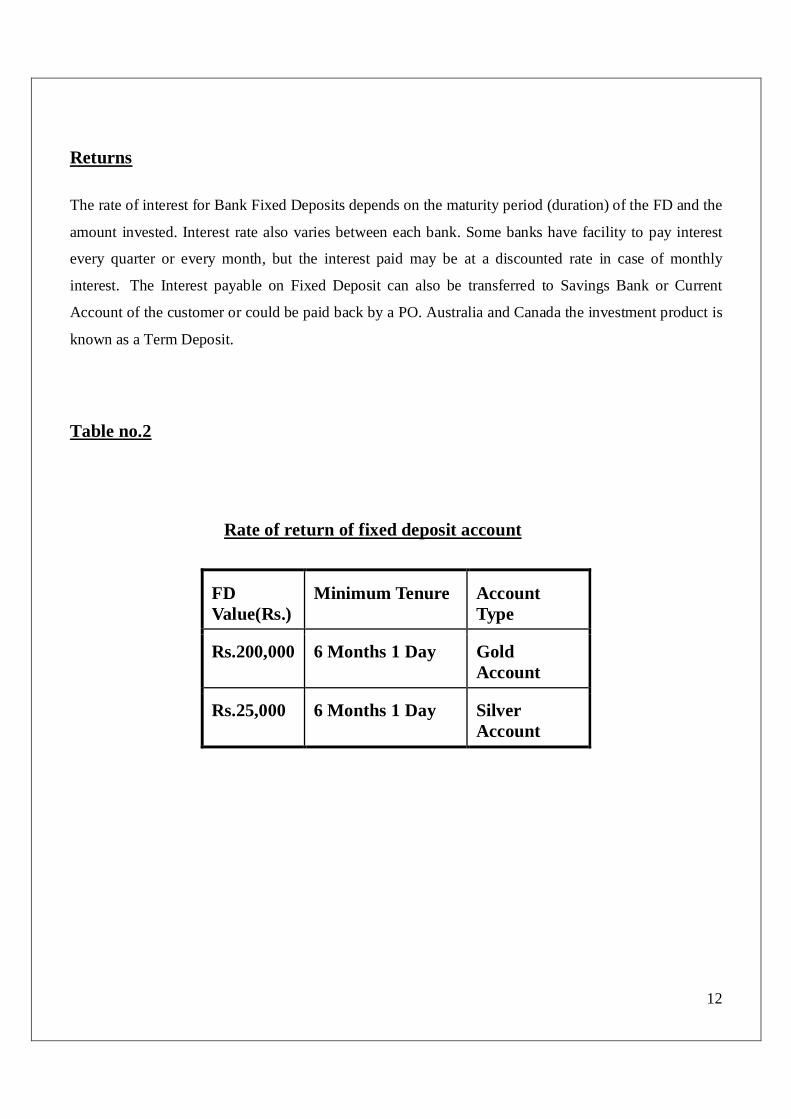

Returns

The rate of interest for Bank Fixed Deposits depends on the maturity period (duration) of the FD and the

amount invested. Interest rate also varies between each bank. Some banks have facility to pay interest

every quarter or every month, but the interest paid may be at a discounted rate in case of monthly

interest. The Interest payable on Fixed Deposit can also be transferred to Savings Bank or Current

Account of the customer or could be paid back by a PO. Australia and Canada the investment product is

known as a Term Deposit.

Table no.2

Rate of return of fixed deposit account

FD Value(Rs.)

Minimum Tenure Account Type

Rs.200,000 6 Months 1 Day Gold Account

Rs.25,000 6 Months 1 Day Silver Account

13

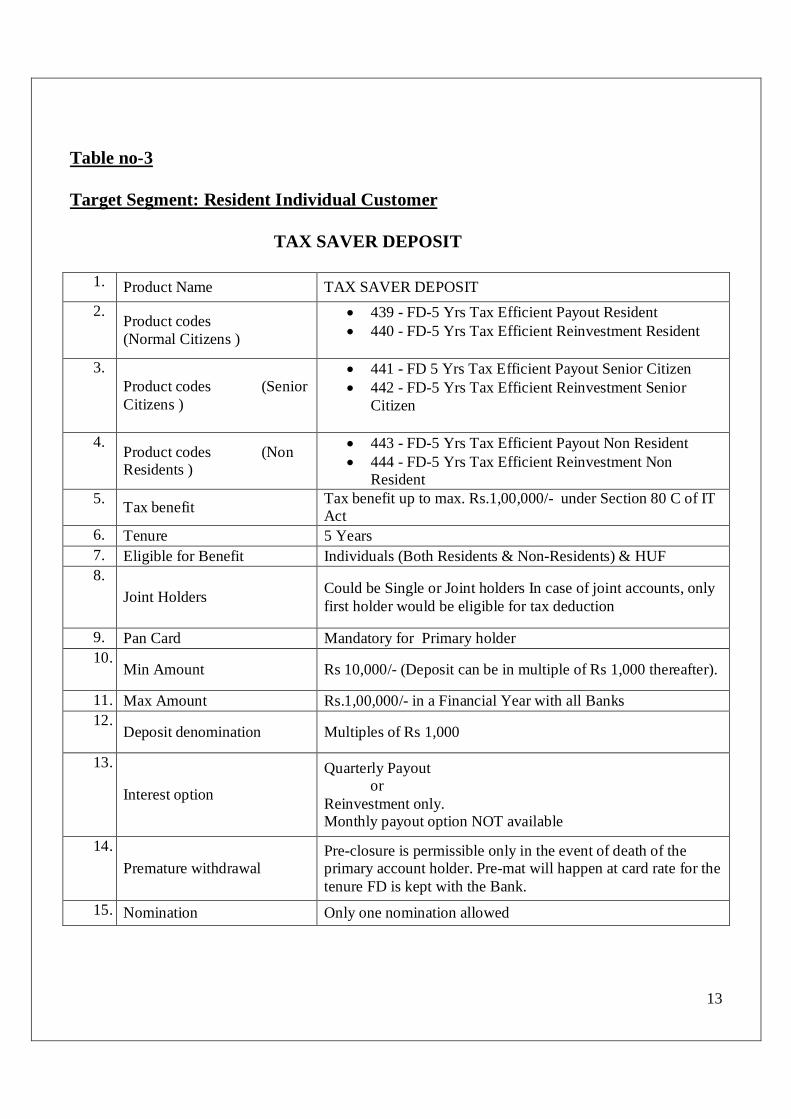

Table no-3 Target Segment: Resident Individual Customer

TAX SAVER DEPOSIT

1. Product Name TAX SAVER DEPOSIT 2. Product codes

(Normal Citizens )

439 - FD-5 Yrs Tax Efficient Payout Resident 440 - FD-5 Yrs Tax Efficient Reinvestment Resident

3.

Product codes (Senior Citizens )

441 - FD 5 Yrs Tax Efficient Payout Senior Citizen 442 - FD-5 Yrs Tax Efficient Reinvestment Senior

Citizen

4. Product codes (Non Residents )

443 - FD-5 Yrs Tax Efficient Payout Non Resident 444 - FD-5 Yrs Tax Efficient Reinvestment Non

Resident 5. Tax benefit Tax benefit up to max. Rs.1,00,000/- under Section 80 C of IT

Act 6. Tenure 5 Years 7. Eligible for Benefit Individuals (Both Residents & Non-Residents) & HUF 8.

Joint Holders Could be Single or Joint holders In case of joint accounts, only first holder would be eligible for tax deduction

9. Pan Card Mandatory for Primary holder 10.

Min Amount Rs 10,000/- (Deposit can be in multiple of Rs 1,000 thereafter).

11. Max Amount Rs.1,00,000/- in a Financial Year with all Banks 12.

Deposit denomination Multiples of Rs 1,000

13.

Interest option

Quarterly Payout or Reinvestment only. Monthly payout option NOT available

14. Premature withdrawal

Pre-closure is permissible only in the event of death of the primary account holder. Pre-mat will happen at card rate for the tenure FD is kept with the Bank.

15. Nomination Only one nomination allowed

14

RECURRING DEPOSIT

Given the volatility and risk of capital and return across various investment options, customers look for

avenues to park funds with assured returns and safety of principal. Recurring Deposit scheme enables

the depositor to make a financial provision by paying equated monthly installments for a pre-agreed

period. At the end of pre-determined period you are paid back the lump sum including the principal and

interest.

Features and benefits of Recurring Deposit 1. Open a Recurring Deposit with a minimum monthly installment of Rs 1,000

2. Choose the convenience of duration between minimum 6 months to maximum 2 years.

3. Lock your interest rate now for future bookings (identical to the Term Deposit interest rates).

4. Senior citizens get an extra benefit in the interest rates (extra 50 basis points).

5. Non-applicability of Tax Deduction at Source (TDS).

6. Encourages savings without stress on customer’s finances.

7. Easy way of paying monthly installment by providing a onetime standing instruction from customers

S.B.I Bank Savings Account.

SMART ACCESS Money kept in the Savings Account earns a lower rate of interest vis a vis the same if placed as a Term

Deposit. Money in the Savings account provides liquidity and cover for day to day or immediately

foreseeable expenses. SMART ACCESS account gives you the flexibility by linking your term

deposit(s) to your savings or current account. Whenever there is a need of funds, the same is swept in

from the linked term deposit to meet the requirements.

15

Features & Benefits 1. Earn high Term Deposit interest rates on your savings

2. Enjoy the flexibility of a S.B.I Bank Savings Account or a Current Account.

3. Get easy access to you money whenever you need it through a ATM or any S.B.I Bank branch

4. Your Deposit is broken in multiples of Re 1

5. Link multiple Term Deposits to your account.

6. Get a personalized cheque book in the Savings Account

7. Your complete access to your account related information on your fingertips with our phone

banking services.

8. No extra fee or cost will be charged to the customer for this facility. The Savings/Current

Account AQB requirements as well as associated service charges will be as per applicable

Schedule of Charges.

9. All unassisted transactions through telephone banking 10. Internet transactions not from an overseas merchant.

DEBIT/ATM CARDS

1. FREE Unlimited Access to over 19000 ATMs across India

2. Free Unlimited Access to over 1.25 million MasterCard ATM’s worldwide and over 19,000

ATM’s in India

16

3. 1st Indian debit card to offer 0% surcharge on fuel purchases at any petrol pump in India- instant

2.5% saving

4. Daily cash withdrawal limit of Rs. 75,000 & purchase limit of Rs.75,000

5. International transactions are always reflected in Indian Rupees

6. Free access to clipper lounges at Airports in major metros

7. State Bank of India offers unparalleled convenience through State Bank ATM-cum-Debit card.

With this card, there is no need to carry cash in your wallet.

MasterCard

1. FREE Unlimited Access to over 19000 ATMs

2. Daily cash withdrawal limit of Rs. 40,000 & purchase limit of Rs. 40,000

3. Instant updating of account to reflect your debit card transactions. Keeping you in the know, so

you can manage your money better

4. International transactions are always reflected in Indian Rupees

5. Annual fee of only Rs149

6. Zero interest or service charge will be charged.

7. Mostly known its service in India.

8. Easy to use by any customer.

17

1. India’s most economical US$ Travel Card: Low fees and cross-currency exchange mark-up not

applicable in U.S.

2. FREE Access to over 9000 Chase ATMs in the U.S.

MOBILE BANKING 1. S.B.I Bank is going to provide its customer a service where they can transfer money, send money

and pay utility bills through their mobile phone. This will be an addition to the existing Mobile

banking facility.

2. The S.B.I BANK OBOPAY Mobile Payment Solution is a mobile payment service by S.B.I

BANK that lets you Send, Spend and Get Money to/from any of the 240+ million mobile phones

in India (provided they are registered users of this service and have a bank account with S.B.I

BANK or any of the partner banks).

Process at the branch 1. For getting registered on the Obopay network customer needs to fill up the application form and

submit the same at the nearest S.B.I Bank branch.(Application form attached)

2. Branch will verify the signature of the customer against the signature present in the FCR

3. Post signature verification branch official will affix a date and time of receipt of application

along with his signatures.

4. Verified forms will be sent to the NOC Mumbai attention to DB Ops team under a covering

schedule.

18

NET BANKING

NET BANKING SETUP FOR RETAIL AND CORPORATE

Retail Net Banking Setup

Retail net banking setup is done for those customers who have not opted for a Debit Card but wish to

avail a Net Banking facility.

Receipt of Data

1. Account opening team receives the forms from the various branches for opening the customer

accounts.

2. Data for customers who have not opted for Debit Card but wish to avail a Net Banking facility is

collated by the account opening team on excel.

3. Data collated at Day 0 till EOD is forward to DB Ops team via mail

4. DB Ops on Day 1 utilizes this data for setting up of Retail Net Banking facility for the customer

through FLEX@ Retail admin module

5. Customer can also submit a letter at the branch for availing net banking facility

6. Branch needs to verify the signature and affix the branch stamp on the letter which is then send

across to DB Ops.

19

Processing of request 1. Retail Net Banking Set up for the mentioned customers is done by in putter in the retail admin

2. After the setup is complete details of the customers are forwarded to the authorizer

3. Authorizer cross checks data provided by the account opening team with the data input done in

the retail admin module

4. On proper verification of the details the data input done is authorized

Corporate Net Banking Setup

Documents required

View Only facility

1. Duly Completed Channel Registration form.

2. Form should be signed as per the mode of operation in the account

Transaction Access

1. Duly Completed Channel Registration form

2. Form Duly Completed Channel Registration form

3. Form should be signed as per the mode of operation in the account

4. Board Resolution for net banking in Desired Format

5. Duly filled bulk upload forms mentioning the payment type & debit account number

signed as per the mode of operation

6. should be signed as per the mode of operation in the account

7. Board Resolution for net banking in Desired Format

20

Factor Authentication 1. Duly Completed Channel Registration form

2. Form should be signed as per the mode of operation in the account

3. 2 Factor authentication should be ticked on the user profile form

4. Email Id of the customer is required to be mentioned on setup form

5. Setup will be done in Port wise for sending the SEED and PIN at the email id provided by the

customer

Note: All the channel registration forms should have the company stamp

Branch to affix date and time stamp on the channel registration form

Receipt of documents

1. Branch to send the complete set of form along with the checklist under a covering schedule

to DB Ops

2. A soft copy of the covering schedule is also sent over email to DB Ops.

3. DB Ops sends acknowledgement over e mail to the branch and updates the record on the ftp

site.

PROCESS FOR BILL PAYMENT

1. S.B.I Bank is providing its customer a service to pay their bills and make charity/subscription

payments through the Internet.

2. This is an extension to the existing Internet Banking facility.

3. All individual customers who have the right to conduct financial transactions in their account

are eligible for this facility.

21

Customer Payment Process

Customer Registration

1. The customer needs to register for each Biller separately before paying the bills through Net

Banking

2. For registration customer needs to submit unique identifiers as per the specifications given by

individual Biller.

3. If the Biller is a Payment type biller, customer can immediately start paying bills after successful

registration

4. If the Biller is a presentment type biller, then the customer will be able to view all the bills

pertaining to the said Biller from the next billing cycle, after successful registration.

5. Customer will able to view and pay presentment type bills under “View & Pay ” option

Payment Process 1. Customer can pay the bill through PAY option in the Bill Pay page

2. Once the customer provides a confirmation for payment of the bill following entry is passed by

the system

A. Customer account Dr --------- Biller account Cr

3. Transactions done by Customers till 11:59:59 pm Day 0 are processed on working Day 1.

4. Transactions done after 12 pm are processed on the next working day.

22

Research design

TITLE OF PROJECT

“A Study on Effectiveness of Retail banking with special reference to”

“STATE BANK OF INDIA”

STATEMENT OF THE PROBLEM As there is an immense opportunity of the retail banking in India. This Dissertation is on the issues and

challenges in the retail banking because of the competition of the various banks and the customer

satisfaction of the services which the banks are providing and at the same time to solve the complaints of

the customer and maintaining the sound relationship for the future and by this way to estimate the future

growth of the retail banking. As service quality reflects the way the banks are performing, this study

attempts to explore the perception of customers in respect to the services provided by the

Banks. The entry of private and foreign banks, the nature of functioning of these banks and the

promotional attempts of these banks has changed the landscape of the Banking sector in India. In

respect to customer services there are notable perceived differences. Hence this study on customer

service quality of Indian banks looks for bringing out the differences between perceptions of

customers of these banks. This study is descriptive and analytical in nature.

23

OBJECTIVES OF STUDY

1. To study the issues and challenges in retail banking

2. To study the recent trends in retail banking

3. To ensure high satisfaction level and reduce percentage of complaints of customers in retail

banking.

4. To estimate the future growth of Indian retail banking.

5. To understand Optimization of retail banking channels.

6. To suggest strategies for improvement in Customer Service. 7. To make suggestions for improvement of quality of services in public, private and foreign

Banks.

8. To find the gap between customers expectations and perceptions of quality of services for Public private and foreign banks.

DATA COLLECTION

The study relies on both primary as well as secondary data. The source of the secondary data is

Drawn from State Bank of India publications and the sites of the banks to which respondents

are customers. Various journal articles have been referenced for understanding the background

of the study. For obtaining primary data, a structured questionnaire is designed to collect data

from customers of Banks. The questionnaire consisted of four parts. Part A had 26 statements

on 6 dimensions to measure the expectations of the customers. Part B consisted of the profile of

the customers; Part C had 26 statements on 6 dimensions to measure the perception of the

Customers of the banks. Part D had open ended questions to avail insights into the

perceptions of the customers. The responses for the statements in Part A and C were

Measured on a likert scale of servqual tool. An interview schedule is prepared to collect data

from Bankers. In depth interviews are conducted with the help of the interview schedule

.

24

Data was collected from two sources-primary and secondary sources.

1. Primary data collection- The primary data was collected by means of survey. It was collected

from different customers through questionnaire.

2. Secondary data collection-This data was collected from Internet, Company’s websites &

Magazines etc.

SAMPLE SIZE

Sample size was restricted to 100 respondents, since it was not possible to cover the whole universe in

the available reference period.

SAMPLING METHOD

Convenience Sampling has been used to collect the data because time limit for the completion of the

work is limited and also managers and employees were not available all the time.

Area of Study- MYSORE

Duration- 2 months

25

LIMITATIONS OF THE STUDY

1. The limitation of the study is lack of information being provided by the staff of the bank because

of the privacy policy of the bank.

2. In my two month project work, I have learnt how the S.B.I Bank runs its huge organization with

the support from various departmental wings.

3. One of the factors of the study was lack of time if it will be more than four months.

26

BANKING IN INDIA

Retail credit outstanding as on March 22, 2003, amounted to Rs 1,60,000 crore. According to one

estimate, the retail segment is expected to grow at 30-40% in the coming years.

Major Players: State Bank of India, HDFC Bank, UTI Bank, IDBI Bank and ICICI Bank.

What about the foreign giants

The foreign banks have identified this problem but there are certain systematic risks involved in operating

in the Retail market for them. These include regulatory restrictions that prevent them from expanding their

Branch network.

So these banks often take the Direct Selling Agent (DSA) route whereby low-end jobs like sourcing or

transaction processing are outsourced to small regional layers. So now on, when you see a loan mela or a

road show showcasing the retail bouquet of an elite MNC giant, you know that a significant commission

earned out of any such booking gets ploughed back to our own economy. Perhaps, one of the biggest

impediments in foreign players leveraging the Indian markets is the absence of positive credit bureaus.

In the west the risk profile can be easily mapped to things like SSNs and this information can be

publicly traded. PAN is a step in this direction but lot more work need to be done. What has been a

positive step towards this is a negative file sharing started by a consortium of 11 banks. However, as a

McKinsey study points out actual write-offs on NPAs show a strong negative correlation with sharing of

positive information. On top of this, the spend-now-pay-later “credit culture” in India is just not picking

up. A swift legal procedure against consumers creating bad debt is virtually non-existent. Finally, the

vast geographical and cultural diversity of the country makes credit policy formulation a tough job and it

simply cannot be dictated from a Wall Street or a Singapore boardroom! All these add up to the

unattractiveness of the Indian retail market to the foreign players. So over the past few years, in spite of

the entry of MNCs in many industries, Retail Banking has seen a flurry of panicky exits. Fewer than 40

remain in India and their share of total bank assets currently 7.2% is falling.

27

Those that remain might be thought to be likely buyers of Indian banks. Yet Citibank, HSBC and

Standard Chartered—all in India for more than a century, and with relatively large retail networks—

seem to have no pressing need to acquire a local bank. Established foreign banks have preferred to take

over customers or businesses from other foreign banks that want to leave. Thus HSBC, in recent years,

has o-Mitsubishi. ABN Amor took over Bank of America's retail business.

So all for the keeping then

This will perhaps be the most wrongful inference that can be drawn from the above. We just cannot

afford to look inwards and repeat the mistakes that were the side effects of the Nationalization of the

Banking System. A growing market can never be an alibi for lack of innovation. Indian banks have

shown little or no interest in innovative tailor-made products. A case in point is the successful

implementation of micro-credit networks in Bangladesh. Positioning a bank as a tech-savvy financial

vendor in a country where Internet penetration is an abysmal 1.65% can only add to the over-leveraging

as pointed out earlier.

The focus of the sector should remain in macroeconomic wealth creation and not increasing the per

capita indebtedness that will do little but add to the NPA burden. Retail Banking in India has to be

developed in the Indian way, notwithstanding the long queues in front of the teller counters in the Public

sector banks!

28

STATE BANK OF INDIA PROFILE

State Bank of India (SBI) is a multinational banking and financial services company

Based in India. It is a government-owned corporation with its headquarters

in Mumbai, Maharashtra. As of December 2013, it had assets of US$388 billion and

17,000 branches, including 190 foreign offices, making it the largest banking and

Financial Services Company in India by assets. State Bank of India is one of the Big Four banks of India, along with ICICI Bank, Punjab National

Bank and Bank of Baroda.

The bank traces its ancestry to British India, through the Imperial Bank of India, to the

founding in 1806 of the Bank of Calcutta, making it the oldest commercial bank in the Indian

Subcontinent. Bank of Madras merged into the other two presidency banks—Bank of Calcutta and Bank

of Bombay—to form the Imperial Bank of India, which in turn became the

State Bank of India. Government nationalized the Imperial Bank of India in 1955,

with Reserve Bank of India taking a 60% stake, and renamed it the State Bank of India. In 2008, the

government took over the stake held by the Reserve Bank of India.

SBI is a regional banking behemoth and has 20% market share in deposits and loans among Indian

commercial banks

History:

The roots of the State Bank of India lie in the first decade of 19th century, when the Bank of Calcutta,

later renamed the Bank of Bengal, was established on 2 June 1806. The Bank of Bengal was one of three

Presidency banks, the other two being the Bank of Bombay (incorporated on 15 April 1840) and the

Bank of Madras (incorporated on 1 July 1843). All three Presidency banks were incorporated as Joint

stock company/joint stock companies and were the result of the royal charters.

29

These three banks received the exclusive right to issue paper currency till 1861 when with the Paper

Currency Act, the right was taken over by the Government of India.

The Presidency banks amalgamated on 27 January 1921, and the re-organised banking entity took as its

name Imperial Bank of India. The Imperial Bank of India remained a joint stock company but without

Government participation

Pursuant to the provisions of the State Bank of India Act of 1955, the Reserve Bank of India, which is

Central Bank India’s central bank, acquired a controlling interest in the Imperial Bank of India. On 1

July 1955, the Imperial Bank of India became the State Bank of India. In 2008 the government of India

acquired the Reserve Bank of India's stake in SBI so as to remove any conflict of interest because the

RBI is the country's banking regulatory authority.

In 1959, the government passed the State Bank of India (Subsidiary Banks) Act, which made eight state

banks associates of SBI. A process of consolidation began on 13 September 2008, when the State Bank

of Saurashtra merged with SBI.

SBI has acquired local banks in rescues. The first was the Bank of Behar (est. 1911), which SBI

acquired in 1969, together with its 28 branches. The next year SBI acquired National Bank of Lahore

(est. 1942), which had 24 branches. Five years later, in 1975, SBI acquired Krishnaram Baldeo Bank,

which had been established in 1916 in Gwalior State, under the patronage of Maharaja Madho Rao

Scindia. The bank had been the ''Dukan Pichadi'', a small moneylender, owned by the Maharaja. The

new banks first manager was Jall N. Broacha, a Parsi. In 1985, SBI acquired the Bank of Cochin in

Kerala, which had 120 branches. SBI was the acquirer as its affiliate, the State Bank of Travancore,

already had an extensive network in Kerala.

The State Bank of India and all its associate banks are identified by the same blue ''keyhole'' logo. The

State Bank of India wordmark usually has one standard typeface, but also utilises other typefaces.

30

OPERATION:

SBI provides a range of banking products through its network of branches in India and overseas,

including products aimed at non-resident Indians (NRIs). SBI has 14 regional hubs and 57 Zonal Offices

that are located at important cities throughout India.

Summary of Seal:

31

Domestic presence

SBI had 14,816 branches in India, as on 31 March 2013, of which 9,851 (66%) were in Rural and Semi-

urban areas. In the financial year 2012-13, its revenue was INR 200,560 Crores (US$ 36.9 billion), out

of which domestic operations contributed to 95.35% of revenue. Similarly, domestic operations

contributed to 88.37% of total profits for the same financial year.

International presence

As of 28 June 2013, the bank had 180 overseas offices spread over 34 countries. It has branches of the

parent in Moscow, Colombo, Dhaka, Frankfurt, Hong Kong, Tehran, Johannesburg, London, Los

Angeles, Male in the Maldives, Muscat, Oman|Muscat, Dubai, New York, Osaka, Sydney, and Tokyo. It

has offshore banking units in the Bahamas, Bahrain, and Singapore, and representative offices in Bhutan

and Cape Town. It also has an ADB in Boston, USA.

The Canadian subsidiary, State Bank of India (Canada) also dates to 1982. It has seven branches, four in

the Toronto area and three in the Vancouver area.

SBI operates several foreign subsidiaries or affiliates. In 1990, it established an offshore bank: State

Bank of India (Mauritius). SBI (Mauritius) has 15 branches in major cities/towns of the country

including Rodrigues.

In 1982, the bank established a subsidiary, State Bank of India (California), which now has ten branches

– nine branches in the state of California and one in Washington, D.C. The 10th branch was opened in

Fremont, California on 28 March 2011. The other eight branches in California are located in Los

Angeles, Artesia, San Jose, Canoga Park, Fresno, San Diego, Tustin and Bakersfield.

In Nigeria, SBI operates as INMB Bank. This bank began in 1981 as the Indo-Nigerian Merchant Bank

and received permission in 2002 to commence retail banking. It now has five branches in Nigeria.

32

In Nepal, SBI owns 55% of Nepal SBI Bank, which has branches throughout the country. In Moscow,

SBI owns 60% of Commercial Bank of India, with Canara Bank owning the rest. In Indonesia, it owns

76% of PT Bank Indo Monex.

The State Bank of India already has a branch in Shanghai and plans to open one in Tianjin.

In Kenya, State Bank of India owns 76% of Giro Commercial Bank, which it acquired for USD 8

million in October 2005.

Associate banks

SBI has five associate banks; all use the State Bank of India logo, which is a blue circle, and all use the

"State Bank of" name, followed by the regional headquarters' name:

1. State Bank of Bikaner & Jaipur

2. State Bank of Hyderabad

3. State Bank of Mysore

4. State Bank of Patiala

5. State Bank of Travancore

Earlier SBI had seven associate banks, all of which had belonged to Indian Princely States|princely

states until the government nationalised them between October 1959 and May 1960. In tune with the

first Five Year Plan, which prioritised the development of rural India, the government integrated these

banks into State Bank of India system to expand its rural outreach. There has been a proposal to merge

all the associate banks into SBI to create a "mega bank" and streamline the group's operations.The first

step towards unification occurred on 13 August 2008 when State Bank of Saurashtra merged with SBI,

reducing the number of associate state banks from seven to six.

33

Then on 19 June 2009 the SBI board approved the absorption of State Bank of Indore. SBI holds 98.3%

in State Bank of Indore. (Individuals who held the shares prior to its takeover by the government hold

the balance of 1.77 %.)

The acquisition of State Bank of Indore added 470 branches to SBI's existing network of branches. Also,

following the acquisition, SBI's total assets will inch very close to the (INR)10 trillion mark (10 billion

long scale). The total assets of SBI and the State Bank of Indore stood at INR 9,981,190 million as of

March 2009. The process of merging of State Bank of Indore was completed by April 2010, and the SBI

Indore branches started functioning as SBI branches on 26 August 2010.

Non-banking subsidiaries

Apart from its five associate banks, SBI also has the following non-banking subsidiaries:

1. SBI Capital Markets Ltd

SBI Capital Markets''' SBICAPS is an investment bank founded in August 1986. It is a wholly owned

subsidiary of State Bank of India (SBI).

Following the crash in MS Shoes share prices in March 1995, the Central Bureau of Investigation (CBI)

started an investigation.

In June 1997 the CBI sought permission from the government to lay charges against senior officials of

the Securities and Exchange Board of India and SBI Capital Markets.

The CBI alleged that senior officials had violated many guidelines and in the process had cheated

investors.

In January 1997 the Asian Development Bank acquired a 13.84% equity stake in SBICAPS.

This share was repurchased by State Bank of India in March 2010.

In January 2006 SBICAP and the international investment banking group CLSA announced a two-year

partnership to work on large joint deals in equity capital and mergers & acquisitions.

34

In September 2006 SBI Caps announced that it had set up a $100 million venture fund in partnership

with the venture capital division of SBI Holdings of Japan.

Air India ran into serious financial difficulties, and in July 2009 SBICAPS was asked by civil aviation

minister Praful Patel to prepare a road map to bring the carrier back into profitability. SBI Capital was

appointed the mandated firm to restructure Kingfisher Airlines loans during the Kingfisher Airlines

financial crisis, starting in 2010.

In February 2012 SBSCAP and other bank lenders were insisting that commissions paid to promoters be

reversed before they would consider providing further funding to the still-troubled airline.

In October 2006 R Sridhar and was appointed managing director and CEO of SBI Capital.

In July 2009 SBICAPS announced that S. Vishvanathan had replaced A.P. Verma as MD & CEO.

Vishvanathan had joined SBI in 1976, had helped set up SBI's New York branch, and had been chief

general manager of SBI’s North Eastern operations.

2. SBI Funds Management Pvt Ltd

3. SBI Factors & Commercial Services Pvt Ltd

4. SBI Cards & Payments Services Pvt. Ltd. (SBICPSL)

35

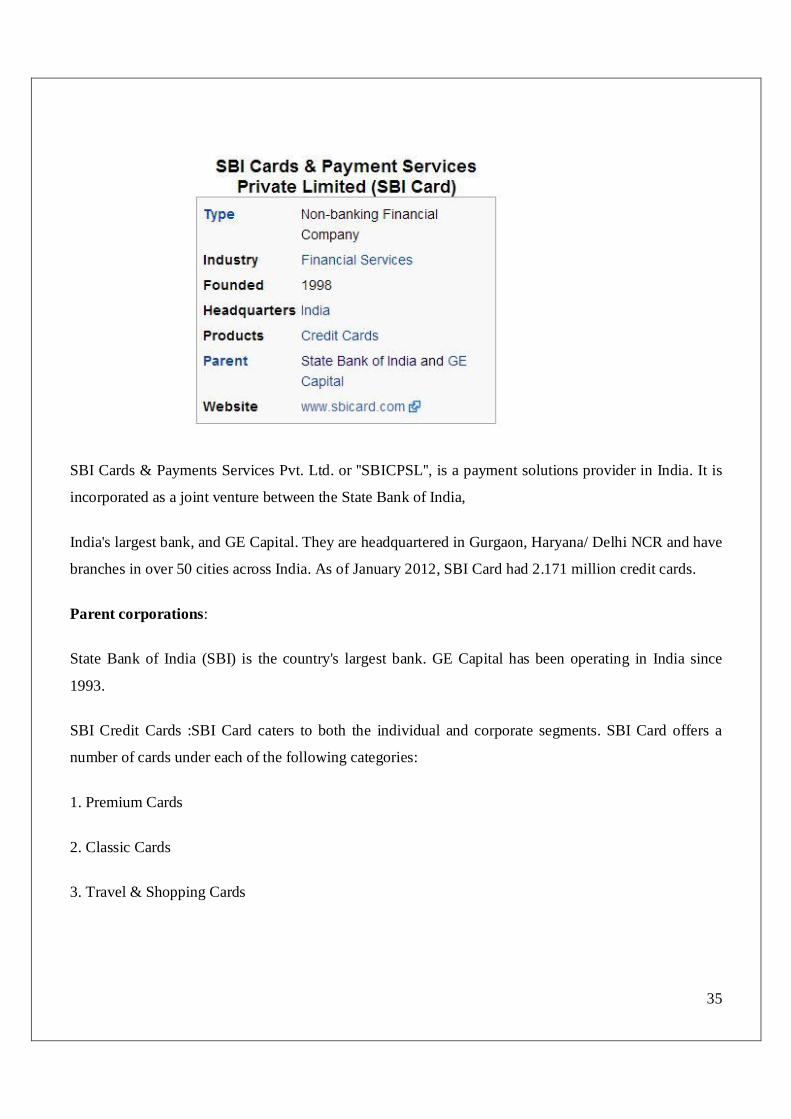

SBI Cards & Payments Services Pvt. Ltd. or ''SBICPSL'', is a payment solutions provider in India. It is

incorporated as a joint venture between the State Bank of India,

India's largest bank, and GE Capital. They are headquartered in Gurgaon, Haryana/ Delhi NCR and have

branches in over 50 cities across India. As of January 2012, SBI Card had 2.171 million credit cards.

Parent corporations:

State Bank of India (SBI) is the country's largest bank. GE Capital has been operating in India since

1993.

SBI Credit Cards :SBI Card caters to both the individual and corporate segments. SBI Card offers a

number of cards under each of the following categories:

1. Premium Cards

2. Classic Cards

3. Travel & Shopping Cards

36

4. Exclusive Cards

5. Corporate Cards

Logo

The SBI Card logo has the symbol of State Bank of India, which is a circle and not key hole and a small

man at the center of the circle.

5. SBI DFHI Ltd

6. SBI Life Insurance Company Limited

SBI Life Insurance''' is a joint venture life insurance company between State Bank of India (SBI), the

largest Government-owned corporation state-owned banking and financial services company in India,

and BNP Paribas Assurance. SBI owns 74% of the total capital and BNP Paribas Assurance the

remaining 26% of the capital. SBI Life Insurance has an authorized capital of INRConvert|20|band a

paid up capital of INRConvert|10|b.

37

History

When the government of India opened the life insurance sector to private companies, State Bank of

India |SBI started SBI Life as a joint venture with BNP Paribas in 2001. While in its initial stage its

business was mainly from bank assurance channel, now it is developing its own agency team for selling

its life insurance products.

7. SBI General Insurance

In March 2001, SBI (with 74% of the total capital), joined with BNP Paribas (with 26% of the remaining

capital), to form a joint venture life insurance company named SBI Life Insurance company Ltd.

In 2004, SBI DFHI (Discount and Finance House of India) was founded with its headquarters in

Mumbai.

Other SBI service points

SBI has 27,000+ Automated teller machine ATMs and SBI group (including associate banks) has

32,752 ATMs. SBI has become the first bank to install an ATM at Drass in the Jammu & Kashmir

Kargil region. This was the Bank's 27,032nd ATM on 27 July 2012.

Logo and slogan

* The logo of the State Bank of India is a blue circle with a small cut in the bottom that depicts

perfection and the small man the common man - being the center of the bank's business.

* Slogans: "PURE BANKING, NOTHING ELSE", "WITH YOU - ALL THE WAY", "A BANK OF

THE COMMON MAN", "THE BANKER TO EVERY INDIAN", "THE NATION BANKS ON US"

38

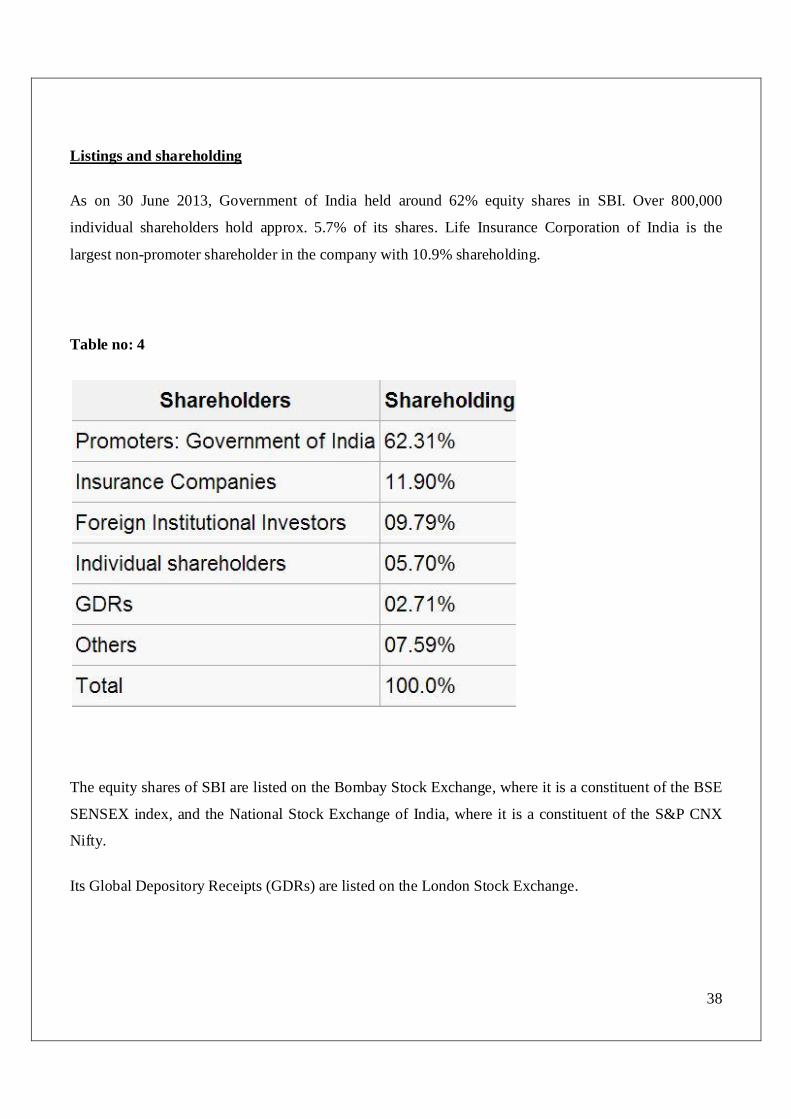

Listings and shareholding

As on 30 June 2013, Government of India held around 62% equity shares in SBI. Over 800,000

individual shareholders hold approx. 5.7% of its shares. Life Insurance Corporation of India is the

largest non-promoter shareholder in the company with 10.9% shareholding.

Table no: 4

The equity shares of SBI are listed on the Bombay Stock Exchange, where it is a constituent of the BSE

SENSEX index, and the National Stock Exchange of India, where it is a constituent of the S&P CNX

Nifty.

Its Global Depository Receipts (GDRs) are listed on the London Stock Exchange.

39

Employees:

SBI is one of the largest employers in the country having 228,296 employees as on 31st March 2013, out

of which there were 46,833 female employees (21%) and 2,402 disabled employees (1%). On the same

date, SBI had 43,550 Schedule Caste (19%) and 16,764 Schedule Tribe employees (7%).

Hiring drive

The bank hired 20,682 Assistants in FY 2012-13, from over 30 lakh applicants, for expansion of the

branch network and to mitigate staff shortage, particularly at rural and semi-urban branches. In the same

year, it recruited 847 probationary officers from around 17 lakh candidates which applied for officers’

position.

Staff productivity

As per its Annual Report for FY 2012-13, each employee contributed to revenues of INR 944 Lacs and

net profit of INR 6.45 Lacs.

Recent awards and recognitions

1. SBI was ranked 298th in the Fortune Global 500 rankings of the world's biggest corporations for

the year 2012.

2. SBI won "Best Public Sector Bank" award in the Dun & Bradstreet| D&B India's study on

'India's Top Banks 2013

3. State Bank of India won three IDRBT Banking Technology Excellence Awards 2013 for

“Electronic Payment Systems”, “Best use of technology for Financial Inclusion”, and “Customer

Management & Business Intelligence” in the large bank category.

4. SBI won National Award for its performance in the implementation of Prime Minister’s

Employment Generation Programme (PMEGP) scheme for the year 2012.

40

5. Best Online Banking Award, Best Customer Initiative Award & Best Risk Management Award

(Runner Up) by IBA Banking Technology Awards 2010

6. SKOCH Award 2010 for Virtual corporation Category for its e-payment solution.

7. SBI was the only bank featured in the "top 10 brands of India" list in an annual survey conducted

by Brand Finance and ''The Economic Times'' in 2010.

8. The Bank of the year 2009, India (won the second year in a row) by The Banker Magazine.

9. Best Bank – Large and Most Socially Responsible Bank by the Business Bank Awards 2009.

10. Best Bank 2009 by Business India

11. The Most Trusted Brand 2009 by The Economic Times.

12. SBI was named the 29th most reputed company in the world according to ''Forbes'' 2009

rankings.

13. Most Preferred Bank & Most preferred Home loan provider by CNBC.

14. Visionaries of Financial Inclusion By FINO.

15. Technology Bank of the Year by IBA Banking Technology Awards.

16. SBI was 11th most trusted brand in India as per the The Brand Trust Report|Brand Trust Report

2010.

41

Major competitors

Some of the major competitors for SBI in the banking sector are Axis Bank, ICICI Bank, HDFC Bank,

Punjab National Bank, Bank of Baroda, Canara Bank and Bank of India. However in terms of average

market share, SBI is by far the largest player in the market.

External links:

1. Official website, VIEWED ON 2ND JAN 2014

2. State Bank Of India on face book VIEWED ON 12th JAN 2014

3. News about State Bank of India at -The Times of India. VIEWED ON 17th JAN 2014

4. State Bank of India IFSC Codes & Branch Details Verified Manually. VIEWED ON 22ND JAN

2014

5. State Bank of India IFSC Codes, MICR Codes, Branch Codes and Branch Complete Details.

VIEWED ON 2ND FEB 2014

Business data :( finance links)

1. State Bank of India at Google finance.

2. State Bank of India at Reuters.

3. State Bank of India at Bombay Stock Exchange.

4. State Bank of India at National Stock Exchange of India.

42

State Bank of India is the largest state-owned banking and financial services company in India. The

Bank provides banking services to the customer. In addition to the banking services, the Bank through

their subsidiaries, provides a range of financial services, which include life insurance, merchant banking,

mutual funds, credit card, factoring, security trading, pension fund management and primary dealership

in the money market. The Bank operates in four business segments, namely Treasury, Corporate/

Wholesale Banking, Retail Banking and Other Banking Business. The Treasury segment includes the

investment portfolio and trading in foreign exchange contracts and derivative contracts. The Corporate/

Wholesale Banking segment comprises the lending activities of Corporate Accounts Group, Mid

Corporate Accounts Group and Stressed Assets Management Group. The Retail Banking segment

consists of branches in National Banking Group, which primarily includes personal banking activities,

including lending activities to corporate customers having banking relations with branches in the

National Banking Group. SBI provides a range of banking products through their vast network of

branches in India and overseas, including products aimed at NRIs. The State Bank Group, with over

16,000 branches, has the largest banking branch network in India. The State bank of India is the 10th

most reputed company in the world according to Forbes. The bank has 156 overseas offices spread over

32 countries. They have branches of the parent in Colombo, Dhaka, Frankfurt, Hong Kong,

Johannesburg, London and environs, Los Angeles, Male in the Maldives, Muscat, New York, Osaka,

Sydney, and Tokyo. They have offshore banking units in the Bahamas, Bahrain, and Singapore, and

representative offices in Bhutan and Cape Town. State Bank of India was incorporated in the year 1955.

The Bank traces their ancestry to British India, through the Imperial Bank of India, to the founding in

1806 of the Bank of Calcutta, making them the oldest commercial bank in the Indian Sub-continent.

The Government of India nationalized the Imperial Bank of India in the year 1955, with the Reserve

Bank of India taking a 60% stake, and name was changed to State Bank of India. In the year 2001, the

SBI Life Insurance Company was started by the Bank.

They are the only Bank that have been permitted 74% stake in the insurance business.

The Bank's insurance subsidiary 'SBI Life Insurance Company' is a joint venture with Cardiff S.A in

which Cardiff holds 26% of the stake. During the year 2005-06, the bank introduced 'SBI e-tax' an

online tax payments facility for direct and indirect tax payment.

43

They also launched the centralized pension processing. The Bank made a partnership with Tata

Consultancy Services for setup C-Edge Technologies and consulting services to the banking, financial

services and insurance industry. The bank was noted as 'The most preferred bank' in a survey by TV 18

in association with AC Nielsen-ORG Marg. Also, the Bank was voted as 'The most preferred housing

loan provider' in AWAAZ consumer awards for the year 2006. In the customer loyalty survey 2006-07

conducted by 'Business World', the Bank was ranked number one in all parameters of customer

satisfaction, service orientation, customer care/ call center, customer loyalty and home loans. SBI Funds

was judged 'Mutual fund of the year' by CNBC/TV-18/CRISL. The Bank introduced new products and

services such as web-based remittance, instant fund transfer, online-trading and comprehensive cash

management. During the year 2007-08, the Bank launched 965 branches all over the country. They

inaugurated a new state-of-the art Dealing Room with online connectivity to all active forex intensive

Branches at Corporate Centre in Mumbai. They launched a new product, Construction Equipment Loan

to cater to construction Companies. Also, they introduced new products such as SBI Reverse Mortgage

Loan and SBI Home Plus in the areas of Home Loans. During the year, the RBI transferred their entire

shareholding in the Bank representing 59.73% of the issued capital of the Bank to the Government of

India.

The Bank acquired 92.03% of equity of Global Trade Finance Ltd. Consequently, GTFL became a

subsidiary of the Bank. They signed a MoU with the Indian railways for installing ATMs at 682 railway

stations. In March 2008, the Bank opened their 10,000th branch and became only the second bank in the

world to have more than 10,000 branches after China's ICBC. During the year 2008-09, the company

launched Import factoring, a new product in association with SBI Factors & Commercial Services Ltd.

They increased the number of branches for retail sale of gold coins from 250 to 518. Also, they re-

launched Gold Deposit Scheme at 50 branches to mobilize gold from domestic market for deployment

as metal loans to jewelers. During the year, the Bank opened their 11,111th Branch at Sonapur (Kamrup

District) in Assam.

They introduced three new products viz., SBI Special Home Loan, SBI Happy Home Loan and SBI

Lifestyle in response to the stimulus package announced by the Government of India.

44

They entered into an exclusive arrangement with TATA Motors for handling the booking process of

TATA 'Nano' cars. During the year, the Bank launched on their web-site an on-line application form for

registering Auto Loan enquiries and expeditiously monitoring and converting these leads into Auto

Loans. Also, they launched 'e-invest' for the ASBA (applications supported by blocked accounts) to aid

investors for their equity subscriptions, IPO and Rights applications. During the year, the Bank set up a

custodial services company namely SBI Custodial Services Pvt. Ltd., in joint venture with Society

Generale, France. They signed letter of intent for setting up of joint venture Company for undertaking

General Insurance Business. Also, they divested 10% equity stake in its wholly owned subsidiary SBI

Pension Fund Pvt. Ltd at cost in favor of its subsidiaries. In October 2008, the Bank signed an MoU with

State General Reserve Fund (SGRF) of Oman, for a general purpose private equity fund. During the

year, State Bank of Saurashtra (SBS), a wholly owned subsidiary of the Bank, amalgamated with the

Bank with effect from August 13, 2008.

They signed a joint venture agreement with Insurance Australia Group for undertaking General

Insurance business. Also, they signed a joint venture agreement with Macquarie Capital Group,

Australia and IFC, Washington for setting up an Infrastructure fund of USD 3 billion for investing in

various infrastructure projects in India. During the year 2009-10, the Bank opened 1,049 branches, out

of which branches were opened in metro and urban areas with a view to increase the Bank's reach and be

more accessible to customers. In July 2009, SBI introduced 'SBI Loan to Affluent Pensioners' enabling

the government pensioners to avail personal loans up to Rs 3 lakh. During the year, the Bank designed a

special package, the Defenses Salary Package, for personnel of the three Armed Forces i.e. the Army,

Navy and Air Force who maintain their Salary accounts with them. As of March 2010, the Bank had

12,496 branches and 21,485 Group ATMs. In June 2009, the company increased their shareholding in

Nepal SBI Bank Ltd to 55.02% and thus Nepal SBI Bank Ltd became a subsidiary of the Bank with

effect from June 14, 2009. In May 2010, the Bank selected consortium of Elavon Incorporation, USA

and Visa International, USA as their joint venture (JV) partner for Merchant Acquiring Business.

They set up a wholly owned subsidiary, namely SBI Payment Services Pvt Ltd for conducting Merchant

Acquiring Business. In August 2010, State Bank of Indore was amalgamated with the Bank as per the

scheme of amalgamation approved by the Central Board. During the year 2010-11.

45

The Bank introduced 2 new products, namely 'Pushpa Ullas' and 'Arthias Plus' on pilot basis. They made

substantial progress in establishing itself as a leading PE fund player of the country. Also, they also

signed a Joint Venture agreement with State General Reserve Fund (SGRF) of Sultanate of Oman, a

sovereign entity, to set up a general purpose private equity fund with an initial corpus of USD 100 mn,

expandable further to USD 1.5 bn. During the year, the Bank opened 576 new branches besides merger

of 470 branches of erstwhile State Bank of Indore. Also, they opened 14 foreign offices during the year,

taking the total to 156.

In July 1, 2010, the Bank launched their 'Green Channel Counter' at select branches across the country.

In General Insurance business, the Bank launched limited operations in April 2010 for the Corporate and

Mid Corporate customers based at Mumbai, and it was expanded to six other major locations in July

2010. In the Retail segment, the Bank launched their Long Term Home Insurance business at Mumbai in

October 2010, which was gradually extended to cover 56 RACPCs and RASMECCs. General Insurance

SME business was launched on a pilot basis in Mumbai and Chennai in February 2011. During the first

quarter of the financial year 2011-12, the Government of India issued the 'Acquisition of State Bank of

India Commercial & International Bank Ltd. vide notification dated July 29, 2011. Consequent to the

said notification, the undertaking of State Bank of India Commercial & International stands transferred

to and vest in State Bank of India with effect from July 29, 2011.

46

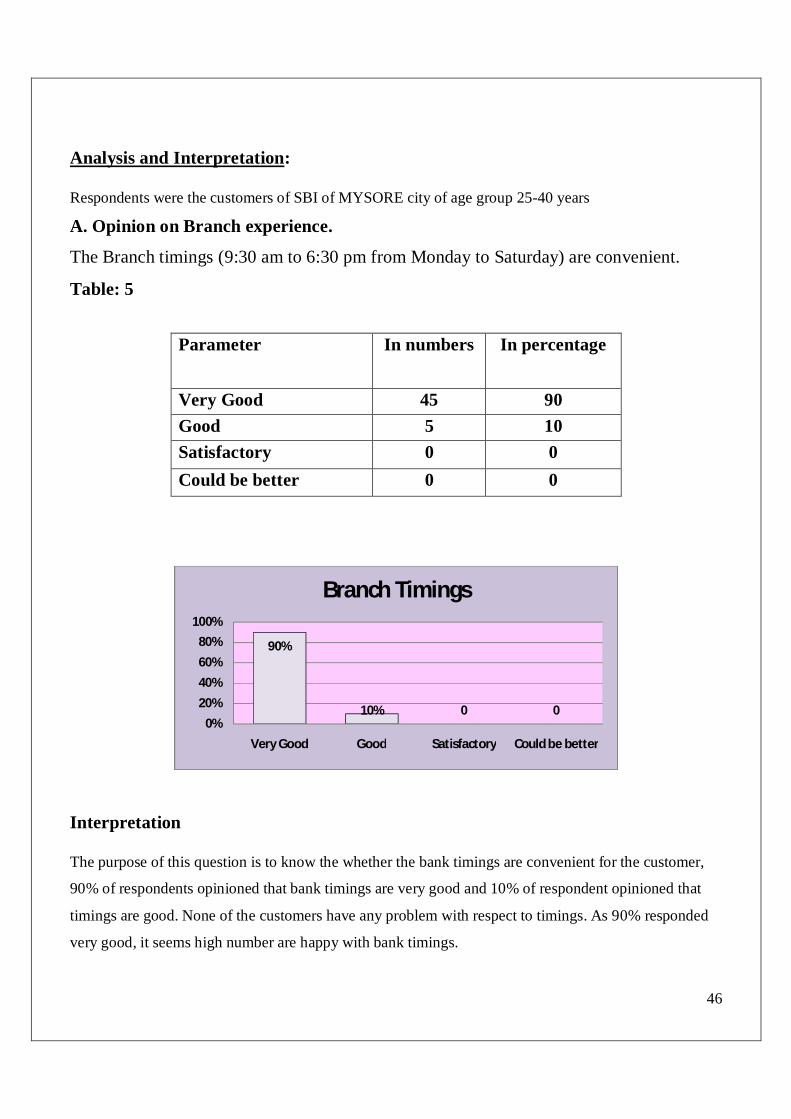

Analysis and Interpretation: Respondents were the customers of SBI of MYSORE city of age group 25-40 years

A. Opinion on Branch experience.

The Branch timings (9:30 am to 6:30 pm from Monday to Saturday) are convenient.

Table: 5

Interpretation The purpose of this question is to know the whether the bank timings are convenient for the customer,

90% of respondents opinioned that bank timings are very good and 10% of respondent opinioned that

timings are good. None of the customers have any problem with respect to timings. As 90% responded

very good, it seems high number are happy with bank timings.

90%

10% 0 00%

20%40%60%80%

100%

Very Good Good Satisfactory Could be better

Branch Timings

Parameter In numbers In percentage

Very Good 45 90 Good 5 10 Satisfactory 0 0 Could be better 0 0

47

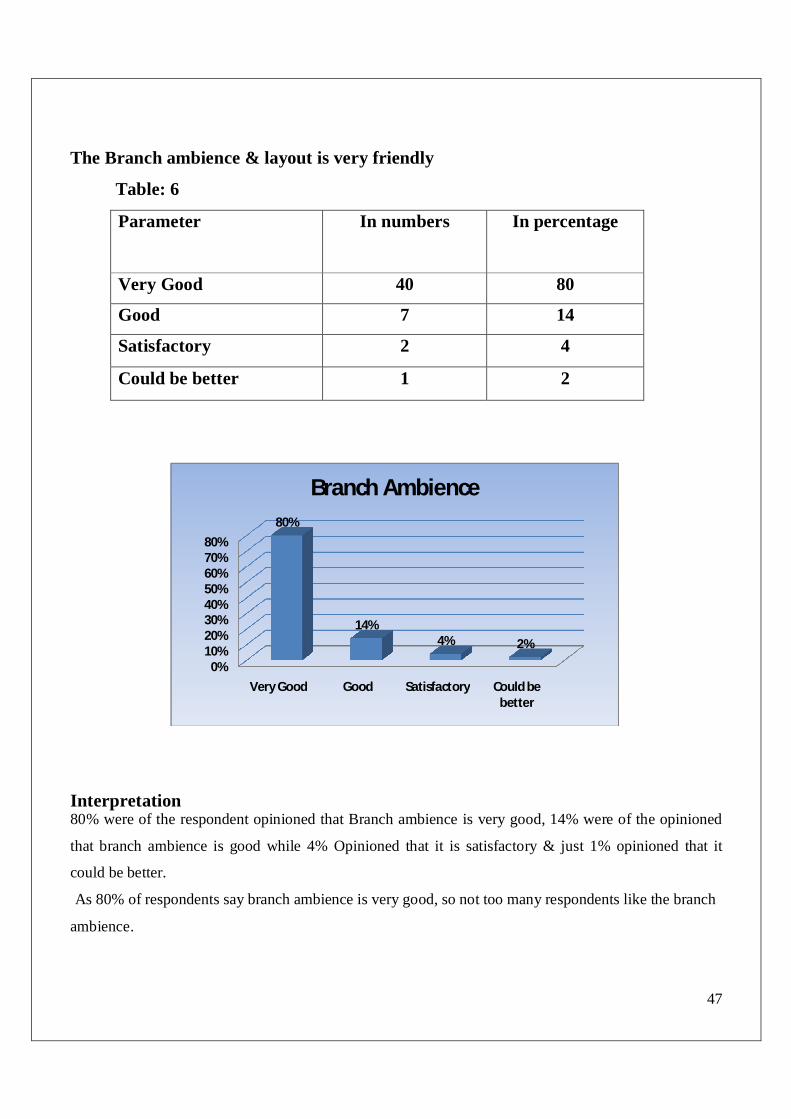

The Branch ambience & layout is very friendly

Table: 6

Parameter In numbers In percentage

Very Good 40 80

Good 7 14

Satisfactory 2 4

Could be better 1 2

Interpretation 80% were of the respondent opinioned that Branch ambience is very good, 14% were of the opinioned

that branch ambience is good while 4% Opinioned that it is satisfactory & just 1% opinioned that it

could be better.

As 80% of respondents say branch ambience is very good, so not too many respondents like the branch

ambience.

0%10%20%30%40%50%60%70%80%

Very Good Good Satisfactory Could be better

80%

14%4% 2%

Branch Ambience

48

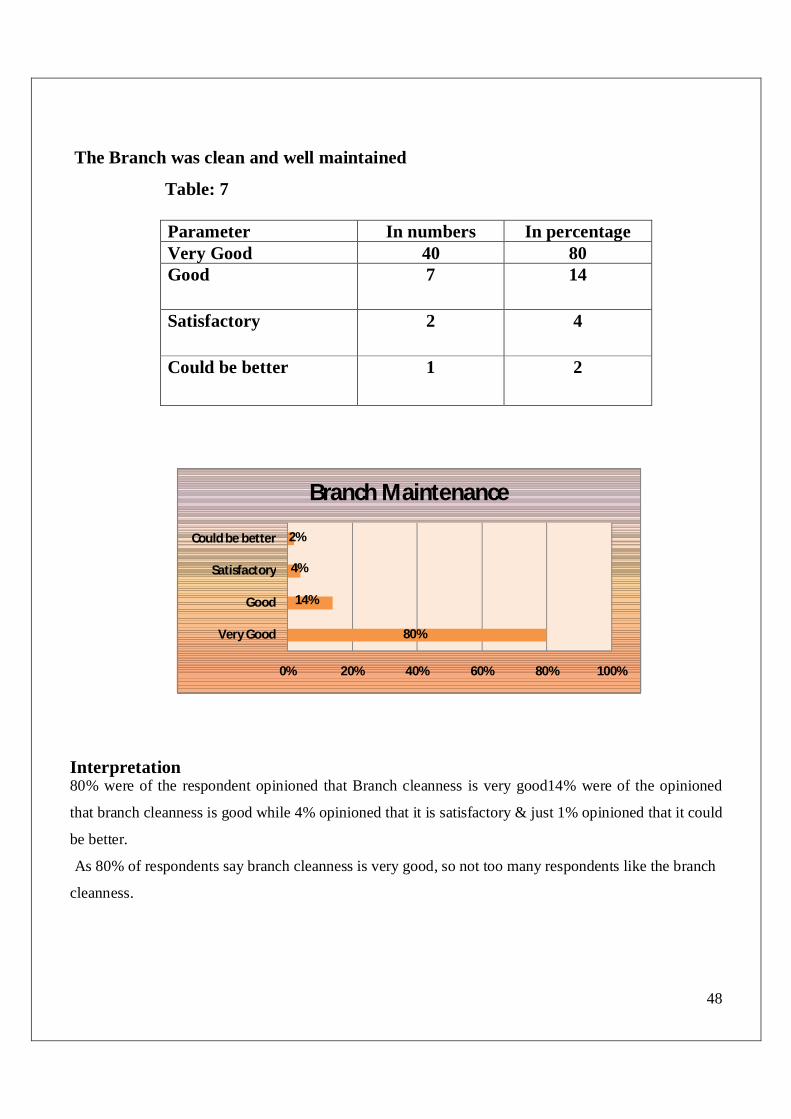

The Branch was clean and well maintained

Table: 7

Parameter In numbers In percentage Very Good 40 80 Good 7 14

Satisfactory 2 4

Could be better 1 2

Interpretation 80% were of the respondent opinioned that Branch cleanness is very good14% were of the opinioned

that branch cleanness is good while 4% opinioned that it is satisfactory & just 1% opinioned that it could

be better.

As 80% of respondents say branch cleanness is very good, so not too many respondents like the branch

cleanness.

80%

14%

4%

2%

0% 20% 40% 60% 80% 100%

Very Good

Good

Satisfactory

Could be better

Branch Maintenance

49

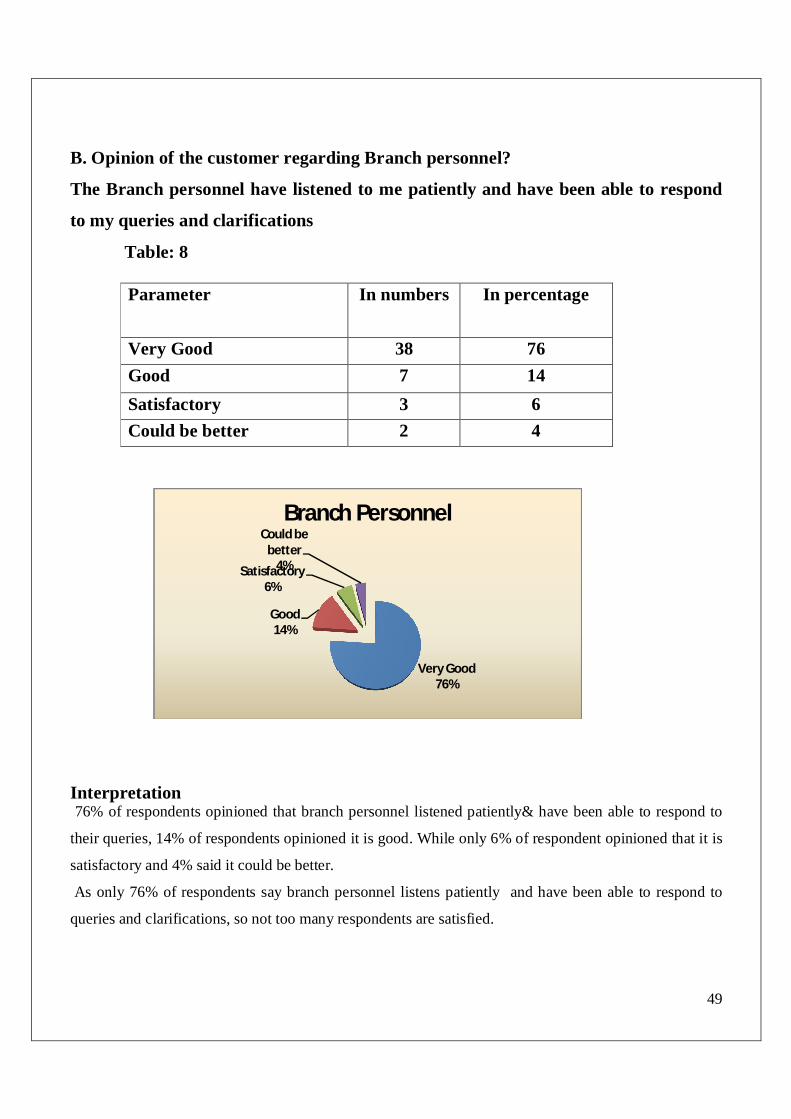

B. Opinion of the customer regarding Branch personnel?

The Branch personnel have listened to me patiently and have been able to respond

to my queries and clarifications

Table: 8

Parameter In numbers In percentage

Very Good 38 76 Good 7 14 Satisfactory 3 6 Could be better 2 4

Interpretation 76% of respondents opinioned that branch personnel listened patiently& have been able to respond to

their queries, 14% of respondents opinioned it is good. While only 6% of respondent opinioned that it is

satisfactory and 4% said it could be better.

As only 76% of respondents say branch personnel listens patiently and have been able to respond to

queries and clarifications, so not too many respondents are satisfied.

Very Good 76%

Good14%

Satisfactory6%

Could be better

4%

Branch Personnel

50

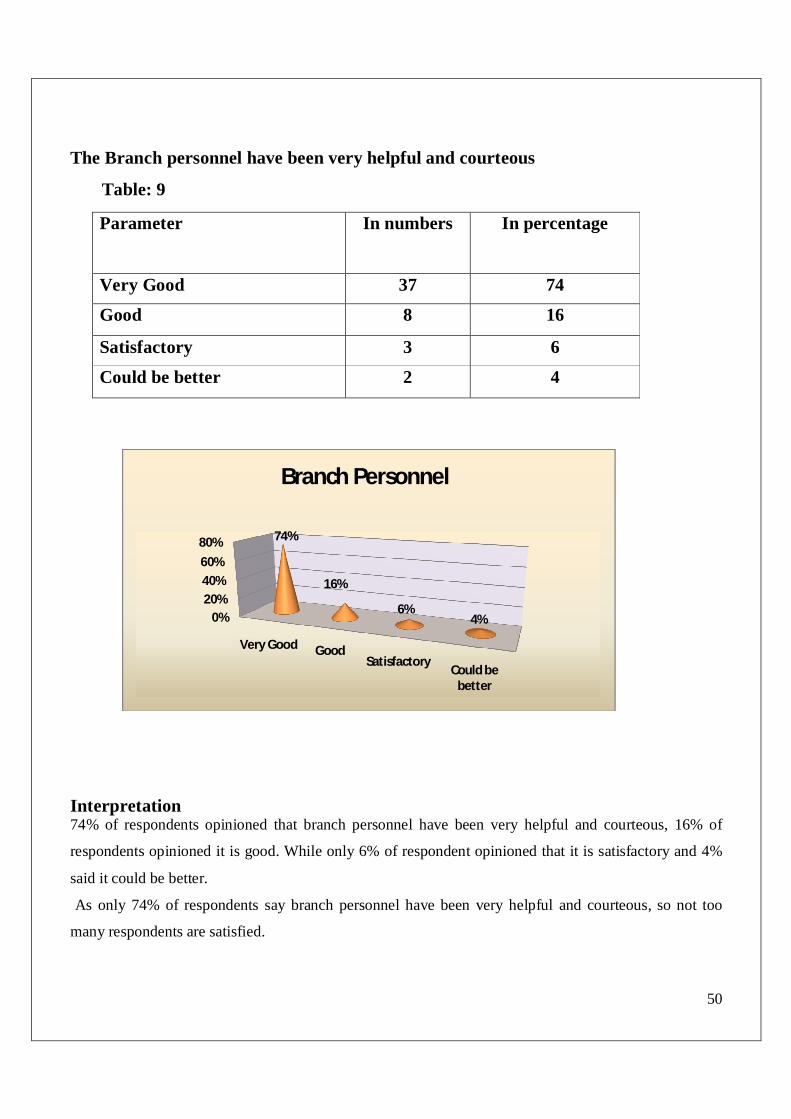

The Branch personnel have been very helpful and courteous

Table: 9

Interpretation 74% of respondents opinioned that branch personnel have been very helpful and courteous, 16% of

respondents opinioned it is good. While only 6% of respondent opinioned that it is satisfactory and 4%

said it could be better.

As only 74% of respondents say branch personnel have been very helpful and courteous, so not too

many respondents are satisfied.

0%20%40%60%80%

Very Good GoodSatisfactory

Could be better

74%

16%

6%4%

Branch Personnel

Parameter In numbers In percentage

Very Good 37 74

Good 8 16

Satisfactory 3 6

Could be better 2 4

51

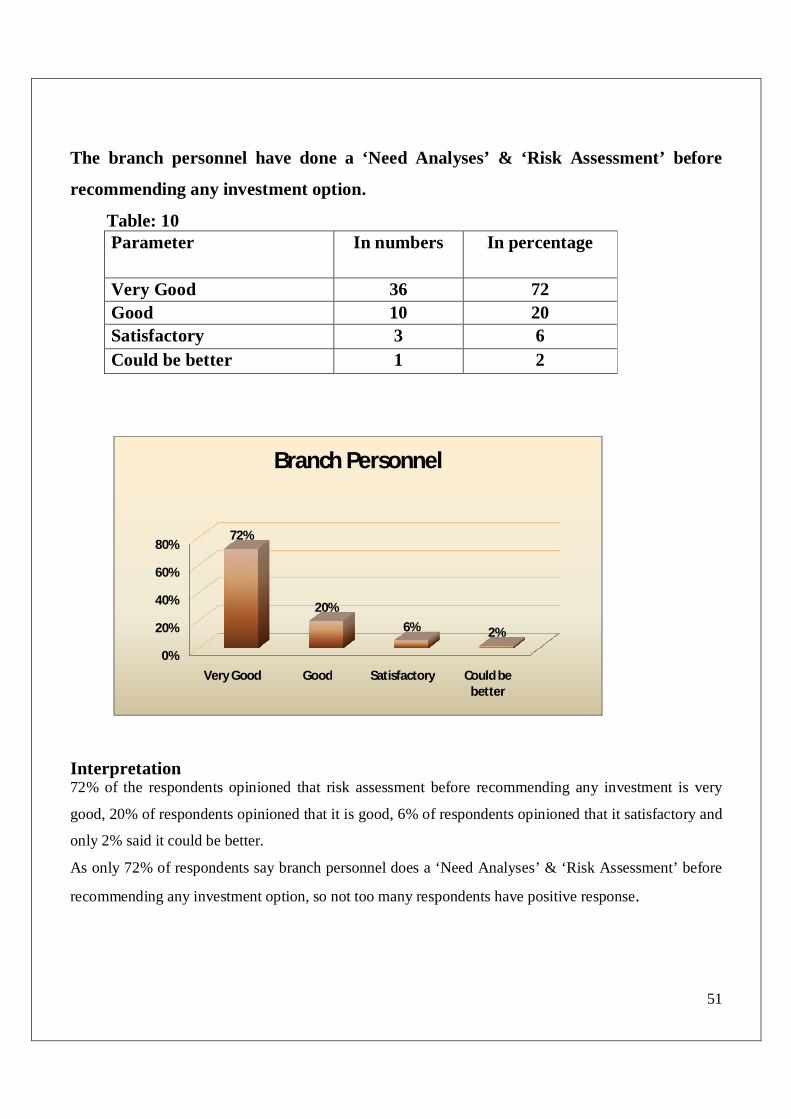

The branch personnel have done a ‘Need Analyses’ & ‘Risk Assessment’ before

recommending any investment option.

Table: 10 Parameter In numbers In percentage

Very Good 36 72 Good 10 20 Satisfactory 3 6 Could be better 1 2

Interpretation 72% of the respondents opinioned that risk assessment before recommending any investment is very

good, 20% of respondents opinioned that it is good, 6% of respondents opinioned that it satisfactory and

only 2% said it could be better.

As only 72% of respondents say branch personnel does a ‘Need Analyses’ & ‘Risk Assessment’ before

recommending any investment option, so not too many respondents have positive response.

0%

20%

40%

60%

80%

Very Good Good Satisfactory Could be better

72%

20%6% 2%

Branch Personnel

52

The branch personnel were aware of Product and Services and responded to your

queries

Table: 11

Parameter In numbers In percentage

Very Good 43 86 Good 3 6 Satisfactory 3 6 Could be better 1 2

Interpretation 86% respondents opinioned that branch personnel responded to their queries and is very good, 6% says

to be good & 6% satisfactory. Only 2% said it could be better.

As 86% of respondents say branch personnel were aware of Product and Services and responded to

customer queries, so not too many respondents are satisfied.

86%

6%

6%

2%

0% 20% 40% 60% 80% 100%

Very Good

Good

Satisfactory

Could be better

Product & Services

53

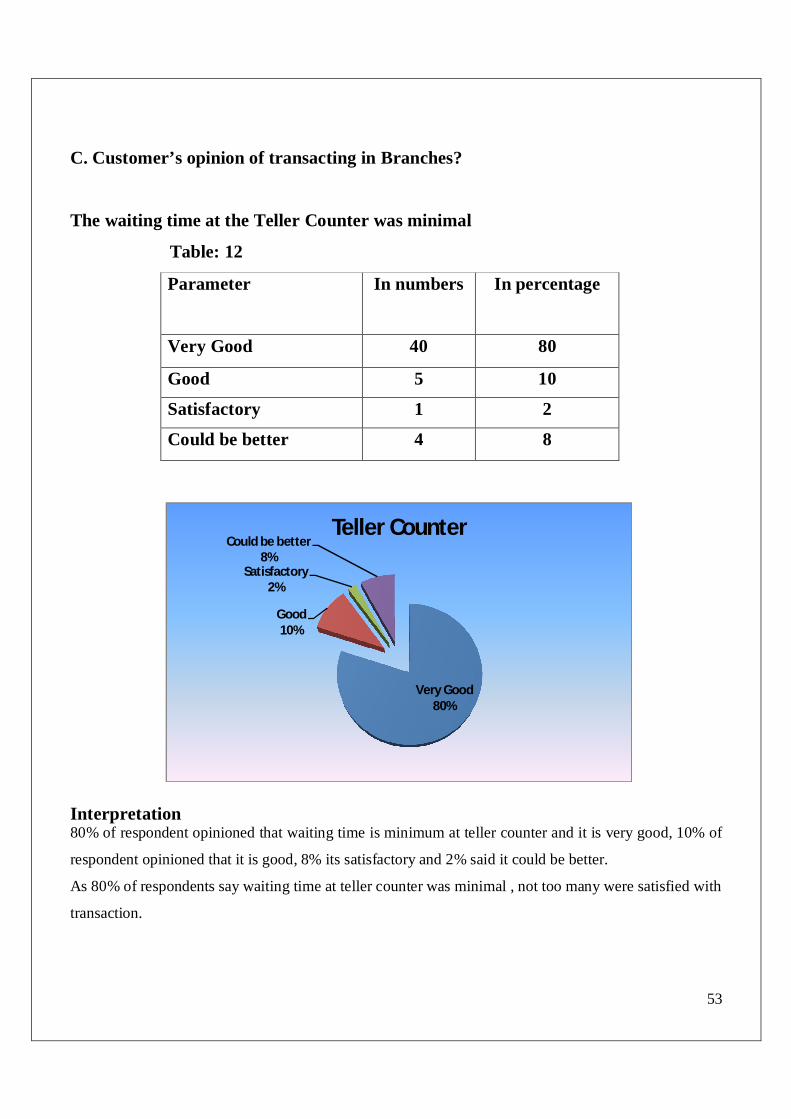

C. Customer’s opinion of transacting in Branches?

The waiting time at the Teller Counter was minimal

Table: 12

Parameter In numbers In percentage

Very Good 40 80

Good 5 10

Satisfactory 1 2

Could be better 4 8

Interpretation 80% of respondent opinioned that waiting time is minimum at teller counter and it is very good, 10% of

respondent opinioned that it is good, 8% its satisfactory and 2% said it could be better.

As 80% of respondents say waiting time at teller counter was minimal , not too many were satisfied with

transaction.

Very Good80%

Good10%

Satisfactory2%

Could be better8%

Teller Counter

54

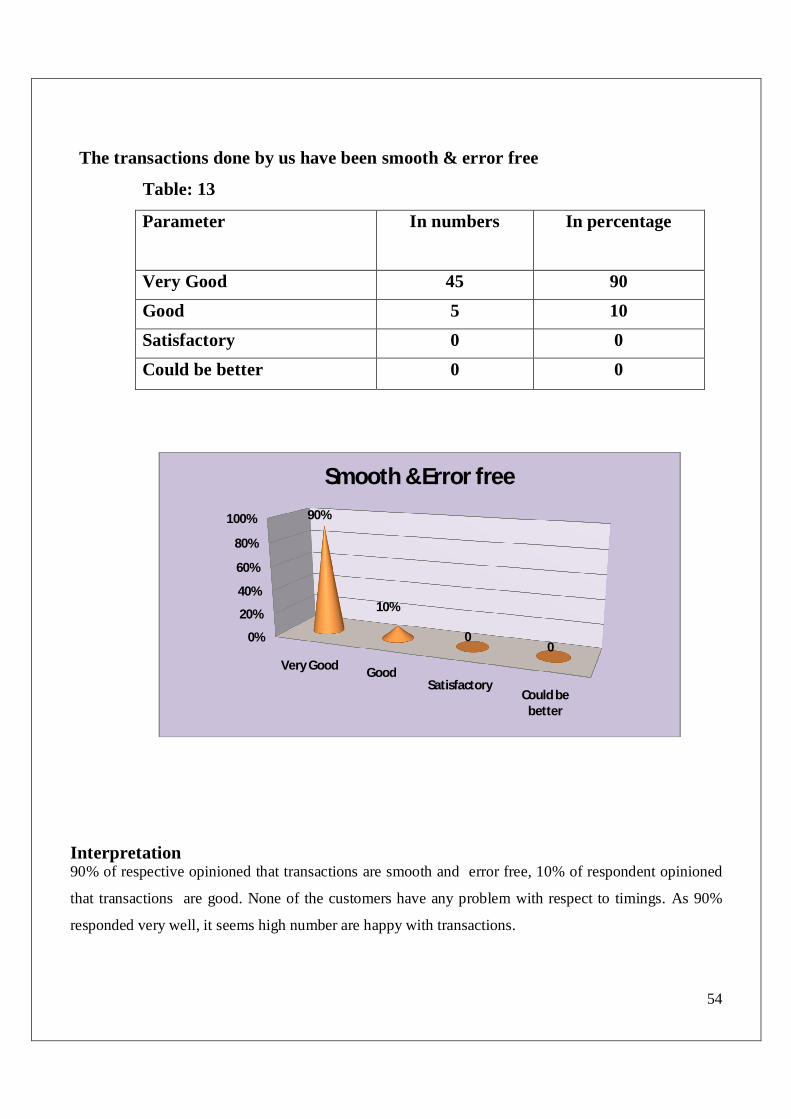

The transactions done by us have been smooth & error free

Table: 13

Parameter In numbers In percentage

Very Good 45 90 Good 5 10 Satisfactory 0 0 Could be better 0 0

Interpretation 90% of respective opinioned that transactions are smooth and error free, 10% of respondent opinioned

that transactions are good. None of the customers have any problem with respect to timings. As 90%

responded very well, it seems high number are happy with transactions.

0%

20%

40%

60%

80%

100%

Very Good GoodSatisfactory

Could be better

90%

10%

00

Smooth &Error free

55

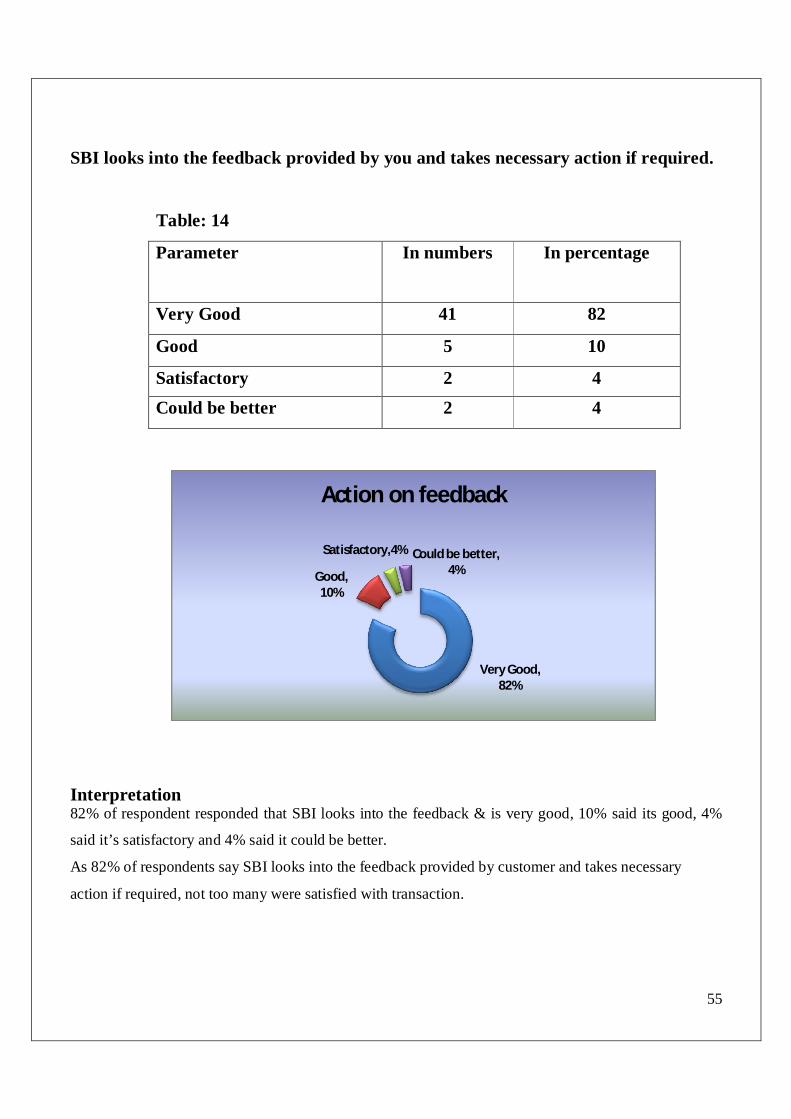

SBI looks into the feedback provided by you and takes necessary action if required.

Table: 14

Parameter In numbers In percentage

Very Good 41 82

Good 5 10

Satisfactory 2 4 Could be better 2 4

Interpretation 82% of respondent responded that SBI looks into the feedback & is very good, 10% said its good, 4%

said it’s satisfactory and 4% said it could be better.

As 82% of respondents say SBI looks into the feedback provided by customer and takes necessary

action if required, not too many were satisfied with transaction.

Very Good,82%

Good,10%

Satisfactory,4% Could be better,4%

Action on feedback

56

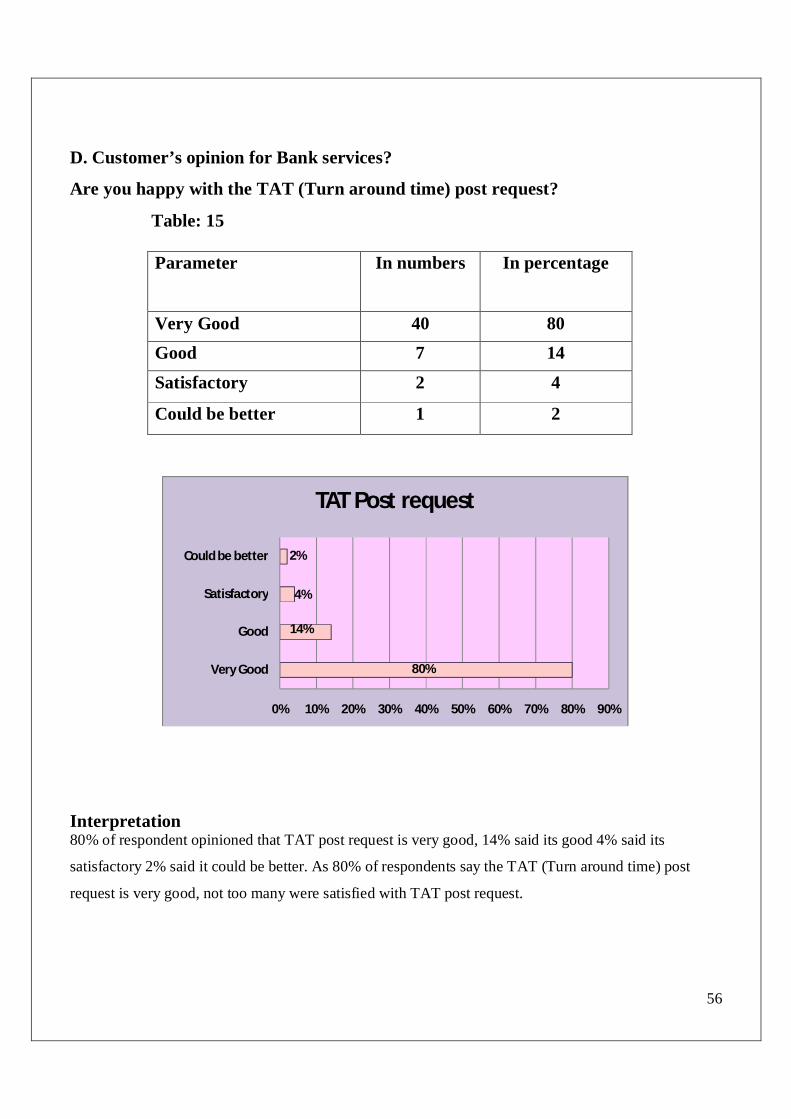

D. Customer’s opinion for Bank services?

Are you happy with the TAT (Turn around time) post request?

Table: 15

Parameter In numbers In percentage

Very Good 40 80 Good 7 14 Satisfactory 2 4

Could be better 1 2

Interpretation 80% of respondent opinioned that TAT post request is very good, 14% said its good 4% said its

satisfactory 2% said it could be better. As 80% of respondents say the TAT (Turn around time) post

request is very good, not too many were satisfied with TAT post request.

80%

14%

4%

2%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Very Good

Good

Satisfactory

Could be better

TAT Post request

57

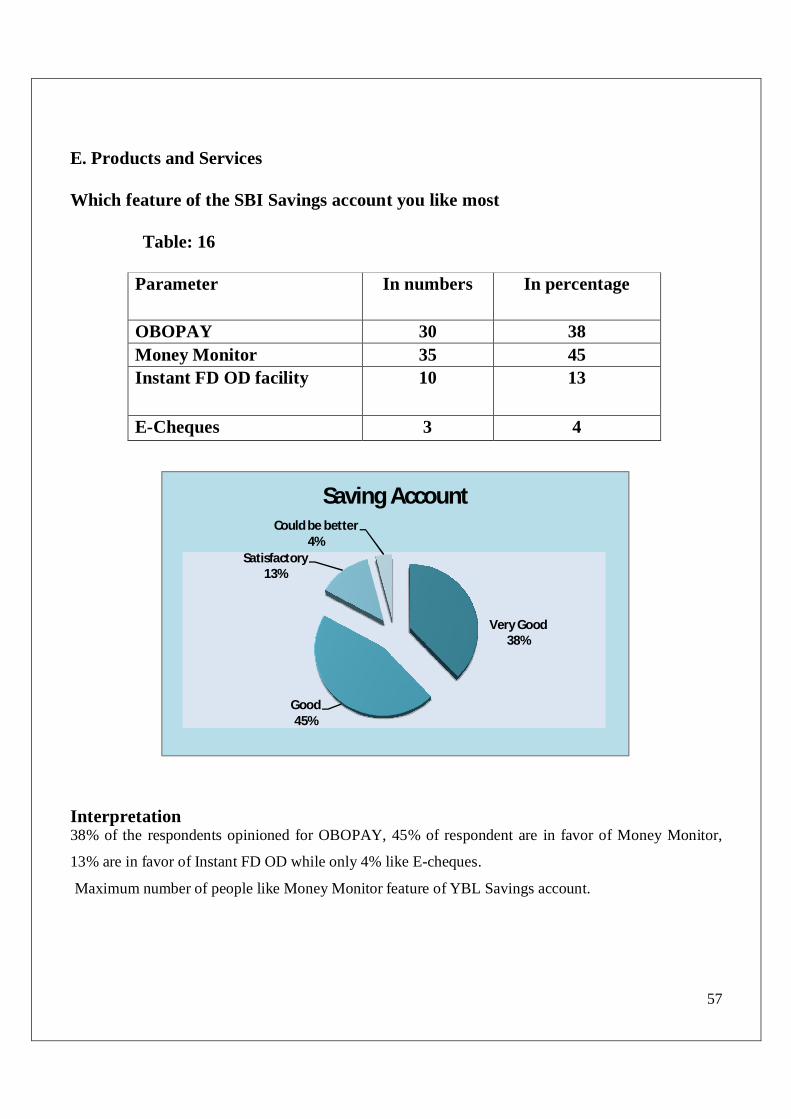

E. Products and Services Which feature of the SBI Savings account you like most Table: 16

Parameter In numbers In percentage

OBOPAY 30 38 Money Monitor 35 45 Instant FD OD facility 10 13

E-Cheques 3 4

Interpretation 38% of the respondents opinioned for OBOPAY, 45% of respondent are in favor of Money Monitor,

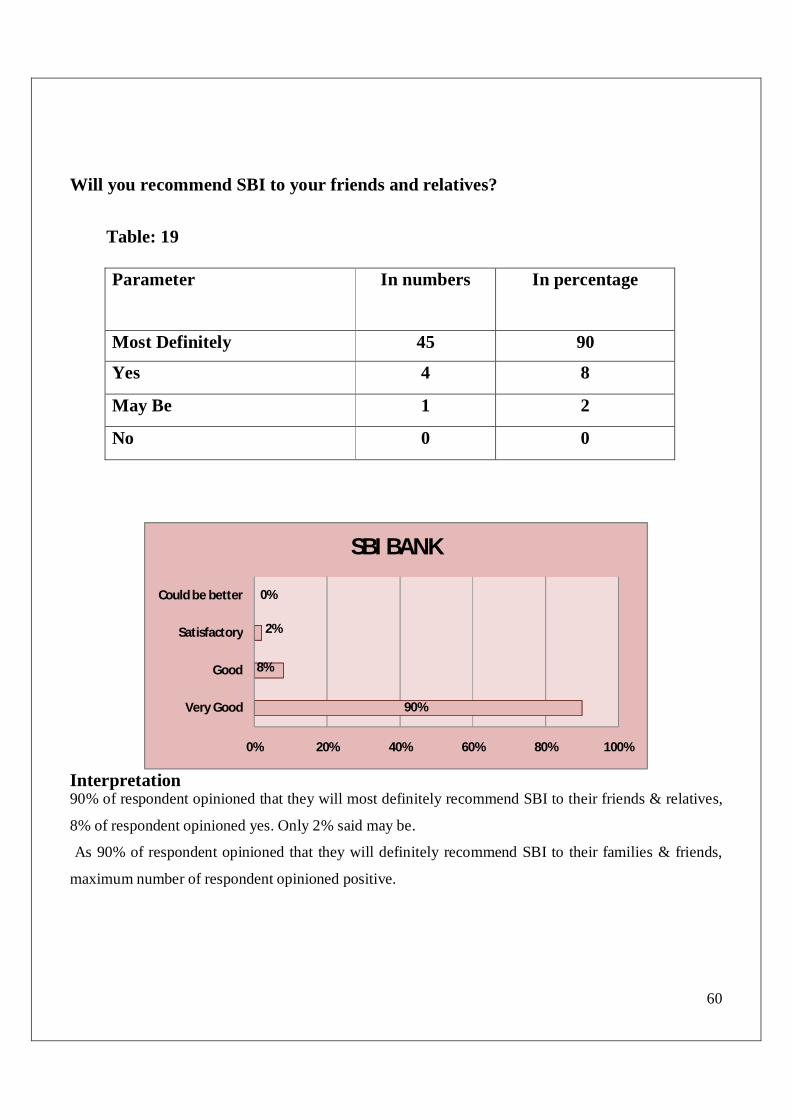

13% are in favor of Instant FD OD while only 4% like E-cheques.