Banking: HOBS Abbreviations First and second conditional II.

23

Banking: HOBS Abbreviations First and second conditional II

-

Upload

elijah-nelson -

Category

Documents

-

view

227 -

download

1

Transcript of Banking: HOBS Abbreviations First and second conditional II.

Banking: HOBS

Abbreviations

First and second conditional II

Banking involves:

Saving money or trusting your money to a financial institution (a bank) so that your money is safeguarded

Providing loans, credit, and payment services such as checking accounts

The possibility of investment and insurance Most frequently banks are used for opening

savings accounts. Other possibilities offer checking accounts and

online banking

Savings accounts:

This account allows you to deposit money in the bank and earn interest on that money over the course of time.

There are different types of savings accounts available and each depends on the amount of money you will be depositing, whether or not you want easy access to your funds and how long you want to keep your money in your account. Some of the types of savings accounts are:

Bank savings account: It is good for short term or long term savings. Money is deposited in an account and interest is earned on that account. Money can be withdrawn from these accounts as well. There may be a minimum balance, which means the depositor is slapped with a penalty for going under the minimum balance.

Certificate of deposit (CD): when you deposit money into this account, it’s meant to stay in that account for a certain period of time. Depending on the account you choose, this can be anywhere from one month to five years. If money is withdrawn within that amount of time, you will be penalized.

Checking accounts:

If you need to pay bills, the last thing you want to do is send cash through the mail. Purchasing a money order for each transaction is not only inconvenient, it’s expensive. Your best bet is to open a checking account. A checking account is similar to a bank savings account in that money is deposited into your account and if you fall below a certain limit you’re penalized. The purpose of a checking account is, of course, to write checks.

You may write checks only for the amount of money in your checking account or less. If you’re overdrawn on your checking account, the check will “bounce” or be returned due to insufficient funds. Not only will you have to pay a bank charge for a bounced check, but you’ll probably incur fees on behalf of the company that received the bounced check.

Online banking:

Thanks to the wonders of technology, banking can now be done over the Internet. With online banking, you can pay bills, deposit or transfer funds, order checks and take care of other banking responsibilities. The benefit of this, of course, is that banking can be done from the comfort of your own home or office.

With online banking, checks are automatically sent to the other part’s account, saving on postage and other checking fees.

Money can be transferred between accounts with the simple click of a mouse, and thanks to service such as Pay Pal, people can even receive payments via e-mail. Benefits of online banking are many. Be sure to research any bank charges that might be incurred as a result of online banking. If it’s too expensive, you may well stick to manual banking.

If you’re looking to open a savings or checking account or take advantage of online banking, research the banks in your area. See which one has the terms, interest rates and customer service that best suits your lifestyle.

Types of banks:

There are several types of banks, which differ in the number of services they provide and the clientele they serve.

Commercial banks, which dominate this industry, offer a full range of services for individuals, businesses, and governments. These banks come in a wide range of sizes, from large global banks to regional and community banks.

Global banks are involved in international lending and foreign currency trading, in addition to the more typical banking services.

Regional banks have numerous branches and automated teller machines (ATM) locations throughout a multi-state area that provide banking services to individuals.

Banks have become more oriented toward marketing and sales. As a result, employees need to know about all types of products and services offered by banks.

Community banks are based locally and offer more personal attention, which many individuals and small businesses prefer.

Savings banks and savings and loan associations, sometimes called thrift institutions, are the second largest group of depository institutions. They were first established as communtity-based institutions to finance mortgages for people to buy homes and still cater mostly to the savings and lending needs of individuals.

Credit unions are another kind of depository institution. Most credit unions are formed by people with a common bond, such as those who work for the same company or belong to the same labour union or church. Members pool their savings and, when they need money, they may borrow from the credit union, often at a lower interest rate than that demanded by other financial institutions.

Federal Reserve banks are Government agencies that perform many financial services for the Government. Their chief responsibilities are to regulate the banking industry and to help implement monetary policy so the economy can run more efficiently. Federal Reserve banks also perform a variety of services for other banks. For example, they may make emergency loans to banks that are short of cash, and clear checks that are drawn and paid out of different banks.

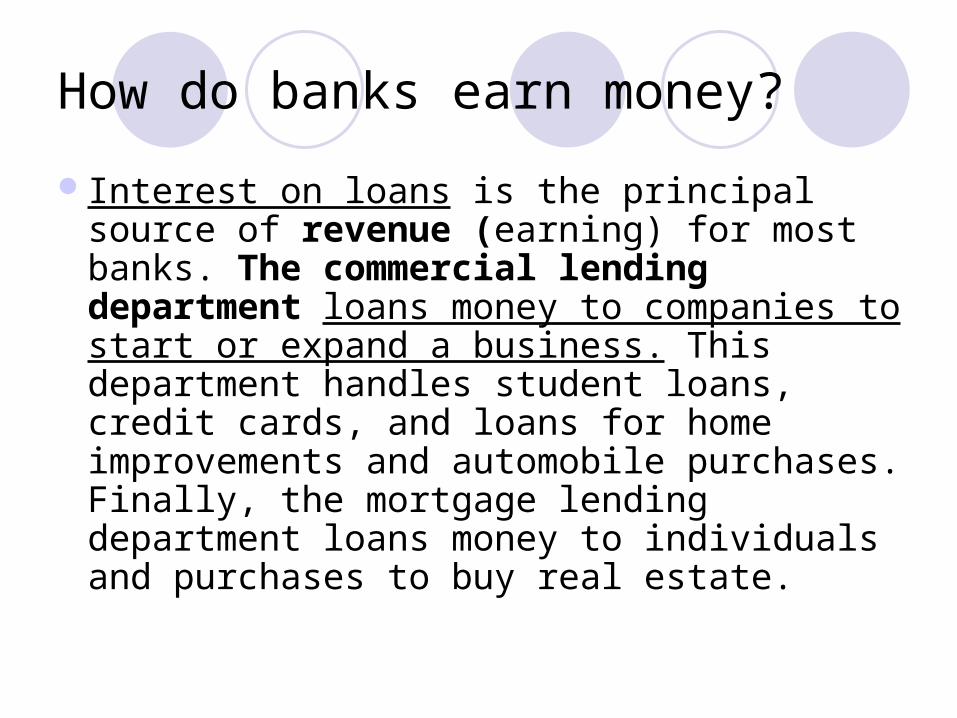

How do banks earn money?

Interest on loans is the principal source of revenue (earning) for most banks. The commercial lending department loans money to companies to start or expand a business. This department handles student loans, credit cards, and loans for home improvements and automobile purchases. Finally, the mortgage lending department loans money to individuals and purchases to buy real estate.

Technology is having a major impact on the banking industry: For example, many routine bank services that

once required a teller, such as making a withdrawal or deposit, are now available through ATMs that allow people to access their accounts 24 hours a day. Also, direct deposit allows companies and governments to electronically transfer payments into various accounts.

Further, debit cards, which are also used as ATM cards, instantaneously deduct money from an account when the card is swiped across a machine at a store’s cash register.

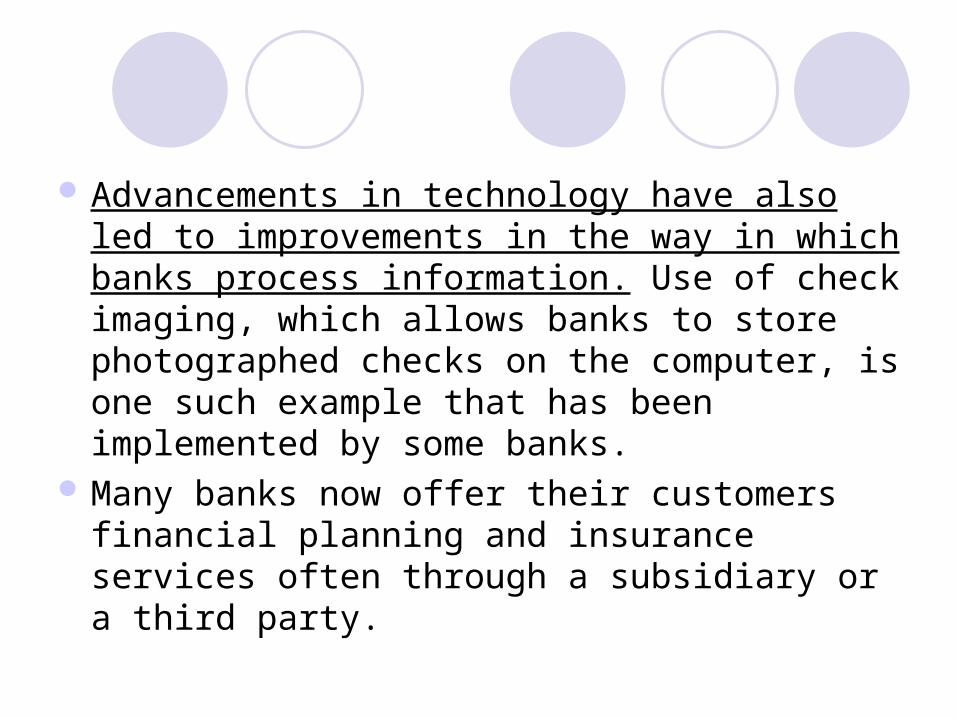

Advancements in technology have also led to improvements in the way in which banks process information. Use of check imaging, which allows banks to store photographed checks on the computer, is one such example that has been implemented by some banks.

Many banks now offer their customers financial planning and insurance services often through a subsidiary or a third party.

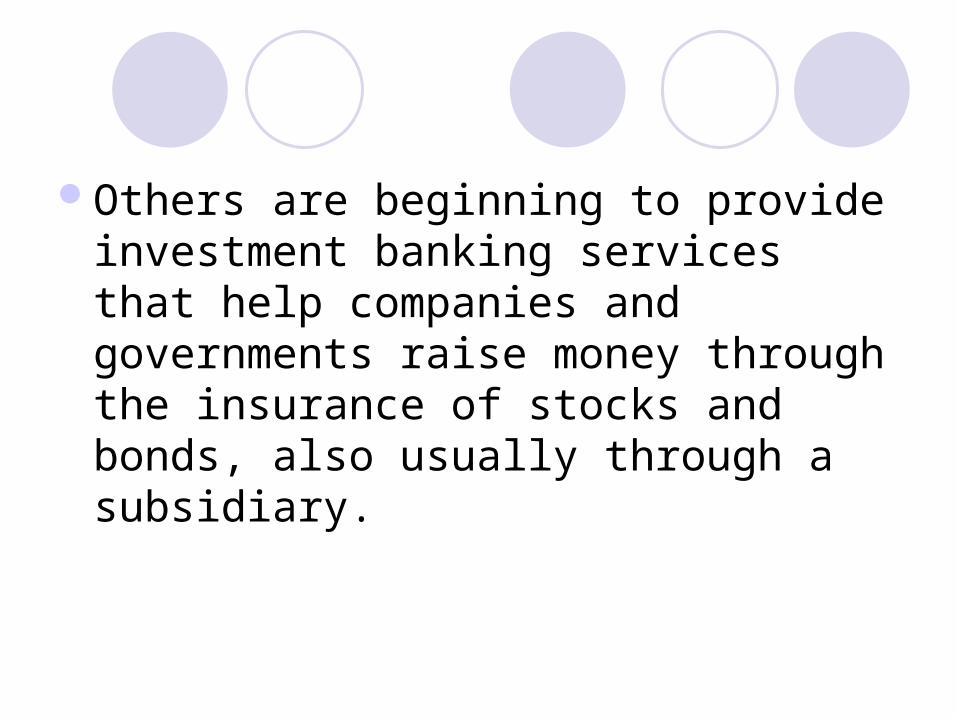

Others are beginning to provide investment banking services that help companies and governments raise money through the insurance of stocks and bonds, also usually through a subsidiary.

HOBS (Home and Office Banking Service)

HOBS is the oldest online banking service, having started out in 1985 by beaming account data down the telephone line to a television monitor, TV banking is the earliest form.

The modern PC HOBS lets you view a large range of services online, from current and savings accounts to currency accounts, mortgages and credit cards.

Abbreviations

First and second conditional II

Here are some abbreviations which are often used in the business world. Match them with their meanings: VAT asap

IOU Corp AOB GMT i.e. e.g. MD N/A PAYE a.m. Ltd AGM CEO p.a. SFr plc

exempli gratia (for example) value added tax pay as you earn chief executive officer as soon as possible not available limited I owe you... personal account corporation any other business managing director Societe Francaise de Radiotelephonie greenwich mean time public limited company annual general meeting id est (that is) ante meridiem

For each of the following sentences write both first and second conditional situation. (use the first person): If / lose / credit card / inform / the bank

immediately. If / need some money / ask / the bank manager

for a loan. If / find / mistakes on my bank statement /

change / to a different bank. If /earn / more money / be able to / save more. If / order / chequebook / get / it before the end of

the week?

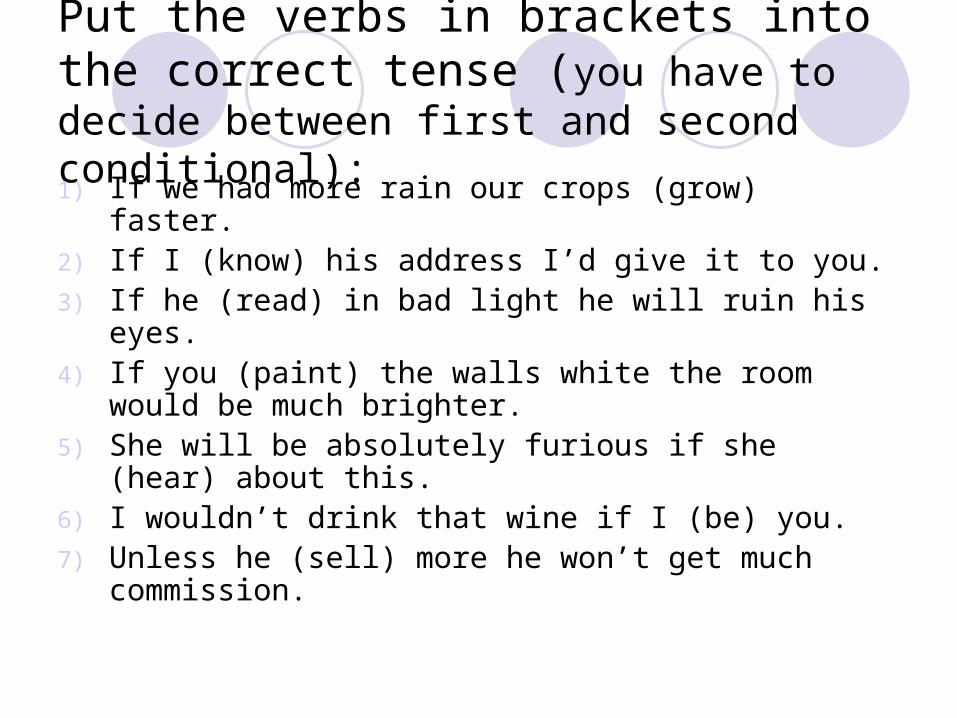

Put the verbs in brackets into the correct tense (you have to decide between first and second conditional):1) If we had more rain our crops (grow) faster.2) If I (know) his address I’d give it to you.3) If he (read) in bad light he will ruin his eyes.4) If you (paint) the walls white the room would be

much brighter.5) She will be absolutely furious if she (hear)

about this.6) I wouldn’t drink that wine if I (be) you.7) Unless he (sell) more he won’t get much

commission.