Bank

54

IOSR Journal of Business and Management (IOSRJBM) ISSN: 2278-487X Volume 1, Issue 5 (July-Aug. 2012), PP 01-05 www.iosrjournals.org www.iosrjournals.org 1 | Page Customer Satisfaction: A Comparison of Public and Private Banks Of Pakistan 1 Waqar ul Haq 2 Bakhtiar Muhammad 1 ShaheedZulfikar Ali Bhutto Institute of Science and Technology, Islamabad 2 Professor, Shaheed Zulfikar Ali Bhutto Institute of Science and Technology, Islamabad Abstract: The purpose of conducting this research is to compare public and private sector banks of Pakistan by evaluating their customer satisfaction. This research is mainly based on primary data which has been collected through a well-structured questionnaire (adapted from three different studies). The questionnaire has been distributed to 351 different respondents on different chosen locations. This paper makes a useful contribution as there are very low number of studies has been conducted in Pakistan on such areas like price, technology, reliability, customer service, location and infrastructure. This research shows that customer satisfaction varies from person to person and, bank managers need to conduct more researches in order to evaluate customer satisfaction more strongly. Keywords: Customer satisfaction, customer services, technology, reliability I. Introduction 1.1 Customer Satisfaction: is a measure of how products and services provide by any organization meet the expectations of a customer. It varies from person to person and service to service. A customer can be defined as a user or potential user of banking services. A customer would include an account holder, or a person carrying out casual business transactions with a bank. The efficiency of a banking sector depends upon how best it can deliver services to its target customers. In order to survive in this competitive environment and provide continual customer satisfaction, the banking services providers are required to frequently increase the quality of services. In banking business it is seen that only 5% increase in customer retention can extend 35% profitability. II. Literature Review 2.1 Entrance of Technology Private sector Banks seem to have satisfied its customers with good services and they have been successful in retaining their customers by providing better facilities than Public sector Banks. But, still Private Banks need to go a long way to become customer‟s first preference. In an economy of innovative technologies and changing markets, each and every service quality variable has become important. New financial products and services have to be continuously introduced in order to stay competent and Private Banks need to concentrate more on their credit facilities and insurance services since customers do not have a very good opinion about these facilities being offered by Private Banks also Public sector banks enjoy the trust of the customers, which they have been leveraging to stay in the race however they need to improve their service quality by improving their physical facility, infrastructure and giving proper soft skill trainings to their employees(Puja et, al). In the banking sector it is necessary to increased adoption of technology to better meet customer requirements, improve efficiencies, reduce costs and ensure customer delight and it was the private sector and foreign banks which established the technological revolution in Indian banking and considering the fact that in the new economy, mind share leads to market share and mind share is influenced not only by the promotions and advertisements but more importantly on favorable customer perception which in turn is based on satisfaction with regard to products, services and interaction (B. K. Tiwary). The private sector banks are providing more satisfied ATM services then public sector banks and the customer perception about Productivity, Security and Sensitivity, Cost Efficiency, Problem Handling, Compensation and Contact services related to ATM service is very less in both the public sector and privates sector banks, Therefore both kinds of banks should be aware about these facets of ATM service to improve customers‟ satisfaction (Vijay M. Kumbhar). The entry of information technology into the banking industry has created a revolution and it has prompted commercial banks of India to design world-class customer service systems and practices, to meet the growing customer needs. It is interesting to note that the results are consistent with the previous studies conducted on customer service aspects, and it has been observed that the foreign and the new generation private sector banks are serving the customers better (Rengasamy et, al).

-

Upload

swapnil-sawant -

Category

Documents

-

view

34 -

download

8

Transcript of Bank

IOSR Journal of Business and Management (IOSRJBM)

ISSN: 2278-487X Volume 1, Issue 5 (July-Aug. 2012), PP 01-05 www.iosrjournals.org

www.iosrjournals.org 1 | Page

Customer Satisfaction: A Comparison of Public and Private Banks Of

Pakistan

1Waqar ul Haq

2Bakhtiar Muhammad

1ShaheedZulfikar Ali Bhutto Institute of Science and Technology, Islamabad 2Professor, Shaheed Zulfikar Ali Bhutto Institute of Science and Technology, Islamabad

Abstract: The purpose of conducting this research is to compare public and private sector banks of Pakistan by evaluating their customer satisfaction. This research is mainly based on primary data which has been collected

through a well-structured questionnaire (adapted from three different studies). The questionnaire has been

distributed to 351 different respondents on different chosen locations. This paper makes a useful contribution as

there are very low number of studies has been conducted in Pakistan on such areas like price, technology,

reliability, customer service, location and infrastructure. This research shows that customer satisfaction varies

from person to person and, bank managers need to conduct more researches in order to evaluate customer

satisfaction more strongly.

Keywords: Customer satisfaction, customer services, technology, reliability

I. Introduction 1.1 Customer Satisfaction: is a measure of how products and services provide by any organization meet

the expectations of a customer. It varies from person to person and service to service. A customer can be defined

as a user or potential user of banking services. A customer would include an account holder, or a person

carrying out casual business transactions with a bank. The efficiency of a banking sector depends upon how best

it can deliver services to its target customers. In order to survive in this competitive environment and provide

continual customer satisfaction, the banking services providers are required to frequently increase the quality of

services. In banking business it is seen that only 5% increase in customer retention can extend 35% profitability.

II. Literature Review 2.1 Entrance of Technology

Private sector Banks seem to have satisfied its customers with good services and they have been

successful in retaining their customers by providing better facilities than Public sector Banks. But, still Private

Banks need to go a long way to become customer‟s first preference. In an economy of innovative technologies and changing markets, each and every service quality variable has become important. New financial products

and services have to be continuously introduced in order to stay competent and Private Banks need to

concentrate more on their credit facilities and insurance services since customers do not have a very good

opinion about these facilities being offered by Private Banks also Public sector banks enjoy the trust of the

customers, which they have been leveraging to stay in the race however they need to improve their service

quality by improving their physical facility, infrastructure and giving proper soft skill trainings to their

employees(Puja et, al).

In the banking sector it is necessary to increased adoption of technology to better meet customer

requirements, improve efficiencies, reduce costs and ensure customer delight and it was the private sector and

foreign banks which established the technological revolution in Indian banking and considering the fact that in

the new economy, mind share leads to market share and mind share is influenced not only by the promotions

and advertisements but more importantly on favorable customer perception which in turn is based on satisfaction with regard to products, services and interaction (B. K. Tiwary).

The private sector banks are providing more satisfied ATM services then public sector banks and the

customer perception about Productivity, Security and Sensitivity, Cost Efficiency, Problem Handling,

Compensation and Contact services related to ATM service is very less in both the public sector and privates

sector banks, Therefore both kinds of banks should be aware about these facets of ATM service to improve

customers‟ satisfaction (Vijay M. Kumbhar).

The entry of information technology into the banking industry has created a revolution and it has

prompted commercial banks of India to design world-class customer service systems and practices, to meet the

growing customer needs. It is interesting to note that the results are consistent with the previous studies

conducted on customer service aspects, and it has been observed that the foreign and the new generation private

sector banks are serving the customers better (Rengasamy et, al).

Customer Satisfaction: A Comparison of Public and Private Banks of Pakistan

www.iosrjournals.org 2 | Page

2.2 Customers Perceptions and Expectations

Quality expectation and the valuation of services received are slightlymore in the private sector banks

as compared with the public sector banks. The effects for tactic since sectorial differentiation become veryblurry

as a result of increasing correspondence between services and struggle from linked and additional industries

(Peter et, al).

Service quality is one of main elements of customer satisfaction and their intention to purchase. However, the customers of public and private sector banks different in terms of their perception of service

quality. Private Banks have been observed to be higher on dimensions of service quality: effectiveness and

convenient while, the nationalized banks are better on the dimensions of price and consistency (Sachinet, al).

Private bank customers are more satisfied with the services then public banks. Managers in the banking

sector undertake significant efforts to conduct customer satisfaction surveys and it is appears that customers are

saying that they expect good products and quality to their banks and that may the only thing important to them

(Muhammad Naveed).

2.3 Image and Reputation of Banks

Some publicly owned banks are scoring well among customers but overall analysis shows that

satisfaction rate in customers of private banks is much higher than public sector banks and people will continue

the mortgage with private banks then public because they're impressed by the level of honesty of private banks (Colin Beasty).

2.4 Performance of Banks

After the privatizations of state-owned banks, their performances in comparison with other banking

groups have increased by 95%. The performance of private banks after privatization of state banks had

significant reduces and this reduction indicates that the share of the market of newly privatized state-owned

banks increased. Although the performance of privatized state banks after privatization has increased

significantly (Khodaei et, al).

The economic reforms and the entry of private players have cause nationalized banks to revamp their

services and product portfolios to incorporate new, innovative customer-centric schemes. Nowadays, due to the

rise in competition, customer satisfaction is considered to be the most important thing in retail services but there is no noteworthy difference in customer satisfaction of public sector and the private sector banks (Vigget, al).

2.5 Price and Packages

Cheque deposits and cheque clearing are most common services used by customers, the charges levied

by the bank on these services are higher in private and foreign banks then in nationalized banks. Their study also

shows that the customers of public banks were not much satisfied with the behavior of employee and

infrastructure, while customers of private and foreign banks were not much satisfied with high charges,

approachability and communication. They have also suggested that training on stress management and public

dealing should be imparted to the employees of nationalized banks and nationalized banks need to improve their infrastructure and ambience to compete with private and foreign banks in India (Surabhiet, al).

Credit cards have become a part of life. In recent years there was a lot of demand has been shown for

credit cards and there is a lot of scope for credit cards business in India. The credit cardholders consider eleven

'very important' variables which "Satisfied" them are: Joining Fee, Annual fee, Minimum payment due, Cash

withdrawal possibility, Availability of ATMs, Life Insurance Cover, Card replacement fee, Air insurance,

Baggage cover, lost card liability-after losing the card and lost card liability-before losing the card (Chennappa,

D; Eliat, M.J).

2.6 Location and Infrastructure

Good sites and suitable site of the branch are essential for bank branches for smooth operation of

banking business. When the private banks were compared with public banks, all the private banks have

excellent locations from business point of view compared to public banks in India and for providing better

service to customers proper training should be given to the staff by the banks also public sector banks should

invest and concentrate more on staff development where as private sector gives more priority on infrastructural

aspects. The rigid policy of public banks creates more dissatisfaction among the customers while for private

banks mostly the value of service is the key factor of satisfaction (Uma et, al).

2.7 Quality of Customer Services

First dimension of customer satisfaction for nationalized banks is Service Orientation but, for private

banks Service orientation appeared as second dimension and they focuses more on customer satisfaction and

nationalized banks give more importance to Flexibility in Use of Services, Vision and Competency. Also

customers of nationalized banks had not been given much importance by the executives. On the other hand

Customer Satisfaction: A Comparison of Public and Private Banks of Pakistan

www.iosrjournals.org 3 | Page

customers of private banks had been offered these services right from the beginning therefore, customers of

private banks more satisfied (Jitendra Kumar Mishra).

The consumers of nationalized banks are more satisfied with service quality, than private banks and it‟s

required to ascertain the key success aspects in the industry, in terms of satisfaction of customers by keeping in

view the growing market size and the strong competition (Pooja Mengi).

The Private Banks came to existence within the last ten years with the objective of to limit the

government intervention in banks and from since then they try hard to obtain customer satisfaction even after a

short period of existence. According to a survey the result shows that private sector banks are more popular to

obtain customer satisfaction than the public sector banks (Farzad Asgarian).

Satisfaction of customers is the most important forecaster of service quality of banking sector.

Management of banks should confirm that the banking atmosphere should focus on quick and fair services to

their customers. Public sector banks are contributing more credit facility to fishermen and farmers than private

banks and the State Government announcement of giving the agricultural loan has given more satisfaction to the

consumers of public banks (N. Senthi kumar et, al).

The effort towards ease of banking and accessibility is preferred by the customer who is more seen in

private banks then public and customer care and customer retention programs should take into consideration by

public banks. In Kuwait Muslim customers are satisfied more with accessibility of ATM machines in multiple

locations, funds safety, ease to use ATM machines and service quality provided, but the worse element which

has been noticed in this study was that the interest rate on loans, which was the indicator of that the most of

customer in Kuwait give more intention to loans (Khaled et, al).

Service quality is an important feature of customer satisfaction in Indian banking industry irrespective

of public sector and the private sector banks and Customer satisfaction is found to be strongly associated with

propensity to recommend (Monica Bedi)

. Some of the respondents choose the SBI bank is because the bank is proving more ATM facility to the

customers and many of the respondents are saying the reason to choose the services of the SBI bank is because

they are good in efficient customer service but many of the respondents are not aware of the many services

Provided by the SBI bank. The few are deposit of cash in ATM, request for cheque book in ATM, end of the

day balance in mobile, etc. While some of the respondents choose the ICICI bank is because the bank is more

reliable to the customers and many of the respondents are saying the reason to choose the services of the ICICI

bank is because they are good in efficient customer service and efficient complaint handling. So finally both the

banks are competing equally with each other but SBI bank is little bit below the line in customer complaints

handling when compared to ICICI bank (M.J. Vidhyaa).

III. Research Framework A research framework has been developed to compare customer satisfaction among private and public

sector banks of Pakistan which includes research methodology, research model and questionnaire.

3.1 Methodology

A method has been designed to meet the objectives of research. For this purpose a questionnaire has

been adapted from three different research studies [1.Salman Khalid et al (2011), 2.Uma Shankar et, al (2010)

and 3.Khaled Al-Hashash et, al (2008)] and circulated in 5 different cities of Pakistan (Sukkur, Lahore, Islamabad, Rawalpindi and Peshawar). This questionnaire consists of two different parts. The first part is

showing respondents personal data such as gender, bank type, income, age, qualification and the second part

asked respondent to rate their satisfaction level to their bank from “strongly agree” to “strongly disagree” on

such variables which lead to build strong relationship with customers such as prices, reliability, technology,

customer service, location and infrastructure etc. This questionnaire was given to 500 different respondents out

of which 351 questionnaires were returned. Most of these responses were conducted myself and rest through the

help of friends and family.

Customer Satisfaction: A Comparison of Public and Private Banks of Pakistan

www.iosrjournals.org 4 | Page

3.2 Research Model

IV. FINDINGS

4.1 Background of Respondents

The first part of this questionnaire was designed to collect personal information of respondents such as

their gender, Age, bank type, income and qualification and the investigation shows that 65% of the respondents

are male and 35% are female of which, 42% of the respondents are having their account in public banks and

58% have their account in private banks. 72.6% respondents are from age group 18 – 25 years, 16.9% are from age group 26 – 33 years, 5.7% are from age group 34 – 41 years, 1.7% is from age group 42 – 50 years and

3.1% are from age group 51+ years. In terms of qualification only 0.6% are under matric, 1.6% have done

matric, 4.4% respondents have done intermediate, 76.2% are graduated and 17% respondents are post graduated.

In income segment 26% of the respondents having less than 20 thousand, 11.8% have 21 – 30 thousand, 18.5%

earn 31 – 50 thousand, 33.5% earn 51 – 100K and only 10.2% of the respondents earn more than 100 thousand

per month.

4.2 Mean Std. Deviation of Each Question

Questions

N Minimum Maximum Mean

Std.

Deviation

My bank gives me good compensation. 349 1.00 5.00 1.8195 1.10592

Services charges my bank imposes is competitive. 350 1.00 5.00 2.0514 .93188

My bank gives good interest rate on saving accounts. 349 1.00 5.00 2.1519 1.06262

My bank provides variety of service charges. 350 1.00 5.00 2.2000 1.07325

My bank provides good credit facilities. 346 1.00 5.00 2.2659 1.19120

My bank doesn‟t charge unnecessarily for not

maintaining minimum balance in account.

346 1.00 5.00 2.3642 1.19917

My bank provides ATM service in multiple locations. 350 1.00 5.00 1.8971 1.05480

My bank provides good E-Banking service. 348 1.00 5.00 2.1810 1.05415

My bank provides Phone account service facilities. 346 1.00 5.00 2.1821 1.12357

My bank provides Internet banking service. 351 1.00 5.00 2.1368 1.14072

My bank provides safety for my funds. 349 1.00 5.00 1.9484 1.00440

My bank‟s image and reputation is good. 344 1.00 5.00 2.1686 1.11473

I have open account in this bank because for personal

relationship with any of the employee.

350 1.00 5.00 2.2486 1.25921

Location of my bank is convenient. 348 1.00 5.00 2.0460 1.14543

Customer

Satisfaction

Customer Satisfaction: A Comparison of Public and Private Banks of Pakistan

www.iosrjournals.org 5 | Page

V. Conclusion Above analysis shows that customer satisfaction vary according to the nature of the services and in this

case, highest customer satisfaction is shown in such areas like price charged by banks is nominal, convenient

location of bank branches and staff attitude toward problem solving of customers. When the private sector banks

are compared with public sector banks, private bank customers were more satisfied with their bank because of

their multiple branches at convenient locations and technology (like check deposit machines, utility bill accepting machines etc.) which were not even seen in public sector banks. But when we talk about public sector

banks customers of public sector banks were more satisfied with reputation, reliability and the prices which

public sector banks impose on services like cheque/cash deposit and cheque/cash withdraw (it has been shown

that price charges are lower in public sector banks than in private sector). When we compare both types of banks

in terms of customer care service, private sector banks are favored more than public sector banks. Although

overall both public and private sector bank customers are satisfied with their banks but due to wide difference of

response, both public and private sector banks should concentrate on their weak areas in order to meet their

customer expectations and this study provides sort of guidelines to managers of banks to take suitable decisions

to get more satisfied responses from their customers.

VI. Limitations of the Study

Four limitations have been observed during this research. First, the research only focuses on public

and private banks, other banks like Foreign and Micro financial institutions that also plays good role

in Pakistani banking industry, has not been included in this research. Second, a limited number of

cities were covered in this research (Sukkur, Lahore, Islamabad, Rawalpindi and Peshawar only).

Third, the sample size and actual respondent numbers were limited because of limited time period.

Finally, permission to carry out study inside and outside banks has not been given so I had to reach

respondents individually which has consumed a lot of time as well.

VII. References

[1]. B. K. Tiwary (2011). Consumer Perception and Satisfaction of Banking Products and Services – A Comparative Study of Select

Indian Public and Private Sector Banks. Indian Streams Research Journal Vol - I. Chennappa, D; Eliat, M.J (2009). Satisfaction of

the Credit Card Holders of the Public, Private and Foreign Sector Banks. European Journal of Management Volume: 9, ISSN: 1555-

4015.

[2]. Colin Beasty (2005). Private Banks Rate High in Customer Satisfaction. CRM Magazine (Article# 43360).

[3]. Farzad Asgarian(2009). A Comparative Study on Service Quality and Customer Satisfaction of Public Banks and Private Banks in

Iran. Las Vegas International Academic Conference. Jitendra Kumar Mishra (2007). Constitute Dimensions of Customer

Satisfaction: A Study of Nationalized and Private Banks. Revista Tinerilor Economisti (The Young Economist Journal)vol. 1, issue

8, pages 40-47.

[4]. Khaled Al-Hashash and Abdulrasoul HussainBahzadi (2008). Bank„s Customer Satisfaction In Kuwait: An Exploratory Study.

Open University Malaysia.

[5]. Mohammad Khodaei Valahzaghard, Parinaz Koozehgar, Hassan Khodaei Valehzagharad & Mostafa Memarzade (2012).The

Comparison of Private State Banks and Other Banks in Iran.European Journal of Social Sciences ISSN 1450-2267 Vol.27 No.4.

[6]. Monica Bedi (2010). An Integrated Framework for Service Quality, Customer Satisfaction and Behavioral responses In Indian

Banking Industry a Comparison of Public and Private Sector Banks. Journal of Services Research Volume: 10, Issue: 1, Pages: 157-

172.

[7]. Muhammad Naveed (2009). Customer Satisfaction in Banking Sector. National University of Modern Languages.

My bank has multiple branches in Pakistan. 347 1.00 5.00 2.0259 1.09751

My bank provides good parking space facility. 347 1.00 5.00 2.1326 1.19718

Infrastructure of my bank is attractive and friendliness. 351 1.00 5.00 2.2393 1.19511

My bank staff attitude is friendliness. 350 1.00 5.00 2.0543 1.07587

My bank staff gives prompt attention to my needs. 345 1.00 5.00 2.0812 .98496

My bank staff understands my needs. 347 1.00 5.00 2.1729 1.06660

My bank staff handles my problems efficiently. 350 1.00 5.00 2.2000 1.13552

My bank provides me a good customer service. 347 1.00 5.00 2.1441 1.09491

My overall opinion about my bank is good. 348 1.00 5.00 2.1810 1.12810

I am satisfied with my bank. 345 1.00 5.00 2.1710 1.08493

I will not switch to any other bank. 348 1.00 5.00 2.3247 1.14170

Customer Satisfaction: A Comparison of Public and Private Banks of Pakistan

www.iosrjournals.org 6 | Page

[8]. M.J. Vidhyaa (2009). A Comparative study of customer services in ICICI (Industrial Credit And Investment Corporation Of India)

and SBI (State Bank of India). ICFAI National College, KEELKATTALAI.

[9]. N. Senthikumar, A.Ananth and A. Arulraj (2011). Impact of Corporate Social Responsibility on Customer Satisfaction in

Banking Service. African Journal of Business ManagementVol.5 (7), pp. 3028-3039.

[10]. Peter Kangis & Vassilis Voukelatos (1997). Private and Public Banks: A Comparison of Customer Expectations and

Perceptions. International Journal of Bank Marketing, Vol. 15 ISSN: 7, pp.279 - 287.

[11]. Puja Khatri & Yukti Ahuja (2010).Comparative Study of Customer Satisfaction in Indian Public Sector and Private Sector

Banks. International Journal of Engineering and Management Sciences Vol. 1: 42-51.

[12]. Pooja Mengi (2009). Customer Satisfaction with Service Quality: An Empirical Study of Public and Private Sector Banks. The

IUP Journal of Management Research, Vol. VIII, No. 9, pp. 7-17.Rengasamy Elango and Vijaya Kumar Gudep (2006). A

Comparative Study on the Service Quality and Customer Satisfaction among Private, Public and Foreign Banks. The IUP Journal of

Marketing ManagementIJMM10608.

[13]. Surabhi Singh &Renu Arora (2011). A Comparative Study of Banking Services and Customer Satisfaction in Public, Private and

Foreign Banks. Kamla- Raj, J Economics J Economics, 2(1): 45-56.

[14]. Uma Sankar Mishra, Bibhuti Bhusan Mishra, Swagat Praharaj & Ramchandra Mahapatra (2011). CRM in Banks: A Comparative

Study of Public and Private Sectors in India. European Journal of Social Sciences Volume 24.

[15]. Dr. Vijay M. Kumbhar (2011). Service Quality Perception and Customers Satisfaction in Internet Banking Service: A Case Study of

Public and Private Sector Banks. Cyber Literature Volume 4 Issue 2 ISSN 0972-0901.

IOSR Journal of Business and Management (IOSRJBM)

ISSN: 2278-487X Volume 1, Issue 5 (July-Aug. 2012), PP 06-08 www.iosrjournals.org

www.iosrjournals.org 6 | Page

Social Marketing: A Classic Case of Sustainability Model by Hindustan

Unilever Ltd.

Abstract: Growing consumer and increasing income growing of consumer opens many avenues for modern marketers to serve consumers. Market and society are the two sides of a single coin. To develop the society,

marketers have a greater role of sustainability. While manufacturing new product for the consumer group,

companies should take every precaution and necessary steps to protect the interest of the consumers as well as

safeguard the consumer’s priorities. A better and sustainable earth is also the concern for Govt. as well as

many companies of the globe, who are using resources of earth like water, minerals, trees etc for further

processing of their products. This paper focus on several steps initiated by HUL for their forthcoming as well as

current products, where company plans to launch many eco-friendly products which save mother earth as well

as protect consumer from any hazards.

Keywords: Sustainability, HUL, Consumer, Market. Social Marketing

I. Introduction: AMA defined Marketing as “Transfer of goods and services from producers/manufacturer to ultimate

consumers.” Social Marketing is the integration of Marketing Philosophy with changing nature of society.

Today consumer needs more comfort, quick solution for his problems, frequent change of his needs and

comfortable zone of shopping. This un-certainty ponders marketers to design their marketing planning in a more

systematic ways. The modified version of recently AMA definition on marketing somehow indicates towards

the above issues.

The revised definition of marketing as AMA stated is:

Marketing is → Creating (New Products Development.)

→ Communicating (Promotional Mix)

→ Supplying (SCM)

↓

→ Maintaining CRM with Consumers

In this process maintaining relationship with consumer play a pivotal role where company keeps every social change in the society into consideration while initiating any new plan of marketing.

II. HUL, A Milestone in FMCG Industry:

The46 billion FMCG giant HUL was formed in 1933 as Lever Brothers India Ltd. and came into being in 1956 as Hindustan Lever Ltd. through a merger of Lever brothers, Hindustan Vanaspati Mfg.co. Ltd.

and United Traders Ltd. HUL distribute its products through 2 million retail outlets across the country directly

and products are available in over 7.2 million outlets in the country. As per AC Nielsen market research data, two out of three Indians use HUL products. HUL is the market leader in Indian consumer products with

presence in over 20 consumer categories such as soaps, tea, detergents and shampoos.

Unilever Sustainable Living Plan (USPL) :

Unilever launched sustainable living plan in on 15th of November, 2010 at London, Rotterdam, New

York and New Delhi simultaneously. Under this plan, Unilever aims to achieve few goals by 2020. These goals

are :

Help more than one billion people to improve their health and well being.

Environment impact of their products should reduce to half of current status.

Outsource 100% of their agricultural raw materials sustainability.

Current Progress Report on Sustainability:

Unilever is on track in sustainable sourcing and livelihoods, but unable to reduce the environmental

impact. Company is currently focusing on seven major areas, where sustainability is required. These areas are :

Health and Hygiene

Nutrition

Waste foot print

Water foot print

Green house gases

Social Marketing: A Classic Case Of Sustainability Model By Hindustan Unilever Ltd.

www.iosrjournals.org 7 | Page

Sustainable sourcing

Better livelihoods

III. Health and Hygiene : According to UN estimates, over 2 billion people have limited access to safe drinking water. Many

Unilever brands offer hygiene benefits. Lifebuoy is one among them. By 2015, this brand aims to change the

hygiene behaviour of 1 billion consumers across Asia, Africa and Latin America by promoting the benefits of

hand washing at key times. In India, HUL has garnered immense learning from its years of experience in

conducting the Lifebuoy hand washing programme. The Madhya Pradesh Govt., impressed by the fact that the

incidence of diarrhea has dipped by 25% in a recent study. In Pakistan, Lifebuoy soap consumption has

increased by 8%. HUL‟s major toothpastes also play an important role helping to prevent tooth decay which is

one of the world‟s most common diseases and can lead to more serious health conditions. The simple practice of

brushing twice a day can make a big difference to oral health.

Also Pureit, company‟s in-home water purifier, provide water „as safe as boiled‟ without needing

electricity and at an affordable price to India‟s middle class consumers. “Khushiyon ka Doli” (Caravan of Happiness) is company‟s Lifebuoy brand promotional activities in rural India where it is reaching to 30 million

rural consumers directly.

IV. Nutrition: High level of obesity is now a concern for urban India where consumers are living more sedentary lives

and calorie rich foods are more available and affordable. Millions of the people around the globe remain hungry

or lack of essential nutrients in their diets. HUL, in its “Nutrition enhancement Programme” plans to improve

the nutritional quality. By 2020, company is planning to motivate around 100 million people to take its „Heart

Age‟ test for better and healthier lifestyle. Unilever has been gradually reducing salt levels in its products without changing its taste, as it is framed under the goal of company. The aim is to reduce the level of salt up to

the mark of 5 gm per day as based on globally dietary guidelines. Under food programme, company providing

micronutrient – enriched school meals to 95,000 school children of India, Bangladesh and Indonesia. Company

also committed to reduce saturated facts, Trans fat and calories from their different products to uplift

consumers‟ healthy eating habits.

V. Waste Foot Print:

Packaging is one of the important Ps defined by Marketing Scientists. It protects the products and

allows company to transport them safely from manufacturing base to consumer end. At the same time it can end up as waste, particularly in those countries where the infrastructure for recycling is poor. So company is

reducing the packaging and saving the materials, energy and transport. By 2020, company will reduce the

weight of packaging that what currently it is using by a third through light weighting materials. Company is

planning to provide consumers with refills for their home and personal care products to make it possible to reuse

the primary pack.

Sachets and pouches are an efficient use of packaging creating less waste by weight per milliliter of

product sold than bottles. Sachets play an important role in making everyday product affordable and accessible

to low income consumers. But recycling sachets really a challenging issue due to its low weight. But Unilever

introduce a technology called “Breakthrough Pyrolysis Process”, where used plastic sachets can be converted to

fuel. Company also eliminating PVC (Polyvinyl Chloride) from all its packaging by 2012. As company is the

firm believer of sustainability, hence it has joined hands with Bharti Retail to implement a programme called

„go recycle‟, where consumers are educated and informed about the practice of waste segregation. As a part or this programme, consumers were encouraged to bring empty plastic bottles and pouches of any brand from

selected FMCG categories. In return, the consumers were given discounts coupons for redemption.

VI. Water foot print: Water is a basic human need. The United Nations estimates that each person needs 20-50 liters per day

for drinking and daily tasks like cooking and washing. Water shortages are increasingly common and water

available per head or population will reduce further in the coming decade, as predicated by UN. Company is

committing to halve the water associated with the consumer use of its products by 2020. For Ex: Company is

planning to launch a dry shampoo that does not need water in a far easier way to reducing water consumption in the bathroom than pleading with them to use less water. The dry shampoo is spray on, absorbs oil from hair and

also lends volume. Company already introduced comfort one Ringe in Vietnam that reduces the use of water

from their buckets to one. Also introduces a leave on hair conditioner that doesn‟t need to be washed away. Also

a detergent that clean at room temperatures, doing away with the need for hot water at 70° Celsius in washing

machines.

Social Marketing: A Classic Case Of Sustainability Model By Hindustan Unilever Ltd.

www.iosrjournals.org 8 | Page

VII. Greenhouse Gases: By 2020 company is committing to halve the greenhouse gas impact of its products. Climate change

will have a growing impact on Unilever‟s business. Changing weather patterns put the suppliers of agriculture

raw materials in mess. So company is planning to set greenhouse gas reduction targets across the valve chain- from sourcing, manufacturing, transport and refrigeration all the way through to consumer use of the products.

Most of the greenhouse gas emissions are come from the hot water needed to use company‟s soaps and

shampoos in the shower. So company is persuading consumers to take shorter showers. By 2020, Co2 emissions

from global logistics network will be below the level of target set for 2010. Truck transportation may replace

with rail or ship to reduce Co2. Also it plans to improve the Energy efficiency of its warehouses.

VIII. Sustainable Sources: Half of Unilever‟s raw materials come from either farms or forests. Agriculture and forestry are the

largest contributors to global greenhouse gas emissions and are the major drivers of climate change. So Unilever is committed to sourcing sustainably all agricultural raw materials by 2020. By 2015, company will purchase all

palm oil from certified sustainable sourcing, for soy beans target set is 2014 and for soy oil by 2020.

Unilever‟s master brand Lipton tea bags will source from Rainforest Alliance certified estates by 2015.

Company will purchase 100%. Sustainable fruits and vegetables by 2015. Sustainable sunflower oil, Rapeseed

oil and diary will be sourced by the company by 2020.

IX. Better Livelihood: Company plans to help small holder farmers and Micro-entrepreneurs under project Shakti. It will

increase the numbers or Shakti Ammas from 45,000 to 75,000 in 2015. To strengthen the project, Company introduced the concept of “Shaktimaan” under which men of Shakti families are given bicycle to cover

surrounding villages to increase HUL‟s distribution and sales as well as enhance the income of Shakti families.

Currently 30,000 Shaktimaans are working across India. HUL is also partnering with a leading public sector

bank in India for enabling banking service to rural consumers and low income people is Shakti villages. HUL is

also entered into a partnership on telecom distribution with a leading telecom company to sell its products and

servicing across rural India. This initiative will help Shakti entrepreneurs to increase their income by selling

telecom products and services to retailers, as well as directly to consumers.

X. Conclusion : Unilever, as in the USLP, has put out a list of clean wants- all focused on sustainability- like fighting

viruses, reduction of salt in food products, preserving food naturally, storing renewable energy, sustainable

showering, and finally twisting the consumer behavior through its nobly created sustainable models. These

factors are also helping company to increase its goodwill and support the sales volume target. Any social

initiatives must be verified and weighted according to the consumer‟s perception and Unilever perfectly did the

same by keeping its ideas fit to the shoes of consumer‟s mentality.

Reference : www.unilever.com/sustainble-living www.hul.co.in

www.wikipedia.com

HUL Bets on innovations to Reach Sustainable goal, The Economics Time, 25th April 2012

IOSR Journal of Business and Management (IOSRJBM)

ISSN: 2278-487X Volume 1, Issue 5 (July-Aug. 2012), PP 09-19 www.iosrjournals.org

www.iosrjournals.org 9 | Page

An Empirical Study of Servqual as a Tool for Service Quality

Measurement

Sabrina Tazreen Lecturer. (Marketing)

Faculty of Business Administration, University of Science and Technology Chittagong.

Abstract: To survive and excel in today’s competitive market organizations must realize the significance of

customer-oriented business philosophies and quality management approaches in managing the business.

Customers are becoming more aware of their requirements. Their expectations and perceptions are continually

evolving making it more difficult for the service providers to measure and manage services effectively and

efficiently. Implementation of total quality in the service industry is comparatively more complex and difficult due

to the fact that quality of services cannot be defined objectively. Additionally, service industry by nature has less control over factors which affect quality. Very few methods are considered to be effective measurement tools for

services so far while a number of methods have been introduced and practiced for measuring the quality of

physical goods. This paper attempts to highlight the implication of SERVQUAL, one of the widely accepted

methods for measuring service quality. The SERVQUAL methodology is briefly demonstrated by a small survey

conducted on a randomly selected bunch of customers regarding the service quality provided by a particular

commercial bank. The paper concludes with some recommendations regarding further research topics related

to service quality measurement.

I. Introduction:

A woman walked up to the branch manager of a bank. "Are you hiring any help?" she asked. "No," he said. "We already have all the staff we need."

"In that case, would you mind trying to find someone to help me in the safe deposit area?" she asked.

This story is just a comical representation of a customer‟s dissatisfactory reaction resulted from a

service failure of a bank. The term Customer Satisfaction has become the prime concern of most of the

organizations to be competitive in the industry. Determining and meeting customer expectation regarding

services is the key to make satisfied customers and the best way for determining customers‟ needs and

expectation is the use of surveys and researches- the key vehicle for understanding customer expectations and

perceptions of services.

This paper attempts to focus the implication of SERVQUAL scale for measuring service quality in

terms of the differences between the customer expectations and their perceptions regarding the service

consumed. Measuring service quality had always been a challenge for service providers because of the intangible

and most notably the inseparable and heterogeneous nature of service. As such services are more akin to

performances rather than objects. These distinctions enabled Parasuranam, Zeithmal & Berry (1985) to develop

an instrument for measuring Service quality, SERVQUAL, which has subsequently dominated both academic

and practitioner perspectives (Buttle, 1996; Robinson,1999). SERVQUAL measures perceptions of service

quality across five dimensions: tangibles; reliability; responsiveness; assurance and empathy.

SERVQUAL (an acronym derived from the term „Service Quality‟) is a well tested survey method for

measuring service quality which focuses on five service quality dimensions. SERVQUAL surveys usually include 22 service areas distributed throughout the five service quality dimensions. The survey often asks the

customers to provide two different ratings on each attribute- one reflecting the level of service they would

expect from excellent companies in a given sector and the other reflecting their perception of the service

delivered by a specific company within a sector. The difference between the expectation and perception rating

constitutes a qualified measure of service quality.

Service industries cover a wide range of differentiated organizations such as health care, education,

banking, insurance, hotels, transport, restaurant, etc. Such systems involve a very large variety of business

processes and a large scale interaction with variety of customers. SERVQUAL method is more or less suitable

for most of the service sectors. Still, the scope of SERVQUAL survey is limited to some particular sectors. The

use of SERVQUAL seems to be most effective in financial services, health care and education sector. This

An Empirical Study of Servqual as a Tool for Service Quality Measurement

www.iosrjournals.org 10 | Page

paper attempts to demonstrate the methodology of SERVQUAL by a survey conducted on the customers of a

local commercial bank regarding the retailing banking services provided by the bank. The bank has been termed

as Bank X (hypothetical name). The sample size includes only forty customers because of the time and cost

constraints. The questionnaire was made shorter by selecting 16 questions from among the 22 structured

questions. In fact the survey only exhibits the implication and methodology of SERVQUAL in a service

industry.

II. Defining Service and Service Quality Measurement:

Thus, Service quality is a concept that has aroused considerable interest and debate in the research

literature because of the difficulties in both defining it and measuring it with no overall consensus emerging on

either (Wisniewski, 2001). There are a number of different "definitions" as to what is meant by service quality.

One that is commonly used defines service quality as the extent to which a service meets customers‟ needs or expectations (Lewis and Mitchell, 1990; Dotchin and Oakland, 1994a; Asubonteng et al., 1996; Wisniewski and

Donnelly, 1996). Service quality can thus be defined as the difference between customer expectations of

service and perceived service. If expectations are greater than performance, then perceived quality is less than

satisfactory and hence customer dissatisfaction occurs (Parasuraman et al., 1985; Lewis and Mitchell, 1990).

However the study of service quality did not come into its own as an area of marketing importance

until research in the early 1980s established that attitude was a significant part of service quality. The earliest

concern for what has become to be known as service quality appeared in 1976. Anderson, et al (1976)

recognized importance of selection as a priority for obtaining and retaining customers.

Churchill and Suprenant (1982) were among the earliest to hold the view later shared by others that

service quality was an attitude. They were the first researchers to see the significance of attitude as a principal

factor leading to superior service quality. One year after this significant research, Lewis and Booms (1983)

concluded that satisfaction was similar to attitude, and consequently they noted the significance of processes and outcomes in defining service quality.

A number of scholars have conducted services quality researches and opined in different ways about

service quality. Some of those are Holbrook and Corfman, Maynes, Zeithaml, Cronin, Jr. and Taylor,

Dabholkar, Bitner and others.

In an attempt to address the issue of how to measure service quality, a scale based upon the utilization

of ten elements was developed by Parasuraman, et al based upon a series of focus group interviews, which could

be used to measure service quality perceptions. Originally, the ten elements developed for use in measuring

service quality were tangibles, reliability, responsiveness, competence, courtesy, credibility, security, access,

communications, and understanding the customer. Further studies by Parasuraman, et al (1988) brought about a

major modification that changed the dimensions that could be used to measure service quality perceptions.

Three of the original ten elements—tangibles, reliability, and responsiveness—remained unchanged. The other seven original elements were combined into two elements. Those elements known as competence, courtesy,

credibility, and security were combined to form one of the new elements known as assurance, and the elements

of access, communications, and understanding the customer were combined to form the new element known as

empathy.

Now, the five elements that made up what the authors called SERVQUAL were the following five

dimensions of service quality: tangibles, reliability, responsiveness, assurance, and empathy. The factors

covered by the dimensions are given in the following table:

Table 1

Dimensions Factors

Tangibles Physical facilities, equipment and appearance of personnel.

Reliability Ability to perform the promised service dependably and

accurately.

Responsiveness Willingness to help customers and provide prompt service.

Assurance Knowledge and courtesy of employees and their ability to

inspire trust and confidence.

Empathy Caring and individualized attention that the firm provides

to its customers.

Table: 1: Dimensions of Service Quality

An Empirical Study of Servqual as a Tool for Service Quality Measurement

www.iosrjournals.org 11 | Page

•Tangibles: Tangibles would include those attributes pertaining to physical items such as equipment, buildings,

and the appearance of both personnel and the devices utilized to communicate to the consumer. Bitner (1992)

presented her conceptual framework for examining the impact of physical surroundings as it related to both

customers and employees. Berry and Clark (1991) provided validation of the physical appearance on the

consumer‟s assessment of quality. With the research by Bitner (1990), it was noted that physical appearance

might influence the consumer‟s level of satisfaction. Tangible was one of the original dimensions that were not modified by Zeithaml, et al (1988).

•Reliability: Reliability relates to the personnel‟s ability to deliver the service in a dependable and accurate

manner. Numerous researchers, including Garvin (1987) found that reliability tends to always show up in the

evaluation of service. Parasuraman, et al (1988) indicated that reliability normally is the most important attribute

consumers seek in the area of quality service. It was also determined by Parasuraman, et al (1991) that the

conversion of negative wording to positive wording as suggested by Babakus and Boller (1991) and Carman

(1990) increased the accuracy of this dimension. Negative wording in the request for a customer response

caused the customer to misinterpret this particular determinant. Walker (1995) found that if there is an adequate delivery of the basic level of service, then peripheral performance leads consumers to evaluate the service

encounter as satisfactory. Reliability was one of the original dimensions not modified by Zeithaml, et al (1988).

•Responsiveness: The desire and willingness to assist customers and deliver prompt service makes up the

dimension of responsiveness. Parasuraman, et al (1991) include such elements in responsiveness as telling the

customer the exact time frame within which services will be performed, promptness of service, willingness to be

of assistance, and never too busy to respond to customer requests. Bahia and Nantel (2000) disregarded

responsiveness in their research, claiming a lack of reliability even though they recognized SERVQUAL and all of its dimensions as the best known, most universally accepted scale to measure perceived service quality.

Responsiveness was also one of the original dimensions not modified by Zeithaml, et al (1988).

•Assurance: Knowledgeable and courteous employees who inspire confidence and trust from their customers

establish assurance. In banking studies by Anderson, et al (1976), it was determined that a substantial level of

trust in the bank and its abilities was necessary to make the consumer comfortable enough to establish a banking

relationship. Parasuraman, et al (1991) included actions by employees such as always courteous behavior instills

confidence and knowledge as prime elements of assurance. Assurance replaces competence, courtesy,

credibility, and security in the original ten dimensions for evaluating service quality (Zeithaml, et al, 1988).

•Empathy: Empathy is the caring and personalized attention the organization provides its customers. Individual

attention and convenient operating hours were the two primary elements included by Parasuraman, et al (1991)

in their evaluation of empathy. The degree to which the customer feels the empathy will cause the customer to

either accept or reject the service encounter. Empathy replaces access, communication, and understanding the

customer in the original ten dimensions for evaluating service quality (Zeithaml, et al, 1988).

III. Methodology Of SERVQUAL Survey For Measuring The Gap Between Customer

Expectation And Their Perception Regarding The Service Provided By Bank X: A small survey has been conducted on the customers of „Bank X‟, locally serving for more than one

decade to represent the way to conduct SERVQUAL survey. The instrument‟s design causes it to be best suited

for use as a diagnostic methodology utilized for determining large areas of service quality strengths and

weaknesses. To evaluate the five service quality dimensions, sixteen statements were selected from the structured

SERVQUAL questionnaire format and then modified to make it precise and best suitable for banking sector.

The number of questions was squeezed because of the convenience of collecting responses from the customers

who were less willing to answer so many questions.

Two sets of questionnaires were prepared including sixteen identical statements. One set of questions

asks the customers to indicate the extent to which the bank‟s services should possess the features described by

each statement. The other set asks about their views regarding the extent to which they believe Bank X has the features and benefits described by the statement.

The questionnaire representing customer expectation focuses on the word „should‟ to state the level of

expectation regarding each criterion. A seven point Likert scale is used to get the level of expectation and

perception associated with each service quality criterion. After conducting the survey all the questionnaires were

collected for tabulation and analysis.

An Empirical Study of Servqual as a Tool for Service Quality Measurement

www.iosrjournals.org 12 | Page

Target sample: Generally, the customers of Bank X are categorized into two major groups: Corporate

customers and Retail customers. The retail customers have been chosen to conduct the survey as corporate

clients are treated to be the most valued ones and they usually get separate concentration and best services.

Moreover they are difficult to access. Thus, the retails customers are more likely to provide the most accurate

response regarding the service.

Sample size: The research sample consists of 40 customers of different branches of Bank X

Data Analysis: For the analysis of the collected data a primary or rough analysis was conducted to validate the

questionnaire for gathering the adequate information. The filled up questionnaires were scanned to discard

unwanted or insincere responses. The data analysis was conducted using SPSS.

Table: 2 The 16 statements used for collecting responses:

An Empirical Study of Servqual as a Tool for Service Quality Measurement

www.iosrjournals.org 13 | Page

Table 3:

To make the calculation clear let’s consider any one statement from the questionnaire. The following

table represents the calculation of the difference between the scores of Questionnaire 1 and 2. Statement

Table: 4

An Empirical Study of Servqual as a Tool for Service Quality Measurement

www.iosrjournals.org 14 | Page

Table 5: The following table shows the average gap between customer expectation and their perception

regarding various service features of Bank X.

Service Quality

Dimensions

Mean

Difference of

each

statement

Mean difference for each SQ

Dimension

Tangibles

Statement 1 -1.2

- 0.61

Statement 2 0.325

Statement 3 -0.05

Statement 4 -1.525

Reliability

Statement 5 -0.85

-0.775

Statement 6 -0.775

Statement 7 -0.55

Statement 8 -0.925

Responsiveness

Statement 9 -2.125

- 1.61 Statement 10 -1.175

Statement 11 -1.525

Assurance

Statement 12 -1.1

- 0.72 Statement 13 -0.825

Statement 14 -0.225

Empathy

Statement 15 -0,07

- 0.0725 Statement 16 -0.075

Table 5 represents the average gap score between customer expectation and perception. The charts of details

analysis have been attached with the appendices. The average gap score for all the service quality dimensions of

Bank X are showing negative figure where the highest gap scores were for responsiveness. The rest four

dimensions show comparatively smaller gap that represents lesser customer dissatisfaction regarding the

services.

IV. Scope of SERVQUAL survey

The concept of measuring the difference between expectations and perceptions in the form of the SERVQUAL

gap score proved very useful for assessing levels of service quality. Parasuraman argued that, with minor

modification, SERVQUAL can be adapted to any service organization. Information on service quality gaps can

help managers diagnose where performance improvement can best be targeted. The largest negative gap,

combined with assessment of where expectations are highest, facilitates prioritization of performance

improvement. Equally, if gap scores in some aspects of service do turn out to be positive, implying expectations

An Empirical Study of Servqual as a Tool for Service Quality Measurement

www.iosrjournals.org 15 | Page

are actually not just being met but exceeded, then this allows managers to review whether they may be "over-

supplying" this particular feature of the service and whether there is potential for re-deployment of resources

into features which are underperforming.

V. Limitations of SERVQUAL Survey

There have been a number of studies that doubt the validity of the 5 dimensions and of the uniform

applicability of the method for all service sectors. Despite Parasuraman et al.'s (1988) initial claim that

their five service quality dimensions are generic, it is generally agreed that this is not the case, and that the

number and definition of the dimensions varies depending on the context. When measuring the quality of

accounting firms, Freeman and Dart (1993) conclude that service quality is a seven-dimensional construct.

Robinson and Pidd (1998) propose 19 dimensions of service quality in the context of management science

projects. According to Stauss & Weinlich (1997), a closer look, however, reveals some deficits of attribute-

based quality measurement (like SERVQUAL). First, the data collected by these methods cannot

completely reflect the customer's quality perception. Second, the respondents are forced to aggregate their

quality experiences in a problematic way. For example, a customer of a bank asked to evaluate the

friendliness of customer contact employees of a bank is forced to tick a single point on a scale even if

he/she had contacts with three employees whose behavior and friendliness differed considerably.

Teas (1994) noted that SERVQUAL expectations have been variously defined as desires, wants, what

a service provider should possess, normative expectations, ideal standards, desired service, and the level of

service a customer hopes to receive. These multiple definitions and corresponding operationalizations of

“expectations” in the SERVQUAL literature result in a concept that is loosely defined and open to

multiple interpretations (Teas, 1994). Different interpretations of “expectations” include a forecast or

prediction, a measure of attribute importance, classic ideal point, and vector attribute (Teas, 1993; Parasuraman et al., 1994b). These various interpretations can result in potentially serious measurement

validity problems.

VI. Recommendation For Further Studies/ Researches Regarding Measuring Service

Quality:

Use of SERVQUAL scale in GAP Analysis model of measuring Service Quality: From the perspective of specific service sector/ organization

Use of some contemporary models to measure service quality. (Like SERVPERF for Education service)

Development of a conceptual framework to measure the web-based service quality using the SERVQUAL model.

Modification of SERVQUAL scale

References: [1]. Bexley, James B. (1999), Service quality: an empirical study of expectations versus perceptions in the delivery of financial services in

community banks, University of Stirling, December 2005

[2]. Parasuraman, A., Valarie A. Zeithaml , and Leonard L. Berry (1985), “A Conceptual Model of Service Quality in its Implications for

Future Research,” Journal of Marketing, 49 (Fall), 41-50.

[3]. Zeithaml, Valarie A., Mary Jo Bitner (1990), Services Marketing, New York, Irwin McGraw Hill.

[4]. Parasuraman, A., Zeithaml, V.A., and Berry, L.L. (1988): SERVQUAL: A multiple-item scale for measuring consumer perceptions of

service quality. Journal of Retailing, 64, 41-50.

[5]. Peter, J. P., Churchill, G. A., & Brown, T. J. (1993). Caution in the use of difference scores in consumer research. Journal of

Consumer Research, 19(1), 655-662.

[6]. Paul R. Messinger, A Service Quality Audit: An Application of the Gap Analysis Model, (University of Alberta, 1990

[7]. http://www.12manage.com/methods_zeithaml_servqual.html

[8]. http://en.wikipedia.org/wiki/SERVQUAL

[9]. http://findarticles.com/p/articles/mi_qa3713/is_200007/ai_n8893832 [10].

Appendix

Customers’ Questionnaire (Expectation)

Dear Respondents,

Any information you provide will be kept strictly confidential. This survey is completely voluntary. Your full participation would greatly help the cause of the study.

Instruction: Please indicate the extent to which the services provided by Bank X should possess the features described

by each statement.

Please circle one number for each statement

An Empirical Study of Servqual as a Tool for Service Quality Measurement

www.iosrjournals.org 16 | Page

Appendix

Customers’ Questionnaire (Expectation)

Dear Respondents,

Any information you provide will be kept strictly confidential. This survey is completely voluntary. Your full

participation would greatly help the cause of the study.

Instruction: Please indicate the extent to which you believe Bank X has the features and benefits described by the

statements.

Appendix

An Empirical Study of Servqual as a Tool for Service Quality Measurement

www.iosrjournals.org 17 | Page

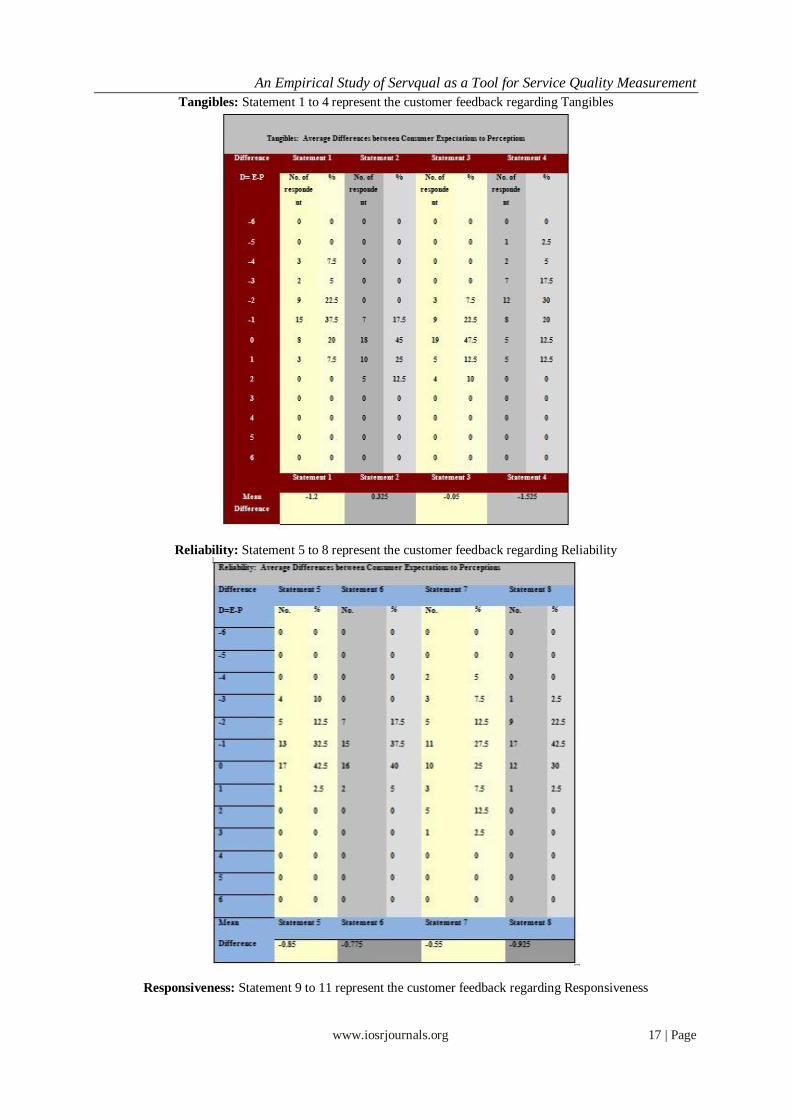

Tangibles: Statement 1 to 4 represent the customer feedback regarding Tangibles

Reliability: Statement 5 to 8 represent the customer feedback regarding Reliability

Responsiveness: Statement 9 to 11 represent the customer feedback regarding Responsiveness

An Empirical Study of Servqual as a Tool for Service Quality Measurement

www.iosrjournals.org 18 | Page

Appendix Assurance: Statement 12 to 14 represent the customer feedback regarding Assurance

An Empirical Study of Servqual as a Tool for Service Quality Measurement

www.iosrjournals.org 19 | Page

Appendix

Empathy: Statement 15 and 16 represent the customer feedback regarding Empathy

Empathy: Average Differences between Consumer Expectations to Perception

Difference

D= E- P

Statement 15 Statement 16

No % No %

-6 0 0 0 0

-5 0 0 0 0

-4 0 0 0 0

-3 2 5 0 0

-2 10 25 5 12.5

-1 9 22.5 8 20

0 13 32.5 16 40

1 5 12.5 8 20

2 1 2.5 2 5

3 0 0 1 2.5

4 0 0 0 0

5 0 0 0 0

6 0 0 0 0

Mean

Difference

Statement 15 Statement 16

-0.07 -0.075

IOSR Journal of Business and Management (IOSRJBM)

ISSN: 2278-487X Volume 1, Issue 5 (July-Aug. 2012), PP 20-27 www.iosrjournals.org

www.iosrjournals.org 20 | Page

Law Enforcement In Malaysian Securities Markets

Asmah Laili Yeon 1, Faridahwati Samsuddin

2

1(Associate Prof. Ph.D, School of Law, College of Law, Government and International Studies,

Universiti Utara Malaysia, Malaysia) 2(Senior Lecturer Ph.D, School of Human Resource, College of Business, Universiti Utara Malaysia, Malaysia)

Abstract : The objective of this paper is to discuss issues of law enforcement in Malaysian Securities Markets.

This survey was conducted among 107 principal and representative licensees registered with the Securities

Commission of Malaysia. They consist of licensed dealers, investment advisers and fund managers. The majority

of the respondents were capital markets and services representative licensees (CMSRL), while only 17 respondents were capital markets and services licensees. On a scale of one to five, respondents were found to be

generally satisfied with the roles and responsibilities of enforcement bodies i.e. Securities Commission and

Bursa Malaysia (mean of satisfaction = 3.660 to 3.952). The study shows that there is a positive relationship

between the views and attitudes of respondents towards the implementation of the legal philosophy by the

enforcement bodies (r= .524, r= .480). As the main enforcement agencies, Securities Commission and Bursa

Malaysia should further enhance efforts to monitor and enforce the law of capital markets. In conclusion, this

paper provides useful information in relation to factors contributing to non compliance of participants of the

capital markets. The enforcement bodies can implement measures on how to curb the unethical behaviour by

carrying out ethics training and introducing new rules and regulations for the industry.

Keywords - enforcement of law, investor protection, non-compliance, securities law, securities commission

I. INTRODUCTION Capital and services markets provide a useful means to mobilize capital and harness economic interests

in an efficient manner to drive innovation and growth. Toward this end, Malaysia has implemented various

measures to make the capital markets more attractive and competitive in the form of Disclosure Based Regulations (DBR) through the Malaysian Capital Markets Master Plan 2000 – 2010. Recently, in 2011, the

Securities Commission of Malaysia launched the second phase of the plan which focuses more on the regulatory

challenges, growth, international standards and governance. In 2010, the Malaysian capital markets generated

substantial income for the country. The equity market generated market RM1,275 billion, the bond market

RM759 billion, the Islamic Capital Markets RM1,050 billion, the investment management RM377 billion, and

the derivatives market RM43 billion (Securities Commission, 2011) [1]. The huge income generated by this

industry is because of the capital and services market in Malaysia is well-regulated and this is recognized by the

International Organization of Securities Commission (IOSCO, 2011) [2]. Further, Malaysia is the signatory to

cross-border enforcement arrangements and known for high standards of regulation internationally. The MMOU

has enhanced the SC's supervision and enforcement capabilities in dealing with cross-border market abuse,

particularly in the area of financial fraud and insider trading, and has raised the level of overall investor

protection in Malaysian market (Neetasha Rauf, 2012) [3]. The main regulator for the industry is the Malaysian Securities Commission which has a legal power under the Securities Commission Act 1993, whereas, the Bursa

Malaysia is the main registered stock exchange in Malaysia and acting as a self regulator body for its members

and recognized and given powers under the Capital Markets and Services Act 2007. They play important roles

to enhance the securities markets and services in Malaysia. The Malaysian securities markets regulation has a

comprehensive legal framework. But looking at the statistic of securities crimes in Malaysia, it shows increasing

numbers in cases of securities crimes (Securities Commission, 2011) [4]. For example between 2004 and 2006,

2006 there were nine cases involving misconduct in securities transactions. The study by Asmah, Nurli, and

Rohana (2002) [5] found that among the categories listed company involved in the non-compliance with the

Listing Requirements of the KLSE (now known as Bursa Malaysia) is the manufacturing industry (24%),

construction (18.7%), and securities market industry (14.7%). Other industries, however, showed a relatively

low percentage of non-compliance. Therefore, it is paramount important to discuss about the findings of the study in relation to law enforcement in Malaysian Securities Markets.

II. LITERATURE REVIEW Malaysia has fully observed one of the 32 benchmarks (on accounting standards) and has largely

observed nearly all of the benchmarks under the six categories of methodology (81% of 32 benchmarks) [6].

Since then, Malaysia continued to close the gaps on the remaining shortcomings, the most significant being amending the Companies Act 1965 (CA) to address gaps in related-party transactions, penalties for

Law Enforcement in Malaysian Securities Markets

www.iosrjournals.org 21 | Page

contravention by directors, private enforcement capacity of investors and disclosure; amending the listing

requirements for stricter disclosures by listed companies; implementing measures to expand the role of the

audit committee in line with international best practices; the Capital Market & Services Act 2007 (CMSA)

enhancing the effectiveness of regulatory oversight of the SC by empowering it to institute civil proceedings;

and transforming GLCs into high-performing entities and upgrading of GLC boards

.

1. Enforcement Bodies: Securities Commission and Bursa Malaysia

The Securities Commission established on 1 March 1993 under the Securities Commission Act 1993.

The Commission is a self-funding statutory body with investigative and enforcement powers. It reports to the

Minister of Finance and its accounts are tabled in Parliament annually. The SC's many regulatory functions

include supervising exchanges, clearing houses and central depositories; registering authority for prospectuses

of corporations other than unlisted recreational clubs; approving authority for corporate bond issues; regulating

all matters relating to securities and futures contracts; regulating the take-over and mergers of companies

;regulating all matters relating to unit trust schemes; licensing and supervising all licensed persons; encouraging

self-regulation; and ensuring proper conduct of market institutions and licensed persons.

Improving transparency and benchmarking against best international practices have been key factor in

transforming the Malaysian capital market as an efficient source for raising longer-term funds to finance

economic activity. Reflecting the importance accorded to meeting international standards, 43 of the 152 recommendations in the Capital Market Master plan that were released in 2002 were related to improving

transparency and promoting higher standards of disclosures. To date, 37 of these 43 recommendations has been

implemented (2010, Securities Commission) [7]. Further, the Securities Commission, as the competent

regulatory authority for oversight of the capital market, has voluntarily undertaken independent assessments

under the various standards set by the IMF/World Bank, and the International Organisation of Securities

Commissions (IOSCO). The SC has also supported the move to comply with international best practices on

accounting-related matters.

In relation to the implementation of Code of Corporate Governance, Malaysia voluntarily agreed to be

assessed under the Corporate Governance Reports on the Observance of Standards and Codes (CG ROSC) by

the World Bank in 2005, based on a methodology that is benchmarked against the internationally accepted

OECD Principles of Corporate Governance. Malaysia has published the CG ROSC that was completed in 2005. Malaysia has fully observed one of the 32 benchmarks (on accounting standards) and has largely

observed nearly all of the benchmarks under the six categories of methodology (81% of 32 benchmarks). Since

then, Malaysia continued to close the gaps on the remaining shortcomings, the most significant being amending

the Companies Act 1965 (CA) [8] to address gaps in related-party transactions, penalties for contravention by

directors, private enforcement capacity of investors and disclosure; amending the listing requirements for

stricter disclosures by listed companies; implementing measures to expand the role of the audit committee in

line with international best practices; the Capital Market & Services Act 2007 (CMSA) enhancing the

effectiveness of regulatory oversight of the SC by empowering it to institute civil proceedings; and

transforming GLCs into high-performing entities and upgrading of GLC boards. In addition, the SC is also

working closely with the respective Malaysian accounting boards to integrate accounting principles, with a

commitment on full convergence with international accounting standards by 2012.

As for Bursa Malaysia, in striving to build a market of quality and integrity, it is guided by regulatory principles to achieve goals in the aspect of (a) investor protection to remain intact, (b) high standards of

business conduct by listed issuers and brokers and (c) efficient and effective (Bursa Malaysia, 2012) [9].

2. Law, Principles, Rules and Policy

The Capital Markets and Services Act 2007 (CMSA 2007) [10] states offences of securities crimes

includes false trading, market rigging, market manipulation, fraudulent and misleading trading, dissemination of

false trading and insider trading. Implementation of dual sanction, criminal and civil actions in combating

securities crimes is seen as an effective strategy. These provisions are stated in the CMSA 2007 in Part V,

Division 1, section 175 to 201.

According to the Bursa Malaysia in managing conflicts of interests with public interest, public interest and in

particular the need for investor protection should prevail and the measures are separation of the regulatory functions from the commercial functions to ensure that these functions operate independently; and that business

units within Bursa Malaysia are not in a position to influence any supervisory or regulatory decisions made by

regulation.(Bursa Malaysia, 2012) [11].

As for Bursa Malaysia in regulating market misconduct, it has the Business Rules of Bursa Malaysia Securities

Berhad (Market Misconduct) [12] where the key trading rules that market surveillance focuses on the following

issues: (a) Rule 401.1(2) where participating Organisations (POs), Heads of Dealing (HD) and Dealer's

Representative (DR) shall refrain themselves from engaging in, or be a party to, any unethical practices that may

Law Enforcement in Malaysian Securities Markets

www.iosrjournals.org 22 | Page

damage the confidence of investors and hamper the sound development of the stock market, (b) Rule

401.1(3)(a) and (b) where POs, HD and DR shall avoid, and shall not participate in any operation by others

which might have the same result, any act or practice which might lead to a false or misleading appearance of

active trading in any securities on the stock market of the Exchange or a false or misleading appearance with