BANK OF UGANDA FOREWARD LOOKING FINANCIAL STABILITY REPORTS Charles Augustine Abuka.

29

BANK OF UGANDA FOREWARD LOOKING FINANCIAL STABILITY REPORTS Charles Augustine Abuka

-

Upload

gary-stafford -

Category

Documents

-

view

220 -

download

2

Transcript of BANK OF UGANDA FOREWARD LOOKING FINANCIAL STABILITY REPORTS Charles Augustine Abuka.

BANK OF UGANDA

FOREWARD LOOKING FINANCIAL STABILITY REPORTS

Charles Augustine Abuka

Introduction

• The global economic and financial crisis has demonstrated the need to strengthen cooperation among countries to improve regulatory requirements for the financial system.

• It has hastened an improvement in the mechanisms for

crisis prevention, management and resolution.

• COMESA member states have made a decision to improve at each country level the understanding of issues related to stress testing, financial stability analysis and reporting.

1

Introduction

• This manual focuses attention to forward looking financial stability analysis, reports and stress-testing.

• COMESA countries are making efforts to provide clear terms of reference for staff working on financial stability assessment.

• The steps to develop and communicate a robust list of

macroprudential instruments to address existing and potential threats to financial stability are being undertaken. 2

Introduction• COMESA countries have started developing their own

stress testing models for both micro and macro stress testing.

• Central banks are also taking steps to become familiar with the models and risk management practices of commercial banks operating in their countries.

• Some member states now run stress testing exercises at home and are improving data about banks’ cross-border exposures.

3

The Role of Financial Stability Reports • Financial Stability Reports that are issued with the aim of limiting

financial instability by pointing out key risks and vulnerabilities to policy makers, market participants and the public at large.

• Effective financial stability analysis should have three main characteristics: It should be forward looking. It should be mainly concerned with

the identification and quantification of (systemic) risks. It is should be comprehensive. Several disciplines, models, sources

of data and expertise are necessary for financial stability analysis. Its purpose should be to motivate action, either by either policy

makers or economic agents.

4

The Role of Financial Stability Reports

• More than 80 central banks around the world now issue Financial Stability Reports.

• The major drawback is that a number of Financial Stability Reports are not forward looking.

• They have insufficient analysis of risks and vulnerabilities and are less useful in the assessment of systemic risk.

5

The Role of Financial Stability Reports

• There are two main aims that should motivate central banks in the COMESA region to publish Financial Stability Reports:These aims are external and internal. The external aims

are: to contribute to overall financial system stability; to increase accountability of the financial stability

function; to strengthen cooperation on the financial stability

function among various relevant authorities. 6

The Role of Financial Stability Reports • The internal aims of financial stability assessment require that central

banks monitor key risks, quantify the impact of shocks and make recommendations to guide policy discussions.

• The production of the FSR should help to: improve the awareness of systemic risks among a various

structural units in a central bank; encourage the exchange of relevant information and analysis across

functional areas to build a “bridge” between economic, financial stability and supervision units;

the discussion of appropriate policy options within an integrated framework;

the taking of timely policy decisions.

7

The Role of Financial Stability Reports

• Central banks in the region should ensure that their Reports put emphasis on financial soundness indicators.

• The Financial Stability Reports should be based on the use of scenarios as an organizing principal for both the main text and stress tests.

• The scenarios should be motivated with crisis story lines that co-mingle triggering events for example, a global shock on agricultural product prices, draught and shock on energy prices.

• The risk transmission channels should also be indicated; for example via the export sector, capital account, and the exchange rate. 8

Organization of work for successful financial stability analysis

• Successful financial stability work in the COMESA region

requires: Separate units with fully dedicated staff strengthens financial stability

analysis. A voids in fighting among various departments and unwillingness to share

information. Encourages inter-departmental cooperation.

• Global practice varies, however the most popular approach is to have a separate department and the second most popular is to locate it within an economic research wing.

9

Organization of work for successful financial stability analysis

• The position and independence of financial stability units should be strengthened in all the COMESA countries.

• This requires more resources devoted to financial stability work and more attention from the central banks’ management.

• In all the COMESA countries financial stability units still need to earn their reputation, establish credibility and strengthen their position. 10

Organization of work for successful financial

stability analysis

• Financial stability units in the COMESA region need clear guidance on

their tasks and responsibilities. • The functions of a financial stability unit should be defined to include:

On-going monitoring of financial stability of financial institutions and markets. Regular reporting on financial stability through payment systems reports, Macroprudential analysis that develops regulatory policies to contain systemic risk.

• The department should participate in research and conferences as well as on-going contact with academia.

• The unit should coordinate with other national agencies such as the Ministry of Finance,

• Financial stability departments should be involved in international engagement with institutions such as BIS and IMF.

11

Recommended framework for financial stability analysis the COMESA Area

• Financial stability analysis and assessment comprises a three pillar structure:

Early identification of potential risks and vulnerabilities; as well as channels of transmission.

The promotion of preventive and timely remedial policies (macroprudential policy measures) to avoid financial instability;

Crisis management and resolution tools when preventive and remedial measures fail.

12

Recommended framework for financial stability analysis the COMESA Area

• Should include:– overall analysis and surveillance of the financial system, – as well as the maintenance of a stable operational environment for

banks and other financial institutions, central bank – identification of systemic risk factors, – strengthening of market discipline. Ensuring the use of prudential

regulation and public disclosure of information about risks to influence behavior.

– In this respect, financial stability analysis differs from day-to-day supervisory work, which aims only at identifying risks to individual institutions.

13

Risk identification process and possible scenarios for stress testing

• Identification of risks is the starting point for financial stability analysis.

• Risks can be classified according to their source: internal risks, external risks and contagion risks. – Internal risks arise due to imbalances within the financial system.– External risks arise from the macro economy; and are usually

evaluated using various micro and macro stress-testing models. – Contagion risks require analysis of cross sector and cross-border

exposures and models which utilize that data.• These risks could be ranked according to their probability of

occurrence and impact using the matrix approach.

15

Table 1: The process of Risk Identification

16

Step 1 Step 2 Step 3

Detect weak spots in the system

Understand how problems might develop

Assess the seriousness of risks

17

Table 2 The Matrix of Relevance

High probability

Low probability

High impact Main Focus Watch

Low impact Summary Mention

Ignore

18

Table 3: Stylised Risk Matrix For a Banking system

IMPACT

Probability of Risk

LOW HIGH

Low Interest rate risk Equity risk

(market risk)

Contagion risk from foreign counterparties

Concentration risk

Highs Foreign exchange risk

Credit risk Liquidity risk

Table 4: Possible risk scenarios for banking systems in COMESA member states

Shock Trigger EventTransmission

Channel(S) Realisation of Risk Impact

External Shock

• Drop in exports • Rise in global

commodity prices

• Local currency depreciates

• Inflationary pressures

• Direct credit risk: increase in NPLs

• Net open position gains/losses

• Capital adequacy• Contagion effect

on interbank market

Internal Shock

• Drop in real estate prices

• Inflationary pressures

• Reduced activity in construction sector

• Rise in interest rates

• Direct credit risk: increase in NPLs

• Capital adequacy• Contagion effect

on interbank market

Liquidity Shock • Capital outflows• Regional

liquidity crisis

• Fire-sale of liquid assets, thus liquidity shortage

• LOLR intervention

• Local currency depreciates

• Losses on net open position

• Capital adequacy• Interbank

market

19

• An external shock: • may present as a rise in annual headline inflation, triggered

by high food prices and high transport costs as a result of rising oil prices,

• may prompt the central bank to tighten monetary policy, thus leading to a rise in interest rates.

• Furthermore, deterioration in the balance of payments leading to exchange rate depreciation may exacerbate inflationary pressures as prices of imported commodities rise.

• For enterprises with a considerable amount of foreign currency debt, the depreciation may increase their loan repayment burden.

20

21

An internal shock: • Could result from the growth in loans that leads to the increase in banks’

exposure to large borrowers, most of whom access credit from multiple banks. • The banking sector could be faced with concentration risk from large

borrowers.• A rise in bank lending rates reflecting the monetary policy actions to

curb inflation could result an increase in the debt service-to-income ratio (DIR) for households and enterprises affecting their ability to service existing debt.

• Enterprises which have borrowed in foreign currency may face higher debt servicing costs due to exchange rate depreciation.

• Risks may also arise from the rise in loan exposure of banks to property developers and estate agents. Adverse economic shocks and rising construction costs may diminish property developer’s profitability, the rising cost of borrowing may affect the demand for property, thus affecting loan repayment rates.

Good practices in financial stability reports

• In terms of frequency, most are either annual or semiannual. • The average length has declined marginally, structure – some countries

have beefed up contents, provide more underlying data, some have started to be more forward looking.

• The coverage of issues has increased reflecting increased capacity by central banks to analyze relevant data.

• The reports have also expanded beyond the banking sector to the: – nonbank financial institutions, – the counterparties (households, non – financial firms), – payments and securities settlement systems, – the regulatory framework.

22

Good practices in financial stability reports

• There has been an increased use of more sophisticated market based indicators in developed country reports.

• The share of Financial Stability Reports using stress testing has grown. – More Financial Stability Reports now present results of their early warning systems, – The calculations are increasingly based on disaggregated data – Attempts are being made to integrate Financial Stability Reports with other policy

areas managed by the central banks such as monetary policy studies.

• FSRs now include discussions of the regulatory framework or self assessments of compliance with regulatory standards.

• Central banks in the region should benchmark their Reports to best practice.

• They should focus on three key characteristics (the CCC framework): – clarity, – consistency, – coverage

23

Areas of Improvement for COMESA Countries in Their Financial Stability Report Production

• Countries focus on the description of past developments and are not sufficiently forward looking.

• The objectives of the Financial Stability Reports should be clarified. • The coverage of key systemic risks should be improved. • It is important to include an analytical not a descriptive coverage of

financial market conditions in the discussion of systemic risks. • The quantitative content of the Reports should be improved. This can

be done by ensuring that FSRs report forward looking stress testing results on a regular basis.

• More discussion of macroprudential policies is required. • FSRs should point out existing data gaps. • The region could benefit from the standardization of Financial Stability

Reports publication.

24

Structure of a forward looking Financial Stability Report for COMESA Countries

• Financial Stability Reports should discuss:– the risks, – transmission channels, – Impact ,– measures available to mitigate the risks.

25

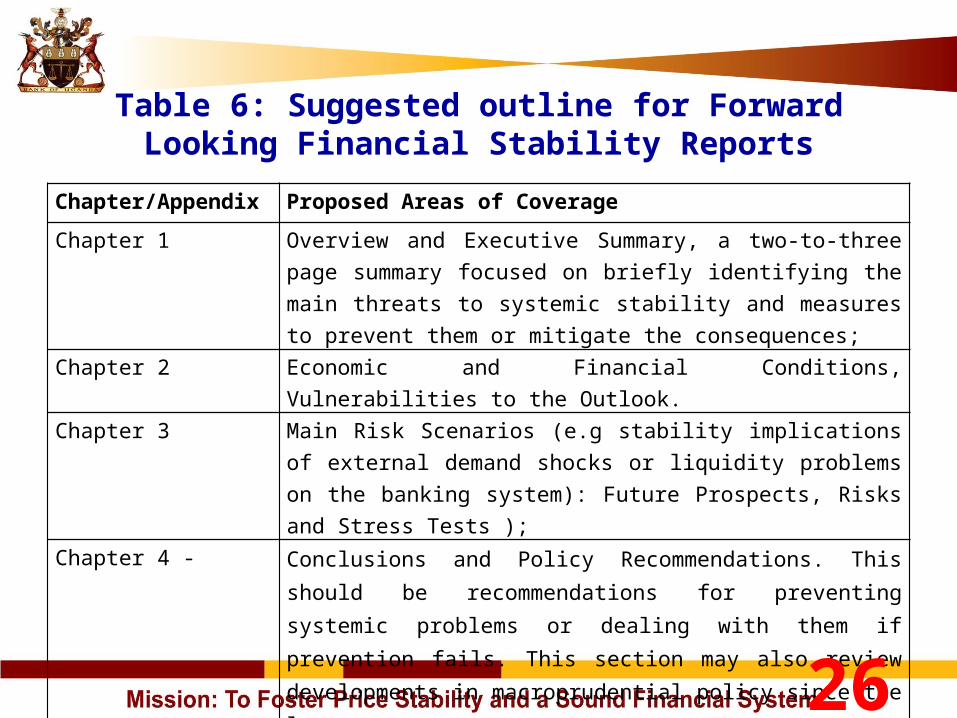

Table 6: Suggested outline for Forward Looking Financial Stability Reports

Chapter/Appendix Proposed Areas of Coverage

Chapter 1 Overview and Executive Summary, a two-to-three page summary focused on briefly identifying the main threats to systemic stability and measures to prevent them or mitigate the consequences;

Chapter 2 Economic and Financial Conditions, Vulnerabilities to the Outlook.

Chapter 3 Main Risk Scenarios (e.g stability implications of external demand shocks or liquidity problems on the banking system): Future Prospects, Risks and Stress Tests );

Chapter 4 - Conclusions and Policy Recommendations. This should be recommendations for preventing systemic problems or dealing with them if prevention fails. This section may also review developments in macroprudential policy since the last report.

Appendix I: Special Topic

This should delve more deeply but concisely into important existing vulnerabilities and sources of risks or policy challenges

Appendix II: Statistical Tables

Financial Soundness Indicators and Consolidated Balance Sheet of the Banking Sector

26

Future work and recommendations

• Improvement of Financial Stability Report writing by enhancing their clarity, coverage of key risks, and consistency overtime

• Make stress testing exercises regular activity and include them in a general macroprudential framework.

• Central banks in the region need to enhance cooperation of all parties involved in the financial stability work.

27

References

Bardsen, Lindquist and Tsomocos (2006), ‘Evaluation of macroeconomic models for financial stability analysis’, Working Paper 2006/01, Norges Bank.

Bowen A. (2007): The Financial Stability Report of the Central Bank of Iceland: a review. Financial Stability 2007, p.p. 83-97.

Bunn, Cunningham and Drehmann (2005), ‘Stress testing as a tool for assessing systemic risks’, Financial Stability Review, Bank of England

Čihák, M., 2006, “How Do Central Banks Write on Financial Stability?", IMF Working Paper No. 06/163 (Washington: International Monetary Fund).

28

References

Cihak, M (2007), ‘Introduction to applied Stress Testing’, IMF Working Paper No. WP/07/59, International Monetary Fund, Washington DC

Čihák, M., Sharifuddin, S.M.S., Tintchev, K.,2012, Financial Stability Reports: What Are They Good For? IMF Working Paper, WP/12/1

Fracasso, F., Genberg, H. and C. Wyplosz, 2003, "How do Central Banks Write? An Evaluation of Inflation Reports by Inflation Targeting Central Banks", Geneva Reports on the World Economy, Special Report 2.

Gai, P. and H.S. Shin (2003): ‘Transparency and financial stability’, Financial Stability Review, No. 10, Bank of England, London, December, pp. 91-98.

29

![Augustine: City of God [1] St. Augustine (354-430 A.D.)](https://static.fdocuments.in/doc/165x107/56649d385503460f94a1120f/augustine-city-of-god-1-st-augustine-354-430-ad.jpg)