Bank of Cyprus Group (BoC) Relations/Presentations... · with further planned strategic actions to...

48

Bank of Cyprus Group (BoC) Non-Deal Roadshow December 2014

Transcript of Bank of Cyprus Group (BoC) Relations/Presentations... · with further planned strategic actions to...

Bank of Cyprus Group (BoC)

Non-Deal Roadshow

December 2014

Presenters

2

John Hourican

Chief Executive Officer

Euan Hamilton

Director of Restructuring and

Recoveries Division

Constantinos Pittalis

Investor Relations Manager

Dr. Chris Patsalides

Finance Director

Michalis Athanasiou

Group Chief Risk Officer

Eliza Livadiotou

Group Chief Financial Officer

3

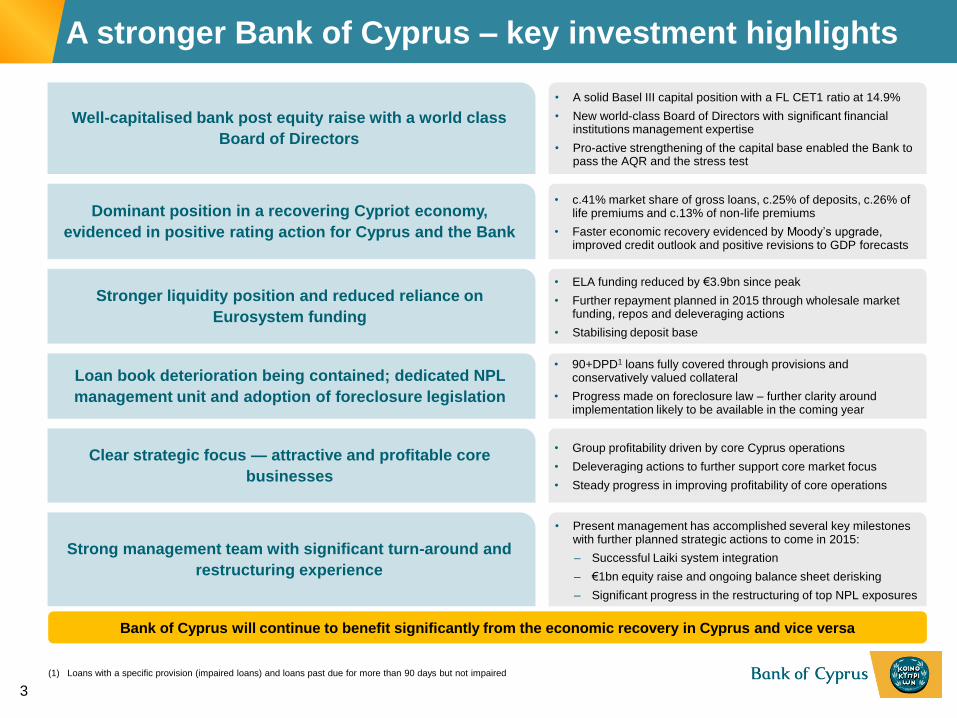

Well-capitalised bank post equity raise with a world class

Board of Directors

• A solid Basel III capital position with a FL CET1 ratio at 14.9%

• New world-class Board of Directors with significant financial institutions management expertise

• Pro-active strengthening of the capital base enabled the Bank to pass the AQR and the stress test

(1) Loans with a specific provision (impaired loans) and loans past due for more than 90 days but not impaired

Dominant position in a recovering Cypriot economy,

evidenced in positive rating action for Cyprus and the Bank

• c.41% market share of gross loans, c.25% of deposits, c.26% of life premiums and c.13% of non-life premiums

• Faster economic recovery evidenced by Moody’s upgrade, improved credit outlook and positive revisions to GDP forecasts

Stronger liquidity position and reduced reliance on

Eurosystem funding

• ELA funding reduced by €3.9bn since peak

• Further repayment planned in 2015 through wholesale market funding, repos and deleveraging actions

• Stabilising deposit base

Loan book deterioration being contained; dedicated NPL

management unit and adoption of foreclosure legislation

• 90+DPD1 loans fully covered through provisions and conservatively valued collateral

• Progress made on foreclosure law – further clarity around implementation likely to be available in the coming year

Clear strategic focus — attractive and profitable core

businesses

• Group profitability driven by core Cyprus operations

• Deleveraging actions to further support core market focus

• Steady progress in improving profitability of core operations

Strong management team with significant turn-around and

restructuring experience

• Present management has accomplished several key milestones with further planned strategic actions to come in 2015:

– Successful Laiki system integration

– €1bn equity raise and ongoing balance sheet derisking

– Significant progress in the restructuring of top NPL exposures

Bank of Cyprus will continue to benefit significantly from the economic recovery in Cyprus and vice versa

A stronger Bank of Cyprus – key investment highlights

48%

31%

5% 10%

6% Customer deposits

ELA

ECB

Total equity

Other liabilities

Euro system

funding

36%

Period of growth

4

(1) As of December 2012

(2) As of June 2014

(3) As of September 2014

(4) Moody’s upgrade of BoC’s long-term deposits to Caa3 as of 17 Nov 2014

2009 - 2013 Pre-2009 2013 2014

Following a traumatic 2013, significant steps were taken in 2014 to

stabilise the Bank

Cyprus bailout by IMF/EC

Resolution & shares suspension

Sale of Greek operations

Sh

are

ho

ldin

g

evo

luti

on

Equity raise

New Board

Rating upgrade4 Depositor bail-in

Laiki acquisition

New CEO

Greek

sovereign

crisis

recession

& property

crisis

81%

18%

1% Bailed-in depositors

Legacy Laiki Bank

Shareholders & debt security holders as at March 2013

72%

5%

10%

13%

Retail investors

Cypriot / Greek institutionals

Foreign institutionals

Others

47%

10%

43%

Bailed-in depositors

Legacy Laiki Bank

New shareholders

Pre bail-in1 Pre-capital increase2 Post-capital increase3

Fu

nd

ing

evo

luti

on

49%

28%

3% 14%

6% Customer deposits

ELA

ECB

Total equity

Other liabilities

92%

1% 7%

Customer deposits

Total equity

Other liabilities

Euro system

funding

31%

Relisting

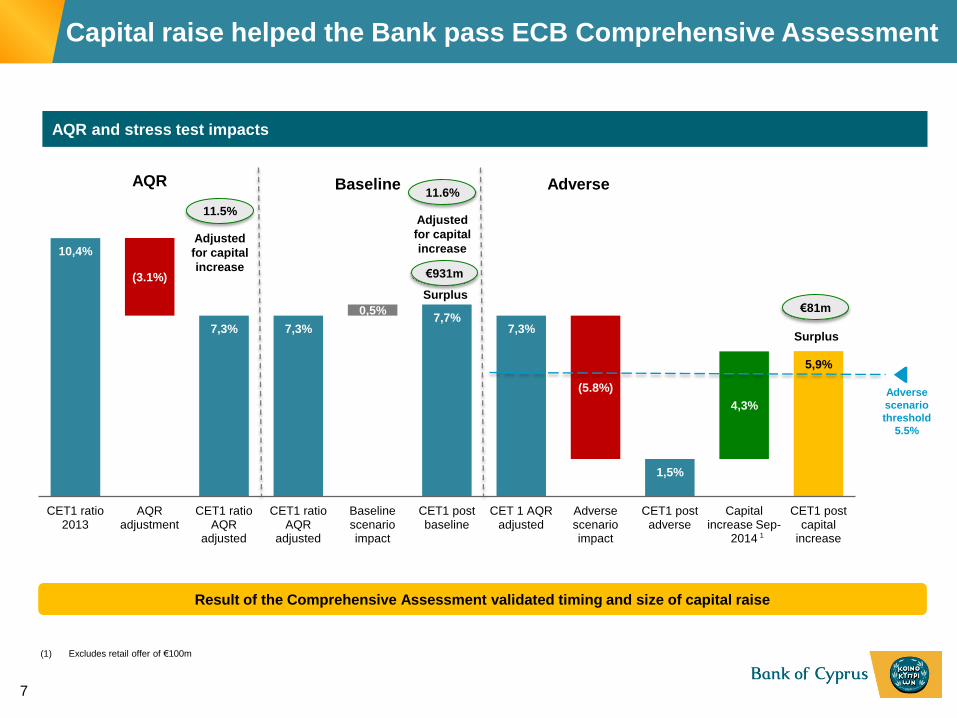

11,3%

15,4% 14,9%

4.3%

(0.2%) (0.5%)

Jun-14 CET1 ratio (transitional

basis)

Capital increase Q3'14 movement Sep-14 CET1 ratio (transitional basis)

Fully loaded impact Sep-14 CET1 ratio (fully loaded)

Capital

increase of

€1bn

€1.6bn buffer

vs 8%

(1) Fully Loaded – main capital deduction from CRD IV transitional to fully loaded is in relation to Deferred Tax Assets (DTAs)

Capital raise increased CET1 position to around 15%

1

5

14.9%

14.9%

12.7%12.4%

12.0% 11.8% 11.7% 11.5% 11.4% 11.3% 11.2%

10.4% 10.4% 10.2%9.9%

BoC Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Peer 10 Peer 11 Peer 12 Peer 13 Peer 14

A solid Basel III capital position leading to successfully clearing the AQR and the stress test

Source: Company financials

(1) Banks include Alpha Bank, National Bank of Greece, Creval, BPS, Piraeus Bank, BPM, BPER, Sabadell, Popular, Carige, Liberbank, BCP, Eurobank and Hellenic bank

BoC now appropriately capitalised relative to peers

6

Basel III fully loaded CET1 ratio of Southern European banks (9M 2014)1

10,4%

7,3% 7,3% 7,7%

7,3%

1,5%

5,9%

(3.1%)

0,5%

(5.8%)

4,3%

CET1 ratio 2013

AQR adjustment

CET1 ratio AQR

adjusted

CET1 ratio AQR

adjusted

Baseline scenario impact

CET1 post baseline

CET 1 AQR adjusted

Adverse scenario impact

CET1 post adverse

Capital increase Sep-

2014

CET1 post capital

increase

Baseline Adverse AQR

Adverse

scenario

threshold

5.5%

Capital raise helped the Bank pass ECB Comprehensive Assessment

11.5%

Adjusted

for capital

increase

11.6%

Adjusted

for capital

increase

Surplus

€81m

Result of the Comprehensive Assessment validated timing and size of capital raise

7

AQR and stress test impacts

Surplus

€931m

1

(1) Excludes retail offer of €100m

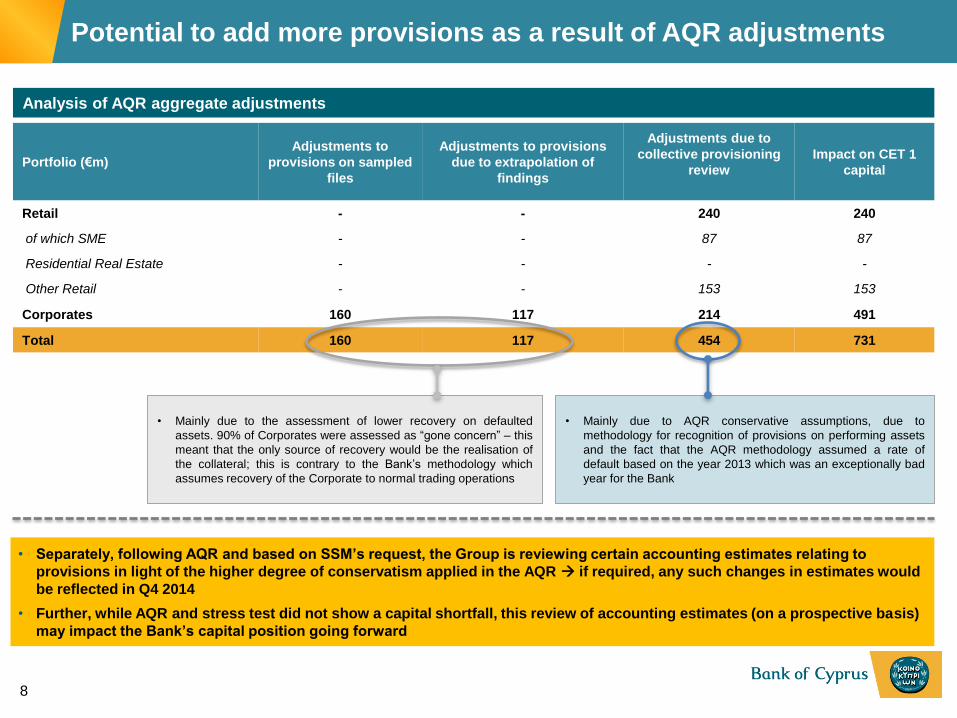

• Separately, following AQR and based on SSM’s request, the Group is reviewing certain accounting estimates relating to

provisions in light of the higher degree of conservatism applied in the AQR if required, any such changes in estimates would

be reflected in Q4 2014

• Further, while AQR and stress test did not show a capital shortfall, this review of accounting estimates (on a prospective basis)

may impact the Bank’s capital position going forward

Potential to add more provisions as a result of AQR adjustments

Portfolio (€m)

Adjustments to

provisions on sampled

files

Adjustments to provisions

due to extrapolation of

findings

Adjustments due to

collective provisioning

review

Impact on CET 1

capital

Retail - - 240 240

of which SME - - 87 87

Residential Real Estate - - - -

Other Retail - - 153 153

Corporates 160 117 214 491

Total 160 117 454 731

Analysis of AQR aggregate adjustments

• Mainly due to the assessment of lower recovery on defaulted

assets. 90% of Corporates were assessed as “gone concern” – this

meant that the only source of recovery would be the realisation of

the collateral; this is contrary to the Bank’s methodology which

assumes recovery of the Corporate to normal trading operations

• Mainly due to AQR conservative assumptions, due to

methodology for recognition of provisions on performing assets

and the fact that the AQR methodology assumed a rate of

default based on the year 2013 which was an exceptionally bad

year for the Bank

8

47%

18%

10%

5%

5%

15%

Bailed-in depositors WL Ross and WL Ross introduced investors

Legacy Laiki Bank Renova Group

EBRD Other new shareholders

9

Current shareholding of BoC (9M’14)

Post-capital increase

Revised Board composition

Name Designation

Dr. Josef Ackermann Chairman

Independent

Mr. Wilbur Ross Vice Chairman

Independent

Mr. Vladimir Strzhalkovskiy Vice Chairman

Independent

Mr. John Patrick Hourican CEO

Dr. Christodoulos Patsalides Finance Director

Mr. Arne Berggren Represents EBRD

Independent

Mr. Maxim Goldman Represents Renova

Mr. Marios Kalochoritis Independent

Mr. Michalis Spanos Senior Independent

Mr. Ioannis Zographakis Independent

Newly elected directors

• AGM of BoC was held on 20 Nov 2014

• 6 directors were newly appointed to the board

• 4 directors were re-elected

Equity raise has attracted high quality professional investors and a world class Board of Directors

• Significant investor interest in all aspects of the Bank of Cyprus

story, including equity, but also potential future corporate actions

• Targeted marketing effort led to 100+ investor meetings and 27 new

high quality investors being added to the shareholder base

10

2014 2015

16

Dec

Cyprus and

Athens

relisting

Retail offer

begins

15

Dec

Listing on a

major

European

exchange

Medium

-term

18

Sep

Close of

€1bn share

capital

increase

20

Nov

AGM and

new Board

election

27

Nov

Q3 results

published

Non-deal

roadshow

Investors have the opportunity to gain or increase exposure in BoC stock following the re-listing - an element of

liquidity is likely to be available from certain bailed in depositors (who have been locked in since the shares were

suspended in Cyprus and Athens)

Scope for investor participation in Bank of Cyprus equity post re-listing

Retail offer

closes

9

Jan

Medium-

term

11

(1,6%)

(2,5%) (2,0%)

(3,7%)

(5,3%)

(6,1%) (5,2%) (5,1%)

(4,0%)

(3,7%)

(4,9%)

(6,2%) (7,4%)

(8,7%)

(7,1%)

(5,5%)

(3,9%)

(2,5%) (2,8%)

0,4% 1,6%

2,0% 2,2% 2,1%

Q1'12 Q2'12 Q3'12 Q4'12 Q1' 13 Q2 '13 Q3 '13 Q4 '13 Q1 '14 Q2 '14 2014E 2015E 2016E 2017E 2018E 2019E

Actual Troika original forecast Forecast

GDP growth expected to be positive from 2015E – significant improvement relative to original Troika expectations

Source: EC, EIU, CBC, Troika, company reports, Cyprus Centre of Economic Research and University of Cyprus

Economic sentiment — values seasonally adjusted

Significant uptick in sentiment – has entered into positive territory in Q3’14 after bottoming in Q3’13

Q1'03 Q1'04 Q1'05 Q1'06 Q1'07 Q1'08 Q1'09 Q1'10 Q1'10 Q1'12 Q1'13 Q1'14

ESI-Cyprus index

Similar to 2008 levels

Improving macro indicators supportive of Cyprus’s economic recovery

Nov-14

Zero level (100)

33,3%

31,4%

30,0%

29,6%

26,0%

23,0%

21,0%

12,5%

12,5%

Business hub given strategic location at the crossroads of Europe, Asia, Middle East and Africa

Small, flexible economy; real unit labour costs dropped by 11% during 2012-2014 boosting competitiveness

Growth prospects in tourism, education & R&D, health & medical, professional and financial services

Budget deficit contracted faster than anticipated- expected to meet the Maastricht criteria in 2014

Potential for energy / hydrocarbon industry (potential c.5Tcf on Aphrodite site)

1

2

3

4

Upside potential for macro recovery

Recovery supported by a resilient tourism sector…

1,5 1,5

1,7

1,9

2,1

2009 2010 2011 2012 2013

Tourism revenues (€bn)

2014 corporate tax rates

Double taxation avoidance treaties

with c. 50 countries

20,7%

40,4%

38,9%

Upper secondary

Less than

Upper Secondary

Tertiary

Education for persons 20-64 (2013)

Cyprus has the highest number

of university graduates per capita

in Europe

…and significant additional growth levers

…an enabling business environment…

Drivers of

macro-

economic

recovery

12 Source: EC, EIU, CBC, Troika, and company reports

1

2

3

CAGR:

9%

5

13

Ratings uplift for Cyprus and the Bank

0

2

4

6

8

10

12

14

Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14

Cyprus Portgual Italy Spain Greece Ireland BoC

Baa1

Baa3 Ba2

B1

B3 Caa2

Ca

Source: Bloomberg, Moody’s, S&P, Fitch, DBRS

0

200

400

600

800

1.000

Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14

CDS spreads significantly narrowed vs. periphery peers

Baa1

Baa2

Ba1

B3 Caa1

Caa3

Baa2

Investor confidence returning as CDS trades inside Greece since February 2014…

…also reflected in ratings, with gap narrowing for Bank of Cyprus

Positive outlook evidenced in credit confidence and ratings

Agency Rating Last

action Outlook

Moody's B3 Upgrade Stable

S&P B+ Upgrade Stable

Fitch B- Affirmed Positive

DBRS B (low) Upgrade Stable

Cyprus sovereign ratings

Moodys ratings

20

30

40

50

60

70

80

Nov-05 Nov-06 Nov-07 Nov-08 Nov-09 Nov-10 Nov-11 Nov-12 Nov-13

Loans Deposits

A smaller, stronger and more stable banking system

14

Recent developments in the Cypriot banking system

Monthly change in banking system deposits (€bn)

• Monthly change in banking system deposits

remain at a manageable level since lifting of

domestic capital restrictions - but significant

system wide funding gap from the bail-in

remains; part of reduction of deposits utilised

to repay loans

• The bulk of the Cyprus banking system is now

under direct supervision of the SSM

• 4 banks participated in the ECB assessment

(BoC, CCB, Hellenic and RCB) – only Hellenic

failed the assessment but then confirmed plans

to raise capital

Source: Central Bank of Cyprus, IMF, ECB and company reports

Loans and deposits (€bn)

Oct-14

0,2

(1,7)

(1,0)

(3,8)

(6,3)

(1,4)

(5,3)

(1,0) (1,4)

(0,8) (0,2) (0,1) (0,2) (0,1)

(0,5) (0,2)

0,2 0,5

(0,4)

0,0

(0,2) (0,4) (0,2)

Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Oct-14

25.8 21.9

13.3

4,4 5,2 1,2 0,8

91

81

15

Gross loans

€bn

Branch network

# branches

Deposits

€bn

26% Insurance

premiums1

€m

Source: CBC, IMF, company disclosure (Bank of Cyprus and competitors) as of 9M 2014

(1) FY2013

(2) 49.9% owned by the Bank

Life

13%

56

54

Non-life

2 2

24.6

11.2 13.4 6,1 2,3 2,8 1,1

203

130

349

68 29 7

14

(Pre-bail in) 9M2014

BoC

Laiki

Laiki

Laiki

(Pre-bail in)

(Pre-bail in)

BoC

BoC

9M2014

9M2014

37%

39%

41%

25%

Dominant position in the Cypriot banking & insurance market

xx% Market share as of Sep 2014

16

BoC: steady balance sheet reduction Q-o-Q

30,3

33,0

30,3

29,4 28,6

27,5

Dec-12 Jun-13 Dec-13 Mar-14 Jun-14 Sep-14

+9%

-3% -8%

-4% -3%

-17% (30 Jun 2013 to 30 Sep 2014)

Combined impact of 2014 transactions on Group: increase in CET1 ratio of 0.8% and

improvement in Group liquidity of about €1.8bn

Continued momentum to execute

specific deleveraging / de-risking

H1 2013 (Resolution)

H2 2013 Q1 2014 Q2 2014 Pending actions

Greek ops (Piraeus)

Romanian assets

(Marfin)

Kyprou AM

(Alpha Trust)

Banca Transilvania

(stake sell down)

Ukrainian operations

(Alfa)

Serbian exposure

(Piraeus)

Govt. bond repayment

“Fix or sell” strategy

• Romania (remaining

exp.)

• Uniastrum

• Cyprus / Greece RE

As

se

t (B

uye

r)

Q3 & Q4 2014

UK loan book

Marriot related assets

in Romania

€bn

Shrink to core strength: significant deleveraging progress

(Pre-bail in)

11,4

9,9 9,6 9,5 8,8

7,7 7,5

1,3 1,4 1,4

1,4

0,9 0,9

11,4 11,2 11,0 10,9

10,2

8,6

Apr-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Nov-14

8.4

ELA ECB funding

(€ bn)

~ €1bn capital market transactions

~ €0.5bn repos & deleveraging

Further actions planned for

2015

37%

Eurosystem funding reliance reducing fast

36% 36% 36% 31% Eurosystem Funding as xx% of

balance sheet

Continuous reduction of ELA and ECB funding with further potential going forward

17

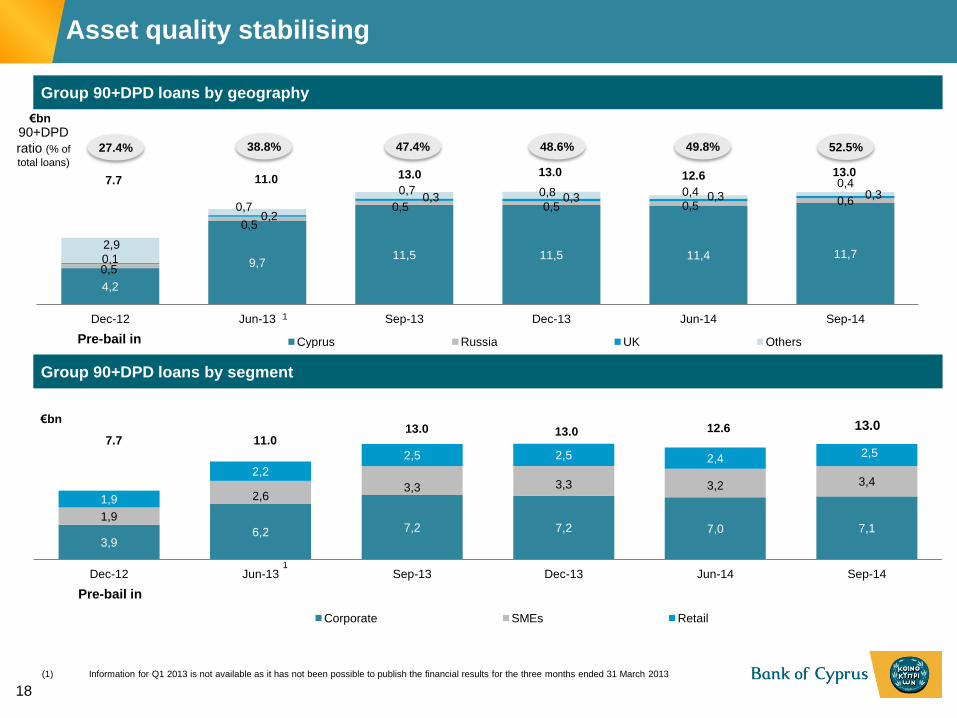

3,9 6,2 7,2 7,2 7,0 7,1

1,9

2,6 3,3 3,3 3,2 3,4

1,9

2,2

2,5 2,5 2,4 2,5

Dec-12 Jun-13 Sep-13 Dec-13 Jun-14 Sep-14

Corporate SMEs Retail

1

13.0

4,2

9,7 11,5 11,5 11,4 11,7

0,5

0,5

0,5 0,5 0,5 0,6

0,1

0,2

0,3 0,3 0,3 0,3

2,9

0,7

0,7 0,8 0,4 0,4

Dec-12 Jun-13 Sep-13 Dec-13 Jun-14 Sep-14

Cyprus Russia UK Others

1

27.4% 38.8% 47.4% 48.6% 49.8%

(1) Information for Q1 2013 is not available as it has not been possible to publish the financial results for the three months ended 31 March 2013

€bn

11.0 13.0 13.0 12.6 7.7

€bn

11.0 13.0 13.0 12.6

7.7

Pre-bail in

Pre-bail in

Group 90+DPD loans by geography

Group 90+DPD loans by segment

90+DPD

ratio (% of

total loans)

52.5%

13.0

18

Asset quality stabilising

19

3,2 1,8 3,8 1,6

11,5

21,9

22,7% 30,5% 16,2%

29,0%

81,9% 53,7%

Loan Loss

Reserve (LLR)

coverage

Tangible

coverage

Total

coverage

90+DPD loans

by segment1

Corporate SMEs Housing Consumer RRD Cyprus

46,0% 29,3% 18,4% 48,6% 36,8% 36,5%

66,0% 81,6% 84,1% 45,7% 76,6% 75,4%

112,0% 110,9% 102,5% 94,3% 113,4% 111,9%

Gross loans

(€bn)

xx % of total gross loans (Cyprus only)

52.3% 7.3% 17.5% 8.1% 14.8%

Significant provision and collateral coverage, with additional comfort from personal guarantees

100.0%

Credit Risk – 90+ DPD fully covered by provisions & tangible collateral

(1) Shown as a % of segmental loans

9M2014

Dedicated NPL unit is fully operational and showing early successes

20

(1) Currently using the services of external property consultants

(2) No retail client ownership within RRD

Restructuring & Recoveries Division (RRD): structure

Strategy

and

analytics

Real estate

manage-

ment1

Corporate

Financial

solutions

Retail2 and

SME

Debt

recovery

services

Restructuring

& Recoveries Division

Dedicated unit housing €11.5bn of exposures supported by c.490 employees, reporting directly to the CEO in

order to manage arrears in an independent and centralised way as required by the Arrears Management Directive

CEO

2 A single unit to manage the customer from early

delinquency until foreclosure

3

Dedicated channels for addressing delinquent

customers per segment (e.g., Retail2, SME and

Corporate)

4

Build internal capabilities in a centralised manner to

effectively and efficiently address arrears (e.g.,

analytics, systems)

1

An independent and centralised unit that is

responsible for and specialises in the management

and monitoring of customers in arrears

€

91 166 222

€5.7 bn €1.6 bn €4.3 bn

22%

41%

26%

6% 5%

Restructuring agreed and implemented

Detailed non binding heads of terms for restructuring agreed

Diligence ongoing

Receiver/manager appointed

Other recovery cases

21

Achievements over the last 6 months (April to September)

Summary of restructuring efforts for

top 30 exposures

€5.0bn

Good progress in restructuring efforts

€330m

Sold the Group’s largest single name NPL exposure

• Loans extended to a Serbian real estate management company sold

to Piraeus Bank for approximately €165m and realised an accounting

gain of €27m

€1.2bn

Restructured loans

• Addressed the restructuring backlog: de-bottlenecking of restructuring

processes

• Designing a workflow process for managing arrears in the retail book

following the restoration of limited underwriting authority within Retail

Arrears Management, following positive discussions with the Central

Bank of Cyprus

• Delivered specialised trainings to upskill employees

€1.1bn Removed from 90+DPD

• Initiated a transformational project to implement best practices and

driving cultural change in managing arrears following a Central Bank

of Cyprus driven audit

15

Appointed Receivers/Managers for the recovery of debt in 2014

• Recently appointed a receiver in a c. €200m Bank exposure – the

island’s largest receivership

• Untested process

• Courts are not adequately

resourced

• Managing reputational

implications

• Delay in the enactment of

related accompanying

regulations

Summary

• Establishes clear procedures for timing of repossession, valuation and

auction, aiming to reduce repossession timetable from 10+ years to as

little as 18 months

• Passing of the Bill was a key requirement for further disbursement of

funds from the Troika

• Insolvency framework (designed to protect vulnerable parties from

foreclosure) is still being discussed at Government and supranational

levels

Passing of Foreclosure law a key step in the recovery process

22

• Bill passed by the House of Representatives on 6 September

• Supreme Court ruled on 31 October, four of the six bills that limited the

effect of the foreclosure bill on low-income groups as unconstitutional

• An internal working group established to design and coordinate the

Bank's processes and procedures in implementing the newly set

provisions of the Law

Recent Developments

Key challenges & issues

23

Phase 1: Restructuring

Phase 2: Today

Phase 3: Delivering

returns

Medium-term objective

(1) Data as of 30 September 2014

Core bank

• Gross loans: 10.41

• Deposits: 10.91

Restructuring & Recoveries

Division • Gross loans: 11.51

• Deposits: 0.31

Overseas & Disposal Group

• Gross loans: 3.01

• Deposits: 2.11

• Comprised of Banking

(Consumer, SME, Corporate,

International), Insurance, AM,

Wealth and Brokerage

• Self funded but largely

encumbered to fund the non-

core balance sheet

• Already generating attractive

returns

• Manages all exposures above

€100m and problem loans

• Decent cash flow generation

• Key remaining transactions

include Romania, Russia, UK

and select Cypriot / Greek

exposures

• Break-even or negative

returns

• Consumes capital and parent

funding

• Engine of growth for Cyprus

• Maintain strong profitability

• Actively manage and collect

• Accelerate run-off where

possible

• Exit as appropriate to repatriate

capital and funding

€bn

Clear strategic segregation leading to a strong Core Bank

42%

46%

12%

Cyprus Core

RRD

Overseas and Disposal Group

Cyprus Core forms 42% of Group loans…

52%

17%

23%

8%

Cyprus Core

… as well as a key driver of profitability (9M’14)

Profit after tax and before one-offs for Cyprus operations of €171m for 9M’14, compared to Group total of €84m

704 826

-280 -373

171

790 941

-367 -492

84

Net interest income Total income Total expenses Provisions Profit after tax & before one-offs

Cyprus (Core + RRD)

Group

89% 88% 76% 76% 204% %

% contribution of

Cyprus operations

Group balance sheet and P&L primarily driven by Cyprus core

Consumer

September 2014: €13.3bn

SME

Corporate

IBS & Others

Time

Current

Savings

€10.4bn

By type

… and 82% of Group deposits

By type

€10.9bn

September 2014: €24.7bn

L/D: Cyprus core — 88% vs. Group — 148%

24

€m

82%

2%

16%

Cyprus Core

RRD

Overseas and Disposal Group

63%

31%

6%

Cyprus Core

Category

Key

performance

indicators

Group

2013

Group

9M’ 14

Cyprus

9M’ 14

Medium-

term

target

(2017)

Asset

quality

90+ DPD

coverage 38% 38% 37% 40%-50%

Provisioning

charge 3.7% 2.6% 2.2% <1.0%

Funding

Eurosystem

funding % total

balance sheet

36% 31% n.a. <25%

Capital

Basel 3

transitional

CET1

10.4% 15.4% n.a. >12%

Margins

and

efficiency

Net interest

margin 3.5% 4.0% 3.9% ~3.25%

Fee and

commission

income/ total

income

14.3% 13.9% 14.2% Increase

Cost to income

ratio 47% 39% 34% 40%-45%

Significant progress made on Group KPIs, with a clear plan of action to

achieve medium-term targets

Key Pillars & Plan of action

• Continue re-structuring capitalising on the foreclosure law

• Seek FDI to enhance business viability • Re-cycle re-structured loans into the lending

business for continued support and service

1. Reverse

trend on

overdue

loans

• Boost deposits by leveraging on stronger capital position

• Access DCM on the back of improved ratings, stronger financial soundness and better prospects

• Proceeds from exiting non-core overseas activities

2. Normalise

funding;

Eliminate

ELA

• Direct lending into promising sectors with a view to funding the recovery of the Cypriot economy

• Further diversify income stream by boosting fee income from new sources in international business and wealth

3. Focus on

core

markets

in Cyprus

• Set-out a digital vision and introduce appropriate technology to enhance product distribution channels

• Introduce technology and processes to reduce operating costs

• Introduce HR policies aimed at enhancing productivity

4. Achieve a

lean

operating

model

• Strengthen governance and risk- management to

deliver appropriate medium-term risk-adjusted returns • Listing of shares on a larger and more liquid

exchange

5. Deliver

returns

25

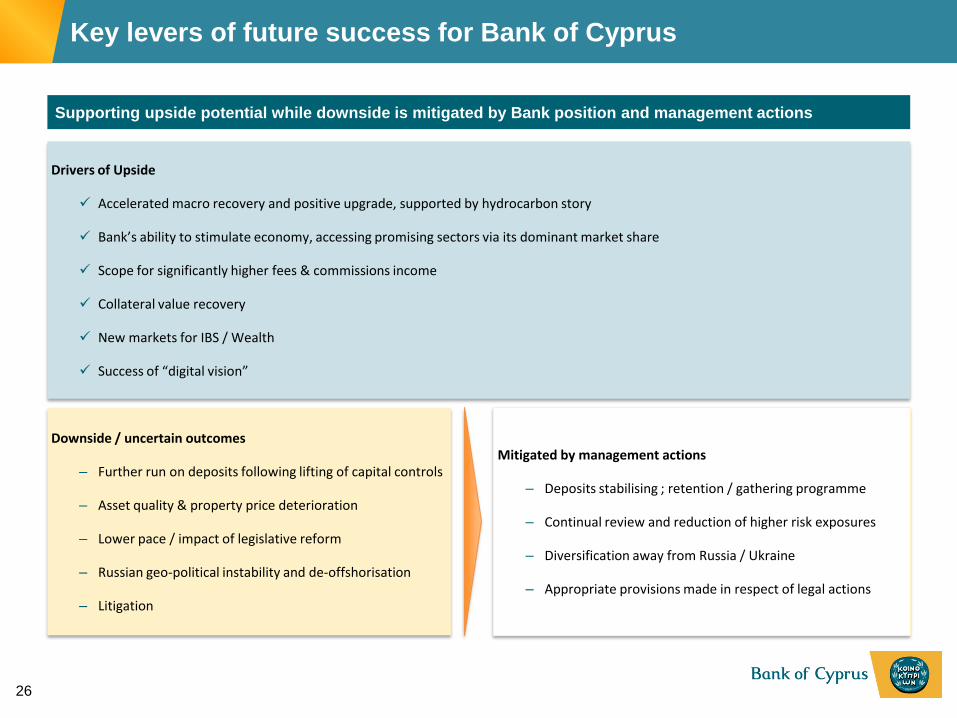

Key levers of future success for Bank of Cyprus

26

Supporting upside potential while downside is mitigated by Bank position and management actions

Drivers of Upside

Accelerated macro recovery and positive upgrade, supported by hydrocarbon story

Bank’s ability to stimulate economy, accessing promising sectors via its dominant market share

Scope for significantly higher fees & commissions income

Collateral value recovery

New markets for IBS / Wealth

Success of “digital vision”

Downside / uncertain outcomes

– Further run on deposits following lifting of capital controls

– Asset quality & property price deterioration

– Lower pace / impact of legislative reform

– Russian geo-political instability and de-offshorisation

– Litigation

Mitigated by management actions

– Deposits stabilising ; retention / gathering programme

– Continual review and reduction of higher risk exposures

– Diversification away from Russia / Ukraine

– Appropriate provisions made in respect of legal actions

Key takeaways

27

• Leading financial institution in an economy that is on the road to economic recovery, as evidenced

by the Moody’s upgrade

• MoU implementation on track with 5th Troika review mission being another positive one

• CET1 ratio improved to 15.4% (transitional basis, 14.9% CET1 B3 FL) driven the successful €1

bn share capital increase through a private placement with international institutional investors and

existing investors

• Deposit base showing signs of stabilisation, with 3Q2014 deposit outflows in Cyprus reduced to

just 3%; early release of all blocked decree deposits

• ELA reduced through deleveraging actions and capital proceeds

• RRD up and running with signs that measures are yielding results, despite the lack of the

appropriate legal infrastructure

• Loan quality challenges remain; 90+ DPD remain high; imperative that the Bank is given the tools

to engage effectively with borrowers

• Election of a new Board with members bringing a wealth of banking and broader corporate

experience

Appendices

Appendices

29

> Income statement 30 - 34

> Balance sheet 35 - 46

> Management team 47

Selected lines from Income Statement (€m) 9M2014 3Q2014 2Q2014 qoq

change % 1Q2014

Net interest income 790 244 279 -12% 267

Net fee and commission income 131 43 43 +1% 45

Insurance income net of insurance claims 35 10 12 -13% 13

Other (expenses)/income (15) (6) (24) -66% 15

Total income 941 291 310 -7% 340

Total expenses (367) (122) (121) +0% (124)

Profit before provisions for impairment of customer loans, restructuring costs and discontinued operations

574 169 189 -11% 216

Provisions for impairment of customer loans (492) (163) (183) -11% (146)

Share of profit /(loss) from associates 2 (2) 2 n/a 2

Profit before tax, restructuring costs and discontinued operations 84 4 8 -68% 72

Tax (15) (5) (8) -27% (2)

Loss attributable to non-controlling interests 15 7 6 2

Profit after tax and before restructuring costs, discontinued operations and net profit from disposal of non-core assets

84 6 6 -15% 72

Restructuring costs (32) (11) (16) - (5)

Loss from discontinued operations (36) - - - (36)

Net profit from disposal of non-core assets1 60 - 60 - -

Profit/(loss) after tax 76 (5) 50 n/a 31

Net interest margin 4.03% 3.83% 4.26% -43 b.p. 3.99%

Cost-to-Income ratio 39% 42% 39% +3 p.p. 36%

b.p. = basis points, p.p. = percentage points ; 100 b.p. = 1 p.p.

(1) This relates to the loss on disposal of the Ukrainian operations (€114m), the profit on disposal of the stake in Banca Tnansilvania (€47m) the profit on disposal of the

loans in Serbia (€27m) and the profit from the early repayment of the Cyprus Government Bond (€100m)

Income Statement Review

30

310

394 380 399

426 383

1H'13¹ 3Q'13 4Q'13 1Q'14 2Q'14 3Q'14

FY2013: 354 9M2014: 403

Net Interest Income (€m)

Net Interest Margin (bp)

• 3Q2014 Net Interest Income (NII) at €244m

(compared to €279m for 2Q2014) on the back of

lower customer spread reflecting reduced lending

rates and lower interest income following the

repayment of €950m of a sovereign bond by the

Republic of Cyprus (Laiki recapitalisation bond)

in July 2014

• During 3Q2014 the Bank reduced its Base

lending rates in order to help the rejuvenation of

the domestic economy

• 3Q2014 Group Net Interest Margin (NIM) at

3.83% (compared to 4.26% for 2Q2014) due to

reduction of net interest income

• NII and NIM continue to be affected by the

competitive conditions in the domestic banking

market and by the high-though-declining reliance

on Eurosystem funding which is cheaper than the

cost of customer deposits

Net Interest Income and Net Interest Margin

246 224 224 235 218

44 44 43 44

26

3Q'13 4Q'13 1Q'14 2Q'14 3Q'14

290 268 267 279

244

Interest income from Laiki Recapitalisation Bond

(1) Information for 1Q2013 and 2Q2013 is not available as it has not been possible to publish the financial results for the three months ended 31 March 2013.

31

Analysis of Non Interest Income (€m)

41 43 45 43 43

12 14 13 12 10 9

23 14

-30

-5

3

-38

1 6

-1

65 42 73 31 47

3Q'13 4Q'13 1Q'14 2Q'14 3Q'14

Fee and commission Income Insurance income net of insurance claims

FX income & Net income/(loss) from financial instruments Other income/(expense)

%

Non Interest

Income %

Operating income 10% 13% 18%

x

Non Interest

income (€m)

• The majority of non-interest income is recurring deriving from fees and commission income

and income from the insurance business

• All businesses are focusing on increasing fee income; e.g. International Banking Services

(IBS), a significant contributor of fee income in the past, is focused on reactivating volumes

in incoming and outgoing payments to improve non-interest income

• Recurring income from insurance business reflecting the Group’s leading position in the

insurance business in Cyprus

21% 16%

Analysis of Non-interest income

32

Group Cost to Income Ratio

Quarterly Total expenses (€m) • 3Q2014 Total expenses of €122m compared

to €121m for 2Q2014

• Staff costs for 3Q2014 at €67m broadly at the

same level as in the previous quarters

• The cost-to-income ratio for 9M2014 has been

broadly stable at 39%

57%

49% 47%

36% 38% 39%

1H'13¹ 9M'13 FY'13 1Q'14 1H'14 9M'14

82 64 67 68 67

52 62 57 53 55

134 126 124 121 122

3Q'13 4Q'13 1Q'14 2Q'14 3Q'14

Other operating expenses Staff costs

Total Expenses

33

(1) Information for 1Q2013 and 2Q2013 is not available as it has not been possible to publish the financial results for the three months ended 31 March 2013.

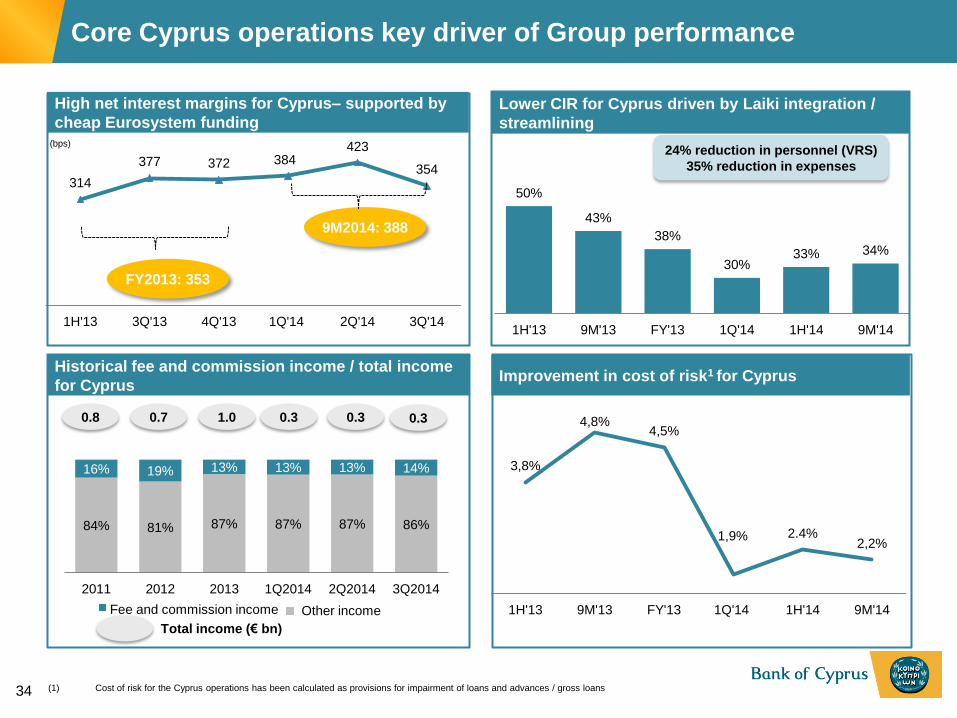

84% 81% 87% 87% 87% 86%

16% 19% 13% 13% 13% 14%

2011 2012 2013 1Q2014 2Q2014 3Q2014

314

377 372 384 423

354

1H'13 3Q'13 4Q'13 1Q'14 2Q'14 3Q'14

3,8%

4,8% 4,5%

1,9% 2.4% 2,2%

1H'13 9M'13 FY'13 1Q'14 1H'14 9M'14

High net interest margins for Cyprus– supported by

cheap Eurosystem funding

50%

43%

38%

30% 33% 34%

1H'13 9M'13 FY'13 1Q'14 1H'14 9M'14

Lower CIR for Cyprus driven by Laiki integration /

streamlining

Historical fee and commission income / total income

for Cyprus

24% reduction in personnel (VRS)

35% reduction in expenses

(bps)

Improvement in cost of risk1 for Cyprus

Fee and commission income Other income

(1) Cost of risk for the Cyprus operations has been calculated as provisions for impairment of loans and advances / gross loans

FY2013: 353

0.8

Total income (€ bn)

0.7 1.0 0.3 0.3

9M2014: 388

Core Cyprus operations key driver of Group performance

0.3

34

€m Jun

2013

Sep

2013

Dec

2013

Mar

2014

Jun

2014

Sep

2014

Change

Since

Jun

2013

Cash & bank placements 3,012 2,578 2,530 2,105 1,973 2,417 -595

Investments 3,413 3,505 3,433 3,475 3,538 2,578 -835

Net Loans 23,769 22,575 21,764 21,234 20,063 19,794 -3,975

Other assets 2,762 2,739 2,622 2,564 2,984 2,694 -68

Total assets 32,956 31,397 30,349 29,378 28,558 27,483 -5,473

Customer deposits 16,970 15,468 14,971 14,066 13,803 13,330 -3,640

ECB funding - 1,301 1,400 1,400 1,400 920 +920

ELA 11,107 9,856 9,556 9,506 8,785 7,684 -3,423

Interbank funding 983 1,038 790 753 802 707 -276

Other liabilities 976 944 895 894 954 1,057 +81

Total equity 2,920 2,790 2,737 2,759 2,814 3,785 +865

Total liab. & equity 32,956 31,397 30,349 29,378 28,558 27,483 -5,473

Balance sheet

deleverage qoq

-1,559 -1,048 -971 -820 -1,075

CET1 ratio

(transitional basis) n/a n/a 10.4% 10.6% 11.3% 15.4%

Leverage ratio

(Assets/Equity) 11.3x 11.2x 11.1x 10.6x 10.1x 7.3x

Deposit reduction less than

reduction in gross loans

Net loans reduction driven by

disposal of non-core assets and

the ongoing deleveraging

Overall ELA reduction from peak

about €3.9 bn (including November

repayment)

CET1 ratio and Leverage ratio

strengthened by Share Capital

Increase

Steady reduction of total assets

Balance Sheet Deleverage - Shrinking to Strength

35

2,95 4,05

4,82

6,66

8,25

10,21

13,13 14,04 14,44 14,58 14,74

4,97 5,13

6,45 7,69

11,01 12,98 13,00 12,76 12,59 12,98

Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

NPLs (Old definition)

NPLs (New definition)

90+ DPD

+1%

NPLs>90+DPD

by €1.8 bn

Problem Loans (€ bn)

Quarterly change in problem loans (€ bn)

+0% +18%

+29% +7%

-2%

+3%

(1) 90+ DPD are loans with a specific provision (i.e. impaired loans) and loans past-due for more than 90 days but not impaired

(2) NPLs as per the Central Bank of Cyprus definition

+1%

-1%

Credit Risk – Quality of Loan portfolio

+3%

1.97

0,02

-0,25 -0,17

0,45 0,39

2.92

0,91

0,40 0,14 0,59

0,15

3Q'13 4Q'13 1Q'14 2Q'14 2Q'14 3Q'14

90+ DPD NPLs

pro-forma

excl.

deleverage

• In 3Q2014, 90+ DPD1 increased by €387m

reflecting the recessionary conditions and

difficult legislative environment.

• NPLs2 continue to rise as restructured loans

remain classified as NPLs for longer

• NPLs growth rate maintained at 1% for 3Q2014

• Adjusting for the disposal of the Ukraine

operations and Serbian loans, the 3Q2014

increase in 90+DPD and NPLs was lower than

the 2Q2014 increase

36

Group loan quality indicators

Trends in 90+DPD and provisions

30% 48% 42% 37% 38% 39% 39% 38%

17,2%

27,4%

38,8%

47,4% 48,6% 48,6% 49,8% 52,5%

Dec-11 Dec-12 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

90+ DPD provision coverage 90+ DPD ratio

Accumulated provisions

1,5 3,7 4,6 4,8 5,0 5,0 4,9 4,9

5,2%

13,1%

16,2% 17,6%

18,6% 19,1% 19,3% 20,0%

Dec-11 Dec-12 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

Accumulated provisions (€ bn)

Provisions % Gross loans

• 90+ DPD ratio at 52.5%

• 90+ DPD provision coverage stood

at 38%; Taking into account

tangible collateral, 90+ DPD are

fully covered

• Accumulated provisions at €4.9 bn

or 20% of gross loans

• Conservative provisioning

assessment takes into account

property value indexation, expected

future evaluation of property prices

and costs incurred during the

recovery period

Credit Risk – Provisions

37

6,2 7,2 7,2 6,8

1,6 1,6

2,6 3,3 3,3 3,5

0,8 0,8

1,0

1,3 1,3 1,3

0,5 0,6

1,2

1,2 1,2 1,2

0,6 0,6

3,9 3,8

1,2 1,2

4,0 4,4

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

Corporate SMEs Retail Housing Retail Consumer and other RRD- Mid and Large Corporates RRD- SMEs RRD- Recoveries

13.0 12.8

11.0 13.0 13.0

12.6

Group 90+DPD loans by type/business line (new presentation adopted as of June 20141)

(1) As part of the restructuring of the Group, management is currently monitoring the loan portfolio of the Group using new business line definitions. An important

component of the Group’s new operational structure is the establishment of the RRD for the purposes of centralising and streamlining the management of its

delinquent loans. No comparative information is available.

Credit Risk – Gross loans and 90+ DPD by Business Line

13,1 12,5 12,2 11,9

5,2 4,9

6,4 6,2 6,1 6,1

2,7 2,6

5,4 5,3 5,4 5,3

3,9 3,9

3,4 3,4 3,0 2,9

2,0 1,9

5,8 5,6

1,5 1,5

4,1 4,4

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

Corporate SMEs Retail Housing Retail Consumer and other RRD- Mid and Large Corporates RRD- SMEs RRD- Recoveries

28.4

Gross loans by type/business line (new presentation adopted as from June 20141)

27.4 26.7 26.3 25.3

(€ bn)

Total 24.7

(€ bn)

Total

38

6,2 7,2 7,2 6,8 7,0 7,1

2,6 3,3 3,3 3,5 3,2 3,4

2,2

2,5 2,5 1,3 2,4

2,5

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

Corporate SMEs Retail

2

13.0 Total 12.6

(€bn)

11.0 13.0 13.0 12.8

Group 90+DPD loans by segment

39

Credit Risk – Gross loans and 90+ DPD by Segment

13,1 12,5 12,2 11,9 12,6 12,2

6,4 6,2 6,1 6,1 5,5 5,5

8,9 8,7 8,4 8,2 7,2 7,0

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

Corporate SMEs Retail

28.4

Gross loans by segment

27.4 26.7 26.3 25.3

(€ bn)

Total 24.7

(1) Other countries: Romania, Ukraine (until March 2014) and Greece

(2) Other countries: Romania and Ukraine (until March 2014)

Gross Loans by Geography

€m 31.12.13 31.03.14 30.06.14 30.09.14

Cyprus 22,964 22,763 22,185 21,881

UK 1,284 1,194 1,172 1,112

Russia 1,429 1,290 1,304 1,208

Other

countries1

1,066 1,016 639 541

Group 26,743 26,263 25,300 24,742

Deposits by Geography

€m

31.12.13 31.03.14 30.06.14 30.09.14

Cyprus non-IBU 8,658 8,196 8,094 7,785

Cyprus IBU 4,047 3,789 3,594 3,458

Cyprus – Total 12,705 11,985 11,688 11,243

UK 1,244 1,249 1,252 1,289

Russia 919 767 845 794

Other countries2 103 65 18 4

Group 14,971 14,066 13,803 13,330

Loans and Deposits by Geography

88,4%

4,5% 4,9% 2,2%

Cyprus

UK

Russia

Romania

Gross Loans by Geography

58,4% 25,9%

9,7%

6,0% 0,0% Cyprus

Cyprus - IBU

UK

Russia

Romania

Total Cyprus

84.3%

Deposits by Geography

40

9,7 8,9 8,7 8,2 8,1 7,8

4,8 4,1 4,0 3,8 3,6 3,5

1,3 1,3 1,2 1,2 1,3 1,3

1,2 1,1 0,9

0,8 0,8 0,8

0.10 0,1 0,1

0,1 0,0 0,0

17,0 15,5 15,0

14,1 13,8 13,3

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

Other countries*

Russia

UK

Cyprus IBU

Cyprus non-IBU

12,7 11,3 10,6 9,6 9,1 8,5

0,8 0,9 0,9

0,9 0,9 0,8

3,4 3,3 3,5

3,5 3,7 4,0

17,0 15.47 15,0

14,1 13,8 13,3

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

Current & demand accounts

Savings accounts

Time deposits

Total

(€ bn)

* Other countries: Romania and Ukraine

Total

(€ bn)

Deposits by geography

Deposits by type of deposit

Analysis of Deposits by Geography and by Type

41

9,7 8,9 8,7 8,2 8,1 7,8

4,8 4,1 4,0 3,8 3,6 3,5

14,4 13,0 12,7 12,0 11,7 11,2

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

IBUs

Non-IBUs

Cyprus Deposits (€ bn)

10,3 9,9 9,9 9,8 3,4 3,2

5,4 5,3 5,2 5,2

1,9 1,8

5,3 5,2 5,3 5,2

3,9 3,8

3,0 2,9 2,6 2,6

1,7 1,6

5,8 5,6

1,5 1,5

4,1 4,4

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

RRD- Recoveries

RRD- Mid Corporations

RRD- Large Corporations

Retail Consumer and other

Retail Housing

SMEs

Corporate

24.0

Gross loans by type/business line (presentation adopted as from June 20141)

23.3 23.0 22.8 22.2

(€ bn)

Total 21.9

(1) As part of the restructuring of the Group, management is currently monitoring the loan portfolio of the Group using new business line definitions. An important

component of the Group’s new operational structure is the establishment of the RRD for the purposes of centralising and streamlining the management of its delinquent

loans

Loans and Deposits in Cyprus

42

90+ DPD ratios by economic activity

40

,7%

37

,6%

40

,1%

54

,8%

46

,0%

25

,6%

40

,8%

41

,1%

44

,1%

49

,7%

51

,1%

69

,6%

51

,7%

32

,1%

56

,8%

64

,7%

44

,4%

51

,1%

46

,8%

72

,1%

50

,4%

33

,0%

53

,5%

64

,0%

44

,8%

53

,3%

51

,9%

76

,7%

48

,0%

34

,1%

54

,9%

59

,6%

46

,7%

55

,3%

59

,8%

78

,3%

51

,2%

36

,8%

57

,7%

60

,5%

30.06.13 31.12.13 31.03.14 30.06.14 30.09.14

3,1

2

1,1

1

1,9

3

4,1

5

4,6

1 8

,73

2,7

8

1,9

2

2,8

3

1,0

0

1,8

9

4,2

5

4,2

0

8,5

4

2,3

1

1,7

3

2,8

2

0,9

5

1,8

5

4,2

1

4,1

2

8,4

1

2,1

8

1,7

2

2,7

4

0,9

6

1,8

2

4,1

3

3,6

3

8,0

5

2,4

4

1,5

3

2,7

0

0,9

5

1,6

1 4,0

9

3,5

9

7,9

6

2,3

2

1,5

3

30.06.13 31.12.13 31.03.14 30.06.14 30.09.14

Trade Manufacturing Hotels &

Restaurants

Construction Real estate Private

Individuals

Professional

& other

services

Other

sectors

Gross loans by economic activity (€ bn)

Trade Manufacturing Hotels &

Restaurants

Construction Real estate Private

Individuals

Professional

& other

services

Other

sectors

15% 11% 32% 9% 6% % of

total 17% 6% 4%

Analysis of Loans and 90+ DPD ratios by Economic Activity

43

90+ DPD (€ bn) and Quarterly change of 90+ DPD (€m)

(1) Information for 1Q2013 and 2Q2013 is not available as it has not been possible to publish the financial results for the three months ended

31 March 2013.

321

380

329

-85

265

410

558

96

232

156

402

609

100

64

1.3

19

1.2

40

3.3

19

1.9

72

20

-247

-165

387

1,3 1,6 2,0 2,3 2,2 2,5 2,9

3,5 3,6 3,8 4,0 4,4

5,0 5,1 5,1

6,5

7,7

11,0

13,0 13,0 12,8 12,6 13,0

De

c-0

8

Mar-

09

Ju

n-0

9

Sep-0

9

De

c-0

9

Mar-

10

Ju

n-1

0

Sep-1

0

De

c-1

0

Mar-

11

Jun

-11

Se

p-1

1

De

c-1

1

Mar-

12

Ju

n-1

2

Sep-1

2

De

c-1

2

Jun-1

3¹

Sep-1

3

De

c-1

3

Mar-

14

Ju

n-1

4

Sep-1

4

Quarterly change of 90+ DPD (€ mn)

90+ DPD (€ bn)

90+ DPD and Quarterly Change of 90+ DPD

FY2009

€945m FY2010

€1,329m FY2011

€1,399m

FY2012

€2,723m FY2013

€5,311m

9M2014

-€25m

90+ DPD

formation

44

58%

49%

9%

58% 60%

51%

9%

60%

53%

47%

6%

53% 55%

47%

8%

55%

Loans more than 90 days past due and Loans restructured and more than 90 days past due

NPLs (based on Central Bank of Cyprus rules)

Total NPL ratio

Loans restructured and less than 90 days past due

Dec-13

Trends in Non-performing loans

Mar-14

• NPL ratio (based on Central Bank of Cyprus rules) at 60% at 30 September 2014. New EBA definition to

be adopted as from December 2014.

• NPLs provisioning coverage ratio at 34% at 30 September 2014

• At 30 September 2014, the NPLs ratio comprises Loans restructured and less than 90 days past due

(9% of gross loans) and Loans more than 90 days past due and Loans restructured and more than

90 days past due (51% of gross loans)

Sep-14 Jun-14

Credit Risk – Non-performing Loans

45

Reversal in customer outflows during H2 2014

46

(49,7) (44,9)

(20,0)

(11,4) (8,8) (4,7)

6,0 1,0

15,0

(8,0) (8,0) (5,0) (4,0)

3,0 4,0 1,0

(3,0)

2,0 3,0 6,0

Ap

r-1

3

Ma

y-1

3

Ju

n-1

3

Ju

l-1

3

Au

g-1

3

Se

p-1

3

Oct-

13

Nov-1

3

Dec-1

3

Ja

n-1

4

Fe

b-1

4

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Ju

n-1

4

Ju

l-1

4

Au

g-1

4

Se

p-1

4

Oct-

14

Nov-1

4

Average daily customer flows per month (€m) • Customer outflows significantly abated during

H2 2014 and the deposit base showed signs of

stabilisation

• Customer outflows during Q1 2014 reflect one

off items and seasonality factors such as

payments of taxes, dividends by international

companies and the impact from the release of

the 6m decree deposits as well as the

relaxation of restrictive measures

• Since May 2014, the Bank experienced

customer inflows every month (with the

exception of August) despite:

– The release of €1.2 bn of blocked

decree deposits in July and October

2014

– The full abolition of internal controls at

the beginning of June 2014

• Fresh funds balance1 increased to €1,538m.

The amount of fresh money is approximately

9.3% of total customer deposits

Increasing fresh funds balances1 (€m)

443 507 599 610 652 700 740

898

1.119 1.188 1.240 1.336 1.394

1.538

Oct-

13

Nov-1

3

Dec-1

3

Ja

n-1

4

Fe

b-1

4

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Ju

n-1

4

Ju

l-1

4

Au

g-1

4

Se

p-1

4

Oct-

14

Nov-1

4

(1) Funds received from abroad minus funds sent abroad per customer, post March 2013 and not subject to restrictive measures

A strong and experienced Management team

47

• Blend of extensive restructuring experience and long standing local market knowledge and client relationships

• Clearly defined separation among business lines, particularly NPL management

Executive management Business segments (origination of new business)

• Wealth/Brokerage/AM: Costas Argyrides

• International Operations: Miltiades Michaelas

• Eurolife: Artemis Pantelidou

• General Insurance: Stelios Christodoulou

• Human Resources: Solonas Matsias

RRD (NPL management and large exposures >€100m)

Finance Director

• Joined 1996

• Strong financial markets experience and longevity

with the Bank

• Former executive at CBC; familiar with local regulations

and government policy making Dr. Chris

Patsalides

Chief Executive Officer

• Joined in October 2013

• Formerly Chief Executive of RBS’s investment bank

division John

Hourican

Group Chief Risk Officer

• Joined Laiki in 1995

• Extensive local and international experience including the

disposal of 2 banking subsidiaries

• Formerly Treasurer and Director of International

Operations of Cyprus Popular Bank

Michalis

Athanasiou

Group Chief Financial Officer

• Joined 1999

• Robust financial knowledge and longevity with the Bank

• Chartered Accountant, formerly at Arthur Andersen Eliza

Livadiotou

Nicolas

Sparsis

Corporate banking

• Joined in 1983

• Significant knowledge of the local business market and

extensive experience in customer relationship

management

Dr. Charis

Pouangare

Consumer & SME banking

• Joined in 1991

• Significant experience with the bank in all local sectors,

Retail, SME and Corporate

• Excellent knowledge of customer needs and market

dynamics

Louis

Pochanis

International Banking Services

• Joined in 1993

• Set up Private Banking and Wealth Management in

Cyprus and then Greece

Director of Restructuring and Recoveries Division

• Joined in December 2013

• Oversaw the run-down of c.£75bn of non-core assets at

RBS Euan

Hamilton

Disclaimer

48

This presentation has been prepared for information and background purposes only. It is confidential and neither it nor

any part of it may be reproduced (electronically or otherwise) or redistributed, passed on, or the contents otherwise

divulged, directly or indirectly, to any other person (excluding the recipient's professional advisers) or published in whole

or in part for any purpose without the prior written consent of the Bank of Cyprus Public Company Ltd (the "Bank"). This

presentation does not purport to be all-inclusive or to contain all of the information that a person considering the

purchase of any offered securities may require to make a full analysis of the matters referred to herein. Certain

statements, beliefs and opinions in this presentation are forward-looking. Such statements can be generally identified

by the use of terms such as “believes”, “expects”, “may”, “will”, “should”, “would”, “could”, “plans”, “anticipates” and

comparable terms and the negatives of such terms. By their nature, forward-looking statements involve risks and

uncertainties and assumptions about the Group that could cause actual results and developments to differ materially

from those expressed in or implied by such forward-looking statements. These risks, uncertainties and assumptions

could adversely affect the outcome and financial effects of the plans and events described herein. We have based

these forward-looking statements on our current expectations and projections about future events. Any statements

regarding past trends or activities should not be taken as a representation that such trends or activities will continue in

the future. Readers are cautioned not to place undue reliance on forward-looking statements, which are based on facts

known to and/ or assumptions made by the Group only as of the date of this presentation. The Bank's ability to achieve

its projected results depends on many factors which are outside management's control. Actual results may differ

materially from those contained or implied in the forward-looking statements. We assume no obligation to update such

forward -looking statements or to update the reasons that actual results could differ materially from those anticipated in

such forward-looking statements. This presentation does not constitute an offer to sell, or a solicitation of an offer to

buy, any security in the United States, or any other jurisdiction. The delivery of this presentation shall under no

circumstances imply that there has been no change in the affairs of the Group or that the information set forth herein is

complete or correct as of any date. This presentation shall not be used in connection with any investment decision

regarding any of our securities, which should only be made based on expressly authorised materials from us identified

as such, nor in connection with any decision whether or how to vote on any matter submitted to our stockholders. The

securities issued by the Bank have not been, and will not be, registered under the US Securities Act of 1933 (“the

Securities Act”), or under the applicable securities laws of any other jurisdiction and may only be offered or sold in the

United States to “qualified institutional buyers” as defined in Rule 144A under the Securities Act and outside the United

States in compliance with Regulation S under the Securities Act.