A data mining approach to the prediction of corporate failure

Upload

nguyencongCategory

view

218download

1

Asian Economic and Financial Review, 2016, 6(9): 522-533

522

† Corresponding author

DOI: 10.18488/journal.aefr/2016.6.9/102.9.522.533

ISSN(e): 2222-6737/ISSN(p): 2305-2147

© 2016 AESS Publications. All Rights Reserved.

BANK FAILURE PREDICTION MODELS FOR THE DEVELOPING AND DEVELOPED COUNTRIES: IDENTIFYING THE ECONOMIC VALUE ADDED FOR PREDICTING FAILURE

Yi-Shu Wang1 --- Xue Jiang2 --- Zhen-Jia-Liu3†

1,2,3School of Business, Changzhou University, Changzhou City, Jiangsu Providence, China

ABSTRACT

This study used data from 2003-2013, and used a logistic model to analyze the factors that influence financial early

warning systems in developing and developed countries. We employed a bank capital adequacy ratio less than 8%,

Tier I capital ratio less than 4%, and nonperforming loan ratio more than one third to measure bank failure and

identify the financial ratio that most accurately predicts bank failure. The results indicate that the economic value

added index is more effective than other indexes in predicting bank failure in NAFTA, ASEAN, EU, NIC, and G20

nations.

© 2016 AESS Publications. All Rights Reserved.

Keywords: Bank failure prediction, Business, Economic value added, Developing countries, Developed countries, Financial early warning.

Contribution/ Originality

The paper contributes the first logical analysis economic value added that influence financial early warning

systems in developing and developed countries.

1. INTRODUCTION

Research on corporate failure prediction is expanding worldwide. From a practical perspective, corporate failure

prediction influences the decisions of stakeholders (e.g., stockholders, creditors, managers, auditors, and employees).

From an academic perspective, several studies have identified various determinants of corporate failure and have

developed optimal models for predicting corporate failure. Banks differ from other industries because they receive

deposits and provide loans for profit. Thus, the collapse of banks, often caused by mismanagement or the economic

environment, negatively affects depositor rights and other industries, can induce international financial distress and

destabilize economic development. Consequently, evaluating bank operations and establishing an early warning

system are a top priority for global financial authority (Huang et al., 2012).

Early warning systems first appeared in the banking industry in 1970s. The effectiveness of financial ratios, such

as current (Jayadev, 2006) EBIT-to-assets (Jayadev, 2006) equity-to-debt (Jayadev, 2006; Distinguin et al., 2011)

equity-to-assets (Shkurti and Duraj, 2010; Maghyereh and Awartani, 2014) net income–to-assets (Li et al., 2011)

expenses-to-assets (Li et al., 2011) working capital-to-assets (Ecer, 2013);and profit before taxes-to-equity ratios

(Shkurti and Duraj, 2010) for predicting and explaining bank failure has been investigated. However, these ratios

follow generally accepted accounting principles, requiring conservatism in preparing financial statements that only

Asian Economic and Financial Review

ISSN(e): 2222-6737/ISSN(p): 2305-2147

URL: www.aessweb.com

Asian Economic and Financial Review, 2016, 6(9): 522-533

523

© 2016 AESS Publications. All Rights Reserved.

reflect historic costs. Thus, traditional financial ratios do not reflect the actual bank value. The economic value added

(EVA) index is calculated “after subtracting the cost of capital from the operating profits” (Stewart, 1991) and

involves using adjustment items to reflect the true value of a firm. Furthermore, Teker et al. (2011) showed that EVA

is useful in determining the true value of a bank. Conversely, numerous studies have adopted EVA to detect corporate

failure (Timo and Virtanen, 2001; Pasaribu, 2008; Klecka and Scholleova, 2010; Anvarkhatibi et al., 2013). However,

these studies have adopted only the unadjusted EVA to predict corporate failure, which does not provide a

comprehensive overview of a company’s economic performance. Therefore, in this study, we employ the unadjusted

EVA and adjusted EVA to predict bank failures and identify which index is superior in comparison to various

financial ratios (accuracy). All the countries have different types of governments and cultures, laws, economic

development. The operational system and environment of banks in nations are also substantially different and

therefore cannot be considered equivalent. We developed an optimal model and compared the early warning

indicators of bank failures in North America Free Trade

2. LITERATURE REVIEW

Classical models for predicting bank bankruptcy have been extensively researched: multivariate adaptive

regression spines (Martin et al., 2011) logistic regression (Al-Saleh and Al-Kandari, 2012; Fungacova and Weill,

2013; Valahzaghard and Bahrami, 2013; Zaghdoudi, 2013; Canicio and Blessing, 2014) back propagation neural

network (Pradhan et al., 2013) hazard model (Kiefer, 2014; Maghyereh and Awartani, 2014) Principal Component

Analysis (Adeyeye et al., 2012) multiple discriminant analysis (Ioannidis et al., 2010) fuzzy C-means clustering

(Martin et al., 2011) group method of data handling (Ravisankar and Rav, 2010) fuzzy adaptive resonance theory map

(Ravisankar and Rav, 2010) artificial neural network (Ioannidis et al., 2010) classification and regression trees

(Ioannidis et al., 2010) genetic algorithm (Martin et al., 2011) partial least square discriminant analysis (Serrano-

Cinca, 2013) k-Nearest neighbours (Ioannidis et al., 2010) counter propagation neural network (Ravisankar and Rav,

2010) ordered logistic regression (Ioannidis et al., 2010) neuro fuzzy (Yildiz and Akkoc, 2010) dynamic slacks based

model (Wanke et al., 2015) neural networks (Lopez and Pastor, 2015) geometric mean based boosting algorithm

(Kim et al., 2015) discriminant analysis (Cox and Wang, 2014). The Federal Deposit Insurance Corporation

constructed financial ratios such as capital adequacy, asset quality, management quality, earnings strength, and

liquidity (collectively referred to as CAMEL) to monitor banks and predict bank failure (Trussel and Johnson, 2012;

Valahzaghard and Bahrami, 2013; Canicio and Blessing, 2014). The application of these traditional accounting tools

for measuring corporate failures has been questioned, for various reasons. The tools are suitable for analyzing

historical data, but not for future decision-making (Rappaport, 1995). Pasaribu (2008) showed that public companies

that do not create EVA are at a high risk of distress. Timo and Virtanen (2001) indicated that EVA can warn about an

approaching bankruptcy because economic bankruptcy occurs when the value of a firm becomes negative (i.e., when

a firm is unable to earn profit in excess of the required return). Anvarkhatibi et al. (2013) asserted that the probability

of bankruptcy decreases with increasing economic value. This is because higher company economic value results in

positive EVA as a result of shareholder return and available opportunities for profitable investments and paying loan

interest. Thus, Anvarkhatibi et al. (2013) indicated that EVA is a superior index for predicting bankruptcy and

providing useful information for shareholders. Hence, the EVA measure could be dangerously susceptible as a distress

warning device. Accordingly, we proposed Hypothesis 1 as follows:

H1: The corporate failure prediction accuracy of economic value added is higher than that of other financial ratios.

Asian Economic and Financial Review, 2016, 6(9): 522-533

524

© 2016 AESS Publications. All Rights Reserved.

3. METHODOLOGY

Financial ratios were used to predict distress in the banking industry, incorporating data from 2003-2013 from

the COMPUSTAT and AREMOS database.

The study comprised 775 banks1 .

A logistic model was adopted to analyze the data. The variables and research model are presented in the

following sections.

3.1. Dependent variables: Bank failures

Lin (2010) showed that a bank capital adequacy ratio less than 8%, Tier I capital ratio less than 4%, and

nonperforming loan ratio more than one third is determined for the distressed bank. In addition, the capital adequacy

ratio is calculated by dividing total capital by average assets; the elements of total capital are used as core capital

combined with additional capital (i.e., Tier I capital plus Tier II capital).2 Tier I capital (i.e., common stock and

qualifying preferred stock) divided by risk-adjusted assets yields the Tier I capital ratio. The nonperforming loan ratio

is measured as the nonperforming loans (i.e., past due loans, the principal and/or interest of which is unpaid for 30

days or more after the due date) divided by all loans (including interbank loans). This formula is based on the 1988

Basel Capital Accord standards for the definition of equity. Overall, the value of the dummy variable was 1

(distressed group), and the value of the contrary variable was 0.

3.2. Independent Variables: Financial Ratios

Jayadev (2006) stated that successful banks have high current ratios, earnings before interest, and taxes-to-assets

ratios. Furthermore, Shkurti and Duraj (2010) stated that successful banks have high profit before taxes-to-equity

ratios, and Li et al. (2011) showed that successful banks have low expenses-to-assets ratios. EVA also can be used to

detect corporate failure (Timo and Virtanen, 2001; Pasaribu, 2008; Klecka and Scholleova, 2010; Anvarkhatibi et al.,

2013).

3.3. Control Variables: Bank Factors

Bank factors reflect bank operating environments, thus explaining how they affect bank failure. Shkurti and

Duraj (2010) showed that successful banks have low interest expenses-to-deposits ratios. Moreover, Öğüt et al.

(2012) asserted that successful banks have high interest revenue minus interest expenses-to-number of bank branches

ratios. Canicio and Blessing (2014) showed that successful banks have high deposits-to-total assets ratios and that

unsuccessful banks have high loans-to-assets ratios.

1NAFTA (North America Free Trade Area): America, Canada, Mexico. ASEAN (Association of Southeast Asian Nations): Indonesia, Thailand, Malaysia, Philippines,

Vietnam, Singapore. EU(European Union): Denmark, Belgium, Lithuania, Hungarian, Spain, Greece, Poland, France, Finland, Bulgaria, Malta, Czech, Netherlands,

Slovak, Slovenia, Cyprus, Austria, Ireland, Sweden, Italy, Portugal, Germany, Romania, United Kingdom, Luxembourg, Latvia, Es tonia).NIC (Newly industrialized

country):South- Africa, Brazil, China, India, Turkey. G20: Argentina, Austrlia, Japan, Korea, Russia, Saudi Arabia

2Tier II capital includes preferred stock, subordinated debt, and loan loss reserves.

Asian Economic and Financial Review, 2016, 6(9): 522-533

525

© 2016 AESS Publications. All Rights Reserved.

3.4. Empirical model3

The study used the logistic method. The proxy variables are as follows: tjCR , represents current assets compared

with current liabilities. tjEBITTA , represents earnings before interest and taxes compared with assets.

tjEBTE ,

represents earnings before taxes compared with equity. tjETA ,

represents expenses compared with assets. tjIED ,

represents interest expenses compared with deposits. tjNETI , represents interest revenue minus interest expenses

compared with number of bank branches. tjDTA , represents deposits compared with total assets.

tjLTA , represents

loans compared with assets. jUAEVA is the unadjusted EVA4 compared with the outstanding shares; jAEVA is the

adjusted EVA5 (join accounting adjusted items) compared with the outstanding shares ; jEDAEVA represents the

adjusted EVA6 (join accounting adjusted items and economic depreciation adjusted items) compared with the

outstanding shares.

3.4. Performance Measures

Fungacova and Weill (2013) proposed an early warning model for the quarters (1Q, 2Q, 3Q, and 4Q) prior to the

event of bank distress that used financial ratios. Banks with cut-off points above 0.5 were classified as bankrupt banks

and banks under 0.5 were classified as successful banks. The overall predictive power is the ratio between the sum of

all safe and failed banks accurately identified and the total number of banks. A more detailed performance analysis

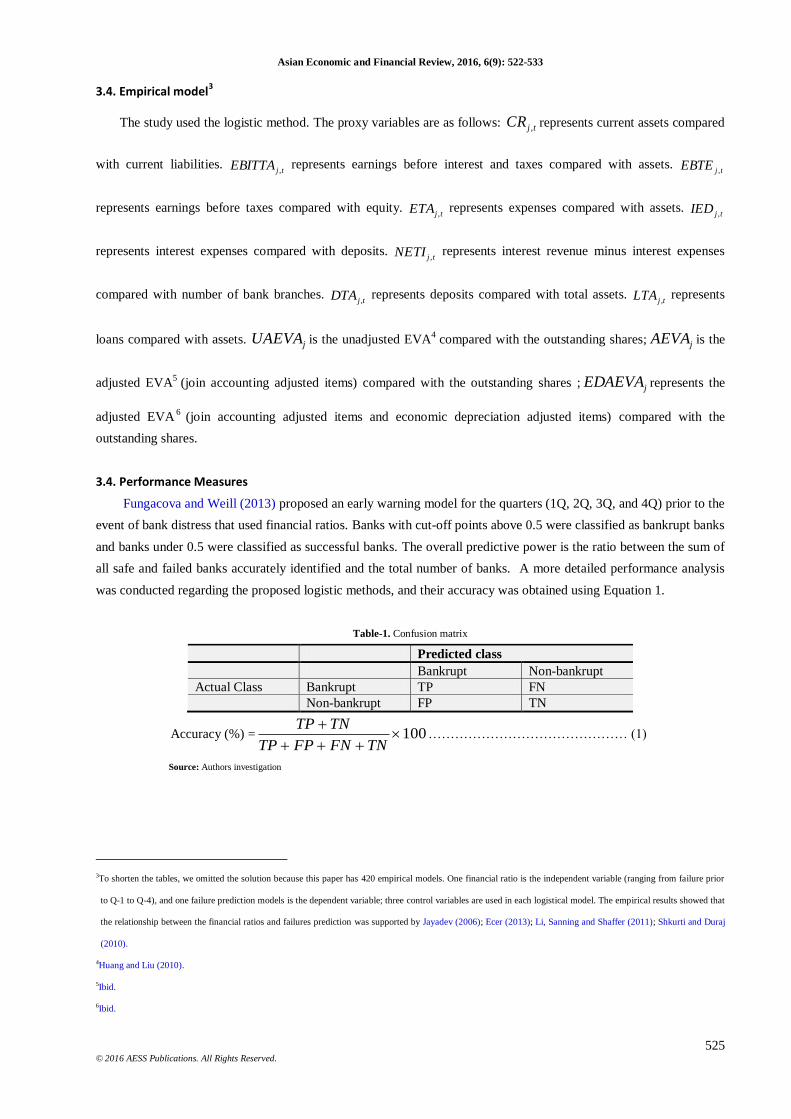

was conducted regarding the proposed logistic methods, and their accuracy was obtained using Equation 1.

Table-1. Confusion matrix

Predicted class

Bankrupt Non-bankrupt

Actual Class Bankrupt TP FN

Non-bankrupt FP TN

Accuracy (%) = 100

TNFNFPTP

TNTP……………………………………… (1)

Source: Authors investigation

3To shorten the tables, we omitted the solution because this paper has 420 empirical models. One financial ratio is the independent variable (ranging from failure prior

to Q-1 to Q-4), and one failure prediction models is the dependent variable; three control variables are used in each logistical model. The empirical results showed that

the relationship between the financial ratios and failures prediction was supported by Jayadev (2006); Ecer (2013); Li, Sanning and Shaffer (2011); Shkurti and Duraj

(2010).

4Huang and Liu (2010).

5Ibid.

6Ibid.

Asian Economic and Financial Review, 2016, 6(9): 522-533

526

© 2016 AESS Publications. All Rights Reserved.

3.5. Robustness Test7

We also repeat the same analyses out‐of‐sample to tackle a possible sample specific issue and get more robust

and general results

4. RESULTS

4.1. Descriptive Statistics

Table 2 shows that the mean of all financial ratios (including EVA). The current ratios all exceed 100%, with

NAFTA at 172.52% (highest) and EU at 117.85% (lowest). Earnings before interest, taxes compared with assets, and

earnings before taxes compared with equity had a positive value for all groups. Expenses compared with assets were

less than 30%, indicating that operating policies were robust. Conversely, the mean of the interest revenue minus

interest expenses compared with the number of bank branches exceeded 08, showing that public banks in these

countries have a large capacity for measuring and managing risk.

Interest expenses compared with deposits ranged from 11.25% to 20.11%, deposits compared with total assets

averaged approximately 50%, and loans compared with assets averaged approximately 45%. These results indicated

that credit policies were robust and stable, and appropriate loan losses are a suitable measure for risk management. In

addition, the mean of the EVA is positive9, showing that the public banks in these countries have a considerable

ability to be profitable or to manage funds efficiently.

4.2. Empirical Test

The comparisons of predicted and actual bankruptcy classifications are shown in Tables 3-6. As indicated in

Table 3 (one quarter before a failure), NAFTA banks had the highest value (the accuracy of the logistic model was

39.57%) when unadjusted EVA was employed to predict bank failure (the proxy variable is the bank capital adequacy

ratio below 8%) and the lowest value (the accuracy of the logistic model was 27.23%) when the expenses compared

with assets were employed to predict bank failure (the proxy variable is bank Tier I capital ratio below 4%);ASEAN

banks had the highest value (the accuracy of the logistic model was 35.08%) when adjusted EVA (join accounting

adjusted items) was employed to predict bank failure (the proxy variable is bank capital adequacy ratio below 8%),

and the lowest value (the accuracy of the logistic model was 26.58%) when adjusted EVA (join accounting adjusted

items) was employed to predict bank failure (the proxy variable is bank Tier I capital ratio below 4%);EU banks had

the highest value (the accuracy of the logistic model was 37.52%) when unadjusted EVA was employed to predict

bank failure (the proxy variable is bank capital adequacy ratio below 8%) and the lowest value (the accuracy of the

logistic model was 28.16%) when the earnings before interest and taxes compared with assets were employed to

predict bank failure (the proxy variable is bank Tier I capital ratio below 4%);NIC banks had the highest value (the

accuracy of the logistic model was 39.98%) when adjusted EVA (join accounting adjusted items and economic

deprecation adjusted items) was employed to predict bank failure (the proxy variable is bank capital adequacy ratio

below 8%), and the lowest value (the accuracy of the logistic model was 27.61%) when adjusted EVA (join

accounting adjusted items) was employed to predict bank failure (the proxy variable is bank Tier I capital ratio below

4%. G20 banks had the highest value (the accuracy of the logistic model was 36.94%) when adjusted EVA (join

accounting adjusted items and economic deprecation adjusted items) was employed to predict bank failure (the proxy

7We adopted 1 (in sample) to 1 (out of sample) and showed that this method is consistent with “performance measures”.

8US ten thousand dollars

9US dollars

Asian Economic and Financial Review, 2016, 6(9): 522-533

527

© 2016 AESS Publications. All Rights Reserved.

variable is bank capital adequacy ratio below 8%), and the lowest value (the accuracy of the logistic model was

19.25%) when unadjusted EVA was employed to predict bank failure (the proxy variable is bank capital adequacy

ratio below 8%).

As indicated in Table 4 (two quarters before a failure), NAFTA banks had the highest value (the accuracy of the

logistic model was 60.91%) when unadjusted EVA was employed to predict bank failure (the proxy variable is bank

capital adequacy ratio below 8%), and the lowest value (the accuracy of the logistic model was 38.57%) when the

expenses compared with assets were employed to predict bank failure (the proxy variable is bank Tier I capital ratio

below 4%);ASEAN banks had the highest value (the accuracy of the logistic model was 54.09%) when adjusted

EVA (join accounting adjusted items) was employed to predict bank failure (the proxy variable is bank capital

adequacy ratio below 8%), and the lowest value (the accuracy of the logistic model was 37.67%) when adjusted EVA

(join accounting adjusted items) was employed to predict bank failure (the proxy variable is bank’s Tier I capital ratio

below 4%);EU banks had the highest value (the accuracy of the logistic model was 57.79%) when adjusted EVA

(join accounting adjusted items and economic deprecation adjusted items) was employed to predict bank failure (the

proxy variable is bank capital adequacy ratio below 8%), and the lowest value (the accuracy of the logistic model was

39.85%) when the earnings before interest and taxes compared with assets was employed to predict bank failure (the

proxy variable is bank Tier I capital ratio below 4%);NIC banks had the highest value (the accuracy of the logistic

model was 57.91%) when adjusted EVA (join accounting adjusted items and economic deprecation adjusted items)

was employed to predict bank failure (the proxy variable is bank capital adequacy ratio below 8%), and the lowest

value (the accuracy of the logistic model was 38.34%) when the earnings before interest and taxes compared with

assets was employed to predict bank failure (the proxy variable is bank Tier I capital ratio below 4%);G20 banks

had the highest value (the accuracy of the logistic model was 56.92%) when adjusted EVA (join accounting adjusted

items and economic deprecation adjusted items) was employed to predict bank failure (the proxy variable is bank

capital adequacy ratio below 8%), and the lowest value (the accuracy of the logistic model was 27.53%) when

adjusted EVA was employed to predict bank failure (the proxy variable is bank Tier I capital ratio below 4%).

Compared to Table 3 and Table 4, as indicated in Table 5 (three quarters before a failure), NAFTA banks had the

highest value (the accuracy of the logistic model was 58.72%) when unadjusted EVA was employed to predict bank

failure (the proxy variable is bank capital adequacy ratio below 8%), and the lowest value (the accuracy of the logistic

model was 36.24%) when adjusted EVA (join accounting adjusted items and economic deprecation adjusted items)

was employed to predict bank failure (the proxy variable is bank non-performing loan ratio above one third or more)

;ASEAN banks had the highest value (the accuracy of the logistic model was 52.12%) when adjusted EVA (join

accounting adjusted items) was employed to predict bank failure (the proxy variable is bank capital adequacy ratio

below 8%), and the lowest value (the accuracy of the logistic model was 36.18%) when unadjusted EVA was

employed to predict bank failure (the proxy variable is bank’s non-performing loan ratio above one third or more);

EU banks had the highest value (the accuracy of the logistic model was 55.79%) when unadjusted EVA was

employed to predict bank failure (the proxy variable is bank capital adequacy ratio below 8%), and the lowest value

(the accuracy of the logistic model was 38.15%) when the current assets compared with current liabilities was

employed to predict bank failure (the proxy variable is bank non-performing loan ratio above one third or more);

NIC banks had the highest value (the accuracy of the logistic model was 55.81%) when adjusted EVA (join

accounting adjusted items and economic deprecation adjusted items) was employed to predict bank failure (the proxy

variable is bank capital adequacy ratio below 8%), and the lowest value (the accuracy of the logistic model was

36.73%) when the current assets compared with current liabilities was employed to predict bank failure (the proxy

variable is bank non-performing loan ratio above one third or more);G20 banks had the highest value (the accuracy

of the logistic model was 54.86%) when adjusted EVA (join accounting adjusted items and economic deprecation

Asian Economic and Financial Review, 2016, 6(9): 522-533

528

© 2016 AESS Publications. All Rights Reserved.

adjusted items) was employed to predict bank failure (the proxy variable is bank capital adequacy ratio below 8%),

and the lowest value (the accuracy of the logistic model was 26.57%) when unadjusted EVA was employed to predict

bank failure (the proxy variable is bank non-performing loan ratio above one third or more).

As indicated in Table 6 (four quarters before a failure), NAFTA banks had the highest value (the accuracy of the

logistic model was 56.59%) when unadjusted EVA was employed to predict bank failure (the proxy variable is bank

capital adequacy ratio below 8%), and the lowest value (the accuracy of the logistic model was 33.72%) when

adjusted EVA (join accounting adjusted items and economic deprecation adjusted items) was employed to predict

bank failure (the proxy variable is bank Tier I capital ratio below 4%);ASEAN banks had the highest value (the

accuracy of the logistic model was 50.36%) when adjusted EVA (join accounting adjusted items) was employed to

predict bank failure (the proxy variable is bank capital adequacy ratio below 8%), and the lowest value (the accuracy

of the logistic model was 33.14%) when unadjusted EVA was employed to predict bank failure (the proxy variable is

bank Tier I capital ratio below 4%);EU banks had the highest value (the accuracy of the logistic model was 53.74%)

when unadjusted EVA was employed to predict bank failure (the proxy variable is bank capital adequacy ratio below

8%), and the lowest value (the accuracy of the logistic model was 35.01%) when the earnings before interest and

taxes compared to assets was employed to predict bank failure (the proxy variable is bank Tier I capital ratio below

4%);NIC banks had the highest value (the accuracy of the logistic model was 53.84%) when adjusted EVA (join

accounting adjusted items and economic deprecation adjusted items) was employed to predict bank failure (the proxy

variable is bank capital adequacy ratio below 8%), and the lowest value (the accuracy of the logistic model was

33.72%) when the earnings before interest and taxes compared to assets was employed to predict bank failure (the

proxy variable is bank Tier I capital ratio below 4%);G20 banks had the highest value (the accuracy of the logistic

model was 52.94%) when adjusted EVA (join accounting adjusted items and economic deprecation adjusted items)

was employed to predict bank failure (the proxy variable is bank capital adequacy ratio below 8%), and the lowest

value (the accuracy of the logistic model was 24.48%) when adjusted EVA was employed to predict bank failure (the

proxy variable is bank Tier I capital ratio below 4%).

Overall, compared with the other traditional financial ratios for all of the tested models, the empirical solutions

show that EVA is superior in predicting bank failure. These findings support Hypothesis 1. The EVA likely reflects

an enterprise’s real economic value and can be employed to prevent the inefficient management of funds (i.e., income

excess capital cost) to ensure that corporations do not waste resources. Thus, the accuracy of bank failure prediction

has been increased. Moreover, the EVA could be the optimal index for predicting bank failure in these countries. In

addition, a bank capital adequacy ratio less than 8%, Tier I capital ratio less than 4%, and nonperforming loan ratio

more than one third can be the optimal index for predicting bank failure in these countries.

Results from variance inflation factors to explain variables for correlation; the result lies between 1.425 and

1.847 (Variance Inflation Factors<10).There is no correlation problem. We repeat the same analyses out‐of‐sample to

tackle a possible sample specific issue and get general robust results10

,11

. Overall, the analysis of the prediction model

show that all measures of predictive ability, there are differences between eight models.

10In order to shorten the tables, we omit the solution

11We adopted 1 (in sample) to 1 (out of sample)

Asian Economic and Financial Review, 2016, 6(9): 522-533

529

© 2016 AESS Publications. All Rights Reserved.

Table-2. Descriptive statistics (%;Average Values)

NAFTA ASEAN EU NIC G20

tjCR , 172.52 148.55 117.85 123.68 124.17

tjEBITTA , 89.21 77.42 93.48 112.08 113.52

tjEBTE , 66.84 56.58 77.18 103.55 128.41

tjETA , 25.36 18.25 21.54 19.23 20.12

tjIED , 17.35 19.21 11.25 19.63 20.11

tjNETI , 102.58 99.31 85.26 91.15 103.25

tjDTA , 52.38 50.05 52.38 55.12 54.31

tjLTA , 44.21 43.34 47.31 43.12 47.31

jUAEVA 0.88 1.73 0.99 1.12 0.79

jAEVA 0.72 0.99 0.78 0.97 0.66

jEDAEVA 0.62 0.98 0.64 0.86 0.56

Samples 205 162 1135 132 245

Source: Authors investigation

Table-3. Performance Measures (Accuracy %)-One quarter before a failure

Bank failure: bank capital adequacy ratio less than 8%

Panel A NAFTA ASEAN EU NIC G20

tjCR ,

37.59 33.63 29.30 28.13 19.98

tjEBITTA , 33.66 34.28 32.57 30.19 20.09

tjEBTE , 28.31 28.93 31.69 29.92 25.66

tjETA , 29.78 30.54 34.45 33.38 29.26

jUAEVA 39.57 27.62 37.52 28.72 19.25

jAEVA 28.31 35.08 29.59 35.56 36.58

jEDAEVA 27.73 34.58 30.11 39.98 36.94

Panel B Bank failure: bank Tier I capital ratio less than 4%

tjCR , NAFTA ASEAN EU NIC G20

tjEBITTA , 35.94 32.96 28.16 27.68 19.49

tjEBTE , 32.25 32.16 31.23 29.25 19.51

tjETA , 27.23 27.81 30.68 28.74 24.74

jUAEVA 28.81 29.29 33.15 31.67 28.83

jAEVA 37.96 26.58 35.88 27.61 19.75

jEDAEVA 27.55 33.59 28.43 34.43 34.74

Panel C

Bank failure: bank nonperforming loan ratio more than one third

tjCR , 36.75 32.95 28.25 27.68 19.85

tjEBITTA , 32.98 33.34 31.93 29.65 19.96

tjEBTE , 27.85 28.44 31.92 29.39 25.65

tjETA , 29.46 29.95 33.74 32.84 28.76

jUAEVA 38.65 27.18 36.68 28.24 19.68

jAEVA 27.85 34.35 29.78 34.65 35.59

jEDAEVA 27.29 33.86 29.58 36.75 36.13

Source: Authors investigation

Asian Economic and Financial Review, 2016, 6(9): 522-533

530

© 2016 AESS Publications. All Rights Reserved.

Table-4. Performance Measures (Accuracy %)-Two quarters before a failure

Bank failure: bank capital adequacy ratio less than 8%

Panel A NAFTA ASEAN EU NIC G20

tjCR , 57.91 51.88 45.35 43.53 31.13

tjEBITTA , 51.92 52.48 50.27 46.66 31.48

tjEBTE , 43.81 44.73 48.93 46.23 39.76

tjETA , 46.35 47.12 53.13 50.97 45.24

jUAEVA 60.91 42.74 57.79 44.48 30.85

jAEVA 43.62 54.09 45.74 54.81 55.94

jEDAEVA 42.91 53.32 46.53 57.91 56.92

Panel B Bank failure: bank Tier I capital ratio less than 4%

tjCR , NAFTA ASEAN EU NIC G20

tjEBITTA , 50.64 45.46 39.85 38.34 27.76

tjEBTE , 45.55 45.98 44.09 41.01 27.92

tjETA , 38.57 39.37 42.95 40.65 35.13

jUAEVA 40.75 41.41 46.53 44.69 39.87

jAEVA 53.16 37.67 50.51 39.11 27.53

jEDAEVA 38.57 47.35 40.23 47.96 48.93

Panel C

Bank failure: bank nonperforming loan ratio more than one third

tjCR , 53.78 48.38 42.48 40.89 29.78

tjEBITTA , 48.42 48.92 46.94 43.73 29.94

tjEBTE , 41.14 41.97 45.74 43.32 37.52

tjETA , 43.43 44.12 49.54 47.57 42.43

jUAEVA 56.47 40.19 53.68 41.69 29.53

jAEVA 41.14 50.36 42.88 51.15 52.26

jEDAEVA 40.34 49.67 43.59 53.78 52.93

Source: Authors investigation

Table-5. Performance Measures (Accuracy %)-Three quarters before a failure

Bank failure: bank capital adequacy ratio less than 8%

Panel A NAFTA ASEAN EU NIC G20

tjCR ,

55.81 49.99 43.63 41.91 29.92

tjEBITTA , 50.33 50.57 48.43 44.94 30.96

tjEBTE , 42.76 43.77 47.13 44.53 38.27

tjETA , 44.64 45.39 51.19 49.11 43.57

jUAEVA 58.72 41.15 55.79 42.77 29.65

jAEVA 42.35 52.12 44.05 52.82 53.91

jEDAEVA 41.31 51.38 44.82 55.81 54.86

Panel B Bank failure: bank Tier I capital ratio less than 4%

tjCR , NAFTA ASEAN EU NIC G20

tjEBITTA , 50.74 45.57 39.93 38.44 27.75

tjEBTE , 45.61 46.09 44.19 41.09 27.97

tjETA , 38.63 39.43 43.45 40.73 35.17

Continue

Asian Economic and Financial Review, 2016, 6(9): 522-533

531

© 2016 AESS Publications. All Rights Reserved.

jUAEVA 40.83 41.49 46.65 44.83 39.87

jAEVA 53.33 37.73 50.65 39.16 27.52

jEDAEVA 38.63 47.47 40.34 48.09 49.06

Panel C

Bank failure: bank nonperforming loan ratio more than one third

tjCR , 48.25 43.43 38.15 36.73 26.79

tjEBITTA , 43.46 43.91 42.14 39.24 26.93

tjEBTE , 36.95 37.77 41.06 38.97 33.71

tjETA , 39.37 39.61 44.43 42.77 38.11

jUAEVA 50.67 36.18 48.17 37.44 26.57

jAEVA 36.47 45.25 38.59 45.78 46.68

jEDAEVA 36.24 44.58 39.14 48.25 47.47

Source: Authors investigation

Table-6. Performance Measures (Accuracy %) - Fourth quarters before a failure

Bank failure: bank capital adequacy ratio less than 8%

Panel A NAFTA ASEAN EU NIC G20

tjCR , 53.84 48.33 42.32 40.72 29.36

tjEBITTA , 48.38 48.89 46.86 43.56 29.52

tjEBTE , 40.72 41.83 45.64 43.17 37.26

tjETA , 43.28 43.99 49.48 47.51 42.27

jUAEVA 56.59 39.98 53.74 41.51 29.11

jAEVA 40.62 50.36 42.72 51.02 52.05

jEDAEVA 40.13 49.66 43.45 53.84 52.94

Panel B Bank failure: bank Tier I capital ratio less than 4%

tjCR , NAFTA ASEAN EU NIC G20

tjEBITTA , 44.25 39.81 35.01 33.72 24.67

tjEBTE , 39.84 40.24 38.63 36.29 24.89

tjETA , 33.91 34.59 37.66 35.69 30.97

jUAEVA 35.78 36.34 40.72 39.15 34.97

jAEVA 46.39 33.14 44.12 34.36 24.48

jEDAEVA 33.72 41.42 35.33 41.95 42.77

Panel C

Bank failure: bank nonperforming loan ratio more than one third

tjCR , 51.57 46.32 40.59 39.05 28.24

tjEBITTA , 46.36 46.85 44.92 41.77 28.45

tjEBTE , 40.32 40.09 43.75 41.41 35.77

tjETA , 41.55 42.18 47.41 45.53 40.54

jUAEVA 54.19 38.36 51.47 39.82 28.11

jAEVA 39.28 48.25 40.97 48.88 49.86

jEDAEVA 38.51 47.58 41.67 51.57 50.71

Source: Authors investigation

5. CONCLUSION

This study used data from 2003-2013, and used a logistic model to analyze the factors that influence financial

early warning systems in developing and developed countries. The results indicate that EVA is superior in predicting

Asian Economic and Financial Review, 2016, 6(9): 522-533

532

© 2016 AESS Publications. All Rights Reserved.

bank failure in NAFTA, ASEAN, EU, NIC, and G20 nations. The EVA likely reflects an enterprise’s real economic

value and can be employed to prevent the inefficient management of funds (i.e., income excess capital cost) to ensure

that corporations do not waste resources. Thus, the accuracy of bank failure prediction has been increased. Moreover,

the EVA could be the optimal index for predicting bank failure in these countries.

In this study, we adopted cut off points greater 0.5 to classify companies as bankrupt, and points below than 0.5

indicated successful companies. However, this value is frequently used and subjective and optimal cut off points

should be determined in future. This study demonstrated the determinants of bank failure in terms of various financial

factors. Therefore, future studies should examine all relevant factors or devise new theories that predict bank crises.

6. ACKNOWLEDGMENTS

This work has been supported by a grant from the Jiangsu Provincial Department of Education

Philosophy and Social Science Foundation (Project Number 2014SJB474).

REFERENCES

Adeyeye, P.O., O.D. Fajembola, M.O. Olopete and D.B. Adedeji, 2012. Predicting bank failure in Nigeria using principal

component analysis and D-score model. Research Journal of Finance and Accounting, 3(8): 159-170.

Al-Saleh, M.A. and A.M. Al-Kandari, 2012. Prediction of financial distress for commercial banks in Kuwait. World Review of

Business Research, 2(6): 26-45.

Anvarkhatibi, S., R. Mohammadi and J. Mohammadi, 2013. Investigation of the effect of the value added, earning quality and

leverage ratio on bankruptcy in organizations accepted in Tehran’s stock market. Journal of Natural and Social Sciences,

2(2): 223-229.

Canicio, D. and K. Blessing, 2014. Determinants of bank failures in multiple-currency regime in Zimbabwe (2009–2012).

International Journal of Economics and Finance, 6(8): 229-246.

Cox, R.A.K. and G.W.Y. Wang, 2014. Predicting the US bank failure: A discriminant analysis. Economic Analysis and Policy,

44(2): 202-211.

Distinguin, I., A. Tarazi and J. Trinidad, 2011. The use of accounting and stock market data to predict bank financial distress: The

case of East Asian banks. Philippine Management Review, 18: 1-18.

Ecer, F., 2013. Comparing the bank failure prediction performance of neural networks and support vector machines: The Turkish

case. Ekonomska Istrazivanja-Economic Research, 26(3): 81-98.

Fungacova, Z. and L. Weill, 2013. Does competition influence bank failures? Evidence from Russia. Economics of Transition,

21(2): 301-322.

Huang, D.T., B. Chang and Z.C. Liu, 2012. Bank failure prediction models: For the developing and developed countries. Quality

and Quantity, 46(2): 553-558.

Huang, D.T. and Z.C. Liu, 2010. Board composition and corporate value in Taiwan high technology firms. International Journal of

Organizational Innovation, 2(4): 126-138.

Ioannidis, C., F. Pasiouras and C. Zopounidis, 2010. Assessing bank soundness with classification techniques. Omega, 38(5): 345-

357.

Jayadev, M., 2006. Predictive power of financial risk factors: An empirical analysis of default companies. Vikalpa, 31(3): 45-56.

Kiefer, M.V., 2014. Bank failures and mergers in Turkey: 1992-2014. International Journal of Finance and Banking, 1(3): 45-64.

Kim, M.J., D.K. Kang and H.B. Kim, 2015. Geometric mean based boosting algorithm with over-sampling to resolve data

imbalance problem for bankruptcy prediction. Expert Systems with Applications, 42(3): 1074-1082.

Klecka, J. and H. Scholleova, 2010. Bankruptcy models enuntiation for Czech glass making firms. Economics and Management,

15: 954-959.

Asian Economic and Financial Review, 2016, 6(9): 522-533

533

© 2016 AESS Publications. All Rights Reserved.

Li, G., L.W. Sanning and S. Shaffer, 2011. Forecasting bank failures: Timeliness versus number of failures. Applied Economics

Letters, 18(16): 1549-1552.

Lin, S.L., 2010. A two-stage logistic regression-ANN model for the prediction of distress banks: Evidence from 11 emerging

countries. African Journal of Business Management, 4(14): 3149-3168.

Lopez, I.F.J. and S.I. Pastor, 2015. Bankruptcy visualization and prediction using neural networks: A study of U.S. commercial

banks. Expert Systems with Applications, 42(6): 2857-2869.

Maghyereh, A.I. and B. Awartani, 2014. Bank distress prediction: Empirical evidence from the gulf cooperation council countries.

Research in International Business and Finance, 30(1): 126-147.

Martin, A., V. Gayathri, G. Saranya and P.V. Gayathri, 2011. A hybrid model for bankruptcy prediction using genetic algorithm,

fuzzy c-means and mars. International Journal on Soft Computing, 2(1): 12-24.

Öğüt, H., M.M. Doğanay, N.B. Ceylan and R. Aktaş, 2012. Prediction of bank financial strength ratings: The case of Turkey.

Economic Modelling, 29(3): 632-640.

Pasaribu, R.B., 2008. Financial distress prediction in indonesia stock exchange case study of trade industry public company.

Journal of Economics Business and Accounting, 11(2): 153-172.

Pradhan, R., K.K. Pathak and V.P. Singh, 2013. Bankruptcy prediction and neural networks clubbed for Z score analysis of

oriental bank of commerce. International Journal of Research in Computer Engineering and Electronics, 2(1): 1-6.

Rappaport, A., 1995. Creating shareholder value: The new standard for business n performance. New York: The Free Press.

Ravisankar, P. and V. Rav, 2010. Financial distress prediction in banks using group method of data handling neural network,

counter propagation neural network and fuzzy artmap. Knowledge Based Systems, 23(8): 823-831.

Serrano-Cinca, C., 2013. Gutiérrez-Nieto, B. Partial least square discriminant analysis for bankruptcy prediction. Decision Support

Systems, 54(3): 1245-1255.

Shkurti, R. and B. Duraj, 2010. The assessment of the financial soundness of the banking sectors in Balkan countries using early

warning indicators- a comparative study with policy implications. CEA Journal of Economics, 5(1): 33-48.

Stewart, G.B., 1991. The quest for value. New York: Harper Business.

Teker, D., S. Teker and M. Sönmez, 2011. Economic value added performances of publicly owned banks: Evidence from Turkey.

International Research Journal of Finance and Economics, 75: 132-138.

Timo, S. and I. Virtanen, 2001. Economic value added: A simulation analysis of the trendy, owner-oriented management tool.

Acta Wasaensia(90).

Trussel, J. and L. Johnson, 2012. A parsimonious and predictive model of the recent bank failures. Academy of Banking Studies

Journal, 11(1): 15-31.

Valahzaghard, M.K. and M. Bahrami, 2013. Prediction of default probability in banking industry using camels index: A case study

of Iranian banks. Management Science Letters, 3(4): 1113-1118.

Wanke, P., C.P. Barros and J.R. Faria, 2015. Financial distress drivers in Brazilian banks: A dynamic slacks approach. European

Journal of Operational Research, 240(1): 258-268.

Yildiz, B. and S. Akkoc, 2010. Bankruptcy prediction using Neuro fuzzy: An application in Turkish banks. International Research

Journal of Finance and Economics, 60: 114-126.

Zaghdoudi, T., 2013. Bank failure prediction with logistic regression. International Journal of Economics and Financial Issues,

3(2): 537-543.

Views and opinions expressed in this article are the views and opinions of the authors, Asian Economic and Financial Review shall not be

responsible or answerable for any loss, damage or liability etc. caused in relation to/arising out of the use of the content.