Bank Credit Instrument

25

Bank Credit Instruments FINBANK

-

Upload

joyce-dimaano -

Category

Documents

-

view

225 -

download

4

description

nn not mine tho. not claiming this

Transcript of Bank Credit Instrument

Bank Credit Instruments

FINBANK

What is Credit Instrument?

• Documents describing details of credit and debit• Provide a written means from future reference

describing terms and conditions of any debit and loan

• May be an order for payment of money to a specified person or it may be a promise to pay the loan

• Cheques, bills of exchange, bank overdraft, etc.

Negotiability of Credit Instruments

• When treating credit instruments, it should be borne in mind that not all are negotiable instruments.

• Qualifications of Credit Instruments– It must be in writing and signed by the drawer or

maker.– It must be made payable to order or to bearer.– It must be payable on demand or at a future

determinable time.– There must be an unconditional order or promise to

pay.

General Division of Credit Instruments

• Promises to Pay• Orders to Pay

Promises to Pay

• Promissory Note– Simplest form of credit instrument– An unconditional promise of the maker to pay a

sum certain in money to order or to bearer on demand at a future determinable time.

– Collateral promissory note – the note is secured

Promises to Pay

• Bank Note– Unconditional promise of a bank to pay a sum

certain in money on demand. – Used as a substitute for money and is exchanged

in standard money at par, provided that the bank issuing it enjoys excellent credit standing

– A direct obligation of the issuing bank

Promises to Pay

• Bank’s Acceptance– Contains the bank’s promise to pay a draft that is

presented to it for acceptance– The word “ACCEPTED” is stamped on the face of

the draft and it is duly signed by the bank’s representative.

– The date of acceptance is also indicated.

Promises to Pay

• Letter of Credit– A promise of a bank to honor drafts drawn against

it or for its account.– A bank substitutes its credit for that of the

accredited buyer and promises to pay the beneficiary or his representative upon presentation of a draft, subject to the conditions in the letter of credit.

Bank Notes Distinguished from Standard Money

• Practically like money• Represents private bank rather than the state’s credit• All appearances and the intent of usage, it resembles

money closely.• In some instances, the note is declared as legal

tender either fully or limited scale.• Fiduciary in nature and their circulation is dependent

upon the credit of the issuing bank

Bank Notes Distinguished from Standard Money

• Desirable characteristics of money are also found in bank notes.

• Necessitate final redemption into standard money• Represents the government notes• Issue is limited to the extend of lawful restrictions on

the issuing bank’s capital as well as the trust and confidence the public has on it.

Bank Notes Distinguished from Deposits

• The circulation of bank notes and deposits necessitates legal reserves.

• Bank notes circulates longer while check drawn against deposits could immediately be presented for payment when endorsed.

• When writing a check: any amount covered by existing deposits may be drawn (except in overdrafts); in bank notes, there are uniform denominations.

• Deposits necessitate the use of checks to circulate them; bank notes constitute the means of payment.

Bank Notes Distinguished from Deposits

• In case of deposits, the bank becomes a debtor to the depositor or the note holder.

• Where a check is endorsed for negotiation, a bank note is passed on to the next holder without documentation.

• In the issue of checks, an aggrieved party has the right of recourse against endorsers except in some instances.

• In case of bank notes, there is no such right of recovery.

Orders to Pay

• Bill of Exchange– An order of one person/ bank to another person

or bank to pay a third person a sum certain in money or demand or at some specified future time.

– Also in the form of a check or a draft.

Orders to Pay

• Check– An order of a depositor to his bank to pay a third person or

himself a sum certain in money on demand.– Commonly known as personal check.– Cashier’s check – bank’s cashier is the drawer of the check– Manager’s check – Manager of a business concern is the

drawer

Orders to Pay

• NOW Account– Negotiable Order of Withdrawal– Earn interest and account holders can write as many NOW

checks as they want on the account– Has a feature of a savings deposit as it earns interest– Like current/ checking account – it offers depositors the

convenience od issuing checks for payments.– No need for a passbook in depositing or withdrawing

Orders to Pay

• Draft– Order to pay and is a bill of exchange

– Classification• Demand drafts – paid as sight upon presentation• Time drafts – payable at future determinable time• Commercial or trade draft – when the draft is drawn by

a merchant against another• Bank draft – Drawn by a bank against another bank

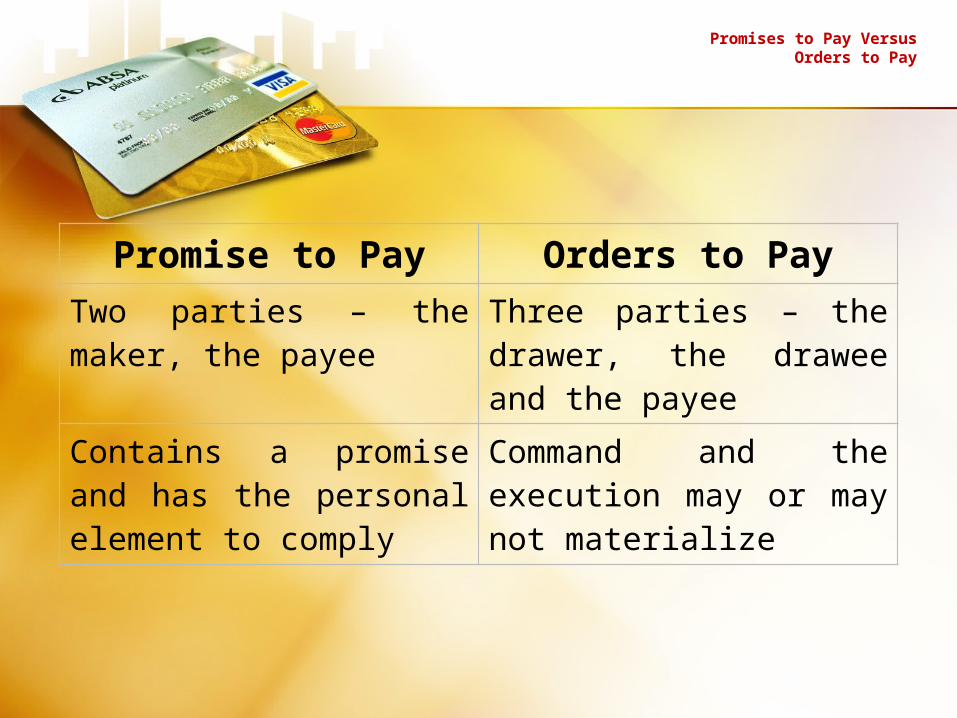

Promises to Pay Versus Orders to Pay

Promise to Pay Orders to PayTwo parties – the maker, the payee

Three parties – the drawer, the drawee and the payee

Contains a promise and has the personal element to comply

Command and the execution may or may not materialize

Checks and Drafts Distinguished

• Both are bills of exchange since both are negotiable instrument

• Three parties involve in a check or in a draftChecks Drafts

Drawn against deposit Orders to payPayable on demand Payable either on demand or at

a future determinable timeSubject to certification Subject to acceptanceDrawn on bank Drawn on a merchant or a bank

Money Market Instruments

• Treasury Bills– Short-term securities issued by country's Treasury– Reduce a bank’s ability to lend to its clients leading to a

contraction of the money supply.– Consists of an obligation to pay the bearer the face value

of the bill upon a given date.– Bill is tradable

Money Market Instruments

• Banker’s Acceptance / Letter of Credit –Have their origin in trade bills issued by

merchants– Important money market instrument– Time draft and accepted by a bank

Money Market Instruments

• Negotiable Certificate of Deposit (NCD)– Like fixed deposits except they are bearer

documents–Offer a market related rate if interest are

completely liquid because they can be negotiated during the term of the deposit.

Money Market Instruments

• Commercial Paper (CP)– Short term CP is a debt instrument

commonly issued by corporations to fund a temporary capital requirement.–Usually matures within 1 year

Money Market Instruments

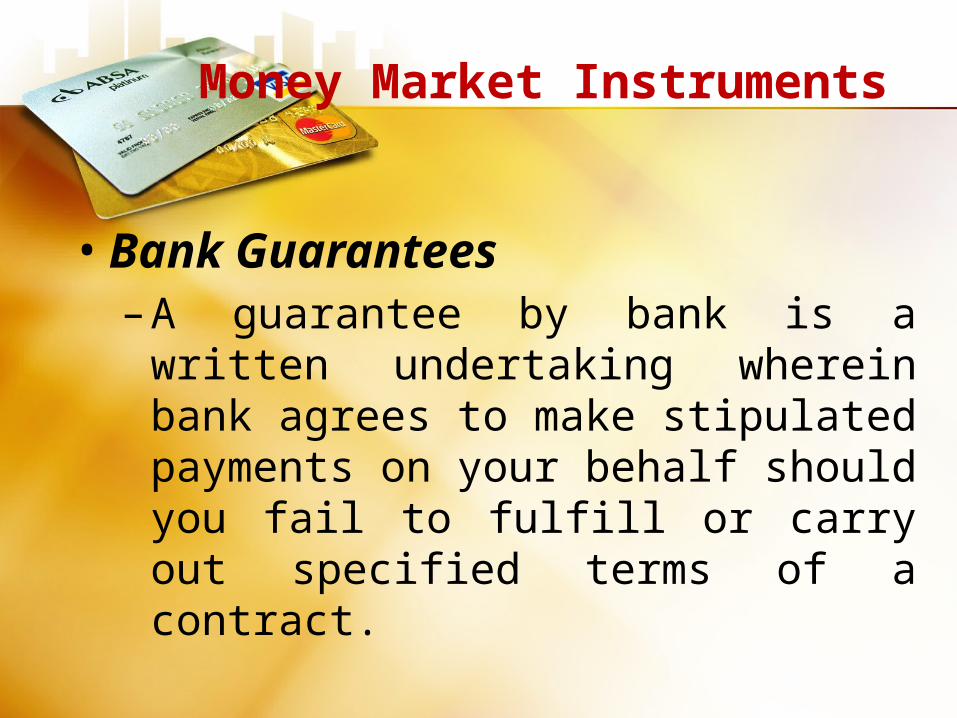

• Bank Guarantees–A guarantee by bank is a written

undertaking wherein bank agrees to make stipulated payments on your behalf should you fail to fulfill or carry out specified terms of a contract.

Significance of Bank Credit Instruments

• Facilitate to the dealings in credit• Bring out losses on the part of the bank• Public confidence in the soundness of

banks and their patronages of the banking system as a whole shall be strengthened.

• Timothy Bunyi• Niña Floralde

• Maria Jana Minela Ilustre• Kathrina Pateña• Mariecon Robles