BANGLADESH - finclusion.orgfinclusion.org/uploads/file/reports/2016 Data at a Glance...

27

BANGLADESH December 2016 QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork completed in September 2016

Transcript of BANGLADESH - finclusion.orgfinclusion.org/uploads/file/reports/2016 Data at a Glance...

BANGLADESH

December 2016

QUICKSIGHTS REPORT

FOURTH ANNUAL FII TRACKER

SURVEYFieldwork completed in September 2016

Access – Access to a bank account or mobile money account means an

individual can use bank/mobile money services either via their own

account or via an account of another person.

Active account holder – An individual who has a registered account and

has used it in the last 90 days.

Active user – An individual who has used any financial services account

for any type of transaction in the past 90 days via his/her own account or

somebody else’s account.

Adults with DFS access – Adults (15+) who either own a DFS account

or have access to someone else’s account.

Advanced use of DFS – Advanced use of digital financial services

includes activities beyond basic cash-in/cash-out and person-to-person

transfers (e.g., savings, bill pay, investment, insurance, etc.).

Below the poverty line – In this particular study, adults living on less

than $2.50 per day, as classified by the Grameen PPI.

Cooperative – Typically, a business or other professional organization

that is owned and run jointly by its members, who share the profits or

benefits. Cooperatives can release some of the profits/funds as loans to

its members.

Digital financial services (DFS) – Financial services provided through

an electronic platform (mobile phones, electronic cards, the internet,

etc.).

Dormant accounts –Registered accounts that have never been used or

that have not been active (e.g., used in the past 90 days).

Grameen Progress out of Poverty Index (PPI) – A poverty

measurement tool from the Grameen Foundation wherein a set of

country-specific questions are used to compute the likelihood that a

household is living below the poverty line.

Informal lending or saving group – These are informal financial

services offered by individuals or groups at the community level. These

services are a part of the NBFI group of services, but do not offer a full

suite of financial services and, therefore, are not a part of formal finance.

Microfinance institution (MFI) – An organization that offers financial

services to low-income populations. Almost all give loans to their

members, and many offer insurance, deposit and other services.

Mobile financial service (MFS) or mobile money (MM) – A service

in which a mobile phone is used to access financial services.

Nonbank financial institution (NBFI) – A financial organization that

is not formally licensed as a bank or a mobile money provider, but whose

activities are regulated, at least to some extent, by the central bank within

the country. Such financial institutions include microfinance institutions

(MFI), cooperatives, Post Office Banks and savings and credit

cooperatives (SACCOs).

Post Office (Savings) Bank – A bank that has branches at local post

offices.

Registered active user – A person with a registered account that has

used it in the last 90 days.

Services beyond basic wallet – DFS transactions that go beyond

simple deposits, withdrawals or money transfers.

Unregistered/over-the-counter (OTC) user – An individual who has

used a financial service through someone else’s account, including an

agent’s account or the account of a family member or a neighbor.

Urban/rural – Urban and rural persons are defined according to their

residence in urban or rural areas as prescribed by the national bureau of

statistics.

BANGLADESH

2

Key definitions

Country context

BANGLADESH

• Bangladesh is going through a period of high economic growth, which is expected to continue in the near future.o The GDP growth rate averaged 6.5 percent over the past five years; the GDP growth rate in 2016 was the highest in the past decade at 7.05

percent.

• Bangladesh Bank, the central bank of Bangladesh, maintained a strong focus on financial inclusion in 2016. o The Bangladesh Bank successfully enacted a number of financial inclusion initiatives despite a major institutional setback in March 2016 when

hackers stole millions from the central bank, which resulted in the resignation of the then-governor.

o References to inclusive finance in the Bangladesh Bank’s 7th Five Year Plan FY2016-2020 and the Strategic Plan (2015-2019) indicate the

importance of financial inclusion as a primary goal.

o In July 2015, a dedicated Financial Inclusion Department was established within the Bangladesh Bank. The aim of the department is to “further

consolidate and better coordinate the financial inclusion initiatives in the central bank and of other public and private sector stakeholder […].”

o Draft Regulatory Guidelines for Mobile Financial Services released in August 2015 are yet to be finalized. These included limited ownership

stakes in mobile financial service providers to 15 percent per entity, and a requirement that at least four banks must form a consortium to achieve

a 51 percent majority-ownership share.

o In an attempt to stop the use of mobile phones for criminal activities, the Bangladesh Telecommunication Regulatory Commission announced a

mandatory “mobile phone SIM reregistration” campaign to increase biometric identification of SIM card holders. Immediately after the

reregistration deadline of May 2016, all unregistered SIM cards were permanently deactivated without any prior notice. This deactivation may

have played a role in reducing mobile phone sharing and borrowing, as individuals are less likely to share SIM cards registered in their names. It

also had an effect on increasing overall SIM card ownership.

• With respect to digital finance, according to Bangladesh Bank statistics, as of October 2016 there were more than 13.8 million

active MFS accounts and approximately 39 million registered MFS accounts.o Bangladesh Bank statistics measure the number of accounts, not the number of individuals as is the case with FII data. Both reflect a clear

growth in the mobile money market and suggest that a substantial minority of the population is utilizing the services.

o Based on the central bank’s supply side statistics, active account use grew in 2016, which closely mirrors the FII growth in active mobile money

account holders (from 8 percent of adult Bangladeshis in 2015 to 10 percent in 2016).

o The agent network in Bangladesh has continued to expand, from fewer than 400,000 agents in May 2014 to 671,300 in October 2016.*

o Despite the large number of mobile money providers, bKash remains the clear market leader, trailed by DBBL, in visibility and customer base.

Many licensed providers have yet to make any impression on the market.

Source: InterMedia Bangladesh FII Tracker survey Wave 4 (N=6,000, 15+), August-September 2016. 3*https://www.bb.org.bd/fnansys/paymentsys/mfsdata.php **http://www.tradingeconomics.com/bangladesh/gdp-growth

BANGLADESH

• Mobile money continues to see strong growth in Bangladesh, whereas the prevalence of

nonbank financial institution (NBFI) accounts dropped significantly, primarily due to a decline

in the use of microfinance institution (MFI) accounts.

o In 2015, mobile money access surpassed NBFI access (33 percent vs. 26 percent) but mobile money

registration (9 percent) remained lower than NBFI registration (24 percent).

o In 2016, NBFI access decreased by 10 percentage points to 16 percent, vs. 2015. At the same time, mobile

money access increased by 7 percentage points, from 33 percent in 2015 to 40 percent in 2016.

o For the first time in the four years of FII research, there are more mobile money registered accounts than

NBFI registered accounts, although the number of registered bank accounts still surpasses that of either

mobile money or NBFI accounts. However, registered mobile money accounts and active use grew between

2015 and 2016 (9 to 13 percent, and 8 to 10 percent, respectively), whereas bank account registration slightly

declined.

• Access and registered use of MFIs dropped from 2015, resulting in an overall decline in financial

inclusion numbers.

o The percentage of adults having access to full service MFIs dropped from 23 percent in 2015 to 14 percent in

2016, with the decline in access higher in rural areas, males, and individuals living below the poverty line.

o A likely explanation is that MFI loans, a primary use of MFIs, are historically used as “insurance credit” (i.e.,

individuals seek out MFI loans in times of economic uncertainty and downturns). However, along with the

recent surge in economic growth, with an average GDP growth of 6.5 percent between 2014 and 2016, there

may have been a simultaneous decline in the demand for loans. This is likely the reason for the drop in MFI

usage.

o This is reflected in the decrease in MFI account holder borrowing, which dropped from 19 percent in 2015

to 6 percent in 2016.

34%

are

financially

included

12% have a

full-service NBFI

account

17% have a

full-service bank

account

13% have a

registered mobile

money account

2016: Financial Inclusion*(Shown: Percentage of Bangladeshi adults,

N=6,000)

*Financial inclusion is defined as the percentage of individuals with a registered bank, mobile money or NBFI account. Overlap representing

those who have multiple kinds of financial accounts is not shown.

Source: InterMedia Bangladesh FII Tracker survey Wave 4 (N=6,000, 15+), August-September 2016.4

Notable statistics

12

17

13

34

24

19

9

43

20

18

5

37

0

18

3

20

Nonbank financialinstitution

Bank

Mobile money

Any financial service

2013 (N=6,000) 2014 (N=6,000) 2015 (N=6,000) 2016 (N=6,000)

9

13

10

27

19

13

8

34

16

12

4

28

0

12

3

14

Nonbank financialinstitution

Bank

Mobile money

Any financial service

16

19

40

55

26

20

33

58

22

19

23

49

20

22

35

Nonbank financialinstitution

Bank

Mobile money

Any financial service

BANGLADESH

Financial account access Registered financial service users(Shown: Percentage of Bangladeshi adults for each year)

Active* financial service users

NBFIs were not included in 2013 survey. Types of account ownership are not mutually exclusive. *A registered account used in the last 90 days.

NANA NA

Source: InterMedia Bangladesh FII Tracker surveys Wave 1 (N=6,000, 15+), September-November 2013; Wave 2 (N=6,000, 15+), June-August 2014; Wave 3

(N=6,000, 15+), August-September 2015; Wave 4 (N=6,000, 15+), August-September 2016. 5

Registered mobile money account use and ownership increased; NBFI access and

registration contracted considerably, decreasing overall registered financial service use

from 2015

BANGLADESH

Survey Summary

• Annual, nationally representative survey (N=6,000) of Bangladeshi adults aged 15+

• Face-to-face interviews lasting, on average, 73 minutes

• Fourth survey (Wave 4) conducted from 8/5/2016 to 9/4/2016

• Tracks trends and market developments in DFS based on the information gathered in the first survey, conducted in 2013, second survey, conducted in 2014, and third survey, conducted in 2015

Data Collection

• Basic demographics and poverty measurement (Grameen Progress Out of Poverty Index)

• Access/use of mobile devices

• Access/use of mobile money

• Access/use of formal financial services (e.g., bank accounts)

• Access/use of semi-formal and informal financial services (e.g., MFIs, cooperatives, village savings groups)

• Financial literacy and preparedness

• General financial behaviors

6

FII Bangladesh Tracker Survey details

Source: InterMedia Bangladesh FII Tracker survey Wave 4 (N=6,000, 15+), August-September 2016.

BANGLADESH

Figures are weighted to reflect national census data demographics.

Source: InterMedia Bangladesh FII Tracker survey Wave 4 (N=6,000, 15+), August-September 2016.

% of survey % of survey

Gender Age

Male 51% 15-24 31%

Female 49% 25-34 26%

Geography 35-44 19%

Urban 32% 45-54 12%

Rural 68% 55+ 12%

Income Aptitude

Above the $2.50/day poverty line 24% Basic literacy 58%

Below the $2.50/day poverty line 76% Basic numeracy 98%

7

Survey demographics

BANGLADESH

Have a full-service NBFI account

Have a full-service bank account**

Have a registered

mobile money account

17%

12%

13%

To be considered

financially included,

individuals must have

accounts with institutions

offering financial services

beyond credit. Some

banks and many NBFIs

only offer credit services to

their customers.

*Overlap representing those who have multiple kinds of financial accounts is not shown.

**Throughout this report, bank account holders have accounts at full-service institutions, unless otherwise noted.

Source: InterMedia Bangladesh FII Tracker survey Wave 4 (N=6,000, 15+), August-September 2016.

34%Financially

included*

8

Just over one in three Bangladeshis are financially included, largely

through bank and mobile money use

BANGLADESH

More than six in 10 Bangladeshis own mobile phones but few have registered

mobile money accounts; very few have completed the customer journey to

monthly active use of advanced services

*Phone owners

2016: Distribution of Bangladeshi mobile phone owners at each major step in the customer

journey for mobile money, and conversion rate between steps(Shown: Percentage of Bangladeshi adults, N=6,000)

Source: InterMedia Bangladesh FII Tracker survey Wave 4 (N=6,000, 15+), August-September 2016.9

62%

Mobile phone

ownership

1%12% 10% 8%33%

.13.80.83.36.53

.19

Advanced active

registered use

(30 days)*

Registration* Active

registered use

(90 days)*

Active

registered use

(30 days)*

Trial/access*

.10

N/A

16

19

40

55

26

20

33

58

22

19

23

49

20

22

35

Nonbank financial institution

Bank

Mobile money

Any financial service

2013 (N=6,000) 2014 (N=6,000) 2015 (N=6,000) 2016 (N=6,000)

BANGLADESH

Access to financial services(Shown: Percentage of Bangladeshi adults for each year)

Access to financial services declined vs. 2015, driven in large part by a

contraction in NBFI access; mobile money access grew by 7 percentage points

Types of accounts are not mutually exclusive.

Source: InterMedia Bangladesh FII Tracker surveys Wave 1 (N=6,000, 15+), September-November 2013; Wave 2 (N=6,000, 15+), June-August 2014; Wave 3

(N=6,000, 15+), August-September 2015; Wave 4 (N=6,000, 15+), August-September 2016. 10

N/A

BANGLADESH

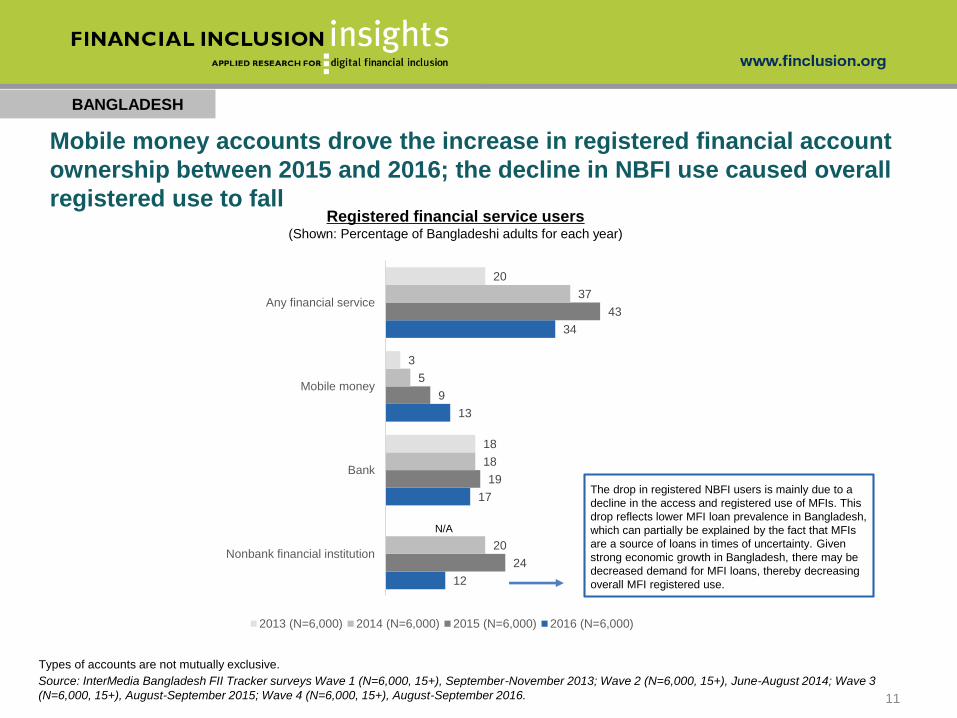

11

Registered financial service users(Shown: Percentage of Bangladeshi adults for each year)

Types of accounts are not mutually exclusive.

12

17

13

34

24

19

9

43

20

18

5

37

18

3

20

Nonbank financial institution

Bank

Mobile money

Any financial service

2013 (N=6,000) 2014 (N=6,000) 2015 (N=6,000) 2016 (N=6,000)

Source: InterMedia Bangladesh FII Tracker surveys Wave 1 (N=6,000, 15+), September-November 2013; Wave 2 (N=6,000, 15+), June-August 2014; Wave 3

(N=6,000, 15+), August-September 2015; Wave 4 (N=6,000, 15+), August-September 2016.

Mobile money accounts drove the increase in registered financial account

ownership between 2015 and 2016; the decline in NBFI use caused overall

registered use to fall

The drop in registered NBFI users is mainly due to a

decline in the access and registered use of MFIs. This

drop reflects lower MFI loan prevalence in Bangladesh,

which can partially be explained by the fact that MFIs

are a source of loans in times of uncertainty. Given

strong economic growth in Bangladesh, there may be

decreased demand for MFI loans, thereby decreasing

overall MFI registered use.

9

13

10

27

19

13

8

34

16

12

4

28

12

3

14

Nonbank financial institution

Bank

Mobile money

Any financial service

2013 (N=6,000) 2014 (N=6,000) 2015 (N=6,000) 2016 (N=6,000)

BANGLADESH

Active financial account holders(Shown: Percentage of Bangladeshi adults)

Types of accounts are not mutually exclusive.

Active financial account holders(Shown: Percentage of registered users for each type of account, by year)

Inferring

few

dormant

accounts

Source: InterMedia Bangladesh FII Tracker surveys Wave 1 (N=6,000, 15+), September-November 2013; Wave 2 (N=6,000, 15+), June-August 2014; Wave 3

(N=6,000, 15+), August-September 2015; Wave 4 (N=6,000, 15+), August-September 2016.

NA

12

77

74

80

79

80

71

86

80

81

63

83

77

65

81

68

2013 2014 2015 2016

NA

Eight in 10 mobile money account holders use their accounts actively,

which is a greater proportion than bank or MFI account holders

85 7872

69

91 8784

75

9

1316 20

2 0 1 3 ( N = 7 5 8 ) 2 0 1 4 ( N = 7 1 6 ) 2 0 1 5 ( N = 8 3 9 ) 2 0 1 6 ( N = 7 9 8 )

Basic activities only (CICO and account management)

Basic activities or P2P only

At least one advanced activity

72

55

24

66

9793

8681

2

713 13

2 0 1 3 ( N = 1 4 1 ) 2 0 1 4 ( N = 2 2 5 ) 2 0 1 5 ( N = 4 0 0 ) 2 0 1 6 ( N = 5 4 9 )

Basic activities only (CICO and account management)

Basic activities or P2P only

At least one advanced activity

BANGLADESH

Bank uses, by type(Shown: Percentage of active bank account holders)

Due to the changes in the questionnaire some data points may not be directly comparable across years. Obtaining airtime through mobile money is no

longer considered an advanced activity.

Mobile money uses, by type(Shown: Percentage of active mobile money account holders)

Source: InterMedia Bangladesh FII Tracker surveys Wave 1 (N=6,000, 15+), September-November 2013; Wave 2 (N=6,000, 15+), June-August 2014; Wave 3

(N=6,000, 15+), August-September 2015; Wave 4 (N=6,000, 15+), August-September 2016. 13

More active mobile money users are using basic account activities only

9

9

10

13

19

17

24

7

5

8

10

15

15

20

10

11

10

9

7

7

7

23

22

24

27

32

31

39

Below poverty line (n=4,622)

Females (n=3,277)

Rural (n=4,016)

Total population (N=6,000)

Urban (n=1,984)

Males (n=2,723)

Above poverty line (n=1,378)

Active bank account holders Active mobile money account holders Active NBFI account holders All active financial account holders

BANGLADESH

Types of accounts are not mutually exclusive.

Source: InterMedia Bangladesh FII Tracker survey Wave 4 (N=6,000, 15+), August-September 2016.

2016: Active account usage by demographic(Shown: Percentage of each subgroup)

Largest gap in

active financial

account

holdings

14

Differences in active use of financial accounts are most pronounced across

the gender and above/below poverty line demographic groups

9-point

gender

gap

BANGLADESH

15

Source: InterMedia Bangladesh FII Tracker survey Wave 4 (N=6,000, 15+), August-September 2016.

2016: Proximity to points-of-service (POS) for financial institutions(Shown: Percentage of Bangladeshi adults, N=6,000)

69

53 53

18

28

19

13

26

16 15 1722

33

20

13

25

3 4 5

12

1815

7 912

2825

48

21

45

67

40

Any POS Retail store withover-the-counter MM

kiosk

MM Agent Banking Agent Bank Branch ATM Informalsaving/lending group

MFI

Less than 1 km from home 1-5 kms from home More than 5 kms from home Don't know

A total of 64% of adults know of an MM kiosk

or agent within 1 km of their homes Nearly half of all adults do not

know of any ATM nearby

Compared to bank branches and ATMs, more consumers know of mobile

money agents within one kilometer of where they live

BANGLADESH

2016: Key indicators of preparedness for digital financial services (Shown: Percentage of Bangladeshi adults, N=6,000)

2015 37% 64% 40% 98% 99% 96%

2014 31% 61% 62% 92% 93% 97%

2013 18% 58% 59% 84% 91% 95%

85%

Have access to

a mobile phone

31%

Ever send/receive

text messages

98%

Have basic

numeracy

98%

Have the

necessary ID*

59%

Own a

SIM card

62%

Own a

mobile phone

Source: InterMedia Bangladesh FII Tracker surveys Wave 1 (N=6,000, 15+), September-November 2013; Wave 2 (N=6,000, 15+), June-August 2014; Wave 3

(N=6,000, 15+), August-September 2015; Wave 4 (N=6,000, 15+), August-September 2016.

Access to mobile phones fell

due to a decline in phone

borrowing. This may have been

brought on by the SIM

reregistration campaign, which

permanently deactivated all

unregistered SIM cards.

16

Lack of mobile phone competency, seen in the low usage of text messages,

is a key challenge to overcome for increasing digital financial services use

The increase in SIM card ownership* from

2015 to 2016 reflects the effectiveness of the

government’s reregistration campaign,

requiring all unregistered SIM cards to be

registered by the May 2016 deadline.

*SIM card ownership is defined as having a SIM card registered in one’s own name.

91%

aware

2014 (N=6,000)

Conversion from awareness of mobile money providers* to mobile money use(Shown: Percentage of Bangladeshi adults for each year)

2015 (N=6,000) 2016 (N=6,000)

MM OTC use, 28%

MM registered

users, 13%

0.25

conversion

rate

0.36

conversion

rate

40% use

mobile

money**

0.44

conversion

rate

*Aware of at least one mobile money provider. **Adds to 40 percent because dormant accounts (0.6 percent) are excluded.

.

BANGLADESH

17

92%

aware91%

aware

Source: InterMedia Bangladesh FII Tracker surveys Wave 2 (N=6,000, 15+), June-August 2014; Wave 3 (N=6,000, 15+), August-September 2015; Wave 4

(N=6,000, 15+), August-September 2016.

MM OTC use, 24%

MM registered users, 9%

33% use

mobile

money

MM OTC use, 18%

MM registered users, 5%

23% use

mobile

money

Awareness of mobile money providers remains high; the conversion rate

from awareness to access grew year on year

BANGLADESH

18

Demographic trends for active registered mobile money account use (Shown: Percentage of Bangladeshi adults who fall into each category*)

*Categories are not mutually exclusive.

Demographic trends for all registered mobile money account use (Shown: Percentage of Bangladeshi adults who fall into each category*)

36

1

53

63

58

2

8

4

9

4

9

13

4

13

7

16

7

13

19

6

17

10

23

10

Total population Males Females Urban Rural Above poverty line Below poverty line2013 2014 2015 2016

The largest increases in registered account holders and active registered

mobile money use were seen among males, urban and above-poverty

populations

Source: InterMedia Bangladesh FII Tracker surveys Wave 1 (N=6,000, 15+), September-November 2013; Wave 2 (N=6,000, 15+), June-August 2014; Wave 3

(N=6,000, 15+), August-September 2015; Wave 4 (N=6,000, 15+), August-September 2016.

35

0.94

25

24

7

1

63

7

3

8

12

4

12

6

14

6

10

15

5

15

8

20

7

Total population Males Females Urban Rural Above poverty line Below poverty line2013 2014 2015 2016

0.8

0.8

1

2

2

3

3

5

Make MM transfers

Transfer money to savings/lendinggroup

Receive government payments

Receive wages

Pay for goods at store

Save/set aside money

Loan activities

Bill pay

BANGLADESH

2015 (n=400)

Advanced mobile money (MM) account uses(Shown: Percentage of active mobile money account holders, n=549)

Due to the changes in the questionnaire some data points may not be directly comparable across years. Obtaining airtime through mobile money

is no longer considered an advanced activity.

13%of active mobile

money account

holders have used at

least one advanced

mobile money

function

(vs. 13% in 2015,

7% in 2014,

and 2% in 2013)

2

2

0.5

1

0.0

3

19

Bill pay, loan activities and saving remain the primary advanced uses of

mobile money among active users

Source: InterMedia Bangladesh FII Tracker surveys Wave 1 (N=6,000, 15+), September-November 2013; Wave 2 (N=6,000, 15+), June-August 2014; Wave 3

(N=6,000, 15+), August-September 2015; Wave 4 (N=6,000, 15+), August-September 2016.

4

0.9

0.5

0.7

0.2

0.4

17

93

0

0.5

0

0

17

91

0.7

0

0.5

0.4

18

89

0

0

0

0.7

28

86

Mobi Cash

U Cash

M Pay

M Cash

DBBL

bKash

2013 (n=141) 2014 (n=225) 2015 (n=400) 2016 (n=549)

BANGLADESH

Active mobile-money account holders can have accounts with more than one provider.

Source: InterMedia Bangladesh FII Tracker surveys Wave 1 (N=6,000, 15+), September-November 2013; Wave 2 (N=6,000, 15+), June-August 2014; Wave 3

(N=6,000, 15+), August-September 2015; Wave 4 (N=6,000, 15+), August-September 2016.

Active mobile-money provider account holdings (Shown: Percentage of active mobile-money account holders who report using selected providers, by year)

20

bKash continues to dominate the market while other providers’ influence

wanes

Question allowed for multiple responses.

Source: InterMedia Bangladesh FII Tracker survey Wave 4 (N=6,000, 15+), August-September 2016.

2016:Top reasons active account holders

start to use mobile money (Shown: Percentage of active mobile money account holders, n=549)

2

3

43

44

Somebody requested I open anaccount

I wanted a safe place tokeep/store money

I had to send money to anotherperson

I had to receive money fromanother person

2016: Top uses of mobile money services

among active account holders(Shown: Percentage of active mobile money account holders, n=549)

16

17

42

63

86

Receive money from another person

Send money to another person

Buy airtime top-ups

Deposit money

Withdraw money

BANGLADESH

21

P2P drives initial use, withdrawing and depositing become the main

reasons for active use

BANGLADESH

70%

30%

Reason for not signing up for mobile money(Shown: Percentage of OTC users, n=1,658)

%

I don’t need to, I don’t make any transactions 31

I can have all the services I need through an agent 14

Using an account is difficult 11

I don’t have a state ID or other required documents 9

I prefer that agents perform transactions for me 7

I don’t see additional advantages to registration over

OTC6

I don’t have enough money to make transactions with

using such an account5

Source: InterMedia Bangladesh FII Tracker survey Wave 4 (N=6,000, 15+), August-September 2016.

2016: Mobile money use: registered vs. OTC(Shown: Percentage of mobile money users, n=2,314)

Registered OTC

The majority of mobile money users continue to access services over-the-

counter using agents to meet their needs

22

1

1

1

1

2

3

4

5

5

6

Pay/receive money to/from asavings/lending group

Made insurance related payments

Pay for large acquisitions

Loan activity

Receive G2P payments

Make bank to other financialinstitution transfer

Save/set aside money

Receive wages

Bought airtime top-ups

Bill pay

BANGLADESH

2015 (n=839)

5

2016: Advanced bank account uses(Shown: Percentage of active bank account holders, n=798)

20%of active bank

account holders have

used at least one

advanced banking

feature

(vs. 16% in 2015,

13% in 2014,

and 9% in 2013)

3

4

2

2

4

1

0

23

The proportion of active bank account holders using their accounts for

advanced purposes is growing

Source: InterMedia Bangladesh FII Tracker surveys Wave 1 (N=6,000, 15+), September-November 2013; Wave 2 (N=6,000, 15+), June-August 2014; Wave 3

(N=6,000, 15+), August-September 2015; Wave 4 (N=6,000, 15+), August-September 2016.

0.4

0.6

BANGLADESH

2016: Nonbank financial institution usage

(Shown: Percentage of Bangladeshi adults, N=6,000)

0.6

0.1

*

*

2015

2016

Source: InterMedia Bangladesh FII Tracker survey Wave 4 (N=6,000, 15+), August-September 2016.

*Base numbers too small to report for OTC use.

Active accounts OTC use

While the use of microfinance institutions still dominates the NBFI sector, the

percentage of active MFI account holders dropped significantly in 2016 vs. 2015

24

0.1

0.1

*

*

2015

2016

2

1

2015

2016

17

8

2

3

2015

2016

Village saving

groups

Post Office Bank

Cooperatives

Microfinance

institutions

BANGLADESH

2016: Microfinance institution usage

(Shown: Percentage of Bangladeshi adults, N=6,000)

2016: Use of microfinance institution accounts*

(Shown: Percentage of microfinance account holders, n=663)

14%

86%

0.5

1

2

3

3

6

6

87

Insurance

Pay for goods at grocery store, etc.

P2P payments

Pay bills

Save/set aside money

Loans

Large acquisitions

Deposit/withdraw

A decline in those taking

MFI loans might reflect the

relatively stable economic

growth conditions in

Bangladesh, since many of

these loans are used as

“insurance” in times of

economic instability.

*Question allowed for multiple responses.

Nonusers of full-

service MFIs

Ever used full-

service MFIs

Source: InterMedia Bangladesh FII Tracker survey Wave 4 (N=6,000, 15+), August-September 2016.

MFI use is primarily driven by deposits and withdrawals; only six percent of

MFI account holders took loans in 2016 vs. 19 percent in 2015

25

BANGLADESH

Digital stored-value accounts: accounts in which a monetary value is represented in a digital electronic format and can be retrieved/transferred by the account

owner remotely. For this particular study, DSVAs include a bank account or NBFI account with digital access (a card, online access or a mobile phone

application) and a mobile money account.

Source: InterMedia Bangladesh FII Tracker surveys Wave 3 (N=6,000, 15+), August-September 2015; Wave 4 (N=6,000, 15+), August-September 2016.

Main FSP Indicator

2015 2016

Base Definition% %

Base n Base n

Adults (15+) who have active digital stored-value accounts15% 15%

All adults6,000 6,000

Poor adults (15+) who have active digital stored-value accounts11% 11%

All poor4,597 4,622

Poor women (15+) who have active digital stored-value accounts8% 7%

All poor females2,546 2,599

Rural women (15+ ) who have active digital stored-value accounts 7% 6%

All rural females2,129 2,179

Adults (15+) who have active digital stored-value accounts and use them to access

other financial services (beyond basic wallet, P2P and bill pay)

2% 2%All adults

6,000 6,000

Poor adults (15+) who have active digital stored-value accounts and use them to

access other financial services (beyond basic wallet, P2P and bill pay)

1% 1%All poor

4,597 4,622

Poor women (15+) who have active digital stored-value accounts and use them to

access other financial services (beyond basic wallet, P2P and bill pay)

1% 0.5%All rural females

2,546 2,599

Rural women (15+) who have active digital stored-value accounts and use them to

access other financial services (beyond basic wallet, P2P and bill pay)

1% 0.4%All poor females

2,129 2,179

26

Digital stored-value account ownership and the use of these accounts for

more advanced functions is static with 2015