Three Q Recruitment All Ireland Marketing Awards Presentation

B&Q UK & Ireland Investor Event

21st October 2014

1

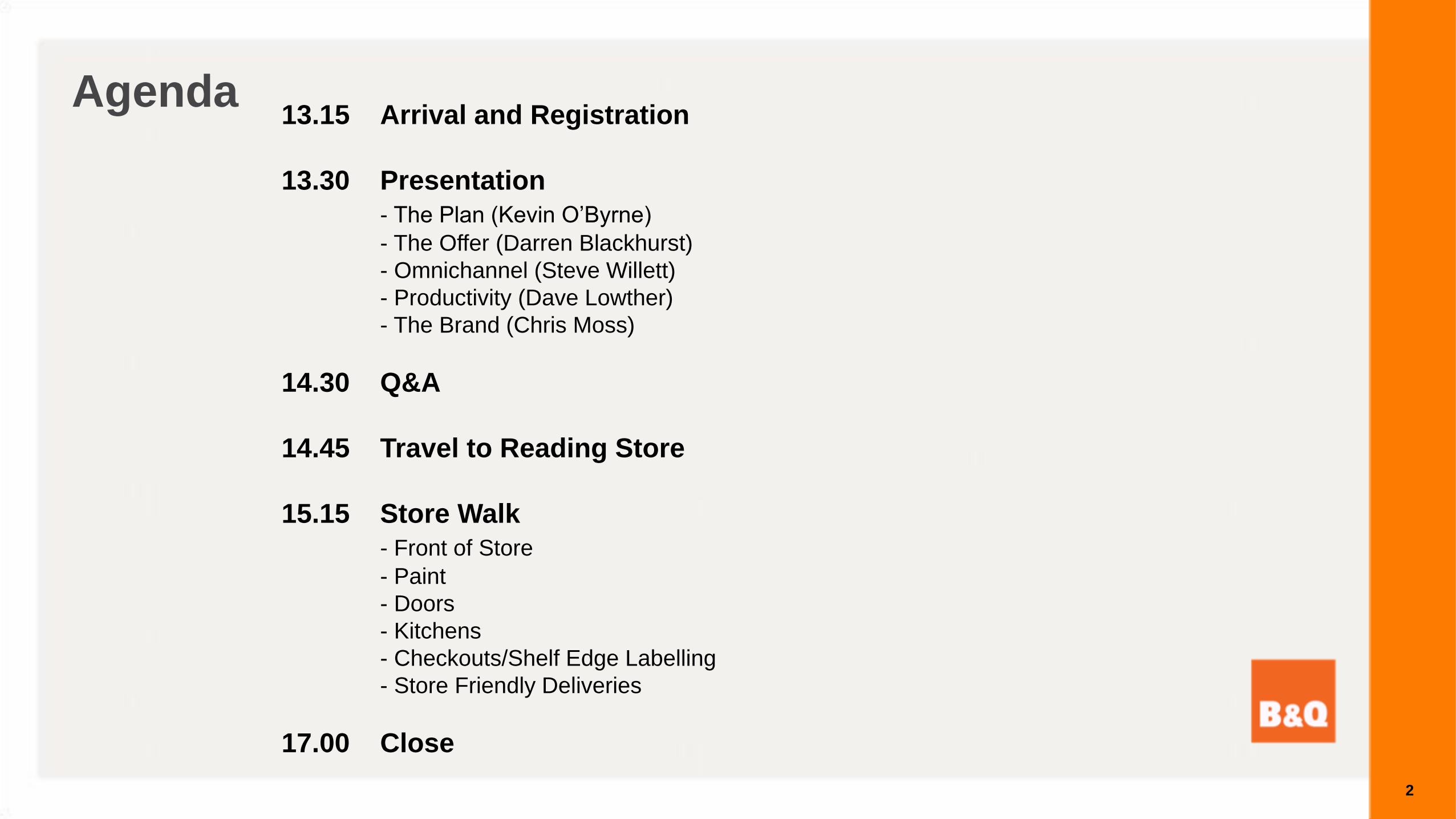

Agenda13.15 Arrival and Registration

13.30 Presentation

- The Plan (Kevin O’Byrne)

- The Offer (Darren Blackhurst)

- Omnichannel (Steve Willett)

- Productivity (Dave Lowther)

- The Brand (Chris Moss)

14.30 Q&A

14.45 Travel to Reading Store

15.15 Store Walk

- Front of Store

- Paint

- Doors

- Kitchens

- Checkouts/Shelf Edge Labelling

- Store Friendly Deliveries

17.00 Close

2

The Team

Christian Mazauric

Finance

Chris Moss

Customer & Marketing

Dave Lowther

Logistics & IT

Damian McGloughlin

Retail

Darren Blackhurst

Commercial

Guy Eccles

Human Resources

Grahame Smith

PropertySteve Willett

Strategy & Productivity

3

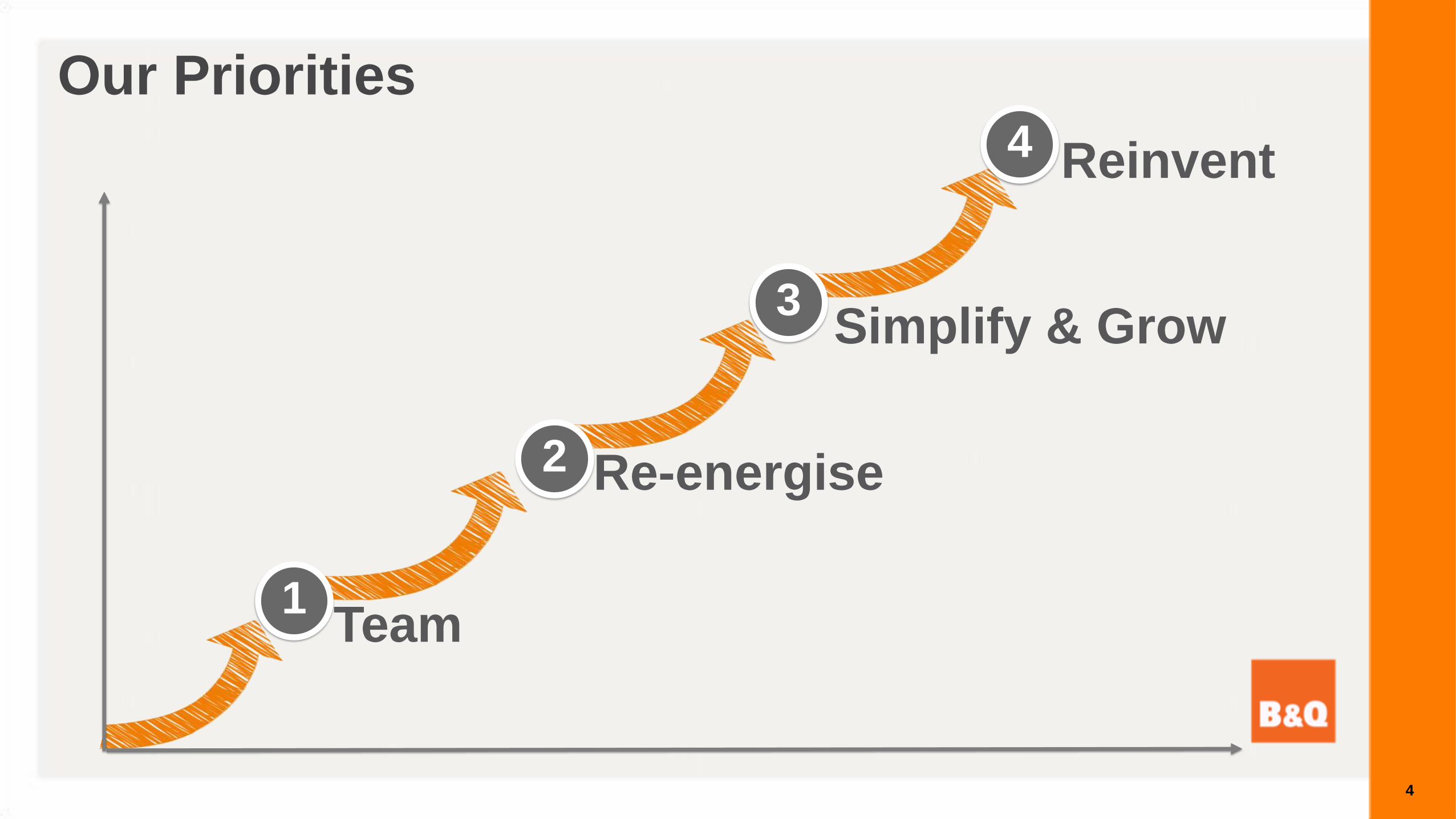

Reinvent4

Simplify & Grow3

Re-energise2

Team1

Our Priorities

4

Great value

Stock volume

Take away today

One stop shop for projects

Knowledgeable, helpful staff

Best of stores:

‘Old Retail’

Click and Collect

Broader complementary

online ranges

Better online content

Digital: ‘New Retail’

Our ambition is to Reinvent home improvement retailing for the digital age

5

We have detailed plans to Simplify & Grow B&Q over the medium term

6

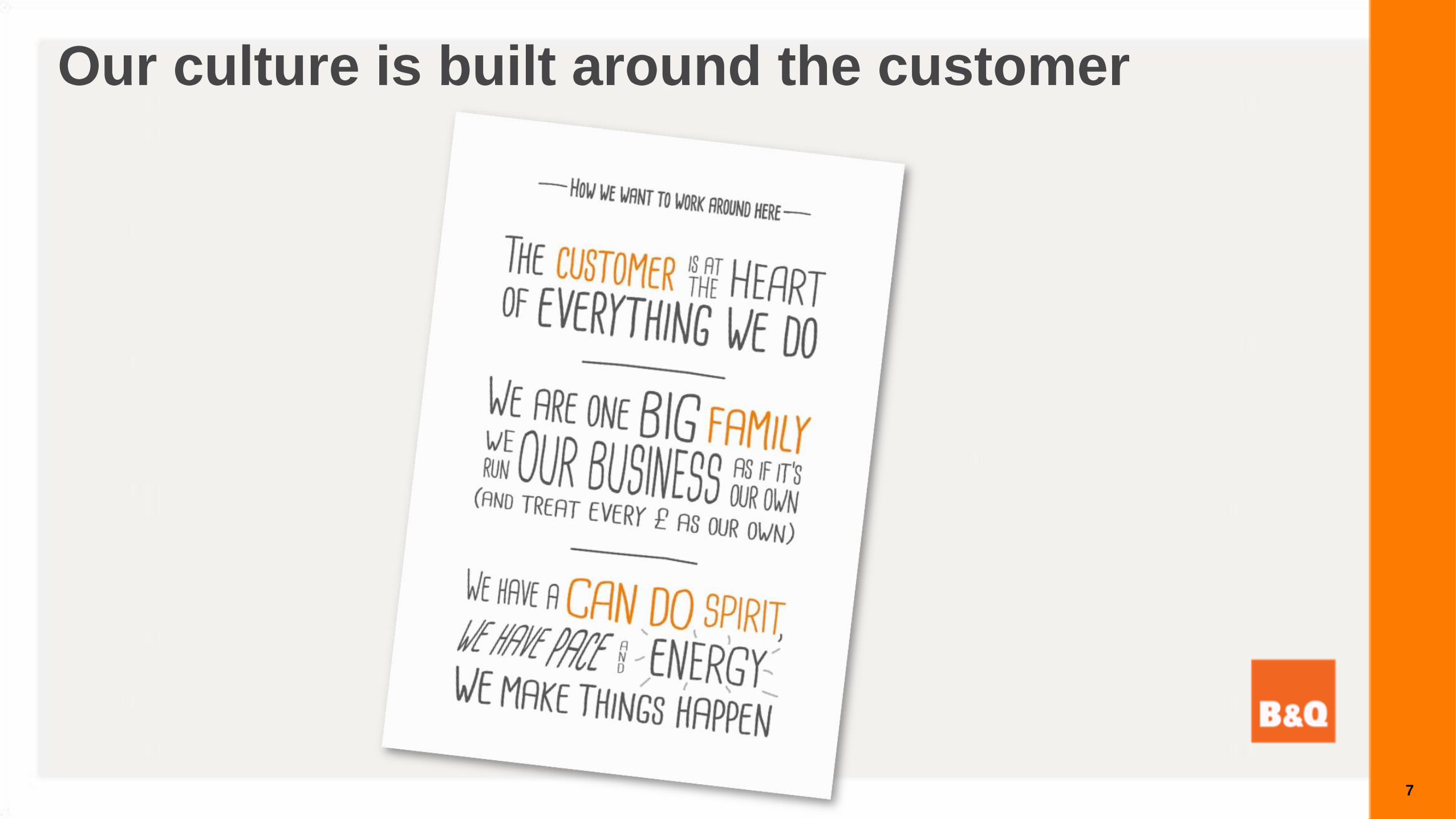

Our culture is built around the customer

7

OfferDarren Blackhurst

8

Everyday Great Value is key to our offer

EDGV

Price

ServiceDifferentiated

Product9

Not making the most of our volume opportunity…

Price: Where we were…

Hiding behind claims…

…and confusing customers

Need to be more competitive…

10

We’re OUT of claims...

We’ve moved from this…

…to this

11

We’re investing in price…

We have invested in over 3,500 prices in first 6 months

Was £1.45

Now £1.17

Was £3.48

Now £3.00

Was £5.00

Now £4.00

Was £3.48

Now £3.00

Was £4.98

Now £4.23

Was £7.98

Now £5.00

12

The Top 50 and Doorbusters have been a success…

5%

6%

7%

8%

9%

10%

11%

T50 basket participation

In over

1 in 10

Customer baskets

+35%

volume

Now

£1m

per week

13

…and customers are noticing the difference…

Perception data shows we’re closing the gap to discounters…

…and growing our advantage over big box rivals

15

20

25

30

35

31-A

ug-1

3

14-S

ep-1

3

28-S

ep-1

3

12-O

ct-

13

26-O

ct-

13

09-N

ov-1

3

23-N

ov-1

3

07-D

ec-1

3

21-D

ec-1

3

04-J

an

-14

18-J

an

-14

01-F

eb-1

4

15-F

eb-1

4

01-M

ar-

14

15-M

ar-

14

29-M

ar-

14

12-A

pr-

14

26-A

pr-

14

10-M

ay-1

4

24-M

ay-1

4

07-J

un

-14

21-J

un

-14

05-J

ul-

14

19-J

ul-

14

02-A

ug-1

4

16-A

ug-1

4

30-A

ug-1

4

ASDA B&Q Wilkinson

0

5

10

15

20

25

30

35

31-A

ug-1

3

14-S

ep-1

3

28-S

ep-1

3

12-O

ct-

13

26-O

ct-

13

09-N

ov-1

3

23-N

ov-1

3

07-D

ec-1

3

21-D

ec-1

3

04-J

an

-14

18-J

an

-14

01-F

eb-1

4

15-F

eb-1

4

01-M

ar-

14

15-M

ar-

14

29-M

ar-

14

12-A

pr-

14

26-A

pr-

14

10-M

ay-1

4

24-M

ay-1

4

07-J

un

-14

21-J

un

-14

05-J

ul-

14

19-J

ul-

14

02-A

ug-1

4

16-A

ug-1

4

30-A

ug-1

4

B&Q Homebase Tesco Wickes

Price Index vs. B&Q (100)

104

121

87

87

102

94

90

+ 2pts

+ 4pts

+ 1pt

+ 12pts

Flat

+ 2pts

+ 2pts

Improvement in 2014

our price position is improving…

14

2) Need to focus on

newness and differentiation

1) Store ranges are too big

Differentiated Product: The need for change

3) Quality is inconsistent

15

We’ve created a clear plan to drive growth

Reduce

Range

Duplication

Differentiate

and Grow

Online

More Space

for Core

Ranges

Sell More

to More

Customers

Grow

Volumes

Lower

Prices

Maximise

efficiency

Lower

Costs

Virtuous

circle of

growth

Right

Offer

16

…transforming major sections of the store

6 Trial Stores

What we’ve done so far…

5 Product Areas

We’ve built new principles…

17

We have a 3 year roll out plan in place

18

OmnichannelSteve Willett

19

101% year on year growth in H1 (+£17m )

From £23m to £65m+ in 18 months

Focus on doing basics well

Our online business is growing at pace driven

by focus on core basics…

20

But still massive opportunity for us in future by

focusing on 3 key areas...

Support Offer Click & CollectNew Online

Ranges

Improve the core Broaden the reach Increase the offer

Range

Rationalisation

in store

supported by

extended

ranges on line

Introduction

and evolution

of click &

collect offering

Complimentary

extensions of

on line range

Extension of

existing & new

21

First implementation of group platform, utilising up to date

technology stack with fully responsive design

100% live since 21st Sept, customer feedback positive and

already performing better than old site

New web site live on new group platform…

22

First key priority supporting the offer

programme…

Range rationalisation in store

supported by extension of

online offer

Click & Collect enables

extension of ranges across the

estate

Customer choice is improved

In StoreSKUs

From c.300 to c.70 in store

500+ online

Volume& Choice

23

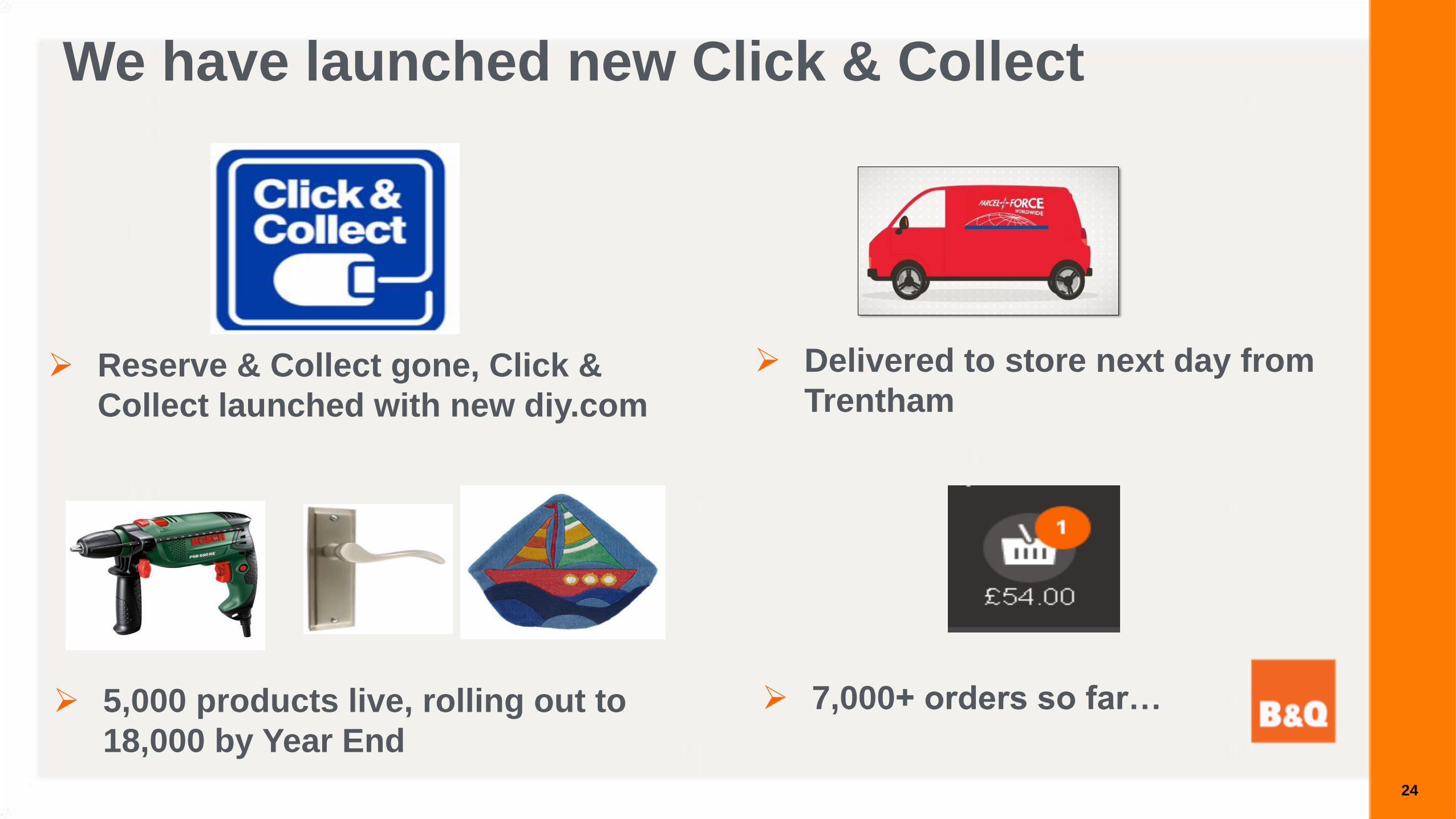

Reserve & Collect gone, Click &

Collect launched with new diy.com

We have launched new Click & Collect

Delivered to store next day from

Trentham

5,000 products live, rolling out to

18,000 by Year End

7,000+ orders so far…

24

Click & Collect will evolve over next 2 years…

Next Day

Promise

Mix of Same

Day

Next Day

Promise

Mostly

Same Day

Promise

c18,000 Sku’s c25,000 Sku’s c35,000 Sku’s

25

Next priority delivering complementary

extensions of online range…

Extended current ranges to

improve customer choice

Introduce new ranges that

enhance our overall offer

26

ProductivityDave Lowther

27

The productivity programme is cross functional and end to end

Range &

Replenishment Distribution

NetworkIn Store Processes Labour Scheduling

• The programme is embedding a low cost by design mindset

• 70 projects have been identified

• Implementation is designed to last

28

We’ve already made good progress

• Cash office optimisation:

• Store own delivery vans: • Southern network solution:

• TradePoint deployment model: • Fleet optimisation:

29

There’s more to come…

• 4 key projects to roll out to all stores starting Q4 2014/15:

4. Roller Checkouts2. Outsourced Returns 3. Store Friendly Deliveries1. Labour Scheduling

30

Customer and Marketing

Chris Moss

31

The customer is at the core of our business

32

Unleashing the brand

33

“The Home Improvement Warehouse for the Digital Age”

34

Reading Store Visit

John Musticone

Store Manager – Reading

35

After

Kitchens

The Solution

1) Price message moving away from claims and yo-yo

pricing

2) Focus on Cooke and Lewis as a brand

3) Launched Spaces and a new suite of selling tools

in-store

The Opportunity

1) Promotional strategy confusing for customers and

unsustainable

2) Not maximising the opportunity around the quality of

our products

3) In-store service model time consuming and

inconsistent

Before

36

Store Friendly Deliveries

The Solution

1) a) Crates are segregated in the Distribution Centre;

b) a lean in store process to standardise

replenishment model in all stores.

2) a) New delivery calendars to smooth stock volumes

and reduce a day from the lead time; b) Visibility report

giving stores 2 weeks notice on what’s being

delivered.

3) New in-store equipment to optimise the

effectiveness of the replenishment process

The Opportunity

1) Up to 50% of our stock is delivered in mixed cages

and tote boxes which creates inefficiency

2) There is variance in daily delivery volumes and little

visibility of what’s being delivered

3) The replenishment equipment is not optimised

After

Before

Cleaning2Lighting1

Batteries

3

Motoring4

5 Electrical

37

Internal Doors

The Solution

1) Online home delivery proposition launched June 2013

2) Volume layflat implemented to allow greater volume of best

sellers and implementation of direct sourcing strategy

3) Proposed store space change

• Rationalised range more than 50% of products listed

online only for home delivery

• Redesigned to simplify customer selection and allow

greater shelf capacity to support sales.

4) Simplified price hierarchy: 250+ price points to 35 price points

5) New promotional mechanics focusing on volume product at

market beating prices

The Opportunity

1) Large store range and footprint delivering insufficient

return on space

2) The size of the existing in store range does not

allow the right volume of product on the shelf

3) The merchandising and large footprint make the offer

confusing for customers to shop

After

Before

38

The Opportunity

In-Store Labelling

The Solution

g

1) Labour intensive method of pricing in-store

2) High frequency of damaged or missing labels

3) Lack of colleague information to aid replenishment

and stock management

4) Limited promotional impact

Label format and design:

1) Improved label design,

font and product

description

2) Use of helpful icons for

customers and colleagues

Roller CheckoutsThe Opportunity

1) Checkouts are difficult for customers to shop

2) Checkouts are difficult for colleagues to use

3) Design leads to scanning and database inaccuracy

The Solution

With rollers and

flatbed scanners,

accuracy of

scanned items

increases

Easier customer

experience and

faster

transaction

speed

Improved scanning

accuracy supports

a more stable

database

Use of data strips:

1) Cleaner, easier

implementation of price

changes

2) Clarity for customer on

products that are on promotion

1) 2) 3)

39

Volume Ends

The Solution

1) Ends are now set up with single products, in volume

and located in high footfall locations

2) All prices are now authoritative and competitor

checked

3) Cross functional sign off process ensures the right

products are selected in the right volume

4) Best selling products more prominently located

and volumes are up

The Opportunity

1) Ends were not set up to drive volume

2) Prices were not always authoritative

3) Internal process for determining ends was

inconsistent

4) Not enough focus on best selling products

After

Before

40

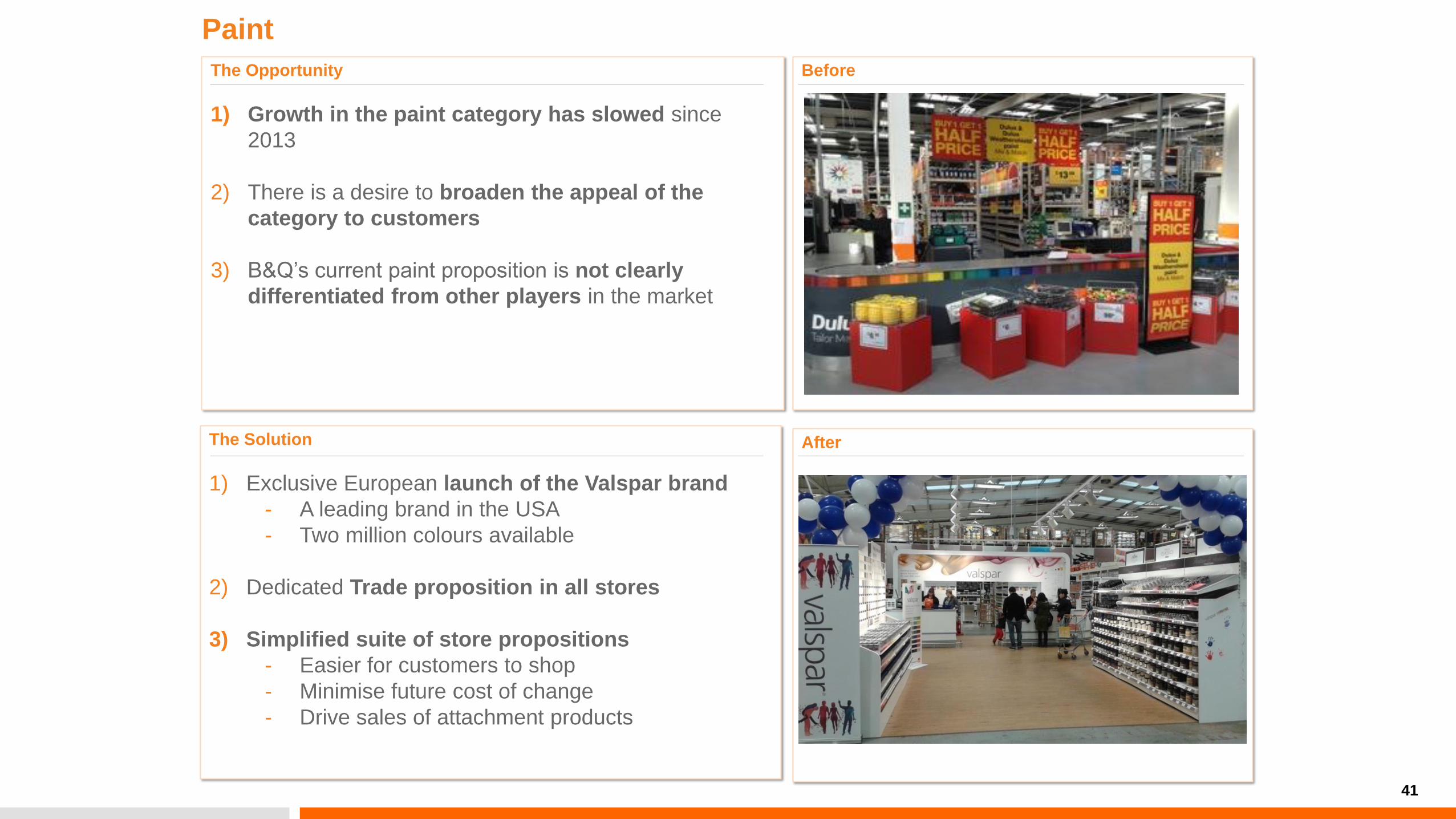

Paint

The Solution

1) Exclusive European launch of the Valspar brand

- A leading brand in the USA

- Two million colours available

2) Dedicated Trade proposition in all stores

3) Simplified suite of store propositions

- Easier for customers to shop

- Minimise future cost of change

- Drive sales of attachment products

The Opportunity

1) Growth in the paint category has slowed since

2013

2) There is a desire to broaden the appeal of the

category to customers

3) B&Q’s current paint proposition is not clearly

differentiated from other players in the market

After

Before

41

Appendix

42

B&Q UK & Ireland Board

Kevin O’Byrne

2013 to date CEO B&Q UK & Ireland

2012 - 2013 Kingfisher plc - Divisional CEO China, Turkey, UK, Germany

(Hornbach Board, Deputy Chairman Koctas)

2008 - 2012 Kingfisher plc – Group Finance Director

2002 - 2008 Dixon Retail plc – Group Finance Director and Head of

Computing Division (PC World & PC City)

1995 - 2002 Quaker Oats (now Pepsi) – European Finance Director

1987 - 1995 Arthur Anderson – Turnaround Consulting

43

2012 to date B&Q UK & Ireland, Finance Director,

2001 - 2012 Castorama

Finance, Supply Chain and IT Director

1995 – 2001 Marks & Spencer

Business Performance Director,

Continental Europe

Christian Mazauric Chris Moss

2013 to date B&Q UK & Ireland, Customer & Marketing Director

2010 - 2012 Truphone, Chief Brand and Marketing Officer

2002 - 2010 118118 and 118218

2002 to 2005 CEO, UK

2005 to 2007 Chief Brand Officer, Europe

2007 to 2010 Chief Brand Office, Group (based in NY)

2000 - 2001 ICO Global Communications, Director of Marketing

1995 - 1998 Lloyds TSB, brands director

1993 - 1994 Orange PCS, Director of Marketing and Brand

1985 - 1993 Virgin Atlantic Airways, Marketing Director

B&Q UK & Ireland Board

44

B&Q UK & Ireland Board

2011 to date B&Q UK & Ireland, Retail Operations

Director

2009 - 2011 B&Q UK & Ireland, Director of Store

Operations & Retail Change

2004 - 2009 B&Q UK & Ireland, Division Director

1999 - 2004 B&Q UK & Ireland, Regional Manager

1986 - 1999 B&Q UK & Ireland, Store Management

Roles

Damian McGloughlinDarren Blackhurst

2014 to date B&Q UK & Ireland, Commercial Director

2011 - 2013 Matalan, CEO

2006 - 2010 Asda Board CMO (Group Trading Director)

2002 - 2005 Tesco Lotus Thailand, Commercial Director

1997 - 2002 Tesco, Category Director

1994 - 1997 Tesco, secondment to ETS Catteau (France)

1988 - 1994 Tesco, Buyer / Buying Controller

45

B&Q UK & Ireland Board

Steve Willett

2012 to date Kingfisher plc: CEO Group Productivity &

Development

B&Q UK & Ireland: Strategy;

Screwfix: Chairman

2009 – 2012 Kingfisher plc: Chief Executive of UK Trade

2005 – 2009 Screwfix, CEO

1999 – 2005 B&Q UK & Ireland, Board Director

Dave Lowther

2013 to date B&Q UK & Ireland, Logistics and IT Director

2006 - 2013 Screwfix Operations Services Director

1999 - 2006 B&Q UK & Ireland, Director of Logistics

1995 - 1999 Tibbett & Britten, Divisional Operations Director

1978 - 1998 AAH Logistics, Nabisco, Imperial Tobacco

46

B&Q UK & Ireland Board

2014 to date B&Q UK & Ireland, HR Director

2005 - 2014 Screwfix, HR Director

1997 - 2005 B&Q UK & Ireland, Director of HR

1992 - 1997 National Power, HR Director

Guy Eccles

2014 to date B&Q UK & Ireland, Property Director

2013 - 2014 Carphone Warehouse, Group Property, Formats

and Business Change Director

2010 - 2013 Carphone Warehouse, Group Property Director

2007 – 2010 Mothercare, Director of Property

1999 – 2007 Arcadia, Director of Property

Grahame Smith

47