BALLARAT TOURISM MARKETING STRATEGY

163

BALLARAT TOURISM MARKETING STRATEGY October 1995 This a true cop•; of th d M; . , f I · · · !l amen :nent approved by the •• ru.ster Ol' p ruiuJnu fl:nd l.Ot::ill Government on 1 5 OCT 1996 Lt.>.igh Phillips Co-ordim..itor Amendment Services Office of P!annmg and Heritage Department of lnfrastmcture

Transcript of BALLARAT TOURISM MARKETING STRATEGY

BALLARAT TOURISM

MARKETING STRATEGY

October 1995

This i~ a true cop•; of th d M; . , f I · · · !l amen :nent approved by the •• ru.ster Ol' p ruiuJnu fl:nd l.Ot::ill Government on

1 5 OCT 1996 ~~ Lt.>.igh Phillips Co-ordim..itor Amendment Services

Office of P!annmg and Heritage Department of lnfrastmcture

EXECUTIVE SUMMARY

BALLARAT

Readers seeking a short summary should read the SWOT analysis on

pages 114 -119 and refer to the Strategy Overview after page 123.

•:. ,· ..

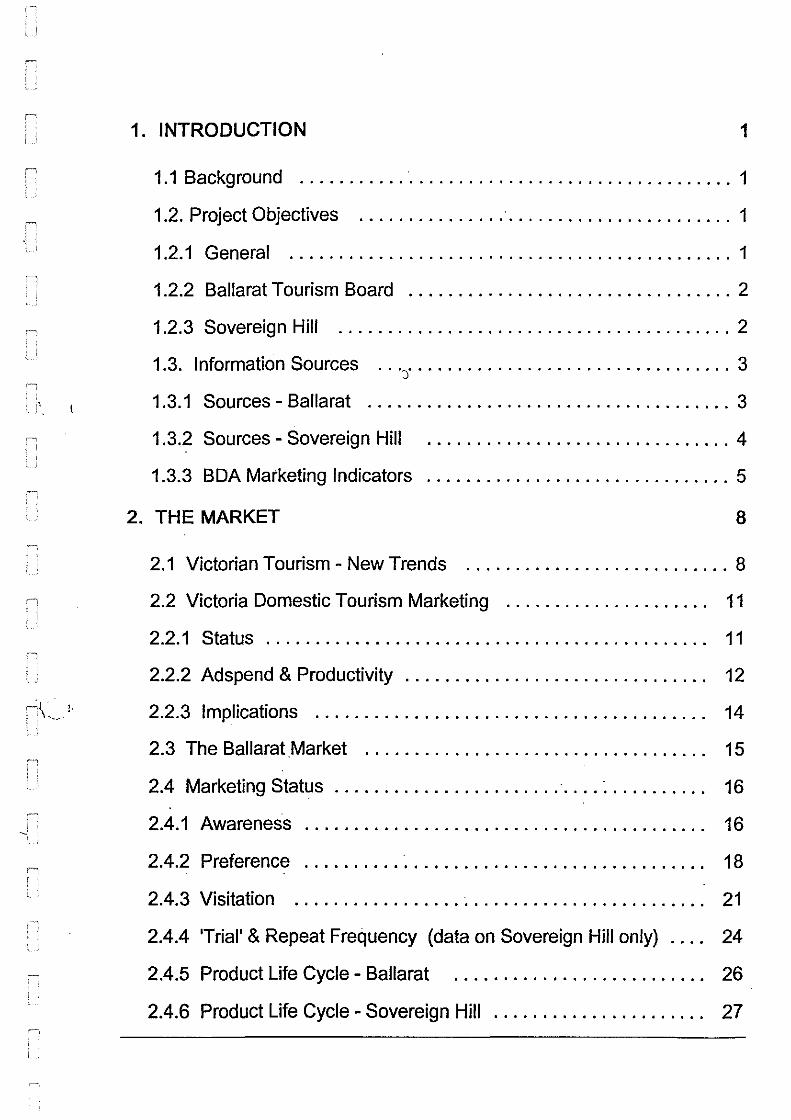

1. INTRODUCTION 1

1.1 Background ........... · ................................. 1

1.2. Project Objectives ...................................... 1

1.2.1 General . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.2.2 Ballarat Tourism Board ................................. 2

1.2.3 Sovereign Hill ........................................ 2

1.3. Information Sources ... ) ................................. 3

1.3.1 Sources - Ballarat ..................................... 3

1.3.2 Sources - Sovereign Hill ............................... 4

1.3.3 BOA Marketing Indicators ............................... 5

2. THE MARKET 8

2.1 Victorian Tourism - New Trends ........................... 8

2.2 Victoria Domestic Tourism Marketing . . . . . . . . . . . . . . . . . . . . . 11

2.2.1 Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2.2.2 Adspend & Productivity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

n\,_ ' 2.2.3 Implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 i :

2.3 The Ballarat Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

2.4 Marketing Status ....................... · .... ~ . . . . . . . . . . 16

2.4.1 Awareness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

2.4.2 Preference . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

2.4.3 Visitation ................. ~ . . . . . . . . . . . . . . . . . . . . . . . . 21

2.4.4 'Trial' & Repeat Frequency (data on Sovereign Hill only) . . . . 24

2.4.5 Product Life Cycle - Ballarat . . . . . . . . . . . . . . . . . . . . . . . . . . 26

2.4.6 Product Life Cycle - Sovereign Hill . . . . . . . . . . . . . . . . . . . . . . 27

,1 \

2.4.7 Visitation Product Life Cycle - Sovereign Hill & Ballarat . . . . . 28

2.5 Market Forecast . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

2.5.1 Domestic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

2.5.2 Inbound ................................ ·. . . . . . . . . . . 30

2.6 Implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

3. VISITOR TRENDS 32

3.1 Origin (at least 1 night, non-business, 40 kms +from home) 32

3.1.1 Domestic Tourists - Goldfields . . . . . . . . . . . . . . . . . . . . . . . . . 32

3.1.2 Domestic Tourists - Sovereign Hill . . . . . . . . . . . . . . . . . . . . . . 34

3.1.3 Inbound Tourists - Goldfields & Sovereign Hill . . . . . . . . . . . . 35

3.1.4 Visitors to Ballarat . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

3.2 Group Type Inbound . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

3.3 Purpose of Trip - Goldfields . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

3.4 Purpose of Trip - Sovereign Hill . . . . . . . . . . . . . . . . . . . . . . . . . . 40

3.5 Reason for Visit - Ballarat . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

3.6 Seasonality . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

3. 7 Distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

· 3.8 Implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

4. CONSUMER PROFILES 47

4.1 Age . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

4.2 Lifecycle . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

4.3 Occupation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

4.3.1 Goldfields . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

4.3.2 Occupation - Sovereign Hill . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

4.4 Holiday Activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

4.4.1 Domestic Tourists . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

4.4.2 Inbound Tourists . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

4.5 Implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

5. CONSUMER - DOMESTIC 54

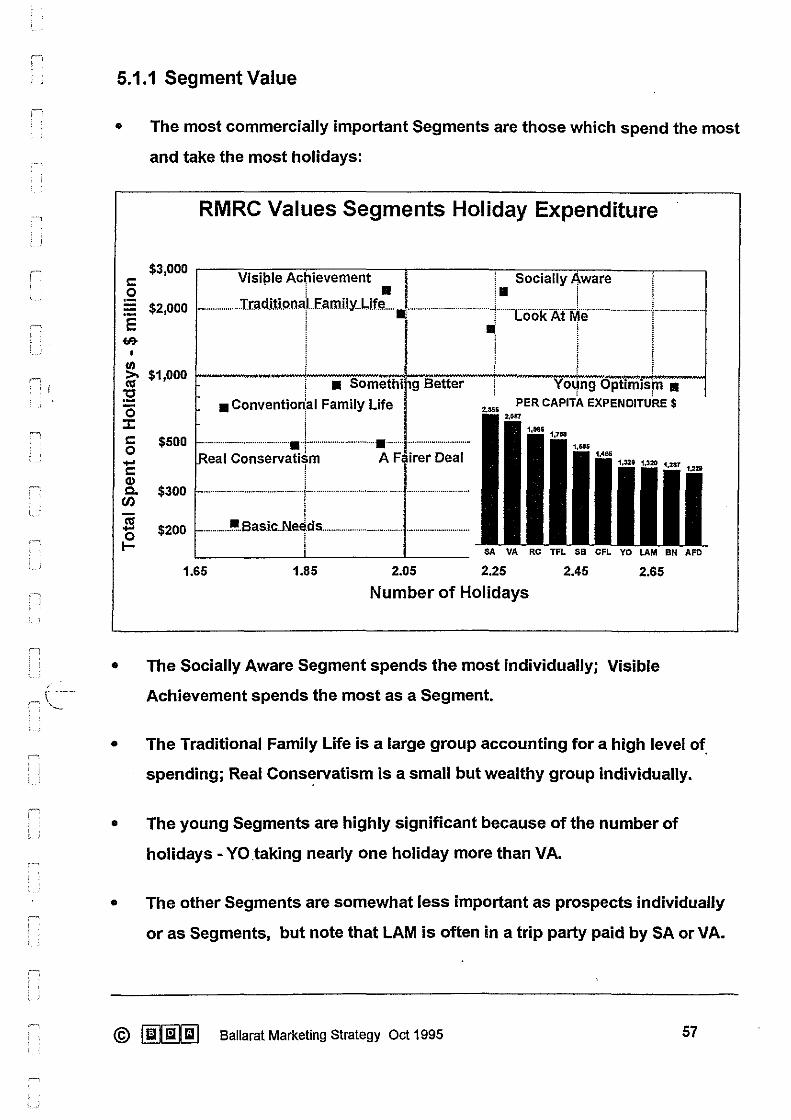

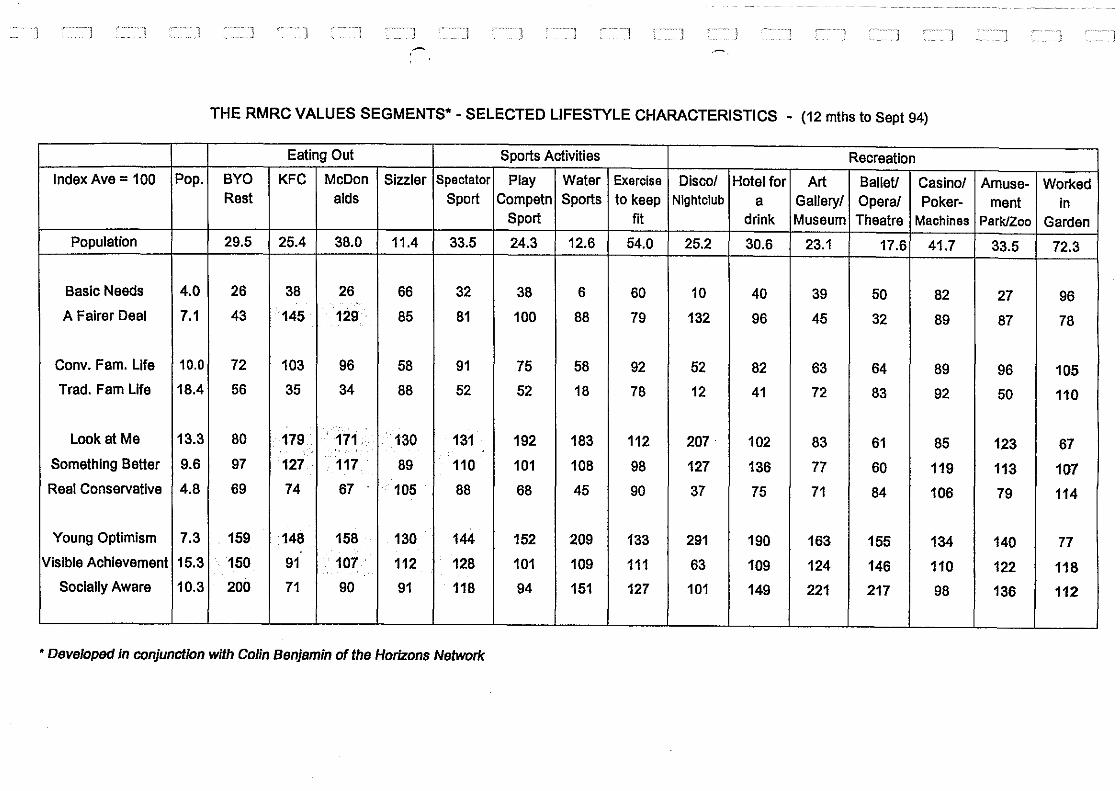

5.1 Introduction to RMR Values Segmentation . . . . . . . . . . . . . . . . . 54

5.1.1 Segment Value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

5.2 Summary of Tourism Victoria Targeting . . . . . . . . . . . . . . . . . . . 58

5.3 Goldfields & Sovereign Hill Compared . . . . . . . . . . . . . . . . . . . . 60

5.4 Segment Profile - Goldfields . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

5.5 Segment Profile - Sovereign Hill .............. _. . . . . . . . . . . 62

5.6 Profile Evolution - Visitation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

5.7 Segment Profiles - Goldfields compared to Sovereign Hill . . . . . 65

5.8 Segment Profiles - Ballarat Daytrippers . . . . . . . . . . . . . . . . . . . 66

5.9 Implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

6. CONSUMERS - INBOUND 68

6.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

6.2 Asia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

6.2.1 General . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

6.2.2 Asia - Singapore, Hong Kong, Malaysia . . . . . . . . . . . . . . . . . 70

6.2.3 Asia - Taiwan, Thailand, Korea . . . . . . . . . . . . . . . . . . . . . . . . . 72

6.3 Japan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

6.4 UK . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 4

6.5 Germany . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

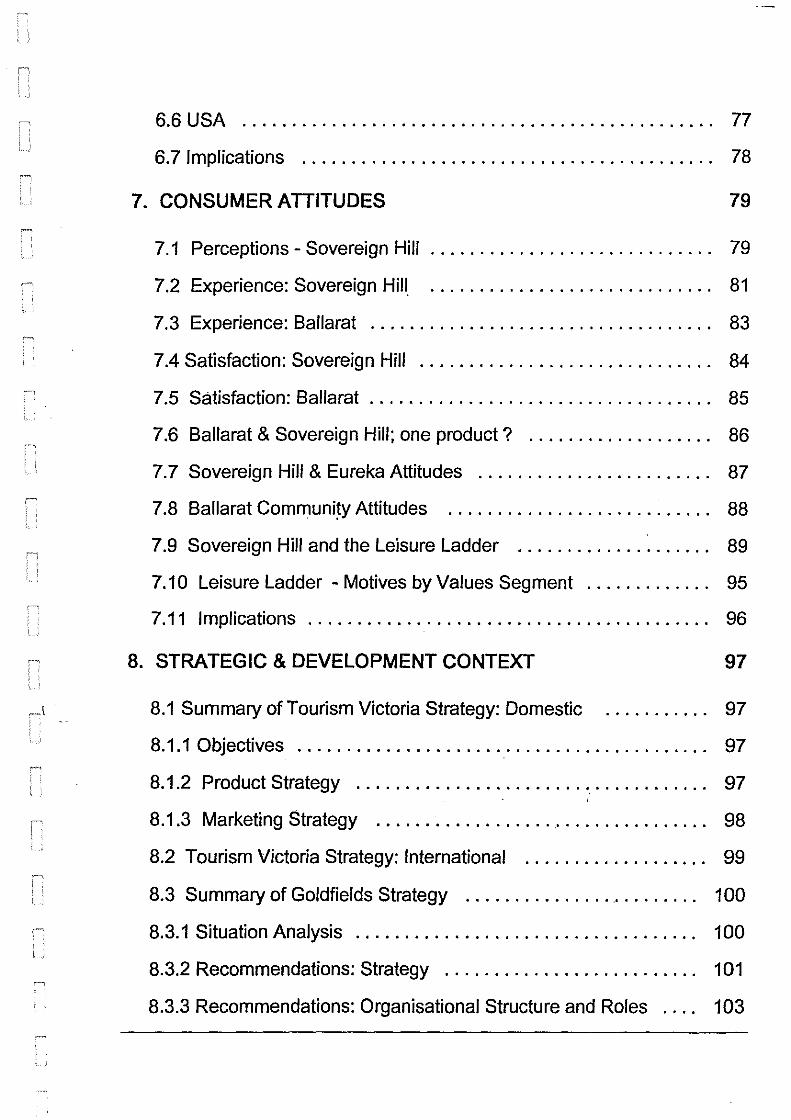

6.6 USA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

6. 7 Implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

7. CONSUMER ATTITUDES 79

7.1 Perceptions - Sovereign Hill . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

7.2 Experience: Sovereign Hill. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

7.3 Experience: Ballarat . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

7.4 Satisfaction: Sovereign Hill . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

7.5 Satisfaction: Ballarat . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

7.6 Ballarat & Sovereign Hill; one product? . . . . . . . . . . . . . . . . . . . 86

7.7 Sovereign Hill & Eureka Attitudes . . . . . . . . . . . . . . . . . . . . . . . . 87

7.8 Ballarat Community Attitudes . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

7.9 Sovereign Hill and the Leisure Ladder . . . . . . . . . . . . . . . . . . . . 89

7 .10 Leisure Ladder - Motives by Values Segment . . . . . . . . . . . . . 95

7.11 Implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

8. STRATEGIC & DEVELOPMENT CONTEXT 97

8.1 Summary of Tourism Victoria Strategy: Domestic . . . . . . . . . . . 97

8.1.1 Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

8.1.2 Product Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

8.1.3 Marketing Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98

8.2 Tourism Victoria Strategy: International . . . . . . . . . . . . . . . . . . . 99

8.3 Summary of Goldfields Strategy . . . . . . . . . . . . . . . . . . . . . . . . 100

8.3.1 Situation Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100

8.3.2 Recommendations: Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . 101

8.3.3 Recommendations: Organisational Structure and Roles . . . . 103

\

8.3.4 Recommendations: Product DevelopmenV Infrastructure . . . 103

8.3.5 Recommendations: Visitor Servicing /Information Provision . . 104

8.3.6 Recommendations: Packaging and Promotion . . . . . . . . . . . . 104

8.3. 7 Other Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 105

8.3.8 Projections . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 105

8.3.9 Monitoring and Evaluation Mechanisms . . . . . . . . . . . . . . . . . 105

8.4 Product Development . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106

8.5 Implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

9. PERFORMANCE & PROJECTIONS 108

9.1 'Blood on the Southern Cross' . . . . . . . . . . . . . . . . . . . . . . . . . . 108

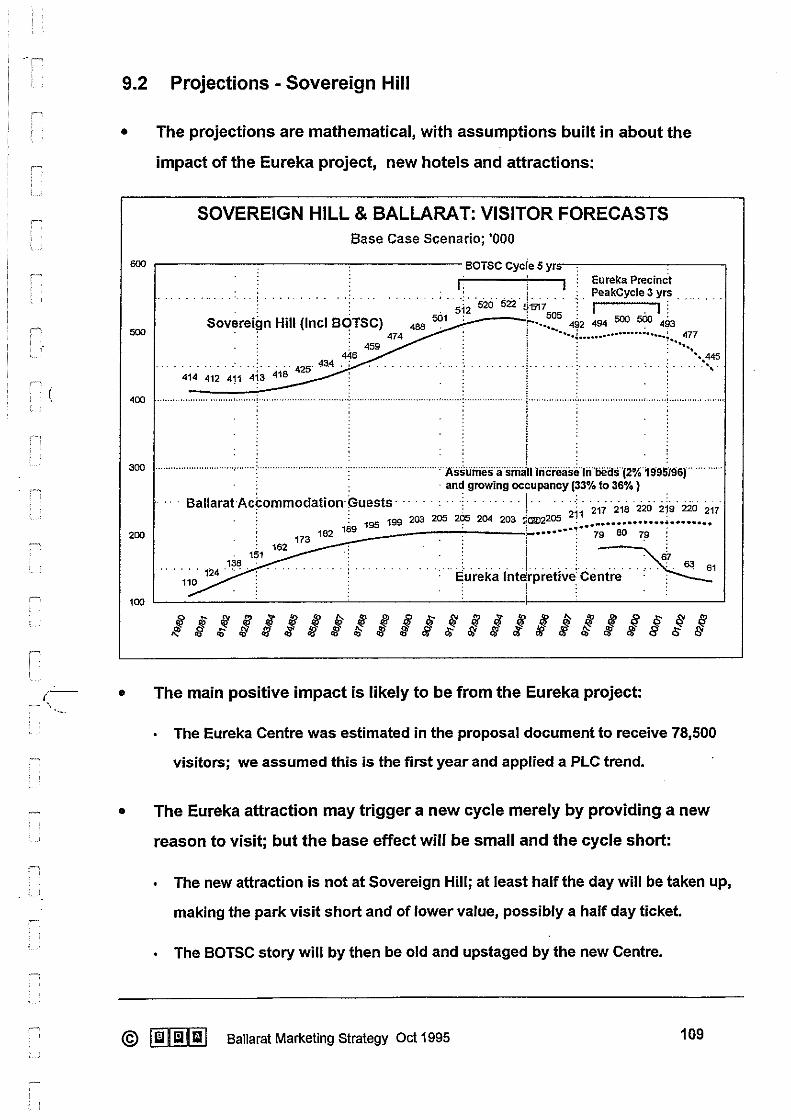

9.2 Projections - Sovereign Hill . . . . . . . . . . . . . . . . . . . . . . . . . . . . 109

9.3 Projections - Ballarat . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110

9.4 Pricing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111

9.5 Advertising Expenditure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112

9.6 Implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 113

10. S.W.O.T. . ........................................... 114

10.1 Strengths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 114

10.2 Weaknesses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 116

10.3 Opportunities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 118

10.4 Threats . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119

11. OBJECTIVES

.11.1 Visitation - Sovereign Hill

11.2 Visitation - Ballarat

120

120

121

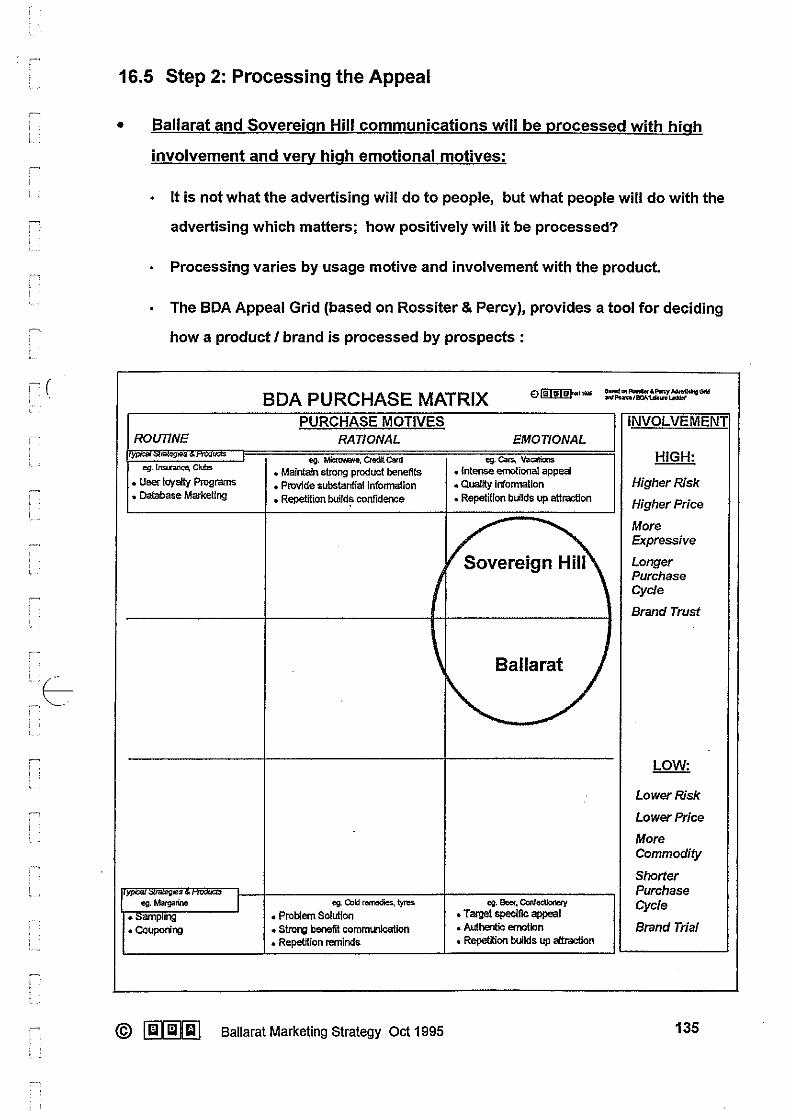

16.5 Step 2: Processing the Appeal

16.6 Step 3: Retrieval Cue

16.7 Step 4: Fitting Into Life

16.8 Step 5: Productivity Plan

16.9 Public Relations

16.10 Setting the Budget

17. NEXT STEPS

APPENDIX

135

136

137

138

143

143

144

1 INTRODUCTION

1.1 Background

• This is the final report on the Marketing Strategy developed jointly for the

Ballarat Tourism Board and Sovereign Hill.

• The development process and review dates are summarised in the

Appendix; BDA's collaboration was facilitated by Clemenger, Melbourne.

1.2. Project Objectives

1\, 1.2.1 General

• The Strategy should provide an enduring framework for Ballarat tourism:

To focus on holiday and VFR purposes only; the potential for the business

travel for conventions will be dealt with separately.

To understand the current status of inter-, intra and inbound tourism sectors

within Victoria and their likely development.

To identify the most profitable consumers with needs which match the existing

Ballarat tourism infrastructure and planned new investment.

To define the most productive ways of stimulating and sustaining new demand

(resources available for communication are extremely limited).

To plan within the Tourism Victoria Strategic Business Plan, Sept 1993.

To ensure that the principle qualitative beneficiaries of the Strategy are the

visitors, who should have a wonderfully satisfying experience during their visit.

To ensure that the principle commercial beneficiaries of the Strategy are the

businesses and employees of tourism related enterprises.

To develop strategies for product, 'pricing', distribution, communication,

research and planning, focusing especially on communication.

© ~ Ballarat Marketing Strategy Oct 1995 1

(

1.2.2 Ballarat Tourism Board

• Specific objectives:

To establish a Ballarat "identity".

To devote specific attention to events, conference and conventions.

To develop a framework for evaluating & prioretising development proposals.

To develop a framework for planning the development of the Eureka precinct,

for which a $3.5 million grant from the State Government has been won.

To develop a framework for an effective and interlinked structure for advertising

and promotion by the Board and individual tourism businesses.

To assess how Ballarat relates to the Goldfields, Great Ocean Road, Southern

Driving Route and other collaborative tourism marketing initiatives.

To achieve compatibility with the University of Ballarat School of Business'

recent 'Goldfields Tourism Strategy Plan'.

1.2.3 Sovereign Hill

• Specific Objectives:

To determine the Product Life Cycle in terms of both attendance and revenue.

To understand how the Product Life Cycle has been influenced by product

initiatives and external factors, including demand for Ballarat.

To focus on the optimisation of attendance rather than accessory businesses.

To provide a framework for launching product initiatives such as the new

Chinese themes, Gold Chamber and Gold Pour.

To assess the impact of infrastructure such as the Eureka Centre on demand.

To provide an enduring structure for advertising and promotions which minimise

wastage and generate a consistent emotive appeal.

© ~I Iii [iJ Ballarat Marketing Strategy Oct 1995 2

1.3. Information Sources

1.3.1 Sources - Ballarat

• There are gaps (eg day trips) & anomalies in all Australian tourism data and

interpretation & estimates must often be made, based on many inputs:

ABS information on tourist accommodation by City (business trips included).

Holiday accommodation component of the CPI and unpublished ABS has been

used to assess the Product Life Cycle for Ballarat in comparison with Victoria.

Overnight visitation to the Goldfields is measured by the DTM, based on a

continuous sample of 65,000 people interviewed at home.

Since 1990/91 Ballarat is reported in the 'Goldfields', bounded by Bendigo,

Daylesford, St Arnaud & Kilmore; visitors still identify places from a map.

Unpublished data shows that Ballarat accounts for nearly 40% of trips in the

region and Ballarat visitors account for a high proportion of other region trips.

The University of Ballarat also found strong linkages between towns within the

Goldfields, with high cross visitation.

The DTM is therefore the main indicator of Ballarat visitor information although

1993/4 is the latest available and no media or gee-demographic data is available.

The RMR Holiday Tracking Study is now carried on the DTM survey; it covers

holidays of 3 days + and also tracks 'Goldfields' visitors.

RMR also provides massive single source lifestyle and media usage data.

• The recent University of Ballarat Study covers many local topics but the

research content is not used in this report:

Access has been incomplete (development documents and the Summary).

Some findings are expressed in terms of the RMR Values Segments, although

there was no access to RMR data; these findings conflict with the actual data.

@ m Ballarat Marketing Strategy Oct 1995 3

' \ ...

1.3.2 Sources - Sovereign Hill

• Studies have been carried out in different formats by AGB, RMR, YCHW,

Newspoll, University of Ballarat and by Sovereign Hill.

This history is full of insights but the inconsistent nature of scope, sample,

questionnaire & presentation inhibits its value, especially trending.

It will be used as qualitative support for interpretation of the main data.

• For this, we will use the RMR Theme Park Tracking Study and the IVS:

Continuous single source data on the RMR Omnibus since 1993 and for 1991

and 1992 on the AGB Omnibus.

Sovereign Hill has purchased access to the RMR Theme Park data. The previous

three waves (AGB) are available from the BOA Library at no charge.

This source covers interstate and intrastate visitations and intentions of

Sovereign Hill in Australian context.

Inbound visitors can be defined within the International Visitor Survey (accessed

via CD-Mota); Sovereign Hill is included in this survey.

• Sovereign Hill has provided records of attendance and revenue; this

information is commercially sensitive and will be restricted in the report.

• BOA has also had some access to the unpublished ATC Segmentation

Studies of 15 overseas markets for 1993.

• Also some ATC country reports and the ATC database of visitor origin both

historic and forecast have been used.

• BOA has commissioned a literature search from Moninfo on historical parks

and open air museums, especially academic & consumer research.

Note: The lack of availability of the planned Victorian Regional Tourism Monitor is a serious handicap to this type of study, particularly with regard to day trips.

© [iiJ"i/[Q] Ballarat Marketing Strategy Oct 1995 4

I \

1.3.3 BDA Marketing Indicators

• RMR Holiday Tracking Survey was set up following the logic of the BOA

Marketing Funnel, which is a model based on marketing theory:

•

•

In the late SO's, Engel, Howard and Sheth showed that purchase was the output

of processing information as part of rational problem solving.

Identification of a need led to information gathering, formation of attitudes,

development of intention and finally purchase.

The process was cognitive decision making, which could be influenced at

various points.

In 1980 and 1988, Ehrenberg and Goodhardt proposed a 'low involvement' or

'simplified model', which suggested that consumers seldom behave rationally.

They have a low level of involvement in most purchases, and most behaviour is

habitual rather than subject to conscious selection.

Awareness of new products encourages trial, and repeat purchase is a result

only of satisfactory trial.

Trial is a function of curiosity aroused by awareness, with a minimum of rational

pre-purchase decision making.

BOA developed the "Marketing Funnel" to help understand and plan the

marketing process:

For products with a high level of consumer purchase involvement as well as a

· lower level of involvement, where aware=trial=satisfactory=repeat.

Demonstrates the progressive development of the decision process, from the

arousal of awareness through to purchase.

Shows the controllable and uncontrollable influences on whether a prospect

moves towards purchase or becomes distracted to a competitor:

© ~I Ill [j] Ballarat Marketing Strategy Oct 1995 5

( '

' ' 1 r. = •c

iE ,_ 00 !::I !C ie ,.... w ::;; F i

•

:~~ ~~.

~ H~

:: ::: :-:::-::

B-~ fl,,~'. :>"·:· ;;;:; ' m~ 1'1'

·~· ~ .

"'" !n:·:

'BB~ g~ ;;-::-; . .. .. ' :::::: ~: ...

TARGET CUSTOMERS

AWARENESS Prompted : Know it when you say it Spontaneous: Comes quickly to mind

POSITIONING Knows how it fits into the scheme of things .. What kind of company - What kind of people use it - What sort of products it sells

CONSIDERATION Now rm in the market - Whafs available - What's important to me

SHOPPING Comparing the options,

benefits, prices

PURCHASE A product for me

EXPERIENCE Promise vs Reality

• Satisfaction Loyalty

'OOOPEOPLE

UNCONTROLLABLE FACTORS

Internal marketing programmes such as advertising, product and distribution

(availability) attempt to convert more people down to purchase

External influences such as the economy, or competitive activity work against

these programmes

Trial, the first purchase, represents the first measure of a successful programme

A satisfactory first product experience loops back for repeat purchase

In the case of Tourism, some adjustment needs to be made to the

description of the stages of the model.

• Advertising awareness:

For the States of Australia awareness cannot be measured in terms of simple

awareness such as for a new grocery product.

Instead, consumers are asked about advertising for holidays or travel they may

have read, seen or heard in the last month for States or Territories.

© I Iii I Ill Im I Ballarat Marketing Strategy Oct 1995 6

(

•

This measure captures awareness generated not just by main media but by

brochures, news items or any communication - including imagination I

Preference:

Consumers are asked about the places they would like to visit for a holiday of

three days or more within the next 2 years. 'Places' means Cities or attractions.

In practice, this measure is a reliable indicator of total preference, including

short breaks; the three day limit serves to impose a degree of commitment.

• Intention:

Measured as "places planning to stay on next holiday trip of 3+ nights"

The variation between intention and actual visit is a good indicator of VFR

visitation, where the planned holiday is replaced by a low cost stay with 'F or R'.

• Purchase behaviour:

•

Visits are measured as " all places visited for a holiday of 3 days or more in last

12 months" or "the last trip".

A quarterly indicator of Trips from the DTM is also included as a point of

reference and to demonstrate the relationship with the '3+ days' measure.

Unfortunately, the DTM is at least 6 months in arrears.

Adspend:

Adspend is measured as all adspend by Tourist Commissions and other

government tourism bodies throughout Australia.

It is expressed in mainly as share of total expenditure: share of Voice (SOV).

© ™ Ballarat Marketing Strategy Oct 1995 7

2 THEMARKET

2.1 Victorian Tourism - New Trends

• Victorian tourism - red - is growing, especially intrastate tourism (to Mar 95):

•

Interstate Non Business Trips

Total Interstate Trips

VIC Interstate Share

Victoria '000 CJ 9,318

9,042 ·~:;cJ:··-·~

iml61M94: ~.0%

:.11 _k.t1.,·~, ._,,,, .... ,:i

::~~J!. ~,1;i521 :~~~i~

VICTORIAN TOURISM OVERVIEW

Intrastate Non Business Trips Inbound Non Business Visitors

Total Intrastate Trips

VIC Intrastate Share

Victoria •ooo CJ

$0/S1 91192 921'33 93194 M 96 - ...... ""

" " "

Total Inbound Visitors '000 Victoria Inbound Share Victoria '000 CJ

Vic Share scales common other scales vary

""

1989 1990 tS51 1992 1993 1994 Scuce: BTR (IVS)

Intrastate tourism in Australia has fallen 1%, but in Victoria has increased

16%, with nearly 1.2 million more Victorian trips.

• Interstate tourism, where Tourism Victoria is spending most advertising

effort, has fallen 2% in a market down 3%; so Vic's share has grown slightly.

• Inbound tourism has grown 13% for Victoria, but the market increased 15%

so share fell again.

• Victoria accommodates 10.8 million trips/visitors, an average 29,500 per day;

eight out of ten are Victorians.

© I Iii I Iii I!] Ballarat Marketing Strategy Oct 1995 8

• A major change in long established Victorian tourism habits has occurred

over the last year, as fewer Victorians travel out of the State:

:g_ ·c

Non Business Interstate Trips '000 Trips - 12 MAT

2,800 ,.-----------------------------~ 9,000

Victorians Travelling Intrastate [RH] 8,000

2,400 7,000

2,200

Victorians Travelling Interstate 6,000

t- 2,000 g !?

6,000

1,800 4,000

1,600 3,000

1,400 Interstate Visitors to Victoria 2,000

Trip Deficit

Trend of outbound travel by Victorians has fallen sharply, causing stress among

northern tourism industry (NB overseas tourism thru Tullamarine is + 2% Q2/95).

The positive interstate trend has also slowed and intrastate tourism surged.

BOA has correlated Consumer Sentiment Index (RMR), unemployment and

various economic indicators with domestic tourism trends; none bettered 0.382.

However caused, Victoria's trip deficit has been running at less than half the

level of 1991 - worth well over $1 billion in retained spending.

Duration of trip and other detailed analysis (available separately) shows little

change for Victorians.

• The reason for such an unexpected change is the disturbance caused to

leisure patterns by the huge increase in trial of gambling ...

© ~ Ballarat Marketing Strategy Oct 1995 9

• •.• taking place in relatively positive economic conditions.

• In Victoria, there has been a dramatic increase in gambling:

Casino/Pokies Last Holiday trip 3 days +

Hol in Vic 240 +46%

Hol in Melb +32%

+60%

Visited Casino in last 12 months

Live Melb

154 +75%

~1i] 1994 • 1995 Source: RMR ~ HTS

26% of Melburnians and 15% of country people visited a casino in the last 12

months to June 1995 - a huge increase of 152% 175%.

This is not nearly up to the Hobart level - 41% visited there.

38% of Melburnians and 46% of country people visited a club with pokies.

There are also big increases in the gambling activity of 3 day + holiday visitors.

• It is likely that as the appeal wears off, the rate of revisit will decline, just as

with any new product; tourism patterns will be permanently changed:

The opening of the new casino building may trigger a new cycle of trial lasting

through 199617; however, the pokie cycle is likely to mature soon.

Trial of the New Media will also impact tourism habits over the next few years.

© I Ill I~[@ Ballarat Marketing Strategy Oct 1995 10

/

I \__

2.2 Victoria Domestic Tourism Marketing

2.2.1 Status

•

•

•

•

RMRC Holiday Tracking Study - Victoria Adspend sourced from AIM Data; Tourism Commission spending only

% Australians 3 month moving average

30

Preference 25

Trips• • 20 Visited • • •

15 Awareness ...... •,':"

10 ·I .. i

i .... i · .•• ]" ! 1 -. ••••• . • i j ! 1 I i f l r ! I

'

% Adspend

• 60

50

40

30

20

10

.. . j I ! I l I 5 ~~-'-'-'-"-'-"'-'"~~~~~~~~~~~~~'-'-'-LW.>-'-'--'-'-".ll..LI'--'-'-~""'-'.LI->....u.J'-"-'"-"""--~o

Trips = 'Xi share of annual non business trips ·Main Destination state S-W.- IJTR.DTM 1996

J A s 0 N D J 94 F M A M % Ad•p•nd(l 8.0 8.8 8.5 11.2 1'4.7 17.11 24.1 17.1 14.5 13.1 21.4

Awaren-- 124 1'8 122 1no 11.0 11.8 13.4 128 128 14.f 18.8

Prefer-no.- 25.0 2•2 24.5 24.7 25.3 2U 24.8 2U 24.f 25.2 2S.0

Intention . 10.4 1n1 11.11 120 120 128 122 125 10.11 11.1 10.e

Vhited - 18.S 17.8 17 ... 17.1 17.3 18.3 17.5 18.0 17.8 18.3 17.7

Trl119 • 21.0 21.1 21.S

J J A s 0 N D 28.8 24.11 25.0 18.5 1ae 1S.2 17.3

18.5 17.8 18.5 1•t8 13.11 14.7 14.8

24,8 2S.2 .... 2S.8 227 222 2S.2 10.4 10.8 10.8 11.0 11.0 10.8 1n8 17.4 17 • .C 17.0 17.1 18.3 15.GI 15.1

21.GI 229 25.2

J 95 F M 20.0 17.1 14.3

14.V 1U 122 2-4,5 24.11 .... 11.3 121 120

1~8 18.0 17.4

211.7

A M 17.2 20,11

11.8 127

2S.S 22.8

10.8 10.1

18.7 15.0

J 27.2

15.8

21.8

1ns

18.8

Goals

20% 27% 16%

This graphic shows how Vic's share of Intrastate tourism (+16%) and trips of

under 3 days surged in a depressed market, with indicators below target.

This is because the trips growth is not marketing programme driven •

A record level of SOV created the highest level of awareness for 9 months, '

but increased awareness of advertising is not yet converted into preference.

After an improvement in summer 1994, preference plummeted to its lowest

level; intentions went the same way, falling under 11%.

• Vic is falling further behind the objectives set in the 1993 Strategic Marketing

Plan; the trip performance is held up by intra, not interstate performance.

© ~ Ballarat Marketing Strategy Oct 1995 11

I ' "

2.2.2 Adspend & Productivity

• There has been a big rise in state tourism adspend over the last two years,

expenditure by state authorities increasing to $20 million:

Holiday Tracking Study - Awareness & Adspend QLD % Aware of Advertising -3MMA; State adspend 12MAT $'000

60

20,000

50

18,000 40 NT

30 16,000

20 14,000

\i1J .,.. ..... ,. ............. ,,.

VIC e 10 12,000

SA

July .... ··~ O<t . .. ••• '~. Fob .., ""' . ., ..... '"' .... ,.,. Cd ... • •• '~ Fob "" ""' . ., '~

" " 17 " " " " " ,,

" " " " " " " " " 10 " " " 17 17 " IC 12 " 12 11 11 12 " 13 12 " 17 " " 11 11 14 1' 11 11 14 12 12 12 " QL .. " .. " .. " 11 " " " " " .. .. 11 .. .. .. •• .. 44 " .. .. .. 10 10 11 10 • 7 7 • • • • • • • • ' ' • • • • • • • 11 12 12 11 10 • • • 7 7 7 7 7 7 7 • • • • • • • • •

TA$'1<11 17 17 1G 11 14 14 " 14 12 12 12 13 " 12 12 " 12 12 11 13 " 12 10 10 NT .. .. " " " " " " " " " 27 " " " " " " " .. .. " " " 3· 1Z1 '"

,., ,., 18,11 17.92 " 11.41 ''"1 "' ..... ... .. " 18,48 19,71 18,11 20,:ZO

Source: RMRC ·HTS; AIM Data

• This excludes any 'below the line spending', brochures etc, but usually the

relative proportion of non measured spend will be similar to the measured.

• The tourism industry adds to this expenditure, but the analysis1 has not .

been updated over this period; total spending will be around $200 million.

• The QTTC has steadily lost advertising awareness, the NTTC has risen.

• Tourism Victoria is fourth best, well up on NSW.

'Analysis of Tourism Industry Advertising Expenditure & Productivity Benchmarks' BDA 5.8.94

© ™ Ballarat Marketing Strategy Oct 1995 12

I

'" (~,

• Big changes are still occurring in state spending policies:

•

•

•

•

•

l-k>liday Tracking Study-Allspend $'000

NSW and Vic spend 12M\T

the most, with Vic Nf

only $400,00 behind

NSW; Queensland

pulling is back

significantly.

Victoria gaJlS most

!i TASINCTT •

'·~ L-=~-'=''~' ~~~~;;;;;l~;;;;;~-=;~7:=~~;_-_-_:~;;;;c.---_____ _Lf.

'" F • A • , , A • 0 N D ... F I I'll I A ., , for awareness at

~2 ger gerson, - . ... .... . .. '"' "'' ..... .... , .. . .. , ... , .. 14 -4,.Q ... (,414 ... ,., " . "" '"' ''" ... ... ' I

, .. '"' "" '"' .... , ... S,1811 :vw 4,l#J :l,~14,CZl . I ' ,. . .. .. U1 "' "' - "' .. ., .. .. 1164 "1.19111,ZQ: 1,:D\ \?11 . ... ... "' ... "' "' "' "' "' .. "' .. "' rn t111 '*' 1,'$1 Ul7

"' . "" "" , .. , .. "" , .. , .. , .. , .. ,., , ... , .. ,., , ... ;J.)):21:1,641

"'TIU• NSW about $1.70.

, .. ' "" ' , .. "" '"" , .. ' , .. ... ... z ,. \7IO 1,llZJ 1,Gll 1,at

Of course many other communications are involved in this effort, so relativities are the key. Brochures, promotions, distribution, famils etc cannot be measured; relative adspend may be an indicator of the total effort.

Marketing productivity

is also measured

by conversion of

preference into visits.

Victoria's record

performance is due

to falling preference

with good visitation.

120

NewSouth 'J'lales

80

60

South Australia

40

Preference IX> Visitation Conversion 3 month moving average

111

' !

112 114 113 ,

105 i '

~'-'--'--'-"-'-'--'--'--'---'--'-+,-'---'--'--'-.L...J'-l_L-'---'--'-.1..J

~~!8~~i~~~i~~l!8~~~~~~i~ Soun::e: ~-HlS

• But as discussed, the increase is from within the State thanks to the impact

of developments which encourage Victorians to holiday near home.

• There is no evidence that Tourism Victoria's expensive marketing efforts are

benefiting the Victorian tourism industry in terms of non business trips.

© ~ Ballarat Marketing Strategy Oct 1995 13

2.2.3 Implications

• Victoria is the only State generating more domestic tourism:

•

This appears to be related to changes in Victorians' tourism patterns caused by

new entertainment infrastructure, especially gambling.

The trial and retrial of new gambling facilities is likely to last for a while before

settling back; however, tourism patterns may be permanently changed.

More Victorians holidaying at home is a positive development which should be

exploited while it lasts; holiday preferences for Victoria have not increased.

Victoria is continuing to lose share of inbound visitors:

This will continue as Australia becomes more successful at converting offshore

preferences for 'Brand Australia' on target, centred on sun, surf, rock and reef.

Victoria will continue to enjoy growing visitor numbers, a high quality niche

market with strong VFR linkages and distinctive attractions (eg GOR) .

• Tourism Victoria is spending more than any other State to make non

Victorians aware of Victoria (per aware person):

But this programme has not yet met the marketing goals set •

In particular, increased awareness of the advertising is not converting into

increased desire to visit nor into more intention at a fast enough rate.

Penetration of high earning longer stay holidays is less than hoped for.

Barriers to conversion are likely to include lack of specific preference for

specific braggable attractions and destinations.

The welcome reductions of the trip deficit is more due to lower outbound travel

by Victorians (recession in 1993 and possibly gambling in 1995).

• The Tourism Victoria programme could support Ballarat or Sovereign Hill

more; but the current market trends and outlook are certainly positive.

© ~ Ballarat Marketing Strategy Oct 1995 14

2.3 The Ballarat Market

• BOA has used a variety of sources to model the current non business

demand level for Ballarat, by domestic and inbound visitors and type of trip:

•

Day Trip

Stay

THE BALLARA T TOURISM MARKET

Estimated Visitor Numbers 1994: 2,932,000

Domestic Stay Visitors: Commercial: 193,000 (7%)

VFR: 210,000 (7%)

Inbound Stay Visitors: 15,000 (1%)

In 1989, RMR estimated that 3.1 million Victorians made 42

million day trips'; aiiowing for population growth, Baiiarat has

about 6% of the market '"Mdtloutt11W1ltr

Refer Appendix for Model details, based on OTM1 ABS, IVS, Sovereign Hill etc

Ballarat is primarily a day visit destination, primarily from Melbourne;

Australians account for the vast majority of visitors.

• Of the 418,000 who stay in accommodation for varying lengths of time,

about half stay with friends or relatives.

• This level of visitation will have enormous economic impact on the region,

which can be calculated quite accurately:

When the new HES is available

And multiplier tables for Victorian tourism.

© ~ Ballarat Marketing Strategy Oct 1995 15

(__ ~-

2.4 Marketing Status

2.4.1 Awareness

• There is no measurement of awareness of Ballarat as a tourism destination:2

In 1993, Ballarat was found to be more successful in generating consumer

enquiries through its tourist office than the other towns in the region:

Ballarat 73 000 (over 80,000 in 1994)

Bendigo 47000

Maldon 23000

Castlemaine 10000

Maryborough 8000

However, awareness for the smaller attractions & events was low:

Average Low

Montrose Cottage

High Awareness

Sovereign Hill

Kryal Castle

Wildlife & Reptile Park

Fine Art Gallery Tuki Fishing/Farm Complex

Lake Wendouree/Gardens

Eureka Stockade

BOTSC

Golda's World of Dolls

Old Curiosity Shop

Creswick Dinosaur Park

• For Sovereign Hill, the AGB study of 1992 is the best source •

• Sovereign Hill (SH) enjoyed a reasonable level of top-of-mind awareness .

among Melbourne residents of 22% (AGB 1992):

Lower than Melbourne Zoo (36%) and Phillip Island (34%).

Close to Healesville Wildlife Sanctuary (24%).

Better then Puffing Billy (16%) and the State Art Gallery (11%).

2 Sources: GTSP Community Survey Questionnaire (03)

© ~ Ballarat Marketing Strategy Oct 1995 16

• Prompted awareness in Melbourne is highly satisfactory and competitive, in

the high 80s; Sovereign Hill is very well known by most potential visitors.3

• In 1991, AGB found that 31% of Australians (3.8 million people) had 'ever

visited' Sovereign Hill, suggesting national awareness of at least 50%:4

• This compares with 40% ever visiting Sea World.

• In 1989, RMR found 91% awareness of Sovereign Hill in Victoria, with 74%

having been and 56% intending to go in the future.5

• Venue Monitor ( 1994) (The more recent Venue Monitor is unreliable for identifying

(_ non-Metro venues because of ambiguous wording of question and is not used here)

measured prompted advertising awareness in Victoria and showed

Sovereign Hill with considerable cut-through:

l/

4th place in Victoria with 52% awareness in summer 1995.

Only beaten by the Casino (90%), Queen Victoria Market (61%) and Royal

Melbourne Zoo (61%).

The major factor was TV ads pend; recalled by 74%, with other media less

significant (TV scores strongly on these measures, whether used or not).

Three years after launch, BOTSC had created 77% awareness in Melbourne.

• There is no measure of inbound awareness, but it is likely to be low.

• Sovereign Hill is clearly very well known, probably as well known as any

other comparable man made attraction nationally and within the State ..

3

4

5

AGB 1992, Theme Park Visitors Wave 2 AGB 1991, Theme Park Visitors Wave 1 RMR 1989, Melbourne Parks & Waterways Study

© fWl Ill!]] Ballarat Marketing Strategy Oct 1995 17

\

'

c_, _,

2.4.2 Preference

• To determine the relative attraction of the Goldfields and Sovereign Hill,

'preference' for each is compared to other Victorian destinations:

Sovereign Hill: 'theme park most likely to go to in the next 12 months'; this is

the most demanding of two preference measures available .

Goldfields: 'place like to go for holiday of 3 days or more in the next two years';

this measures real interest in holiday visitation (implies overnight, not day trip).

Preference for Victoria; 0/o of Australians

Melbourne

Vic Snow

Great Ocean Rd

(Sov Hill)

Phillip Island

Grampians

Lakes Entr

Murray

Vic High

Wilsons Prom

Dand. I Yarra

Goldfields

Source: RMR • HTS

3.3 million people (23%), year to June 1995

5.7

Note: Preference ror Sovereign Hill measures theme park most likely to visit In next 12 months. Preference for other destinations is place like to visit for a holiday In next 2 years ...

• The Goldfields are 12th (223,000 people) and only 4 regions are lower:

•

Preferred regions are linked to specific activities or attractions with powerful

product images: Philip Island = Penguins, Snow= Skiing, GOR = Scenery etc

Sovereign Hill is 4th Victorian 'destination' (524,000 people) and 4th theme

park nationally after Movie-, Sea- and Dreamworld; a clear image.

@ ~ Ballarat Marketing Strategy Oct 1995 18

.~

,, .. I \ '·.

• Preference by origin is charted below:

Preference for Victoria; °lo of Australians 3.3 mllllon people (23%), year to June 1995

Melbourne

Vic Snow .. u

Preference for Victoria; °lo Melbourne Residents 800,000 peop!e (31%), year to June 1995

Melbourne

Vic Snow

Great Ocean Rd u Great Ocean Rd ,. (Sovlill) .,

Phillip Island

Grampians u

Lakes Entr ,, Mumy u

Vic High ,, WllsonsProm

Dand. / Yarra

Goldflelds

Preference for Victoria; °lo Vic Country Residents 261,000 people (26%), year to June 1995

Melbourne .. Vic Snow

Great Ocean Rd

(Sov lill)

Phllllp Island

Grampians

Uikes Entr ... Murray "'

Vic High "' Wllsons Prom ••• Oand. / Yarra

Goldfields

(Sov Hill) u Phillip Island

Gra!11)1ans

Lakes Entr "' Murray

Vic High u

Wilsons Prom. ••• Oand • I Yarra

Goldftelds

Preference for Victoria; °lo Interstate Residents 2.2 milllon (21%), year to June 1995

Melboumeiiiiii!E~===~···,. u .. u

Lakes Entr 1.1

Murray 1.1

Vic High 1.1

WlsonsProm

Dand.1 Yarra Goldfields

u

u

Preference f'or Sovereign H~I measures 'theme park most likely to visit in next 12 rronths.', Preference for other destinations is ' .. place ~ke to visit!« a hOllday in next2 ~ars. . .'

• Interpretation of this data must take account of two dimensions:

•

•

•

Penetration ("./o data labels), indicative of relative strength of appeal & saliency.

Absolute numbers (population in heading), indicative of visitation potential.

The Goldfields has a very low appeal in each area monitored; it is very likely

that Ballarat is the main component and will be even lower:

In numbers, Goldfields attract most from interstate, 73% of preferrers.

Among Melburnians and Victorian country residents, Sovereign Hill is by far

the most appealing destination, with GOR second.

Among lnterstaters, Victoria means Melbourne and the snow .

© [iij Ill@ Ballarat Marketing Strategy Oct 1995 19

(

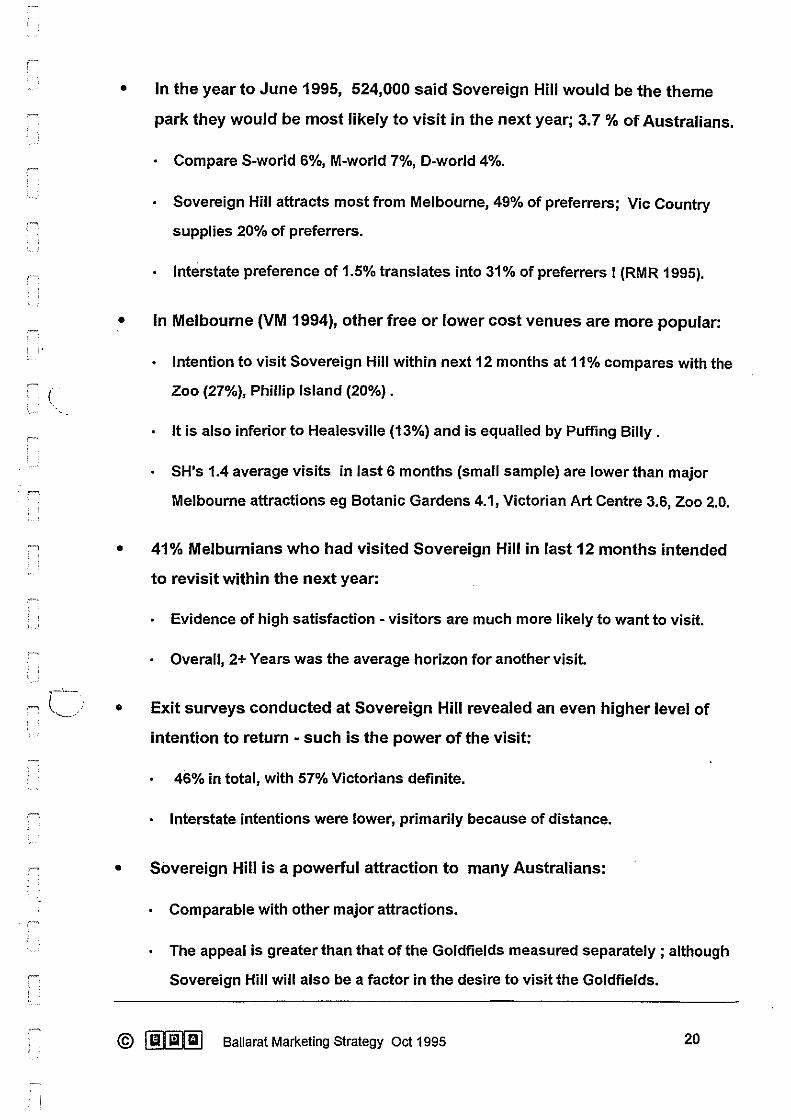

• In the year to June 1995, 524,000 said Sovereign Hill would be the theme

park they would be most likely to visit in the next year; 3.7 % of Australians.

•

Compare S-world 6%, M-world 7%, D-world 4%.

Sovereign Hill attracts most from Melbourne, 49% of preferrers; Vic Country

supplies 20% of preferrers.

Interstate preference of 1.5% translates into 31% of preferrers I (RMR 1995).

In Melbourne (VM 1994), other free or lower cost venues are more popular:

Intention to visit Sovereign Hill within next 12 months at 11 % compares with the

Zoo (27%), Phillip Island (20%) .

It is also inferior to Healesville (13%) and is equalled by Puffing Billy.

SH's 1.4 average visits in last 6 months (small sample) are lower than major

Melbourne attractions eg Botanic Gardens 4.1, Victorian Art Centre 3.6, Zoo 2.0.

• 41% Melbumians who had visited Sovereign Hill in last 12 months intended

to revisit within the next year:

•

•

Evidence of high satisfaction - visitors are much more likely to want to visit.

Overall, 2+ Years was the average horizon for another visit.

Exit surveys conducted at Sovereign Hill revealed an even higher level of

intention to return - such is the power of the visit:

46% in total, with 57% Victorians definite.

Interstate intentions were lower, primarily because of distance.

Sovereign Hill is a powerful attraction to many Australians:

Comparable with other major attractions.

The appeal is greater than that of the Goldfields measured separately ; although

Sovereign Hill will also be a factor in the desire to visit the Goldfields.

© I Ill I ~I]] Ballarat Marketing Strategy Oct 1995 20

\ ___ .

2.4.3 Visitation

• Sovereign Hill is by far the biggest attraction in Ballarat, free or pay to go:

The Ballarat Product Claimed Attendance Figures; only Sovereign Hill data is audited

Sov Hill + BOTSC Eureka Stockade

Kryal Castle Gold Museum

Begonia Festival Tourist Info Ctr

Royal Sth Street Scout Jamboree Ballarat Wildlife

100,000 74,400

68,000 50,000 52,000

38,000 28,000 25,000 .

17,000

191,000 172,500

355,000

The Ballarat Botanic Gardens The ABS Population Survey Monitor does not include the Ballarat Botanic Gardens. However, the estimate of 1.5m provided to BOA is most unlikely to be accurate.

511,000

World Dinosaurs Fine Art Gallery

Swap Meet Montrose Cottage Eureka Exhibition

Old Curiosity Shop Ballarat Cup

Golda's World Dolls Easter Festivals

Basketball Toum't

16,000 13,000

In 1993, the Royal Botanic Gardens in Melbourne was visited by 1.13 m people, in Sydney 1.08 m.

12,000 7,000 3,500 3,000

These were far higher than regional gardens. More than 100,000 but Jess than 250,000 is more probable for Ballarat Gardens.

Source: BTB, Sov Hill; BOA cannot verify any claims except Sovereign Hill

• Bearing in mind that nearly 3 million people visit Ballarat, the penetration of

most attractions is low:

The vast majority who visit - especially for VFR - do not use any attractions.

The festivals do well in a relatively short period, but are seasonal.

There are also a number of very small attractions with fewer than 500 visitors

per month, compared to Sovereign Hill with nearly 10,000.

Enhancements to the Lake and Gardens precinct may not change this status.

• Sovereign Hill is the only attraction of standing, capable of identifying

Ballarat as a worthwhile tourism destination.

© Im Im Im I Ballarat Marketing Strategy Oct 1995 21

(

( '-····'

• Sovereign Hill is significant at the national level:

Aust War Museum

Power House

SA Museum

Sovereign Hill

Qld Museum

Australian Museum

Vic Museum

Nat Sci & Tech Cntr

History Trust SA

0

Source: Council of Aust Museum Directors

Top 1 O Museums 1993/94

200,000 400,000 600,000

No of Visitors

% Market Share of Theme Parks in last 4 weeks (June 95)

Wonderland

Movieworld

Seaworld

Sov Hill

Dreamworld

Wet'n Wild

Currumbin Bird

Old Syd Town

Gumbuya Park

Aus Wildlife Pk

Lone Pine Sanct

0

Source: RMR Theme Park Monitor June 96

5 10 15

% Visited

© [~I Iii@] Ballarat Marketing Strategy Oct 1995

931,428

800,000 1,000,000

21.1

20 25

22

.~

.~

.~

• Sovereign Hill counts as fourth biggest museum and theme park nationally

and is by far the most significant man-made, pay-to-go attraction in Victoria.

• Even among international visitors, Sovereign Hill is a strong performer:

Phillip Island Penguin Parade

187,621

Sovereign Hill

107,756 107,056

84,162 84,780

1989 1990 Source: BTR-IVS

Victorian Attractions International Visitors

216,981

12 Apostles I Great Ocean Road

111,945 90,63S

1991 1992

121,341

2,535

1993

264,988

136,768

114,000

1994

• Philip Island and the penguins continue to strengthen, with an excellent 2

year trend; although share of visitors is falling.

• Sovereign Hill's share of inbound visitors is falling even faster and has been

overtaken by Great Ocean Road.

Neither Ballarat nor Sovereign Hill is keeping up with the rapidly growing

inbound market.

These trends are primarily distribution driven; the Penguins and GOR are often

features of pre-purchased tour arrangements.

Tourism Victoria has considerable influence on this process.

© ~ Ballarat Marketing Strategy Oct 1995 23

( ___ .;

2.4.4 'Trial' & Repeat Frequency (data on Sovereign Hill only)

• Access has been arranged to the AGB Theme Park Monitor carried out in

Mar/Apr 1992 on a national sample of 4156 people aged 14 years and over:

After the transfer to RMR, the format was changed and ever visited I frequency

and motives were no longer included; this is the latest available data.

This study was conducted after the opening of Movieworld but before the start of

'Blood on the Southern Cross' (Jan 1993).

• 'Ever visited'/ trial of Sovereign Hill is extremely high, especially in Victoria:

% Ever Visited Total NSW/ VIC QLD SA ACT

Sea World 53 49 43 l~~j!,~§;tt~\\ 42

Sovereign Hill 39 17 ;t,~i~~~~~1 ~~~~~~: 14 75

Old Sydney Town 35 ::~;~~~t~~~~~/~~ 16 22 25

• Sea World is the most visited theme park, it has been there longest:

•

It is also situated in the centre of a major holiday tourism region supported with

massive infrastructure, far greater than will ever exist for Victoria.

But 80% of Victorians have ever visited Sovereign Hill compared with lower

proportions of home state residents sampling Old Sydney Town & Sea World.

Sovereign Hill reached a ceiling of trial three years or longer ago.

6 month share of the state market is also very strong for Sovereign Hill:

% Visits last six Total months

Sea World

Sovereign Hill

Old Sydney Town

NSW/ ACT

VIC QLD SA

• Sovereign Hill captured 30% of all the visits made by Victorians to theme

parks, by far the highest; also no 1 for South Australians too.

© ~ Ballarat Marketing Strategy Oct 1995 24

"'--··

• But the frequency reported in the last 6 months was lower than other parks:

Average visit Total frequency (state

last six months data n/a)

Sea World 1.3

Sovereign Hill 1.2

Old Sydney Town 1.5

Wonderland 1.6

AGB (1992 SH survey) found that "Melbourne ever-visited" averaged 2.2 times

Only 17% had visited four+ times, these accounted for a quarter of all visits.

Exit surveys in 1995 suggested that 47% of all visitors (including inbound) were

on their first visit, but 37% had been 3 or more times (Vic visitors: 17% and 50%).

• Visits tend to be spaced over many years, regardless of origin:

70% of visits had been more than 3 years ago, over 25% more than 10 years.

Time elapsing between visits is growing: 12 months 16%, 1-2 years 22%, 3-4

years 27%, 4+ years 34%; however this may also be the growth effect.

• Sovereign Hill conforms to the familiar cyclical pattern of theme park

visitation, with frequent new 'rides' necessary to achieve revisits:

•

18 months after spending $83M on Movieworld, the new Batman ride cost $12M

and now a new roller coaster is being built.

Regular reinvestment is necessary to maintain market share although more

profit can often be made on a lower level of higher spending visitation.

The majority of visits from Victoria are made by car, mainly at weekends,

arriving before midday, with an average stay of 4.8 hours.

• Theme park rule of thumb is that 80% of the visitors are in the park by midday.

• Overall, a visit to Sovereign Hill 'lasts longer' than to similar attractions.

© [il1Jiiijj} Ballarat Marketing Strategy Oct 1995 25

{ \

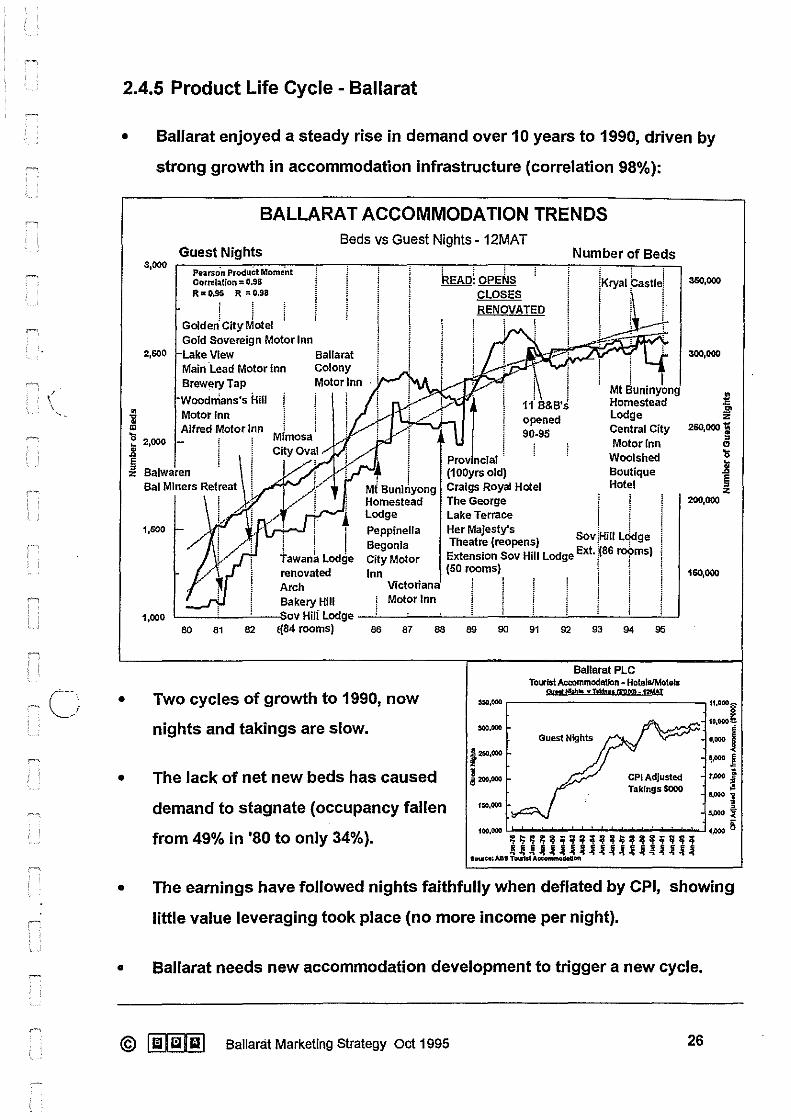

2.4.5 Product Life Cycle - Ballarat

• Ballarat enjoyed a steady rise in demand over 10 years to 1990, driven by

strong growth in accommodation infrastructure (correlation 98%):

•

•

BALLARAT ACCOMMODATION TRENDS

Guest Nights Beds vs Guest Nights - 12MAT

3,000 Pearso"n ProcluCt Mome.nt Correlation= 0,98 R•0.95 R =D.98

! ! Golden· City Motel Gold Sovereign Motor Inn

2,600 Lake View Ballarat Main ·Lead Motor Inn Colony Brewery Tap Motor Inn

Woodnians's km i! Motor Inn ~ Allred Motor Inn ~ 2,000 .8 § z Balwaren

Bal Miners Retreat

! 1,600 --'..f~·

. ! I tawan~ Lodge renovated Arch Bakery Hill

, I Mi Buniriyong Homestead Lodge Peppinella Begonia City Motor Inn

Victoriana ! Motor Inn

CLOSES RENOVATED

11' B&B'J opened 90-95

(1 OOyrs old) Cralgs Royal Hotel The George Lake Terrace

Number of Beds

! I Mt Buninyong Homestead Lodge Central City Motor Inn

Wool shed Boutique Hotel

Her Majesty's ; . ; Theatre (reopens) Sov !Hiii L<j<lge Extension Sov Hill Lodge Ext. ;(86 1"09ms)

I ! (50 rooms) \ :

f ! ! ! !

360,000

300,000

160,000

1,000 ~-~-~--o.ov Hili Lodge-~-~-~-~~-~-~---~-~~ 80 81 82 i(84 rooms) 86 87 88

Two cycles of growth to 1990, now

nights and takings are slow.

The lack of net new beds has caused

demand to stagnate (occupancy fallen

from 49% in '80 to only 34%).

89 90 91 92 93 94 95

Ballarat PLC Tourist.Accommodation~ HotelslMote&I

~---=™="~"""~·=·'=""~·~·rro~M=-'~""'=r:___~ *·000 ::::~ "'·""

l2$l,OOO

• 1 a 200,000 CPI Adjusted Takings $000

•ooo J , ... ~ 7,000 i

~ ..,, 1

' 15,000 ~

100,000 u-.................... - ................. _._ ............. ......., 4,000 &

• The earnings have followed nights faithfully when deflated by CPI, showing

little value leveraging took place (no more income per night).

• Ballarat needs new accommodation development to trigger a new cycle.

© l:!!!Tu!JBJ Ballarat Marketing Strategy Oct 1995 26

(

-~

2.4.6 Product Life Cycle - Sovereign Hill

• Sovereign Hill displays a classic Product Life Cycle, with 'Blood on the

Southern Cross' arriving on cue to extend the maturing cycle:

•

SOVEREIGN HILL: VISITOR TRENDS Annual Visits '000

550 ,--~~~~.,--~...,.-~~~~~-.~~~,,---~~~~~~~~~~~~-

500

450

400

INTR

350

. . •

• ' ' • ' . . • • • Sovereign Hill (Incl BOTSC) .. ~ . ... · :

•' . .. • • •• .. •

• ,.-i· ............. _ .. "/····· :

•'' : ·' : . -· • • • • • • .'· : ' • • Sovereign Hlll (Exel BOTSCJ

-~ : : .• ~ - I .... : : :

: : : . . ' . . ' • • • • • • Cycle 1: 10 yrs· : : : ' : Cycle 2: 1s vrs to date .>- : • - -

~-'--~~~·~ --:''--~~~~--...... ----~·:-----·------·;------~·:--------1--GROwrH : ir

• ::::J "' 3 :~

72fl3 74

DECLINE 6

RE-ENTRY : GROWlli 3 5

MATIJRITY ; DECLINE 3 : 4

• 76fl7 78179 BOl81 62183 84185 86J87 88189 90J91 9293 94195

Sovereign Hill is now passed the maturity phase, with strong support from

BOTSC as underlying demand for the main park cycles down.

Energetic management and creative re-investment has extended the cycles and

avoided stagnation; but in 1996, it will be time for another re-entry.

There are barriers to visitation rising above the present levels:

Lack of critical mass of attractions, low preference for Ballarat and the

Goldfields and remoteness from a large tourist centre (cf Gold Coast).

And BOTSC has confirmed that repeat visits can be attracted by new shows.

© ~ Ballarat Marketing Strategy Oct 1995 27

r··

~.

( r~

2.4.7 Visitation Product Life Cycle - Sovereign Hill & Ballarat

• Overlaying the Ballarat cycle on Sovereign Hill shows a close correlation:

•

550

500

450

400

350

300

INTR

SOVEREIGN HILL: VISITOR TRENDS Annual Visits '000

Pearson Product Moment Correlation 0.82

Cycle 1: 10 yrs ,./ • t ,/ . . ,

Sovereign Hill (Incl BOTSC) ' ' ' L···· .... ... .. ' .. ' . ' .. ' . '

, .. .\.-' -. •

' ' ' . • • • . •

_,, .. .-·-·•"": ........ -····-········-

:sanarat Visitor Nights :(Accommodation Base) . . • • ' . ' . ' . ' . • • • • • • • • . • .

• Cycle 2: 1s yrs to date :~ : _, .. /·

~-GROWTH----~@~-,-~~.'---O-E-CL-IN-E---,ji-R-S-ENTR---Y~:--G_RO_WTH ______ :,__M_/\f_U_R_ITY_,..: __ o_E_CL-IN_E __ 4

3 :!< ·: 6 3: 5 : 3: 4 250 ~~~~~·~ ~~~~~~~~~~~·~~~~~~·~~~~·~~~~~

72fi3 7..,,~ 76177 76179 80/81 82183 84185 86187 88189 90/91 92133 94195

It is apparent that the lack of new accommodation infrastructure may have

limited the growth of the BOTSC initiative, despite the low occupancy:

Because of the late finish to the show, it is demanding of accommodation.

This is not a matter of physical room to sleep, rather the experiential appeal of

interesting new places to stay; as much a part of the experience as the show.

The lack of investment in Ballarat may have made the destination less attractive

than other places ·such as Melbourne - with plenty of new product.

• This slowness to build appealing new beds - added value beds - may also

have limited Ballarat's ability to exploit the surge in intrastate tourism.

© I El I llJ [@ Ballarat Marketing Strategy Oct 1995 28

·r~

,~

(

2.5 Market Forecast

2.5.1 Domestic

• Domestic non business tourism is forecast to grow at an average annual

rate of 1.9%; 5 million more domestic trips are forecast by 1999 on 1993:

Forecast of Domestic Tourism '000,000 Trips

85 86 87 88 89 90 91 92 93 94e 95e 96e 97e 98e 99e Total - 45 45 45 47 46 50 49 48 48 49 50 51 52 53 54 NonBusineS&o 38 39 38 40 39 43 41 40 40 41 42 43 43 44 45

Sou~e: Tourism Forecasting Council Aug 1994

• The BTR finds6 that tourism activity is related to real household disposable

income and unemployment-1% more income gives 0.4% more tourism.

•

6

The resulting straight line forecast should be treated with caution:

Surges in activity and changes to pattern are also driven by changes to the

relative attractiveness of destinations, especially from new infrastructure.

Examples include the 'Spirit of Tasmania' for Tasmania, Movieworld for the Gold

Coast & the Casino for Melbourne; visitation is the outcome of trial and revisit .

Tourism Forecasting Council - domestic forecast August 1994

© 00 Ill I ril I Ballarat Marketing Strategy Oct 1995 29

(

2.5.2 Inbound

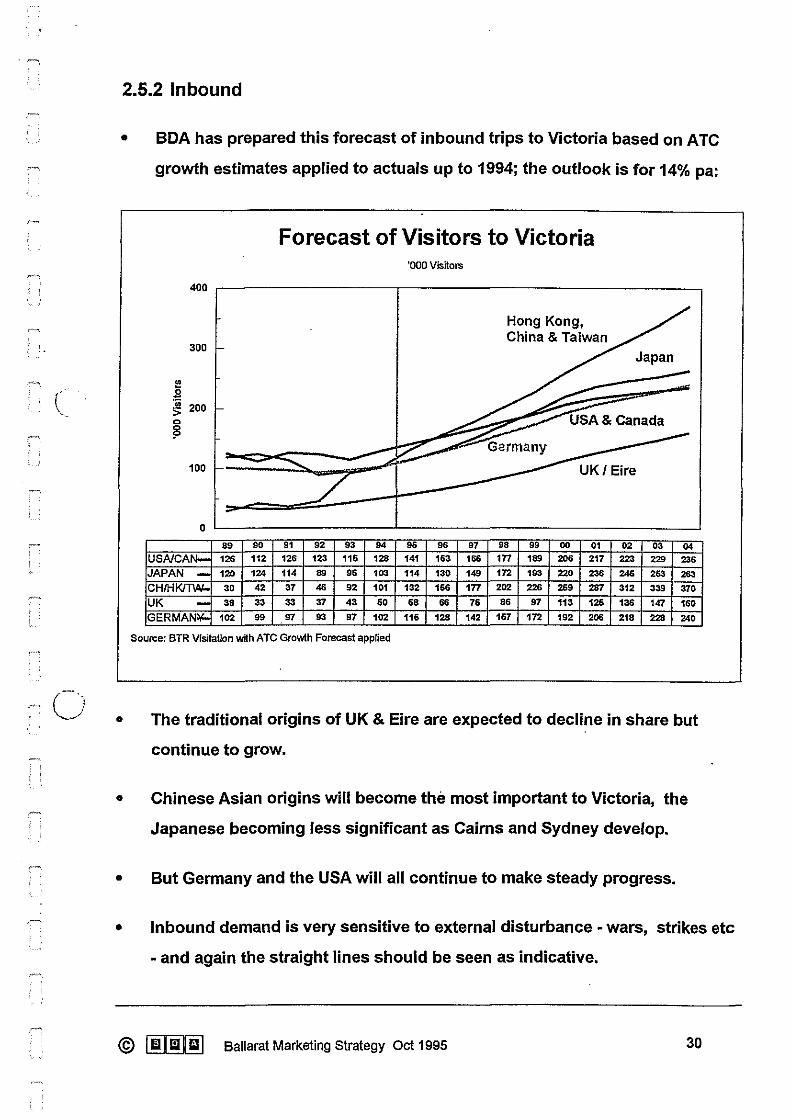

• BOA has prepared this forecast of inbound trips to Victoria based on ATC

growth estimates applied to actuals up to 1994; the outlook is for 14% pa:

Forecast of Visitors to Victoria

~ .9

300

~ 200 0

~

100

USNCAN-JAPAN -CH/HKf!W.. UK -GERMANl.<.

89 90

126 112

120 124

30 42

38 33

102 99

91 92 93 94

126 123 116 128

114 89 96 103

37 46 92 101

33 37 43 60

97 93 97 102

Souroe: BTR Visitation with ATC Growth Forecast applied

'000 Visitors

96 96 97

141 163 166

114 130 149

132 166 1n

68 66 76

116 128 142

Hong Kong, China & Taiwan

98 99 00 01 1n 189 206 217

172 193 220 236

202 226 269 267

86 97 113 126

167 172 192 206

02 03 04 223 229 236

246 263 263

312 339 370

136 147 160

218 228 240

• The traditional origins of UK & Eire are expected to decline in share but

continue to grow.

• Chinese Asian origins will become the most important to Victoria, the

Japanese becoming less significant as Cairns and Sydney develop.

• But Germany and the USA will all continue to make steady progress.

• Inbound demand is very sensitive to external disturbance - wars, strikes etc

- and again the straight lines should be seen as indicative.

© l!!J II.I 00 Ballarat Marketing Strategy Oct 1995 30

~

,., /

r \_,

r'

,~

2.6 Implications

• Ballarat visitation benefits from the presence of Sovereign Hill, one of

Australia's main man made attractions and a leading one in the State.

• Festivals and events concentrate visitation into seasons but otherwise the

Ballarat product comprises many low profile attractions.

•

•

•

•

Ballarat tourism has grown with the development of infrastructure but over

the last five years this has slowed, causing stagnation in the local industry.

This lack of fresh product appeal has possibly prevented Ballarat from

exploiting the rise in intrastate tourism to the fullest extent.

Sovereign Hill achieved a remarkable penetration of Victorians (over 80% &

39% of Australians) and a high market share (30% of Vic visits) in 1992.

The growth since then from the new investment in 'Blood on the Southern

Cross' shows that revisits and new visits have been successfully won.

• .It also shows that relevant re-investment works as well for Sovereign Hill as

well as for other theme parks; no investment results in decline.

• Although the management of the Sovereign Hill Cycle has been masterful,

there are clear signs that a new 'trigger' will be required soon.

• Even with a new trigger, Sovereign Hill visitation will depend on external ·

critical mass factors - on all the other things to enjoy in Ballarat.

• Equally, the appeal of Ballarat will depend to a great extent on the

performance and vigour of its main attraction - Sovereign Hill.

• Outlook for tourism growth is strong; intrastate tourism will always provide

the critical volume, with interstate, Asia, UK and USA providing support.

© I Ill Im Im I Ballarat Marketing Strategy Oct 1995 31

~

f

~

'"'~--

~,

r' \

r'""'\

3. VISITOR TRENDS

3.1 Origin (at least 1 night, non-business, 40 kms +from home)

3.1.1 Domestic Tourists - Goldfields

• Australian visitors to the Goldfields come mainly (89%) from Victoria:

•

•

Domestic Visitors to Goldfields 1993/94 %SHARE

Melbourne 693 50.1%

Vic C'try 39.4%

NSW/ACT 5.3%

SA 2.8%

QLD 1.5%

WA 10 INTERSTATE 0.4% ACCOUNTS

Tasmania 4 FOR ONLY 10.5% 0.4%

NT 1 0.1%

0 200 400 600 800

'000 Trips Source: BTR-DTM

Melbourne contributes half the visitors, which is normal for regional centres •

Interstate tourism is related more to the relative population size of the origin

State:

© I Ill I w I t:i1 I Ballarat Marketing Strategy Oct 1995 32

•

0 0 ?

The Goldfields trend is encouraging, with growth of around a third, and

Melbourne is supplying more and more visitors:

Domestic Trends Trips to Victorian Goldfields Region

1,300 ~-----------~

1,200

Domestic Trends Trips to Victorian Goldtields Region by Origin

BOO

700 693

§ 1,100

l • ~ .. c ~

0 0

,g 1,000 l'l. ;:

900

Victorian Goldfields Region

800 '--'---------'--------'-' 1992 1993 1994

200

146 -104 100 INTERSTA E -·~------~-----~ 91/92 92/93 93/94

~~BTR-OTM sourc.; BTR-NS

This trend is subject to a very small sample and is liable to fluctuation, so

should be treated as indicative only.

Although no formal tracking is undertaken, Melbourne provides an even higher

proportion of day trips, contributing the bulk of visitors.

• The recent lift in Sovereign Hill may have boosted the Goldfields appeal:

BOTSC prompting VFR reunions.

Promotion which increased conversion of Goldfields preference relative to other

destinations in Victoria.

© I Ill I Ill[~ Ballarat Marketing Strategy Oct 1995 33

~

n

.~

'

"

3.1.2 Domestic Tourists - Sovereign Hill

• Melbourne is also the prime source of domestic visitors:

VIC

Melbourne

Vic Country

Ballarat

NSW

NSW Country

Sydney

SA

QLD

Rest Of Aust

Domestic Visitors to Sovereign Hill Share of domestic visitors, 1994/95

INTERSTATE ACCOUNTS FOR24.4%

OF DOMESTIC VISITORS

S~urce: Sovereign Hill postcode analysis

75.6

• Ballarat residents account for 11% of visitors and a good proportion of them

would be hosting a friend or relative.

• Note that visitors from interstate to Sovereign Hill account for a quarter of

domestic visitors, compared to only 11 % of those staying in the Goldfields.

This may show the pulling power of SH into the region, but the difficulty of

comparing day trips with overnight mean this cannot be conclusive.

NSW is the main interstate origin, well ahead of Qld, the home of theme parks.

Vic Country provides twice as many visitors as NSW, emphasising the

importance of the local market.

However, the preference for Sovereign Hill in NSW particularly is not being

converted, a lost opportunity for Victoria.

© ~ Ballarat Marketing Strategy Oct 1995 34

, '

3.1.3 Inbound Tourists - Goldfields & Sovereign Hill

• This chart compares Sovereign Hill with the Goldfields:

ASIA (Ex Japan)

Europe

UK & Ireland

USA/Canada

Japan

New Zealand

Other

Source: BTR-IVS

International Visitors Goldfields vs Sovereign Hill

33.3

Goldfield: 30,000 Sovereign Hill:114,000

'000 Visitors

• Goldfields • Sovereign Hill

• Although a day visit not an overnight stay, Sovereign Hill is nearly four times

~ (__ more popular than Goldfields, especially strong with Asians.

International Visitor Trends

• Goldfields, on the other hand, Victorian Goldflelds vs Sovereign Hill

30.5 120

appeals strongly to visitors to " 30.0

ii 1 115

Europe and New Zealand, c 29,5 ~ j ~

thanks to the VFR connections. .. 21.0 110 5

~ 107 107 I c

" ;g 29.5 105 .s

" " • Both destinations are following ~ 2B,O ~ ~ > , ..

a similar trend, recovering from 27,5

27.0 .. the dip in 1991: 1989 1990 1991 1992 1993 1994

.. in•:ITA.M.,ttt ..

© ™ Bailarat Marketing Strategy Oct 1995 35

(

• Overseas visitors account for a quarter of Sovereign Hill visitors - not that

far off Melbourne residents:

Origin of Visitors to Sovereign Hill 1994/95

Melbourne

Overseas

Vic Country

NSW

Balla rat

Sth Aust

Queensland

Rest of Aust

0 5 10 15 20 25 % of Visitors

Source: Sov Hill

Excludes Don't Know etc

• Although the performance with

Asians has been strong, share

of other origins has been variable:

•

•

European demand is strong, but j • visitors from the UK /Ireland are

tending to fall away.

And from USA/Canada, a clear

decline compared to Victoria.

•

lntematlonal VS.ilor Tr.nchi

--""'-"-'""_w_-_"' __ D8!

1111 1fft '911 1HZ UU UM

-

29.6

30 35

ltc!emiltlonal \lb.Hor Trends _,._,,.

• The appeal of Sovereign Hill to people from these countries may be a shared

historical perspective and culture.

@ [!)Ill I!] Ballarat Marketing Strategy Oct 1995 36

( '

(

3.1.4 Visitors to Ballarat

• In 1991 & 1995, the University surveyed visitors to Ballarat; different

methodologies and time periods invalidate direct comparisons:

In 1991 there was face to face sampling at the Tourism Centre, the Lake & Bridge

Mall in Sept/October of 270 visitors; an overweighting to locals occurred.

In 1995, self completion forms were distributed from accommodation,

attractions, retail & info centre; overweighting to overnighters occurred (80%}.

The graphic is more revealing of the different profiles of the samples than of any

changes between the years:

Visitors to Ballarat by Origin % responses; 1991 - face to face, ex Gold N=270; 1995 self completion N=434

Melbourne

Country Vic

Interstate

Overseas

• 1991 • 1995 Source:BTA Survey 1991

• Melbourne provides the most visitors in each sample and the strong

presence of interstaters in the 1995 sample shows the national appeal of

Ballarat.

© ~ Ballarat Marketing Strategy Oct 1995 37

(

3.2 Group Type Inbound (This information not available for domestic tourism)

• Sovereign Hill welcomes more groups, a benefit of the inbound distribution

systems; these groups are mainly pre-sold through wholesalers:

•

International Visitors

Group Tours 5 Year sample 1989-93

Holiday group

International Visitors

Travel Party 5 Year sample 1989-93

11.0 Unaccompanied

Adult Couples

Friends/Relatives

39.5

39.9

Sporting/special int • Goldfields

Other Group Tour

% of Visitors Source: BTR~VS : Note Goldfields 2 year sample

Parents & children

Bus associates 1.6

1.2

% of Visitors Source: BTR~IVS : Note Goldfields 2 yr sample

Both destinations are very strong with the so-called 'FIT' or independent

traveller - accounting for 40% of visits.

• There are few children and family groups - reflecting the distance and cost

involved in reaching Australia.

Note: Interpretation must bear in mind that Sovereign Hill is recorded as a day trip, Goldfields as an overnight destination. Also, that this data is derived from an average of 5 years combined results.

© [!l I iu lil] Ballarat Marketing Strategy Oct 1995 38

~'

3.3 Purpose of Trip - Goldfields

• VFR looms large as a reason for visiting the Goldfields:

•

Domestic Visitors to Goldfields Main Purpose of Trip

93194

VFR

Holiday

Business VFR: 463,000 Holiday: 428,000 Total: 1,264,000

Convention 1.8

Other 19.2

% of Trips Soun:o: BTR-DTM

International Visitors to Goldfields Main Purpose of Trip

2 yr ave to 1993

VFR

Holiday

Business VFR: 7,400 Holiday: 15,500 Total: 28,000

Convention 1.5

Other 7.6

% of Trips SOurce: BTR-IVS

At 37%, domestic VFR is higher than the Victorian average of 29%:

55.

Residents become effectively tour guides, organising entertainment for their

visitors.

'Other' reasons are also high, includes sporting & special events (Vic 15%)

• For inbound, 27% VFR is a very high proportion (Victorian average 18%).

• Although convention is a very small 'reason', both for domestic and

inbound, the Victoria domestic average is only 1.8% and inbound 2.3%.

© ~ Ballarat Marketing Strategy Oct 1995 39

3.4 Purpose of Trip - Sovereign Hill

• International visitors to Sovereign Hill are mainly on holiday:

International Visitors to Sovereign Hill Main Purpose of Trip

VFR

Holiday

Business

Convention 0.9

Other

Source: BTR~VS

9.6

1994

VFR: 24,400 Holiday: 65,600 Total: 105,000

· % Visitors

63.2

• Sovereign Hill sees more international VFR than the Victorian average, but

this is less than the Goldfields.

• Business, convention and other reasons are also under represented.

• Sovereign Hill is a powerful attraction to bring international visitors to

Ballarat, which the City would never have otherwise.

© Im I Ill I fil I Ballarat Marketing Strategy Oct 1995 40

r

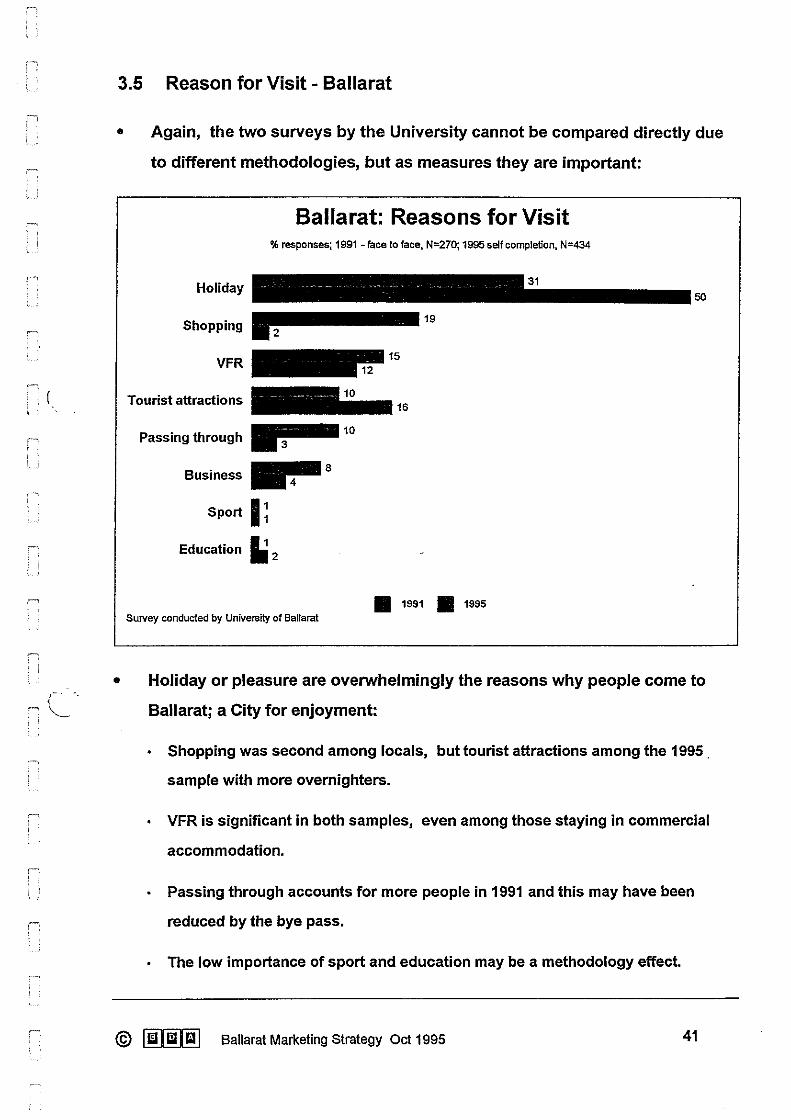

3.5 Reason for Visit - Ballarat

• Again, the two surveys by the University cannot be compared directly due

to different methodologies, but as measures they are important:

•

Balla rat: Reasons for Visit % responses; 1991 -face to face, N=270; 1995 self completion, N=434

Holiday

VFR-- 15 -12

Tourist attractions --. 16

-3 10 Passing through - 3

Business ... 8

Sport I~

Education 11 2

Survey conducted by University of Ballarat • 1991 • 1995

31 -·50

Holiday or pleasure are overwhelmingly the reasons why people come to

Ballarat; a City for enjoyment:

Shopping was second among locals, but tourist attractions among the 1995 .

sample with more overnighters.

VFR is significant in both samples, even among those staying in commercial

accommodation.

Passing through accounts for more people in 1991 and this may have been

reduced by the bye pass.

The low importance of sport and education may be a methodology effect.

© 00 Ii.I I g J Ballarat Marketing Strategy Oct 1995 41

r~

r~

3.6 Seasonality

• Sovereign Hill and Ballarat have different seasonalities:

12

!!! 0 :!::

"' > 10 ... 0 ::!;! 0

:>. :c - 8 c 0 :E

6

Ballarat Seasonality Tourist Accommodation v Sovereign Hill

Guest ArrivalsNisitors - 4 year average

ourist Accommodation 12.4

Sovereign Hill

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

\~ • Winter in Ballarat is not the best time of year for tourism, nor is February

after the schools have gone back.

• But Sovereign Hill has a huge January, while the City is busiest in October -

springtime.

• And Easter is much better for the Park than the City, thanks to school

holidays and those wonderful autumn daytrips.

• However, this pattern is changing.

© I Ill I Ill Im I Ballarat Marketing Strategy Oct 1995 42

(

c_-

• Ballarat has seen a lower proportion of visits occurring in January:

12

e 10 Ill ..c IJ)

>. . :c .... 8 c 0 :E '#.

6

4 Jul

91/9l- 8.1

92/9l- 7.7

93/9- 8.0

Ballarat Seasonality Tourist Accommodation Basis

Guest Arrivals

- .,,_ "' ~~ Royal South " ·-"' ~ "'"- c > "' 0·- s~ Street Festival 'iii "' <1>

Cl-

"' "' ;:: "' <1> "' Dl if &! if Dl (I) :;:

Aug Sep Oct Nov Dec Jan Feb Mar 7.1 8.5 11.2 8.4 6.2 11.2 7.1 9.0 6.7 8.1 12.2 8.6 6.6 9.7 7.2 9.1 6.5 8.4 11.5 8.6 7.0 8.3 6.6 9.4

Source: ABS Tourist Acconmodation

-_c - "' "'E £! "' ~E "' :i "'0 ED I-

Apr May 9.3 7.2

9.7 7.9

Jun 6.7

6.6

• The impact of Ballarat special events can be clearly seen on this chart.

• The sustained fall off in the main holiday month, which accounts for 16% of

Victorians holidays, is a threat, especially in a rising holiday market.

• Sovereign Hill is also very dependant on this month and increased visitation

by 7,800 in January 1994 compared to 1993.

• A certain lack of synergy between Ballarat and its' major attraction may be

revealed by this trend.

© [ii] ll1 I Iii I Ballarat Marketing Strategy Oct 1995 43

r-

(

(__~;

3.7 Distribution

• The RMR pilot study of how people choose, book and plan their holidays

(June 1995 - 752 nationally) helps understand the distribution priorities:

•

Holiday Decision Influences -Choosing(%)

No Info

Been before

Friend/Rel lives

Friend/Rel visited -17

Direct o

AgenUairtinelRAC

Brochures -12

Books -11

TV/Radio/Print • 6

State Tour Info 14 Tour Operator I 2

Other 12 Source: RMR June 1995, N = 752

Choosing:

32

20

Holiday Decision Influences - Booking(%)

No Info

Been before o

Friend/Rel lives o

Friend/Rel visited o

Direct

AgenUairline/RAC

Brochures o

Books o

TV/Radio/Print o

State Tour Info I 2

Tour Operator I 1

Other la Source: RMR June 1995, N = 752

29

29

36

The majority of information comes from previous personal experience and word

of mouth from friends or relatives who live there or have visited • 78% mention.

The selection process is outside the direct influence of tourism marketers; the

place itself and every visitor or resident is the most influential sales tool.

Agents and brochures are used by about a third and media by about 10%.

Ballarat visitors are also most influenced by word of mouth and previous visit

(80% of cases) before the trip (University 1995).

© I Ill I r:J I Iii J Ballarat Marketing Strategy Oct 1995 44

c '·-

• Booking:

•

Nearly 40% of people do not book - jump in the car and go to friend or relative.

As many people book direct as book through agents.

Holiday Decision Influences -Planning Before(%) Holiday Decision Influences - Planning During(%)

No Info 55 No Info 36

Been before • 7 Been before -16

Friend/Rel lives • 9 Friend/Rel lives -17

FriendJRel visited 1 s Friend/Rel visited o

Direct o Direct o

AgenUairfinelRAC .11 Agent/airlineJRAC • 6

Brochures .11 Brochures -16

Books .7 Books .9

lV/Radio/Print 12 lV/Radio/Print • 9

State Tour Info - 14 State Tour Info • s

Tour Operator I 2 Tour Operator 14 Other I 1 other I 1

Source: RMR June 1995, N = 752 Source: RMR June 1995, N = 752

Planning Before:

Also very little controllable information, mainly experience or nothing;