BALFOUR BEATTY PLC RESULTS FOR THE FULL Following dividend reinstatement recommended final dividend...

64

BALFOUR BEATTY PLC RESULTS FOR THE FULL-YEAR ENDED 31 DECEMBER 2016 16 March 2017 Financial Highlights · Order book £12.7bn, up 15% (up 4% at constant exchange rates (CER)) · Underlying revenue £8.5bn, up 4% (down 3% at CER) · Group returned to profit following two years of losses; underlying profit from operations (PFO) £67m · In the second half of 2016 UK construction returned to underlying profitability · Strong balance sheet: net cash at £173m, underpinned by £1.2bn Investments portfolio · Following dividend reinstatement recommended final dividend of 1.8 pence per share (full year 2.7 pence) Build to Last Highlights · Significantly exceeded 24-month Phase One targets – £439m cash in: £123m cost out · Continued to simplify the Group; exiting non-core assets · Upgraded leadership and de-layering of management in UK and US · Improving risk management and order book from strengthened governance · Increased customer satisfaction · Favourable medium and long term market outlook · Reiterated Phase Two targets: industry-standard margins by end of 2018 (£ million unless otherwise specified) 2016 2015 Underlying 3 Statutory Underlying 3 Statutory Revenue 1,2 8,530 6,923 8,235 6,955 Profit (loss) from operations 2 (PFO) 67 15 (106) (182) Pre-tax profit (loss) 2 60 8 (123) (199) Total profit (loss) 48 24 (135) (206) Profit (loss) per share 7.0p 3.5p (19.8p) (30.1p) Dividends per share 2.7p - 2016 2015 Order book 1,2,3 £12.7bn £11.0bn Directors' valuation of Investments portfolio 1,220 1,244 Net cash – recourse 173 163 Net borrowings – non-recourse (233) (365) Leo Quinn, Group Chief Executive, commented “The transformation of Balfour Beatty is well underway. We have returned the Group to profit and significantly exceeded our Build to Last Phase One targets. We have upgraded leadership, processes and controls while continuing to invest in the Group’s unique strengths. As a result, we have improved not just the quality of our order book but our customer satisfaction scores. “Having simplified the Group, we are focused on our core markets in the UK and US, where governments are committed to large scale expenditure on infrastructure. “All this positions us for future profitable growth. During the next two-year phase of Build to Last, we expect to achieve industry- standard margins and over the medium term, industry-leading performance.”

Transcript of BALFOUR BEATTY PLC RESULTS FOR THE FULL Following dividend reinstatement recommended final dividend...

BALFOUR BEATTY PLC RESULTS FOR THE FULL-YEAR ENDED 31 DECEMBER 201616 March 2017

Financial Highlights

· Order book £12.7bn, up 15% (up 4% at constant exchange rates (CER))

· Underlying revenue £8.5bn, up 4% (down 3% at CER)

· Group returned to profit following two years of losses; underlying profit from operations (PFO) £67m

· In the second half of 2016 UK construction returned to underlying profitability

· Strong balance sheet: net cash at £173m, underpinned by £1.2bn Investments portfolio

· Following dividend reinstatement recommended final dividend of 1.8 pence per share (full year 2.7 pence)

Build to Last Highlights

· Significantly exceeded 24-month Phase One targets – £439m cash in: £123m cost out

· Continued to simplify the Group; exiting non-core assets

· Upgraded leadership and de-layering of management in UK and US

· Improving risk management and order book from strengthened governance

· Increased customer satisfaction

· Favourable medium and long term market outlook

· Reiterated Phase Two targets: industry-standard margins by end of 2018

(£ million unless otherwise specified)2016 2015

Underlying3 Statutory Underlying3 Statutory

Revenue1,2 8,530 6,923 8,235 6,955Profit (loss) from operations2 (PFO) 67 15 (106) (182)Pre-tax profit (loss)2 60 8 (123) (199)Total profit (loss) 48 24 (135) (206)Profit (loss) per share 7.0p 3.5p (19.8p) (30.1p)

Dividends per share 2.7p -

2016 2015

Order book1,2,3 £12.7bn £11.0bn

Directors' valuation of Investments portfolio 1,220 1,244

Net cash – recourse 173 163

Net borrowings – non-recourse (233) (365)

Leo Quinn, Group Chief Executive, commented “The transformation of Balfour Beatty is well underway. We have returned the

Group to profit and significantly exceeded our Build to Last Phase One targets. We have upgraded leadership, processes and

controls while continuing to invest in the Group’s unique strengths. As a result, we have improved not just the quality of our order

book but our customer satisfaction scores.

“Having simplified the Group, we are focused on our core markets in the UK and US, where governments are committed to large

scale expenditure on infrastructure.

“All this positions us for future profitable growth. During the next two-year phase of Build to Last, we expect to achieve industry-

standard margins and over the medium term, industry-leading performance.”

Notes:1 including share of joint ventures and associates2 from continuing operations3 before non-underlying items (Note 8)

Alternative performance measures (APM), including constant exchange rates (CER), are defined in the section Measuring Our

Performance.

Investor and Analyst enquiries:Angus Barry

Tel. +44 (0)20 7216 6824

Media enquiries:Louise McCulloch

Tel. +44 (0)20 7216 6846

Investor and Analyst presentation:A presentation to investors and analysts will be made at Numis Securities, The London Stock Exchange Building, London EC4M

7LT at 09:00 (UK time) on 16 March 2017. There will be a live webcast of this presentation on: www.balfourbeatty.com/webcast

2016 FULL-YEAR RESULTS ANNOUNCEMENT

· GROUP CHIEF EXECUTIVE’S REVIEW

· RESULTS OVERVIEW AND OUTLOOK

· BUILD TO LAST

· DIVISIONAL OPERATING REVIEWS

· OTHER FINANCIAL ITEMS

· MEASURING OUR PERFORMANCE

GROUP CHIEF EXECUTIVE’S REVIEW

The Group’s results for 2016 demonstrate that the fundamental changes made under Build to Last are driving positive and

sustainable improvements. Balfour Beatty has returned to profit, while increasing both the value and the quality of its order book

through disciplined bidding. The £200 million cash in and £100 million cost out targets have been delivered – enabling the Board to

reinstate the dividend as promised – and were significantly exceeded by the end of Phase One.

The Build to Last transformation programme launched at the start of 2015 addresses Balfour Beatty’s performance with all

stakeholders – customers and suppliers, employees and subcontractors, investors and communities. Targets were set against four

objectives: building a business which is Lean, Expert, Trusted and Safe. The first phase – a 24-month self-help plan – has just

delivered its goals, tackling the root causes of previous poor performance in order to provide a strong platform for future profitable

growth.

In UK construction, the Group met its year-end target, with 90% of the legacy projects having reached practical completion and

over 70% having reached financial completion. Importantly, the UK construction business reported an underlying profit from

operations in the second half of the year.

By 2014 Balfour Beatty had become overly complex following more than a decade of acquisition-led forced growth. There was an

overall lack of leadership and strategic direction. Operationally, project bidding and delivery lacked standard processes and internal

systems and controls were weak with little focus on cash management. A federated culture had resulted in layers of unnecessary

cost and a tendency for elements of the business to compete with one another. Inevitably, performance had deteriorated not only

financially but in terms of customer and employee satisfaction.

The decisions and actions taken under Build to Last were often, in themselves, simple and straightforward. However, taken early

and in combination, they are now transforming Balfour Beatty. The introduction of new standardised disciplines has strengthened

governance and transparency. The upgrade in leadership and the Group’s simplified structure, with shared back office functions,

have enabled the business units to focus on their core markets while benefiting from a more competitive cost base. Stronger

finance and IT systems have helped drive leaner management of cash and spending, and better project visibility. Overall, the ability

to forecast, manage and control performance has been greatly enhanced and customer satisfaction has risen significantly. A more

unified Balfour Beatty culture is beginning to develop, with increased collaboration starting to leverage the Group’s strengths.

Strategically, this provides the framework for the Group to enter its second two-year phase of Build to Last with greater confidence.

In each business we will build carefully on the positive trajectory to date. The Group will apply appropriate criteria to invest in the

people and capabilities of our Construction Services and Support Services businesses to grow earnings, and in the assets of our

Investments portfolio to grow overall returns. In this way the Group intends to drive value, achieving industry-standard margins by

the end of 2018 and thereafter market-leading performance in its third phase of Build to Last.

RESULTS OVERVIEW AND OUTLOOK

Unless otherwise stated, all commentary in this section, the Divisional operating reviews and Other Financial Items is on an

underlying continuing operations basis.

Throughout this report, Balfour Beatty has presented financial performance measures which are used to manage the Group’s

performance. These financial performance measures are chosen to provide a balanced view of the Group’s operations and are

considered useful to investors as these measures provide relevant information on the Group’s past or future performance, position

or cash flows. These measures are also used internally to assess business performance in its budgeting process and when

determining compensation. An explanation of the Group’s financial performance measures and appropriate reconciliations to its

statutory measures is provided in the Measuring Our Performance section. Non-underlying items and the results from discontinued

operations are the causes of the differences between underlying and statutory profitability. Additionally, underlying revenue

includes the Group’s share of revenue in joint ventures and associates and is presented on a continuing operations basis.

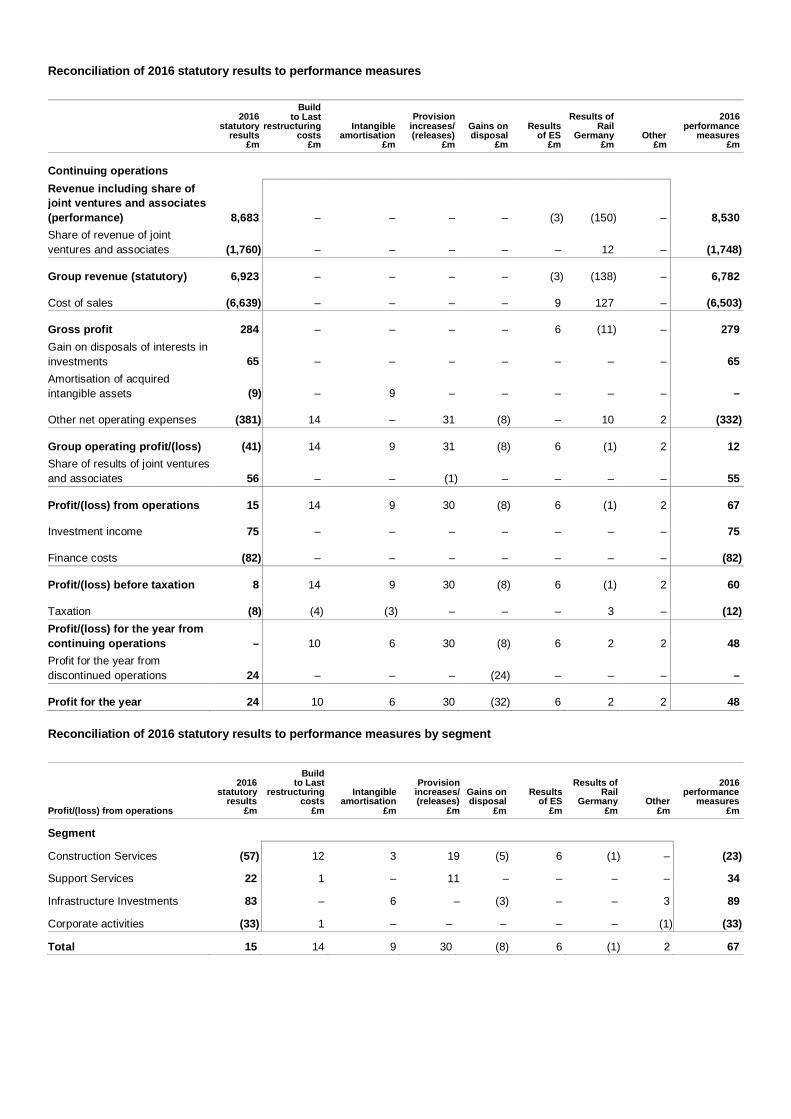

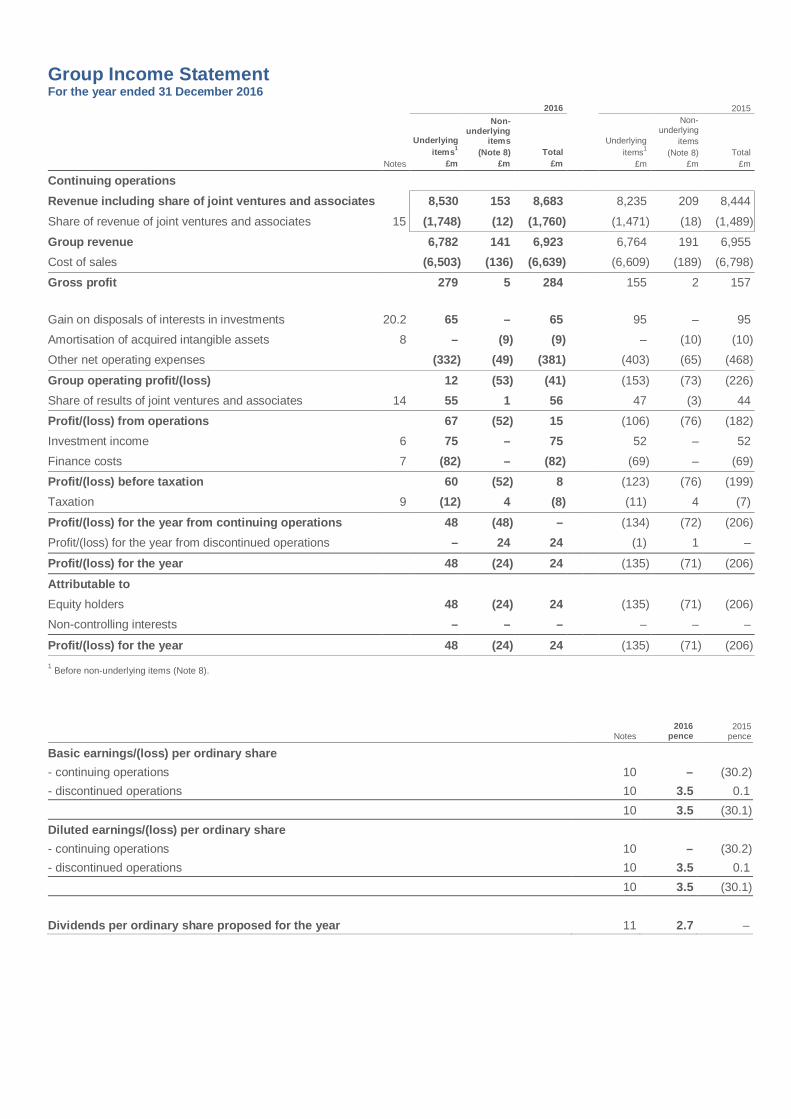

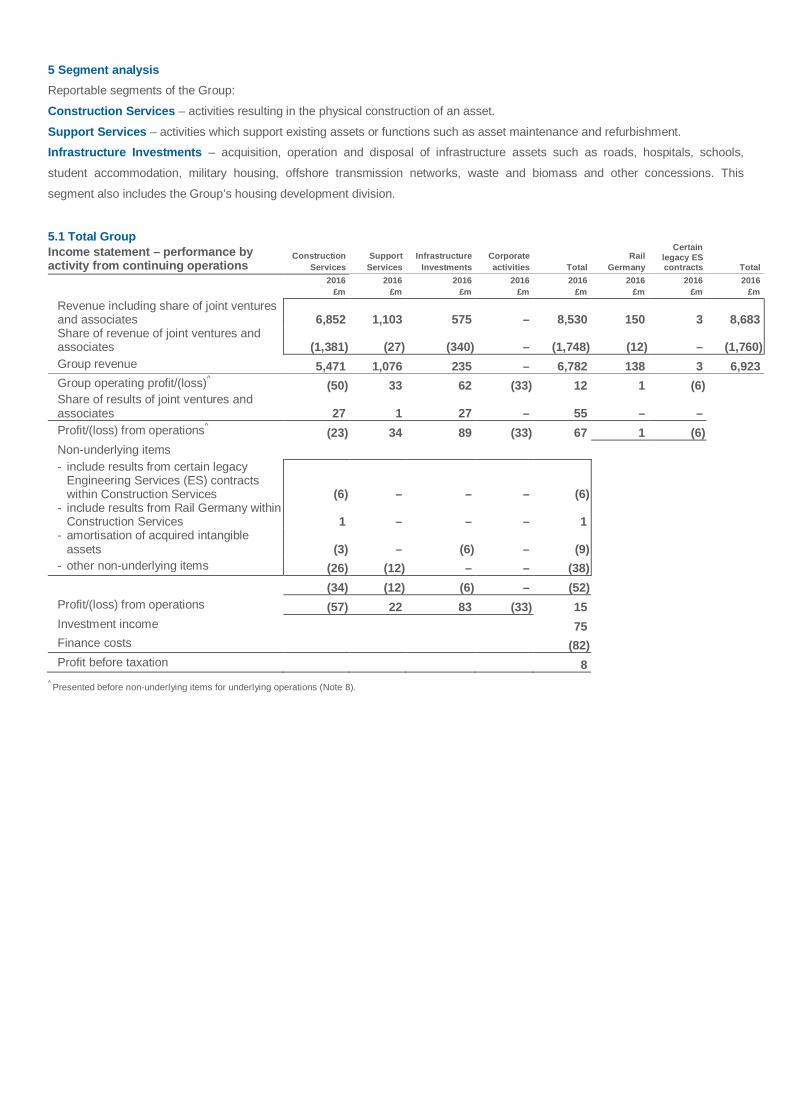

Group financial summaryIn 2016, the Group returned to both underlying and statutory profitability. On an underlying basis, order book, revenue, profit from

operations, earnings and net cash all improved year-on-year as the progress made with Phase One of Build to Last translated into

improved financial metrics.

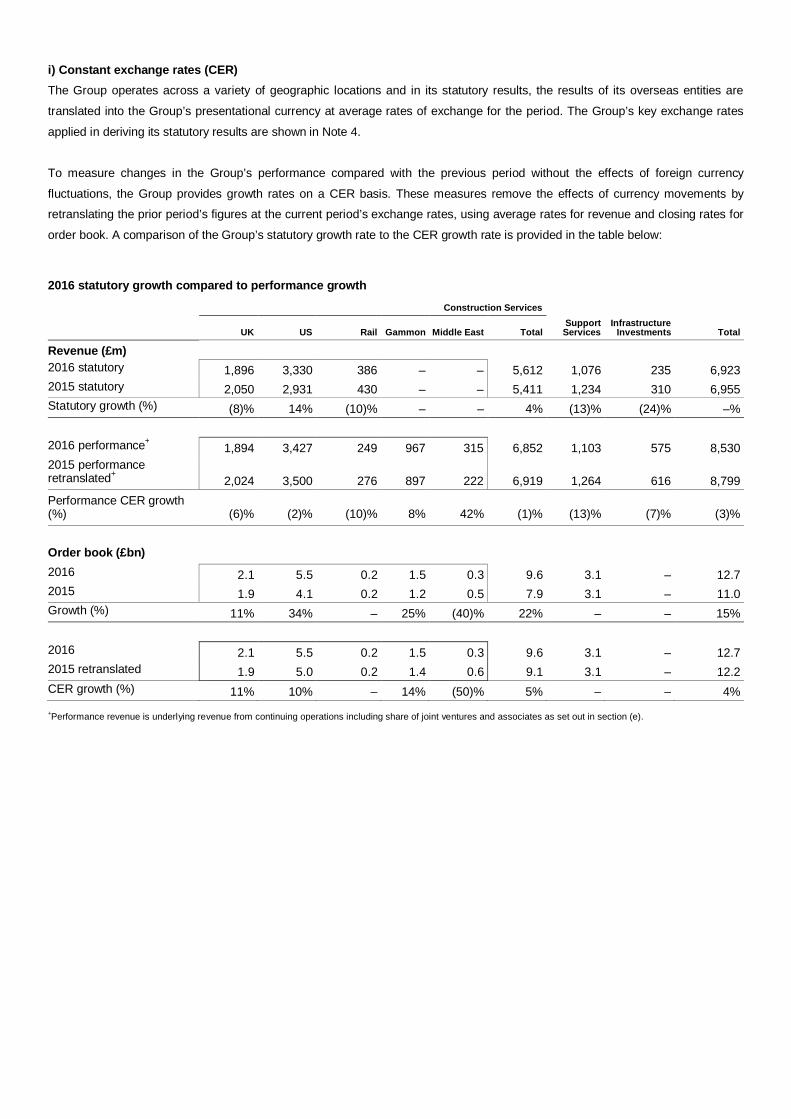

Underlying revenue increased by 4% to £8,530 million (2015: £8,235 million). Underlying revenue at constant exchange rates

(CER) fell by 3% as the Group continued with its more disciplined and selective approach to bidding. Statutory revenue, which

excludes joint ventures and associates, was £6,923 million (2015: £6,955 million).

Construction Services underlying revenue was up 7% at £6,852 million (2015: £6,388 million) as growth in the US offset an

expected decline in the UK; underlying revenue at CER fell by 1%. Support Services underlying revenue declined 12% at £1,103

million (2015: £1,259 million) due to the phasing of contract and regulatory cycles.

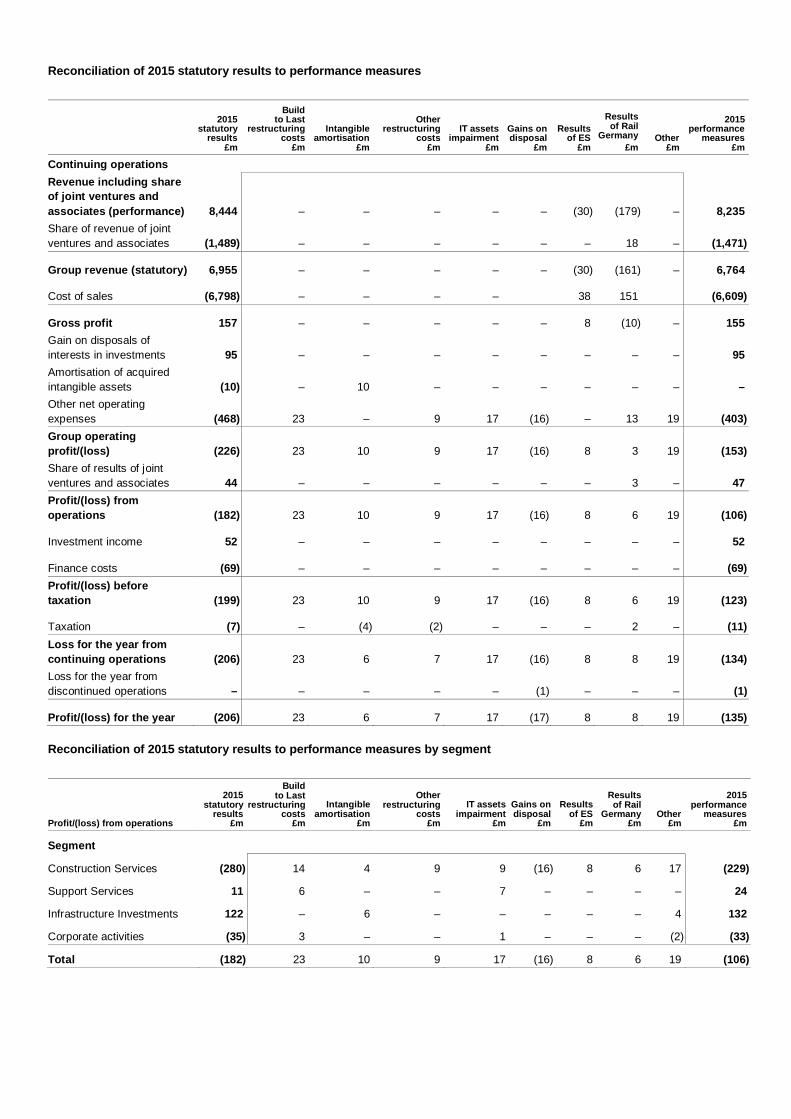

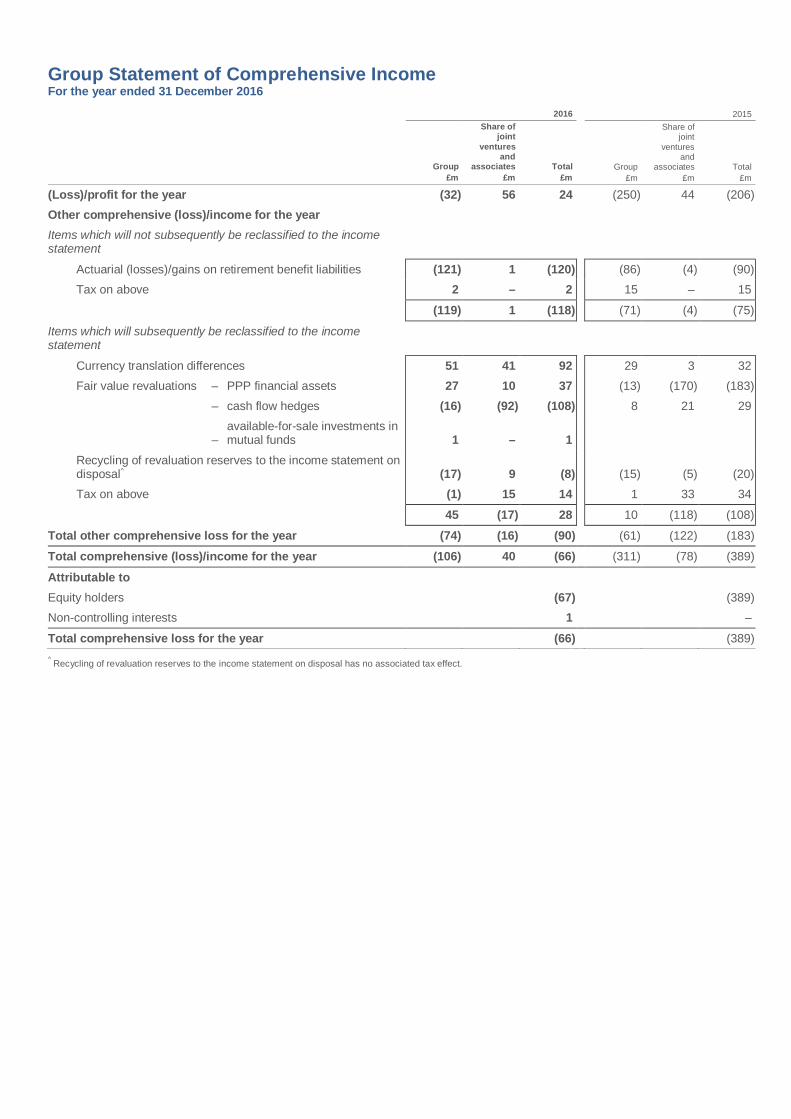

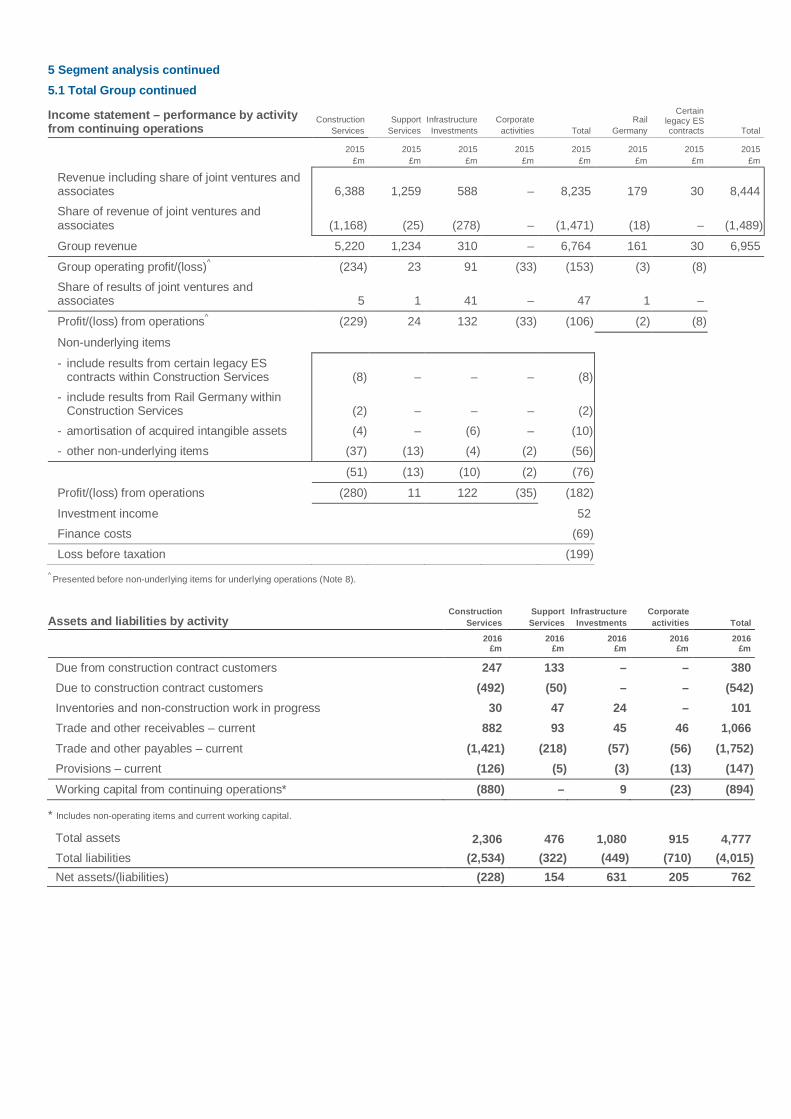

The Group returned to profitability in 2016 with underlying profit from operations at £67 million (2015: £106 million loss). Statutory

profit from operations improved from a loss of £182 million to a profit of £15 million primarily driven by the increase in underlying

profit and a reduction in non-underlying costs.

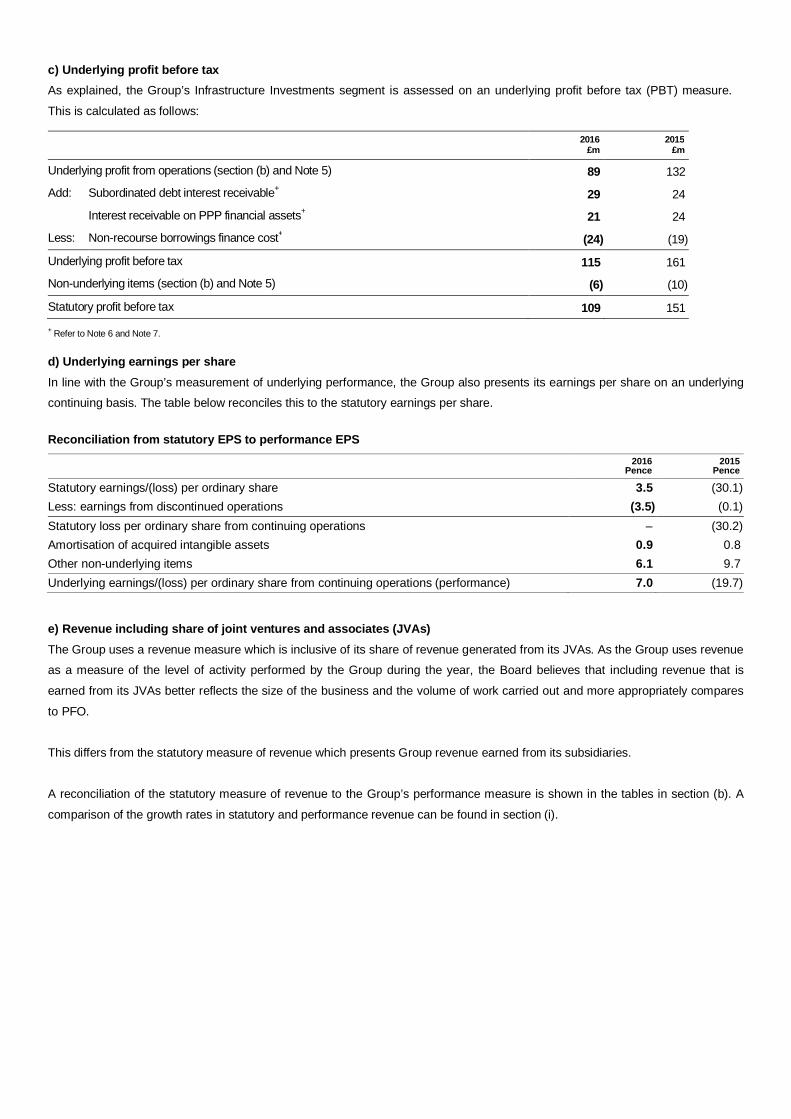

Infrastructure Investments continued to deliver excellent results with underlying profit from operations of £89 million (2015: £132

million), including the benefit of £65 million of profits from investment disposals (2015: £95 million). Support Services rebounded to

more normal levels, compared to the prior year, with underlying profit from operations of £34 million (2015: £24 million). Underlying

loss from operations in Construction Services reduced to £23 million (2015: £229 million loss), where losses in the UK of £64

million (2015: £187 million loss) were only partially offset by profits in the US of £33 million (2015: £22 million loss).

The half-yearly contribution of the Group’s £67 million underlying profit from operations was £5 million in the first half, with £62

million in the second half of the year. Infrastructure Investments, Support Services and Construction Services all reported

underlying profit from operations in the second half of 2016, with UK construction continuing its positive trajectory as it returned to

underlying profitability, a modest £2 million in the second half of the year.

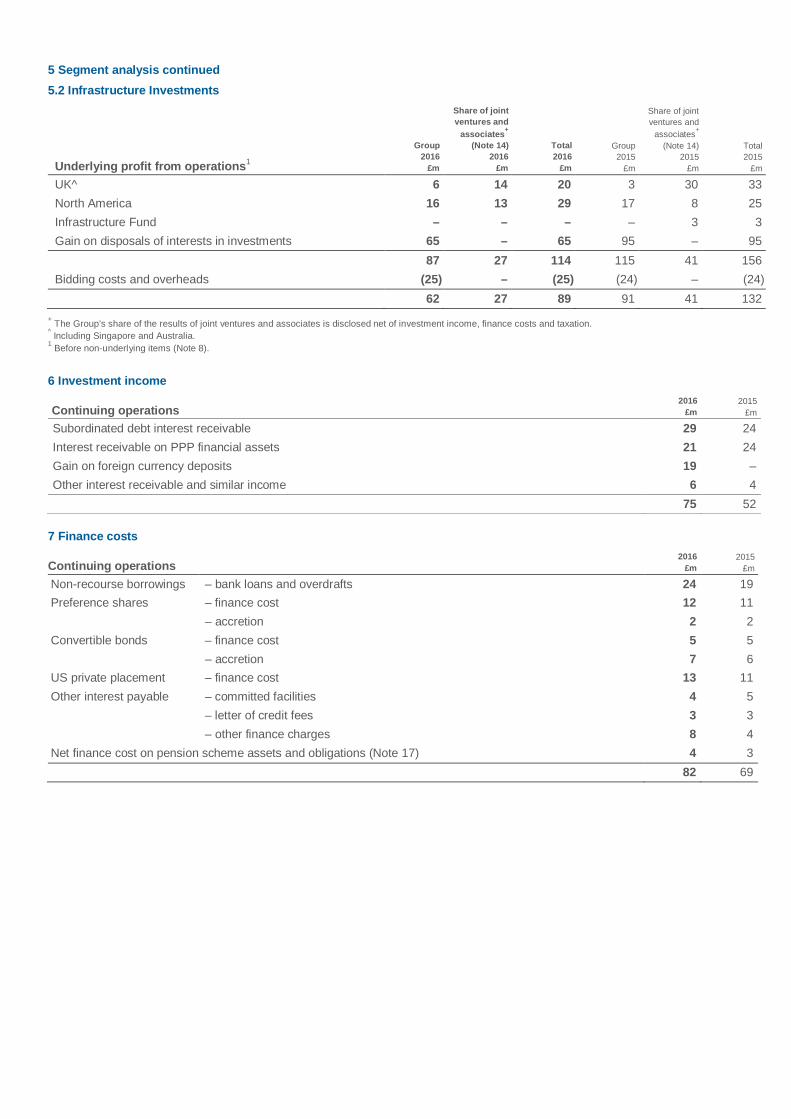

Net finance costs decreased to £7 million (2015: £17 million) predominantly due to a £19 million gain on foreign currency deposits.

The taxation charge on underlying profits increased to £12 million (2015: £11 million).

Underlying profit after tax for the year at £48 million (2015: £135 million loss) represents a material improvement over the previous

year, primarily driven by the improvement in Construction Services. Total statutory profit after tax for the year was £24 million

(2015: £206 million loss).

The order book increased by 15% to £12.7 billion (2015: £11.0 billion), up 4% at CER, despite the more disciplined and selective

approach to bidding. Additionally, the quality of the order book improved as the business increased bid margin thresholds and

focused on jobs where the Group can deliver value.

The improved order book was predominantly due to Construction Services at £9.6 billion (2015: £7.9 billion), with increases in all

material geographical regions: UK construction up 11%; US construction up 10% at CER; and Far East construction up 14% at

CER. The Support Services order book was stable at £3.1 billion (2015: £3.1 billion).

Earnings per shareUnderlying earnings per share from continuing operations was 7.0 pence (2015: 19.7 pence loss), which along with a non-

underlying loss per share from continuing operations of 7.0 pence (2015: 10.5 pence loss) resulted in earnings per share from

continuing operations of nil pence (2015: 30.2 pence loss). Statutory earnings per share was 3.5 pence (2015: 30.1 pence loss).

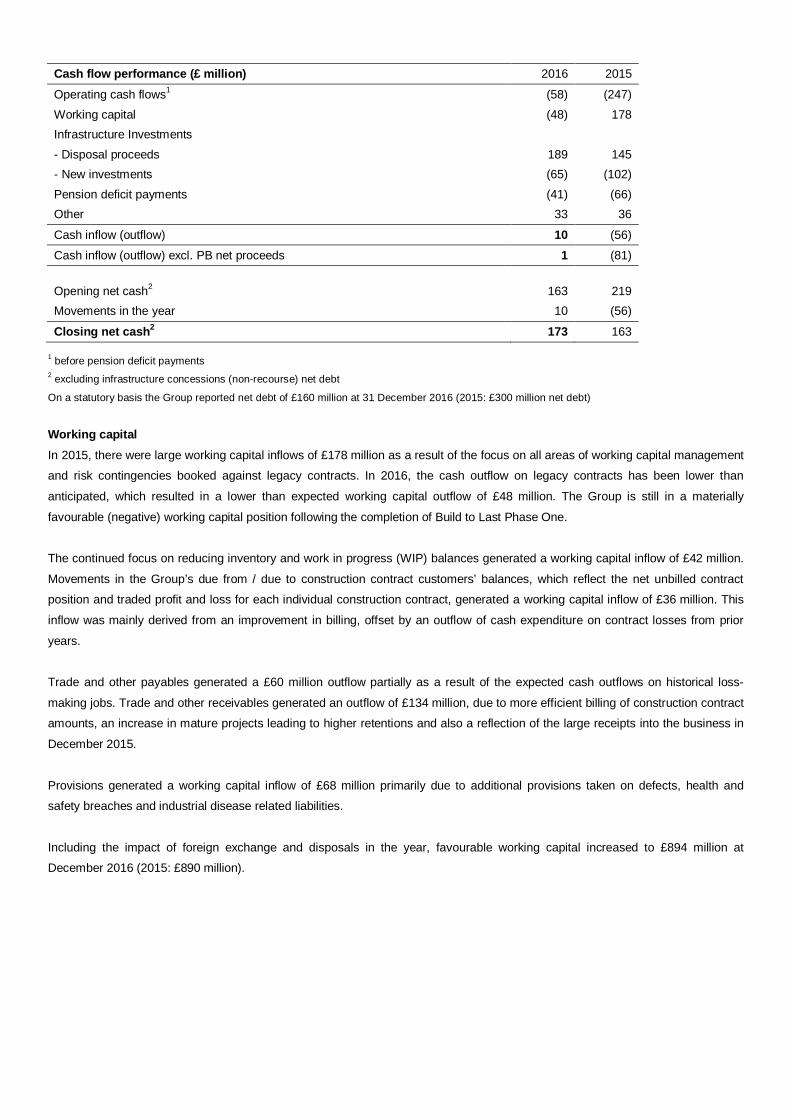

Cash flow performanceThe total cash movement in the period resulted in a £10 million increase to the Group’s net cash position, excluding non-recourse

net borrowings, to £173 million. This compares to a decrease in the Group’s net cash position of £56 million in 2015. The increase

in net cash was driven by proceeds from investment disposals and favourable US dollar foreign exchange movements, partly offset

by new investments in infrastructure assets, negative operating cash flows, working capital movements and pension deficit

payments.

Operating cash flows, before movements in working capital and pension deficit payments, improved to an outflow of £58 million

(2015: £247 million outflow). This reduced outflow is predominantly as a result of the improved financial performance from

Construction Services. Working capital had an outflow of £48 million (2015: £178 million inflow) and pension deficit payments were

an outflow of £41 million (2015: £66 million). Total cash used in operations before tax was £147 million (2015: £135 million), a

decline of £12 million compared to the prior year. Currency translation differences on net cash generated a positive movement of

£30 million (2015: £12 million negative).

The total cash movement in the period excluding Parsons Brinkerhoff (PB) proceeds resulted in a £1 million increase in the Group’s

net cash position. This represented an £82 million improvement on 2015, and a £439 million improvement on 2014 - an excellent

performance against the Build to Last Phase One target of £200 million cash flow improvement versus 2014.

Cash flow performance (£ million) 2016 2015

Operating cash flows1 (58) (247)Working capital (48) 178Infrastructure Investments- Disposal proceeds 189 145- New investments (65) (102)Pension deficit payments (41) (66)Other 33 36

Cash inflow (outflow) 10 (56)

Cash inflow (outflow) excl. PB net proceeds 1 (81)

Opening net cash2 163 219Movements in the year 10 (56)

Closing net cash2 173 163

1 before pension deficit payments2 excluding infrastructure concessions (non-recourse) net debt

On a statutory basis the Group reported net debt of £160 million at 31 December 2016 (2015: £300 million net debt)

Working capitalIn 2015, there were large working capital inflows of £178 million as a result of the focus on all areas of working capital management

and risk contingencies booked against legacy contracts. In 2016, the cash outflow on legacy contracts has been lower than

anticipated, which resulted in a lower than expected working capital outflow of £48 million. The Group is still in a materially

favourable (negative) working capital position following the completion of Build to Last Phase One.

The continued focus on reducing inventory and work in progress (WIP) balances generated a working capital inflow of £42 million.

Movements in the Group’s due from / due to construction contract customers’ balances, which reflect the net unbilled contract

position and traded profit and loss for each individual construction contract, generated a working capital inflow of £36 million. This

inflow was mainly derived from an improvement in billing, offset by an outflow of cash expenditure on contract losses from prior

years.

Trade and other payables generated a £60 million outflow partially as a result of the expected cash outflows on historical loss-

making jobs. Trade and other receivables generated an outflow of £134 million, due to more efficient billing of construction contract

amounts, an increase in mature projects leading to higher retentions and also a reflection of the large receipts into the business in

December 2015.

Provisions generated a working capital inflow of £68 million primarily due to additional provisions taken on defects, health and

safety breaches and industrial disease related liabilities.

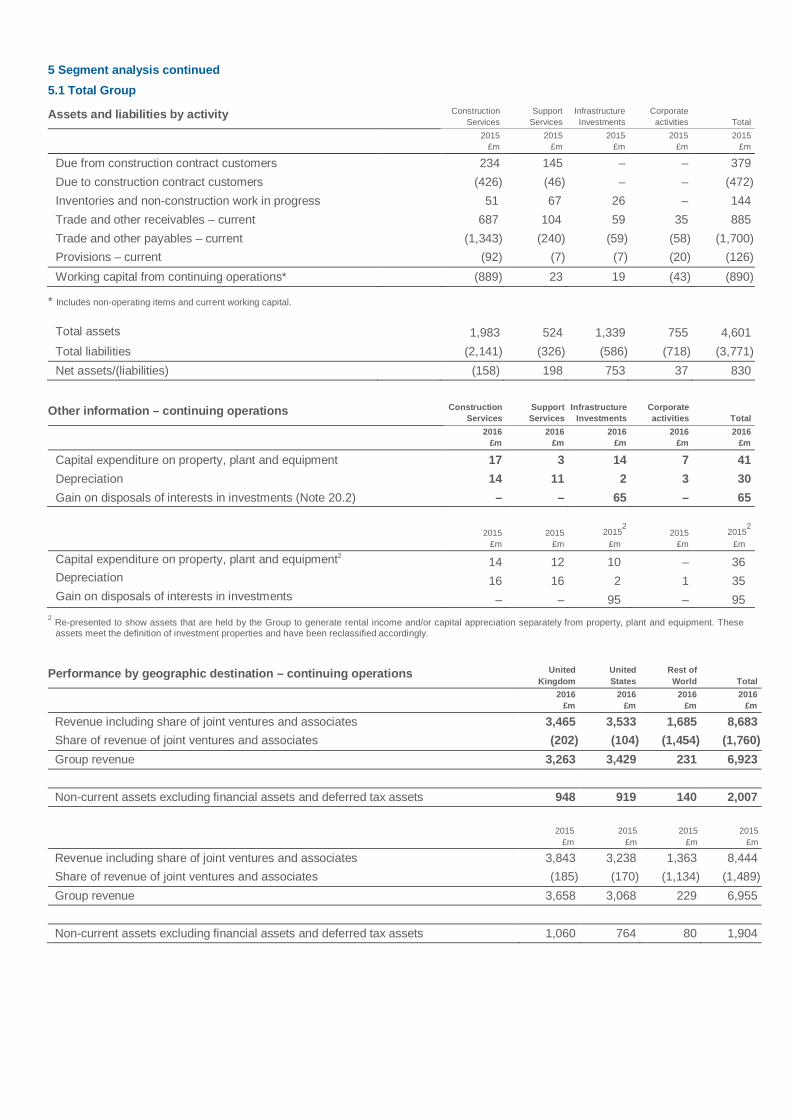

Including the impact of foreign exchange and disposals in the year, favourable working capital increased to £894 million at

December 2016 (2015: £890 million).

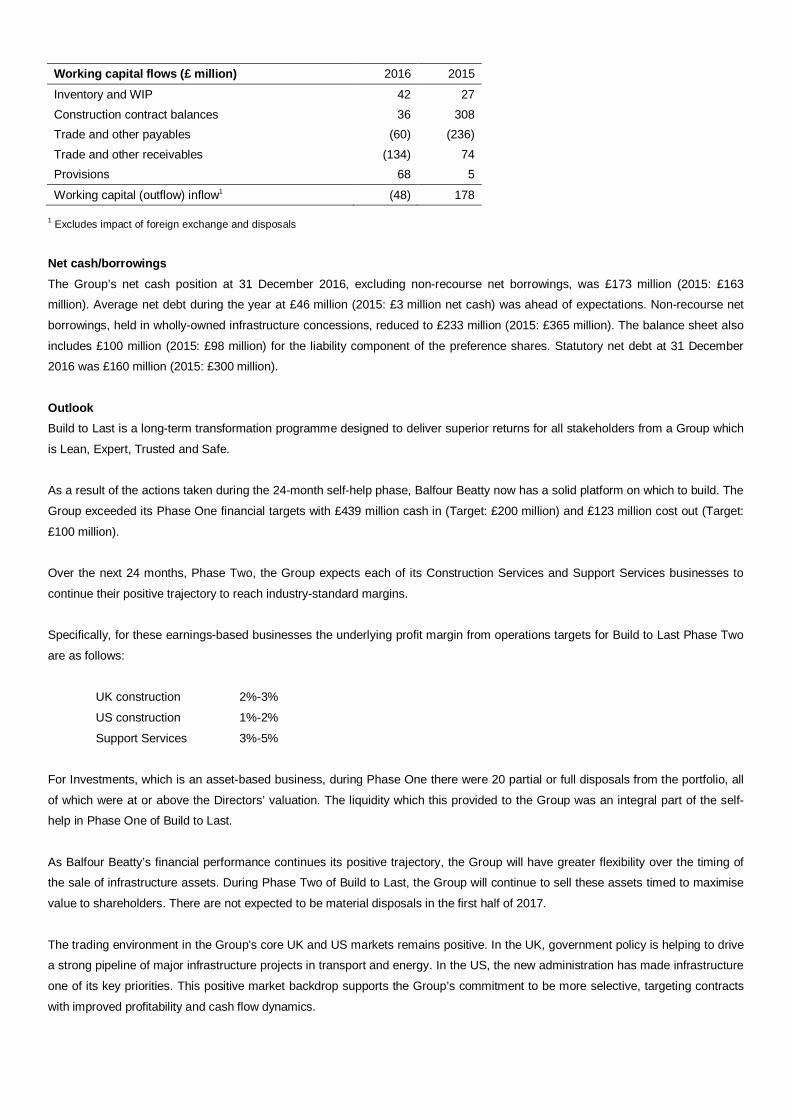

Working capital flows (£ million) 2016 2015

Inventory and WIP 42 27Construction contract balances 36 308Trade and other payables (60) (236)Trade and other receivables (134) 74Provisions 68 5

Working capital (outflow) inflow1 (48) 178

1 Excludes impact of foreign exchange and disposals

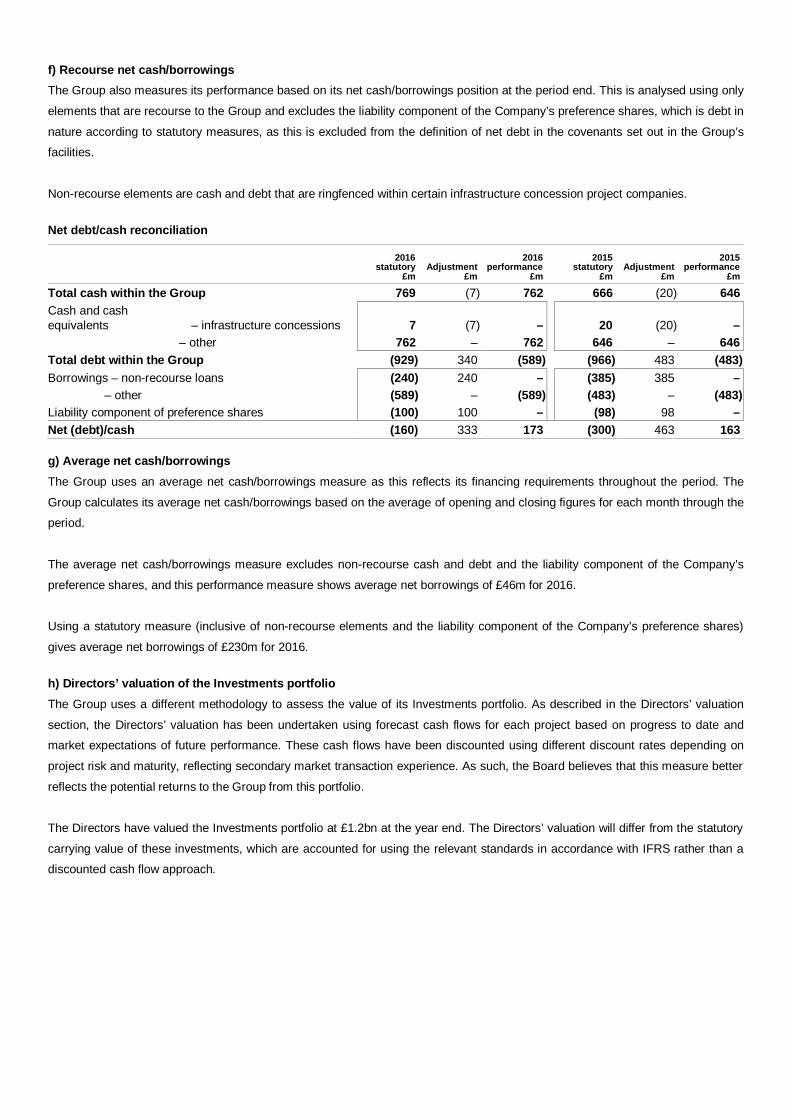

Net cash/borrowingsThe Group’s net cash position at 31 December 2016, excluding non-recourse net borrowings, was £173 million (2015: £163

million). Average net debt during the year at £46 million (2015: £3 million net cash) was ahead of expectations. Non-recourse net

borrowings, held in wholly-owned infrastructure concessions, reduced to £233 million (2015: £365 million). The balance sheet also

includes £100 million (2015: £98 million) for the liability component of the preference shares. Statutory net debt at 31 December

2016 was £160 million (2015: £300 million).

OutlookBuild to Last is a long-term transformation programme designed to deliver superior returns for all stakeholders from a Group which

is Lean, Expert, Trusted and Safe.

As a result of the actions taken during the 24-month self-help phase, Balfour Beatty now has a solid platform on which to build. The

Group exceeded its Phase One financial targets with £439 million cash in (Target: £200 million) and £123 million cost out (Target:

£100 million).

Over the next 24 months, Phase Two, the Group expects each of its Construction Services and Support Services businesses to

continue their positive trajectory to reach industry-standard margins.

Specifically, for these earnings-based businesses the underlying profit margin from operations targets for Build to Last Phase Two

are as follows:

UK construction 2%-3%

US construction 1%-2%

Support Services 3%-5%

For Investments, which is an asset-based business, during Phase One there were 20 partial or full disposals from the portfolio, all

of which were at or above the Directors’ valuation. The liquidity which this provided to the Group was an integral part of the self-

help in Phase One of Build to Last.

As Balfour Beatty’s financial performance continues its positive trajectory, the Group will have greater flexibility over the timing of

the sale of infrastructure assets. During Phase Two of Build to Last, the Group will continue to sell these assets timed to maximise

value to shareholders. There are not expected to be material disposals in the first half of 2017.

The trading environment in the Group's core UK and US markets remains positive. In the UK, government policy is helping to drive

a strong pipeline of major infrastructure projects in transport and energy. In the US, the new administration has made infrastructure

one of its key priorities. This positive market backdrop supports the Group’s commitment to be more selective, targeting contracts

with improved profitability and cash flow dynamics.

In Phase Three (2019+), Balfour Beatty aims to command a premium to industry-standard margins as market-leading strength

should be matched by market-leading performance.

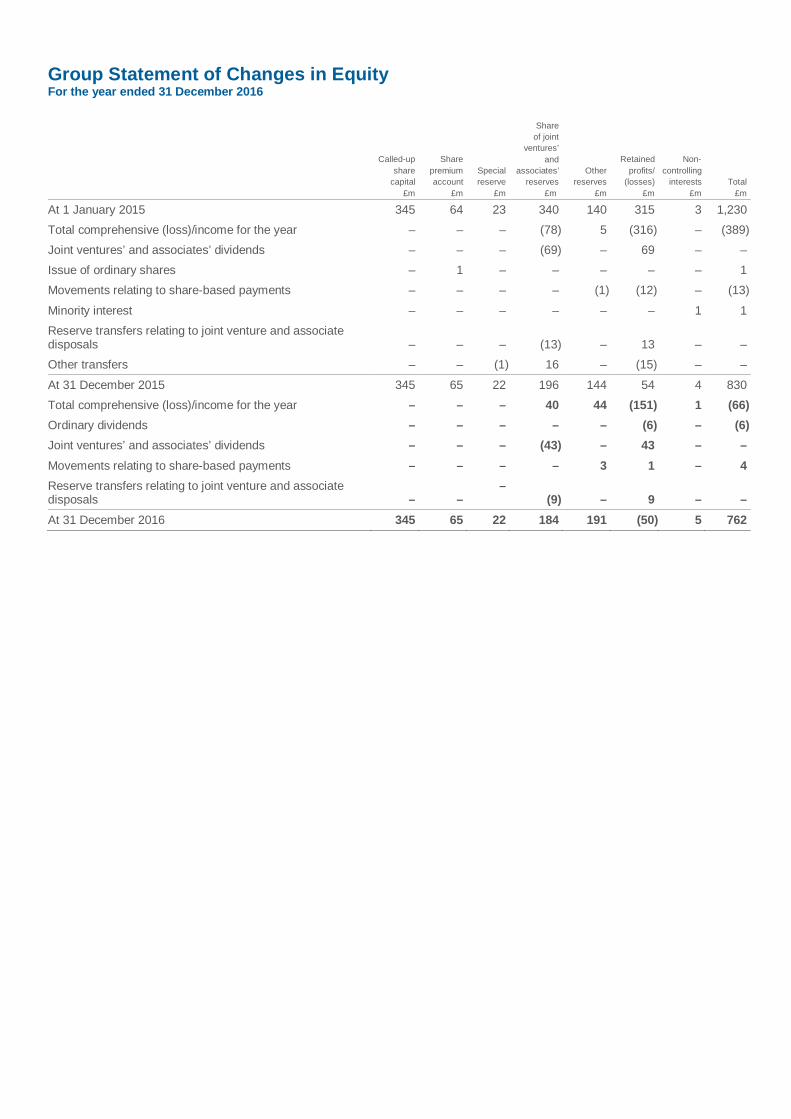

DividendThe Board took the decision to suspend the dividend in 2015, to ensure balance sheet strength was maintained during initial stages

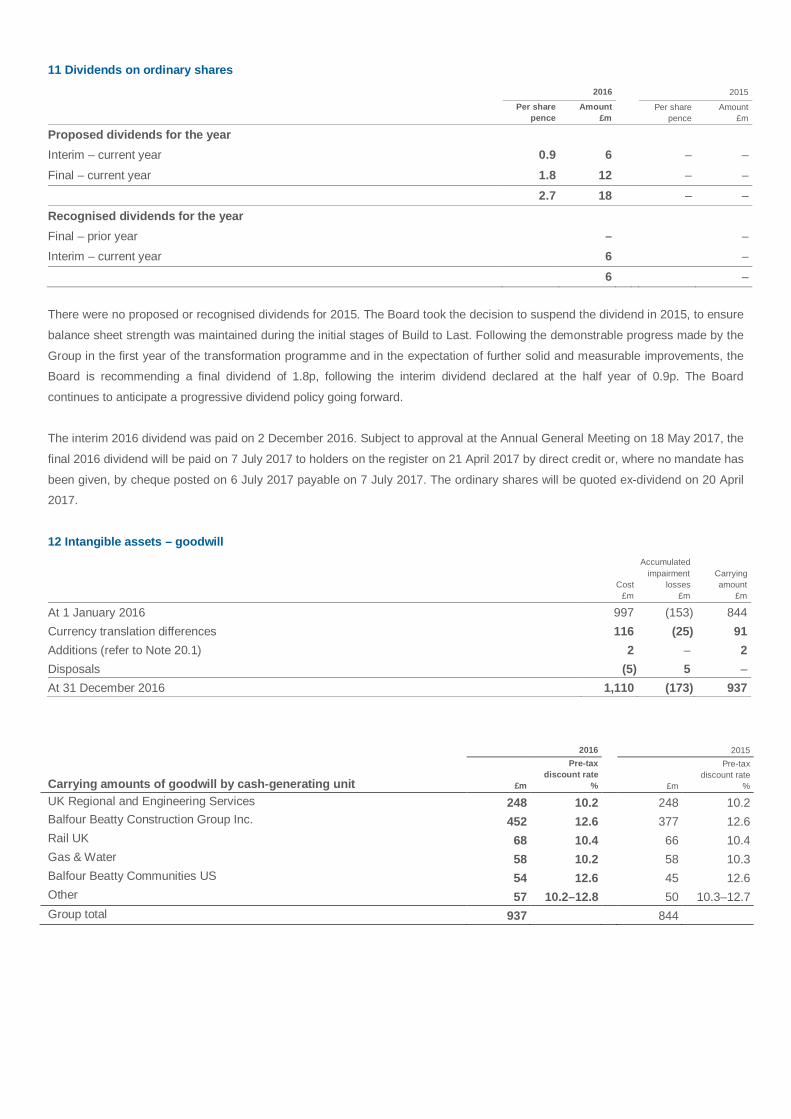

of Build to Last. Following the demonstrable progress made by the Group in the first year of the transformation programme and in

the expectation of further solid and measurable improvements, it was decided to reinstate the dividend at an appropriate level in

2016.

Following the 0.9 pence per share dividend declared at the half year, the Board is recommending a final dividend of 1.8 pence per

share, giving a total recommended dividend for the year of 2.7 pence per share. The Board recognises the importance of dividends

to shareholders and anticipates a progressive dividend policy going forward.

BUILD TO LAST

Balfour Beatty launched its Build to Last transformation programme in early 2015 as a framework to drive continuous improvement

for all stakeholders against four goals – Lean, Expert, Trusted and Safe – as measured by cash flow and profits from operations,

employee engagement, customer satisfaction and Zero Harm.

Phase One consisted of 24 months self-help. Rapid action was taken to remove management layers, upgrade leadership and

strengthen governance within a simplified Group structure. In Phase Two (2017-2018) Balfour Beatty will return to industry-

standard margins and in Phase Three deliver a Group with market-leading strengths and performance.

During Phase One, Balfour Beatty made significant progress on its four goals:

Lean• Deliver value to customers by improving operational efficiency and eliminating waste right through the supply chain.

• The Group metric is cash flow and underlying profit from operations – in Phase One, delivering £200 million of cash in and

£100 million of cost out in the first 24 months.

Group net cash at 31 December 2016 was £173 million, a £10 million improvement on 2015.

Overall in Phase One the Group exceeded the £200 million cash in target: cash flow in 2016 was £439 million better than in 2014,

excluding the proceeds from the sale of Parsons Brinckerhoff. This is the result of the continuing focus on tight management of

cash and working capital, improvements to financial systems and controls, employee training and aligning incentives to deliver

better performance.

A new Group financial consolidation system has been introduced and the process to transfer data from the ERP system to the

consolidation system has been automated, building on the progress made in 2015. Improved weekly cash flow performance

reconciliations are leading to significant improvement in the business’ ability to forecast cash flow, enabling more effective

management of draw-down of the Company’s debt facility.

Further progress was made on the £60 million of annualised cost savings achieved in 2015. By the end of 2016, £123 million of

annualised savings (compared to 2014) had been achieved, exceeding the £100 million target. The business continues to exploit

opportunities to make further savings through standardisation and leaning out processes.

Savings have been driven by simplifying the business, including creating unified back office operations, eliminating waste,

standardising working practices and moving the culture of the organisation to encourage and reward efficient practices. During

2016:

· The US construction and infrastructure businesses have been brought together under a single leader with back office

functions (IT, legal, finance etc.) unified to provide high-quality, efficient support (in a similar model to that deployed in the

UK during 2015) and leadership across the business has been upgraded;

· The IT service which had previously been delivered though a sub-optimal outsourcing agreement was successfully

brought back in-house. This continues to deliver a more responsive and efficient IT operation with annualised savings of

approximately £5 million;

· The Site Mobilisation Hub was introduced for all UK contract start-ups in the summer. By centralising and standardising

this process, resources can be efficiently redeployed from one job to the next. This reduces wastage, cost and delays

caused by sites not being operationally ready. At the same time, project managers are freed up to focus on their project

rather than site set-up. The Hub has engaged with 445 projects, of which 45 mobilisations have now been delivered, all

on time and to budget or better, achieving significant savings;

· Framework agreements have been developed with a shortlist of preferred design consultants with the express aims of

strengthening business relationships and providing greater consistency in the way that design services are provided,

reducing cost and delivering greater value to customers;

· The US strategic procurement group established over 40 national agreements with suppliers selected on their ability to

deliver superior products and services to all major US geographies, as well as offer highly competitive pricing; and

· Further progress has been made in rationalising the property portfolio, bringing business units together in shared offices,

thus aiding collaboration, reducing floor space requirements by 35% and providing more productive working

environments. Over the first two years of Build to Last, UK property costs have been cut by approximately 25%.

The Group has made considerable progress in simplifying its portfolio with the disposal of non-strategic businesses, in order to

focus on its core markets:

· Balfour Beatty Infrastructure Partners, an independently managed infrastructure fund business focusing on secondary

opportunities, was disposed of to Wafra Investment Advisory Group, Inc;

· Balfour Beatty Investments’ sole project in Australia was sold and Balfour Beatty staff and pipeline transferred to Infrared;

· Balfour Resource Group, a healthcare facilities planning consultancy that became part of Balfour Beatty through the

Centex acquisition, was sold to management;

· The sale of Balfour Beatty’s share of its Indonesian joint venture, Balfour Beatty Sakti, to its joint venture partner;

· In early 2017, Balfour Beatty’s entire share of its Middle Eastern joint ventures, Dutco Balfour Beatty and BK Gulf, were

sold to its joint venture partner; and

· Following completion of the sole rail maintenance contract in Chile, the decision was taken to wind up that business.

Expert

· Ensure that Balfour Beatty is attracting, retaining and motivating employees to enable it to offer customers the best

engineering, design, project management and delivery capabilities.

· The Group metric is average employee satisfaction.

Quality of leadership is the number one factor in driving a world class organisation. During 2016, the Group built on its progress in

2015 by further upgrading the quality of senior management, particularly through promotion.

In addition to the unification of the US businesses described in the previous section: in the UK, Engineering Services and

Engineering Construction were brought together under the banner of Balfour Beatty Kilpatrick and a unified leadership; and a new

leadership team was put in place in the UK Power business.

The model of centralised support functions (HR, IT, finance etc.) as first rolled out in the UK continues to provide higher service

levels to the business compared to the previous devolved model, whilst continuing to outperform with respect to re-engineering

process and reducing cost.

During the year, further work has been completed to build communities of practice for key skills across the business. These

communities allow the sharing of best practice across the Group and provide opportunities for career development to the staff

involved.

· A Group-level Project Management Academy has been developed, aligned to international standards through an

accredited training programme, to provide a common approach to professional development and practice. This initiative

provides clarity on the competence level required for each project manager (PM) role and provides an Assignment

Database to match PM competence to contract risk and complexity, greatly enhancing the probability of a successful

outcome for customers.

· Building on the success of the Project Management Competency Assessment carried out across all levels of Balfour

Beatty’s project management employees, work is underway to extend the assessment process into several key Alliances.

· A new strategic approach to bidding and winning key business has been introduced to co-ordinate major opportunities

which straddle business units, in order to ensure that Balfour Beatty has a unified and compelling offer. Business

Acquisition Method training has been rolled out to 200 employees across the UK and US businesses, introducing a

common and systematic approach to winning business. The new training programme boosts estimating skills and

improves the quality of proposals, reducing the risk of underbidding.

· A similar focus on the commercial expertise within the business has enabled better sharing of best practice and a forum

for senior commercial professionals to identify training and development opportunities. As a result an extensive

programme of training has commenced to give the Commercial team the skills to work more productively with customers

on more collaborative forms of contract.

During 2016, Balfour Beatty made significant progress towards becoming a digitally empowered business. Development of staff

capabilities such as the training of six new drone pilots, a digital surveying team with full laser scanning service, a high-end

visualisation team and a significant increase in BIM support have all led to an increase in quality, a leaner approach and a safer

working environment. As a result of Balfour Beatty’s investment in BIM, in 2016 it became one of the first companies to receive the

British Standards Institute’s BIM Kitemark, an accolade only three other companies have achieved. The Group also achieved

another first during the year by winning the V3 Digital Technology Leaders Award for best Public Sector Project in partnership with

Southampton Council.

2016 also saw global collaboration in the fields of Virtual Reality and construction robotics, utilising skills from the UK, US and Hong

Kong. Both technologies are vital to the future of Balfour Beatty as an industry leader.

Training and retaining staff remain critical to the long-term success of Balfour Beatty and is therefore a central tenet of Build to Last.

A new redeployment tool was introduced during the year to identify appropriate opportunities for staff when their current project

concludes, keeping skilled workers in the business and reducing redundancy and recruitment costs.

Two leadership development programmes have been launched, with 50 delegates in 2016. One works with the leadership teams to

actively improve and measure the culture and climate they create in their business. The second identifies high-potential employees

to join a 12-month programme to develop their management skills and capabilities and their transition to leadership roles.

Skills shortages within construction have been a challenge for several years. The UK’s decision to leave the European Union with

the potential for reduction in free movement of people is likely to exacerbate the situation at a time when demand for skilled workers

will increase given the pipeline of projects due to start in the coming years.

Balfour Beatty believes that employers are best placed to determine and train their required future capabilities and therefore must

take the lead by making a long-term commitment to invest in the next generation workforce. For this reason, Balfour Beatty belongs

to and is sponsoring The 5% Club, an employer-led organisation whose members commit to striving to achieve 5% of their UK

workforce in ‘earn and learn’ positions within five years of joining.

During 2016 Balfour Beatty recruited 114 apprentices and 110 graduate trainees. The percentage of the workforce in ‘earn and

learn’ positions at year end stood at 4.3%, a slight reduction on the 2015 number as a result of an unusually high level of

recruitment to these positions in the previous two years, where participants have now been appointed into mainstream roles.

Balfour Beatty’s aspiration remains to reach 5% or above.

My Contribution is the mechanism which directly engages all staff in Build to Last by enabling employees to suggest and drive

changes in the business to help deliver on Build to Last’s Lean, Expert, Trusted and Safe goals. In 2016, 3,114 ideas for business

benefits were logged by Balfour Beatty employees, of which 417 were progressed as projects and delivered with financial savings

of £19 million and over 230,000 hours of time savings.

For the second year a company-wide employee engagement survey was carried out. This is the first time that all the necessary

questions have been asked which allows for Balfour Beatty’s performance to be benchmarked against other businesses by Best

Companies. Balfour Beatty’s employee engagement score was 626.4, which is regarded by Best Companies as demonstrating

good levels of employee engagement. Response rate for the survey at 67% was up on the 2015 survey (61%). The Group

employee satisfaction score for 2016 was 58% (2015: 60%).

Trusted• Be the construction partner of choice for customers and supply chain by delivering on promises.

• The Group metric is customer satisfaction.

Customer satisfaction is achieved by doing what we say we will do. Balfour Beatty continued to win landmark contracts in all its

selected markets with the order book up 15% (4% at CER) at £12.7 billion.

During 2015, the 8-Gated Lifecycle was introduced across Balfour Beatty. In 2016, the framework has been further refined with the

addition of a ‘make or buy’ decision step to promote greater use of internal capabilities. Internal reviews of the bidding Gates (1-4)

across all UK and US business units demonstrate compliance with all new processes. As a result of the early qualification Gates (1-

2) there has been a sharp reduction in the value of work tendered and lost. The UK win rate for 2016 was almost double that of

2015.

To further enhance the control and rigour of the Gated Lifecycle, a secure web-based platform effectively digitises the governance

and document control through all stages and gates of acquiring contracts and delivering projects. This Digital Briefcase was

released at the end of 2016 and is now installed across UK business units with over 500 key users and approvers trained and

utilising the functionality successfully.

Within the industry there continues to be a strong dependence on joint ventures to execute major projects. A key area of focus

going forward will be to ensure the Group can exercise the same degree of governance and control in these instances as it is

gaining through its Build to Last transformation on sole projects.

The rationalisation, upgrade and standardisation of the ERP systems continues. The use of data analytics and automated risk

scoring is now fully embedded in both UK Regional Construction and Balfour Beatty Kilpatrick where the majority of legacy losses

have previously been recorded. Following a successful pilot in 2016 this is now being rolled out across buildings and civils in the

US in conjunction with a simplification of their associated legacy system architecture. This now provides management with

consistent and timely information in regards to project performance (Project on a Page) based on an increasingly broadening

balanced scorecard of metrics. Looking forwards, with further planned improvements and development, it is expected that

integrating multiple key operational data sources in 2017 will maximise the ability to influence project performance at the earliest

possible stage.

A major review of the Business Management System (BMS) was undertaken in 2016 to create a single refreshed and improved

system across all UK businesses. The BMS provides guidance and rules about how Balfour Beatty delivers tasks. The new system

includes offline access and simplified access to information. The BMS will continue to be improved throughout the year and will

define how the Group manages and delivers activities.

During the year 2,107 customer satisfaction reviews were carried out, primarily in the UK. The Group customer satisfaction average

was 91% (2015: 82%). Scores in the UK were generally significantly higher than those in the US.

Safe• Ensure the health and safety of everyone who comes into contact with Balfour Beatty’s activities.

• The Group metric is Zero Harm.

Many of the activities carried out by Balfour Beatty can be, by their nature, potentially dangerous. It is therefore essential that the

health, both physical and mental, and safety of employees, and those who come into contact with Balfour Beatty, including

subcontractors and the general public, are always Balfour Beatty’s first priority.

Health and Safety takes a risk-based approach to identify and prioritise action plans, focused on communicating the Zero Harm

vision, leadership, learning and sharing, clear co-ordinated governance, supply chain engagement, health and safety by design

(including offsite modular assembly), simplifying and improving management systems and processes, training and competence,

behavioural safety, innovation, recognition and reward, clear performance indicators and locally sponsored initiatives. Group

initiatives are proactive and evidence based and include quarterly campaigns and Group-wide stand downs. In 2016 fatal risk

groups were reviewed with leadership at managing director level and initiatives taken to increase skills and awareness, improve

performance and promote employee and supply chain engagement.

Each week senior management report and consider any accident or near misses that have occurred and a weekly report, available

to all employees, shares safety best practice as well as reporting on significant incidents and learning which can be drawn from

Balfour Beatty or elsewhere in the industry.

In May 2016, a Balfour Beatty company was sentenced in connection with its conviction and guilty plea to breaches of Section 3 of

the Health & Safety at Work Act 1974 and related health and safety regulations. The HSE prosecution was in relation to a fatality

on the Heysham Power Station project in Lancashire on 14 April 2010. Balfour Beatty received a fine of £2.6 million. The fine was

judged on the basis of the new sentencing guidelines published by the Department of Justice and demonstrates the increasingly

heavy financial consequences for failures to meet the necessary safety and environmental standards.

Safety is monitored through a combination of leading and lagging performance indicators. The Group Lost Time Incident Rate

excluding international joint ventures fell to 0.22 (2015: 0.24), however, very regrettably there were a number of serious incidents

which resulted in a total of five fatalities, one in each of the UK and US and three in the Far East.

DIVISIONAL OPERATING REVIEWS

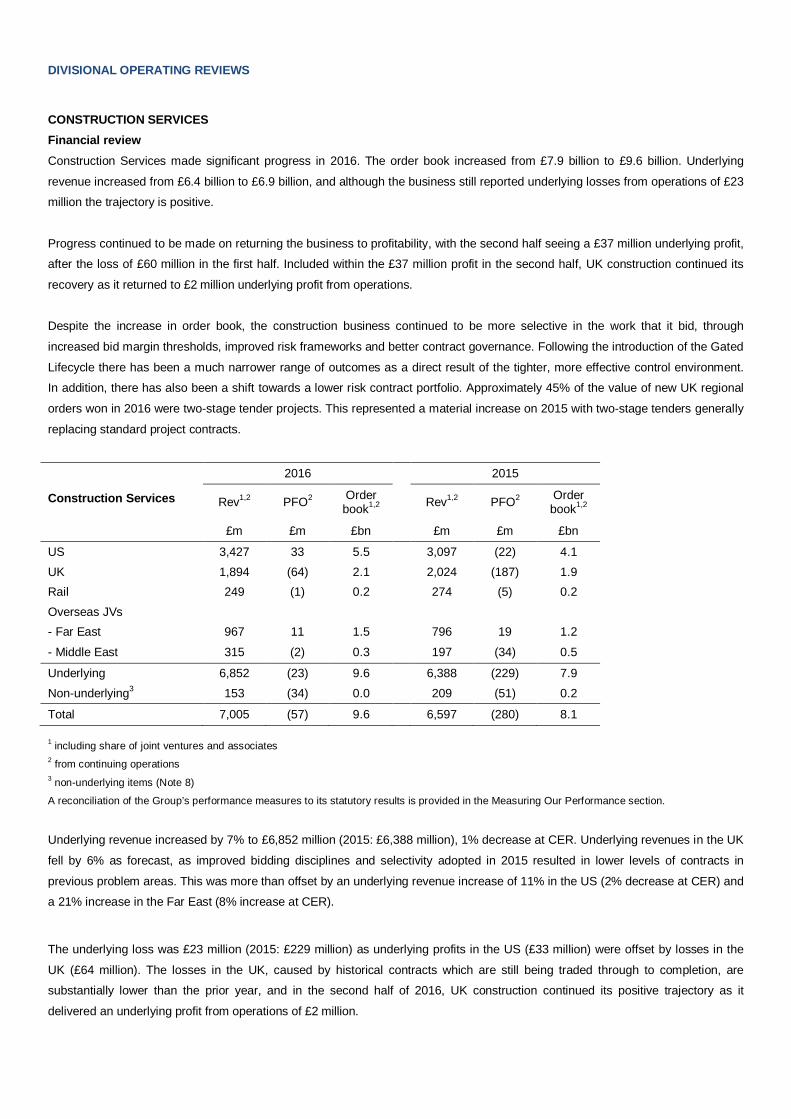

CONSTRUCTION SERVICESFinancial reviewConstruction Services made significant progress in 2016. The order book increased from £7.9 billion to £9.6 billion. Underlying

revenue increased from £6.4 billion to £6.9 billion, and although the business still reported underlying losses from operations of £23

million the trajectory is positive.

Progress continued to be made on returning the business to profitability, with the second half seeing a £37 million underlying profit,

after the loss of £60 million in the first half. Included within the £37 million profit in the second half, UK construction continued its

recovery as it returned to £2 million underlying profit from operations.

Despite the increase in order book, the construction business continued to be more selective in the work that it bid, through

increased bid margin thresholds, improved risk frameworks and better contract governance. Following the introduction of the Gated

Lifecycle there has been a much narrower range of outcomes as a direct result of the tighter, more effective control environment.

In addition, there has also been a shift towards a lower risk contract portfolio. Approximately 45% of the value of new UK regional

orders won in 2016 were two-stage tender projects. This represented a material increase on 2015 with two-stage tenders generally

replacing standard project contracts.

1 including share of joint ventures and associates2 from continuing operations3 non-underlying items (Note 8)

A reconciliation of the Group’s performance measures to its statutory results is provided in the Measuring Our Performance section.

Underlying revenue increased by 7% to £6,852 million (2015: £6,388 million), 1% decrease at CER. Underlying revenues in the UK

fell by 6% as forecast, as improved bidding disciplines and selectivity adopted in 2015 resulted in lower levels of contracts in

previous problem areas. This was more than offset by an underlying revenue increase of 11% in the US (2% decrease at CER) and

a 21% increase in the Far East (8% increase at CER).

The underlying loss was £23 million (2015: £229 million) as underlying profits in the US (£33 million) were offset by losses in the

UK (£64 million). The losses in the UK, caused by historical contracts which are still being traded through to completion, are

substantially lower than the prior year, and in the second half of 2016, UK construction continued its positive trajectory as it

delivered an underlying profit from operations of £2 million.

Construction Services

2016 2015

Rev1,2 PFO2 Orderbook1,2 Rev1,2 PFO2 Order

book1,2

£m £m £bn £m £m £bn

US 3,427 33 5.5 3,097 (22) 4.1UK 1,894 (64) 2.1 2,024 (187) 1.9Rail 249 (1) 0.2 274 (5) 0.2Overseas JVs- Far East 967 11 1.5 796 19 1.2

- Middle East 315 (2) 0.3 197 (34) 0.5

Underlying 6,852 (23) 9.6 6,388 (229) 7.9Non-underlying3 153 (34) 0.0 209 (51) 0.2

Total 7,005 (57) 9.6 6,597 (280) 8.1

The order book increased by 22% (5% at CER) due to growth in both the UK and the US core markets. The UK order book

increased by 11% to £2.1 billion, despite the more disciplined and selective approach to bidding. The US order book increased by

34% (10% at CER) due to strong levels of order intake, such as the Caltrain rail corridor electrification contract. The Far East order

book increased by 25% (14% at CER) with a number of notable awards during the year including the redevelopment of Somerset

House, Hong Kong.

Across the construction portfolio there remain a small number of long-term and complex projects where the Group has incorporated

significant judgements over contractual entitlements. The range of potential outcomes could result in a materially positive or

negative swing to profitability and cash flow. In the UK, the majority of these contracts are within the Major Projects business unit.

Outside the UK, the Group still has a number of significant contracts in Hong Kong where the range of potential outcomes could

result in a materially positive or negative swing to profitability.

UKThe UK construction business is organised into two business units consisting of:

· Major Projects: focused on complex projects and ground engineering services in key market sectors such as

transportation, heavy infrastructure and energy.

· Regional: private and public, civil engineering, mechanical and electrical engineering and building, providing customers

with locally delivered, flexible and fully integrated civil and building services.

During the year, the business continued to simplify. Engineering Construction and Engineering Services (mechanical and electrical

engineering) merged in August 2016, with the new business rebranded as Balfour Beatty Kilpatrick, led by a new managing director

and standardised on a single ERP system. Within Regional, the number of live projects continued to fall from around 400 at

December 2015 to around 250 by December 2016. Over 150 of the current live projects have been through the Gated Lifecycle

process.

Underlying revenue in the UK fell by 6% to £1,894 million (2015: £2,024 million), predominantly due to a decline in the Regional

construction business. The UK business continued to be more selective in the work that it bid, through increased bid margin

thresholds, improved risk frameworks and better contract governance. The Group qualified out nearly £7 billion worth of projects in

2016, whilst at the same time almost doubling the win rate.

Despite the focus on improving the quality of new orders, the UK order book increased by 11% to £2.1 billion (2015: £1.9 billion)

following a number of notable awards including: a contract to widen a 10-mile stretch of the existing A14; a contract to upgrade

baggage screening and handling systems for Heathrow airport; the main construction works for The Madison Tower, a 53-storey

residential building in Canary Wharf; and construction of engineering and training facilities at RAF Marham in Norfolk.

The underlying loss from the UK construction business was £64 million (2015: £187 million), representing an improvement from the

prior year. The loss in the period was caused by three main factors: additional losses incurred on historical contracts; lower

overhead absorption due to the lower revenue base; and newer projects not being progressed to a stage where it is appropriate to

begin to recognise gross margin.

There is a positive trajectory, with the £64 million underlying loss from operations in 2016 split between a £66 million loss in the first

half and a £2 million profit in the second half of the year.

The business is continuing to manage historical problem contracts through to completion. At the 2015 half year 89 historical

contracts were identified that had a material negative impact on profitability and cash. As at the end of December 2016, and in line

with previous guidance given, 90% of these projects were at practical completion (60% at end December 2015) with over 70% at

financial completion. Four of the remaining nine contracts are expected to reach practical completion in 2017, with the remainder in

2018.

The Group is working constructively with industry bodies and the UK Government to identify and manage any direct challenges

caused by the UK’s exit from the European Union. At this stage Balfour Beatty has not seen an impact on the building market;

however the Group remains vigilant to respond to any changes in market conditions.

In 2016, the Major Projects business successfully completed the complex engineering transformation of the former London Olympic

stadium, to allow West Ham United FC to start using the multi-purpose venue in time for the new football season. Work was also

completed on the upgrade to Junction 30 of the M25 in Essex.

On Crossrail, Balfour Beatty’s three major projects: C510 (Liverpool Street and Whitechapel Station tunnels); C512 (Whitechapel

Station); and C530 (Woolwich Station) all made significant progress during the year. At the Thames Tideway Tunnel work has

commenced on the 6-kilometer ‘West’ section which runs from Acton to Wandsworth. In Highways, material ongoing work includes

the conversion of the M3 Motorway (J2-J4) into a Smart Motorway and the construction of dual carriageways for the A21 between

Tonbridge and Pembury, the Aberdeen Western Peripheral Route and the Norwich Northern Distributor Road.

Notable new contract awards in the period include a £146 million construction package to widen a critical and complex 10-mile

stretch of the existing A14 and a contract to build an energy from waste facility for Gloucestershire County Council. Included within

awarded but not contracted (ABNC), the Highways business has been selected to deliver a Smart Motorway package to upgrade

sections of the M6 and M4 (J3–J12). Additionally, a contract from Highways England for the construction of a proposed lorry area

near the M20, worth up to £130 million, has been awarded but is currently under consultation.

The Major Projects business continues to pursue a number of major infrastructure opportunities across core transportation and

energy markets. Over the next few years High Speed 2 (HS2) rail, new nuclear power stations at Hinkley Point C and Wylfa and the

third runway at Heathrow airport will all contribute to the Government’s investment in infrastructure target, which is forecast to rise

to over 1% of GDP by 2020-21.

The proposed HS2 rail route will connect London, Birmingham, Leeds and Manchester with total estimated costs of over £50 billion.

Balfour Beatty and VINCI are in a joint venture pursuing work on HS2, utilising the expertise acquired by both companies on High

Speed 1, VINCI’s involvement on the €8 billion Tours-Bordeaux high-speed rail project in France, and Balfour Beatty’s extensive

work on transport networks across the UK and overseas. Balfour Beatty VINCI were unsuccessful in tendering for the enabling

works packages during the year, but the joint venture has recently tendered for four major civil engineering works packages (two in

the Central section, two in the North section), with contract awards expected in 2017. In addition, the highways market continues to

provide good growth opportunities following the Government’s commitment of £15 billion to Highways England in order to deliver

the first Roads Investment Strategy.

The Regional business is organised into four regions and Balfour Beatty Kilpatrick, following the merger of Engineering

Construction and Engineering Services in August 2016.

· Regional Construction: four regions (Scotland, North & Midlands, South and London) providing public and private

customers with locally delivered, flexible and fully integrated civil and building services.

· Balfour Beatty Kilpatrick: heavy mechanical and electrical (M&E) installations and building services.

As a result of the focus on bidding for contracts with increased margins and more favourable contract terms, the Regional business

is now focused on fewer, larger contracts and continues to reduce its exposure to contracts under £5 million. This allows the

business to focus on projects with better pricing and risk dynamics, but also improves the span of control as it operates fewer sites.

As a result, the total number of live jobs in the Regional business has reduced from over 400 at December 2015 to approximately

250 at December 2016. Over 150 of the current live projects have been through the Gated Lifecycle process.

In 2016, the Regional business successfully completed the A1 improvement scheme where lane capacity was increased from two

lanes to three lanes in each direction from the Metro Centre to Coal House junction. Other key milestones included the completion

of the Kent bound platform at the new Abbey Wood Crossrail station and the North Ayrshire community hospital. Material ongoing

projects include the Kennedy Street student accommodation project in Glasgow, Clyde and Pen y Cymoedd windfarms, Redwood

luxury retirement village for Audley and the renovation and new build scheme at No. 1 Palace Street in St James’, London.

The Regional business had a number of landmark successes in 2016. Notable new contract awards in the period included:

· £170 million contract to upgrade baggage screening and handling systems for Heathrow airport;

· £150 million contract to deliver the main construction works of The Madison Tower, a 53-storey residential building in

Canary Wharf, London;

· £82 million contract to build engineering and training facilities at RAF Marham in Norfolk, in readiness for the arrival of the

UK’s first F-35 Lightning aircraft in 2018;

· £47 million contract to deliver a 1,350 pupil academy on behalf of Hub North Scotland and Aberdeen City Council; and

· Having previously delivered 2,520 units across five Central London student accommodation schemes, the latest contract

with Urbanest is a £42 million development in Vauxhall, London.

Following its reorganisation, Balfour Beatty Kilpatrick has been awarded a contract in excess of £20 million for the mechanical and

electrical services for a pharmaceutical research and innovation facility being built in Hull. The Government’s approval for Hinkley

Point C formalised the selection of a 50:50 joint venture between Balfour Beatty and NG Bailey for the £460 million power station

electrical package. The work will deliver the critical infrastructure to power the station, including cabling totalling over 3,000

kilometres in length, fire and environmental sealing and specialist packages associated with data acquisition and plant control.

The Regional business also continues to secure a number of significant projects operated by Scape Group, which is open to all

public sector bodies in the UK and covers projects ranging from road repairs, new bridges and coastal defence works to light rail

schemes and major road projects. In 2016, the Group was awarded a £35 million contract to deliver the first phase of the Perth

Transport futures project and a £14 million contract to deliver the second phase of the Almond Bank flood defence scheme.

Included within ‘awarded but not contracted’, Balfour Beatty has been selected as construction partner on Manchester University’s

flagship project, the £350 million Engineering Campus development and has also been awarded the Eastwick and Sweetwater

residential development project.

The Regional business continues to pursue a number of opportunities across its core defence, education, health, residential-led

neighbourhoods, student accommodation and transportation markets.

USUnderlying revenues in the US grew by 11% in the period (2% decline at CER) and the order book increased by 34% (10%

increase at CER). The business reported an underlying profit from operations for the year of £33 million (2015: £22 million loss), as

the US returned to profitability following a number of write-downs in the prior year. The underlying operating profit margin at 1.0% is

at the low end of the Group’s Build to Last Phase Two target of 1%-2% for US construction, as the effects of legacy contracts trade

out, but the trajectory is positive and market conditions are considered favourable.

The US business continued to drive operational focus and business simplification. The general building business and the

infrastructure business have now been united under a single leader, which further develops and complements the move to a leaner

organisational structure. The business has been refocused on certain geographies, known as ‘The Southern Smile’. This starts in

the Pacific North West, runs through California, Texas, Florida and up through Georgia and the Carolinas to Washington DC. In the

US approximately 85% of revenues are generated from the general building market, with the infrastructure market (rail, road and

water) accounting for the remaining 15%.

In the building business, underlying revenues were up 12% (stable at CER). The order book increased by 30% (5% at CER), as the

business continued to see strong order intake, notwithstanding the improved bidding disciplines. The business remains focused on

working with repeat customers, in known geographies where it can deliver value. It has therefore intentionally withdrawn from

bidding on most stick frame multi-family housing, in order to switch to better quality revenues in core markets such as office,

education, hospitality, residential and healthcare.

Notable awards in the period included a US$276 million contract for a 42-storey mixed-use residential project in downtown San

Francisco; a US$199 million contract for a mixed-used development in Dallas, comprising a 20-storey office tower and a second

34-storey tower with 253 residential units; a US$196 million contract in Washington for the construction of two 12-storey office

towers to be built on top of an existing platform; a US$126 million contract for Ohlone College, in California, for the development of

three new multi-storey academic core buildings that will house classrooms, laboratories, offices, conference rooms and a library; a

US$110 million contract to construct four new elementary schools and renovate a fifth school for the Highland Park Independent

School District in Texas; a US$99 million contract for the BPM Real Estate Group in downtown Portland to construct a 19-storey

office and hotel development; and a US$84 million contract to build a luxury mixed-use residential tower in midtown Atlanta.

In the infrastructure business, underlying revenues were up 4% (8% down at CER). The order book increased 38% (12% up at

CER) following the notable award of a US$697 million contract for the electrification of the 52-mile Caltrain rail corridor between

San Francisco and San Jose, laying the foundations for the operation of high-speed trains from 2020. This award leverages

expertise demonstrated in constructing the extension of Regional Transport District’s light-rail line across Denver’s south-east

suburbs, which was successfully opened in April 2016.

The infrastructure business continues to pursue design-build and alternative delivery projects in its key rail, highway and water

markets to reflect ongoing changes in procurement trends in the marketplace.

Even before the election of the new President, there was a strong market outlook for construction in the US. In December 2015, the

FAST Act (Fixing America’s Surface Transportation), a US$305 billion transportation bill was signed, providing guaranteed funding

for a five-year period. This bill permits longer term project planning horizons in the public market and is leading to improved visibility

for public funded projects that had been slow to come to market. There are further opportunities being created with the number of

state backed infrastructure bonds (US$30 billion of education bonds in California, US$190 billion multi-state transportation bonds),

and potentially an increase in US private public partnership schemes.

RailUnderlying revenue in the rail business fell by £25 million to £249 million (2015: £274 million). Underlying losses in the year were

£1 million (2015: £5 million) as the business continued to be impacted by poor contract performance on a small number of historical

rail projects. The order book was stable at £0.2 billion. Given the materiality of the segment, future results announcements will

include Rail within UK construction.

InternationalUnderlying revenue in the Group’s Hong Kong and Singapore joint venture, Gammon Construction, increased by 21% (8% at

CER), due to growth in major building projects including the construction of seven towers at the TW5 Cityside residential property

development, 33 Tong Yin Street (residential towers and retail areas) and the conversion of the ex-government Murray building into

a hotel.

Underlying profit from operations in the region reduced to £11 million (2015: £19 million) as new contracts are yet to meet the

required revenue recognition milestones. In Hong Kong there are a number of significant contracts where the range of potential

outcomes could result in a materially positive or negative swing to profitability.

The order book grew by 25% (14% at CER), following the award of a number of notable major building projects: a HK$4 billion

contract for the redevelopment of Somerset House into a 48-storey office building; a HK$2.6 billion contract for a residential

development project for 12 residential towers and five four-storey houses, which together will provide 857 new homes; and a

HK$1.6 billion contract for the construction of the Lee Garden Three Project, which will include 20 floors of office space atop a five-

level retail podium.

In the Middle East, underlying revenue increased to £315 million (2015: £197 million). However, the business continued to make

underlying losses, £2 million in the year (2015: £34 million), reflecting the challenging nature of the region. In early 2017, Balfour

Beatty sold the Group’s entire share in Dutco Balfour Beatty and BK Gulf, for a total cash consideration of £11 million, to its joint

venture partner. As part of the transaction, the local partner assumed responsibility for Balfour Beatty’s guarantees of bonding

obligations in the joint ventures.

Since the start of 2015, Balfour Beatty has exited the Middle East, Indonesia and Australia in order to focus on its chosen markets,

in the UK, US and Far East.

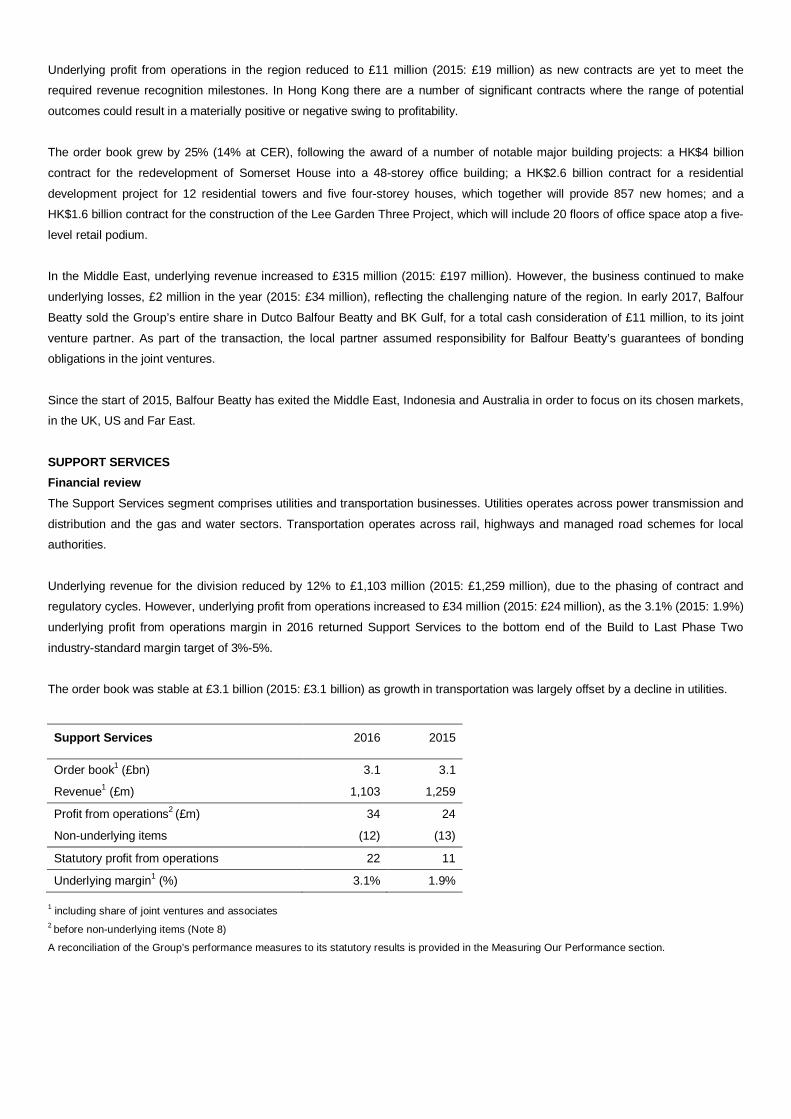

SUPPORT SERVICESFinancial reviewThe Support Services segment comprises utilities and transportation businesses. Utilities operates across power transmission and

distribution and the gas and water sectors. Transportation operates across rail, highways and managed road schemes for local

authorities.

Underlying revenue for the division reduced by 12% to £1,103 million (2015: £1,259 million), due to the phasing of contract and

regulatory cycles. However, underlying profit from operations increased to £34 million (2015: £24 million), as the 3.1% (2015: 1.9%)

underlying profit from operations margin in 2016 returned Support Services to the bottom end of the Build to Last Phase Two

industry-standard margin target of 3%-5%.

The order book was stable at £3.1 billion (2015: £3.1 billion) as growth in transportation was largely offset by a decline in utilities.

Support Services 2016 2015

Order book1 (£bn) 3.1 3.1

Revenue1 (£m) 1,103 1,259

Profit from operations2 (£m) 34 24

Non-underlying items (12) (13)

Statutory profit from operations 22 11

Underlying margin1 (%) 3.1% 1.9%

1 including share of joint ventures and associates2 before non-underlying items (Note 8)

A reconciliation of the Group’s performance measures to its statutory results is provided in the Measuring Our Performance section.

Operating reviewUnderlying utilities revenue reduced by 6% to £590 million, with power transmission and distribution down 10% and gas and water

down 3%. The utilities order book reduced by 10%, with power transmission and distribution down 13% and gas and water down

9%.

Volumes in power transmission and distribution saw a decline in cabling and distribution network operator works, with 2015 also

having significant one-off repair works in offshore transmission.

The power business has undertaken a significant restructure and cost removal during 2016, including the internal appointment of a

new managing director, along with several other senior changes. The business has also focused on qualifying out low-value works

and areas which do not align to its risk profile, including significantly reducing its reliance on volume-based and second-tier

subcontracting projects.

In March 2016, power transmission and distribution was awarded contracts worth £35 million by Scottish Hydro Electric for the

design and construction of the Bhlaraidh and Beinnuen wind farms connections project near Fort Augustus, in Scotland. Most of the

project was successfully delivered during 2016.

In November 2016, the power business was awarded a £120 million contract by ElecLink Ltd to install two 50-kilometer electricity

cables between France and Great Britain through the Channel Tunnel. This will be the first ever installation of a High Voltage Direct

Current (HVDC) interconnector in a live rail tunnel environment.

The slight reduction in gas and water underlying revenue was caused by the dip in the UK water regulatory cycle between the

completion of Asset Management Period 2010-2015 (AMP5) and new contracts continuing to mature under AMP6 (2015-2020).

The reduction in the order book was as expected, given the progress of the AMP6 delivery cycle. Many water contracts are

extended over multiple AMP periods and the Group has already started to engage on the AMP7 planning cycle.

In 2016, gas and water secured an extension, through to 2020, to the gas transmission and distribution contract worth £130 million

for Bord Gais, in Ireland, and also won a £38 million water treatment scheme for South West Water. The delivery of key and

complex schemes remains on track. Gas and water expect a peak volume year in 2017, as it represents the middle of the current

AMP6 cycle.

Underlying transportation revenues reduced by 18% to £513 million, due to expected volume declines from rail and highways.

Underlying rail revenues were lower following the completion of a rail grinding contract in the prior year. Underlying highways

revenues declined due to lower capital spend on a number of contracts for Highways England and completion of the contract for

Area 4 during the period.

The transportation order book grew by 14%, due to strong order intake in rail and from local authorities. The rail business was

awarded a £170 million two-year extension to its Track Partnership contract with London Underground, to deliver essential track

renewal work across the network. In local authorities Balfour Beatty was awarded a £245 million seven-year highways maintenance

contract for Coventry City Council, Solihull Metropolitan Borough Council and Warwickshire County Council. This unique

collaborative arrangement will deliver better value for money, improved service resilience and flexibility in services. Additionally the

Group was awarded a £55 million two-year extension by West Sussex County Council to continue its highways maintenance and

improvement scheme works and Connect Roads signed a £36 million, 10-year extension to its Balfour Beatty Major Projects

Highway Services contract to deliver the essential maintenance works on the A50. The contract covers a 56-kilometer section of

the A50 between Stoke and Derby which acts as a strategic east to west link between the M1 and M6.

In September, the Group acquired Omnicom Engineering Ltd. Omnicom complements Balfour Beatty’s existing rail technology

business by bringing remote surveying hardware and software to enhance the Group’s Digital Rail strategy.

INFRASTRUCTURE INVESTMENTS

Financial reviewThe Investments business delivered another strong performance, having continued its strategy of optimising value through the

disposal of mature assets, whilst also continuing to invest in new opportunities and expanding the breadth of assets.

During the year Investments made significant progress in simplifying its operations by exiting Balfour Beatty Infrastructure Partners

(BBIP), an infrastructure fund run at arm’s length and focused on secondary opportunities, and exiting from the Australian market.

In total 16 assets were either sold or part sold in the period, with all transactions either at, or above, the Directors’ valuation.

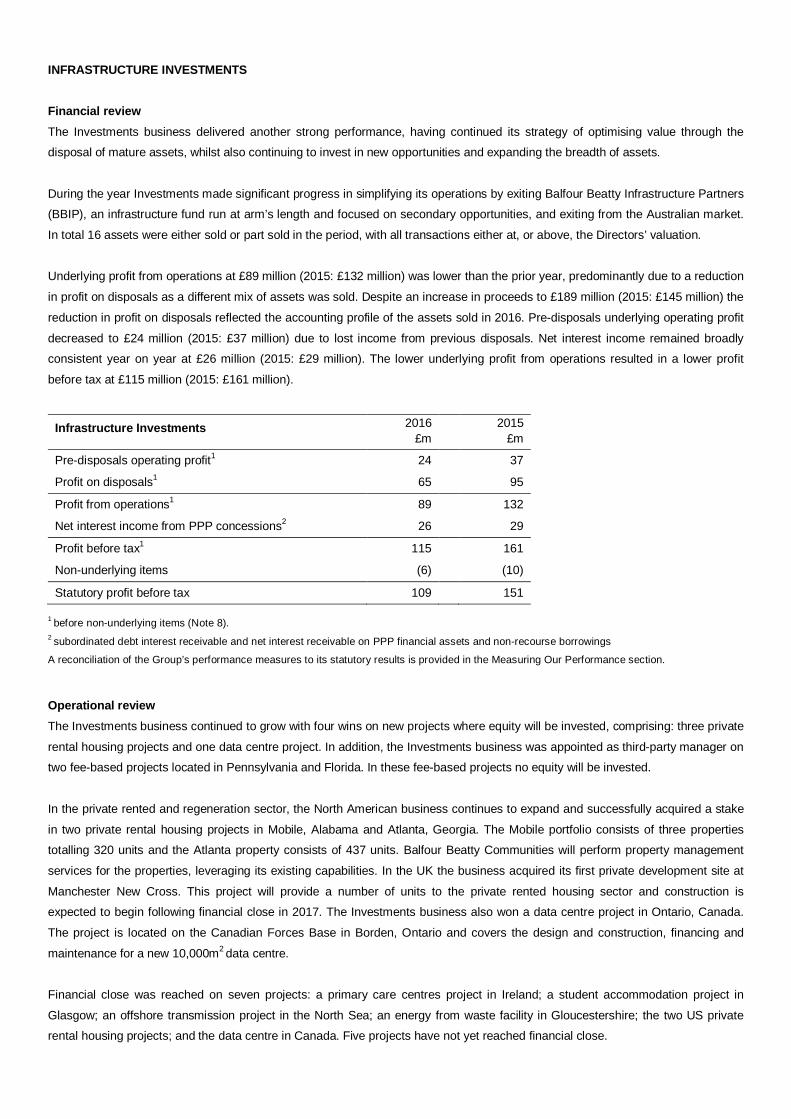

Underlying profit from operations at £89 million (2015: £132 million) was lower than the prior year, predominantly due to a reduction

in profit on disposals as a different mix of assets was sold. Despite an increase in proceeds to £189 million (2015: £145 million) the

reduction in profit on disposals reflected the accounting profile of the assets sold in 2016. Pre-disposals underlying operating profit

decreased to £24 million (2015: £37 million) due to lost income from previous disposals. Net interest income remained broadly

consistent year on year at £26 million (2015: £29 million). The lower underlying profit from operations resulted in a lower profit

before tax at £115 million (2015: £161 million).

Infrastructure Investments 2016 £m

2015 £m

Pre-disposals operating profit1 24 37

Profit on disposals1 65 95

Profit from operations1 89 132

Net interest income from PPP concessions2 26 29

Profit before tax1 115 161

Non-underlying items (6) (10)

Statutory profit before tax 109 151

1 before non-underlying items (Note 8).2 subordinated debt interest receivable and net interest receivable on PPP financial assets and non-recourse borrowings

A reconciliation of the Group’s performance measures to its statutory results is provided in the Measuring Our Performance section.

Operational reviewThe Investments business continued to grow with four wins on new projects where equity will be invested, comprising: three private

rental housing projects and one data centre project. In addition, the Investments business was appointed as third-party manager on

two fee-based projects located in Pennsylvania and Florida. In these fee-based projects no equity will be invested.

In the private rented and regeneration sector, the North American business continues to expand and successfully acquired a stake

in two private rental housing projects in Mobile, Alabama and Atlanta, Georgia. The Mobile portfolio consists of three properties

totalling 320 units and the Atlanta property consists of 437 units. Balfour Beatty Communities will perform property management

services for the properties, leveraging its existing capabilities. In the UK the business acquired its first private development site at

Manchester New Cross. This project will provide a number of units to the private rented housing sector and construction is

expected to begin following financial close in 2017. The Investments business also won a data centre project in Ontario, Canada.

The project is located on the Canadian Forces Base in Borden, Ontario and covers the design and construction, financing and

maintenance for a new 10,000m2 data centre.

Financial close was reached on seven projects: a primary care centres project in Ireland; a student accommodation project in

Glasgow; an offshore transmission project in the North Sea; an energy from waste facility in Gloucestershire; the two US private

rental housing projects; and the data centre in Canada. Five projects have not yet reached financial close.

The Investments business continued to make substantial equity investments in the portfolio, with £65 million invested in the period

(2015: £102 million), of which £8 million was invested in the BBIP infrastructure fund before its sale.

Interests in 16 assets were sold in the period, seven of which were partial sales, generating total book gains on disposal of £65

million (2015: £95 million from four assets).

The Investments business continues to see significant opportunities for future investment in its core geographic markets in the UK

and North America, across its existing market sectors and as it continues to grow into new adjacent sectors. The business

continues to monitor both the US and UK PPP markets for opportunities, especially following the recent announcements regarding

PF2 in the UK and by the new administration in the US.

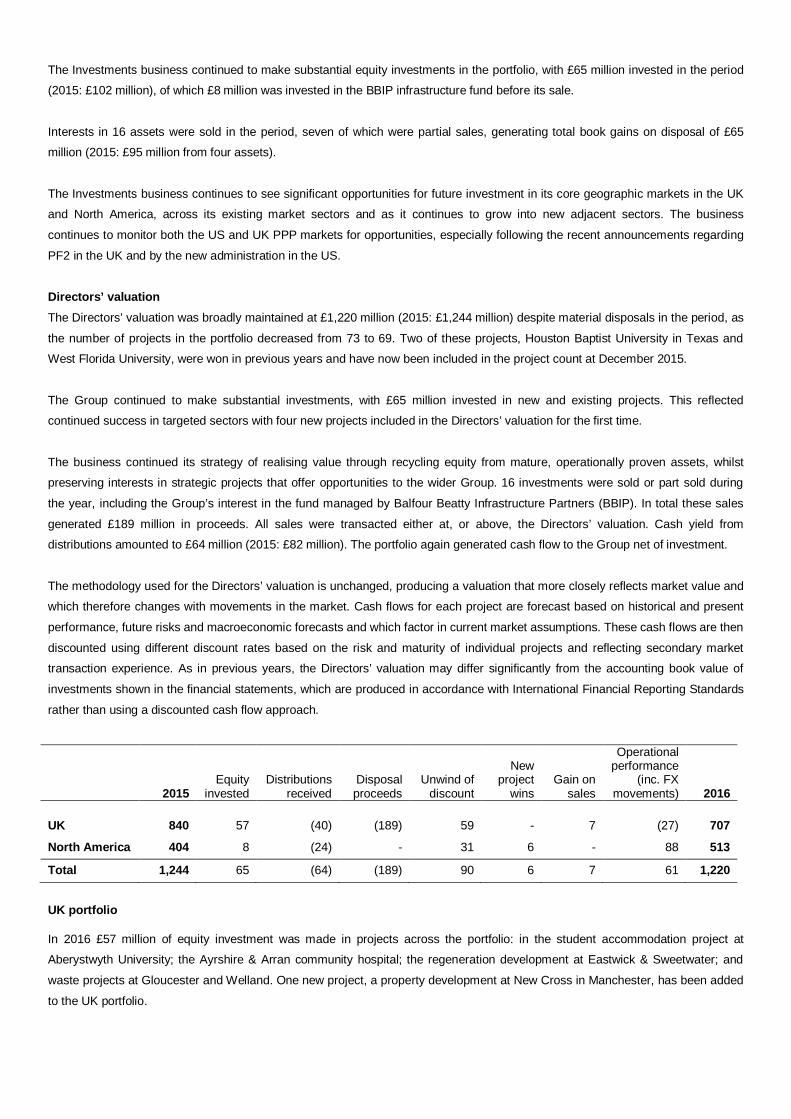

Directors’ valuationThe Directors’ valuation was broadly maintained at £1,220 million (2015: £1,244 million) despite material disposals in the period, as

the number of projects in the portfolio decreased from 73 to 69. Two of these projects, Houston Baptist University in Texas and

West Florida University, were won in previous years and have now been included in the project count at December 2015.

The Group continued to make substantial investments, with £65 million invested in new and existing projects. This reflected

continued success in targeted sectors with four new projects included in the Directors’ valuation for the first time.

The business continued its strategy of realising value through recycling equity from mature, operationally proven assets, whilst

preserving interests in strategic projects that offer opportunities to the wider Group. 16 investments were sold or part sold during

the year, including the Group’s interest in the fund managed by Balfour Beatty Infrastructure Partners (BBIP). In total these sales

generated £189 million in proceeds. All sales were transacted either at, or above, the Directors’ valuation. Cash yield from

distributions amounted to £64 million (2015: £82 million). The portfolio again generated cash flow to the Group net of investment.

The methodology used for the Directors’ valuation is unchanged, producing a valuation that more closely reflects market value and

which therefore changes with movements in the market. Cash flows for each project are forecast based on historical and present

performance, future risks and macroeconomic forecasts and which factor in current market assumptions. These cash flows are then

discounted using different discount rates based on the risk and maturity of individual projects and reflecting secondary market

transaction experience. As in previous years, the Directors’ valuation may differ significantly from the accounting book value of

investments shown in the financial statements, which are produced in accordance with International Financial Reporting Standards

rather than using a discounted cash flow approach.

2015Equity

investedDistributions

receivedDisposalproceeds

Unwind ofdiscount

Newproject

winsGain on

sales

Operationalperformance

(inc. FXmovements) 2016

UK 840 57 (40) (189) 59 - 7 (27) 707

North America 404 8 (24) - 31 6 - 88 513

Total 1,244 65 (64) (189) 90 6 7 61 1,220

UK portfolio

In 2016 £57 million of equity investment was made in projects across the portfolio: in the student accommodation project at

Aberystwyth University; the Ayrshire & Arran community hospital; the regeneration development at Eastwick & Sweetwater; and

waste projects at Gloucester and Welland. One new project, a property development at New Cross in Manchester, has been added

to the UK portfolio.

Demand for high-quality infrastructure investments in the secondary market remained strong and the Group took advantage of this

through further sales of mature assets. Investor appetite for yield in the ongoing, low interest rate environment continues unabated

and pricing in the secondary market is therefore expected to remain strong for the foreseeable future.

Interests in 16 assets were sold in the period, seven of which were partial sales, generating total book gains on disposal of £65

million (2015: £95 million from four assets). The business sold its entire 50% interest in the Wollongong project in Australia, a 30%

interest in the M1/A1 project (where the Group retains a 20% interest), a 40% interest in the Humber Gateway OFTO (where the

Group retains a 20% interest), its entire interest in the BSF portfolio comprised of seven schools projects and an 80% interest in

five street lighting projects (where the Group retains a 20% interest). The Group’s interest in Balfour Beatty Infrastructure Partners

(BBIP), which was included in the Directors’ valuation but not as a line item in the project total, was sold during the year. All

disposals were either at, or above, the Directors’ valuation.

Operational performance movements resulted in a £27 million reduction in value. The most significant components of this were