Bachelor thesis - Ian Beck - 2015

66

Exploratory research THE DISRUPTION OF ONLINE FOOD PLATFORMS IN THE DUTCH FOOD INDUSTRY Bachelor Thesis by Ian Beck - 111471 June 2015 NHTV University of Applied Sciences – International Hotel Management Graduation subject Innovation Graduation coach - Eric Andersen

Transcript of Bachelor thesis - Ian Beck - 2015

Exploratory research

THE DISRUPTION OF ONLINE FOOD PLATFORMS IN THE DUTCH FOOD INDUSTRY Bachelor Thesis by Ian Beck - 111471 June 2015 NHTV University of Applied Sciences – International Hotel Management Graduation subject Innovation Graduation coach - Eric Andersen

2

GENERAL INFORMATION

STUDENT

Name: Ian Beck

Student number: 111471

Address: Minister Nelissenstraat 58, 4818 HT Breda

E-mail: [email protected]/ [email protected]

EDUCATIONAL INSTITUTE

Academy: NHTV University of Applied Sciences

Programme: International Hotel Management

Address: Sibeliuslaan 13, 4837 CA Breda

PARTNER INSTITUTES

Name: Abn-Amro

Address: Gustav Mahlerlaan 10, 1082 PP Amsterdam

Name: Foodservice Instituut Nederland

Address: Galvanistraat 1, 6716 AE Ede

E-mail: [email protected]

THESIS COACH

Name: Eric Andersen

E-mail: [email protected]

ABN-AMRO COACH

Name: Stef Driessen

E-mail: [email protected]

3

EXECUTIVE SUMMARY

The new digital era we live in is disrupting the world of food and beverages. The Dutch food industry is

at the beginning of a digital revolution. The concepts of online food platforms provide new

opportunities for consumers to purchase food and beverage products. The Dutch food market lingers

around traditional thinking patterns awaiting the disruptive effects of the online food platforms.

The online disruption means that boundaries that have come to exist in the market, are fading.

The disrupting effects of online food platforms are a result of the industry’s changing environment,

while also being a driver of change itself. The rise of the concept of online food platforms is

demanding awareness, inducing urgency among existing food businesses as well as new businesses to

cope with the changing environment. The goal of this research is to identify the driving forces of the

disruption of online food platforms, what the impact is and how the food industry can react to the

changing environment.

The online disruption is driven by:

- The social-behavioural developments in the consumer-market.

- International trends and developments that play a key role in the growth of the Dutch food

industry.

The disruption of online food platforms is accelerated by the digital evolution which induces the food

industry to deal with the changing environment.

Not only should food businesses be aware of the disruptive effects of online food platforms, but by

accepting the opportunities to engage in the online food market, centralising consumers and by

thinking outside traditional processes, a food business stays relevant during the period of transition.

The data collected, derived from the insights and experiences by industry experts and professionals,

has resulted in the following implications:

The Dutch food industry should widen their perspective by means of observing foreign trends more

intensively. The current state of the industry lacks pro-activity regarding adapting to the disruption of

online food platforms. Progressed food markets suggests valuable solutions, such as expansion

strategies in order to create more volume, optimise content management via online channels, and the

extension of offered product selection.

4

To compete with large firms, who obtain a larger amount of market share, collective solutions should

be set up to strengthen the positions of smaller initiatives.

Due to the wide arrange of product choice by various online and offline food companies, the

distinction of food products, brand and service in order to create uniqueness is most relevant.

Strengthen the relationship between business and consumer. Due to the digital developments, more

personal and specific consumer information is openly attainable and easy to utilise. Food businesses

should invest in strengthening the relationship with the consumer engaging more intensively to the

personal needs.

The convenience-driven society suggests online food platform as an ideal solution to traditional food

purchasing, as food business can optimise the display of their end-products as an alternative to offline

channels.

5

PREFACE

This bachelor thesis is written upon my completion of the International Hotel Management

programme at NHTV University of Applied Sciences. The primary goal of this research is to identify

what the drivers are for the disruption of online food platforms in the Dutch food industry, what the

influence is and provide recommendations for food businesses to react to the disruption.

The research topic derived from the main graduation project I was assigned to. Foodservice Instituut

Nederland and the Abn-amro allowed me to assist in the development of the second edition of the

foodservice magazine the Food 500. During this project it became clear that online food platforms are

a trending development and have not been thoroughly researched in the Dutch food industry.

Therefor I choose to write the bachelor thesis on this topic with regard to the outcome being worthy

enough to graduate as beneficial to food businesses in the Dutch food industry.

To successfully complete this research I would like to start by thanking all the contributors involved

during the completion of the bachelor thesis.

First off I would like to thank Stef Driessen, my graduation coach at Abn-amro, who allowed me to be

part of the Food 500 project, providing me with the assistance and coaching to successfully complete

my tasks for Food 500, and by providing guidance during my thesis research.

I would like share my appreciation with Anique Grievink and Ubel Zuiderveld, who allowed me to be

part of the team of the Food 500 project and support me during my research. Particularly I would like

to thank Ubel Zuiderveld by taking the time to provide his knowledge and expertise on my research

topic in form of an interview.

I would like to thank Eric Andersen my graduation coach at NHTV, who provided me with frequent

feedback sessions, which where most valuable. Furthermore the assistance by Michel Altan, strategic

manager lecturer at NHTV, is very much appreciated. Additionally I would like to share my gratitude to

the individuals working at the Abn-amro at the advisory and sustainability department for always

creating a pleasant and interesting working environment.

Finally I would like to acknowledge the food industry experts and professionals who contributed to my

research, by taking the time to share their insights and experiences regarding the research topic. An

extensive acknowledgement per industry expert have been given in chapter 6. Methodology.

The process of writing my bachelor thesis was a pleasant and an educational experience. The

literature studies and field research on topics such as innovative food business concepts, food shopper

behaviour, and digitalisation provided me with inspiring insight which has led to broaden my career

goals in overall foodservice industry.

6

TABLE OF CONTENT CHAPTER 1. INTRODUCTION ........................................................................... 8

1.1 ASSIGNMENT OVERVIEW .................................................................................................... 8

1.1.1. PROBLEM STATEMENT ................................................................................................................... 8

1.1.2. RESEARCH QUESTION ..................................................................................................................... 9

1.1.3. SUB QUESTIONS ............................................................................................................................. 9

1.1.4. RESEARCH METHOD ..................................................................................................................... 10

1.1.5. THE SCOPE OF THE RESEARCH ...................................................................................................... 12

1.2. FSIN & ABN-AMRO ........................................................................................................... 12

1.3. THESIS OUTLINE ............................................................................................................... 13

CHAPTER 2. DIGITAL EVOLUTION .................................................................. 14

2.1. INTRODUCTION ................................................................................................................ 14

2.2. DRIVERS OF CHANGE ........................................................................................................ 15

CHAPTER 3. STRUCTURING THE (ONLINE) FOOD INDUSTRY ........................... 17

3.1. INTRODUCTION TO THE DUTCH FOOD CHANNELS ............................................................. 17

3.2. FRAMING THE ONLINE FOOD OUTLETS ............................................................................. 19

3.2.1. INTERNATIONAL DEVELOPMENTS .............................................................................. 19

CHAPTER 4. THE FOOD SHOPPER ................................................................... 21

4.1. INTRODUCTION ................................................................................................................ 21

4.2. THE DUTCH FOOD SHOPPER ............................................................................................. 21

4.2.1. EXTERNAL FORCES THAT INFLEUNCE THE FOOD SHOPPER ........................................................... 21

4.2.2. PERSONAL NEEDS AND MOTIVES ................................................................................................. 24

4.3. INTERNATIONAL FOOD SHOPPER BUYING BEHAVIOUR ..................................................... 25

4.3.1. EXTERNAL FORCES INFLEUNCING THE FOOD SHOPPER ................................................................ 25

4.3.2. PERSONAL NEEDS AND MOTIVES ................................................................................................. 26

4.4. SEGMENTATION ............................................................................................................... 28

CHAPTER 5. ONLINE DISRUPTION .................................................................. 29

5.1. WHAT IS ONLINE DISRUPTION? ........................................................................................ 29

5.2. THE EFFECT OF ONLINE DISRUPTION IN THE FOOD INDUSTRY ............................................ 30

5.3. DEFINITION ...................................................................................................................... 31

CHAPTER 6. METHODOLOGY ......................................................................... 32

6.1. INTRODUCTION ................................................................................................................ 32

6.2. SCOPE AND LIMITATIONS ................................................................................................. 32

6.3. RESEARCH METHOD ......................................................................................................... 33

6.4. METHOD OF DATA COLLECTION ........................................................................................ 34

7

6.4.1. THE FOOD INDUSTRY EXPERTS ........................................................................................ 35

6.5. ANALYSIS ......................................................................................................................... 37

CHAPTER 7. ANALYSIS ................................................................................... 38

7.1. INTRODUCTION ................................................................................................................ 38

7.2. BEHAVIOUR OF TODAY’S FOOD SHOPPER ......................................................................... 38

7.2.1. CHANGING DEMOGRAPHICS ........................................................................................................ 39

7.2.2. PRICE & QUALITY ......................................................................................................................... 39

7.2.3. CONVENIENCE-DRIVEN ................................................................................................................. 41

7.2.4. PUSH & PULL FACTORS ................................................................................................................. 41

7.2.5. INDIVIDUAL NEEDS ....................................................................................................................... 42

7.2.6. PHYSICAL EXPERIENCE .................................................................................................................. 43

7.3. THE IMPACT OF DIGITALISATION ...................................................................................... 43

7.3.1. DIGITAL FORCES INFLICTING CHANGE .......................................................................................... 43

7.3.2. THE AWERENESS OF ONLINE FOOD PURCHASING ........................................................................ 45

7.4. THE DEVELOPMENT OF THE DUTCH FOOD INDUSTRY ........................................................ 45

7.4.1. ENFORCING INTERNATIONAL DEVELOPMENTS ............................................................................ 45

7.4.2. OFFER DISTINGUISHED PRODUCT ................................................................................................. 47

7.4.3. SEEK COLLABORATION ................................................................................................................. 47

7.4.4. STRENGHTEN FOOD SHOPPER RELATIONSHIP .............................................................................. 47

7.4.5. SIMPLYFYING PROCESSES ............................................................................................................. 48

7.4.6. PROSPECT .................................................................................................................................... 49

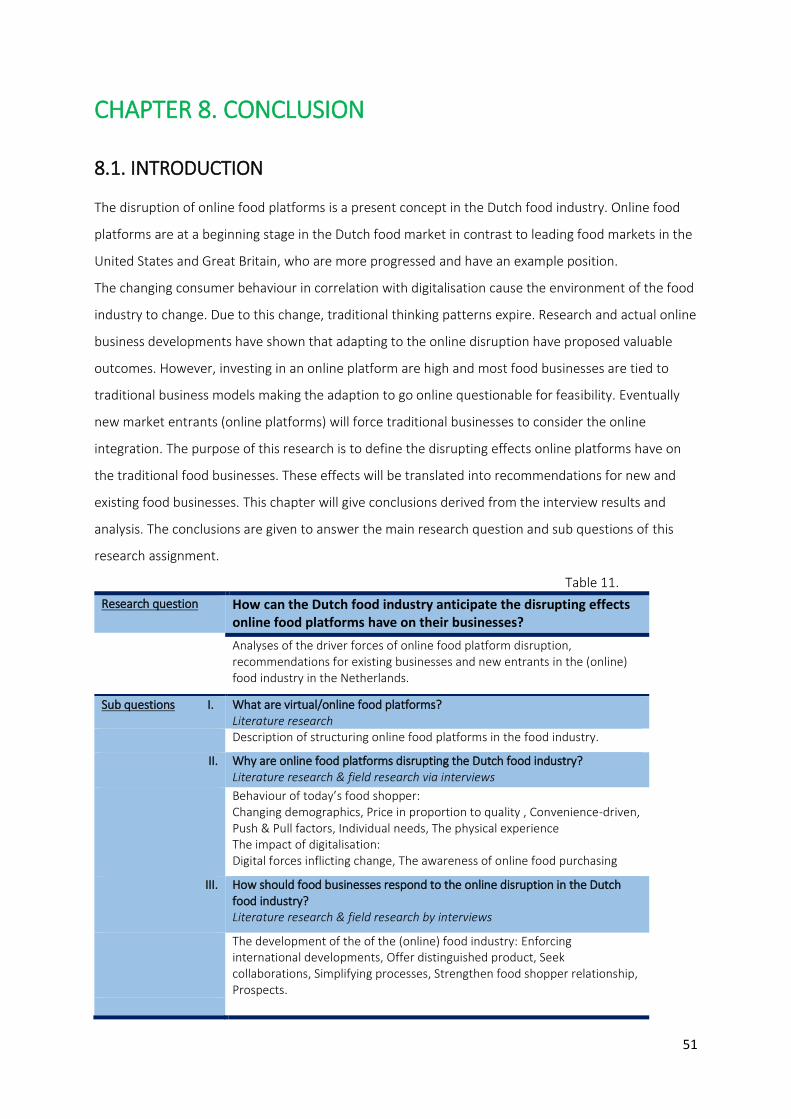

CHAPTER 8. CONCLUSION.............................................................................. 51

8.1. INTRODUCTION ................................................................................................................ 51

8.2. ONLINE FOOD PLATFORMS ............................................................................................... 52

8.3. THE DRIVING FORCES OF ONLINE FOOD PLATFORM DISRUPTION ...................................... 53

8.4. IMPLICATIONS FOR FOOD BUSINESSES ............................................................................. 54

8.5. EXPLORING THE FUTURE .................................................................................................. 55

CHAPTER 9. DISCUSSION ............................................................................... 57

9.1. THE CURRENT PRESENCE OF ONLINE FOOD PLATFORMS ................................................... 57

9.2. THE INCREASING RELEVANCE TO ADAPT TO THE ONLINE DISRUPTION ............................... 58

9.3. THE RELEVANCE OF THE PHYSICAL EXPERIENCE ................................................................. 59

9.4 LIMITATIONS OF DISRUPTION OF ONLINE FOOD PLATFORMS ............................................. 60

CHAPTER 10. RECOMMENDATIONS ............................................................... 61

BIBLIOGRAPHY .............................................................................................. 62

8

CHAPTER 1. INTRODUCTION

1.1 ASSIGNMENT OVERVIEW

This bachelor thesis is the concluding assignment of the International Hotel Management studies at

the NHTV University of Applied Sciences. This research assignment is commissioned by FoodService

Instituut Nederland (FSIN) and the Abn-Amro bank. FSIN is an independent institute that monitors

data and trends in the food industry, which they translate into market insights.

The Abn-amro bank analyses different markets to financially attend the supply and demand. Their roll

during this assignment is observing the overall condition of the food industry, providing insight on

Dutch food industry. This report is exploratory by nature and addresses the concept of “disruption” by

online food platforms and its implications in the Dutch food industry.

1.1.1. PROBLEM STATEMENT

The food industry is divided into two channels: the foodservice and the food retail. The division is

based on which food outlets the consumer purchases their food and beverage products. Traditionally,

the foodservice channels offer products to consumers via out-of-home food outlets and food retail

offers products via at-home food outlets.

FSIN indicates a new rising culture of purchasing food in form of groceries, prepared meals or meal

kits through online food platforms. Various companies now provide the option to order such food

products online. Online food platforms are becoming more popular among the Dutch consumers. The

online food margins tripled between 2012 and 2014. (Bladel et al. 2015). Well-known formulas now

focus on going digital, with Albert heijn online as the market leader in the Netherlands.

Since 2014, 6% of the Dutch consumers ordered their groceries from online retail stores such as Albert

Heijn online. Moreover, nearly 1% of the total Dutch food and beverage expenses were on online

meals via platforms as Just.eat.com and newyorkpizza.nl. (CBS, 2014-2015)

The internet’s reach is expanding throughout the Netherlands, increasing internet activities, such as

online food purchasing. CBS stated that 90% of the Dutch population uses internet on a daily base, via

mobile, tablet and laptop/computer.

International developments in the online food market show far more progress in the United States.

Not only food related companies focus on digital integration non-food companies, Amazon and

Google capture a fair amount of the online food share as well. (Grievink, 2015)

9

According to Jan-Willem Grievink, digitalisation is a fact and the food industry cannot avoid the digital

transformation. The new digital era we live in is disrupting the world of food and beverages. We are at

the beginning of a digital revolution in the food industry. In correlation with the changing behaviour of

the food shopper the disruption of online food platforms are becoming a fact. FSIN defines

‘consumers’ as ‘food shopper’, which is apprehended during this research.

The concept of “disruption of online food platforms” is slowly integrating in the Dutch food market.

This research assignment investigates the driving forces of the disruption of the online food platforms

and how they are influencing the total food market. The purpose of this research is to identify the

factors that drive the online disruption and make recommendations for existing and new food

businesses on how to anticipate to a changing environment.

1.1.2. RESEARCH QUESTION

The main research question is as followed: “How can the Dutch food industry anticipate the disrupting

effects online food platforms have on their businesses??”

The answer to this question will be given through implications and subjects that are important to

consider when the market is disrupted. The awareness of the changing environment and the

awareness on how to anticipate are key.

1.1.3. SUB QUESTIONS

Before answering the main research question and provide recommendations, a range of factors need

to be examined and defined. The following sub questions describe those factors to answering the

main research question.

1. What are online food platforms?

Before examining the consequences of the online disruption of food platforms, it is important to

identify what food platforms are and how the operate.

2. Why are online food platforms disrupting the Dutch food industry?

In order to understand how the market is being influenced by online food platforms, it is important to

find out where they come from and the reason why they are here. By identifying what the drivers are

behind the growth of online food platforms lays the base of the concept online disruption.

10

3. How should food businesses respond to online disruption in the Dutch food industry?

In order to react to the changing environment, it is important to know how to anticipate to change. It

is essential to explore the reactions to the changing environment.

1.1.4. RESEARCH METHOD

The methodology that is used to answers the main research question and sub questions consists of

literature research and field research.

In order to understand the context in which the online disruption of food platforms is examined,

chapter 2, 3, and 4 explain the changing digital environment, the consumer in the food industry, the

relevant food industry segments and international trends and developments . These chapters are

based on desk research.

Then, starting with defining what online disruption is, chapter 5 describes what already is known

about online disruption. What can be derived from food outlets in the Netherlands and abroad, and

what is written about the concept.

In combination with the previous chapters the literature research about disruption by online food

platforms has led to the definition of the concept and the integrated subjects which is used as base to

formulate the qualitative interview questions.

The process of the field research exists of semi-structured interviews with industry professionals and

experts. This research aims to find the answers and recommendations on the integrating concept

online disruption in the food industry. Nine experts from various food related organisations in the

Dutch market were selected based on their different standpoints in the Dutch food industry to discuss

their opinion. Table 1. Introduces the experts per name, organisation and position.

11

Table 1.

Names

Position Organisation

Stef Driessen

Sectorbanker leisure Abn-Amro bank

Bartho Schols Manager NHTV learning company -

International Hotel Management

Academy

NHTV University of Applied

Sciences

Remko Klasen Lecturer NHTV/ Operational manager

learning company - International Hotel

Management Academy

NHTV University of Applied

Sciences

Ubel Zuiderveld Manager researcher & publisher/

foodservice watcher/ independent

publicist

Foodservice Institute

Nederland & UZMedia

Michiel van Noort

Managing senior consultant HTC advisory bureau

Liewe van der Werff

Assistant advisor HTC advisory bureau

Guido Verschoor Senior advisor Van Spronsen & Partners

Horeca - advisory

Marketing manager

Team leader/ manager marketing

department, head office.

Online food platform

organisation (fast food/ home

delivery)

Bas van der Krogt Head E-commerce manager Hoogvliet supermarkets head

office

The gathered data is analysed and themes and issues arrive from the input. The purpose of the field

research is to identify the online disruption in the Dutch food industry and to give more depth to the

concept from various viewpoints. From the conclusions and recommendations the answers to the

main research question and sub questions are given.

12

1.1.5. THE SCOPE OF THE RESEARCH

This research is conducted to get a deeper insight on the impact of online food platforms in the Dutch

food industry, and how the industry should respond to the disrupting factors. It does not further

investigate non-food activities. The research deals with Business to consumer, the direct interaction

between (online) food businesses and the food consumers. Business to Business is not included, such

as food production and manufacturing companies, or food sellers to food businesses, such as catering

organisations.

The main focus of this research is limited to the effects of the online food platforms in the Dutch food

industry. However relevant trends & developments from abroad are part of the literature studies and

outcomes of the field research. These trends & developments are solely focused on the food markets

of the United States of America and Great Britain.

Finally, the emphasis lies on existing food businesses and new entrants that will come to deal with the

changing environment. The recommendations are intended for the member of the Abn-Amro bank m,

FSIN, and existing and new food businesses in Dutch food industry. The main focus lies on online sales

of food and beverage products. Not every online force of possible industry influences are thoroughly

examined due to relevance and time limitations.

1.2. FSIN & ABN-AMRO

The Foodservice institute’s mission is to contributes to the emancipation of the Out-of-home and At-

Home consumption in the Dutch food industry. It aims improve the quality of processes and activities

with this industry and increase the level of professionalization. (FSIN,2015) FSIN represents the

public’s interest of the total Dutch food industry. For the last ten years, FSIN has been monitoring the

positive and negative factors influencing the Dutch food industry.

FSIN contributes to this research by providing insight on the Dutch food market, identifying current

issues and developments that eventually set up this research. Moreover their input they contributed

to the outcome of the thesis.

ABN-AMRO bank is one of the most prominent banks in the Netherlands. They contribute to the Dutch

economy by monitoring and analysing different markets and assist in corporate credit loans to Dutch

businesses, such as in the food industry.

The department of advisory & sustainability were involved during this research. Their interest lie in

concept improvements, and the development of new business models in the food and hospitality

business. Their goal is to identify and assist in business affairs and the prospects from various sectors

13

in different branches. They contribute to this report by providing Marco-economical figures and by

giving insight on relevant trends and developments in the total food industry. Moreover Abn-Amro

contribute to the findings of this research assignment.

FSIN and Abn-Amro have joined forces in order to improve the quality of the processes and activities

within the total food Dutch food industry. With that said, both parties are mutually interested in

affairs regarding the public interest and food businesses in the total food market. Both parties do

groundwork by analysing the Dutch food industry, as their research contributes to development of the

overall food market.

1.3. THESIS OUTLINE

This section describes the content of each chapter. Table 2.

Chapter 1: Introduction Problem statement description, the description of the research

question and sub questions. Research method and the scope and

limitations of the research. Introduction of commissioning

institutes and the relevance and contribution to the research

assignment.

Chapter 2: Digital Evolution Explanation of the driving force of digitalisation and its effect in the

food industry.

Chapter 3: Structuring the (online) food

industry

Overview of the (online) food industry in the Netherlands,

regarding international developments.

Chapter 4: The online food shopper Description of the food shopper’s buying behaviour in regard to

online food purchasing.

Chapter 5: Online disruption Description of the concept, and the criteria that determine the

online disruption.

Chapter 6: Methodology Explanation of the methodology used for data collection.

Description of the participants and their relevance to this research.

Chapter 7: Analysis Analysis of the input of the participants, derived from the collected

data.

Chapter 8: Conclusion Conclusion of the analysis by answering the research question and

sub questions.

Chapter 9: Discussion Discussion of the research results and literature research, regarding

the current state, the challenges, and the limitations.

Chapter 10: Recommendations List of recommendation for future research.

14

CHAPTER 2. DIGITAL EVOLUTION

2.1. INTRODUCTION

Digitalisation is a fact and the food industry cannot avoid the digital transformation. “The new digital

era we live in is disrupting the world of food and beverages. We are at the beginning of a digital

revolution in the food industry.“(J.W. Grievink, 2014)

The traditional retail business is fundamentally changing due to the digital revolution. It is becoming

clear that consumers nowadays are more adapted to online food purchasing. For instance, consumers

view their products online and purchase them online, or they view their products online and purchase

them in the store. Various combinations of online purchasing are being integrated in the consumers

food shopping process. (G. Heaton, 2014)

Online food purchasing, in form of groceries and meals is becoming more popular. Since 2014, 6% of

the Dutch consumer orders groceries from online retail stores such as Albert.nl. Moreover nearly 1%

of the total spending of food and beverages was on online home delivery products, via platforms as

Just.eat.com and newyorkpizza.nl. (CBS, 2014-2015) The internet’s reach is expanding geographically,

more Dutch citizens have access to the internet. CBS stated that 90% of the Dutch population uses

internet on a daily base, via mobile, tablet and laptop/computer. Due to the reach and accessibility of

the internet online activities increase, such as online food purchasing.

In order for a food businesses to keep pace with digital trends and developments, a food business

should take the innovation curve by Roger’s into account, as can be seen in model 3. The model shows

how quickly a digital reality comes to an existence, especially for the role of online buying channels in

the food market. Trend watchers from FSIN indicate via the innovation model how rapid the digital

reality is coming to an existence, especially in the online food sector. (Bladel et al. 2015)

Model 3.

Source: Christensen, 2014. FSIN Beleidsmonitor, 2015.

15

Model 3. illustrates that the Dutch online food market is still at a beginning stage at this point. Only a

small amount of companies offer food products via online platforms. These innovators and early

adopters are a small group in the Dutch food market who adapt to changing environment. Via the

innovation’s Curve by Roger’s it can be stated that when the segment ‘Early Majority’ adapts to the

digital changes in the Dutch food industry, the digital existence of the online sector will drastically

grow.

2.2. DRIVERS OF CHANGE

In order to understand the changing environment of the online food platforms in the Dutch food

industry, the drivers of digital change are identified. The digital evolution represents a fundamental

sea of change in businesses and consumer behaviour, bringing forth a force of disruption. It must be

understood that the fundamental drivers of change are trends that are driving the digital

transformation. It is clear that the digital transformation is a major challenge for small- and medium

sized organisations and as it is for large organisations.

Ira Kaufman & Chris Horton (2014) discuss the four drivers of change. Which are, internet, social,

mobile and data.

The internet nowadays has the role of the primary driver of change in marketing, its impact on the

business communication and commerce is far reaching, and continually growing. Information is

power, which makes the internet supreme. It has fundamentally changed the way of distribution,

classify, seek out, and act on information.

Social networking connects people and communities, allow them to share and transfer messages in

real time. Social media can be regarded as the virtual marketplace of online communication and

engagement in the digital culture. 27% of all time spent online is on social networking.

Unlike many forms of marketing, whose forms tends to be simple, the power of social media is in its

growing stage. Social media enlarges brand reach, empowering companies to leverage their content

and messages more efficiently. (Kaufman & Horton, 2014)

Mobile implies “proximity”, being geological located and online. The mobile is a real-time enabler of

the digital culture, it is present in the physical and virtual space of consumers. The future of mobile is

linked with social media and “proximity”. A average person uses some form of “connected device” 34

times a day. The advanced use of mobile provide (on-the-go) consumers numerous of options and

capabilities, empowering them as never before.

16

Businesses may struggle with digital marketing, as a business must cope with the increasing

expectations and demands of mobile users. The mobile users now expects businesses to provide

relevant online resources that inform, entertain, and/or resolve. In short, mobile with the integration

of social media and proximity has shifted power to consumers, who are highly aware of this.

Data can be thought of as a functional brain, the underlying intelligence that provides content and

context to the digital culture. The advancement in technology and the collection of data allows

marketeers to track, review and refine every aspect of the digital business. Garten (2015) defines “big

data”, where the quantity, the speed and the diversity of data forms data sets, produced by

consumers who save more and more data via various channels. (e.g. social media platforms such as

Facebook, Google and Pinterest)

The ability to compare marketing initiatives with real-world results, allows businesses to continually

refine their brand message and marketing plans, by using content and context to better connect with

consumers.

The Dutch food industry is at a stage that it cannot avoid the impact of digitalisation. When the Dutch

food market embraces the digital forces the online industry will radically grow.

17

CHAPTER 3. STRUCTURING THE (ONLINE) FOOD INDUSTRY

3.1. INTRODUCTION TO THE DUTCH FOOD CHANNELS

In order to understand the online food industry better, the traditional food industry and online food

channels are elaborated on, to draw a structure of the overall industry.

This report defines the food industry as the industry where the consumers purchases their food and

beverages for at-home consumption or out-of-home consumption.

The Dutch food industry had a rough period during the financial crisis in the last six years. At the start

of 2015 it is showing promise again, as the Dutch consumers are optimistic which influences the food

revenue streams. The online food sector plays a key role regarding the positive revenue streams. The

total online food margin between 2012 and 2014 tripled. The main actor in the online market is the

retail sector. In 2013 the online sales were estimated at €290 mil. by which the market leader Albert

Heijn already obtained two third of the revenue. (Bladel et al, 2015)

To understand the various branches in the (online) food industry, the food sector is divided into two

channels, which are foodservice and food retail. Traditionally the foodservice market provides in

products that are being consumed out-of-home and the food retail market provides in products that

are consumer at-home. (Bladel et al. 2015) FSIN makes a distinction between food outlets in the at-

home and out-of-home channels.

FSIN monitors the data of all food outlets and indicates which outlets showed growth potential or

declining results. Table 4. shows the traditional food segments plus the online food platforms,

integrated in the new (mix) retail segment. Table 4. also indicates the segment’s growth in 2014.

18

Table 4.

OUT OF HOME Classic Food & Beverage Fine dining and casual dining restaurants, bar, café, coffee

place, hotel, leisure

Examples include: Wolfslaar restaurant, Humprey’s

restaurant, Coffee company, Van der Valk Hotels, Efteling

Growth

Catering Corporate catering, Institutional catering (care, education)

leisure

Examples include: Albron, Hutten, Deli Xl

Convenience Fast service restaurants, travel, petrol stations

Examples include: McDonalds, La Place, AH to Go, BP

AT HOME New (mix) retail Real food retail, evening + convenience, online/Pick up,

Food/non-food

Examples include: De Foodhallen, Albert.nl, Thuisbezorgd.nl,

the Action

Supermarket Assorted food retail

Examples include: Albert Heijn, Jumbo, Aldi, Plus

Specialty shop Specialized food retail

Examples include: Bakkerij Bart, De Keurslager

Market and other retail Specialized food retail non-fixed location.

Examples include: Local market, agricultural

Source: FSIN Beleidsmonitor 2015

The new (mix) retail is a mix of new food retailers. FSIN monitors this group due to blurring concepts

and digital food sellers. This report focuses solely on the online food sector, exclusively on the

business to consumers processes.

The online food market in the Netherlands already established different forms of food platforms, who

show constant growth. Online food retailing in form of online grocery shopping is most popular among

the Dutch consumers. Other forms of online food purchasing are via intermediary platforms which

allows consumers to order food in form of meals. The next paragraph elaborates on different

branches in the online food industry.

19

3.2. FRAMING THE ONLINE FOOD OUTLETS

3.2.1. INTERNATIONAL DEVELOPMENTS

The prosperity of the Dutch food industry is mainly influenced by successful developments of foreign

food markets, such as that of the United States and in the United Kingdom. (A. Grievink, 2015)

A DESTEP analysis is created to identify similar factors in the food industries in the United States,

United Kingdom and the Netherlands.

Please see the DESTEP analysis for comparison of the Dutch and U.S. food market in appendix 1.

The online food industry is well established in the United States. Their online food market is similar to

the Dutch market as they segment their online consumer-market as followed, prepared meal delivery,

meal kit delivery, grocery/packaged goods delivery. (Food logistics, 2014)

Their formats of reaching these segments are more progressed then the Dutch industry.

Virtual businesses or e-tailers in the US market are establishing themselves by means of offering food

concepts based on the these three markets. Food logistics (2014) identifies the following types of

virtual food platforms in the United states;

Retail stores with online stores

These stores offer home delivery and pickup. The orders are fulfilled from store shelves and e-

commerce distribution centres. Examples include Target.com Meijer.com and the Freshmarket.com.

In the Netherlands Albert Heijn online is the main player acting on this format. Other food retail stores

such as Jumbo, Plus, Spar and Hoogvliet are catching up providing their own online grocery shopping

platforms. (Meijers, 2014)

Dedicated e-tailers that stock inventory

The company does not have a physical storefront, but maintains its own warehouse.

Examples include Amazon, Vitacost and MyNaturalMarket.com. Stores in the Netherlands body and

fitshop, ekokopen.nl or degroentetas.nl.

Virtual e-tailers

The company does not have a physical store or warehouse, they function as an intermediary for

manufacturers and producers. Examples include Takeaway.com. Such platforms show much potential

in the Dutch food market. Thuisbezorgd.nl, justeat.com and etenbestellen.nl are the frequently used

platforms among the Dutch consumers. (consumentenvergelijking.nl, 2015)

20

E-tailers that provide their own delivery

Examples include Newyorkpizza, Hellofresh and amazon fresh. Currently Hellofresh is a popular e-

tailer in the Netherlands. Newyorkpizza and Domino’s are presently main players in this area. (Bladel

et al.)

Virtual home delivery (food retail intermediaries)

This is a company that operates as an intermediary for food retailers.

Examples include Google Shopping Express, Amazon and Instacart. Due to the fact that Albert Heijn

online is dominating the Dutch food retail sector, no intermediate platforms are demanded by

consumers for purchasing food products from different food retailers. The future may hold such

virtual formats as more national food retailers are expanding into e-commerce. (Meijers, 2015)

It can be stated that the Dutch online food industry is comparable to that of the certain regions in the

United States due to the similar Demographic, Economic, Social-behavioural, Technological,

Environmental, and Political factors. The foundation for distinguishing such online food platforms is

well established in the food industry and will definitely grow in future of this digital era. (Bladel et al.

2015)

21

CHAPTER 4. THE FOOD SHOPPER

4.1. INTRODUCTION

A series of different drivers have triggered the change of consumer buying behaviour, which has led to

a new segment in the traditional food service model, new (mix) retail. (Bladel et al. 2015) As stated

before several new entrants are integrated in this segment, only this report focuses solely on the

online food sector. The online segment is not showing an immediate threat, but due to the growth of

online food purchasing, other segments should take notice in order to anticipate future disruption.

The food shopper should be centralized in food businesses, they are now in control. The underlying

causes and conditions have influenced consumers to no longer think in channels, but in needs.

(Meijers, 2015)

Before explaining what those needs are, the following paragraph explains the external factors

influencing buying behaviour. The analysed factors in this chapter evolve around online as well as

offline buying behaviour.

4.2. THE DUTCH FOOD SHOPPER

In order to understand the general buying behaviour, all external forces influencing food buying

behaviours should be identified. These forces influence the Dutch food shopper in both the out-of-

home and the at-home channel.

4.2.1. EXTERNAL FORCES THAT INFLEUNCE THE FOOD SHOPPER

The external forces that influence food shoppers behaviour are distinguished by the following five

themes:

Figure 5.

22

Figure 5. indicates which factors have a positive or negative influence on the food shopper’s buying

behaviour. (Abel et al, 2015)

Economy and the perception on welfare.

Due to the financial crisis, the consumer trust in the market declined. Since 2013 the consumers trust

in the Dutch economy is increasing again (GFK, 2015). The derived attitude of the economic time is the

financial awareness. Consumers are aware of the financial situation of the market as well as personally

and are searching for the best price-quality relation.

Innovations by technique.

Digitalisation is putting consumers in charge (Grievink, 2014)

Ira Kaufman & Chris Horton discuss the four drivers of change. (p.15) Which are, internet, social,

mobile and data. It must be understood that the fundamental drivers of change are trends that are

driving the digital transformation. Several factors are derived from the study of FSIN’s food shopper,

which are coherent to the drivers of change by Ira Kaufman & Chris Horton. These factors are, the

need for convenience, socially connected, and the role of the mobile devices in daily life. The Digital

Needs model by Microsoft (Appendix 2) supplements by illustrating the difference between internal

and external needs of consumers. On the one side people explore the external world versus the

control of their internal emotions. Consumers also switch between self-focus as an individual versus

the need to connect with others and share experiences.

Furthermore FSIN distinguishes the contrast of digitalisation between elder and young generations.

Stating that elder consumer are complex to reach in contrary to young consumer, who evolve through

digitalisation. The millennials (network generation 1985-2000) are highly involved in the digitalisation,

due to the integration of internet, mobile and social forces in their daily lives.

The generation gap between Dutch consumers regarding digital transformation is high as can be seen

in table 4.

23

Table 6.

GENERATION

VALUES & PRIORITIES

INVOLVEMENT IN DIGITAL TRANSFORMATION

Silent Generation 1930-1945

Materialistic, out-of-home consumption

Protest Generation 1945-

1955

Economical behaviour, Consistency (career, family, privacy)

Generation X 1955-1970

Quality, diversity, professionalise

Pragmatic Generation 1970-

1985

Comfort, dynamics, and content

Network Generation 1985-

2000

Originality, participate in networking, and development

Source: FSIN, 2015 & CBS, 2014

Innovations in the food sector.

Due to new supply, new demand is created. Online food purchasing is a key segment of innovation in

the food sector. In the US, the research firm Food logistics (2014) defined the online food market in

three categories: prepared meal delivery, as prepared meal delivery, meal kit delivery,

grocery/packaged goods delivery market.

The aspect of purchasing online or physically influences the attitude during the food shoppers buyers

process, as the effort is minimised in buying process. (Abel et al, 2015)

Time, spare time and urgent time spending.

Saving time is the new “money”. (Abel et al, 2015) Time is short, a large part of the Dutch households

are one-person households in which the consumer behaviour orientates more individually. Food

consumption is being combined during travels, social activities (meeting friends), working and

studying. Therefor time-management regarding consumption is critical for food shoppers.

Example behaviour by friends is influential.

Social media has a major role in informing about new trends and developments. Due to distributing of

information, society has become aware on authenticity. The sense if a product or brand is genuine or

just a marketing proposition is high. (Abel et al. 2015) Food shoppers are aware of their surroundings,

making their buying behaviour more critical.

24

4.2.2. PERSONAL NEEDS AND MOTIVES

FSIN indicates that the Dutch food shopper’s needs are established via the motives routine,

convenience and comfort. Additionally the location where the food shopper consumes food &

beverage products plays a role in their choice of purchasing. These are: At-home, On-the-road, and at-

location. The model identifies the food shopper’s internal factors that influences the buying process.

FSIN states the popularity of food outlets among the Dutch food shoppers.

Table 7.

As can be seen, the routine and the at-home factor are the main reasons for online food purchasing.

Routine and the at-home channel suggests online food retailing such as grocery shopping, for as the

convenience and comfort factor suggests prepared meal delivery.

Table 7. indicates that routine, convenience and comfort are main drivers for online food purchasing

in the Dutch food market. The at-home factor suggests that food shoppers demands their products

digitally ordered at-home.

25

4.3. INTERNATIONAL FOOD SHOPPER BUYING BEHAVIOUR

Throughout this chapter similar social-behavioural factors compared to the food shopper in the more

progressed market of the UK are identified. For this reason the consumers buying attitude is

presumed identical, making current and future developments of online consumers behaviour in the

UK most relevant.

The Mintel Group Ltd. have done research on the online buying behaviour in the UK. The report

focuses on the incentives that influences consumers to order food via food retail outlets as well as

food take-away or home-delivery outlets. Their research is based on adult consumers aged 16+. Their

study captures data out of the Silent generation (born 1930-1945) and the Network generation (born

1985-2000). The results are based on young consumers fully integrated in the digital transformation

and elderly less involved in the virtual industry, making the results transparent.

As previously stated, identical factors are discussed, and thus the opportunities for the British industry

are applicable to the Dutch food industry.

4.3.1. EXTERNAL FORCES INFLUENCING THE FOOD SHOPPER

The Mintel Group discusses several factors that are identical to the external forces in the Dutch

market.

New technology

As previously stated, the use of mobile is a huge driver for the changing environment. The UK online

market is already at such a state that most online food home deliveries are done via a smartphone.

Internet accessibility and speed are considered to have a large impact on the online food shopping

behaviour as it increased food activities online.

Economy

The economy in the UK is recovering, wages are expected to increase faster than inflation, reducing

the pressure on incomes that drove much of the post-recession era. Despite the rising confidence

levels, the food shopper are aware on their financial situation, making them enormously price-

sensitive.

26

Innovation by technology in the food sector

The consumer culture in Britain is highly convenience-driven, derived by the food shoppers need for

direct comfort and satisfaction. This is mainly influenced by the developments of digital technology as

products and services are obtained much quicker. In the UK this also reflects on the food industry, as

food companies are launching more home delivery platforms. Moreover innovating solutions are

implemented for quicker processes, by means of using different equipment and transport.

Ageing generation

Britain’s ageing consumers pose challenges for the at-home delivery market online as the at-home

delivery is not well integrated in this segment. Moreover the British involvement in digital technology

is slightly higher than Dutch 55+. Nevertheless digitalisation is mostly integrated in the Pragmatic

generation (1970-1985) and the millennials (1985-2000).

4.3.2. PERSONAL NEEDS AND MOTIVES

Online food retailing

The study of Mintel Group Ltd. research (2014) explored the food shoppers online buying behaviour in

the at-home channel, or grocery/packaged goods delivery market (Foodlogistics, 2014). The

overarching themes in their findings were control and clarity, consumers want more information on

their products, how and when they are delivered and a finer two-way- dialogue with food retailers

regarding their order. The report state five personal needs and motives that influence food shoppers

to purchase online in food retail (at-home channels). These factors are:

Time, money, convenience, online accessibility, responsibility.

Saving time

Time is precious to today’s food shoppers. Grocery shoppers today see online as beneficial as it saves

time travelling to or from a grocery store. The research also indicates that food shoppers think they

use less time to shop online then physically in-store.

Reducing costs

The general perception of online shopping suggest consumers are saving money when shopping

online. Making it easier to stick to a budget than they would do in a physical store. Consumers

perception towards delivery costs is lower and acceptable in contrary to the costs of fuel to get to a

physical store, which would be higher.

27

Minimising the effort

42% of the online British food shoppers see online as a good way to avoid the effort of shopping in-

store. The perception of numerous of grocery shoppers when entering a store is a stressful and

pressured experience. Therefore they want to avoid such environments via online retail platforms.

Online shopping accessibility

Due to online food platforms consumers can shop whenever they are willing or wherever they are,

providing a more beneficial way of grocery shopping for food shoppers further located from a physical

store.

Responsible nutrition

Consumers nowadays want to take care of themselves eating responsible and healthy and taking

notice of the environment. Organic and fresh food is a popular among the British food shoppers.

Online food home delivery

The Mintel Group Ltd. (2014) continues their research on the online prepared meal delivery and meal

kit delivery markets (Foodlogistic, 2014)

The consumers committed behaviour to convenience-driven services has influenced the growth of

home delivery and takeaway concepts. Both for online foodservice outlets as intermediary online

platforms. The results of the Mintel Group’s research identifies the main drivers that influence food

shoppers to order online in contrary to home cooked meals or physically consume in the out-of-home

channel (restaurant, café fats food etc.).

These drivers are: Convenience, price, familiarity, responsibility and diversity.

Responsibility

Consumers nowadays want to take care of themselves eating responsible, healthy and taking notice of

the environment. Organic and fresh food is becoming more popular among the British food shoppers.

Price range

The online food shopper is price-focused during their decision-making process.

40% of the online consumers stated that price range affects their decision-making process whilst 23%

say that cost delivery does. Meanwhile, 21% of the online food shopper states that special

offers/money-off deals have effect on their decisions.

28

Convenience

Similar to food retail, the current food shopper culture is increasingly convenience-driven,

characterised by the consumers need for instant gratification, particularly as the growth in digital

technology has helped them get products and services quicker. Digitalisation influences the

convenient attitude of the food shopper. Particularly the growth of digital technology has helped

consumers to obtain their demanded products and services much quicker.

Familiarity of brand/products

Disrupting consumers from their ordering habits/ product is complex as the research points out that

brand familiarity is a key influencer in the purchasing behaviour. Whilst such loyalty is beneficial for

existing food operator, those looking to win market share from established players are likely to rely on

price promotions to encourage consumers to change their habits. (Mintel Group Ltd. 2014)

Diversity of products

Diversity in product possibilities stimulates online food shopping. Consumers benefit from the variety

of kitchens due to the lack of self-triggering cooking.

4.4. SEGMENTATION

The response of the online food shopper is determined by the discussed external forces and personal

needs and motives. In combination with the food shoppers own characteristics they respond to the

changes in the food industry. Their actions define their motives and needs. It can be stated that based

on DESTEP analyses, the Mintel Group Ltd and FSIN studies, factors influencing the British food

shopper are similar to the factors that drive the Dutch buying behaviour. Consequently, the future

may hold similar consumer developments to that of the British market as the UK is on a more

progressed level.

As derived from the literature studies the online food shopper can be divided in three categories, the

prepared meal food shopper, the meal kit delivery food shopper, and the grocery goods food shopper.

These market segments are integrated in both at-home as well as in the out-of-home sector.

To segment food outlets in at-home or out-of-home channels, is becoming less relevant. Instead

outlets are developing new means of meeting consumer’s needs, while reasoning out the food

shopper’s motives. FSIN has defined this as the consumer-oriented approach. The result is that all

food products from household groceries to prepared meals can be ordered and delivered at home,

eliminating the physical process, all in fulfilment of the food shoppers needs. This process can be

defined as online disruption.

29

CHAPTER 5. ONLINE DISRUPTION

5.1. WHAT IS ONLINE DISRUPTION?

The term “online disruption” is defined as the change that occurs when new digital technologies and

business models affect the value proposition of existing products and services. (Christenen, 2014)

Online disruption is a concept that is slowly settling in the Dutch Food industry. The term is used to

identify disruptions in the food industry that hold consequences for doing business as well as

designing organisations. (Mesters, 2015). The concept of online disruption by food platforms is driven

by two forces, which are the consumer buying behaviour and digitalisation.

Foodservice Institute Nederland discussing four causes that lead to these radical changes.

Technology and digitalisation put food shoppers in charge

Lines between offline and online shopping experiences are blurring. The traditional retail business is

fundamentally changing due to the digital revolution. It is becoming clear that food consumers

nowadays do not make a difference between online or offline shopping. For instance, consumers view

their products online and purchase them online, or they view their products online and purchase them

in the store. Various combinations of online shopping are being integrated in the consumers food

shopping process. (Heaton, 2014) The ‘connected consumer’ does not follow standard marketing laws,

as they have the opportunity to seek own information about products in order to make decisions.

Values in today’s society are shifting

Values in today’s society is shifting thereby also the value in food. Food and lifestyle is becoming more

interconnected for the food shoppers. Food is used to distinguish a lifestyles among other food

shoppers in order to indicate what they value in life (Nieuwjaarsmonitor, 2015)

Social media plays key role in distinguishing the food shoppers values.

FSIN’s former president Frederik Masselink discussed that traditional values are shifting rapidly and

that we did not anticipated it. He quoted the chairman of Sainsbury, who stated that the supermarket

branch has changed more in twelve months than in than last twenty years. The prospects are looking

beneficial as margins are shifting back from food retail towards foodservice. Finally he demanded that

Dutch food industry professionals should adapt to the disruptive developments and engage in the

opportunities which the industry is providing.

30

Lifestyle & food reinforce hybrid models

Within the food industry opportunities arise for hybrid models, FSIN defines this as “Blurring”.

Concepts that are relevant for food shoppers daily food consumption, offering a total solution for each

eating-moment during the day. These concepts distribute via various channels in order to satisfy the

consumers food consumption now, later, at-location and, at-home. Online platforms are part of this

total solution, offering virtual access to a wide variety of food products on each moment of the day.

Old business models are under pressure.

Grocery stores feel the presence of online disruption as more retail stores are integrating virtual

access to their assortment. A business model without an online platform are considered out-dated.

This pressure will be noticed in the prospect of the Dutch food retail. (Nieuwjaarsmonitor & Meijers,

2015)

5.2. THE EFFECT OF ONLINE DISRUPTION IN THE FOOD INDUSTRY

In the US, online food platforms are a well-integrated concept in the food industry. The Dutch food

market is influenced by such developments (A. Grievink, 2015) in the US, the food market

distinguishes all online food platforms in several distributions categories, Retail stores with online

stores, dedicated e-tailers that stock inventory, virtual e-tailers, e-tailers that provide their own

delivery, virtual home delivery (food retail intermediaries) (Foodlogistics, 2014)

Nevertheless, a common mistake is that organisations avoid/ignore the disruption effects made by

implementations such as online food platforms. Ignoring or avoiding the changing environment will

cause crucial damages to a company. (Mcquivey, 2014) Technological advances are rapidly creating

numerous of opportunities for more people to meet consumers’ needs at minimal costs. That is the

essence of the concept “online disruption”.

Businesses who confront digital disruption will use disruption as a forcing function. Organisations use

it as the necessity to engage consumers differently, more effectively across all interaction touch points

(Mcquivey, 2014)

Several factors derived from the rotating forces constantly influencing each other, digitalisation and

consumer behaviour, are discussed:

Pace of innovation. Technological and digital developments now occur at increasingly faster intervals.

Consumers can be sceptical about “new and improved” as new food related products will quickly

enter the market.

31

Increased competition. The concept of online disruption enforces competing ideas. The effect of new

entries in the online market can be devastating for companies operating their business with outdated

business models.

Personalisation of interactions. Large data analytics enable marketeers to communicate with

consumers on a more relevant, personalised and targeted level than ever before. By using data-driving

marketing, businesses learn how to optimize their appeal to individual food shoppers. To keep an

competitive advantage this is essential.

Speed interactions. Digital communication between consumer and organisations is also based on

speed. Consumers increasingly expect personalisation, they also increasingly expect real-time

interaction with different brands.

Complete integration. Without integration, food businesses are not able to unleash the full potential of

digital technologies. Integration is needed to create cohesion across all marketing channels and

platforms. Furthermore and integrated internal marketing attributes helps to better understand data

patterns and consumer interactions.

5.3. DEFINITION

The change in lifestyle and the effect of digitalisation changed the customs of purchasing food and

beverages. The definition of disruption by online food platforms will be indicated in the period of the

concept’s transition into the food industry. The definition is applicable in various industries as well as

situations and is not tight to the food outlets and platforms and their way of serving the food shopper.

The following chapter describes the methodology of the literature research, aiming to seek evidence

how online food platforms are disrupting the Dutch food industry, and how food businesses should

react to the developments in the food industry

32

CHAPTER 6. METHODOLOGY

6.1. INTRODUCTION

This chapter explains the methodology that is used for this exploratory research. When it is unclear

what the problem and the impacts are, exploratory research is applied. This research explores the

overall concept of disruption by online food platforms as well as identifying what the impact and

implications are in the (online) food industry.

Due to the nature of this research, the data is collected via the insights of food industry experts and

professionals. Nine experts from various food related organisations in the Dutch market are selected

based on their different standpoints and experiences in the Dutch food industry.

The changing environment will confront food businesses to consider adjusting business strategies to

successfully adapt to the developments. The process of collecting data will lead to advice and

implications that can be considered as policy makers. The level of impact of online disruption differs

per business, depending via which channel and outlet a company operates. That means that some

companies are directly dealing with online disruption and others are limited to the experiences. In

order to get insight on online disruption of food platforms on various levels, it is relevant to analyse

multiple perspectives.

6.2. SCOPE AND LIMITATIONS

The intend of the research is to provide useful insight for established businesses and new entrants

that need to deal with a changing environment. Online disruption by food platforms is a result of

different factors that induce change. The collected data is focussed on the experiences and insight of

individuals operating in the online food business/platforms as well as individuals with an analysing and

consulting position in the food market.

The emphasis mostly lies on established food businesses of a certain scale who are likely to be more

flexible in adopting new strategies. In contrast with new entrants who have little obstacles to adopt

due to their nature of their organisation. This is due to their new business models which differ from

traditional business models, as they do not face transition. Nevertheless, the research

recommendations provided are also implacable for new market entrants.

33

The research is limited to the expertise and experiences of the industry professionals who are dealing

with the disruption in the Dutch food market. The experts understand the complexity of the relevant

topics and processes and have the experience to overview the overall industry, making their input

highly valuable. The author deliberately did not choose for qualitative research in form of consumer

surveys or questionnaires to identified consumer behaviour. The reason being that the principal part

of this research is the food industry’s reaction to the changing environment. A consumer inquiry

would propose a new research as the derived outcomes would be to comprehensive for this research.

Moreover, the experts interviewed provide contemporary knowledge on consumer behaviour in the

food industry in regards to the online disruption of online food platforms.

6.3. RESEARCH METHOD

The following table shows the methods of answering the sub questions, and the main research

question

Table 8.

Research question How can the Dutch food industry anticipate the disrupting effects online food

platforms have on their businesses?

Literature studies and field research

Sub questions

I What are online/virtual food platforms?

Research method Literature study

II Why are online food platforms disrupting the Dutch food industry?

Research method Literature study & field research via interviews

III How should the Dutch food industry respond to the online disruption in the

market?

Research method Desk research and field research via interviews.

The desk research is done by collecting relevant data from existing sources about a certain topic or

theme. The previous chapters were set up via the literature sources, visible evidence, and ‘authors’

experiences. The following chapters will describe the outcomes of the field research.

The field research is done to obtain unregistered data that is relevant for answering the research

questions. It is essential to collect data via field research as the meaning of understanding the concept

of online disruption in the food market comes from insights and experiences of the industry experts

and professionals.

34

6.4. METHOD OF DATA COLLECTION

It is vital to conduct research in such a way in order to present representative data. The concept of

online disruption of food platforms is relevant for businesses in the at-home channels and out-home

channels. Therefor it is decided to select a number of sources relevant to the subject.

To achieve the aim of this study a indeductive research will be performed consisting of a qualitative

semi-structured research interview. Indeductuve approach is reasoned as this report moves from

specific observations to broader generalizations and theories. The nature of this report is therefore

open-ended and exploratory. (Bryman & Bell, 2011)

To get an in-depth insight on the Dutch foodservice industry, a qualitative research in form of a semi-

structured interview will be held. This research aims to find the answers and recommendations on the

integrating concept of online disruption of food platforms in the food industry.

During the research assignment collecting answers from one of the industry experts was more

beneficial to gather via a written correspondence. Due to business circumstances Bas van der Krogt

was not able to share information via a physical meeting or telephone in the given time. Therefore

both parties agreed upon this method of data sharing. Unclear answers were verified in order to get

in-depth answers.

All the data collected for this research are based on experiences of experts and industry professionals.

The experts were selected on experience in the at-home and out-of-home channel as well as in the

online and offline food market. By selecting these experts the problem is examined form multiple

angles. The selection was done with the support of ABN-AMRO, and via self-effort, by contacting

various companies, industry experts and professionals relevant for this research.

During the literature research stage an conceptual model was formulated based on the literature

study. Please find the conceptual model in appendix 3.

Based on the model an interview guide was developed to formulate the interview questions.

Please find the interview guide in appendix 4.

35

6.4.1. THE FOOD INDUSTRY EXPERTS

For this research various food industry experts and professionals were approached to share their

vision on the impact of online food platforms in the total food industry. These experts are highly

experienced individuals who operate and view the food industry from multiple angels, which is

relevant for assessing this research. The experts were approached based on the following aspects,

online & offline food business experience, and the experience in different food outlets in the at-home

& out-of-home channel.

Stef Driessen

Stef Driessen is the sector banker leisure and team leader at department of sustainability and advisory

at the Abn-Amro bank. He focuses on strategic affairs with management teams ore clients in de

Leisure, Travel & Hospitality Industry. His interested lie in digital innovations, changing consumer

behaviour and improving business models. Stef Driessen was approached for his experience and ability

to overview the industry and the ongoing change that the industry faces.

Bartho Schols

Bartho Schols is a the current manager of the learning company at NHTV University of Applied

sciences, International Hotel Management Breda. Next to managing the NHTV outlets he helps steer

your professionals during their operational development. He has an experienced background in Dutch

food industry, particularity in the out-of-home channel. His interest, knowledge, and experience on

the Dutch food industry lead me to approach him for an interview.

Remko Klasen

Remko Klasen is a lecturer at the NHTV International Hotel Management Breda

Next to lecturing and steering hotel students to their management degree he has an operational

management position in the food and beverage outlets at the NHTV. Remko Klasen was approached

for the interview due to his experiences and knowledge about the Dutch food industry developments

and international developments.

Ubel Zuiderveld

Ubel Zuiderveld is a foodservice watcher, an independent publicist, and a researcher. Specialised in

the foodservice industry. Furthermore he is manager researching & publishing at Foodservice Institute

Nederland. Due to his expertise in researching and defying trends and developments in the total food

industry he was approached for the interview.

36

Michiel van Noort & Liewe van der Werff

Michel van Noort & Liewe van der Werff are the managing Senior Consultant & Assistant advisor at

HTC advisory bureau. In the last 35 years HTC advisory bureau have established themselves to a

specialist position in the Dutch food industry (hotel, restaurant, café), recreation, and catering

industry. Michiel van Noort and Liewe van der Werff were particularity approached due to their

experience and knowledge on digital developments in the Dutch food industry as well as in

international markets.. Their knowledge was valuable due to the fact it gave great insight current

business activities in the food industry.

Guido Verschoor

Guido Verschoor is the Senior Horeca Advisor at van Spronsen & Partners Horeca – advise.

Van Spronsen & Partners is an advisory bureau for the hospitality and leisure industry.

Guido Verschoor was approached for his experience in strategic consultancy for traditional

foodservice companies regarding future developments in the Dutch food industry.

Bas van der Krogt

Bas van der Krogt is the E-commerce manager at the head office of Hoogvliet supermarkets. Bas van

der Krogt was approached as he is a highly experienced e-commerce manager for online food retailer.

Since 1988 he has consulted and guided offline retailers into the online sector in grating the online

channel in the overall business plan. His experiences provide insight from an internal perspective.

Marketing manager at an online food platform

The marketing manager is the marketing manager and team leader at the marketing department at

the head office of a well-established online food organisation in the Netherlands. The food company

can be categorised as fast food/ home delivery. She was approached as she is active for an online food

platform providing insight form an internal perspective. Furthermore she is well experienced in the

marketing department of the food organisation and other food industry companies. Her contribution

is valuable as company she works, gives a vision on the role of a food platform in the (online) food

industry. She wished to stay anonymous, therefore she will be referred to as the marketing manager

or candidate 8.

37

6.5. ANALYSIS

The collected data from the interviews are structured via the qualitative research method coding.

The coding method is used as it is a tool that helps during the analytical process to structure

qualitative data and order it logical information. The following chapter describes the main findings per

industry expert. The findings are coded and subdivided under themes based of the conceptual model.

The codes are derived from the following criteria: relevant words, phrases, sentences or sections and

from relevant actions, activities, concepts, differences, opinions, processes.

The codes are written out and themed as follows:

1. The behaviour of today’s food shopper

2. The impact of digitalisation

3. The online food industry

The research results per industry expert can be found in following appendices: Table 9.

Industry experts Appendices

Stef Driessen Appendix 5.A. Interview Stef Driessen Appendix 5.B. Research results Stef Driessen

Bartho Schols Appendix 6.A. Interview Bartho Schols Appendix 6.B. Research results Bartho Schols

Remko Klasen Appendix 7.A. Interview Remko Klasen Appendix 7.B. Research results Remko Klasen

Ubel Zuiderveld Appendix 8.A. Interview Ubel Zuiderveld Appendix 8.B. Research results Ubel Zuiderveld